Download - Welcome from John Hancock - nbsbenefits.com

If you’re like most people, you’re hoping for a financially secure retirement. Achieving your retirement

dreams requires more than just hope, it requires a plan.

This PDF is one key to that plan. It can help get you on the path toward a financially secure retirement.

It will also walk you step-by-step through how to enroll.

It’s as easy as 1,2,3 Go!

Your retirement plan is a powerful savings tool that your employer is making available to you as a value-

added benefit. Seize this opportunity to quickly and easily lay the foundation for your financial future.

John Hancock – helping you enjoy getting there

How to use this PDF:

We highly recommend that you don’t print this entire PDF. Instead use it as

an electronic resource

Form to enroll – print pages |

Form to rollover qualified retirement accounts – print pages |

A chapter menu exists on the left hand side of the file so you can easily

navigate to each section.

This kit is current as of:This kit expires on:

Welcomefrom John Hancock

November 16, 2010December 16, 2010

51 - 64

125 - 126

P 17769-LTR-GE 07/10-18105

Your Personal Identification Number (PIN) will arrive shortly after John Hancock receives

your completed enrollment form. Use it to securely access your account.

In the meantime take advantage of a number of online retirement planning tools, calculators

and more on John Hancock’s website www.jhpensions.com or www.jhnypensions.com

(for plans domiciled in New York).

For a quick overview of the website

How to register for the website

1. Enter your contract number

Enter the contract number in the space provided.

You can obtain this number from your plan

administrator, enrollment form or your

quarterly statement.

2. Create a username and password

Once you’ve entered your contract number, you

will be asked to create a unique username and

password. You will need these to access your

account online in the future.

3. Enter your Personal Identification

Number (PIN)

You will be prompted to enter your PIN.

(Note: Contract and PIN numbers are not the

same and will be required at different times

when using John Hancock’s services).

Lost your PIN or forgotten yourlogin information?

If you forget your login information, you can

always use the number from your PIN and

the balance of a recent statement to access

your account.

If you receive two PIN’s, use the one with

the most recent date. Only the PIN with the

most recent issue date will permit access to

your account.

If you forget your PIN, contact a John Hancock

Retirement Plan Services customer service

representative at 1-800-395-1113 to request

a new PIN.

Accessingyour account

Take a Tour

Retirement planning that’s as easy as 1, 2, 3, Go!

EnjoyGetting

There

P 17658-GE 07/10-17658

KIT351405

John Hancock – helping you enjoy getting thereEnrolling is just the beginning!

John Hancock is there to support you every step of the way. We have more than 100 years

of leadership and experience helping millions of Americans prepare for their financial futures.

Take advantage of our award-winning communications, manage your account through our easy-to-

use website and get the tools, information and resources you need to plan for a secure retirement.

1ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-WEL-G

E 07/10-17324

Welcome from John HancockIf you’re like most people, you’re hoping for a financiallysecure retirement. Achieving your retirement dreams requiresmore than just hope, however. It requires a plan.

The booklet you’re holding is one key to that plan. It’s simple and can help get you onthe path toward a financially secure retirement.

It’s as easy as 1, 2, 3, Go!Participating in your company’s qualified retirement plan is easy. This booklet will walkyou step-by-step through how to enroll.

Whether you were enrolled in a retirement plan with a previous employer or you’restarting fresh, participating is extremely important. It’s never too early (or too late) tostart saving for your future. And participating can provide you with key benefits, such as potential tax savings, the power of compound earnings and more.

Your retirement plan is a powerful savings tool that your employer is making availableto you as a value-added benefit. Seize this opportunity to quickly and easily lay thefoundation for your financial future.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!2

1

2

3

GO

John Hancock Life Insurance Company (U.S.A.) (John Hancock USA) and John Hancock Life Insurance Companyof New York (John Hancock New York) are herein collectively referred to as “John Hancock”.

P 17324-WEL-G

E 07/10-17324

What is a qualified retirement plan?A qualified retirement plan is a powerful savings tool that millions of Americans arecurrently using to help prepare for their retirement.

This plan has been set up by your employer and is being offered to you as a benefit.Typically, employees make pre-tax contributions to their retirement plan accounts throughautomatic deposits from their paychecks. Over time, your savings may grow, helping you prepare for retirement.

Your qualified retirement plan can provide you with a number of savings advantages,such as the potential for reduced taxes, the ability to take advantage of compoundearnings and more. You can read more about the benefits of participating in yourretirement plan in the following pages.

Using this bookletThis guide will walk you step-by-step through how to enroll in your company’sretirement plan.

Getting started is easy. Along the side of this booklet, you’ll notice tabs, labeled 1, 2, 3 and Go! These are the main steps you will follow to enroll:

Step 1: Find out how much money you will need in retirement.

Step 2: Determine how much you will need to contribute.

Step 3: Choose your investment options.

Go!Complete your enrollment form and find answers tofrequently asked questions.

At the end of the booklet, you’ll find two additional sections. The first, called InvestmentOptions, contains details about the investments available to your plan. The other, calledWhat’s Next?, tells you what you can expect after enrollment, includes tips on investingand introduces you to online tools that can help you prepare for retirement.

Step 1How much do I need?

Learn about the benefits of participating and find retirement profiles to help you picture your retirement lifestyle.

Step 2How much do I need to contribute?

Discover potential sources of retirement income, how to calculate your contributions and find tips to help you save more.

Step 3How should I invest my retirement savings?

Learn about the fundamentals of investing and your personal tolerance for investment risk before choosing your investment options.

Go!Let the saving begin!

Find your enrollment form, an enrollment worksheet, frequently asked questions and important terminology.

Investment OptionsDiscover Fund fact sheets.

Review detailed information on the investmentoptions available under your plan.

What’s Next?What to expect after you enroll.

Discover the benefits of the website, how to read your quarterly statement and how to contact John Hancock.

How much do I need?Everyone hopes for a happy retirement, free from worries aboutmoney. But a financially secure future doesn’t just happen by itself.

A successful retirement requires a bit of foresight and planning. The good news is that there aresome things you can do right now to help put you on the path toward making your retirementdreams a reality.

The first step is to figure out how much income you’ll need once you retire. That’s the question we’ll help you answer in this section.

In the pages that follow, you’ll see:

� Why a retirement plan is so important to your future

� The tax advantages that come with your retirement plan

� How easy it can be to save

� Profiles of a cross section of Americans who are saving for retirement to help give you an idea of how much money you might need for yours.

1

Everyone has different ideas of what they want their retirement to be.

What is your life going to be like in retirement?

P 17324-S1-Tab-GE 07/10-17324

These are potential tax

savings that can really add up!

1ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

* Social Security Administration, Social Security Basic Facts, 2009

**Withdrawals of taxable amounts will be subject to ordinary income tax (state and local taxes may apply) and, if taken prior to age 591⁄2, a 10% IRS tax penalty may apply.

1 32

P 17324-S1-GE 07/10-17324

Why you need to start saving todayWould it surprise you to learn that a significant portion of your retirement income willneed to come from your personal savings?

Consider the following:

� Social Security currently covers just 40% of the income of retirees.*

� Your savings will need to last for the rest of your life. In 1935, the average lifeexpectancy of a 65-year-old was 121⁄2 years. Today, it’s 18 years.*

� Many experts believe you’ll need to replace 60% to 80% of your current annualincome, adjusted for inflation.*

� Social Security may not be sustainable. By 2016, it’s estimated that Social Securitycould be paying more in benefits than it collects in taxes.*

When you stop and think about it, these are some compelling reasons to participate in your company’s retirement plan.

The benefits of participatingBy participating in your company’s retirement plan, you’ll be able to take greater controlover your financial future. It can also let you take advantage of some attractive benefits.

The potential to pay less in taxesThe more you contribute to your plan, the larger your retirement savings (and tax savings)may be.

� Each dollar you contribute to your retirement plan is taken from your paycheck beforetaxes are applied. This may lower your taxable income. It might even put you in alower tax bracket.

� The earnings on contributions to your plan grow tax-deferred until withdrawn. Andsince you may be in a lower tax bracket in retirement, you might pay less tax when themoney is withdrawn** than if you were taxed today.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!2

P 17324-S1-GE 07/10-17324

Watch your savings grow with compound earningsYou don’t have to pay taxes on your contributions or on the investment income those contributions generate – as long as thefunds remain in your plan. Your contributions and earnings can grow tax-deferred (also known as compounding) until youbegin taking withdrawals. As you can see from the accompanying example, compound earnings can really add up!

Y E A R S

5$33,907

$77,182

$132,412

$202,902

$292,867

$407,688

AC

CU

MU

LA

TIO

N

10 15 20 25 30

If Leslie and John saved $500 a month for 30 years,and earned an average tax-deferred annual return of5%, they would end up with$407,688! Their contributionswould total $180,000. All therest – $227,688 – would becompounded earnings!°

Howard’s taxes would be

HOWARD’S TAXABLE INCOME BEFORE CONTRIBUTING $35,000 $5,308•

ANNUAL PRE-TAX CONTRIBUTIONS ($200 X 12) $2,400

HOWARD’S TAXABLE INCOME AFTER CONTRIBUTING $32,600 $4,708§

Hypothetical mathematical illustration only.

° This example is not intended to represent investment advice. Talk to your financial representative about how this situation may relate to your own. This hypothetical example is forillustrative purposes only. There is no guarantee that the results shown will be achieved or maintained over any time period. This example assumes no withdrawals, does not takeinto account fees associated with investing which, if included, would reduce the account balance, and assumes reinvestment of earnings. Taxes are due upon withdrawal.

Howard now pays $600 less in taxes than he would if hedidn’t contribute to his plan!

See the potential tax savings from contributing

Howard earns an annual income of $35,000 and wants a retirement income of $32,000 ayear. He plans on starting his own small carpentry business when he retires. He is currentlycontributing $200 per month to his qualified retirement plan.

• This hypothetical example is for illustrative purposes only.§ Based on 2009 IRS tax tables.

3ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-S1-GE 07/10-17324

So, how much will I really need?Envision your retirementYou already know the first step to a comfortable retirement is to figure out how much income you’ll need once you leave thework force. The six retirement profiles on the following pages can help you get an idea of the level of income you might need in your retirement.

Each profile shows a different retirement lifestyle, along with the estimated annual retirement income (in today’s dollars) neededto pay for that lifestyle. Choose the profile that best reflects your ideal retirement. Think about the activities you enjoy and howyou envision living in retirement. We’ll show you what it might cost to get there.

Note: While retirement profiles are helpful in planning the necessary contributions for retirement savings, there is no guarantee that any investment strategy will be successful in achieving investment objectives. The profiles assume a planned retirement age of 67, a life expectancy of 86 and investing with a balanced strategy. It also considers married individuals starting at age 49with an average rate of return of 3.5% and single individuals starting at age 30 with an average rate of return of 4%. The rate of return has been adjusted for an inflation rate of 3.1% and also considers the number of years to retirement.

* These MapInfo profiles are for illustrative purposes only, are not intended as financial or investment advice, and are not intended to represent the past or future performance of any investment option. Talk to your financial representative about how this situation may relate to your own.

1 32

Set a goal

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!4

P 17324-S1-GE 07/10-17324

Profile $17,500* – Debbie & Mike Wright� The Wrights have lived and worked in the same small community for years. They don’t plan on moving

when they retire.

� They enjoy a modest, yet comfortable, lifestyle. They’re involved in the community and are careful shoppers.

� In retirement, Debbie and Mike look forward to socializing, going to movies, reading and spending timewith family and friends. They may continue to work to keep busy and supplement their retirement income.

Income from retirement savings§ $2,500

Income from Social Security benefits $15,000

Total annual household income in retirement $17,500

Profile $32,000* – Maria & Tony Sanchez� Maria and Tony are active people who love spending time with family and participating in events for the

organizations they belong to.

� They attend church and share a desire to give back to the community.

� In retirement, Maria and Tony look forward to traveling occasionally, enjoying their hobbies, visiting withfamily and possibly working part-time.

Profile $45,000* – Sherry & Nigel Palmer� The Palmers dream of moving to a retirement community in Florida once they retire.

� They’re disciplined savers and smart shoppers. They’re hoping their good habits will help them live a simple,yet comfortable, life once they retire.

� In retirement, Sherry and Nigel look forward to visiting their kids. They plan on financing their visits byflying during the off-season and making their car last.

Is this you?� Do you like to take occasional trips to

relax or spend time with family?

� Would you like to devote more time toyour favorite organization once you retire?

� Are you looking at retirement as anopportunity to turn a hobby into a part-time business?

Is this you?� Do you take advantage of coupons to

help cut your grocery bills?

� Do you opt for previously-owned carsrather than buying new?

� Are you a disciplined saver?

§ Assumes a current combined annual income of $17,500, existing tax-deferred savings of $10,000 and making a combined monthly contribution of $80.∞ Assumes a current combined annual income of $32,000, existing taxable savings of $21,000 and tax-deferred savings of $15,000, and making a combined monthly contribution of $388. †Assumes a current combined annual income of $45,000, existing taxable savings of $30,000 and tax-deferred savings of $21,000, and making a combined monthly contribution of $755.

Is this you?� Do you enjoy being involved in the

community, vacationing close to home and spending time with family?

� Do you keep a car as long as you can tosave on car payments?

� Do you consider yourself a value shopper?

Income from retirement savings∞ $12,000

Income from Social Security benefits $20,000

Total annual household income in retirement $32,000

Income from retirement savings† $21,000

Income from Social Security benefits $24,000

Total annual household income in retirement $45,000

5ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-S1-GE 07/10-17324

1 32

Profile $62,000* – Alan Browne� In retirement, Alan plans to pursue interests he doesn’t have time for today, like attending sporting

events, dinners out and visiting with friends.

� Alan is a conservative spender and plans to continue to live moderately once he retires.

� In retirement, Alan is looking forward to spending time with friends and completing some homeimprovement projects.

Is this you?� Do you occasionally dine out?

� Do you enjoy leisure activities close to home?

� Do you enjoy attending sporting events?

Profile $90,000* – Grace & Peter Wong� Grace and Peter are busy with their careers and are about to move into their dream home,

where they will continue to live once they retire.

� They want to stay active by working out and playing golf.

� In retirement, they are looking forward to spending more time with family and takingyearly vacations.

Profile $120,000* – Helen & David Burrows� Helen and David enjoy city life – museums, restaurants and theatre. They plan to live in the city when

they retire so they can continue to enjoy these pastimes.

� They have done well financially and enjoy luxuries such as new cars and exotic vacations.

� They are disciplined investors who have a clear idea of how they want to spend their retirement years.

Is this you?� Do you belong to a gym?

� Do you buy a new car every few years?

� Do you occasionally travel?

Is this you?� Do you belong to a golf, tennis or

health club?

� Do you regularly purchase new homefurnishings, automobiles, etc.?

� Do you enjoy traveling every year?

Ω Assumes a current annual income of $62,000, existing taxable savings of $7,000 and tax-deferred savings of $4,000, and making a monthly contribution of $432.≈Assumes a current combined annual income of $90,000, existing taxable savings of $62,000 and tax-deferred savings of $41,000, and making a combined monthly contribution of $2,026.ø Assumes a current combined annual income of $120,000, existing taxable savings of $82,000 and tax-deferred savings of $55,000, and making a combined monthly contribution of $2,896.

Income from retirement savingsΩ $36,000

Income from Social Security benefits $26,000

Total annual household income in retirement $62,000

Income from retirement savings≈ $52,000

Income from Social Security benefits $38,000

Total annual household income in retirement $90,000

Income from retirement savingsø $74,000

Income from Social Security benefits $46,000

Total annual household income in retirement $120,000

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!6

P 17324-S1-GE 07/10-17324

Step 1– RecapBy now, you should have an idea of which retirement profile most closely matches the retirement lifestyle you aspire to. This information will help you decide how much to contribute to reach your goal. You’re one step closer to making yourretirement dreams a reality.

Before we move on to Step 2, here’s a quick recap of what we’ve covered so far:

� A retirement plan is a powerful and important tool for your financial future

� Participating in your company’s retirement plan can translate into benefits such as:

• The potential to pay less in taxes

• The ease and convenience of automatic contributions

• Watching your savings grow with compound earnings

� Setting a retirement goal is an important first step.

Go to the Enrollment Worksheet in the Go! section to make noteof your retirement profile.

Now, let’s move on to Step 2, where you will figure out your

contribution amount.

2Step

How much do I needto contribute?After reviewing Step 1, you should have an idea of the level ofincome you’d like to have in retirement. Now it’s time to figureout how much of your current salary you should contribute toachieve your goal.

In the pages that follow, you’ll see:

� The different sources of retirement income

� How to calculate your contribution amount

� How dollar cost averaging, making small contribution increases and the advantages of starting early can help your retirement savings grow

� Where to find additional dollars to put toward your retirement.

Did you know?

“The average U.S. participant contribution is 6%”. The more you contribute today, the more you’ll have to enjoy in retirement.Source: 2009 PSCA 52nd Annual Survey.

2

P 17324-S2-Tab-GE 07/10-17324

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1 ,2 ,3 , GO!

* Source: Social Security Administration, 2009.+ Assumes you retire at the age when you can begin receiving full Social Security benefits (ranges from 65 to 67, depending on your current age), that you work your

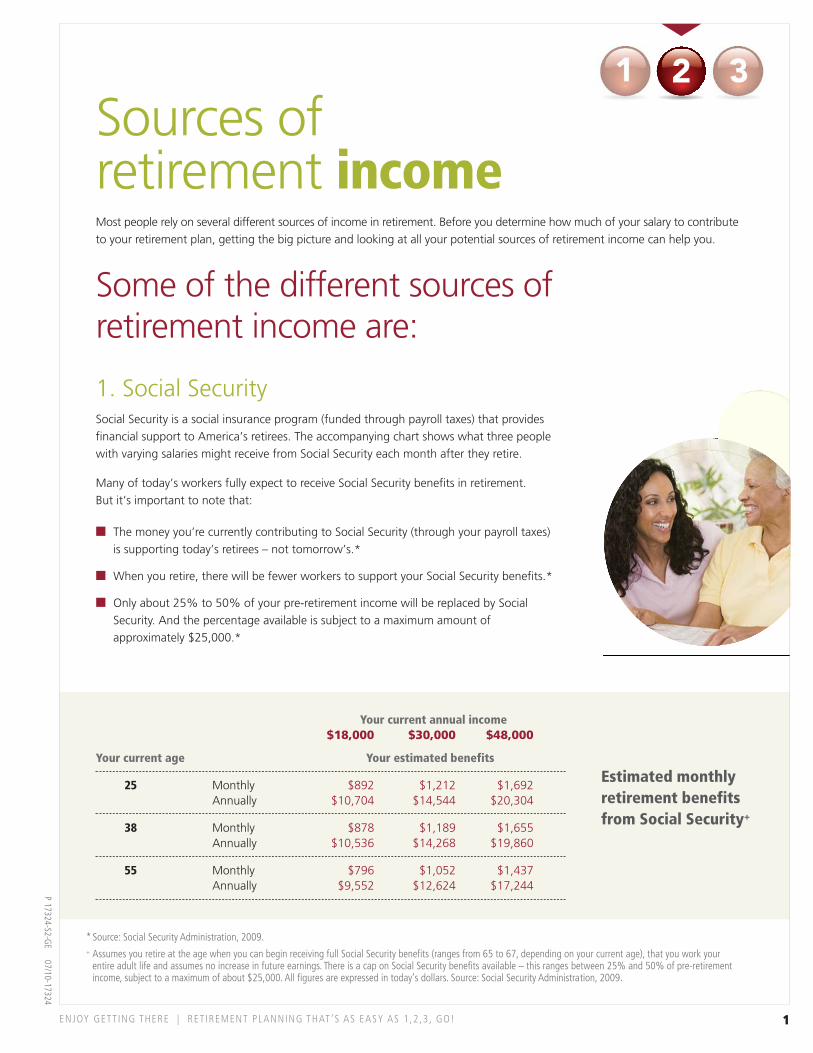

entire adult life and assumes no increase in future earnings. There is a cap on Social Security benefits available – this ranges between 25% and 50% of pre-retirementincome, subject to a maximum of about $25,000. All figures are expressed in today’s dollars. Source: Social Security Administration, 2009.

