employee vs. independent contractor – is your business compliant with wage and hour law?

TRANSCRIPT

Employee vs. Independent Contractor – Is your Business Compliant with Wage and Hour Law?

How to stay compliant and avoid legal liability.

Bret YawAssociate,

Ford and Harrison, LLP

Moderator

Rebecca Ward

Sr. Marketing Content Specialist

(303) 219-7802

Questions

If you have questions during

the presentation, please

submit them using the

“Questions” feature

Questions will be answered

at the end of the webinar

5

Which is Which and Why Does it Matter?

• Fair Labor Standards Act (FLSA) issues

• Withholding and other tax issues

• Exposure to discrimination liability

• State workers’ compensation laws

• State unemployment liability

• The definition of an independent contractor may vary between the IRS and other agencies (Department of Labor, EEOC) and courts tasked with determining whether the individual is an employee or independent contractor

6

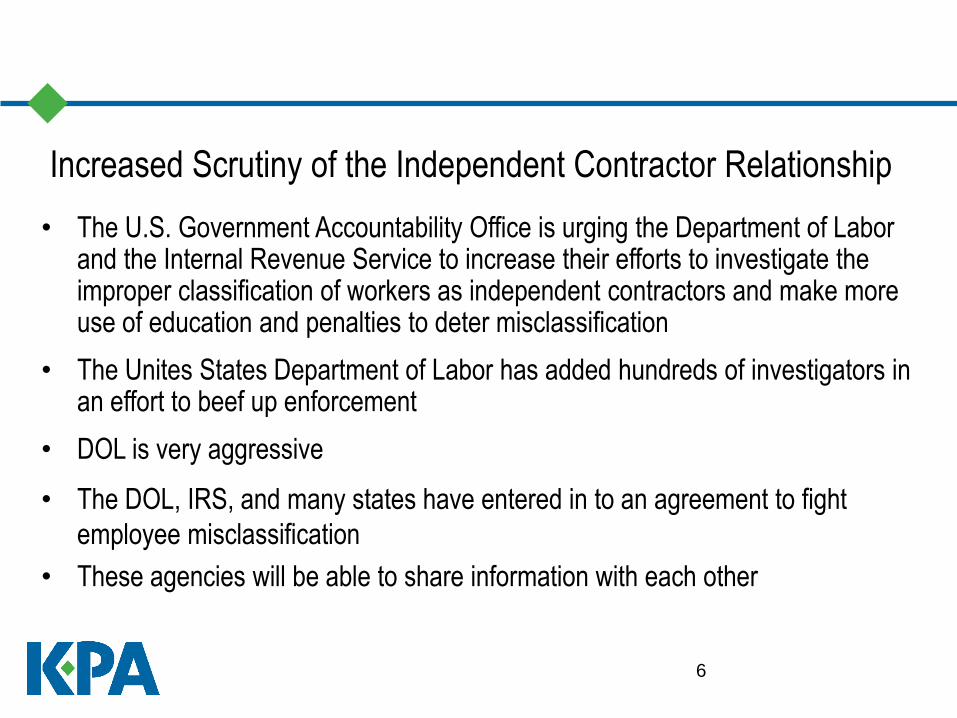

Increased Scrutiny of the Independent Contractor Relationship

• The U.S. Government Accountability Office is urging the Department of Labor and the Internal Revenue Service to increase their efforts to investigate the improper classification of workers as independent contractors and make more use of education and penalties to deter misclassification

• The Unites States Department of Labor has added hundreds of investigators in an effort to beef up enforcement

