effective tax structures for acquisitions in indonesia ... · 3. treaty shopping: the corporation...

TRANSCRIPT

Effective Tax Structures for Acquisitions in Indonesia, Indochina and Myanmar

2

At a Glance

Southeast Asia’s first full service international law firm with a major specialization in taxation

Our Vision

We sell results, not time.

We believe that you don’t want our time.

We believe you want results.

That’s our value. That’s how we bill.

Our Commitment

More than 50

professional staff

Laos

Cambodia

Singapore

Vietnam

Indonesia

6 countries

Myanmar

3

Our Practice Areas

Tax Advisory

Corporate tax planning strategies

Tax-efficient market entry advisory services

Real estate tax structuring

Oil, gas and mining tax services

Customs and excise advisory

Mergers & acquisitions and tax due diligence

International and regional tax optimization

Transfer pricing advisory and benchmarking

Taxation of banks, insurance & financial services

Controversy and litigation in tax matters

Government Relations

In a region where regulations and legal precedents are

not always clear, local knowledge and relationships are

the key to getting results. Our advisers’ excellent and

long-standing working relationships with government

authorities throughout the region enable us to advise

you on relationships with government agencies and

provide strategic guidance on maneuvering the

intricacies of a country’s regulatory and legislative

framework.

Legal Advisory

Mergers & acquisitions (cross-border and single market)

Real estate projects (including legal structuring)

Corporate & commercial law

Investment licensing and market entry

Capital markets

Compliance (including FCPA and regulatory

compliance)

Trade (treaty analysis and anti-dumping)

Infrastructure, mining and energy (including project

financing)

Intellectual property

Corporate Advisory

Expatriate employee tax services

Payroll administration

Corporate tax compliance

Accounting services

4

Overview of taxes across the region

Indonesia – Tax rates, holding structures

General due diligence issues that can kill a deal

Myanmar – Due diligence concerns, acquisition structures

Vietnam – Deal structuring

Trapped cash

Cambodia – Buyout structure example and tax concerns

Laos – Exit structure

Contents

5

Key Tax Rates Laos

Dividends 10%

Gains on shares: 10%

Interest 10%

Fees

5.6% (effective rate)

Vietnam

Dividends 0%

Gains on shares: 25%

Interest 5% CIT*

Fees 5% + 5%

Cambodia

Dividends 14% Gains on shares: Not always subject to tax for non-residents

Interest 14%

Fees 14%

Myanmar

Dividends 0% Gains on shares (non-resident): 40% (non- oil & gas); 40-50% (oil & gas)

Interest 15%

Fees 3.5%

Singapore

Dividends 0% Gains on shares: 0%

Interest 15%

Fees 17%

Indonesia

Dividends 20% Gains on shares: 5% effective rate

Interest 20%

Fees 20%

*Note: VAT portion is unclear; may be 3% or 5%

6

Interesting Tax Treaties

Vietnam

Dividends 0% Gains on shares: 25% SIN: Exempt HK: Exempt if alienated shares <15% or not holding principally immovable property Korea: Exempt if not holding principally immovable property NL: Exempt if not holding principally immovable property Malaysia: Exempt if not holding principally immovable property France: Exempt if not holding principally immovable property

Interest CIT 5% + VAT 3% or 5% France 0% Netherlands 0% (Gov & banks)

Fees CIT 5% + VAT 5% SIN, France no service PE, no technical fee provisions Malaysia up to 10% (technical fees) Germany up to 7.5% (technical fees)

Myanmar

Dividends 0% Gains on shares: 40% (non-oil & gas); 40-45-50% (oil & gas) SIN: reduced to 10%

Interest 15% All treaties 10%; exempt for Gov. SIN 8% for banks

Fees 3.5% Korea Exempt if < 6 months SIN Exempt if < 6 months India, Thailand 10% (fees included in royalty provision)

Laos

Dividends 10% Korea 5% (participation of 10%) China 5% Malaysia 5% (participation of 10%)

Gains on shares: 10% Thailand: Exempt Interest 10%

China 5%

Fees 5.6% (effective rate)

