effectiveness of imf-supported stabilization...

TRANSCRIPT

Journal of International Money and Finance21 (2002) 565–587

www.elsevier.com/locate/econbase

Effectiveness of IMF-supported stabilizationprograms in developing countries

Ayse Y. EvrenselDepartment of Economics, Portland State University, Portland, OR 97207-0751, USA

Abstract

This paper examines the effectiveness of Fund-supported stabilization programs byinvestigating whether the IMF achieves its own objectives in such programs. Even though theFund’s conditionality prescribes fiscal and monetary discipline in program countries, the resultsof the empirical analysis show that the IMF cannot impose its conditionality even duringprogram years. Furthermore, when successive interprogram periods are considered, programcountries enter a new program in a worse macroeconomic condition than they entered theprevious program. These results and the fact that stabilization programs have a revolving natureare inconsistent with the effectiveness of IMF-supported stabilization programs and may signalthe existence of moral hazard. 2002 Elsevier Science Ltd. All rights reserved.

JEL classification: E63; F33; F40

Keywords: IMF; Stabilization programs; Conditionality; Moral hazard

1. Introduction

In its 58 years of existence, the IMF has been criticized because of its institutionalstructure and lending practices. Some argue that the IMF is a bureaucratic and non-transparent institution with no accountability for its actions. It has also been sug-gested that Fund-supported stabilization programs are ineffective and may createmoral hazard.

The motivation to provide another study on the IMF is based on three points.First, although there are a large number of publications about the IMF and its pro-

E-mail address: [email protected] (A.Y. Evrensel).

0261-5606/02/$ - see front matter 2002 Elsevier Science Ltd. All rights reserved.PII: S0261 -5606(02 )00010-4

566 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

grams, most publications express opinions about the Fund without providing quanti-tative evidence. There are several quantitative evaluations of Fund programs, mostof which have been provided by the IMF (Reichmann and Stillson, 1978; Donovan,1982; Loxley, 1984; Goldstein and Montiel, 1986; Khan, 1990; Joyce, 1992; Dorood-ian, 1993; Conway, 1994; Killick, 1995; Santaella, 1996; Knight and Santaella,1997).1

Second, the recent efforts to widen the IMF’s responsibilities make a quantitativestudy on the effectiveness of Fund-supported adjustment programs both timely andappropriate. In 1997, the IMF introduced the Supplemental Reserve Facility thatprovides large, short-term loans to countries in financial crises, as in the cases ofKorea, Russia, and Brazil. Third, motivated by the idea that Fund resources provideex-post assistance in a crisis, but realizing that they do not reduce the frequency andintensity of financial crises, it has recently been suggested that the IMF shouldassume the role of an international lender of last resort (Fischer, 1999). However,before defining new responsibilities for the IMF, one should be concerned with theperformance of the Fund in its traditional roles.

This paper focuses on the effectiveness of Fund-supported stabilization programsfor developing countries and has four characteristics. First, this study does not ques-tion the IMF’s existence, its rationale, its programs, and the content of conditionalityassociated with these programs.2 This paper’s approach to program evaluation is touse the IMF’s criteria to see whether the IMF achieves its own goals in these pro-grams. Second, this study uses a broader data set than previous program evaluationsin terms of the types of balance of payments programs (four types), the number ofprogram countries (91), and the length of the period under investigation (1971–97).Third, it provides a discussion of alternative evaluation methods and their weaknessesbefore the selection of the evaluation method. Fourth, the method of program evalu-ation is based on the observation of relevant variables during pre-program, program,and post-program years. Additionally, this paper attempts to relate program evalu-ation to moral hazard associated with the Fund’s lending.

The organization of the paper is as follows. Section 2 describes this study’sapproach to program evaluation, and provides a critique of previous evaluations.Section 3 constitutes the empirical part in which Fund-supported stabilization pro-grams are evaluated using the data on 91 developing countries for the period 1971–97. Finally, Section 4 summarizes the results of the empirical analysis and discussesthe effectiveness of stabilization programs.

2. Approach to program evaluation

2.1. Alternative approaches to program evaluations

There are three alternative approaches to the evaluation of adjustment programs.First, the outcome vs. alternative outcome approach compares the actual outcome in

1 Ul Haque et al. (1998) provide a review of previous program evaluations.2 See Vaubel (1991) and Willett (2000) on the political economy of international financial institutions.

567A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

an adjustment program with the outcome in an alternative program that would haveachieved a similar degree of adjustment. This approach has been suggested as theclosest approach to the ideal evaluation (Edwards, 1989; Krueger, 1998). However,in addition to the difficulty associated with estimating a robust alternative model, itis problematic to provide a meaningful definition of the term “similar degree ofadjustment” (Edwards, 1989). Therefore, this approach has not been used in pre-vious evaluations.

Second, the outcome vs. counterfactual approach describes the program effect asthe difference between the actual performance observed in a program and the per-formance that would have taken place in the absence of a program. Some evaluationstudies use this approach by considering the developing members of the IMF thathave not been involved in any IMF program as the control group (Goldstein andMontiel, 1986; Khan, 1990; Santaella, 1996).

The third way of evaluating adjustment programs is the outcome vs. targetapproach that determines whether the program objectives have been achieved. Theoutcome vs. target approach is difficult to implement, because the IMF does notmake the content of individual adjustment programs public.3 However, a generalizedversion of this approach, the outcome vs. purpose approach, has been used in almostall previous evaluations (Reichmann and Stillson, 1978; Donovan, 1982; Loxley,1984; Goldstein and Montiel, 1986; Khan, 1990; Santaella, 1996; Joyce, 1992;Doroodian, 1993; Conway, 1994; Knight and Santaella, 1997).

The outcome vs. purpose approach is based on the fact that the Fund’s purposein adjustment programs is to reduce or eliminate balance of payments problems. TheMonetary Approach to Balance of Payments (MBOP) that underlines the Fund’sconditionality suggests that the balance of payments problems are caused by incom-patible exchange rate, monetary, and fiscal policies in program countries. Therefore,the main purpose of adjustment programs is to induce program countries to controlthe size of the public sector and to exercise monetary discipline under peggedexchange rate regimes to prevent the depletion of international reserves.

2.2. Critique of previous program evaluations

The outcome vs. counterfactual approach (Goldstein and Montiel, 1986; Khan,1990; Santaella, 1996) has been applied to the program country vs. nonprogramcountry comparison, where nonprogram countries are believed to represent the con-trol group. The estimation of the counterfactual through the control group approachmay be misleading. Viewing the control group as the counterfactual implies thatthe macroeconomic performance of nonprogram IMF-members is indicative for the

3 This means that the selection of target variables, their values as suggested by conditionality, and anychanges in conditionality due to Article IV consultations are not made public. These consultations referto the periodic meetings between the Fund’s staff and the authorities of member countries that take placein the member country to collect and analyze economic data (IMF, Annual Report, 1992). Since May1997, the results of Article IV consultations are made public with the permission of the member country(IMF, Annual Report, 1998).

568 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

macroeconomic performance of program countries in the absence of an IMF pro-gram. However, being a program or a nonprogram country is a self-selected attribute.If anything, the difference between program and nonprogram countries in their mac-roeconomic performance will determine which country will become a program coun-try. Therefore, the outcome vs. counterfactual approach will not be used in thisstudy.4

Previous evaluations that use the outcome vs. purpose approach employ differentmethods to capture the Fund-effect: pooled regressions with a program year dummy,logit or probit models to discriminate between program and nonprogram years, andthe before–after method.

Pooled regressions with a program year dummy are used to explain the determi-nation of the subaccounts of the balance of payments where the sign and the signifi-cance of the program dummy is believed to explain the program effect on balanceof payments (Goldstein and Montiel, 1986; Khan, 1990; Doroodian, 1993). Thereare two problems associated with this approach. First, the fundamental problem isthe lack of theoretical background. Dependent and independent variables are inter-changed without any consideration of the direction of causality.

Second, the meaning of the program year dummy in pooled regressions shouldbe reconsidered. The program year dummy implies that adjustment programs affectthe outcome in target variables in a way that is not captured by other independentvariables in the model. For example, if being in a program year leads to significantlyhigher reserves, then this could be interpreted as the catalytic effect of adjustmentprograms. Such effects imply that program countries may have an easier access toprivate capital markets, if lenders view the IMF’s involvement in a country as asignal of stability. Therefore, the program dummy in pooled regressions does notreflect whether conditionality is imposed successfully.

Third, there is an implied assumption regarding the counterfactual in pooledregressions with a program dummy. It is assumed that nonprogram years representthe counterfactual for program years. However, they do not, because the informationregarding the availability of Fund programs is already imbedded in the variables fornonprogram years. Countries may follow riskier macroeconomic policies that willlead to a balance of payments crisis, knowing that Fund support will be available.Also, there may be a feedback from IMF programs on variables in question. There-fore, the sign and significance of the program year dummy in pooled regressionscannot be generalized as the program effect.

The discrimination analysis (logit or probit) is also employed to distinguishbetween program and nonprogram years (Joyce, 1992; Conway, 1994; Knight and

4 Although nonmembers of the IMF may be a proxy for the counterfactual, there are various problemsassociated with using them as such. Monaco, Liechtenstein, Andorra, and Vatican City do not qualify tobe in the sample not only because these countries do not have any control over their monetary policies,but also they are considered developed countries. No data are available for Nauru, Palau, and Tuvalu.Zaire became a nonmember country in 1997, which marks the end of the sample period. Taiwan is leftas the only nonmember country that could be used as the counterfactual sample, which is not enough todraw any conclusions.

569A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

Santaella, 1997). The problem with this technique is that it is difficult to find explana-tory variables that are not simultaneously determined. That is, it is very difficult tocome up with truly exogenous variables with which one can distinguish betweenprogram and nonprogram years.5 Additionally, the problem with the counterfactualstill exists. In this setting, the program year dummy is the dependent variable; how-ever, the right-hand side variables may not appropriately distinguish between pro-gram and nonprogram years because of the above mentioned effects of expectationsand feedback.

The before–after method of program evaluation has also been used where thedifference in the mean values of evaluation variables between program and nonpro-gram years is interpreted as the program effect (Reichmann and Stillson, 1978; Dono-van, 1982; Loxley, 1984; Khan, 1990). As in other types of evaluations, the problemwith the counterfactual also exists in the before–after method. Ul Haque et al. (1998)note that the before–after approach implies a constant counterfactual with respect tothe policies and the external environment of the program country.

