dynamic wacc: re-enrichment of discounted cash flow

TRANSCRIPT

DYNAMIC WACC: RE-ENRICHMENT OF

DISCOUNTED CASH FLOW VALUATION TECHNIQUE

SKRIPSI

Presented in partial fulfillment of the requirements for

The Bachelor’s Degree in Accounting

By:

Nico

008201500065

FACULTY OF BUSINESS

ACCOUNTING STUDY PROGRAM

PRESIDENT UNIVERSITY

CIKARANG, BEKASI

2019

i

PLAGIARISM CHECK RESULT

DYNAMIC WACC: RE-ENRICHMENT OF DISCOUNTED CASH FLOW VALUATION TECHNIQUE

ii

iii

iv

v

vi

vii

viii

ix

x

ACKNOWLEDGEMENT

With blessing of God, the researcher has finally finished the skripsi entitled Dynamic

WACC: Re-enrichment of Discounted Cash Flow Valuation Technique. This page

thus is entitled to all of the people, friend, and colleagues who have been supporting

the researcher in finishing the skripsi. Without their supports, it is impossible for the

researcher to get to this point.

The researcher would like to show high appreciation and gratitude to all of the

individuals who are involved in the process of this skripsi writing, those individuals

are:

1. Dr. Josep Ginting, CFA as the skripsi advisor who has been guiding the

researcher to explore further about the art of researching and logical thinking

in research process,

2. The researcher’s beloved family member who have been encouraging the

researcher to do better every time the burnout comes during the skripsi writing

process,

3. Friends and colleagues from President University who have become the

source of motivation for the researcher. The researcher will never forget the

time when we motivate each other to achieve the goal together,

4. All of the examiners, lecturers, and staffs whom the researcher cannot

mention one by one, without your support, it is impossible for the researcher

to finally achieve this point.

May all of us live a happy life and achieve the goals that we have set. The researcher

will not forget the merits and contribution that you have done to the researcher.

Cikarang, 1st February 2019

Nico

xi

TABLE OF CONTENTS

PLAGIARISM CHECK RESULT ............................................................................. i

DECLARATION OF ORIGINALITY .................................................................. viii

PANEL OF EXAMINERS APPROVAL ................................................................. ix

ACKNOWLEDGEMENT .......................................................................................... x

TABLE OF CONTENTS ........................................................................................... xi

LIST OF TABLES AND FIGURES ....................................................................... xiii

ABSTRACT .............................................................................................................. xiv

INTISARI ................................................................................................................... xv

CHAPTER I: INTRODUCTION .............................................................................. 1 1.1. Background of the Study .................................................................................... 1

1.2. Problem Statement .............................................................................................. 5

1.3. Study Objectives ................................................................................................. 7

1.4. Significant of the Study ...................................................................................... 8

1.5. Organization of Writing ..................................................................................... 9

CHAPTER II: LITERATURE REVIEW ............................................................... 11 2.1. Definition of Value and Valuation ................................................................... 11

2.2. Variety of Techniques in Valuation ................................................................. 14

2.3. Valuation Using Discounted Cash Flow Technique ........................................ 18

2.4. Forecasting Cash Flows .................................................................................... 23

2.5. Capital Structure and Cost of Capital ............................................................... 26

2.6. Cost of Capital, Pecking Order Theory, and DCF Problems ........................... 30

2.7. Proposed Valuation Technique ......................................................................... 32

CHAPTER III: METHODOLOGY ........................................................................ 36

3.1. Research Design ............................................................................................... 36

3.2. Sampling Design .............................................................................................. 40

3.3. Data Collection and Data Processing ............................................................... 44

3.3.1. Conducting Preliminary Filtering and Testing .......................................... 45

xii

3.3.2. Classifying Financial Informations into Forecasting Format .................... 46

3.3.3. Forecasting the Explicit and Post-Horizon FCF ........................................ 47

3.3.4. Determining the WACC of Each Model ................................................... 49

3.3.5. Discounting FCF to NPV for Each Model ................................................ 50

3.3.6. Comparing Fair Value per Stock for Each Model with Market ................ 51

3.4. Statistical Analysis ........................................................................................... 52

CHAPTER IV: DATA ANALYSIS AND INTERPRETATION OF RESULTS 55

4.1. Data Description ............................................................................................... 55

4.2. Results and Discussion ..................................................................................... 59

4.2.1. Data Interpretation and Theoretical Integration ........................................ 59

4.2.2. Data Validation Result through Quantitative Approach ............................ 65

CHAPTER V: CONCLUSION AND RECOMMENDATION ............................ 69

5.1. Conclusion ........................................................................................................ 69

5.2. Limitations and Recommendations .................................................................. 70

5.2.1. Limitations of Dynamic WACC Model .................................................... 70

5.2.2. Recommendations for Future Research ..................................................... 71

5.3. Implications ...................................................................................................... 72

REFERENCES .......................................................................................................... 74

APPENDIX ................................................................................................................ 97

xiii

LIST OF TABLES AND FIGURES

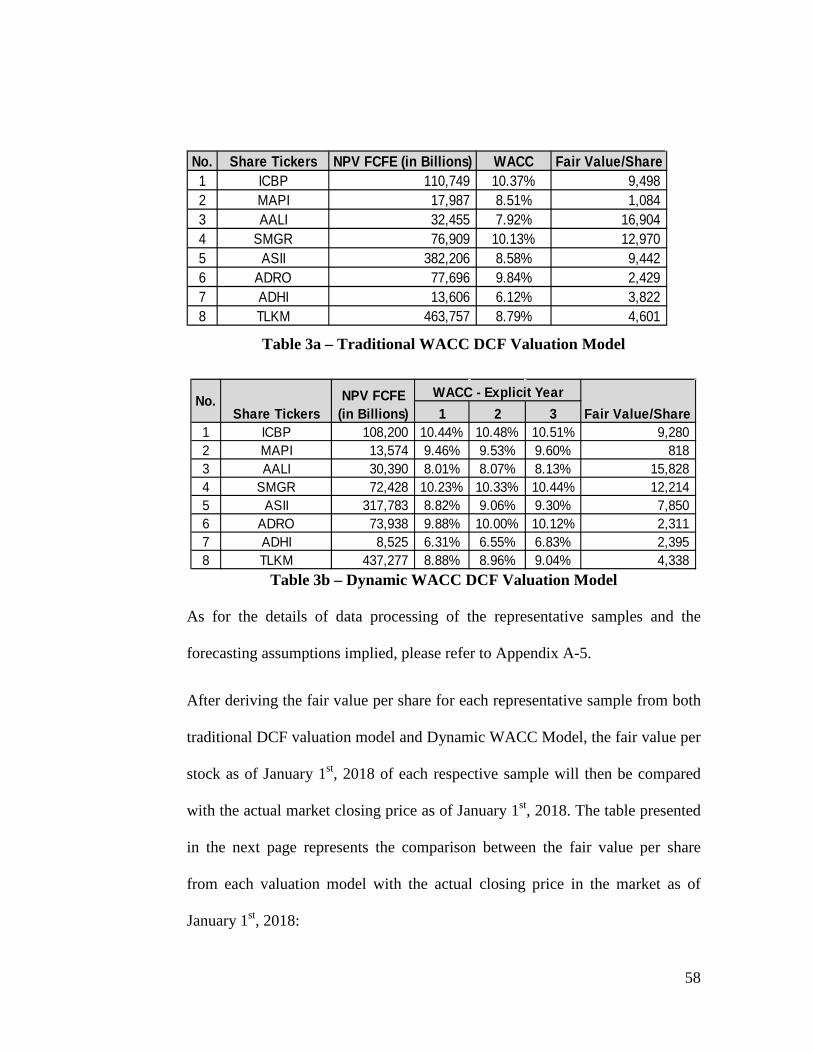

Table 1 – Representative Samples Chosen ............................................................. 55

