dr. md chase long beach state university accounting 300a 21a introduction to inventories

TRANSCRIPT

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 1 ACCOUNTING FOR INVENTORIES I. Key Concepts and Terms:

A. The Matching Principle posits that the costs incurred to generate revenues should be charges against revenues (expensed) in the period in which the goods or services acquired by those costs contribute to the revenue production process.

--In a merchandising (retail) firm emphasis is placed on matching the costs of goods sold with the revenue generated by the sales of these goods.

--In a manufacturing firm the emphasis shifts to computing the value of the various inventories being produced and comparing the value of these inventories, in various states of completion, against the revenues generated from selling finished goods.

1. The sequence of events in a sale is as follows:

a. A purchase requisition is initiated by individual department heads of the purchasing firm when quantities of the item fall below a predetermined amount or upon authorization from department heads or other authorized personnel;

b. The purchasing department prepares a purchase order after determining the best source of the product based on price, availability and quality of competing sources;

c. Upon receipt of the purchase order, the selling company prepares an invoice defining the terms of the transaction and authorizing terms of the shipment to the purchasing firm. This one invoice is called a sales invoice by the selling firm and a purchase invoice by the purchasing firm. Note the difference between the purchase order (step b) and the purchase invoice (step c);

d. Upon receipt of the goods, the purchasing firm creates a receiving report detailing the date, type and quantity of goods received. This receiving report is checked against a copy of the purchase order to insure that the goods received were in fact ordered and that they are the correct goods;

e. The accounts payable department compares copies of the receiving report, purchase order and purchase invoice to insure that the goods received were ordered, that the proper quantity was received etc.

2. Accounting for Inventories in a merchandising operation

a. Although inventory may be purchased for cash or on credit, the vast majority of sales are "on account" (for credit). The time period for which credit is granted is called the credit period. In order to encourage the prompt payment of invoiced, most firms offer cash/sales discounts if the invoices are paid within the discount period. A typical sales invoice might describe credit terms such as 2/10,n/30. This is interpreted as follows:

The terms cash, sales or purchase discounts are synonymous. Purchasing firms usually refer to such discounts as cash or purchase discounts and selling firms often refer to them as cash or sales discounts. However, the terms are often used interchangeably by both selling and purchasing firms.

2/10: the purchaser may deduct 2% of the invoice price if the bill is paid within ten days of the invoice date. For example, if the invoice is for $1,600 and is

dated is September 1, the purchasing firm may deduct $32 if paid by September 11. The 2 represents the cash discount available and the 10 represents the discount period.

n/30: if the purchaser does not pay in the discount period the net amount is due in 30 days. Note that the credit period is 30 days and the discount period is

ten days.

It pays to take advantage of these cash discounts. Assuming that a year is @ 360 days and extra time gained by not taking the discount is only 20 days, the annualized cost of forgoing a 2% cash discount is 36% computed as follows: 360/20 (.02).

b. In addition to cash discounts, firms in a given industry also receive trade discounts. Trade discounts are reductions of the retail price offered to members of the industry. These trade discounts are often referred to as wholesale prices.

c. Net and gross methods of recording purchases/sales of inventory:

1. The theoretically correct cost of inventory is its net cost (cost net of all cash discounts available). Measuring inventory cost net of cash discounts is known as the net method. The net cost represents the cash equivalent price of inventory and the amount of the discount lost represents a financing cost imposed for failure to pay within the discount period.

2. In practice, many companies record inventories at gross amounts. Measuring inventories at the gross amount is known as the gross method. If the gross method is used the balance in purchase discounts account must be deducted from the purchases account to correctly measure the cost of goods sold. The gross method is considered theoretically unsound for three reasons:

a. it violates the matching principle by recording discounts when the payment is received rather than when the sale was made;

b. it fails to differentiate discounts taken between goods on hand and goods sold which results in an understatement of cost of goods sold and an overstatement of net income and ending inventory; c. it identifies companies taking the discount as opposed to those not taking it. As pointed out above, it is very expensive (36% per annum on a 2/10,n/30 discount scheme) not to take advantage of cash discounts. Firms failing to take these discounts are either poorly managed or experiencing cash flow or credit problems. Such firms should be identified. Using the net method solves this problem by identifying those firms

3. Net and gross methods illustrated: Assume Dallas Inc. purchases $1,000 merchandise form LYC Inc on 9/1/x1 terms 2/10,n/30. Dallas uses a periodic inventory system.

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 2 Books of Dallas Inc.

Transaction

Gross Method

Net Method

9/1/x1 Purchase $1,000 Inventory on account, terms 2/10,n/30

Purchases...................1,000 Accounts Payable......... 1,000

Purchases................... 980 Accounts Payable......... 980

Dallas pays within the discount period (pays on or before 9/11/x1)

Accounts Payable............1,000 Purchase Discounts....... 20 Cash..................... 980

Accounts Payable............ 980 Cash..................... 980

Dallas pays after the discount period (pays after 9/11/x1)

Accounts payable............1,000 Cash...................... 1,000

Accounts payable............ 980 Purchase discounts lost*. 20 cash..................... 980 * could also be called interest expense

3. The matching principle as applied to a merchandising firm is largely concerned with the accurate valuation of net income after adjustments of the following items:

a. Sales Revenues: revenues must be adjusted for returns and allowances and sales (cash) discounts. This process along with appropriate journal entries is illustrated below:

Sales: (Sales represent the gross (unadjusted) amount of merchandise sold, measured in dollars)

Accounts receivable (or cash)..............xxxx Sales.............................. xxxx

Note: This represents Gross Sales; this amount will be adjusted by the entries that follow to arrive at net sales

Less: Sales returns and allowances: (An adjustment to reflect returned or damaged merchandise)

Sales returns and allowances...............xxxx Accounts receivable (or cash)...... xxxx

Less: Sales (Cash) discounts: (An adjustment to reflect the discount for cash received within a specified time period) Sales (or Cash) discounts.................. xxxx Accounts receivable*............... xxxx (*assumes the gross method of recording)

b. Cost of Goods Sold: the values of beginning and ending inventory must be computed; purchases must be adjusted to reflect purchase returns and allowances, trade discounts and certain transportation costs (transportation in).

Beginning Inventory: (The value of last periods ending inventory as determined by a physical inventory) Add: Purchases: (The gross (unadjusted) cost of goods purchased in the present period) Purchases..................................xxxx Accounts Payable (or Cash)......... xxxx Less: Purchases returns and allowances: (Adjustments for purchases returned or allowances for damaged goods etc.) Accounts Payable...........................xxxx Purchases returns and allowances... xxxx Less: Purchase (Cash) discounts: (Reductions in purchase price for cash payment within a specified time period) Accounts payable...........................xxxx Purchase (Cash) discounts*......... xxxx (*assumes the gross method of recording) Add: Transportation In: (The cost associated with the transportation of goods shipped FOB Shipping Point) Transportation In..........................xxxx Cash (or Accounts Payable)......... xxxx

NOTE: Transportation-In is an "Inventoriable cost"; i.e. it is added to the cost of inventory and is not charged against income until the inventory is sold. We must differentiate between Transportation In and Transportation Out. Transportation-Out (Delivery Expense) is a "period cost"; i.e. it is charged against income in the period in which it is incurred. Transportation out is part of selling and administrative expenses and has no affect on the value of inventories. The affects of these differences are illustrated on the income statement which follows.

c. Accounting for Inventory in transit: Inventory is transported on common carriers (trucking companies, railroad, UPS etc) which because of interstate commerce laws, never assume title of the goods being shipped. Title to inventory in transit is determined by the terms of the purchase or sales invoice.

1. FOB shipping point: goods shipped FOB (free on board) shipping point are included in the inventory of the purchaser as soon as they are loaded on the common carrier. 2. FOB destination: goods shipped FOB destination are carried in the inventory of the seller until delivered.

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 3 ILLUSTRATIVE EXAMPLE OF A MULTIPLE-STEP INCOME STATEMENT WITH BEGINNING AND ENDING INVENTORIES: These adjustments are reflected in the computation of Gross Profit in the comprehensive Income Statement illustrated below: Sales............................................................. $102,000 Less: Sales returns and allowances.......... $ 5,000 Sales discounts....................... 1,000 6,000 Net Sales......................................................... $ 96,000 (100%) Cost of Goods Sold: Beginning Inventory.......................... $ 78,000 Add: Purchases......................... $ 63,000 Transportation In................. 1,000 (Note: Transportation In is part of COGS) Less: Purchase Returns and allowances... (2,000) Purchases discounts............... (700) Net Purchases........................... 61,300 Cost of goods available for sale............. $139,300 Less: Ending Inventory....................... (75,300) Cost of Goods Sold...................................... 64,000 (.677) ratio of COS/Sales Gross Profit on Sales............................................. $ 32,000 (.333) ratio of GP/Sales Operating expenses: Selling expenses: Sales salaries.......................... $ 700 Transportation Out (FOB Destination).... 100 (Note: Transportation out is part of Operating Expenses) Advertising............................. 500 $ 1,300 General and administrative expenses: Office salaries......................... $ 2,500 Utilities............................... 1,200 3,700 Total operating expenses................ 5,000 Income before tax................................................. $ 27,000 Less: Provision for income taxes.................................. 10,800 Income from Continuing Operations................................. $ 16,200

• Note that columns begin with $ Signs;

• Totals amounts of sub-categories also have $ signs

Discontinued operations: Loss from operations of business segment, net of applicable income tax savings........ $ (1,200) Gain on disposal of business segment, net of applicable income tax expense........ 800 (400) Income before Extraordinary Item and cumulative effect of change in accounting principle......... $ 15,800 Extraordinary Item: gain on forced sale of assets to federal government net of tax effect.......... $ 2,300 Cumulative effect of change in accounting method, net of applicable income tax effect ............. (1,200) 1,100 Net income ...................................................... $ 14,700

NOTE: The presentation above assumes the use of the periodic inventory system. The differences between the periodic and perpetual inventory systems are discussed in

part C below.

NOTE: Explanations of Discontinued operations, Extraordinary Items and Changes in Accounting Methods are presented in part F below.

B. Gross Profit (often called gross margin) is the difference between revenues and the cost of goods sold. It has many useful purposes:

1. It reflects the revenues available to cover of the operating expenses of the business and produce net income. a. operating expenses are those expenses that can be directly traced to selling activities (such as advertising) and general and administrative activities (such as accounting, janitorial etc).

