e-way bill under gst act - bill new.pdf · e-way bill under gst act suresh aggarwal advocate...

TRANSCRIPT

E-WAY BILL UNDER GST ACT

SURESH AGGARWAL

ADVOCATEMOBILE NO. 9810032846

EMAIL ID: [email protected]

WEBSITE: WWW.SURESHTAXATION.COM

E-WAY BILL RULES 2017

Till such time as an E-Way bill system isdeveloped and approved by the Council,the Government may, by notification,specify the documents that the person incharge of a conveyance carrying anyconsignment of goods shall carry whilethe goods are in movement or in transitstorage.

E-WAY BILL RULES 2017

MeaningThis is an Electronic document generated on theGSTN common portal by the supplier or buyer ortransporter and is required to be carry by the driverwhile moving the goods from one place to anothereither under local act or central act and to beaccompanied along with tax invoice or bill of supplyor delivery challan or debit note etc.

Every Registered person eitherSupplier , or

Buyer, or

Transporter

Who causes movement of goods

1. Supplier in case of supply of goods, or

For reason other than supply either in on self vehicleor hired vehicle through a transporter.

LIABILITY OF THE PERSON TO GENERATE E-WAY BILL

2. Buyer in case of goods purchased at counter ofthe supplier or purchase from unregistereddealers and goods moved either in own vehicleor hired vehicle through transporter.

3. If neither supplier nor buyer then transporteris liable to generate E- Way Bill on the basis ofinvoice and information furnished by suchsupplier or buyer after taken delivery of thegoods for transportation.

LIABILITY OF THE PERSON TO GENERATE E-WAY BILL

E-Way Bill is to be generated on the GSTN common portal byfiling GST INS-01 before the commencement of movement ofgoods if the consignment value 50,000/-.

Form GST INS -01 as two parts known as part A and part B

Part A consist of details in relation to invoice and goods i.e.invoice number, date of invoice, HSN code of the product,description of goods, quantity, rate of tax, value, amount of tax,name , address, and GSTIN of supplier and buyer.

Part B consist of details in respect of transporter i.e. name ,address, GSTIN, mobile number of the transporter, name andmobile number of the driver, vehicle number , place of supplyand address, place of origin and address etc.

WHEN TO GENERATE E-WAY BILL, CONSIGNMENT VALUE AND CONTENTS OF GST INS-01.

Two situation arises for optional generating of E-Way Bills

1. Each Consignment value Rs. 50,000/- or lesser .

2. Movement of goods from unregistered supplier tounregistered buyer (means both areunregistered)

OPTIONAL GENERATING OF E-WAY BILL

1. It applies only for movement of goods means notapplicable where movement of goods notrequired in case of supply of goods.

2. It is applicable for all movement of goods eitherunder local act or under central act.

3. Upon generation of E-Way Bill on the commonportal, a unique E-Way Bill Number (EBN) shallbe made available to the supplier, recipient,transporter on the common portal.

