dst policy and procedure - nc treasurer · dst policy and procedure . and lgers boards of trustees...

TRANSCRIPT

DST POLICY AND PROCEDURE DST Reference: RSD-POL-1110-ALL Title: Pensions Funding Policy Cross Reference: Chapter: Retirement Administration Current Effective Date: January 30, 2015 Revision History: Original Effective Date: January 30, 2015 Applies to: NC Department of State Treasurer – Retirement Systems Division

Keywords: Board of Trustees, Pension Funding, Actuary, GASB

Background

The Retirement Systems Division (RSD) of the NC Department of State Treasurer (DST) administers the retirement plans of the NC Retirement Systems (NCRS). The plans listed below are collectively referred to as the NCRS:

• Teachers’ and State Employees’ Retirement System (TSERS) • Local Governmental Employees’ Retirement System (LGERS) • Consolidated Judicial Retirement System (CJRS) • Legislative Retirement System (LRS) • Registers of Deeds’ Supplemental Pension Fund (RODSPF) • North Carolina National Guard Pension Fund (National Guard) • Firefighters’ and Rescue Squad Workers’ Pension Fund (FRSWPF)

Purpose

This policy sets forth the implementation of Governmental Accounting Standards Board (GASB) Statements 67 and 68 requiring enhanced accounting and financial reporting related to pensions for governments. Related Statutes, Rules, and Policies

The following N.C. General Statutes, Administrative Code and/or Executive Orders relate to the Pensions Funding Policy content: N.C.G.S. §§135-6, 135-8 N.C.G.S. §§128-28, 128-30 N.C.G.S. §§135-52, 135-69 N.C.G.S. §§120-4.10, 120-4.20 N.C.G.S. §§161-50.1, 161-50.2 N.C.G.S. §§127A-40(f) N.C.G.S. §§58-86-10, 58-86-20

DST Reference: RSD-POL-1110-ALL Page 1 of 4 Title: Pensions Funding Policy Cross Reference: Chapter: Retirement Administration Current Effective Date: January 30, 2015

DST POLICY AND PROCEDURE 20 NCAC 02A.0101 20 NCAC 02A.0103 Board of Trustees Governance Oversight Policy – RSD-POL-1109-ALL Policy

Governmental Accounting Standards Board (GASB) Statements 67 and 68 establish and define standards of accounting and financial reporting requirements for the activities of pension plans that are administered through trusts. The funding policies in the NCRS are expressed across a variety of legal platforms and independent actuarial valuation reports. This policy is a compilation of the NCRS funding policies for the purposes of disclosure. Nature of the Policy

This Policy concerns only the internal management of the Department of State Treasurer. If this Policy directly or substantially affects any procedural or substantive rights or duties, it does so only for persons who are (or were) Department employees or contractors. The Policy serves as a nonbinding interpretative statement, within the delegated authority of the Department of State Treasurer that defines, interprets, or explains the meaning of the laws and/or regulations listed above. Those laws or regulations, not this Policy, shall take priority if they conflict in any way. Implementation

Actuarial Assumptions used for the funding policy in the North Carolina Retirement Systems vary by plan. After collecting each system’s census, asset and benefit information, the actuary makes use of the actuarial assumptions developed in the quinquennial experience review and funding policy as outlined in the appendices to develop the actuarially determined contributions. Each retirement system’s assets, liabilities, and required contribution are determined in an actuarial valuation on an annual basis, performed and provided to RSD by our actuaries (Buck Consultants), then reviewed and accepted by the Boards of Trustees, a process that then incorporates this actuarial valuation as a part of the plan documentation under the statute.

Included in the appendices below are the Schedules of Actuarial Assumptions and Methods for each retirement system. Our actuaries recommend these assumptions with assistance from RSD. The Retirement Systems’ Boards adopt these assumptions after consultation with the actuary and RSD. These recommendations are included in the Experience Investigation performed quinquennially by Buck Consultants. This Experience Investigation serves to evaluate the accuracy of the actuarial assumptions made during the previous five-year period. The TSERS

DST Reference: RSD-POL-1110-ALL Page 2 of 4 Title: Pensions Funding Policy Cross Reference: Chapter: Retirement Administration Current Effective Date: January 30, 2015

DST POLICY AND PROCEDURE and LGERS Boards of Trustees vote and approve the underlying Actuarial Assumptions to be used for the following 5 years.

An Administrative Memorandum and schedules of Actuarial Assumptions for each of the NCRS plans are attached for the purposes of disclosure.