2. It highlights the relationship (ratio) between total revenues and gross profit. This ratio is an important indicator of the performance of the business.

C. Inventory represents goods held for resale and may be accounted for using either the Periodic or Perpetual inventory system.

1. Periodic Inventory System: Inventory quantities are not maintained on a constant basis. In order to establish the quantity (as opposed to the value) of ending inventory, a physical count is made at the end of the accounting period.

a. advantages of periodic inventory systems: 1. requires no special hardware;

2. appropriate for items of low unit cost and high turnover

b. disadvantages of periodic inventory systems:

1. no identification of inventory costs of theft, spoilage or related losses;

a. the valuation of ending inventory (physical quantity on hand times value per unit) is subtracted from the cost of goods available for sale, cost of goods sold is a "residual" amount that is not computed directly.

2. requires a complete physical count to reasonably determine quantities on hand at the end of the period.

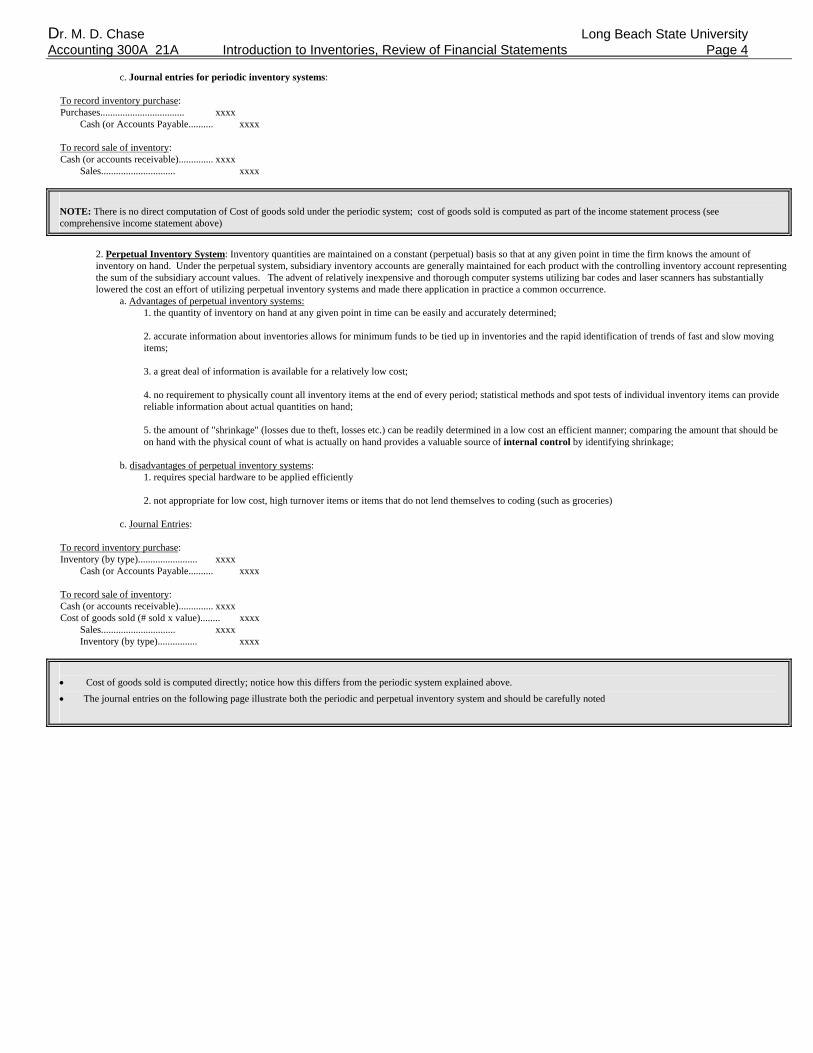

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 4

c. Journal entries for periodic inventory systems: To record inventory purchase: Purchases.................................. xxxx Cash (or Accounts Payable.......... xxxx To record sale of inventory: Cash (or accounts receivable).............. xxxx Sales.............................. xxxx

NOTE: There is no direct computation of Cost of goods sold under the periodic system; cost of goods sold is computed as part of the income statement process (see comprehensive income statement above)

2. Perpetual Inventory System: Inventory quantities are maintained on a constant (perpetual) basis so that at any given point in time the firm knows the amount of inventory on hand. Under the perpetual system, subsidiary inventory accounts are generally maintained for each product with the controlling inventory account representing the sum of the subsidiary account values. The advent of relatively inexpensive and thorough computer systems utilizing bar codes and laser scanners has substantially lowered the cost an effort of utilizing perpetual inventory systems and made there application in practice a common occurrence.

a. Advantages of perpetual inventory systems: 1. the quantity of inventory on hand at any given point in time can be easily and accurately determined;

2. accurate information about inventories allows for minimum funds to be tied up in inventories and the rapid identification of trends of fast and slow moving items;

3. a great deal of information is available for a relatively low cost;

4. no requirement to physically count all inventory items at the end of every period; statistical methods and spot tests of individual inventory items can provide reliable information about actual quantities on hand;

5. the amount of "shrinkage" (losses due to theft, losses etc.) can be readily determined in a low cost an efficient manner; comparing the amount that should be on hand with the physical count of what is actually on hand provides a valuable source of internal control by identifying shrinkage;

b. disadvantages of perpetual inventory systems:

1. requires special hardware to be applied efficiently

2. not appropriate for low cost, high turnover items or items that do not lend themselves to coding (such as groceries)

c. Journal Entries: To record inventory purchase: Inventory (by type)........................ xxxx Cash (or Accounts Payable.......... xxxx To record sale of inventory: Cash (or accounts receivable).............. xxxx Cost of goods sold (# sold x value)........ xxxx Sales.............................. xxxx Inventory (by type)................ xxxx

• Cost of goods sold is computed directly; notice how this differs from the periodic system explained above. • The journal entries on the following page illustrate both the periodic and perpetual inventory system and should be carefully noted

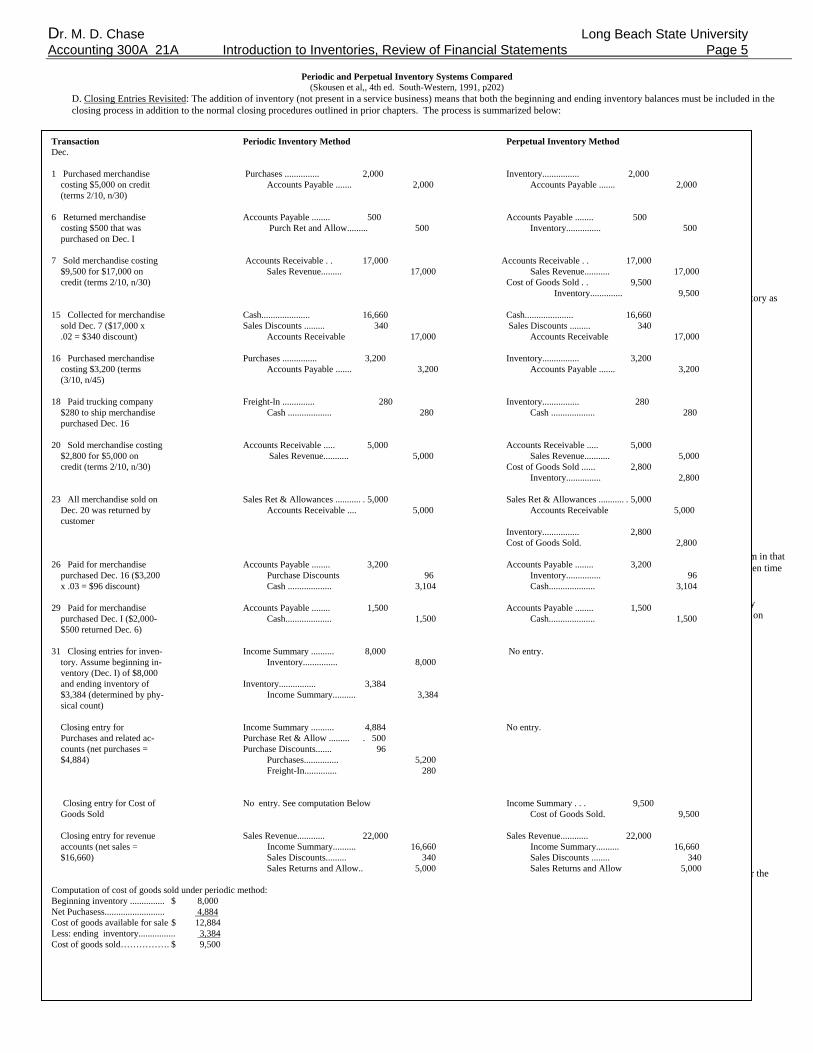

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 5 Periodic and Perpetual Inventory Systems Compared (Skousen et al,, 4th ed. South-Western, 1991, p202)

D. Closing Entries Revisited: The addition of inventory (not present in a service business) means that both the beginning and ending inventory balances must be included in the closing process in addition to the normal closing procedures outlined in prior chapters. The process is summarized below:

1. Credit balance nominal accounts (revenues and contra-expenses) are closed to income summary:

All credit balance nominal accounts............ xxxx Income summary............................. xxxx

2. Debit balance nominal accounts (expenses and contra-revenues) are closed to income summary: Income summary...................................... xxxx All debit balance nominal accounts......... xxxx

3. Ending inventory is booked (recorded in the ledger) as a current asset and income summary is credited a like amount; Inventory (end of period value)..................... xxxx Income summary............................. xxxx

4. Beginning Inventory is eliminated (the value of beginning inventory is not relevant; the inventory on hand at the end of the period is represented by ending inventory as booked in step three above);

Income summary...................................... xxxx Inventory (beginning of period value)...... xxxx

5. The balance in the Income Summary is closed to Retained Earnings; Income summary...................................... xxxx Retained earnings.......................... xxxx

6. Dividends declared and any prior period adjustments (net of tax effects) are closed to retained earnings; Retained earnings................................... xxxx Prior period adjustment (net of tax)................ xxxx1 Dividends.................................. xxxx Prior period adjustment (net of tax)....... xxxx2

1 If the prior period adjustment reflects a loss (debit) 2 If the prior period adjustment reflects a gain (credit)

E. Special Issues Involving Inventory

1. Shrinkage: Shrinkage represents the loss of inventory due to theft or other unaccountable reasons. In a periodic inventory system, shrinkage may cause a problem in that inventory will be overstated on the books until the physical inventory is taken. A perpetual system helps reveal shrinkage problems much sooner because at any given time the book inventory can be quickly verified against physical inventory in a spot check.