OTHER POINT FOR CONSIDERATION

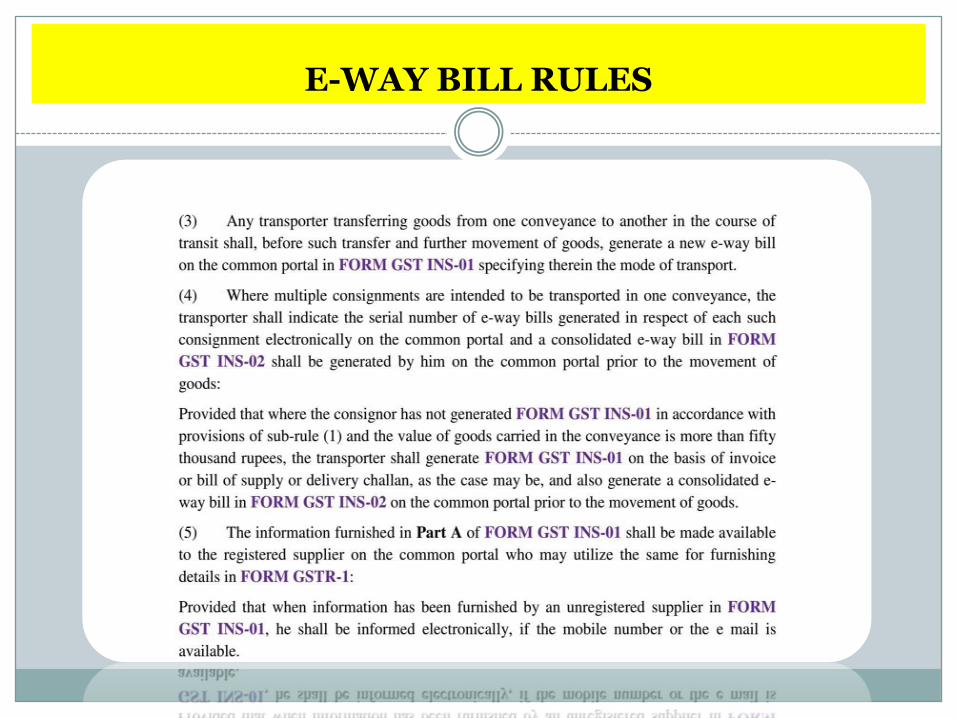

4. Transporter if change the vehicle in transit dueto any reason then he will generate a new E-Way Bill on the common portal in GST INS-01specifying there in the new details of vehiclestransporting the goods.

5. Where multiple consignment are transported inone conveyance then transporter shall generateconsolidated E-Way Bill in FORM GST INS-02which shall include serial number of each E-Way Bill already issued, prior to the movementof goods.

OTHER POINT FOR CONSIDERATION

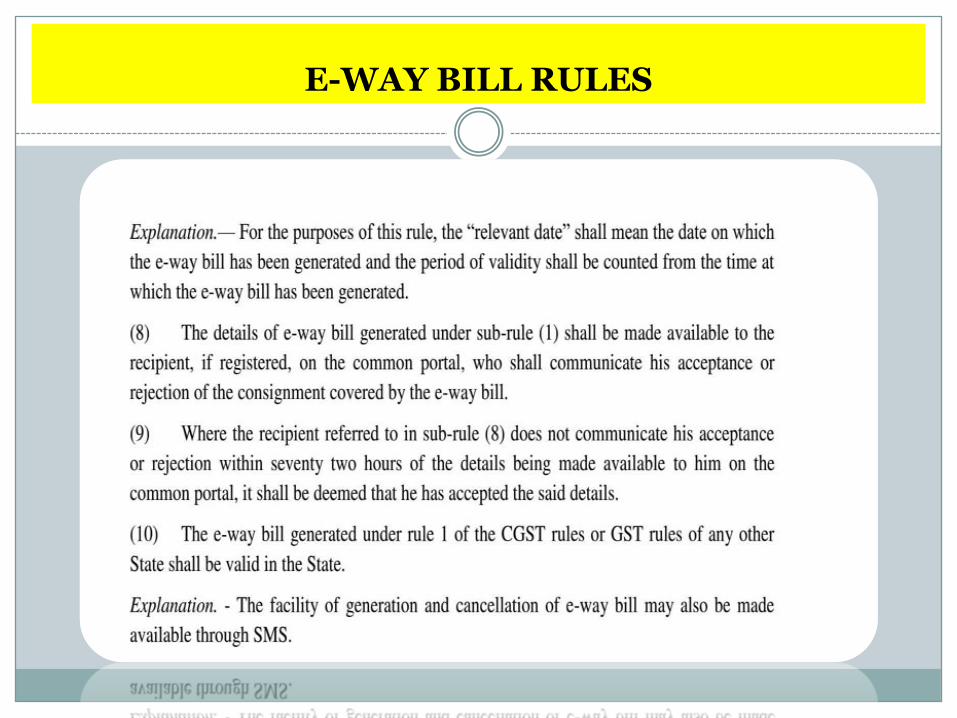

6. The E-Way Bill generated by supplier shall becommunicated to the registered buyer on thecommon portal, who shall communicate eachacceptance or rejection of the consignmentwithin 72 hours otherwise it shall be deemedthat he has accepted the said details.

7. The facility of generation or cancellation of E-Way Bill may also made available through SMS.

OTHER POINT FOR CONSIDERATION

8. The Commissioner may issued a notificationrequiring a class of transporter to obtain a uniqueRFID device and get the said invoice embedded onto the vehicle and mapped the E-Way Bill to theRFID prior to the movement of goods.

