e-payments: cardholder privacy and non-repudiation · number of fraudulent payments made with falsi...

TRANSCRIPT

E-Payments: Cardholder Privacy andNon-Repudiation

David John Boyd

Technical ReportRHUL–MA–2009–2511 January 2010

Department of MathematicsRoyal Holloway, University of LondonEgham, Surrey TW20 0EX, England

http://www.rhul.ac.uk/mathematics/techreports

E-Payments: Cardholder Privacy and

Non-Repudiation

David John Boyd

Thesis submitted to the University of London

for the degree of Doctor of Philosophy

Information Security Group

Department of Mathematics

Royal Holloway, University of London

2009

Declaration

These doctoral studies were conducted under the supervision of Dr. Mick Ganleyand Prof. Chris Mitchell.

The work presented in this thesis is the result of original research carried outby myself, in collaboration with my supervisors, whilst enrolled in the Departmentof Mathematics as a candidate for the degree of Doctor of Philosophy. This workhas not been submitted for any other degree or award in any other university oreducational establishment.

David J. BoydOctober, 2009

2

Abstract

The development of electronic payment cards has been evolutionary, of late pushingto protect the card issuers’ financial interests by counteracting an increase in thenumber of fraudulent payments made with falsified cards. The cardholders havea different emphasis: only to be liable for their own payments and to be able toevidence the payments that they have or have not made. Card payments tendnot to keep the cardholder’s details private, which can facilitate fraud, and it canbe exceedingly difficult for a cardholder to repudiate a completed payment. Thisthesis aims to support cardholders by enhancing their privacy and non-repudiationcapabilities.

This thesis is divided into four parts.

The first part looks at how privacy and non-repudiation fit into the informationsecurity hierarchy, and then the cryptographic mechanisms and algorithms used inthis thesis are described. The widely-used EMV electronic payment card system isreviewed; followed by card-not-present transactions, which are particularly problem-atical.

The main contribution follows where four novel schemes are proposed that pro-vide enhanced privacy and non-repudiation services for both card-present and card-not-present payments. Each of these four categories of payment and security servicerequires its own scheme. Privacy is enhanced by stripping out personally identifi-able information and using a different account number for each transaction. Non-repudiation is enhanced by leaving an electronic footprint after each transaction.

Web payments require particular attention. Banks are adept at authenticatingclients. The third part of this thesis brings together those factors and proposestwo further schemes that provide a single sign-on service to the Web and clientauthentication for the Transport Layer Security communications protocol. The cardissuer provides privacy by vouching that it knows the cardholder and some non-repudiation properties by maintaining an audit trail.

Finally the thesis concludes and outlines some opportunities for further research.

3

Contents

1 Introduction 22

1.1 Motivation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1.2 Main Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

1.3 Structure of Thesis . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

1.4 Scope: E-payments and Payment Cards . . . . . . . . . . . . . . . . 28

I Overview 29

2 Security Building Blocks 30

2.1 Foundation Security Services . . . . . . . . . . . . . . . . . . . . . . 31

2.1.1 Confidentiality . . . . . . . . . . . . . . . . . . . . . . . . . . 31

2.1.2 Integrity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

2.1.3 Availability . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

2.2 Privacy and Non-Repudiation . . . . . . . . . . . . . . . . . . . . . . 33

2.2.1 Privacy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

2.2.2 Non-Repudiation . . . . . . . . . . . . . . . . . . . . . . . . . 40

2.2.3 Authentication . . . . . . . . . . . . . . . . . . . . . . . . . . 44

2.3 Principal Cryptographic Primitives and Constructs . . . . . . . . . . 45

2.3.1 Hash Function . . . . . . . . . . . . . . . . . . . . . . . . . . 45

2.3.2 Symmetric Cryptography . . . . . . . . . . . . . . . . . . . . 46

2.3.3 Message Authentication Code . . . . . . . . . . . . . . . . . . 48

2.3.4 Asymmetric Cryptography . . . . . . . . . . . . . . . . . . . 50

4

CONTENTS

2.3.5 Nonce . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

2.3.6 Pseudorandom Functions . . . . . . . . . . . . . . . . . . . . 53

2.4 Principal Algorithms . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

2.4.1 Data Encryption Standard . . . . . . . . . . . . . . . . . . . 54

2.4.2 RSA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

2.4.3 Secure Hash Algorithm . . . . . . . . . . . . . . . . . . . . . 56

3 Methods of Payment 58

3.1 Cash: The Benchmark . . . . . . . . . . . . . . . . . . . . . . . . . . 59

3.2 EMV . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

3.2.1 Introduction to EMV . . . . . . . . . . . . . . . . . . . . . . 60

3.2.2 EMV Authentication . . . . . . . . . . . . . . . . . . . . . . . 60

3.2.3 EMV Cryptography . . . . . . . . . . . . . . . . . . . . . . . 63

3.3 Card Not Present Payments . . . . . . . . . . . . . . . . . . . . . . . 63

3.3.1 CNP - The Problem . . . . . . . . . . . . . . . . . . . . . . . 64

3.3.2 CNP - Deployed Solutions . . . . . . . . . . . . . . . . . . . . 64

4 Attributes 67

4.1 Privacy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

4.1.1 Anonymity . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

4.1.2 Pseudonymity . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

4.1.3 Unlinkability . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

4.1.4 Unobservability . . . . . . . . . . . . . . . . . . . . . . . . . . 70

4.1.5 Privacy Summary . . . . . . . . . . . . . . . . . . . . . . . . 71

4.2 Non-Repudiation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

4.3 Internet Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

II E-Payment Schemes:

