e-money in hong kong - harvard computer societye-money in hong kong winnie nip ’08 many people...

TRANSCRIPT

the Analyst Fall 2006 Emerging Markets �

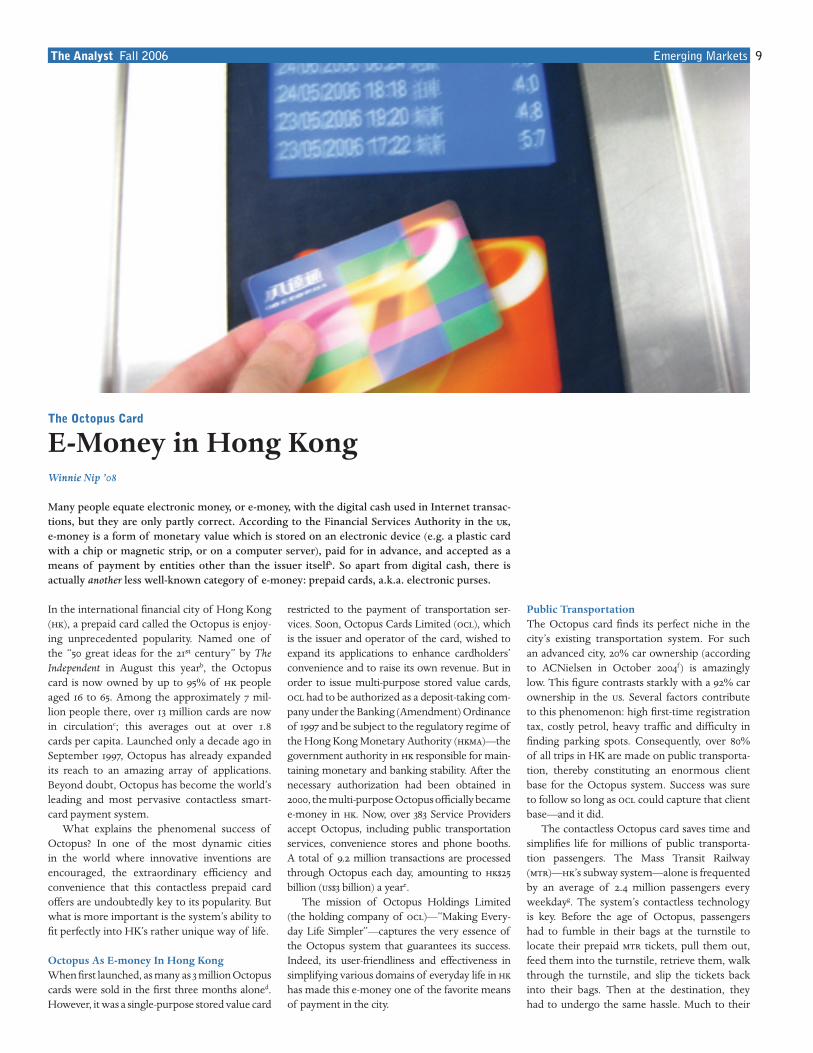

the octopus Card

E-Money in Hong KongWinnie Nip ’08

Many people equate electronic money, or e-money, with the digital cash used in Internet transac-tions, but they are only partly correct. According to the Financial Services Authority in the uk, e-money is a form of monetary value which is stored on an electronic device (e.g. a plastic card with a chip or magnetic strip, or on a computer server), paid for in advance, and accepted as a means of payment by entities other than the issuer itselfa. So apart from digital cash, there is actually another less well-known category of e-money: prepaid cards, a.k.a. electronic purses.

In the international financial city of Hong Kong (hk), a prepaid card called the Octopus is enjoy-ing unprecedented popularity. Named one of the “50 great ideas for the 21ST century” by The Independent in August this yearb, the Octopus card is now owned by up to 95% of hk people aged 16 to 65. Among the approximately 7 mil-lion people there, over 13 million cards are now in circulationc; this averages out at over 1.8 cards per capita. Launched only a decade ago in September 1997, Octopus has already expanded its reach to an amazing array of applications. Beyond doubt, Octopus has become the world’s leading and most pervasive contactless smart-card payment system.

What explains the phenomenal success of Octopus? In one of the most dynamic cities in the world where innovative inventions are encouraged, the extraordinary efficiency and convenience that this contactless prepaid card offers are undoubtedly key to its popularity. But what is more important is the system’s ability to fit perfectly into HK’s rather unique way of life.

