email: [email protected] email: [email protected]...

TRANSCRIPT

James D. Gilson (5472)Zachary T. Shields (2947)Marc Turman (11967)CALLISTER NEBEKER & McCULLOUGHZions Bank Building, Suite 90010 East South TempleSalt Lake City, Utah 84133Telephone: (801) 530-7300Facsimile: (801) 364-9127Email: [email protected] Email: [email protected]: [email protected]

Attorneys for the Warner Parties

UNITED STATES DISTRICT COURT FOR THE DISTRICT OF UTAH

CENTRAL DIVISION

SECURITIES AND EXCHANGECOMMISSION,

Plaintiff,

v.

MANAGEMENT SOLUTIONS, INC., aTexas corporation; WENDELL A.JACOBSON; and ALLEN R. JACOBSON,

Defendants.

SUR-REPLY MEMORANDUM INOPPOSITION TO RECEIVER’SMOTION TO CONFIRM A PRIVATESALE OF STONE BROOK ANDTETONIAN PROPERTIES

Civil No. 2:11-cv-01165

Judge Bruce S. Jenkins

Intervening Plaintiffs B.C. Warner Investments, L.C.; SLEA 423 L.L.C.; B.C. Warner

Revocable Trust; BCW - S.F. L.L.C.; Bart C. Warner; and James N. Warner (collectively,

"Warner" or the “Warner Parties”), through counsel, hereby file this Sur-Reply Memorandum in

opposition to the Receiver’s Motion to Confirm Private Sale of Stone Brook and Tetonian

Properties and to Approve Sale Fee and Clear of Liens With Valid Liens to Attach to Proceeds

[Docket No. 1588] (the “Motion” or “Private Sale Motion”), as follows:

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 1 of 24

2616269.1

BACKGROUND

In his Reply Memorandum filed on March 11, 2014, the Receiver John A. Beckstead (the

“Receiver”) questioned the validity of Warner’s claim to ownership of a 49.5% tenant-in-

common interest of the Tetonian Apartments property. At the hearing held the following day,

March 12, 2014, the Court raised additional issues regarding the validity of Warner’s ownership

interest. Warner has not had an opportunity to respond to the new issues raised by the Receiver

and the Court. Accordingly, in anticipation of the continued hearing on this matter, Warner

hereby files this Sur-Reply Memorandum for the purpose of providing a brief overview of the

legal authorities relevant to the present dispute.

DISCUSSION

I. Burden of Proof

In questioning the validity of Warner’s ownership of the property, the Receiver bears the

burden of proof to show the invalidity of Warner’s Special Warranty Deed by clear and

convincing evidence. (See Grgich v. Grgich, 2011 UT App 214, 262 P.3d 418, 422 (“party

attacking the validity of a written instrument must do so by clear and convincing evidence.”);

26A C.J.S. Deeds § 459 (“A deed is presumed to be that which it purports to be, and the burden

is on the one asserting otherwise to prove otherwise, by clear and convincing evidence.”); 5

Causes of Action 2d 471 (“A party asserting the invalidity of a deed for non-delivery ordinarily

has the burden of proving that there was no effective delivery of the deed.”); 26A C.J.S. Deeds §

478 (“A deed which is regular on its face is clothed with a presumption of validity, and where it

is attacked as invalid, the burden of proof rests on the person making such attack to establish the

invalidity” (footnotes omitted))).

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 2 of 24

3616269.1

II. Delivery

In determining whether there has been “delivery” of a deed, the controlling factor is the

intent of the parties:

Delivery of a deed is a question of intent. A conveyance is valid only upondelivery of a deed with present intent to transfer. Thus, the intention of theparties is an essential and controlling element of delivery of a deed, andsuch intention may be inferred from the circumstances. Intention has beencalled the "essence of delivery," and not only is it often the determiningfactor among other facts and circumstances but also it is the crucial testwhere constructive delivery is relied upon.

23 Am. Jur. 2d Deeds § 105 (2014).

The real test of the delivery of a deed is this: Did the grantor by hisacts or words, or both, intend to divest himself of title? If so, thedeed is delivered.