It is obvious that estimating the counterfactual represents the main problem inprogram evaluations. In an attempt to calculate the “ true” effects of Fund-supportedprograms, some studies employ an estimator of the Fund effect that distinguishesbetween policy and target variables (Goldstein and Montiel, 1986; Khan, 1990).6

The target variables are determined by the vector of policy variables, exogenousshocks, and the program dummy. Similar to pooled regressions, the program dummyis assumed to reflect the Fund effect. These studies recognize that policy variablesare not directly observable in program countries. The counterfactual for policy vari-ables is constructed by using the difference between desired and actual (lagged)values of the target variables. This estimation of the Fund effect suffers from thepractice of interchanging the dependent and independent variables, because targetvariables are affected by policy variables and vice versa.7

The discussion of evaluation methods indicates that all types of program evalu-ations are problematic, and a perfect solution to the problems of program evaluationdoes not exist. However, the recognition of these problems is important with regardto the selection of the evaluation method and the interpretation of evaluation results.

2.3. This study’s approach to program evaluation

Although there are many interesting questions regarding the effectiveness of Fundsupported programs, the question to which there is a methodologically correct answer

5 The lack of exogeneity represents a problem also in the simulation study of Khan and Knight (1981)in which a system of equations determines output, prices, reserves, money, and fiscal policy.

6 In Goldstein and Montiel (1986), this is called the modified estimator of the Fund effect.7 Theoretically, there is a superior way of estimating the counterfactual. Because an IMF member is

expected to include the availability of Fund support in her macroeconomic decisions, the data based onmembership years should not be used to estimate the counterfactual. Table 1 indicates that some countriesbecame IMF members during the early or mid-1980s. Using the data from nonmember years, the coun-terfactual may be estimated for the member years. Unfortunately, the pre-membership data have manymissing observations regarding late members so that forecasting the counterfactual was not possible.

570 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587T

able

1IM

F-su

ppor

ted

adju

stm

ent

prog

ram

sin

deve

lopi

ngco

untr

ies,

1971

–97a

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Afg

hani

stan

MSB

SBSB

SBA

lger

iaM

SBSB

SBSB

SBSB

/E

FFE

FFE

FFA

ngol

aM

Ant

igua

Man

dB

arbu

daA

rgen

tina

MSB

SBSB

SBSB

SBSB

SBSB

SBSB

SB/

EFF

EFF

EFF

SB/

SBE

FFE

FFB

angl

ades

hM

SBSB

SBSB

SB/

EFF

EFF

EFF

/SB

SBSB

/SA

FSA

FSA

F/SA

F/SA

F/SA

F/SA

FSA

FSA

FE

FFSB

SAF

ESA

FE

SAF

ESA

FE

SAF

Bar

bado

sM

SBSB

SBSB

SBB

eliz

eM

SBSB

SBB

enin

MSA

FSA

FSA

FSA

FSA

F/SA

F/SA

F/SA

F/E

SAF

ESA

FE

SAF

ESA

FB

huta

nM

Bol

ivia

MSB

SBSB

SBSB

/SB

/SA

F/SA

F/SA

F/SA

F/SA

F/SA

F/SA

F/SA

F/SA

F/E

SAF

SAF

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FB

otsw

ana

MB

razi

lM

SBSB

EFF

EFF

EFF

EFF

SBSB

SBSB

SBB

urki

noM

SAF

SAF

SAF/

SAF/

SAF/

SAF/

Faso

ESA

FE

SAF

ESA

FE

SAF

Bur

undi

MSB

SBSB

/SB

/SB

/SA

FSA

FSA

F/SA

F/SA

F/SA

F/SA

FSA

FSA

FSA

FSA

FE

SAF

ESA

FE

SAF

ESA

FC

ambo

dia

MN

BM

ESA

FE

SAF

ESA

FE

SAF

Cam

eroo

nM

SBSB

SBSB

SBSB

SBSB

Cap

eV

erde

MC

entr

alM

SBSB

SBSB

SBSB

SB/

SB/

SAF

SAF

SAF

SAF

SAF

SB/

SB/

SAF

Afr

ican

SAF

SAF

SAF

SAF

Rep

.C

had

MSA

FSA

FSA

FSA

FSA

FSA

FSA

FSA

F/SA

F/SA

F/E

SAF

SBSB

/E

SAF

ESA

FC

hile

MSB

SBSB

SBSB

SB/

EFF

EFF

EFF

EFF

/SB

EFF

SBC

hina

MSB

SBSB

(Con

tinu

edov

erle

af)

571A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587T

able

1(C

onti

nued

)

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Col

ombi

aM

SBSB

SBC

omor

osM

SAF

SAF

SAF

SAF

SAF

SAF

Con

goM

SBSB

SBSB

SBSB

SBSB

SBSB

SBC

osta

Ric

aM

SBSB

SBSB

/SB

/SB

/E

FFSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

EFF

EFF

EFF

Cot

eM

EFF

EFF

EFF

EFF

SBSB

SBSB

SBSB

SBSB

ESA

FE

SAF

ESA

FE

SAF

d’Iv

oire

Cyp

rus

MSB

SBD

jibou

tiM

SBSB

Dom

inic

aM

EFF

EFF

EFF

EFF

/SB

SAF

SAF

SAF

SAF

SAF

SAF

SAF

SAF

SAF

SAF

SAF

SBD

omin

ican

ME

FFE

FFE

FF/

EFF

/SB

SBSB

Rep

.SB

SBE

cuad

orM

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBE

gypt

MSB

SB/

EFF

EFF

EFF

SBSB

SBSB

SB/

EFF

EFF

EFF

EFF

EFF

El

Salv

ador

MSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

Equ

ator

ial

MSB

SBSB

SBSA

FSA

FSA

FSA

FSA

FSA

F/SA

F/SA

F/SA

F/G

uine

aE

SAF

ESA

FE

SAF

ESA

FE

ritr

eaM

Eth

iopi

aM

SBSB

SAF

SAF

SAF

SAF

SAF

Fiji

MSB

SBG

abon

MSB

SBE

FFE

FFE

FFSB

SBSB

SBSB

SBSB

SBSB

EFF

/E

FFE

FFSB

Gam

bia,

MSB

SBSB

SBSB

SBSB

SBSB

/SB

/SA

F/SA

F/SA

F/SA

F/SA

FSA

FSA

FSA

FSA

FT

heSA

FSA

FE

SAF

ESA

FE

SAF

ESA

FG

hana

MSB

SBSB

SBSB

SBSB

/E

FF/

EFF

/E

FF/

SAF/

SAF/

SAF

SAF

SAF/

SAF/

ESA

FE

FF/

SAF/

SAF/

SAF/

ESA

FE

SAF

ESA

FE

SAF

SAF

ESA

FE

SAF

ESA

FG

rena

daM

SBSB

SBSB

SBSB

EFF

EFF

EFF

EFF

(Con

tinu

edon

next

page

)

572 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587T

able

1(C

onti

nued

)

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Gua

tem

ala

MSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBG

uine

aM

SBSB

SBSB

/SB

/SA

FSA

FSA

F/SA

F/SA

F/SA

F/SA

F/SA

F/SA

FSA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FG

uine

a-M

SAF

SAF

SAF

SAF

SAF

SAF

SAF

SAF

SAF/

SAF/

ESA

FB

issa

uE

SAF

ESA

FG

uyan

aM

SBSB

SBSB

SBSB

SBSB

SB/

EFF

EFF

EFF

EFF

SB/

SB/

ESA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

EFF

ESA

FE

SAF

Hai

tiM

SBSB

SBSB

SBSB

SBSB

/E

FFE

FFE

FFSB

SBSB

SBSA

FSA

FSA

FSB

/SB

/SA

FSA

FSA

FSA

FSB

/SB

/E

FFSA

FSA

FSA

FSA

FH

ondu

ras

MSB

SBSB

EFF

EFF

EFF

EFF

/SB

SBSB

SB/

ESA

FE

SAF

ESA

FE

SAF

ESA

FSB

ESA

FIn

dia

ME

FFE

FFE

FFE

FFSB

SBSB

Indo

nesi

aM

SBSB

SBIr

anM

Iraq

MJa

mai

caM

SBSB

SBSB

/SB

/E

FFE

FFE

FFE

FFE

FF/

SBSB

SBSB

SBSB

SBSB

/E

FFE

FFE

FFE

FFE

FFE

FFSB

EFF

Jord

anM

SBSB

SBSB

SBSB

/E

FFE

FFE

FFE

FFK

enya

ME

FFE

FFE

FFE

FF/

SBSB

SBSB

SBSB

SBSB

SB/

SB/

SAF/

SAF/

SAF/

SAF/

SAF/

SAF

SAF/

ESA

FSB

SAF

SAF/

ESA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FK

irib

ati

MK

orea

MSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

Lao

MSB

SBSA

FSA

FSA

FSA

FSA

F/SA

F/SA

F/SA

F/Pe

ople

’sE

SAF

ESA

FE

SAF

ESA

FD

em.