1 32

Your current annual income $18,000 $30,000 $48,000

Your current age Your estimated benefits

25 Monthly $892 $1,212 $1,692 Annually $10,704 $14,544 $20,304

38 Monthly $878 $1,189 $1,655 Annually $10,536 $14,268 $19,860

55 Monthly $796 $1,052 $1,437 Annually $9,552 $12,624 $17,244

Estimated monthlyretirement benefitsfrom Social Security+

P 17324-S2-GE 07/10-17324

Most people rely on several different sources of income in retirement. Before you determine how much of your salary to contributeto your retirement plan, getting the big picture and looking at all your potential sources of retirement income can help you.

Some of the different sources of retirement income are:

1

Sources of retirement income

1. Social SecuritySocial Security is a social insurance program (funded through payroll taxes) that providesfinancial support to America’s retirees. The accompanying chart shows what three people with varying salaries might receive from Social Security each month after they retire.

Many of today’s workers fully expect to receive Social Security benefits in retirement. But it’s important to note that:

� The money you’re currently contributing to Social Security (through your payroll taxes) is supporting today’s retirees – not tomorrow’s.*

� When you retire, there will be fewer workers to support your Social Security benefits.*

� Only about 25% to 50% of your pre-retirement income will be replaced by SocialSecurity. And the percentage available is subject to a maximum amount ofapproximately $25,000.*

Consider tax-deferred savings limitsWhile you can save as much as you want toward your retirement, you should know there are limits to how much of your savings can be tax-deferred.

For example, the 2010 IRS pre-tax contribution limit is $16,500.

If you are 50 years of age or older, you may be eligible for an additional annual catch-up contribution of $5,500.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!2

P 17324-S2-GE 07/10-17324

2. Personal savingsAre you someone who has been putting away retirement savings over the years in places such as savings accounts and individual retirement accounts? All of thesepersonal savings sources will help contribute toward your total income once you retire.

3. Guaranteed sources of incomeMany Americans have or choose to invest in guaranteed sources of income, such as defined benefit pension plans, annuities and other investments that provide apredictable, steady stream of income on a regular basis. A guaranteed source ofretirement income lets you know how much money you will have coming in eachmonth for the rest of your life.

4. Your company’s qualified retirement planSince you’re reading this booklet, your company is offering you an opportunity toparticipate in its qualified retirement plan. Participating in this plan can be a simple yet effective way for you to save toward your retirement. Learn about a number of significant benefits from participating in this plan. All in all, it’s a simple and practicalway to help you prepare for your retirement.

Want to know what your personal Social Security benefits might look like? Call the Social Security Administration at 1-800-772-1213, or go online atwww.ssa.gov. Don’t forget to check your annual Social Security statement.

3ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-S2-GE 07/10-17324

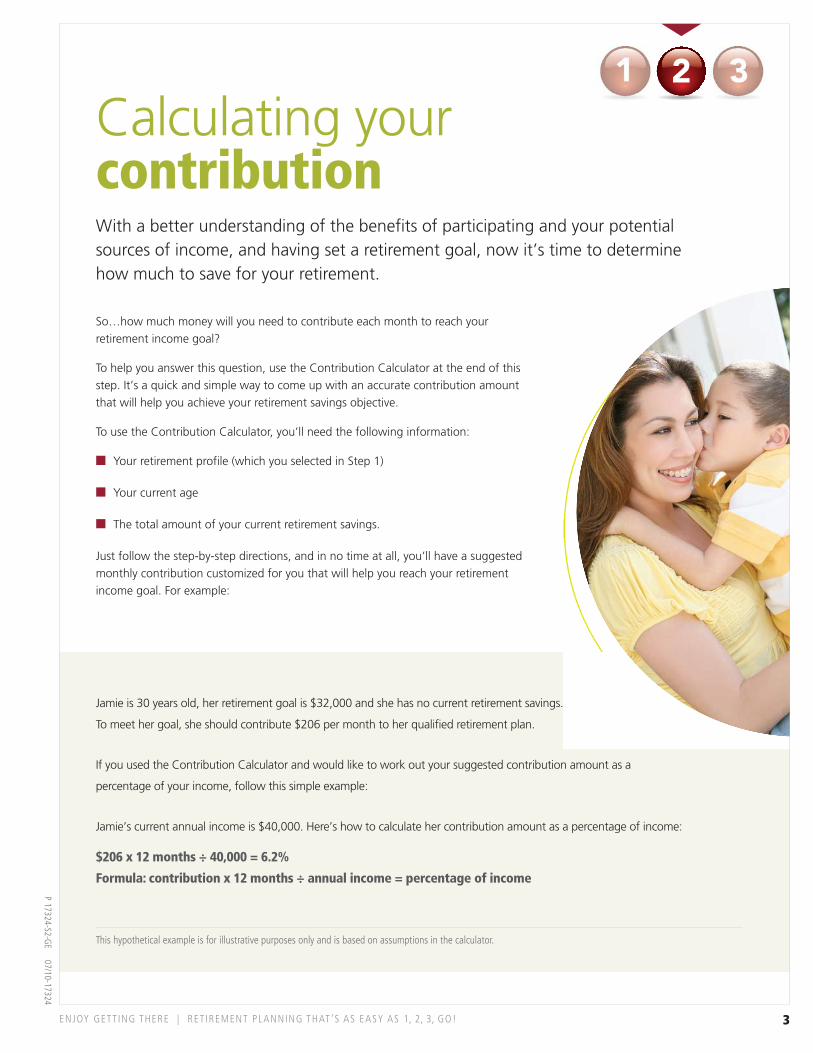

Calculating your contributionWith a better understanding of the benefits of participating and your potentialsources of income, and having set a retirement goal, now it’s time to determinehow much to save for your retirement.

Jamie is 30 years old, her retirement goal is $32,000 and she has no current retirement savings.

To meet her goal, she should contribute $206 per month to her qualified retirement plan.

If you used the Contribution Calculator and would like to work out your suggested contribution amount as a

percentage of your income, follow this simple example:

Jamie’s current annual income is $40,000. Here’s how to calculate her contribution amount as a percentage of income:

$206 x 12 months ÷ 40,000 = 6.2%

Formula: contribution x 12 months ÷ annual income = percentage of income

1 32

So…how much money will you need to contribute each month to reach your retirement income goal?

To help you answer this question, use the Contribution Calculator at the end of thisstep. It’s a quick and simple way to come up with an accurate contribution amountthat will help you achieve your retirement savings objective.

To use the Contribution Calculator, you’ll need the following information:

� Your retirement profile (which you selected in Step 1)

� Your current age

� The total amount of your current retirement savings.

Just follow the step-by-step directions, and in no time at all, you’ll have a suggestedmonthly contribution customized for you that will help you reach your retirementincome goal. For example:

This hypothetical example is for illustrative purposes only and is based on assumptions in the calculator.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!4

P 17324-S2-GE 07/10-17324

This table can be used as a planning tool to helpdetermine your contributionamounts, and shows thelevel of tax savings youmight be able to benefitfrom. Average salary rangesand contribution amountsas a percentage of salaryare also shown. Select yoursalary today, then reviewthe columns to see thecontribution amounts andpotential tax savings.

This table is intended as an educational tool only and represents hypothetical mathematical illustrations only. Calculations are estimates and may not provide accurateprojections. Your actual circumstances, including current income or retirement needs, may vary. Withdrawals of taxable amounts will be subject to ordinary income taxand, if taken prior to age 591⁄2, a 10% IRS tax penalty may apply. This is not intended as investment or legal advice. To determine the actual tax impact of contributionsyou make to your retirement plan, consult your tax advisor.

++ Contribution amounts may include employee and employer contributions made to your company’s qualified retirement plan, as well as deposits to other tax-shelteredand non-tax-sheltered accounts. Contributions to tax-sheltered accounts may not exceed plan or regulatory limits.

## Calculations for those with a salary from $15,000 to $50,000 are based on an individual who is married filing jointly, reporting a taxable income of $62,000 and amarginal tax rate of 15%.

•• Calculations for those with a salary from $60,000 to $80,000 are based on an individual who is married filing jointly, reporting a taxable income of $120,000 and amarginal tax rate of 20%.

