Workers Compensation: Economic & Regulatory Considerations

Workers Compensation Educational ConferenceOrlando, FL

August 17, 2010Download at www.iii.org/presentations

Robert P. Hartwig, Ph.D., CPCU, President & EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

2

Presentation Outline

Workers Compensation and the Economy

Labor Market Trends & Workers Comp

Employment, Unemployment & Payroll Exposure

Measures of Production and Capacity Utilization

Labor Market Performance and Workers Comp Claiming Behavior

Industry and Occupation Growth Analysis through 2018

Crisis and Recovery Exposure Drivers in Workers Comp Investment Outlook, Regulation, Torts, Terrorism, Healthcare Reform

Sources of Future Exposure Growth Favored industries and occupations: 2010 - 2018

Inflation Outlook: Workers Comp Cost Driver

Financial Market Impacts

Persistently low interest rates and the long-tailed nature of worker comp

Healthcare Reform and Workers Compensation

Q&A

3

Workers Compensation and the Economy

Workers Comp Exposure and Performance is Intimately Linked to

the Economy and Labor Market

4

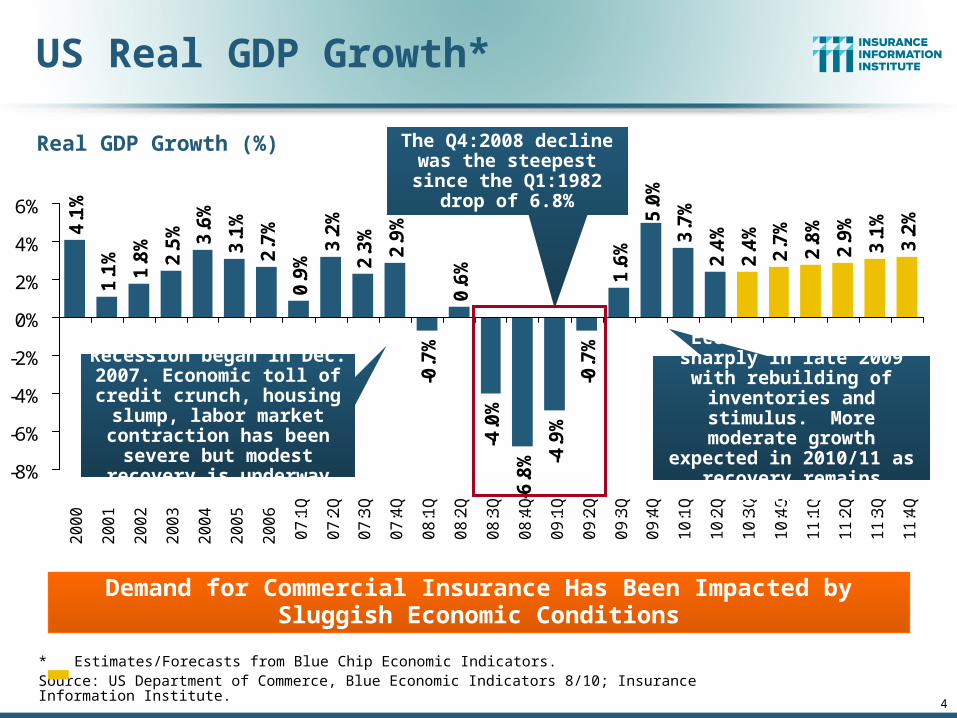

US Real GDP Growth*

* Estimates/Forecasts from Blue Chip Economic Indicators.Source: US Department of Commerce, Blue Economic Indicators 8/10; Insurance Information Institute.

2.7

%

0.9

%

3.2

%

2.3

%

2.9

%

-0.7

%

0.6

%

-4.0

%

-6.8

% -4.9

%

-0.7

%

1.6

%

5.0

%

3.7

%

2.4

%

2.4

%

2.7

%

2.8

%

2.9

%

3.1

%

3.2

%

4.1

%

1.1

%

1.8

%

2.5

% 3.6

%

3.1

%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2

00

0

2

00

1

2

00

2

2

00

3

2

00

4

2

00

5

2

00

6

07

:1Q

07

:2Q

07

:3Q

07

:4Q

08

:1Q

08

:2Q

08

:3Q

08

:4Q

09

:1Q

09

:2Q

09

:3Q

09

:4Q

10

:1Q

10

:2Q

10

:3Q

10

:4Q

11

:1Q

11

:2Q

11

:3Q

11

:4Q

Demand for Commercial Insurance Has Been Impacted by Sluggish Economic Conditions

Real GDP Growth (%)

Recession began in Dec. 2007. Economic toll of credit

crunch, housing slump, labor market contraction has

been severe but modest recovery is underway

The Q4:2008 decline was the steepest since the Q1:1982 drop of 6.8%

Economic growth up sharply in late 2009 with rebuilding

of inventories and stimulus. More moderate growth expected in 2010/11 as

recovery remains sluggish.

7

Labor Market Trends

Massive Job Losses Sapped the Economy and the Workers Comp

Payroll Exposure BaseThe Long Road to Recovery

8

Unemployment and Underemployment Rates: Rocketed Up in 2008-09; Stabilizing in 2010?

2

4

6

8

10

12

14

16

18

Jan 00 Jan 01 Jan 02 Jan 03 Jan 04 Jan 05 Jan 06 Jan 07 Jan 08 Jan 09 Jan 10

Traditional Unemployment Rate U-3

Unemployment + Underemployment Rate U-6

Jun10

Unemployment rate was 9.5% in

June

Unemployment peaked at 10.1%

in Oct. 2009, highest monthly rate since 1983.

Peak rate in the last 30 years: 10.8% in Nov -

Dec 1982

Source: US Bureau of Labor Statistics; Insurance Information Institute.

U-6 went from 8.0% in March

2007 to 17.5% in Oct 2009; Stood at 16.5% in June

2010

January 2000 through June 2010, Seasonally Adjusted (%)

Recession ended in

November 2001

Unemployment kept rising for

19 more months

Recession began in

December 2007

10

US Unemployment Rate

4.5

%

4.5

%

4.6

%

4.8

%

4.9

% 5.4

% 6.1

%

6.9

%

8.1

%

9.3

%

9.6

% 10

.0%

9.7

%

9.7

%

9.6

%

9.4

%

9.2

%

9.0

%

8.8

%9.5

%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

07

:Q1

07

:Q2

07

:Q3

07

:Q4

08

:Q1

08

:Q2

08

:Q3

08

:Q4

09

:Q1

09

:Q2

09

:Q3

09

:Q4

10

:Q1

10

:Q2

10

:Q3

10

:Q4

11

:Q1

11

:Q2

11

:Q3

11

:Q4

Rising unemployment eroded payrolls

and workers comp’s exposure base.