Rep

.L

eban

onM

Les

otho

MSA

FSA

FSA

FSA

F/SA

F/SA

F/SA

F/SA

F/E

SAF

ESA

FE

SAF

ESA

F/SB

SB(C

onti

nued

over

leaf

)

573A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587T

able

1(C

onti

nued

)

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Lib

eria

MSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBM

adag

asca

rMSB

SBSB

SBSB

SBSB

SBSB

SB/

SB/

SB/S

AF/S

AF/

SAF/

SAF/

SAF

SAF

SAF

SAF

SAF

SAF

ESA

FE

SAF

ESA

FE

SAF

Mal

awi

MSB

SBSB

SBSB

/E

FFE

FFE

FFSB

/SB

/E

SAF

ESA

FE

SAF

ESA

FSB

/SB

/E

SAF

ESA

FE

FFE

SAF

ESA

FE

SAF

ESA

FM

alay

sia

MM

aldi

ves

MM

ali

MSB

SBSB

SBSB

SBSB

SBSB

/SB

/SB

/SA

FSA

F/SA

F/SA

F/SA

F/SA

F/E

SAF

SAF

SAF

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FM

arsh

all

MIs

land

sM

auri

tani

aM

SBSB

SBSB

SBSB

SB/

SB/

SB/

SAF/

SAF/

SAF/

SAF/

SAF/

SAF/

SAF/

SAF/

ESA

FSA

FSA

FSA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FM

auri

tius

MSB

SBSB

SBSB

SBSB

SBSB

Mex

ico

ME

FFE

FFE

FFE

FFE

FFE

FFSB

SBSB

EFF

EFF

EFF

EFF

EFF

SBSB

Mic

rone

sia

MM

ongo

liaM

SBSB

ESA

FE

SAF

ESA

FE

SAF

Mor

occo

ME

FFE

FFE

FF/

EFF

/SB

SBSB

SBSB

SBSB

SBSB

SBSB

SBM

ozam

biqu

eM

SAF

SAF

SAF

SAF/

SAF/

SAF/

SAF/

SAF/

SAF/

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

Mya

nmar

MSB

SBSB

SBSB

SBSB

SBN

amib

iaM

Nep

alM

SBSB

SBSB

SB/

SAF

SAF

SAF

SAF

SAF/

SAF/

SAF/

SAF/

SAF

SAF

ESA

FE

SAF

ESA

FE

SAF

Nic

arag

uaM

SBSB

SBSB

SBSB

SBE

SAF

ESA

FE

SAF

ESA

FN

iger

MSB

SBSB

SB/

SB/

SAF/

SAF/

SAF/

SAF/

SAF

SAF

SB/

SB/

SAF

SAF

SAF

ESA

FE

SAF

ESA

FE

SAF

SAF

SAF

Nig

eria

MSB

SBSB

SBSB

SBPa

kist

anM

SBSB

SBSB

SBSB

EFF

EFF

EFF

EFF

SB/

SB/

SB/

SAF

SAF

SAF/

SAF/

SB/

SB/

SB/

SAF

SAF

SAF

SBSB

/E

FF/

EFF

/E

FF/

EFF

/E

SAF

ESA

FE

SAF

ESA

FPa

nam

aM

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

Papu

aN

ewM

SBSB

SBSB

SBSB

Gui

nea

(Con

tinu

edon

next

page

)

574 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587T

able

1(C

onti

nued

)

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Para

guay

MPe

ruM

SBSB

SBSB

EFF

EFF

EFF

/E

FF/

EFF

EFF

EFF

EFF

SBSB

Phili

ppin

esM

SBSB

SBSB

SB/

EFF

EFF

EFF

/SB

SBSB

SBSB

SBSB

SBE

FFE

FFSB

/SB

/SB

EFF

EFF

EFF

EFF

EFF

SBE

FFE

FFR

wan

daM

SBSB

SAF

SAF

SAF

SAF

SAF

SAF

StK

itts

and

MN

evis

StL

ucia

MSt

Vin

cent

Man

dth

eG

rena

dine

sSa

oT

ome

and

Prin

cipe

MSA

FSA

FSA

FSA

FSA

FSA

FSA

FSA

FSe

nega

lM

SBSB

/SB

/SB

/SB

/SB

SBSB

/SB

/SB

/SA

F/SA

F/SA

F/SA

F/SA

FSB

/SB

/SA

F/E

SAF

EFF

EFF

EFF

EFF

SAF

SAF

SAF/

ESA

FE

SAF

ESA

FE

SAF

SAF/

SAF/

ESA

FE

SAF

ESA

FE

SAF

Seyc

helle

sM

Sier

raM

SBSB

SBSB

EFF

EFF

EFF

EFF

/SB

SB/

SB/

SAF

SAF

SAF

SAF

SAF

SAF

SAF/

SAF/

SAF/

ESA

FL

eone

SBSA

FSA

FE

SAF

ESA

FE

SAF

Solo

mon

MSB

SBSB

SBIs

land

sSo

mal

iaM

SBSB

SBSB

SBSB

SBSB

/SB

/SB

/SA

FSA

FSA

FSA

FSA

FSA

FSA

FSA

FSA

FSA

FSo

uth

MA

fric

aSr

iL

anka

MSB

SBSB

SBE

FFE

FFE

FFE

FFSB

SBSA

FSA

FSA

FSA

F/SA

F/SA

F/SA

F/SA

F/SA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

Suda

nM

SBSB

SBSB

EFF

EFF

EFF

EFF

/SB

SBSB

SBSu

rina

me

MSw

azila

ndM

(Con

tinu

edov

erle

af)

575A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587T

able

1(C

onti

nued

)

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Syri

anM

Ara

bR

ep.

Tan

zani

aM

SBSB

SBSB

SBSB

SB/

SB/

SAF

SAF

SAF/

SAF/

SAF/

SAF/

SAF

SAF

SAF

SAF

ESA

FE

SAF

ESA

FE

SAF

Tha

iland

MSB

SBSB

SBSB

SBSB

SBT

ogo

MSB

SBSB

SBSB

SBSB

SBSB

SB/

SB/

SAF/

SAF/

SAF/

SAF/

SAF/

SAF/

SAF/

ESA

FSA

FSA

F/E

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FT

onga

MT

rini

dad

MSB

SBSB

and

Tob

ago

Tun

isia

MSB

SBSB

/E

FFE

FFE

FFE

FFE

FFT

urke

yM

SBSB

SBSB

SBSB

SBSB

SBSB

SBU

gand

aM

SBSB

SBSB

SBSB

SBSA

FSA

FSA

F/SA

F/SA

F/SA

F/SA

F/SA

F/SA

F/SA

F/E

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

ESA

FE

SAF

Uru

guay

MSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

SBSB

Van

uatu

MV

enez

uela

ME

FFE

FFE

FFE

FFE

FFV

ietn

amM

SBSB

/E

SAF

ESA

FE

SAF

ESA

FW

este

rnM

SBSB

SBSB

SBSB

SBSB

SBSa

moa

Yem

enM

SBSB

Zai

reM

SBSB

SBSB

SBSB

/E

FFE

FF/

EFF

/SB

SBSB

/SB

/SB

/SB

/SA

FSA

FSA

FSA

FSA

FSA

FN

ME

FFSB

SBSA

FSA

FSA

FSA

FZ

ambi

aM

SBSB

SBSB

SBSB

SBE

FFE

FFE

FF/

EFF

/SB

SBSB

SBSA

F/SA

F/E

SAF

SBSB

ESA

FE

SAF

Zim

babw

eM

SBSB

SBSB

EFF

/E

FF/

EFF

/E

FF/

ESA

FE

SAF

ESA

FE

SAF

EFF

,E

xten

ded

Fund

Faci

lity;

ESA

F,E

xten

ded

Stru

ctur

alA

djus

tmen

tFa

cilit

y;SA

F,St

ruct

ural

Adj

ustm

ent

Faci

lity;

SB,

Stan

dby.

aT

his

tabl

eis

cons

truc

ted

base

don

the

info

rmat

ion

prov

ided

inva

riou

sis

sues

ofth

eA

nnua

lR

epor

tpu

blis

hed

byth

eIM

F.M

indi

cate

sth

eye

arw

hen

aco

untr

ybe

cam

ean

IMF

mem

ber.

NM

indi

cate

sno

n-m

embe

r,an

dit

isus

edfo

rZ

aire

whi

chdi

scon

tinue

dits

IMF

mem

bers

hip

in19

97.

576 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

is the one regarding the conditional effect of a program. For example, the Fundviews an unsustainable increase in domestic credit (unsustainable at the givenexchange rate) as the main cause of balance of payments problems. Therefore, con-ditionality associated with adjustment programs prescribes a reduction in domesticcredit creation. One can ask whether domestic credit creation differs significantlybetween the pre-program, program and post-program periods.

In this paper, the premise of program evaluation is what the Fund expects programcountries to do and whether these objectives are achieved. The Fund expects programcountries to reduce their domestic credit creation, budget deficit, domestic borrowing,inflation rate, current account and capital account deficit. The relevant question iswhether we observe significant improvement in these variables under an IMF pro-gram.

At this point, the following trio of critique appears immediately. First, the IMFdoes not have any authority over sovereign countries, which means that programcountries may not follow the IMF’s advice. Second, even if program countries tryto follow the IMF’s advice, they may face exogenous shocks that prevent countriesfrom improving upon evaluation variables. Third, program countries may have scoredworse without an IMF program.

With regard to the first point, there is a valid reason for conducting programevaluations to measure the IMF’s success, and not program countries’ willingnessto improve their macroeconomic performance. Since the IMF provides programcountries with subsidized loans justified by the existence of conditionality, the Fundis expected to demonstrate its ability to impose the content of conditionality. Second,if program countries were struck by exogenous, adverse shocks in a systematicfashion during a period of, say, 30 years, program countries would be consideredas victims of economic disasters. Then the IMF would become the financial RedCross and provide disaster relief without imposing conditionality.

Third, the fact that program countries may have been worse off without the IMF’ssupport is not the only possible outcome. Suppose the inflation rate in a countrybefore and during an IMF program was 40 and 60%, respectively. Although onemay interpret this as a sign of IMF’s ineffectiveness in reducing the inflation rate,it is possible that the inflation rate could have been 80% in the absence of an IMFprogram. However, it is also possible that, in the absence of the IMF support, coun-tries may have decided to follow sounder macroeconomic policies. Again, the pointis that the IMF’s conditionality is supposed to increase the shadow price of the IMFsupport to program countries. The question is whether it does so. This does not meanthat the counterfactual is irrelevant. However, the actual data should not be dismissedtoo quickly, because it shows the extent to which conditionality is enforced, every-thing else remaining the same.

In this paper, Fund-supported programs are evaluated based on the outcome vs.purpose approach using the before–after method. As opposed to previous before–after evaluations that consider one-year lags before and after a program, this studyuses lags of up to three years to observe changes in the evaluation variables fromthree years before the start of a program to three years after the end of a program.This method demonstrates how evaluation variables gradually change toward a pro-

577A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

gram and after a program. To support the results of the before–after analysis, thetemporal interprogram analysis is used to illustrate the possibility of moral hazardassociated with Fund programs.