Garrett v. Garrett, 154 Idaho 788, 791-92, 302 P.3d 1061, 1064-65 (2013) (quotation omitted).

(See also Barmore v. Perrone, 179 P.3d 303, 307 (Idaho 2008) ("The controlling element in the

question of delivery is the intention of the grantor and grantee." (quotation omitted))).

Because the intention of the parties is the essence of delivery, it is not necessary that

there be an actual physical transfer of the deed from the grantor to the grantee to accomplish

delivery. The Idaho Supreme Court has explained that a deed may be validly delivered

notwithstanding the fact that there was no manual delivery of the deed:

Delivery is merely a symbol indicating, as interpreted by the courts,complete and fixed relinquishment of title by the grantor to the grantee. Such delivery may be actual or constructive. . . .

The deducible rule is that, even though the grantor retain physicalpossession of the deed, if surrounding and attendant facts andcircumstances are sufficient to clearly show an irrevocable intent totransfer the title, and there are some physical acts supporting such

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 3 of 24

4616269.1

intention and fixing with definiteness symbolical or constructive delivery,the requirements for the transfer of the title have been complied with.. . .. . . The absence of actual delivery does not disprove constructivedelivery.

Hogg v. Wolske, 142 Idaho 549, 556, 130 P.3d 1087, 1094 (2006) (formatting modified and

internal citations and quotations omitted). (See also Flynn v. Flynn, 104 P. 1030 (Idaho 2009)

(finding that there was a delivery of the deed notwithstanding that the deed remained in the

possession of the grantor's attorney because the evidence showed that the grantor intended to

divest himself of title to the property when he signed the deed); 129 A.L.R. 11 (2014) (stating

that “a manual delivery is not essential to effectuate a valid legal delivery if such acts or words

indicate an intent on the part of the grantor to relinquish all dominion or control over the deed,

and to have it become presently effective as a conveyance of title” and citing numerous cases);

Garrett v. Garrett, 302 P.3d at 1065 (“A deed does not need to be delivered directly to the

grantee to be effective.”).

III. The Effect of Failing to Record a Deed

As set forth in Warner’s initial opposition memorandum, Utah law provides that the

failure to record a real property deed does not affect the validity of such deed – except with

respect to an intervening bona fide purchaser who has purchased the property for value and

without knowledge of the unrecorded interest. (See Memorandum in Opposition to Receiver’s

Motion to Confirm a Private Sale of Stone Brook and Tetonian Properties [Docket No. 1621], at

pp. 8-9). Further research reveals that this principle is likewise true under Idaho law. (See

Hartley v. Stibor, 96 Idaho 157, 160, 525 P.2d 352, 355 (1974) (“recordation is not essential to

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 4 of 24

5616269.1

the validity of a deed (absent intervening rights)”)). Indeed, this principle is basic, horn-book

law recognized across the country:

Since recording is required for the protection of third persons, therecording statutes do not change the rule that an unrecorded deed,mortgage, lease, or other instrument affecting the title to land is valid asbetween the parties thereto and against everyone else who is not within theprotection of the recording laws. The fact that a deed is unrecorded doesnot affect the efficacy or validity of the instrument as between the grantorand grantee or those with notice. Indeed, even an unrecorded instrument isfully enforceable between the parties to the transaction.

66 Am. Jur. 2d Records and Recording Laws § 117 (footnotes omitted).

Recording a deed is not necessary to effectively deliver it. The fact that adeed is not recorded, or intended by the grantee to be recorded, does notshow a lack of delivery by the grantor.

26A C.J.S. Deeds § 71 (footnotes omitted).

IV. A Receiver is Not a Bona Fide Purchaser

A review of the relevant legal authorities shows that a receiver does not hold the status of

a bona fide purchaser. (See 75 C.J.S. Receivers § 94 (“A receiver is in no sense a bona fide

purchaser and does not and cannot acquire any other, greater, or better interest than the debtor

had in the property.” (footnotes omitted)); In re Careful Laundry, 204 Md. 360, 366, 104 A.2d

813, 817 (1954) (“neither assignees nor receivers are bona fide purchasers”); Chalmers &

Williams v. Surprise, 70 Ind. App. 646, 123 N.E. 841, 844 (1919) (receiver does not occupy

relationship of bona fide purchaser).