Unemployment likely peaked at 10% in late 2009.

* = actual; = forecastsSources: US Bureau of Labor Statistics; Blue Chip Economic Indicators (8/10); Insurance Information Institute

2007:Q1 to 2011:Q4F*

Unemployment forecasts remain stubbornly high

through 2011

12

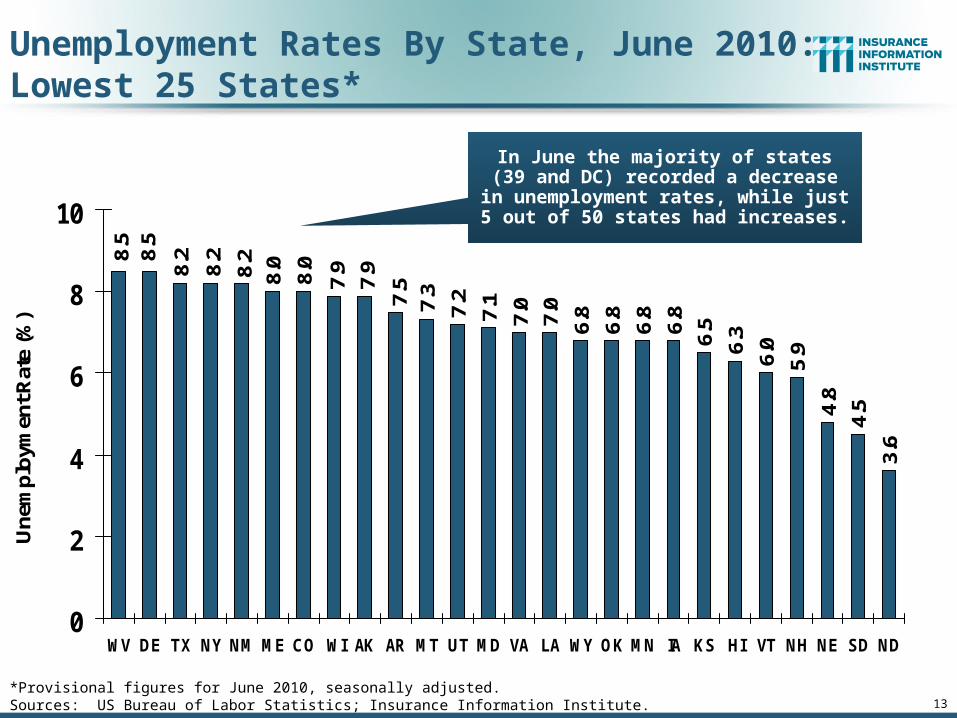

Unemployment Rates by State, June 2010:Highest 25 States*

10.0

10.0

10.1

10.0

10.0

10.1

9.2

9.0

9.1

8.89.

6

8.8

8.99.

610.711

.4

10.3

10.4

10.5

10.511

.0

13.2

12.3

12.0

14.2

0

2

4

6

8

10

12

14

16

NV MI CA RI FL MS SC OR OH IL AL TN IN NC KY GA DC NJ AZ PA MO MA WA ID CT

Une

mpl

oym

ent R

ate

(%)

*Provisional figures for June 2010, seasonally adjusted.

Sources: US Bureau of Labor Statistics; Insurance Information Institute.

In June the majority of states (39 and DC) recorded a decrease in unemployment rates, while just 5 out of 50 states had

increases.

13

6.8

6.5

6.3

6.0

6.8

6.87.

17.

2

4.54.

85.

9

7.0

7.0

3.6

6.8

8.08.2

7.37.57.

97.

98.08.

5

8.2

8.28.

5

0

2

4

6

8

10

WV DE TX NY NM ME CO WI AK AR MT UT MD VA LA WY OK MN IA KS HI VT NH NE SD ND

Une

mpl

oym

ent R

ate

(%)

Unemployment Rates By State, June 2010: Lowest 25 States*

*Provisional figures for June 2010, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute.

In June the majority of states (39 and DC) recorded a decrease in unemployment rates, while just 5 out of 50 states had

increases.

14

Monthly Change Employment*-7

2

-14

4-1

22

-16

0-1

37

-16

1

-12

8-1

75

-32

1

-38

0-5

97

-68

1-7

79

-72

6

-75

3-5

28 -3

87

-51

5 -34

6 -21

2-2

25

-22

46

4

-10

9

14 39

20

8 31

3 43

2

-22

1-1

31

-1,000

-800

-600

-400

-200

0

200

400

600

Jan

08

Fe

b 0

8

Ma

r 0

8

Ap

r 0

8M

ay

08

Jun

08

Jul 0

8

Au

g 0

8

Se

p 0

8O

ct 0

8

No

v 0

8

De

c 0

8Ja

n 0

9

Fe

b 0

9M

ar

09

Ap

r 0

9

Ma

y 0

9Ju

n 0

9

Jul 0

9A

ug

09

Se

p 0

9

Oct

09

No

v 0

9

De

c 0

9

Jan

10

Fe

b 1

0

Ma

r 1

0A

pr

10

Ma

y 1

0

Jun

10

Jul 1

0

Monthly Losses in Dec. 08–Mar. 09 Were

the Largest in the Post-WW II Period

*Estimate based on Reuters poll of economists.Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Information Institute

Job Losses Since the Recession Began in Dec. 2007 Peaked at 8.4 Mill in Dec. 09; Stands at 7.7 Million Through June 2010;

14.6 Million People are Now Defined as Unemployed

January 2008 through July 2010* (Thousands)

May’s gain of 432,000 jobs was distorted by the hiring of 411,000 temporary Census workers. Census job losses totaled 225,000 in June and

143,000 in July, distorting figures in both months. Private sector employment was up 31,000 in May,

51,000 in June and 71,000 in July.