• DOL is very aggressive

• The DOL, IRS, and many states have entered in to an agreement to fight

employee misclassification

• These agencies will be able to share information with each other

Focus on Independent Contractor Misclassification

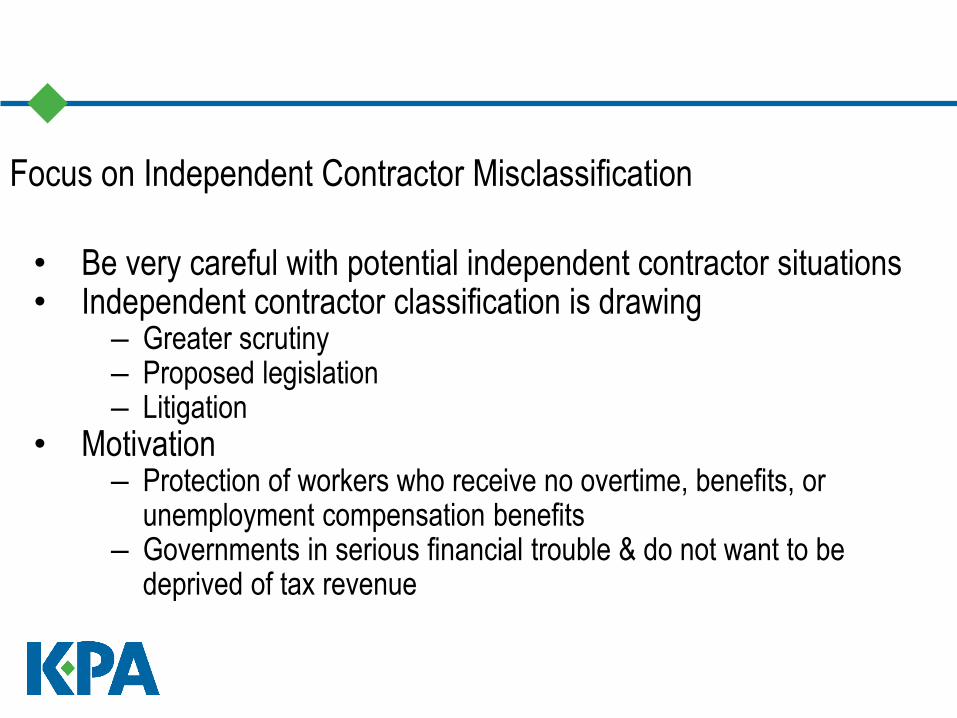

• Be very careful with potential independent contractor situations • Independent contractor classification is drawing

– Greater scrutiny– Proposed legislation– Litigation

• Motivation – Protection of workers who receive no overtime, benefits, or

unemployment compensation benefits– Governments in serious financial trouble & do not want to be

deprived of tax revenue

8

General Test for Independent Contractor

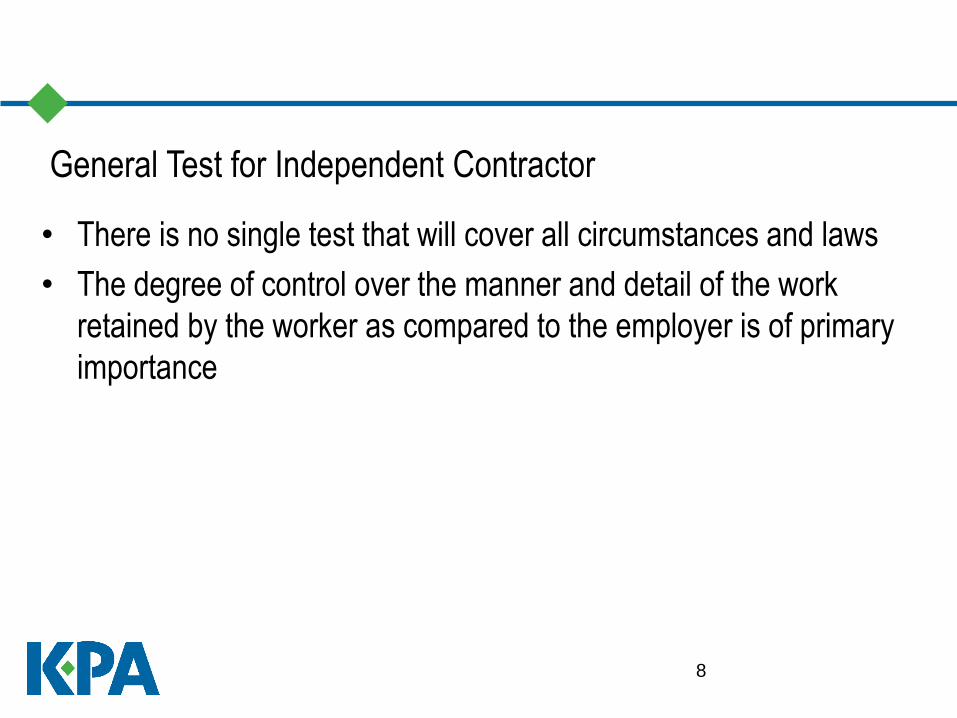

• There is no single test that will cover all circumstances and laws

• The degree of control over the manner and detail of the work

retained by the worker as compared to the employer is of primary

importance

9

Basic Questions to Ask

• Is the worker free to perform similar work for others?

• If so, does the worker perform work for others? Relatedly, what percentage of the worker’s time is spent doing work for the Company and for how long?

o i.e., is the worker’s business primarily as a contractor for the Company?

