emerging risks and the impact on … risks and the impact on your audit plan iia luncheon –...

TRANSCRIPT

Emerging Risks and theImpact on Your Audit Plan

IIA Luncheon – October 2012

www.pwc.com

Speakers

Denise McCurryPricewaterhouseCoopers Director

Husam BrohiPricewaterhouseCoopers Director

PwC 2October 2012

Agenda

Why are we here

Identification/Management of Emerging Risk

Potential Emerging Risk

PwCOctober 2012

3

Why are we here

Internal audit’s role in emerging risk

PwC 4October 2012

State of the internal audit profession study

• 8th Annual State of the Internal Audit Profession Study

• Focus on the rising importance of risk managementand the increasing expectations of internal audit’scontribution to the effort

• New methodology: For the first time, an “outside-in”look at the internal audit profession through points of

PwC

look at the internal audit profession through points ofview of:

- Over 660 stakeholders and 870 chief auditexecutives through an online survey

- Nearly 100 stakeholders, including board membersand executives in one-on-one interviews

- 64 countries globally

- 16 industry sectors

• Full study available at:www.pwc.com/us/2012internalauditstudy

5October 2012

Stakeholders value internal audit’s contribution…Importance of internal audit’s contribution to monitoringrisks

Important Very important

Fraud and ethics

Data privacy and security

Business continuity

Large program risk

Mergers, acquisitions, and JVs

Regulations and government policies 47%

58%

47%

54%

39%

26%

38%

30%

45%

39%

59%

71%

42%

54%

42%

49%

27%

30%

36%

26%

40%

38%

69%

67%

PwC 6October 2012

Regulations and government policies

Reputation and brand

Financial markets

New product introductions

Talent and labor

Energy and commodity costs

Government spending and taxation

Economic uncertainty

Commercial market shifts

Competition 38%

41%

46%

50%

56%

59%

48%

59%

64%

47%

5%

6%

5%

10%

9%

10%

19%

15%

21%

38%

34%

35%

40%

39%

44%

50%

46%

46%

50%

42%

7%

8%

10%

11%

11%

10%

19%

21%

26%

36%

0 20 40 60 80 100Stakeholders CAEs

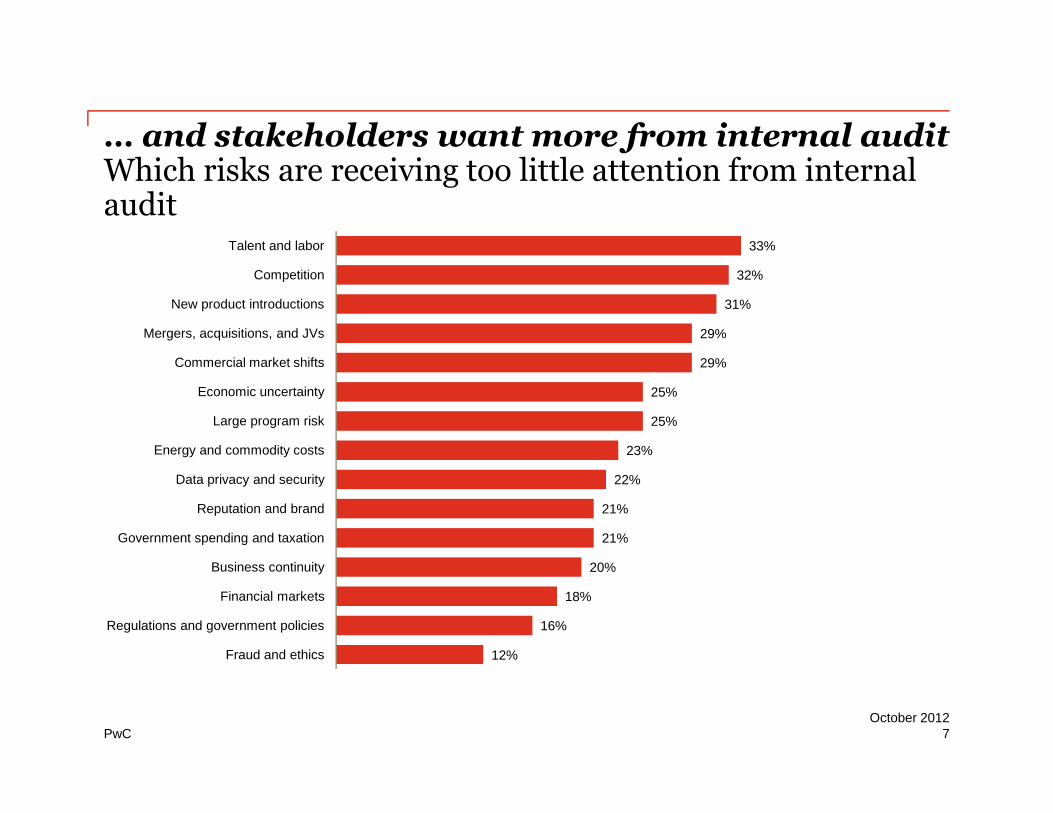

… and stakeholders want more from internal auditWhich risks are receiving too little attention from internalaudit

25%

29%

29%

31%

32%

33%

Economic uncertainty

Commercial market shifts

Mergers, acquisitions, and JVs

New product introductions

Competition

Talent and labor

PwC 7October 2012

12%

16%

18%

20%

21%

21%

22%

23%

25%

Fraud and ethics

Regulations and government policies

Financial markets

Business continuity

Government spending and taxation

Reputation and brand

Data privacy and security

