eitf issue no. 16-a, “statement of cash flows: … · eitf issue no. 16-a, ... 13. a professional...

TRANSCRIPT

Page 1 of 33

Memo No. Issue Summary No. 1, Supplement No. 1

Memo Issue Date September 8, 2016

Meeting Date(s) EITF September 22, 2016

Contact(s) Jenifer Wyss Lead Author, Project Lead (203) 956-3479

Andrew McClaskey Co-Author (203) 956-3442

Rob Moynihan EITF Coordinator (203) 956-5239

Robert Uhl EITF Liaison

Project

EITF Issue No. 16-A, “Statement of Cash Flows: Restricted Cash” (previously included in EITF Issue No. 15-F, “Statement of Cash Flows: Classification of Certain Cash Receipts and Cash Payments”)

Project Stage Redeliberations

Dates previously discussed by EITF

May 14, 2015 (Educational Meeting); June 18, 2015; September 17, 2015; March 3, 2016

Previously distributed Memo Numbers

Issue Summary No. 1, dated June 4, 2015; Supplement No. 2, dated October 29, 2015, both generated under EITF Issue No. 15-F; Issue Summary No. 1, dated February 18, 2016

Background and Objective of this Memo

1. At the March 3, 2016 EITF meeting, the Task Force reached a consensus-for-exposure that

the statement of cash flows should explain the change during the period in the total of cash,

cash equivalents, and amounts generally described as restricted cash or restricted cash

equivalents. The Task Force also reached a consensus-for-exposure that certain disclosures

should be required to supplement the statement of cash flows. Specifically, an entity should

disclose (a) the nature of the restrictions on cash, cash equivalents, and amounts generally

described as restricted cash or restricted cash equivalents and (b) on the face of the statement

The alternative views presented in this Issue Summary Supplement are for purposes of

discussion by the EITF. No individual views are to be presumed to be acceptable or

unacceptable applications of Generally Accepted Accounting Principles until the Task Force

makes such a determination, exposes it for public comment, and it is ratified by the Board.

Page 2 of 33

of cash flows or in the notes to the financial statements, if the total of cash, cash equivalents,

and amounts generally described as restricted cash and restricted cash equivalents at the

beginning and end of the period shown on the statement of cash flows cannot be reconciled

to the amounts of similarly titled line items on the statement of financial position, the

amounts and line items in which such amounts are reported within the statement of financial

position.

2. The Board ratified the consensuses-for-exposure on April 20, 2016, and a proposed Update

was issued on April 28, 2016, with a June 27, 2016 comment letter deadline.

3. At the September 22, 2016 EITF meeting, the Task Force will have the opportunity to

consider the feedback received through comment letters as it redeliberates the consensus-

for-exposure. The Task Force will then be asked whether it wishes to affirm its consensus-

for-exposure on this Issue as a final consensus. This memo summarizes the comment letters

received from stakeholders on the proposed amendments and provides the staff’s analysis

and recommendations on how to proceed. To assist the Task Force as it redeliberates, the

staff has provided a summary of the staff recommendations in Appendix A of this memo.

Summary of Comment Letters

4. Nineteen comment letters were received in response to the proposed Update. The number of

comment letters by type of respondent is included in the table below:

Respondent Type Number of Comment Letters

Accounting Firm 4

Preparer 8

Professional Accounting Association 6

Individual 1

Page 3 of 33

Presentation of Changes in Restricted Cash and Restricted Cash Equivalents on the Statement of Cash Flows

5. The proposed Update included the following question about the presentation of changes in

restricted cash and restricted cash equivalents on the statement of cash flows:

Question 1: Do you agree that the statement of cash flows should explain the change during

the period in the total of cash, cash equivalents, and amounts generally described as restricted

cash or restricted cash equivalents? If not, please explain what presentation is more

appropriate and why?

6. Ten respondents, including 4 preparers, 4 accounting firms, and 2 professional accounting

associations, agreed with the proposed amendments that the statement of cash flows should

explain the change during the period in the total of cash, cash equivalents, and amounts

generally described as restricted cash or restricted cash equivalents.

7. Two of the accounting firms and one of the professional accounting associations that agreed

with the proposed amendments indicated that presenting the overall activity of cash in the

statement of cash flows, without regard to whether the cash is restricted, would provide

meaningful and decision-useful information to financial statement users and would reduce

diversity in practice.

8. Another one of those professional accounting associations that agreed stated that the

proposed amendments represent the most effective way of communicating cash inflows and

outflows for an entity as a whole. That professional accounting association and one of the

accounting firms noted that the proposed amendments eliminate the need to address the most

appropriate cash flow classification of internal transfers between unrestricted cash and

restricted cash.

9. One of the preparers that agreed stated that explaining the change during the period in cash,

cash equivalents, restricted cash, and restricted cash equivalents in the statement of cash

flows is a conceptually sound approach and is operationally efficient when compared to

classifying changes in restricted cash on the basis of nature or purpose, which would add

complexity to the preparation and understanding of the information presented in the

statement of cash flows.

Page 4 of 33

10. Eight respondents, including four preparers, three professional accounting associations, and

the individual, disagreed with the proposed amendments that the statement of cash flows

should explain the change during the period in the total of cash, cash equivalents, and

amounts generally described as restricted cash or restricted cash equivalents.

11. One of those preparers that disagreed stated that the beginning-of-period and end-of-period

total cash on the statement of cash flows should reconcile directly to cash and cash

equivalents as presented on the statement of financial position, and that including restricted

cash and restricted cash equivalents with cash and cash equivalents on the statement of cash

flows will add complexity and confusion.

12. Two other preparers that disagreed noted that the purpose of the statement of cash flows is

to provide financial statement users with unbiased, objective, and relevant information about

the sources and uses of an entity’s cash and to assess that entity’s ability to meet its

obligations. Those two preparers and two of the professional accounting associations that

disagreed asserted that presenting restricted cash and restricted cash equivalents with cash

and cash equivalents in the beginning-of-period and end-of-period reconciliation on the

statement of cash flows would confuse financial statement users about how much cash is

available for an entity’s operations. Each of those four respondents separately noted that

since cash available for general operations is distinguishable from cash that is restricted as

to withdrawal or use, explaining the change during the period in the total cash, cash

equivalents, restricted cash, and restricted cash equivalents will not provide users with a

reporting entity’s true liquidity position and, therefore, may impair the usefulness of the

statement of cash flows. Those four respondents also stated that although internal transfers

between cash and cash equivalents and restricted cash and restricted cash equivalents do not

represent actual cash flows, they do represent a change in a reporting entity’s liquidity

position and the amount of cash available to meet its other general obligations.

13. A professional accounting association stated that in the Master Glossary of the Codification,

cash includes demand deposits that the customer may deposit at any time and also effectively

may withdraw at any time without prior notice or penalty. Conversely, restricted cash and

restricted cash equivalents are generally unavailable for current use. Restricted cash and

restricted cash equivalents are fundamentally different from cash and cash equivalents and,

Page 5 of 33

therefore, changes in restricted cash and restricted cash equivalents should be presented

separately in the statement of cash flows.

14. Two preparers stated that presenting changes in restricted cash, resulting from both internal

transfers and cash flows with a source outside the entity, on the basis of the nature of or the

purpose for the restrictions as operating, investing, or financing activities provides

meaningful information to financial statement users and those changes should continue to be

presented in the body of the statement of cash flows.