Quick Guide: Contribution amounts and potential tax savings

AnnualSalary

% ofAnnualSalary

Pre-tax MonthlyContribution++

Approx. Pre-tax AnnualContribution++

Approx. After-tax AnnualContribution

15%12%9%6%3%

15%12%9%6%3%

15%12%9%6%3%

15%12%9%6%3%

15%12%9%6%3%

15%12%9%6%3%

15%12%9%6%3%

15%12%9%6%3%

$188 $150 $113 $75 $38

$250 $200 $150 $100 $50

$375 $300 $225 $150 $75

$500 $400 $300 $200 $100

$625 $500 $375 $250 $125

$750 $600 $450 $300 $150

$875 $700 $525 $350 $175

$1,000 $800 $600 $400 $200

$161 $129 $97 $65 $32

$215 $172 $129 $86 $43

$323 $258 $194 $129 $65

$430 $344 $258 $172 $86

$538 $430 $323 $215 $108

$600 $480 $360 $240 $120

$700 $560 $420 $280 $140

$800 $640 $480 $320 $160

$2,250 $1,800 $1,350 $900 $450

$3,000 $2,400 $1,800 $1,200 $600

$4,500 $3,600 $2,700 $1,800 $900

$6,000 $4,800 $3,600 $2,400 $1,200

$7,500 $6,000 $4,500 $3,000 $1,500

$9,000 $7,200 $5,400 $3,600 $1,800

$10,500 $8,400 $6,300 $4,200 $2,100

$12,000 $9,600 $7,200 $4,800 $2,400

$1,935##

$1,548 $1,161 $774 $387

$2,580##

$2,064 $1,548 $1,032 $516

$3,870##

$3,096 $2,322 $1,548 $774

$5,160##

$4,128 $3,096 $2,064 $1,032

$6,450##

$5,160 $3,870 $2,580 $1,290

$7,200••

$5,760 $4,320 $2,880 $1,440

$8,400••

$6,720 $5,040 $3,360 $1,680

$9,600••

$7,680 $5,760 $3,840 $1,920

$15,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

Approx. After-tax MonthlyContribution

Approx.Annual TaxSavings

$315 $252 $189 $126 $63

$420 $336 $252 $168 $84

$630 $504 $378 $252 $126

$840 $672 $504 $336 $168

$1,050 $840 $630 $420 $210

$1,800 $1,440 $1,080 $720 $360

$2,100 $1,680 $1,260 $840 $420

$2,400 $1,920 $1,440 $960 $480

5ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

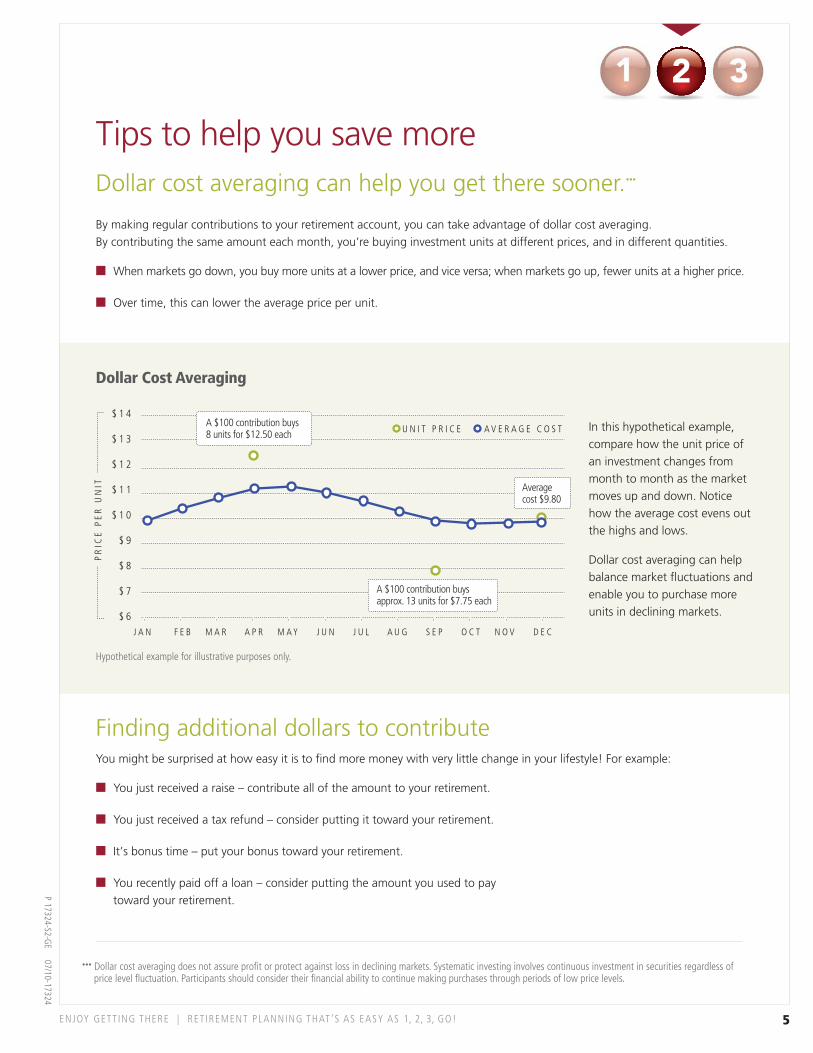

Tips to help you save moreDollar cost averaging can help you get there sooner.•••

By making regular contributions to your retirement account, you can take advantage of dollar cost averaging. By contributing the same amount each month, you’re buying investment units at different prices, and in different quantities.

� When markets go down, you buy more units at a lower price, and vice versa; when markets go up, fewer units at a higher price.

� Over time, this can lower the average price per unit.

••• Dollar cost averaging does not assure profit or protect against loss in declining markets. Systematic investing involves continuous investment in securities regardless ofprice level fluctuation. Participants should consider their financial ability to continue making purchases through periods of low price levels.

Finding additional dollars to contributeYou might be surprised at how easy it is to find more money with very little change in your lifestyle! For example:

� You just received a raise – contribute all of the amount to your retirement.

� You just received a tax refund – consider putting it toward your retirement.

� It’s bonus time – put your bonus toward your retirement.

� You recently paid off a loan – consider putting the amount you used to pay toward your retirement.

1 32

$ 1 4

$ 1 3

$ 1 2

$ 1 1

$ 1 0

$ 9

$ 8

$ 7

$ 6

PR

ICE

PE

R U

NIT

U N I T P R I C E A V E R A G E C O S TA $100 contribution buys 8 units for $12.50 each

A $100 contribution buys approx. 13 units for $7.75 each

Averagecost $9.80

J A N F E B M A R A P R M A Y J U N J U L A U G S E P O C T N O V D E C

Dollar Cost Averaging

In this hypothetical example,compare how the unit price ofan investment changes frommonth to month as the marketmoves up and down. Noticehow the average cost evens outthe highs and lows.

Dollar cost averaging can helpbalance market fluctuations andenable you to purchase moreunits in declining markets.

Hypothetical example for illustrative purposes only.

P 17324-S2-GE 07/10-17324

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!6

P 17324-S2-GE 07/10-17324

A small increase can have a big impactIt’s surprising how making small increases to your monthly contributions can really add up overtime. Let’s see exactly how it works by looking at the examples of John, Rose and Carlos.*

$ 0

$ 5 0 , 0 0 0

$ 1 0 0 , 0 0 0

$ 1 5 0 , 0 0 0

$ 2 0 0 , 0 0 0

$ 2 5 0 , 0 0 0

$ 3 0 0 , 0 0 0

$58,573

John invests$100.00 per month

$117,147

Rose invests$200.00 per month

Carlos invests$300.00 per month

$58,574more!

$117,147 more!

$175,720C O M P O U N D E A R N I N G S

T O T A L C O N T R I B U T I O N S

* Based on a 5% compound interest and monthly contributions over a 25-year period. This example is not intended to represent investment advice. Talk to your financialrepresentative about how this situation may relate to your own. This hypothetical example is for illustrative purposes only. There is no guarantee that the results shownwill be achieved or maintained over any time period. This example assumes no withdrawals, does not take into account fees associated with investing which, if included,would reduce the account balance, and assumes reinvestment of earnings. Taxes are due upon withdrawal.

John decides to invest $100 every month toward hisretirement. At the end of 25 years, he will have a total of$58,573. His actual contributions (shown in green) will total$30,000, while his compound earnings (the money he earnedon his investment, shown in red) will amount to $28,573.

Now, let’s look at Rose. After recently paying off her car loan,Rose decides to use that extra money to increase her totalinvestment to $200 per month. She still has the same amountof disposable income each month. At the end of 25 years,however, Rose will have $117,147. Her actual contributions willtotal $60,000, while her compound earnings will be $57,147.Notice that simply by increasing her monthly investment by$100, Rose retires with $58,574 more than John.

Carlos recently enjoyed a raise in pay and opts to invest ittoward his retirement, bringing his total monthly investment to $300. Carlos is still taking home the same amount of moneyeach month. He may not experience any difference in lifestyle,but at the end of the same 25-year period, Carlos will have$175,720. His actual contributions will total $90,000, while his compound earnings will amount to a whopping $85,720.Simply by putting his raise to work for his future, Carlos retireswith $117,147 more than John and $58,573 more than Rose.

7ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-S2-GE 07/10-17324

1 32

Enjoy the ease and convenience of automaticcontributions

One of the most effective ways to achieve your savings goal is to “pay yourself first”. Withautomatic payroll deductions, your contributions are automatically directed to your retirementplan with each paycheck. It’s easy. It’s convenient. And it works!

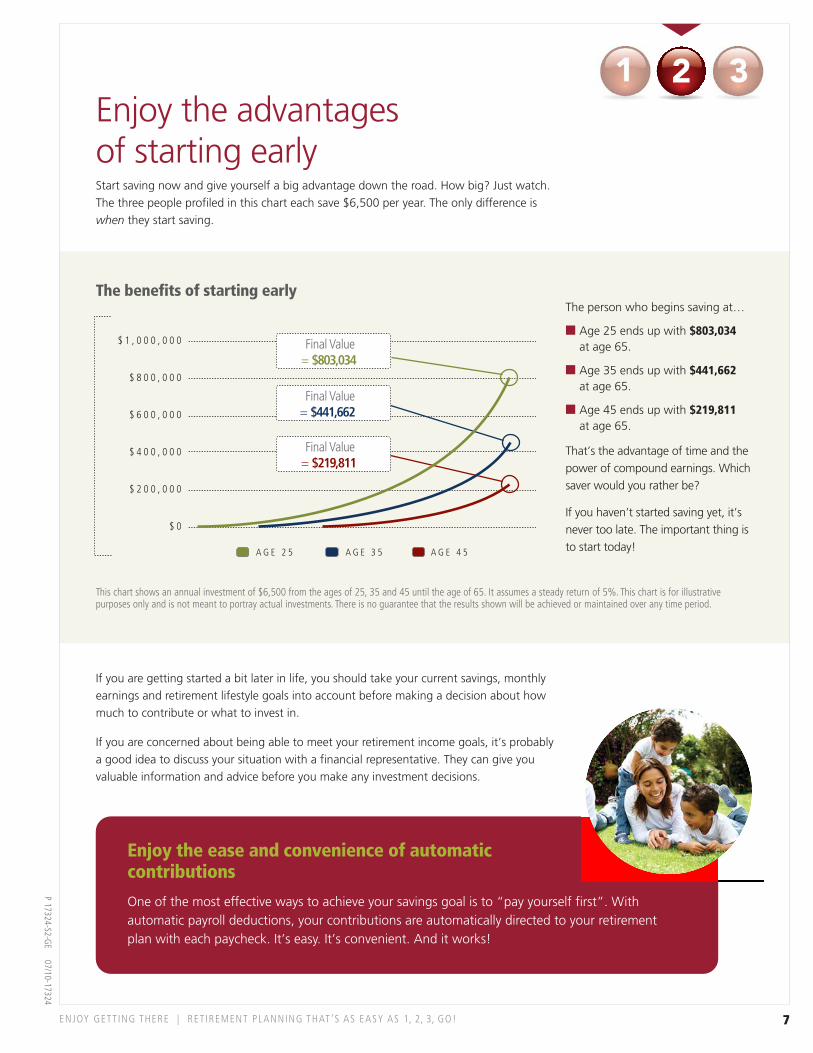

Enjoy the advantages of starting early Start saving now and give yourself a big advantage down the road. How big? Just watch.The three people profiled in this chart each save $6,500 per year. The only difference iswhen they start saving.

