enabled by real-world solutions supported by analysis and ......

TRANSCRIPT

©OECD/IEA2017

TheIEAworksaroundtheworldtosupportacceleratedcleanenergytransitionsthatare

enabledbyreal-world SOLUTIONSsupportedbyANALYSIS

andbuiltonDATA

World Energy Investment 2017

Simon Bennett, Economics and Investment OfficeCOP23 IETA Pavilion, 9 NOVEMBER 2017

0

250

500

750

1000

USD(2016)billion

Globalenergyinvestmentfell12%in2016,asecondconsecutiveyearofdecline

Totalenergyinvestmentwas$1.7trillionin2016.Electricitysectorinvestmentovertookoilandgasforthefirsttime,whileenergyefficiencywasthebiggestgrowthsector.

Globalenergyinvestment2016

-25%-1%

+9%

Networks

Renewable

Thermal

Oil&gas

Coal

Electricity Oil,gas&coal RenewablesintransportandheatEnergyefficiency

-25%

Theroleofstateactorsinenergyinvestmentshasincreased

Theshareofstateactorsintotalenergyinvestmentreached42%in2016,largelythankstostate-ownedenterprisesinelectricitysectorinvestment,notablyinChina,andNOCsinupstreamoil&gas

Sourcesoffinancefor2016energyinvestmentsbyfinancingmechanism

7%

93%

ProjectfinanceBalancesheet

42%

47%

11%

Government/SOEsPrivatesectorHouseholds,communitiesandself-consumption

Ownershipof2016energyinvestmentsbytypeoforganisation

0

20

40

60

80

Europe China UnitedStates RestofAsia

USD(2016)billion

EuropeleadsefficiencyspendingbutChinaissettoovertakeitby2018

Policycontinuestounderpinefficiencyspending,especiallyinbuildingsinsulation,heatingsystemsandhomeappliances.Muchofthegrowthintransportefficiencyspendingisinelectricvehicles.

Globalenergyefficiencyinvestment,2016

Electrificationoftransportandheatisprogressing

Electricvehicle(EV)salesgrew38%in2016,bringand,at$6billion,nowrepresent10%ofalltransportefficiencyspending.Another$6billionwasspentgloballyonEVchargingstations.

GlobalelectricvehiclesalesElectricitydemandfromnewheatpumpssold

0

2

3

5

6

2010 2012 2014 2016

TWh

0

250

500

750

1000

2010 2012 2014 2016

Thou

sand

units

0100200300400500600700800

2010 2011 2012 2013 2014 2015 2016 2017

USDbillion

(nom

inal)

0100200300400500600700800

2010 2011 2012 2013 2014 2015 2016 2017

USDbillion

(nom

inal)

USindependents Majors Otherprivate NOCs

37%

12% 14% 14% 14% 16% 10% 13%18% 19% 20% 21% 20%

19% 17%

28%

42%

29%

39%

28%

38%

27%

38%

27%42%

26%

44% 45%

25%

12%21%

25%

405060708090100110120

0100200300400500600700800

2010 2011 2012 2013 2014 2015 2016 2017

USDbillion

(nom

inal)

GlobalCostIndex(Rightaxis)

Global upstream investment rebounds modestly in 2017

RampupofactivitiesleadstocostinflationinUStightoilbutelsewhereupstreamcostsdeclinefurther.NOC’shareintotalinvestmentreachesanotherrecordhigh.

Globaloilandgasupstreamcapitalspending2010-2017

+6%-26%

25%

37%

Oilandgasprojectsmovingtoshortertimelinesandsmallersizes

Ashiftincompanystrategiesandtechnologydevelopmentsleadstoshorterprojectcyclesacrossalltheoilandgasindustry

Averagesizeofconventionalresourcessanctioned andtime-to-market

Deepwateroffshore

Otheroffshore

Onshore

GlobalAverage

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0 100 200 300 400 500 600 700

Timetom

arket(years)

Averagesizeofresources(Millionbarrels)

2010-20142016-2017

Awaveofcoalpowerinvestmentiscomingtoapause

In2016,sanctioningofnewcoalpowerfelltothelowestlevelinnearly15years,hamperedbycompetitionfromrenewablesandenvironmentalchallenges.GaspowerFIDsexceededthoseforcoalbyover1.5times.

Averageannualfinalinvestmentdecisionsfornewcoal-firedpowercapacity

0

20

40

60

80

100

120

140

2001-2005 2006-10 2011-15 2016

GW China

India

SoutheastAsia

Restofworld

Globalaverageactualadditions

Investmentincleanpowerisnotkeepingpacewithdemand

WhilethecontributionofnewsolarPVandwindhasgrownnearlythree-quartersinthepastfiveyears,FIDsfornuclearandhydropowerhaveslowed.CleanpowerFIDsin2016generateatonlytwo-thirdsthelevelofpowerdemandgrowth.

