economic challenges and opportunities sa will be facing over the next 5 years

TRANSCRIPT

Challenges & Opportunities Manufacturing and Economic Growth Outlook

www.frost.com [email protected]

[email protected] www.frost.com

AGENDA

1) INTRODUCTION

Overview

Key influencers, challenges and enablers

2) MACROECONOMIC OVERVIEW

External influencers and challenges

3) DOMESTIC ECONOMY

Growth trajectory

Key domestic influencers to manufacturing sector – supply & demand factors

Manufacturing sector growth

4) GROWTH DRIVERS AND OPPORTUNITIES IN AFRICA

Realistic expectations

Explore growth & key enablers

Where do the opportunities lie

Craig Parker

Programme Manager,

Mobility

Africa

External Influences:

Macroeconomic Overview

[email protected] www.frost.com

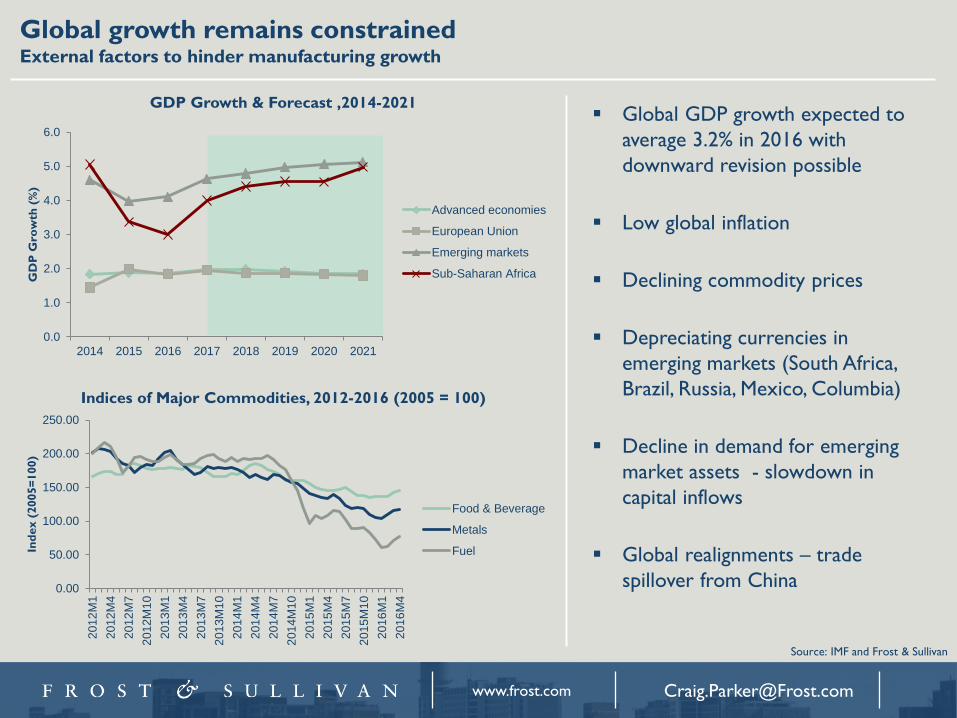

Global growth remains constrained External factors to hinder manufacturing growth

Global GDP growth expected to

average 3.2% in 2016 with

downward revision possible

Low global inflation

Declining commodity prices

Depreciating currencies in

emerging markets (South Africa,

Brazil, Russia, Mexico, Columbia)

Decline in demand for emerging

market assets - slowdown in

capital inflows

Global realignments – trade

spillover from China 0.00

50.00

100.00

150.00

200.00

250.00

201

2M

1

201

2M

4

201

2M

7

201

2M

10

201

3M

1

201

3M

4

201

3M

7

201

3M

10

201

4M

1

201

4M

4

201

4M

7

201

4M

10

201

5M

1

201

5M

4

201

5M

7

201

5M

10

201

6M

1

201

6M

4

Ind

ex (

2005=

100)

Food & Beverage

Metals

Fuel

Indices of Major Commodities, 2012-2016 (2005 = 100)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2014 2015 2016 2017 2018 2019 2020 2021

GD

P G

row

th (

%)

