economic uncertainty and the cross-section of hedge … · economic uncertainty and the...

TRANSCRIPT

Economic Uncertainty and

the Cross-Section of Hedge Fund Returns

Turan Bali, Georgetown University

Stephen Brown, New York University

Mustafa Caglayan, Ozyegin University

Introduction

• Knight (1921) draws a distinction between risk and true uncertainty and

argues that uncertainty is more common in decision-making process.

• Risk occurs where the future is unknown, but the probability of all possible

outcomes is known.

• Uncertainty occurs where the probability distribution is itself unknown.

• In empirical asset pricing literature, not much attention has been paid to this

distinction so far.

Introduction

• This paper investigates whether standard measures of risk or economic

uncertainty is a more powerful determinant of the cross-sectional differences

in hedge fund returns.

• Knight (1921) draws the important distinction between risk, in the sense of a

measurable probability, and uncertainty, which cannot be measured and by

that fact is uninsurable.

• While uncertainty of its nature cannot be measured, economic change which

he argues is the source of this uncertainty can indeed be measured.

Introduction

• Economic uncertainty, as calibrated by the the time-varying conditional

volatility of macroeconomic variables, is associated with business cycle

fluctuations:

• Default spread, term spread, TED spread

• Short-term interest rate changes

• Aggregate dividend yield

• Equity market index

• Inflation rate, unemployment rate, growth rate of real GDP per capita, and the

Chicago Fed National Activity (CFNAI) index.

Introduction

• Alternative measures of economic uncertainty are generated by estimating

time-varying volatility of 10 economic indicators based on the GARCH model.

• Monthly uncertainty betas are estimated for each fund from the time-series

regressions on the basis of 36-month rolling regressions of hedge fund

excess returns on these uncertainty factors.

• We examine the performance of these uncertainty betas in predicting the

cross-sectional variation in hedge fund returns.

Introduction

• Portfolio level analyses and cross-sectional regressions indicate a positive

and significant link between uncertainty beta and future hedge fund returns.

• Funds in the highest uncertainty beta quintile generate 5.5% to 7.5% higher

average annual returns than do funds in the lowest uncertainty beta quintile.

• The positive relation between uncertainty beta and risk-adjusted returns (9-

factor alpha) remains economically and statistically significant.

• We control for a large set of fund characteristics and risk attributes, and find

that the average slope on uncertainty beta remains positive and highly

significant.

Introduction

• Why hedge funds with higher exposure to economic uncertainty generate

higher returns?

• Is there a theoretical framework supporting this finding?

• The positive relation between uncertainty beta and expected returns is

justified in Merton’s (1973) intertemporal capital asset pricing model.

Conditional ICAPM with Risk and Uncertainty

• Merton’s ICAPM:

• We provide a time-series and cross-sectional investigation of the conditional

ICAPM with time-varying covariances:

• In Merton’s (1973) ICAPM, investors are concerned not only with the terminal

wealth that their portfolio produces, but also with the investment and

consumption opportunities that they will have in the future.

Conditional ICAPM with Risk and Uncertainty

• Hence, when choosing a portfolio at time t, ICAPM investors consider how

their wealth at time t+1 might vary with future state variables.

• ICAPM investors prefer high expected return and low return variance, but

they are also concerned with the covariances of portfolio returns with state

variables that affect future investment opportunities.

• ICAPM investors are concerned with hedging more specific state-variable

(consumption-investment) risks.

Conditional ICAPM with Risk and Uncertainty

• Bloom (2009) and Bloom et al. (2007) introduce a theoretical model linking

economic uncertainty shocks to aggregate output, employment and

investment dynamics.

• Chen (2010) introduces a model that shows how business cycle variation in

economic uncertainty and risk premia influences firms’ financing decisions.

• Stock and Watson (2012) indicate that the decline in aggregate output and

employment during the recent crisis period are driven by financial and

economic uncertainty shocks.

• Allen, Bali, and Tang (2012) show that systemic/downside risk in the financial

sector predicts future economic downturns.

Conditional ICAPM with Risk and Uncertainty

• Hence, economic uncertainty is a relevant state variable that affects

investors’ expectations about future consumption and investment

opportunities.

• Hence, the state variable is proxied by economic uncertainty.