Table 2 – Descriptive Statistics of Actual Market Price ........................................ 55

Table 3a – Traditional WACC DCF Valuation Model .......................................... 57

Table 3b – Dynamic WACC DCF Valuation Model .............................................. 57

Table 4a – Traditional WACC Model and Market Price Comparison ............... 58

Table 4b – Dynamic WACC Model and Market Price Comparison.................... 58

Table 5a – Error in Traditional WACC Model ..................................................... 59

Table 5b – Error in Dynamic WACC Model ........................................................ 59

Figure 1 – Box Plot of Actual Market Price .......................................................... 56

xiv

DYNAMIC WACC: RE-ENRICHMENT OF DISCOUNTED CASH FLOW VALUATION TECHNIQUE

ABSTRACT

The current and widely used traditional Discounted Cash Flows (“DCF”) valuation

technique implements constant Weighted Average Cost of Capital (“WACC”) as

discount factor in estimating the company’s value. However, previous studies in

firms’ financing behavior have shown that the implementation of constant WACC is

not applicable to real finance practice. Moreover, the recent studies in finance have

highlighted the importance of internal financing towards the financing behavior and

WACC of the company. In this study, the researcher would like to introduce new

DCF valuation technique which implements the dynamic WACC rather than the

constant one by emphasizing on the impact of a firm’s internal financing capability in

accordance to Pecking Order Theory. Based on the Root Mean Square Error

(“RMSE”) and Standard Error (“SE”) indicated by the statistical analysis from eight

public-listed non-financing companies from various industry sectors in Indonesia

Stock Exchange, the implementation of the dynamic WACC has better accuracy in

estimating the company’s value as indicated by the share price, aligned with the

Pecking Order Theory. Future research should develop and enrich the currently

implemented traditional DCF valuation technique from other dimensions, such as the

Free Cash Flows and the Terminal Value.

Keywords: DCF, WACC, Pecking Order Theory, Internal Financing

xv

DYNAMIC WACC: RE-ENRICHMENT OF DISCOUNTED CASH FLOW VALUATION TECHNIQUE

INTISARI

Teknik penilaian tradisional Discounted Cash Flows (“DCF”) yang saat ini

digunakan dengan luas mengimplementasikan Weighted Average Cost of Capital

(“WACC”) yang konstan sebagai faktor diskonto dalam mengestimasikan nilai

perusahaan. Namun, penelitian-penelitian sebelumnya telah menunjukan bahwa

implementasi WACC yang konstan tidak berlaku untuk praktek keuangan yang nyata

di lapangan. Selain itu, penelitian terkini di bidang keuangan telah menekankan

pentingnya pendanaan internal terhadap perilaku pendanaan dan WACC perusahaan.

Dalam penelitian ini, peneliti ingin memperkenalkan teknik penilaian DCF baru yang

mengimplementasikan WACC yang dinamis daripada konstan dengan menekankan

pada pengaruh kemampuan pendanaan internal perusahaan berdasarkan Pecking

Order Theory. Berdasarkan analisa statistik Root Mean Square Error (“RMSE”) dan

Standard Error (“SE”) yang dilakukan terhadap delapan perusahaan publik non-

keuangan di Bursa Efek Indonesia yang berasal dari beragam sektor industri,

implementasi WACC yang dinamis memiliki akurasi yang lebih baik dalam

mengestimasikan nilai perusahaan sebagaimana diindikasikan dengan harga saham,

sejalan dengan Pecking Order Theory. Penelitian selanjutnya seharusnya dapat

mengembangkan dan memperkaya teknik penilaian DCF tradisional dari dimensi-

dimensi lain, seperti Free Cash Flow dan Terminal Value.

Keywords: DCF, WACC, Pecking Order Theory, Internal Financing

1

CHAPTER I:

INTRODUCTION

1.1. Background of the Study

Valuation is one of the most commonly discussed subject in finance study and

it plays vital roles in the practices of finance fields. Damodaran (2012) stated

that valuation is commonly used in portfolio management, acquisition

analysis and corporate finance. In regards with its practice in finance field, the

studies on valuation have been also developed rapidly. Therefore, it is not

surprising that there exists various valuation techniques in finance practice. In

his paper, Fernández (2007) classified the currently implemented valuation

techniques into six which are the Balance Sheet technique, Income Statement

technique, Mixed technique, Discounted Cash Flows (“DCF”) technique,

Value Creation technique, and Options technique. Each of the valuation

technique implements different assumptions and framework in estimating the

value of an asset.

Among all of the valuation techniques mentioned above, one of the most

commonly accepted valuation technique is the DCF technique (Fernández,

2007). While Balance Sheet and Income Statement techniques focus on the

accounting earnings reported in the financial statements, DCF technique is

2

more focused in measuring the economic profit generated by the company.

Miller and Modigliani (1958) explained that the earnings generated from an

asset must be compared with the costs to obtain the respective earnings since

that will determine the “true worth” of the earnings. This concept was then

implemented in the widely used DCF valuation technique in current days.

In the DCF technique, the firm’s value is equivalent to the present value of its

expected free cash flows. This approach requires free cash flows forecasts

which are the proxies of the firm’s operation in future. After the free cash

flows have been estimated, the free cash flows will be discounted to Present

Value by using the Weighted Average Cost of Capital (“WACC”) to arrive at

the firm’s value. According to Fernández (2007), adjusting the forecasted free

cash flows with WACC to derive firm’s value reflects the “true” return for the

firm’s by utilizing the combination of debt and equity as capital. Based on the

aforementioned explanation, the implementation of DCF technique requires

quantitative process in determining the firm’s value.

Though the DCF technique involves quantitative process in determining the

firm’s value, it should be noted that the DCF method has limitation due to its

implied assumptions. One of the limitations implemented in the DCF

valuation technique is the application of WACC which then will be used as

the discount factor in the valuation technique. Since the current DCF model

3

adopts the Miller and Modigliani (1958) framework, current DCF model also

assumes that the WACC used will be constant throughout the firms’ life

cycle. This was aligned with the capital structure theory proposed by Miller

and Modigliani (1958) which stated that under perfect market condition the

changes in financing mix will not affect the WACC. The capital structure

theory proposed by Miller and Modigliani (1958) thus referred as the

“Irrelevancy Theory”.

The implementation of this constant WACC in DCF valuation technique thus

raises questions regarding the applicability of DCF model in the current

market. Myers (2001) argued that should a firm’s WACC remain constant in

spite of its financing mix, a firm will not generate any innovation in financing

instruments and there will be no development in financing strategies.

However, the proof of existing major development in the financing innovation

has become the evidence that firms consider the financing mix in order to

maximize its performance and therefore, it shows that there is a limitation in

the concept of Miller and Modigliani (1958). In addition to that, Vélez-Pareja,

Ibragimov, and Tham (2008) found out that the constant WACC does not hold

true since the WACC also depends on the discount rate of the tax shield.

While the DCF technique focuses on the firms’ financing mix which is

constituted by the composition of external financing instruments, such as debt

4

and equity instruments, there exists increasing attention in the internal

financing of the company as well. This can be seen from the research

conducted by Vogt (1994) which proved that the internal financing

capabilities could affect the investment and financing decisions of the firms.

Ross, Westerfield, Jaffe, Lim, and Tan (2015) also pointed out about the Cost

of Retained Earnings (“Kr”) which is resulted from the internal financing

capability as the component which constitutes the WACC. These literatures

imply that there should be a consideration of internal financing component in

calculating the WACC in the DCF valuation technique.