Advanced economies

European Union

Emerging markets

Sub-Saharan Africa

GDP Growth & Forecast ,2014-2021

Source: IMF and Frost & Sullivan

[email protected] www.frost.com

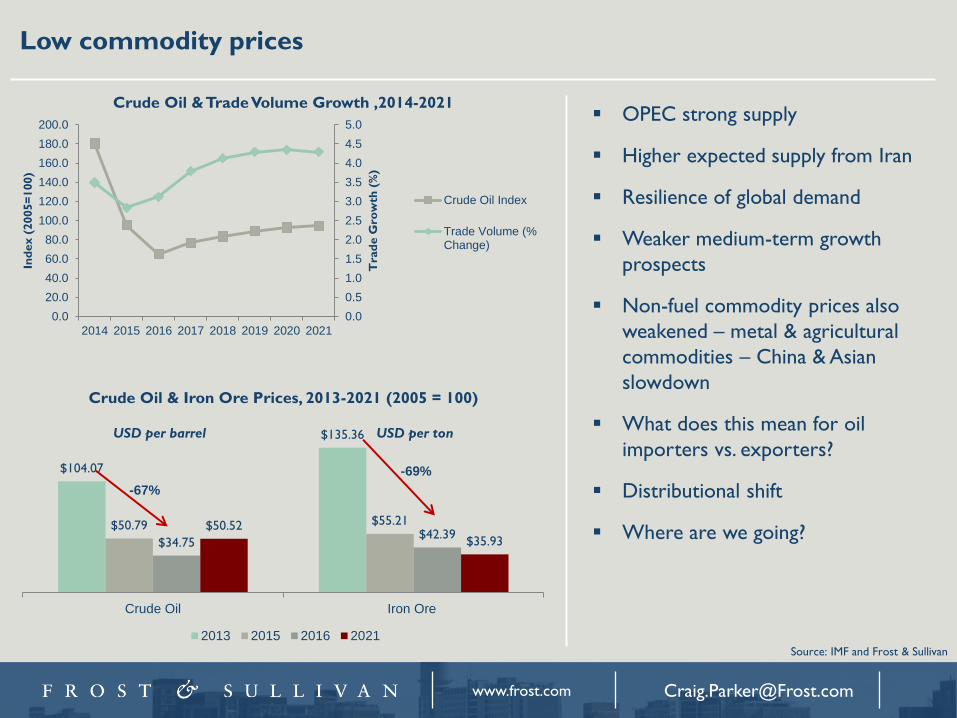

Low commodity prices

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

2014 2015 2016 2017 2018 2019 2020 2021

Tra

de G

row

th (

%)

Ind

ex (

2005=

100)

Crude Oil Index

Trade Volume (%Change)

OPEC strong supply

Higher expected supply from Iran

Resilience of global demand

Weaker medium-term growth

prospects

Non-fuel commodity prices also

weakened – metal & agricultural

commodities – China & Asian

slowdown

What does this mean for oil

importers vs. exporters?

Distributional shift

Where are we going?

Source: IMF and Frost & Sullivan

$104.07

$135.36

$50.79 $55.21

$34.75 $42.39

$50.52

$35.93

Crude Oil Iron Ore

2013 2015 2016 2021

USD per barrel USD per ton

Crude Oil & Trade Volume Growth ,2014-2021

Crude Oil & Iron Ore Prices, 2013-2021 (2005 = 100)

-67%

-69%

[email protected] www.frost.com

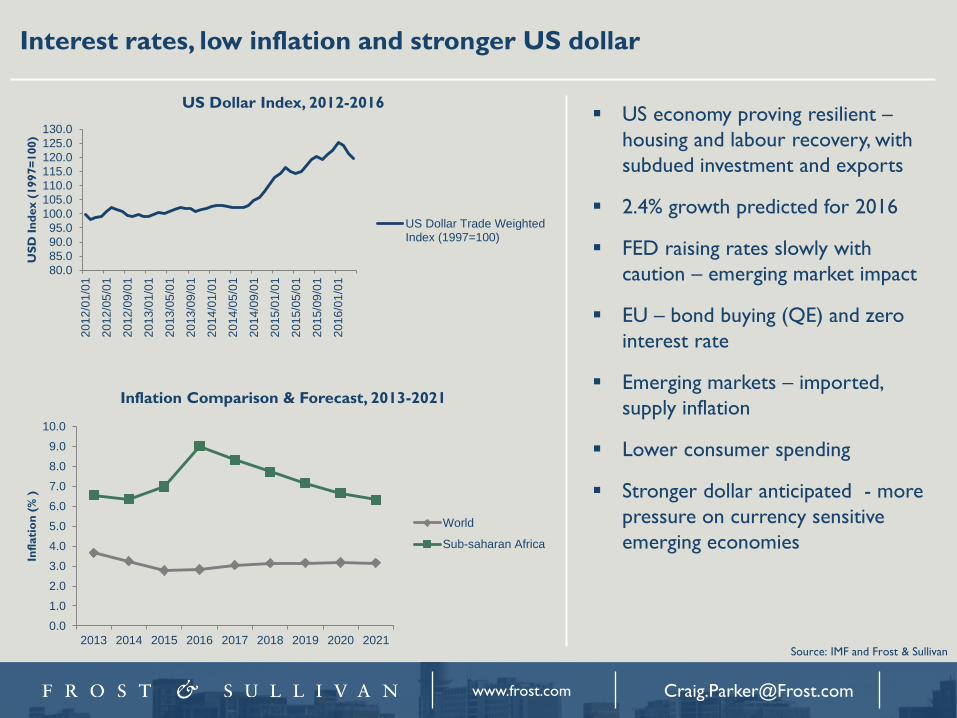

Interest rates, low inflation and stronger US dollar

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

125.0

130.0

201

2/0

1/0

1

201

2/0

5/0

1

201

2/0

9/0

1

201

3/0

1/0

1

201

3/0

5/0

1

201

3/0

9/0

1

201

4/0

1/0

1

201

4/0

5/0

1

201

4/0

9/0

1

201

5/0

1/0

1

201

5/0

5/0

1

201

5/0

9/0

1

201

6/0

1/0

1

US

D I

nd

ex (

1997=

100)

US Dollar Trade WeightedIndex (1997=100)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2013 2014 2015 2016 2017 2018 2019 2020 2021

Infl

ati

on

(%

)