• ICAPM in terms of conditional betas:

Why do we investigate hedge funds?

• Hedge funds use a wide variety of dynamic trading strategies, and make

extensive use of derivatives, short-selling, and leverage.

• Hedge fund managers actively vary their exposures to changes in

macroeconomic conditions and to fluctuations in financial markets.

• Hedge fund managers have heterogeneous expectations and different

reactions to changes in the state of the economy.

Why do we investigate hedge funds?

• Disagreement among professional forecasters and investors on expectations

about macroeconomic fundamentals (e.g., Kandel and Pearson (1995),

Lamont (2002), and Mankiw et al. (2004)).

• Hence, economic uncertainty plays a critical role in generating cross-

sectional differences in fund managers’ expectations about the level and

volatility of economic indicators.

Number of Hedge Funds: 1994 - 2011

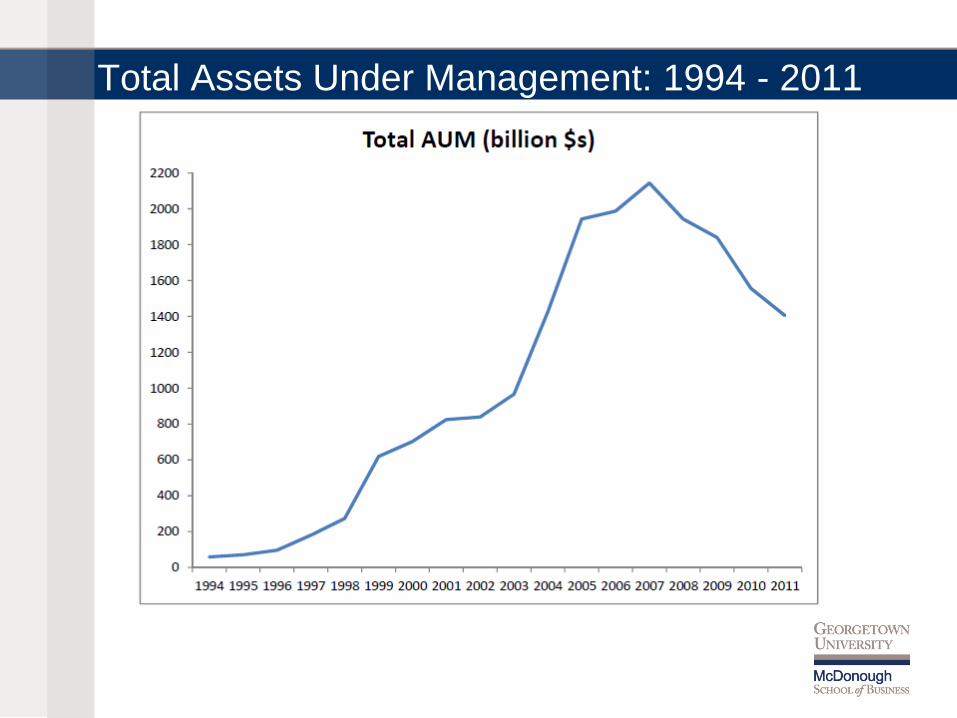

Total Assets Under Management: 1994 - 2011

Literature Review

• Sadka (2010) → Liquidity risk

• Bali, Brown, and Caglayan (2011) → Default premium and inflation beta

• Titman and Tiu (2011) → Manager skill

• Bali, Brown, and Caglayan (2012) → Systematic risk vs. residual risk

• Cao, Chen, Liang, and Lo (2012) → Exposure to market illiquidity

• Patton and Ramadorai (2013) → Time-varying exposures

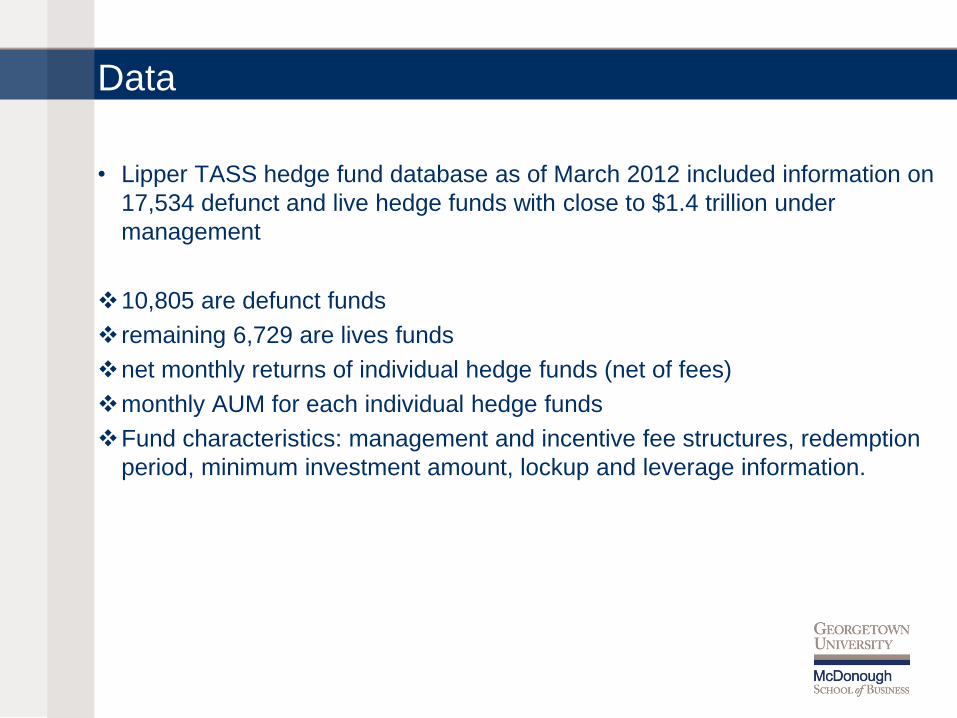

Data

• Lipper TASS hedge fund database as of March 2012 included information on

17,534 defunct and live hedge funds with close to $1.4 trillion under

management

10,805 are defunct funds

remaining 6,729 are lives funds

net monthly returns of individual hedge funds (net of fees)

monthly AUM for each individual hedge funds

Fund characteristics: management and incentive fee structures, redemption

period, minimum investment amount, lockup and leverage information.