This chart shows an annual investment of $6,500 from the ages of 25, 35 and 45 until the age of 65. It assumes a steady return of 5%. This chart is for illustrativepurposes only and is not meant to portray actual investments. There is no guarantee that the results shown will be achieved or maintained over any time period.

A G E 2 5 A G E 3 5 A G E 4 5

$ 1 , 0 0 0 , 0 0 0

$ 8 0 0 , 0 0 0

$ 6 0 0 , 0 0 0

$ 4 0 0 , 0 0 0

$ 2 0 0 , 0 0 0

$ 0

Final Value= $803,034

Final Value= $441,662

Final Value= $219,811

The person who begins saving at…

� Age 25 ends up with $803,034at age 65.

� Age 35 ends up with $441,662at age 65.

� Age 45 ends up with $219,811at age 65.

That’s the advantage of time and thepower of compound earnings. Whichsaver would you rather be?

If you haven’t started saving yet, it’snever too late. The important thing isto start today!

If you are getting started a bit later in life, you should take your current savings, monthlyearnings and retirement lifestyle goals into account before making a decision about howmuch to contribute or what to invest in.

If you are concerned about being able to meet your retirement income goals, it’s probably a good idea to discuss your situation with a financial representative. They can give youvaluable information and advice before you make any investment decisions.

The benefits of starting early

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-S2-GE 07/10-17324

8

Step 2 – RecapNow you have a better idea of how much to contribute to achieveyour retirement income goal.

Before we move on to Step 3, here’s a quick summary of what you covered in Step 2:

� There are several different sources of retirement income you may be able to use to achieveyour goals

� You calculated your personal contribution amount

� Dollar cost averaging and making small increases to your contributions can help strengthenyour retirement savings

� It can be easy to find additional dollars to contribute

� Starting early is best, but it’s never too late to start.

Now that you have an idea of how much to save, go to the EnrollmentWorksheet in the Go! section to make a note of how much you’regoing to contribute.

Now, let’s move on to Step 3, where you’ll choose an investment option.

Click the button to use the calculator

Contribution Calculator

P 17770-CALC-GE 07/10-18107

Note: internet access is required

Use Calculator

3Step

How should I investmy retirement savings?You’re almost there!

In Step 1, you set a goal and determined what level of income you want in retirement. In Step 2, you decided how much of your salary to contribute.Now, in Step 3, it’s time to choose how to invest your contributions.

In the following pages, you’ll learn:

� How the relationship between risk and return can impact your investment strategy

� How diversification can benefit you

� What asset allocation is and why it’s important to your retirement savings

� About different investment types to help decide which might be appropriate for you

� About your personal tolerance for investment risk.

3

What kind of investor are you?

Regardless of your risk tolerance or investment approach,there’s an option that’s right for you.

P 17324-S3-Tab-GE 07/10-17324

The relationship between risk and returnRisk and return are directly related. While most investments entail a risk that you may lose part (or all) of the original moneyyou invested, it’s important to consider the following:

� Historically, investments with greater risk have also offered greater potential for long-term return.

� More conservative investments have lower volatility, but tend to grow more slowly and steadily.

1 5 0 %

1 0 0 %

5 0 %

0 3.7% 5.4% 9.8% 11.9%14.7%

40.4%

5.9%

42.6%54.0%

142.9%

0.0% -14.9% -8.1%

-43.3%-58.0%

L O W R I S K H I G H R I S K

Conservative Moderate Growth & Income Growth Aggressive Growth I N V E S T M E N TS T Y L E :

I N V E S T M E N TV E H I C L E :

30-DayT-Bills

Long-TermGovernment

Long-TermCorporate

S&P500

SmallStocks

RIS

K A

ND

RE

TU

RN

S

This chart shows the historicalrange of returns for differenttypes of investments. As you cansee, history has shown that themore aggressive an investment is,the more volatile it is. A goodrule of thumb is to balance theamount of risk you are willing to assume with an investment’spotential for growth.

†† The performance data shown represents past performance. Past performance is no guarantee of future results and current performance may be lower or higher than theperformance shown. Each bar represents the range of annual returns, along with compound average returns, for each asset class over the period January 1926 – December2009. Average annual rate of inflation over the same time period was 3%. The return and principal value of stocks will fluctuate with changes in market conditions.

Long-term Government bonds are represented by the Ibbotson Associates Long-term Government TR. Long-term Corporate bonds are represented by the Ibbotson AssociatesLong-term Corporate TR. Treasury bills are represented by the U.S. 30 day T-bill TR. Government bonds and treasury bills are guaranteed by the U.S. Government and, if held tomaturity, all bonds offer both a fixed rate of return and fixed principal value. The S&P 500 Stock Index is an unmanaged but commonly used measure of common stock totalreturn performance. Small Cap stocks are represented by the Ibbotson Associates Long-term U.S. Small Stock TR, an unmanaged historic index of U.S. Small Cap stockscompiled by Dimensional Fund Advisors. Small Cap stocks may be subject to a higher degree of market risk than Large Cap or more established companies’ securities. Theliquidity of the Small Cap market may adversely affect the value of an investment so that shares, when redeemed, may be worth more or less than their original cost.

Source: Ibbotson Associates, 2009. Investors may not invest directly in an index.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1 ,2 ,3 , GO!

A few words oninvestingRetirement planning involves understanding investing and how to allocate and diversifyyour investments so that you can better withstand the ups and downs of investing.

While knowing how to invest the dollars in your retirement plan might seem complicatedright now, the choices will become clearer as you go through the terms, ideas andinvestment options outlined in this section.

1 32

Range of returns 1926 – 2009††

P 17324-S3-GE 07/10-17324

KIT351405

1

Hypothetical example for illustrative purposes only.

* Neither asset allocation nor diversification ensures a profit or protection against a loss. Please note that asset allocation may not be appropriate for all participants, particularly those interested in directing investment options on their own.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-S3-GE 07/10-17324

$ 3 0 , 0 0 0

$ 2 0 , 0 0 0

$ 1 0 , 0 0 0

$ 0B O B J A N E T

$30,000 $30,000

I N V E S T M E N T A I N V E S T M E N T B

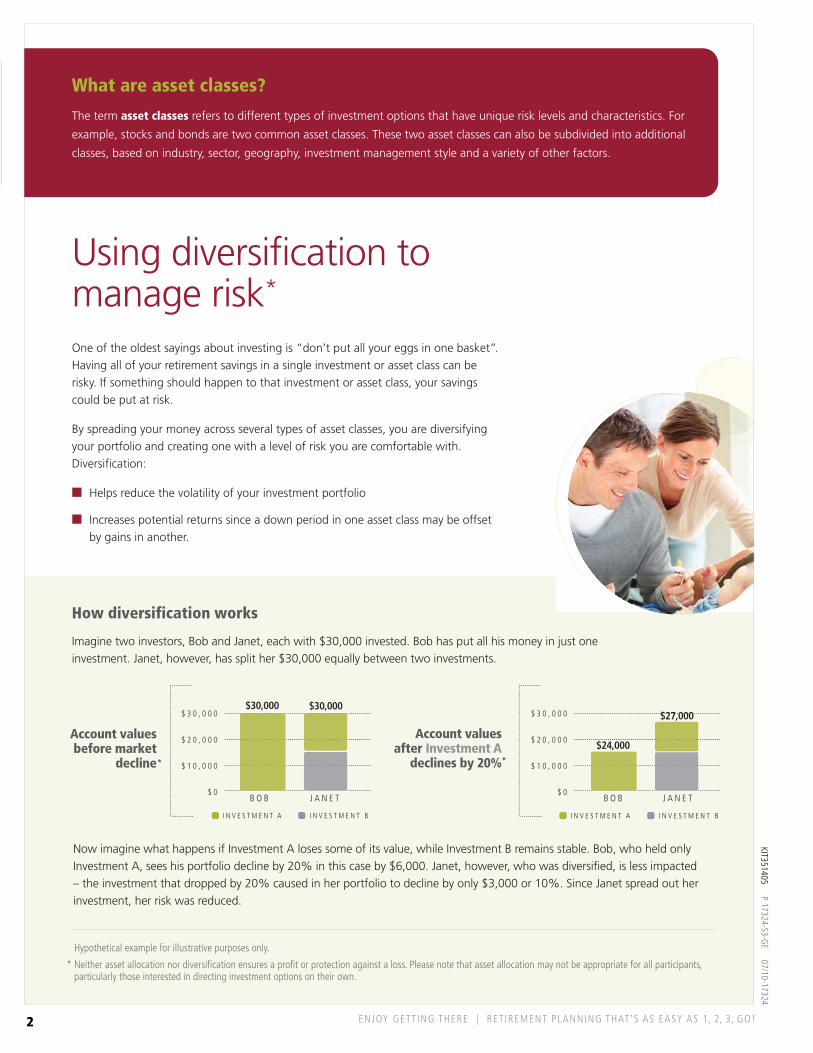

What are asset classes?