3. Empirical analysis

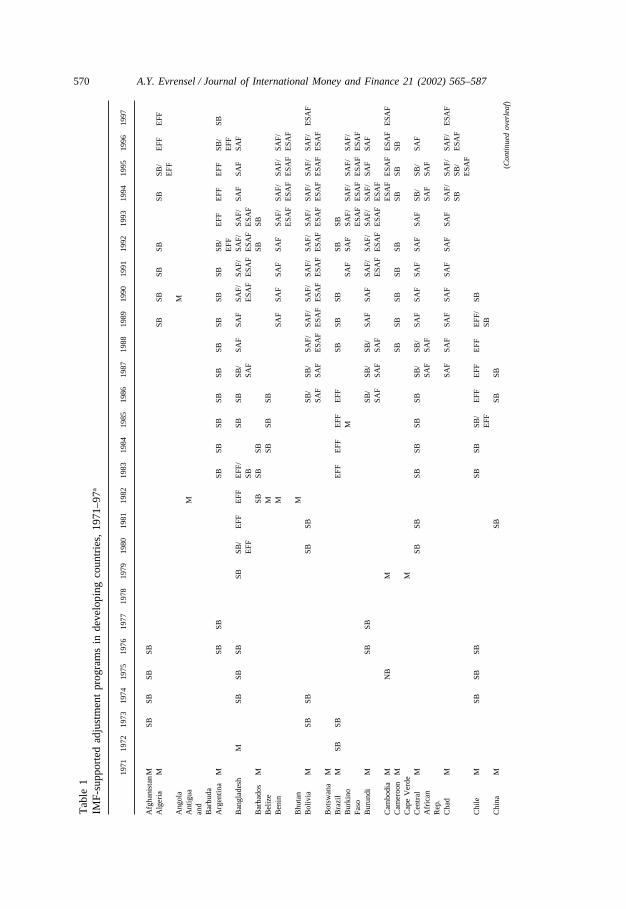

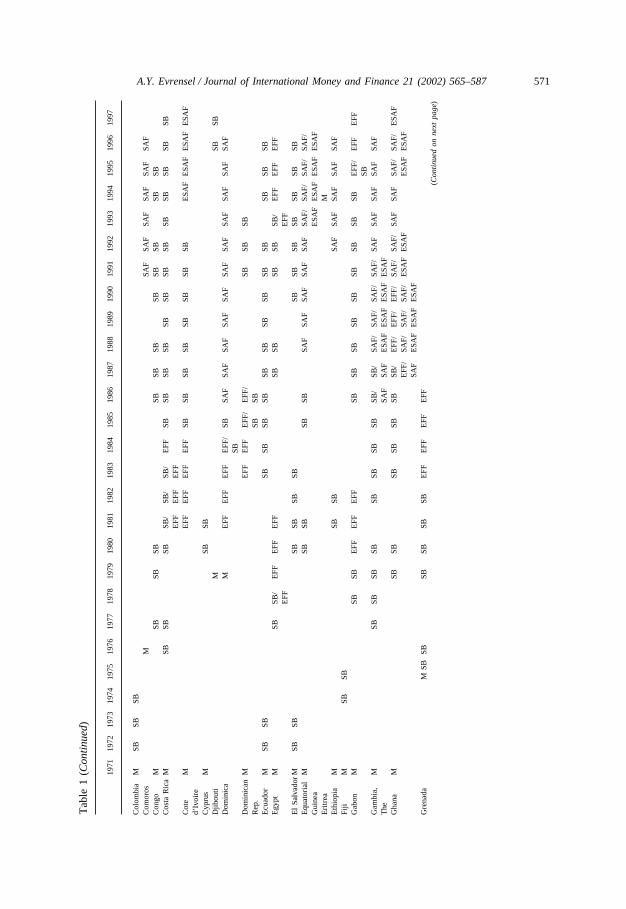

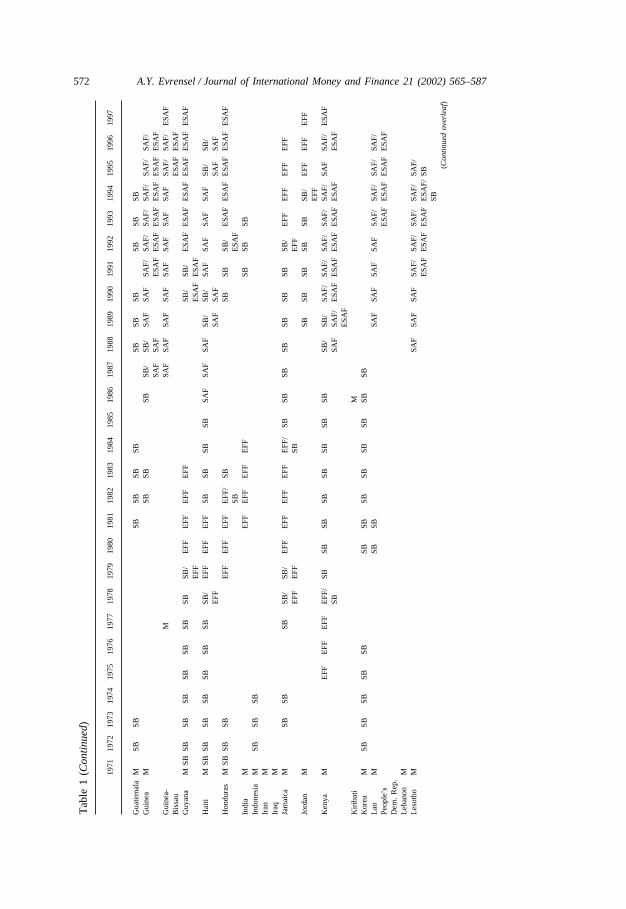

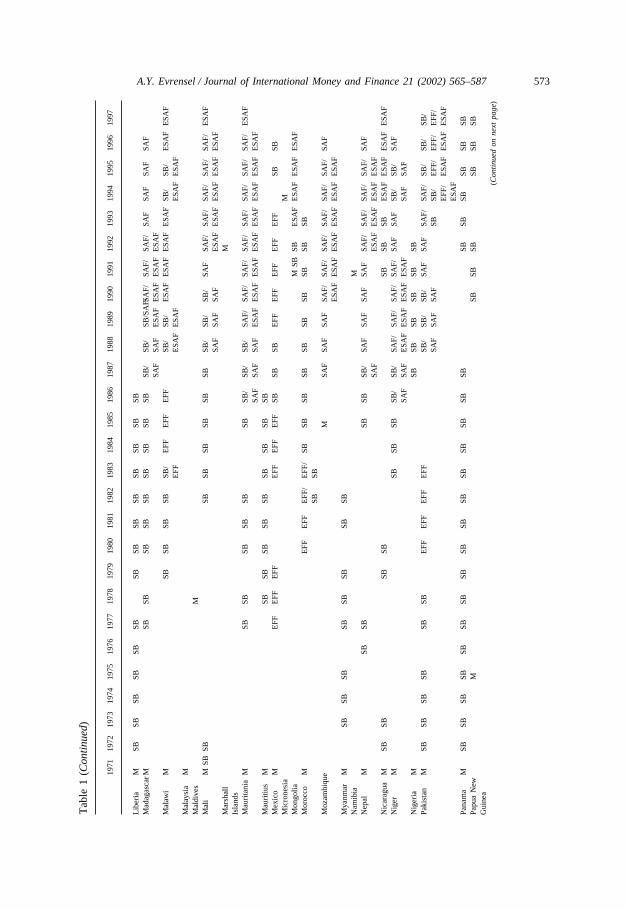

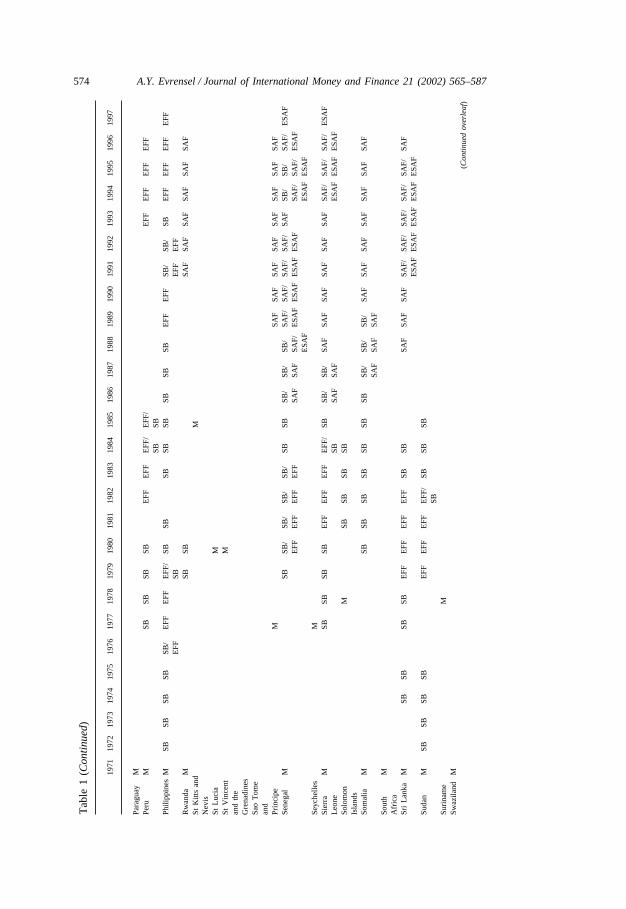

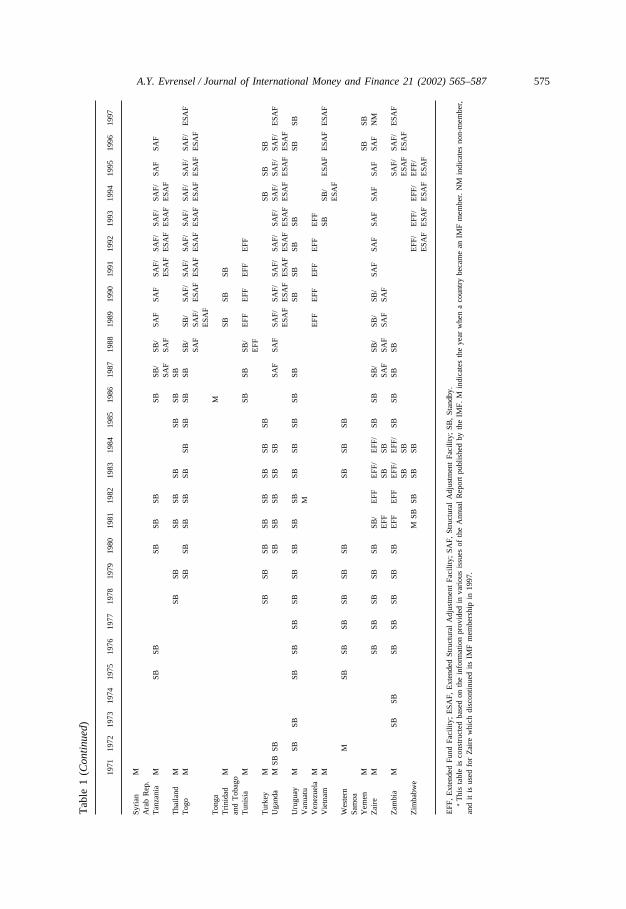

3.1. Participation in IMF programs, 1971–978

In 1997, 181 out of 191 independent countries in the world were IMF-members.9

Table 1 contains 118 developing members of the IMF during the period 1971–97,and the types of adjustment programs they have received.10 During the sample period,91 countries received any of the four structural adjustment programs: standby,Extended Fund Facility (EFF), Structural Adjustment Facility (SAF), and EnhancedStructural Adjustment Facility (ESAF).11 Table 1 indicates an increase in the fre-quency of IMF-supported stabilization programs since the mid-1980s, which can beexplained by the introduction of SAF and ESAF in 1986 and 1987, respectively.Prior to the mid-1980s, only standby and EFF agreements were available. With theintroduction of SAF and ESAF, most low-income developing countries have receiveddifferent types of programs simultaneously.12

A summary of Table 1 in the form of chi-squared tables indicates that, during theperiod 1971–97, the probability of any developing IMF member receiving a structural

8 The choice of the period rests on the availability of data. Data on macroeconomic variables areobtained from the IMF’s International Financial Statistics of March 1997 on CD-ROM. Informationregarding the type of programs comes from Annual Reports of the IMF for the years 1971 through 1997.