15

US Nonfarm Private Employment1

38

.01

38

.11

38

.01

37

.91

37

.81

37

.81

37

.71

37

.61

37

.61

37

.41

37

.01

36

.71

36

.21

35

.11

33

.51

32

.81

32

.11

31

.51

31

.21

30

.61

30

.31

30

.11

29

.91

29

.61

29

.71

29

.61

29

.61

29

.61

29

.81

30

.21

30

.61

30

.41

30

.2

129130131132133134135136137138139

No

v 0

7D

ec

07

Jan

08

Fe

b 0

8M

ar

08

Ap

r 0

8M

ay

08

Jun

eJu

l 08

Au

g 0

8S

ep

08

Oct

08

No

v 0

8D

ec

08

Jan

09

Fe

b 0

9M

ar

09

Ap

r 0

9M

ay

09

Jun

09

Jul 0

9A

ug

09

Se

p 0

9O

ct 0

9N

ov

09

De

c 0

9Ja

n 1

0F

eb

10

Ma

r 1

0A

pr

10

Ma

y 1

0Ju

n 1

0Ju

l 10

Monthly, Nov 2007 – July 2010 (Millions)

The US Economy Lost About 8.4 Million Jobs in the Two

Years from Dec. 07 – Dec. 09.

As employment expands, workers comp will be among the first lines to see exposure

gains

Employment Peak; Recession Starts

Seasonally adjusted. Source: US Bureau of Labor Statistics

16

U.S. Nonfarm Employment,Monthly, 1990–2010*

*As of July 2010; Not seasonally adjustedNote: Recessions indicated by gray shaded columns.Sources: US Bureau of Labor Statistics; National Bureau of Economic Research (recession dates); Insurance Information Institutes.

Millions

105

110

115

120

125

130

135

140

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

The number of employed people in the US today is

approximately the same as it was in late 2004

Estimated Effect of Recessions* on Payroll (Workers Comp Exposure)

*Data represent maximum recorded decline over 12-month period using annualized quarterly wage and salary accrual dataSource: Insurance Information Institute research; Federal Reserve Bank of St. Louis (wage and salary data); National Bureau of Economic Research (recession dates).

-4.4%

-2.0%-1.1%

1.1%

3.7%4.6%

8.5%

3.5%

2.1%

-0.5%

-3.6%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1948-1949

1953-1954

1957-1958

1960-1961

1969-1970

1973-1975

1980 1981-1982

1990-1991

2001 2007-2009

Recessions in the 1970s and 1980s saw smaller exposure impacts

because of continued wage inflation, a factor not present

during the 2007-2009 recession

The Dec. 2007 to mid-2009 recession

caused the largest impact on WC

exposure in 60 years

(Percent Change)

(All Post WWII Recessions)

Recession Dates (Beginning/Ending Years)

18

Wage & Salary Disbursement (Private Employment) vs. WC NWP ($ Billions)

Wage & Salary Disbursements (Payroll Base) vs. Workers Comp Net Written Premiums

* Average Wage and Salary data as of 10/1/2009. Shaded areas indicate recessions. **Estimated “official” end of recession June 2009.Source: US Bureau of Economic Analysis; Federal Reserve Bank of St. Louis at http://research.stlouisfed.org/fred2/series/WASCUR ; I.I.I. Fact Books

Weakening Payrolls Have Eroded $2B+ in Workers Comp Premiums; Nearly 29% of NPW Has Been Eroded Away by the Soft Market and Weak Economy

7/90-3/91 3/01-11/01

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09*

$0

$10

$20

$30

$40

$50

$60

Wage & SalaryDisbursements

WC NPW

WC net premiums written were down $13.7B or 28.7%

to $34.1B in 2009 after peaking at $47.8B in 2005

12/07-6/09**

Soft Labor Markets and Impacts on WC Claim Frequency

19

Net Impact of Recession Appears to Be a Decline in Frequency;

Swaps and Layoff-Induced Effect

20

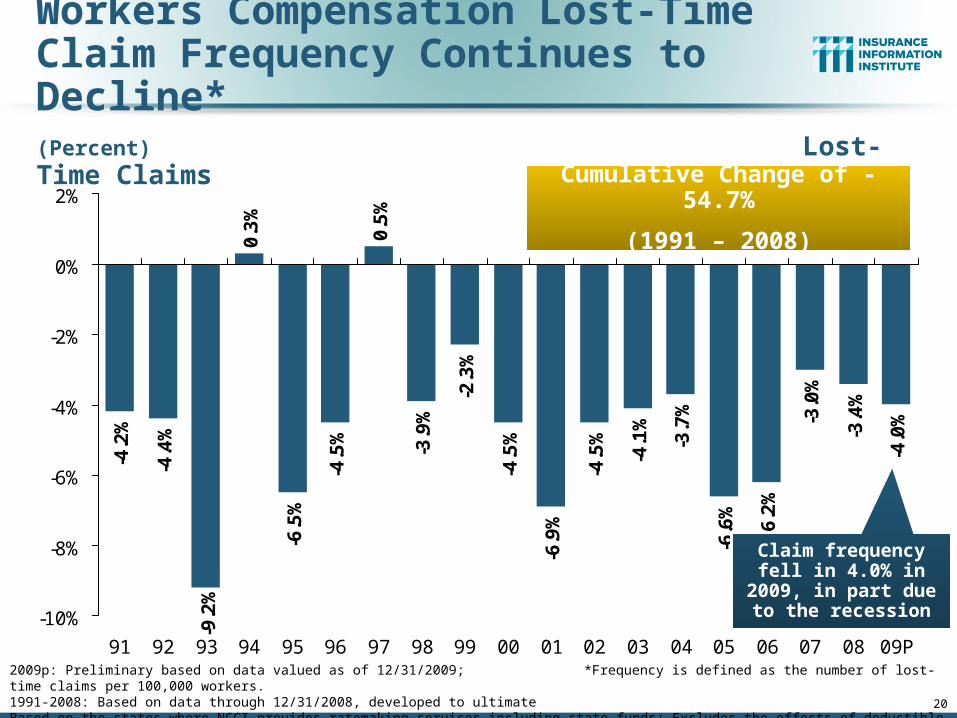

Workers Compensation Lost-Time Claim Frequency Continues to Decline*

-4.4

%

0.3

%

-6.5

%

-4.5

%

0.5

%

-3.9

%

-2.3

%

-4.5

%

-6.9

%

-4.5

%

-4.1

%

-3.7

%

-6.6

%

-6.2

%

-3.0

%

-3.4

%

-4.0

%

-9.2

%

-4.2

%

-10%

-8%

-6%

-4%

-2%

0%

2%

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09P

(Percent) Lost-Time Claims

Claim frequency fell in 4.0% in 2009, in part due to the recession

Cumulative Change of -54.7%

(1991 – 2008)

2009p: Preliminary based on data valued as of 12/31/2009; *Frequency is defined as the number of lost-time claims per 100,000 workers.1991-2008: Based on data through 12/31/2008, developed to ultimateBased on the states where NCCI provides ratemaking services including state funds; Excludes the effects of deductible policies