The term asset classes refers to different types of investment options that have unique risk levels and characteristics. For

example, stocks and bonds are two common asset classes. These two asset classes can also be subdivided into additional

classes, based on industry, sector, geography, investment management style and a variety of other factors.

Now imagine what happens if Investment A loses some of its value, while Investment B remains stable. Bob, who held onlyInvestment A, sees his portfolio decline by 20% in this case by $6,000. Janet, however, who was diversified, is less impacted – the investment that dropped by 20% caused in her portfolio to decline by only $3,000 or 10%. Since Janet spread out herinvestment, her risk was reduced.

Account valuesbefore market

decline

Using diversification tomanage risk*

One of the oldest sayings about investing is “don’t put all your eggs in one basket”.Having all of your retirement savings in a single investment or asset class can berisky. If something should happen to that investment or asset class, your savingscould be put at risk.

By spreading your money across several types of asset classes, you are diversifying your portfolio and creating one with a level of risk you are comfortable with.Diversification:

� Helps reduce the volatility of your investment portfolio

� Increases potential returns since a down period in one asset class may be offset by gains in another.

$ 3 0 , 0 0 0

$ 2 0 , 0 0 0

$ 1 0 , 0 0 0

$ 0B O B J A N E T

$24,000

$27,000

I N V E S T M E N T A I N V E S T M E N T B

Account valuesafter Investment A

declines by 20%* *

How diversification works

Imagine two investors, Bob and Janet, each with $30,000 invested. Bob has put all his money in just oneinvestment. Janet, however, has split her $30,000 equally between two investments.

KIT351405

2

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-S3-GE 07/10-17324

Achieving diversificationthrough asset allocationAsset allocation is the process of deciding how much of your retirement savings toallocate to different asset classes (such as stock funds, bond funds or money marketfunds). Diversification through asset allocation helps to minimize your risk and maximizeyour returns.

When allocating your money you may want to think about a number of factors, including:

� Your anticipated retirement date

� The length of time you have to save

� Your tolerance for risk.

Through asset allocation you create a diversified portfolio with a level of risk thatyou feel comfortable with. One way to achieve an appropriate balance is to invest in asset allocation funds.

Ways to investIn the following pages, you will learn more about variousinvestment options offered by your company’s plan.

1 32

KIT351405

3

Asset allocation portfolios are "fund of funds" which invests in a number of underlying funds. A Fund's ability to achieve its investment objective will depend largely onthe ability of the subadviser to select the appropriate mix of underlying funds and on the underlying funds' ability to meet their investment objectives. There can be noassurance that either a Fund or the underlying funds will achieve their investment objectives. A Fund is subject to the same risks as the underlying funds in which itinvests. Each Fund invests in underlying funds which invest in fixed-income securities (including in some cases high yield securities) and equity securities, includingforeign securities and engage in Hedging and Other Strategic Transactions. To the extent the Fund invests in these securities directly or engages in Hedging and OtherStrategic Transactions, the Fund will be subject to the same risks. As a Fund's asset mix becomes more conservative, the fund becomes more susceptible to risksassociated with fixed-income securities. For a more complete description of these risks, please review the underlying fund's prospectus, which is available uponrequest.

The revenue John Hancock Retirement Plan Services receives from any of its internally-managed Funds and certain asset allocation portfolios (i.e., the LifestylePortfolios and Guaranteed Income Feature Portfolios) may be higher than those advised or sub-advised exclusively by unaffiliated mutual fund companies. JohnHancock Retirement Plan Services' affiliates provide advisory and sub-advisory services to these internally-managed funds.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-LS-GE 09/10-18143

John Hancock Lifestyle Portfolios∞

Retirement planning based on yourtolerance for riskDo you want to employ an asset allocation strategy based on your individual tolerance forinvestment risk? If so, Lifestyle Portfolios may be for you. They require regular ongoingmonitoring of the investments in your retirement account.

How Lifestyle Portfolios workWith Lifestyle Portfolios, simply determine your level of risk tolerance in order to establishyour investment strategy and style. Then, choose the corresponding Lifestyle Portfoliobased on your risk profile. You should periodically review your risk tolerance.

� Lifestyle Portfolios provide one-step diversification in the form of five color-codedinvestment alternatives that match five distinct risk strategies.

� Each of our Lifestyle Portfolios are carefully divided among a mix of funds under thewatchful eye of our professional fund management team.

� They review and rebalance the mix of the underlying funds for each risk target with a goal of enhancing potential returns and minimizing risk.

Each Lifestyle Portfolio corresponds to aunique risk strategy

∞ Each of the JH Lifestyle Funds invests in a pre-determined mix of underlying Funds. Not all underlying Funds may be available for direct investment through yourqualified retirement plan.

ConservativePortfolio

ModeratePortfolio

BalancedPortfolio

GrowthPortfolio

AggressivePortfolio

DetermineRiskStrategy

SelectLifestylePortfolio

Conservative Moderate Balanced Growth Aggressive

KIT351405

4

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-LS-GE 09/10-18143

Risk and return – the trade-offThe accompanying graph shows the historical trade-off between risk and return for the fivedifferent Lifestyle Portfolios. Over the long term, you would expect a portfolio with greaterrisk to generate a higher level of return.

1 32

To help identify your personal risk tolerance, take our simple six-question Risk Quiz in this booklet. Once you’ve determinedyour comfort level with risk, select the Lifestyle Portfolio option that is right for you. As your risk tolerance may change overtime, retake the Risk Quiz periodically to determine whether you are still in the appropriate Portfolio.

Lifestyle Portfolios may be for you if you want: � To regularly review your investments

� To gain a better understanding of your unique tolerance for risk

� Specialists to adjust and rebalance the Portfolio for you, to maintain its risk target

� A simple choice at enrollment when it comes to allocating your retirement contributions

� To revisit your risk tolerance annually.

L O W E R E X P E C T E D R I S K

EX

PE

CT

ED

RE

TU

RN

H I G H E R

HIG

HE

R

C O N S E R V A T I V E

M O D E R A T E

B A L A N C E D

G R O W T H

A G G R E S S I V E

LO

WE

R

If you think that Lifestyle Portfolios may be for you, take the Risk Quiz andgo to the Investment Options tab for more information on each Portfolio.Then, proceed to the Go! tab and complete the enrollment form.

I N C O M E

G R O W T H & I N C O M E

G R O W T H

A G G R E S S I V E G R O W T H

Investment types

KIT351405

5

Try to include several different types of funds within each risk category to builda properly diversified portfolio mix that matches your overall risk strategy.

The Risk Quiz will help you determine your personal risk tolerance.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

Build Your Own Portfolio MixDo-it-yourself retirement planningAre you the type of person who wants to be actively involved in the research, selection and management of your retirementaccount? If this is the case, constructing your own portfolio mix from the available Funds and handling the asset allocationyourself may be for you.

It is important to start by understanding the relationship between your tolerance for risk and the types of investments that willbe most appropriate. Below is a list of the investment types available. More information about each type is available underImportant Terminology in the Go! section.

Investment types available:� Guaranteed Interest Accounts‡

� Sub-accounts (Funds)‡‡:• Money Market Funds• Bond Funds• Stock Funds.

Although a Money Market Fund seeks to preserve the value of your investment, it is possible to lose money by investing insuch a fund. Not insured by the FDIC, the Federal Reserve Board or any agency.

Contributions to a sub-account – also called a Fund – are pooled with those of other plan participants and are invested in underlying mutual funds. The underlying mutual fundsmay invest in stocks, bonds, money market instruments and other securities. When you invest in a sub-account your contribution purchases units of that Fund. For example, if theunit value is $50 and you contribute $100, then you purchase two units of that Fund. Unit values rise and fall each day and their movements affect the overall value of the Fundand your contributions to that Fund. Sub-accounts include the Lifestyle Portfolios, the Lifecycle Portfolios and other fund options, color-coded to indicate investment risk.

Build Your Own Portfolio Mix may be for you if you want:� To frequently review your investments� To be in control of your asset allocation and construct your own portfolio mix� To handle the ongoing monitoring and rebalancing of your portfolio.

‡ When contributions are allocated to the Guaranteed Interest Account, they will be held in the John Hancock USA general account or John Hancock New York generalaccount, as applicable. Both the principal invested and interest on guaranteed accounts are subject to the claims-paying ability of John Hancock USA or John HancockNew York, as applicable, but are not insured by the FDIC, the Federal Reserve Board or any agency.

‡‡ A sub-account is an account within a separate account established or maintained by an insurance company. John Hancock’s group annuity contracts offer varioussub-accounts. These separate accounts operate apart from and are insulated from the general assets and liabilities of the company. Sub-accounts are not insured by the FDIC, the Federal Reserve Board or any agency and are subject to investment risks, including possible loss of the principal amount invested.

P 17324-BO-G

E 09/10-18143KIT351405

6

Sources: National Association of Theatre Owners, natoonline.org and boxofficemojo.com; Allears.net historical ticket prices; U.S. Department of Commerce, Bureau ofEconomic Analysis, National income and product accounts and U.S. Department of Energy. Prices based on the years 1988, 1993, 1998 and 2008.

1 32

Things to consider when building your own portfolio

1. Determining your risk tolerance and strategy

To create a portfolio that is properly diversified (and with a risk level you are comfortable with), it’s necessary to determine your risk tolerance level. Complete our short Risk Quiz to help you understand your attitudestoward risk and return. Each Fund in our lineup is color-coded to match one of five risk categories. Then,research and select the appropriate funds to create your own portfolio mix.

2. Remember to consider investment and inflation risk

When choosing your investment options, be mindful of two other types of risk that can affect your savings: investment risk and inflation risk.