9 Nonmembers of the IMF include micro-states in Europe (Andorra, Liechtenstein, Vatican City, andMonaco), the Pacific (Tuvalu, Palau, and Nauru), Zaire, Cuba, and Taiwan. The remaining 63 nonde-veloping members of the IMF include the former Soviet Union and the countries of Europe, EasternEurope, North America, the Pacific, and the Middle East (oil exporters). Twenty-seven developing mem-bers of the IMF have never received stabilization programs and constitute the so-called nonprogramIMF members.

10 In Table 1, the duration of each program is not marked to keep the table simple, which means thattabulated standby, EFF, SAF, and ESAF arrangements correspond to different arrangements that last twoto four years. Typically, there is a relatively short period between successive programs that extends froma couple of weeks to a couple of months.

11 While standby arrangements provide balance of payments support to middle- and high-incomedeveloping countries, EFF, SAF, and ESAF are designed for low-income developing countries. Standbysare provided for a year with a possible extension up to three years. Other programs last longer and implylonger periods of repayment (5–10 years). See Johnson (1993), Guitian (1995), and Schadler et al. (1995)for more information on these programs.

12 During the pre-1986 period, some countries received standby and EFF simultaneously. During theperiod 1986–97, the combination was changed to SAF and ESAF, and was primarily given to low-income countries.

578 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

adjustment program is 0.3242.13 If 1986 is taken as a benchmark to divide the periodin two sections, it becomes apparent that the probability of being in a program ishigher during the period 1986–97. While the probability of receiving any programis 0.2192 for the pre-1986 period, it increases to 0.5054 during the period 1986–97.For low-income countries, the likelihood of being in a program increased from 0.216to 0.6235 between the two periods. Similarly, middle-income countries were twiceas likely to be in a program during the period 1986–97 (0.432) than during the pre-1986 period (0.2177).

Although the Fund’s Articles of Agreement state the temporary nature of theFund’s financial support, the data on program status indicate that many programcountries have been under the IMF’s care almost continuously. This raises the ques-tion as to why most of the program countries are repeat offenders, i.e., they keepgetting into balance of payments problems and receiving financial support from theIMF. Provided that conditionality contains the correct description of and solution tobalance of payments problems of program countries, and that conditionality is fullyimplemented during the program period and sustained by program countries’ govern-ments during the post-program periods, it is plausible that continuing IMF supportshould be rare or nonexistent. In the following, using the before–after and temporalinterprogram analysis, the revolving nature of program participation is explained.

3.2. Before–after analysis

The almost continuous nature of Fund-supported programs creates a problem forthe comparison of pre-program, program, and post-program years in terms of relevantvariables. For the majority of low-income countries in the sample, as one programends, another one starts in the same year. Additionally, since the mid-1980s mostprogram countries have been involved in more than one program in a given year,which makes pre-program, program, and post-program comparisons noisy. If onlyone type of program is considered, the before–after comparison may be affected byanother type of IMF-program. If all programs are considered, a possible differenceamong programs may be overlooked. To reduce the noise, mean values of the evalu-ation variables in different periods are compared not only for all programs but alsofor different program types (standby, EFF, SAF, and ESAF). Since program typesand income levels of program countries are closely related, by considering thebehavior of evaluation variables for all programs and under different programs, someof the noise associated with the aggregation of the Fund-effect under different (andsometimes overlapping) programs may be reduced.

13 Chi-squared tables are constructed using program types and income levels of countries. Income cate-gories are defined based on the following levels of 1995 GDP per capita (Y): low-income country ifY�US$1500; middle-income country if Y�US$6000; high-income country if Y�US$6000. The Pearsonc2 test on the independence of rows and columns indicates that program types and income levels are notindependent, which is consistent with the IMF’s attempt to provide different programs to countries withdifferent income levels.