• Is the worker paid on a per-job basis, instead of a salary or hourly basis like other employees?

• Can the worker set his/her own work hours and routines?

10

Basic Questions to Ask

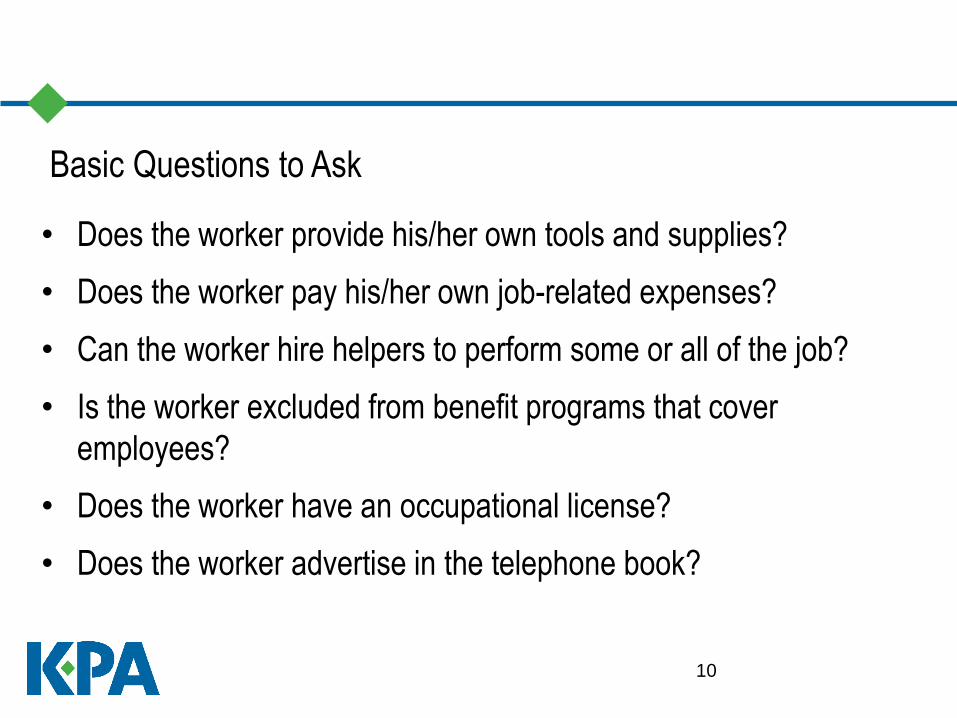

• Does the worker provide his/her own tools and supplies?

• Does the worker pay his/her own job-related expenses?

• Can the worker hire helpers to perform some or all of the job?

• Is the worker excluded from benefit programs that cover

employees?

• Does the worker have an occupational license?

• Does the worker advertise in the telephone book?