The general rule is that a receiver “stands in the shoes” of the entity over whom the

receivership was established, and holds only the rights of such entity. 75 C.J.S. Receivers § 94

(“the receiver has been held to stand in the shoes of the debtor or insolvent, having the same

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 5 of 24

6616269.1

right which the latter would have had and being unable to set up any rights against claims which

the debtor could not have set up. A receiver can have no greater rights than the creditors whom

he or she represents” (footnotes omitted)). Some courts have expanded a receiver’s rights to

allow the assertion of claims on behalf of creditors, but such expansion does not go so far as to

grant the receiver the rights of a hypothetical bona fide purchaser. (See Camerer v. California

Sav. & Commercial Bank of San Diego, 4 Cal. 2d 159, 172, 48 P.2d 39, 46 (1935) (“although the

receiver is in exceptional circumstances accorded rights denied to the insolvent, the receiver

does not have the status of a bona fide purchaser for value.”).

In this regard, there is a significant difference between the powers granted to a receiver

and the powers granted to a trustee in bankruptcy. The U.S. Bankruptcy Code contains a

specific provision which grants a bankruptcy trustee the “rights and powers” of a “bona fide

purchaser of real property . . . whether or not such a purchaser exists.” (See 11 U.S.C. §

544(a)(3)). To the Warner Parties’ knowledge, Congress has not seen fit to enact such a statute

granting such powers to receivers outside of bankruptcy court. The absence of such a statute

confirms that receivers are not bona fide purchasers, and that they cannot cut off the rights of

deedholders with unrecorded deeds.

V. The Receiver Has No Authority To Sell Non-Estate Property

A receiver’s authority over property is limited to the property of the receivership estate,

and the receiver does not have authority to sell property belonging to third parties who are not

subject to the receivership. (See 75 C.J.S. Receivers § 94 (“A receiver generally has no right to

property which does not belong to the individual or corporation over whose estate the receiver

was appointed”); Perry Ctr., Inc. v. Heitkamp, 1998 ND 78, 576 N.W.2d 505, 511 (“A receiver

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 6 of 24

1 The statute provides that a bankruptcy trustee may sell the interests of non-debtor co-owners “only if” four different tests are met:

(1) partition in kind of such property among the estate and such co-ownersis impracticable;(2) sale of the estate's undivided interest in such property would realizesignificantly less for the estate than sale of such property free of theinterests of such co-owners;(3) the benefit to the estate of a sale of such property free of the interestsof co-owners outweighs the detriment, if any, to such co-owners; and(4) such property is not used in the production, transmission, ordistribution, for sale, of electric energy or of natural or synthetic gas forheat, light, or power.

11 U.S.C.§ 363(h). Moreover, a bankruptcy trustee may not obtain court authority to sell a co-owner’s property through the mere filing of a motion, but is required to initiate a separateadversary proceeding against the co-owner. (See Fed. Rule Bankr. Pro. 7001(3); In re Lyons,995 F.2d 923, 924 (9th Cir. 1993)).

7616269.1

has no right to property which does not belong to the entity over which the receiver was

appointed.”); State ex rel. Pancol v. Cleveland, 241 Ind. 206, 210, 171 N.E.2d 255, 257 (1961)

(“A receiver has no right to property which does not belong to the debtor for whose property he

is the receiver.”)).

Again, in this regard there is a significant difference between the authority of a

bankruptcy trustee and a receiver. The U.S. Bankruptcy Code contains a specific statute which

grants a bankruptcy trustee, in certain limited circumstances, the power to sell the interests of

those who are co-owners of property with the bankruptcy estate. (See 11 U.S.C. § 363(h)).1

Congress has not enacted a statute which grants such authority to receivers.

