editorial board - home - insurance institute of india · editorial board s. balachandran s. j....

TRANSCRIPT

KARNATAK UNIVERSITY - DHARWAD

EditorV.H.P. Pinto

Editorial BoardS. Balachandran

S. J. Gidwani

Secretary-GeneralS. J. Gidwani

Designed byEastern Printing Press

Printed and Published byS. J. Gidwani, Secretary-General,

for the Insurance Institute of India (Regd.)Universal Insurance Building,

Sir P. M. Road,Fort, Mumbai - 400 001.

Printed atEastern Printing PressCrescent Chambers,56, Tamarind Lane,

Fort, Mumbai - 400 001.Tel. : 2265 5467, 2265 2337

NOTICE TO READERS

Publication of papers and othercontributions in this journal does not

necessarily imply agreement withstatement made or opinions

expressed; for which the respectivewriters alone are responsible.

Registered with the office of theRegistrar of Newspapers for India

(Regd. No. 31878/77)

C O N T E N T SEDITORIAL 2

PRESIDENT�S ADDRESS 4- Shri R. Beri

INSURANCE REGULATIONS IN INDIA AND FUTURE DIRECTIONS 8- Shri T. K. Banerjee

HEALTH PROTECTION FOR ALL 14- Shri P.C. James

BANCASSURANCE CONCEPT, FRAMEWORK & IMPLEMENTATION 34- Shri Vineet Aggarwal

NEED OF THE HOUR "RISK MANAGEMENT VIS-A-VIS INSURANCEEDUCATION " (ROLE OF INSURANCE INSTITUTE OF INDIAIN LIBERALISED ENVIRONMENT) 52

- Dr. A. K. Jain

49TH ANNUAL CONFERENCE 62

BRAND IDENTITY- ITS INFLUENCE IN CUSTOMER DECISION MAKING 74- Ms. Suranjita Lahiri

LAPSATION OF LIFE INSURANCE POLICIES - A CRITICAL STUDY 82- Shri N.V. Subramanyan

PROMOTING INSURANCE THROUGH INFORMATION TECHNOLOGY 94- Shri SNSSB Srinivasa

INSURANCE BROKING IN INDIA SCOPE, CHALLENGESAND PROSPECTS 106

- Shri Vinay Verma

ROAD SAFETY - ROLE OF INSURANCE COMPANIES 118- Shri G. Venkatesh

TOWARDS A BETTER WORKING CULTURE INTHE PLACE OF EMPLOYMENT 120

- Shri T. S. V. Subramanian

CONCEPT SELLING IN LIFE INSURANCE 122- Shri Sekhar Chandra Sahoo

AROUND THE INSTITUTES 124

°

°

EDITORIALThe Institute has notable achievements to its credit in terms of, inter alia, awide network of Associated Institutes, committed administrative staff, I.T.applications in the examination system, devoted support from insuranceprofessionals in service or in retirement and, now its own physicalinfrastructure which is at an advanced planning phase.

On these solid foundations it should be easier to build a superstructure ofquality education for the decades following the Golden Jubilee.

Professional education demands strong academic underpinnings in termsof appropriate syllabus reflecting the current realities and likely trends in themarket and preparation of study material. There has been commendablecontribution from insurance professionals in the past but it is time to inductyounger professionals into the academic aspects of the Institute agenda.It may not be an exaggeration to say that there is abundant hidden talentin the insurance industry, as is evident, for example, from the number ofentries to the S.K.Desai, D.Subrahmaniam and Technical Competitions. It isencouraging to observe that for the first time three entries have securedprizes in the competition and this augurs well for the Institute.

Retired professionals should not be allowed to fade away but may beentitled to guide the deliberations of various expert committees. There maybe many available who believe in Bacon's dictum: �Every person is a debtorto his profession.�

Another area which needs to be examined is the current Postal TuitionService introduced decades ago with laudable objectives. But in recentyears, there appears to be a large number of drop-outs amongst thecandidates who enrol for this service. Why this is so needs to be examined.In any case, distance education is absolutely necessary in a large countrylike ours and specially so, because Oral tuition facilities may not be availablein many centres and where available may not be availed of due to timeconstraints or other reasons.

The demand for distance education is pronounced in university,management and professional education. The Institute may address this

2 THE JOURNAL

issue to extend its reach to the large number of candidates whether inurban or rural areas, who may not have the confidence to study on theirown but would welcome external aids. Distance learning is commonplacein the U. K, the U.S.A., Canada and Australia. In India, nearly 25 percent ofUniversities have in place distance learning systems. The All IndiaManagement Association has plans to extend management educationeven at the zila parishad level.

Advances In Information Technology have impacted all aspects of our livesand, In education we have open universities, online universities, etc. Onlinecourses have become more accessible in many areas of educationincluding professional education.

According to President A.P.J. Abdul Kalam, quality education in remoteareas requires tele education. After visiting a number of laboratories lastyear and interacting with the scientific and technological community, hehas identified education as one of the major areas where the influence ofScience and Technology will be strongly felt. In this context, he has made aspecific reference to the Indian Space Research Organisation's E D U S A T(Educational Satellite) which will be useful for Schools, Colleges, higher levelof education and non-formal education and will provide both-wayinteractivity and collaboration between the students and the educationprovider.

This may be in a long term scenario but the possibilities are infinite. TheInstitute, which has I.T. applications in place in many of its activities, mayexplore the possibilities of e-learning in insurance.

Innovation and creativity should be the mantra of the educational policyand mobilisation of the hidden talent in the insurance industry its actionplan. With this two-pronged effort, we may strive for academic excellence.

JULY - DECEMBER 2004 3

Hon�ble Dr.M.Khajapeer, Vice Chancellor, KarnatakaUniversity, Dharwad; Hon�ble members of the Councilof Insurance Institute of India; members of the Boardof Education and Administration Committee; Hon.Secretaries of Associated Institutes; invitees,distinguished guests; members of Media and my dearcolleagues from Insurance Industry.

I have great pleasure to welcome you all to the 49th

Annual Conference and the 96th Council Meeting ofthe Insurance Institute of India. I am specially gratefulto Dr.M.Khajapeer, the Hon�ble Vice Chancellor ofKarnataka University for sparing his valuable time andto be present at this august gathering as the ChiefGuest at this solemn function and to address thedistinguished gathering at this annual function.Dr.Khajapeer, I am indebted to you for your presencehere.

This event is being hosted by Dharwad InsuranceInstitute, one of the Associated Institutes of theInsurance Institute of India. The Dharwad InsuranceInstitute was established in the year 1967 and it has amembership strength of over 4000. I am thankful tothe Chairman, Honorary Secretary and other Membersof the Dharwad Insurance Institute for organizing thisconference under their auspices. They have taken allefforts to place the members comfortably during thestay at Dharwad.

Dharwad is a small town in the state of Karnataka andit is known as an educational center. This is evidentfrom the fact that Dharwad Insurance Institute has amembership strength of over 4000 despite beinggeographically a small place. This is the first time thatthe Dharwad Insurance Institute organizes the AnnualConference and the Council Meeting.

PRES IDENT � S

A D D R E S S

Speech of

Shri R. Beri

President

Insurance Institute of India

At the

49th Annual Conference

at Dharwad

on 11th September, 2004

4 THE JOURNAL

Achievements during the year

During the year 2003-04 the Insurance Institute of India has shown satisfactory progress both interms of financial performance and examination activities. As members are aware, besidesthe professional certificate and diploma examinations, the institute also provides regulationrelated qualification both for agents and surveyors. The Institute in its objective of having itsown building, made payment for the cost of land in the Bandra - Kurla complex in Mumbai. Asper the decision of the Administration Committee of the Institute, the construction of the buildingwill be entrusted to LIC of India.

The Institute also brought out new text books covering the subjects of insurance broking andinsurance survey for the first time and these have been well received in the industry circle. TheInstitute also revised the text books for Pre-recruitment examination for life and general insuranceagents. The examination based on revised syllabus for Pre-recruitment of agents however, willbe starting in case of life insurance from July , 2004 and for general insurance from October,2004.

On the international plane I am happy to report that the Regulatory Authority in Nepal and SriLanka now insist upon Associateship qualification of Insurance Institute of India for licensing ofbrokers. Besides, the number of candidates appearing for Sri Lanka has crossed 300 mark forthe professional examination. Invitation also received from the Chairman, Insurance Associationof Pakistan for discussions on, inter-alia, of extending Insurance Institute of India�s services toPakistan Insurance Industry.