21

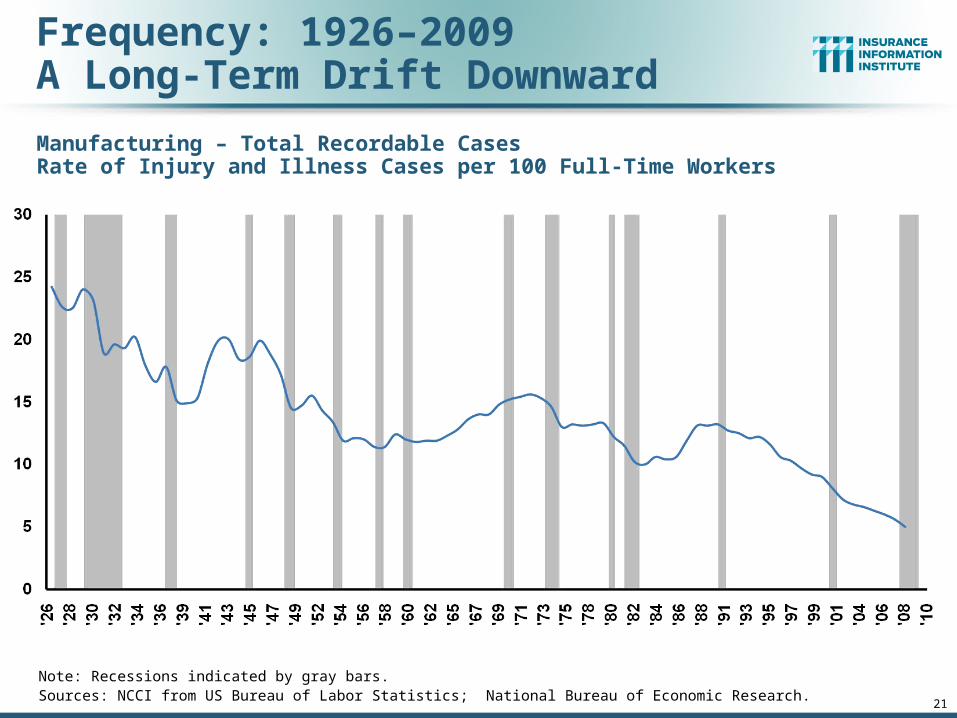

Frequency: 1926–2009A Long-Term Drift Downward

Note: Recessions indicated by gray bars.Sources: NCCI from US Bureau of Labor Statistics; National Bureau of Economic Research.

Manufacturing – Total Recordable CasesRate of Injury and Illness Cases per 100 Full-Time Workers

22

Note: Recessions indicated by gray bars.Sources: NCC, US Bureau of Labor Statistics;

Workplace Injury Incidence Rates Declined in Last Four Economic Downturns

Crisis and Recovery-Driven Exposure Drivers in WC

23

Myriad of Impacts on Workers Comp Exposure

Filling the Economic Crater

24

43,6

9448

,125

69,3

0062

,436

64,0

04 71,2

77 81,2

3582

,446

63,8

5363

,235

64,8

5371

,549

70,6

4362

,304

52,3

7451

,959

53,5

4954

,027

44,3

6737

,884

35,4

7240

,099

38,5

4035

,037

34,3

1739

,201

19,6

95 28,3

2243

,546

60,8

3714

,607

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 0910

:Q1

Business Bankruptcy Filings,1980-2010:Q1

Source: American Bankruptcy Institute; Insurance Information Institute

Significant Exposure Implications for All Commercial Lines

There were 60,837 business bankruptcies in 2009, up 40% from 2008 and the most since 1993. 2010:Q1 bankruptcies totaled 14,607, up 18% from Q1:2009

% Change Surrounding Recessions

1980-82 58.6%1980-87 88.7%1990-91 10.3%2000-01 13.0%2006-09 208.9%*

25

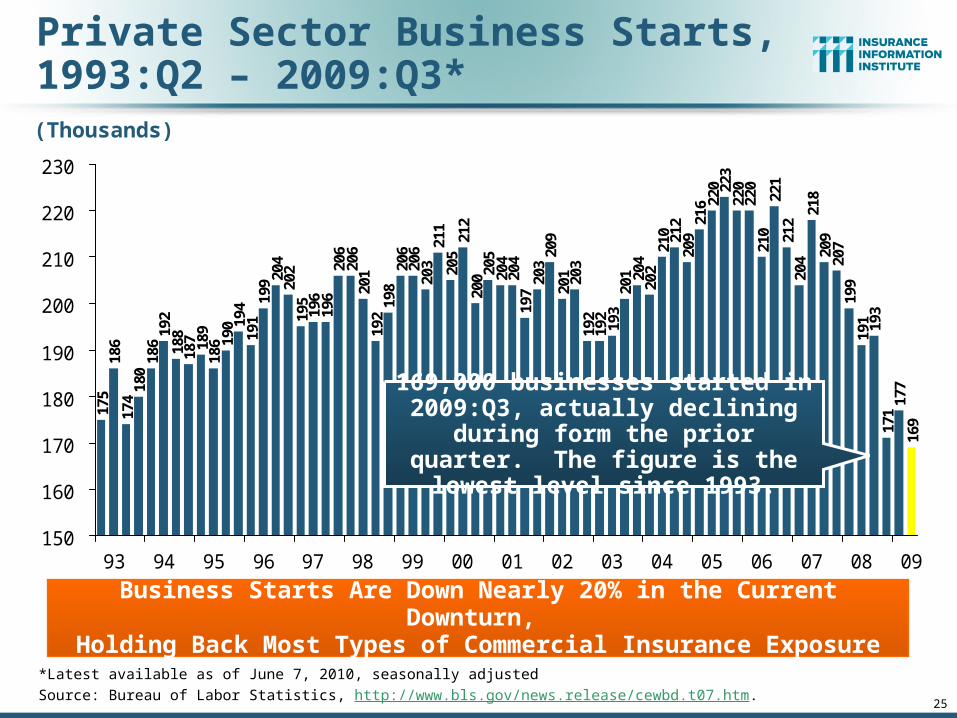

Private Sector Business Starts,1993:Q2 – 2009:Q3*

175

186

174

180

186

192

188

187 18

918

6 190 19

419

119

9 204

202

195

196

196

206

206

201

192

198

206

206

203

211

205

212

200 20

520

420

419

720

320

920

1

192

192

193

201 20

420

221

0 212

209

216 22

0 223

220

220

210

221

212

204

218

209

207

199

191 19

317

117

716

9

203

150

160

170

180

190

200

210

220

230

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Business Starts Are Down Nearly 20% in the Current Downturn, Holding Back Most Types of Commercial Insurance Exposure

*Latest available as of June 7, 2010, seasonally adjustedSource: Bureau of Labor Statistics, http://www.bls.gov/news.release/cewbd.t07.htm.