In the Receiver’s Reply Memorandum, at p. 7, the Receiver cites to four cases which

purport to support his assertion that he has the legal authority to sell Warner’s property interests

without Warner’s consent. In fact, none of the cases support such assertion. Three of the cases

are bankruptcy cases which are governed by Section 363 of the Bankruptcy Code. Such cases

are inapplicable in the receivership context where there is not a statute equivalent to Section 363

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 7 of 24

2 The Affidavit shows that the source of the consideration was Warner’s pro-rata share ofthe proceeds from the sale of another parcel of property in which Warner had an interest,Sycamore Farms, which sale was an arm’s length transaction to a third party not related to theJacobsons. It further shows that Warner’s interest in Sycamore Farms originated in 2005 fromfunds which Warner received from the sale of a Ford automobile dealership unrelated theJacobsons.

8616269.1

of the Bankruptcy Code granting receivers authority to sell a co-owner’s property. The fourth

cases cited by the Receiver is an unpublished case that is inapplicable to the circumstances of the

present case. (See In re Orchards Vill. Investments, LLC, 09-30893-RLDLL, 2010 WL 143706

at *4-5 (Bankr. D. Or. Jan. 8, 2010)). That case did not address the issue of a receiver’s

authority to sell a co-owner’s property. Rather, it addressed the extent of the coverage of the

initial receivership order – finding that such order impliedly included certain limited partnerships

within the property of the receivership estate.

Thus, the Receiver has provided no authority that is contrary to the legal authorities

(cited above) establishing that a receiver has no authority to sell the property of co-owners who

are not part of the receivership estate.

VI. The Receiver’s Motion Should be Denied

Accompanying this Sur-Reply is the Affidavit of Wendell Jacobson, dated March 17,

2014. Such Affidavit confirms the validity of Warner’s ownership of the property. It confirms

that there was a legitimate sale of the property from Tetonian Properties to Warner entity SLEA

423, LLC, in 2009, which included the execution of sale documents and a Special Warranty

Deed. It confirms that Warner provided appropriate consideration for the purchase.2

Importantly, it confirms that it was the intent and understanding of the parties that a conveyance

of ownership of the property from Tetonian Properties to Warner took place.

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 8 of 24

3 This includes copies of the following documents: a signed purchase contract, a signedsettlement statement, a copy of the signed Special Warranty Deed, and annual real property taxstatements indicating a 49.5% real property ownership interest.