9. The Commissioner may issued a notificationrequires the driver to carry the followingdocuments instead of E-Way Bills

a. A Tax Invoice, Bill of supply, Bill of entry, or

b. A delivery Challan where the goods are transportedother than by way of supply.

OTHER POINT FOR CONSIDERATION

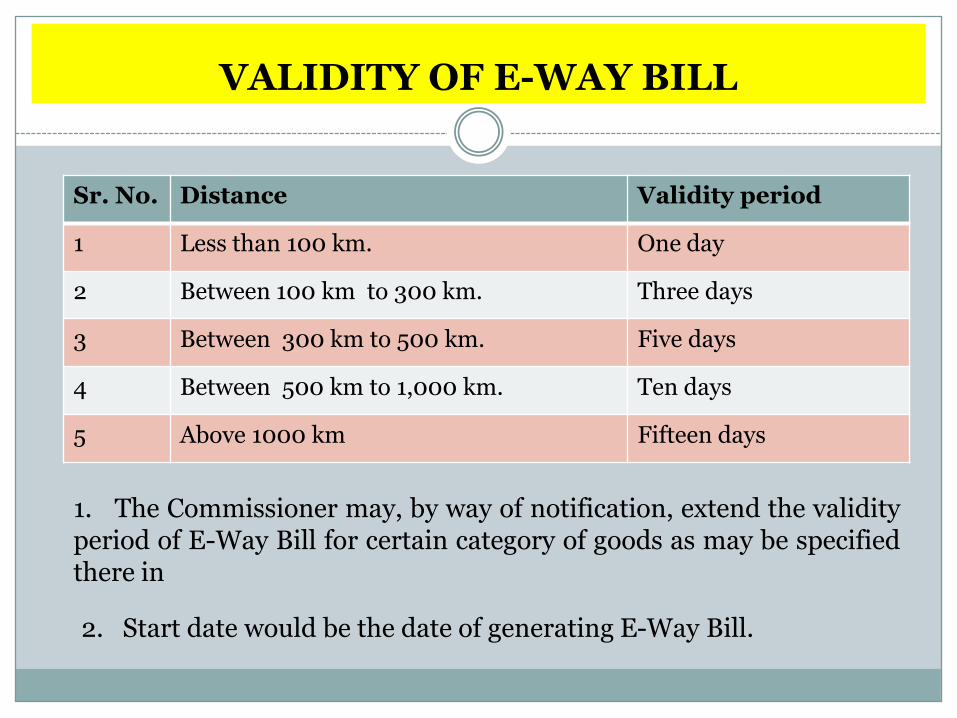

Sr. No. Distance Validity period

1 Less than 100 km. One day

2 Between 100 km to 300 km. Three days

3 Between 300 km to 500 km. Five days

4 Between 500 km to 1,000 km. Ten days

5 Above 1000 km Fifteen days

VALIDITY OF E-WAY BILL

2. Start date would be the date of generating E-Way Bill.

1. The Commissioner may, by way of notification, extend the validityperiod of E-Way Bill for certain category of goods as may be specifiedthere in

CANCELATION OF E-WAY BILL

Where an E-Way Bill has been generating but eitherthe goods not transported or furnish details areincorrect then the said E-Way Bill may be cancelledelectronically on common portal within 24 hours ofgeneration of E-Way Bills by the person who asgenerated the E-Way Bill.

Provided that an E-Way Bill cannot be cancelled if ithas been verified in transit by the transporter whileshifting the goods from one conveyance to anotherin the course of transit.

