dragon energy limited

DESCRIPTION

Major drill programme complete...Resource update imminentTRANSCRIPT

Page 1 – Copyright © 2012 RM Research – www.rmresearch.com.au - Please read the disclaimer for terms.

Dragon Energy Limited (“Dragon” or the Company”) has very much being flying “underthe radar” since listing in 2009 however there has been considerable progress on itsflagship Pilbara Iron Ore Project (“PIOP”) situated in the Pilbara Region of WesternAustralia.

The PIOP, purchased from AusQuest Limited (ASX: AQD) in October 2010, comprisesthe Rocklea and Nameless Projects that contain channel iron deposits (“CID”) and detritalmineralisation that have potential for export as Direct Shipping Ore (“DSO”).

Rocklea is situated approximately 33 kilometres southwest of Tom Price, just north ofMurchison Metals Limited (ASX: MMX) Rocklea CID project while Nameless is located10 kilometres north-west of Tom Price.

Dragon has recently completed two RC drilling programmes. The first programme aims toextend Rocklea’s resource and upgrade JORC Inferred to Indicated resources. Theobjective of the second phase programme was to outline a maiden JORC Inferredresource at Nameless.

The Rocklea Project currently contains a JORC resource of 62.7Mt @ 53.4% Fe (60.4%caFe) and includes 28.0Mt of higher grade @ 55.6% (62.7% caFe). RM Researchbelieves that there is upside for a further 40-50Mt @ 56-62% caFe in the near term.

At the Nameless Project, the Company has outlined an Exploration Target in the range of140 to 190Mt @ 48-52% Fe (54–56% caFe).

RM Research believes that Rocklea and Nameless have the potential to support a nearterm 2Mtpa scenario based at Rocklea utilising trucks on public roads to a West PilbaraPort. An expanded case scenario could see production of up to 10Mtpa utilisingfuture/proposed rail/port infrastructure.

We believe that JORC resources, should they fulfil the exploration targets in excess of200Mt, should be capable of sustaining a 2-10Mtpa operations. RM Research considersthat trucking to a West Pilbara Port is possible on the lower end of the production scalewhereas an expanded case scenario is somewhat more speculative at this stage due tothe requirement to negotiate port/rail access with third parties. The recent 50:50 jointventure between BC Iron Limited (ASX: BCI) and Fortescue Metals Group Limited(ASX: FMG) would indicate that Company’s may be forced to give away much of theproject upside to gain access.

The Company is currently examining development options in 2013/2014 subject to portaccess and defining sufficient iron ore JORC reserves.

Our six month share price target of 62 cents per share is based on 200Mt JORC Inferred+ Indicated Resources at Rocklea and Nameless valued alongside the nearestcomparable company (Flinders Mines Limited, ASX: FMS) with a market capitalisationof A$540 million and an Enterprise Value of 60 cents per tonne JORC iron ore resources.

Capital Structure

Sector Materials

Share Price (A$) 0.17

Fully Paid Ordinary Shares (m) 206.4

Opt (ex 30c, exp 30/5/12) (m) 11.5

Opt (ex 35c, exp 30/11/14) (m) 47.4

Market Cap (undil) (A$m) 35.1

Share Price Year H-L (A$) 0.25-0.08

Approx Cash (A$m) 12.5

Directors

Jie Chen Chairman

Gang Xu Managing Director

Qingyong Guo Executive Director

Tim Williams COO & Exec Director

Anthony Ho Executive Director

Major Shareholders

Shandong Taishan Sun. Gp. Co. Ltd 70.3%

Gang Xu 6.6%

Analyst

GT Le Page +61 8 9488 0800

Share Price Performance

Dragon Energy LimitedMajor drill programme complete...Resource update imminent

4 April 2012

ASX Code: DLESpeculative BuySix month target 62 cents

Page 2 – Copyright © 2012 RM Research - www.rmresearch.com.au

4 April 2012

INVESTMENT CASERESOURCE UPSIDE: RM Research believes that Rocklea and Nameless have significantnear term resource upside in the range of 200-300Mt from the current JORC InferredResource of 62.7Mt @ 53.4% Fe at Rocklea.

IRON ORE OUTLOOK REMAINS FIRM: Iron ore prices are anticipated to hold up overUS$150/tonne in CY 2012 rising to US$165/tonne in the June Quarter 2013. Despite a slowstart to steel production and consumption activity in China in September Quarter 2012, RMResearch envisages a tighter seaborne market over 2012 on the back of firming demand fromChina. Notably at the Global Iron Ore & Steel Forecast Conference in Perth this week, BHPBilliton Ltd’s (ASX: BHP) Ian Ashby considered a floor iron ore floor price of US$120 waslikely.

DEVELOPMENT POTENTIAL: RM Research believes that subject to defining adequateJORC Reserves and securing adequate port facility, Nameless and Rocklea could represent amedium term development scenario.

PROJECT SIZE/CHARACTERISTICS – POTENTIALLY FAVOURABLE ECONOMICS: Webelieve the grade of Rocklea and Nameless together with its access to public roads andproximity to existing rail facilities has the potential to deliver a profitable mining operation inthe medium term.

TIGHT SHARE REGISTER: Shandong Taishan Sunlight Group Company Limited(“Shandong Group”) holds approximately 70% of the Shares with the top 20 holding 84%.RM Research believes that positive news relating to resource upgrades/mining studies arelikely to be quickly reflected in the share price of Dragon.

EXPERIENCED MANAGEMENT: The board of Dragon packs some heavy hitting miningexecutives including Shandong Group Chairman Mr Chen with nearly 30 years operationaland management experience and current MD Mr Gang Xu, a geologist with over 20 yearsincluding 9 years as a senior uranium exploration geologist with the China National NuclearCorporation. COO Tim Williams (fluent Mandarin) has also had extensive experience withChinese investment in the Australian iron ore sector.

COMPANY BACKGROUNDDragon listed on ASX in February 2009underpinned by privately owned Chinesecornerstone investor Shandong Group. Thisgroup controls 1.5 billion tonnes of coal and100 Mt of iron ore resources in China. TheShandong Group is also involved in steel andpower generation and is an active participant inthe Chinese resources sector.

The main focus of the Company is the PilbaraIron Ore Project which comprises the Rockleaand Nameless Projects situated in thePilbara region of Western Australia. Theseprojects consist of channel iron deposits (“CID”)with significant exploration upside from thecurrent JORC Resource of 62.7Mt @ 53.2%Fe.

Mining studies are currently underway with aview to examining the development potential ofthe Pilbara iron ore projects. The balance of theexploration portfolio in Western Australiaconsists of iron, manganese, gold, base metalsand uranium projects.

Nameless and Rockleacould represent amedium termdevelopment scenario

FIGURE 1: DragonEnergy Limited WesternAustralian explorationportfolio (source: DragonEnergy LimitedDecember 2011 QuarterlyReport, 1 February 2012).