9616269.1

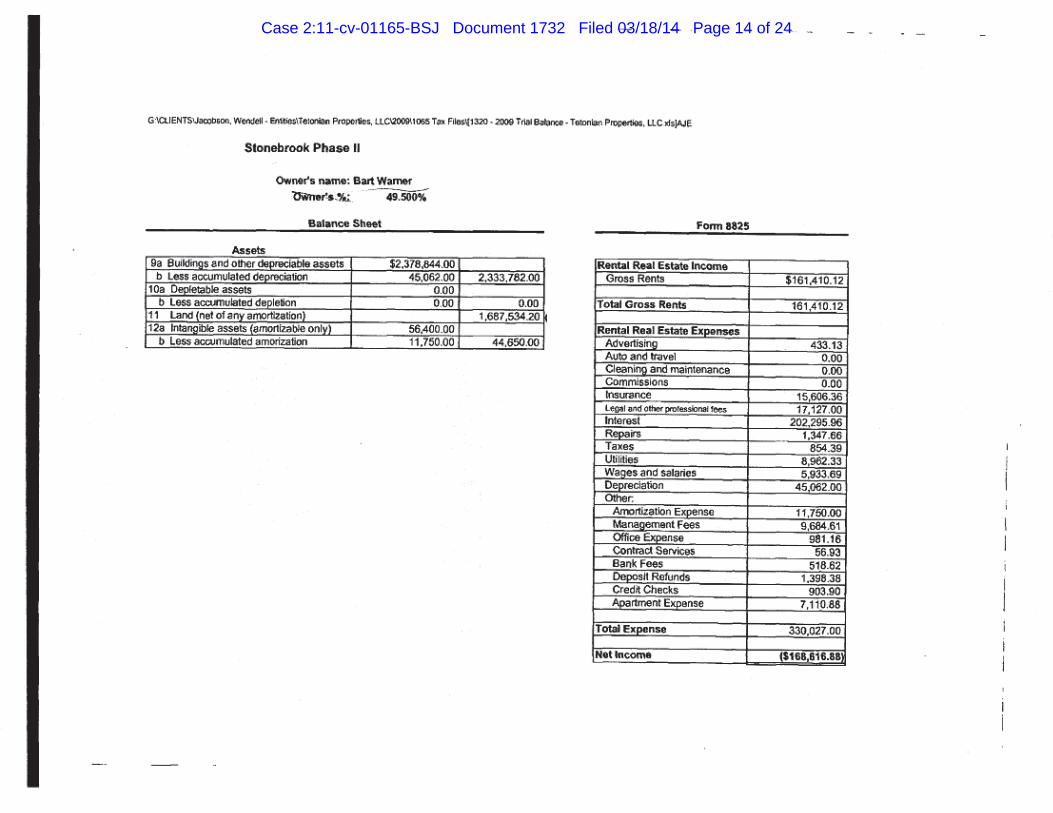

Moreover, the fact that Warner became an actual owner of the property is shown by

Exhibits “A” through “D” attached hereto. Such documents are the annual tax statements for the

Tetonian Apartments property, which Tetonian Properties and the Receiver provided to Warner

each year following the purchase of the property (for the tax years 2009 to 2012). Such

documents confirm that Warner was the owner of a 49.5% real property interest, that it shared in

the expenses and income of the property on a pro-rata 49.5% basis, and that it paid taxes

accordingly.

Thus, in applying the law to the facts of this case, it is apparent that Warner’s property

interest is valid. Given the testimony of the parties regarding their intent in selling the property,

and given the documentary evidence supporting such testimony,3 it is clear that the sale took

place and that there was legal delivery of the deed.

Under the law, the fact that the Deed was not recorded is of no consequence as between

Warner and the seller Tetonian Properties. Moreover, because the Receiver does not have the

status of a bona fide purchaser, the unrecorded deed is valid and binding as to the Receiver as

well.

Accordingly, because Warner’s property interest is valid, such property is not an asset of

the receivership estate, and the Receive has no authority to sell such asset.

The Receiver’s requests that the Court order that Warner’s property interest be

immediately sold – before the Court has even had an opportunity to fully adjudicate the validity

of Warner’s property interest. Such approach is backwards. It is based upon an unfounded

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 9 of 24

4 Even if the authority of the Bankruptcy Code were applicable as to receivers (which it isnot), the Receiver would not be authorized to sell Warner’s property under such statute. TheReceiver could not obtain such relief by motion, but would be required to file a Complaint in anAdversary Proceeding – which would give Warner appropriate due process with a reasonabletime to defend the validity of its ownership (something which has been denied to Warner in thepresent Private Sale Motion). Moreover, the Receiver would have the burden of establishingeach of the four requirements necessary for relief under Section 363(h) of the Bankruptcy Code –which the Receiver has not done in the present Motion.

5This is especially true in the present case, where the Receiver has done almost nothing tomarket the property, and is attempting to sell the property for an amount which is substantiallylower than what could be obtained with a reasonable marketing efforts.

10616269.1

assumption that Warner’s property interest in invalid, and that Warner has the burden of proof to

establish the validity of its ownership. In fact, as discussed above, Warner’s ownership is

presumed to be valid until and unless it is proven otherwise. Moreover, the Receiver has the

burden of proof to establish the invalidity of Warner’s property interest.

Until and unless the Receiver meets his burden to establish that Warner’s property

interest is invalid – which he has not done – the Receiver lacks the authority to sell such

property. The proposal to sell first, and figure out ownership later is improper and contrary to

law. Rather, the law is clear that a receiver may not sell property which is not an asset of the

receivership estate. Unlike bankruptcy trustees, who are given authority under an express

statute, receivers have no authority to sell the property of co-owners.4 Moreover, it would be

greatly inequitable to seize Warner’s property and then force Warner to accept a share of the

proceeds of sale in the event Warner is subsequently successful in establishing the validity of its

ownership of the property.5 To assert control over Warner’s property without consent and then

force Warner to accept cash payment contrary to Warner’s wishes would constitute conversion

and an unconstitutional taking.