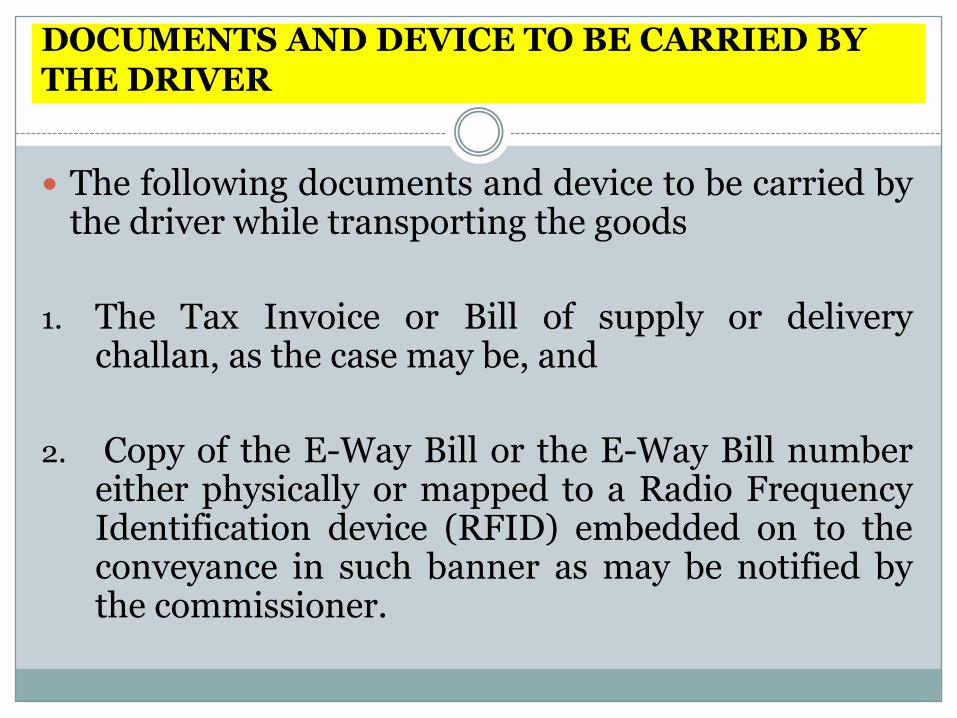

DOCUMENTS AND DEVICE TO BE CARRIED BY THE DRIVER

The following documents and device to be carried bythe driver while transporting the goods

1. The Tax Invoice or Bill of supply or deliverychallan, as the case may be, and

2. Copy of the E-Way Bill or the E-Way Bill numbereither physically or mapped to a Radio FrequencyIdentification device (RFID) embedded on to theconveyance in such banner as may be notified bythe commissioner.

VERIFICATION OF DOCUMENT AND VEHICLE

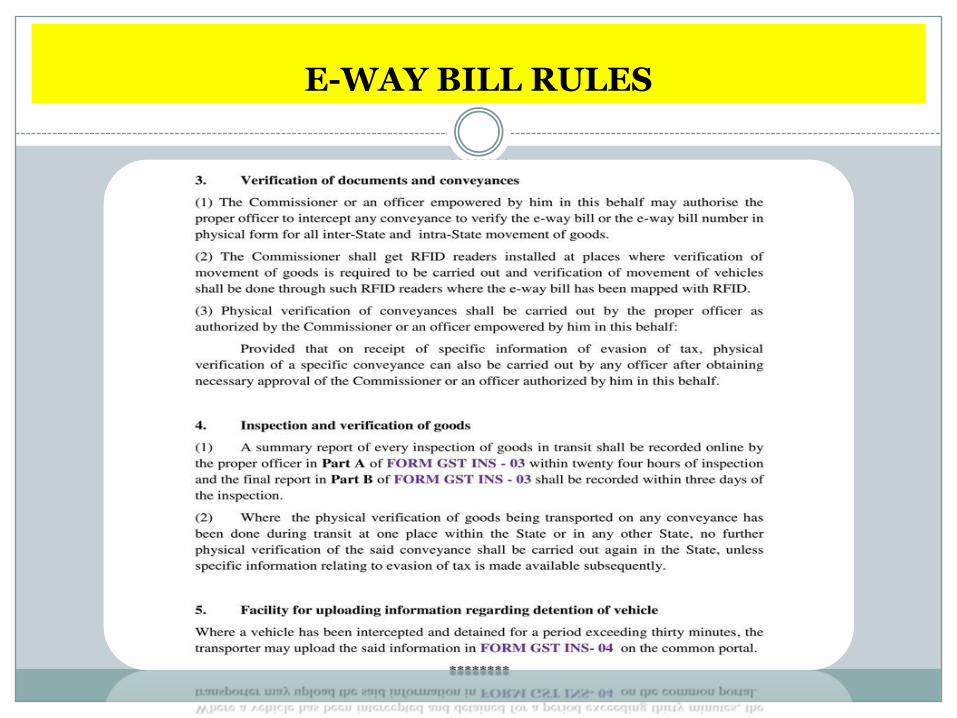

The Commissioner may authorized a proper officer tointercept any vehicle to verified the E-Way Bill for allmovement of goods within local and interstate.