Page 3 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

PILBARA IRON EXPLORATION AND DEVELOPMENT

Australia is the world’s 2nd largest producer of iron ore producing 420Mt in 2010 with theHamersley Range (Pilbara region of northwest Australia) hosting approximately 98% ofAustralia's iron ore mines. BHP Billiton Limited (ASX: BHP) and Rio Tinto Ltd (ASX: RIO)account for the bulk of production with the massive Mt Whaleback mine, established in 1968.Smaller ore bodies 29, 30 and 35, with smaller satellite mines – Jimblebar and Orebodies 18,23 and 25 are situated just outside of Newman. The Yandi and Area C mines are locatedabout 100 kilometres north-west of Newman. The Yarrie Mine is 200 kilometres east of PortHedland.

RIO currently has capacity for approximately 220Mt and is projected to ramp up to 283Mt by2013. Total investment is forecast at around $8 billion over the next five years to expandannual production by 50% to 333Mt by 2015.

FMG’s port, rail and mine project commenced in February 2006 and was completed in 2008.Operations commenced at the Fortescue Herb Elliott Port and at Cloudbreak. FMG shipped inexcess of 27 million tonnes of iron ore to Chinese customers in its first year of operations. Asecond minesite has been established at Christmas Creek to create the Chichester Hub. InJuly 2009, FMG announced a 1.23Bt Inferred Resource for the Glacier Valley tenement and inFebruary 2011, FMG announced the discovery of over 1Bt of high grade Brockman ironformation (Nyidinghu project), situated 35 kilometres south of the Cloudbreak. In 2011, RIO,BHP and FMG announced that it would collectively target iron ore production of 1,000Mtpa by2020, representing a doubling of current capacity. Recent new industry entrants such asHancock, Atlas Iron Limited (ASX: AGO) and Brockman Resources Limited (ASX: BRM)through Port Hedland and API and others through the proposed Port of Anketell.

AGO has a portfolio covering over 18,000km², mostly in the northeast Pilbara, Newman areaof Western Australia. This includes the Pardoo and Wodgina Operations near Port Hedland,advanced projects at Abydos and Mt Webber and greenfields projects in the Newman area.The Pardoo Operation commenced mining in October 2008. Mining commenced at Wodginain 2010, and by October 2010, DSO exports had increased to a rate of 6Mtpa. Abydos and MtWebber will round off target production of 12Mtpa in CY 2012.

FIGURE 2: MajorPilbara Iron OreDeposits and networks.

The Whaleback mine isone of the largestsingle pit mines in theworld

Page 4 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

BC Iron Limited’s (ASX: BCI) focus is the Nullagine Iron Ore Project (Inferred and IndicatedJORC Resources of 101.7Mt @ 54.1% Fe), a 50/50 JV with FMG. The JV uses FMG’sinfrastructure at Christmas Creek, 50km south of the Mine, to rail its ore to Port Hedland. BCIis the third company to use FMG’s Herb Elliott Port to export iron ore from Port Hedland.Annualised production of >3Mpta by late 2011 ramping up to annualised production of 5.0Mtby June 2012.

Flinders Mines Limited (ASX: FMS) (currently subject of a takeover bid by Magnitgorsk Ironand Steel Works) Pilbara Iron Ore Project (“PIOP”) (comprising the Blacksmith and Anviltenements) is located approximately 60 kilometres north-west of Tom Price and comprisesJORC Indicated and Inferred Resources of 748Mt @ 55.4% Fe. The Blacksmith tenementhosts the Delta deposit (a focus of near term production) is located between a number ofexisting and proposed developments. The DFS is scheduled for completion in June Quarter2012 and will target an annualised production of 15Mtpa.

BRM’s Marillana Iron Ore Project is located in the Hamersley Iron Province approximately100km north west of Newman. The Project covers 96km2 of the Fortescue Valley and bordersthe Hamersley Range, where extensive areas of supergene iron ore mineralisation havedeveloped within the dissected Brockman Iron Formation. Marillana is in close proximity toexisting infrastructure, with BHP’s railway traversing the lease, RIO’s Yandicoogina mine 40kilometres south and FMG’s Cloud Break mine approximately 35 kilometres north east.Brockman will export its ore through the Port of Port Hedland.

Figure 3 summarises projected iron ore production by developer in the Pilbara region.

RESOURCES AND RESERVES

Category Mt Fe caFe SiO2 Al2O3 P LOI (1000oC) Cut Off

(%) (%) (%) (%) (%) (%) Grade (%)

Rocklea

Inferred 62.7 53.41 60.39 7.73 2.8 0.034 11.56 50.0

including 28 55.62 62.89 6.03 2.06 0.034 11.31 54.0

Explor Target 40-51 50-55 56-62

Nameless

Explor Target 140-190 48-52 54-56

The recent takeover ofFlinders Mines valuedJORC Inferred andIndicated Resources atapproximately 60 centsper tonne (marketcapitalisation A$550million)

FIGURE 3: Projected ironore production in thePilbara region of WesternAustralia (source: CMEPresentation 2011, TheFuture of the ResourcesSector in the Pilbara).

TABLE 1: JORCResources and Reserves(source: Dragon EnergyLimited ASXAnnouncement 20th

January 2012).

Page 5 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

Both Rocklea and Nameless host near surface CID style mineralisation formed in meanderingriver channels. As bedded iron deposits were eroded by weathering, iron particles wereconcentrated in river channels. These particles were rimmed with goethite deposited by iron-enriched ground water around 15-30 million years ago which fused the particles together.These deposits occur as low flat-topped mesas as well as being concealed under cover.

Their chief characteristic is their pisolitic 'texture': rounded hematitic 'pea-stones', 0.1mm to5mm in diameter, rimmed and cemented by a goethitic matrix. The ore is brown-yellow incolour. They typically contain minor amounts of clay in discrete lenses.

Dragon has recently completed two RC drilling programmes. The first programme aims toextend Rocklea’s resource and upgrade JORC Inferred to Indicated resources. The objectiveof the phase 2 programme is to outline a JORC Inferred resource at Nameless.

The Rocklea Project, containing JORC resources of 62.7Mt @ 53.4% Fe (60.4% caFe), alsoincludes 28.0Mt of higher grade material @ 55.6% (62.7% caFe) (Table 1). RM Researchbelieves that there is upside for a further 40-50Mt @ 56-62% caFe in the near term.

At the Nameless Project, the Company has outlined an Exploration Target in the range of 140- 190Mt @ 48-52% Fe (54–56% caFe). A maiden JORC Resource is imminent.