Energy and commodity costs

Large program risk

Stakeholders want focus in all critical risk areasRisk areas in which stakeholders and CAEs want/plan toadd IA capabilities

32%

21%

27%

22%

31%

46%

34%

22%

24%

32%

47%

52%

Regulations and government policies

Reputation and brand

Talent and labor

Business continuity

Fraud and ethics

Data privacy and security

PwC 8October 2012

11%

14%

10%

10%

26%

29%

23%

29%

22%

7%

12%

10%

12%

27%

23%

21%

33%

24%

Government spending and taxation

Energy and commodity costs

Commercial market shifts

Competition

Mergers, acquisitions and JVs

New product introductions

Economic uncertainty

Large program risk

Financal markets

CAEs Stakeholders

Barriers to internal audit playing a moresubstantive role

43%

44%

57%

Lack of expertise

Lack of resources

Organizational/cultural resistance

PwC 9October 2012

6%

34%

35%

36%

43%

Other/none

Lack of budget

Lack of awareness of internal audit

Lack of mandate

Lack of expertise

Identification & Management ofemerging risk

Responding to stakeholder expectations

PwCOctober 2012

10

The new floor

The “new floor” for effective internal audit

Navigate the new risklandscape

• Think and act strategically

• Align resource allocations

• Leverage the second line ofdefense

Provide deeper insight

• Understand the business

• Deliver advice and bestpractices

• Leverage specialists

Cut through the clutter

• Build trust through ongoingdialogue

• Simplify reporting, make itconsumable

• Connect the dots

New risklandscape

Higherstakeholderexpectations

PwC 11October 2012

Eight core attributes

defense • Connect the dots

The foundation

1 Focus on criticalrisks and issues 2 Align value proposition with

stakeholders’ expectations

3 Match talent model tothe value proposition 4 Engage and manage

stakeholder relationships 5 Enable a clientservice culture

6 Deliver cost-effective services 7 Leverage technology

efficiently 8 Promote qualityimprovement and innovation

Traditional risk assessment and audit planning

Shareholder Value Based Approach

"Top-down" approach where coverage isdriven by issues that directly impactshareholder value, with clear and explicitlinkage to strategic issues of theorganization. The approach focuses onemerging risks and their impact on theorganization.

Identify Shareholder ValueCreating Activities

Understanding EnterpriseRisks (Strategic, Financial,Operations, Compliance)

Evaluate Impact toShareholder Value

PwC

Audit Plan

Traditional Approach

Traditional "bottom-up" approach based onstakeholder interviews and analysis. Focusis on coverage of identified riskareas, geography, andbusiness operations.