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 10 of 24

11616269.1

There is no reason to hastily proceed with the proposed sale given Warner’s property

rights. Rather, until and unless the Receiver meets his evidentiary burden to disprove the

validity of Warner’s property rights – after giving Warner full due process of law in which to

defend its property interests – the Receiver should not be permitted to sell property that does not

belong to the receivership estate.

CONCLUSION

For the above-stated reasons, Warner respectfully requests that the Receiver’s Private

Sale Motion be denied.

Dated: March 18, 2014 CALLISTER NEBEKER & McCULLOUGH

/s/ James D. Gilson James D. GilsonZachary T. ShieldsAttorneys for the Warner Entities

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 11 of 24

12616269.1

CERTIFICATE OF SERVICEI hereby certify that I caused a true copy of the foregoing SUR-REPLY

MEMORANDUM IN OPPOSITION TO RECEIVER’S MOTION TO CONFIRM A

PRIVATE SALE OF STONE BROOK AND TETONIAN PROPERTIES to be delivered

via ECF notification to all counsel of record in this matter (Civil No. 2:11-cv-01165), and to the

following parties by U.S. Mail, on this 18th day of March, 2014.

Greg B. BaileyPO BOX 298FOUNTAIN GREEN, UT 84632

Douglas M. DurbanoDURBANO LAW FIRM476 W HERITAGE PARK BLVDSTE 200LAYTON, UT 84041

Matthew L. Moncur BALLARD SPAHR LLP (UT)201 S MAIN STE 800SALT LAKE CITY, UT 84111-2221

/s/ James D. Gilson

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 12 of 24

EXHIBIT “A”

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 13 of 24

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 14 of 24

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 15 of 24

EXHIBIT “B”

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 16 of 24

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 17 of 24

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 18 of 24

EXHIBIT “C”

