electronic payment systems in e commerce

TRANSCRIPT

ELECTRONIC PAYMENT SYSTEMS

BACHU VINAY CHAITHANYA (1421408)

E-Commerce or Electronics Commerce sites use electronic payment where electronic payment refers to paperless monetary transactions.

Electronic payment has revolutionized the business processing by reducing paper work, transaction costs, labour cost.

Being user friendly and less time consuming than manual processing, helps business organization to expand its market reach / expansion.

Credit Card

Debit Card

Smart Card

E-Money

Electronic Fund Transfer (EFT)

E- Wallet

ELECTRONIC PAYMENT SYSTEMS

Types of EPSE Cash / E Money:

A system that allows a person to pay for goods or services by transmitting a number from one computer to another.

Like the serial numbers on real currency notes, the E-cash numbers are unique.

This is issued by a bank and represents a specified sum of real money.

It is anonymous and reusable.

E-Wallet:

The E-wallet is another payment scheme that operates like a carrier of e-cash and other information.

The aim is to give shoppers a single, simple, and secure way of carrying currency electronically.

Trust is the basis of the e-wallet as a form of electronic payment.

Smart Card:

A smart card, is any pocket-sized card with embedded integrated circuits which can process data.

This implies that it can receive input which is processed and delivered as an output.

Types of EPS

Credit Card :

It is a Plastic Card having a Magnetic Number and code on it.

It has Some fixed amount to spend.

Customer has to repay the spend amount after sometime.

Debit Card :

Similar to Credit card on coding and encryption.

Purchase limit depends on the available balance in the account.

Types of EPS (Electronic Payment Systems) - Interfaces

No Security Model

Examples : Bill payments, Mobile Recharges on calling to customer care.

Third Party Processor

Processing payments using encrypted credit cards

Customer

Merchant's server

Send encrypted credit card number

Send information

Online credit card

processors

Customer’s bank

Monthly purchase statement

verify

authorize

OKCheck for credit card

authenticity and sufficient funds

Sequence of steps for secure transaction

1. Customer presents card to the merchant

2. Merchant validates customer’s identity as the owner of the card

3. Merchant relays credit card charge & signature to its bank

4. Bank relays this info to customer’s bank for authorization approval

5. Customer’s bank returns authentication & authorization to the

merchant

Encryption & credit cards

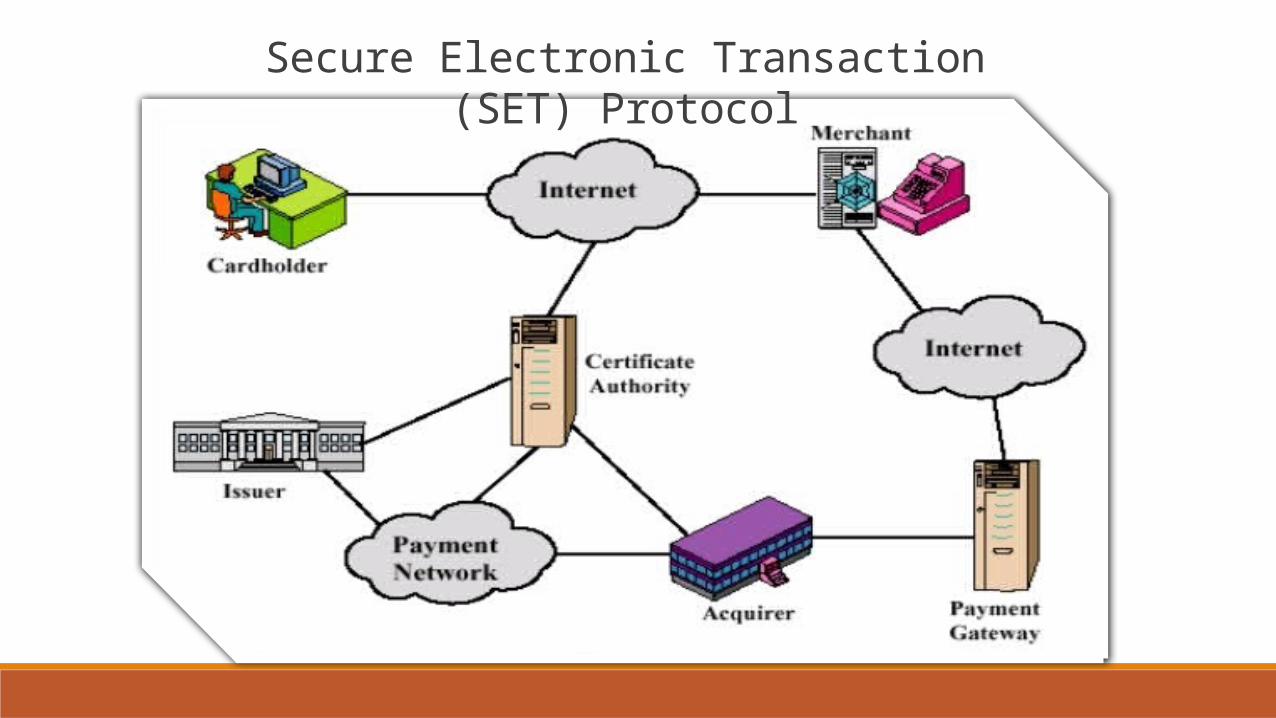

Secure Electronic Transaction (SET) Protocol

Blowfish provides a good encryption rate in software and no effective cryptanalysis of it has been found to date.

However, the Advanced Encryption Standard (AES) now receives more attention.

Widely Applicable E Payment System

Pros

It’s easier for customers to buy your products or services.

You can add custom loyalty programs, gift cards and customized e-commerce websites.

You can integrate it with accounting software, making it easier to manage money.

You don’t have to waste as much time depositing paper checks and cash at the bank.

Cons

You have to pay a processing fee to accept plastic and some other electronic payments.

If you use a traditional physical credit card terminal, monthly or annual fees might apply.

Some payment processing services lock you into contracts that are costly to terminate early.

To accept credit cards you usually need a merchant account, which is a bank account where payments

are deposited. Many electronic payment systems include one as a built-in feature. Note that you don’t

need a merchant account if you use a third-party processor such as PayPal.

Pros and cons