15. A preparer noted that internal changes in restricted cash balances that result from either

contractual or settlement agreements should be classified as investing activities because the

nature of those changes in restricted cash is similar to other investing activities in which

funds are invested and accessed for a future use. Similarly, cash payments made directly

from restricted cash accounts should be characterized and classified in the statement of cash

flows based on the underlying nature (that is, operating, investing, or financing activities) of

the associated payment.

16. One respondent, a professional accounting association, did not directly respond to Question

1.

17. To assist the Task Force in reaching its consensus-for-exposure, the staff conducted outreach

with four financial statement users, one FASB Advisory Group entirely composed of

financial statement users, and another FASB Advisory Group partially composed of financial

statement users. Feedback obtained from those users about the presentation of changes in

restricted cash on the statement of cash flows is summarized in the following four

paragraphs.

18. One FASB Advisory Group whose members are financial statement users and two of the

financial statement users in the staff’s outreach disagreed with including restricted cash and

restricted cash equivalents with cash and cash equivalents when reconciling the beginning-

of-period and end-of-period total amounts shown on the statement of cash flows. Those users

indicated that commingling cash that is unavailable to be used because of a third-party

restriction with cash that is highly liquid on the statement of cash flows would result in a

loss of information and, therefore, diminish the value of the information presented on the

statement of cash flows. Two of those users commented that because it is important for users

Page 6 of 33

to understand how liquidity is affected by movements in restricted cash, the changes in

restricted cash should be presented on the basis of the nature of the restriction and presented

separately on the statement of cash flows.

19. One user included in the staff’s outreach conditionally agreed that it is appropriate to include

restricted cash with cash and cash equivalents on the statement of cash flows only when the

restriction relates to routine (operating) purposes, such as restrictions on cash for workers’

compensation claims. The user did not think it was appropriate to include restricted cash

with cash and cash equivalents on the statement of cash flows when the restrictions are long-

term and non-routine. When the restrictions are long-term and non-routine, the user prefers

that the transfers between unrestricted cash and restricted cash be presented as a line item on

the statement of cash flows so that movement between restricted and unrestricted cash is

transparent.

20. Another user conditionally agreed with including restricted cash and restricted cash

equivalents with cash and cash equivalents when reconciling the beginning-of-period and

end-of-period total amounts shown on the statement of cash flows, but thinks that there is a

loss of information because the statement of cash flows would not individually present the

changes in restricted cash and changes in cash and cash equivalents. The user suggested that

such presentation be combined with a requirement to provide supplemental information

about changes in restricted cash so that there is no loss of information. This user also stated

that classifying changes in restricted cash as investing activities would be misleading and

would adversely affect investor models used to determine regular investing needs of a

company from a cash flow perspective.

21. One FASB Advisory Group partially comprised of financial statement users noted that

diversity in practice on the presentation of changes in restricted cash might be resolved by

presenting restricted cash and restricted cash equivalents together with cash and cash

equivalents on the statement of cash flows.

Question 1 for the Task Force

1. Does the Task Force want to affirm its consensus-for-exposure that the

statement of cash flows should explain the change during the period in the total of

Page 7 of 33

cash, cash equivalents, and amounts generally described as restricted cash or

restricted cash equivalents?

Staff Recommendation

22. The staff recommends that the Task Force affirm its consensus-for-exposure that a statement

of cash flows should explain the change during the period in the total of cash, cash

equivalents, and amounts generally described as restricted cash or restricted cash

equivalents. While feedback obtained from comment letter respondents and outreach with

financial statement users was mixed, the staff believes that during the comment letter

process, no new concerns were raised and no new information materialized related to

Question 1 that was not previously discussed and deliberated by the Task Force.

23. The staff believes that regardless of whether cash is restricted or unrestricted, the proposed

amendments support the primary objective of the statement of cash flows, which is to

provide relevant information about the cash receipts and cash payments of an entity during

a period, and, therefore, presenting the ultimate cash inflows and outflows of an entity

provides the most meaningful information. The staff acknowledges that eight respondents

disagreed with the proposed amendments. In reaching its consensus-for-exposure, the Task

Force previously discussed those opposing views, which are summarized in the following

paragraphs.

24. Several respondents indicated that the proposed amendments would confuse financial

statements users about how much cash is available for an entity’s operations because

restricted cash is fundamentally different from unrestricted cash and cannot be used to meet

general obligations. The Task Force previously discussed this concern and noted that insight

into the availability of cash can be gleaned from the statement of financial position and from

the proposed disclosure of the nature of restrictions on cash and cash equivalents.

25. One respondent asserted that the proposed amendments do not clearly address the

presentation of restricted cash amounts received from or paid to external sources. The Task

Force previously observed that some entities disclose the ultimate cash flows of a segregated

restricted cash or restricted cash equivalents account as noncash investing or financing

activities, while others categorize them as operating, investing, or financing activities. The

Page 8 of 33

Task Force previously noted that including amounts generally described as restricted cash

and restricted cash equivalents in the beginning-of-period and end-of-period reconciliation

of total cash and cash equivalents on the statement of cash flows would resolve the diversity

in practice about how to present cash flows that directly affect restricted cash. This is because

those direct cash flows would be presented in the statement of cash flows regardless of

whether restricted cash or restricted cash equivalents are in a segregated account or

commingled with unrestricted cash and cash equivalents, and regardless of the timing of

when the restrictions are established or released.

26. One respondent suggested that, in some cases, changes in restricted cash that result from

transfers between cash and unrestricted cash should be classified as investing activities. Two

other respondents suggested that changes in restricted cash should be classified based on the

purpose for the restriction. The Task Force previously considered but rejected classifying

changes in restricted cash or restricted cash equivalents that result from transfers between

cash, cash equivalents, and amounts generally described as restricted cash or restricted cash

equivalents on the basis of either the nature of the restriction (that is, investing activities) or

the purpose for the restriction. The Task Force noted that such internal transfers do not

represent a cash inflow or outflow of the entity because there is no cash receipt or payment

with a source outside the entity. Some Task Force members noted that those internal transfers

do not faithfully represent an entity’s investing activities. Furthermore, some Task Force

members noted that classification of changes in restricted cash or restricted cash equivalents

on the basis of the purpose for the restriction could result in a duplicate cash flow

classification, as described in the next paragraph.

27. For example, if an entity is required by its lender to establish a restricted cash account for

the future payment of debt, the entity establishes the restricted cash account by transferring

cash from cash to restricted cash and then classifies the change in restricted cash as a cash

outflow for financing activities even though the change does not represent repayments of

amounts borrowed. When the restriction is released, the following occurs: (a) cash is

transferred from restricted cash to cash and the change in restricted cash is classified as a

cash inflow from financing activities, and (b) a cash payment is made to the lender to pay

down the debt and is classified as a cash outflow for financing activities. In this example,

Page 9 of 33

the statement of cash flows presents a financing outflow twice even though there was only

one repayment of amounts borrowed.

Disclosure of Amounts and Line Items

28. The proposed Update included the following question on disclosures:

Question 2: Do you agree that if the total of cash, cash equivalents, and amounts generally

described as restricted cash or restricted cash equivalents at the beginning and end of the

period shown on the statement of cash flows cannot be reconciled to the amounts of similarly

titled line items on the statement of financial position, an entity should disclose on the face

of the statement of cash flows or in the notes to the financial statements, the amounts and

line items in which such amounts are reported within the statement of financial position? If

not, please explain why that information would not be useful.