World

Sub-saharan Africa

Source: IMF and Frost & Sullivan

US Dollar Index, 2012-2016

Inflation Comparison & Forecast, 2013-2021

US economy proving resilient –

housing and labour recovery, with

subdued investment and exports

2.4% growth predicted for 2016

FED raising rates slowly with

caution – emerging market impact

EU – bond buying (QE) and zero

interest rate

Emerging markets – imported,

supply inflation

Lower consumer spending

Stronger dollar anticipated - more

pressure on currency sensitive

emerging economies

[email protected] www.frost.com

Trade spillover and China correction

Correction after rapid growth –

heavy investment in public

infrastructure & manufacturing

Nature of industries built

contributed to slowdown

Structural nature – long term

growth a function of labour, capital

and productivity

Working age pop peaked in 2012

Investment peaked (49% of GDP)

Tech gap decreasing

Drivers of slowdown:

Debt – 250% of GDP – 100%

increase since 2008 – housing

sector slowdown (25% of GDP)

Global manufacturing slowdown –

59% GDP contribution

Steel commodity prices –

automotive sector slow

7.7%

6.9% 6.5%

6.2%

2.6%

1.4% 1.8% 2.0%

2012 2015 2016 2017

GDP Growth

Inflation

China GDP Growth & Inflation, 2012-2017

46.5%

41.8%

37.0%

2012 2016 2021

Investment (% of GDP)

China Investment Outlook, 2012-2021

Source: IMF and Frost & Sullivan

[email protected] www.frost.com

Macroeconomic outlook

1.8%

1.9%

2010-2015 Average 2016-2021 Average

Advanced economies

1.2%

1.9%

2010-2015 Average 2016-2021 Average

European Union

7.4%

6.3%

2010-2015 Average 2016-2021 Average

Emerging and developing Asia

5.4%

5.2%

2010-2015 Average 2016-2021 Average

ASEAN-5

3.0%

1.9%

2010-2015 Average 2016-2021 Average

Latin America and the Caribbean

3.6%

3.4%

2010-2015 Average 2016-2021 Average

Middle East and North Africa

4.9%

4.2%

2010-2015 Average 2016-2021 Average

Sub-Saharan Africa Note: Indonesia, Malaysia, the Philippines, Singapore and

Thailand

Why growth slowing in emerging markets? Subdued investment

Risk aversion

Geopolitical tensions

Commodity ‘super-cycle’ & trade spillover from China

Currency pressure: Developed stronger, developing weaker with capital

flow constraints Source: IMF and Frost & Sullivan

Local Influences: Domestic

Economy, Policy &

Investment

[email protected] www.frost.com

Domestic Influences to South Africa’s Economy

Political risk and uncertainty

Greatest threat to economic stability>

rand volatility

Rand volatility linked to uncertainty and

risk aversion

Growth outlook remains uncertain

Ratings important to investors –

Standard & Poor’s and Fitch to release

reviews in June. Moody’s left rating at

Baa2 – 2 levels above sub-investment

grade

FDI in 2015

Developed economies up to

$963b (2nd highest level)

EU gained traction

US at $384b highest since 2000

Developing Asia rose by 15% to

$548b

Africa declined by 31% to $38b:

Nigeria (-27%), Mozambique (-

21%)

South Africa dramatic decline, 74%

to $1.5b

2.22% 2.21%

1.55%

1.28%

0.61%

1.21%

2.06%

2.40% 2.40% 2.40%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

South Africa Growth Outlook (GDP), 2012-2021

R10.00

R11.00

R12.00

R13.00

R14.00

R15.00

R16.00

R17.00

South Africa Exchange Rate, 2012-2021

Source: IMF and Frost & Sullivan

[email protected] www.frost.com

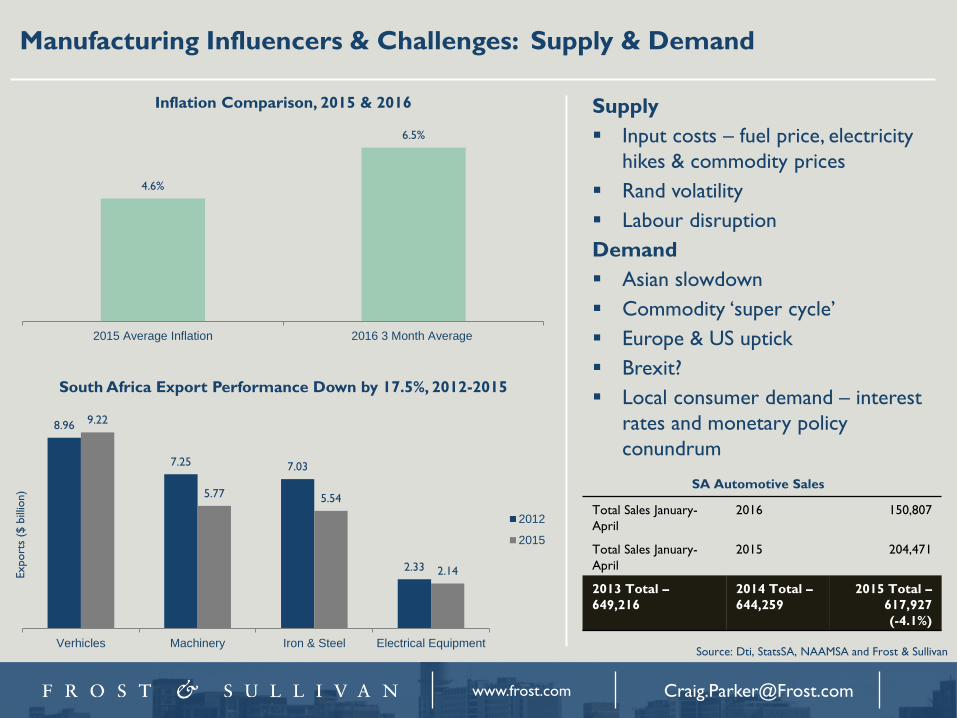

Manufacturing Influencers & Challenges: Supply & Demand

4.6%

6.5%

2015 Average Inflation 2016 3 Month Average

South Africa Export Performance Down by 17.5%, 2012-2015

Inflation Comparison, 2015 & 2016 Supply

Input costs – fuel price, electricity

hikes & commodity prices

Rand volatility

Labour disruption

Demand

Asian slowdown

Commodity ‘super cycle’

Europe & US uptick

Brexit?

