Download - Vietnam Pharmaceutical Industry

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 1/28

www.VPBS.com.vn Page |

INDUSTRY COVERAGE

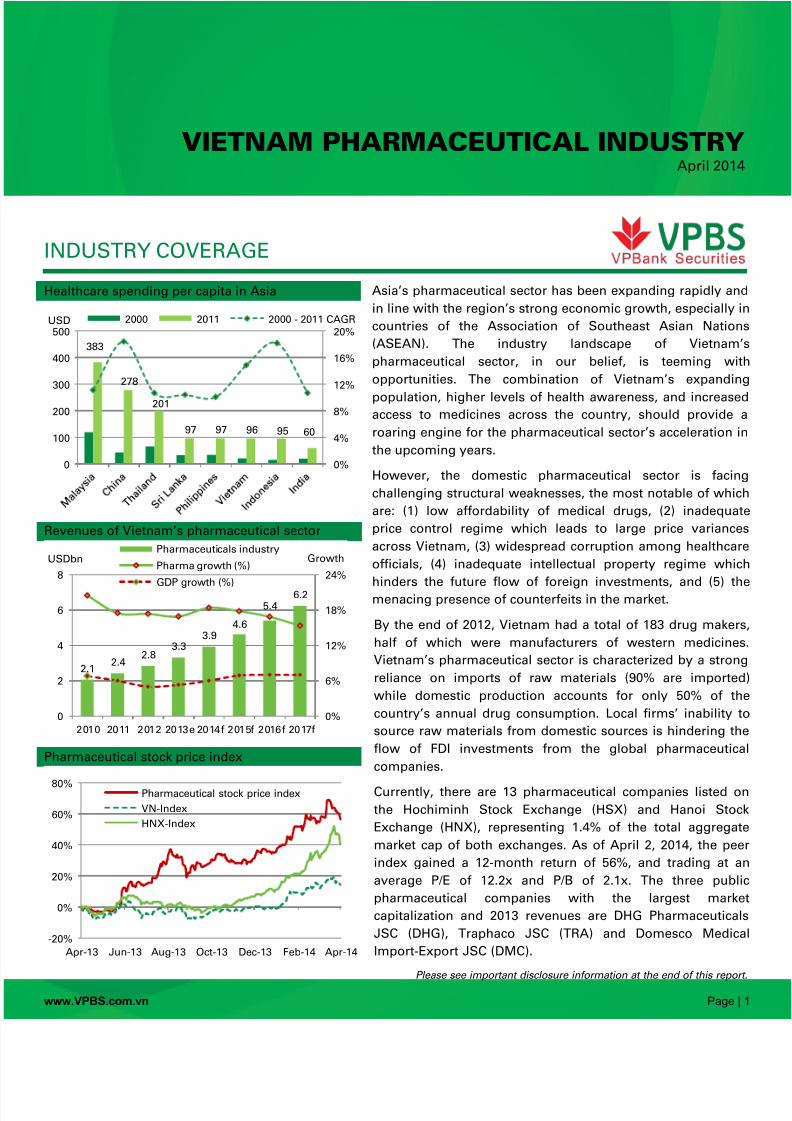

Healthcare spending per capita in Asia Asia’s pharmaceutical sector has been expanding rapidly an

in line with the region’s strong economic growth, especially i

countries of the Association of Southeast Asian Nation

(ASEAN). The industry landscape of Vietnam

pharmaceutical sector, in our belief, is teeming wit

opportunities. The combination of Vietnam’s expandin

population, higher levels of health awareness, and increase

access to medicines across the country, should provide

roaring engine for the pharmaceutical sector’s acceleration i

the upcoming years.

However, the domestic pharmaceutical sector is facin

challenging structural weaknesses, the most notable of whic

are: (1) low affordability of medical drugs, (2) inadequat

price control regime which leads to large price variance

across Vietnam, (3) widespread corruption among healthcar

officials, (4) inadequate intellectual property regime whic

hinders the future flow of foreign investments, and (5) th

menacing presence of counterfeits in the market.

By the end of 2012, Vietnam had a total of 183 drug maker

half of which were manufacturers of western medicines

Vietnam’s pharmaceutical sector is characterized by a stron

reliance on imports of raw materials (90% are imported

while domestic production accounts for only 50% of th

country’s annual drug consumption. Local firms’ inability t

source raw materials from domestic sources is hindering th

flow of FDI investments from the global pharmaceutica

companies.