2. Consignments: Inventory on consignment remains the property of the consignor and is carried on the consignors books. The consignee has usally has no liability (contingent or otherwise) unless so specified in the consignment agreeemnt. The consignor is usually entitled to the return of the merchandise at a specified time or on demand.

F. Classification of the Accounts on the Financial Statements: In order the make the financial statements more meaningful and to facilitate the use of financial statement information for analytical purposes, the accounts of the financial statement are usually classified (categorized) as follows:

1. Balance Sheet Classifications: Classified Balance Sheets make the distinction between current, noncurrent and other. a. Assets:

1. Current assets: cash and other assets which are reasonably expected to be converted to cash, sold or consumed within one year or the operating cycle, whichever is longer.) Examples:

a. cash b. short-term investments (expect to convert to cash in less than one year) c. receivables d. inventory e. prepaid expenses

2. Noncurrent assets: assets that do not qualify as current assets Examples:

a. Long-term investments b. Property, plant and equipment c. Intangibles (patents, copyrights, trademarks, franchise licenses, goodwill, etc) d. Other

b. Liabilities: 1. Current liabilities: obligations that must be settled within one year or the operating cycle, whichever is longer; will require the use of current assets or the creation of new current liabilities to satisfy Examples:

a. accounts payable b. short-term notes payable c. the current portion of any long-term debt d. prepayments received from customers/clients

2. Long-term liabilities obligations that do not meet the definition of short-term liabilities; Examples:

a. bonds payable b. long-term debt

Transaction Periodic Inventory Method Perpetual Inventory Method Dec. 1 Purchased merchandise Purchases ............... 2,000 Inventory................ 2,000 costing $5,000 on credit Accounts Payable ....... 2,000 Accounts Payable ....... 2,000 (terms 2/10, n/30) 6 Returned merchandise Accounts Payable ........ 500 Accounts Payable ........ 500 costing $500 that was Purch Ret and Allow......... 500 Inventory............... 500 purchased on Dec. I 7 Sold merchandise costing Accounts Receivable . . 17,000 Accounts Receivable . . 17,000 $9,500 for $17,000 on Sales Revenue......... 17,000 Sales Revenue........... 17,000 credit (terms 2/10, n/30) Cost of Goods Sold . . 9,500 Inventory.............. 9,500 15 Collected for merchandise Cash..................... 16,660 Cash..................... 16,660 sold Dec. 7 ($17,000 x Sales Discounts ......... 340 Sales Discounts ......... 340 .02 = $340 discount) Accounts Receivable 17,000 Accounts Receivable 17,000 16 Purchased merchandise Purchases ............... 3,200 Inventory................ 3,200 costing $3,200 (terms Accounts Payable ....... 3,200 Accounts Payable ....... 3,200 (3/10, n/45) 18 Paid trucking company Freight-ln .............. 280 Inventory................ 280 $280 to ship merchandise Cash ................... 280 Cash ................... 280 purchased Dec. 16 20 Sold merchandise costing Accounts Receivable ..... 5,000 Accounts Receivable ..... 5,000 $2,800 for $5,000 on Sales Revenue........... 5,000 Sales Revenue........... 5,000 credit (terms 2/10, n/30) Cost of Goods Sold ...... 2,800 Inventory............... 2,800 23 All merchandise sold on Sales Ret & Allowances ........... . 5,000 Sales Ret & Allowances ........... . 5,000 Dec. 20 was returned by Accounts Receivable .... 5,000 Accounts Receivable 5,000 customer Inventory................ 2,800 Cost of Goods Sold. 2,800 26 Paid for merchandise Accounts Payable ........ 3,200 Accounts Payable ........ 3,200 purchased Dec. 16 ($3,200 Purchase Discounts 96 Inventory............... 96 x .03 = $96 discount) Cash ................... 3,104 Cash.................... 3,104 29 Paid for merchandise Accounts Payable ........ 1,500 Accounts Payable ........ 1,500 purchased Dec. I ($2,000- Cash.................... 1,500 Cash.................... 1,500 $500 returned Dec. 6) 31 Closing entries for inven- Income Summary .......... 8,000 No entry. tory. Assume beginning in- Inventory............... 8,000 ventory (Dec. I) of $8,000 and ending inventory of Inventory................ 3,384 $3,384 (determined by phy- Income Summary.......... 3,384 sical count) Closing entry for Income Summary .......... 4,884 No entry. Purchases and related ac- Purchase Ret & Allow ......... . 500 counts (net purchases = Purchase Discounts....... 96 $4,884) Purchases............... 5,200 Freight-In.............. 280 Closing entry for Cost of No entry. See computation Below Income Summary . . . 9,500 Goods Sold Cost of Goods Sold. 9,500 Closing entry for revenue Sales Revenue............ 22,000 Sales Revenue............ 22,000 accounts (net sales = Income Summary.......... 16,660 Income Summary.......... 16,660 $16,660) Sales Discounts......... 340 Sales Discounts ........ 340 Sales Returns and Allow.. 5,000 Sales Returns and Allow 5,000 Computation of cost of goods sold under periodic method: Beginning inventory ............... $ 8,000 Net Puchasess.......................... 4,884 Cost of goods available for sale $ 12,884 Less: ending inventory................ 3,384 Cost of goods sold……………. $ 9,500

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 6

c. Owners Equity:

1. Paid-in capital: amounts stockholders have paid into the company in exchange for the capital stock of the company; Paid-in capital consists of two components: Capital Stock and Paid-in Capital in excess of par.

Note the difference between Paid-in Capital and Paid-in Capital in Excess of Par:

Paid-in Capital: The total of capital stock and paid-in capital in excess of par Paid-in Capital in Excess of Par: The excess of the price received for the capital stock over the par or stated value of the stock. These differences will be discussed again in AP-35A.

a. Capital stock

1. Preferred Stock: capital stock that receives preference over common stockholders in terms of dividends from earnings and distributions in the event of the dissolution of the firm; this preference is usually attained in return for preferred stockholders giving up their voting rights. Valuation: Number of shares issued and outstanding times par value of the preferred stock. 2. Common Stock: capital stock that gives the stockholder voting rights and a "residual" interest in profits and assets in the event of the dissolution of the firm. Valuation: Number of shares outstanding times the par value of the common stock

b. Paid-in Capital in Excess of Par: the excess of cash received for capital stock over and above the par value of the stock. Valuation: The excess of the issue price of the stock less par value times the number of shares issued. For example: if the stock (preferred or common) has a par value of $10 per share and is issued for $13.50 per share, $3.50 ($13.50-$10.00) of paid-in capital in excess of par is created on a per share basis. Therefore if 1000 shares are issued, Paid-in capital in excess of par would be $3,500 ($3.50 x 1000).

2. Retained earnings: The cumulative net income of the company from its inception to the balance sheet date less cumulative dividends, prior period adjustments and quasi-reorganizations. Refer to the statement of retained earnings.

2. Income Statement Classifications:

a. Income statements are usually classified as single step or multiple step. 1. Single-step income statements are greatly condensed such that all revenues and expenses are shown as single numbers (one revenu number and one expense number). Thise types of statements are usually restricted to situations in which preenting a broad picture (without detail) is all that is required. A typical single-step incoe statement is presented below:

Revenue: Sales..................................... $ 40,000 Other..................................... 5,000 $ 45,000 Expenses: Cost of Sales............................ $ 10,000 Selling Expenses......................... 2,000 Administrative Expenses.................. 4,000 Tax Expense.............................. 3,000 19,000 Net Income................................. $ 26,000

2. Multiple-step income statememts derive there name from the steps required to arrive at the specific totals included in the statement. See comprehensive income statement illustrated on page 3 above.

G. Working Capital: Working capital is the excess of current assets over current liabilities and is an important indicator of short-term solvency. Solvency is a measure of a firms ability to meet their debts as they becom due. Because of the relative importance (in terms of total dollar amount) of inventory, it has a significant effect on working capital. Analyst examine working capital as one means of evaluating the viability of one company in comparison to others.

1. Current Ratio: the current ration is the ratio of current assets/current liabilities. Like working capital, it is an indicator of a firms short-term solvency. A current ratio should normally fall between 2 and 2.5 to 1.

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 7 II. SUMMARY OF KEY ISSUES IN REPORTING THE RESULTS OF OPERATIONS FOR MERCHANDISING OPERATIONS

--In a merchandising business, the main source of revenue is from sales of inventory as opposed to the service revenues used for service firms. Sales represent the amounts customers pay or promise to pay for products (inventory) they received from the company.

--When using a periodic inventory system the ending inventory is subtracted from goods available for sale to derive cost of goods sold.

--When using a perpetual inventory system the cost of goods sold is computed directly by multiplying the number of units sold by the cost of the inventory. This is possible because perpetual systems keep a constant record of the amount of inventory on hand by recording its increases and decreases directly into the inventory account. This ability to maintain a constant count of inventory on hand on a per item basis is a very valuable tool form management.

--Under the periodic inventory system, a physical count of merchandise on hand is required for all inventory at the end of each accounting period to determine the ending inventory value, which, for accounting purposes, is only available after a physical count has been made.

--Under the perpetual inventory system, a physical count of merchandise on hand is made to corroborate the count maintained in the accounting records. The physical count may be applied to inventory on a categorical basis using statistical techniques, thereby avoiding counts of the entire inventory. The ability to compare the accounting records of inventory quantity with a physical count provides internal control by highlighting the shrinkage of inventory items from loss, theft and other causes.

--Sometimes customers return goods or are granted special allowances that are set up in a separate contra-account called Sales Returns and Allowances. This account is deducted from the gross sales of the company to give the company's net sales.

--Sometimes a customer is given a sales discount if his/her account is paid within a specified period. The Sales (Cash) Discounts account is also subtracted from gross sales to arrive at the company's net sales.

--Purchases represent the cost of merchandise acquired by the company for resale to its customers.

--Sometimes the company returns merchandise to its suppliers or receives allowances from its suppliers. These amounts are credited to a Purchases Returns and Allowances account and are subtracted from gross purchases to arrive at net purchases. In addition, suppliers sometimes grant discounts for prompt payment. These price reductions are credited to a Purchases Discounts account and are subtracted from gross purchases to arrive at net purchases for the accounting period.