5

CONTENTS

Cardholder Privacy and Non-Repudiation 73

5 Payment Cards: Privacy 74

5.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

5.2 Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

5.3 A Card Not Present Scheme . . . . . . . . . . . . . . . . . . . . . . . 77

5.4 The Proposed Mechanism . . . . . . . . . . . . . . . . . . . . . . . . 78

5.4.1 Anonymity . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

5.4.2 EMV: Anonymity . . . . . . . . . . . . . . . . . . . . . . . . 80

5.4.3 Pseudonymity and Unlinkability . . . . . . . . . . . . . . . . 81

5.4.4 EMV: Pseudonymity and Unlinkability . . . . . . . . . . . . . 83

5.4.5 Effect on Payment Processing Entities . . . . . . . . . . . . . 90

5.5 Residual Threat Analysis . . . . . . . . . . . . . . . . . . . . . . . . 91

5.5.1 Passive Attack . . . . . . . . . . . . . . . . . . . . . . . . . . 92

5.5.2 Active Attack . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

5.5.3 Size of Anonymity Set . . . . . . . . . . . . . . . . . . . . . . 93

5.5.4 Floor Limits . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

5.5.5 Birthday Attack . . . . . . . . . . . . . . . . . . . . . . . . . 95

5.5.6 Issuer Impersonation . . . . . . . . . . . . . . . . . . . . . . . 95

5.5.7 Non-Repudiation . . . . . . . . . . . . . . . . . . . . . . . . . 95

5.5.8 Physical Security . . . . . . . . . . . . . . . . . . . . . . . . . 96

5.5.9 Legal Precedent . . . . . . . . . . . . . . . . . . . . . . . . . 96

5.6 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

6 Payment Cards: Non-Repudiation 99

6.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

6.2 Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

6.3 The Proposed Mechanisms . . . . . . . . . . . . . . . . . . . . . . . . 103

6.3.1 Electronic Receipts . . . . . . . . . . . . . . . . . . . . . . . . 104

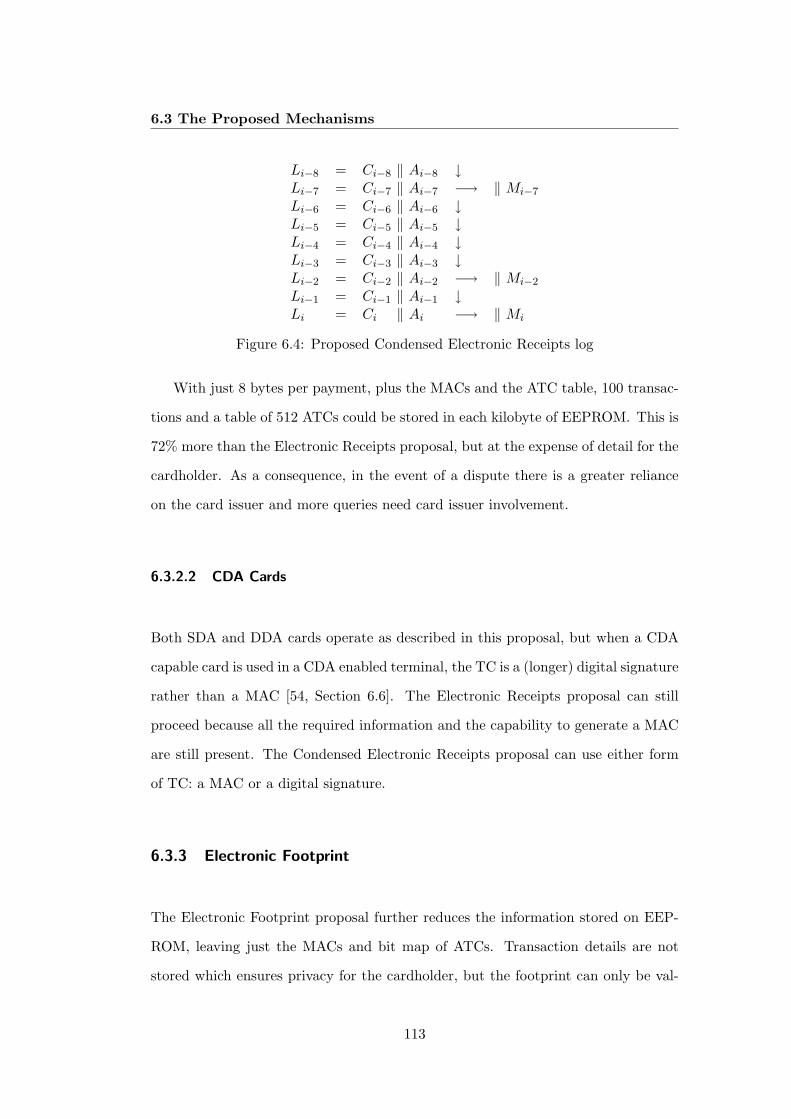

6.3.2 Condensed Electronic Receipts . . . . . . . . . . . . . . . . . 109

6

CONTENTS

6.3.3 Electronic Footprint . . . . . . . . . . . . . . . . . . . . . . . 113

6.4 Privacy and Integrity . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

6.5 Residual Threat Analysis . . . . . . . . . . . . . . . . . . . . . . . . 117

6.5.1 The Evidence Causing Disputes . . . . . . . . . . . . . . . . . 117

6.5.2 Too Much Trust in the System . . . . . . . . . . . . . . . . . 117

6.5.3 Race Conditions . . . . . . . . . . . . . . . . . . . . . . . . . 118

6.5.4 Misplaced Trust . . . . . . . . . . . . . . . . . . . . . . . . . 119

6.5.5 Cardholder Practices . . . . . . . . . . . . . . . . . . . . . . . 120

6.5.6 Inconsistencies Between Statements . . . . . . . . . . . . . . 121

6.6 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121

7 CNP Payments: Privacy 123

7.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

7.2 Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127

7.3 Temporary Card Number Schemes . . . . . . . . . . . . . . . . . . . 128

7.3.1 Controlled Payment Numbers™ . . . . . . . . . . . . . . . . . 128

7.3.2 SecureClick® . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

7.3.3 Rubin and Wright . . . . . . . . . . . . . . . . . . . . . . . . 130

7.3.4 Li and Zhang . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

7.3.5 Assora, Kadirire and Shirvani . . . . . . . . . . . . . . . . . . 134

7.4 The Proposed Mechanism . . . . . . . . . . . . . . . . . . . . . . . . 135

7.4.1 Protecting Identity . . . . . . . . . . . . . . . . . . . . . . . . 136

7.4.2 Allocating Temporary Card Numbers . . . . . . . . . . . . . 137

7.4.3 Allocating a Card Verification Value . . . . . . . . . . . . . . 139

7.4.4 Address Verification . . . . . . . . . . . . . . . . . . . . . . . 142

7.4.5 Operating the Scheme . . . . . . . . . . . . . . . . . . . . . . 144

7.4.6 Privacy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

7.4.7 Non-Repudiation and Other Security Services . . . . . . . . . 147

7.5 Residual Threat Analysis . . . . . . . . . . . . . . . . . . . . . . . . 147

7

CONTENTS

7.5.1 Insufficient TCNs . . . . . . . . . . . . . . . . . . . . . . . . . 148

7.5.2 No TCNs Left on Card . . . . . . . . . . . . . . . . . . . . . 149

7.5.3 Guessing TCNs . . . . . . . . . . . . . . . . . . . . . . . . . . 150

7.5.4 Reduction of Privacy . . . . . . . . . . . . . . . . . . . . . . . 150

7.5.5 Re-use of TCNs . . . . . . . . . . . . . . . . . . . . . . . . . . 150

7.5.6 Cardholder Practices . . . . . . . . . . . . . . . . . . . . . . . 151

7.5.7 Proof of Payment Source . . . . . . . . . . . . . . . . . . . . 151

7.5.8 Merchant Practices . . . . . . . . . . . . . . . . . . . . . . . . 152

7.6 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

8 CNP Payments: Non-Repudiation 154

8.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 155

8.2 Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 156

8.3 Biometrics for Non-Repudiation . . . . . . . . . . . . . . . . . . . . . 157

8.3.1 Which Biometric? . . . . . . . . . . . . . . . . . . . . . . . . 157

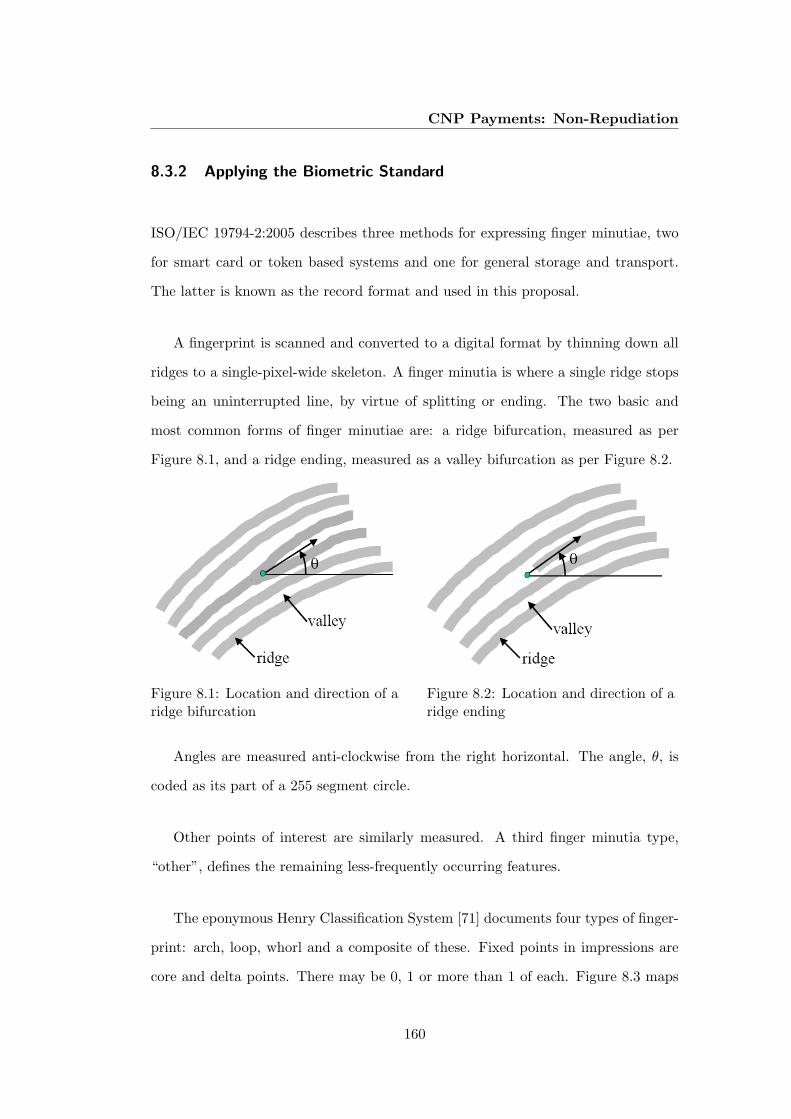

8.3.2 Applying the Biometric Standard . . . . . . . . . . . . . . . . 160

8.4 The Proposed Mechanism . . . . . . . . . . . . . . . . . . . . . . . . 163

8.4.1 The Trusted Third Party . . . . . . . . . . . . . . . . . . . . 163

8.4.2 Calling the TTP Service . . . . . . . . . . . . . . . . . . . . . 164

8.4.3 Processing the Transaction . . . . . . . . . . . . . . . . . . . 165

8.4.4 When There is a Dispute . . . . . . . . . . . . . . . . . . . . 169

8.4.5 Privacy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172

8.5 Residual Threat Analysis . . . . . . . . . . . . . . . . . . . . . . . . 174

8.5.1 Availability of the TTP . . . . . . . . . . . . . . . . . . . . . 174

8.5.2 TTP Impersonation or Interception . . . . . . . . . . . . . . 175

8.5.3 Sensitivity of Biometric Data . . . . . . . . . . . . . . . . . . 176

8.5.4 Integrity of TTP . . . . . . . . . . . . . . . . . . . . . . . . . 177

8.6 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 178

8

CONTENTS

III Web Schemes:

Cardholder Authentication 179

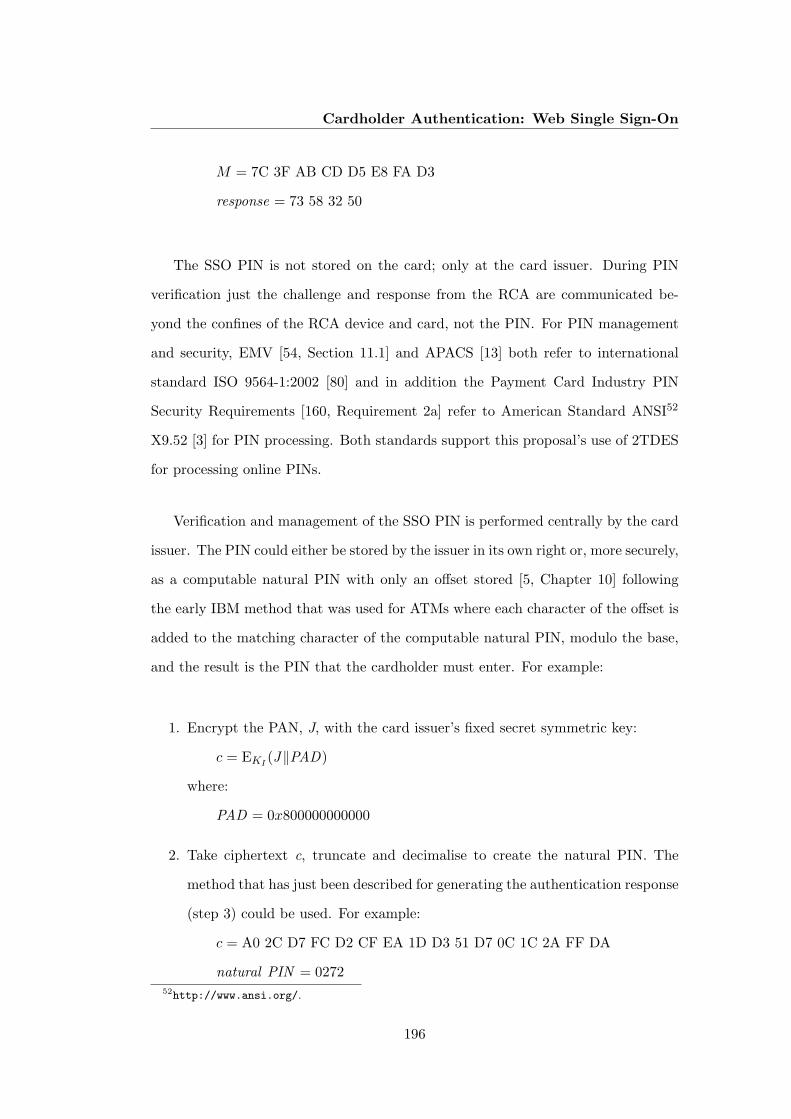

9 Cardholder Authentication: Web Single Sign-On 180

9.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182

9.2 Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 184

9.3 An EMV-Based SSO Scheme . . . . . . . . . . . . . . . . . . . . . . 184

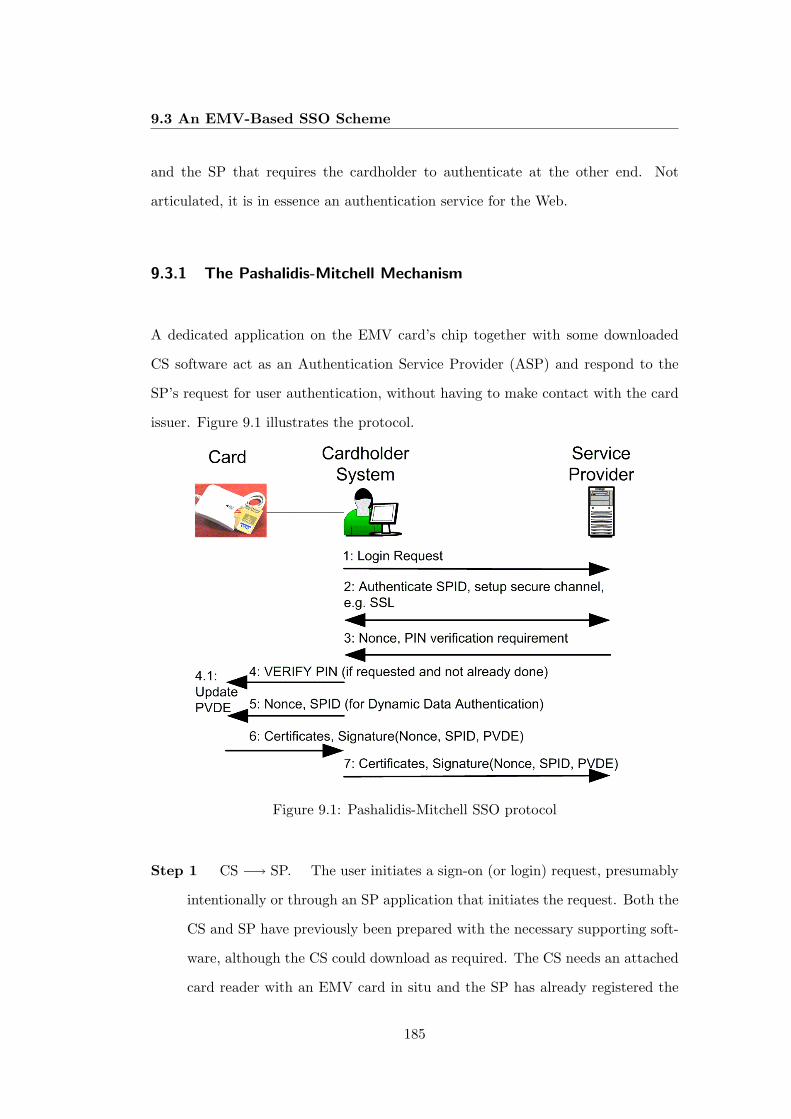

9.3.1 The Pashalidis-Mitchell Mechanism . . . . . . . . . . . . . . 185

9.3.2 Areas for Potential Improvement . . . . . . . . . . . . . . . . 187

9.4 The Proposed Mechanism . . . . . . . . . . . . . . . . . . . . . . . . 191

9.4.1 An Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . 192

9.4.2 The SSO Infrastructure . . . . . . . . . . . . . . . . . . . . . 194

9.4.3 Avoiding Changes to the Card . . . . . . . . . . . . . . . . . 198

9.4.4 SSO User Registration . . . . . . . . . . . . . . . . . . . . . . 198

9.4.5 SSO Operation . . . . . . . . . . . . . . . . . . . . . . . . . . 200

9.4.6 The SSO Protocol . . . . . . . . . . . . . . . . . . . . . . . . 203

9.4.7 CMS Maintenance and Administration . . . . . . . . . . . . . 206

9.5 Residual Threat Analysis . . . . . . . . . . . . . . . . . . . . . . . . 207

9.5.1 Issuer Impersonation or Interception . . . . . . . . . . . . . . 208

9.5.2 Use of Other User’s Attestation . . . . . . . . . . . . . . . . . 208

9.5.3 Cardholder Practices . . . . . . . . . . . . . . . . . . . . . . . 209

9.5.4 Leakage of Information . . . . . . . . . . . . . . . . . . . . . 209

9.5.5 Availability of the Authentication, CMS and NTP Components210

9.5.6 Integrity of the Authentication, CMS and NTP Components 211

9.5.7 Time of Check to Time of Use . . . . . . . . . . . . . . . . . 212

9.5.8 Incomplete Audit Trail . . . . . . . . . . . . . . . . . . . . . . 213

9.5.9 Strength of Response . . . . . . . . . . . . . . . . . . . . . . . 213

9.6 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 213

10 Cardholder Authentication: TLS Client Authentication 215

9

CONTENTS

10.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 217

10.2 Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 219

10.3 Scope . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 220

10.4 The TLS Protocol . . . . . . . . . . . . . . . . . . . . . . . . . . . . 220

10.4.1 The TLS Record Protocol . . . . . . . . . . . . . . . . . . . . 220

10.4.2 The TLS Handshake Protocol . . . . . . . . . . . . . . . . . . 222

10.4.3 Keys and Algorithms . . . . . . . . . . . . . . . . . . . . . . . 225

10.5 The Proposed Mechanism . . . . . . . . . . . . . . . . . . . . . . . . 228

10.5.1 The Extended TLS Handshake Protocol . . . . . . . . . . . . 229

10.5.2 Authenticating the Client . . . . . . . . . . . . . . . . . . . . 233

10.5.3 Other Considerations . . . . . . . . . . . . . . . . . . . . . . 235

10.5.4 Security Services . . . . . . . . . . . . . . . . . . . . . . . . . 236

10.6 Residual Threat Analysis . . . . . . . . . . . . . . . . . . . . . . . . 237

10.6.1 Issuer Impersonation or Interception . . . . . . . . . . . . . . 238

10.6.2 Leakage of Information . . . . . . . . . . . . . . . . . . . . . 239

10.6.3 Financial Exposure . . . . . . . . . . . . . . . . . . . . . . . . 239

10.6.4 Cardholder Practices . . . . . . . . . . . . . . . . . . . . . . . 240

10.6.5 Issuer Availability . . . . . . . . . . . . . . . . . . . . . . . . 240

10.6.6 Changing IP Address . . . . . . . . . . . . . . . . . . . . . . 241

10.6.7 Data on Client and Server . . . . . . . . . . . . . . . . . . . . 241

10.6.8 Time of Check to Time of Use . . . . . . . . . . . . . . . . . 241

10.6.9 Incomplete Audit Trail . . . . . . . . . . . . . . . . . . . . . . 242

10.7 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 242

IV Conclusions 244

11 Conclusions and Further Research 245

11.1 Summary and Conclusions . . . . . . . . . . . . . . . . . . . . . . . . 245

11.2 Opportunities for Further Research . . . . . . . . . . . . . . . . . . . 248

10

CONTENTS

Bibliography 250

11

List of Figures

2.1 Common Criteria privacy class . . . . . . . . . . . . . . . . . . . . . 35

2.2 Common Criteria communication class . . . . . . . . . . . . . . . . . 42

5.1 EMV transaction flow example . . . . . . . . . . . . . . . . . . . . . 79

6.1 Example of EMV log format . . . . . . . . . . . . . . . . . . . . . . . 105

6.2 Proposed Electronic Receipts log . . . . . . . . . . . . . . . . . . . . 105

6.3 Bit map of the ATCs . . . . . . . . . . . . . . . . . . . . . . . . . . . 112

6.4 Proposed Condensed Electronic Receipts log . . . . . . . . . . . . . . 113

6.5 Proposed Electronic Footprint . . . . . . . . . . . . . . . . . . . . . . 114

7.1 Citibank account online: sign-on Web page . . . . . . . . . . . . . . 129

8.1 Location and direction of a ridge bifurcation . . . . . . . . . . . . . . 160

8.2 Location and direction of a ridge ending . . . . . . . . . . . . . . . . 160

8.3 Core and delta fingerprint features . . . . . . . . . . . . . . . . . . . 161

8.4 Fingerprint coordinates . . . . . . . . . . . . . . . . . . . . . . . . . 161

8.5 Calling the TTP with an API . . . . . . . . . . . . . . . . . . . . . . 165

8.6 Calling the TTP with https . . . . . . . . . . . . . . . . . . . . . . . 165

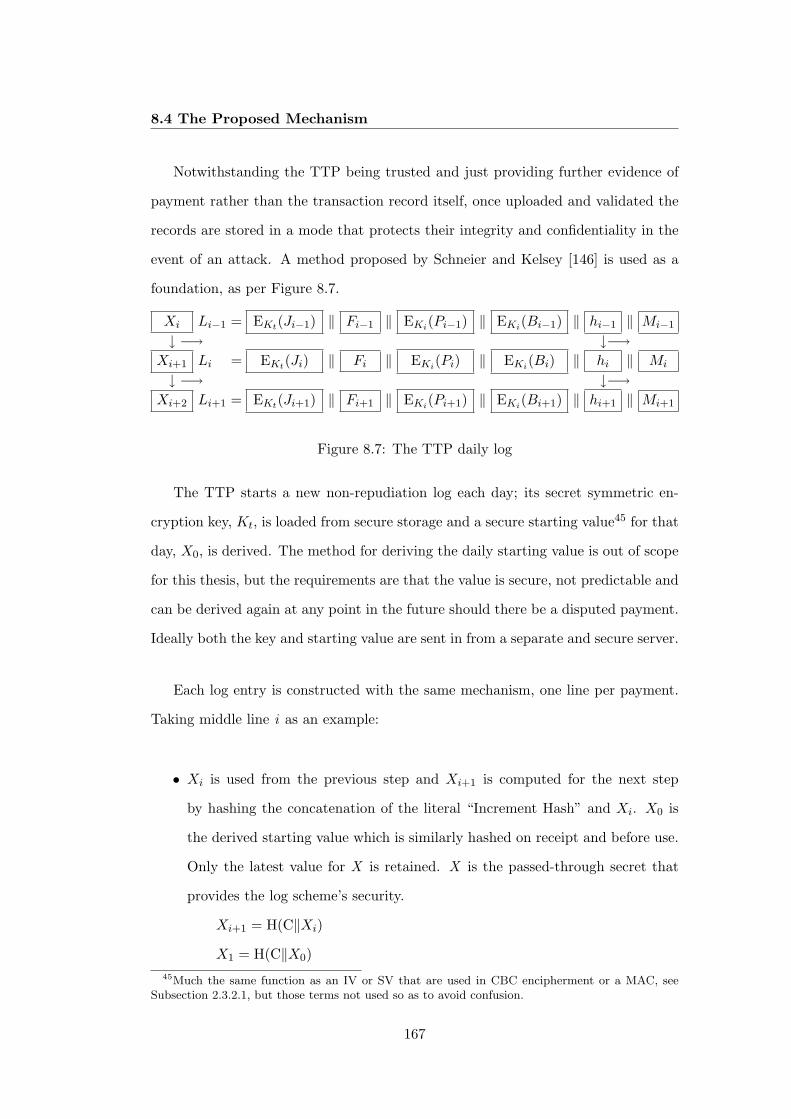

8.7 The TTP daily log . . . . . . . . . . . . . . . . . . . . . . . . . . . . 167

9.1 Pashalidis-Mitchell SSO protocol . . . . . . . . . . . . . . . . . . . . 185

9.2 Participating entities in the enhanced SSO proposal . . . . . . . . . 193

10.1 TLS handshake protocol . . . . . . . . . . . . . . . . . . . . . . . . . 223

12

LIST OF FIGURES

10.2 Extended TLS handshake protocol . . . . . . . . . . . . . . . . . . . 229

13

List of Tables

7.1 Payment card data elements . . . . . . . . . . . . . . . . . . . . . . . 138

8.1 Finger minutia record format . . . . . . . . . . . . . . . . . . . . . . 162

10.1 TLS record layer fields . . . . . . . . . . . . . . . . . . . . . . . . . . 221

14

Acknowledgements

This thesis is the culmination of four years of study which has been both an inter-esting and stimulating experience. It is a stark contrast to my previous 32 years,working in the IT department of a large multinational company. That businessexperience helped me afford to pursue this lifelong ambition and gain the personalorganisation skills that are necessary to undertake such a large project.