579A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

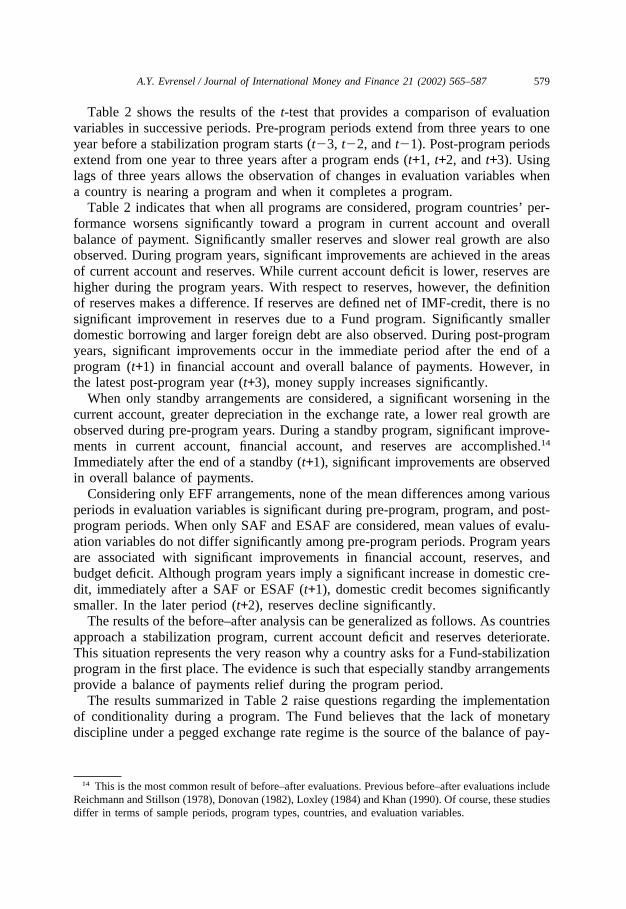

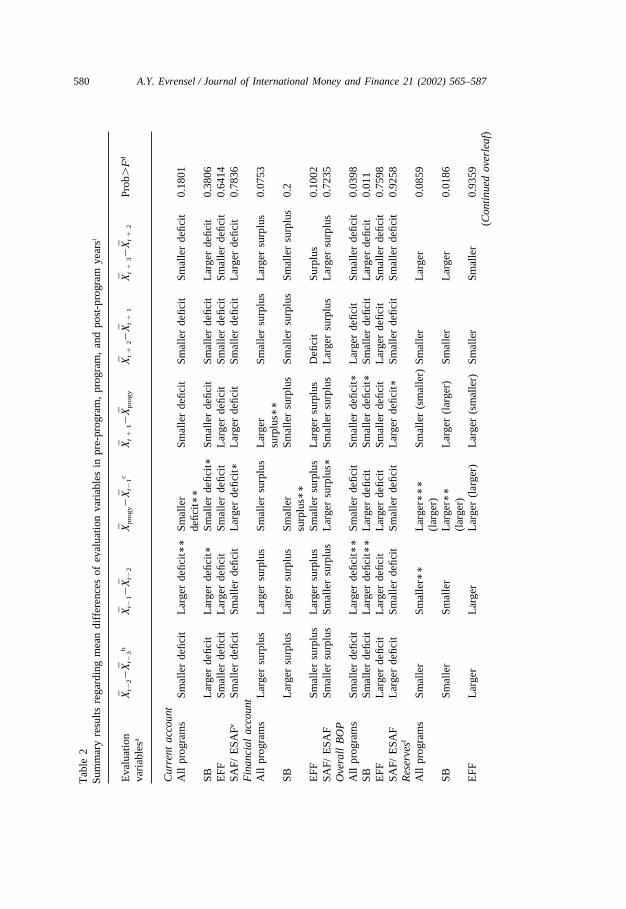

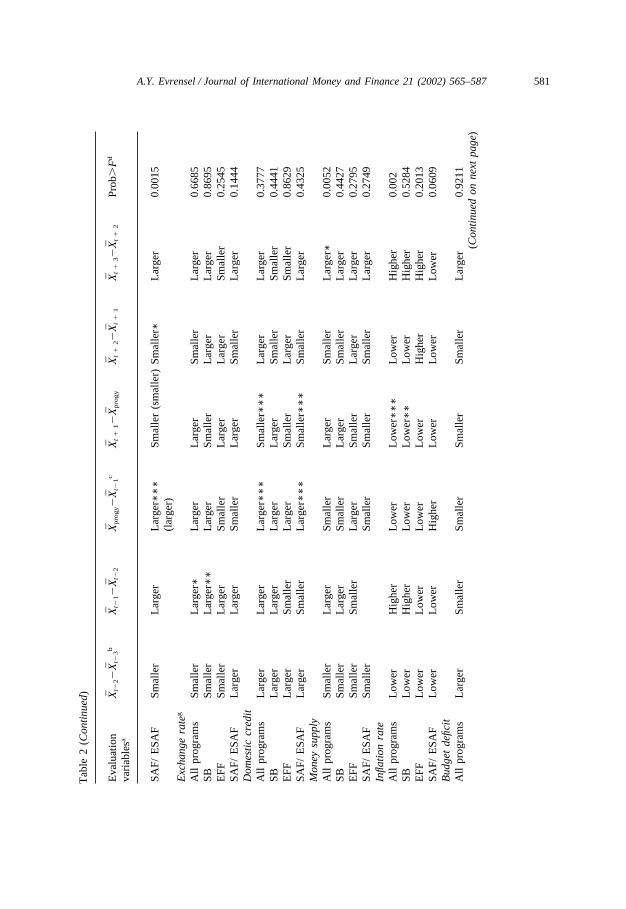

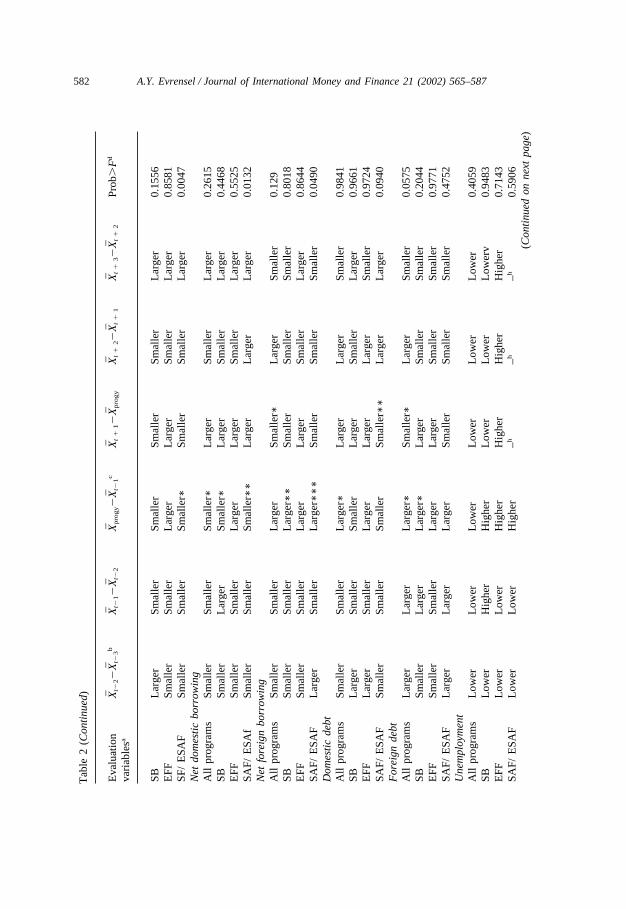

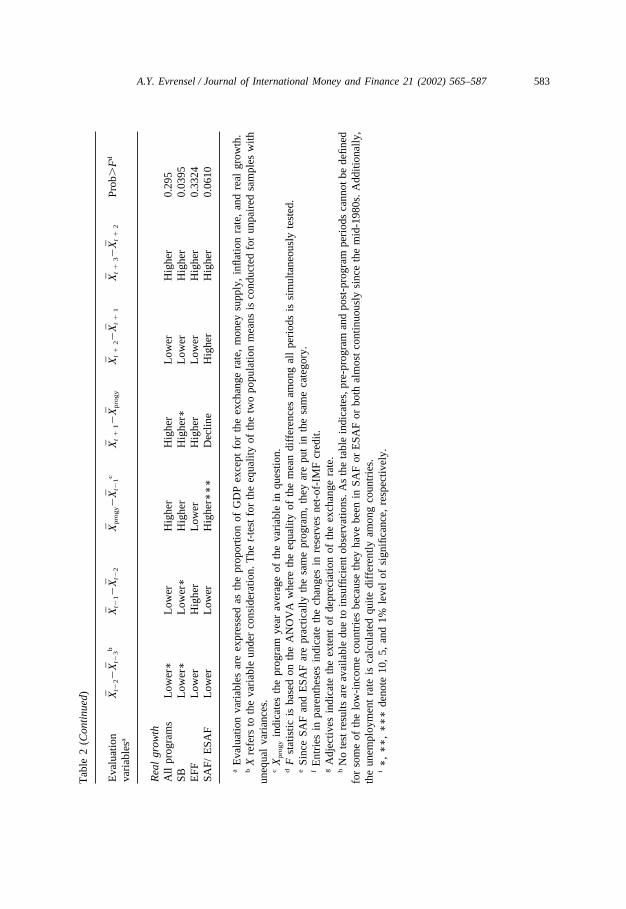

Table 2 shows the results of the t-test that provides a comparison of evaluationvariables in successive periods. Pre-program periods extend from three years to oneyear before a stabilization program starts (t�3, t�2, and t�1). Post-program periodsextend from one year to three years after a program ends (t+1, t+2, and t+3). Usinglags of three years allows the observation of changes in evaluation variables whena country is nearing a program and when it completes a program.

Table 2 indicates that when all programs are considered, program countries’ per-formance worsens significantly toward a program in current account and overallbalance of payment. Significantly smaller reserves and slower real growth are alsoobserved. During program years, significant improvements are achieved in the areasof current account and reserves. While current account deficit is lower, reserves arehigher during the program years. With respect to reserves, however, the definitionof reserves makes a difference. If reserves are defined net of IMF-credit, there is nosignificant improvement in reserves due to a Fund program. Significantly smallerdomestic borrowing and larger foreign debt are also observed. During post-programyears, significant improvements occur in the immediate period after the end of aprogram (t+1) in financial account and overall balance of payments. However, inthe latest post-program year (t+3), money supply increases significantly.

When only standby arrangements are considered, a significant worsening in thecurrent account, greater depreciation in the exchange rate, a lower real growth areobserved during pre-program years. During a standby program, significant improve-ments in current account, financial account, and reserves are accomplished.14

Immediately after the end of a standby (t+1), significant improvements are observedin overall balance of payments.

Considering only EFF arrangements, none of the mean differences among variousperiods in evaluation variables is significant during pre-program, program, and post-program periods. When only SAF and ESAF are considered, mean values of evalu-ation variables do not differ significantly among pre-program periods. Program yearsare associated with significant improvements in financial account, reserves, andbudget deficit. Although program years imply a significant increase in domestic cre-dit, immediately after a SAF or ESAF (t+1), domestic credit becomes significantlysmaller. In the later period (t+2), reserves decline significantly.

The results of the before–after analysis can be generalized as follows. As countriesapproach a stabilization program, current account deficit and reserves deteriorate.This situation represents the very reason why a country asks for a Fund-stabilizationprogram in the first place. The evidence is such that especially standby arrangementsprovide a balance of payments relief during the program period.

The results summarized in Table 2 raise questions regarding the implementationof conditionality during a program. The Fund believes that the lack of monetarydiscipline under a pegged exchange rate regime is the source of the balance of pay-

14 This is the most common result of before–after evaluations. Previous before–after evaluations includeReichmann and Stillson (1978), Donovan (1982), Loxley (1984) and Khan (1990). Of course, these studiesdiffer in terms of sample periods, program types, countries, and evaluation variables.

580 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587T

able

2Su

mm

ary

resu

ltsre

gard

ing

mea

ndi

ffer

ence

sof

eval

uatio

nva

riab

les

inpr

e-pr

ogra

m,

prog

ram

,an

dpo

st-p

rogr

amye

arsi

Eva

luat

ion

Xt�

2�

Xt�

3b

Xt�

1�

Xt�

2X

pro

gy�

Xt�

1c

Xt

�1�

Xpro

gy

Xt

�2�

Xt

�1

Xt

�3�

Xt

�2

Prob

�F

d

vari

able

sa

Cur

rent

acco

unt

All

prog

ram

sSm

alle

rde

ficit

Lar

ger

defic

it∗∗

Smal

ler

Smal

ler

defic

itSm

alle

rde

ficit

Smal

ler

defic

it0.

1801

defic

it∗∗

SBL

arge

rde

ficit

Lar

ger

defic

it∗Sm

alle

rde

ficit∗

Smal

ler

defic

itSm

alle

rde

ficit

Lar

ger

defic

it0.

3806

EFF

Smal

ler

defic

itL

arge

rde

ficit

Smal

ler

defic

itL

arge

rde

ficit

Smal

ler

defic

itSm

alle

rde

ficit

0.64

14SA

F/E

SAFe

Smal

ler

defic

itSm

alle

rde

ficit

Lar

ger

defic

it∗L

arge

rde

ficit

Smal

ler

defic

itL

arge

rde

ficit

0.78

36F

inan

cial

acco

unt

All

prog

ram

sL

arge

rsu

rplu

sL

arge

rsu

rplu

sSm

alle

rsu

rplu

sL

arge

rSm

alle

rsu

rplu

sL

arge

rsu

rplu

s0.

0753

surp

lus∗

∗SB

Lar

ger

surp

lus

Lar

ger

surp

lus

Smal

ler

Smal

ler

surp

lus

Smal

ler

surp

lus

Smal

ler

surp

lus

0.2

surp

lus∗

∗E

FFSm

alle

rsu

rplu

sL

arge

rsu

rplu

sSm

alle

rsu

rplu

sL

arge

rsu

rplu

sD

efici

tSu

rplu

s0.

1002

SAF/

ESA

FSm

alle

rsu

rplu

sSm

alle

rsu

rplu

sL

arge

rsu

rplu

s∗Sm

alle

rsu

rplu

sL

arge

rsu

rplu

sL

arge

rsu

rplu

s0.

7235

Ove

rall

BO

PA

llpr

ogra

ms

Smal

ler

defic

itL

arge

rde

ficit∗

∗Sm

alle

rde

ficit

Smal

ler

defic

it∗L

arge

rde

ficit

Smal

ler

defic

it0.

0398

SBSm

alle

rde

ficit

Lar

ger

defic

it∗∗

Lar

ger

defic

itSm

alle

rde

ficit∗

Smal

ler

defic

itL

arge

rde

ficit

0.01

1E

FFL

arge

rde

ficit

Lar

ger

defic

itL

arge

rde

ficit

Smal

ler

defic

itL

arge

rde

ficit

Smal

ler

defic

it0.

7598

SAF/

ESA

FL

arge

rde

ficit

Smal

ler

defic

itSm

alle

rde

ficit

Lar

ger

defic

it∗Sm

alle

rde

ficit

Smal

ler

defic

it0.

9258

Res

erve

sf

All

prog

ram

sSm

alle

rSm

alle

r∗∗

Lar

ger∗

∗∗Sm

alle

r(s

mal

ler)

Smal

ler

Lar

ger

0.08

59(l

arge

r)SB

Smal

ler

Smal

ler

Lar

ger∗

∗L

arge

r(l

arge

r)Sm

alle

rL

arge

r0.