--In addition to the cost of a purchase, a business normally incurs additional related costs, such as freight-in costs. These costs are usually segregated in an account called Transportation In. Transportation in is an inventoriable cost because it is added to the cost of inventory and becomes part of cost of goods sold. Transportation out is a period cost and does not effect the cost of goods sold or the gross profit of the firm. Transportation out is part of selling and administrative expenses and is deducted from gross profit (gross margin) to compute net income from continuing operations.

--A classified balance sheet enables the users of these statements to easily interpret the data it contains by classifying the assets liabilities as current or non-current and classifying the stockholders' equity accounts separately from the assets and liabilities.

--A multiple-step income statement shows important sub-totals, i.e., net purchases, gross profit, operating expenses, and extraordinary items.

--A statement of retained earnings depicts the changes in this account, i.e., net income (loss) for the period and prior period adjustments.

--The use of ratio analysis may be helpful in the evaluation of the entity by both internal and external users of financial statements (refer to chapter on financial statement analysis for more detail in this area).

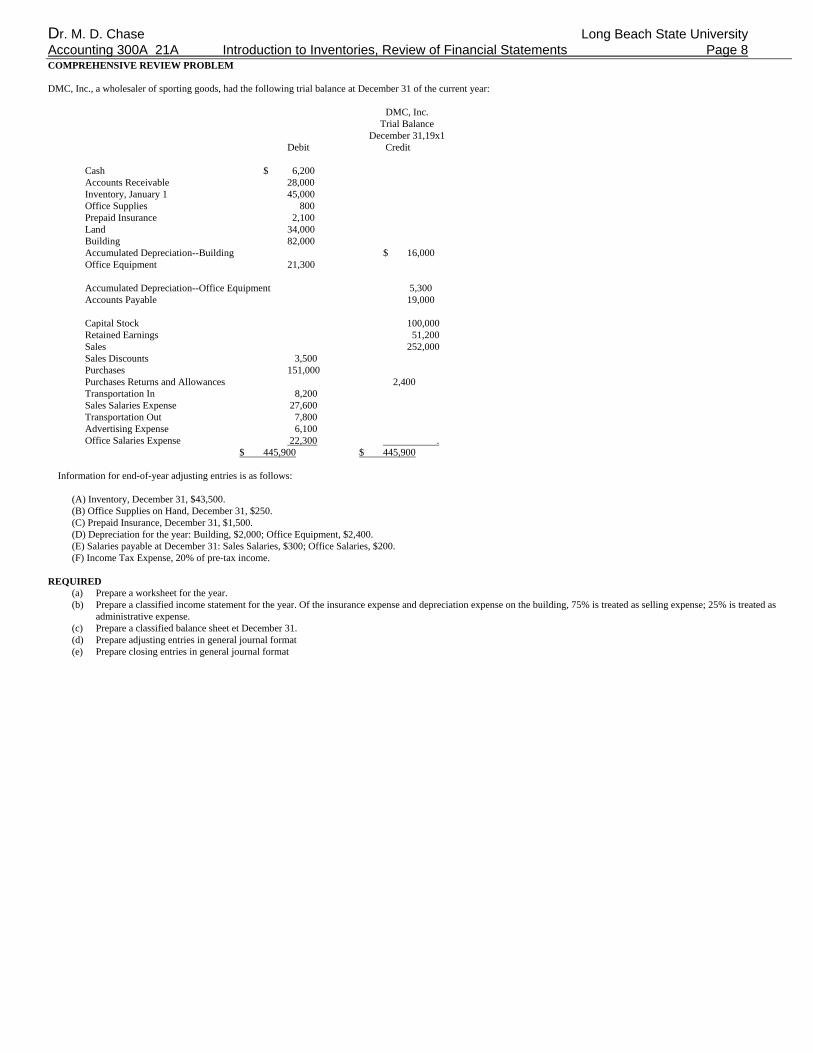

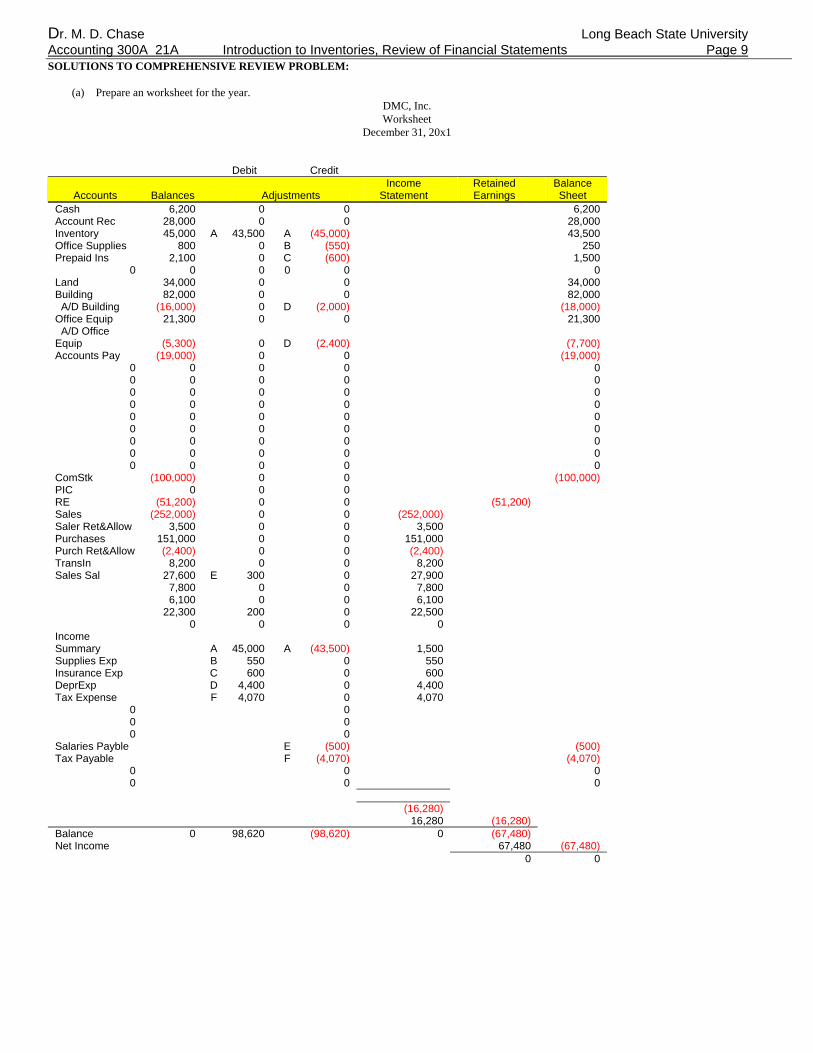

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 8 COMPREHENSIVE REVIEW PROBLEM DMC, Inc., a wholesaler of sporting goods, had the following trial balance at December 31 of the current year: DMC, Inc. Trial Balance December 31,19x1 Debit Credit Cash $ 6,200 Accounts Receivable 28,000 Inventory, January 1 45,000 Office Supplies 800 Prepaid Insurance 2,100 Land 34,000 Building 82,000 Accumulated Depreciation--Building $ 16,000 Office Equipment 21,300 Accumulated Depreciation--Office Equipment 5,300 Accounts Payable 19,000 Capital Stock 100,000 Retained Earnings 51,200 Sales 252,000 Sales Discounts 3,500 Purchases 151,000 Purchases Returns and Allowances 2,400 Transportation In 8,200 Sales Salaries Expense 27,600 Transportation Out 7,800 Advertising Expense 6,100 Office Salaries Expense 22,300 . $ 445,900 $ 445,900 Information for end-of-year adjusting entries is as follows:

(A) Inventory, December 31, $43,500. (B) Office Supplies on Hand, December 31, $250. (C) Prepaid Insurance, December 31, $1,500. (D) Depreciation for the year: Building, $2,000; Office Equipment, $2,400. (E) Salaries payable at December 31: Sales Salaries, $300; Office Salaries, $200. (F) Income Tax Expense, 20% of pre-tax income.

REQUIRED

(a) Prepare a worksheet for the year. (b) Prepare a classified income statement for the year. Of the insurance expense and depreciation expense on the building, 75% is treated as selling expense; 25% is treated as

administrative expense. (c) Prepare a classified balance sheet et December 31. (d) Prepare adjusting entries in general journal format (e) Prepare closing entries in general journal format

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 9 SOLUTIONS TO COMPREHENSIVE REVIEW PROBLEM:

(a) Prepare an worksheet for the year. DMC, Inc. Worksheet December 31, 20x1

Debit Credit

Accounts Balances Adjustments Income

Statement Retained Earnings

Balance Sheet

Cash 6,200 0 0 6,200 Account Rec 28,000 0 0 28,000 Inventory 45,000 A 43,500 A (45,000) 43,500 Office Supplies 800 0 B (550) 250 Prepaid Ins 2,100 0 C (600) 1,500

0 0 0 0 0 0 Land 34,000 0 0 34,000 Building 82,000 0 0 82,000 A/D Building (16,000) 0 D (2,000) (18,000) Office Equip 21,300 0 0 21,300 A/D Office Equip (5,300) 0 D (2,400) (7,700) Accounts Pay (19,000) 0 0 (19,000)

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

ComStk (100,000) 0 0 (100,000) PIC 0 0 0 RE (51,200) 0 0 (51,200) Sales (252,000) 0 0 (252,000) Saler Ret&Allow 3,500 0 0 3,500 Purchases 151,000 0 0 151,000 Purch Ret&Allow (2,400) 0 0 (2,400) TransIn 8,200 0 0 8,200 Sales Sal 27,600 E 300 0 27,900 7,800 0 0 7,800 6,100 0 0 6,100 22,300 200 0 22,500 0 0 0 0 Income Summary A 45,000 A (43,500) 1,500 Supplies Exp B 550 0 550 Insurance Exp C 600 0 600 DeprExp D 4,400 0 4,400 Tax Expense F 4,070 0 4,070

0 0 0 0 0 0

Salaries Payble E (500) (500) Tax Payable F (4,070) (4,070)

0 0 0 0 0 0

(16,280) 16,280 (16,280) Balance 0 98,620 (98,620) 0 (67,480) Net Income 67,480 (67,480) 0 0