However research and writing a thesis take a lot more than time and organisa-tion. My particular thanks go to my immediate supervisor, Dr. Mick Ganley, for hisinvaluable guidance and support throughout my studies at Royal Holloway. Mickalso supervised my dissertation towards an MSc in Information Security. My thanksalso go to Prof. Chris Mitchell, my other supervisor, for overseeing my doctoralstudies and in particular for providing strategic direction. Prof. Fred Piper gave mesound advice when I was deliberating whether to commence these doctoral studiesand he provided considerable help by reviewing the iterations of my draft thesis.Finally, during my studies I needed to contact various academic staff at Royal Hol-loway’s Information Security Group for specific advice and that timely assistance(and knowing it was available) helped keep me on track.

15

List of Publications

This thesis contains research that has been published as six refereed papers in ajournal and various conference proceedings.

David J. Boyd. Towards a private and anonymous EMV payment application.In John Haggerty and Madjid Merabti, editors, Proceedings of the 3rd Confer-ence on Advances in Computer Security and Forensics (ACSF 2008), pages53-59, July 2008. ISBN: 978-1902560205 [30].

David J. Boyd. Enhancing the non-repudiation properties of EMV paymentcards. In Sanjay Goel, editor, Proceedings of the 3rd Annual Symposium onInformation Assurance (ASIA ’08): The Academic Track of the 11th AnnualNew York State Cyber Security Conference, pages 63-70, June 2008 [27].

David J. Boyd. A pragmatic approach to temporary payment card numbers.International Journal of Electronic Security and Digital Forensics (IJESDF),Volume 2, Number 3, pages 253-268, July 2009 [31].

David J. Boyd. Enhancing the non-repudiation properties of Internet pay-ments through a third dimension. In Kamel Adi, Mourad Debbabi, and LuigiLogrippo, editors, Proceedings of the 2nd Workshop on Practice and Theory ofIT Security (PTITS 2008), pages 33-39, January 2008 [28].

David J. Boyd. Single sign-on to the Web with an EMV card. In WaleedW. Smari and William McQuay, editors, Proceedings of the 2008 InternationalSymposium on Collaborative Technologies and Systems (CTS 2008), pages 112-120. IEEE, May 2008. ISBN: 978-1424422487 [29].

David J. Boyd. TLS client handshake with a payment card. In Proceedingsof the 23rd IEEE International Parallel and Distributed Processing Symposium(IPDPS 2009). IEEE, May 2009. ISBN: 978-1424437504 [32].

Additionally one short paper resulting from this research has been presented.

David J. Boyd. Increasing the Non-Repudiation Properties of EMV PaymentCards. The 12th Nordic Workshop on Secure IT Systems (NordSec 2007),October 2007.

16

Abbreviations

2FA: Two-Factor Authentication2TDES: Double-length key Triple Data Encryption Standard3TDES: Triple-length key Triple Data Encryption Standard4DBC: Four-Digit Bank CodeAA: Amount AuthorisedAAC: Application Authentication CryptogramAC: Application CryptogramAFL: Application File LocatorANO: ANOnymityAPI: Application Programming InterfaceASP: Authentication Service ProviderATC: Application Transaction CounterATM: Automatic Teller MachineCA: Certification AuthorityCBC: Cipher Block ChainingCC: Currency CodeCCD: Common Core DefinitionsCDA: Combined DDA/Application cryptogram generationCID: Card Identification CodeCMS: Central Mapping ServiceCNP: Card Not PresentCP: Card PresentCRV: Client Random ValueCS: Cardholder SystemCSC: Card Security CodeCVC: Card Verification CodeCVM: Cardholder Verification MethodCVV: Card Verification ValueDDA: Dynamic Data AuthenticationDES: Data Encryption StandardDH: Diffie-HellmanDNA: DeoxyriboNucleic AcidDNS: Domain Name SystemDoS: Denial of ServiceE-commerce: Electronic commerce

17

LIST OF TABLES

ECB: Electronic Code BookEEPROM: Electrically Erasable Programmable Read-Only MemoryEMV: Europay MasterCard VisaE-payment: Electronic paymentEXP: EXPiry dateHMAC: keyed-Hash Message Authentication Codehttps: HyperText Transfer Protocol SecureIAD: Issuer Application DataICC: Integrated Circuit Cardid: identifierIEC: International Electrotechnical CommissionIETF: Internet Engineering Task ForceIP: Internet ProtocolISO: International Organization for StandardizationISP: Internet Service ProviderIV: Initialisation VectorMAC: Message Authentication CodeMS: Master SecretNIST: National Institute of Standards and TechnologyNRO: Non-Repudiation of OriginNRR: Non-Repudiation of ReceiptNTP: Network Time ProtocolOAN: One-time Account NumberPAN: Primary Account NumberPANSEQ: PAN SEQuence numberPDA: Personal Digital AssistantPII: Personally Identifiable InformationPIN: Personal Identification NumberPKI: Public Key InfrastructurePRF: PseudoRandom FunctionPS: Premaster SecretPSE: PSEudonymityPVDE: PIN Verification Data ElementRAN: Real Account NumberRCA: Remote Card AuthenticationSDA: Static Data AuthenticationSHA: Secure Hash AlgorithmSP: Service ProviderSPID: Service Provider IDentifierSRP: Secure Remote PasswordSRV: Server Random ValueSSL: Secure Sockets LayerSSO: Single Sign-OnSV: Starting VariableSYN: SYNchroniseTC: Transaction Certificate

18

LIST OF TABLES

TCN: Temporary Card NumberTCP: Transmission Control ProtocolTDES: Triple Data Encryption StandardTLS: Transport Layer SecurityTRUN: TRUNcateTTP: Trusted Third PartyTVR: Terminal Verification ResultsUAN: Umbrella Account NumberUNL: UNLinkabilityUNO: UNObservabilityURL: Uniform Record LocatorVPN: Virtual Private NetworkWeb: World Wide WebXOR: eXclusive OR

19

Notation

‖: Concatenation⊕: Exclusive or (XOR)a: Personal identification number (PIN)A: Amount authorised (AA)b: Identification numberB : Biometric sampleB2D: Binary to decimal functionc: CiphertextC: LiteralsC : Currency code (CC)d : Private key for asymmetric decryptionD: Decrypt functionD : Datee: Public key for asymmetric encryptionE: Encrypt functionE : Expiry date (EXP)F: Diversification functionF : Finger positiong : NonceG : Counter or sequence numberh: Hash valueH: Hash functionHK : Keyed-hash message authentication code (HMAC) with secret key KHS : Keyed-hash message authentication code (HMAC) with secret SH : Labeli : Current line, operation or valueI : Seedj : Last line, operation or valueJ : Primary account number (PAN)k : Current line, operation or value. Used to avoid confusion with iK : Secret key for symmetric encryptionKB : Key blockKI : Card issuer’s secret symmetric encryption keyKIM : Card issuer’s master key for deriving other keysKM : Card’s master key for deriving other keys

20

LIST OF TABLES

KS : Card’s session key for symmetric encryptionKt: Trusted third party’s (TTP) secret symmetric encryption keyl : ChallengeL: Function that extracts characters from the left-hand sideL: Log entry or left-hand side componentm: Length of cryptographic output, in bitsM : Output from a MAC functionn: Block size of a symmetric cipher or modulus of an asymmetric cipherN : Application transaction counter (ATC)O : One-time account number (OAN) - Chapter 5,

Temporary card number (TCN) - Chapter 7, or equivalent.Also: Online value

p: Input message, often plaintext.Also indicates a prime number for RSA algorithm

P : Transaction or request parametersPAD : Padding valuePAR: Function that sets the least significant bits of each byte to odd parityq : Prime number for RSA algorithmQ : Primary account number sequence number (PANSEQ)r : Client random value (CRV)R: Real account number (RAN) or right-hand side components: Server random value (SRV)S : Shared secrett : Low thresholdT : Timeu: Check digit(s)U : Umbrella account number (UAN)v : Premaster secret (PS)V : Merchant identifierw : Master secret (MS)W : Transaction certificate (TC)X : DataY : DataZ : Data

21

Chapter 1

Introduction

Contents

1.1 Motivation . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1.2 Main Contributions . . . . . . . . . . . . . . . . . . . . . . 24

1.3 Structure of Thesis . . . . . . . . . . . . . . . . . . . . . . 26

1.4 Scope: E-payments and Payment Cards . . . . . . . . . . 28

This chapter provides an overview of the thesis, outlines its contribution to the

field of secure electronic payment systems and describes the structure of the thesis.

1.1 Motivation

Since the dawn of commerce mechanisms have been devised for paying a consid-

eration to recompense, after an offer has been made and accepted, to fulfil a con-

tract. The method of recompense has been evolutionary with gradual change over

many thousands of years and taking many guises to represent value to the recipient;

physical items of value such as precious metals evolved into coins and eventually

promissory notes from banks or possibly other issuers.

The rate of change has increased, particular in the past century, with banks

playing a dominant role and building on their promise of payment. Promissory

notes are often thought of as being transferrable and to pay the bearer a fixed sum,

but nowadays that note can be an electronic payment (e-payment) that exactly

22

1.1 Motivation

matches the consideration and only payable to one entity.

Credit cards were mentioned in futuristic fiction in 1887 [21]. According to the

Encyclopædia Britannica [57], credit cards were first issued in a limited form by

individual suppliers for use in their outlets in the 1920s, and in a universal form

that could be used in a variety of establishments in the 1950s. Today credit cards

are just one of several types of payment card which are typically issued by banks,

although cards tied to individual suppliers or products still have a role to play: store

cards and fuel cards for example. Payment cards are now a ubiquitous source for

consumer e-payments; some 84% of the UK’s adult population hold a debit card and

62% a credit or charge card [8].

Consumers, merchants and financial institutions like the convenience of payment

cards and the growth of the Internet has fuelled a remote dimension to e-payments:

Card-Not-Present (CNP) payments. The traditional methods of payment whereby

monies are physically exchanged for goods do not lend themselves to the Internet.