.

The current studies in valuation field are dominated with the comparative

researches which focus on proving the superiority of one valuation technique

over the others, such as the studies conducted by Sayed (2017), Courteau,

Kao, and Richardon (2000), Francis, Olson, and Oswald (2000), and Penman

and Sougiannis (1998). According to Lundholm (2001), the future research in

the valuation field must not focus on comparing the valuation techniques but

concern more on the methods to increase the accuracy of valuation technique.

The researcher believes that each of the existing valuation technique provides

estimated firm’s value based on its implied assumptions. However, the issue

with the valuation study field is to analyze whether the assumptions implied

by each valuation technique are still applicable in the practical world and

5

whether there should be any re-enrichment that can be done to increase the

accuracy of the traditional model. The study conducted by Vélez-Pareja et al

(2008) integrated the Tradeoff Theory into the traditional DCF model and

concluded that the WACC shall follow the principle of tax shield benefits. It

is interesting for the researcher to analyze the WACC assumptions from the

perspective of other capital structure theory, especially by integrating the

internal financing components into the DCF valuation model. This could

provide new framework in valuing the firms and develop the traditional DCF

model.

1.2. Problem Statement

Myers (2001) pointed out that the implementation of constant WACC in DCF

valuation technique may not be congruent with the real economic

environments that the market faces. This statement then is strengthened by the

inquiry of Vélez-Pareja et al (2008) which stated that WACC cannot be

constant due to the tax shield considerations.

The issue to be highlighted in this study would be the incorrect application of

WACC in DCF valuation. By using the constant discount rate for discounting

the expected free cash flows, it implies that the company will use the same

capital structure throughout the firm’s life. However, it should be noted that

6

the net income generated in the current year will increase the portion of equity

(internal financing capability), changing the capital structure and therefore

changing the cost of capital (WACC) to be then used as the discount factor in

discounting the free cash flows to the firm’s value. While the portion of equity

increase, under the constant cost of capital assumption, the company will be

assumed to issue more debt with the same cost of debt to maintain the current

cost of capital. However, it should be noted that issuance of debt would

depend on the company’s action and would be a matter of bias in the cash

flows forecast of the firm.

There raises questions regarding the capability for the debt holders to obtain

the exact same cost of debt in the future and the allocation of the debt

financing resources to the company’s investment. In accordance with the

Pecking Order Theory introduced by Myers (1984), for companies that have

better internal financing capability, the issuance of new debt will not be seen

as rational since the management of the firms could employ the internal

financing resources for the investment projects and therefore could conduct an

investment with lower-risk.

To sum it all, this study would like to highlight the problem of incorrect

discount factor errors due to the constant WACC implementation in DCF

valuation technique and offers new valuation model which covers the

7

weakness of the traditional DCF model. Since internal financing capability is

also one of the drivers which affect WACC, the researcher would like to

develop new constructed valuation model which focuses on the influence of

internal financing capability towards the WACC.

1.3. Study Objectives

Based on the research problems mentioned in the previous section, the

objective of this research is to develop the concept of DCF practice and

implementation which adopts the capital structure theory of Miller and

Modigliani (1958) by addressing the constant WACC problem so that the

current valuation model would be more comprehensive and accurate.

As for the constant WACC as discount factor problem, the researcher would

like to develop a model in which the WACC as discount factor will be

assumed to be changed over the forecast period by referring the equity capital

component as the function of previous equity. WACC is constructed through

the elements of capital structure and in this study, the researcher will focus on

the influence of changes in internal financing capability as the variable which

will affect the WACC.

8

This study aims to provide the readers about the logical framework behind the

traditional DCF valuation technique and the implied capital structure theory

and provide sufficient evidence regarding the better applicability of the

dynamic WACC model in terms of accuracy.

1.4. Significance of the Study

Recalling that the valuation process is one of the core subjects in the finance

study, the result of this research would be beneficial for both academicians

and practitioners in finance fields.

The result of this research would provide more insights for the academicians

regarding the exploration of alternative element in the DCF analysis approach

in the business valuation and therefore would enrich the finance literatures,

especially in terms of DCF valuation approach.

In addition to that, by emphasizing on the development of dynamic WACC,

the managements of companies will be able to utilize more comprehensive

version of DCF technique, resulting in better decision making in the business

management process.

9

The development of DCF technique offered in this research will also be

beneficial for the shareholders who provide capital to the business or

companies. The shareholders will be able to have a more accurate target value

so that they could maximize their potential return and avoid the unfavorable

investments.

Since the valuation process is also one of the core parts in the merger and

acquisition, the development of DCF approach which is widely used in the

merger and acquisition (“MnA”) deals will provide better insights for the

public accountants regarding the assessment of the fairness in the merger and

acquisition deal which then would affect the goodwill account as reported in

the Statement of Financial Position of respective company.

1.5. Organization of Writing

This research paper is organized into five chapters from Chapter I until

Chapter V. Chapter I provides the introduction about the research problems

and the background which motivates the author to write this research paper.

Chapter II provides the literature reviews which emphasize the development

of prior theories regarding the concept of valuation and DCF approach and

supporting theories in the new valuation model proposed in this study. The

proposed model will be explained after the literature reviews in “Proposed

10

Method” section. Chapter III provides the methodology including the

sampling and data processing methods in testing the validity and accuracy of

proposed method mentioned in prior section. Chapter IV provides the result of

the data processing as mentioned in prior chapter and interprets the

quantitative result of data processing. Chapter V provides the conclusion

regarding the research, limitations of the research, and the direction for the

future research.

11

CHAPTER II:

LITERATURE REVIEW

2.1. Definition of Value and Valuation

Valuation is not a new topic in the accounting and finance field of studies. It is

widely used for the purpose of measuring and understanding the value of an

asset, investment, or even a company. According to Koller, Goedhart, and

Wessels (2010), value is interpreted as the defining measurement dimension in

the market’s economy. It integrates the long-term perspective and expectations

of the market towards an asset. The term “value” can be interpreted simply as

the “true worth” of an asset. Damodaran (2012) argued that understanding the

true value of an asset is crucial since an investor shall not purchase an asset at

the price beyond its expected value.

In determining the true worth of an asset, there will be a quantitative process to

be utilized in order to estimate the value of respective asset which is referred as

“valuation”. Damodaran (2012) stated that different assets require different

information inputs and valuation techniques in order to derive the estimated

value. For example, valuing real estate property will require different details of

12

information inputs and different valuation formats from the process of valuing

publicly traded stocks.

As what has been mentioned on the first paragraph, understanding the value of

an asset would be critical since it would provide insights for investors regarding

the “ceiling” or limit that investor should pay in order to acquire those assets.

According to Damodaran (2012) and Koller, et.al (2010), there are some

practical roles of valuation in the business fields, which are:

a. In the portfolio management, understanding the value of an asset would

be useful for the long-term investors who are more focused on the firm-

specific valuation rather than the market valuation. It plays central role

for the fundamental analyst and provides peripheral role for the technical

analyst.

b. In the merger and acquisition analysis, valuation will provide the

bidding firm the fair value of the target firm before making the bid to

acquire the target firm, while for the target firm itself, the valuation will

provide them insights regarding minimum price before accepting the

deal offered by the bidding firm based on the fair value of the firm.

c. In corporate finance, understanding the value of the managed firm is

crucial since the main objective of the corporate finance is to maximize

the value of the firm. By utilizing the valuation, the managers could

13

assess the impact of their financial policies, operational policies, and

corporate strategies towards the firm’s value.