0186

(lar

ger)

EFF

Lar

ger

Lar

ger

Lar

ger

(lar

ger)

Lar

ger

(sm

alle

r)Sm

alle

rSm

alle

r0.

9359

(Con

tinu

edov

erle

af)

581A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587T

able

2(C

onti

nued

)

Eva

luat

ion

Xt�

2�

Xt�

3b

Xt�

1�

Xt�

2X

pro

gy�

Xt�

1c

Xt

�1�

Xpro

gy

Xt

�2�

Xt

�1

Xt

�3�

Xt

�2

Prob

�F

d

vari

able

sa

SAF/

ESA

FSm

alle

rL

arge

rL

arge

r∗∗∗

Smal

ler

(sm

alle

r)Sm

alle

r∗L

arge

r0.

0015

(lar

ger)

Exc

hang

era

teg

All

prog

ram

sSm

alle

rL

arge

r∗L

arge

rL

arge

rSm

alle

rL

arge

r0.

6685

SBSm

alle

rL

arge

r∗∗

Lar

ger

Smal

ler

Lar

ger

Lar

ger

0.86

95E

FFSm

alle

rL

arge

rSm

alle

rL

arge

rL

arge

rSm

alle

r0.

2545

SAF/

ESA

FL

arge

rL

arge

rSm

alle

rL

arge

rSm

alle

rL

arge

r0.

1444

Dom

esti

ccr

edit

All

prog

ram

sL

arge

rL

arge

rL

arge

r∗∗∗

Smal

ler∗

∗∗L

arge

rL

arge

r0.

3777

SBL

arge

rL

arge

rL

arge

rL

arge

rSm

alle

rSm

alle

r0.

4441

EFF

Lar

ger

Smal

ler

Lar

ger

Smal

ler

Lar

ger

Smal

ler

0.86

29SA

F/E

SAF

Lar

ger

Smal

ler

Lar

ger∗

∗∗Sm

alle

r∗∗∗

Smal

ler

Lar

ger

0.43

25M

oney

supp

lyA

llpr

ogra

ms

Smal

ler

Lar

ger

Smal

ler

Lar

ger

Smal

ler

Lar

ger∗

0.00

52SB

Smal

ler

Lar

ger

Smal

ler

Lar

ger

Smal

ler

Lar

ger

0.44

27E

FFSm

alle

rSm

alle

rL

arge

rSm

alle

rL

arge

rL

arge

r0.

2795

SAF/

ESA

FSm

alle

rSm

alle

rSm

alle

rSm

alle

rL

arge

r0.

2749

Infla

tion

rate

All

prog

ram

sL

ower

Hig

her

Low

erL

ower

∗∗∗

Low

erH

ighe

r0.

002

SBL

ower

Hig

her

Low

erL

ower

∗∗L

ower

Hig

her

0.52

84E

FFL

ower

Low

erL

ower

Low

erH

ighe

rH

ighe

r0.

2013

SAF/

ESA

FL

ower

Low

erH

ighe

rL

ower

Low

erL

ower

0.06

09B

udge

tde

ficit

All

prog

ram

sL

arge

rSm

alle

rSm

alle

rSm

alle

rSm

alle

rL

arge

r0.

9211

(Con

tinu

edon

next

page

)

582 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587T

able

2(C

onti

nued

)

Eva

luat

ion

Xt�

2�

Xt�

3b

Xt�

1�

Xt�

2X

pro

gy�

Xt�

1c

Xt

�1�

Xpro

gy

Xt

�2�

Xt

�1

Xt

�3�

Xt

�2

Prob

�F

d

vari

able

sa

SBL

arge

rSm

alle

rSm

alle

rSm

alle

rSm

alle

rL

arge

r0.

1556

EFF

Smal

ler

Smal

ler

Lar

ger

Lar

ger

Smal

ler

Lar

ger

0.85

81SF

/E

SAF

Smal

ler

Smal

ler

Smal

ler∗

Smal

ler

Smal

ler

Lar

ger

0.00

47N

etdo

mes

tic

borr

owin

gA

llpr

ogra

ms

Smal

ler

Smal

ler

Smal

ler∗

Lar

ger

Smal

ler

Lar

ger

0.26

15SB

Smal

ler

Lar

ger

Smal

ler∗

Lar

ger

Smal

ler

Lar

ger

0.44

68E

FFSm

alle

rSm

alle

rL

arge

rL

arge

rSm

alle

rL

arge

r0.

5525

SAF/

ESA

fSm

alle

rSm

alle

rSm

alle

r∗∗

Lar

ger

Lar

ger

Lar

ger

0.01

32N

etfo

reig

nbo

rrow

ing

All

prog

ram

sSm

alle

rSm

alle

rL

arge

rSm

alle

r∗L

arge

rSm

alle

r0.

129

SBSm

alle

rSm

alle

rL

arge

r∗∗

Smal

ler

Smal

ler

Smal

ler

0.80

18E

FFSm

alle

rSm

alle

rL

arge

rL

arge

rSm

alle

rL

arge

r0.

8644

SAF/

ESA

FL

arge

rSm

alle

rL

arge

r∗∗∗

Smal

ler

Smal

ler

Smal

ler

0.04

90D

omes

tic

debt

All

prog

ram

sSm

alle

rSm

alle

rL

arge

r∗L

arge

rL

arge

rSm

alle

r0.

9841

SBL

arge

rSm

alle

rSm

alle

rL

arge

rSm

alle

rL

arge

r0.

9661

EFF

Lar

ger

Smal

ler

Lar

ger

Lar

ger

Lar

ger

Smal

ler

0.97

24SA

F/E

SAF

Smal

ler

Smal

ler

Smal

ler

Smal

ler∗

∗L

arge

rL

arge

r0.

0940

For

eign

debt

All

prog

ram

sL

arge

rL

arge

rL

arge

r∗Sm

alle

r∗L

arge

rSm

alle

r0.

0575

SBSm

alle

rL

arge

rL

arge

r∗L

arge

rSm

alle

rSm

alle

r0.

2044

EFF

Smal

ler

Smal

ler

Lar

ger

Lar

ger

Smal

ler

Smal

ler

0.97

71SA

F/E

SAF

Lar

ger

Lar

ger

Lar

ger

Smal

ler

Smal

ler

Smal

ler

0.47

52U

nem

ploy

men

tA

llpr

ogra

ms

Low

erL

ower

Low

erL

ower

Low

erL

ower

0.40

59SB

Low

erH

ighe

rH

ighe

rL

ower

Low

erL

ower

v0.

9483

EFF

Low

erL

ower

Hig

her

Hig

her

Hig

her

Hig

her

0.71

43SA

F/E

SAF

Low

erL

ower

Hig

her

–h–h

–h0.

5906

(Con

tinu

edon

next

page

)

583A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587T

able

2(C

onti

nued

)

Eva

luat

ion

Xt�

2�

Xt�

3b

Xt�

1�

Xt�

2X

pro

gy�

Xt�

1c

Xt

�1�

Xpro

gy

Xt

�2�

Xt

�1

Xt

�3�

Xt

�2

Prob

�F

d

vari

able

sa

Rea

lgr

owth

All

prog

ram

sL

ower

∗L

ower

Hig

her

Hig

her

Low

erH

ighe

r0.

295

SBL

ower

∗L

ower

∗H

ighe

rH

ighe

r∗L

ower

Hig

her

0.03

95E

FFL

ower

Hig

her

Low

erH

ighe

rL

ower

Hig

her

0.33

24SA

F/E

SAF

Low

erL

ower

Hig

her∗

∗∗D

eclin

eH

ighe

rH

ighe

r0.

0610

aE

valu

atio

nva

riab

les

are

expr

esse

das

the

prop

ortio

nof

GD

Pex

cept

for

the

exch

ange

rate

,m

oney

supp

ly,

infla

tion

rate

,an

dre

algr

owth

.b

Xre

fers

toth

eva

riab

leun

der

cons

ider

atio

n.T

het-

test

for

the

equa

lity

ofth

etw

opo

pula

tion

mea

nsis

cond

ucte

dfo

run

pair

edsa

mpl

esw

ithun

equa

lva

rian

ces.

cX

pro

gy

indi

cate

sth

epr

ogra

mye

arav

erag

eof

the

vari

able

inqu

estio

n.d

Fst

atis

ticis

base

don

the

AN

OV

Aw

here

the

equa

lity

ofth

em

ean

diff

eren

ces

amon

gal

lpe

riod

sis

sim

ulta

neou

sly

test

ed.

eSi

nce

SAF

and

ESA

Far

epr

actic

ally

the

sam

epr

ogra

m,

they

are

put

inth

esa

me

cate

gory

.f

Ent

ries

inpa

rent

hese

sin

dica

teth

ech

ange

sin

rese

rves

net-

of-I

MF

cred

it.g

Adj

ectiv

esin

dica

teth

eex

tent

ofde

prec

iatio

nof

the

exch

ange

rate

.h

No

test

resu

ltsar

eav

aila

ble

due

toin

suffi

cien

tob

serv

atio

ns.A

sth

eta

ble

indi

cate

s,pr

e-pr

ogra

man

dpo

st-p

rogr

ampe

riod

sca

nnot

bede

fined

for

som

eof

the

low

-inc

ome

coun

trie

sbe

caus

eth

eyha

vebe

enin

SAF

orE

SAF

orbo

thal

mos

tco

ntin

uous

lysi

nce

the

mid

-198

0s.

Add

ition

ally

,th

eun

empl

oym

ent

rate

isca

lcul

ated

quite

diff

eren

tlyam

ong

coun

trie

s.i∗,

∗∗,

∗∗∗

deno

te10

,5,

and

1%le

vel

ofsi

gnifi

canc

e,re

spec

tivel

y.

584 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

ments problems. Consequently, the conditionality attached to stabilization programsadvises a reduction in the size of the public sector and money creation along withthe depreciation of the currency. At least during the program years, one would expecta significantly lower budget deficit, domestic creation, money supply, domestic bor-rowing, and inflation rate. However, these primary targets of stabilization programsare not significantly affected during the program period. When looking at the post-program performance of program countries, the improvements in balance of pay-ments and reserves achieved during an IMF program disappear. This raises questionswith respect to the sustainability of the balance of payments improvement in thepost-program period.

