draft for discussion. subject to change. package...

TRANSCRIPT

Package 2COMPREHENSIVE TAX REFORM PROGRAM

Cost-benefit analysis of fiscal incentives

As of 15 October 2018 9:00 pm

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

2. Cost-benefit analysis What do we gain from a review of past incentives and benefits received?

1. Why is reform necessary?

Cont

ent

4. ResultsWhat have we learned?

3. MethodsHow do we account for total

benefits and costs?

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

The Philippines has the highest corporate income tax rate in the ASEAN region.

Source: Asian Development Bank and PWC

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

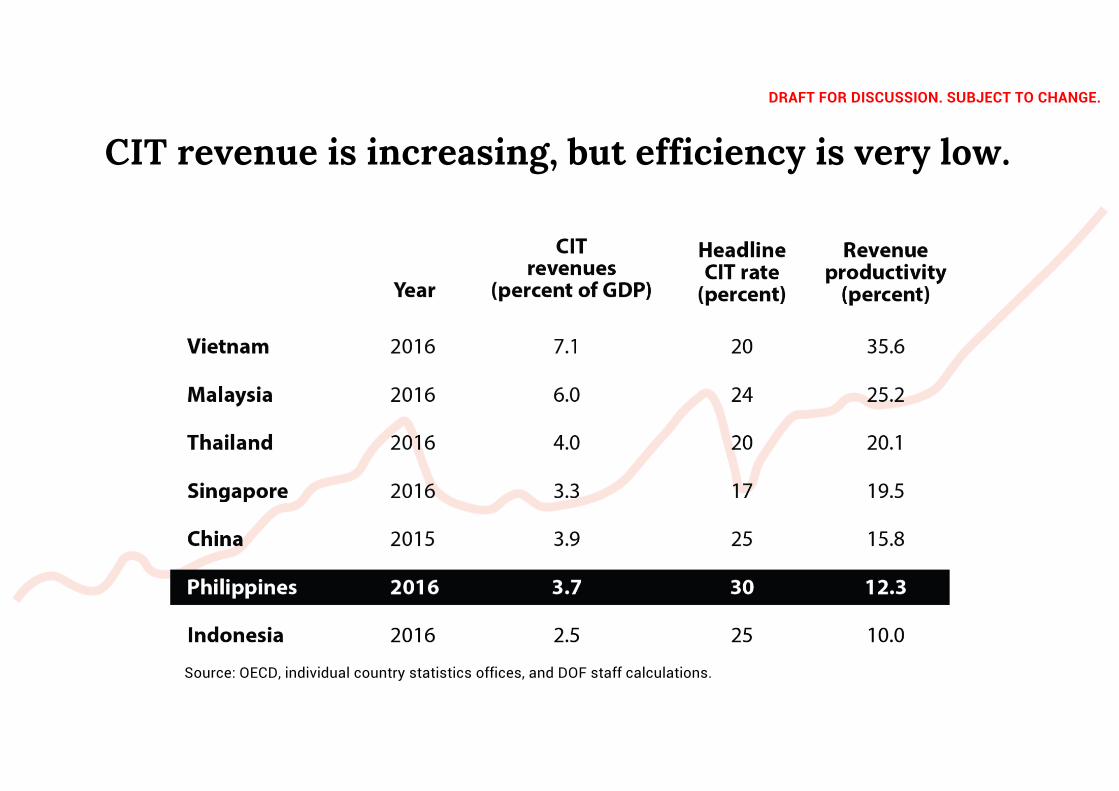

CIT revenue is increasing, but efficiency is very low.

Source: OECD, individual country statistics offices, and DOF staff calculations.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

We have a complex tax incentives system.

- 14 IPAs - 136 investment laws

200 non-investment laws

- 546 ‘ecozones’ and freeports

We grant the most generous fiscal incentives since they are in lieu of all taxes and given forever.

Source: Individual country finance agencies and investment promotion offices.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Huge inequity under the current system: ● Firms with no incentives pay

the regular rate of 30% of net taxable income

● Firms with incentives pay between 6% and 13%

For example, almost all of the 90,000 SMEs pay the regular 30%

rate.Source: DTI and TIMTA

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Estimated forgone revenue due to tax incentives

Tax incentives in billion pesos

Type of tax

Income tax

Customs duties

Subtotal

Import VAT (gross)

Local VAT (gross)

Local business tax

Subtotal for incentives

Leakage

Total

No. of recipients

2015

86

18

104

160

37

TBD

301

43

344

2,844

2016

121

57

179

TBD

TBD

TBD

TBD

TBD

TBD

3,102

Source: TIMTA, DOF estimates

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

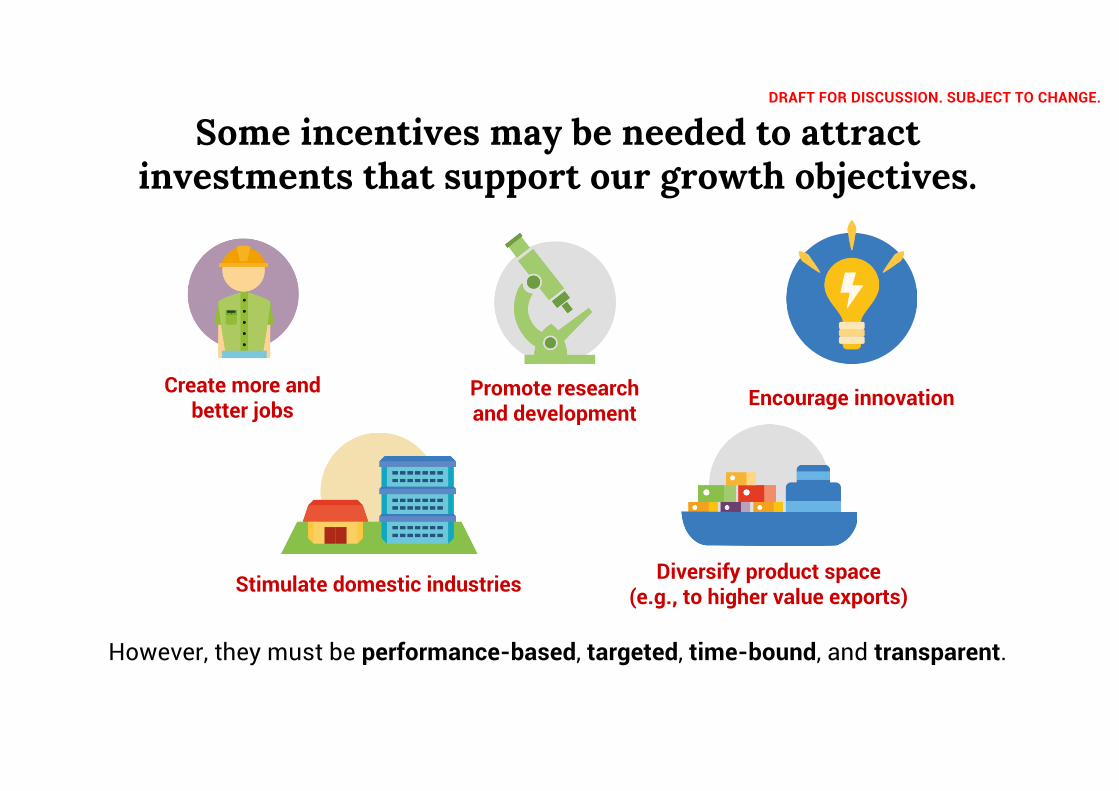

Some incentives may be needed to attract investments that support our growth objectives.

Create more and better jobs

Promote research and development

Encourage innovation

Stimulate domestic industries Diversify product space (e.g., to higher value exports)

However, they must be performance-based, targeted, time-bound, and transparent.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Number of firms enjoying incentives for at least 15 years

We have been supporting many firms unnecessarily.

645 firms receiving incentives for at least 15 years.

Source: TIMTA.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

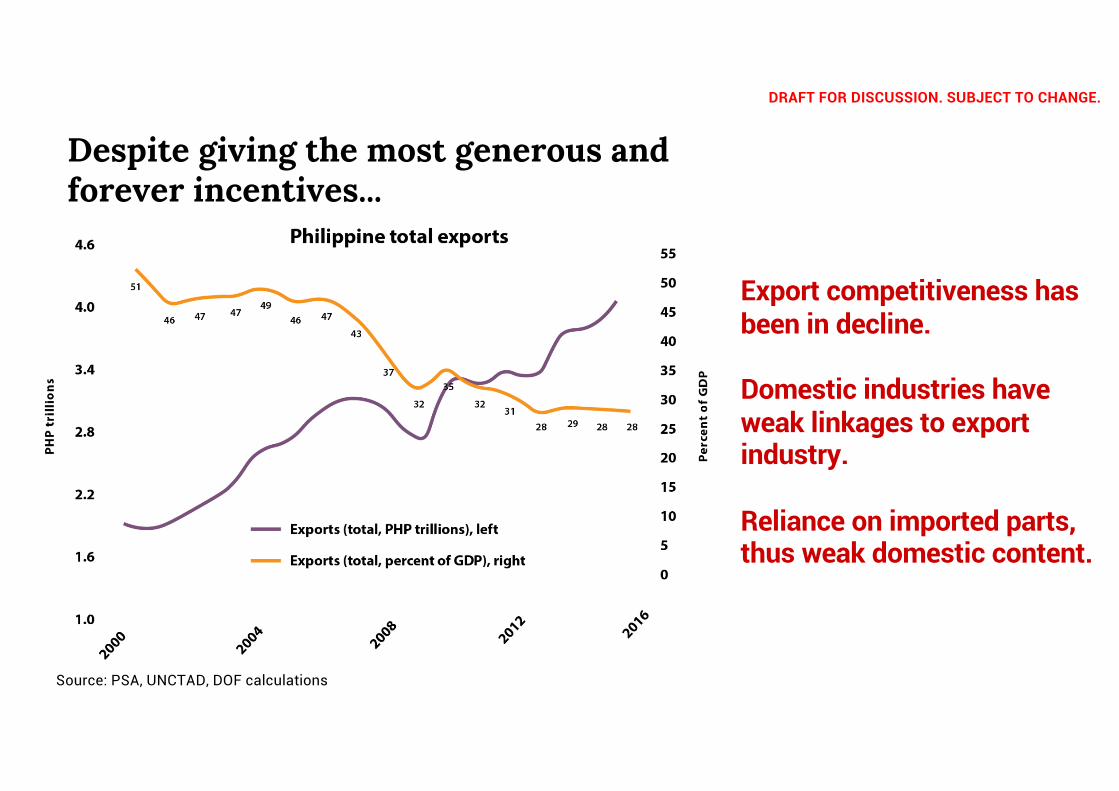

Despite giving the most generous and forever incentives...

FDI pales in comparison to our neighbors.

Source: BSP, UNCTAD, and DOF calculations

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Export competitiveness has been in decline.

Domestic industries have weak linkages to export industry.

Reliance on imported parts, thus weak domestic content.

Despite giving the most generous and forever incentives...

Source: PSA, UNCTAD, DOF calculations

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

The current incentives system has a big room for improvement.

- Complexity and inequity- Lack of monitoring and evaluation,

accountability, and transparency- Incentives as band-aid solution to

compensate for past structural weaknesses

It is time that we revisit our incentives system to ensure that we gain from every peso that we grant.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Incentives may be important to encourage investments that promote growth and jobs...

Some incentives are unnecessary, i.e., investment would have happened anyway even without the incentives (e.g., available

market, quality labor, land, resources, etc.).

...but, investment tax incentives are tax expenditures that someone else has to pay.It is not free money from heaven.

Government needs to ensure efficiency in spending.

(How much tax incentive can we afford?)

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Package 2Fair and accountable tax incentives system

Every peso granted as tax incentive is a peso off the budget that could have been spent for infrastructure, health, education, and social protection that

benefit all, and not only a few.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

“Ex-post” cost-benefit analysis

This is done so that we can determine if the tax incentives given to recipients benefit our economy more than it costs.

Note: Evaluation of the past performance does not necessarily indicate future priority or preference over some industries.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Tax incentives usually violate the principles of:

Efficiency Equity Simplicity

However, incentives may be justified if they provide net benefit to society as a whole.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Basis for cost-benefit analysis

Economic value

Social value

Political value

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Cost-benefit analysis: Methods

1. Estimating implicit labor subsidyWhat is the cost for each job created?

3. Estimating net government revenue Do we generate more revenue from the tax we forego?

2. Performing a counterfactual analysisDo firms with registered activities for incentives perform better in terms of job creation, R&D investments, productivity, etc. when compared to non-registered firms?

4. Accounting of direct and indirect cost and benefitDo total benefits from incentives, both private and social, outweigh total costs?

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

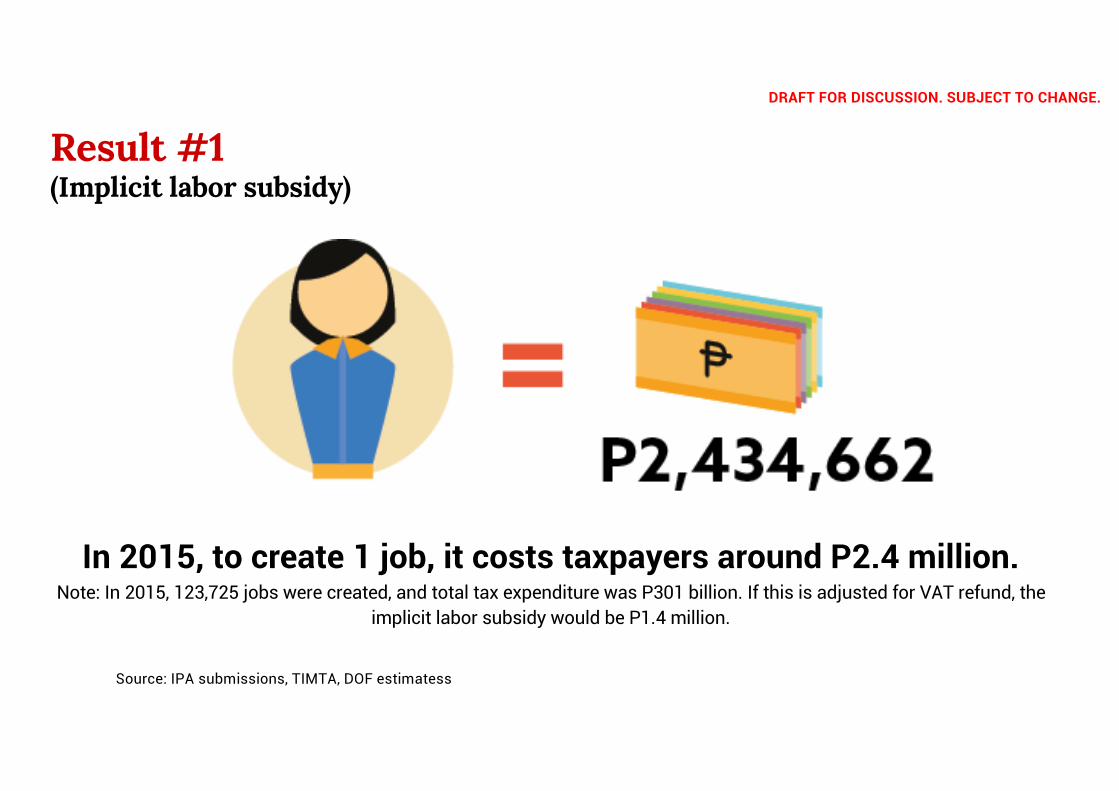

Result #1 (Implicit labor subsidy)

Source: IPA submissions, TIMTA, DOF estimatess

In 2015, to create 1 job, it costs taxpayers around P2.4 million.Note: In 2015, 123,725 jobs were created, and total tax expenditure was P301 billion. If this is adjusted for VAT refund, the

implicit labor subsidy would be P1.4 million.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

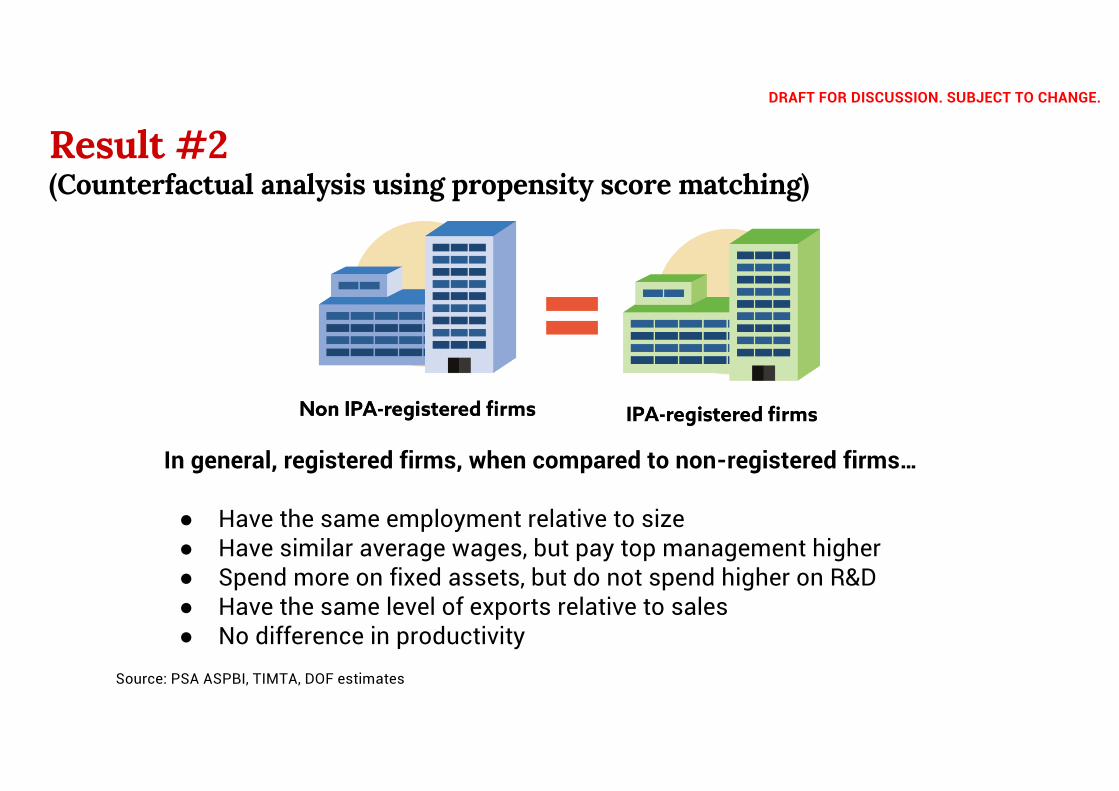

In general, registered firms, when compared to non-registered firms…

● Have the same employment relative to size● Have similar average wages, but pay top management higher● Spend more on fixed assets, but do not spend higher on R&D● Have the same level of exports relative to sales● No difference in productivity

Result #2 (Counterfactual analysis using propensity score matching)

Source: PSA ASPBI, TIMTA, DOF estimates

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Summary(all firms)

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

On average, for every peso we grant as incentive, we collect 34 cents in taxes, even after accounting for taxes from indirect employment and domestic inputs.

If taxes from unnecessary incentives are accounted for, we collect 95 cents.

Result #3 (Net government revenue effect)

Taxes collected from:FirmsEmployeesDividends

Indirect employeesDomestic inputs

Tax incentives on:IncomeDuties (30%)VAT (net of refund)Local taxes

Source: IPA submissions, SEC, TIMTA, DOF estimates

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

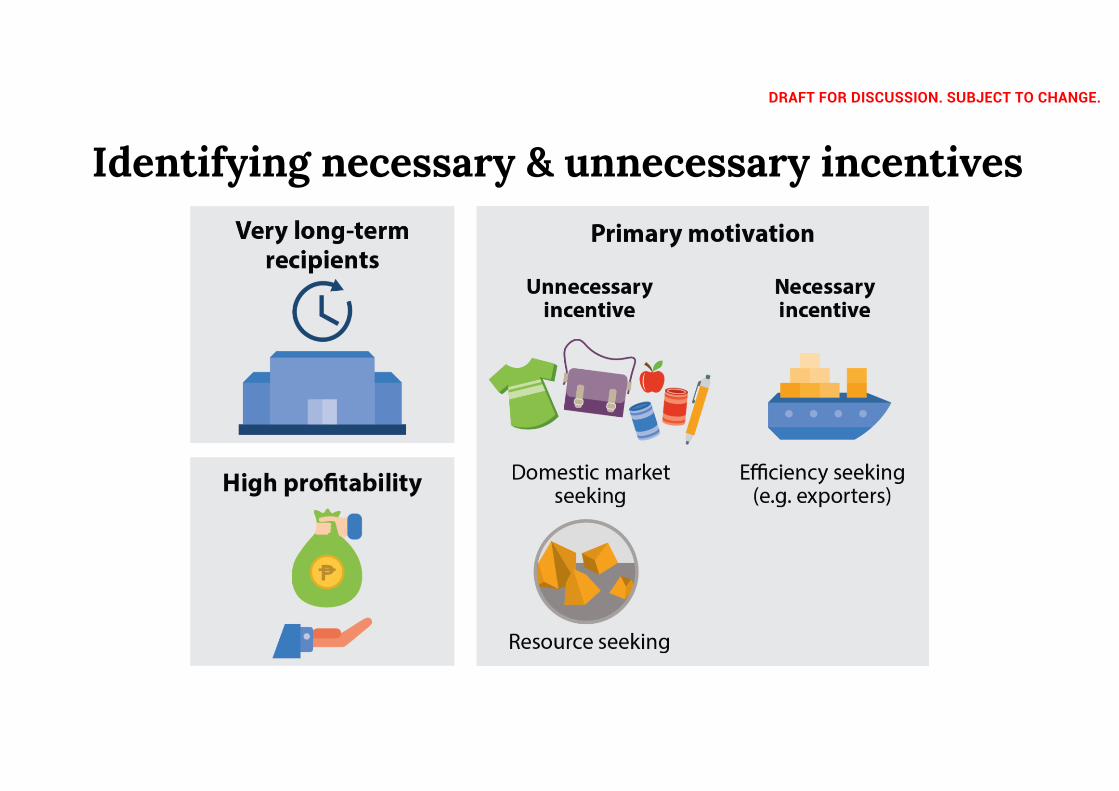

Identifying necessary & unnecessary incentives

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

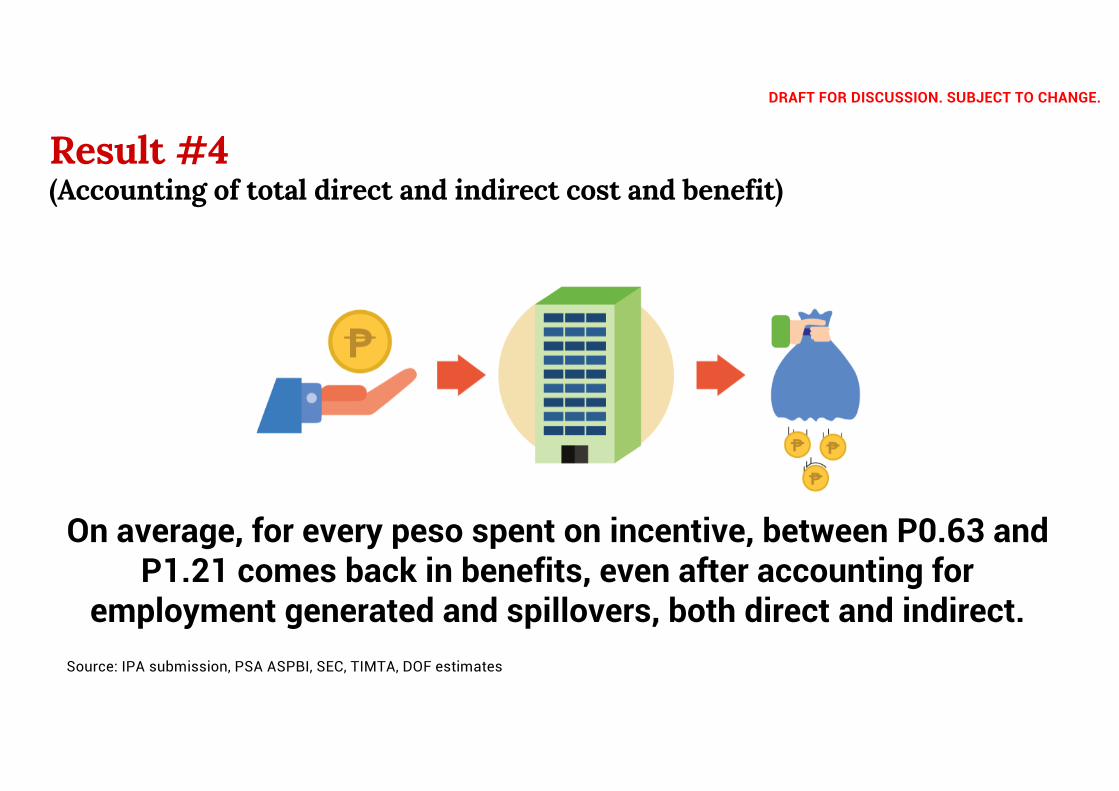

On average, for every peso spent on incentive, between P0.63 and P1.21 comes back in benefits, even after accounting for

employment generated and spillovers, both direct and indirect.

Result #4 (Accounting of total direct and indirect cost and benefit)

Source: IPA submission, PSA ASPBI, SEC, TIMTA, DOF estimates

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Dividends declared at 164% of income tax incentives received

Source: SEC, TIMTA

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Source: TIMTA, DOF estimates

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Resu

lt #2

Resu

lt #1

Sum

mar

y

Resu

lt #3

Resu

lt #4For every peso we

grant as incentive, we collect 34 cents

in taxes.

For every peso spent on incentive, between P0.63 and P1.21 comes back in

benefits.

In general, registered firms do not perform better on employment,

exports, and productivity compared to non-registered firms.

To create 1 job, it costs taxpayers at least

P2,434,662.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

There are other and may be better ways to support firms

Granting tax incentives is not the only way to

directly help firms

The government can use more efficient and targeted subsidies

The real solution in the medium-term is to address

infrastructure gaps, corruption, inefficiency in government, and complex

business regulations

Ex. lifeline subsidies, power subsidies, housing vouchers, skills training, etc.

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Incentives must be

With effective monitoring and evaluation system and anchored on a strategic investment priority plan that emphasizes:

Job creation Research & development

Countrysidedevelopment

Skills training Innovation

DRAFT FOR DISCUSSION. SUBJECT TO CHANGE.

Thank you!