29. Twelve respondents, including 4 professional accounting associations, 5 preparers, and 3

accounting firms agreed with the proposed amendments in Question 2. Two of those

preparers indicated that such disclosure would provide beneficial information to financial

statement users. Another preparer stated that they support the latitude to disclose the

information either on the face of the statement of cash flows or in the notes to the financial

statements.

30. Five respondents, including two professional accounting associations, one preparer, one

accounting firm, and the individual disagreed with certain aspects of the proposed

disclosures in Question 2. While those five respondents agree that a disclosure should be

provided in situations in which the total of cash, cash equivalents, and amounts generally

described as restricted cash or restricted cash equivalents at the beginning and end of the

period shown on the statement of cash flows cannot be reconciled to the amounts of similarly

titled line items on the statement of financial position, the respondents provided views about

the location, format, and content of the disclosure that differ from the proposed amendments.

31. The preparer that disagreed with the proposed disclosures stated that financial statement

users are accustomed to agreeing the beginning and end of the period cash and cash

equivalents on the statement of cash flows to similarly titled line items on the statement of

Page 10 of 33

financial position and stated that omitting such a reconciliation or including it in the notes to

the financial statements would not improve the usefulness of the financial statements.

32. The accounting firm that disagreed stated that the proposed disclosures should be required

to be presented on the face of the statement of cash flows given the importance of being able

to reconcile the amounts in the statement of cash flows with the amounts in the statement of

financial position. Additionally, the accounting firm recommended that the Task Force

consider expanding the circumstances under which an entity would be required to prepare a

reconciliation of total cash and cash equivalents, including restricted cash and restricted cash

equivalents, on the statement of cash flows to the amounts on the statement of financial

position. That accounting firm recommended that a reconciliation be required in any

situation in which the statement of financial position includes multiple line items of cash,

cash equivalents, restricted cash, and restricted cash equivalents even when the titles of those

line items are similar to the titles of the line items on the statement of cash flows. Given the

importance of understanding the total amounts of cash and cash equivalents, including both

unrestricted and restricted, the accounting firm stated that financial statement users should

not be required to prepare their own reconciliation to determine whether the total amounts

of cash, cash equivalents, and amounts generally described as restricted cash or restricted

cash equivalents on the statement of financial position agree with the total amounts shown

in statement of cash flows.

33. Similar to the accounting firm, two professional accounting associations that disagreed with

the proposed disclosures recommended that such disclosure be required even when those

line items are similarly titled on the statement of cash flows and on the statement of financial

position. One of those professional accounting associations preferred that a quantitative

disclosure in a tabular format be presented on the face of the statement of cash flows while

the other professional accounting association noted the disclosure could be provided either

on the face of the statement of cash flows or in the notes to the financial statements.

34. The FASB’s Taxonomy (XBRL) staff believes that the proposed disclosure could result in

difficulties for users of the XBRL data as they try to understand and compare the amounts

reported in the statement of financial position and the statement of cash flows. Specifically,

in some instances, a financial statement user may be able to make a visual connection

Page 11 of 33

between the total amounts of cash reported in the statement of financial position and the

statement of cash flows, but without modifying the proposed disclosure so that it relates

those amounts, machine-readable data tagged with XBRL would not be connected, resulting

in difficulties in understanding the relationship between the two statements. The XBRL staff

recommends that a disclosure be required in any situation in which the statement of financial

position includes more than one line item of cash, cash equivalents, restricted cash, and

restricted cash equivalents even when the titles of those line items are similar to the title of

the beginning and end of the period totals of cash, cash equivalents, and amounts generally

described as restricted cash or restricted cash equivalents shown on the statement of cash

flows. The XBRL staff indicated that such disclosure could be provided in a narrative or

tabular format and could be presented in the notes to the financial statements or on the face

of the statement of cash flows.

35. Two respondents did not respond to Question 2.

Question 2 for the Task Force

2. Does the Task Force want to affirm its consensus-for-exposure that if the total of

cash, cash equivalents, and amounts generally described as restricted cash or

restricted cash equivalents at the beginning and end of the period shown on the

statement of cash flows cannot be reconciled to the amounts of similarly titled line

items on the statement of financial position, an entity should disclose on the face of

the statement of cash flows or in the notes to the financial statements, the amounts

and line items in which such amounts are reported within the statement of financial

position?

Staff Analysis and Recommendation

36. The disclosure included in the proposed Update would require that an entity disclose the

amounts and line items of amounts generally described as restricted cash or restricted cash

equivalents reported in the statement of financial position if not similarly titled to the totals

at the beginning and end of the period shown on the statement of cash flows. To facilitate

the use of XBRL data and in response to feedback received during the comment letter

process, the staff recommends the Task Force build upon the proposed disclosure and require

disclosure of all amounts included in the totals shown at the beginning and end of the period

on the statement of cash flows, and the line items in which those amounts are reported in the

Page 12 of 33

statement of financial position, in any situation in which the statement of financial position

includes more than one line item of cash, cash equivalents, and amounts generally described

as restricted cash or restricted cash equivalents. This incremental requirement would more

clearly present the connection between amounts and line items of cash, cash equivalents, and

amounts generally described as restricted cash or restricted cash equivalents on the statement

of financial position and the statement of cash flows. The staff recommends that, as

proposed, flexibility be given to reporting entities to disclose that information in the notes to

the financial statements or to present it on the statement of cash flows. Furthermore, the staff

recommends that such information be allowed to be provided in either a narrative or a tabular

format. With the revisions noted above, the staff recommends the following changes to the

proposed amendments (both the original amendments from the proposed Update and the

revised amendments are shown below):

Amendments as originally proposed

230-10-45-4 A statement of cash flows shall explain the change during the period

in the total of cash, cash and cash equivalents, and amounts generally described as

restricted cash or restricted cash equivalents. The statement shall use descriptive

terms such as cash or cash and cash equivalents rather than ambiguous terms such

as funds. The total amounts of cash and cash equivalents at the beginning and end

of the period shown in the statement of cash flows shall be the same amounts as

similarly titled line items or subtotals shown in the statements of financial position

as of those dates. If the total of cash, cash equivalents, and amounts generally

described as restricted cash or restricted cash equivalents at the beginning and end

of the period shown on the statement of cash flows cannot be reconciled to the

amounts of similarly titled line items on the statement of financial position, an

entity shall provide the disclosures required in paragraph 230-10-50-8.

Revised amendments

230-10-45-4 A statement of cash flows shall explain the change during the period

in the total of cash, cash and cash equivalents, and amounts generally described as

restricted cash or restricted cash equivalents. The statement shall use descriptive

terms such as cash or cash and cash equivalents rather than ambiguous terms such

Page 13 of 33

as funds. The total amounts of cash and cash equivalents at the beginning and end

of the period shown in the statement of cash flows shall be the same amounts as

similarly titled line items or subtotals shown in the statements of financial position

as of those dates. The total amounts of cash, cash equivalents, and amounts

generally described as restricted cash or restricted cash equivalents at the beginning

and end of the period shown in the statement of cash flows shall reconcile to the

amounts and line items in which such amounts are reported in the statement of

financial position. When cash, cash equivalents, and amounts generally described

as restricted cash or restricted cash equivalents are presented in more than one line

item within the statement of financial position, an entity shall provide the

disclosures required in paragraph 230-10-50-8.