The roles of valuation are crucial not only for the practice in finance field but

also for the practice in accounting field. Since the valuation affects the financial

substance of transactions, it will directly affects the way of those transactions to

be reported which would be the main concern of accounting field.

In accordance with the Conceptual Framework of Financial Reporting, one of

the crucial issue in the accounting field is the measurement or valuation of

accounting items so that all of the economic transactions can be presented in

financial statements at the fair value. After the adoption of International

Financial Reporting Standards (IFRS) in accounting practice, the fair value

concept which is explained in the International Accounting Standard (IAS) 39 is

heavily implemented in the financial reporting since it would increase the value

relevance of the informations provided in the financial reports for the decision

making process done by the users. In Indonesia which adopts the IFRS, the

importance of valuation is also recognized through the Pernyataan Standar

Akuntansi Keuangan (PSAK) 68 regarding the Fair Value Measurement.

It should be noted that even though valuation involves complex and analytical

process in order to derive the expected value of an asset, there are some pitfalls

that must be taken into the considerations according to Damodaran (2012):

14

a. Valuation is not a pure science in which its proponents make it out to be

or will result in a pure objective true value. Even though the valuation

process involves quantitative model, however, the information inputs

might be colored with highly subjective bias. Therefore, it is important

to reduce the bias in the process of valuing an asset,

b. Valuation process is not timeless which means the derived value from

previous valuation may be changed due to the new information reveal in

the market which then will affect the perspective of an asset’s value,

c. Valuation doesn’t provide precise value since all of the inputs are in

form of estimation as well,

d. Good valuation doesn’t require complex quantitative model. Providing

too much financial details may result in the bias of input errors as well.

For the simplicity purposes, Koller, et al (2010) pointed out that the key

drivers of value creation are the growth and return on invested capital,

e. Good valuation shall not ignore the perspectives of other investors in the

current market and,

f. The most important thing about valuation is the process rather than the

outputs.

2.2. Variety of Techniques in Valuation

15

Recalling that different assets require different information inputs and formats,

the valuation process can be classified into various techniques. Every valuation

techniques implies different concepts and approaches in order to estimate the

value of an asset, investment, or company. Based on the valuation objects and

techniques, Fernández (2007) classified the valuation techniques as follow:

a. Balance Sheet Technique

This technique implies that the value of a company would be equivalent

to the amount that is reflected in the company’s balance sheet without

considering the market’s condition, human resources, or other

organizational issues in the future which are not depicted in the

company’s balance sheet. There are so many indicators that can be used

for this balance sheet technique and one of the most common indicator

would be the book value of the company which is defined as the

difference between the total assets and liabilities.

b. Income Statement Technique

This techniques implies that the value of the company would be shown

by the income indicators such as earnings, sales, or other indicators.

Unlike balance sheet technique which is derived from pure accounting

value, the income statements techniques emphasized on the comparison

16

of multiples by comparing the accounting income indicators with the

other relevant market indicator, commonly market price to derive a ratio.

It implies that the value of a company would be at the multiples of its

income indicators.

Until now, this technique is still used for providing quick valuation

insights regarding a company due to its simplicity in process. One of the

most commonly used multiple in finance practice would be the Price-

Earning Ratio (PER) in which the share value of a company would be the

multiples of its earnings.

c. Mixed (Goodwill) Valuation Technique

Since balance sheet method don’t provide insights regarding the impact

of non-accounting items towards the value of the company, the mixed

valuation method is formulated. This techniques implies that the value of

a company is equivalent to the sum of its accounting net assets value and

its goodwill. The “classic” goodwill valuation is expressed in form of the

equation below:

𝑽 = 𝐀 + (𝒏 × 𝑩) or 𝑽 = 𝐀 + (𝒛 × 𝑭)

Where A= net assets value, n=coefficient (1.5-3), B= net income,

z= percentage of sales, F= sales turnover.

17

The first formula is commonly used for manufacturing companies while

the second formula is commonly used for retail companies. This

techniques implies that the goodwill of a company is derived from a

multiples of an economic indicator and will be added to the substantial

net asset value.

d. Discounted Cash Flows Technique

This technique seeks to determine company’s value by forecasting the

expected cash flows in the future and then discount them to the present

value by using certain discount factor which reflects the risk.

Up to now, this method is the most commonly used in the fundamental

analysis due to its rational concept and its generality to be used in valuing

not only equity instruments or companies but also most of the financial

instruments including debt instruments.

The discounted cash flow valuation formula is depicted as follow:

𝑉 =𝐶𝐹1

(1 + 𝑘)1 +𝐶𝐹2

(1 + 𝑘)2 +𝐶𝐹3

(1 + 𝑘)3 + ⋯+𝐶𝐹𝑛 + 𝐶𝑅𝑛(1 + 𝑘)𝑛

Where V= value of the company, CF= expected cash flows in the future,

k= discount factor, n= forecast period, and CR= terminal cash flow.

e. Value Creation Technique

This technique implies that the value of a company could be assessed

from the excess of returns it generated from the capital employed in its

18

operation. One of the most common indicators to be used in this

technique is the Economic Value Added (EVA) indicator. According to

Chen and Dodd (1997), the formula of EVA is depicted as follow:

𝐸𝑉𝐴 = (𝑅𝑜𝐼𝐶 − 𝐶𝑜𝐶) × 𝐶

Where EVA= Economic Value Added, RoIC= return on invested capital,

CoC= Cost of Capital, C= total capital employed

This EVA valuation though cannot be used as the proxy in the market

price like Discounted Cash Flow Technique. It only provides a sole

amount which then can be used to determine the performance of the

company.

f. Black-Scholes-Merton Technique

This technique is only applicable to the option instrument in which the

option price will be affected by the underlying instruments and therefore

requires considerations regarding the changes in the underlying option

instruments. After the establishment of Black-Scholes model in the

option pricing in 1973, Merton (1976) provided additional insights

regarding the option pricing for discontinuous stock price return and

creating Black-Scholes-Merton model. The formula is depicted as below:

𝐹(𝑆, 𝜏) = �𝑃𝑛(𝜏)𝜀𝑛{𝑊(𝑉𝑛, 𝜏;𝐸,𝜎2, 𝑟)}∞

𝑛=0

19

2.3. Valuation Using Discounted Cash Flow Technique

As mentioned in the previous section, Discounted Cash Flow (DCF) technique

implies that the value of a company is derived by discounting the expected cash

flows in the future by using certain discount factor which reflects the risk. The

formula of DCF technique is depicted as follow:

𝑉 =𝐶𝐹1

(1 + 𝑘)1 +𝐶𝐹2

(1 + 𝑘)2 +𝐶𝐹3

(1 + 𝑘)3 + ⋯+𝐶𝐹𝑛 + 𝐶𝑅𝑛

(1 + 𝑘)𝑛

Where V= value of the company, CF= expected cash flows in the future,

k= discount factor, n= forecast period, CR= terminal cash flow.

The core concept of DCF is aligned with the economic theory introduced by

Miller and Modigliani (1958) which stated that the value of an asset should be

perceived from economic perspective rather than solely accounting perspective

by taking into the account the risk factor.