The Internet has brought its own set of problems, notably opportunities for payment

fraud.

E-payment security could be seen as somewhat single-sided. The card issuers

trust their e-payment systems and payment cards. The card issuer usually carries

the liability should anything go wrong unless the card issuer considers the cardholder

or other identifiable party to have been at fault. The temptation is for the card issuer

to build an infrastructure to mitigate its financial risks in a cost-effective manner by

increasing the difficulty for committing fraud, rather than creating an environment

where it can be demonstrated whether the cardholder was behind the payment.

A particular need is for a stronger binding of both the card and its holder to their

payments: to assure any payment to be genuine, to hold the cardholder accountable,

but just for his or her payments, and to stop the cardholder repudiating his or

23

Introduction

her authorised payments. Often authentication, accountability and non-repudiation

counteract privacy. Privacy allows the cardholder to be secluded and to be selective

about the release of his or her personal and payment information. In the wrong

hands, card and cardholder information can facilitate subsequent crime, notably:

payment fraud and identity theft.

The motivation for this research is that I frequently use payment cards and

have (so far) avoided security problems, but get the impression that cardholders

with security problems sometimes feel like David facing Goliath. This research is

to move the next stage of e-payment evolution towards addressing the risks for

and concerns of honest and prudent cardholders, through the provision of privacy

and non-repudiation security services. Some research has been done to look at the

reported and theoretical methods of attack, but far less research has sought solutions.

1.2 Main Contributions

This thesis proposes a novel set of six complementary modular solutions that en-

hance the privacy and non-repudiation security properties of chip-card orientated

e-payments, and the authenticating infrastructure that protects Internet payments1.

The solutions have the cardholders’ interests at heart and are independent so one,

some or all of the solutions can be selected to meet the cardholders’ and card issuers’

needs.

First, a scheme is proposed for making Card-Present (CP) payments that are

effected with a payment card private for the cardholder at the point of payment

and through clearing . By using a one-time account number and not using the card-

holder’s name, the proposal allows the cardholder to be anonymous and for his or1These are web payments made over the Internet. This thesis follows common parlance: Internet

payments.

24

1.2 Main Contributions

her payments not to be linkable to his or her other payments, whilst still allowing

the cardholder to evidence making payment should the payee repudiate receipt. The

cardholder has his or her personal and account details hidden by default, making

one less enabler for identity theft.

The second scheme extends the non-repudiation boundary for CP payments by

proposing three methods for leaving a cryptographic mark of previous payments on

a payment card’s chip to demonstrate whether the card was present for any recent

transaction that is disputed. For the cardholder the three methods provide a trade-

off between ease of reading the cryptographic mark and privacy; for the card issuer

the balance is between processing overhead and storage space on the card’s chip.

The third and fourth schemes extend the security services offered by the first two

schemes to CNP payments and in particular: Internet payments. The methods are

different because the card’s physical presence and chip’s contents do not play a direct

part in the transaction. One scheme allocates an offline Temporary Card Number

(TCN) for each transaction and the other scheme uses a Trusted Third Party (TTP)

to store a biometric sample from the person making the Internet payment.

However authenticating web users remains a particular problem. The fifth

scheme proposes to extend the use of a payment card to provide a Single Sign-

On (SSO) scheme that could be adapted to provide both authentication for the

scheme and the authentication component for other SSO schemes. The sixth scheme

proposes to facilitate client authentication for the Transport Layer Security (TLS)

protocol2 by authenticating with a payment card rather than Public Key Infrastruc-

ture (PKI - outlined in Subsection 2.3.4.1). In both proposals the web server does

not need to know the identity or invade the privacy of the client (cardholder) and

the card issuer maintains a log which could vouch for some of the actions taken by2TLS is used in this thesis as the indicated abbreviation and sometimes to refer to the TLS

protocol.

25

Introduction

the cardholder.

With one, some or all of these proposed schemes, a cardholder can make pay-

ments whilst maintaining as much privacy as he or she wishes. Notwithstanding

this privacy, a cardholder is able to evidence making those payments. Additionally,

with the SSO or TLS schemes there is evidence of any prior authentication over the

Internet. However in certain situations a cardholder may be held accountable for

actions that he or she may (incorrectly) wish to repudiate, for example a purchase

or actions that the cardholder later regrets.

1.3 Structure of Thesis

This thesis is organised as follows:

Chapter 2 provides a hierarchical overview of the security definitions, services

and components on which this thesis builds. First the three foundation information

security services are described, followed by the subservient security services that are

of particular interest for this thesis, next the cryptographic primitives and constructs

that build those services and finally an outline of the three principal cryptographic

algorithms used by this thesis.

Chapter 3 introduces three cornerstones for the e-payment systems that are dis-

cussed in this thesis. Cash is the traditional method of payment and a yardstick

for e-payment systems. Its pros and cons with respect to security services are dis-

cussed. EMV (Europay, MasterCard, Visa) is a widely-used e-payment system for

consumers and where this thesis needs to exemplify with a specific system, then it

is with EMV. Finally CNP payments are discussed because they require special

26

1.3 Structure of Thesis

attention due to the higher risks involved when a card does not directly participate

in a transaction.

Chapter 4 provides a summary of the privacy and non-repudiation attributes

from which specific schemes can be developed and measured. The chapter links the

overview in Chapters 2 and 3 with the next six chapters where schemes are proposed.

Chapter 5 proposes a scheme to enhance the privacy properties of CP payments

made with chip-based payment cards. The scheme uses a one-time account number

for each transaction which acts as the cardholder’s pseudonym and only identifying

mark. It is up to the cardholder whether he or she wishes to disclose any information

that erodes his or her anonymity or allows others to link his or her payments.

Chapter 6 proposes a non-repudiation scheme that leaves a cryptographic mark

on a payment card’s chip each time it is used for a CP payment. The absence or

presence of a mark can show whether the card was involved with a recently-made

payment that is disputed.

Chapter 7 proposes a scheme to enhance the privacy properties of CNP payments.

This offers a comparable service to Chapter 5, but in an environment where the card

does not make direct contact with the merchant.

Chapter 8 proposes a scheme to enhance the non-repudiation properties of pay-

ments made over the Internet. This offers a comparable service to Chapter 6, but

stores a biometric sample from the person making the payment with a TTP as

evidence of participation in the transaction.

27

Introduction

Chapter 9 proposes a scheme to extend the reach of the identity checks that are

undertaken by a bank before it issues a payment card to provide an SSO service for

the World Wide Web (Web). The proposal provides a Two-Factor Authentication

(2FA) framework and a basic single point of user registration that respects the user’s

right to privacy. It also offers certain non-repudiation services.

Chapter 10 proposes another general authentication scheme for a payment-card

holder: client authentication for the TLS protocol. Again, the user’s privacy is

respected and some non-repudiation services are delivered. Typically only the server

is authenticated for a TLS session due to most users not being enrolled in a PKI.

This TLS protocol extension allows a user to authenticate himself or herself with a

payment card instead of PKI.

Chapter 11 gives the conclusions to this thesis and discusses opportunities for

further research.

1.4 Scope: E-payments and Payment Cards

A payment system in this thesis refers to an e-payment system that is associated

with a chip-based payment card, although alternative authentication mechanisms

are not precluded for the two proposed web authentication schemes.

28

Part I

Overview

29

Chapter 2

Security Building Blocks

Contents

2.1 Foundation Security Services . . . . . . . . . . . . . . . . 31

2.1.1 Confidentiality . . . . . . . . . . . . . . . . . . . . . . . . . 31

2.1.2 Integrity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

2.1.3 Availability . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

2.2 Privacy and Non-Repudiation . . . . . . . . . . . . . . . . 33

2.2.1 Privacy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

2.2.2 Non-Repudiation . . . . . . . . . . . . . . . . . . . . . . . . 40

2.2.3 Authentication . . . . . . . . . . . . . . . . . . . . . . . . . 44

2.3 Principal Cryptographic Primitives and Constructs . . . 45

2.3.1 Hash Function . . . . . . . . . . . . . . . . . . . . . . . . . 45

2.3.2 Symmetric Cryptography . . . . . . . . . . . . . . . . . . . 46

2.3.3 Message Authentication Code . . . . . . . . . . . . . . . . . 48

2.3.4 Asymmetric Cryptography . . . . . . . . . . . . . . . . . . 50

2.3.5 Nonce . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

2.3.6 Pseudorandom Functions . . . . . . . . . . . . . . . . . . . 53

2.4 Principal Algorithms . . . . . . . . . . . . . . . . . . . . . 54

2.4.1 Data Encryption Standard . . . . . . . . . . . . . . . . . . 54

2.4.2 RSA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

2.4.3 Secure Hash Algorithm . . . . . . . . . . . . . . . . . . . . 56

30

2.1 Foundation Security Services

This chapter provides a hierarchical overview of the security definitions, services

and components on which this thesis builds. First, the three foundation information

security services are described and then those services are subdivided into some spe-

cific security services that are at the heart of this thesis. Underpinning those specific

security services are some cryptographic primitives and constructs which are then

described. Finally, the three main cryptographic algorithms and their variants that

provide those primitives and constructs are outlined.

2.1 Foundation Security Services

No description of information security services is complete without mentioning the

widely-used CIA (or C-I-A) triad information security model which identifies con-

fidentiality, integrity and availability as the fundamental security characteristics of

information. Started by Clark and Wilson [36], it is an idealised model that “strips

away” all properties that are believed to be irrelevant and focuses on a limited set

of properties in isolation.

2.1.1 Confidentiality

Confidentiality is the quality or state of information being protected against disclo-

sure to unauthorised entities: individuals or systems. For example when using a

payment card over the Internet to make a payment, sensitive information need to

be transferred from the client’s computer to the merchant’s computer over a net-

work that is not trusted. Confidentiality during transmission is typically ensured by

encrypting the card number and other payment details whilst in transit. This is a

narrower view than the dictionary definition which covers all types of information,

31

Security Building Blocks

including the spoken word, and without specifying which entities must not know the

information [127].

Confidentiality is about protecting READ access.

2.1.2 Integrity

Integrity is the condition of (the protected information) not being marred or vio-

lated; being in unimpaired or uncorrupted condition; being in its original perfect

state [127]. For a payment this is to prevent fraud or error, or both: in other words,

intentional or accidental harm. Integrity can be protected through various mecha-

nisms; often a cryptographic mark accompanies the protected information in order

that the verifier can recompute that mark to make sure that the information of

interest and its mark tally.

Integrity is about protecting WRITE access.

2.1.3 Availability

Availability is about ensuring that information and services are capable of producing

the desired result when needed [127]. An online system has greater demands for

availability than an offline system. Many of the proposals in this thesis require an

online service to be provided for real-time operations.