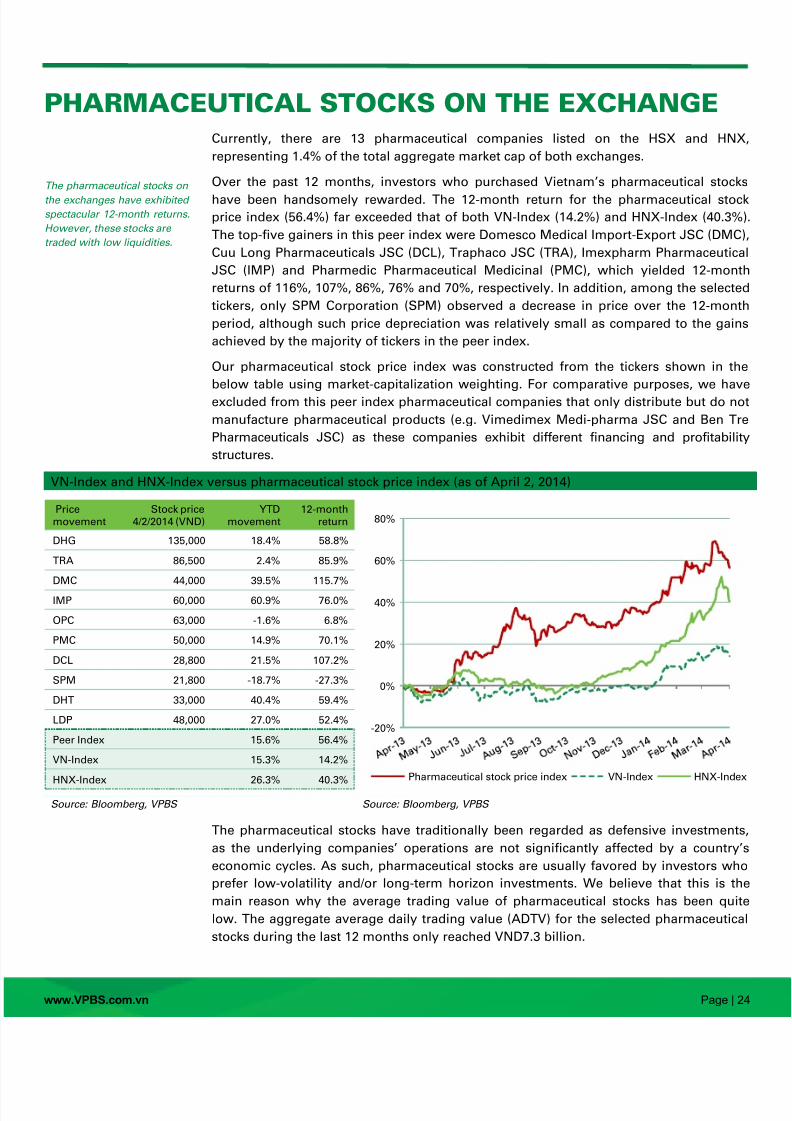

Currently, there are 13 pharmaceutical companies listed o

the Hochiminh Stock Exchange (HSX) and Hanoi Stoc

Exchange (HNX), representing 1.4% of the total aggregat

market cap of both exchanges. As of April 2, 2014, the pee

index gained a 12-month return of 56%, and trading at a

average P/E of 12.2x and P/B of 2.1x. The three publ

pharmaceutical companies with the largest marke

capitalization and 2013 revenues are DHG Pharmaceutica

JSC (DHG), Traphaco JSC (TRA) and Domesco Medica

Import-Export JSC (DMC).

Please see important disclosure information at the end of this repo

Revenues of Vietnam’s pharmaceutical sector

Pharmaceutical stock price index

383

278

201

97 97 96 95 60

0%

4%

8%

12%

16%

20%

0

100

200

300

400

500USD 2000 2011 2000 - 2011 CAGR

2.12.4

2.83.3

3.94.6

5.46.2

0%

6%

12%

18%

24%

0

2

4

6

8

2010 2011 2012 2013e 2014f 2015f 2016f 2017f

GrowthUSDbnPharmaceuticals industry

Pharma growth (%)

GDP growth (%)

-20%

0%

20%

40%

60%

80%

Apr-13 Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14

Pharmaceutical stock price index

VN-Index

HNX-Index

VIETNAM PHARMACEUTICAL INDUSTRYApril 2014

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 2/28

www.VPBS.com.vn Page |

CONTENTS

“PHARMERGING” – THE NEW GLOBAL TREND ...........................................................................................................

PHARMACEUTICAL TRENDS IN ASIAN MARKETS ........................................................................................................

VIETNAM PHARMACEUTICAL INDUSTRY .....................................................................................................................

KEY INDUSTRY PLAYERS ....................................................................................................................................................

VALUE CHAIN...................................................................................................................................................................... 1

Raw materials: 90% are imported ................................................................................................................................. 1

Domestic medicines: an uphill battle against imported products .............................................................................. 1

Distribution channel: of maze and matrix .................................................................................................................... 1

Pharmaceutical advertising ............................................................................................................................................ 2

LEGAL FRAMEWORK ......................................................................................................................................................... 2

Regulatory bodies ........................................................................................................................................................... 2

Intellectual property protection ..................................................................................................................................... 2

Trans-Pacific Partnership ............................................................................................................................................... 2

Government’s master plans ........................................................................................................................................... 2

PHARMACEUTICAL STOCKS ON THE EXCHANGE ................................................................................................... 2

CONCLUSION ....................................................................................................................................................................... 2