The Chartered Insurance Institute, London continues to provide exemptions for the associatesand fellows of the Insurance Institute of India ( 4 & 7 subjects respectively in their ACII ) and it isunder active consideration of the Chartered Insurance Institute to provide exemptions in somesubjects for candidates having passed Licentiate examination under their revised system ofqualifications. An agreement in this area is likely to be reached in a couple of months.

A proposal of the Australian and New Zealand Institute of Insurance and Finance (ANZIIF) topermit Licentiate qualified members of the Institute to be become Associate members of ANZIIFis under discussions. It is also expected that some progress will be made with the CanadianInsurance Institute for providing cross credit to persons having I.I.I. qualifications.

With the cross credit already existing between USA and India, it is expected that all the majormarkets of the world in insurance will have cross credits in their qualification for qualifiedprofessionals from Insurance Institute of India. The Institute will launch a global qualification ofInstitute of Global Insurance Education (IGIE) co-founded by the Insurance Institute of America,Canada and England in electronic form in a couple of months from now. Discussions withLOMA ( Life Office Management Association, America) for incorporating Indian content ofInsurance Institute of India in their international qualification FLMI are likely to begin this month.

The institute is also taking steps to position itself as provider of insurance education for specificneeds of call centres and BPO organization and also planning to provide qualification framework for regulatory compliance by these organizations as per regulatory requirements of WesternEurope and America and the scheme of co-operation will be discussed with the InsuranceInstitutes in UK,USA, Canada, Australia and New Zealand.

JULY - DECEMBER 2004 5

The Institute will continue to build on information technology platform for wider reach and forimprovement in services to members and members can now view the journal of Institute on itswebsite regularly and very soon provision is expected to be made for issue of digital certificatefor IRDA examination.

Golden Era � 1955-2005

I am very pleased to inform this august gathering that the Institute has entered 50th year of itsoperations and it is time to both celebrate as well as to acknowledge the contribution madeby thousands of insurance professionals who worked without any reward for building thisinstitution. In particular, I would like to thank the contribution of, besides the Council membersand the members of the Board of Education and the Administration Committee, the variousoffice bearers of Associated Institutes in India and affiliated Institutes abroad for helping in thedevelopment of this institution. My thanks to all of you for contributing so much to the presentstatus of the Institute.

The Challenges Ahead

So far, I have outlined all the good things and good news, let me now share with you the futurechallenges. The growth in the operations of the Institute during the last 4 years has imposedserious burden on the administration of the Institute. While I compliment the Officers and theemployees of the Institute for standing as a one man team to deliver the promises to theInsurance Industry, it is time to set up systems and procedures to consolidate the growth achievedso far. This does not mean that the Institute should not plan further growth. It is, however, importantto have proper balances and checks before further growth is achieved otherwise in the absenceof changes in the organizational structure, growth may be counter productive.

The Institute needs to expand both in terms of infrastructure facilities and human resources.Enormous financial resources will be needed in the next 5 years for completing the buildingproject on time. To continue to enjoy the status of premier Institute in insurance education, theInstitute is examining the possibility of converting itself into an insurance university as a privateuniversity.

In the context of changes in the insurance industry the role of Associated Institutes can nolonger be limited to public sector companies who do not employ new manpower and hasfloated VRS schemes. The control over sale of study courses and the accounting needs to beredefined in the light of observations from the auditors.

I am sure with the expertise that Institute has acquired it can address these challenges giventhe support of the Associated Institutes and I hope that the details will be worked out duringthe current year.

Professionalism � Key to Industry Development

Insurance, being a knowledge subject, the need for insurance education can hardly beemphasized with an ever demanding customer on one hand and a vigilant regulator on theother, in the competitive environment with a large number of players having enormous financialresources, the key to success will lie with the quality of manpower with the individual organization.

6 THE JOURNAL

While technical knowledge itself may not be very essential for some of the functions, possessingthe same always means an additional advantage.

The blurring of boundaries between insurance and banking and new methods of risk financingand risk management are serious challenges for future managers in retaining the distinct identityand the role for insurance industry. Demographic changes of vast scale, difference in life stylesand need for post retirement income besides the new type of risks that the community is facingcan be addressed by application of knowledge acquired through professional qualification.

The insurance industry has opened a flood gate of new opportunities and challenges in othersectors of economy as well, particularly, for call centres and BPO companies. In order to satisfytheir customers, the call centres and BPO companies need to train their employees in thedomain knowledge of insurance. Theses companies will also have to satisfy regulatoryrequirements of overseas companies.

The opportunities of self employment in the field of insurance selling, marketing, survey andbroking operation can provide self employment opportunities for career development to scoresof qualified people in India. Insurance education and qualification, therefore, will be requiredin a greater measure and the Institute will have to reposition its courses to cater to the variety ofdemands emanating from the new face of insurance industry.

Acknowledgement

In the first year of my association with the Insurance Institute of India being its President, I amhappy to note the progress made by the Institute during the year. I must extend my sincerethanks to IRDA for keeping the Institute in high esteem for examination related activities. Thishelps immensely for the progress and prosperity of the Institute. The members of Council,Administration Committee, Board of Education and other sub-committee deserve myappreciation for their contribution through their valuable suggestions and advices. My thanksto the Editor of the Journal and some Board Members who have provided expert opinion onadministrative and accounts reforms. My thanks also to management of all insurancecompanies in private and public sector for their support and co-operation.

Before I conclude my address, let me once again thank the members and volunteers ofDharwad Insurance Institute for hosting this conference.

Thanking you.

JULY - DECEMBER 2004 7

HISTORICAL BACKGROUND

Insurance in India has progressedthrough several evolutionary phases inits more than one and half centuryhistory. The origins of the Indianinsurance industry can be traced wayback to the pre-independence era to1818 when it was conceived as ameans to provide for English widows.Interestingly in those days a higherpremium was charged for Indian livesthan the non-Indian lives as Indian liveswere considered more risky forcoverage. The first Indian LifeCompany, Bombay Mutual LifeInsurance Society started its businessin 1870. It was the first company tocharge same premium for both Indianand non-Indian lives. The OrientalAssurance Company was establishedin 1880. The first general insurancecompany in India - Triton InsuranceCompany Limited was established in1850. Till the end of nineteenth centuryinsurance business was almost entirelyin the hands of overseas companies.

Insurance regulation formally beganin India with the passing of the LifeInsurance Companies Act of 1912 andthe Provident Fund Act of 1912.Several frauds during 1920's and1930's sullied insurance business inIndia. By 1938 there were 176insurance companies. The firstcomprehensive legislation wasintroduced with the Insurance Act of1938 that provided strict State Controlover insurance business.

The insurance business grew at a fasterpace after independence. Indiancompanies strengthened their hold on

INSURANCE REGULATIONSIN INDIA AND FUTURE

DIRECTIONSBy : Shri T. K. Banerjee,

Member - Life, Insurance Regulatory and Development Authority,Hyderabad.

this business. Life insurance industrywas nationalised in 1956 with themerger of 245 private life insurancecompanies, and the Life InsuranceCorporation (LIC) of India was formed.The (non-life) insurance business,however, continued to thrive with theprivate sector till 1972 before it wasalso nationalized, and GeneralInsurance Corporation (GIC) wasformed in 1972 by merging 106 privateinsurance companies. GIC in turn hadfour subsidiary companies.

It was expected that the nationalisedinsurance companies would enhancethe spread of insurance to the hithertoneglected areas of the countrybesides improving security of assetsand quality of service to customersand also aiding in mobilising savingsfor the economic growth of thecountry. It was also felt that the growthof the insurance business would befaster and consumers would haveaccess to insurance coverage ofworld class standard. Although thenationalized insurers contributed tothe development and spread ofinsurance, there continued to be awide gap in terms of the marketpotential which the country offered.

OPENING UP OF INSURANCE

In 1991 there was a paradigm shift ingovernment policy with the advent ofeconomic liberalisation. Financialsector reforms in the mutual funds andbanking sectors allowed foreign directinvestment and foreign institutionalinvestment. In the insurance sector aCommittee on Reforms in theInsurance Sector, popularly known as

Malhotra Committee in 1993, wasappointed by the Government toreview the working of the insuranceindustry.

The Committee in its report submittedin 1994 recommended opening upof the insurance industry. Thekey recommendations includedpermitting private companies with aminimum paid up capital of rupeesone hundred crores to enter theindustry, prohibition of compositeinsurers and permitting foreigncompanies to enter the industry in thejoint venture mode with the domesticcompanies. Other recommendationswere introduction of alternatedistribution channels for improving theinsurance penetration, the setting upof an insurance regulatory body andmaking the Controller of Insuranceindependent, and also amendments/changes to the Insurance Act, 1938.