Octopus As E-money In Hong KongWhen first launched, as many as 3 million Octopus cards were sold in the first three months aloned. However, it was a single-purpose stored value card

restricted to the payment of transportation ser-vices. Soon, Octopus Cards Limited (ocl), which is the issuer and operator of the card, wished to expand its applications to enhance cardholders’ convenience and to raise its own revenue. But in order to issue multi-purpose stored value cards, ocl had to be authorized as a deposit-taking com-pany under the Banking (Amendment) Ordinance of 1997 and be subject to the regulatory regime of the Hong Kong Monetary Authority (hkma)—the government authority in hk responsible for main-taining monetary and banking stability. After the necessary authorization had been obtained in 2000, the multi-purpose Octopus officially became e-money in hk. Now, over 383 Service Providers accept Octopus, including public transportation services, convenience stores and phone booths. A total of 9.2 million transactions are processed through Octopus each day, amounting to hk$25 billion (us$3 billion) a yeare.

The mission of Octopus Holdings Limited (the holding company of ocl)—“Making Every-day Life Simpler”—captures the very essence of the Octopus system that guarantees its success. Indeed, its user-friendliness and effectiveness in simplifying various domains of everyday life in hk has made this e-money one of the favorite means of payment in the city.

Public TransportationThe Octopus card finds its perfect niche in the city’s existing transportation system. For such an advanced city, 20% car ownership (according to ACNielsen in October 2004f) is amazingly low. This figure contrasts starkly with a 92% car ownership in the us. Several factors contribute to this phenomenon: high first-time registration tax, costly petrol, heavy traffic and difficulty in finding parking spots. Consequently, over 80% of all trips in HK are made on public transporta-tion, thereby constituting an enormous client base for the Octopus system. Success was sure to follow so long as ocl could capture that client base—and it did.

The contactless Octopus card saves time and simplifies life for millions of public transporta-tion passengers. The Mass Transit Railway (mtr)—hk’s subway system—alone is frequented by an average of 2.4 million passengers every weekdayg. The system’s contactless technology is key. Before the age of Octopus, passengers had to fumble in their bags at the turnstile to locate their prepaid mtr tickets, pull them out, feed them into the turnstile, retrieve them, walk through the turnstile, and slip the tickets back into their bags. Then at the destination, they had to undergo the same hassle. Much to their

Emerging Markets the Analyst Fall 200610

annoyance, this lengthy process often resulted in long lines at the turnstile during rush hour. Now, the lines have disappeared. The contactless Octo-pus smartcard needs not be fed into the turnstile at all. Without even leaving the wallet and the lady’s handbag, the card can communicate with the card reader on top of the turnstile, instructing the electronic Octopus system to automatically deduct the correct amount from the card’s built-in microchip. In an extremely efficient city such as Hong Kong, it is no wonder such an ingenious time-saving invention skyrocketed in popularity.

Apart from the contactless design, the card’s technical compatibility with the complex trans-portation fare systems is equally remarkable. On most modes of public transportation in hk, the fare is proportional to the distance travelled; different fares are charged for different routes and sometimes even for different sections of the same route. While this is meant to be a fair payment system, it created a lot of trouble for the passengers. Buses, for example, only accept exact change, forcing passengers to carry a heavy assortment of coins unless they were willing to pay extra. But now, because the Octopus system is able to automatically deduct from the card’s built-in microchip the exact amount requested for each route or each section thereof, passen-gers are no longer required to carry bulky coins in different denominations or gather the exact change before boarding the bus.

Payment CultureGiven its early popularity in the transportation system, Octopus easily ascended to the next level as a multi-purpose stored value card and a form of e-money in hk. But its later success must also be attributed to the prominent role of cash in retail payments in hk. Unlike Americans, for example, people in hk seldom settle petty pay-ments with credit cards. If you walk into Seven Eleven in hk to buy half a dozen of Red Bulls in the past, you would almost definitely pay with notes and coins. Now, however, you will no lon-ger have to count your cash or wait for change if you use your Octopus card, because the card reader instantaneously deducts the exact amount from your card at the point of sale.

Time is money. And this is true for both cus-tomers and businesses. Five to ten seconds saved per customer snowballs into many minutes, and if customers are spared the trouble of waiting in line forever, they will visit the store more often and bring more revenue. This is particularly true for retail firms whose business comes in clustered spurts. For example, the Octopus system could easily double the revenue and efficiency for bak-eries during morning rush hour. This is because the time-consuming part is done electronically behind the scenes. With a quick beep of the card reader, transaction information will be uploaded to Octopus Cards Limited (ocl)’s system, which will then send a clearing report to its agent bank for processing. The day after the transaction, the agent bank of ocl will pay the retail firm through Hong Kong’s advanced Real-time Gross Settlement system. Once the settlement has been completed, the firm’s account will be credited with the correct amount.