Based on the formula depicted above, the value derived from the DCF valuation

technique is influenced by several factors which are:

a. Forecasted Cash Flow, this variable is the expected cash flows in the

future which act as numerators in the DCF formula. To be specific,

the forecasted cash flows discussed in DCF formula are the Free Cash

Flows which are derived from the reconciliation of some accounting

items. In the implementation of cash flows forecast, the free cash

20

flows would be forecasted for several period which is referred by

Jennergren (2008) as the explicit period while the rest of free cash

flows will be presented in terms of lump sum which reflects the post-

horizon period of free cash flows. Depending on the type of DCF

valuation implemented, the reconciliation process to arrive at the free

cash flows amount will be different.

b. Discount Factor, this variable reflects the risk in respect to the

forecasted free cash flows. By implementing the discount factor as

the denominator, the expected free cash flows in the future will be

brought back to its present value which represents the value of the

future free cash flows as in the present. Depending on the type of

DCF valuation implemented, the determination of the discount factor

will be different as well.

c. Period, this variable shows the so-called “explicit” cash flow period

in which the free cash flows are predicted explicitly by using given

assumptions. The remaining of the forecasted free cash flows will be

presented in lump sum with the basis of the latest forecasted free cash

flows in the explicit period. The lump-sum amount which represents

the rest of the forecasted cash flows is referred by Jennergren (2008)

as the post-horizon forecasted cash flows period.

21

According to Damodaran (2012), the Discounted Cash Flows valuation

technique may also be classified into two techniques in accordance with the

purpose of the valuation, they are Free Cash Flows to Equity (FCFE) technique

and Free Cash Flows to Firm (FCFF) technique. Both of those DCF techniques

provides different approach in deriving the value of a company, however,

theoretically speaking, the value derived from both approach shall be the same.

The implementation of different DCF techniques will result in different process

of reconciling the free cash flows and different discount factor to be used.

Free Cash Flow to Equity (FCFE) technique reflects only the value of the equity

holders of the company. It reflects the value of the company from the perspective

of the shareholders and excluding the claim from the debt holders in the

company. The FCFE is commonly used to determine the value of a company’s

stock and fundamentally provides insights regarding the “intrinsic value” of a

company’s stock to be then compared with the current market price. By

implementing the FCFE technique, the reconciliations of forecasted free cash

flows shall start from the Net Operating Profit After Tax (Koller, et al, 2010) of

the company which reflects the residual claim of the shareholders towards the

results of the company’s operation after deducted by the claim of the debt

holders which is in form of interest expense. As for the discount factor, the Cost

of Equity will be used to discount all of the FCFE to the present value. Further

22

literatures about the FCFE reconciliations and Cost of Equity will be discussed

in the next sections.

Free Cash Flow to Firm (FCFF) technique reflects the value of both the equity

and debt holders of the company. It reflects the value of the company from the

perspective of all capital holders in the company. The FCFF is commonly used

in the merger and acquisition analysis since both of the bidding and target firms

would like to know the value of the company as a whole rather than solely the

value of the company’s share. Implementing the FCFF in acquisition analysis

would also provide better insights regarding the impact of current capital

structure towards the value of the company.

By implementing the FCFF technique, the reconciliations of forecasted free cash

flows shall start from the Earnings Before Interest and Taxes (EBIT) of the

company which reflects the results of the company’s operation before deducted

by the claim of the debt holders which is in form of interest expense and also the

tax component. As for the discount factor, the Weighted Average Cost of Capital

(WACC) will be used to discount all of the FCFF to the present value. Further

literatures about the FCFF reconciliations and Weighted Average Cost of Capital

will be discussed in the next sections.

Even though the classification and formats of DCF technique are quite

distinguishable, Koller et al (2010) stated that there is a pitfall in the

implementation of DCF technique which would be about the matching between

23

the free cash flows and the discount factor for the FCFE technique. In FCFE

technique, it must be ensured that the free cash flows streams which act as the

numerator is actually resulted only from the equity capital and not debt capital.

FCFE technique will not be an issue if the company utilizes 100% equity capital

for the company’s operations but in the reality, most companies used the mix of

debt and equity as the capital and therefore it is very hard to trace the “real” free

cash flows from equity capital. To solve this issue, Koller et al (2010) suggested

that to arrive at the value of share price of the company, the valuation shall start

from the FCFF technique and by the end of the process, the firm value will be

deducted by the market value of the debt which represents the claim of the debt

holders to arrive at the share value for the equity holders’ claim.

2.4. Forecasting Cash Flows

In the DCF technique, the expected free cash flows in the future will be

discounted back to the present value, therefore, the forecasted free cash flows

would be one of the influencing variables in the DCF. According to Weygandt et

al (2010), the term “free cash flows” is defined as the excess of the operating

cash flows after deducted by the investment for non-current assets to be then

utilized in the operations of the company. It is mathematically expressed as

follow:

24

𝐹𝐶𝐹 = 𝐶𝐹𝑂 − 𝐶𝐹𝐼

Where FCF= free cash flows, CFO= operating cash flows, and CFI= investment

cash flows.

The excess represents the cash available for the capital holders of the company

and therefore, the free cash flows are perceived as proxy of value by capital

holders to determine company’s value since the free cash flows represent the

excess cash from the operation which are available to the capital holders. Thus,

this framework becomes the rationale of the DCF technique.

As what has been explained in the previous section, in order to derive the

numerator of DCF technique which is the free cash flows, a reconciliation

process of accounting earnings is required. Depending on the DCF technique

implemented and the desired goals of valuation, the free cash flows for each

respective technique will be derived by using different reconciliation process and

resulting in different amount of FCF.

For FCFE technique, the highlight of the valuation issue would be to determine

the company’s value from the perspective of the shareholders, the ones who

inject equity capital into the company (Damodaran, 2012). Therefore, the free

cash flows should represent the available claims only for the shareholders after

deducted by the claim of the debt holders. The reconciliation of free cash flows

of FCFE would start from the Net Operating Profit After Tax (NOPAT), adjusted

25

by the non-cash operating expenses such as amortization and depreciation. After

that it will be deducted by the reinvestment needs in both long-term assets and

working capital.

For FCFF technique, the highlight of the valuation issue would be to determine

the company’s value from the perspective of all capital holders, including both

debt holders and equity holders (Damodaran, 2012). Therefore, the free cash

flows should represent the available claims for all of the capital holders. The

reconciliation of free cash flows of FCFF would start from the Earnings Before

Interest and Taxes (EBIT), adjusted by tax expense and non-cash operating

expense such as amortization and depreciation. After that it will be deducted by

the reinvestment need in both long-term assets and working capital.

In addition to the reconciliation of free cash flows, the forecasting of FCF in

DCF technique can be classified into the explicit period and post-horizon period

(Jennergren, 2008). In the explicit period forecasting, the free cash flows are

forecasted based on the future assumptions implied by the analysts while in the

post-horizon forecasting, the free cash flows are presented as a lump sum which

is derived from the calculation of perpetuity based on the last explicit period

forecasting (Jennergren, 2008). The lump sum of FCF in the indefinite period is

commonly referred as “Terminal Value” (Damodaran, 2012). The

implementation of post-horizon period forecasting assumes that business will be

26

going-concern and continues to operate and generate cash flows for an undefined

period.

Another issue that could be highlighted in the forecasting of free cash flows is

the quality of analysts’ cash flow forecasts. According to Givoly, Hayn, and

Lehavy (2009), the analysts’ cash flow forecast quality has less accuracy

compared with the analysts’ earnings forecast. The analysts’ cash flow forecast

is weakly associated with the stock price movement and thus reflecting that the

analysts’ cash flow forecast can be considered as the so-called “naïve” extension

of analysts’ forecast (Givoly et al, 2009).

In addition to that, the research conducted by Walther and Willis (2013)

suggested that there is an influence of investor sentiment towards the analysts’

bias in forecasting which will result in optimistic approach and least accurate

forecasts.

2.5. Capital Structure and Cost of Capital

While the free cash flows are the numerators in the DCF formula which reflects

the expected benefits in the future that can be claimed by whether the equity

holders or all capital holders, the cost of capital is acting as the denominator in

the DCF formula which adjusts those expected benefits as quoted in present

value.