The Government responded byestablishing an interim InsuranceRegulatory Authority in January, 1996.However, on the issue of opening upof the sector an intense debatefollowed for several years before aconsensus emerged that this step wasjustified for increasing the penetrationof insurance in the country. And itultimately led to the passage of theInsurance Regulatory AndDevelopment Authority Act, 1999. It ispertinent to mention that the word'Development� was inserted in the Billat the last stage as the legislators wereconcerned that with competition boththe regulator and the regulated wouldlose sight of the more important

Keynote Addressdelivered at

the 49th AnnualConference of Insurance

Institute of India atDharwad, on 12thSeptember, 2004

8 THE JOURNAL

aspect of the development of theinsurance market in India therebydefeating the very objective of theopening up of this sector. Today interms of its mandate and the numberof people to be served by way ofincreased penetration of insurance,the Indian insurance regulator isperhaps the largest developer ofinsurance business in the world.

Insurance liberalisation promises manyadvantages which include better riskmanagement, product innovation,and wider customer choice. However,if implemented unwisely, it has theinherent potential to generateunprecedented inequalities withdestabilising effects on domesticmarkets. In order to allay our fears afterconsidering the present state ofdevelopment of the Indian insuranceindustry that more will be lost thangained by a complete opening up ofthe market, reforms have beenincremental in nature. As domesticpolicymakers, we are also responsibleto ensure that government ownedinstitutions have been given a fairchance to equip themselves to facecompetition.

The economic reform process is'irreversible' and the new insurancecompanies are expected to hastenthe process of producing a strong andefficient insurance market. The growthof the debt market is also expectedto get a fi l l ip as the funds frominsurance companies start flowing intothe coffers of the corporate sector.Similarly, stock market investments willfurther aid the growth of the capitalmarket and equity cult. The multipliereffect will be enormous.

CHALLENGES

In India, our approach to reforms hasbeen built on the belief thatsustainable growth is only possible inan environment which values andpromotes financial strength andstability, management capability andpublic accountability.

Reforms have included the setting upof a modern well resourced supervisor,the Insurance Regulatory andDevelopment Authority (IRDA). IRDA's

hallmark has been its belief inopenness and transparency. It hasfollowed the practice of priorconsultation with various stakeholdersbefore notification of regulations, andthis has resulted in a broadacceptance of the regulations.

To operationalise various provisions ofthe IRDA Act and Insurance Act, so far29 regulations have been notifiedcovering all aspects of insurancebusiness. Four broad areas ofoperation have been carved byregulations for the Authority to functionand these are:-(i) admission of insurersincluding powers of on site and off sitesupervision; (ii) functioning of theintermediaries; (iii) control on rates ofpremium , terms and conditions, and(iv) policyholders protection. These areinter-related. The misunderstandingthat may develop in the functioningof the various players are sought to besettled by the Authority - initially bypersuasion, failing which, by issue ofdirections.

The Authority has also helped inestablishing support mechanisms tosustain the Insurance Ombudsmansystem under the Settlement of PublicGrievances Scheme, 1998. Twelveombudsmen have been appointed inthe country. This has created a veryimportant grievance settlementmachinery for customers. Complaintsof non-settlement or delayedsettlements of claims received fromcustomers have been attended to.Many a time insurers have beenpenalized for breach of tariff termsand conditions.

Today, to the credit of combinedefforts by both the regulators andindustry players, the benefits ofinsurance are widely acknowledged,public confidence in the industry hasbeen very much visible and theindustry on the whole is far morerelevant than it has ever been in thiscountry. The industry is expected tosignificantly improve its public imagein years to come.

A healthy insurance market is an

important source of long-term capitalin domestic currency, especially forinfrastructure financing. Reforms ininsurance is therefore expected tostrengthen the capital market bygiving it greater depth or liquidity.

We are already witness to somefundamental changes in thelandscape. The insurance industry hasbeen opened up, with a restriction of26% on foreign ownership to Indianinsurers. Foreign participation hasenabled local players to form joint-ventures with foreign insurancepartners, and benefit from transfer oftechnical know-how and increasedfinancial strength. This has alsoenhanced the local insurers' ability tomodernise, expand, and to becomecredible players. Insurers are beingencouraged to form strategicalliances with other financial industryplayers, in order to flourish in aliberalised environment. Inspite of this,the sector still has many featurescharacteristic of an infant industry.

REGISTRATION OF INSURERS

The Authority has fixed a strict criterionfor awarding registration. The criteriafor awarding direct insuranceregistrations have been: financialstrength, track record and reputationof the promoters. Other aspectsexamined have been theircompliance with law and regulations,the strength of internal control systems;and commitment to contribute toIndia's development. IRDA has beenkeen to see the industry develop interms of product innovation and theuse of alternative distributionchannels. Applicants with a strongrecord in these areas, or in specialistand niche fields, and who have alsoundertaken upon themselves tounderwrite health insurance businesshave received favourableconsideration.

The experience so far in India is thatthe local partners are sound with anexcellent track record in theirrespective fields, and their foreigncollaborators are very well establishedinsurance companies with vast

JULY - DECEMBER 2004 9

experience in both developed andemerging insurance markets. Wehave, thus, sound companiespresently operating in the Indianinsurance scene. What should beensured is that they remain healthy.Adherence to regulations andobservance of sound principles ofgovernance should ensure that.

FINANCIAL HEALTH AND SOLVENCY

To guard against excessive insolvencyrisk insurers are required to meetcertain financial standards and actprudently in managing their affairs. Thestatutes require insurers to meetminimum capital and surplusstandards and financial reportingrequirements and authorise regulatorsto examine insurers. Solvencyregulations involve various aspects ofinsurers operations including:

(i) capitalisation

(ii) pricing and products

(iii) investments

(iv) reinsurance

(v) reserving

(vi) asset liability matching

New companies have substantialcapital adequacy therebyencouraging the market place tounleash the forces that are importantto compete on the basis of solvency.A rigorous scrutiny of the companiesat the entry level coupled with diligentmonitoring of their activities withspecial reference to maintenance ofsolvency margins and prudentinvestment policy ensures that themanagement of the companies is notlax and that proper corporategovernance practices are adoptedby them.

FINANCIAL REPORTING

Our accounting standards are inalignment with international standardsand regulations set out in detail themanner in which the information is tobe furnished to the Regulatoralongwith disclosure norms. IRDA isworking with the professional

accountants' institute in a bid to refinethe responsibilities of auditors and thestandards of audits, besides helping inbuilding the capacity of the domesticactuarial profession, a crucial elementof the regulatory framework.

INVESTMENT

Prudential investment norms havebeen notified to further enhance thefinancial flexibil ity and riskmanagement ability of insurers, andfor better management of investmentportfolios. In addition guidelines onrelated-party transactions to ensuremanagement integrity and publicaccountability in the conduct ofinsurance business are also in place.The guidelines reinforce the fiduciaryduty owed by insurers to properlymanage insurance funds in anindependent and transparent mannerfor the interest of policyholders at alltimes.

REINSURANCE

The need to enhance local retentioncapacity and conserve foreignexchange reserves has been ofstrategic economic priority. The lifereinsurance portfolio is very small.In non life insurance the Indianinsurers, through carefullydesigned reinsurance programmesadministered on a market wide basis,have managed to retain within thecountry as large a percentage of thegross direct premium as is desirableconsistent with safety. As a NationalReinsurer the General InsuranceCorporation of India receives statutorycessions of 20 percent from all generalinsurance companies on all classes ofbusiness.

TERRORISM AND CATASTROPHEINSURANCE

The Terrorism Pool formed jointly by thepublic and private insurancecompanies and managed by GICremains a singular example of how themarket responded to the post 9/11events. The contributing share of eachcompany was directly related to itspremium income. Terrorism Pool offersinsurance cover against terrorism for

a maximum of Rs 300 crores perlocation. Those who seek a terrorismcover for more than Rs 300 crores arefree to go to foreign insurancecompanies, but the rates from theoverseas players are much steeper.

Although the net account forcatastrophic losses is protected byExcess of Loss covers, a series of suchlosses can erode an insurer's netaccount and its financial stability.Indian insurers have not yet set upspecific reserve provisions forcatastrophes. Expert opinion suggeststhat it shall be prudent for insurers tomaintain a Catastrophe Reserve at 2%of net premium of individualcompanies with a cap, based on astipulated percentage, to allow foraccumulation to take place in thisaccount for a specified number ofyears. However, in the absence ofincentives to these funds in the formof tax exemptions very little of paidpremiums shall become available tomeet future catastrophe claimsliabilities under the policies issued. Thisis an area of concern and requires tobe addressed.