Expectedannualpowergenerationfromfinalinvestmentdecisions

0

100

200

300

400

500

2012-13 2014-15 2016

TWh

Nuclear Hydropower&otherrenewablesWind SolarPVAveragepowerdemandgrowth(2012-16)

We'vetrackedasteady$37billion/yearofcleanenergyandelectricitynetworksR&Dspending,withroomforgrowthfromtheprivatesector.AsashareofGDP,ChinanowspendsmostonenergyR&D

GlobalcleanenergyR&Dfundingneedsastrongboost

GlobalR&Dspendingoncleanenergyandelectricitynetworks

Top3ITcompanyR&Dspenders

0

10

20

30

40

2012 2015

USD(2016)billion

Private Public

Conclusions

o Investmentfellby12%in2016,asecondconsecutiveyearofdecline,andelectricitysectorinvestmentovertookoil,gasandcoalinvestmentscombined

o AnupswingofUSshaleinvestmentiscreatingatwo-speedoilmarketandtriggeringarapidtransformationoftheoilandgasindustry

o Althoughelectricityinvestmentremainsrobust,policiesneedtofocusonmaintainingsupplyadequacy,stimulatinganaccelerationofcleanpowerandstrengtheningmarketsignalsforinvestmentinflexibility

o ThecleanenergytransitionneedsmoreR&DbutenergyR&Dexpendituresarestable;thereisalotofscopeforincreasedspendingonenergyinnovationbygovernmentsand,inparticular,theprivatesector

o Investmentdecisionstodaywillleavetheirmarkonenergyonenergyinfrastructurefordecadestocome;theIEAwillcontinuetofocusoninvestmentasacornerstoneofasecureandsustainableenergysystem

Energy Efficiency 2017

Brian Dean, Energy Efficiency DivisionCOP23 IETA Pavilion, 9 NOVEMBER 2017

©IEA2017

Key messages

• 2016confirmedtherecentstepupinglobalenergyefficiencygains

• Thisisgeneratingeconomic,socialandenvironmentalbenefits

• Butstrongerpolicyimplementationisessential

Freedownload:www.iea.org/efficiency

©IEA2017

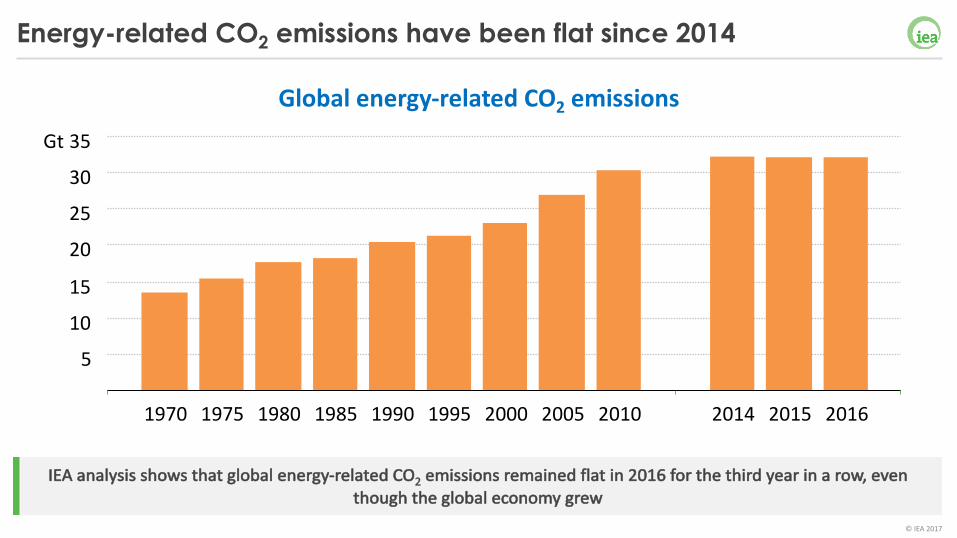

Energy-related CO2 emissions have been flat since 2014

IEAanalysisshowsthatglobalenergy-relatedCO2 emissionsremainedflatin2016forthethirdyearinarow,eventhoughtheglobaleconomygrew

5

10

15

20

25

30

35

1970 1975 1980 1985 1990 1995 2000 2005 2010 2014 2015 2016

Gt

Globalenergy-relatedCO2 emissions

©IEA2017

28

30

32

34

36

2014 emissions GDP growth Renewables and fuel mix

Energy intensity 2016 emissions

Emiss

ions (

Billio

n ton

nes C

O 2e)