Other Advantageshk’s e-money also boasts other advantages. As opposed to the buy-now-pay-later principle of the credit card, Octopus works on the instanta-neous debit principle and allows practically no overdraft on the card. While this curbs consump-tion capability to a certain extent, the inability to significantly overspend implies healthier spend-ing habits in the society.

Moreover, the worst-case consequences of losing an Octopus card are arguably much less serious than those of losing a credit card. The Octopus cardholder will only incur a maximum loss of hk$1,000 (approx. us$130), which is the maximum amount one can store on an Octo-pus card. What’s more, if the cardholder has previously registered the card with ocl, s/he can report the loss to deactivate the card and prevent unauthorized use. ocl will refund to the customer any value remaining on the lost card six hours after the loss has been reported. While credit card companies offer similar services, a credit limit which almost certainly exceeds hk$1,000 exposes the credit cardholder to much greater risks. Thus the above safety feature of Octopus cards makes it possible even for young

children to possess their own cards, giving the statistics yet another boost.

Hong Kong’s success story replicated?Within a decade, Octopus has risen to a formi-dable status in hk. It might even be the only real multi-application card in the world. Is Hong Kong simply lucky to be sharing in the glamor, or does the city play an indispensable role in the success story of Octopus? I believe it is the latter.

For a comparison, consider the probability of Octopus’ success in the United States. The small role of public transportation in the lives of the Americans and the relative simplicity of its fare system do not warrant the colossal cost of introducing and monitoring a new form of payment for public transportation in the u.s. In a wider context, the American society’s relatively heavy reliance on credit and the buy-now-pay-later mentality would be one of many obstacles for a prepaid card to gain popularity. Indeed, the credit card has long been a popular substitute for cash in retail payments in the u.s. but not in hk. While paying with a prepaid card is much faster and more convenient than fumbling for cash and waiting for change, it is only marginally more so than swiping a credit card and signing a receipt. Thus the existing payment culture in the u.s. leaves less room for a prepaid card to shine.

Indeed, the amazing market penetration of Octopus in Hong Kong is the product of a magic formula unique to the dynamic city. The hk people’s desire for ever higher efficiency, their obsession with convenience and their willingness to embrace new inventions raised the well-de-signed Octopus card from being a favorite means of payment for its popular public transportation to becoming a form of e-money—a considerably faster and more convenient substitute for cash in retail payments. Unless another society is able to offer a similarly nurturing environment for the development of a prepaid card, hk will continue to boast the world’s leading and most extensive contactless smartcard payment system. And who knows what next? With such a popular payment system in place, hk might well become the first cashless society in the world. /A

a “consumer updates: e-money update—the regulation of e-money issuers.” financial services authority. http://www.fsa.gov.uk/consumer/updates/updates/e_money/mn_e_money.html

b “50 great ideas for the 21st century”, august 6, 2006. the independent. http://news.independent.co.uk/world/science_tech-nology/article1213576.ece

c octopus cards ltd. website http://www.octopuscards.com/cor-porate/why/statistics/en/index.jsp

d octopus holdings ltd. website http://www.octopus.com.hk/milestones/en/index.jsp

e octopus cards ltd. website http://www.octopuscards.com/cor-porate/why/statistics/en/index.jsp

f online consumer survey of acnielson, which polled over 14,100 internet users in 28 countries across asia pacific, eu-rope and the us in october 2004. the countries are: australia, china, hong Kong, india, indonesia, Japan, Korea, malaysia, new Zealand, philippines, singapore, taiwan, thailand, viet-nam, austria, belgium, denmark, finland, france, germany, germany, italy, netherlands, norway, portugal, spain, sweden, uK, us. http://asiapacific.acnielsen.com/news/20050316.shtml

g mass transit railway website http://www.mtr.com.hk/eng/train/intro.html

the Analyst Fall 2006 Emerging Markets 11

China

Divulging Trade SecretsAlex Sloane ’09

Deng Xiaoping, former leader of the People’s Republic, went on his Southern Tour of China in 1992. His encouragement of economic reform took seed throughout the nation, and for well over a decade China has been the world’s most alluring market for foreign corporations. Pictur-ing themselves as modern-day Andrew Carnegies and J.P. Morgans, CEOs drool at the lucrative prospects that abound in China: with over 1.3 billion potential consumers, the chance of striking it big in this still-developing market seems pretty good. Accordingly, corporations and individuals have turned East in a rush that would put 1849 to shame, investing billions of dollars over the last twenty years.