HEALTH INSURANCE

Though the Insurance Act 1938 andthe IRDA Act, 1999, prescribe that theregulator would encourage thesetting up of health insurance businesson a stand-alone basis, no one has yetapproached to set up an exclusivehealth insurance business. Due to lackof applications in this particular area,the Authority has encouraged both lifeand general insurance companies,old and new, to go in for rider policiesoffering health covers. It is gratifyingto note that the new companies haveseized this opportunity and many ofthem have gone in for riders offeringa variety of health insurance products.Additionally, for balanced and rapidgrowth of the health insuranceportfolio, with the introduction of ThirdParty Administrators in this areacashless hospitalization covers havebeen introduced for the first time inIndia. A Health Insurance WorkingGroup has been formed to increasethe penetration of health insurance

10 THE JOURNAL

and suggest ways and means toremove the structural bottle necks.

RURAL AND SOCIAL SECTORINSURANCE

Though the Government has tried topromote insurance business in ruralIndia through Public Sector InsuranceCompanies for nearly two decadesthere still remains a vast untappedpotential considering that 74.3 percent of the total population lives inrural India. At present in rural areasinsurance cover is low, and there arefew insurance covers, available onaffordable terms, for rural producersand consumers. One of the prioritiesfor fostering expansion of domesticinsurance would be identification ofproductive potential and specificinsurance needs in areas not yetreached by insurance and enhancingcooperation between insurance andrural credit schemes and institutions.

MICRO INSURANCE

The potential of insurance as a tool toreduce poor households' vulnerabilityto risk needs to be examined andadvanced. Insurance can play apositive role in meeting the financialservices needs of the poor, and onewould need to examine the manychallenges involved in offeringinsurance, through micro-insuranceagents simpler forms of insurance suchas property, personal accident healthand life insurance.

INSURANCE INTERMEDIARIES

The Indian insurance industry reliesheavily on the traditional agencydistribution channel, with a largenumber of agents of varying levels ofprofessionalism and productivity.There is thus scope for developingalternative distribution channels,which are often more efficient, andwhich can offer lower costs and betterbenefits for policyholders. We need todevelop alternative distributionchannels, which cost less, and canreach a wider target market.

Initially there was a demand from thelife insurers to have higher commissionsfor first year's premium in line with the

practices in developed market.However, over a period of time thisdemand has waned with the insurershaving realized that such high level ofcommissions will result in the existingunhealthy practices gettingmanifested manifold. In manycountries, the presence of professionalinsurance brokers and independentfinancial advisers who represent theinterests of the client is a majormotivating factor for insurers to raiseefficiency and give better value topolicyholders.

There has been some concern atcertain quarters on the appropriateremuneration structure for insuranceagents and brokers, and also on thepractice of offering special discountin l ieu of agency commission orbrokerage in the area of GeneralInsurance. Perhaps this has arisen asa result of introduction of the insurancebrokers as an intermediary channel.The role of an insurance broker doesnot seem to have been properlyunderstood and appreciatedbecause of the primordial role of tariffin the non life insurance. In additionthe brokers have also not been ableto deliver the value added servicesexpected of them.

Intermediaries and other practitionersare subject to professional conductstandards and a licensing procedure.This involves the professionals passingan examination, after completing arequired course. The idea is to makesure the professional has basicknowledge to protect the public andto provide a mechanism to removethe dishonest from business.

THE ROAD AHEAD

Most of these developments havecommenced only in the last few years.In the near future the industry isexpected to grow both in stature andstrength. It has to come a long wayfrom the days when private insurancewas seen in the public eye assomething to be avoided as far aspossible and misconduct in variousforms was rife in the industry.

In the near future insurers, in particular,shall be less financially vulnerable tothe vagaries of the market becauseof the adoption of a prudentialregulatory regime, which has set veryhigh solvency requirements andcapital adequacy norms. Domesticinstitutions, be they insurers orintermediaries are expected to catchup with their international counterpartsin terms of efficiency, innovation andcustomer service. Productivity levelsare expected to be as perinternational best practices. The levelof market penetration is also expectedto substantially improve.

DYNAMIC REGULATORY STRUCTURE

With the rate at which businessesevolve, rules and regulations becomeobsolete almost as soon as they areformulated. Regulators have to keepup with the burst of productinnovations, alternative distributionchannels, electronically-l inkedpayment systems, e-commerce,investment avenues and alternativerisk transfers, just to mention a few.These developments create intricatelinks in a commercial chain which arepotentially fragile in the sense that ifone link snaps, the whole chain comesapart. No member of the chain will bespared from the domino effects of acrisis anywhere along the chain.

With such complex and uniqueinterdependencies, it would bevirtually impossible to prescriberegulations that deal with everypossible contingency. In the first place,regulators may not even be aware ofthe potential risk factors emergingevery day. Secondly, regulators maybe faced with constraints ofjurisdiction. The answer to this dilemmais not deregulation but finding the rightregulatory structure.

In other aspects of regulatory reformconvergence of financial products willalso create the need for domesticregulators to re-examine financialsector regulation at a macro level.One option would be to createfirewalls within financial groupstructures to contain the spread of

JULY - DECEMBER 2004 11

intra-group exposures.

Instead of being watchdogs,regulators should act more likepacesetters, catalysts and navigators.This approach recognises that theindustry is often best placed to makedecisions concerning the rapidchanges revolutionising insurancemarkets. In an environment wheretime is of the essence, greater relianceshould be placed on the inherentknowledge and capabilities of theindustry to adapt to these changes.

LEGAL REFORMS

Institutional and regulatory reforms arealready well underway in India. Thecurrent statute was drafted in 1938and has seen numerous amendmentsand changes. Many of its provisionshave become outdated and somehave lost their relevance. Newdevelopments have taken place inthe insurance world, which do not finda reflection in the law. Therefore thereis an urgent need to overhaul theInsurance Act, 1938 in order to reflectthe new circumstances that existtoday. The Law Commission has in therecent past submitted itsrecommendations on the proposedamendments to the Insurance Act,1938. Even so, we must realise thatchanges do not take place overnight.The institutional and regulatory reformstake time to accomplish. For thispurpose discussions have alreadytaken place and the suggestionsreceived from various quarters havebeen sent to the Government. Wehope to see the new insurancelegislation in times to come.

DE-TARIFFING

The general insurance market hasbeen predominantly a tariff drivenmarket. Fire, engineering, motor andmarine hull insurance are under thetariff, regulated by a statutory TariffAdvisory Committee. The non tarifflines of general insurance and all lifeinsurance products are subject to a"file and use" process wherein theinsurers are required to file theirproduct to the Authority thirty daysprior to its launch. In case the Authority

has no reservations they can goahead with the marketing of the saidproduct.

All over the world it is well recognizedthat deregulation and tariff cannotexist together. Competition is aprocess where no player achieves adominant position. Transparency andinformation conditions are reinforcedto allow for "informed" decisions bothby buyers and sellers. Price fixingmechanisms are changed, away fromcoordinated systems; rates as well asproduct design, are determined bymarket forces. Price controls oninsurance should not be justified withconsumer protection. There has beena heavy cross subsidy from propertyclasses to motor insurance and tomotor third party insurance inparticular. Market based pricingshould lead to lower and more risksensitive premium rates over time andensure that databases becomealigned with key rating factors.

However, in order to ensure thatdismantling of tariffs does not result inrate wars and insurers are able to ratethe risks they underwrite in a scientificmanner based on historical data, theinitial step in regard to detariffing ofthe motor own damage premium hasbeen proposed with effect from 1stApril, 2005. To consider the alternativesavailable, to have a free marketavailability of the products in thisregard and to suggest to the Authority,the measures to be taken in this regardincluding adoption of differentialrating, the Authority had formed anexpert group to recommend the roadmap which has recently submitted itsreport. The detariffing of the otherportfolios will be considered thereafter.