27

According to a widely used theory of capital structure proposed by Miller and

Modigliani (1958), the accounting profits are not the same with the economic

profits. One of the factors that need to be considered is the risk in which the

profits bear. The return of an investment shall be defined as profit if it exceeds

the risks of respective investment.

In the DCF technique, the free cash flows expected in the future are discounted

by the discount factor to bring the value of those expected free cash flows in the

future as in present value after taking into the account the risks related in

obtaining the free cash flows (Berk, et al, 2015). This framework is aligned with

the core postulate in finance which states that a “risky” dollar will be less

valuable compared with “safer” dollar.

As what has been mentioned in the previous section, different DCF technique

will require different discount factor as well. As for the FCFE, since the focus

of valuation would be from the perspective of the equity holders, the discount

factor applied in the FCFE would be the cost of equity that is derived from

Capital Asset Pricing Model (CAPM) (Fazzini, 2018). The CAPM formula is

presented as follow:

𝐾𝑒 = 𝑅𝑓 + (𝑅𝑚 − 𝑅𝑓) × 𝛽

Where Ke= cost of equity, Rf= risk free, Rm= market risk, β= correlation for

unsystematic risk.

28

The CAPM formula implies that the risk of equity holder would be the same as

the sum of risk free and a risk premium related with the respective company’s

share. This “risk” then will adjust the perception of equity holders towards the

expected free cash flows in the future through the desired minimum return since

they are allocating the financial resources to risky investment. (Fazzini, 2018).

In addition to the external equity sources of the company, the studies in finance

have developed increasing attention on the internal financing sources of the

company which is commonly called the “Cost of Retained Earnings”. Berk et al

(2015) states that the cost of retained earnings will be the same with the cost of

external equity since the internal company’s financing resources are actually the

company’s profit that is not distributed as dividends to the equity holders and

retained for the operation of the company. Therefore, the equity holders expect

a certain level of return from that undistributed dividends and it is reflected as

the same cost of equity. In this study, the term cost of equity will refer to the

combination of both internal and external equity financing resources.

As for the FCFF technique, the discount factor implied would be the so-called

Weighted Average Cost of Capital (WACC) which is the weighted average of

risks entitled in the capitals employed by the company since the main concern

of this technique would be the perspectives of all capital investors in the

company (Fazzini, 2018). This means the WACC will also incorporate the costs

incurred for debt financing. The formula is presented as below:

29

𝐾𝑐 = (𝐾𝑒 × 𝐸) + (𝐾𝑑 × (1 − 𝐸))

Where Kc= weighted average cost of capital, Ke= cost of equity, E= weight of

equity towards the capital employed, Kd= after-tax cost of debt,

(1-E)= weight of debt towards the capital employed. Based on the formula

above, it is clear that the costs of capital is highly influenced by the composition

of the capital structure in the company.

As for the theory of capital structure, there are some theories which are still

implemented currently. These theories of capital structure reflects the financing

behavior of each firm and how the financing strategies are used by the financial

managers to maximize the company’s value. According to Myers (2001), there

are some theories of capital structure which are:

a. Tradeoff Theory which states that the optimal capital structure will seek a

way to balance the tax advantages obtained from the debt financing with

the cost of financial distress.

b. Pecking Order Theory which states that the financing strategy of a

company will start from the safer financing instruments to risky

instruments (from internal funds to additional issuance of equity).

c. Free Cash Flow Theory which states that dangerous leverage effect

would be favorable for the value of the company.

30

d. Irrelevant Theory of Miller-Modigliani (1958) which states the capital

structure will not change the cost of capital and influence the initial value

of the company whatsoever.

From the dimension of discount factor, there are some issues that the

researchers had been pointed out. According to Koller et al (2010), predicting

the capital structure of a company, especially for the long-term period, might

not be possible since the issuance of new financing instruments is the corporate

action taken by the company. To tackle this issue, Koller et al (2010) suggested

that the debt instruments shall be forecasted under the same level for the future

forecast, implying that the current level of debt would provide enough leverage

for the operation in the future. On their research, Vélez-Pareja, Ibragimov, and

Tham (2008) had pointed out that the assumptions of constant discount factor is

misleading. A constant discount factor implies constant capital structure and

this cannot be true for most of the scenarios.

2.6. Cost of Capital, Pecking Order Theory, and DCF Problems

According to the historical evaluation conducted by Parker (1968), the early

concept of Discounted Cash Flows was found in Old Babylonian period (1800-

1600 B.C.) in Mesopotamia to be then widely used in actuarial science and

economy from 1200s until 1900s. In 1930, Fisher introduced the Theory of

31

Interest which explains the basic concepts of representing the future cash flows

as the present value. In 1950s, the implementation of discounted cash flows

began to be used widely due to the theoretical contribution by researchers such

as F. and V. Lutz, J. Hirshleifer, J.H Lorie and L.J Savage, Miller and

Modigliani, and Ezra Solomon while in 1959, the term internal rate of return was

popularized by Joel Dean.

Based on the historical development mentioned by Parker (1968), the theories in

1950s such as Miller and Modigliani (1958) theory had been adopted in the

implementation of Discounted Cash Flows valuation. As what is mentioned by

Myers (2001), the Miller and Modigliani (1958) assumes that company’s cost of

capital will be constant over the time and there would be no “magic” of financial

leverage towards the value of the company. This proposition is proven by

solving the cost of equity components in Weighted Average Cost of Capital

(WACC) which is presented as follow:

𝐾𝑒 = 𝐾𝑐 + (𝐾𝑐 − 𝐾𝑑) ×𝐷𝐸

The solving implies that any choices to inject debt with lower cost will result in

increasing “hurdle rate” of equity investors which is high enough to balance the

cost of capital and resulting in constant amount. Therefore, the adoption of this

theory in DCF valuation will justify the implementation of constant WACC as

discount factor.

32

While Miller-Modigliani (1958) argued that the capital structure is not

influencing the value whatsoever, Pecking Order Theory proposed by Myers

(1984) argued that due to the information asymmetries between investors and

managers, the company will tend to use internal funds first since the information

disclosure will happen for external financing. In addition to that, the managers

will focus on the safer financing instruments first to finance the company.

According to the research conducted Yulianto, Suseno, and Widiyanto (2017),

there exists applicability of Pecking Order Theory in the Indonesia’s companies

in spite of the fact that the results support weak form of Pecking Order Theory.

Up to now, many studies such as Baskin (1989) and Frank and Goyal (2003)

have proved that there is still no consistent evidence regarding the external firms’

financing behavior in accordance with the Pecking Order Theory. Yulianto et al

(2017) pointed out that one of the causes could be the market timing effect in the

decision of capital market structure. Unlike the external financing dimensions in

Pecking Order Theory, the internal financing dimension studies in Pecking

Order Theory obtained more robust and consistent result.

Vogt (1994) stated that the internal financing of a company affects the

investment decision of the company and had become alternative in the capital

structure while the recent research of Chen (2011) stated that the internal

financing is used for funding the company’s investment and thus it will change

the way investment behavior of the firm as well. In addition to that, Noor, Sinaga,

33

and Maulana (2015) also stated that companies listed in Indonesia, especially in

the agriculture sector, are applying the Pecking Order Theory in financing their

investment starting from the cheapest one, which is the internal financing. Study

of Noor et al (2015) also pointed out that the external financing will only be

issued if the company has internal financing deficit.

2.7. Proposed Valuation Technique

As what has been mentioned in the previous sub-section, Vélez-Pareja et al

(2008) argued that the implementation of constant cost of capital is misleading

and doesn’t reflect the economic reality. Though, the current practice of DCF

valuation technique still implements constant cost of capital as the discount

factor in deriving the present value of the free cash flows.