Evaluate Impactof Risks withinAudit Universe

Identify Risks (Financial,Operations, Compliance)

Define Audit Universe(e.g. geography, business unit, etc.)

12October 2012

A sample monitoring emerging risks

Continuousrisk assessment

• Periodic update of bottom-up and top-down risk assessment

• Provides early warning of high risk activities

• Can trigger changes to risk assessment and/or audit plan

Key attributes:

• Frequency and focus of all threeprocesses will be based on the priorityand risks identified foreach risk unit.

• Formal process for elevatingand reporting output from allthree processes.

Benefits/Attributes

PwC

Linkage to audit plan - Business/risk monitoring as required in the audit frequency and intensity matrix ideallyentails a well-developed continuous risk assessment and monitoring process for each risk unit

Continuous monitoring

Continuous auditing

• Involves monitoring of KRIs and KPIs

• Provides insights into current performance, changes,emerging risks, etc.

• Can trigger changes to risk assessment and/oran audit

• Can detect control deficiencies

• Can trigger and/or direct additionalaudit procedures

• Involves independent automated testing(e.g., use of CAATs)

• Findings require management responseand remediation

13October 2012

The current state of risk partner convergence

The business and regulatory environments have become increasingly complex, raising corporate risk profiles. Strategic consequences exist ifcompanies are unable to systemically manage governance, risk and compliance requirements effectively. Most attempts to date have been adhoc and produced limited results.

Internal audit Compliance Risk management Finance

PwC

SOXNew Regulation

Anti-fraud

Businesses

Internal audits New Product

development

Lack of coordination

Competition for attention

Risks/issues fallingthrough the cracks

Duplicate efforts

PrivacyCost Efficiency

14October 2012

How have organizations made it work

• Utilize a standard framework

• Consider structure across/within functions, businesses and regulatory requirements

• Align with regulatory expectations

• Choose the right place to start: new and developing functions, union of similar silos,areas ripe with duplication, integrated/related environments

PwC

Internal audit Compliance Risk management Finance

Businesses

Objective setting Risk ID/assess Control ID/assess Deficiency mgmt

15October 2012

Potential emerging risk

PwCOctober 2012

16

Current emerging risk

• Cloud computing

• Social media

• Customs import/export

• Cyber security

• Mobile devices

PwC

• Mobile devices

• IT governance

• Software asset management

• Spreadsheet management

• ERM

• New regulations

17October 2012

Cyber security

PwC 18October 2012

CEOs/Boards are no longer ignoring cybersecurity

Cyber Security is an enterprise-wide issue. Specific types of Cyber Securityrisks organizations are facing include:

• Increase in Privacy and Security regulatory mandates in recent years, as well asexpected changes in upcoming years.

• Boards are no longer willing to accept the risk that technology can pose to thebusiness.

PwC

business.

• Growing demand by business leaders to understand how security integrates withprivacy (“what” data is sensitive to the business) and security (“how” they protect thedata deemed sensitive).

• Increase in threats and vulnerabilities to sensitive data and corporate assets.

• Businesses continue to struggle to maintain accountability to their stakeholders andestablish effective strategies and standards for security risk management and privacycontrol activities.

19October 2012

CEOs/Boards are no longer ignoring cybersecurity

Security Hot Topics: Balancing Business Enablers vs Business Risks

Organizations looking to improve privacymanagement in the event of a breach "haveto continually plan and prepare.

PrivacySocial media can make or break a brandand the fine line between the two must bemanaged.

Social Media

Organizations in all industries are underincreased scrutiny by regulatoryRegulatory

Cloud computing, Mobile platforms andaccelerated product life cycles are just the

Mobile & EmergingTech

PwC

increased scrutiny by regulatorygovernance bodies.

Regulatory accelerated product life cycles are just thelatest contributors to risk of an enterprise.

Tech

Company’s reputation is paramount andthe risk of loss of sensitive customer datathreaten this fragile asset.