11

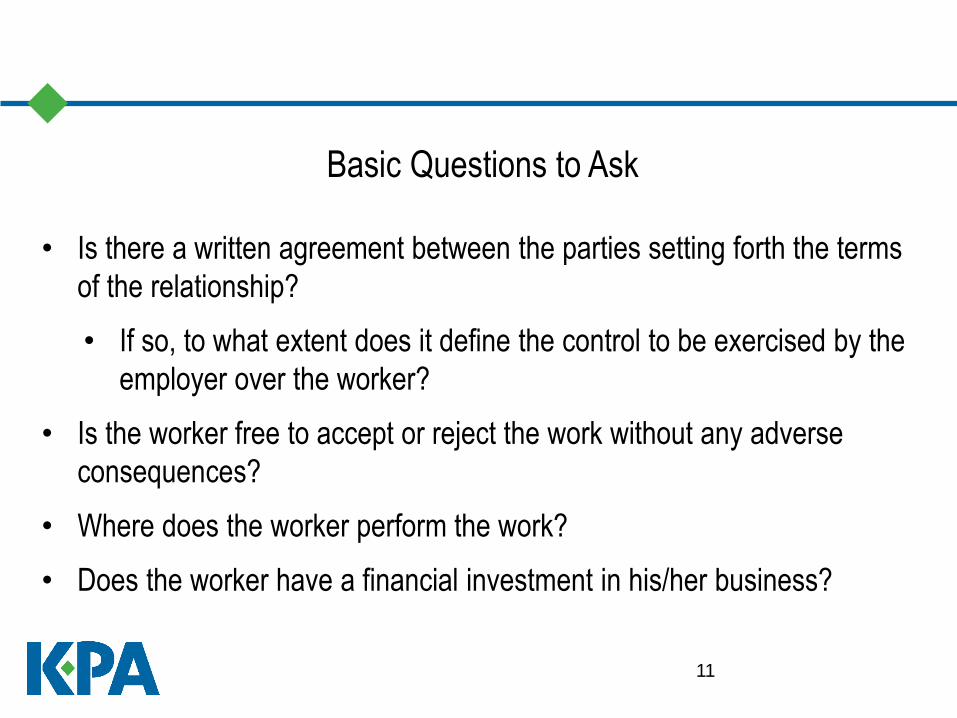

• Is there a written agreement between the parties setting forth the terms

of the relationship?

• If so, to what extent does it define the control to be exercised by the

employer over the worker?

• Is the worker free to accept or reject the work without any adverse

consequences?

• Where does the worker perform the work?

• Does the worker have a financial investment in his/her business?

Basic Questions to Ask

12

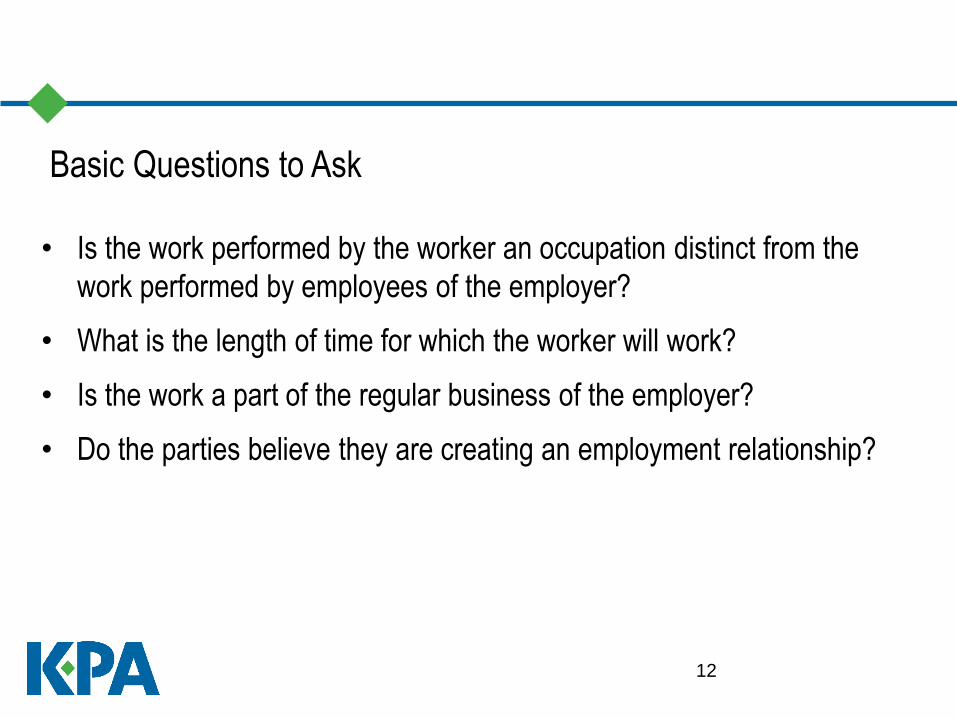

Basic Questions to Ask

• Is the work performed by the worker an occupation distinct from the

work performed by employees of the employer?

• What is the length of time for which the worker will work?

• Is the work a part of the regular business of the employer?

• Do the parties believe they are creating an employment relationship?