Cambodia – No DTAs

Dividends 14% Gains on shares: Non-residents are exempt

Interest 14%

Fees 14%

7

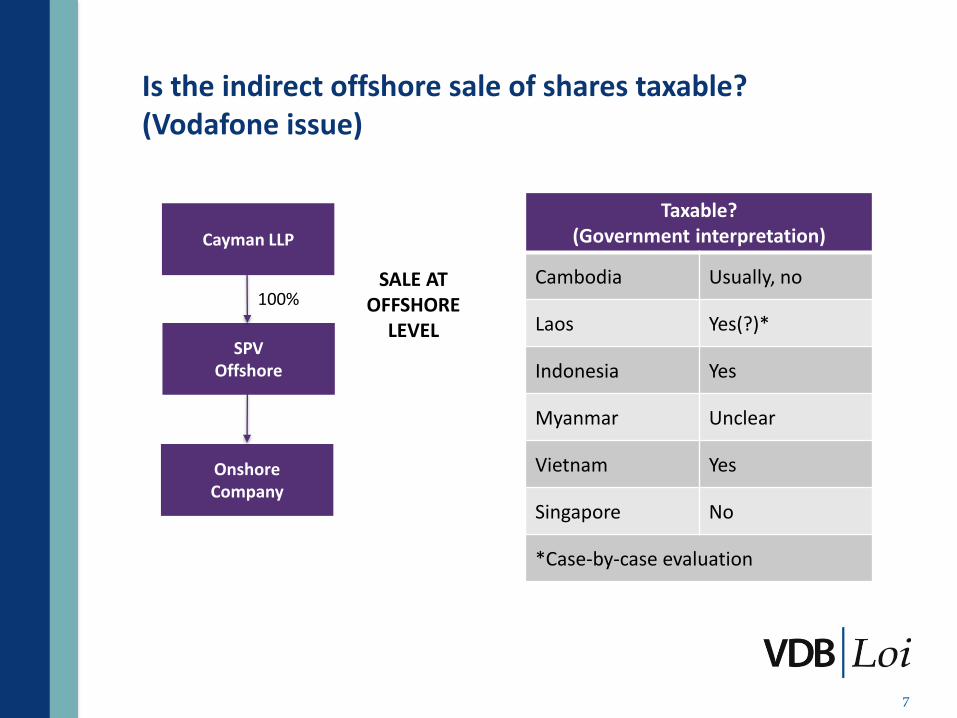

Is the indirect offshore sale of shares taxable? (Vodafone issue)

Cayman LLP

SPV Offshore

Onshore Company

100% SALE AT

OFFSHORE LEVEL

Taxable? (Government interpretation)