32

2.2 Privacy and Non-Repudiation

2.2 Privacy and Non-Repudiation

Confidentiality can be achieved through one or more security services; privacy is

a confidentiality security service which pertains to a person or persons. In turn

privacy is not a solitary security service but an umbrella service for four other

services: anonymity, pseudonymity, unlinkability and unobservability, which can also

be subdivided.

Integrity can also be achieved through one or more security services and non-

repudiation is one such service. Non-repudiation provides integrity by giving evi-

dence that binds an action to an entity, although non-repudiation is not exclusively

an integrity security service.

Payment systems, privacy services and non-repudiation services all rely on other

security services. For example: a consumer payment system needs to authenticate

the card’s data and cardholder to ensure that a payment is authorised, legal consid-

erations require the cardholder to be held accountable for his or her e-payments and

noteworthy events are often recorded in an audit trail for potential analysis.

This section defines the above-mentioned security services in the context of a

card-based payment system.

2.2.1 Privacy

Privacy is the state or condition of being withdrawn from others, or from public

interest, or secluded as a matter of choice or right [127].

Many states protect their citizens’ privacy, particularly European states3:3Member states of The Council of Europe - http://www.coe.int/.

33

Security Building Blocks

• With respect to public (state) authorities “everyone has the right to respect

for his private and family life, his home and his correspondence” [42, Article

8.1] [154, Article 8.1]. However this is not an absolute right but a qualified

right: the public authority is allowed to interfere with this right to privacy,

in part, where necessary in the interests of national security, the economic

wellbeing of the country and the prevention of crime [42, Article 8.2] [154,

Article 8.2].

• With respect to Personally Identifiable Information (PII), this is information

unique to a person and can act as a locator for that person or distinguish that

person from others, the level of protection is more prescriptive [62,153]. Data

solely related to payments and payment cards typically do not fall into the

elevated classification of sensitive data, but they could if a payment were to

point to an unrelated sensitive facet such as a payment to a political party.

Privacy is not a solitary security service. Privacy is a combination of security

services meeting to provide a cohesive service. Particularly for a payment system, the

bounds of the service may change in certain circumstances such as: the cardholder

waiving his or her rights, or where the public authorities exert their rights.

2.2.1.1 Privacy: Terminology and Interrelationship

ISO/IEC 15408-2:2008 is the second part of the three-part international standard

from the International Organization for Standardization (ISO)4 and the Interna-

tional Electrotechnical Commission (IEC)5 that covers evaluation criteria for infor-

mation technology security and, in particular, security functional components [101].

First published in 1999, it is often referred to by its formative name: Common Crite-4http://www.iso.org/.5http://www.iec.org/.

34

2.2 Privacy and Non-Repudiation

ria (for Information Technology Security Evaluation)6. It states that the majority of

terms are used either according to their accepted dictionary definitions or according

to commonly accepted definitions.

The Common Criteria expresses security functional requirements in terms of

classes, families and components. Privacy is a functional class with four member

families: ANOnymity (ANO), PSEudonymity (PSE), UNLinkability (UNL) and UN-

Observability (UNO). These families are subdivided into one or more components.

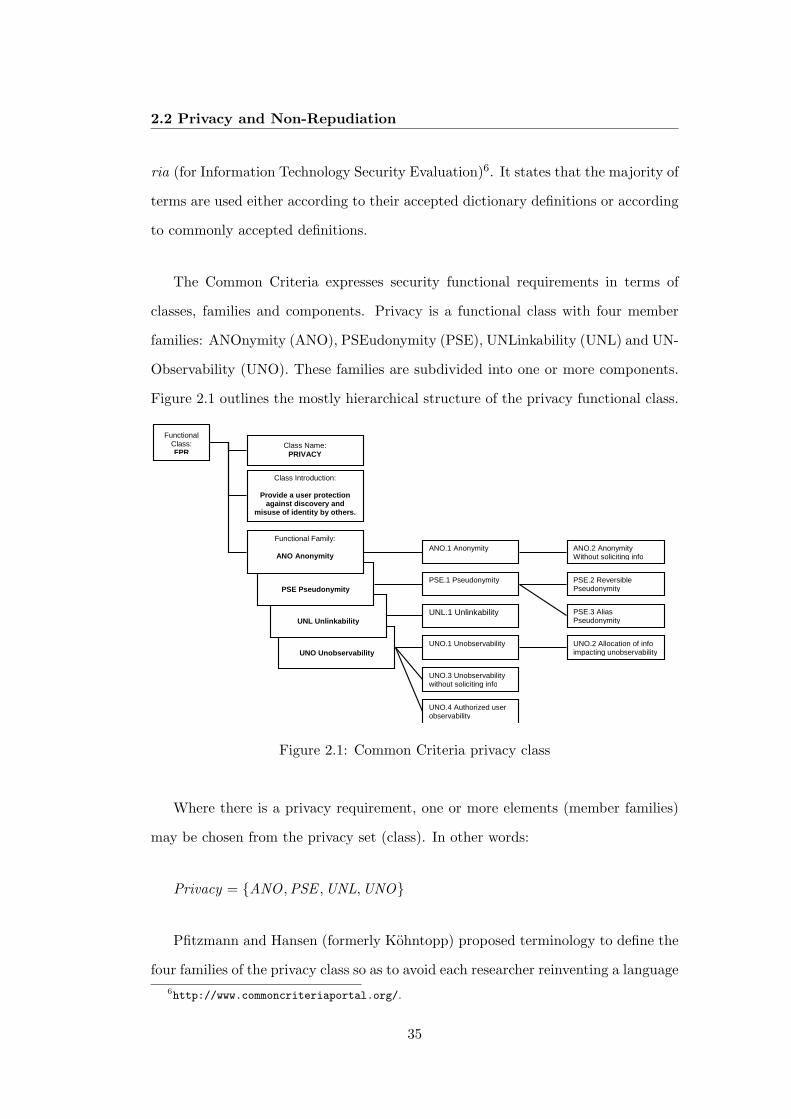

Figure 2.1 outlines the mostly hierarchical structure of the privacy functional class.

UNO Unobservability

UNL Unlinkability

PSE Pseudonymity

Functional Class: FPR

Class Name: PRIVACY

Class Introduction:

Provide a user protection against discovery and

misuse of identity by others.

Functional Family:

ANO Anonymity ANO.1 Anonymity

ANO.2 Anonymity Without soliciting info

PSE.1 Pseudonymity

PSE.2 Reversible Pseudonymity

PSE.3 Alias Pseudonymity

UNL.1 Unlinkability

UNO.1 Unobservability

UNO.2 Allocation of info impacting unobservability

UNO.3 Unobservability without soliciting info

UNO.4 Authorized user observability

Figure 2.1: Common Criteria privacy class

Where there is a privacy requirement, one or more elements (member families)

may be chosen from the privacy set (class). In other words:

Privacy = {ANO ,PSE ,UNL,UNO}

Pfitzmann and Hansen (formerly Kohntopp) proposed terminology to define the

four families of the privacy class so as to avoid each researcher reinventing a language6http://www.commoncriteriaportal.org/.

35

Security Building Blocks

from scratch and to give consistency [133]. The challenging nature of the task is

illustrated by the paper now (October 2009) being in its 31st iteration [132]. The

definitions are in the specific setting of senders sending messages to recipients using

a communications network, with the thrust being towards unauthorised access by

an attacker rather than access in general (that is: authorised and unauthorised

access) and the assumption that the attacker is not able to get information on the

sender or recipient from the message content. This limitation is partly articulated

by Clauß and Schiffner [39]: “On the network layer, message content is considered

as a black box.” For a payment system it is the message content that is of essence;

the application layer where it can be seen who is paying whom and the details of

the payment. Vice versa, the network layer information and routing do not have

any bearing on cardholder privacy. Integrity and availability are already suitably

protected and, in difference with both papers, unauthorised and authorised read

access is the concern. Pfitzmann-Hansen recognise that in other settings their terms

may need to be derived by abstraction, which this thesis does.

2.2.1.2 Anonymity

Anonymity is the state of being nameless, having no name or of unknown name [127].

The Common Criteria is dependent upon there being a distinction between user

identity and subject identity: the user’s real identity (user identity) versus the

identity or identities representing the user (subject identity). Anonymity is not

intended to protect the subject’s identity, only the user’s identity.

Component ANO.1 contains all the requirements of the anonymity family and

requires that other users or subjects are unable to determine the identity of a user

bound to a subject or activity. Enhanced component ANO.2 requires that the

system does not ask for user identity and the component can be used to satisfy all of

36

2.2 Privacy and Non-Repudiation

ANO.1’s requirements. Both components can allow authorised users to know users’

identities and only protect a defined user or set of users: the anonymity set7.

ANO = ANO .1 or ANO .2

ANO .2 ⊂ ANO .1

2.2.1.3 Pseudonymity

Pseudonymity is the fact or condition of bearing or assuming a false or fictitious

name; the use of an alias or assumed name [127]. A pen name of an author is an

often cited example, but the author’s true name is not necessarily unknown.

The Common Criteria takes a tougher stand than the dictionary and describes

three components that employ a pseudonym when using a resource or service so as

not to disclose its user’s identity, but that user can still be held accountable. Again

a defined set of users are generally protected against unauthorised users. A user (or

cardholder) could be the holder of a subject pseudonym (account number).

Component PSE.1 is the broadest of these components and contains all of those

pseudonymity family requirements. Either or both of the enhanced components

PSE.2 and PSE.3 can be used to satisfy all of PSE.1’s requirements by making the

pseudonymity reversible by the system’s security functions (PSE.2) or by following

certain construction rules for the alias (PSE.3).

PSE = PSE .1 or PSE .2 or PSE .37Chaum introduced the concept of an anonymity set with his Dining Cryptographers’ Prob-

lem [33]. For this thesis, it is the set of all users who could be the anonymous entity. As thesize of an anonymity set increases, so does the strength of anonymity for the elements of that set.The anonymity set is relative to the attacker, context dependent and the set’s size decreases as theattacker’s knowledge increases.

37

Security Building Blocks

PSE .2 ⊂ PSE .1

PSE .3 ⊂ PSE .1

2.2.1.4 Unlinkability

The Common Criteria states that unlinkability allows a user to make multiple uses

of resources or services without unauthorised users being able to link those uses

together. Solitary component UNL.1 satisfies that family requirement. Effectively:

UNL = UNL.1

2.2.1.5 Unobservability

The Common Criteria states that unobservability ensures that a user may use a

resource or service without others, especially third parties, being able to observe

that the resource or service is being used. The unobservability family consists of four

components but this family is not a privacy objective for this thesis (see Subsection

4.1.4).