But how far is too far? The fear of missing out on what is potentially the world’s biggest mar-ket has led established companies to do business in China in spite of very disadvantageous condi-tions. Let us take a look at the surprising lengths to which companies will go, in order to secure an opportunity to compete overseas.

at&t is one mega-corporation that has found a footing in China. To get there, however, it had to make a conscious sacrifice of coveted technological and managerial trade secrets. at&t entered China in 1984, when the Ministry of Posts and Telecommunications was put in charge of modernizing China’s telephone sys-tem. The goal of the upgrade was to facilitate the wider economic growth of the country. at&t, nec Corporation, and Siemens AG were all eyeing the lucrative contract, and, under such competitive conditions, were forced to divulge plans that included technology secrets to the Chinese. at&t won the contract—but the requirements didn’t stop there. at&t also had to train the employees of a Chinese “partner” company. For every dollar the foreign corpora-tion received from the Chinese government, it was required to train Chinese employees for

a proportionate amount of time. James Mc-Gregor, former Wall Street Journal China bureau chief, puts it this way: “The companies knew they were training their future competitors, but what choice did they have? The market was growing too fast, and had too much potential, to ignore. To miss out in China could jeopardize a company’s global competitiveness.” To ensure its future global competitiveness, at&t sent almost fifty Chinese executives to an American university and gave them a full year’s training at at&t and Bell labs, going beyond its training requirement in order to create additional good-will within the Chinese government.

The aircraft manufacturing industry has entered China by following a similar strategy. Boeing, foreseeing the Chinese air industry boom, has steadily built its 65% market share over the last twenty years by courting favor with the Chinese government. Boeing, like at&t, has shown a willingness to help Chinese suppliers by introducing them to its latest tech-nological advances. “Our emphasis,” said David Wang, president of Boeing China, “is that these programs should be able to add value to our Chinese partners as much as possible as soon

as they can.” Accordingly, Boeing is helping China Aviation Industry Corp I to build its own state-of-the-art jet—this government-owned aerospace company will launch a line of rival aircrafts as early as 2018. Boeing is not the only aircraft manufacturer that divulges its trade se-crets. Airbus, too, has a large presence in China. The Chinese government decides which manu-facturer to employ based not only on price, but also on the amount of technology the company is willing to share. In 1999, the u.s. Department of Commerce acknowledged this trend in a report: “u.s. aerospace companies, represented primarily by Boeing… appear to be willing to make significant concessions to Chinese state planners in co-production agreements in return for increased market access.” As a result of these practices, China has become one of the world’s largest centers for aircraft parts—but at significant initial cost to the foreign corpora-tions.

Thus, for all foreign businesses seeking to enter China, a truly formidable obstacle is the lax treatment of intellectual property laws. Corporations that release technological or trade secrets in China know that the information

Emerging Markets the Analyst Fall 200612

essentially goes public, and that battles to any other effect are futile. Pfizer, the pharmaceuti-cal giant, found out the hard way. Because the chemical compositions of many drugs are read-ily available, many Chinese companies release generic-brand drugs for which large corpora-tions hold patents. When Pfizer attempted to protect its Viagra patent by withholding details concerning the drug’s main chemical, the Chi-nese government simply denied the company’s patent application. Pfizer’s subsequent attempts to challenge this ruling in China’s court systems inevitably failed, and the resulting ill-will from the Chinese government continues to obstruct Pfizer’s place in China’s markets. For a contrast that casts Pfizer in stark relief, GlaxoSmithKline, another pharmaceutical giant, relinquished patent rights to their most successful diabetes drug, Avandia, and the Chinese government will likely respond with lenient regulations and lucrative contracts. The somewhat unfortunate conclusion seems to be that most foreign cor-porations must make great sacrifices in return for developing opportunities in China.

Tremendous initial costs, however, do have the potential to pay off big. Motorola, for ex-ample, was eager to make up for past mistakes in the Japanese market, and it jumped at the opportunity to be the first market-mover in China. The company took an enormous risk in equipping China with the latest in mobile

phone technology and cutting-edge telecom-munications infrastructure. Christopher Galvin, Motorola’s ceo at the time, knew that doing this would generate formidable Chinese com-petitors, but despite this, Motorola went ahead and did so, betting on adequate market share of the enormous population. These days, China is the largest mobile-phone market in the world. There are currently over 300 million cellular phone users in China and almost five million new subscribers every month, and the cellular telephone market is saturated—Motorola is holding its own.

The Chinese government, however, should not be blamed for taking advantage of its mar-

ket’s potential. Countries and companies, alike, have always used their advantages to improve bargaining power and win concessions. Unlike past examples, however, China is an enormous new market, and an emerging economic and military superpower. Its strength and influence are frightening. For foreign corporations, the question is merely one of profitability: they must be accurate in business projections and dynamic in strategy. Certainly the market is huge and the prospects golden, but companies must be confident that they can recover the initial costs they must first sink into China. A misjudgment can spell financial disaster—but a correct one, inconceivable heights. /A