Amendments as originally proposed

230-10-50-8 If the total of cash, cash equivalents, and amounts generally described

as restricted cash or restricted cash equivalents at the beginning and end of the

period shown on the statement of cash flows cannot be reconciled to the amounts

of similarly titled line items on the statement of financial position (see paragraph

230-10-45-4), an entity shall disclose on the face of the statement of cash flows or

in the notes to the financial statements, the amounts and line items in which such

amounts are reported within the statement of financial position.

Revised amendments

230-10-50-8 When cash, cash equivalents, and amounts generally described as

restricted cash or restricted cash equivalents are presented in more than one line

item within the statement of financial position, an entity shall, for any such period

presented, present on the face of the statement of cash flows or disclose in the notes

to the financial statements, the line items and amounts of cash, cash equivalents,

and amounts generally described as restricted cash or restricted cash equivalents

reported within the statement of financial position that reconcile to the total

amounts of cash, cash equivalents, and amounts generally described as restricted

cash or restricted cash equivalents at the beginning and end of the period shown in

the statement of cash flows.

Page 14 of 33

37. The staff also recommends the following changes to the proposed illustrative example: (text

added to the proposed disclosure is underlined, and text deleted from the proposed disclosure

is struck out):

230-10-55-12A Illustrative disclosures of the nature of restrictions on cash and cash

equivalents required by paragraph 230-10-50-7 and disclosure reconciling the

amounts of cash, cash equivalents, and amounts generally described as restricted

cash or restricted cash equivalents and the line items in which such amounts are

reported in the statement of financial position to the totals of such amounts shown

in the statement of cash flows as required by paragraph 230-10-50-8 are as follows.

(In this illustrative example, Entity A has no restricted cash equivalents.)

Restricted cash of $225 and $125 as of 1/1/19X1 and 12/31/19X1,

respectively, represents amounts required to be set aside by an insurer for

the payment of specific workers’ compensation claims. Other long-term

assets on the statement of financial position include restricted cash of $100

$75 as of 1/1/19X1 and 12/31/19X1 that is pledged as collateral for long-

term financing arrangements. Those restricted cash amounts, combined

with cash and cash equivalents of $300 and $1,465 as of 1/1/19X1 and

12/31/19X1, respectively, are equal to the amounts reported on the

statement of cash flows at the beginning and end of the year of $600 and

$1,665, respectively.

38. The staff believes that the recommended incremental change to the disclosure requirement

and, consequently, the incremental change to the illustrative example, are responsive to the

data-tagging concerns raised by the XBRL staff (that is, without such a disclosure, machine-

readable data are not connected resulting in difficulties in understanding the relationship

between the two statements) and respondent feedback. The recommended changes also

maintain the Task Force’s objective of allowing flexibility for reporting entities.

Disclosure of Nature of Restrictions

39. The proposed Update included the following question on disclosures:

Page 15 of 33

Question 3: Do you agree that an entity should be required to disclose information about the

nature of restrictions on its cash and cash equivalents? If not, please explain why that

information would not be useful.

40. Seventeen respondents agreed with the proposed amendments to require an entity to disclose

information about the nature of restrictions on its cash and cash equivalents. Several

respondents commented on how the proposed disclosure would be relevant to a financial

statement user and the type of information that would be provided by the disclosure. The

staff observed that those respondents had differing interpretations of what information they

thought would be provided by the proposed disclosure. Those differing interpretations could

be the result of the general wording of the proposed disclosure as opposed to a detailed and

prescriptive list of disclosures. Those respondents’ differing interpretations of what

information would be provided by the proposed disclosure include:

(a) A description of individual restrictions

(b) Reasons why the restrictions are in place

(c) An indication of when and how the restriction will be satisfied

(d) The amount of the restricted cash

(e) How the amount of restricted cash was determined.

41. Six of the 17 respondents provided suggestions to enhance the proposed nature of restrictions

disclosure and the related proposed illustrative example. One accounting firm recommended

that the disclosure specifically state whether the restriction is a legal, contractual, or

company-designated restriction. Another accounting firm recommended that entities be

required to disclose the changes in the nature of restrictions that occur during the period,

including changes in the amount of restrictions that are material to the financial statements.

A third accounting firm recommended that consideration be given to encourage more robust

disclosures than those illustrated in the proposed Update. For example, when cash

restrictions constitute a significant constraint for the reporting entity, disclosures could be

enhanced to discuss how the restricted amount of cash is determined so that financial

statement users have a better understanding of how the restricted amount may fluctuate from

one period to the next.

Page 16 of 33

42. Two professional accounting associations agreed that while an entity should be required to

disclose the nature of restrictions on its cash and cash equivalents, it is unclear what “nature”

means. Rather than broadly requiring an entity to disclose its nature of restrictions on cash

and cash equivalents, the Task Force should provide specific disclosure guidance that

represents what is meant by “nature.” Those two professional accounting associations

recommended that entities be required to disclose the amounts and terms of each restriction

on cash, including when those restrictions will cease to be in effect.

43. A preparer stated that while an entity should be required to disclose the nature of restrictions

on its cash and cash equivalents, the disclosure should be consistent with Securities and

Exchange Commission (SEC) Regulation S-X Rule 5-02.1 which states, in part:

Separate disclosure shall be made of the cash and cash items which are

restricted as to withdrawal or usage. The provisions of any restrictions shall be

described in a note to the financial statements. Restrictions may include legally

restricted deposits held as compensating balances against short-term borrowing

arrangements, contracts entered into with others, or company statements of

intention with regard to particular deposits; however, time deposits and short-term

certificates of deposit are not generally included in legally restricted deposits.

44. Two respondents did not respond to Question 3.

45. The staff conducted outreach with three private company financial statement users. Those

users indicated that disclosures of the nature of restrictions on cash, including information

about the expected duration of the restriction, the amount and source of the restriction, and

the purpose and terms of the restriction, would provide sufficient relevant information to

enable private company financial statement users to ask management follow-up questions.

Question 3 for the Task Force

3. Does the Task Force want to affirm its consensus-for-exposure that an entity

should be required to disclose information about the nature of restrictions on its cash

and cash equivalents?

Staff Analysis and Recommendation

46. The staff recommends that the Task Force revise the proposed disclosure to clarify the type

of information that might be provided by an entity when disclosing the nature of restrictions

on its cash and cash equivalents. The staff understands that it might seem unusual to

Page 17 of 33

recommend a change when all respondents to Question 3 of the proposed Update agreed

with the proposed amendments. However, six respondents made suggestions to enhance the

proposed disclosure and other respondents had differing interpretations about the type of

information that would be provided by the proposed disclosure. The staff conducted outreach

with multiple respondents (that is, three professional accounting associations, two preparers,

and one accounting firm) to seek clarity and additional information about the feedback

received in the comment letters. Therefore, in response to feedback received from

respondents through comment letters and outreach, the staff applied the decision questions

in the proposed FASB Concepts Statement, Conceptual Framework for Financial

Reporting-Chapter 8: Notes to Financial Statements (proposed Concepts Statement), to

identify the nature of the disclosure. In the following paragraphs, the staff analyzes those

decision questions that are most relevant to the proposed nature of restrictions disclosure.