Local consumer demand – interest

rates and monetary policy

conundrum

Total Sales January-

April

2016 150,807

Total Sales January-

April

2015 204,471

2013 Total –

649,216

2014 Total –

644,259

2015 Total –

617,927

(-4.1%)

SA Automotive Sales

8.96

7.25 7.03

2.33

9.22

5.77 5.54

2.14

Verhicles Machinery Iron & Steel Electrical Equipment

2012

2015

Export

s ($

bill

ion)

Source: Dti, StatsSA, NAAMSA and Frost & Sullivan

[email protected] www.frost.com

Manufacturing Sector Growth Enablers

Rand depreciation for export

competitiveness?

Feedback mechanism was not

working

Improved demand from Europe

Shift in export dependence &

diversification of markets to Africa

Macroeconomic challenges, but

small scale business has

opportunities – business incubation

and World Bank view on Africa

Value chain enhancement and

SMME involvement in larger value

chains – SEZ’s

Possible small business incubation

policy? (Department of Small

Business Development – DSBD) –

R475m from National Budget

South Africa Export Partners, 2011 & 2015

China 12%

United States of

America

7%

Germany 5%

Namibia 4%

Botswana 4% Japan

7%

United Kingdom

4%

India 3%

ROW 54%

China 9%

United States of America

8%

Germany 7%

Namibia

5%

Botswana 5%

Japan

5% United

Kingdom

4%

India 4%

ROW 53%

2011 2015

20

40

60

80

100

120

140

160

MO

012

012

MO

032

012

MO

052

012

MO

072

012

MO

092

012

MO

112

012

MO

012

013

MO

032

013

MO

052

013

MO

072

013

MO

092

013

MO

112

013

MO

012

014

MO

032

014

MO

052

014

MO

072

014

MO

092

014

MO

112

014

MO

012

015

MO

032

015

MO

052

015

MO

072

015

MO

092

015

MO

112

015

MO

012

016

MO

032

016

Ind

ex (

2010 =

100)

Food andbeverages

Basic chemicals

Basic iron andsteel products

GeneralpurposemachineryHouseholdappliances

Electricalmachinery

South Africa Production Indices, 2012-2016

Source: Dti, StatsSA and Frost & Sullivan

Growth Drivers & Opportunities within

Africa

[email protected] www.frost.com

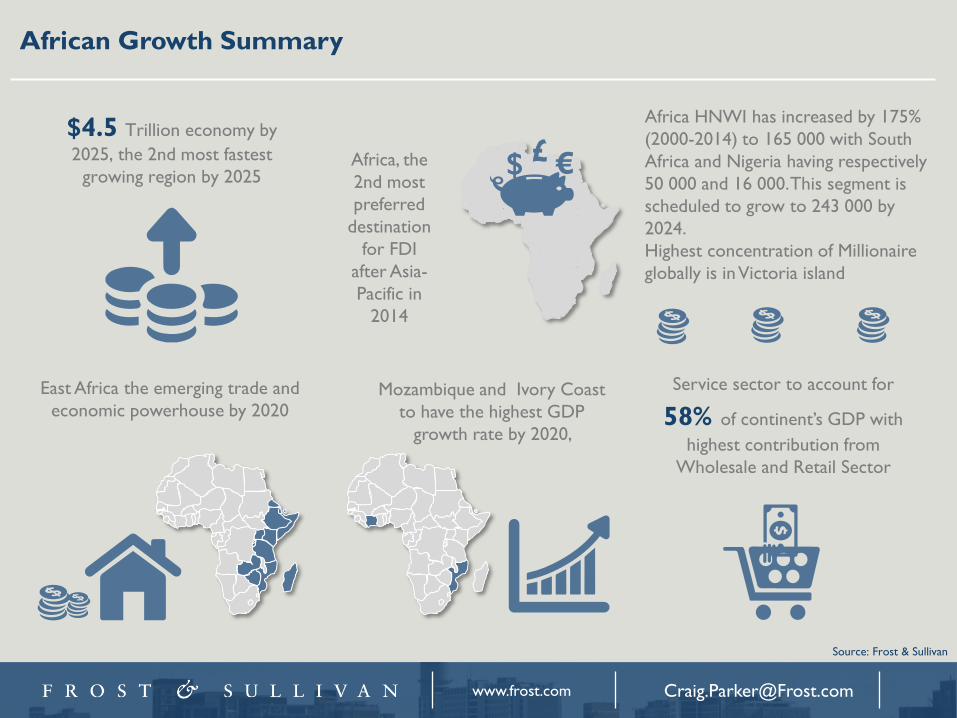

African Growth Summary

Service sector to account for

58% of continent’s GDP with

highest contribution from

Wholesale and Retail Sector

East Africa the emerging trade and

economic powerhouse by 2020 Mozambique and Ivory Coast

to have the highest GDP

growth rate by 2020,

Africa HNWI has increased by 175%

(2000-2014) to 165 000 with South

Africa and Nigeria having respectively

50 000 and 16 000. This segment is

scheduled to grow to 243 000 by

2024.