EXPLORATION OVERVIEWPilbara Iron Ore ProjectsBackground

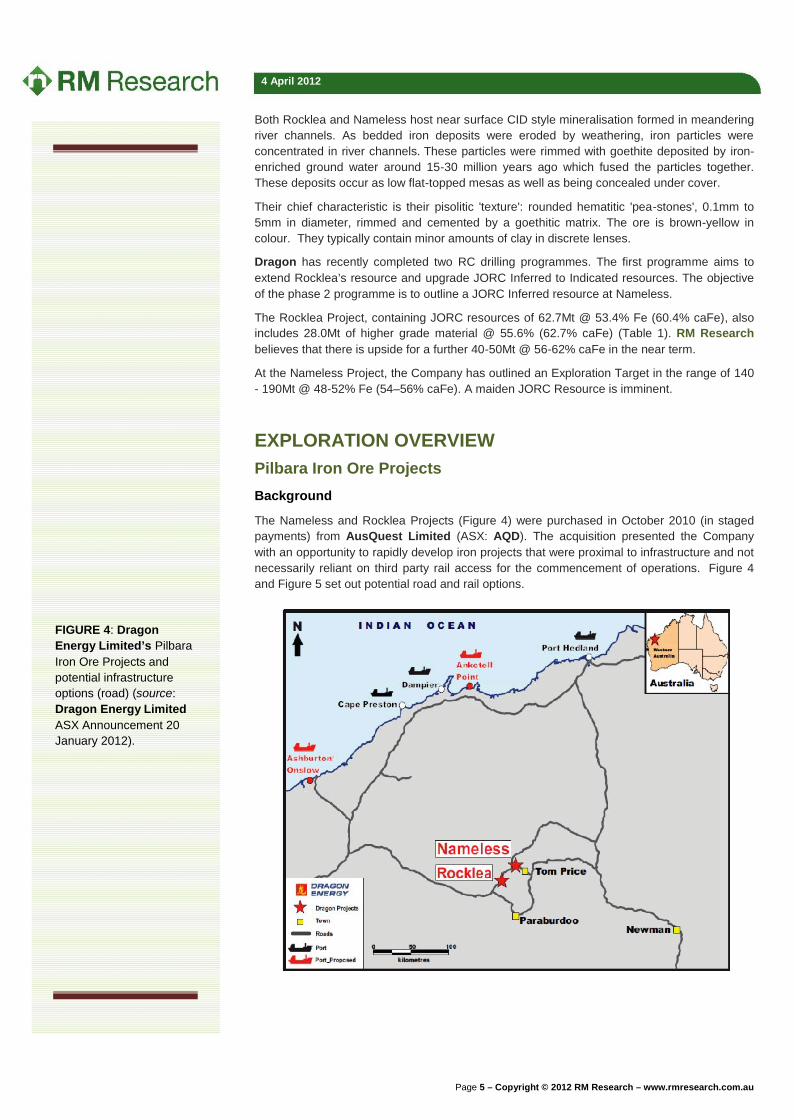

The Nameless and Rocklea Projects (Figure 4) were purchased in October 2010 (in stagedpayments) from AusQuest Limited (ASX: AQD). The acquisition presented the Companywith an opportunity to rapidly develop iron projects that were proximal to infrastructure and notnecessarily reliant on third party rail access for the commencement of operations. Figure 4and Figure 5 set out potential road and rail options.

FIGURE 4: DragonEnergy Limited’s PilbaraIron Ore Projects andpotential infrastructureoptions (road) (source:Dragon Energy LimitedASX Announcement 20January 2012).

Page 6 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

Rocklea Project (M47/1471, E47/1024)

FIGURE 5: DragonEnergy Limited’sPilbara Iron OreProjects and potentialinfrastructure options(rail) (source: DragonEnergy Limited ASXAnnouncement 20January 2012).

FIGURE 6: DragonEnergy Limited’sRocklea Project,location, JORCresource outline and RCdrillhole locations andtargets from 2Q 2012(source: DragonEnergy LimitedDecember 2011Quarterly ActivitiesReport, ASXAnnouncement 31st

January 2012).

Page 7 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

Location and Access

Rocklea is situated approximately 33 kilometres southwest of Tom Price, just north ofMurchison Metals Limited (ASX: MMX) Rocklea CID project (Figure 6).

The project is situated on the eastern margin of the Rocklea dome where Archaean ageFortescue Group Formations dip to the east and are overlain by Tertiary age CID and otherCainozoic deposits. Iron mineralisation consists of goethitic and hematitic detrital deposits ofthe Tertiary Robe Pisolites.

Previous Exploration

The presence of CID in the region was first identified by RIO subsidiary HamersleyExploration Pty Ltd in the 1970’s and from 2005-2009 drilling by AQD was successful inoutlining JORC Inferred Resources of 62.7Mt @ 53.41% Fe (60.39% caFe). This resourceremains open to the south and east. Further exploration upside for CID was later identified byDragon with the identification of outcropping mineralisation and subsequent drilling in thenorth-eastern portion of the tenement.

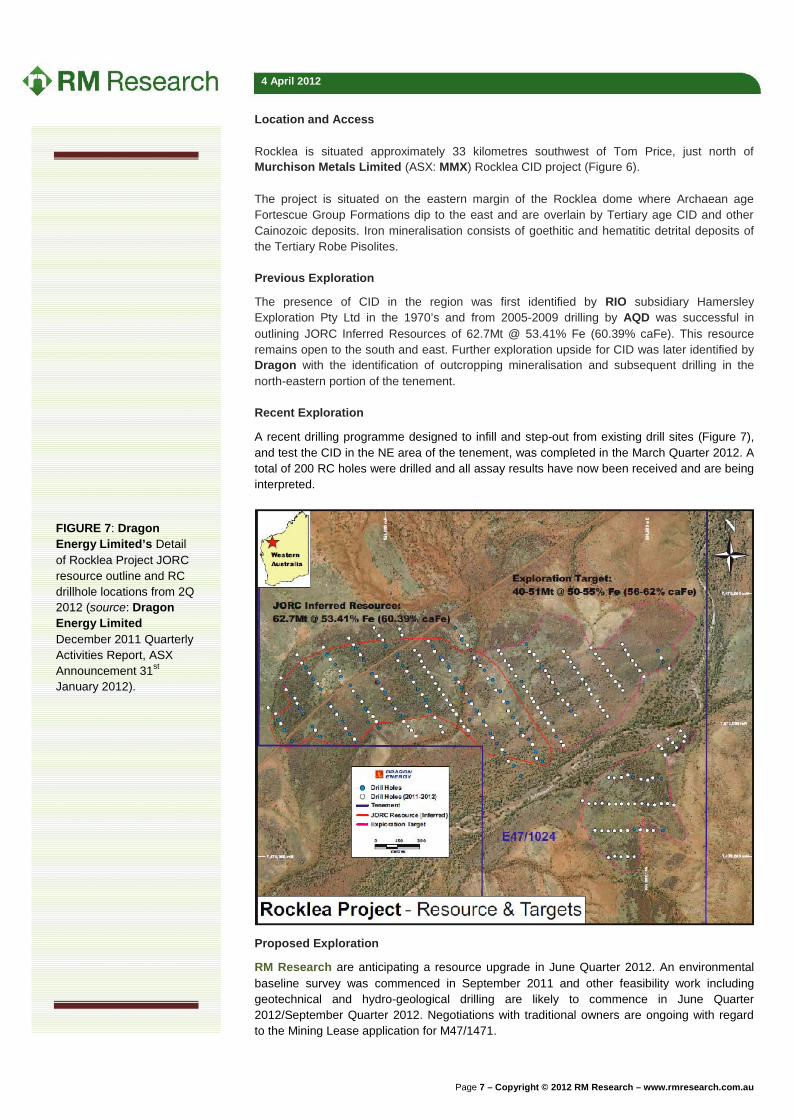

Recent Exploration

A recent drilling programme designed to infill and step-out from existing drill sites (Figure 7),and test the CID in the NE area of the tenement, was completed in the March Quarter 2012. Atotal of 200 RC holes were drilled and all assay results have now been received and are beinginterpreted.