While the latest research of Vélez-Pareja et al (2008) had proposed a valuation

model which implied Tradeoff Theory in which they took into the account the

marginal benefits of the tax shield which will affect the capital structure and

therefore cost of capital, there is still no valuation model proposed regarding the

effects of internal financing as from the Pecking Order Theory towards the

change in capital structure and therefore the costs of capital to be then used in the

DCF valuation model.

34

The author would like to propose a DCF valuation model which will integrate

the effect of internal financing towards the costs of capital. The results of the

model and implication of using this model will be then explained in Chapter IV:

Results.

The model which is proposed by the researcher is as follows:

𝐾𝑐 = 𝐾𝑒 ∗ 𝐸𝑛−1 ∗ (1 + 𝑆𝑛)𝑛

𝐷 + 𝐸𝑛−1 ∗ (1 + 𝑆𝑛)𝑛 + 𝐾𝑑 ∗ (1 − 𝑇) ∗ 𝐷

𝐷 + 𝐸𝑛−1 ∗ (1 + 𝑆𝑛)𝑛

Where Ke= cost of equity, Kd= cost of debt, En-1= equity position from prior

year, D= debt position from the last year, Sn= rate of equity growth in the next

year, T=Tax.

The model proposed above is for the determination of costs of capital to be then

used in the DCF valuation model. The increase in equity position from last year

will be assumed from purely the increase of internal financing from the retained

earnings which is part of the equity while the debt level will be assumed at

constant level as in accordance with suggestion of Koller et al (2010) regarding

the forecast of corporate actions.

The fundamental of the model is to adjust the cost of capital from the increase

of internal financing and eliminating the effect of leverage to derive the value of

the company in case it utilizes current debt level with capabilities to grow

internal funds in the future. This can be seen from the return generated by the

company which is then retained as the part of equity. The changes in the

35

retained earnings thus changes the capital structure and therefore, dynamic

discount factor may be more appropriate rather than the constant one.

The implementation of dynamic cost of capital model could provide some

advantages as follows:

1. The capability of the model to capture and integrate the growth of internal

financing capacity and resources of the company towards the company’s

value;

2. The value derived from the dynamic WACC model will reflect the true

value of the company which represents the value of the company by relying

on its internal strength rather than the external financing capabilities. The

traditional model doesn’t only take into the account the operation of the

company as the proxy of value but also the additional cash flows from

external financing which then will be discounted and mislead the users who

perceive the capital injection as the increasing of value in the company;

3. The dynamic WACC model implies lower subjective assumptions about the

capital structure in the future and therefore a great valuation technique for

conservative company’s value analysis.

Like the other valuation techniques, the dynamic WACC model also implies

certain assumptions and therefore imposes several limitations for its

implementation in the practice. The limitations can be listed down as follows:

36

1. Due to its conservative nature of valuation, the dynamic WACC model may

undervalued startups firms with lower capability to generate internal

financing or even tend to have negative cash flow;

2. The dynamic WACC model doesn’t cover the valuation framework of

financial institutions due to its difference in nature of business and financial

structure;

3. Since this model covers only the analysis on the changes of WACC, there

could be some limitations on the other components of DCF analysis which

then could become the opportunity for the future researchers to be analyzed

further.

CHAPTER III:

METHODOLOGY

3.1. Research Design

This study implements the mixed method in constructing the model and testing

the constructed model. According to Sekaran (2016), mixed method is

implemented in a research to provide answers that cannot be provided solely by

implementing whether quantitative or qualitative approach alone. The

implementation of mixed method in a research requires both inductive and

37

deductive thinking, using multiple research methods or theories to provide

answers for the research problem using different inputs. Wiggins (2011) stated

that there is no rigid methodological approaches in conducting the mixed method

research. In addition to that, Tashakkori and Creswell (2007) argued that mixed

method research could provide more comprehensive understanding regarding a

phenomenon due to the combination of both qualitative and quantitative

approaches in analyzing a phenomenon which will result in offsetting the

weaknesses of each.

Wiggins (2011) stated that there are three ways to mix the qualitative and

quantitative methods, they are:

a. Triangulation which is simply defined as the utilization of multiple

methods to increase validity of a study,

b. Demarcation which is defined as the process of relating both the

qualitative and quantitative approaches in which one approach is used as

the dominant method while the other is used as the supporting method,

c. Reclassification which is referred as the application of how to utilize

both quantitative and qualitative methods so that they can be used as

exploratory and confirmatory ways.

According to Sekaran (2016), even though mixed methods could provide some

advantages for the research process, on the other hand the implementation of

mixed methods research will result in more complex research design and

38

therefore demands for comprehensive and clear explanation to enable the readers

to differentiate and understand each research component.

In this study, the researcher implemented the mixed methods model due to its

competitive advantage of explaining a particular phenomenon from the

perspectives of both quantitative and qualitative approaches. There were some

additional considerations that had been taken into the account by the researcher

and therefore had become the rationale for the researcher to implement mixed

methods approach in the study.

The first consideration is about the purpose of this research. The purposes of this

research is to develop new DCF valuation model and provide new insights for

the readers regarding the concept of DCF valuation. To achieve the purposes, the

researcher was concerned in both the conceptual framework of model

construction and the process of proving the accuracy of the model constructed.

The explanation of the conceptual framework of model construction requires

qualitative approach which analyzes and contrasts the existing capital structure

theories while the process of providing sufficient evidence regarding the model’s

accuracy requires quantitative approach which utilizes statistic analysis.

The second consideration would be about the type of data sources to be then

used as the basis of deriving the model and testing the accuracy. The data

sources which were taken for this study are in form of theories, hypothesis, and

secondary data. The implementation of qualitative approach alone will not be

39

sufficient for the researcher since it will provide a limitation regarding the

processing of secondary data as the evidence of the model’s accuracy while the

implementation of quantitative approach alone will also not be sufficient for the

research since it will provide a limitation regarding the comprehensiveness and

conceptual framework of the model construction which then can only be

comprehended by utilizing the theoretical integration provided in qualitative

approach.

In addition to that, the mixed method implied in this research can be classified as

the triangulation method in which the process of model constructing was done by

using qualitative approach in order to provide comprehensive logical flow and

then the validity of the constructed model was tested using quantitative approach.

Even though commonly, the qualitative approach focuses on the theory-building

approach, the implementation of theoretical integration approach in qualitative

research is also common (e.g.: Aselage and Eisenberger (2003) regarding the

perceived organizational support and psychological contracts, Rosso, Dekas, and

Wrzesniewski (2010) regarding the meaning of work, and other researches which

commonly focuses on behavioral and psychological researches). In this study,

the construction of model was rooted from the theoretical integration of firms’

financing behavior which up until now has been developed to several

independent theories as explained in Chapter II.

40

On the other side, the quantitative model was used as the supporting method in

which the process of providing sufficient evidence was done by utilizing

statistical analysis to ensure that there exists higher accuracy in the constructed

model compared with the traditional one. In addition to that, the implementation

of quantitative approach is also implemented in the process of sampling design

which will be explained in the next section.

To sum it all, the researcher implements mixed methods to conduct the research.

The research process will be done by using the triangulation mixing approach in

which the qualitative approach will be utilized in explaining the conceptual

framework of the DCF valuation model while the quantitative approach will be

utilized as the tool in providing sufficient evidence regarding the accuracy of the

model compared with the traditional one.

3.2. Sampling Design

In determining the samples, the researcher had set several criteria and scope

limitations to ensure that the samples selected are representative, valid, reliable,

and aligned with the purpose of the research.