The funding policies are based on generally accepted actuarial principles for public plans in the United States. A summary of the components is as follows:

• Actuarial Cost Method is the technique used to allocate the total present value of future benefits over an employee's career (i.e., the normal cost)

• Annual Required Contribution is an amount actuarially-determined each year as a part of the statutorily-required valuation that is accepted by the Boards of Trustees

• Asset Smoothing/Valuation Method refers to the technique used to recognize gains or losses in pension assets over some period of time so as to reduce the effects of market volatility and stabilize contributions

• Amortization Policy is the length of time and structure selected for adjusting contributions to systematically eliminate any unfunded actuarial accrued liability or surplus

• Funding of Normal Cost is funded on no less than an annual basis. Enforcement

The Retirement Systems Division shall have authority to interpret and apply this procedure. This procedure may be modified or amended at any time. Failure to comply with this procedure could result in disciplinary action up to and including dismissal. Non-compliance with this procedure by RSD employees and systems users without proper approval is a serious matter and will be dealt with accordingly on a case-by-case basis. Depending on severity of violations and applicable legal statutes, consequences could result in removal of access rights and special system privileges, removal of system access, or, for RSD employees, disciplinary action to include potential termination of employment. In cases of fraud, misuse, or breach of privacy laws, legal action may be taken (see N.C.G.S. §14-454, 14-455, and 14-458). References

Statement No. 67 of the Governmental Accounting Standards Board, Financial Reporting for Pension Plans (an amendment of GASB Statement No. 25) Statement No. 68 of the Governmental Accounting Standards Board, Accounting and Financial Reporting for Pensions (an amendment of GASB Statement No. 27) DST Reference: RSD-POL-1110-ALL Page 3 of 4 Title: Pensions Funding Policy Cross Reference: Chapter: Retirement Administration Current Effective Date: January 30, 2015

DST POLICY AND PROCEDURE Administrative Memorandum 2014-001, Funding Policy Compilation for GASB Purposes

Appendix A - Teachers’ and State Employees’ Retirement System

Appendix B - Local Governmental Employees’ Retirement System

Appendix C - Consolidated Judicial Retirement System

Appendix D - Legislative Retirement System

Appendix E - National Guard Pension Fund

Appendix F - Registers of Deeds’ Supplemental Pension Fund

Appendix G - Firefighters’ and Rescue Squad Workers’ Pension Fund Revision History

Version/Revision Date Approved Description of Changes

Ver 1.0 January 30, 2015 New Policy For questions or clarification on any of the information contained in this policy, please contact the policy owner or designated contact point: [email protected]. For general questions about department wide policies and procedures, please contact the DST Policy Coordinator: [email protected].

DST Reference: RSD-POL-1110-ALL Page 4 of 4 Title: Pensions Funding Policy Cross Reference: Chapter: Retirement Administration Current Effective Date: January 30, 2015

DST POLICY AND PROCEDURE

NORTH CAROLINA

DEPARTMENT OF STATE TREASURER RETIREMENT SYSTEMS DIVISION

________________________________________________________________________________

JANET COWELL STEVE TOOLE TREASURER RETIREMENT SYSTEMS DIRECTOR May 15, 2014 TO: Staff of the Department of State Treasurer FM: Steve Toole, Retirement Director RE: Administrative Memorandum 2014-001, Funding Policy Compilation for GASB Purposes The Department of State Treasurer’s implementation of GASB Statements 67 and 68 require a compilation of the funding policy of the retirement systems that are subject to the new accounting statements. The funding policy in the North Carolina Retirement Systems is expressed across a variety of legal platforms and actuarial valuation reports that, independent of each other, do not provide a suitable single vehicle for all systems for the transparent accounting disclosure now required. Since those platforms dictate the actual funding policy of the system, this memorandum serves as a compilation of the existing policies in one document for purposes of the disclosure.

I. INTRODUCTION AND PURPOSE a. Program Overview

The North Carolina Retirement Systems include the following, which are collectively known as the “Retirement Systems,” or the “NCRS”: • the Teachers’ and State Employees’ Retirement System (TSERS), • the Local Governmental Employees’ Retirement System (LGERS), • the Consolidated Judicial Retirement System (CJRS), • the Legislative Retirement System (LRS), • the Registers of Deeds’ Supplemental Pension Fund (RODSPF), • the North Carolina National Guard Pension Fund (National Guard), and • the Firefighters’ and Rescue Workers’ Pension Fund (FRSWPF) The statutes governing the NCRS are established by the North Carolina General Assembly in law for each respective plan and may be amended only by the North Carolina General Assembly. The Retirement Systems Division (RSD) of the North Carolina Department of

DST POLICY AND PROCEDURE

State Treasurer (DST) administers the funding of the NCRS under direction of the State Treasurer.

b. Purpose The purpose of this funding policy statement is to set forth the funding objectives and guidelines implemented by RSD in administering the funding of the NCRS.