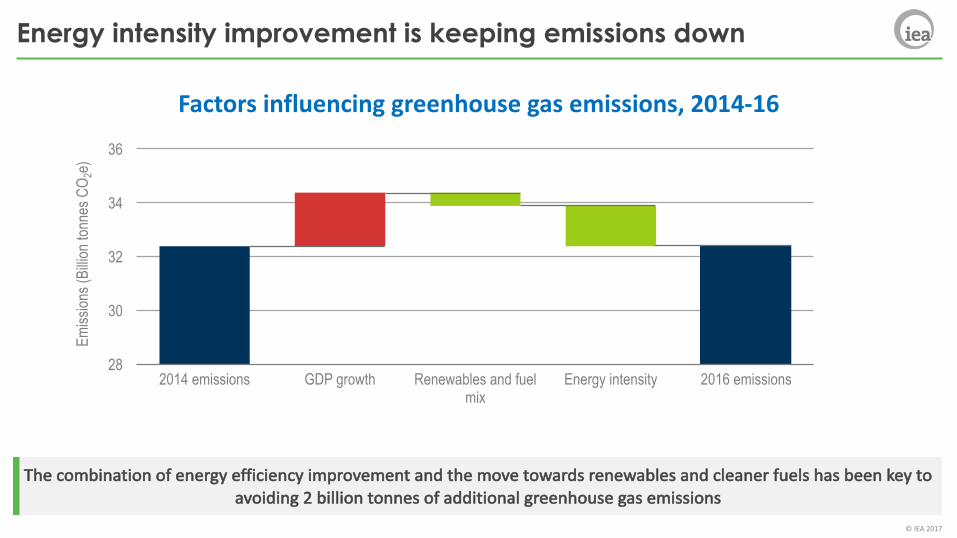

Energy intensity improvement is keeping emissions down

Thecombinationofenergyefficiencyimprovementandthemovetowardsrenewablesandcleanerfuelshasbeenkeytoavoiding2billiontonnesofadditionalgreenhousegasemissions

Factorsinfluencinggreenhousegasemissions,2014-16

©IEA2017

The world is generating more value from its energy use

Thisdecadehasseenintensityimprovementratesatalmostdoublethehistoricaverage,suggestingthattheworldhasenteredaneweraoffasterintensitygains.

Changesinglobalenergyintensity(energyperunitofGDP)

-3.0%

-2.0%

-1.0%

0.0%

1981-90 1991-2000 2001-10 2011 2012 2013 2014 2015 2016

Annu

al ch

ange

in en

ergy

inten

sity

Average annual change 1981-2010 Average annual change 2011-2016

©IEA2017

Efficiency delivers a global energy productivity bonus

The2016intensityimprovementrepresentsanadditionalUSD2.2trillionofvaluecreatedfromglobalenergyuse,equivalenttotwicethesizeoftheAustralianeconomy.

Economicvalueofimprovedenergyintensity,2016(USDbillion)

32260114

532

1127

2174

0%

2%

4%

6%

8%

0 1 2 3 4 5 6 7

2016

impr

ovem

ent in

ener

gy in

tensit

y

Japan European Union

India United States China World

©IEA2017

Global energy use is significantly changing

Energyefficiencyreducedglobalenergyuseby12%in2016,anamountequivalenttotheenergyuseoftheEuropeanUnion.