As for the source of data, the researcher selected companies listed in Indonesia

Stock Exchange (IDX). The considerations for the researcher to select companies

listed in Indonesia Stock Exchange are not only due to the accessibility of the

secondary data but also the internal reliability and validity of the data. According

41

to Seale (1999), reliability and validity of the research are the crucial part which

ensures the trustworthiness.

The financial reporting of companies listed in IDX must follow regulation

implemented by Financial Services Authority (Otoritas Jasa Keuangan/ OJK)

regarding the financial reporting standards reflected in Regulation No.

KEP-347. In the Regulation No. KEP-347, it is stated that all financial reporting

for companies listed in IDX must follow the Statement of Financial Accounting

Standards of Indonesia (Pernyataan Standar Akuntansi Keuangan/ PSAK) which

has adopted the International Financial Accounting Standards (IFRS). By

following the unified measurements of financial reporting which is PSAK, all

accounting items reported in the financial reports are measured by using

consistent and representative measurement which therefore guarantees the

internal reliability and validity of the secondary data.

The companies taken in this study were from non-financial institutions. The

exclusion of financial institutions was done due to the differences of valuation

approach of financial institutions. According to Damodaran (2012), in non-

financial institutions, debts are perceived as the source of capital for the

operation of the companies while for financial institutions, debts are perceived as

the “raw materials” which then could be processed then sold at the higher price.

Thus, there is a vague definition for the source of capital for financial institutions

which doesn’t match with the framework of model constructed by the researcher.

42

In addition to that, Damodaran (2012) explained that the reinvestment of

financial institutions is different with non-financial institutions. While non-

financial institutions reinvest in fixed assets and working capital to support and

expand the operation, financial institutions reinvest heavily in intangible assets

such as brands and reputation. Thus, the problem in determining the

reinvestment rate could become challenges in determining the forecasted free

cash flows which is used in this model as well.

After the process of narrowing the samples’ scope, the next step would be to

determine the sample size. In this study, the researcher took eight public listed

companies in IDX which represents each of nine business industries listed in

Jakarta Stock Industrial Classification (JASICA), except for financial industries.

The researcher was aware that the determination of sample size in quantitative

research commonly requires a set of statistical guideline to ensure that the

number of selected samples are representative and therefore could lead to a valid

research conclusion, such as Hair (2010) or Burmeister and Aitken (2012).

However, it is worth mentioning that the quantitative process in this research was

utilized to obtain supporting evidence for the qualitative theoretical integration

and therefore the selection of samples follows the framework of qualitative

research to provide in-depth understanding regarding a phenomenon. Jason and

Glenwick (2016) stated that unlike quantitative research, the process of data

collection and analysis of qualitative research is interrelated. There are certain

43

points in the data collection and analysis of qualitative research which are

saturation and extension (Crabtree and Miller, 1999). Saturation refers to a

condition in which the addition of new data or sample will not provide new

understanding of the phenomenon while extension refers to a condition in which

the addition of new data or sample will provide new comprehension regarding

the study object.

The researcher argues that the selection of eight samples in this study has

reached a saturation point from the qualitative perspective since it already

provides sufficient understanding regarding the mechanism of constructed model

in each industries in JASICA, excluding the financial institutions. As long as the

limitation and mechanism of the constructed model are followed, the results

obtained within each population will be the same and the addition of new

samples will not be value-adding to the understanding of the results in the

constructed model.

To ensure that the selected companies of each industry are representative, there

are some filtering processes and criteria conducted as the basis of sample

selection. After the preliminary filtering, the representative samples were taken

by random sampling. The followings are criteria for the selection of

representative samples:

a. Completeness of financial information from year 2015-2017,

44

b. Exclusion of any negative equity total amount whether due to financial

distress or other causes. According to Damodaran (2012), distressed

companies require different valuation approach which is not integrated

in the constructed model,

c. Comparison test of Price-Earning Ratio (PER). According to Basu

(1975), PER implies the expectation of the investors regarding the

growth of respective companies and sometimes may be biased due to

information asymmetry. By ensuring that the PER of selected

companies are in range with the industries, the perspective of the

investors in the market regarding the fair value of the share will not be

biased.

After the determination of sample size, the next issue in the sampling design is

the determination of time-horizon. This study took three-year time horizon for

each representative sample. As what has been mentioned in the literature review,

the DCF valuation is influenced by risk perception of equity investors reflected

in the equation as the discount factor (cost of equity) and also the forecasted free

cash flows. The forecasted free cash flows are derived from the growth

assumptions regarding the prior performance of the company. Since

macroeconomic condition affects the company’s performance, therefore to avoid

bias for free cash flows forecast, the researcher took three years of time horizon

considering the similar pattern of macroeconomic condition throughout the years.

45

According to Statistics Bureau of Indonesia, the year-on-year (YoY) growth of

Indonesia’s GDP from 2015-2017 ranges from 4.88% to 5.07%, implying similar

macroeconomic condition pattern throughout the years. In addition to that, the

increasing of Bank Indonesia’s 7-Days Repo Rate in 2018 implies that there was

a changes in macroeconomic condition in 2018 and therefore, to adjust the effect

of this changes, the basis of years input for forecasting should be limited.

In overall, this study took samples of eight public listed companies in IDX which

are the representatives of each industry in JASICA. As for each sample taken,

the input for forecast years is deemed as three-years-time-horizon due to the

similar macroeconomic pattern which implies the similarity of both the

perception of risk from the investors and the companies’ performance. As for the

collection and analysis of the samples taken will be explained in the next section.

3.3. Data Collection and Processing

The steps of data collection and processing conducted in this study utilizes the

DCF valuation technique and can be classified as follow:

a. Conducting preliminary test and filtering to determine the samples taken

in the study,

b. Classifying financial informations derived from the financial statements

of respective samples from year 2015-2017 into forecasting format,

46

c. Forecasting for three years for both the explicit and post-horizon FCF by

using the historical 2015-2017 financial performance,

d. Determining the Weighted Average Cost of Capital (WACC) for both

Traditional and Proposed Model,

e. Discounting the forecasted FCF into Net Present Value (NPV) as of

January 1st, 2018 to determine the stock’s fair value of respective

samples based on each respective model, and

f. Comparing the stock’s fair value derived from DCF valuation technique

with the stock’s actual market price in January 1st, 2018 based on each

respective model.

3.3.1 Conducting Preliminary Filtering and Testing

As mentioned in previous section, prior to the data collection and

processing, the preliminary filtering and testing were conducted to

determine the public listed companies taken as samples.

The comparison test of Price-Earning Ratio (PER) was done by

comparing the 2017 PER of comparable in the respective industry

with each of the 2017 PER of the company sample taken. This step

was done by using Median Absolute Deviation (MAD) which was

introduced by Leys, Ley, Klein, Bernard, and Licata (2013). The

definition of this MAD analysis will be explained in the next section.

47

The purpose of conducting this PER comparison test is to eliminate

any outliers companies from the population in the industry, then after

considering the completeness of financial information and condition

of company’s equity, the respective sample can be taken for each

respective industry in JASICA.

By combining the PER comparison test with the other qualitative

criteria such as the completeness of financial information and equity

position, the number of samples taken can be narrowed down. Shall

all of the criteria is followed by the all of the comparable, then the

representative sample will be taken with random sampling.

3.3.2 Classifying Financial Informations into Forecasting Format

After the preliminary process had been conducted and samples had

been determined, the financial informations regarding the respective

companies are gathered from the financial reports from 2015-2017,

then those compiled data are classified into groups of major

accounting items. The purpose of classifying the financial data into

forecasting format was done so that the forecasting process can be

done in more convenient process.

48

3.3.3 Forecasting the Explicit and Post-Horizon FCF

The historical financial performance of each respective samples will