The results of the before–after analysis should be considered in connection withTable 1, which indicates an almost continuous IMF-support in program countries.The revolving nature of the IMF support may be due to the short-term nature of itseffects. The results indicate that the Fund provides program countries with hardcurrency, and eliminates the balance of payments crisis during the program period.However, in the absence of long-term incentives, the short-term improvement inbalance of payments does not last, and it is even reversed once the program is over.15

3.3. Temporal interprogram analysis

The issue of moral hazard regarding Fund-supported programs implies the possi-bility that the governments of program countries may adopt unsustainable macroe-conomic policies due to the availability of the Fund credit. If stabilization programscreated moral hazard, this would be inconsistent with the effectiveness of stabiliz-ation programs. Moreover, one would expect that the interprogram periods wouldbe associated with increasingly unsustainable macroeconomic policies as the numberof programs a country receives increases.16 If a country has had Fund support before,the cost of macroeconomic policies that lead to the depletion of international reservesmay be lower to the country.

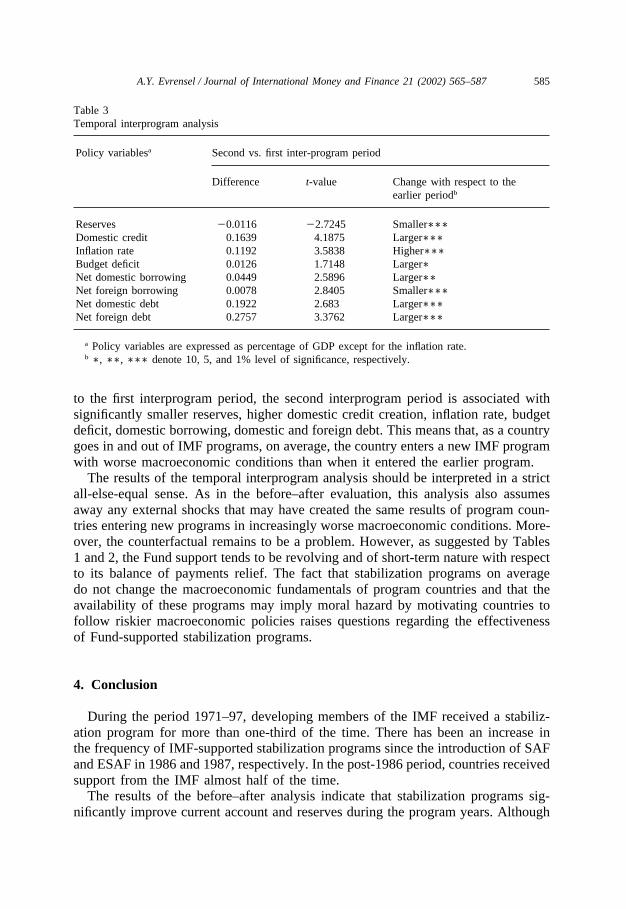

The identification of interprogram periods is based on Table 1. The identificationprocess is quite problematic, because the continuous nature of the Fund makes itdifficult to identify two interprogram periods. It turns out that there are only 42countries for which two interprogram periods can be identified during the period1971–97.17 Table 3 shows the results of the temporal interprogram analysis. Theresults suggest that the second interprogram period is associated with significantlyworsening macroeconomic performance than the first interprogram period. Compared

15 This point that the short-run nature of program effects is responsible for the ineffectiveness of IMFprograms is also suggested by Edwards (1989).

16 Interprogram periods are defined as periods that are not associated with any of the four IMF programsand are located between two program periods.

17 It is important to realize that the temporal interprogram analysis requires the actual data. As discussedearlier, the use of the actual data in program evaluations is problematic, because the actual data incorporateprogram countries’ expectations regarding the availability of Fund programs. However, the actual dataare exactly what is needed here.

585A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

Table 3Temporal interprogram analysis

Policy variablesa Second vs. first inter-program period

Difference t-value Change with respect to theearlier periodb

Reserves �0.0116 �2.7245 Smaller∗∗∗Domestic credit 0.1639 4.1875 Larger∗∗∗Inflation rate 0.1192 3.5838 Higher∗∗∗Budget deficit 0.0126 1.7148 Larger∗Net domestic borrowing 0.0449 2.5896 Larger∗∗Net foreign borrowing 0.0078 2.8405 Smaller∗∗∗Net domestic debt 0.1922 2.683 Larger∗∗∗Net foreign debt 0.2757 3.3762 Larger∗∗∗

a Policy variables are expressed as percentage of GDP except for the inflation rate.b ∗, ∗∗, ∗∗∗ denote 10, 5, and 1% level of significance, respectively.

to the first interprogram period, the second interprogram period is associated withsignificantly smaller reserves, higher domestic credit creation, inflation rate, budgetdeficit, domestic borrowing, domestic and foreign debt. This means that, as a countrygoes in and out of IMF programs, on average, the country enters a new IMF programwith worse macroeconomic conditions than when it entered the earlier program.

The results of the temporal interprogram analysis should be interpreted in a strictall-else-equal sense. As in the before–after evaluation, this analysis also assumesaway any external shocks that may have created the same results of program coun-tries entering new programs in increasingly worse macroeconomic conditions. More-over, the counterfactual remains to be a problem. However, as suggested by Tables1 and 2, the Fund support tends to be revolving and of short-term nature with respectto its balance of payments relief. The fact that stabilization programs on averagedo not change the macroeconomic fundamentals of program countries and that theavailability of these programs may imply moral hazard by motivating countries tofollow riskier macroeconomic policies raises questions regarding the effectivenessof Fund-supported stabilization programs.

4. Conclusion

During the period 1971–97, developing members of the IMF received a stabiliz-ation program for more than one-third of the time. There has been an increase inthe frequency of IMF-supported stabilization programs since the introduction of SAFand ESAF in 1986 and 1987, respectively. In the post-1986 period, countries receivedsupport from the IMF almost half of the time.

The results of the before–after analysis indicate that stabilization programs sig-nificantly improve current account and reserves during the program years. Although

586 A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

stabilization programs seem to provide short-term balance of payments relief, theseimprovements are not sustained during the post-program period. Additionally, con-ditionality may not be effectively imposed even during the program years. Althoughconditionality prescribes a reduction in the size of the public sector, variables suchas domestic credit creation and budget deficit are not significantly affected by con-ditionality during the program years.

The results of the temporal interprogram analysis suggest that, on average, pro-gram countries enter a new program in a worse macroeconomic situation than before.Considering the revolving nature of the Fund support, this result is inconsistent withthe effectiveness of stabilization programs and may be interpreted as a signal ofmoral hazard.

The currency crises of the last few years have intensified discussions regardingthe role of the IMF in the international financial system where the emphasis hasbeen on the future role of the Fund. More recently, some would like to give the IMFthe responsibility of becoming the international lender of the last resort. Suggestionsregarding the Fund’s future will be misguided if its past performance is ignored.

Acknowledgements

I am grateful to Gerald P. Dwyer Jr for his comments on the paper. Commentsreceived from S. Nuri Erbas, David B. Gordon, Erdogan Kumcu, James R. Lothian,Gary Santoni, Myles Wallace, John T. Warner, Thomas D. Willett, and two anony-mous referees are also greatly appreciated. All errors are mine.

References

Conway, P., 1994. IMF lending programs: participation and impact. Journal of Development Economics45, 365–391.

Donovan, D., 1982. Macroeconomic performance and adjustment under Fund-supported programs: theexperience of the seventies. IMF Staff Papers 29 (June), 171–203.

Doroodian, K., 1993. Macroeconomic performance and adjustment under policies commonly supportedby the IMF. Economic Development and Cultural Change 41 (4), 849–864.

Edwards, S., 1989. The International Monetary Fund and the developing countries: a critical evaluation.In: Brunner, K., Meltzer, A.H. (Eds.), IMF Policy Advice, Market Volatility, Commodity Price Rules,and Other Essays. Carnegie-Rochester Conference Series on Public Policy 31, pp. 7–68.

Fischer, S., 1999. On the need for an international lender of last resort. Presented at the joint luncheonof the American Economic Association and the American Finance Association in New York on 3January 1999. IMF website, speeches.

Goldstein, M., Montiel, P., 1986. Evaluating Fund stabilization programs with multicountry data: somemethodological pitfalls. IMF Staff Papers 33 (June), 304–344.

Guitian, M., 1995. Conditionality: past, present, future. IMF Staff Papers 42 (December), 792–835.IMF, various years. Annual Report. The International Monetary Fund, Washington, DC.Johnson, M.E., 1993. The International Monetary Fund, 1944-1989. A Research Guide. Garland Pub-

lishing Inc.Joyce, J.P., 1992. The economic characteristics of IMF program countries. Economics Letters 38, 237–

242.

587A.Y. Evrensel / Journal of International Money and Finance 21 (2002) 565–587

Khan, M.S., Knight, M., 1981. Stabilization programs in developing countries: a formal framework. IMFStaff Papers 28 (March), 1–53.

Khan, M.S., 1990. The macroeconomic effects of Fund-supported adjustment programs. IMF Staff Papers37 (June), 195–231.

Killick, T., 1995. IMF Programmes in Developing Countries: Design and Impact. Routledge, London.Knight, M., Santaella, J.A., 1997. Economic determinants of IMF financial arrangements. Journal of

Development Economics 54, 405–436.Krueger, A.O., 1998. Whither the World Bank and the IMF? Journal of Economic Literature 36 (4),

1983–2020.Loxley, J., 1984. The IMF and the Poorest Countries: The Performance of the Least Developed Countries

under IMF Stand-By Arrangements. The North–South Institute, Ottawa.Reichmann, T.M., Stillson, R.T., 1978. Experience with programs of balance of payments adjustment:

stand-by arrangements in the higher tranches, 1963–72. IMF Staff Papers 25 (June), 293–309.Santaella, J.A., 1996. Stylized facts before IMF-supported macroeconomic adjustment. IMF Staff Papers

43 (September), 502–544.Schadler, S., Bennett, A., Carkovic, M., Dicks-Mireaux, L., Mecagni, M., Morsink, J.H.J., Savastano,

M.A., 1995. IMF conditionality: experience under stand-by and extended arrangements. Occasionalpaper (128). The International Monetary Fund, Washington, DC.

Ul Haque, N., Khan, M.S., 1998. Do IMF-supported programs work? A survey of the cross-countryempirical evidence. Working paper (169). The International Monetary Fund, Washington, DC.