CORPORATE GOVERNANCE

Another area of reforms is the processof corporate governance. Todaycorporate governance is strictlyapplicable to listed companies andnone of the insurance companies inIndia are so far l isted. The IRDArecognizes that weak corporategovernance and lax managementwithin the companies undermine thecredibility of the general public in the

companies as well as the Regulatorand cause severe setback to thegrowth of the industry. This problemhas been addressed through arigorous system of scrutiny ofapplications for setting up insurancecompanies coupled with stringentnorms relating to solvency. They arefurther reinforced with appropriateregulations on investment of funds bythe companies. Guidelines have beenset that clearly enunciate the role andfunctions of directors and AppointedActuaries of life insurance companies,so that they can provide greaterprofessional stewardship to protectand enhance the interests ofpolicyholders.

With greater competition in themarketplace, enhanced standards ofcorporate governance investmentmanagement and market conductare necessary to protectpolicyholders' interests. Regulationsneed to be introduced to strengthenthe corporate governance ofinsurance companies in line withinternational best practices.

INSURANCE AWARENESS & MARKETCONDUCT

Enhancing consumer informationabout insurers' prices, products andfinancial strength is a critical functiongiven the heavy reliance oncompetition to ensure good marketperformance. IRDA would also moveaway from merit-based regulation toa disclosure-based regime. IRDA, forinstance, will look to market institutionsand intermediaries to ensure thatprospectuses contain all the relevantinformation necessary to enable thepotential policyholder to make aninformed decision. Through regularchecks and reviews of practices of themarket institutions and throughpunitive action against therecalcitrant, the IRDA will ensurecompliance with a prudential regime.

Market discipline will also become amore prominent feature in theregulatory infrastructure. However, thekeys to effective market discipline liein public disclosure and consumer

12 THE JOURNAL

education. These will becomeimportant aspects of the regulator'srole in the years ahead. Informed andeducated consumers are often themost effective means of commercialdiscipline as they can exert significantinfluence over an institution's businessdecisions and practices, as well aspricing policies.

SHIFT IN FOCUS: FROM REGULATIONMAKING TO COMPLIANCE

With the insurance regulatoryframework now in place the focus ofthe regulator is shifting towards thecompliance aspects of theregulations. In this process theregulator will adopt a proactive anddynamic attitude and will be settingan example in terms of certainty ofregulatory action. To enable this, thereis need to develop suitable systemsand procedures and devise analyticaltechniques based on keyperformance indicators. This will alsohelp to develop a basis for the levelof regulatory response for a givensituation besides providing aconsistent approach which respondsto the seriousness of the problem.Action can be escalated or de-escalated as the severity of thesituation increases or decreases. Thiswil l enhance the efficiency ofsupervision and provide both thesupervisor and the regulated entitieswith enhanced certainty of law.

SELF REGULATORY ORGANISATIONS

Ineffective market discipline is one ofthe issues identified by theInternational Association of InsuranceSupervisors as a threat to the emergingmarkets. This is an issue that has to beeffectively tackled for the healthygrowth of the insurance market. TheRegulator has a role to play in ensuringmarket discipline, the role played bythe insurance companies in bringingabout discipline in the market placecannot be ignored. The key toeffective market discipline lies in publicdisclosure and consumer education.Informed and educated consumersare often the most effective means ofenforcing commercial discipline.

As our market develops, the role of theSelf-Regulatory Organisations (SROs)will take on greater significance. Theempowerment of the SRO essentiallygives greater rights and responsibilitiesto market participants who, for theirpart, must be capable of ensuringeffective regulation and must be ableto meet these challenges. Failure toregulate effectively will lead to adeterioration of market integrity andstability and, ultimately, theintervention of the IRDA as supervisoryregulator with oversight responsibilities.We also expect that, in time, much ofthe current developmental rolecurrently played by the IRDA will betaken over by the SROs. In anenvironment of growth andexpansion, it is the SRO who can bestfacilitate innovation and adaptationto seize competitive opportunities andmeet challenges. The Life InsuranceCouncil and the General InsuranceCouncil are presently performing therole of an SRO in a limited manner bysetting up market conduct standardsfor insurers. An exercise is already onto grant the Actuarial Society of Indiaa statutory status on the lines of theInstitute of Chartered Accountants ofIndia. A similar exercise has also beeninitiated to set up a self regulatorybody for insurance surveyors and lossassessors.

INSURANCE EDUCATION ANDRESEARCH

One of the spin-offs of liberalisation ofthe insurance sector has been thedemand for insurance education,training and research. The InsuranceInstitute of India's role appears to havebeen confined to the professionalexaminations conducted by it, andwhich has been recognized asacceptable qualification insofar asprofessional competence in the areaof insurance is concerned. What hasperhaps been ignored is the tappingof the vast potential by way ofintroduction of new subjects in tunewith the demand and expectations ofan evolving market after a thoroughreview of the existing courseware.Examples of such subjects are HealthInsurance, Unit Linked Insurance, andInsurance Regulations. These areas

today require to be dealt in muchgreater detail than what is being doneat present.

Similarly research in insurance remainsa neglected area in this country andthere is need for a concerted effort todevelop and define areas of focus forresearch in tune with the requirementsof the industry. Without a researchfocus no institute can expect to maketangible contribution in terms of valueaddition and meeting theexpectations of its members and theindustry.

Although one is witness to a lot ofinstitutions offering insurance coursesthere is need to develop an initiativeto set up a nodal body for accreditingvarious courses to lend an element ofcredibility and standardisation in thearena of insurance education.

The Insurance Institute of India mayconsider seizing this initiative and leadfrom the front by creating a researchwing and a standardization body withthe involvement of other insuranceeducation service providers.

CONCLUSION

The insurance industry will face greatercompetition from other financialservice providers along all aspects oftheir value chain. Insurers, for instance,with their significant and growing assetbase, shall have to develop assetmanagement capabilities andexpertise on par with professional fundmanagers, otherwise they will facepressure to farm out their funds forprofessional management.

IRDA will monitor the progress of theindustry and make further changeswhere necessary. It will continue toconsult industry representatives indeveloping a conducive regulatoryenvironment, and formulatingincentives to enhance the operationalcapabilities of insurers, for instance, inproduct development, distributionand asset management. Suchpartnership and dialogue will be vitalfor the growth of the industry, and formeeting the challenge of makingIndia a regional insurance hub and aninternational financial center.

JULY - DECEMBER 2004 13

1. CONCERN FOR HEALTH:

Health has always been a matter ofcritical concern for all. This is especiallytrue for persons who earn solely frommanual work, as their bodies are theirprime assets. Even for others, healthsignificantly affects both productivityas well as quality of life as good healthgives a feeling of general wellness andvitality. Good health, thus, has aprofound impact on the overall valueand capability of human capital.Illness, disease, accident on the otherhand not only creates pain andsuffering, but also erodes financialsecurity and reduces productivity andwell being. It also increases costs forthe society and the country ininnumerable ways. Organisedmedical and health care systems,which began to evolve about 100years ago, have become an effectiveboon to improve healthcare all overthe world by its increasing reach andcapability in combating diseases anddisability. As a result, longevity hasincreased, prosperity and general wellbeing have gone up, and people areexperiencing new frontiers of wellnessand freedom from disease.

In this scenario of improved healthoutcomes, the cost of healthcare isseen to be ballooning to becomeprohibitive and unaffordable. Ashealth is a valuable asset and anessential part of the human capital,the large and unpredictable risksaffecting it needs financial protection,from the point of view of allconcerned, namely individuals,

HEALTH PROTECTIONFOR ALL

By: Shri P.C. James, National Insurance Co. Ltd., Kolkata.

because many risks, which becomeevident, appear to be rooted in theirbehavioural characteristics. This hasled to the lifestyle approach in healthpromotion. However, there are alsoissues beyond the individual levelwhich require regulatory interventionsuch as in food and drug quality,health and safety aspects at work oron the roads and so on. There is alsothe need for international safetystandards in areas such asenvironmental and chemical risks, useof agro chemicals, food additives etc.Thus the concern for health hasimplications at individual, community,national and international levels.

In a different dimension, good healthis not only a concern for the poor butalso for the rich. Poor people aredriven to disease and disability due tofactors such as undernutrition, as wellas their unhygienic surroundings,which affect the quality of water theyuse as also their general l ivingconditions. These lead to poor healthconditions, giving rise to manycommunicable diseases that oftenlead to higher morbidity and mortalityrates. The rich in their turn are notspared from health hazards caused byproblems related to overnutrition,obesity, sedentary and stressfullifestyles. These generate what arecalled lifestyle diseases. Thus whilepoor countries have to deal primarilywith the consequences ofcommunicable diseases, the richcountries have to grapple with thefallout of the more expensive lifestylediseases. Countries in between aresaid to be compelled to carry adouble burden of both the "old"communicable diseases as also of the"new" lifestyle diseases.

families, employers, the society andthe country. Assured paying capacityis also a benefit that is looked forwardto and gives stability to the health careproviders who need the financing tosustain their capital spending, skillupgradation, and their rising researchand service costs.