Cambodia Usually, no

Laos Yes(?)*

Indonesia Yes

Myanmar Unclear

Vietnam Yes

Singapore No

*Case-by-case evaluation

8

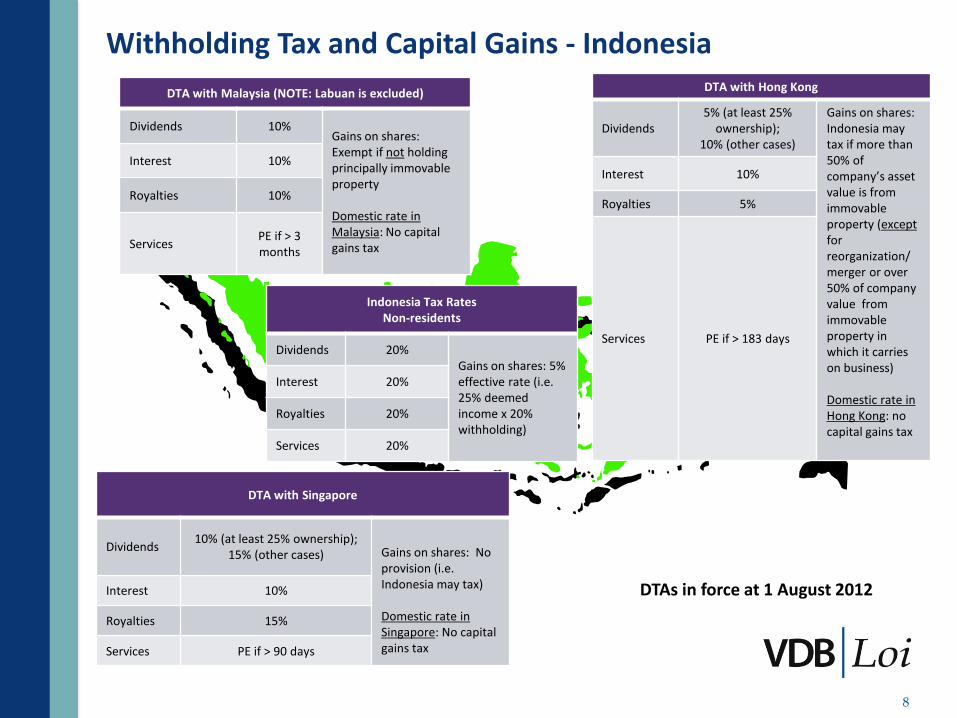

Withholding Tax and Capital Gains - Indonesia

Indonesia Tax Rates Non-residents

Dividends 20% Gains on shares: 5% effective rate (i.e. 25% deemed income x 20% withholding)

Interest 20%

Royalties 20%

Services 20%

DTA with Malaysia (NOTE: Labuan is excluded)

Dividends 10% Gains on shares: Exempt if not holding principally immovable property Domestic rate in Malaysia: No capital gains tax

Interest 10%

Royalties 10%

Services PE if > 3 months

DTA with Hong Kong

Dividends 5% (at least 25%

ownership); 10% (other cases)

Gains on shares: Indonesia may tax if more than 50% of company’s asset value is from immovable property (except for reorganization/merger or over 50% of company value from immovable property in which it carries on business) Domestic rate in Hong Kong: no capital gains tax

Interest 10%

Royalties 5%

Services PE if > 183 days

DTA with Singapore

Dividends 10% (at least 25% ownership);

15% (other cases)

Gains on shares: No provision (i.e. Indonesia may tax) Domestic rate in Singapore: No capital gains tax

Interest 10%

Royalties 15%

Services PE if > 90 days

DTAs in force at 1 August 2012

9

Withholding Tax and Capital Gains – Indonesia

DTA with Luxembourg

Dividends 10% (at least 25%

ownership); 15% (other cases) Gains on shares:

Only Luxembourg may tax Domestic law: Provides tax exemption for gains on shares

Interest 10%

Royalties 12.5%

Services 10%

DTA with Netherlands

Dividends 10% Gains on shares: only Netherlands may tax Domestic law: provides tax exemption for gains on shares

Interest 10%*

Royalties 10%

Services PE if > 3 months

DTA with Belgium

Dividends 10% (at least 25%

ownership); 15% (other cases)

Gains on shares: Only Belgium may tax Domestic law: Provides tax exemption for gains on shares

Interest 10%

Royalties 12.5%

Services 10%

DTA with Seychelles

Dividends 10% Gains on shares: Only Seychelles may tax Domestic rate in Seychelles: No capital gains tax

Interest 10%

Royalties 10%

Services PE if > 3 months

*Interest may be exempt if it is paid on a loan made for a period of more than 2 years or for a sale on credit of any industrial, commercial or scientific equipment. NOTE: This exemption is currently not being implemented by the Indonesian tax authorities.

10

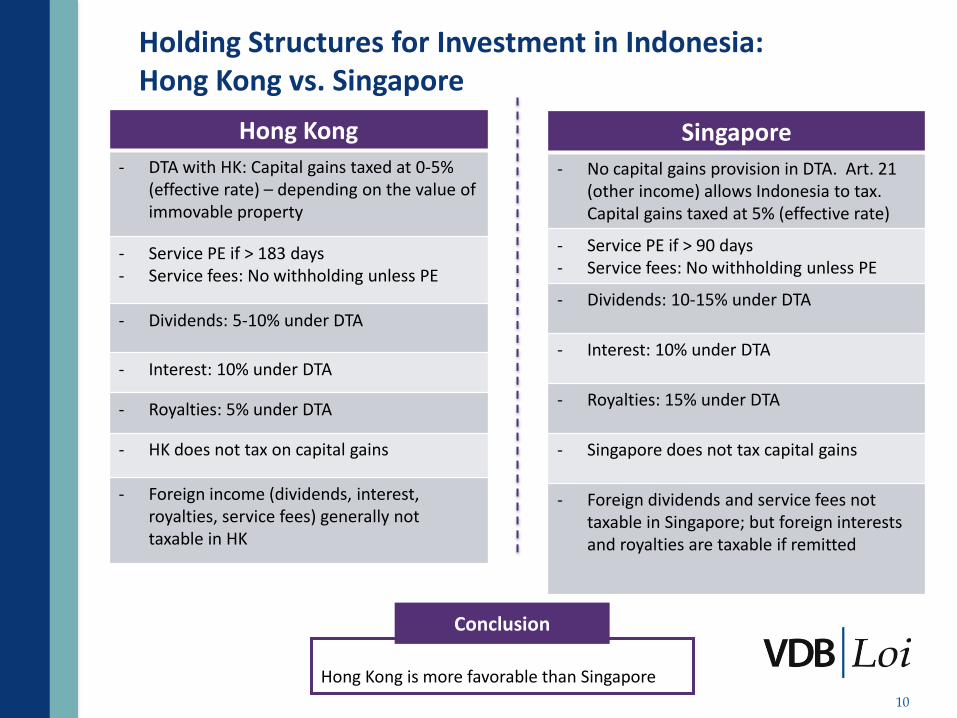

Holding Structures for Investment in Indonesia: Hong Kong vs. Singapore

Hong Kong

‐ DTA with HK: Capital gains taxed at 0-5% (effective rate) – depending on the value of immovable property

‐ Service PE if > 183 days ‐ Service fees: No withholding unless PE

‐ Dividends: 5-10% under DTA

‐ Interest: 10% under DTA

‐ Royalties: 5% under DTA

‐ HK does not tax on capital gains

‐ Foreign income (dividends, interest, royalties, service fees) generally not taxable in HK

Singapore

‐ No capital gains provision in DTA. Art. 21 (other income) allows Indonesia to tax. Capital gains taxed at 5% (effective rate)

‐ Service PE if > 90 days ‐ Service fees: No withholding unless PE

‐ Dividends: 10-15% under DTA

‐ Interest: 10% under DTA

‐ Royalties: 15% under DTA

‐ Singapore does not tax capital gains

‐ Foreign dividends and service fees not taxable in Singapore; but foreign interests and royalties are taxable if remitted

Hong Kong is more favorable than Singapore

Conclusion

11

Key points of attention:

Obtain a “Certificate of Residence” from HK tax authorities, which may depend on substance and shareholding

Indonesian dividends not taxed in hands of HK Co

Stamp duty

Obtain approval from Indonesian tax authorities for application of DTA

Example: Tax-Efficient Holding Structure for Indonesia

Cayman Co

?? %

Hong Kong Holding Co

Indonesia Company

If divesting of HK Holding Co: No tax in HK

Dividend 20% WHT (reduced to 5-10% under DTA)

100%

PROJECT

If divesting of Indonesia Co: Tax at 0-5%, depending on shareholding %

12

Example: Tax-Efficient Holding Structure for Indonesia

Dutch Antilles

100 %

Dutch BV

Indonesia Company

If divesting of Dutch BV: No tax in Netherlands

Dividend 20% WHT (reduced to 10% under DTA)

100%

PROJECT

If divesting of Indonesia Co: Only Netherlands may tax (participation exemption)

*Interest may be exempt if it is paid on a loan made for a period of more than 2 years or for a sale on credit of any industrial, commercial or scientific equipment. NOTE: This exemption is currently not being implemented by the Indonesian tax authorities.