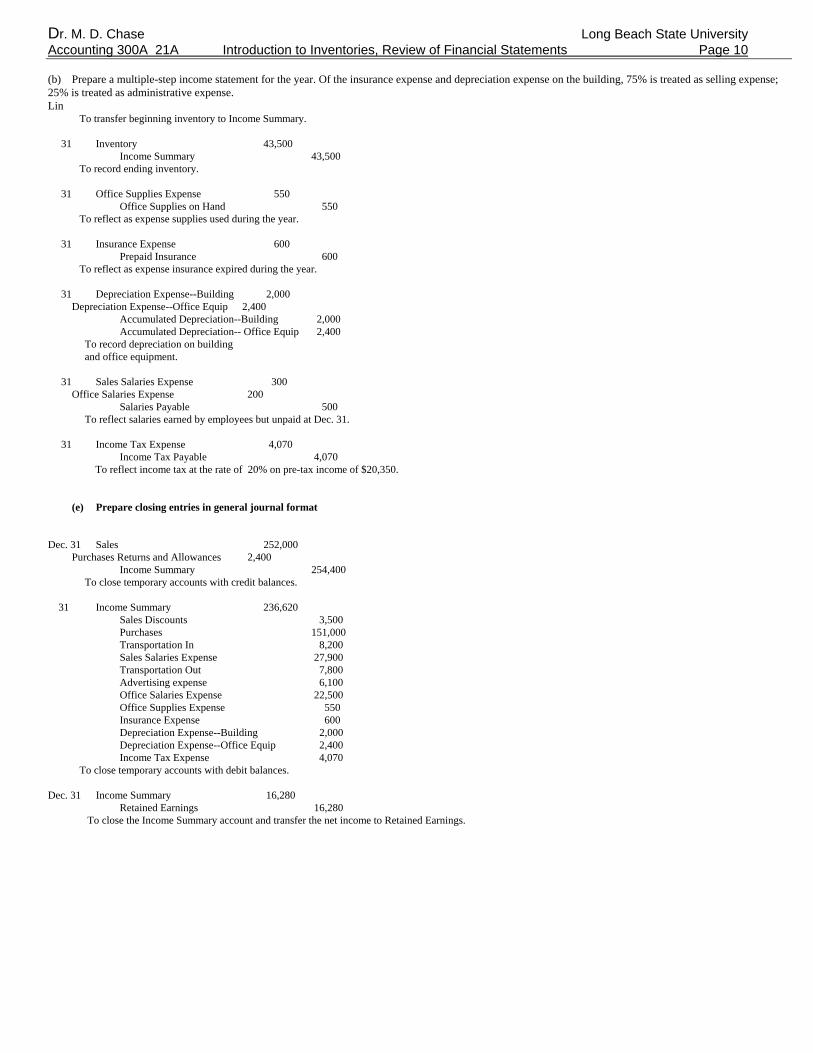

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 10 (b) Prepare a multiple-step income statement for the year. Of the insurance expense and depreciation expense on the building, 75% is treated as selling expense; 25% is treated as administrative expense. Lin To transfer beginning inventory to Income Summary. 31 Inventory 43,500 Income Summary 43,500 To record ending inventory. 31 Office Supplies Expense 550 Office Supplies on Hand 550 To reflect as expense supplies used during the year. 31 Insurance Expense 600 Prepaid Insurance 600 To reflect as expense insurance expired during the year. 31 Depreciation Expense--Building 2,000 Depreciation Expense--Office Equip 2,400 Accumulated Depreciation--Building 2,000 Accumulated Depreciation-- Office Equip 2,400 To record depreciation on building and office equipment. 31 Sales Salaries Expense 300 Office Salaries Expense 200 Salaries Payable 500 To reflect salaries earned by employees but unpaid at Dec. 31. 31 Income Tax Expense 4,070 Income Tax Payable 4,070 To reflect income tax at the rate of 20% on pre-tax income of $20,350.

(e) Prepare closing entries in general journal format Dec. 31 Sales 252,000 Purchases Returns and Allowances 2,400 Income Summary 254,400 To close temporary accounts with credit balances. 31 Income Summary 236,620 Sales Discounts 3,500 Purchases 151,000 Transportation In 8,200 Sales Salaries Expense 27,900 Transportation Out 7,800 Advertising expense 6,100 Office Salaries Expense 22,500 Office Supplies Expense 550 Insurance Expense 600 Depreciation Expense--Building 2,000 Depreciation Expense--Office Equip 2,400 Income Tax Expense 4,070 To close temporary accounts with debit balances. Dec. 31 Income Summary 16,280 Retained Earnings 16,280 To close the Income Summary account and transfer the net income to Retained Earnings.

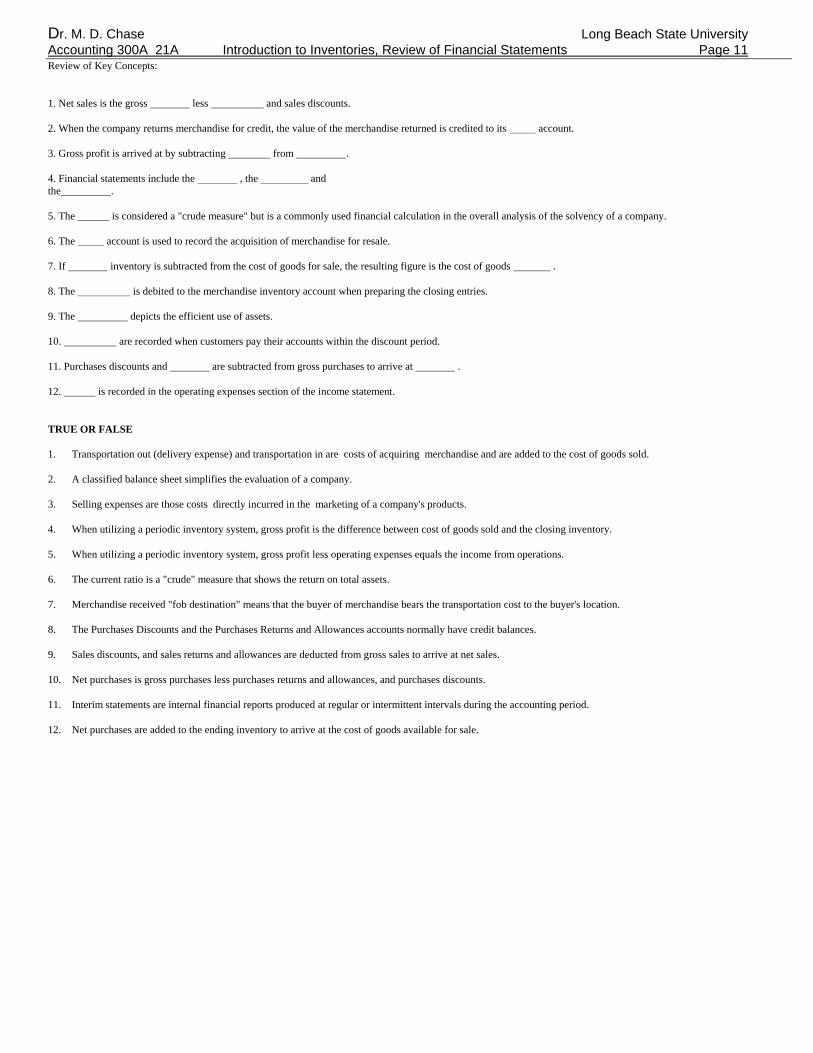

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 11 Review of Key Concepts: 1. Net sales is the gross less and sales discounts. 2. When the company returns merchandise for credit, the value of the merchandise returned is credited to its account. 3. Gross profit is arrived at by subtracting from . 4. Financial statements include the , the and the . 5. The is considered a "crude measure" but is a commonly used financial calculation in the overall analysis of the solvency of a company. 6. The account is used to record the acquisition of merchandise for resale. 7. If inventory is subtracted from the cost of goods for sale, the resulting figure is the cost of goods . 8. The is debited to the merchandise inventory account when preparing the closing entries. 9. The depicts the efficient use of assets. 10. are recorded when customers pay their accounts within the discount period. 11. Purchases discounts and are subtracted from gross purchases to arrive at . 12. is recorded in the operating expenses section of the income statement. TRUE OR FALSE 1. Transportation out (delivery expense) and transportation in are costs of acquiring merchandise and are added to the cost of goods sold. 2. A classified balance sheet simplifies the evaluation of a company. 3. Selling expenses are those costs directly incurred in the marketing of a company's products. 4. When utilizing a periodic inventory system, gross profit is the difference between cost of goods sold and the closing inventory. 5. When utilizing a periodic inventory system, gross profit less operating expenses equals the income from operations. 6. The current ratio is a "crude" measure that shows the return on total assets. 7. Merchandise received "fob destination" means that the buyer of merchandise bears the transportation cost to the buyer's location. 8. The Purchases Discounts and the Purchases Returns and Allowances accounts normally have credit balances. 9. Sales discounts, and sales returns and allowances are deducted from gross sales to arrive at net sales. 10. Net purchases is gross purchases less purchases returns and allowances, and purchases discounts. 11. Interim statements are internal financial reports produced at regular or intermittent intervals during the accounting period. 12. Net purchases are added to the ending inventory to arrive at the cost of goods available for sale.