Data LossPrevention

A Major bank’s share price dropped threepercent after Wiki Leaks threatened to ‘takedown a major American bank and reveal anecosystem of corruption’ using documentsfrom an executive’s hard drive

Threat & VulnerabilityManagement

While risks associated with third partiescontinue to increase, many companies areless prepared to defend their data.

3rd Parties

The cyber threat landscape continues toyield an increasingly sophisticatedunderworld of criminals. Companies needto remain prepared for such cyber crises.

Cyber CrisisManagement

20October 2012

Mobile security

PwCOctober 2012

21

Level Set – Basic mobile device characteristics

• Generally, “mobile devices” refers to mobile phones, smart phones, tablets andspecialized mobile computing devices that primarily connect to a wireless carrier forcommunications. Excluded are traditional portable computing platforms such aslaptops and touch screen computers running a laptop operating system (i.e. Windows).

• Mobile devices will normally include a tailored purpose operating system such as iOS,Android, Blackberry OS, Windows Phone, Symbian or a proprietary device OS

PwC

• Mobile devices generally include the option to connect to available wireless broadbandservices in addition to the carrier network

• Many types of mobile devices will be able to download applications from the Internetor proprietary services unless specifically blocked by the device configuration

• Generally, users will be able to synchronize their devices with enterprise applicationsvia desktop/laptop computers and/or wirelessly

22October 2012

Mobile access at work – Use cases and risk profiles

• Organization provides only Internet access via Wi-Fi,normally via a guest network arrangement

• Organization provides access to e-mail and calendar viamobile browser (i.e. Outlook Web Access)

• Organization provides synchronization of e-mail andcalendar via a mobile application

Low Low

Fu

nct

ion

ali

ty

PwC

Ris

k

calendar via a mobile application

• Organization provides access to corporate applications anddata via a thin client model (e.g. Citrix)

• Organization provides access to corporate applications anddata with on-device data storage

• Organization develops and delivers custom applications tomobile users with data modification, direct input and on-device storage