(Thousands)

169,000 businesses started in 2009:Q3, actually declining during

form the prior quarter. The figure is the lowest level since 1993.

66%

68%

70%

72%

74%

76%

78%

80%

82%

Ma

r 0

1

Ju

n 0

1

Se

p 0

1

De

c 0

1

Ma

r 0

2

Ju

n 0

2

Se

p 0

2

De

c 0

2

Ma

r 0

3

Ju

n 0

3

Se

p 0

3

De

c 0

3

Ma

r 0

4

Ju

n 0

4

Se

p 0

4

De

c 0

4

Ma

r 0

5

Ju

n 0

5

Se

p 0

5

De

c 0

5

Ma

r 0

6

Ju

n 0

6

Se

p 0

6

De

c 0

6

Ma

r 0

7

Ju

n 0

7

Se

p 0

7

De

c 0

7

Ma

r 0

8

Ju

n 0

8

Se

p 0

8

De

c 0

8

Ma

r 0

9

Ju

n 0

9

Se

p 0

9

De

c 0

9

Ma

r 1

0

Ju

n 1

0

Recovery in Capacity Utilization is a Positive Sign for Insurance

Source: Federal Reserve Board statistical releases at http://www.federalreserve.gov/releases/g17/Current/default.htm. 26

Hurricane Katrina

March 2001-November 2001

recession

“Full Capacity”

The closer the economy is to operating at “full

capacity,” the greater the demand for insurance

Manufacturing capacity stood at 74.1% in June 2010, above the June 2009 low of 68.3% but

well below the pre-crisis peak of 80%+

Recession began December 2007

Percent of Total Industry Capacity

Where Will the Growth in WC Exposure Come From?

27

Industry and Occupation Growth Analysis

28

Fastest Growing Occupations, 2008–2018:Health/Science/Tech Dominate

Sources: US Bureau of Labor Statistics: Occupational Outlook Handbook, 2010-2011 Edition; Insurance Information Institute

OccupationsPercent change

Number of

new jobs(in thousands)

Wages (May 2008 median) Education/training category

Biomedical engineers 72 11.6 $ 77,400 Bachelor's degree

Network systems and data communications analysts

53 155.8 71,100 Bachelor's degree

Home health aides 50 460.9 20,460 Short-term on-the-job training

Personal and home care aides 46 375.8 19,180 Short-term on-the-job training

Financial examiners 41 11.1 70,930 Bachelor's degree

Medical scientists, except epidemiologists

40 44.2 72,590 Doctoral degree

Physician assistants 39 29.2 81,230 Master's degree

Skin care specialists 38 14.7 28,730 Postsecondary vocational award

Biochemists and biophysicists 37 8.7 82,840 Doctoral degree

Athletic trainers 37 6.0 39,640 Bachelor's degree

Physical therapist aides 36 16.7 23,760 Short-term on-the-job training

Dental hygienists 36 62.9 66,570 Associate degree

Veterinary technologists and technicians

36 28.5 28,900 Associate degree

Dental assistants 36 105.6 32,380 Moderate-term on-the-job training

Computer software engineers, applications

34 175.1 85,430 Bachelor's degree

Medical assistants 34 163.9 28,300 Moderate-term on-the-job training

Physical therapist assistants 33 21.2 46,140 Associate degree

Veterinarians 33 19.7 79,050 First professional degree

Self-enrichment education teachers

32 81.3 35,720 Work experience in a related occupation

Compliance officers, except agriculture, construction, health and safety, and transportation

31 80.8 48,890 Long-term on-the-job training

SOURCE: BLS Occupational Employment Statistics and Division of Occupational Outlook

WC exposure growth the fastest in the health, science and tech areas

29

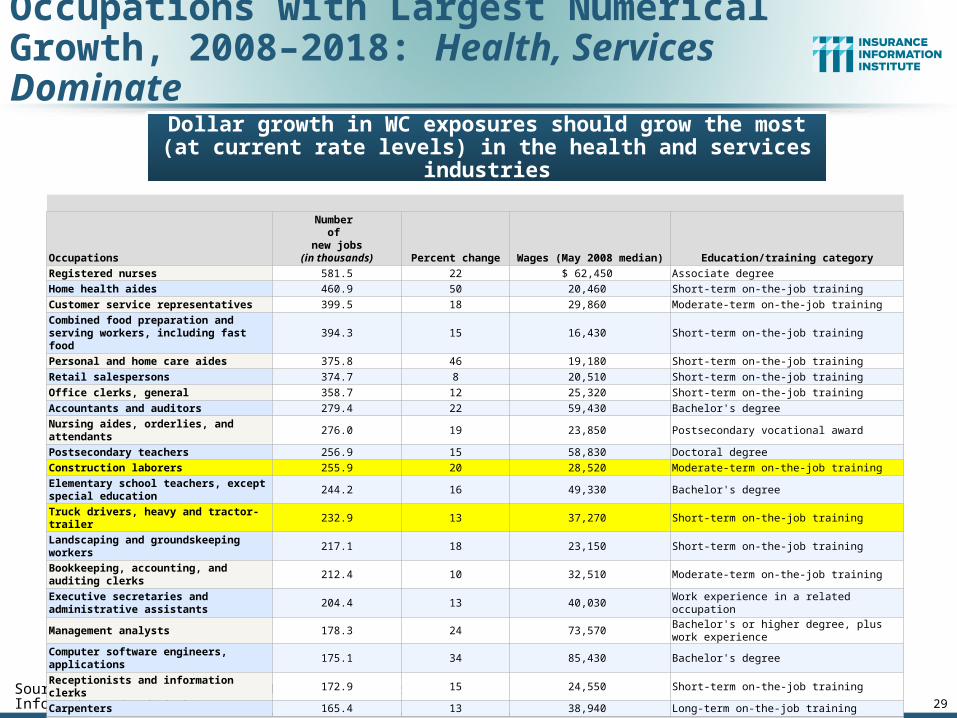

Occupations with Largest Numerical Growth, 2008–2018: Health, Services Dominate

Sources: US Bureau of Labor Statistics: Occupational Outlook Handbook, 2010-2011 Edition; Insurance Information Institute