That on receipt of specific information of evasion of tax,physical verification of specific vehicle can also be carriedout by the proper officer after obtaining necessaryapproval of the commissioner for this purpose.

The Commissioner shall arranged to get RFID Readersinstall at places where verification of movement of goodsis required is to be carried out and at such placesverification shall be done through RFID Readers wherethe E-Way Bill has been mapped with RFID.

INSPECTION AND VERIFICATION OF GOODS

The proper officer shall submit a online summaryreport within 4 hours of every inspection in PART-Aof GST INS-03 and shall upload final report inPART-B of GST INS-03 within 3 days of inspectionon the common portal.

Where physical verification of goods beingtransported in any vehicle is carried out at one placein a state the same cannot be verified again in thesame state unless specific information relating toevasion of tax is made available subsequently .

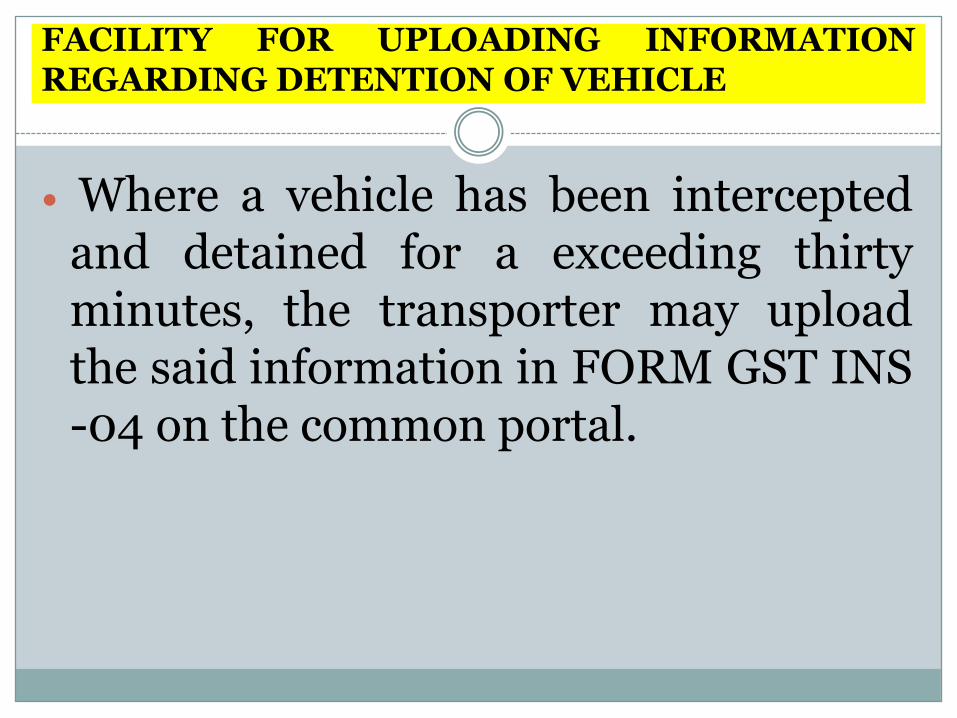

FACILITY FOR UPLOADING INFORMATIONREGARDING DETENTION OF VEHICLE

Where a vehicle has been interceptedand detained for a exceeding thirtyminutes, the transporter may uploadthe said information in FORM GST INS-04 on the common portal.

SURESH AGGARWAL

Any Question Please

SURESH AGGARWAL

MOBILE NO.-9810032846

PPT Available on our website www.sureshtaxation.com

SURESH AGGARWAL

E-WAY BILL RULES

E-WAY BILL RULES

E-WAY BILL RULES

E-WAY BILL RULES

E-WAY BILL RULES

E-WAY BILL RULES

E-WAY BILL RULES