13

1. Anti-treaty shopping rules*: only “beneficial owners” of the payments are entitled to treaty benefits

2. Criteria of “beneficial owner” are as follows:

Recipient of income

An individual or corporation that is:

Subject to domestic tax in a tax-treaty partner nation;

An institution whose name is specifically referred to in a tax treaty;

A non-resident taxpayer who is paid income through a custodian arising out of the transfer of shares or bonds that are traded on the Indonesian stock exchange;

A bank;

A corporation that fulfills some requirements.

3. Treaty shopping: The corporation or individual will not be permitted to benefit from the relevant treaty provision. The domestic tax rate will apply.

Anti-Treaty Shopping Provisions in Indonesia

*Regulation PER-62/PJ/2009

14

1. Unrealistic “Conditions Precedent” (CPs): The timing of CPs prior to closing a deal are critical, and some may be unrealistic – e.g. settlement of all outstanding employee disputes.

NOTE: Better to make such CPs into “Conditions Subsequent” (CSs) or Post-Closing Undertakings (PCUs), with purchase price offsets for non-compliance.

2. Treaty Compliance (Trade & Investment): There are a myriad of international (UN and WTO), regional (ASEAN) and bilateral treaties (US-Vietnam BTA, EU-Korea BTA, etc.), as well as international conventions and protocols that may contain provisions that have not yet been implemented by a local treaty partner, so get your legal adviser to undertake the necessary DD. (Luckily, most missed treaty terms only serve to enhance a foreign investor’s position – like greater foreign equity – but sometimes this is not the case, e.g. the banning of substances for environmental protection.)

Legal DD Issues that Can “Kill” an M&A Deal (Indonesia and generally)

15

3. Intellectual Property (IP) Issues: If IP is critical to the deal, don’t rely on the seller’s word (even if given in good faith) that all IP filings (trademarks, license agmts, etc.) are up to date (in many emerging markets, it’s not always clear), or that all IP approvals have been granted (e.g. licensor in a sub-licensing agreement in an APB purchase of a Vietnam brewery).

4. Compliance Issues: Check a target’s internal guidelines/manuals to be sure there are no lurking compliance issues (e.g. routine entertainment and/or travel benefits for government officials which violate not only foreign laws (FCPA or UK Bribery Act), but also local laws (often stricter).

5. Local Government Approvals (Ultra Vires Problem): Always double-check that the local government authorities have not over-stepped their bounds (ultra vires or beyond the powers” issue), as there are cases where deals have been killed (or later “unwound”) because the national authority overruled the local deal – e.g. J. Walter Thompson Vietnam had it’s ad license revoked a year after approval by the HCMC People’s Committee because it contained a prohibited “media buying” provision.

Legal DD Issues that Can “Kill” an M&A Deal (Indonesia and generally)

16

Legal DD

Government databases exist, but are not readily accessible

Some local press databases are available (Burmese language)

Burmese Business Associations can be helpful to get DD info on companies

NOTE: Be careful to check the USA’s “Specially Designated Nationals” (SDN) list, which includes companies run by SDN officials

Also, US State Dept requires annual report s if US$500K+ investment (incl. details of workers’ rights, land purchases and payments of US$10K+ to government officials)

Myanmar M&A Due Diligence Pointers

17

Tax DD

Tax compliance is the main issue of concern in an M&A transaction. Need to consider:

Did the target company pay advance income tax?

Did the target company submit the annual accounts and documents for final assessment?

Are there any tax arrears and pending/delayed tax assessments?

‐ Successor will be responsible

Myanmar M&A Due Diligence Pointers

18

Myanmar Acquisition Structures

Which offshore location?

Singapore Myanmar may tax if at least 35%

participation and alienated shares at least 20% of shareholding OR principally holding immovable property

Capital gains rate is capped at 10%

Malaysia Myanmar may tax if at least 35%

participation OR principally holding immovable property

Hong Kong No DTA; subject to Myanmar capital

gains tax

BVI No DTA; subject to Myanmar capital

gains tax

SHARE PURCHASE ASSET PURCHASE

CORPORATE

Issues will arise re: licensing/approvals, but each investment will have different receiving criteria and different lead and coordinating ministries, depending on the investment.