II. GOALS OF THE FUNDING POLICIES a. To achieve long-term full funding of the cost of benefits provided by NCRS.

b. To seek reasonable and equitable allocation of the cost of benefits over time.

c. To minimize volatility of employers and sponsors contributions to the extent reasonably

possible, consistent with other policy goals.

III. COMPONENTS OF THE FUNDING POLICIES The funding policies are based on generally accepted actuarial principles for public plans in the United States. A summary of the components is as follows: a. Actuarial Cost Method – The actuarial cost method is the technique used to allocate the

total present value of future benefits over an employee's career (i.e., the normal cost).

b. Annual Required Contribution – This is amount is actuarially-determined each year as a part of the statutorily-required valuation that is accepted by the Boards of Trustees.

c. Asset Smoothing/Valuation Method – The asset smoothing method refers to the technique used to recognize gains or losses in pension assets over some period of time so as to reduce the effects of market volatility and stabilize contributions.

d. Amortization Policy – The length of time and structure selected for adjusting contributions to systematically eliminate any unfunded actuarial accrued liability or surplus.

e. Funding of Normal Cost – The Normal Cost is funded on no less than an annual basis.

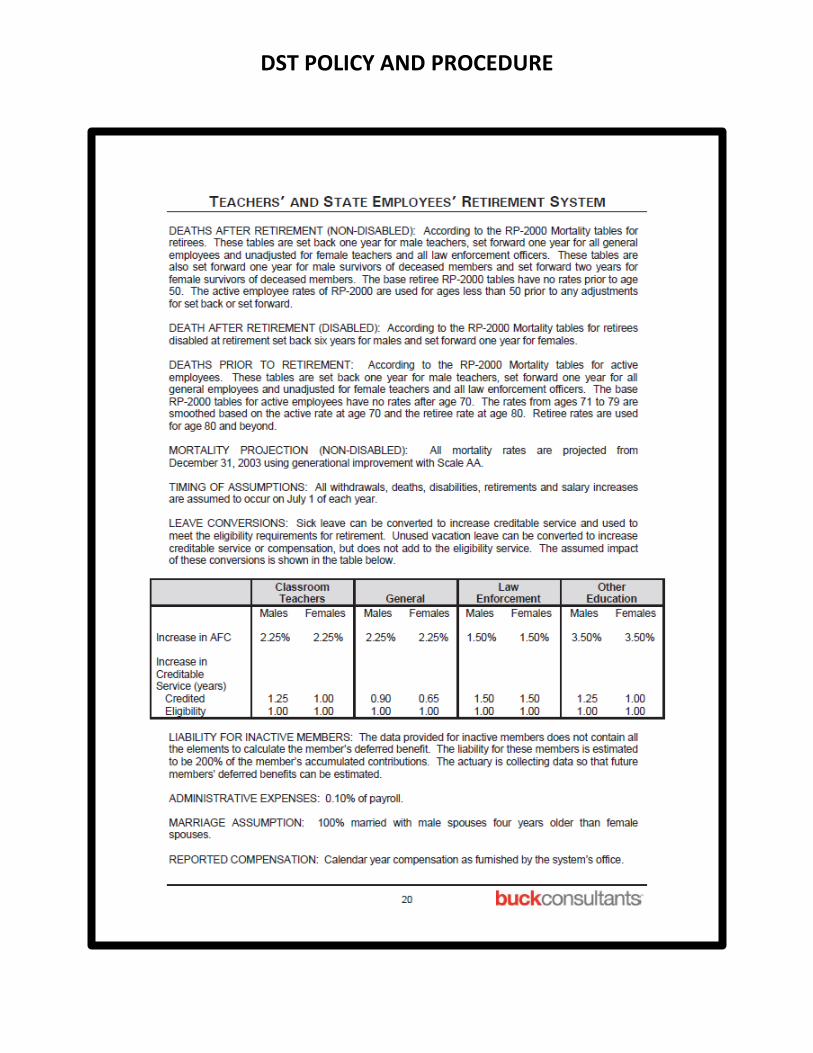

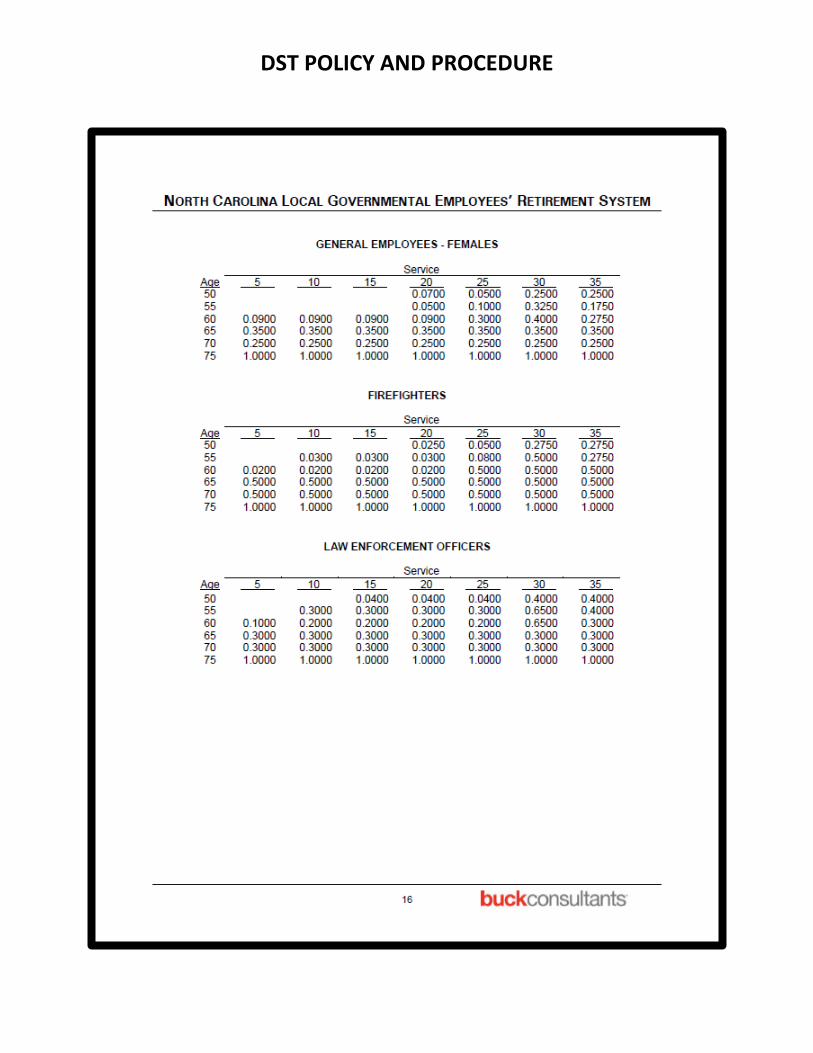

f. Actuarial Assumptions – The assumptions used for the funding policy in the North Carolina Retirement Systems vary by plan. After collecting each system’s census, asset and benefit information, the actuary makes use of the actuarial assumptions developed in the quinquennial experience review and funding policy as outlined below to develop the actuarially-determined contributions. Each retirement system’s assets, liabilities, and required contribution are determined in an actuarial valuation on an annual basis, performed and provided