Dollar growth in WC exposures should grow the most (at current rate levels) in the health and services industries

Occupations

Number of

new jobs(in thousands) Percent change

Wages (May 2008 median) Education/training category

Registered nurses 581.5 22 $ 62,450 Associate degree

Home health aides 460.9 50 20,460 Short-term on-the-job training

Customer service representatives 399.5 18 29,860 Moderate-term on-the-job training

Combined food preparation and serving workers, including fast food

394.3 15 16,430 Short-term on-the-job training

Personal and home care aides 375.8 46 19,180 Short-term on-the-job training

Retail salespersons 374.7 8 20,510 Short-term on-the-job training

Office clerks, general 358.7 12 25,320 Short-term on-the-job training

Accountants and auditors 279.4 22 59,430 Bachelor's degree

Nursing aides, orderlies, and attendants

276.0 19 23,850 Postsecondary vocational award

Postsecondary teachers 256.9 15 58,830 Doctoral degree

Construction laborers 255.9 20 28,520 Moderate-term on-the-job training

Elementary school teachers, except special education

244.2 16 49,330 Bachelor's degree

Truck drivers, heavy and tractor-trailer

232.9 13 37,270 Short-term on-the-job training

Landscaping and groundskeeping workers

217.1 18 23,150 Short-term on-the-job training

Bookkeeping, accounting, and auditing clerks

212.4 10 32,510 Moderate-term on-the-job training

Executive secretaries and administrative assistants

204.4 13 40,030 Work experience in a related occupation

Management analysts 178.3 24 73,570 Bachelor's or higher degree, plus work experience

Computer software engineers, applications

175.1 34 85,430 Bachelor's degree

Receptionists and information clerks

172.9 15 24,550 Short-term on-the-job training

Carpenters 165.4 13 38,940 Long-term on-the-job trainingSOURCE: BLS Occupational Employment Statistics and Division of Occupational Outlook

30

(Thousands)

704

654

446

322

304

256

236

118

102

788

838

1,431

1,683

2,657

4,017

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500

Health Care and Social Assistance

Professional, Scientific, Tech. Srvs.

Education Services

Administration, Support, Waste Mgmt & Removal

Accomodation & Food Services

Government

Other Services (excl. Govt.)

Retail Trade

Transportation and Warehousing

Finance & Insurance

Arts, Entertainment & Recreation

holesale Trade

Real Estate, Rental & Leasing

Information

Mgmt. of Companies & Enterprises

Health, Science and Education will be

important sources of exposure growth for WC

insurers this decade

Sources: US Bureau of Labor Statistics: Occupational Outlook Handbook, 2010-2011 Edition; Insurance Information Institute

Numeric Change in Wage and Salary Employment in Service-Providing Industries: 2008-2018P

31

Mounting Pressure on Claim Cost Severities?

Inflation Trends:Concerns Over Stimulus Spending

and Monetary Policy

32

Annual Inflation Rates(CPI-U, %), 1990–2011F

2.8 2.6

1.51.9

3.3 3.4

1.3

2.5 2.3

3.0

3.8

2.8

3.8

-0.4

1.6 1.5

2.92.4

3.23.0

5.14.9

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10F11F

Sources: US Bureau of Labor Statistics; Blue Chip Economic Indicators, 8/2010 (forecasts).

There is So Much Slack in the US Economy Inflation Should Not Be a Concern Through 2010/11, but Deficits and Monetary Policy Remain Longer

Run Concerns

Annual Inflation Rates (%) Inflation peaked at 5.6% in August 2008 on high energy and commodity crisis. The recession and the collapse of the

commodity bubble have reduced inflationary pressures

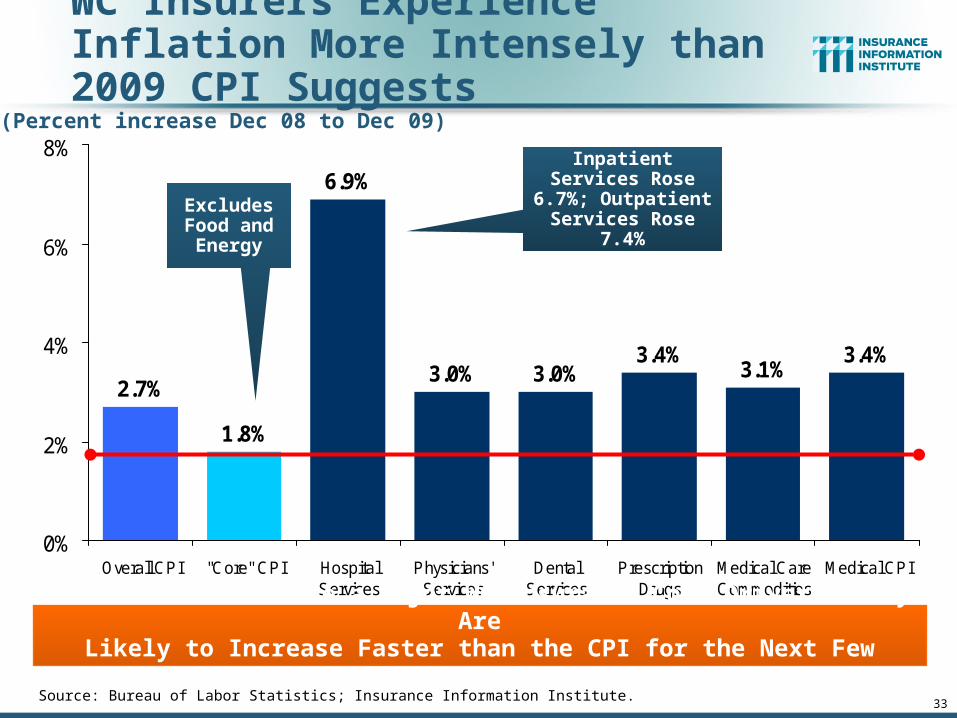

WC Insurers Experience Inflation More Intensely than 2009 CPI Suggests

Source: Bureau of Labor Statistics; Insurance Information Institute.