TAX

- Capital gains: 40% for non-residents; if oil & gas sector, 40-45-50% - Stamp duty: 0.3% of transaction value - Successor will inherit tax liabilities - 3-year statute of limitations - Tax clearance necessary for company registration extension once every 3 years

- Capital gains: 10% for residents; if oil & gas sector, 40-45-50% - Stamp duty: 5% on the amount/value of the transfer - No commercial tax - In a transfer of business, buyer becomes an agent of seller and is responsible for the tax liabilities of the previous year (Section 25 of Income Tax Law)

OFFSHORE SPV

NEW CO

INVESTOR

PURCHASE OF MYANMAR CO

A

PURCHASE OF MYANMAR

ASSET/BUSINESS

B

SELLER

MYANMAR ONSHORE COMPANY

19

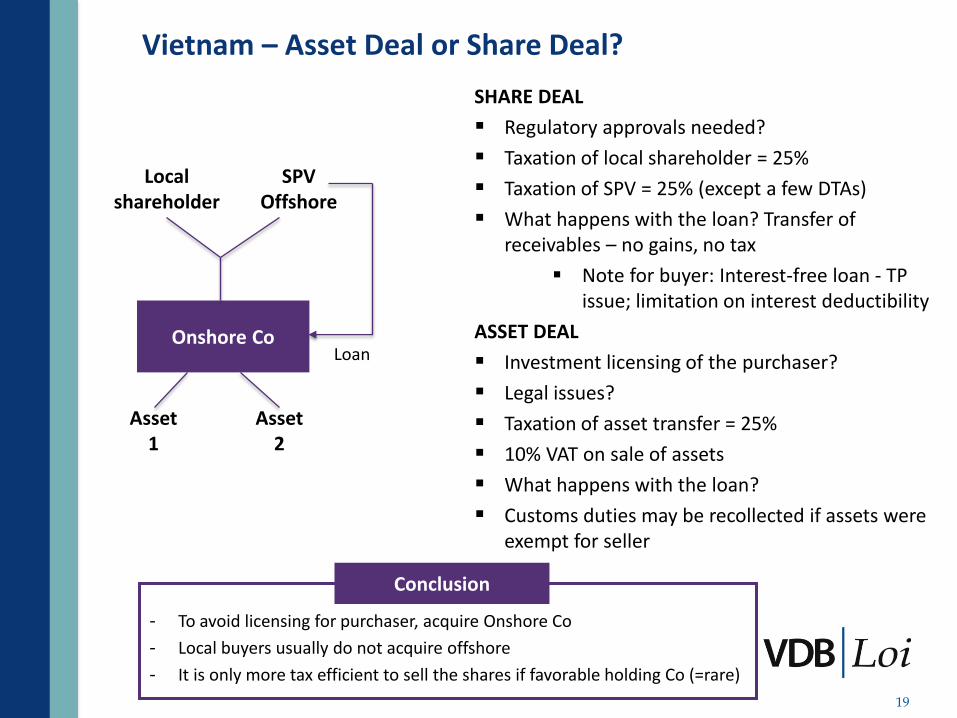

Vietnam – Asset Deal or Share Deal?

Onshore Co Loan

SPV Offshore

Local shareholder

Asset 1

Asset 2

SHARE DEAL

Regulatory approvals needed?

Taxation of local shareholder = 25%

Taxation of SPV = 25% (except a few DTAs)

What happens with the loan? Transfer of receivables – no gains, no tax

Note for buyer: Interest-free loan - TP issue; limitation on interest deductibility

ASSET DEAL

Investment licensing of the purchaser?

Legal issues?

Taxation of asset transfer = 25%

10% VAT on sale of assets

What happens with the loan?