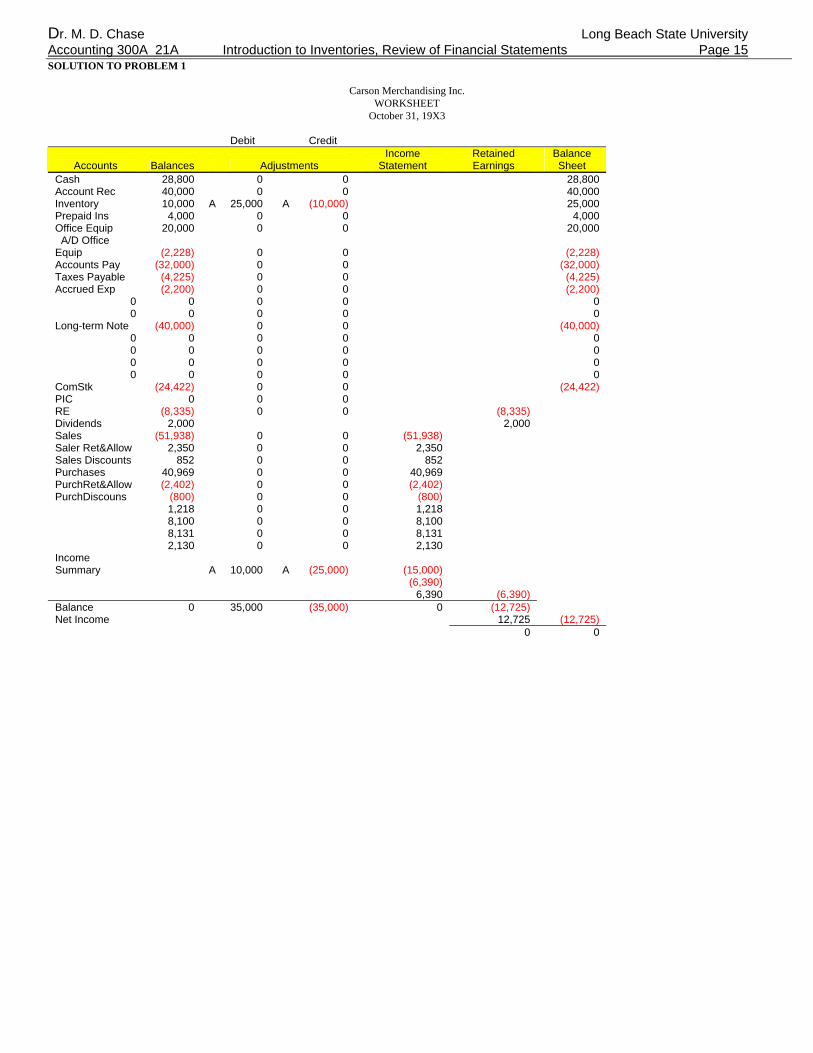

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 12 Problem 1 (Preparation of a worksheet for a merchandising firm) Following is the adjusted trial balance of the Carson Merchandising Inc. for its fiscal year ended October 31, 19X3. The ending inventory was determined to be $25,000. Carson Merchandising Inc. ADJUSTED TRIAL BALANCE October 31, 19X3 Account Title Debit Credit Cash $ 28,800 Accounts Receivable 40,000 Merchandise Inventory 10,000 Prepaid Insurance 4,000 Office Equipment 20,000 Accumulated Depreciation-Office Equipment $ 2,228 Accounts Payable 32,000 Income Taxes Payable 4,225 Accrued Expenses Payable 2,200 Long-Term Notes Payable 40,000 Common Stock 24,422 Retained Earnings 8,335 Dividends 2,000 Sales 51,938 Sales Returns and Allowances 2,350 Sales Discounts 852 Purchases 40,969 Purchases Returns and Allowances 2,402 Purchases Discounts 800 Transportation In 1,218 Selling Expenses 8,100 General and Administrative Expenses 8,131 Income Tax Expense 2,130 Totals $168,550 $168,550 Required: Enter Carson's adjusted trial balance for the year ended October 31, 20X3, on a worksheet and complete the worksheet.

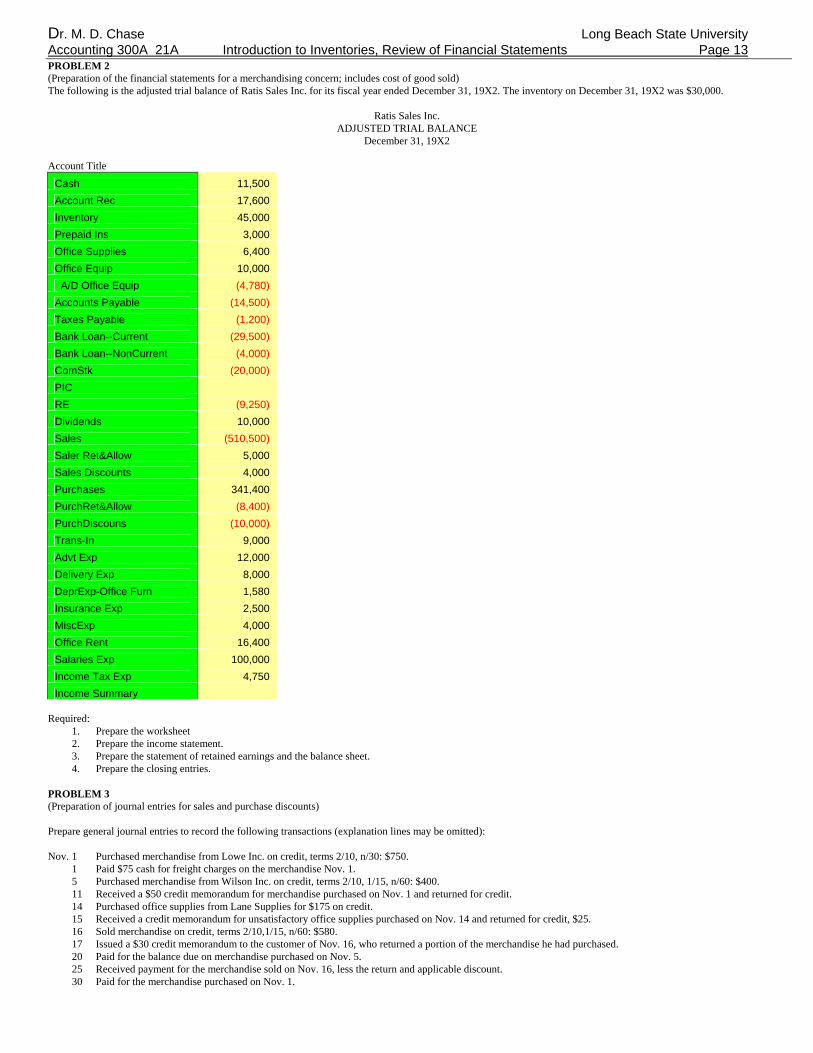

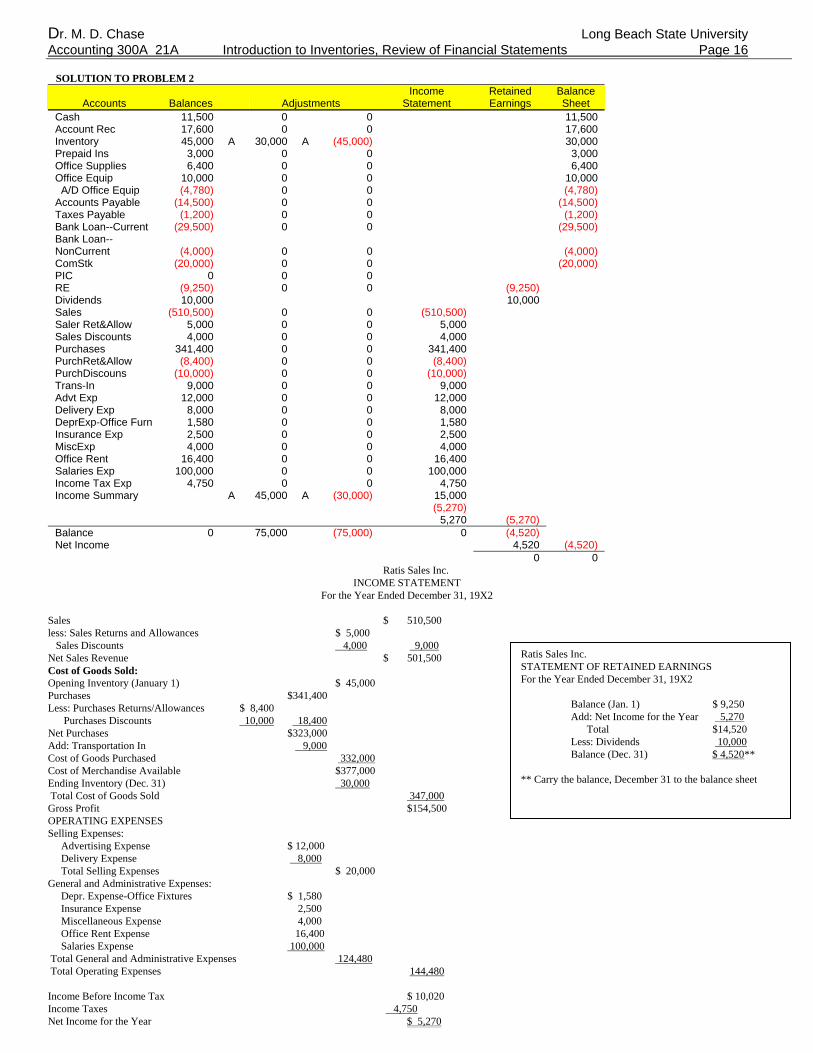

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 13 PROBLEM 2 (Preparation of the financial statements for a merchandising concern; includes cost of good sold) The following is the adjusted trial balance of Ratis Sales Inc. for its fiscal year ended December 31, 19X2. The inventory on December 31, 19X2 was $30,000. Ratis Sales Inc. ADJUSTED TRIAL BALANCE December 31, 19X2 Account Title

Cash 11,500 Account Rec 17,600 Inventory 45,000 Prepaid Ins 3,000 Office Supplies 6,400 Office Equip 10,000 A/D Office Equip (4,780) Accounts Payable (14,500) Taxes Payable (1,200) Bank Loan--Current (29,500) Bank Loan--NonCurrent (4,000) ComStk (20,000) PIC RE (9,250) Dividends 10,000 Sales (510,500) Saler Ret&Allow 5,000 Sales Discounts 4,000 Purchases 341,400 PurchRet&Allow (8,400) PurchDiscouns (10,000) Trans-In 9,000 Advt Exp 12,000 Delivery Exp 8,000 DeprExp-Office Furn 1,580 Insurance Exp 2,500 MiscExp 4,000 Office Rent 16,400 Salaries Exp 100,000 Income Tax Exp 4,750 Income Summary

Required:

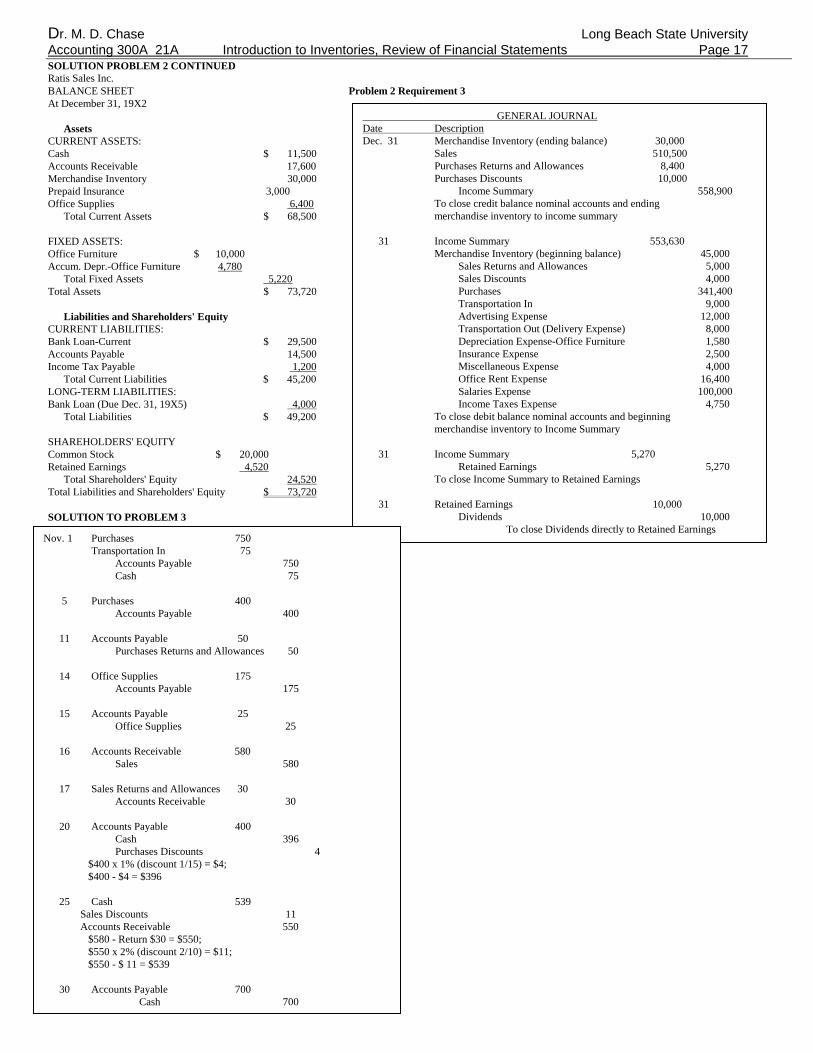

1. Prepare the worksheet 2. Prepare the income statement. 3. Prepare the statement of retained earnings and the balance sheet. 4. Prepare the closing entries.

PROBLEM 3 (Preparation of journal entries for sales and purchase discounts) Prepare general journal entries to record the following transactions (explanation lines may be omitted): Nov. 1 Purchased merchandise from Lowe Inc. on credit, terms 2/10, n/30: $750.

1 Paid $75 cash for freight charges on the merchandise Nov. 1. 5 Purchased merchandise from Wilson Inc. on credit, terms 2/10, 1/15, n/60: $400. 11 Received a $50 credit memorandum for merchandise purchased on Nov. 1 and returned for credit. 14 Purchased office supplies from Lane Supplies for $175 on credit. 15 Received a credit memorandum for unsatisfactory office supplies purchased on Nov. 14 and returned for credit, $25. 16 Sold merchandise on credit, terms 2/10,1/15, n/60: $580. 17 Issued a $30 credit memorandum to the customer of Nov. 16, who returned a portion of the merchandise he had purchased. 20 Paid for the balance due on merchandise purchased on Nov. 5. 25 Received payment for the merchandise sold on Nov. 16, less the return and applicable discount. 30 Paid for the merchandise purchased on Nov. 1.

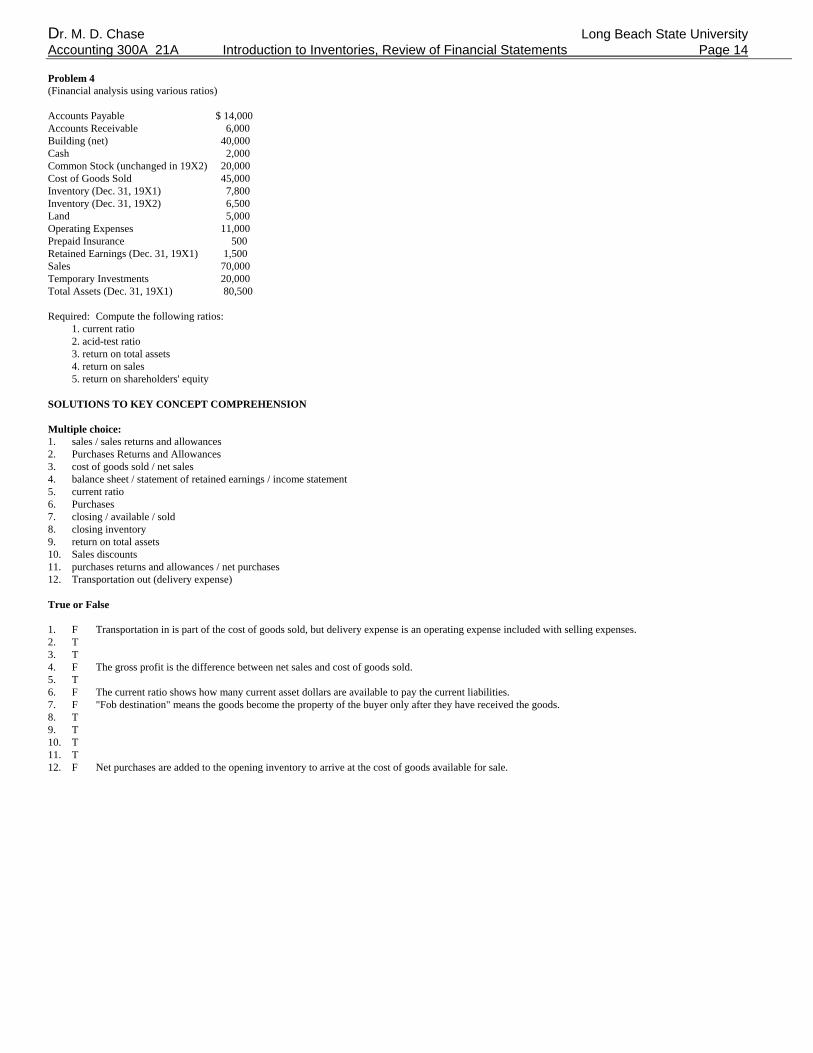

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 14 Problem 4 (Financial analysis using various ratios) Accounts Payable $ 14,000 Accounts Receivable 6,000 Building (net) 40,000 Cash 2,000 Common Stock (unchanged in 19X2) 20,000 Cost of Goods Sold 45,000 Inventory (Dec. 31, 19X1) 7,800 Inventory (Dec. 31, 19X2) 6,500 Land 5,000 Operating Expenses 11,000 Prepaid Insurance 500 Retained Earnings (Dec. 31, 19X1) 1,500 Sales 70,000 Temporary Investments 20,000 Total Assets (Dec. 31, 19X1) 80,500 Required: Compute the following ratios:

1. current ratio 2. acid-test ratio 3. return on total assets 4. return on sales 5. return on shareholders' equity

SOLUTIONS TO KEY CONCEPT COMPREHENSION Multiple choice: 1. sales / sales returns and allowances 2. Purchases Returns and Allowances 3. cost of goods sold / net sales 4. balance sheet / statement of retained earnings / income statement 5. current ratio 6. Purchases 7. closing / available / sold 8. closing inventory 9. return on total assets 10. Sales discounts 11. purchases returns and allowances / net purchases 12. Transportation out (delivery expense) True or False 1. F Transportation in is part of the cost of goods sold, but delivery expense is an operating expense included with selling expenses. 2. T 3. T 4. F The gross profit is the difference between net sales and cost of goods sold. 5. T 6. F The current ratio shows how many current asset dollars are available to pay the current liabilities. 7. F "Fob destination" means the goods become the property of the buyer only after they have received the goods. 8. T 9. T 10. T 11. T 12. F Net purchases are added to the opening inventory to arrive at the cost of goods available for sale.

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 15 SOLUTION TO PROBLEM 1 Carson Merchandising Inc. WORKSHEET October 31, 19X3

Debit Credit

Accounts Balances Adjustments Income

Statement Retained Earnings

Balance Sheet

Cash 28,800 0 0 28,800 Account Rec 40,000 0 0 40,000 Inventory 10,000 A 25,000 A (10,000) 25,000 Prepaid Ins 4,000 0 0 4,000 Office Equip 20,000 0 0 20,000 A/D Office Equip (2,228) 0 0 (2,228) Accounts Pay (32,000) 0 0 (32,000) Taxes Payable (4,225) 0 0 (4,225) Accrued Exp (2,200) 0 0 (2,200)

0 0 0 0 0 0 0 0 0 0

Long-term Note (40,000) 0 0 (40,000) 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

ComStk (24,422) 0 0 (24,422) PIC 0 0 0 RE (8,335) 0 0 (8,335) Dividends 2,000 2,000 Sales (51,938) 0 0 (51,938) Saler Ret&Allow 2,350 0 0 2,350 Sales Discounts 852 0 0 852 Purchases 40,969 0 0 40,969 PurchRet&Allow (2,402) 0 0 (2,402) PurchDiscouns (800) 0 0 (800) 1,218 0 0 1,218 8,100 0 0 8,100 8,131 0 0 8,131 2,130 0 0 2,130 Income Summary A 10,000 A (25,000) (15,000) (6,390) 6,390 (6,390) Balance 0 35,000 (35,000) 0 (12,725) Net Income 12,725 (12,725) 0 0

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 16 SOLUTION TO PROBLEM 2

Accounts Balances Adjustments Income

Statement Retained Earnings

Balance Sheet

Cash 11,500 0 0 11,500 Account Rec 17,600 0 0 17,600 Inventory 45,000 A 30,000 A (45,000) 30,000 Prepaid Ins 3,000 0 0 3,000 Office Supplies 6,400 0 0 6,400 Office Equip 10,000 0 0 10,000 A/D Office Equip (4,780) 0 0 (4,780) Accounts Payable (14,500) 0 0 (14,500) Taxes Payable (1,200) 0 0 (1,200) Bank Loan--Current (29,500) 0 0 (29,500) Bank Loan--NonCurrent (4,000) 0 0 (4,000) ComStk (20,000) 0 0 (20,000) PIC 0 0 0 RE (9,250) 0 0 (9,250) Dividends 10,000 10,000 Sales (510,500) 0 0 (510,500) Saler Ret&Allow 5,000 0 0 5,000 Sales Discounts 4,000 0 0 4,000 Purchases 341,400 0 0 341,400 PurchRet&Allow (8,400) 0 0 (8,400) PurchDiscouns (10,000) 0 0 (10,000) Trans-In 9,000 0 0 9,000 Advt Exp 12,000 0 0 12,000 Delivery Exp 8,000 0 0 8,000 DeprExp-Office Furn 1,580 0 0 1,580 Insurance Exp 2,500 0 0 2,500 MiscExp 4,000 0 0 4,000 Office Rent 16,400 0 0 16,400 Salaries Exp 100,000 0 0 100,000 Income Tax Exp 4,750 0 0 4,750 Income Summary A 45,000 A (30,000) 15,000 (5,270) 5,270 (5,270) Balance 0 75,000 (75,000) 0 (4,520) Net Income 4,520 (4,520) 0 0