UNO = UNO .1 or UNO .2 or UNO .3 or UNO .4

UNO .2 ⊂ UNO .1

2.2.1.6 Caveats on Privacy

The Common Criteria recognises that for “ultimate privacy”, no user or authorised

user can see the identity of anyone performing any action. Privacy is also dependent

38

2.2 Privacy and Non-Repudiation

on the “strength of function”, that is the minimum efforts assumed necessary to

defeat the expected security behaviour.

Cardholder’s Actions. For all four families, the Common Criteria excludes the

user’s explicit actions that disclose his or her identity. This thesis similarly excludes

such explicit actions. The proposed privacy properties are optional and there will

be situations where these properties are not desirable or not possible.

Statutory and Regulatory Requirements. In most states the statutory and

regulatory framework does not allow credit and financial institutions to keep anony-

mous accounts [63, Article 6] [147, Section 326.a.2] [155, Regulation 16.(3)], but

not all states [75]. However most states allow anonymity for the cardholder with

other entities in the payment chain when paying for uncontrolled products or ser-

vices, and some digital cash service providers claim their payment application to be

anonymous [58,129].

Per the Common Criteria’s ANO family definitions, a payment system where the

card issuer knows its cardholders’ identities but does not allow other entities to know

that information in normal operation could be deemed anonymous.

Police Investigations. Notably had anonymity been readily available, the UK

Police’s Operation Ore would not have been able to identify 6,000 suspected users of

child pornography that was accessed over the Internet and make 1,300 arrests [19].

By paying the service provider with traceable payment cards, a large number of

the cardholders could be identified to the Police through the card issuers and held

accountable.

39

Security Building Blocks

Pragmatism. Providers of payment systems usually have privacy policies, possi-

bly coupled with an opt-in or opt-out clause depending upon the perceived value

of the information, to clarify the terms and details of the service with the payment

system users. Apart from ensuring compliance with most data protection legislation

by virtue of subject consent, it also adds clarity to the terminology.

2.2.2 Non-Repudiation

Repudiation is an action of rejection or denial of, for example: a thing, an action, a

contract, a person or an obligation [127].

International standard ISO/IEC 10181-4:1997 [84] provides a non-repudiation

framework and discusses non-repudiation in terms of evidence: “The goal of the non-

repudiation service is to collect, maintain, make available, and validate irrefutable

evidence concerning a claimed event or action in order to resolve disputes about the

occurrence or non-occurrence of the event or action”. Earlier international stan-

dards (for example ISO 7498-2:1989 [79]) tended to use the term “proof” rather

than “evidence” and did not use a term akin to “evidence subject” to recognise that

the entity involved in the event or action may not be same as the entity in dispute.

The latest framework is also more open-minded about the technical mechanisms

for providing a non-repudiation protocol and no longer implies digital signatures

(Subsection 2.3.4.3) to be the only mechanism for non-repudiation services. Sub-

sequent three-part international standard ISO/IEC 13888 describes mechanisms for

non-repudiation services using secure envelopes with the participation of a TTP as

well as digital signatures [85,87,91].

The mentioned international standards again concentrate on the specific setting

of senders sending messages to recipients using a communications network. For

this thesis, in the context of a consumer e-payment system there are two main non-

40

2.2 Privacy and Non-Repudiation

repudiation services: non-repudiation of making (or originating) a payment and non-

repudiation of receiving a payment. Often a payer claims to have made payment

which the payee claims not to have received, but it can also be vice versa where

the recipient claims to have received a payment that the payer claims not to have

made. For example, when a stolen payment card is used or the recipient is handling

ill-gotten gains. There are other payment-related actions that could be repudiated

such as a payment processor could deny processing a payment.

The term non-repudiation has differing interpretations in electronic commerce

(e-commerce); a cardholder may be liable irrespective of who made the payment.

Bohm et al. [25] state that “A technical assessment may prove that it is highly

probable that (the payment) was made by its apparent maker. A legal assessment

may hold that the apparent maker (of the payment) is bound by it whether the

apparent maker made it or not.” This thesis looks at the technical assessment.

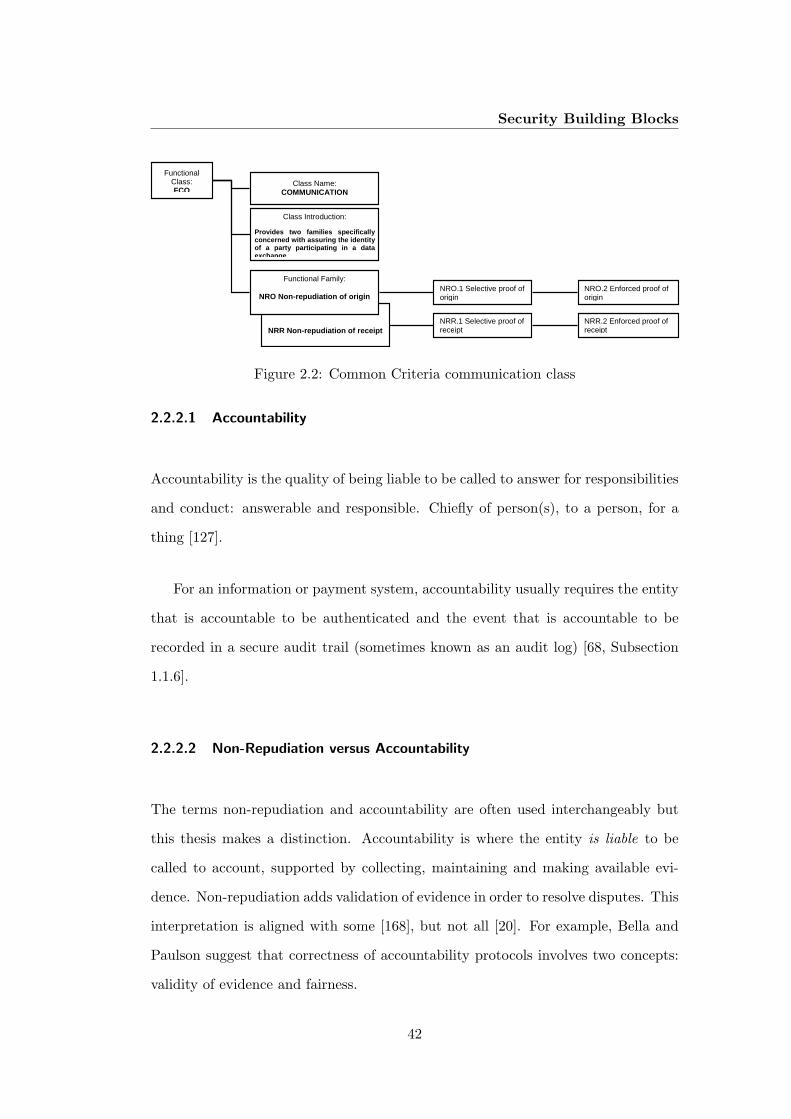

Figure 2.2 outlines the mostly hierarchical structure of the Common Criteria’s

communication functional class which contains two families: Non-Repudiation of

Origin (NRO) and Non-Repudiation of Receipt (NRR). Each family is divided into

two components. NRO.1 provides proof of origin on request whereas enhanced

component NRO.2 provides that proof all of the time. Either can be used to meet

all the requirements of the NRO family. Similarly, NRR.1 provides proof of receipt

on request whereas NRR.2 provides that proof all of the time. It is for the chosen

Common Criteria protection profile to define the security requirements and to specify

the recipient of the proof.

Communication = {NRO ,NRR}

NRO = NRO .1 or NRO .2

NRR = NRR.1 or NRR.2

41

Security Building Blocks

NRR Non-repudiation of receipt

Functional Class: FCO

Class Name: COMMUNICATION

Class Introduction:

Provides two families specifically concerned with assuring the identity of a party participating in a data exchange.

Functional Family:

NRO Non-repudiation of origin NRO.1 Selective proof of origin

NRO.2 Enforced proof of origin

NRR.1 Selective proof of receipt

NRR.2 Enforced proof of receipt

Figure 2.2: Common Criteria communication class

2.2.2.1 Accountability

Accountability is the quality of being liable to be called to answer for responsibilities

and conduct: answerable and responsible. Chiefly of person(s), to a person, for a

thing [127].

For an information or payment system, accountability usually requires the entity

that is accountable to be authenticated and the event that is accountable to be

recorded in a secure audit trail (sometimes known as an audit log) [68, Subsection

1.1.6].

2.2.2.2 Non-Repudiation versus Accountability

The terms non-repudiation and accountability are often used interchangeably but

this thesis makes a distinction. Accountability is where the entity is liable to be

called to account, supported by collecting, maintaining and making available evi-

dence. Non-repudiation adds validation of evidence in order to resolve disputes. This

interpretation is aligned with some [168], but not all [20]. For example, Bella and

Paulson suggest that correctness of accountability protocols involves two concepts:

validity of evidence and fairness.

42

2.2 Privacy and Non-Repudiation

Zhou and Gollmann [168] consider fairness to be optional and for a fair non-

repudiation protocol not to give one party an advantage over the other or vice

versa, although Gollmann et al. later describe that as vague [114]. This thesis

proposes schemes that are intended to be advantageous for the cardholder and does

not consider a point of balance for fairness.

Non-repudiation services establish evidence: evidence establishes accountabil-

ity [91].

2.2.2.3 Audit

Although it is preferable to prevent unauthorised activity and problems, it is not

always possible or practical. Further mechanisms are therefore required to help

detect security and other noteworthy events. Auditing is the process of recording

relevant events in an audit trail for potential later analysis: an audit [68, Subsection

1.1.6].

To be effective the audit trail needs to be held in a secure place that is not

susceptible to the same perils as the subject(s) being monitored. The volume of

data written to an audit trail also has to strike a balance between being sufficient

and not capturing every detail so as to create storage problems and an audit trail

that is too large for effective analysis.

An audit trail can be a repository of evidence that supports accountability and

non-repudiation although auditing has a wider remit. An audit trail can also help

other security services, for example confidentiality: a review may identify an entity

reading beyond its intended bounds.

43

Security Building Blocks

2.2.3 Authentication

Authentication both needs and supports other security services. It is implicit for

many of the mentioned security services.

Authentication in the context of this thesis is the action or processes of es-

tablishing the validity of a claim [127]. This can be a claim to be a particular

identity: entity authentication, or a claim that data originated from a particular

source: data origin authentication. International standards describe authentication

terminology [79], albeit in a networking setting, and others describe the protocols:

most notably ISO/IEC 9798-1:1997 [86] and ISO 16609:2004 [82].

Unilateral authentication is entity authentication which provides one entity with

assurance of the other’s identity but not vice versa. Mutual authentication provides

each entity with assurance of the other’s identity.

Entity authentication only provides confidence at the time of check and authen-

tication of origin only provides confidence of source and does not, on its own, provide

confidence that the data have not been altered or duplicated.