Highest concentration of Millionaire

globally is in Victoria island

$4.5 Trillion economy by

2025, the 2nd most fastest

growing region by 2025 Africa, the

2nd most

preferred

destination

for FDI

after Asia-

Pacific in

2014

$ € £

Source: Frost & Sullivan

[email protected] www.frost.com

The Urbanization of Africa and the Development of Smart Cities Almost Half of the African Population is Expected to Be Living in Urban Areas by 2025

Rising Urban Population Proportion (% of total

population) across Africa, 2000, 2014, 2025

AFRICA

34.5

40.0

44.9

Western Africa

34.7

41.4

51.4

Southern Africa

53.8 61.2

66.1

Eastern Africa

25.2 30.3

20.6

48.4 51.4

54.3

Northern Africa

Middle Africa

36.8

43.5 49.0

Cairo, Egypt

2000

2014

2025

Megacities

Lagos,

Nigeria

Kinshasa, Congo

Source: Frost & Sullivan

Africa is expected to get 5 smart cities by 2030 and a

consolidated investment of $59.8billion through PPP funding.

Rwanda

Smart

City

$10 Billion

(2013–

2018)

Modderfont

ein Smart

City

$7 Billion

(2014–2030)

Konza

Techno City

$14.5 Billion

(2010–2030)

Hope City,

Ghana

$10 Billion

(2013–2023)

Abuja

Centenary

City

$18.3 Billion

(2013–2018)

[email protected] www.frost.com

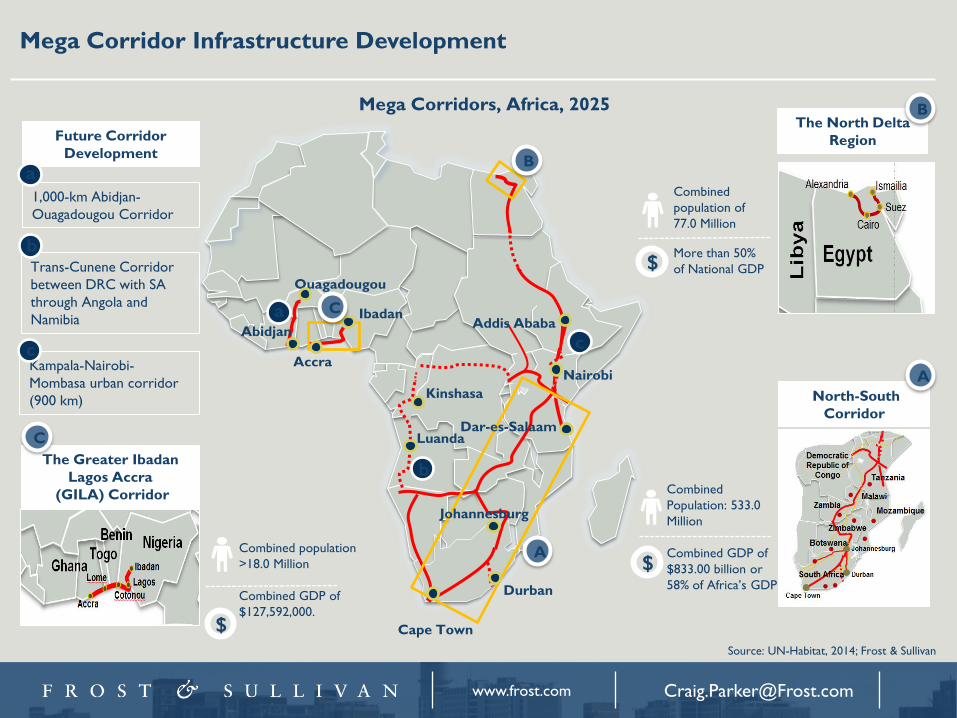

Mega Corridor Infrastructure Development

Source: UN-Habitat, 2014; Frost & Sullivan

Combined population

>18.0 Million

Combined GDP of

$127,592,000.

North-South

Corridor

The Greater Ibadan

Lagos Accra

(GILA) Corridor

The North Delta

Region

Combined

Population: 533.0

Million

Combined GDP of

$833.00 billion or

58% of Africa’s GDP

More than 50%

of National GDP

Abidjan

Ouagadougou

Ibadan

Accra

Luanda

Kinshasa

Cape Town

Durban

Johannesburg

Dar-es-Salaam

Nairobi

Addis Ababa

A

Future Corridor

Development

1,000-km Abidjan-

Ouagadougou Corridor

Trans-Cunene Corridor

between DRC with SA

through Angola and

Namibia

Kampala-Nairobi-

Mombasa urban corridor

(900 km)