Ratis Sales Inc. INCOME STATEMENT For the Year Ended December 31, 19X2 Sales $ 510,500 less: Sales Returns and Allowances $ 5,000 Sales Discounts 4,000 9,000

Ratis Sales Inc. STATEMENT OF RETAINED EARNINGS For the Year Ended December 31, 19X2 Balance (Jan. 1) $ 9,250 Add: Net Income for the Year 5,270 Total $14,520 Less: Dividends 10,000 Balance (Dec. 31) $ 4,520** ** Carry the balance, December 31 to the balance sheet

Net Sales Revenue $ 501,500 Cost of Goods Sold: Opening Inventory (January 1) $ 45,000 Purchases $341,400 Less: Purchases Returns/Allowances $ 8,400 Purchases Discounts 10,000 18,400 Net Purchases $323,000 Add: Transportation In 9,000 Cost of Goods Purchased 332,000 Cost of Merchandise Available $377,000 Ending Inventory (Dec. 31) 30,000 Total Cost of Goods Sold 347,000 Gross Profit $154,500 OPERATING EXPENSES Selling Expenses: Advertising Expense $ 12,000 Delivery Expense 8,000 Total Selling Expenses $ 20,000 General and Administrative Expenses: Depr. Expense-Office Fixtures $ 1,580 Insurance Expense 2,500 Miscellaneous Expense 4,000 Office Rent Expense 16,400 Salaries Expense 100,000 Total General and Administrative Expenses 124,480 Total Operating Expenses 144,480 Income Before Income Tax $ 10,020 Income Taxes 4,750 Net Income for the Year $ 5,270

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 17 SOLUTION PROBLEM 2 CONTINUED Ratis Sales Inc. BALANCE SHEET Problem 2 Requirement 3 At December 31, 19X2 Assets CURRENT ASSETS: Cash $ 11,500 Accounts Receivable 17,600 Merchandise Inventory 30,000 Prepaid Insurance 3,000 Office Supplies 6,400 Total Current Assets $ 68,500 FIXED ASSETS: Office Furniture $ 10,000 Accum. Depr.-Office Furniture 4,780 Total Fixed Assets 5,220 Total Assets $ 73,720 Liabilities and Shareholders' Equity CURRENT LIABILITIES: Bank Loan-Current $ 29,500 Accounts Payable 14,500 Income Tax Payable 1,200 Total Current Liabilities $ 45,200 LONG-TERM LIABILITIES: Bank Loan (Due Dec. 31, 19X5) 4,000 Total Liabilities $ 49,200 SHAREHOLDERS' EQUITY Common Stock $ 20,000 Retained Earnings 4,520 Total Shareholders' Equity 24,520 Total Liabilities and Shareholders' Equity $ 73,720 SOLUTION TO PROBLEM 3

GENERAL JOURNAL Date Description Dec. 31 Merchandise Inventory (ending balance) 30,000 Sales 510,500 Purchases Returns and Allowances 8,400 Purchases Discounts 10,000 Income Summary 558,900 To close credit balance nominal accounts and ending merchandise inventory to income summary 31 Income Summary 553,630 Merchandise Inventory (beginning balance) 45,000 Sales Returns and Allowances 5,000 Sales Discounts 4,000 Purchases 341,400 Transportation In 9,000 Advertising Expense 12,000 Transportation Out (Delivery Expense) 8,000 Depreciation Expense-Office Furniture 1,580 Insurance Expense 2,500 Miscellaneous Expense 4,000 Office Rent Expense 16,400 Salaries Expense 100,000 Income Taxes Expense 4,750 To close debit balance nominal accounts and beginning merchandise inventory to Income Summary 31 Income Summary 5,270 Retained Earnings 5,270 To close Income Summary to Retained Earnings 31 Retained Earnings 10,000 Dividends 10,000 To close Dividends directly to Retained Earnings

Nov. 1 Purchases 750 Transportation In 75 Accounts Payable 750 Cash 75 5 Purchases 400 Accounts Payable 400 11 Accounts Payable 50 Purchases Returns and Allowances 50 14 Office Supplies 175 Accounts Payable 175 15 Accounts Payable 25 Office Supplies 25 16 Accounts Receivable 580 Sales 580 17 Sales Returns and Allowances 30 Accounts Receivable 30 20 Accounts Payable 400 Cash 396 Purchases Discounts 4 $400 x 1% (discount 1/15) = $4; $400 - $4 = $396 25 Cash 539 Sales Discounts 11 Accounts Receivable 550 $580 - Return $30 = $550; $550 x 2% (discount 2/10) = $11; $550 - $ 11 = $539 30 Accounts Payable 700 Cash 700

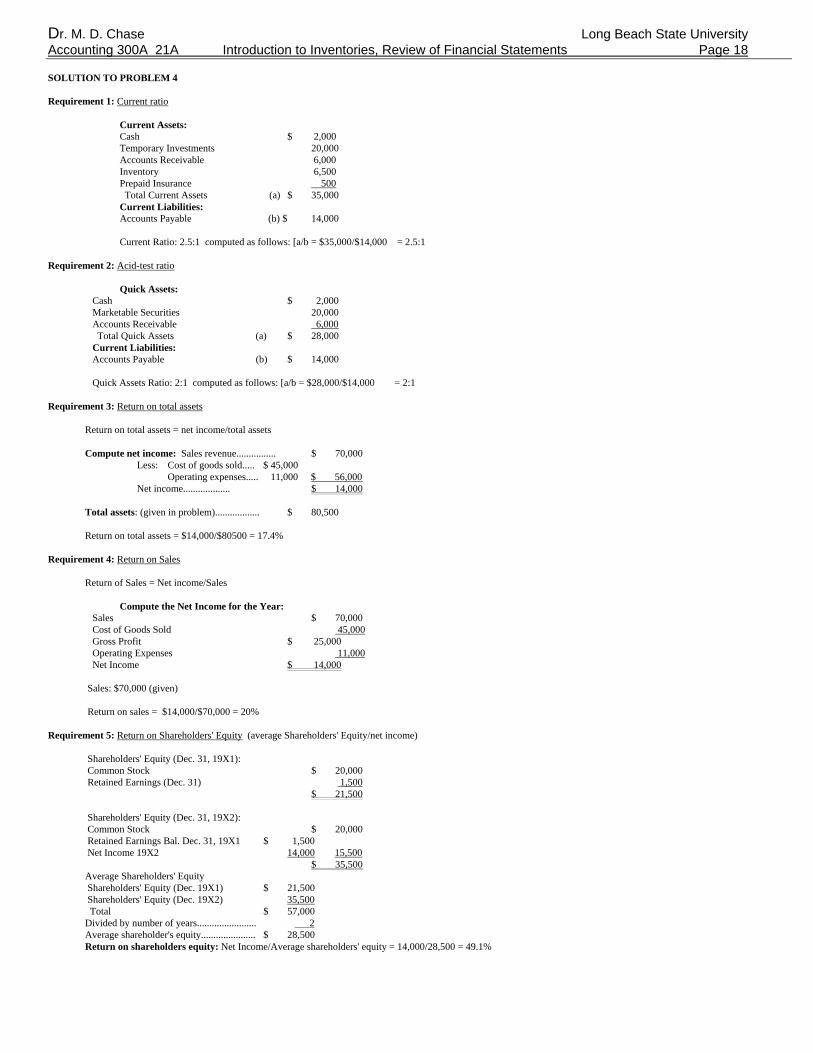

Dr. M. D. Chase Long Beach State University Accounting 300A 21A Introduction to Inventories, Review of Financial Statements Page 18 SOLUTION TO PROBLEM 4 Requirement 1: Current ratio

Current Assets: Cash $ 2,000 Temporary Investments 20,000 Accounts Receivable 6,000 Inventory 6,500 Prepaid Insurance 500 Total Current Assets (a) $ 35,000 Current Liabilities: Accounts Payable (b) $ 14,000

Current Ratio: 2.5:1 computed as follows: [a/b = $35,000/$14,000 = 2.5:1

Requirement 2: Acid-test ratio

Quick Assets: Cash $ 2,000 Marketable Securities 20,000 Accounts Receivable 6,000 Total Quick Assets (a) $ 28,000 Current Liabilities: Accounts Payable (b) $ 14,000 Quick Assets Ratio: 2:1 computed as follows: [a/b = $28,000/$14,000 = 2:1 Requirement 3: Return on total assets Return on total assets = net income/total assets Compute net income: Sales revenue................ $ 70,000 Less: Cost of goods sold..... $ 45,000 Operating expenses..... 11,000 $ 56,000 Net income................... $ 14,000 Total assets: (given in problem).................. $ 80,500 Return on total assets = $14,000/$80500 = 17.4% Requirement 4: Return on Sales Return of Sales = Net income/Sales

Compute the Net Income for the Year: Sales $ 70,000 Cost of Goods Sold 45,000 Gross Profit $ 25,000 Operating Expenses 11,000 Net Income $ 14,000 Sales: $70,000 (given) Return on sales = $14,000/$70,000 = 20% Requirement 5: Return on Shareholders' Equity (average Shareholders' Equity/net income) Shareholders' Equity (Dec. 31, 19X1): Common Stock $ 20,000 Retained Earnings (Dec. 31) 1,500 $ 21,500 Shareholders' Equity (Dec. 31, 19X2): Common Stock $ 20,000 Retained Earnings Bal. Dec. 31, 19X1 $ 1,500 Net Income 19X2 14,000 15,500 $ 35,500 Average Shareholders' Equity Shareholders' Equity (Dec. 19X1) $ 21,500 Shareholders' Equity (Dec. 19X2) 35,500 Total $ 57,000 Divided by number of years........................ 2 Average shareholder's equity...................... $ 28,500 Return on shareholders equity: Net Income/Average shareholders' equity = 14,000/28,500 = 49.1%