Fu

nct

ion

ali

ty

High High

23October 2012

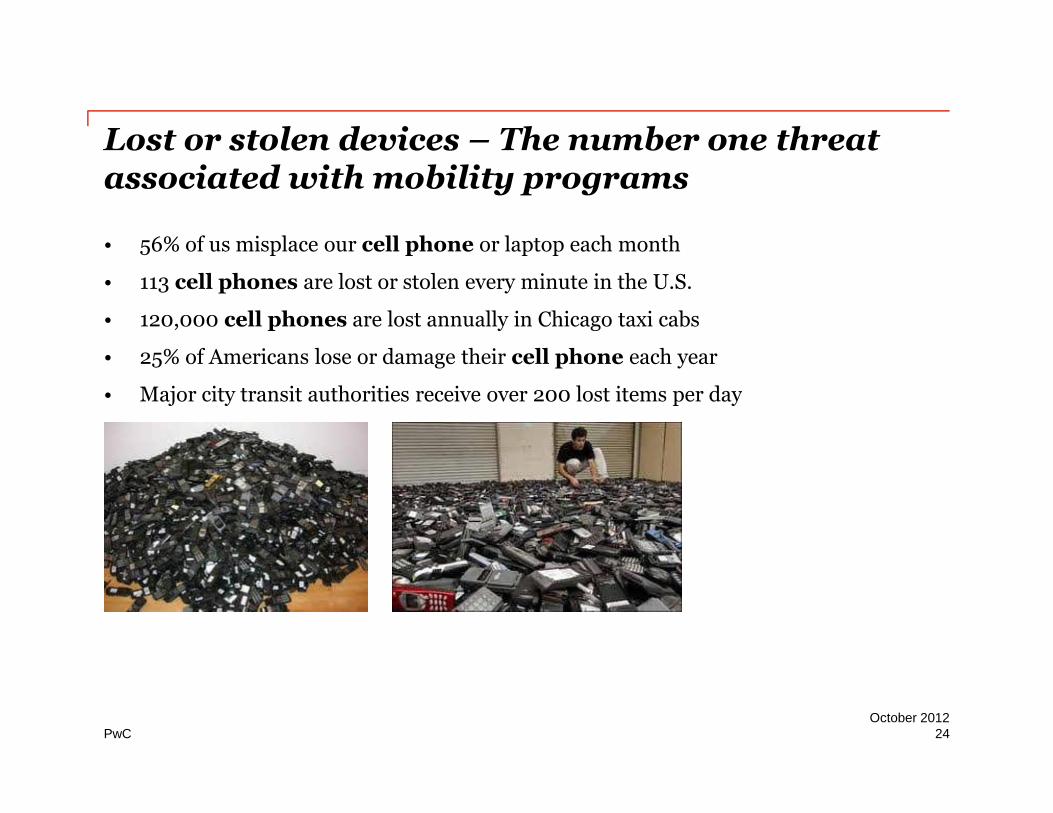

Lost or stolen devices – The number one threatassociated with mobility programs

• 56% of us misplace our cell phone or laptop each month

• 113 cell phones are lost or stolen every minute in the U.S.

• 120,000 cell phones are lost annually in Chicago taxi cabs

• 25% of Americans lose or damage their cell phone each year

• Major city transit authorities receive over 200 lost items per day

PwC

• Major city transit authorities receive over 200 lost items per day

24October 2012

“Bring your own” device security considerations

• Many organizations have now opted to allow employees to procure their own deviceswhich will ultimately connect to enterprise data and resources

• A “Bring Your Own” strategy presents additional security and privacy challengeswhich should be carefully considered prior to implementation

• Policies must be carefully crafted that mandate certain restrictions on the employee’saccess to corporate data with a personally owned device. Policies should coverminimum device security standards, use of anti-virus or endpoint security software

PwC

minimum device security standards, use of anti-virus or endpoint security softwarebased on legal or compliance requirements and clear language regarding consent forthe enterprise to access enterprise data on the device on a timely basis.

• The enterprise should aggressively monitor access by employees with personallyowned devices and consider restricting access to the minimum level required toperform the employee’s role (e.g. e-mail and calendar)

• The enterprise should reserve the right to rapidly bar access to data and resources byemployees with personally owned devices if necessary to protect enterprise data,address newly identified risks or to comply with legal or compliance requirements

• It is becoming increasingly hard to efficiently operate a BYOD program without usinga Mobile Device Management (MDM) platform

25October 2012

Common BYOD Challenges and risks

• BYOD increasingly reopens traditional debates on use of personally owned laptopsand computing equipment (i.e. Macs, external storage, printers)

• Use of personally owned devices blurs owner responsibilities regarding devicesupport, ownership of data and how much access and control the organization mayhave to data on the device

• There is still frequent resistance by users to sign acknowledgements or acceptable useagreements (“It’s my device!”)

PwC

agreements (“It’s my device!”)

• Users want the latest smartphone, regardless of what operating system or features theorganization is able to support

• Users have little incentive to report lost or stolen devices on a timely basis. In manycases the organization will only learn of a lost device when the user requests access fora new device

• If the user cancels carrier service, it is impossible to complete over the air devicewiping

26October 2012

Mobile security – Controls

Policies and Procedures *

• Acceptable Use Policy

• Data Classification and Handling Policy

• Social Media Policy

• Information Security

• Policy

• Device Loss Process/Workflow

User Acknowledgement and Opt-In

• Signed User Acceptance Form

• Clear Instructions For Reporting Loss of Device

• Consent to Geo-Track (As Applicable)

• Potential Tax Impact (Certain States and Countries)

• Specific Security Training for Users

• Limits on Supported Devices

PwC

• Device Loss Process/Workflow

• Incident Management Plan

• Limits on Supported Devices

Technical Controls and Platforms

• Blackberry Enterprise Server• Exchange ActiveSync• Vendor Security Controls• On Device Encryption• Mobile Management Platform (MDM)• Mobile Device Anti-Virus/Malware (As Warranted)

Auditing, Logging and Monitoring

• Periodic Audits of Mobile Program and Key Controls

• Integration with Log Management and SIEM Platforms

• Periodic Survey of Users to Confirm Compliance

Risk ReductionOptions

* With Specific Content for Mobile Device Use

27October 2012

Social media

PwCOctober 2012

28

What is social media today

It is a channel for engagement that enables involvement, interaction,intimacy and influence between you, your customers and your employees

Outlet Type Microblogs Blogs Media Sharing SocialNetworks

Collaboration

Description Content is muchshorter than ablog.