47. Decision Question L2 states:

Does the line item represent any of the following:

a) Financial instruments issued or held by the entity

b) Other contracts or legally binding documents

c) Other binding agreements?

48. The staff notes that there could be contracts or legally binding documents that restrict an

entity’s cash and cash equivalents. In the proposed Concepts Statement, information to be

considered for disclosure on decision Question L2 includes the amount and timing of future

cash flows. Therefore, the staff thinks that disclosure of the terms (for example, the stated or

expected duration of each restriction and estimated amounts of future cash flows associated

with each restriction) of an entity’s restricted cash could assist users in their decisions about

whether to provide resources to the entity. The staff recognizes the duration of the restriction

may not always be known by the entity and disclosure of the duration would not

communicate the ultimate use of the cash, that is, whether there would be a cash payment to

a source outside the entity specifically related to the restriction or whether the cash would

be released from restriction and transferred to an unrestricted cash account. However, the

staff thinks that the expected duration could be an indicator of a future cash flow. Therefore,

Page 18 of 33

the staff recommends revising the proposed disclosure to include the expected duration of

the restriction.

49. Decision Question L4 states, “Does the line item include components of different natures

that could affect prospects for net cash flows differently?” Amounts generally described as

restricted cash and restricted cash equivalents may be presented in various line items on the

financial statements (for example, restricted cash and restricted cash equivalents, assets

whose use is limited, or restricted cash may be presented with other assets) and an entity

could have multiple restrictions within a line item. Those line items and individual

restrictions within a particular line item can be of different natures. The staff believes that

disaggregation could help users understand the reasons why the restrictions exist (that is, the

purpose and terms of each restriction), the source of each restriction, including whether the

restriction is external or internal, and the amount of each restriction. Therefore, the staff

recommends revising the proposed disclosure to explicitly include such information.

50. Based on the decision questions in the proposed Concepts Statement and the feedback

received from respondents, the proposed disclosure could be revised as follows (text added

to the proposed disclosure is underlined):

230-10-50-7 An entity shall disclose information about the nature of

restrictions on its cash, cash equivalents, and amounts generally described

as restricted cash or restricted cash equivalents, which may include the

following information about restrictions that are significant either

individually or in the aggregate:

a. Expected duration of the restriction

b. Purpose and terms of the restriction

c. Source of the restriction (for example, internal or external)

d. Amount of the restriction.

Entities within the scope of Topic 958 also shall provide the disclosures

required in paragraph 958-210-50-3.

51. The Task Force also could consider enhancing the proposed illustrative disclosure in

paragraph 230-10-55-12A, as follows (text added to the proposed disclosure is underlined,

and text deleted from the proposed disclosure is struck out):

230-10-55-12A Illustrative disclosures of the nature of restrictions on cash

and cash equivalents required by paragraph 230-10-50-7 and the amounts

of restricted cash and the line items in which such amounts are reported in

Page 19 of 33

the statement of financial position as required by paragraph 230-10-50-8 are

as follows. (In this illustrative example, Entity A has no restricted cash

equivalents.)

Restricted cash of $225 and $125 as of 1/1/19X1 and 12/31/19X1,

respectively, represents amounts required to be set aside by a contractual

agreement with an insurer for the payment of specific workers’

compensation claims. Other long-term assets on the statement of financial

position included restricted cash of $100 $75 as of 1/1/19X1 and

12/31/19X1 that is pledged as collateral for long-term financing

arrangements as contractually required by a lender. The restriction is

expected to expire in a time period that is consistent with the maturity of the

long-term debt.

52. While the staff is recommending changes to the proposed amendments, the staff believes

that the changes are limited to clarifying what is meant by “nature,” which will promote

consistency and comparability in financial reporting. The staff acknowledges that

disclosures that are more prescriptive could result in a loss of useful information because

entities might omit other relevant information beyond what is prescribed and, thereby,

provide only boilerplate disclosures. In contrast, the staff notes that less prescriptive

disclosure requirements may not improve consistency and comparability in financial

reporting.

53. The staff acknowledges that another respondent recommended that entities should be

required to disclose the changes in the nature of restrictions that occur during the period,

including changes in the amount of restrictions. The staff thinks that disclosing the nature of

restrictions that exist at the end of a reporting period provides adequate information about

the amounts generally described as restricted cash or restricted cash equivalents presented

on the statement of financial position and included in the total amount of cash presented on

the statement of cash flows. Furthermore, the staff thinks that changes in the amount of

restricted cash and restricted cash equivalents could be gleaned from the statement of

financial position, and from the proposed disclosure on amounts and line items in which such

amounts are reported within the statement of financial position. Therefore, the staff does not

think that it is necessary to revise the proposed disclosure on the nature of restrictions related

to this recommendation.

54. Another respondent indicated that the proposed disclosure on the nature of restrictions on

cash and cash equivalents should be consistent with the disclosure required by SEC

Page 20 of 33

Regulation S-X Rule 5-02.1 (see paragraph 38 of this memo). The Task Force previously

noted that requiring expansive disclosures, such as the disclosure required by the SEC, would

go beyond the primary focus of Issue 16-A, which is to provide guidance on the presentation

of changes in restricted cash on the statement of cash flows. The staff also notes that

paragraph D21 of the proposed Concepts Statement states that the Board attempts to avoid

requiring information in notes that entities are otherwise required to provide, for example,

in SEC filings. However, the staff notes that the Board at times considers requiring disclosure

of information that duplicates or overlaps with SEC rules because FASB standards apply to

reporting entities that are not SEC registrants and the proposed disclosures would apply to

all entities. Disclosure guidance about restrictions on cash and cash equivalents currently

does not exist for other-than-public business entities, aside from limited guidance for not-

for-profit organizations and a disclosure that is specific to financial institutions.

Disclosure of Gross Transfers

55. The proposed Update included the following question on disclosures:

Question 4: Would disclosures of the amounts of gross transfers between cash, cash

equivalents, and amounts generally described as restricted cash or restricted cash equivalents

(excluding transfers, constructive or actual, that result in a concurrent cash receipt from or a

concurrent cash payment to an outside source) provide meaningful information to financial

statement users? Please explain why.

56. Eleven respondents, including 4 professional accounting associations, 4 preparers, and 3

accounting firms, replied that disclosures of the amounts of gross transfers between cash,

cash equivalents, and amounts generally described as restricted cash or restricted cash

equivalents (excluding transfers, constructive or actual, that result in a concurrent cash

receipt from or a concurrent cash payment to an outside source) would not provide

meaningful information to financial statement users.

57. Some of those 11 respondents stated that disclosures of the amounts of gross transfers would

not provide useful information about an entity’s operating, investing, and financing activities

because there is no cash flow with a source outside the entity, and financial statement users

Page 21 of 33

are focused on the period-end balances of restricted cash that will be disclosed. One of those

respondents, an accounting firm, asserted that the primary concern for financial statement

users is understanding the nature and amount of material restrictions, rather than the amount

of gross transfers during the period. A preparer stated that disclosure of net transfers would

provide meaningful information, while disclosure of gross transfers would overemphasize

or give more prominence to restricted cash movements and serve as a distraction to financial

statement users. Lastly, another preparer stated that gross transfers and restricted cash

amounts received from and paid to external sources would both need to be disclosed to

clarify a reporting entity’s liquidity position.