2.7%

1.8%

6.9%

3.0% 3.0%3.4%

3.1%3.4%

0%

2%

4%

6%

8%

Overall CPI "Core" CPI HospitalServices

Physicians'Services

DentalServices

PrescriptionDrugs

Medical CareCommodities

Medical CPI

(Percent increase Dec 08 to Dec 09)

Healthcare Costs Are a Major WC Insurance Cost Driver. They AreLikely to Increase Faster than the CPI for the Next Few Years, at Least

33

Excludes Food and Energy

Inpatient Services Rose 6.7%;

Outpatient Services Rose 7.4%

4.5%

3.5%2.8%

3.2% 3.5%4.1%

4.6% 4.7%4.0%

4.4% 4.2% 4.0%4.4%

3.7% 3.4%

5.1%

7.4%

10.1%

8.3%

10.6%

7.3%

13.5%

8.8%

7.3%

5.6%

7.4%

5.4% 5.4%

6.7%

5.0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Change in Medical CPI

Change Med Cost per Lost Time Claim

WC Medical Severity Risingat Twice the Medical CPI Rate

Sources: Med CPI from US Bureau of Labor Statistics, WC med severity from NCCI based on NCCI states.

Average annual increase in WC medical severity form 1995 through 2009 was nearly twice the medical CPI (7.6% vs.

3.9%). New healthcare reform legislation is unlikely to have any

impact on the gap.

4.2%

5.2%5.6%

4.7%

6.3%

2.3%

1.1%

2.7%

1.7%

4.7% 4.6%

2.3%

5.9%

7.7%

9.0%

10.1%

4.1%

1.7%

3.1%

5.0% 5.0%5.8%

4.5%

-1.0%

3.5%

3.6%

1.7%

10.1%

9.2%

3.1%

-2%

0%

2%

4%

6%

8%

10%

12%

1995 1997 1999 2001 2003 2005 2007 2009p

Change in CPS Wage Change in Indemnity Cost per Lost-Time Claim

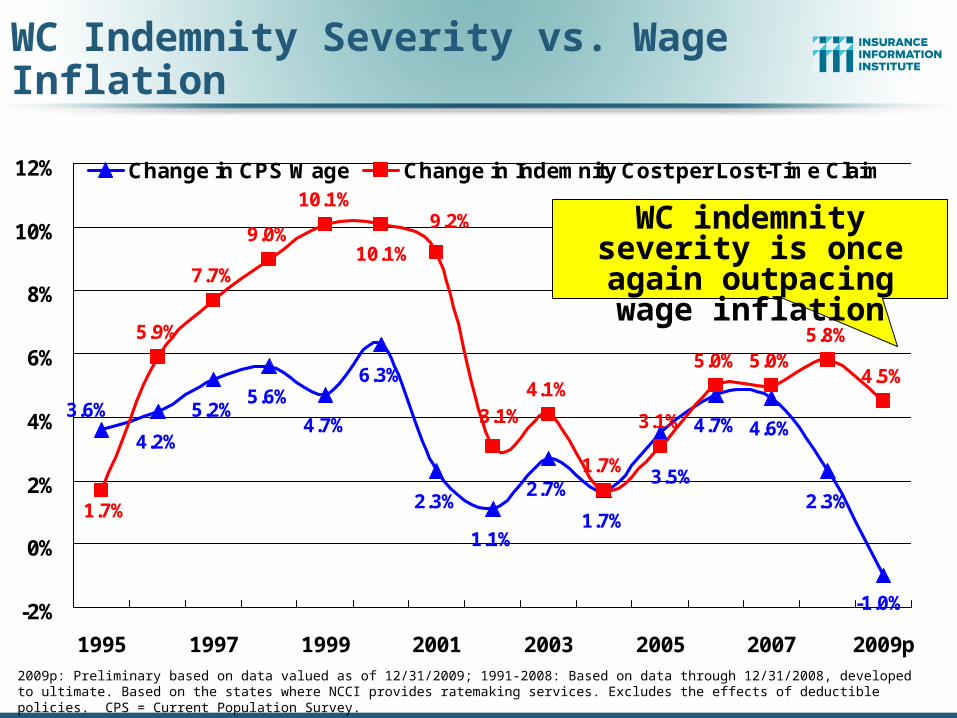

WC Indemnity Severity vs. Wage Inflation

2009p: Preliminary based on data valued as of 12/31/2009; 1991-2008: Based on data through 12/31/2008, developed to ultimate. Based on the states where NCCI provides ratemaking services. Excludes the effects of deductible policies. CPS = Current Population Survey.Source: NCCI

WC indemnity severity is once again outpacing

wage inflation

Investment Performance

36

Persistently Low Interest Rates Must Eventually Impact Pricing as Underwriting Losses Mount

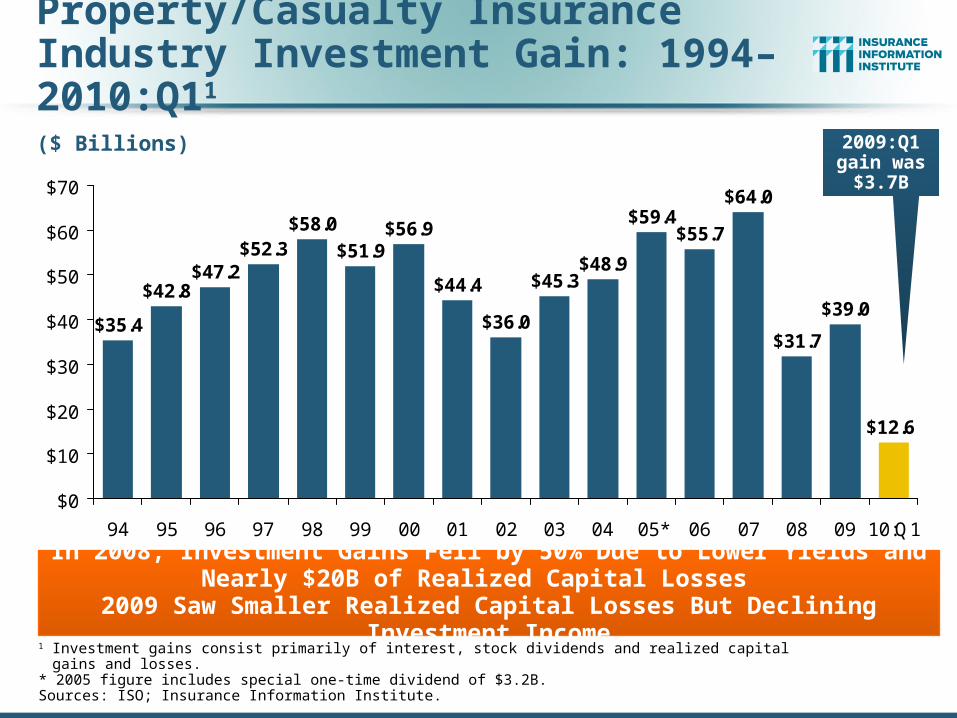

Property/Casualty Insurance Industry Investment Gain: 1994–2010:Q11

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7

$64.0

$31.7

$39.0

$12.6

$58.0

$51.9$56.9

$0

$10

$20

$30

$40

$50

$60

$70

94 95 96 97 98 99 00 01 02 03 04 05* 06 07 08 09 10:Q1

In 2008, Investment Gains Fell by 50% Due to Lower Yields andNearly $20B of Realized Capital Losses

2009 Saw Smaller Realized Capital Losses But Declining Investment Income

1 Investment gains consist primarily of interest, stock dividends and realized capital gains and losses.* 2005 figure includes special one-time dividend of $3.2B.Sources: ISO; Insurance Information Institute.