Proposed Exploration

RM Research are anticipating a resource upgrade in June Quarter 2012. An environmentalbaseline survey was commenced in September 2011 and other feasibility work includinggeotechnical and hydro-geological drilling are likely to commence in June Quarter2012/September Quarter 2012. Negotiations with traditional owners are ongoing with regardto the Mining Lease application for M47/1471.

FIGURE 5: DragonEnergy Limited’sRocklea Project showingthe adjacent RockleaProject of MurchisonMetals (source: DragonEnergy Limited ASXAnnouncement 20January 2012).

FIGURE 7: DragonEnergy Limited’s Detailof Rocklea Project JORCresource outline and RCdrillhole locations from 2Q2012 (source: DragonEnergy LimitedDecember 2011 QuarterlyActivities Report, ASXAnnouncement 31st

January 2012).

Page 8 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

Nameless Project (M47/1452, E47/1485, E47/2456–2458)

Location and Access

The Nameless Project is located 10 kilometres north-west of Tom Price (Figure 1, 4), alongthe south-dipping northern limb of the Mt Turner Syncline within the South Pilbara Basin of theHamersley Basin. Bedrock lithologies comprise volcano-sedimentary rocks from the Fortescueand Hamersley Groups, with the Marra Mamba Iron Formation paralleling the southernboundary of the tenement. Cainozoic cover sequences include the Robe Pisolite Formation.

Previous Exploration

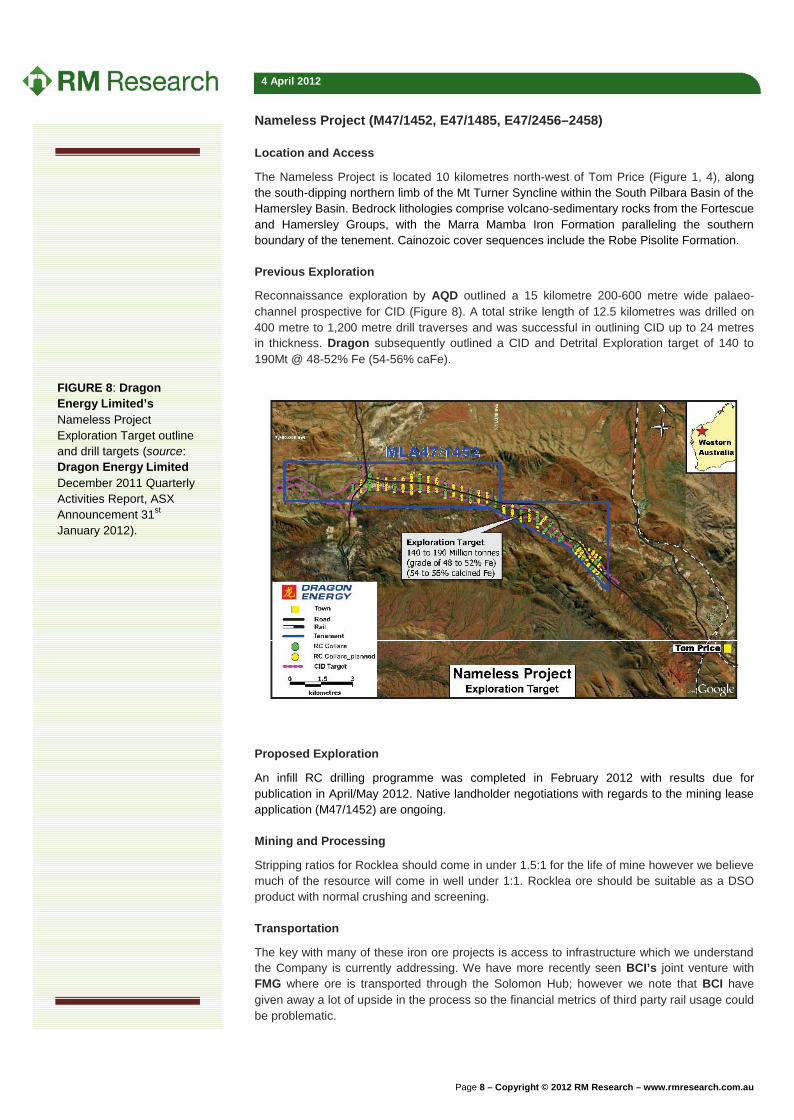

Reconnaissance exploration by AQD outlined a 15 kilometre 200-600 metre wide palaeo-channel prospective for CID (Figure 8). A total strike length of 12.5 kilometres was drilled on400 metre to 1,200 metre drill traverses and was successful in outlining CID up to 24 metresin thickness. Dragon subsequently outlined a CID and Detrital Exploration target of 140 to190Mt @ 48-52% Fe (54-56% caFe).

Proposed Exploration

An infill RC drilling programme was completed in February 2012 with results due forpublication in April/May 2012. Native landholder negotiations with regards to the mining leaseapplication (M47/1452) are ongoing.

Mining and Processing

Stripping ratios for Rocklea should come in under 1.5:1 for the life of mine however we believemuch of the resource will come in well under 1:1. Rocklea ore should be suitable as a DSOproduct with normal crushing and screening.

Transportation

The key with many of these iron ore projects is access to infrastructure which we understandthe Company is currently addressing. We have more recently seen BCI’s joint venture withFMG where ore is transported through the Solomon Hub; however we note that BCI havegiven away a lot of upside in the process so the financial metrics of third party rail usage couldbe problematic.

FIGURE 8: DragonEnergy Limited’sNameless ProjectExploration Target outlineand drill targets (source:Dragon Energy LimitedDecember 2011 QuarterlyActivities Report, ASXAnnouncement 31st

January 2012).

Page 9 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

IRON ORE MARKET OUTLOOKFollowing a slow start to CY 2012, iron ore volumes and prices in the seaborne market haverecently improved with spot prices trading at US$143/tonne (62% fines; CFR China).

Despite the recent sharp correction, iron ore has held around US$140/tonne through most ofthe recent period of weak demand. RM Research believes that this is the effective cost-support level, set by high cost domestic iron ore production in China. China steel production isanticipated to grow by 5% in 2012, indicating that seaborne iron ore supply will fall short ofdemand.

Iron ore prices are anticipated to hold up over US$150/tonne in CY 2012 rising toUS$165/tonne in CY 2013. Despite a slow start to steel production and consumption activity inChina in late CY 2012, RM Research envisages a tighter seaborne market over 2012 on theback of increasing demand from China.

Recent developments

Worldsteel is projecting steel production to hit a record 1.526Bt in CY 2011 representing a6.8% increase YOY. Seaborne iron ore also reached a record high of 1.08Bt in CY 2011(1.03Bt in CY 2010). Despite the strong demand, the European debt crisis together with atightening monetary policy in China and declining construction and manufacturing activity,there was a decline in sentiment towards iron ore (source: Goldman Sachs Global InvestmentResearch).

Figure 9 supports theabove observationswith China’s averagemonthly steelproduction in JuneQuarter 2011 of52.2Mt (June Quarter59.6Mt).

Followng a 23-monthlow of US$117/t inOctober 2011 (Figure9), strong buying from

Chinesemills/merchants inlate CY 2011 saw arebound toUS$139.50/t (source:Goldman SachsGlobal InvestmentResearch).

Chinese oreinventories at ports(Figure 10) reached arecord 101.5Mt inearly February 2012,with February 2012trade data revealing adrop in iron oreimports to 59.3Mt in

January (source: Goldman Sachs Global Investment Research).

Despite recent negativesentiment, iron ore priceshave held aroundUS$140/t

Worldsteel is projectinga record 1.562Bt of steelproduction in CY 2011

FIGURE 9: Platts IODEXand Australia 62% Finesspot prices January 2010-January 2012 (source:Goldman Sachs GlobalInvestment Research, 29February 2012).

FIGURE 10: China IronOre Imports vs ChinaSteel Production (source:Goldman Sachs GlobalInvestment Research, 29February 2012).

Page 10 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

Near term outlook remains positive

Statistics for late February2012 indicate a solid reboundin iron ore demand;

Inventories of iron ore atChinese ports havedropped <100Mt to98.9Mt on February 24.

Steel prices in Chinahave posted modestgains from a mid-January2012 low of RMB 4348/t.

The volume of inquiry for steel, and on a modest upturn in steel production rates (Reuters28/02/12).

China’s daily steel production rate rose above 1.7Mt in the first ten days of February forthe first time in three months.

Freight rates for Cape size vessels have improved slightly.

The above data set should support a 5% growth forecast in Chinese steel production over CY2012. Outside of China, we believe demand for seaborne iron ore will be flat in 2012. A 5% fallin European steel production is projected for this year offset by improvements in output in Asia(ex-China) and the Middle East (source: Goldman Sachs Global Investment Research).

Medium term…unchanged

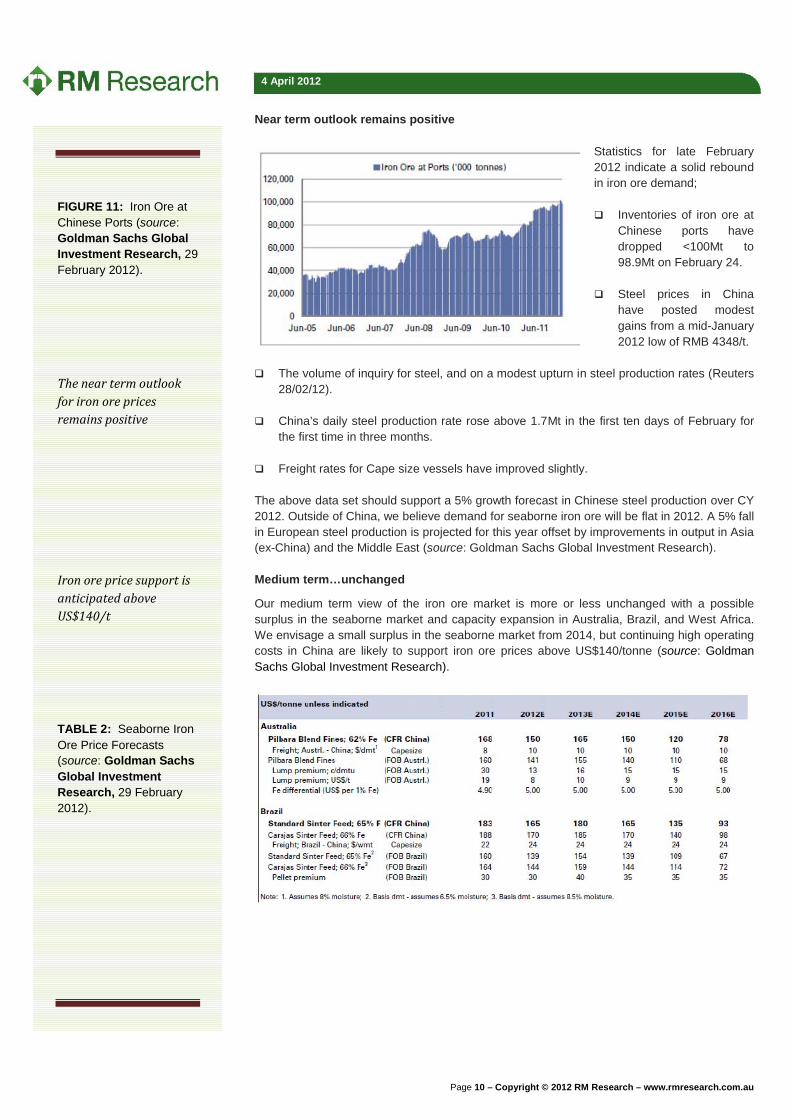

Our medium term view of the iron ore market is more or less unchanged with a possiblesurplus in the seaborne market and capacity expansion in Australia, Brazil, and West Africa.We envisage a small surplus in the seaborne market from 2014, but continuing high operatingcosts in China are likely to support iron ore prices above US$140/tonne (source: GoldmanSachs Global Investment Research).

FIGURE 11: Iron Ore atChinese Ports (source:Goldman Sachs GlobalInvestment Research, 29February 2012).

The near term outlookfor iron ore pricesremains positive

Iron ore price support isanticipated aboveUS$140/t

TABLE 2: Seaborne IronOre Price Forecasts(source: Goldman SachsGlobal InvestmentResearch, 29 February2012).

Page 11 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

Based on FY 2011 figures, we note that Australia’s share of China’s iron ore importsincreased to a record 43.2% in 2011 (42.5% in 2010; Figure 11). Brazil remained China’ssecond largest supplier with 20.8%. The largest fall in market share was India dropping from15.5% (CY 2010) to 9.9% (CY 2011), mostly due to the Karnataka mining ban (source:Goldman Sachs Global Investment Research).

TABLE 2: Seaborne IronOre Price Forecasts(source: Goldman SachsGlobal InvestmentResearch, 29 February2012) (cont).

Australia’s share of ironore supply to Chinaincreased from 43.2% in2011 from 42.5% in theprevious year

FIGURE 12: Major ironore producing countriesand market share (source:Goldman Sachs GlobalInvestment Research, 29February 2012).

Page 12 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

OTHER PROJECTS LEE STEERE PROJECT: (DLE 100%, Wiluna Area, Western Australia) Iron Ore.

Situated approximately 200km NE of Wiluna in the Earaheedy Basin (Midwest). Previousexploration identified hematite mineralisation of BIF’s and Superior-type iron within theFrere Formation. Rock chip samples returned assays up to 66.1% Fe withreconnaissance exploration identifying a prospective strike length in the Frere formationof approximately 48 kilometres.

MT GIBSON PROJECT: (DLE 100, Mt Gibson Area, Western Australia). Gold.Situated in the mid west region of the Yilgarn, 80 kilometres NE of Wubin. Strategicallylocated south and east of the Extension Hill Hematite/Magnetite Project (hosts part of MtGibson Gold Operation). A surface geochemical programme is likely to commenceshortly.

CARTERS WELL PROJECT: (DLE 100%, Mt Magnet Area, Western Australia). Gold.Situated 30 kilometres south of Mt Magnet near the Great Northern Highway the projectcomprises four Au-Ag, Ce-Pb, Pb-Zn-Cu, Pb-Zn anomalous zoned derived from mobilemetal ion sampling.

ASHBURTON PROJECT: (DLE 100%, Ashburton Area, Western Australia). Iron Ore,Base Metals, Gold. The project is situated between 10 and 40 kilometres from existingrail/ infrastructure at Paraburdoo (Rio Tinto Iron Ore). The project is prospective for CIDwithin braided drainages of Turee and Seven Mile Creeks (draining from the BrockmanIron Formation near Paraburdoo).

MILLY MILLY PROJECT: (DLE 100%, Mid West Region, Western Australia). Iron Ore.The Milly Milly Project covers an area of in excess of 1,500 km2 and is prospective formagnetite mineralisation (similar to Jack Hills). The tenements are situated 196kilometres west of Meekatharra and 58 kilometres east of Jack Hills (Murchison MetalsLimited, ASX: MMX). Previous rock chip samples have returned up to 44% Fe.

YARMANA PROJECT: (DLE 100%, Ashburton Area, Western Australia). Gold.Located 120 kilometres NE of Laverton between two greenstone belts; the Cosmo-Newberry Greenstone belt to the west and the Yamarna Greenstone belt to the east.Gold mineralisation identified to the east is hosted by laminated quartz-mica-amphiboleschist units- altered and sheared mafic volcanics and sediments.

MEEKATHARRA PROJECT: (DLE 100%, Ashburton Area, Western Australia). Gold.Located 13 kilometres SE of Meekatharra within the N-NE trending Meekatharragreenstone belt. Mineralisation is mostly associated with quartz veins within sheared andfoliated mafic units. Limited exploration activities in the project area identified linearnortherly trending arsenic anomalies with coincident weakly anomalous goldmineralisation to the north, and gold anomalies on lithological contacts with stronglyanomalous arsenic to the south.

CORPORATEThe last major capital raising (January 2011) was a 1 for 2 non-renounceable rights issue at30 cents each to raise approximately A$21.4 million and was underwritten by majorshareholder Shandong Group. At the same time the Company also completed a 1 for 3 pro-rata non-renounceable option (exercisable at A$0.35, expiring 18/11/2014) entitlement issueat an issue price of A$0.001 each that raised approximately A$47,460. The funds were usedin part for the acquisition of Rocklea with the balance applied to new acquisitions and workingcapital.

For other projects ownedby Dragon Energy...

...landholding In excess of1,500km2

100% owned

Multiple commoditiestargeted...

...gold, iron ore, basemetals and manganese

A 1 for 2 rights issue at30 cents per share raisedA$21.4 million in January2011

Page 13 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

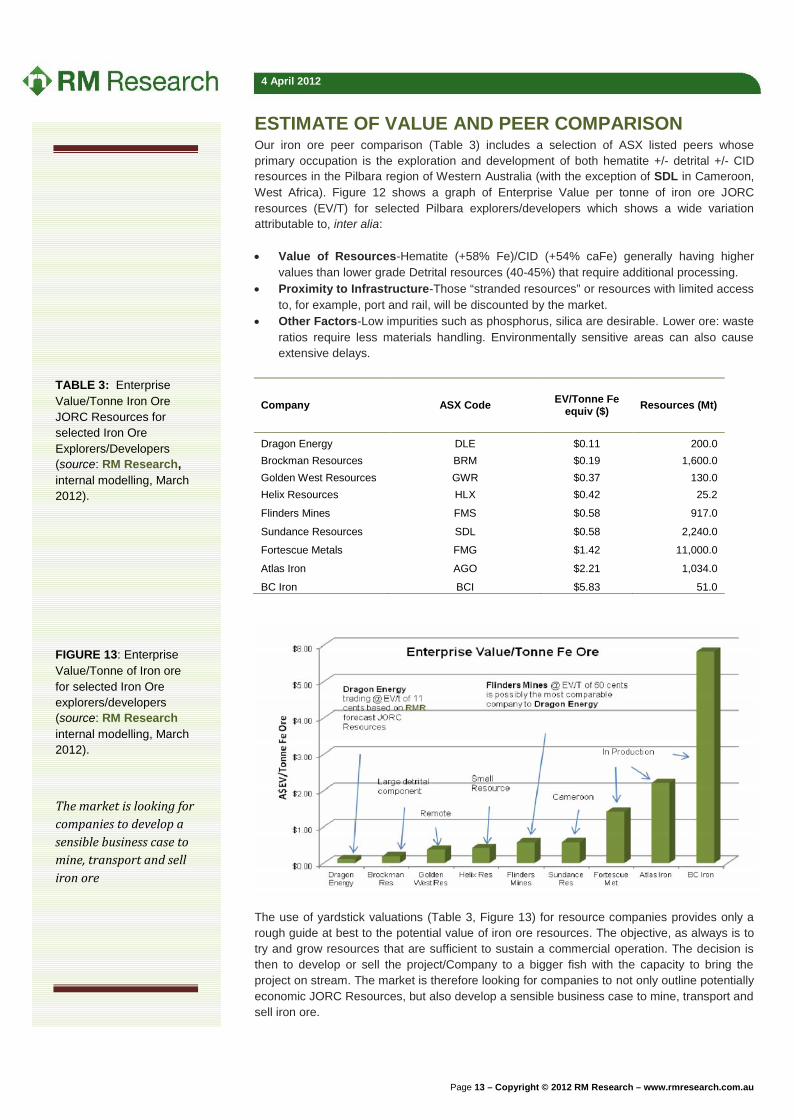

ESTIMATE OF VALUE AND PEER COMPARISONOur iron ore peer comparison (Table 3) includes a selection of ASX listed peers whoseprimary occupation is the exploration and development of both hematite +/- detrital +/- CIDresources in the Pilbara region of Western Australia (with the exception of SDL in Cameroon,West Africa). Figure 12 shows a graph of Enterprise Value per tonne of iron ore JORCresources (EV/T) for selected Pilbara explorers/developers which shows a wide variationattributable to, inter alia:

Value of Resources-Hematite (+58% Fe)/CID (+54% caFe) generally having highervalues than lower grade Detrital resources (40-45%) that require additional processing.

Proximity to Infrastructure-Those “stranded resources” or resources with limited accessto, for example, port and rail, will be discounted by the market.

Other Factors-Low impurities such as phosphorus, silica are desirable. Lower ore: wasteratios require less materials handling. Environmentally sensitive areas can also causeextensive delays.

Company ASX Code EV/Tonne Feequiv ($) Resources (Mt)

Dragon Energy DLE $0.11 200.0Brockman Resources BRM $0.19 1,600.0Golden West Resources GWR $0.37 130.0Helix Resources HLX $0.42 25.2

Flinders Mines FMS $0.58 917.0

Sundance Resources SDL $0.58 2,240.0

Fortescue Metals FMG $1.42 11,000.0

Atlas Iron AGO $2.21 1,034.0

BC Iron BCI $5.83 51.0

The use of yardstick valuations (Table 3, Figure 13) for resource companies provides only arough guide at best to the potential value of iron ore resources. The objective, as always is totry and grow resources that are sufficient to sustain a commercial operation. The decision isthen to develop or sell the project/Company to a bigger fish with the capacity to bring theproject on stream. The market is therefore looking for companies to not only outline potentiallyeconomic JORC Resources, but also develop a sensible business case to mine, transport andsell iron ore.

TABLE 3: EnterpriseValue/Tonne Iron OreJORC Resources forselected Iron OreExplorers/Developers(source: RM Research,internal modelling, March2012).

FIGURE 13: EnterpriseValue/Tonne of Iron orefor selected Iron Oreexplorers/developers(source: RM Researchinternal modelling, March2012).

The market is looking forcompanies to develop asensible business case tomine, transport and selliron ore

Page 14 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

Property Name Type US/T Res US$m % Country Buyer Seller

Mt Value Trans

DSO Iron Ore DSO 4.75 79 300 80% Canada Tata Steel New Millen.

Schefferville DSO 4.60 79 291 80% Canada Tata Steel New Millen.

Mayoko DSO 1.78 33 47 80% Congo Stirling Mins Cape Lambert

Yangqueqing DSO 1.63 18 29.4 100% China China Van. Huilixian Yang

Pilbara Iron Ore DSO 0.60 917 550 100% Australia Magnitogorsk Flinders Mines

Hercules DSO 1.11 59 33 50% Australia MCCM Capital Ironclad Min

Western Ck DSO 4.21 19 80 100% Australia Atlas Iron Warwick Res

Jupiter DSO 0.70 1890 1324 100% Brazil ECE (China) Unknown

Simandou DSO 0.60 2255 1350 100% Guinea Chalco (China) Rio Tinto

Hamersley DSO 0.14 143 10 51% Australia Saint Istvan Cazaly Res.

Roper Bar DSO 0.11 117 2.6 20% Australia Western Desert Itochu

Iron ore producers (and producers in general) are more commonly valued onpremium/discount to Net Present Value, so EV/Tonne figures for AGO, BCI and FMG areprobably less accurate as cash flow methods of valuation are preferred.

Table 4 (acquisitions) and Figure 13 (EV/Tonne of iron ore) give a wide range of valuationswith smaller projects (e.g. Hamersley, Cazaly Resources Ltd (ASX: CAZ)) attracting lowerEV/T values while strategically located resources such as Western Creek (WarwickResources Ltd – acquired by AGO) attracting good premiums on acquisition.

The most comparable metrics in our view would include the recent takeover bid for FMS byMagnitogorsk Iron and Steel Works which valued their Pilbara Iron Ore Project at around 60cents per tonne. Given the favourable location of Nameless and Rocklea, proximity toinfrastructure, together with the potential for JORC CID and Detrital resources up to 300Mt,RM Research considers EV/t of in excess of 60 cents are not unreasonable for our base casescenario (Figure 14).

TABLE 4: Recenttakeover metrics forselected DSO Iron Oreexplorers/developers(source: RM Research,internal modelling, March2012).

FIGURE 14: Possibleshare price outcomes forDragon Energy Limitedbased on EV/tonnemethods (source: RMResearch internalmodelling, March 2012).

Page 15 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

RISK ANALYSIS Exploration Risk: Infill drilling at Rocklea and Nameless may fail to convert JORC

resources to reserves or even upgrade JORC resources from the current Inferredcategory. Exploration on other projects in the DLE portfolio may fail to identify anymineralisation of economic value.

Traditional Owners: Negotiations with traditional owners at Rocklea and Nameless mayfail to deliver necessary site clearances for additional exploration/development. Wecurrently view this risk as very low given the concentration of mineralisation in and aroundpalaeo-channels.

Financial Position: The Company has insufficient cash reserves (around A$12.5 million)to progress its key projects (Rocklea and Nameless) into production, however thefinancial hurdles are not onerous in the scheme of iron ore development and RMResearch believe there are a number of financing options available.

Infrastructure Risks: One of the keys to iron ore development is access to adequateinfrastructure to enable delivery of product to market. RM Research believes there arepotential sites on the West Pilbara coastal region that could represent a temporarysolution while options for rail access (e.g. Solomon hub) are investigated.

Environmental/Permitting Risks: There may be delays in obtaining environmental andmining lease approvals. This is relevant for Rocklea and Nameless as well as theproposed port sites on the West Pilbara coast.

Commodity Risks: The Company is primarily exposed to iron ore. The demand/supplyscenario (see Iron Ore Market) remains strong with supply likely to be constrained byinfrastructure bottlenecks in the medium term. The ramp up of iron ore development inWest Africa poses a medium-long term risk to the competitiveness of Western Australianiron ore projects.

Market Risks: Further declines in equity markets may continue to put pressure on juniorresource companies as investors switch out of “risk” into perceived safe haveninvestments such as cash, gold and counter cyclical equities. Our medium term view isthat the risk premium has been eroded for many junior resource companies and we seenear term upside.

Currency Risks: A strengthening Australian dollar (as funds flow back into riskiercurrencies) may make the price of iron ore in local (Australian) currency terms lessattractive. This could have negative influences on Australian iron oreexplorers/developers.

Infrastructure risksremain the primaryconcern for iron oreexplorers/developers

West Africa poses a riskfor iron ore supply andmay threatencompetitiveness ofWestern Australia

Page 16 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

DIRECTORS AND MANAGEMENT

Jie Chen EXECUTIVE CHAIRMAN

Mr Chen has nearly 30 years operational and management experience, starting his career in1979 in a large state-owned coal mining enterprise in the PRC. Mr Chen has been chairmanof Shandong Group since 2002 and under his leadership, Shandong Group has formedvertically integrated businesses in coal, iron ore mining, processing and manufacturing withoperations in Shandong, Guizhou, Ningxia and Xinjiang. Mr Chen holds a master’s degree ineconomics and is currently completing a doctorate degree in mine engineering. He hasreceived multiple awards at provincial and national levels for achievements including being inthe 10 excellent entrepreneurs in Shandong Province, top 20 mine managers in the PRC, andPRC’s excellent entrepreneur.

Gang Xu, BSc, MSc, MBA, MAusIMM, MAICD MANAGING DIRECTOR

Mr Xu is a geologist with over 20 years experience. He spent 9 years as a senior uraniumexploration geologist with the China National Nuclear Corporation. Mr Xu spent a period asfinance and marketing manager for Sino Gold Limited as it developed the first internationalstandard mining operation in the PRC. He also has diverse experience in business research,marketing and finance. Mr Xu completed an MBA in the USA in 1997 and a masters ofgeology in the PRC. He is a member of AusIMM and AICD.