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 19 of 24

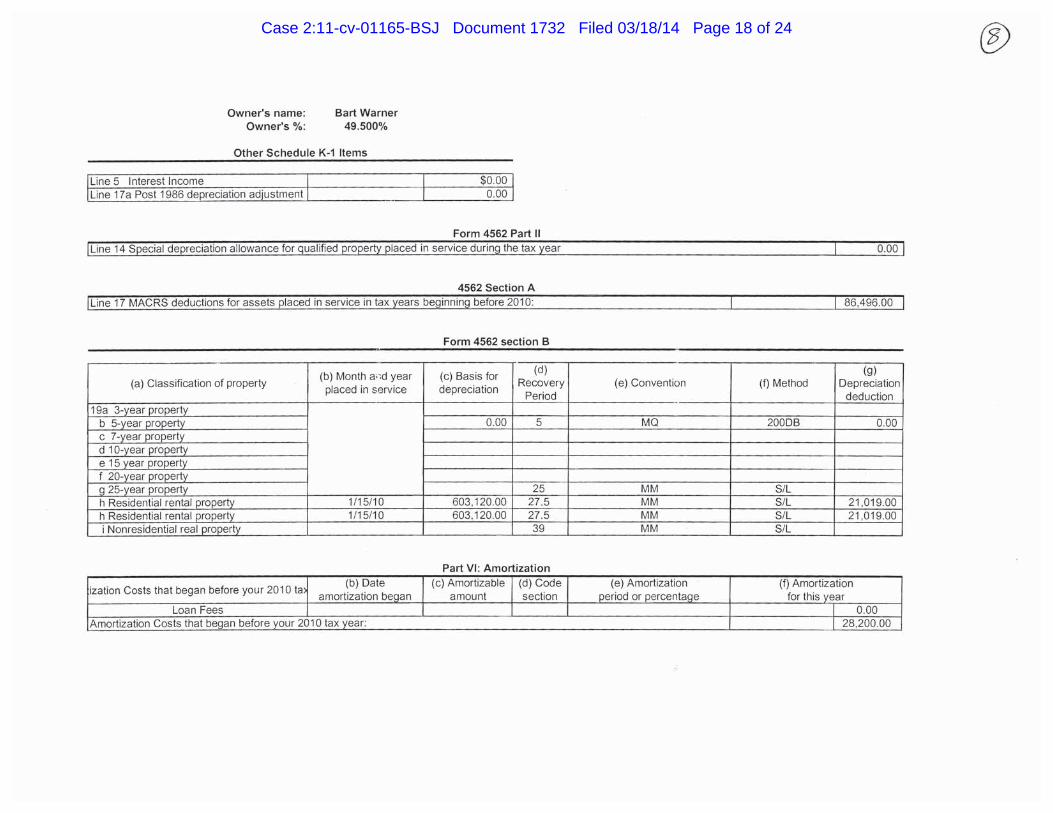

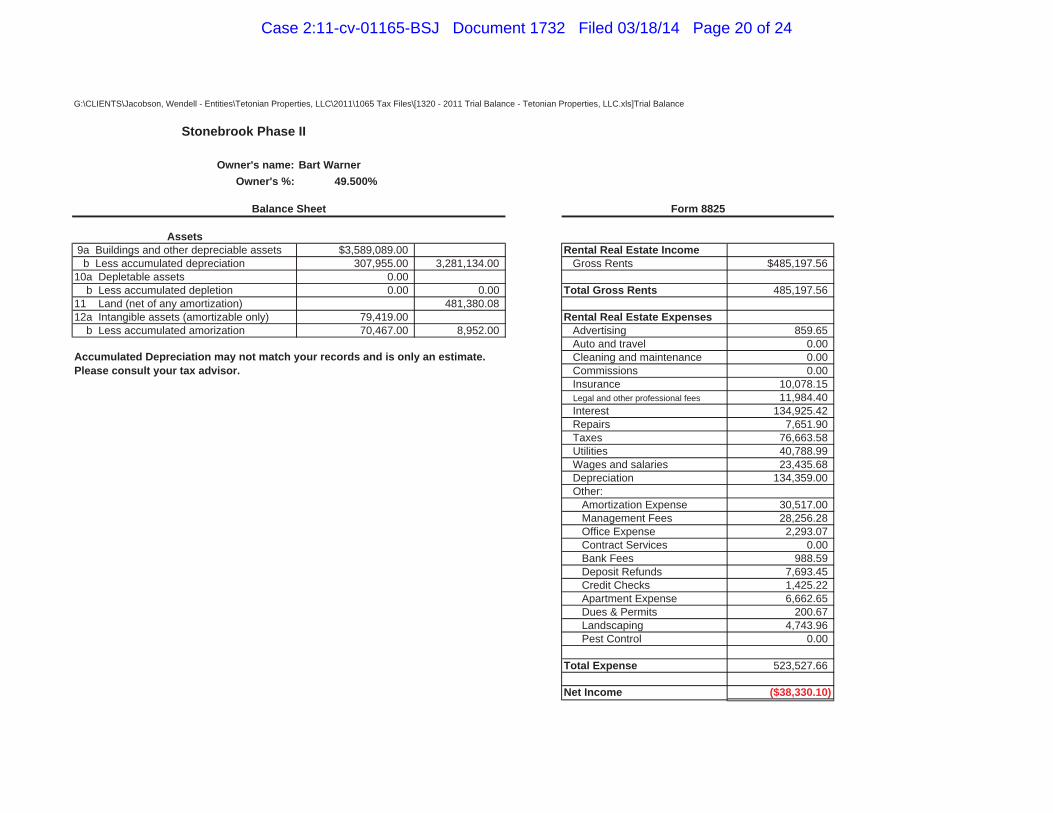

G:\CLIENTS\Jacobson, Wendell - Entities\Tetonian Properties, LLC\2011\1065 Tax Files\[1320 - 2011 Trial Balance - Tetonian Properties, LLC.xls]Trial Balance

Owner's name: Bart WarnerOwner's %: 49.500%

Assets 9a Buildings and other depreciable assets $3,589,089.00 Rental Real Estate Income b Less accumulated depreciation 307,955.00 3,281,134.00 Gross Rents $485,197.5610a Depletable assets 0.00 b Less accumulated depletion 0.00 0.00 Total Gross Rents 485,197.5611 Land (net of any amortization) 481,380.0812a Intangible assets (amortizable only) 79,419.00 Rental Real Estate Expenses b Less accumulated amorization 70,467.00 8,952.00 Advertising 859.65