Globalfinalenergyconsumptionandsavingsfromenergyefficiency

0

2 000

4 000

6 000

8 000

10 000

12 000

2000 2016

MtoeEfficiency savings

©IEA2017

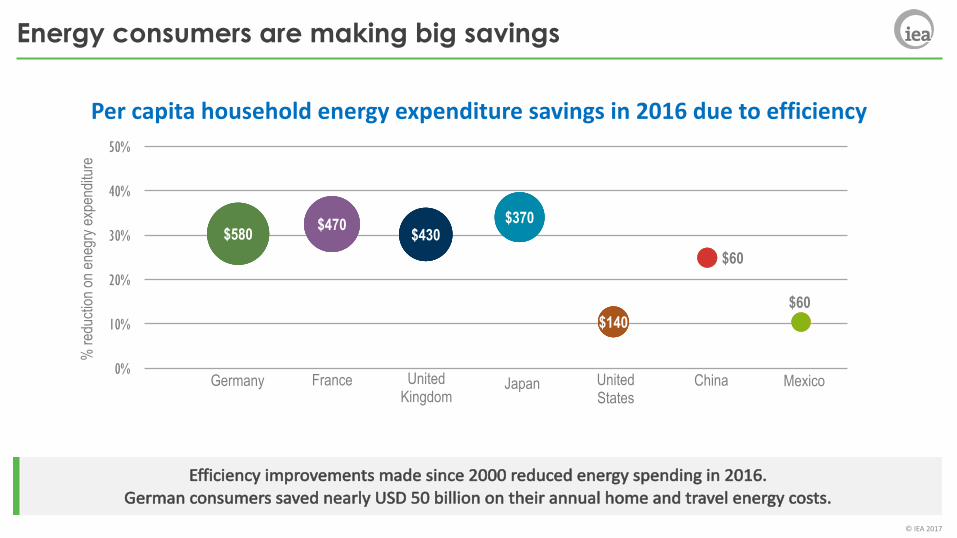

Energy consumers are making big savings

Efficiencyimprovementsmadesince2000reducedenergyspendingin2016.GermanconsumerssavednearlyUSD50billionontheirannualhomeandtravelenergycosts.

Percapitahouseholdenergyexpendituresavingsin2016duetoefficiency

$60

$580 $470 $430$370

$140

$60

Germany France United Kingdom

Japan UnitedStates

China Mexico0%

10%

20%

30%

40%

50%

% re

ducti

on on

eneg

ry ex

pend

iture

©IEA2017

24% 26% 28% 30% 32%

2016

2015

2014

2013

2012

% of global energy use covered by mandatory efficiency policies

Existing policies New policies

Policies of the past drive progress of today

Theamountofglobalenergyusecoveredbymandatoryefficiencypoliciesgrewin2016,but68%ofenergyuseremainsuncovered.Weowetheefficiencygainsoftodaytothepoliciesofthepast.

Annualadditionstotheglobalpolicycoverageofmandatorycodesandstandards

Existing policies New policies

©IEA2017

Vehicle efficiency policy is two-speed

Nearly40countrieshavefuelefficiencystandardsforcars.OnlyCanada,China,JapanandtheUnitedStateshavestandardsfortrucks.

Efficiencystandardcoveragebytransportend-use,2016

0%

10%

20%

30%

40%

50%

60%

Cars

Ener

gy us

e cov

ered

by fu

el eff

icien

cy

stand

ards

Trucks

Europe

Asia

North America

ChinaUSA Japan

Canada

©IEA2017

Space cooling energy use growth

Spacecoolingwillcontinuetobethefastestgrowingsourceofenergydemandinbuildings.

0

100

200

300

400

500

600

1990 2000 2010 2020 2030 2040 2050

Inde

x 19

90 =

100

Space cooling

Appliances and other equipment

Lighting

Water heating

Cooking

Space heating

Globalenergyconsumptionbybuildingend-use,1990-2050

©IEA2017

Demand for space cooling is heating up

Thereissignificantfuturecoolingenergygrowththathasminimalpolicyprogresstoday

Spacecoolingenergyuseandpolicyprogress

0%

5%

10%

15%

20%

25%

30%

35%

40%Policy progress index

Australia Korea United States Japan China India Italy Indonesia Mexico Brazil

2015 energy use 2050 energy use (projected)

©IEA2017

Concluding points

• EnergyEfficiency2017 showsthecriticalimportanceofenergyefficiencytoeconomies,householdsandtheenvironment.

• Therehasbeenastepupinefficiencygainsinrecentyears,despitelowerenergyprices,andthisishavingmanypositiveimpacts.

• However,68%ofglobalenergyuseremainsuncoveredbymandatoryefficiencypolicyandthecurrentlowrateofpolicyimplementationneedstoaccelerate.

• Decarbonisationrequirestheintegrationofefficiencyandrenewablesintotheenergysystemthroughaharmonisedpolicyapproach.

• TheIEAisattackingtheunmetenergyefficiencypotentialbyfacilitatingknowledgesharingandprovidingconcretepolicyrecommendations.