58. Four respondents, two professional accounting associations, one accounting firm, and one

preparer, stated that disclosures of the amounts of gross transfers would provide meaningful

information to financial statement users. Those respondents stated that disclosing gross

transfers between unrestricted cash and restricted cash would provide meaningful

information about the availability of an entity’s cash resources and liquidity.

59. Four respondents did not respond to Question 4.

60. In prior outreach conducted, two users who prefer that changes in restricted cash resulting

from internal transfers be presented as line items in the body of the statement of cash flows

indicated that if restricted cash and restricted cash equivalents were required to be included

with cash and cash equivalents when reconciling the beginning-of-period and end-of-period

total amounts shown on the statement of cash flows, then disclosures of gross transfers might

provide useful information. Those users noted that such disclosures would provide

information about the changes in the nature of cash, that is, cash that is available becomes

unavailable when there is a transfer from unrestricted cash to restricted cash, and cash that

is unavailable becomes available when there is a transfer from restricted cash to unrestricted

cash.

Question 4 for the Task Force

4. Does the Task Force think that disclosures of the amounts of gross transfers

between cash, cash equivalents, and amounts generally described as restricted

cash or restricted cash equivalents (excluding transfers, constructive or actual, that

result in a concurrent cash receipt from or a concurrent cash payment to an outside

source) should be required?

Page 22 of 33

Staff Recommendation

61. The staff recommends that disclosures of the amounts of gross transfers between cash, cash

equivalents, and amounts generally described as restricted cash or restricted cash equivalents

not be required. The staff notes that a majority of respondents indicated that such disclosures

are not necessary.

62. The staff acknowledges that several comment letter respondents and a couple of users

indicated that such disclosures would provide meaningful information to financial statement

users about an entity’s liquidity position. However, the staff notes that paragraph 230-10-

10-1 states that the primary objective of a statement of cash flows is to provide relevant

information about the sources and uses of cash of an entity during a period. Therefore, the

staff believes that it is most meaningful to present the ultimate cash inflows and outflows of

an entity. Disclosures of gross transfers between cash, cash equivalents, and amounts

generally described as restricted cash or restricted cash equivalents would not provide

information about the ultimate cash inflows and outflows of an entity.

Other Disclosures

63. The proposed Update included the following question on disclosures:

Question 5: Should any other disclosures be provided? If so, please explain what disclosures

should be provided and why that information would be useful.

64. Nine respondents, including three professional accounting associations, three accounting

firms, and three preparers, stated that no additional disclosures are necessary.

65. Six respondents, including three professional accounting associations, one accounting firm,

one preparer, and one individual, recommended that additional disclosures be required. Two

professional accounting associations and the accounting firm recommended a disaggregated

rollforward by items or by groups of items included within restricted cash from the beginning

to end of the period that identifies third-party cash inflows and outflows (that is, direct cash

receipts into and direct cash payments from restricted cash and restricted cash equivalents)

as well as amounts of gross transfers received from or returned to operating cash accounts

as noted in Question 4 of the Exposure Draft.

Page 23 of 33

66. Two of the professional accounting associations recommended that entities disclose

information about the forward liquidity of restricted cash accounts, including disclosures of

amounts expected to be available for use within the 12-month period subsequent to the date

of the financial statements, and any contractual obligations to replenish the restricted cash

accounts. A third professional accounting association and the accounting firm recommended

disclosure of an accounting policy for determining which items are treated as restricted cash

and restricted cash equivalents because such disclosure would provide context in the event

that two entities reach different financial reporting conclusions about whether conditions of

restrictions exist. One preparer who opposed the proposed amendments in Question 1

recommended disclosing the various types of restrictions that exist and the associated cash

flow statement classification of changes in restricted cash.

67. The staff conducted outreach with five financial statement users, three of whom are private

company financial statement users. The three private company financial statement users

indicated that disclosures of the nature of restrictions on cash would provide sufficient

relevant information and that no additional disclosures are necessary. The other two users

indicated that it is important for users to understand how restricted cash affects liquidity so

that users can exclude such cash from measures of liquidity, and therefore disclosures about

liquidity and availability of cash would provide meaningful information.

68. Four respondents did not respond to Question 5.

Question 5 for the Task Force

5. Does the Task Force think that any other disclosures should be required?

Staff Recommendation

69. The staff notes that a majority of respondents indicated that additional disclosures are not

necessary and the staff thinks that most of the disclosures suggested by several respondents

go beyond the primary focus of Issue 16-A (for example, information about the forward

liquidity of restricted cash accounts), which is to provide narrow guidance about the

presentation of changes in restricted cash or restricted cash equivalents on the statement of

cash flows, thereby reducing diversity in practice. The staff also notes that the Task Force

Page 24 of 33

previously discussed and reached a consensus-for-exposure to require certain limited

disclosures to supplement the statement of cash flows.

70. The staff recognizes that a few respondents recommended that entities be required to disclose

a disaggregated rollforward of restricted cash and restricted cash equivalents. Because a

disaggregated rollforward could provide relevant information about changes in restricted

cash, the staff applied the relevant decision question in the proposed Concepts Statement to

evaluate whether such disclosure would be appropriate for inclusion in the notes to financial

statements and relevant to financial statement users. Decision Question L7 states, “Are the

causes of the changes in an entity’s line item of an asset, liability, or equity instrument not

easily understood?” In the proposed Concepts Statement, information to be considered for

disclosure on decision Question L7 is the cause of changes from the prior period such as

major inflows and outflows summarized by type of a detailed roll forward. Changes in

restricted cash result from both internal transfers between cash and restricted cash and cash

receipts from and cash payments to a source outside the entity. The staff believes that

because the ultimate cash inflows and outflows of amounts generally described as restricted

cash and restricted cash equivalents would be presented in the statement of cash flows, a

detailed roll forward would not provide significantly incremental relevant information about

the sources and uses of cash of an entity during a period. Therefore, the staff does not

recommend revising the proposed disclosure to include a detailed roll forward.

71. The staff recognizes that a couple of respondents recommended an accounting policy

disclosure for determining which items are treated as restricted cash and restricted cash

equivalents. The staff thinks that guidance on the disclosure of accounting policies in Topic

235, Notes to Financial Statements, is adequate and no specific accounting policy disclosure

guidance for determining which items are treated as restricted cash and restricted cash

equivalents is necessary.

72. The staff thinks there are current FASB projects or potential future FASB projects that would

be more appropriate for broader standard-setting activities related to disclosures about

restrictions on cash. The Disclosure Framework project, whose objective and primary focus

is to improve the effectiveness of disclosures in notes to financial statements by clearly

communicating the information that is most important to users of each entity’s financial

Page 25 of 33

statements, could holistically consider disclosures about restrictions on cash. The staff also

notes that the FASB issued an Invitation to Comment (ITC) in August 2016 to solicit

feedback about financial reporting issues that the FASB should consider adding to its agenda.

Included in the ITC is a chapter about reporting performance and cash flows (including

income statement, segment reporting, other comprehensive income, and statement of cash

flows). For those reasons, the staff recommends that the Task Force not require additional

disclosures beyond those recommended elsewhere in this memo as a part of this Issue.