Auto and travel 0.00 Cleaning and maintenance 0.00 Commissions 0.00 Insurance 10,078.15 Legal and other professional fees 11,984.40 Interest 134,925.42 Repairs 7,651.90 Taxes 76,663.58 Utilities 40,788.99 Wages and salaries 23,435.68 Depreciation 134,359.00 Other: Amortization Expense 30,517.00 Management Fees 28,256.28 Office Expense 2,293.07 Contract Services 0.00 Bank Fees 988.59 Deposit Refunds 7,693.45 Credit Checks 1,425.22 Apartment Expense 6,662.65 Dues & Permits 200.67 Landscaping 4,743.96 Pest Control 0.00

Total Expense 523,527.66

Net Income ($38,330.10)

Stonebrook Phase II

Form 8825Balance Sheet

Accumulated Depreciation may not match your records and is only an estimate.Please consult your tax advisor.

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 20 of 24

Owner's name: Bart WarnerOwner's %: 49.500%

Line 5 Interest Income $0.00Line 17a Post 1986 depreciation adjustment 0.00

Line 14 Special depreciation allowance for qualified property placed in service during the tax year 4,005.00

Line 17 MACRS deductions for assets placed in service in tax years beginning before 2011: 130,354.00

(a) Classification of property (b) Month and year placed in service

(c) Basis for depreciation

(d)Recovery

Period(e) Convention (f) Method

(g)Depreciation

deduction19a 3-year property b 5-year property 4,005.00 5 MQ 200DB 0.00 c 7-year property d 10-year property e 15 year property f 20-year property g 25-year property 25 MM S/L h Residential rental property 27.5 MM S/L h Residential rental property 27.5 MM S/L i Nonresidential real property 39 MM S/L

rtization Costs that began before your 2010 tax (b) Date amortization began

(c) Amortizable amount

(d) Code section

(e) Amortization period or percentage

Loan Fees 01/28/11 23,019.00 461 1.5 14,067.00Amortization Costs that began before your 2011 tax year: 16,450.00

(f) Amortization for this year

Part VI: Amortization

4562 Section A

Other Schedule K-1 Items

Form 4562 section B

Form 4562 Part II

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 21 of 24

EXHIBIT “D”

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 22 of 24

Owner's Name: Bart WarnerOwner's % 49.50%

Note: The #s on this schedule reflect your ownership portion only.

Rental Real Estate IncomeGross Rents $473,163.42

Total Gross Rents $473,163.42

Rental Real Estate ExpensesAdvertising $2,232.45Auto and Travel $0.00Cleaning and Maintenance $0.00Commissions $0.00Insurance $5,197.22Legal and Other Professional Fees $1,659.54Interest $132,917.88Repairs $17,598.53Taxes $77,309.88Utilities $47,928.85Wages and Salaries $35,157.62Other:Management Fees $12,008.21Office Expense $787.47Bank Fees $863.40Credit Reporting $0.00Rental Expense $3,648.67Cable Service $0.00Landscaping $3,933.61Pest Control $0.00Security System $0.00Trash Removal $0.00Telephone Expense $0.00License and Fees $0.00

Total Expenses $341,243.31

Net Income $131,920.10

Stone Brook Phase II

2012 Income & Expenses

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 23 of 24

Owner's Name: Bart WarnerOwner's % 49.50%

Property Additions:Calssification Date in Service Recovery Amount

Period5 year Property 7/1/2012 5 $3,662.01Residential Rental Property 7/1/2012 27.5 $550.22Land Improvements 7/1/2012 15 $671.86

Property Disposals:None

Note on depreciation and amortization: This schedule shows additions and disposals for the current year only. Yourtotal depreciation and amortization expense for the year will depend on your basis in the property from your originalinvestment and any property additions and disposals from that point forward. You should be tracking this informationon depreciation schedules from year to year. Your schedules should be updated with the above information. Pleaseconsult your tax advisor.

Stone Brook Phase II

Fixed Assets

Case 2:11-cv-01165-BSJ Document 1732 Filed 03/18/14 Page 24 of 24