©IEA2017

Renewables 2017

Caroline Lee, Environment and Climate Change UnitCOP23 IETA Pavilion, 9 NOVEMBER 2017

©IEA2017

2016 – Renewables hitting new records driven by solar PV

Renewablesbreakinganall-timerecordaccountingfortwothirdsofglobalnetcapacityadditions;ForthefirsttimesolarPVbecomingthegloballeaderinnetcapacitygrowth

Powercapacityadditionsbyfuel2016

Retirements

0 50 100 150 200

Renewables

Gas

Wind

Solar PV

Coal

Additions (GW)

©IEA2017

Pricediscoverythroughcompetitiveauctionseffectivelyreducescostsalongtheentirevaluechain

AnnouncedwindandsolarPVaverageauctionpricesbycommissioningdate

Competition driving costs down

020406080

100120140160180

2012 2013 2014 2015 2016 2017 2018 2019 2020

USD/MWh

Onshore wind average auction price

Solar PV average auction price

©IEA2017

Renewables growth more and more dependent on wind and solar

SolarPVentersanewera,becomingtheundisputedleaderinrenewablepowercapacitygrowth;PValsoaccountsfor60%oftheupsidepotentialintheacceleratedcase

Renewableelectricitycapacitygrowthbytechnology

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

200

400

600

800

1 000

1 200

1999-2004 2005-10 2011-16 2017-22

Capacity growth (GW)Additional -accelearated caseOther renewables

Hydropower

Solar PV

Wind

% from wind and solar PV (right axis)

©IEA2017

China continues to lead growth while India overtakes the EU

Theforecastis12%moreoptimisticvs.lastyearmainlyduetosolarPVrevisionsinChinaandIndia;Growthcouldbe27%higherwithenhancedpoliciesaddressingregulatoryuncertaintiesandgridintegration

Renewablecapacitygrowthbycountry/region

050

100150200250300350400450500

China United States EU India Japan Brazil Africa & Middle East

Capacity growth (GW)

2011-16 2017-22 main case Additional accelerated case

©IEA2017

Renewables closing the gap with coal

Renewablegenerationtoexpandbyoverathirdwithitsshareincreasingfrom24%in2016to30%in2022,rapidlyclosingthegapwithcoal

Electricitygenerationbyfuel

0

2 000

4 000

6 000

8 000

10 000

12 000

2002 2006 2010 2014 2018 2022

Generation (TWh)

Coal

Natural gas

Nuclear

Renewables

©IEA2017

Surging EVs to complement biofuels in renewable transport

Shareofrenewablesinroadtransportincreasesfrom4%in2016toalmost5%in2022,withbiofuelsrepresenting80%ofthegrowthledbyAsia&Brazil;EVelectricityconsumptiondoublesby2022,withrenewablesproviding30%ofdemand

2016 2022

7%

Biofuelsandelectricvehiclescontributiontorenewableenergyconsumptioninroadtransport

4%Biofuels

EV 2/3 wheelers

Electrc cars and buses

©IEA2017

Progress in renewable heat depends on strong policies

Renewablesshareinheatconsumptionrisesfrom9%in2016to11%in2022.Chinaleadsabsolutegrowthwithnewtargets;EUremainsthelargestrenewableheatconsumerwhiletotalheatdemandoutpacesrenewablesgrowthinIndia

Shareofrenewablesinheatconsumptionbyselectedcountries

0%

5%

10%

15%

20%

25%

2010 2012 2014 2016 2018 2020 2022

% of renewables

European Union

USA

India

China

©IEA2017

Concluding remarks

Ø Renewablesriseby1,000GWto2022,equaltohalfofcurrenttotalcoalcapacity

Ø Renewablesgenerationexceeds8,000TWh by2022,equaltototalelectricityconsumptionofChina,India&Germanycombined

Ø SolarPVentersaneweraleadingthegrowthinrenewables,drivenbyarapidexpansionindeployment&manufacturingcapacityinChina

Ø DespiterapidgrowthinEVs,decarbonisationoftransportisalongwayoff

Ø Only30%ofelectricityusedbyEVsissourcedfromrenewables

Ø Advancedbiofuelsrequirespecificincentivestobolsterdeployment

Ø Policymakershavetoturntheirfocustosystemintegration&expandingtheuseofrenewablesforheating&cooling

©IEA2017

Thank you

Renewables2017TeamYasminaAbdelilah

HeymiBaharEmanueleBianco

UteCollierKarolinaDaszkiewiczPharoahLeFeuvreMeganMercerYasuhiroSakuma

Questionsandcomments:[email protected]

©IEA2017

©IEA2017

Wind and solar transforming power sector - system integration becomes key

Moreflexiblepowersystems,adaptedmarketdesignandpolicieswillhavetoplayakeyroleinintegratinglargersharesofwindandsolarinasecureandcost-effectiveway

VREshareinannualelectricitygeneration2016-22

0% 10% 20% 30% 40% 50% 60% 70% 80%

JapanBrazilIndia

ChinaUnited States

AustraliaItaly

United KingdomGermany

SpainIreland

Denmark

% of total generation

PV share in 2016

Wind share in 2016

Additional PV share in 2022

Additional wind share in 2022