A

B

B

C

C

a

Mega Corridors, Africa, 2025

$

Combined

population of

77.0 Million

$

$

b

c

a

b

c

[email protected] www.frost.com

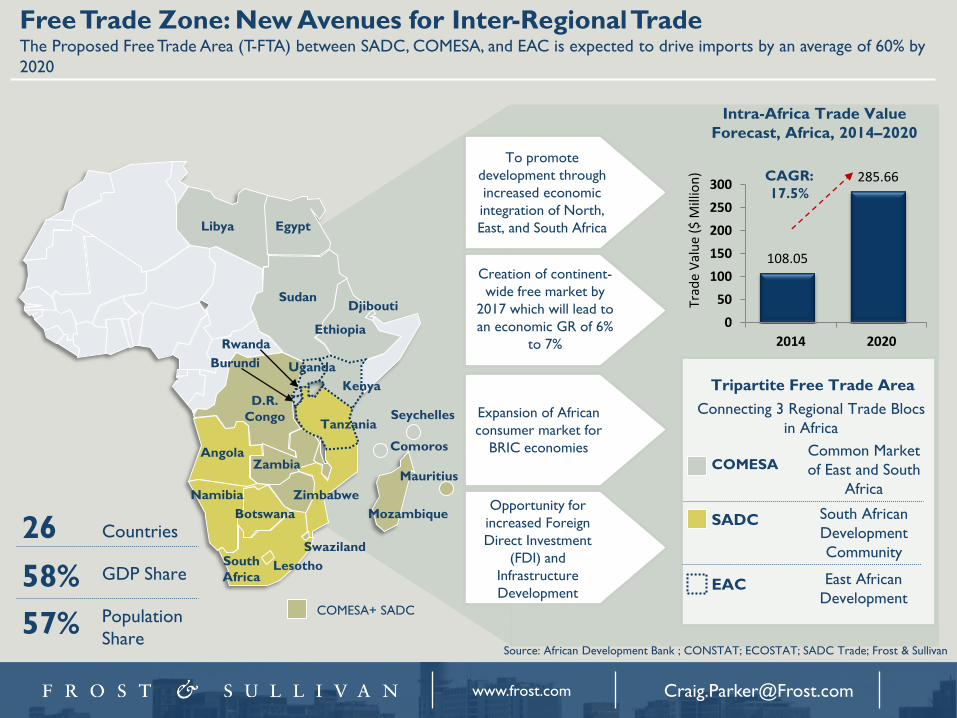

Free Trade Zone: New Avenues for Inter-Regional Trade The Proposed Free Trade Area (T-FTA) between SADC, COMESA, and EAC is expected to drive imports by an average of 60% by

2020

Tripartite Free Trade Area

Connecting 3 Regional Trade Blocs

in Africa

Libya Egypt

Sudan

Ethiopia

Djibouti

Kenya

Uganda

D.R.

Congo Tanzania

Rwanda

Burundi

Angola

Namibia

Botswana

South

Africa Lesotho

Mozambique

Zimbabwe

Zambia

Swaziland

Mauritius

Comoros

Seychelles

COMESA+ SADC

To promote

development through

increased economic

integration of North,

East, and South Africa

Intra-Africa Trade Value

Forecast, Africa, 2014–2020

26

58%

57%

Countries

GDP Share

Population

Share

COMESA

SADC

EAC

Common Market

of East and South

Africa

South African

Development

Community

East African

Development

Creation of continent-

wide free market by

2017 which will lead to

an economic GR of 6%

to 7%

Expansion of African

consumer market for

BRIC economies

Opportunity for

increased Foreign

Direct Investment

(FDI) and

Infrastructure

Development

Source: African Development Bank ; CONSTAT; ECOSTAT; SADC Trade; Frost & Sullivan

108.05

285.66

0

50

100

150

200

250

300

2014 2020

Trad

e V

alu

e ($

Mill

ion

) CAGR:

17.5%

[email protected] www.frost.com

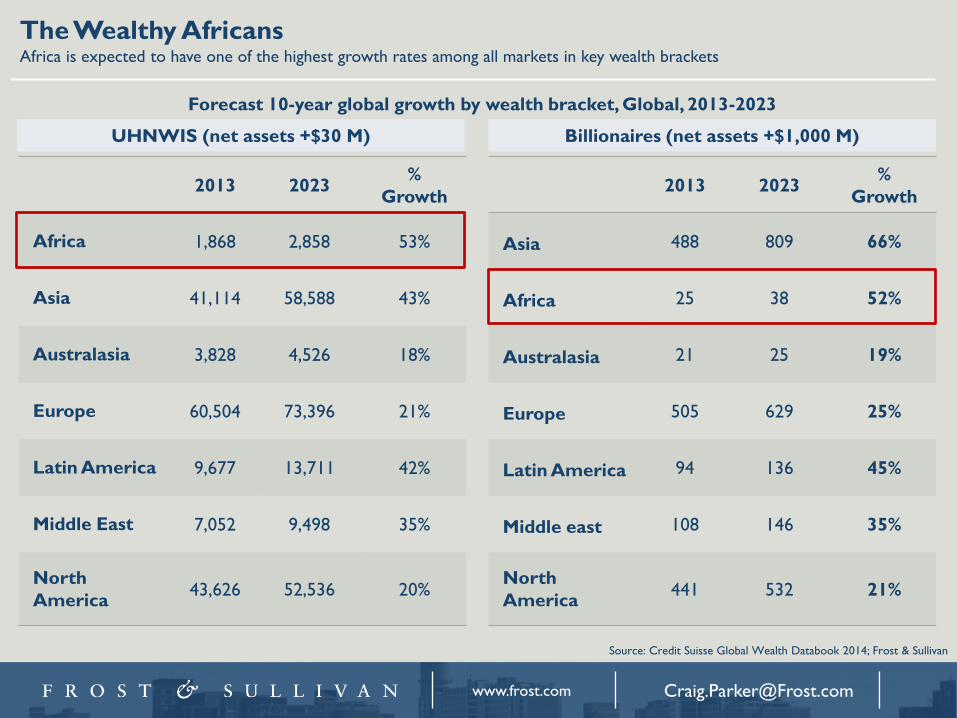

The Wealthy Africans Africa is expected to have one of the highest growth rates among all markets in key wealth brackets