Customs duties may be recollected if assets were exempt for seller

- To avoid licensing for purchaser, acquire Onshore Co

- Local buyers usually do not acquire offshore

- It is only more tax efficient to sell the shares if favorable holding Co (=rare)

Conclusion

20

Vietnam – Offshore Shareholder Restructuring

KEY: OPTIMIZE VIETNAM CAPITAL GAINS TAX

Holding

SPV Offshore

Op Co Onshore

Holding

SPV Singapore

Bought for US$100

Bought for US$200

Potential sale at US$200

Op Co Onshore

Spin off in SPV SIN OR Transfer seat of effective management to Singapore

A

B

PRACTICAL POINTS

Need to obtain a ruling in Vietnam?

Change in investment certificate?

Singapore corporate issues, tax notification

21

Specialist investment fund targeting Southeast Asia

Acquires 100% equity interests in companies holding fixed assets

Focuses on acquiring assets in scenarios involving corporate divestiture or restructuring

Provides innovative, efficient solutions for companies seeking to release trapped cash or realise the value of trapped assets

Can act as a third party in large transactions

Trinity Structure & Finance

22

Trapped Cash – Key Causes

CAUSES Cambodia Laos Vietnam Indonesia Myanmar

No accounting profit

Approval needed to pay out dividends

- - -

Capital cannot be reduced

- - -

Liquidation subject to extreme delays

- - -

Foreign exchange restrictions

-

Deferred taxes certain cases

23

Trapped Cash Case Study

Shareholder Hong Kong

Op Co Vietnam

Specialized Fund

SALE OF OP CO

Fixed Assets

Op Co Vietnam

SALE OF FIXED ASSETS

1

Buyer Vietnam

TO BE WOUND

OP

2 3

Capital Shareholder Loan

Cash

When can Op Co revert its cash in full to shareholder?