to RSD by our actuaries (Buck Consultants), then reviewed and accepted by the Boards of Trustees, a process which then incorporates this actuarial valuation as a part of the plan documentation under the statute. Included in the appendices below are the Schedules of Actuarial Assumptions and Methods for each retirement system.

DST POLICY AND PROCEDURE

Each Schedule is labeled with its retirement system at the beginning of each appendix section. These assumptions are recommended by our actuaries with assistance from RSD. The Retirement Systems’ Boards adopt these assumptions after consultation with the actuary and RSD. These recommendations are included in the Experience Investigation, which is performed quinquennially by Buck Consultants. This Experience Investigation serves to evaluate the accuracy of the actuarial assumptions made during the previous five-year period. The TSERS and LGERS Boards of Trustees vote and approve the underlying Actuarial Assumptions to be used for the following 5 years.

IV. STATUTES AND ADMINISTRATIVE CODE PROVISIONS The funding policies are a product of the administrative authority statutes, the method of financing statutes, the delegation of authority in the administrative code, and the actuarial assumptions in the annual valuations when read in by the Board of Trustees as supplements to plan documentation under the Duties of the Actuary statutes. Retirement System Administration Statute Method of Financing Statute TSERS § 135-6 § 135-8 LGERS § 128-28 § 128-30 CJRS § 135-52 § 135-69 LRS § 120-4.10 § 120-4.20 RODSPF § 161-50.1 § 161-50.2 NGPF § 127A-40(f) § 127A-40(f) FRSWPF § 58-86-10 § 58-86-20 These statutes are read in conjunction with the administrative code for authority of the Director and delegations from the Boards of Trustees in: 20 NCAC 02A.0101 and 20 NCAC 02A.0103. Furthermore, the actuarial assumptions become a part of plan documentation under: NCGS 135-6(i) for TSERS, LRS, CJRS, and National Guard; and NCGS 128-28(m) for LGERS, FRSWPF, and ROD.

DST POLICY AND PROCEDURE

V. SUMMARY OF THE FUNDING POLICIES

Teachers' and State

Employees' Retirement

System

Local Governmental

Employees' Retirement

System

Consolidated Judicial

Retirement System

Legislative Retirement

System

National Guard

Pension Fund

Registers of Deeds'

Supplemental Pension Fund

Firefighters' and Rescue

Squad Workers'

Pension Fund

Amortization Method

Level dollar closed

Level percent closed

Level dollar closed

Level dollar open

Level dollar closed

Level dollar closed

Level dollar closed

Asset Valuation Method

20% of market value plus 80% of expected actuarial value (not greater than 120% of market value and not less than 80% of market value)

20% of market value plus 80% of expected actuarial value (not greater than 120% of market value and not less than 80% of market value)

20% of market value plus 80% of expected actuarial value (not greater than 120% of market value and not less than 80% of market value)

20% of market value plus 80% of expected actuarial value (not greater than 120% of market value and not less than 80% of market value)

20% of market value plus 80% of expected actuarial value (not greater than 120% of market value and not less than 80% of market value)

20% of market value plus 80% of expected actuarial value (not greater than 120% of market value and not less than 80% of market value)

20% of market value plus 80% of expected actuarial value (not greater than 120% of market value and not less than 80% of market value)

Investment Rate of Return

(IRR)7.25% 7.25% 7.25% 7.25% 7.25% 5.75% 7.25%

Projected Salary Increases

(PSI)4.25% - 9.10% 4.25% - 8.55% 5.00% - 5.95% N/A N/A 4.25% - 7.75% N/A

IRR Includes inflation of

3.00% 3.00% 3.00% 3.00% 3.00% 3.00% 3.50%

PSI Includes inflation and

productivity of3.50% 3.50% 3.50% 0.50 per anum N/A 3.50% N/A

Cost-of-living Adjustments

N/A N/A N/A N/A N/A N/A N/A

Entry age Entry age Entry age

Amortization Period 12 years Varies 12 years 8 years+

Actuarial Cost Method

Entry age Frozen entry age

Projected unit credit

Projected unit credit

12 years N/A++ 12 years

+ If the annual required employer contribution (ARC) is based on 8-year amortization of the unfunded accrued liability, the ARC is less than $0, which is not allowed under the funding policy. Therefore, the accrued liability contribution has been set such that the total employer ARC equals $0++ If the annual required employer contribution (ARC) is based on 30-year amortization of the unfunded accrued liability, the ARC is less than $0, which is not allowed under the funding policy. Therefore, the accrued liability contribution has been set such that the total employer ARC equals $0

Actuarial Assumptions

DST POLICY AND PROCEDURE

VI. APPENDICES – SCHEDULES OF ACTUARIAL ASSUMPTIONS

Appendix A Teachers’ and State Employees’ Retirement System Page 6

Appendix B Local Governmental Employees’ Retirement System Page 14

Appendix C Consolidated Judicial Retirement System Page 21

Appendix D Legislative Retirement System Page 25

Appendix E National Guard Pension Fund Page 28

Appendix F Registers of Deeds’ Supplemental Pension Fund Page 32

Appendix G Firefighters’ and Rescue Squad Workers’ Pension Fund Page 37

DST POLICY AND PROCEDURE

APPENDIX A

TEACHERS’ AND STATE EMPLOYEES’ RETIREMENT SYSTEM:

Schedule of Actuarial Assumptions

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

APPENDIX B

LOCAL GOVERNMENTAL EMPLOYEES’ RETIREMENT SYSTEM:

Schedule of Actuarial Assumptions

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

APPENDIX C

CONSOLIDATED JUDICIAL RETIREMENT SYSTEM:

Schedule of Actuarial Assumptions

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

APPENDIX D

LEGISLATIVE RETIREMENT SYSTEM: Schedule of Actuarial Assumptions

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

APPENDIX E

NATIONAL GUARD PENSION FUND: Schedule of Actuarial Assumptions

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

APPENDIX F

REGISTERS OF DEEDS’ SUPPLEMENTAL PENSION FUND:

Schedule of Actuarial Assumptions

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

APPENDIX G

FIREFIGHTERS’ AND RESCUE SQUAD WORKERS’ PENSION FUND:

Schedule of Actuarial Assumptions

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE

DST POLICY AND PROCEDURE