The physical integrity and dignity of theindividual is now a well-recognisedright in law and fact. Healthcare is thusan important right for all. Therefore,denial of access to healthcare owingto geographical, infrastructural, socialor financial l imitations is notappropriate and needs to be rectifiedby all concerned as a part of socialengineering and a necessarycomponent in upholding basic humanrights. In fact, it is seen that such adenial perpetuates the vicious cycleof poverty, malnutrition, lowproductivity and early mortality. Thuslack of access to healthcare is not onlya cause for individual trauma andtragedy, but it also stunts the progressof the society on both economic andsocial planes. Conversely the ability tohave access to healthcare hasproved to be a powerful weaponagainst poverty as also against socialand economic inequality.

The health of a person is subject towide variety of risks, which trigger bothpredictable and unpredictable costs.Risks to the health of any personseldom occur in isolation but are theresult of both proximal and distal socio-economic causes. These risks affecthealth not only at the individual levelbut also at the society level. At thelevel of individuals, it was thought thatthey are mainly responsible forhandling their own health risks

S. K. DesaiMemorial

Medal AndPrize Winning

Essay2003-04

14 THE JOURNAL

The concept of good health is alsobroadening from a traditionalplatform of merely treating disease orinjury, to one where promotive,preventive and rehabilitative care isalso given increasing attention, eventhough the curative treatment stilldominates the mindset of healthcarestakeholders. The potential ofpreventive care is yet to be fullyexplored and the savings therefrom isyet to be completely understood.

Health risks thus affect all sections ofthe society. Statistics starkly reveal thedeep dichotomy between theconditions of the rich and the poor.Undernutrition and related conditionsaffect no less than 170 million poorchildren worldwide and about 3.4million of them die as a result of thiseach year. On the other hand amongthe well to do, there are one billionadults who are overweight and atleast 300 million of them are clinicallyobese. There is also the phenomenonof risk transition due to changes in thepattern of living arising from migrationfrom the rural to the urban, fromunderdevelopment to thedevelopment stage and fromagricultural occupations to theindustrial or the service sectors.

2. HEALTH CONCERNS OF THE POOR

For the poor their bodies are mostoften their only asset and thereforeapart from issues of physical integrityand dignity, good health is directlyrelated to their daily earnings. In sharpcontrast to this, there is often aninevitable denial of access tohealthcare to them, which is one ofthe reasons why their l ives arefundamentally linked to poverty. Atthe same time it is seen that while lackof access to healthcare perpetuatespoverty, access to healthcare is apowerful weapon in economicempowerment.

Developmental economics show thatthere is a health-wealth connection.A healthy workforce is the key tohigher productivity, less absenteeism,

less expenditure on curative care andso on. Worldwide, it has been seenthat ill health disproportionately affectthe poor, and they bear a higherburden of both morbidity andmortality. Ill health triggers a chain ofadversities for the poor which mayconsist of loss of work, deprivation ofearnings, expenditure for medicaltreatment, sale of essential assets todefray the costs and falling prey toloan sharks leading to unaffordableborrowings and indebtedness.

In the Indian context it has beenestablished that the poorest 20% havemore than double the mortality ratescompared to that of the richest 20%.They suffer disproportionately morethan others from pre-transitionaldiseases like Malaria or TB. To add toall as an NCAER (National Council forApplied Economic Research) studyreveals, the richest 20% enjoy threetimes the share of public subsidy forhealth as compared to the poorestquintile.

In the area of health expenditure,figures show that while the rich needto spend around 2% of their incomeon healthcare, the burden on the pooris far higher at 12%. Hospitalisationoften means the liquidation of theirmeagre assets and not infrequentlypermanent indebtedness. Thus, thethreat of financial disaster prevents thepoor from seeking treatment, and thepercentage of people avoidingtreatment due to potential financialruin have increased in the decade of1986-96 from 15 to 24% in the ruralareas and from 10 to 20% in the urbanareas.

A recent analysis of the World Bank isillustrative of the plight of the poor. Itsays that a hospitalised person in Indiaspends more than half of his totalexpenditure on hospitalisation, andmore than 40% of those hospitalisedhave to borrow money or sell assetsto cover their expenses and 35% fallbelow the poverty line owing to this.The study also suggests that such outof pocket medical costs alone maypush 2.2% of the population below thepoverty line in one year.

3. THE INDIAN HEALTHCARE SCENE :

Healthcare has been recognised asan essential social sector investmentsince independence. In the initialdays, therefore, it was envisaged thathealth services in governmentinstitutions, which were to play a majorrole in healthcare, would be providedfree of cost to all. However, theincreasing expectations regardinghealthcare could not be matchedowing to escalating costs andunaffordable expenditures.

The health spend in India, currently isaround Rs.103, 000 crores or 5.2% of itsGDP. Over the last five decades Indiahas built up a vast health infrastructureand manpower in the primary,secondary and tertiary care areas,involving government, voluntary andprivate sectors. However, even nowthe extent of access as also utilisationrates varies between states andregions, between the urban and therural, and between the rich and thepoor.

The public infrastructure is fairlyextensive both in the rural and urbanareas. In the rural areas, thegovernment has set up a vast networkof sub-centres, primary health centresand community health centres.Despite this, it is seen that patientsoften turn to private providers for theirneeds, as doctors and medicines aremore easily available there and thepatients perceive a better quality ofcare. However, the utilisation of privatecare puts a serious strain on personalfinances on the one hand, and on theother, often puts the patient to risk dueto the large numbers of unqualifiedpractitioners especially in the rural belt.

In the urban areas, the public sectorinfrastructure consists of urban health-posts, taluk hospitals, district hospitalsand medical colleges having tertiaryfacilities. In the private healthcarearea, there are private practitioners,for profit hospitals and nursing homesas also charitable institutions. However,even here, there are deficiencies in

JULY - DECEMBER 2004 15

the delivery of healthcare as it islargely unregulated, leading to themushrooming of sub-standard facilitiesand malpractices such as overdiagnosis and over treatment. Thusthere is a general perception of limitedavailability of facilities, combined withpoor delivery.

4. PROFILE OF THE INDIAN HEALTHCAREEXPENDITURE:

It is estimated that 61% of the privatehealthcare spending is on outpatientcare, and over 55% of the outpatientexpenditure is on acute infection suchas fevers, diarrhoea andgastrointestinal diseases. The inpatientexpenses are mainly towards cure ofacute infections, accidents andinjuries, cancer, heart diseases andmaternal care. The CII-Mckinseyreport on healthcare in India estimatethat healthcare spending will increasefrom the present Rs.86, 000 crores(2000-01) to over Rs.200,000 crores inreal terms in 2012. Private healthcarewill grow faster from today's Rs.69, 000crores to Rs.1, 56,000 crores and thiscould rise by an additional Rs.39, 000crores if health insurance coverbecomes available to the rich and themiddle class.

Given the gigantic needs of thecountry there is a crying need for alarge amount of investment in healthinfrastructure, skills and capabilities.The indicative factors for theseinclude:

a. The overall number of beds,physicians, and nurses is lowcompared with otherdeveloping countries and worldaverages.

b. The quality levels in mosthealthcare centres are poor,and many lack essentialequipment and instruments.

c. The number of beds in hospitalsis generally low. The majority ofprivate hospitals have less than30 beds.

d. There is overcrowding and overutilisation especially in publichospitals.

e. Private providers are allowed tofunction in an unregulatedenvironment and reportsindicate that many run practicesand treatment without minimumstandards. There is no all Indiaregulation for provider standardsand treatment protocols.

As per experts the future of healthcarein the country is expected to move inthe following directions:

1. As the country progresses in thedevelopmental index, the shareof communicable and other"old" diseases will drop to bereplaced by lifestyle diseases, ofwhich cancer and heartdiseases will be the mostprominent.

2. Outpatient treatment carewhich now constitute the majorpart of the health spend willdecrease and the inpatienttreatments will increase, thoughthrough technologicalimprovements day caretreatment also will rise.

3. The healthcare market will showrapid growth due to higher levelsof awareness and concern. Itcould even reach a level ofRs.2,70,000 crores by 2012 in viewof the changing demographics,disease profiles and due tomedical inflation.

4. All the above will necessitate theneed for rapid spread of riskfinancing and risk transfersthrough insurance andalternative channels, as theincreasing cost of medicare willnot be affordable even to thewell to do classes.