1 Final tax audit Vietnam

2 Winding-up procedure completed

3 Agreement of tax authorities

4 Assuming no objections from any third parties

After

24

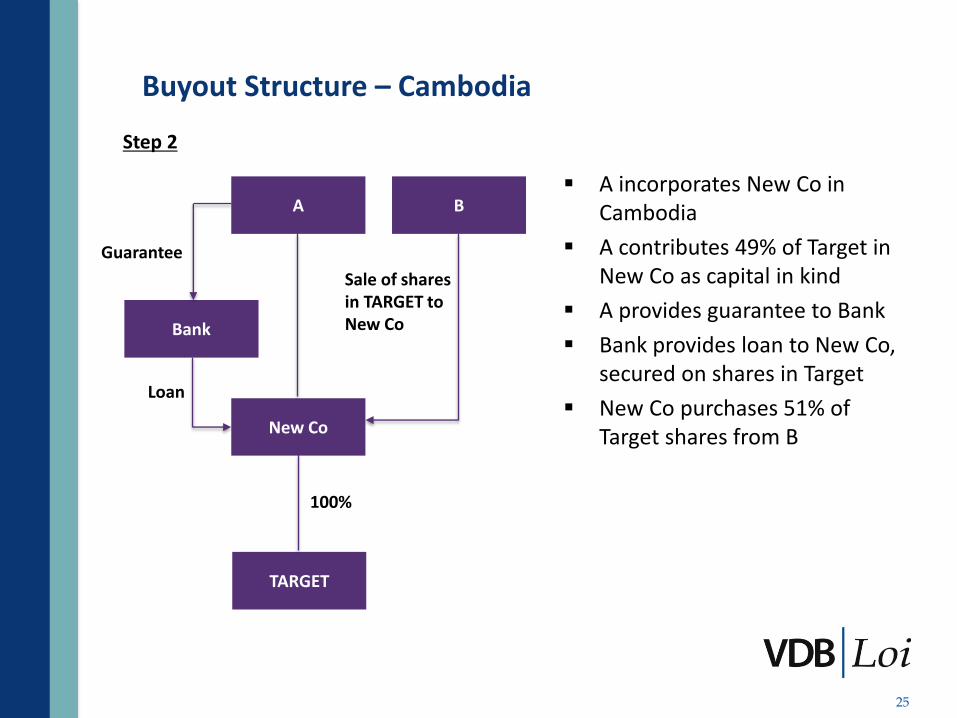

Buyout Structure – Cambodia

Shareholders A and B own Target

A (holding 49%) wants to buy out B (holding 51%) in a tax-efficient manner

A

49%

TARGET

B

51%

Step 1

25

Buyout Structure – Cambodia

A incorporates New Co in Cambodia

A contributes 49% of Target in New Co as capital in kind

A provides guarantee to Bank

Bank provides loan to New Co, secured on shares in Target

New Co purchases 51% of Target shares from B

A

100%

New Co

B

Bank

TARGET

Loan

Guarantee

Sale of shares in TARGET to New Co

Step 2

26

Buyout Structure – Cambodia

A

100%

New Co

B

Bank

TARGET

Loan

Guarantee

Sale of shares in TARGET to New Co

2. Dividend or liquidation bonus

1. Sale of business division (or all assets)

Taxation of New Co

Interest Deductible up to threshold (50% business income)

Depreciation of business goodwill

Deductible

Dividend from Target Not taxed

Taxation of Target

Sale of business/assets No VAT CIT on gain (subject to loss carry forward)

Liquidation Final tax audit (3-5 years)

Pay dividend (LIQ bonus) No WHT

More VAT credits Possible through supply

Target transfers all or part of assets to New Co

New Co offers interest on loan with business income

Target (if empty) liquidates

Step 3

27

Law on Financial Management 1995: Article 71 In the case of selling business, enterprise, property, the buyer and the seller shall be co-responsible in the payment of tax, fine which shall be paid by the seller at the time of sale up to the sale price.

Is the buyer of assets or shares co-responsible for the seller’s unpaid taxes? – Cambodia

28

Is the buyer of assets or shares co-responsible for the seller’s unpaid taxes? – Cambodia

Notification 437

According to Article 71 of the Law on Financial Management for year 1995, in case of selling a business, enterprise or property, the buyer and the seller shall be co-responsible for payment of taxes and fines that shall be paid by the seller at the time of sale.

Accordingly, the General Department of Taxation (GDT) is pleased to inform directors or owners of real regime taxpayers as follows:

1. In case of buying-selling an enterprise including buying-selling of all shares or any part of shares, the seller must settle its tax liabilities before the disposal. The settlement of any tax liability must be done through payment of all tax liabilities found after a tax audit has been conducted.

2. The buyer must be responsible for all tax liabilities incurred either during the period in which the enterprise is owned by the seller or the buyer.

29

Is a buyer in an asset deal co-responsible for the seller’s unpaid taxes?

Yes, the buyer of assets may, under Article 71 and Notification 437, be co-responsible for the tax owed by the seller, but only for taxes that are payable on the sale, at the time of the sale (such as VAT and registration tax for the transfer of immovable property).

In a share deal, is the transferred company or the shareholder-buyer responsible for the unpaid taxes of such company?

The company is definitely responsible for historical tax issues and tax debts originating from the period before transfer.

The shareholder of a company can, in certain limited circumstances, (intention to evade taxes), be held liable for tax debts of the company under Article 108 LOT.

30

Exit Structure – Laos

Offshore Shareholder

Offshore SPV

Onshore Co Laos

Key Tax Facts

Domestic capital gains tax onshore

10%

Indirect offshore sale of shares taxable?

Yes

Who has to file and pay tax?

The buyer

DTA exemption? Korea China Vietnam Malaysia Thailand

Exempt Exempt if not holding principally immovable property or participation less than 25% Exempt No provision on capital gains; Laos may tax other income (Art. 21) Exempt

31

Problem: How to create a tax efficient exit?

Thailand resident

Place of effective management

100%

Onshore Co

SPV

100%

Singapore

Laos

Dual Residence

Offshore Shareholder

Thai Holding

Onshore Co

Thai Holding?

Shareholder loan

Gain taxed at 10%

Gain taxed at 30%

WHT on interest 15%

32

Get on our Mailing List!

Professional Services Ahead of the Curve

www.VDB-Loi.com