13

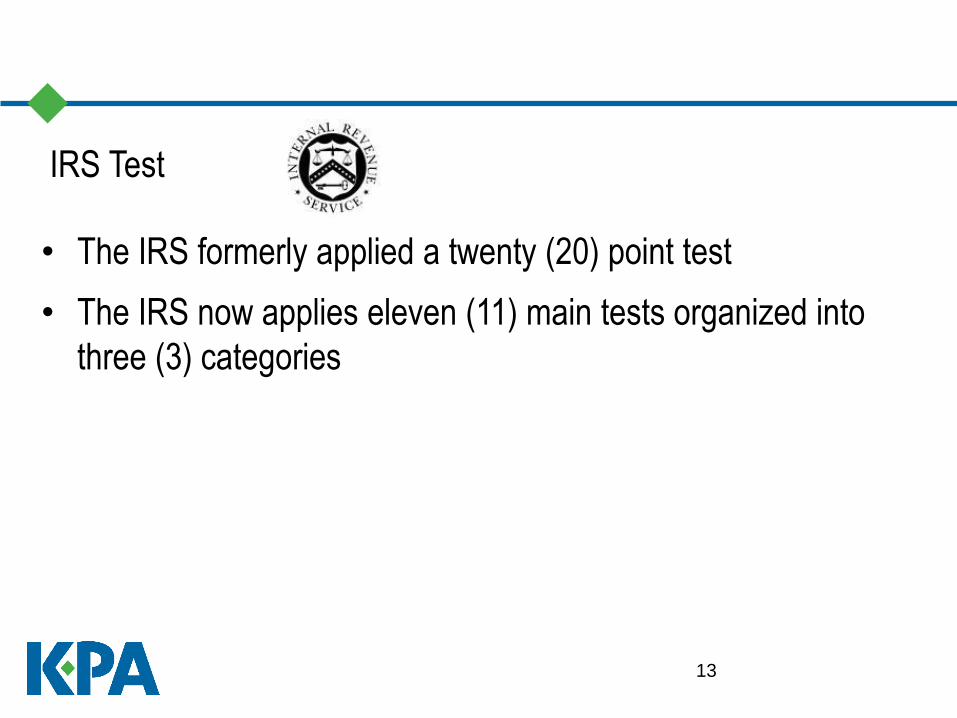

IRS Test

• The IRS formerly applied a twenty (20) point test

• The IRS now applies eleven (11) main tests organized into

three (3) categories

14

1. Behavioral Control - This category examines facts that show whether the business has a right to direct and control how the worker performs the tasks for which the worker is hired.

• Instructions that the business gives to the workers

o - When and where to do the work

o - What tools or equipment to use

o - What workers to hire or assist with the work

o - Where to purchase supplies and services

o - What work must be performed by a specified individual

o - What order or sequence to follow

• Training that the business gives the worker

IRS Test

15

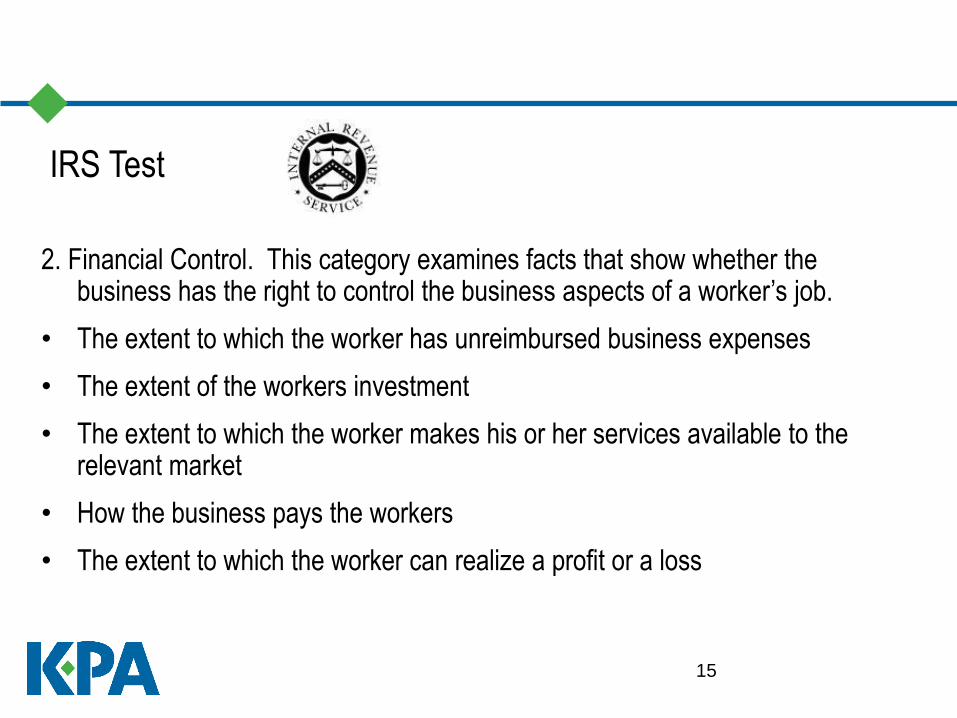

2. Financial Control. This category examines facts that show whether the business has the right to control the business aspects of a worker’s job.