Publishingplatforms to postfree-form UserGenerated

Share variousmedia types(photo, video,slides)

Onlinecommunity ofinterest withblogging and

Enterpriseplatforms to enableexternal or internalcollaboration.

PwC

GeneratedContent (UGC)

slides) blogging andsharing features.

collaboration.

KeyCharacteristics

Limited amountof characters;Strong following;extensiveoutreach.

Un-edited usercontent posted;User can makemoney blogging.

Media oftenranked bypopularity basedon views.

Hybrid platformscan share fromother outlets.

Private/publiccommunities fortargeted objectives.

Popular Outlets

29October 2012

Social media in the news

Social media opens the door to new methods of engaging customers and employees. Therapid adoption of social networking, blogs and user-created videos is revolutionizingcustomer expectations of how they want to interact with each other.

Unfortunately, there are also implications, including reputational risk, regulatoryrequirements, intellectual property, employee relations, informationsecurity and international considerations.

PwC

• Multi-million dollar headache for a large healthcare as a result of social media revoltover an offensive ad campaign.

• Food chain loses 10% of its value in one week, resulting in multi-million dollar losses,due to negative videos posted on YouTube.

• Several banks face severe security challenges – fake Facebook pages and phishing.

30October 2012

Social media: New rules and new risks

Organizations are beginning to implement strategies to keep pace with employeeadoption of mobile devices and social networking, as well as use of personal technologywithin the enterprise. Yet much remains to be done: Less than half of respondents haveimplemented safeguards to protect the enterprise from the security hazards that mobiledevices and social media can introduce.

50%

PwC

43%

37%

32%

10%

20%

30%

40%

Have a security strategy foremployee use of personal devices

Have a security strategyfor mobile devices

Have a security strategyfor social media

Question 17: “What process information security safeguards does your organization currently have in place?” (Not all factors shown. Total doesnot add up to 100%.)

31October 2012

Typical social media risks

Data Security andProtection

1. Identify theft

2. Malware propagation

3. Social engineering

Financial andOperational

1. Lack of centralizedgovernance

2. Measuring success

Legal &Compliance

1. Foreign and domesticprivacy laws

2. Data retention

Information risk imperatives

Reputational &Perception

1. Reputational threat

2. Lack of Monitoring

3. Negative brand

PwC

3. Social engineering

4. Disclosure ofintellectual property orother sensitiveinformation

5. Unauthorized accessand breaches throughphishing, spam, andtrojan horses.

3. Lack of employeeproductivity

4. Regulatoryinquiries andpossible fines

3. Regulatory compliance(PCI, FINRA, FDA)

4. Content ownership

5. Civil litigation

6. Lack of separation ofpersonal andprofessionalcommunication

3. Negative brandimpacts

4. Crisis management

5. Insufficient employeetraining

32October 2012

Social enterprise

Social Media Governance and Executive Sponsorship

Social Media Strategy, Objectives, and Policy

PwC 33October 2012

Social Media Strategy, Objectives, and Policy

BusinessSponsorship

Marketing &Communications

HumanResourcesand Legal

InformationSecurity

Risk, Compliance,and Audit

• Risk assessments• Risk management• Regulatory

compliance• Internal controls• Internal audit

enforcement

• Authentication andauthorization

• Certification &accreditation

• Monitoring &incident response

• Vulnerabilityscanning

• Terms of use• Code of conduct and

staff rules• Partnership

agreements• Training and

awareness

• Social mediauniverse and policy

• Communitymanagement

• Brand management• Crisis management

• Business objectivesand KPIs

• Monitoring metricsand ROImeasurement

• Informationmanagement

• Staffing

Cloud computing

PwCOctober 2012

34

Introduction to cloud computingOverview

What is cloud computing?