Transition Method

73. The proposed Update included the following question on transition method:

Question 6: Do you agree that the proposed amendments should be applied using a

retrospective transition method? If not, please explain what transition method would be more

appropriate and why?

74. Fifteen respondents supported retrospective transition of the proposed amendments because

it would enhance the consistency and comparability of financial information. Four

respondents did not respond to Question 6.

Question 6 for the Task Force

6. Does the Task Force want to affirm that the proposed amendments should be

applied using the retrospective transition method?

Staff Recommendation

75. The staff recommends the Task Force affirm its consensus-for-exposure to apply the

amendments retrospectively to all periods presented because the staff thinks that

retrospective application of the proposed amendments would enhance interperiod

consistency and comparability of financial information.

Page 26 of 33

Transition Disclosures

76. The proposed Update included the following question on transition disclosures:

Question 7: Do you agree that an entity should be required to provide the transition

disclosures specified in the proposed Update? Should any other transition disclosures be

required? If so, please explain what transition disclosures should be required and why.

77. The proposed Update stated that an entity would provide the disclosures in paragraphs 250-

10-50-1(a) and (b)(1) and 250-10-50-2, as applicable, in the first interim and annual period

of adoption. Those paragraphs disclose the nature of and reason for the change in accounting

principle (that is, the changes in the presentation of changes in restricted cash and restricted

cash equivalents on the statement of cash flows) and a description of the prior period

information that has been retrospectively adjusted.

78. Eleven respondents agreed with the transition disclosures in the proposed Update. Several

of those respondents noted that the proposed transition disclosures would provide sufficient

information to financial statement users and no additional transition disclosures should be

required. One of those 11 respondents, a professional accounting association, stated that it

should be made clearer that in transition paragraph 230-10-65-3(c), it is not necessary for an

entity to establish preferability of the change in accounting principle because the issuance of

a Codification Update that requires use of a new accounting principle constitutes sufficient

support for making such a change.

79. One accounting firm indicated that it is unclear whether the Task Force intends to allow

entities to change their policy for identifying and reporting restricted cash or restricted cash

equivalents (that is, adopting a new definition of restricted cash or restricted cash

equivalents) upon adoption of the final amendments or whether entities need to maintain

their existing definitions. The accounting firm asserted that the proposed transition

disclosures would provide meaningful information when an entity changes its policy for

identifying and reporting restricted cash or restricted cash equivalents upon adoption of the

final amendments, but would provide less meaningful information simply for a change in

the presentation of restricted cash and restricted cash equivalents on the statement of cash

flows.

Page 27 of 33

80. Seven respondents did not respond to Question 7.

Question 7 for the Task Force

7. Does the Task Force want to affirm its consensus-for-exposure that the

transition disclosures in paragraphs 250-10-50-1(a) and (b)(1) and 250-10-50-2, as

applicable, in the first interim and annual period of adoption, be required?

Staff Recommendation

81. The staff recommends that the Task Force affirm its consensus-for-exposure that the

transition disclosures in paragraphs 250-10-50-1(a) and (b)(1) and 250-10-50-2, as

applicable, in the first interim and annual period of adoption, be required.

82. The staff acknowledges the concern raised by a professional accounting association about

clarifying that it is not necessary for an entity to establish preferability upon adoption of the

new guidance. The staff thinks that clarification is not necessary because of existing

guidance, which is as follows:

250-10-45-13 The issuance of a Codification update that requires the use of a

new accounting principle, interprets an existing principle, expresses a

preference for an accounting principle, or rejects a specific principle may

require an entity to change an accounting principle. The issuance of such an

Update constitutes sufficient support for making such a change.

83. The staff also acknowledges the concern raised by an accounting firm. The staff thinks the

proposed transition disclosures only relate to the adoption of the proposed amendments (that

is, the proposed changes in the presentation of changes in restricted cash and restricted cash

equivalents on the statement of cash flows and the proposed related disclosures) and not

whether an entity changes its policy for identifying and reporting restricted cash or restricted

cash equivalents. The staff also notes that paragraph BC7 of the proposed Update states that

the Task Force’s intent is not to change practice for what an entity reports as restricted cash

or restricted cash equivalents.

Effective Date and Early Adoption

84. The proposed Update included the following questions on effective date and early adoption:

Page 28 of 33

Question 8: How much time will be necessary to implement the proposed amendments? Do

entities other-than-public business entities need additional time to apply the proposed

amendments? Why or why not?

Question 9: Should early adoption be allowed? Why or why not?

85. Four respondents stated that the amount of time needed to implement the amendments as

described in the proposed Update would not be significant. Six respondents indicated that a

transition period of one year from the issuance of the new standard should give entities

enough time to implement the amendments. One respondent recommended a two-year

transition period to implement the amendments. Several respondents were unable to estimate

the time needed to implement the amendments. Four respondents did not respond to Question

8.

86. Six respondents stated that entities other-than-public business entities should be permitted

an additional year to implement the proposed amendments. Six other respondents either

stated that additional time would not be needed by other-than-public business entities to

implement the proposed amendments or that all entities should have the same effective date.

Seven respondents did not comment on whether entities other-than-public business entities

would need additional time to apply the proposed amendments.

87. Thirteen respondents agreed that early adoption should be allowed. An accounting firm

stated that while early adoption will reduce comparability with entities that do not early

adopt, the benefits of early adoption justify the potential lack of comparability considering

the divergence in practice and the resulting lack of comparability that currently exists in

practice. Another accounting firm stated that whether the new guidance is early adopted or

not, there will be sufficient information disclosed to give financial statement users the ability

to compare financial statements of different fiscal years, as well as the financial statements

of different entities.

88. Two preparers did not think that early adoption should be allowed because it may reduce

comparability of different entities’ statements of cash flows. Four respondents did not

respond to Question 9.

Page 29 of 33

Questions 8 and 9 for the Task Force

8. What should be the effective date?

9. Should early adoption be permitted?

Staff Recommendation

89. Based on comment letter feedback, the staff believes that the time required to implement the

amendments in the proposed Update would be minimal. The staff thinks that because the

amendments in this Update only require a change in the presentation and classification of

the statement of cash flows and limited disclosures, minimal time would be required to

implement the amendments. Therefore, the staff recommends that for public business

entities, the amendments in the proposed Update should be effective for fiscal years

beginning after December 15, 2017, and interim periods within those fiscal years.

90. Respondents were evenly split on whether the effective date should be the same for all

entities or different for other-than-public business entities. The staff considered the Private

Company Decision-Making Framework. It recommends that, generally, (a) the amendments

in an Accounting Standards Update should be effective for other-than-public business

entities one year after the first fiscal year for which public business entities are required to

adopt them and (b) other-than-public business entities should not be required to adopt

amendments during an interim period within the initial fiscal year of adoption. The additional

one-year transition period will allow a complete training cycle to occur, which will enable

other-than-public business entities to become aware of the changes. For entities other-than-

public business entities, the staff recommends that the amendments in the proposed Update

should be effective for fiscal years beginning after December 15, 2018, and interim periods

within fiscal years beginning after December 15, 2019.