There are several types of investment risk inherent in different varieties of investments. For example:

Inflation risk refers to the fact that prices go up over time (as shown below). Invest too conservatively and the growth of yourretirement savings may not keep pace with inflation and tax increases.

This chart shows the impact inflation can have on the prices of everything from movie tickets to automobiles.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

P 17324-BO-G

E 09/10-18143

MOVIE T ICKET DISNEYLAND TICKET NEW CAR

20 years ago $4.11 $28.00 $13,932

15 years ago $4.14 $35.00 $16,871

10 years ago $4.69 $42.00 $20,364

Now $7.08 $75.00 $23,098

� Funds that invest in stocks can decline due to market,regulatory or economic developments.

� Foreign securities may carry risks such as currencyfluctuations and changes in political or economic conditions.

� Securities of smaller companies are generally more volatilethan those of larger, more established companies.

� Specific sectors may be more volatile than a broader rangeof industries. They may also be subject to additional risks,such as increased competition or changes in legislation orgovernment regulation affecting the sector.

� Funds investing in high-yield bonds are subject to additionalrisks, such as the increased risk of default.

If you think that Build Your Own Portfolio Mix may be for you, take the Risk Quiz,and then go to the Investment Options tab for more information and to pick yourinvestments. Then, proceed to the Go! tab and complete the enrollment form.

KIT351405

7

Predictable growth year after year.

Every dollar you contribute to this feature up to retirement builds a Benefit Base, which is used to determineyour future income in retirement. Once a year before you retire, the Benefit Base will increase by 3%.1

Greater certainty in retirement.

You will have a source of guaranteed income of up to 5% of your Vested Benefit Base during yourretirement years.

Protection from unpredictable markets.

The Benefit Base will never decline due to market downturns both before and after retirement.

1 The increase is calculated by applying the equivalent daily compounding rate of 3% to the Benefit Base for each day in the 12-month period preceding the anniversarydate. See the How it works section for more information.

Guaranteed Income for Life Select provides dependable income for your retirement yearsthat is protected from market conditions.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

1

3

2

Guaranteed Income for Life SelectRetirement planning that incorporates a guarantee Do you want to have a source of guaranteed income for the rest of your life? If so, thenGuaranteed Income for Life Select may be for you. It can add some certainty to yourretirement planning and help address some of your concerns.

Guaranteed Income for Life Select can give you:

P 17324-GIFLS-G

E 09/10-18143KIT351405

8

Is it right for you?

While having a source of guaranteed retirement income mightsound appealing, there are some important details you shouldconsider before determining whether it is right for you.

The benefits available under Guaranteed Income for Life Select are provided subject to the terms of your company’s qualified retirement plan. Before selecting thisfeature, speak to the plan’s administrator to find out if such benefits are permitted under the terms of your plan. You must meet both the requirements of this featureand of your plan before you can take withdrawals or begin taking retirement income.

2 See the “How it works” section for a definition of terms.3 For more information on the Spousal Option see the “And the benefits continue” section.4 The investment return and principal value of Guaranteed Income for Life Select Funds are not guaranteed and will fluctuate.5 See the “Important Considerations” section for more details.6 This fee can change in accordance with the provisions of your plan’s contract with John Hancock, but will not exceed 1%.

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

Over the next few pages, you’ll find details on the terms and conditions regardingthis feature. Review them carefully before making your enrollment decision.

1 32

� If you are approaching retirement, it is important for you toknow that you must be invested in Guaranteed Income forLife Select for at least five years before you can take income.

� If you are planning on taking early retirement (before age65), your Lifetime Income Amount (LIA) will be set at 4% of the Vested Benefit Base2 instead of 5%. You must be atleast age 591⁄2 to begin taking income.

� If you choose to extend the benefit to include your spouse,your Lifetime Income Amount will be set at 4.5%.3 Both you and your spouse will need to be 65 years old to begintaking income.

� To maximize the benefits of Guaranteed Income for LifeSelect, it is important to regularly invest and not takewithdrawals before retirement. If you are planning on taking a withdrawal or loan, or transferring out money from theGuaranteed Income for Life Select Funds,4 your Benefit Basewill be reduced. Any excess withdrawal after retirement willreduce your LIA.

� You will always have access to the market value of yourinvestments. If your company terminates its contract withJohn Hancock and you do not have a distributable event, youwill lose your guarantees from the feature.5 In some cases,you may receive a refund of the fee for this feature for up tothree years. If you are eligible to receive distributions, youmay roll over your investments in this feature.

� There is an additional annual fee to invest in this feature.This fee is deducted from the market value on a monthlybasis, and is in addition to the expense ratio of the Fundthat you select and other applicable fees. The fee is 0.50% of the Benefit Base6.

P 17324-GIFLS-G

E 09/10-18143KIT351405

9

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

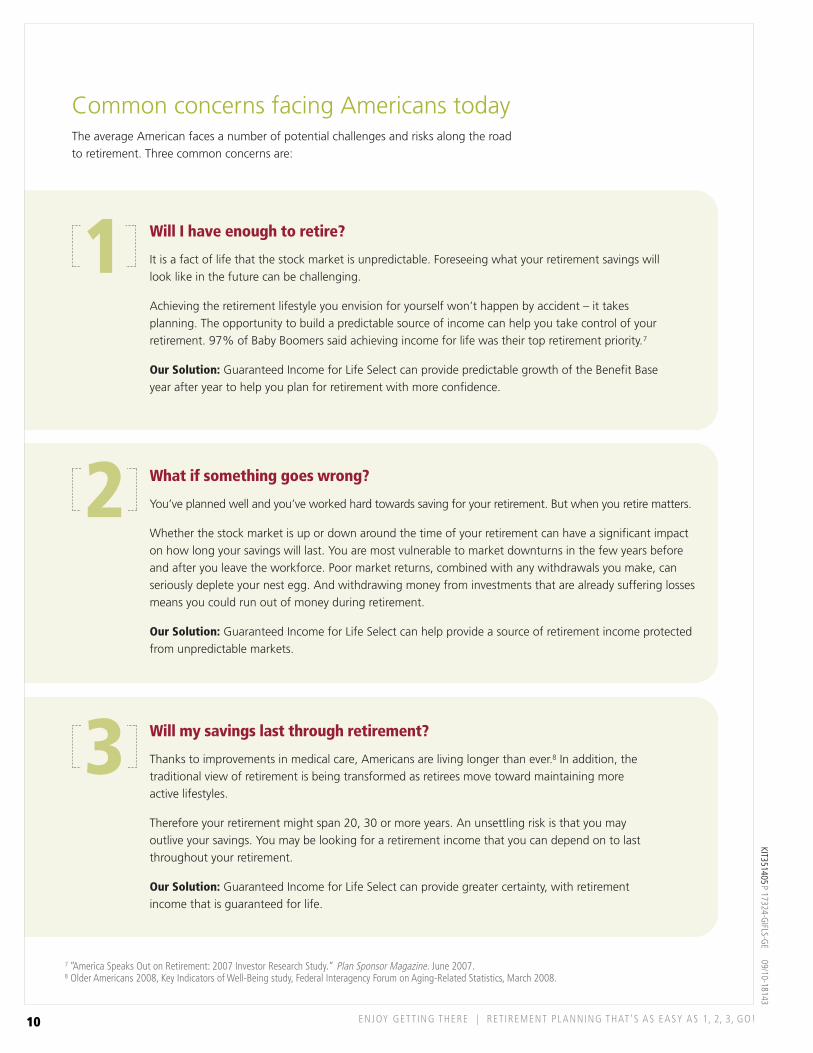

Common concerns facing Americans today The average American faces a number of potential challenges and risks along the road to retirement. Three common concerns are:

7 “America Speaks Out on Retirement: 2007 Investor Research Study.” Plan Sponsor Magazine. June 2007.8 Older Americans 2008, Key Indicators of Well-Being study, Federal Interagency Forum on Aging-Related Statistics, March 2008.

What if something goes wrong?

You’ve planned well and you’ve worked hard towards saving for your retirement. But when you retire matters.

Whether the stock market is up or down around the time of your retirement can have a significant impacton how long your savings will last. You are most vulnerable to market downturns in the few years beforeand after you leave the workforce. Poor market returns, combined with any withdrawals you make, canseriously deplete your nest egg. And withdrawing money from investments that are already suffering lossesmeans you could run out of money during retirement.

Our Solution: Guaranteed Income for Life Select can help provide a source of retirement income protectedfrom unpredictable markets.

Will my savings last through retirement?

Thanks to improvements in medical care, Americans are living longer than ever.8 In addition, thetraditional view of retirement is being transformed as retirees move toward maintaining moreactive lifestyles.

Therefore your retirement might span 20, 30 or more years. An unsettling risk is that you mayoutlive your savings. You may be looking for a retirement income that you can depend on to lastthroughout your retirement.

Our Solution: Guaranteed Income for Life Select can provide greater certainty, with retirementincome that is guaranteed for life.

Will I have enough to retire?

It is a fact of life that the stock market is unpredictable. Foreseeing what your retirement savings willlook like in the future can be challenging.

Achieving the retirement lifestyle you envision for yourself won’t happen by accident – it takesplanning. The opportunity to build a predictable source of income can help you take control of yourretirement. 97% of Baby Boomers said achieving income for life was their top retirement priority.7

Our Solution: Guaranteed Income for Life Select can provide predictable growth of the Benefit Baseyear after year to help you plan for retirement with more confidence.

1

3

2

P 17324-GIFLS-G

E 09/10-18143KIT351405

10

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

How it worksGuaranteed Income for Life Select can provide you with benefits when you’recontributing to your retirement account and when you begin withdrawing from yourretirement account.

Finding a dependable source of retirement income

Investing in Guaranteed Income for Life Select is easy, and you can allocate as much or as little of your contributions as you want to this feature. It is a flexible choice that canprovide a guaranteed amount of income that you can count on in retirement.