Source: Credit Suisse Global Wealth Databook 2014; Frost & Sullivan

2013 2023 %

Growth

Africa 1,868 2,858 53%

Asia 41,114 58,588 43%

Australasia 3,828 4,526 18%

Europe 60,504 73,396 21%

Latin America 9,677 13,711 42%

Middle East 7,052 9,498 35%

North

America 43,626 52,536 20%

2013 2023 %

Growth

Asia 488 809 66%

Africa 25 38 52%

Australasia 21 25 19%

Europe 505 629 25%

Latin America 94 136 45%

Middle east 108 146 35%

North

America 441 532 21%

UHNWIS (net assets +$30 M) Billionaires (net assets +$1,000 M)

Forecast 10-year global growth by wealth bracket, Global, 2013-2023

[email protected] www.frost.com

Infrastructure Spending Growth Infrastructure gap in SSA to drive infrastructure spending and PPP opportunities in the next decade

• Strong drive to

agricultural development

in Zambia, Kenya and

Nigeria

• 40,000 MW Grand Inga

Hydropower project

(DRC, South Africa)

• Significant gas development in

Mozambique and Nigeria

• Trans-Sahara natural gas

project (Nigeria, Niger,

Algeria)

•Mombasa-Kigali railway and highway (Kenya

and Tanzania)

•North-South Africa corridor (South Africa,

Zambia, Botswana, DRC, Malawi)

• LAPSSET Corridor (Kenya, South Sudan,

Ethiopia)

Nigeria DRC

Ghana

South Africa

Infrastructure spending to

grow by more than 10% annually in SSA to 2025

48 countries in SSA

(population 800 million)

generate the same amount of

power as Spain (population 45

million)

Addressing Africa’s

infrastructure deficit is

estimated at $90bn

new investment per

year till 2025

Kenya

Mozambique

Angola

Key Investment Destinations In SSA, 2015-

2025

Source: Frost & Sullivan

[email protected] www.frost.com

African Airport Infrastructure Development Major developments in air transport infrastructure underway in Africa

Asia Pacific

34.6%

Europe

21.4%

North America

19.4%

Middle East

11.5%

Africa

8.5%

Latin America

4.6%

$467.9 B Global airport infrastructure

investment in on-going

projects

$39.6 B African airport

infrastructure

investment in on-

going projects

Share of Global Airport Infrastructure Investment,

On-going & Planned as of 2015

Source: Frost & Sullivan

[email protected] www.frost.com

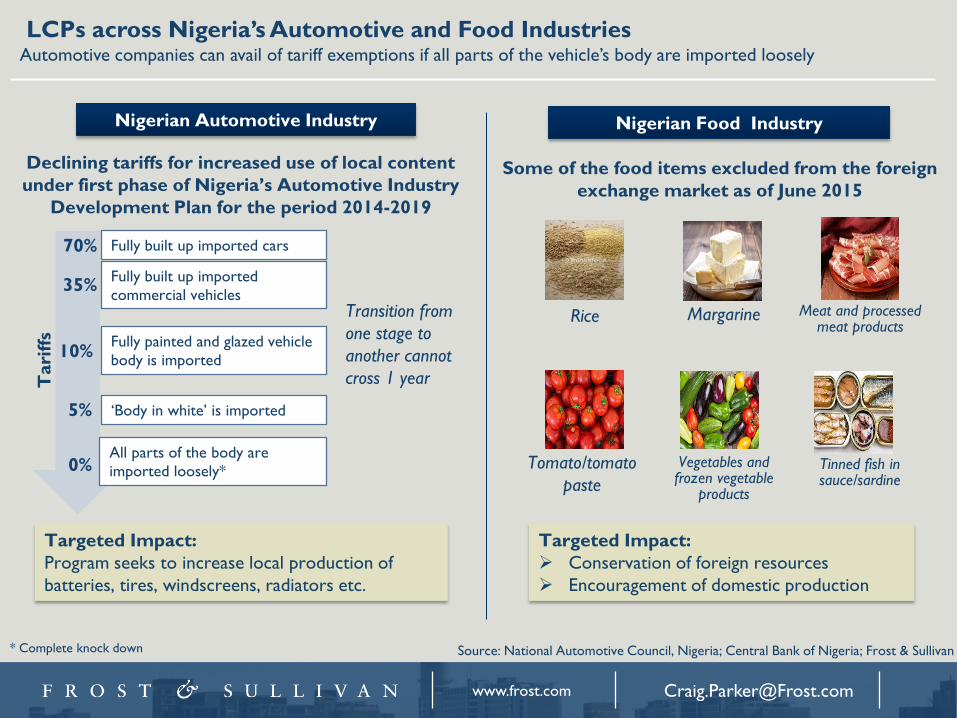

LCPs across Nigeria’s Automotive and Food Industries Automotive companies can avail of tariff exemptions if all parts of the vehicle’s body are imported loosely