When a card payment is initiated typically two things are authenticated: the

cardholder as an entity and the origin of the card’s data. Subsection 3.2.2 describes

the authentication of an EMV payment card’s data and its cardholder. Later on in

the EMV payment cycle the card issuer, transaction data and secure messages may

also be authenticated.

44

2.3 Principal Cryptographic Primitives and Constructs

2.3 Principal Cryptographic Primitives and Constructs

This section describes the cryptographic building blocks that are used in this thesis

to provide the desired security services.

X‖Y is used throughout this thesis to denote the concatenation of data items X

and Y .

2.3.1 Hash Function

A hash function is a cryptographic algorithm that takes input of an arbitrary length

and creates an output, or hash, of a fixed length. Some other terms are used for a

hash and hash functions; for consistency this thesis avoids those other terms. The

assumption is that a hash can be created by any entity with access to the input

so on its own a hash only provides integrity protection against accidental harm. It

is usual to find a hash as a building block of a larger construct. A hash value, h,

calculated by a hash function, H, on an input message, p, is written thus:

h = H(p)

A hash function is associated with the following properties [68, Subsection 12.2.1]:

• Deterministic: for a given input, p, the same hash value, h, is always gener-

ated.

• Ease of computation: given p, it is easy and typically efficient to compute

H(p).

• Compression: function H maps arbitrary length input p to fixed-length out-

put h. The length is algorithm dependent.

45

Security Building Blocks

• Preimage resistance: one-way. Given a value h it is generally computation-

ally infeasible to find value p.

• 2nd preimage resistance: weak collision resistance. Given both h and p it

is computationally infeasible to find another and different message, the hash

of which matches h.

• Collision resistance: strong collision resistance. It is computationally in-

feasible to find two different inputs that generate the same h. Outputs are

mapped evenly over the range and are uniformly distributed.

2.3.2 Symmetric Cryptography

Symmetric or secret key cryptography uses a secret data string, known as a key,

and an algorithm to transform a plaintext (or cleartext) message into ciphertext

and vice versa with the same key. This cryptographic primitive can be used in

different constructs to offer various security services, but its main drawback is that

the participating entities must know the key before they can transform data. In this

thesis specific key derivation functions are discussed but key management generally

entails prior knowledge of the key, or deriving the key from a shared secret and a

salting value, or from a transfer of secret(s) using another cryptographic channel.

2.3.2.1 Symmetric Encryption

Symmetric encryption provides confidentiality security services and uses secret key

K to encrypt (E) message p into ciphertext c. For the purposes of this thesis the

following representation is used:

c = EK(p)

46

2.3 Principal Cryptographic Primitives and Constructs

That ciphertext can be decrypted (D) with the same key into the original plaintext:

p = DK(c)

There are two widely-used categories of symmetric encryption schemes: block and

stream ciphers. Both are mentioned in this thesis, although only block ciphers

are explored. Block ciphers break the input data into fixed size blocks (that are

algorithm dependent) and encrypt or decrypt in sequence. This simple mode of

operation is referred to as Electronic Code Book (ECB) mode.

2.3.2.2 Cipher Block Chaining

Cipher Block Chaining (CBC) is a mode of encipherment that was patented by IBM

in 1978 [77]. CBC is similar to ECB except that each block of plaintext is processed

by an eXclusive OR (XOR) operation with the previous block’s ciphertext before

being encrypted. This gives some integrity to the ciphertext because each cipher

block is dependent on its preceding cipher block; should one or more bits of a block

of ciphertext be altered then that block and the following block will be corrupt when

decrypted. Confidentiality is also enhanced because if the same plaintext block in a

message is encrypted at two points, then each will give different cipher blocks. An

Initialisation Vector (IV) is used in place of input ciphertext for the first block, which

in the case of EMV and the UK’s payment card processors8 is always set to binary

zeros [54, Annex A.1.1] [14, Subsection 10.2.2]. The CBC encryption operation is as

follows:

ci = EK(pi ⊕ ci−1)

where: c0 is the IV.

The CBC decryption operation is as follows:8CBC is only specified by APACS for message authentication between the card acceptor and

acquirer. APACS is the UK trade association for payment service providers.

47

Security Building Blocks

pi = DK(ci)⊕ ci−1

where: c0 is the IV.

2.3.3 Message Authentication Code

A cryptographic Message Authentication Code (MAC) can provide integrity assur-

ance and data origin authentication services to the other holder(s) of the secret key.

If a TTP is involved and it shares the only other key, then a MAC can in some

situations also provide non-repudiation services.

A MAC function must be resistant to chosen plaintext attack forgeries.

Two inputs are necessary: an arbitrary-length message that is to be authen-

ticated and a secret key. The output is a short m-bit cryptographic check value.

International standards are in place for creating a MAC with a symmetric block

cipher or a hash function. This subsection gives examples of both.

2.3.3.1 Message Authentication Code with a Block Cipher

International standard ISO/IEC 9797-1:1999 covers the use of an n-bit symmetric

block cipher in CBC mode: a CBC-MAC [88].

m ≤ n

In this thesis a MAC is a CBC-MAC unless stated to the contrary and created

in a four-step process:

1. Padding: message p is padded so that its length is a multiple of n bits. The

padding is not retained with the message and only used for creating a MAC.

48

2.3 Principal Cryptographic Primitives and Constructs

This thesis uses a method of padding that is consistent with international

standards ISO/IEC 7816-4:2005 [94], method 2 of ISO/IEC 9797-1:1999 and

EMV [54, Annex A.1.2]. Specifically: a binary “1” is always appended followed

by the fewest binary “0”s necessary.

p = (p‖PAD)

where: PAD = (binary 1‖ . . . ‖0‖ . . . ‖0)

(That is: add a mandatory “1” and then “0”s if or as needed.)

2. Encipherment: p is CBC enciphered with just the last cipher block retained.

The Starting Variable (SV) is binary “0”s9.

ci = EK(pi ⊕ ci−1), for i = 1, 2, . . . , j

where: c0 is the SV.

3. Optional Encipherment: optionally (but encouraged and used in this the-

sis) cj is encrypted with a second key, K ′.

Either: cj+1 = EK′(cj)

Or: cj+1 = EK(DK′(cj))

Should a 2nd key not be available then K ′ = K is possible in conjunction with

the 1st method of optional encipherment.

However EMV specifies no optional encipherment when using a double key or

the 2nd method of optional encipherment when a double key is split and used

as two single keys. Subsection 2.4.1 describes double and single key operation

of a block cipher.

4. Optional Truncation: the resulting MAC is equal to the most significant m

bits of cj+1.

9MACs refer to an IV as an SV. However the TLS specifications use the term IV throughout.This thesis follows the convention for the specifications under discussion.

49

Security Building Blocks

2.3.3.2 Keyed-Hash Message Authentication Code

A keyed-Hash Message Authentication Code (HMAC) uses an iterative crypto-

graphic hash function with a shared secret key to create its message authentication

code. The strength of the HMAC depends on the key, the properties of the un-

derlying hash function and the size of hash output. First published by Bellare et

al. in 1996 [22], there are now a few international standards which all cover a sim-

ilar definition [90, 108, 123]. This thesis uses the Internet Engineering Task Force’s

(IETF)10 definition because the discussed HMACs are primarily used to protect the

integrity of Internet communications. An HMAC, HK (or sometimes HS), performs

the following computation on message p:

HK(p) = H((K ⊕X )‖H((K ⊕Y )‖p))

Where:

K is the secret key. Bytes 0x00 appended as required to make the key equal

to the hash’s input block length.

X is the outer key pad. The byte 0x5C repeated to the hash’s input block

length.

Y is the inner key pad. The byte 0x36 repeated to the hash’s input block

length.

2.3.4 Asymmetric Cryptography

The technique for asymmetric or public key cryptography was first published by

Diffie and Hellman in 1976 [46] and is characterised by each participant using its

own key pair: a mathematically related public and private key. The public key can

be freely distributed and the private key must be kept secret by its user. The use10http://www.ietf.org/.

50

2.3 Principal Cryptographic Primitives and Constructs

of the keys depends on the cryptographic scheme. Two cryptographic schemes and

an infrastructure to support public keys are covered in this subsection.

When compared to symmetric keys, an asymmetric public key can be communi-

cated over a public channel without having to protect the key’s confidentiality, but

when enciphering or deciphering the level of computation is significantly higher mak-

ing asymmetric cryptography computationally expensive or even prohibitive, partic-

ularly in a resource constrained environment such as a low-cost payment card [17]11.

2.3.4.1 Public Key Infrastructure

Integrity of public keys is a particular problem, specifically: knowing who is using

the matching private key and ensuring that the public key has not been changed.

Should a public key be altered then any data processed by the corrupt key would

not tally with the data processed by the genuine private key. However a public key

could be substituted by an attacker who then uses his or her own private key to

assume the capabilities of the original private key user.

A Public Key Infrastructure (PKI) is typically a scheme whereby public keys

are bound to their respective user by a Certification Authority (CA) [1, 67]. A

CA is a form of TTP that registers users once they have been identified and can

demonstrate possessing the private key that matches the public key12. A digital

certificate is issued to bind the verified public key to the registered using entity. The

certificate also contains other details such as period of validity and the cryptographic11Tested on a specific hand-held device: an iPAQ H3630.

A digital signature and verification with a 1,024-bit RSA key took 83 milliseconds, and 513 mil-liseconds with a 2,048-bit key. One symmetric encryption and decryption with the DES algorithmtook just 0.07 milliseconds. However RSA works with far larger input blocks (the size of modulus)versus just 64 bits for DES, but the difference remains significant.The mentioned cryptographic operations and algorithms are discussed in the remaining pages ofthis chapter.

12The role of registering users may be delegated to a registration authority by the CA.

51

Security Building Blocks

purpose of the key.

2.3.4.2 Asymmetric Encryption

Asymmetric encryption is where the data recipient’s public key is used to encrypt

and only the corresponding private key can be used to decrypt those data. This

offers confidentiality services for information passing from the entity that encrypts

to the entity that is using the private key. Often hybrid encryption is used where

the entity that encrypts communicates a secret to the private key user. That secret

can be used as a key for symmetric encryption or be used to derive a shared secret.

2.3.4.3 Digital Signatures

Digital signatures are where the key user signs (deciphers) with his or her private

key (at minimum) a hash of a protected message that anyone with access to the

public key can verify (encipher) [89, 95, 98–100]. If used in conjunction with a PKI

then a digital certificate can be used to tie the public key to the signing entity. A

digital signature can provide data integrity, authentication and non-repudiation of

message origin.

2.3.5 Nonce

The term “nonce” stands for “number used once”. It is a finite sequence of bits that

is selected to ensure uniqueness of the output by only being used once within a given

setting. The choice should be unpredictable to any third party. A nonce has many

cryptographic applications including: prevention of message replay attacks, ensuring