Cloud computing is defined by the US National Institute of Standards and Technology(NIST) as a:

Model for enabling convenient, on-demand network access to a shared pool ofconfigurable computing resources (e.g., networks, servers, storage, applications, andservices) that can be rapidly provisioned and released with minimal management effort

PwC

services) that can be rapidly provisioned and released with minimal management effortor service provider interaction.

• Cloud computing is often likened to utility service. Utilities, such as electricity, areavailable as needed and users only pay for the amount used.

• Cloud Service Providers (CSP’s) have adopted the bill-for-service model, whichenables companies to save money by not paying for unused or underutilizedequipment, power, etc.

• Particular service offerings vary, but the largest cloud services providers (such asAmazon.com, Google, and Salesforce.com) provide computing services on what isessentially a commoditized basis – much like a utility company provides water, gas,or electricity

October 201235

Threats to cloud computing

• Compliance Complexity – Moving data to a 3rd party cloud provider does notrelieve the organization of its compliance responsibilities. A cloud based data breachcan negatively impact both the organization and the cloud provider.

• Cloud Resilience – Moving critical data to the cloud – and then having a cloudprovider go out of business or be acquired – will have some level of disruption on theorganization.

PwC

• Data Format Impact – Some cloud providers have proprietary data formats forcloud based data. This can add complexity to change providers or terminate contractsfor non-performance.

• Security Expertise – The level of in-house security and monitoring expertise varieswidely between cloud providers. This should be a key consideration during cloudprovider selection.

• Trust But Verify – Organizations tend to lower their guard once they outsource to acloud provider. In reality, organizations should increase their oversight andmonitoring activities.

October 201236

Service delivery models and deployment modelsOverview

Three Service Delivery Models:

1. Infrastructure as a Service (IaaS)

2. Platform as a Service (PaaS)

3. Software as a Service (SaaS)

Four Deployment Models:

PwC

Four Deployment Models:

1. Private Cloud

2. Public Cloud

3. Hybrid Cloud

October 201237

Considerations for internal audit

Regulatory/Legal:

• Physical location of data storage

• Ownership of data in the cloud

• Notifications of breaches/incidents

• Responsibility for non-compliance

PwC

• Responsibility for non-compliance

• Impact on SOX requirements

Due Diligence:

• Right to audit

• Assured continuity

• Security policy and process transparency

• Vendor selection/management process

October 201238

Cloud computing – Controls

Policies and Procedures *

• Policy for Approval of Virtualization/Cloud

• Acceptable Use Policy

• Data Classification and Handling Policy

• Social Media Policy

• Information Security Policy

• Incident Management Plan

Contractual Controls

• Clear delineation of responsibilities betweenorganization and cloud provider

• Standardized or generally accepted language in cloudcontracts

• Service Level Agreements (SLAs) that can bemeasured and enforced

• Right to Audit Clause

PwC

• Incident Management Plan

Technical Controls

• Access to cloud provider’s dashboards and monitoringtools

• Plug Ins to Organization’s Ticketing System• Real Time Access to Cloud Provider’s Change and

Issue Management platform• Requirement for Vulnerability Scans and

Attack/Penetration Testing

Other Considerations

• Exit strategy at end of contract

• Process to get data back from provider

• Contingency plan for data format conversion

• Contingency plan if cloud provider is acquired or goesout of business

• Cure provisions in the event of a data breach

Risk ReductionOptions

* With Specific Content for Virtualization/Cloud

39October 2012

Questions

PwCOctober 2012

40

© 2012 PricewaterhouseCoopers LLP. All rights reserved. PwC refers to the United Statesmember firm, and may sometimes refer to the PwC network. Each member firm is a separatelegal entity. Please see www.pwc.com/structure for further details.