• The extent to which the worker has unreimbursed business expenses

• The extent of the workers investment

• The extent to which the worker makes his or her services available to the relevant market

• How the business pays the workers

• The extent to which the worker can realize a profit or a loss

IRS Test

16

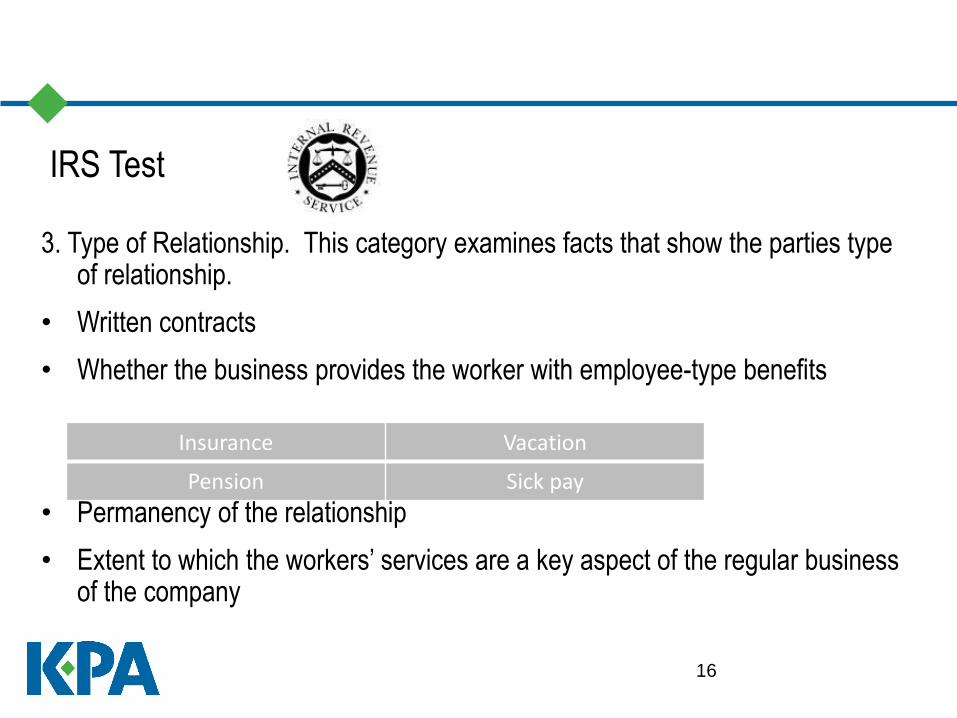

3. Type of Relationship. This category examines facts that show the parties type of relationship.

• Written contracts

• Whether the business provides the worker with employee-type benefits

• Permanency of the relationship

• Extent to which the workers’ services are a key aspect of the regular business of the company

IRS Test

Insurance Vacation

Pension Sick pay

17

Not Knowing the Difference Could Be Costly

• Employers caught incorrectly classifying workers are billed by the IRS for all or

a part of the uncollected payroll and income taxes

• EVEN IF THE CONTRACTOR HAS ALREADY BEEN PAID!

• Failure to identify workers properly may cost employers a great deal in

o Lost management time

o Legal fees

o Back taxes and payments

o Minimum wage and overtime

o Interest and penalties

18

But I gave him a 1099!!! Doesn’t that mean I’m

covered?!

Working under the cover of a Form 1099 does not mean that the contractor is completely free of

the hiring employer’s control

19

OK, What if we sign a Contract?

• If it looks like a duck and it quacks like a duck

• A written contract won’t make it a chicken!

20

Written Contracts

• A written contract relinquishing the right to control and specifying that

the worker will not be treated as an employee is important in helping to

structure the relationship with the worker…however...