Every dollar you contribute to Guaranteed Income for Life Select adds to the Benefit Baseuntil retirement.9 While your market value can increase or decrease on a daily basis, theBenefit Base is unaffected by market fluctuations.10 Also, each year before retirement, onthe Anniversary of your first contribution, the Benefit Base will increase by 3%.11

Retirement income that lasts a lifetime

Guaranteed Income for Life Select will provide you with a steady, predictable source ofincome every year, beginning on the day you are eligible to retire and choose to starttaking income, and lasting as long as you live.

When you decide to retire, the Vested Benefit Base is used to determine the LifetimeIncome Amount (LIA).12 If the vested portion of the market value of your investments inthe Guaranteed Income for Life Select Funds is higher than the Vested Benefit Base whenyou retire, the Vested Benefit Base will increase to match the market value. This meansthat the LIA is set at a higher amount. Note: Once the LIA is set, you can no longer makeadditional contributions to Guaranteed Income for Life Select.

If you take early retirement (after age 59½, but before 65), the LIA is set at 4% of theVested Benefit Base. However, if you retire at age 65, your LIA is set at 5%.

For example: Vested Benefit Base = $100,000 LIA = $5,000 (5%) every year for life

Before you start taking income:

� You must have been invested in Guaranteed Income for Life Select for at least five years13

� You must be at least age 59½.

9 The maximum Benefit Base is $5,000,000.00.10 The Benefit Base will be reduced if you take withdrawals, loans or transfer money out of this feature.11 The increase is calculated by applying the equivalent daily compounding rate of 3% to the Benefit Base for each day in the 12-month period preceding the Anniversary.

The Benefit Base is adjusted for such increase only once a year on the Anniversary. If the Benefit Base is reduced to zero at any time prior to an Anniversary, any interestaccrued after the most recent Anniversary will be forfeited.

12 Before establishing the LIA, you should consult your plan administrator to determine the vested percentage of the Benefit Base and how that will affect the amount of the LIA.13 This reset is waived for any contributions or transfers in during the first 120 days after your first contribution to Guaranteed Income for Life Select. However, this minimum

holding period will extend for five more years if your total contributions (other than regular contributions or regular loan repayments) to this option in any 365 day period exceed 20% of your Benefit Base.

1 32

P 17324-GIFLS-G

E 09/10-18143KIT351405

11

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

Protection from declining markets

A G E

B E N E F I T B A S E M A R K E T V A L U E

5 9 6 0 6 1 6 2 6 3 6 4 6 5 6 6 6 7 6 8 6 9

VA

LU

E (

$)

Lifetime Income set at 5% of Benefit Base

G U A R A N T E E D L I F E T I M E I N C O M E

RE

TIR

EM

EN

T

Hypothetical example for illustrative purposes only.

Jim is six years from retiring, and concerned about not being able to recover if markets fall. He opted for Guaranteed Income forLife Select because every dollar he contributes builds the Benefit Base before retirement.14 Since the value of the Benefit Base isnot impacted by the markets, he is more confident investing in the market. In fact, the Benefit Base is guaranteed to increaseeach year. Jim can accurately predict his minimum Lifetime Income Amount, since he knows the Benefit Base will grow 3% eachyear before retirement.

When he retires at age 65, the Lifetime Income Amount is set at 5% of the Vested Benefit Base. He’s not concerned aboutpoor markets, since he knows he can withdraw the Lifetime Income Amount each year, no matter how long he lives, evenafter his account balance has dropped to zero. Guaranteed Income for Life Select allowed him to participate in the marketswhile not leaving his entire retirement to chance.

DefinitionsThe Benefit Base is the sum of all contributions and transfers to Guaranteed Income for Life Select, reduced bywithdrawals, transfers and loans before retirement. It is completely independent of the actual market value of yourinvestments in this feature; it has no cash value and cannot be withdrawn.

The Market Value is the amount your investments are worth if cashed out at a particular point in time. Your marketvalue changes as the market goes up and down.

P 17324-GIFLS-G

E 09/10-18143KIT351405

12

ENJOY GETTING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

14 Reduced by withdrawals, loans and transfers from this feature.

Participation in strong markets

G U A R A N T E E D L I F E T I M E I N C O M E

RE

TIR

EM

EN

T

A G E

B E N E F I T B A S E M A R K E T V A L U E

4 9 5 1 5 3 5 5 5 7 5 9 6 1 6 3 6 5 6 7 6 9

VA

LU

E (

$)

Lifetime Income set at 5% of Benefit Base

Hypothetical example for illustrative purposes only.

Julie is a conservative investor and, given recent market events, is less comfortable investing in the markets. She choseGuaranteed Income for Life Select and contributed regularly. Since the Benefit Base is guaranteed never to decline due to poormarkets, it will never be less than what she contributes.14 Plus, the Benefit Base will grow 3% each year before retirement.

When Julie retires at age 65, if the market value is higher than the Benefit Base, the Benefit Base is set to equal her marketvalue. The Lifetime Income Amount will then be set at 5% of this elevated Vested Benefit Base for as long as she lives.Although her minimum scenario was 3% growth, Julie benefited from being invested in the markets, while never risking theBenefit Base.

1 32

DefinitionsThe Lifetime Income Amount (LIA) is the amount that you can withdraw every year in retirement regardless of marketconditions – guaranteed. It is available to you when you are eligible to retire and have set the LIA.

The Vested Benefit Base is the portion of the Benefit Base comprised of all employee contributions and employercontributions that you have allocated to this feature and in which you are vested in accordance with the vestingschedule of your retirement plan. Your plan administrator will be able to provide details on the vesting schedule foryour retirement plan. It has no cash value and cannot be withdrawn.

P 17324-GIFLS-G

E 10/10-181511

Benefit Base grows

KIT351405

13

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

And the benefits continueIn addition to predictable growth and guaranteed income in retirement, this simplefeature provides a wide range of other benefits.

You’re in controlYou can choose from a range of professionally managed asset allocation investment options15 with this feature. Once you meet the retirement criteria, you choose:

� When to retire

� How much of the LIA to withdraw each year.

However, any unused portion cannot be carried over to the next year and any excess taken will result in adecreased Benefit Base and the LIA will be recalculated. (See “Important considerations”).

The ability to transfer moneyinto this featureIf you have money in other qualified retirement plans, youcan transfer a limited amount of money into GuaranteedIncome for Life Select at any time before retirement, as long as your plan permits. In some instances this may result in a reset of your minimum holding period.16 If your totalcontributions (other than regular contributions or regular loanrepayments) to this feature in any 365-day period exceed20% of the Benefit Base, your minimum holding period willreset to five years. (See “Important considerations”).

The Spousal Option17

If you are married, the spousal option allows you to extendthe lifetime income guarantee to cover both you and yourspouse. However, the LIA is reduced to 4.5% of the VestedBenefit Base. You may elect the spousal option only:

� At the time the LIA is set,

� When you and your spouse are at least age 65, and

� Where your spouse is your sole beneficiary under yourretirement plan.

Once you elect this option you cannot change this election.You should consult a tax adviser to discuss your situation.

A choice of investments You can invest in a broad choice of diversified18 professionallymanaged asset allocation portfolios with Guaranteed Incomefor Life Select. Simply determine your risk tolerance level tohelp select the appropriate fund for you.

15 The revenue John Hancock receives from any of its internally-managed Funds, and certain asset allocation portfolios (i.e., GIFL Select Funds) may be higher than those advisedor sub-advised exclusively by unaffiliated mutual fund companies. John Hancock’s affiliates provide advisory and sub-advisory services to these internally-managed funds.

16 You have to wait five years from the date of the transfer before you can take income. However, this reset is waived for any transfers in during the first 120 days after your firstcontribution to this feature.

17 For purposes of the Spousal Option, the term “spouse” is determined in accordance with the provisions of your company’s retirement plan. Note that the federal Defense ofMarriage Act (“DOMA”) defines “marriage” as a “legal union between one man and one woman as husband and wife”, and “spouse” as “a person of the opposite sex whois a husband or a wife”. DOMA applies in determining the meaning of any federal legislation, including federal tax law. Accordingly, a person who is considered a spouseunder an employer’s plan but who does not satisfy the definition of a “spouse” under DOMA will not be eligible for the favorable income-deferral options or treatmentotherwise available under federal tax law for spouses who satisfy such definition. You are strongly advised to discuss your situation with a tax advisor before selectingGuaranteed Income for Life Select.

18 Diversification does not guarantee a profit or assure against a loss. There is no guarantee that an investment strategy will achieve its objective.

P 17324-GIFLS-G

E 09/10-18143KIT351405

14

ENJOY GETT ING THERE | RET IREMENT PLANNING THAT’S AS EASY AS 1, 2, 3, GO!

1 32

Leaving Guaranteed Income for Life SelectIf your company terminates its contract withJohn Hancock

If you are not eligible to receive distributions, you forfeit anybenefits in connection with Guaranteed Income for LifeSelect, but we will refund the fees you paid for up to threeyears prior to the contract termination date.

If you are eligible to receive distributions under your plan, you may roll over the market value of your investments inthis feature (and, if applicable, the Vested Benefit Base andLIA) to an available eligible John Hancock investmentvehicle19 and maintain your guarantees.

If you are eligible to receive distributions and choose not toroll over to an eligible John Hancock investment vehicle, youwill not receive a fee refund.

If your company terminates GuaranteedIncome for Life Select

If you are eligible to receive distributions under your plan, you may rollover the market value of your investments in thisfeature (and, if applicable, the Vested Benefit Base and LIA)to an available eligible John Hancock investment vehicle19

and maintain your guarantees.

If you are not eligible to receive distributions, you are entitled to the market value of your investments in this feature. The Benefit Base and LIA will be reduced to zero as of thetermination date.

If you leave your job

Should you change your job and you are eligible to receivedistributions, you may roll over the market value of youraccount (and, if applicable, the Vested Benefit Base and LIA) to an eligible John Hancock investment vehicle and maintainyour guarantees.19

If you choose to cancel Guaranteed Income for Life Select