Descriptive Statistics

Descriptive Statistics

Risk Factors

• MKT: Excess return on the value-weighted market index

• SMB: Fama-French size factor

• HML: Fama-French book-to-market factor

• MOM: Carhart momentum factor

• ∆10Y: Fung-Hsieh long-term interest rate factor

• ∆CrdSpr: Fung-Hsieh credit spread factor

• BDTF: Fung-Hsieh bond trend-following factor

• FXTF: Fung-Hsieh currency trend-following factor

• CMTF: Fung-Hsieh commodity trend-following factor

• IRTF: Fung-Hsieh short-term interest rate trend-following factor

• SKTF: Fung-Hsieh stock index trend-following factor

Correlation between Risk Factors

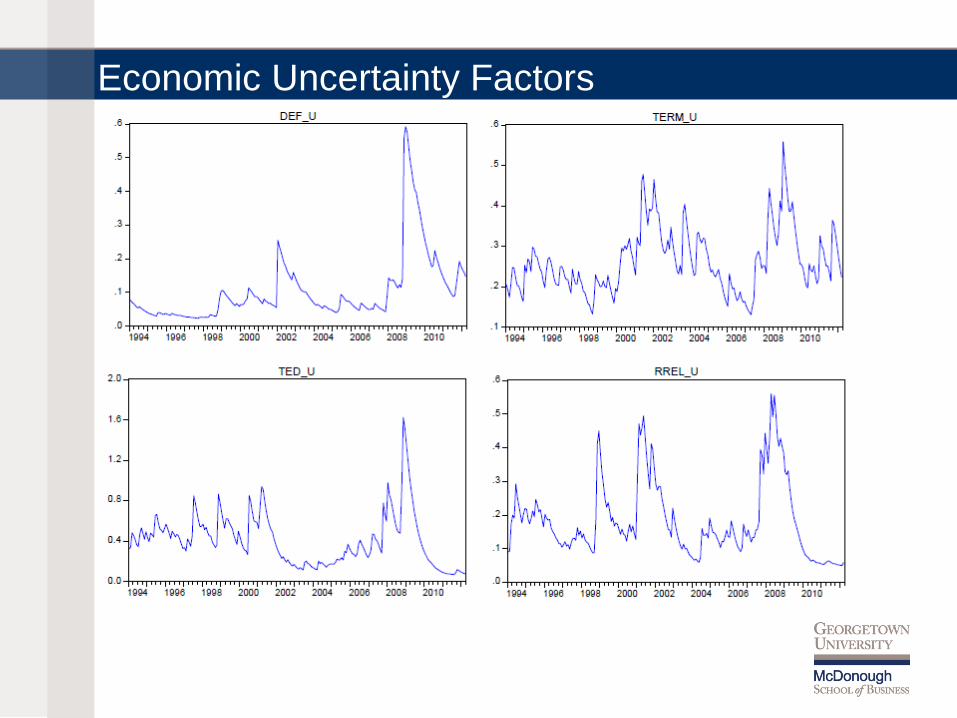

Economic Uncertainty Factors

• DEF_U: Uncertainty about default premium

• TERM_U: Uncertainty about term spread

• TED_U: Uncertainty about credit risk

• RREL_U: Uncertainty about short-term interest changes

• DIV_U: Uncertainty about aggregate dividend yield

• MKT_U: Uncertainty about the equity market

• INF_U: Uncertainty about the inflation rate

• UNEMP_U: Uncertainty about the unemployment rate

• GDP_U: Uncertainty about real GDP per capita

• CFNAI_U: Uncertainty about macroeconomic activity

Economic Uncertainty Factors

• Alternative measures of economic uncertainty are estimated using the time-

varying conditional volatility of the state variables based on the Asymmetric

GARCH model with AR(1) process:

Economic Uncertainty Factors

Economic Uncertainty Factors

Correlation between Uncertainty Factors

Correlation between Risk and Uncertainty Factors

Uncertainty Beta

• We use a monthly rolling regression approach with a fixed estimation window

of 36 months to generate the risk factor and uncertainty betas:

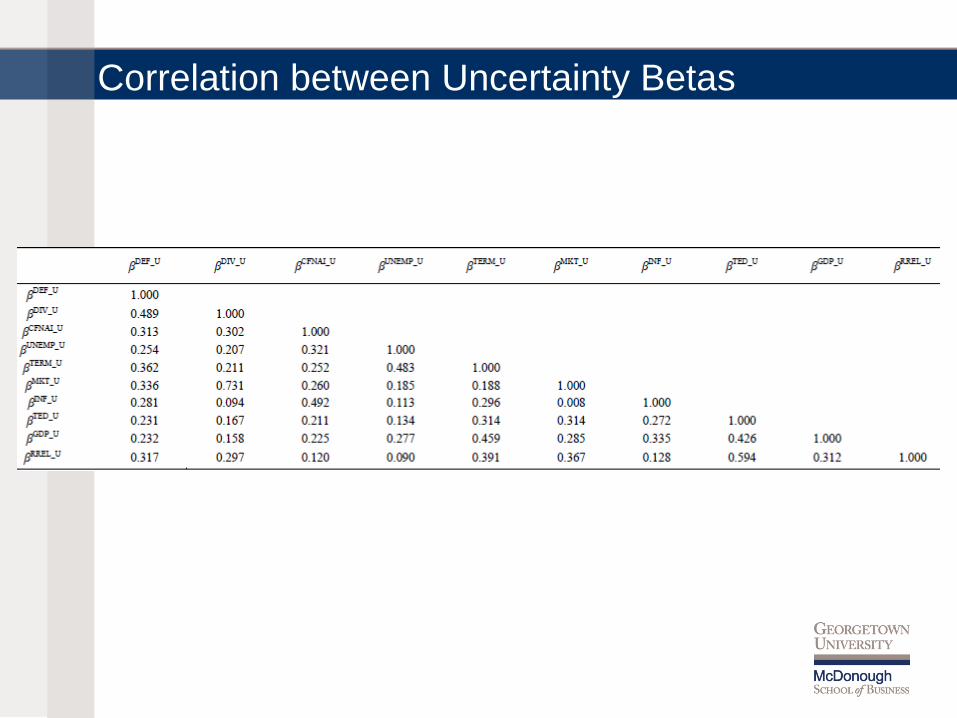

Correlation between Uncertainty Betas

Univariate Portfolios of Risk Factor Betas

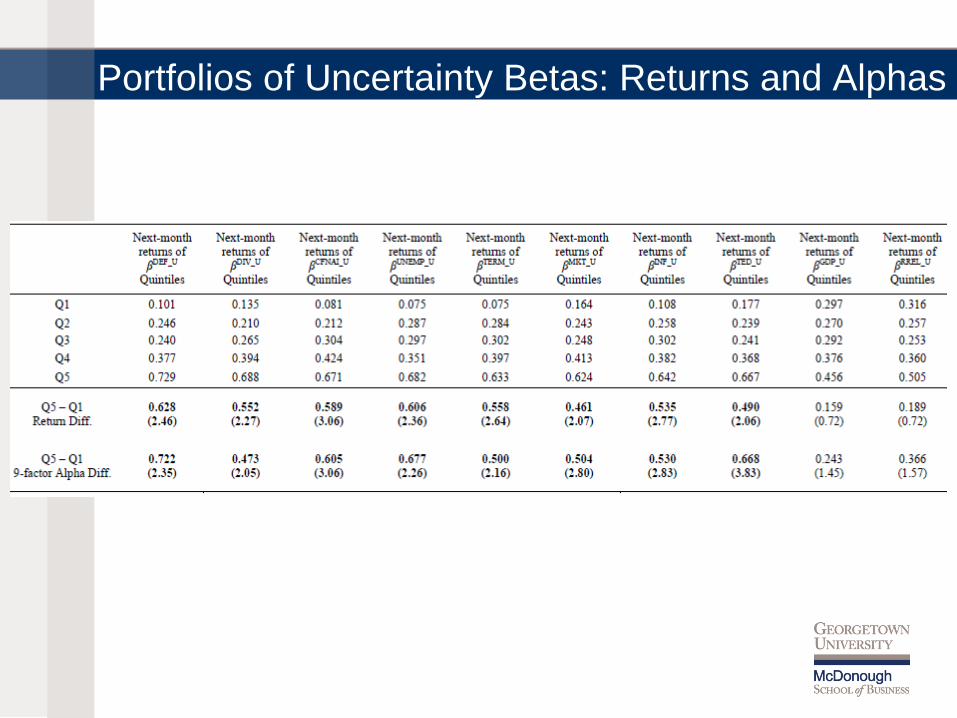

Portfolios of Uncertainty Betas: Returns and Alphas

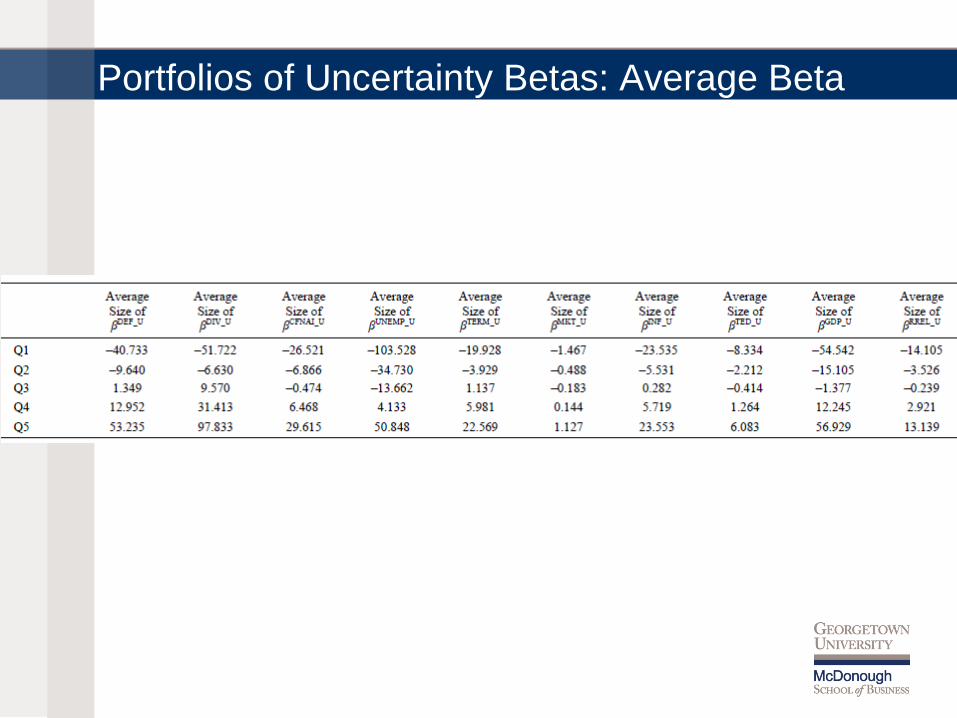

Portfolios of Uncertainty Betas: Average Beta

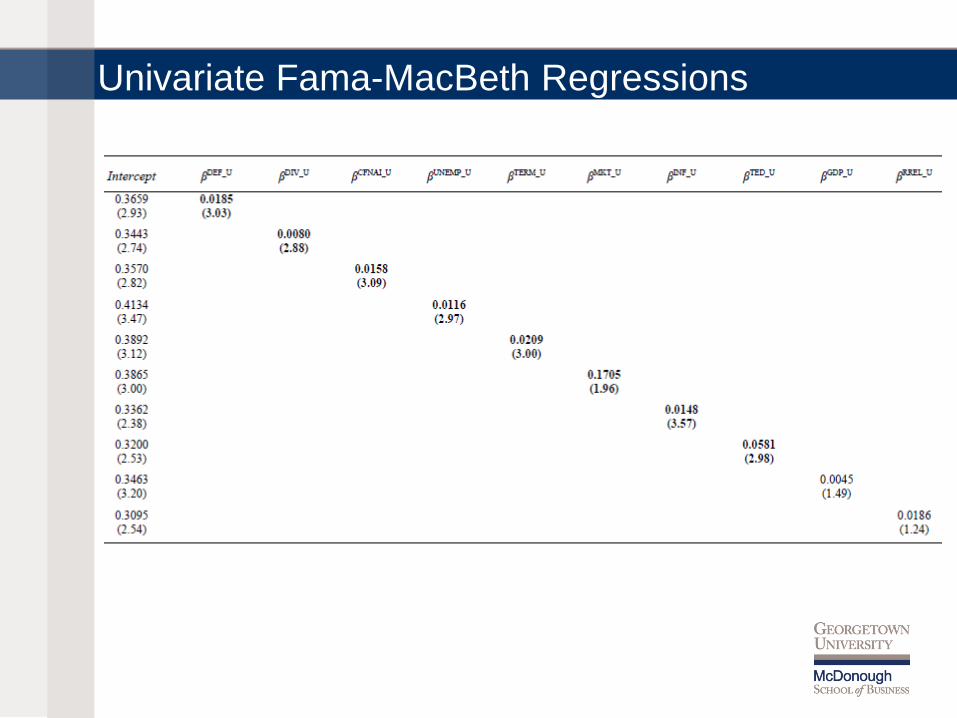

Univariate Fama-MacBeth Regressions

Multivariate Fama-MacBeth Regressions

Subsample Analysis

Subsample Analysis

Subsample Analysis

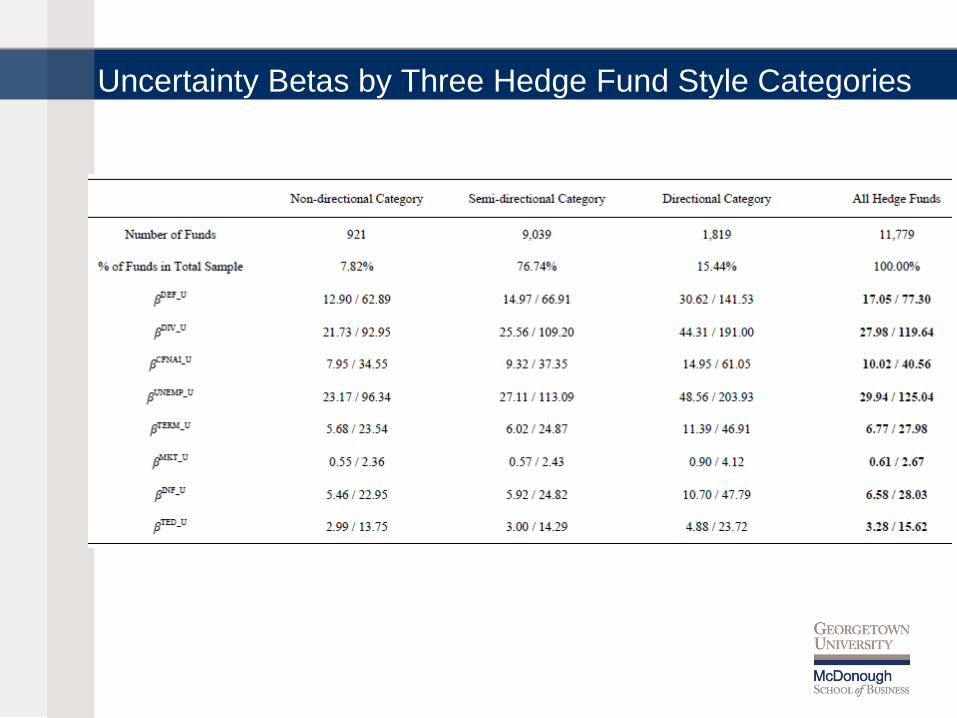

Uncertainty Betas by Three Hedge Fund Style Categories

Portfolios of Uncertainty Betas by Three Hedge Fund Styles

Portfolios of Uncertainty Betas by Three Hedge Fund Styles

Canonical Correlation Analysis

• We construct univariate measures of hedge fund-related economic

uncertainty by considering the portfolio returns of 11 hedge fund investment

styles, and the 10 measures of economic uncertainty.

• We then generate a linear combination of the 11 hedge fund portfolio

investment style returns and a linear combination of the 10 economic

uncertainty factors which leads to the highest correlation between these two.

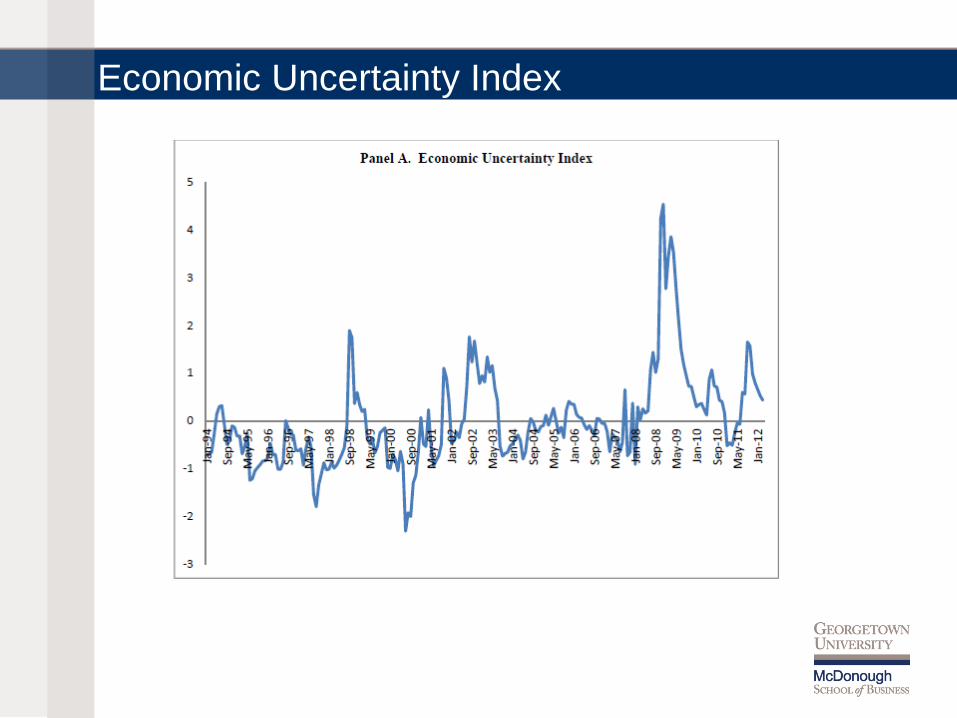

• Economic Uncertainty Index: A univariate index of hedge fund-related

economic uncertainy (the linear combination of economic uncertainty factors)

• Hedge Fund Index: A univariate index of economic uncertainty-related hedge

fund investment style portfolio returns (the linear combination of hedge fund

style index returns)

Economic Uncertainty Index

Hedge Fund Index

Canonial Correlation Analysis

Economic Uncertainty Index Beta

• After building the two univariate indices of economic uncertainty, we test their

performance in predicting the cross-sectional variation in hedge fund returns.