91. The staff recommends that all entities should be permitted to early adopt the amendments in

the proposed Update. Specifically, entities would be permitted to apply the proposed

amendments for any annual or interim period for which the entity’s financial statements have

not yet been issued or made available for issuance; however, application would be as of the

beginning of the annual period.

Page 30 of 33

Definition of Restricted Cash and Restricted Cash Equivalents

92. While the proposed Update did not include a question about a definition of restricted cash

and restricted cash equivalents, multiple respondents provided feedback about the lack of a

definition of restricted cash and restricted cash equivalents.

93. One preparer recommended that to further the goal of reducing diversity, a definition of

restricted cash and restricted cash equivalents should be established. Given the absence of a

clear definition, preparers find it challenging to identify restricted cash and restricted cash

equivalents. That preparer observed that guidance that explicitly defines restricted cash and

restricted cash equivalents would provide financial statement preparers a basis for consistent

application.

94. Another respondent, an accounting firm, stated that given the lack of definition of restricted

cash and restricted cash equivalents, there could be continued diversity in practice in both

the statement of financial position and the cash flow statement presentation. The term

“restricted” carries a certain distinction for not-for-profit entities because it relates to a

donor’s intentions for the use of cash contributed. However, this term also can apply to cash

that has a legal or contractual restriction, whether held by a third party or not. Finally, the

term “restricted” can be broadly interpreted to include self-designated cash. The respondent

recommended that regardless of the outcome of the proposed amendments, the Task Force

should bring more clarity to the definition of restricted cash either by providing a definition

for the Master Glossary or by providing examples in the Codification of amounts generally

described as restricted cash or restricted cash equivalents.

95. Another accounting firm suggested that the Task Force reconsider developing a definition

of restricted cash and restricted cash equivalents. The respondent asserted that it is likely that

diversity exists in the way these instruments are defined as evidenced by the differing views.

96. A professional accounting association recognized that restricted cash and restricted cash

equivalents do not meet the existing Master Glossary definitions of cash and cash

equivalents. Accordingly, the respondent recommended that if restricted cash and restricted

cash equivalents are combined with cash and cash equivalents for purposes of presentation

on the statement of cash flows, the existing definitions of cash and cash equivalents should

Page 31 of 33

be amended so that cash and cash equivalents includes cash, cash equivalents, restricted

cash, and restricted cash equivalents. The respondent asserted that changing the definitions

may be useful in eliminating differences in interpretations.

97. While the staff recognizes the respondents’ concerns, the staff notes that the Task Force

previously considered defining restricted cash; however, it ultimately decided that the issue

resulting in diversity in practice is the presentation of changes in restricted cash on the

statement of cash flows. The staff also notes that the Task Force’s intent is not to change

practice for what an entity reports are restricted cash or restricted cash equivalents. The staff

does not recommend any action to be taken by the Task Force in Issue 16-A about these

concerns.

Page 32 of 33

Appendix A: Summary of Staff Recommendations

Cash Flow Issue Consensus-For-Exposure Staff Recommendation

Presentation of changes in restricted cash

A statement of cash flows should explain the change during the period in the total of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents.

Affirm the consensus-for-exposure

Disclosures:

Amounts and line items If the total of cash, cash equivalents, and amounts generally described as restricted cash and restricted cash equivalents at the beginning and end of the period shown on the statement of cash flows cannot be reconciled to the amounts of similarly titled line items on the statement of financial position, an entity should disclose on the face of the statement of cash flows or in the notes to the financial statements, the amounts and line items in which such amounts are reported within the statement of financial position.

Revise the proposed requirement to include any situation in which the statement of financial position includes more than one line item for cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents even when the titles of those line items on the statement of financial position are similar to the title of the total amounts of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents at the beginning and end of the period shown on the statement of cash flows.

Nature of restrictions An entity should disclose the nature of the restrictions on cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents.

Revise the proposed disclosure to clarify the type of information that might be provided by an entity when disclosing the nature of restrictions on its cash and cash equivalents.

Gross transfers Not applicable. Do not require disclosures of gross transfers.

Transition method Retrospective transition for all prior periods presented.

Affirm the consensus-for-exposure

Transition disclosures Provide the disclosures in paragraphs 250-10-50-1(a) and (b)(1) and 250-10-50-2, as applicable, in the first interim and annual period of adoption.

Affirm the consensus-for-exposure

Page 33 of 33

Cash Flow Issue Consensus-For-Exposure Staff Recommendation

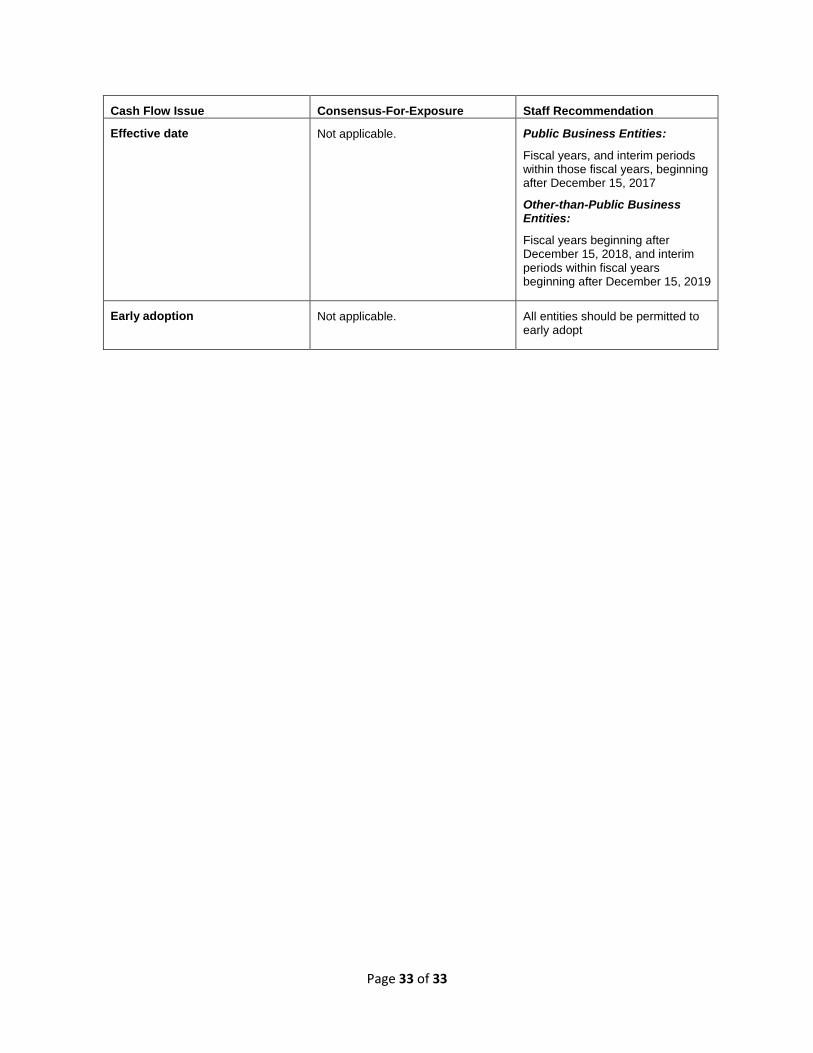

Effective date Not applicable. Public Business Entities:

Fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017

Other-than-Public Business Entities:

Fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019

Early adoption Not applicable. All entities should be permitted to early adopt