5. WHY HEALTH INSURANCE?

Insurance and development are

critically linked, and wherever risks existwhich gives rise to unforeseen financiallosses, insurance has a place asindemnifier. Health insurance hasbecome an essential requirement foreveryone for the following reasons:

1) Health risks are pervasive amonghuman beings across all ages,classes, social groups andeconomic categories. Morbidityconditions can affect anyone atany time in a sudden andunforeseen manner.

2) Medical costs are rising and canbe very high. Research,technology, skills and capital areall costs associated withhealthcare and their combinedcosts are ballooning, makingmedical costs vulnerable torapid rise, and the term"mediflation" has come intovogue characterising the regularrise of medical costs.

3) Health risks have a frequencylevel that is high requiringcontinuous cash flow or cashavailability. Such being the caserisk transfer to a cash rich entityis logical and essential, to avoidfalling into a debt trap andfacing impoverishment.

4) While diseases per se may not beincreasing newer and bettercures and treatments are rapidlybecoming commonplace inview of the increasingrequirements of wellness andgood health. The treatmentvalue chain keeps expandingboth vertically and horizontally toinclude not only curative, butalso rehabilitative treatmentsand includes pain management,diet advice, physiotherapy,preventive care and so on.

5) Disease patterns are changingdue to economic and socialchanges. The widespreadprevalence of communicablediseases is being replaced by the

16 THE JOURNAL

more insidious lifestyle diseaseswhich brings on critical illnessesthat raises expenses ofcatastrophic dimensions for thepatient and the need for lifelongcare. Lifestyle disease conditionssuch as diabetes is becomingpandemic in India. A surveydone in six Indian cities show that12% of the population could bediabetic and more worryinglyanother 14% could be pre-diabetic.

6) Development and economicwell being is raising expectationsof good health and fitness. It isseen that as people move up theincome ladder, they begin tospend disproportionately largersums on healthcare. A surveyconducted by NSSO (NationalSample Survey Organisation) in1999-2000 found that out of the12 types of households classifiedbased on their monthly percapita expenditure (MPCE), thetop class has an average percapita expenditure of about 12times that of the bottom class,but in the case of healthcareexpenditure the difference isabout 28 times.

7) Human morbidity conditions notonly affect everyone, but alsotends to increase andaccelerate with aging, needinglifelong protection, which shouldideally start from the cradle.

8) Health and disability losses havegreat immediacy as it involvescurative and rehabilitativeexpenses, trauma and pain andany delay in treatment owing toinability to pay can affect futurehealth and destroy a person'sincome and wealth.

Risk transfer mechanisms thus need tocome into the daily lives of everyoneand into the mainstream of theeconomic landscape as quickly aspossible.

6.HEALTH INSURANCE AND ITSCHARACTERISTICS:

Health Insurance is a method of risktransfer, by which an insurer assumesresponsibility for costs that arise due tocovered il lness, disease and/oraccident. Health Insurance is thus amethod of financial protection in theform of a contract containing terms,conditions, warranties and exclusionsby which in the event of a coveredloss taking place, the insurerindemnifies the insured by paying thecosts incurred, to the insured or themedical provider as the case may be,directly or through a Third PartyAdministrator.

The basic benefit of health insuranceis that all those covered getprotection, by paying a small price orpremium for the protection and thefew who incur unforseen but insuredmedical costs are paid for the same.Therefore, through the medium ofinsurance a known and affordablecost of protection is incurred everyyear to cover against the unknown,and often unaffordable costs ofhealth, which may also includecatastrophic losses. Thus by means ofinsurance, an insured person is giventhe necessary "deep pockets" to payfor unforseen health costs. Insurersbring to the public by this an assuranceof "affordability", which is very criticalin medical care, where the costoverhang, especially in the tertiarycare is very forbidding, and requiresrisk transfer. In addition in medicalinsurance insurers can also add theservice of "assistance" through ThirdParty Administrator (TPA) Service.

Broadly Insurance of persons can bethrough two types of indemnification:

a) Reimbursement of Expenses

b) Benefit Payments

Generally health covers are in theform of reimbursement of necessaryand reasonable medical costs, and inorder to avoid the burden of sourcing

the money first and then the insurerreimbursing the costs, insurers provide"cashless" service through their TPAs inhospitals that have been networkedby the TPAs. Benefit payments are onthe other hand, amounts which arefixed at the time of taking theinsurance, and on the happening ofthe contingency, paid in full or asagreed, to the beneficiary. Healthinsurance, though popularly is of thereimbursement of cost type, is seeingan increasing use of critical illnesspolicies as also disability policies,which are in the form of benefitpayments.

Unlike life insurance, which dealsprimarily with mortality, healthinsurance deals with the complexphenomena known as morbidity.Whereas in conventional life insurancethere will generally be one claim,health insurance risk typically involvesthe possibility of multiple claims andhence the health underwriter's task isto gauge the morbidity level consistingof both frequency and severity.Human morbidity conditions cannotbe measured or defined exactly andtheir manifestation depends on thecombination of a variety of factorssuch as age, sex, heredity,environment, lifestyle, occupation,food habits, economic status and soon. Morbidity conditions are also notreported on a regular basis, and thedata that may be gathered in thisregard cannot be universalised.Furthermore, morbidity conditions alsoindicate an evolution as new diseasestrains and new cures are coming intovogue over the course of time.

Health Insurance is different from theinsurance of all other assets, which aregenerally insured, in as much as healthcoverage deals with human beingsand with the less understood andcomplex phenomena of humanmorbidity. The following featurestherefore, tend to stand out:

1. A market value cannot beplaced against a human beingand hence in health indemnity

JULY - DECEMBER 2004 17

policies it is difficult to place aceiling on health coveragesbased on strict value or costparameters.

2. Ageing brings on more risks.Rejection of coverageparticularly at renewals due toage and/or aggravation of riskfactors are often neither possibleas in other asset insurances normay be permitted by law orcourts in the absence specificsocial security schemes and suchother safety nets. Rejection ofhigh risk coverage being difficult,there is an implicit cross subsidyin all health schemes wherebythe young subsidises the old, therich subsidises the poor andhealthy persons those who areoften ill.

3. Unlike many other insurancecovers, health insurance is claimintensive, that is, the frequencyof claiming is high. Empiricalevidence shows that out of 100persons covered an average of4 to 5 persons claim. Statisticalanalysis also shows, as seen in theCII-Mckinsey study, that there isa link between developmentand hospitalisation, that if in 2001when the per capita income wasaround US$ 2100 there were 31hospital admissions per thousandpeople, this is expected to rise to39 hospitalisations in 2012 whenthe per capita income is likely tobe US$ 3600.

4. Cost-push factors are generallylikely to be high and can beunaffordably pushed higher inmedical insurance owing to thefollowing two factors.

a. Moral hazard. Moral hazardproblems arise when thepolicyholder demands allkinds of medical facilitiesand services regardless ofcost. This coupled withmedical providers who donot have any incentive to

lessen costs, recommendthe costliest treatments,even if they are of littlevalue to the patient. Theyare also found to be proneto charge more merelybecause the patient isinsured.

b. Adverse Selection. Adverseselection can take placewhen people with high riskare likely to buy healthpolicies, rather than personswith medium or low risk.Another aspect of adverseselection manifests whenindividuals take the policywithout family members orif they are included in thecoverage the sum insuredchosen for family memberswho are covered, is oftenskewed in favour of thosewith the highest risk.

5. Morbidity conditions as alreadystated before are difficult tocomprehend and relevantauthentic researched data ishard to come by. Its range,scope and extent havevariations depending on age,sex, living conditions, lifestylesand so on. Hence, healthinsurance has traditionallyfollowed a rating pattern basedon experience basis.

6. Medical costs are continuouslydisplaying inf lat ionarytendencies and the beneficiariesof policies show increasing levelsof util isation. These twophenomena always combine toput pressure on premium levels.Hence, premium rates needfrequent revisions, and the ratesare generally perceived by theinsuring public to be high. In viewof the resistance from the insuredin paying higher premiums andthe various other characteristicsof health coverage as7explained elsewhere, health

insurance business is normallycharacterised as a high volume,low margin business.

7. Control on selection and controlon costs are the two vital factorsthat can assure health insuranceof long-term success andsustainability. Since healthinsurance coverage is for humanbeings, screening out personsfrom coverage would not beeasy and there could be actualor potential regulationsprohibiting discontinuance ofinsurance coverage. Therefore,the right method would be toexpand the base by coveringmore of the population, throughwell-distributed groups so as tobalance the portfolio. As thepooling concept in health impliesa certain amount of subsidy fromlow risk to high-risk sections of thepopulation, it is important to bringin balanced groups.