• The results indicate a positive and significant relation between exposures to

the newly proposed economic uncertainty index and future fund returns.

• Funds in the highest economic uncertainty index beta quintile generate 6%

higher annual returns and alphas than do funds in the lowest economic

uncertainty index beta quintile.

Survey of Professional Forecasters

• The Federal Reserve Bank of Philadelphia releases measures of cross-

sectional forecast dispersion for the Survey of Professional Forecasters.

• The cross-sectional forecast dispersion measures the degree of

disagreement among the expectations of different forecasters.

• We use measures of cross-sectional dispersion for quarterly forecasts for the

U.S. gross domestic product (GDP), industrial production (IP), and inflation

rate (INF).

Survey of Professional Forecasters

• These measures are the percent difference between the 75th percentile and

the 25th percentile (the interquartile range) of the projections for the quarterly

level:

Survey of Professional Forecasters

Survey of Professional Forecasters

Conclusion

• Earlier studies have so far paid no attention to the distinction between risk

and uncertainty in the cross-sectional pricing of individual hedge funds.

• We contribute to the literature by examining the relative performance of

hedge funds’ exposures to risk and uncertainty factors in terms of their ability

to explain cross-sectional differences in hedge fund returns.

• In the literature, this is the first sensitivity analysis of expected future hedge

fund returns to loadings on economic uncertainty.

Conclusion

• Consistent with the market-timing ability of hedge funds, our results

suggest that by predicting fluctuations of financial and economic

variables, fund managers can adjust their portfolio exposures up or

down in a timely fashion to generate superior returns.

• We find that hedge funds following directional and semi-directional

trading strategies correctly adjust their aggregate exposure to

economic uncertainty, and hence there exists a positive and stronger

link between their uncertainty beta and future returns.

• However, the cross-sectional relation between uncertainty beta and

future returns is relatively weaker or insignificant for the funds

following non-directional strategies.

3-month ahead predictability

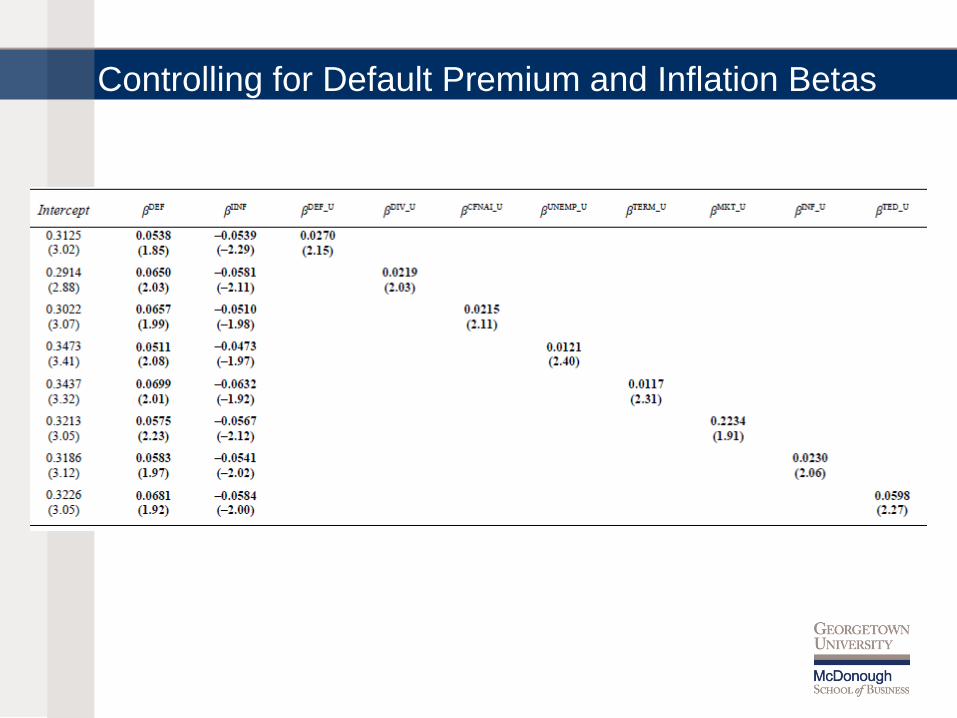

Controlling for Default Premium and Inflation Betas