Nigerian Automotive Industry Nigerian Food Industry

Declining tariffs for increased use of local content

under first phase of Nigeria’s Automotive Industry

Development Plan for the period 2014-2019

Tari

ffs

Fully built up imported cars

Fully built up imported

commercial vehicles

Fully painted and glazed vehicle

body is imported

‘Body in white’ is imported

All parts of the body are

imported loosely*

Transition from

one stage to

another cannot

cross 1 year

70%

35%

10%

5%

0%

Source: National Automotive Council, Nigeria; Central Bank of Nigeria; Frost & Sullivan

Some of the food items excluded from the foreign

exchange market as of June 2015

* Complete knock down

Targeted Impact:

Conservation of foreign resources

Encouragement of domestic production

Targeted Impact:

Program seeks to increase local production of

batteries, tires, windscreens, radiators etc.

Rice Margarine Meat and processed meat products

Tomato/tomato

paste

Vegetables and frozen vegetable

products

Tinned fish in sauce/sardine

[email protected] www.frost.com

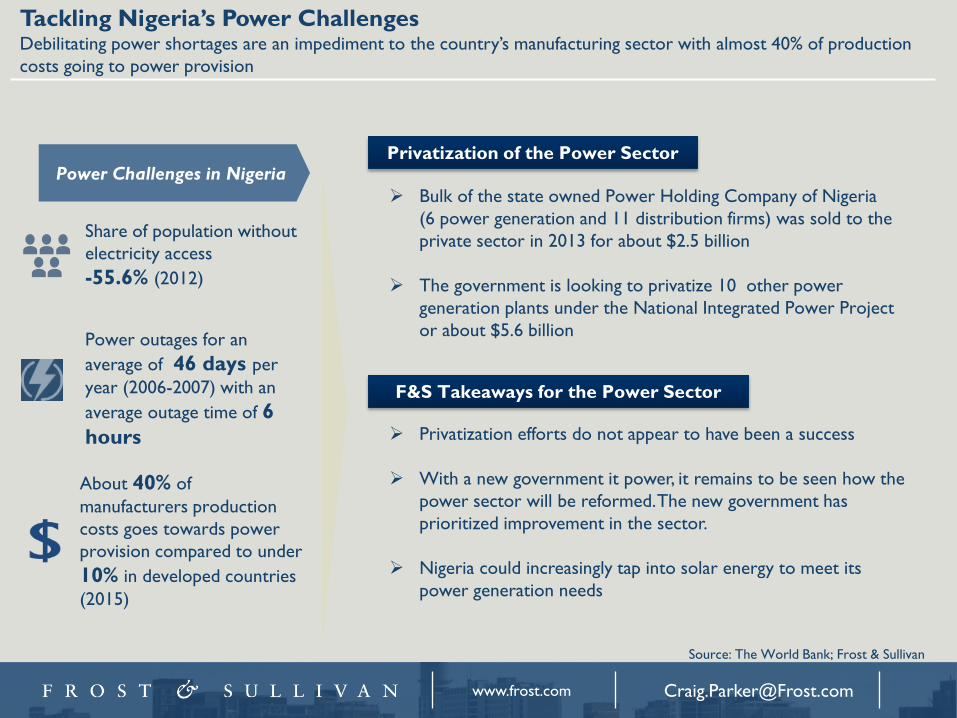

Tackling Nigeria’s Power Challenges Debilitating power shortages are an impediment to the country’s manufacturing sector with almost 40% of production

costs going to power provision

Source: The World Bank; Frost & Sullivan

Power Challenges in Nigeria

Share of population without

electricity access

-55.6% (2012)

Power outages for an

average of 46 days per

year (2006-2007) with an

average outage time of 6

hours

About 40% of

manufacturers production

costs goes towards power

provision compared to under

10% in developed countries

(2015)

Privatization of the Power Sector

Bulk of the state owned Power Holding Company of Nigeria

(6 power generation and 11 distribution firms) was sold to the

private sector in 2013 for about $2.5 billion

The government is looking to privatize 10 other power

generation plants under the National Integrated Power Project

or about $5.6 billion

F&S Takeaways for the Power Sector

Privatization efforts do not appear to have been a success

With a new government it power, it remains to be seen how the

power sector will be reformed. The new government has

prioritized improvement in the sector.

Nigeria could increasingly tap into solar energy to meet its

power generation needs

[email protected] www.frost.com

Africa growth drivers and opportunities – challenges ahead

$645

$383

$138 $164 $150

$40 $108

$811

$408

$241 $249

$168

$91

$199

2010

2014

$373 $410

$342

$295

$157

$276

$66

$533

$470

$410 $393

$316 $279

$119

2010

2014

Nigeria DRC

Ghana

South Africa

Kenya

Mozambique

Angola 3.4%

1.8%

3.4%

6.3%

Ethiopia

6.9%

Tanzania 6.7%

7.5%

3.5% 5.7%

Automotive Exports to Africa, 2010 and 2014 (US$ million)

Machinery Exports to Africa, 2010 and 2014 (US$ million)

Average GDP Growth Forecast, 2016-2021

Source: Trademap, IMF and Frost & Sullivan

Thank you Samantha James

Corporate Communications

Frost & Sullivan Africa

+27 (0) 21 680 3574