8. This ties in with the concept thathealth insurance is ideal fromcradle to grave. A mix of coversare available to take care oflifecycle requirements and thehabit of insuring everyone fromyoung age helps to ensure notonly protection for all but alsolong term sustainability of healthschemes.

9. Control on costs is an area wherethe insurer needs to work with theproviders and insureds, to ensurefairness and adequacy oftreatment on the one side, butat the same time to prevent overutil isation of facil it ies andservices, and limit the cost oftreatment within agreed orreasonable cost bands. Historicalevidence shows that medicalcosts tend to balloon over timeand headlines will continue to bemade such as: "Biggest carmaker spends more onhealthcare than steel for cars".(Business Standard, Kolkata

18 THE JOURNAL

edition, 20.8.03) Therefore, thefinancing of healthcare involvescertain amount of oversight andinter ference on the part ofinsurers and their facilitatorsthrough various methods ofutilisation review, agreementswith providers, casemanagement methods and soon. This may be perceived asrestricting of choices andfreedom for insureds. However atrade off is required betweenpremium paying capacity andthe availability of choice levels.

10. To offset complaints againstinsurers regarding impededaccess to care, the problems of"risk selection" by insurers toattract and retain only healthypersons, rejection of renewal ofpolicy or increase of sum insuredetc. courts, regulators andgovernments are often forced tostep in. In the US a draft Patients'Bil l of Rights contains thefollowing rights for patients:

� Information disclosure

� Adequate choice ofProviders and Plans

� Access to emergencyservices

� Participation in treatmentdecisions

� Respect and non-discrimination

� Confidentiality of healthcare information

� Complaints and appeals

Insurers are bound to takecognisance of customers voiceand rights in the area of healthcare more than in any othercategory of insurance.

11. Health Insurance, as alreadyindicated, can generate high

emotional responses from customers. Not only is good health a matter ofconcern, the frequency of claims, the controls and the "gag" clausessupposedly or actually contained in the policy wording, the service andadministrative failures in assisting the patient and settling the bills, easilytouch a raw nerve in insureds. Medical care also involves pain and trauma,affect issues of human dignity, confidentiality of health information,adequacy and quality of treatment etc. Therefore, in health insurance,insurers and their related service providers need to be highly responsiveand proactive and many assistance services will have to be offered toreassure and satisfy customers.

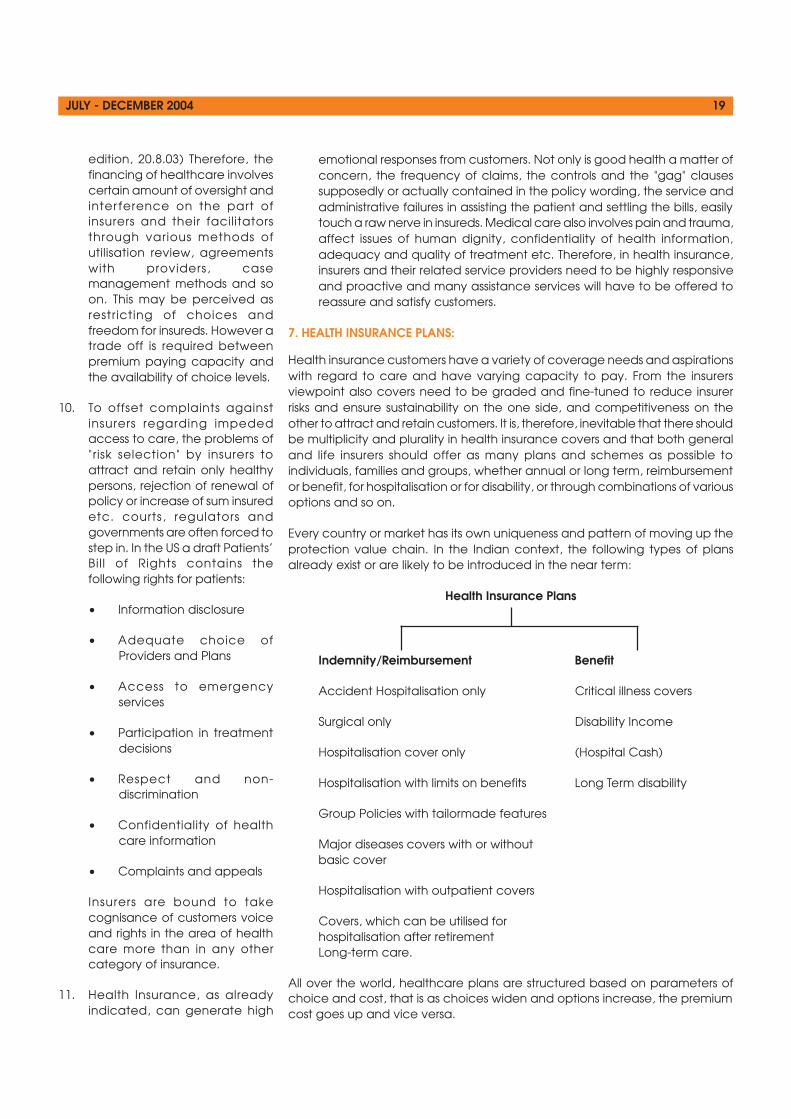

7. HEALTH INSURANCE PLANS:

Health insurance customers have a variety of coverage needs and aspirationswith regard to care and have varying capacity to pay. From the insurersviewpoint also covers need to be graded and fine-tuned to reduce insurerrisks and ensure sustainability on the one side, and competitiveness on theother to attract and retain customers. It is, therefore, inevitable that there shouldbe multiplicity and plurality in health insurance covers and that both generaland life insurers should offer as many plans and schemes as possible toindividuals, families and groups, whether annual or long term, reimbursementor benefit, for hospitalisation or for disability, or through combinations of variousoptions and so on.

Every country or market has its own uniqueness and pattern of moving up theprotection value chain. In the Indian context, the following types of plansalready exist or are likely to be introduced in the near term:

Health Insurance Plans

Indemnity/Reimbursement Benefit

Accident Hospitalisation only Critical illness covers

Surgical only Disability Income

Hospitalisation cover only (Hospital Cash)

Hospitalisation with limits on benefits Long Term disability

Group Policies with tailormade features

Major diseases covers with or withoutbasic cover

Hospitalisation with outpatient covers

Covers, which can be utilised forhospitalisation after retirementLong-term care.

All over the world, healthcare plans are structured based on parameters ofchoice and cost, that is as choices widen and options increase, the premiumcost goes up and vice versa.

JULY - DECEMBER 2004 19

Cost

Choice

7.1 Health Insurance Benefit Covers:

Benefit covers are policies where onthe occurrence of covered losses, theagreed amounts are paid,irrespective of the costs incurred.Benefit policies are popular becausethe policies are simpler and theformalities and documentationrequired to settle the claims are fewerand evidences of expenses incurredare not required. However, theeconomic status of the beneficiaryand the moral hazard of the proposerbecome important considerations,particularly as the sum insured or thebenefit amount rises higher andhigher.

7.2 Critical Illness Cover

Among the more popular benefitpolicies is the Critical Illness Cover, alsoknown as Dreaded Disease Cover. Ina world where lifestyle diseases areincreasingly dominating, this coverbecomes more and more essential. Itcan be sold both by general and lifeinsurers. It is said that in today's world,the white collared, highly drivenexecutive, working round the clock,with non-negotiable deadlines anderratic eating schedules is anaccident waiting to happen. The worsthit segments in this regard are peoplein the productive 30 to 65 age group,according to experts. Theconsequences of a critical illness canbe manifold:

� Possible loss of employment

� Physical disability

� High medical expenditure

� Need to change lifestyle

� Dependency on others in day-to-day life.

Expenditures that can arise from theabove are difficult to quantify andreimburse, and therefore, it makeseminent sense to offer a benefit coverfor a sufficiently high sum insuredbased on income levels. Since acritical illness can affect employment,companies can ideally take annualcritical i l lness policies for theiremployees, especially executives.

The critical illnesses generally coveredare the following: stroke, coronaryartery surgery, cancer, kidney failure,surgery for a disease of the Aorta,heart valve replacement, organtransplant, paralysis, total blindness,multiple sclerosis, myocardialinfraction.

7.3 Hospitalisation Covers :