Tim Williams, B.Comm, LLB, Dip. Lan. COO & EXECUTIVE DIRECTOR

Mr Williams was most recently an associate of a corporate law firm in Adelaide, SouthAustralia. He has spent the last five years working predominantly in the areas of resourcesand energy law and has advised ASX listed companies on capital raisings, internationalinvestment, exploration and mining licensing, Corporations Act and ASX Listing Rulescompliance, native title negotiations and commercial contracts. Mr Williams holds Bachelor ofLaws and Bachelor of Commerce degrees as well as a Diploma of Languages from theUniversity of Adelaide. He has lived and studied in China and in recent years formed and ledthe resources and energy division of the Australia China Business Council in South Australia.

Anthony Ho, CA EXECUTIVE DIRECTOR

Mr Ho is a commerce graduate of the University of Western Australia, and qualified as aChartered Accountant in 1983 with Deloittes. He is the principal of a public practicespecialising in corporate and financial services to ASX-listed companies. Prior to establishingthe practice in 1991, Mr Ho spent 7 years in a senior corporate role with a major investmentand resource group in Western Australia. He is a director of a number of companies listed onASX.

Qingyong Guo, M.Min.Eng. EXECUTIVE DIRECTOR

Mr Guo is a graduate in mine engineering from the China University of Mining and Technologyand worked as a mine engineer for a large China state-owned coal mine and is GeneralManager of the Coal Project Generation Department for Shandong Group. He was creditedfor securing Chinese government approvals of two iron ore mining licenses in ShandongProvince and one coal mining licence in Northwest China. In 2004 he completed a master’sdegree in mine engineering.

Karen Logan, B.Com, Grad Dip AppCorpGov, ACIS, F Fin COMPANY SECRETARY

Ms Logan graduated with a Bachelor of Commerce majoring in Accounting and Business Lawfrom Curtin University in Western Australia and completed a Graduate Diploma in AppliedCorporate Governance with Chartered Secretaries Australia. She is a Chartered Secretaryand a Fellow of the Financial Services Institute of Australasia. Ms Logan has been a partnerof a public practice since 2006 and has significant experience in capital raising projects andASX listings. She is currently the secretary of a number of ASX-listed companies andprovides corporate and accounting advice and services to those clients.

The Shandong Group is avertically integratedcoal, iron ore, mineralprocessing andmanufacturingcompany...

Gang is a geologist withover 20 years’ experience

Tim has lived and studiedin China

Anthony qualified as aChartered Accountantwith Deloittes in 1983

Qingyong has worked asa mine engineer for astate owned coal mine

Karen has significantcapital raisingexperience

Page 17 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

Mark Hafer, B.Sc (Hons), B.Bus (Finance), MAIG, Affiliate Finsia EXPLORATION MANAGER

Mr Hafer is a geologist with more than 10 years experience and is a member of theAustralasian Institute of Geoscientists and an affiliate of the Financial Services Institute ofAustralasia. Mr Hafer has undertaken and managed greenfields to brownfields explorationprogrammes for gold and base metals predominantly in Australia, and in Kazakhstan. Prior tocommencing with DLE Mark was Senior Exploration Geologist at Mount Gibson Iron.Previously he has also worked in the finance industry, including a Mining Commodity Analystrole.

CONCLUSIONRM Research considers the Company represents outstanding value with our base casescenario of 200Mt suggesting a near term price target of 62 cents compared to the currentmarket price of 17 cents. In addition to the compelling valuation metrics, we believe the tightlyheld register together with support of Shandong Group and its board representatives will putthe Company in an excellent position to advance Nameless and Rocklea. The caveats, asever, are the various approval processes together with access to port facilities and third partyrail. As BCI have discovered, this can be an expensive exercise. Speculative Buy.

Mark was previously aSenior Geologist with MtGibson Iron

The caveats are access toPort and Rail....

...this could be expensive

Page 18 – Copyright © 2012 RM Research – www.rmresearch.com.au

4 April 2012

Registered OfficesPerthLevel 2, 6 Kings Park RdWest Perth WA 6005

Phone: +61 8 9488 0800Fax: +61 8 9488 0899

PO Box 154West Perth WA 6872

Email / [email protected]

RM Research Recommendation CategoriesCare has been taken to define the level of risk to return associated with a particular company.Our recommendation ranking system is as follows:

Buy Companies with ‘Buy’ recommendations have been cash flow positive for some time and have a moderate tolow risk profile. We expect these to outperform the broader market.

Speculative Buy We forecast strong earnings growth or value creation that may achieve a return well above that of thebroader market. These companies also carry a higher than normal level of risk.

Hold A sound well managed company that may achieve market performance or less, perhaps due to anovervalued share price, broader sector issues, or internal challenges.

Sell Risk is high and upside low or very difficult to determine. We expect a strong underperformance relative tothe market and see better opportunities elsewhere.

Disclaimer / DisclosureThis report was produced by RM Research Pty Ltd, which is a Corporate Authorised Representative of RM Capital Pty Ltd (Licence no. 221938). RM Research will receivepayment of A$17,500 for the compilation and distribution of two research reports. RM Research Pty Ltd has made every effort to ensure that the information and materialcontained in this report is accurate and correct and has been obtained from reliable sources. However, no representation is made about the accuracy or completeness of theinformation and material and it should not be relied upon as a substitute for the exercise of independent judgment. Except to the extent required by law, RM Research Pty Ltddoes not accept any liability, including negligence, for any loss or damage arising from the use of, or reliance on, the material contained in this report. This report is forinformation purposes only and is not intended as an offer or solicitation with respect to the sale or purchase of any securities. The securities recommended by RM Researchcarry no guarantee with respect to return of capital or the market value of those securities. There are general risks associated with any investment in securities. Investorsshould be aware that these risks might result in loss of income and capital invested. Neither RM Research nor any of its associates guarantees the repayment of capital.WARNING: This report is intended to provide general financial product advice only. It has been prepared without having regarded to or taking into account any particularinvestor’s objectives, financial situation and/or needs. Accordingly, no recipients should rely on any recommendation (whether express or implied) contained in this documentwithout obtaining specific advice from their advisers. All investors should therefore consider the appropriateness of the advice, in light of their own objectives, financialsituation and/or needs, before acting on the advice. Where applicable, investors should obtain a copy of and consider the product disclosure statement for that product (if any)before making any decision.DISCLOSURE: RM Research Pty Ltd and/or its directors, associates, employees or representatives may not effect a transaction upon its or their own account in theinvestments referred to in this report or any related investment until the expiry of 24 hours after the report has been published. Additionally, RM Research Pty Ltd may have,within the previous twelve months, provided advice or financial services to the companies mentioned in this report. As at the date of this report, the directors, associates,employees, representatives or Authorised Representatives of RM Research Pty Ltd and RM Capital Pty Ltd may hold shares in Dragon Energy Limited.