• Employers should keep in mind that a contract designating an individual

as an “independent contractor” does not control over other facts that

demonstrate that the worker is treated like an employee

21

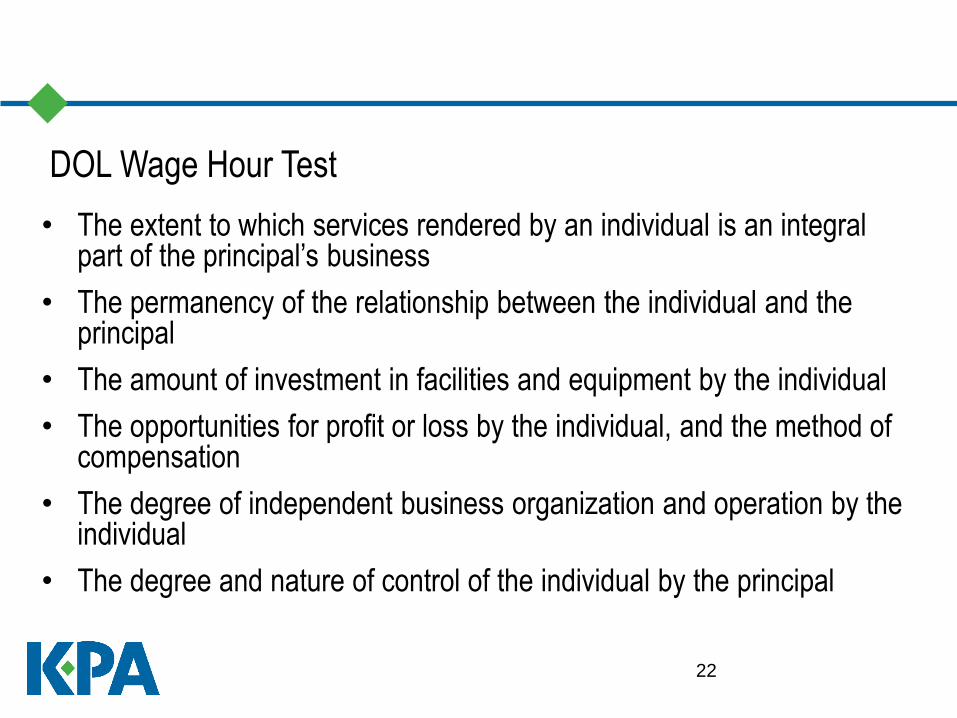

DOL Wage Hour Test

• Wage hour provisions apply only to “employees”

• FLSA defines employee as any individual employed by an employer

• Independent contractors, subcontractors, contract workers or

consultants may be “employees”

• The Wage/Hour Division of the DOL and the courts apply an “economic

reality” 6 factor test that focuses on the following factors:

22

DOL Wage Hour Test

• The extent to which services rendered by an individual is an integral part of the principal’s business

• The permanency of the relationship between the individual and the principal

• The amount of investment in facilities and equipment by the individual

• The opportunities for profit or loss by the individual, and the method of compensation

• The degree of independent business organization and operation by the individual

• The degree and nature of control of the individual by the principal

23

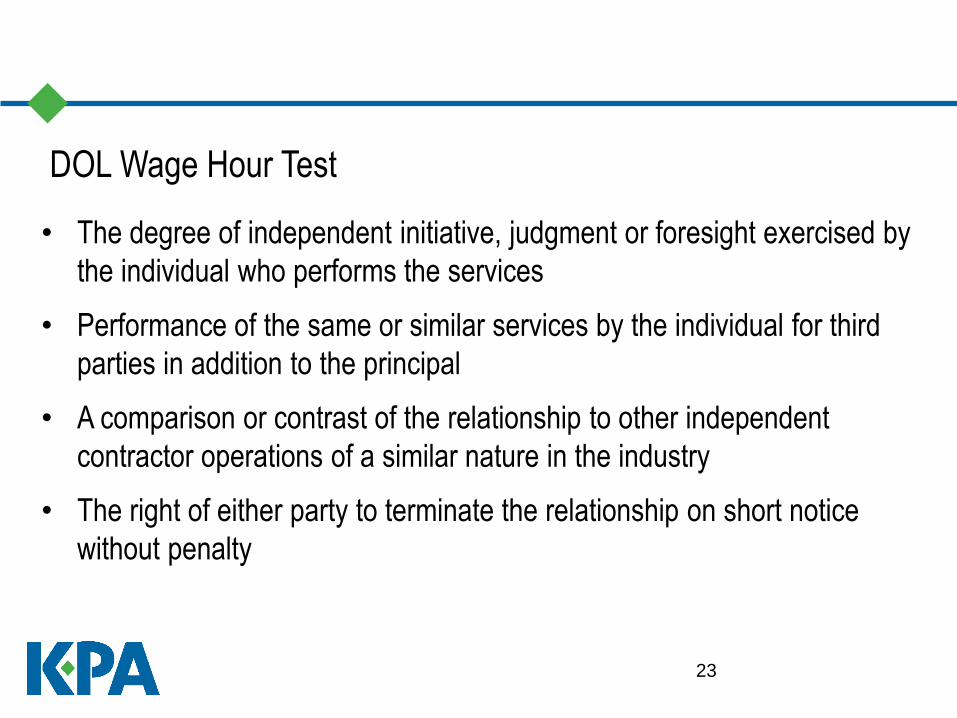

DOL Wage Hour Test

• The degree of independent initiative, judgment or foresight exercised by

the individual who performs the services

• Performance of the same or similar services by the individual for third

parties in addition to the principal

• A comparison or contrast of the relationship to other independent

contractor operations of a similar nature in the industry

• The right of either party to terminate the relationship on short notice

without penalty

24

Independent Contractors

State Law

• Employers should file informational returns for their

independent contractors (such as 1099’s) and comply with

state laws regarding workers’ compensation and

unemployment compensation

25

Scantland v. Jeffrey Knight, Inc.