($ Billions) 2009:Q1 gain was

$3.7B

38

Treasury Yield Curves: Pre-Crisis (July 2007) vs. July 2010

0.16% 0.16% 0.20% 0.29%0.62%

2.43%

3.01%

4.82% 4.96% 5.04% 4.96% 4.82% 4.82% 4.88% 5.00% 4.93% 5.00%5.19%

1.76%

0.98%

3.99%3.80%

0%

1%

2%

3%

4%

5%

6%

1M 3M 6M 1Y 2Y 3Y 5Y 7Y 10Y 20Y 30Y

July 2010 Yield Curve*Pre-Crisis (July 2007)

Treasury yield curve is near its most depressed level in at least 45 years. Investment

income is falling as a result

Stock Dividend Cuts Have Further Pressured Investment Income

Sources: Board of Governors of the United States Federal Reserve Bank; Insurance Information Institute.

39

-1.8

%

-1.8

%

-2.0

%

-3.6

%

-3.3

%

-3.3

%

-3.7

%

-4.3

%

-5.2

%

-5.7

%

-7.3%

-1.9

%

-2.1

%

-3.1

%

-8%-7%-6%-5%-4%-3%-2%-1%0%

Perso

nal L

ines

Pvt Pass

Aut

o

Pers P

rop

Comm

ercia

l

Comm

l Auto

Credit

Comm

Pro

p

Comm

Cas

Fidelity

/Sure

ty

War

rant

y

Surplu

s Line

s

Med

Mal

WC

Reinsu

ranc

e**

Lower Investment Earnings Place a Greater Burden on Underwriting and Pricing Discipline

*Based on 2008 Invested Assets and Earned Premiums**US domestic reinsurance onlySource: A.M. Best; Insurance Information Institute.

Reduction in Combined Ratio Necessary to Offset 1% Decline in Investment Yield to Maintain Constant ROE, by Line*

Healthcare Reform & Workers Compensation

40

Likely a Slight, Net Positive for Workers Comp in the Long Run

41

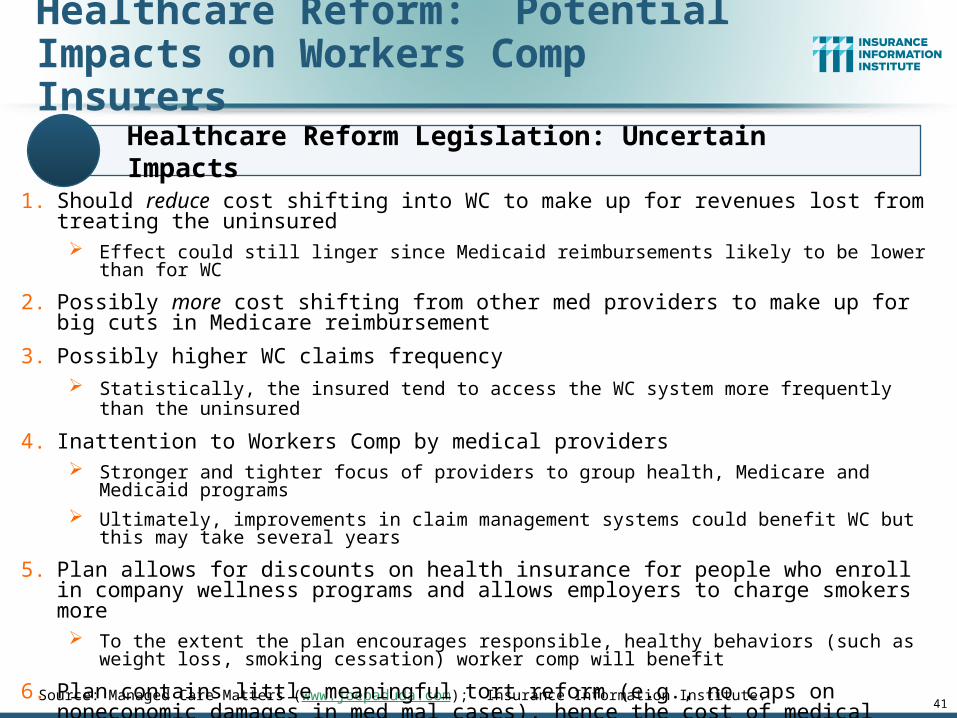

Healthcare Reform: Potential Impacts on Workers Comp Insurers

Source: Managed Care Matters (www.joepaduda.com); Insurance Information Institute.

1. Should reduce cost shifting into WC to make up for revenues lost from treating the uninsured Effect could still linger since Medicaid reimbursements likely to be lower than for WC

2. Possibly more cost shifting from other med providers to make up for big cuts in Medicare reimbursement

3. Possibly higher WC claims frequency Statistically, the insured tend to access the WC system more frequently than the uninsured

4. Inattention to Workers Comp by medical providers Stronger and tighter focus of providers to group health, Medicare and Medicaid programs

Ultimately, improvements in claim management systems could benefit WC but this may take several years

5. Plan allows for discounts on health insurance for people who enroll in company wellness programs and allows employers to charge smokers more To the extent the plan encourages responsible, healthy behaviors (such as weight loss, smoking

cessation) worker comp will benefit

6. Plan contains little meaningful tort reform (e.g., no caps on noneconomic damages in med mal cases), hence the cost of medical care, will be inflated by tort costs and the cost of defensive medicine, including care provided through the WC system The CBO priced the savings from tort reform, if adopted, at $54 billion over 10 years.

Healthcare Reform Legislation: Uncertain Impacts

www.iii.org

Thank you for your timeand your attention!

Twitter: twitter.com/bob_hartwig

Insurance Information Institute Online: