dr. varadraj bapat, iit mumbai1 module 12. cost volume profit analysis dr. varadraj bapat

TRANSCRIPT

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 11

Module 12.

Cost Volume Profit Analysis

Dr. Varadraj Bapat

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 22

Cost Volume Cost Volume Profit (CVP)Profit (CVP)

IntroductionIntroduction Fixed costsFixed costs Variable costsVariable costs Semi variable costsSemi variable costs Contribution marginContribution margin Break even pointBreak even point PV RatioPV Ratio

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 33

CVP AnalysisCVP Analysis

CVP analysis is the analysis of three CVP analysis is the analysis of three variable viz. cost, volume and variable viz. cost, volume and profit. Such analysis explores the profit. Such analysis explores the relationship existing amongst costs, relationship existing amongst costs, revenue, activity level and resulting revenue, activity level and resulting profit. It aims at measuring profit. It aims at measuring variation of cost with profit.variation of cost with profit.

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 44

Fixed CostFixed Cost

These are the costs which incurred These are the costs which incurred for a period and which within for a period and which within certain output and turnover limits, certain output and turnover limits, tend to be unaffected by tend to be unaffected by fluctuations in the levels of activity fluctuations in the levels of activity (Output or turnover). (Output or turnover).

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 55

For example: Rent, insurance of For example: Rent, insurance of factory building etc. remain the factory building etc. remain the same for different levels of same for different levels of production.production.

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 66

Fixed Cost GraphFixed Cost Graph

Fixed Cost

Total Cost

Am

t

Units

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 77

Variable CostVariable Cost

These costs tend to very with the These costs tend to very with the volume of activity. Any increase volume of activity. Any increase in activity results in an increase in activity results in an increase in the variable cost and vice in the variable cost and vice versa. versa.

For example: Cost of direct For example: Cost of direct labour, direct material, etc. labour, direct material, etc.

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 88

Variable Cost Variable Cost GraphGraph

Variable Cost

`

Units

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 99

These costs contain both fixed These costs contain both fixed and variable components and and variable components and thus partly affected by thus partly affected by fluctuation in the level of activity. fluctuation in the level of activity. Examples of semi variable costs Examples of semi variable costs are telephone bill, gas and are telephone bill, gas and electricity etc. electricity etc.

Semi-Variable CostSemi-Variable Cost

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 1010

Semi-Variable Cost Semi-Variable Cost GraphGraph

Semi-Variable Cost

`

Units

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 1111

Cost-Volume-Profit Cost-Volume-Profit AnalysisAnalysis

CVP analysisCVP analysis:: Takes into account Takes into account

– the total costs (fixed and the total costs (fixed and variable)variable)

– the total sales revenuesthe total sales revenues– desired profits vis-a-vis the desired profits vis-a-vis the sales volumesales volume

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 1212

It is used for forecasting or It is used for forecasting or predicting how the changes in predicting how the changes in costs and sales volume affect costs and sales volume affect profit. It is also known as 'Break-profit. It is also known as 'Break-Even Analysis'.Even Analysis'.CVP analysis could be helpful in CVP analysis could be helpful in the following situations:the following situations:

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 1313

Budget planning: for forecasting Budget planning: for forecasting profit by considering cost and profit by considering cost and profit relation, and volume of profit relation, and volume of production volume. This will help production volume. This will help in determining the sales volume in determining the sales volume required to make a profit.required to make a profit.–To make decisions regarding To make decisions regarding pricing and sales volume.pricing and sales volume.

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 1414

Determining the sales mix of different Determining the sales mix of different products, in what proportions each of products, in what proportions each of the the products can be soldproducts can be sold..– Preparing flexible budget considering Preparing flexible budget considering

costs at different levels of productioncosts at different levels of production

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 1515

Objectives of CVP Objectives of CVP AnalysisAnalysis

– Understand the interaction Understand the interaction amongamong Prices of products Prices of products Volume or level of activity Volume or level of activity Per unit variable cost Per unit variable cost Total fixed cost Total fixed cost Mix of product sold Mix of product sold

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 1616

Assumptions of CVP Assumptions of CVP AnalysisAnalysis

• Expenses can be classified as either Expenses can be classified as either variable or fixed.variable or fixed.

• CVP relationships are linear over a CVP relationships are linear over a wide range of production and sales.wide range of production and sales.

• Sales prices, unit variable cost, and Sales prices, unit variable cost, and total fixed expenses will not vary total fixed expenses will not vary within the relevant range.within the relevant range.

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 1717

• Volume is the only cost driver.Volume is the only cost driver.• The relevant range of volume is The relevant range of volume is

specified.specified.• Inventory levels will be Inventory levels will be

unchanged.unchanged.• The sales mix remains The sales mix remains

unchanged during the period.unchanged during the period.

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 1818

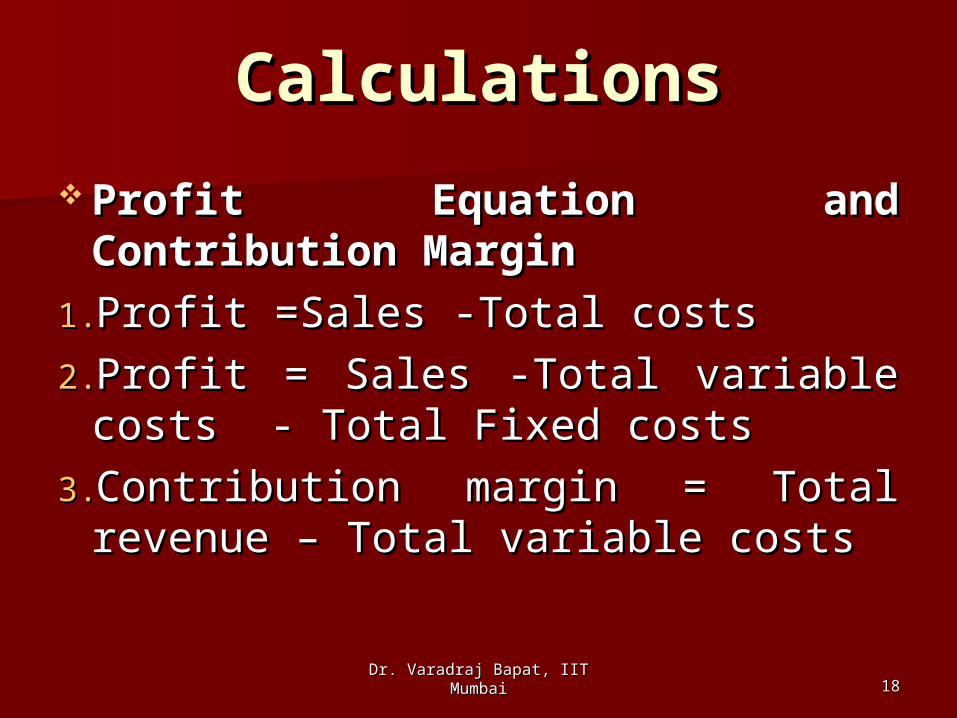

CalculationsCalculations

Profit Equation and Profit Equation and Contribution MarginContribution Margin

1.1.Profit =Sales -Total costsProfit =Sales -Total costs

2.2.Profit = Sales -Total variable costs Profit = Sales -Total variable costs - Total Fixed costs- Total Fixed costs

3.3.Contribution margin = Total Contribution margin = Total revenue – Total variable costsrevenue – Total variable costs

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 1919

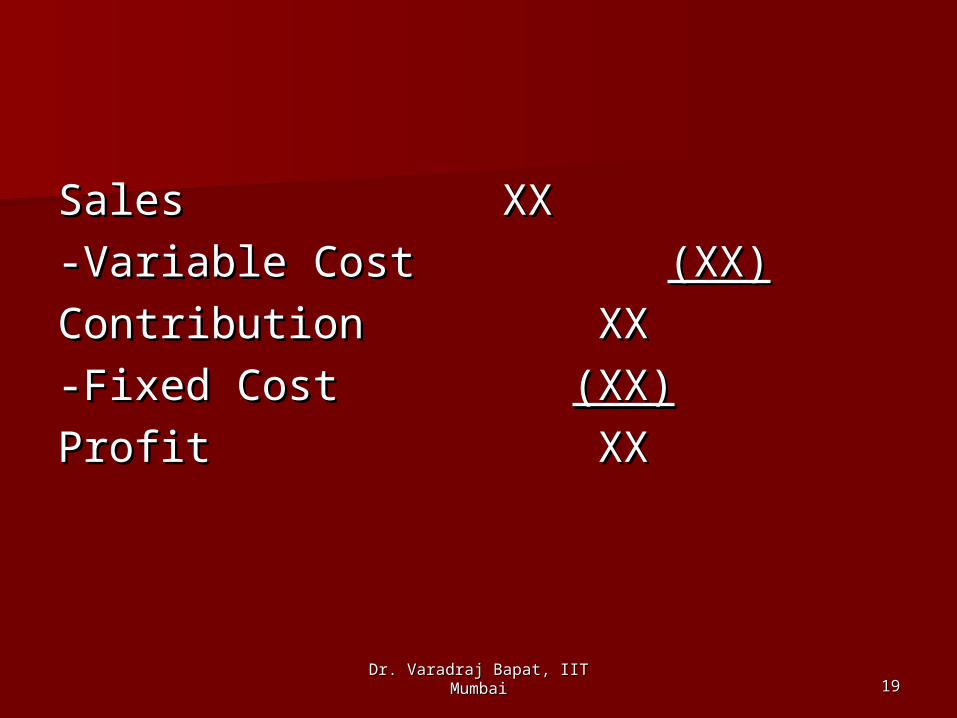

SalesSales XX XX

-Variable Cost-Variable Cost (XX)(XX)

ContributionContribution XX XX

-Fixed Cost-Fixed Cost (XX)(XX)

ProfitProfit XX XX

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 2020

Profit = (S-V)*Q – FCProfit = (S-V)*Q – FC Q = (FC + Expected Profit)Q = (FC + Expected Profit)

(S-VC)(S-VC) Q is the no. of units required to Q is the no. of units required to

be sold to obtain target profit.be sold to obtain target profit. S=Selling Price p.u. VC=Variable S=Selling Price p.u. VC=Variable

cost p.u. FC=Fixed Costcost p.u. FC=Fixed Cost

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 2121

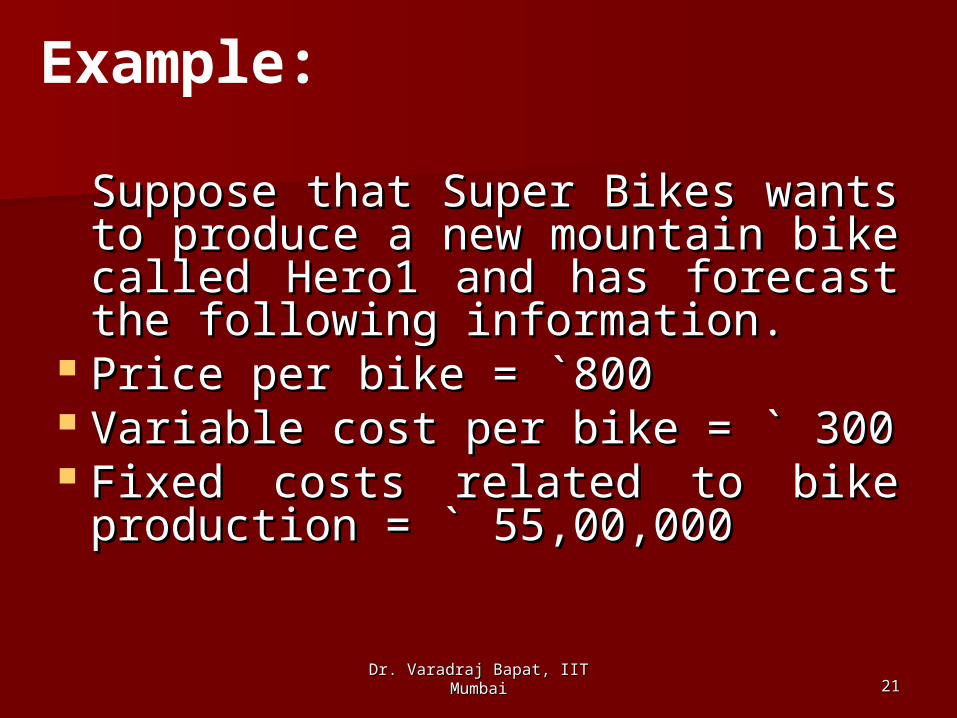

Suppose that Super Bikes wants Suppose that Super Bikes wants to produce a new mountain bike to produce a new mountain bike called Hero1 and has forecast called Hero1 and has forecast the following information.the following information.

Price per bike = Price per bike = `̀800800 Variable cost per bike = Variable cost per bike = ` ` 300300 Fixed costs related to bike Fixed costs related to bike

production = production = `̀ 55,00,000 55,00,000

Example:

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 2222

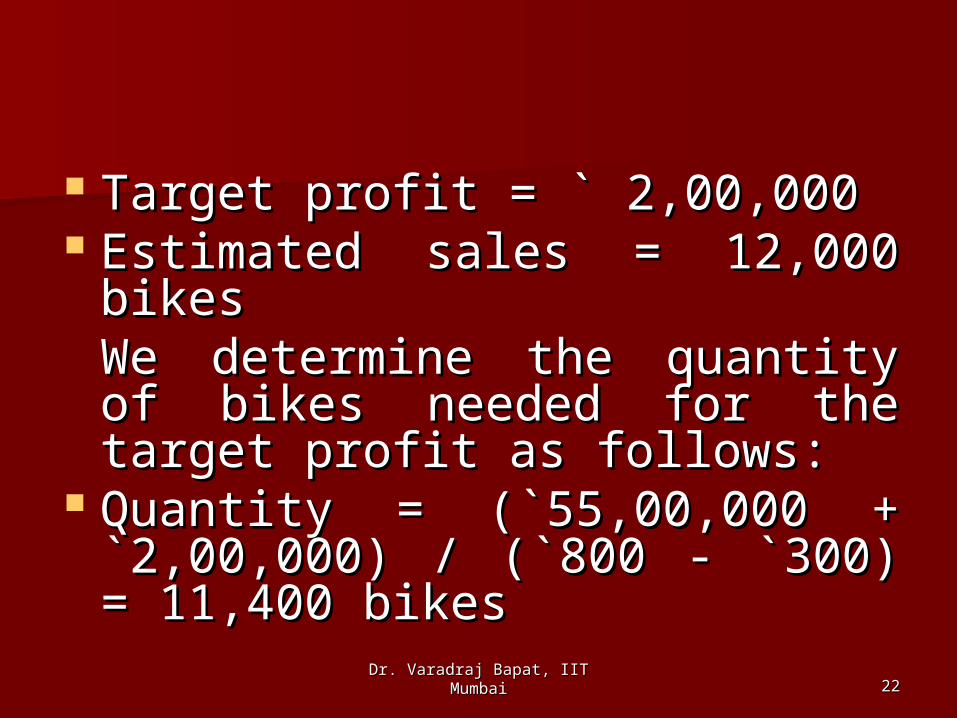

Target profit = Target profit = `̀ 2,00,000 2,00,000 Estimated sales = 12,000 bikesEstimated sales = 12,000 bikes

We determine the quantity of We determine the quantity of bikes needed for the target bikes needed for the target profit as follows:profit as follows:

Quantity = (Quantity = (`̀55,00,000 + 55,00,000 + `̀2,00,000) / (2,00,000) / (`̀800 - 800 - `̀300) = 300) = 11,400 bikes11,400 bikes

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 2323

Profit Volume Ratio Profit Volume Ratio (PV)(PV)

The contribution margin ratio The contribution margin ratio (CMR) i.e. PV ratio is the (CMR) i.e. PV ratio is the percentage by which the selling percentage by which the selling price (or revenue) per unit price (or revenue) per unit exceeds the variable cost per exceeds the variable cost per unit, or contribution margin as a unit, or contribution margin as a percentage of revenue. percentage of revenue.

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 2424

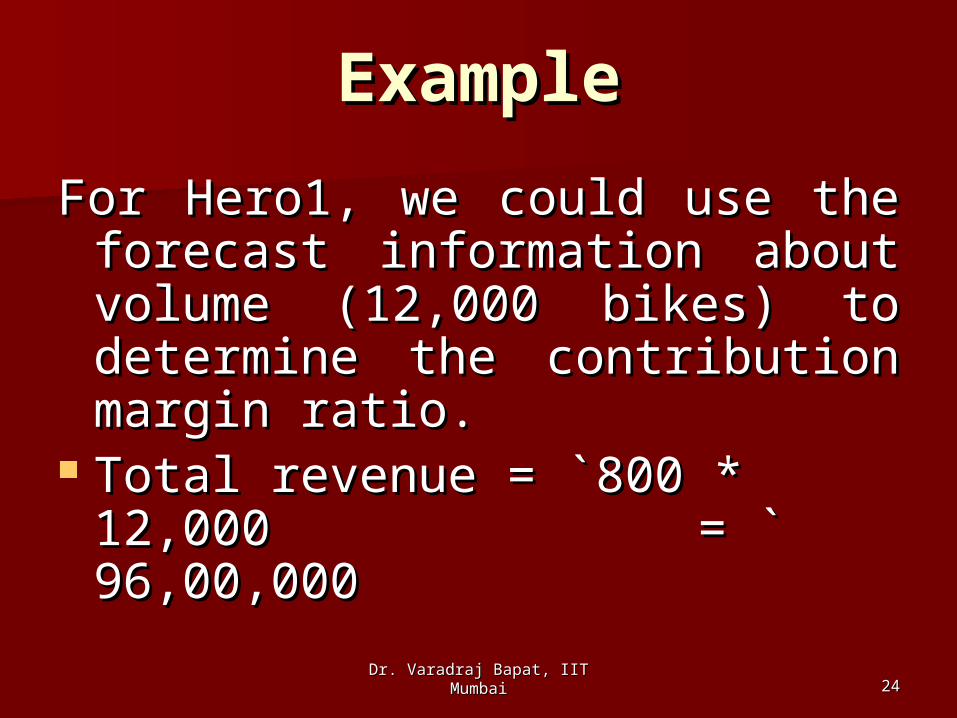

ExampleExample

For Hero1, we could use the For Hero1, we could use the forecast information about forecast information about volume (12,000 bikes) to volume (12,000 bikes) to determine the contribution determine the contribution margin ratio.margin ratio.

Total revenue = Total revenue = `̀800 * 12,000 800 * 12,000 = = `̀ 96,00,000 96,00,000

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 2525

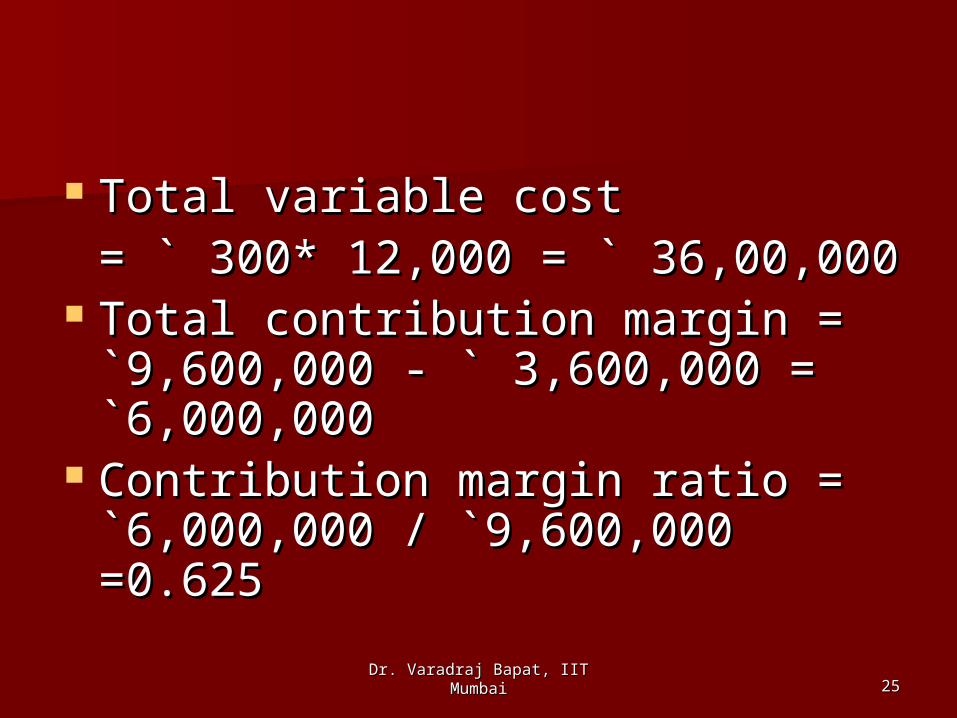

Total variable cost Total variable cost = = `̀ 300* 12,000 = 300* 12,000 = `̀ 36,00,000 36,00,000

Total contribution margin = Total contribution margin = `̀9,600,000 - 9,600,000 - `̀ 3,600,000 = 3,600,000 = `̀6,000,0006,000,000

Contribution margin ratio = Contribution margin ratio = `̀6,000,000 / 6,000,000 / `̀9,600,000 =0.6259,600,000 =0.625

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 2626

BEP analysisBEP analysis

Breakeven analysis is used to Breakeven analysis is used to find the minimum level of find the minimum level of production required production required

Evaluates both fixed and Evaluates both fixed and variable costsvariable costs

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 2727

Uses:Uses:

1.1. To find a suitable product mixTo find a suitable product mix

2.2. To find the sales required to To find the sales required to reach a desired revenue.reach a desired revenue.

3.3. The profits at certain price The profits at certain price level and saleslevel and sales

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 2828

Break even Point Break even Point (BEP)(BEP)

A CVP analysis can be used to A CVP analysis can be used to determine the BEP, or level of determine the BEP, or level of operating activity at which operating activity at which revenues cover all fixed and revenues cover all fixed and variable costs, resulting in zero variable costs, resulting in zero profit.profit.

In other words this is the point In other words this is the point where no profit or losses have been where no profit or losses have been mademade

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 2929

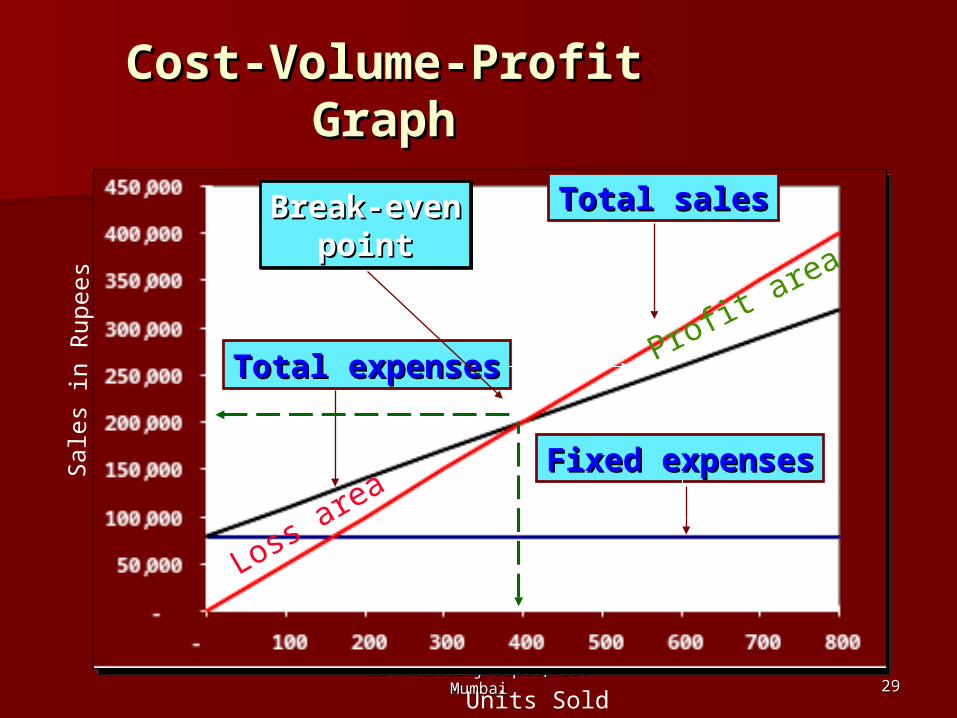

Cost-Volume-Profit Cost-Volume-Profit GraphGraph

Fixed expensesFixed expenses

Units Sold

Sale

s in

Rupees

Total expensesTotal expenses

Total salesTotal salesBreak-evenBreak-evenpointpoint

Break-evenBreak-evenpointpoint

Profit area

Loss area

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 3030

Break even Break even ApplicationsApplications

• New Product decisions :- Enables to determine the sale volume required for a firm (or an individual product) to breakeven , given expected sales price and expected costs.

• Pricing decisions:- Enables to study the effect of changing price and volume relationship on total profits.

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 3131

• Modernizations or automation decisions:- Analysis the profit in implication of a modernization or automation programme.

• Expansion Decisions :- studies the aggregate effect of a general expansion in production and sales.

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 3232

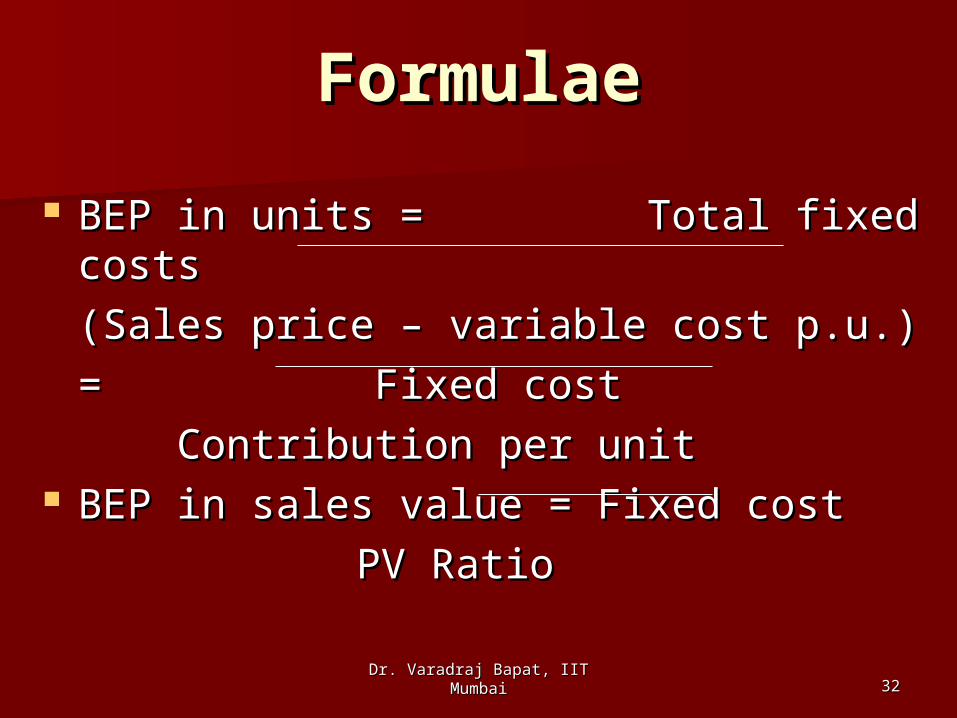

FormulaeFormulae

BEP in units = Total fixed costsBEP in units = Total fixed costs

(Sales price – variable cost (Sales price – variable cost p.u.)p.u.)

= Fixed cost= Fixed cost

Contribution per unitContribution per unit BEP in sales value = Fixed cost BEP in sales value = Fixed cost

PV RatioPV Ratio

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 3333

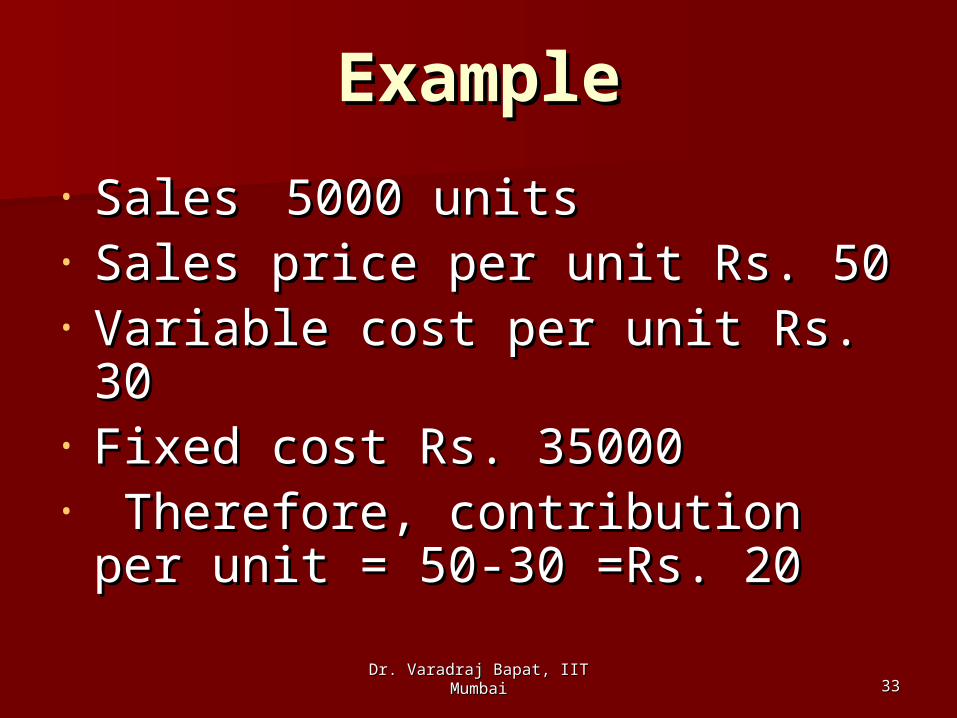

ExampleExample

• SalesSales 5000 units5000 units• Sales price per unit Rs. 50Sales price per unit Rs. 50• Variable cost per unit Rs. 30Variable cost per unit Rs. 30• Fixed cost Rs. 35000Fixed cost Rs. 35000• Therefore, contribution per unit Therefore, contribution per unit

= 50-30 =Rs. 20= 50-30 =Rs. 20

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 3434

BEP in units = 35000/20 BEP in units = 35000/20 = 1750 units = 1750 units

1750 * 50 = Rs. 1750 * 50 = Rs. 8750087500

BEP in sales value = 35000 * BEP in sales value = 35000 * 250000 / 87500250000 / 87500

= Rs. 100000= Rs. 100000

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 3535

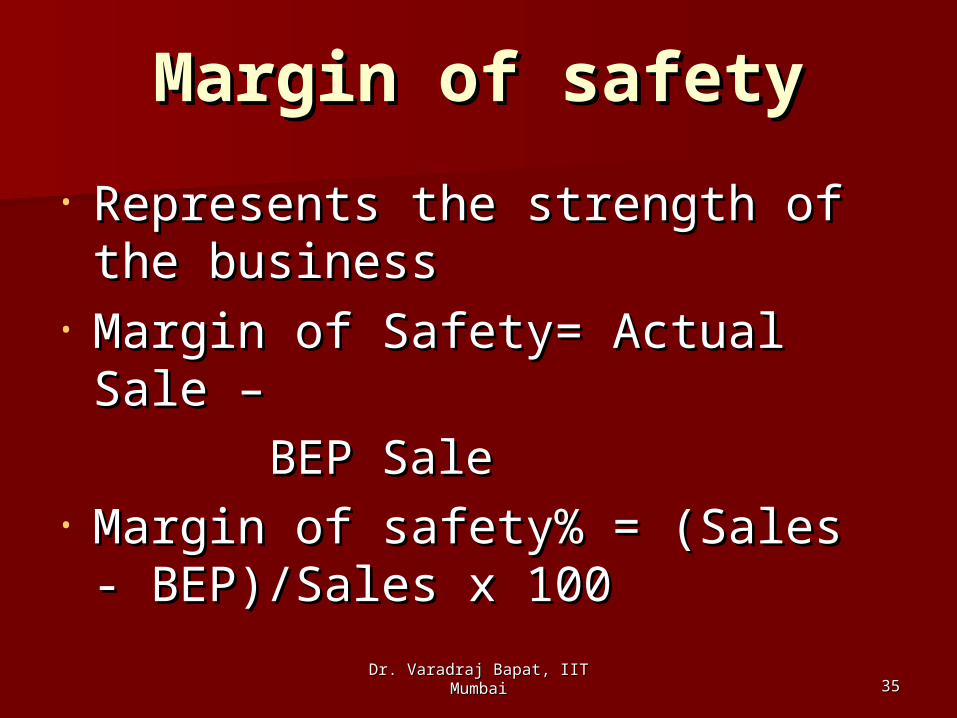

Margin of safetyMargin of safety

• Represents the strength of the Represents the strength of the businessbusiness

• Margin of Safety= Actual Sale –Margin of Safety= Actual Sale –

BEP BEP SaleSale

• Margin of safety% = (Sales - Margin of safety% = (Sales - BEP)/Sales x 100BEP)/Sales x 100

Dr. Varadraj Bapat, IIT MumbaiDr. Varadraj Bapat, IIT Mumbai 3636

• Margin of safety = (5000-1750) Margin of safety = (5000-1750) 5000 5000

=65% =65%• Hence even if the sales Hence even if the sales

decrease by 65%, the business decrease by 65%, the business wont face any losswont face any loss