11th Cir. July 16, 2013

• The technicians installed and repaired cable, Internet, and digital

phone services for the contractor.

• Collective Action FLSA case

• District Court ruled against Contractors

• 11th Cir used Six Factor Test

26

6 Factor Test: “ECONOMIC REALITY TEST”

• The nature and degree of the alleged employer's control as to the manner in which the work is to be performed

• Contractors were required to report to work at specific times, contractor received work orders, could not reject orders without threat of termination

• The alleged employee's opportunity for profit or loss depending upon his managerial skill

• Plaintiffs' opportunity for profit was largely limited to their ability to complete more jobs than assigned, which is analogous to an employee's ability to take on overtime work or an efficient piece-rate worker's ability to produce more pieces

• The alleged employee's investment in equipment or materials required for his task, or his employment of workers

• This factor weakly favored IC status

27

6 Factor Test: “ECONOMIC REALITY TEST”

• Whether the service rendered requires a special skill

• This factor weakly favored IC status

• The degree of permanency and duration of the working relationship

• Plaintiffs worked for Knight for an average of more than five years. Their contracts were for year terms, were automatically renewed, and were terminable only with thirty days' notice

• The extent to which the service rendered is an integral part of the alleged employer's business

• Knight relies on approximately five hundred technicians to perform installations and repairs in BHN customers' homes and businesses. Knight's website described its Installation Services department as the "backbone" of its business

28

Clincy v. The Onyx, N.D. Ga., No. 1:09-cv-2082, 9/7/11

• Exotic dancers at the Onyx sued their employer for misclassifying them at independent contractors

• Onyx classified the dancers as independent contractors, not employees

• Onyx never paid any of the dancers a wage or other compensation. Their earnings came directly from customers through table dances and tips

• Onyx would take certain deductions from the dancers’ pay, including stage fees, late fees, and fines for various infractions. In addition to the fines and fees, the dancers were required to share a percentage of their earnings with the club’s disk jockey and “house moms,” who oversee the dancers’ dressing room and help them prepare for their shifts

29

Clincy v. The Onyx, N.D. Ga., No. 1:09-cv-2082, 9/7/11

• Onyx had control of the dancers

• The dancers were required to work a minimum number of four shifts per week, and were fined if they were tardy or failed to show up to work

• The dancers also received written rules of conduct from the Club that set forth various guidelines covering dress and appearance, the cost of table-side and VIP dances, and conduct on stage

• Onyx argued that because the dancers had to buy uniforms and props and had opportunity to earn profits and losses they were ICs

• Court rejected this argument defendant is primarily responsible for drawing customers into the club

• In addition, decisions about marketing and promotions, pricing, and atmosphere are also made by the “defendants and/or their employees, not the entertainers.”

30

Clincy v. The Onyx, N.D. Ga., No. 1:09-cv-2082, 9/7/11

• COURT USED THE FOLLOWING TEST

• The degree to which the person is independent or is controlled by the employer with respect to the way the work is done

• The individual's opportunities for profit or loss

• The individual's investment in the facilities and equipment of the business

• The permanency and length of the relationship between the business and the individual

• The degree of skill needed to do the person's work; and

• If, and how much, the work performed by the individual is a major part of the employer's business

31

Clincy v. The Onyx, N.D. Ga., No. 1:09-cv-2082, 9/7/11

• Dancer’s investment is minor when compared to the club’s investment. Even though they have to pay a $350 licensing fee

• Stilettos and a smile are all that’s required --The Court also found that no special skills or training were required to be an exotic dancer at the Club. While the Club may prefer prior exotic dancing experience, the Club admitted that a dancers’ beauty is the primary qualification for the job

• The defendants’ final argument was that “nude dancing, while also contributing to the Club’s cache, is not its essential function. The Court, pointed out that the Club has three stages for dancing, its websites and billboards feature scantily clad women, it advertises in adult magazines, and it admits that it is an adult entertainment nightclub.

• The Court agreed with the plaintiffs’ assessment that to argue that nude dancers are not integral to the Club’s business is “absurd.”