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 3/28

www.VPBS.com.vn Page |

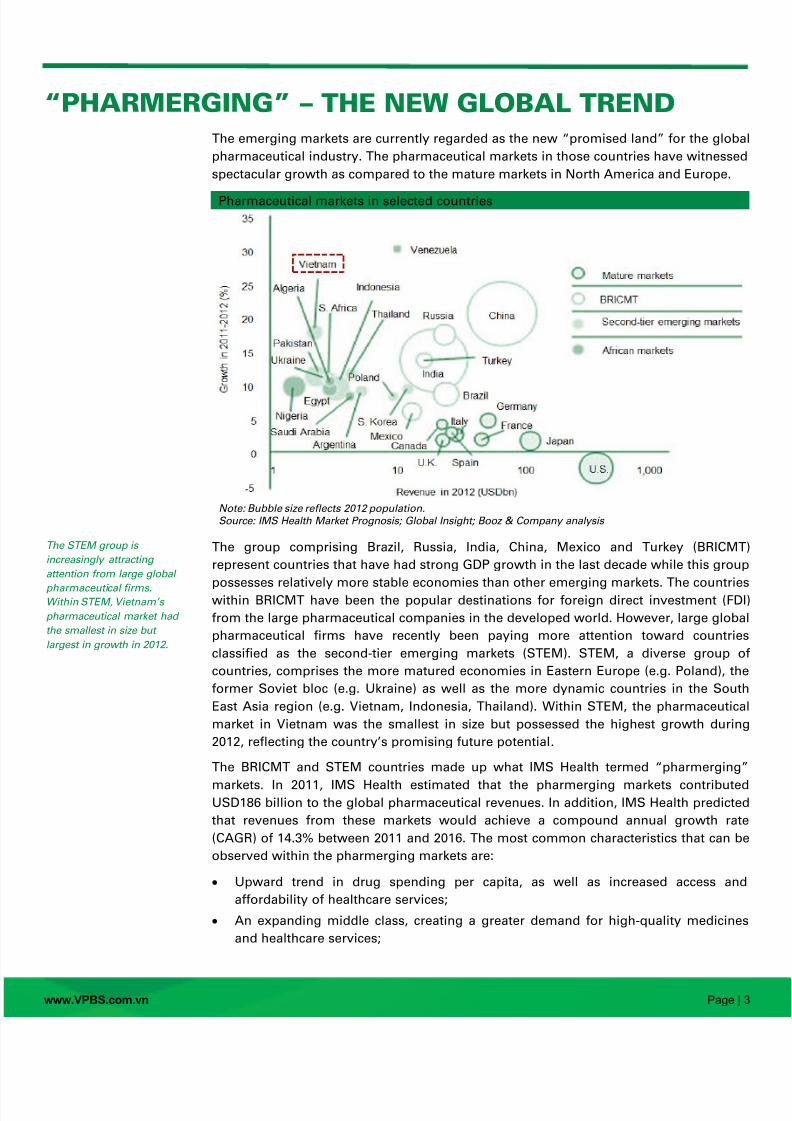

“PHARMERGING” – THE NEW GLOBAL TRENDThe emerging markets are currently regarded as the new ‚promised land‛ for the globa

pharmaceutical industry. The pharmaceutical markets in those countries have witnesse

spectacular growth as compared to the mature markets in North America and Europe.

Pharmaceutical markets in selected countries

Note: Bubble size reflects 2012 population.Source: IMS Health Market Prognosis; Global Insight; Booz & Company analysis

The group comprising Brazil, Russia, India, China, Mexico and Turkey (BRICMT

represent countries that have had strong GDP growth in the last decade while this grou

possesses relatively more stable economies than other emerging markets. The countrie

within BRICMT have been the popular destinations for foreign direct investment (FD

from the large pharmaceutical companies in the developed world. However, large globa

pharmaceutical firms have recently been paying more attention toward countrie

classified as the second-tier emerging markets (STEM). STEM, a diverse group o

countries, comprises the more matured economies in Eastern Europe (e.g. Poland), th

former Soviet bloc (e.g. Ukraine) as well as the more dynamic countries in the Sout

East Asia region (e.g. Vietnam, Indonesia, Thailand). Within STEM, the pharmaceutica

market in Vietnam was the smallest in size but possessed the highest growth durin

2012, reflecting the country’s promising future potential.

The BRICMT and STEM countries made up what IMS Health termed ‚pharmerging

markets. In 2011, IMS Health estimated that the pharmerging markets contributeUSD186 billion to the global pharmaceutical revenues. In addition, IMS Health predicte

that revenues from these markets would achieve a compound annual growth rat

(CAGR) of 14.3% between 2011 and 2016. The most common characteristics that can b

observed within the pharmerging markets are:

Upward trend in drug spending per capita, as well as increased access an

affordability of healthcare services;

An expanding middle class, creating a greater demand for high-quality medicine

and healthcare services;

The STEM group is

increasingly attracting

attention from large global

pharmaceutical firms.Within STEM, Vietnam’s

pharmaceutical market had

the smallest in size but

largest in growth in 2012.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 4/28

www.VPBS.com.vn Page |

Changing lifestyles that increase the prevalence of cardiovascular and respirator

diseases and cancer;

Improvements in the protection regimes of intellectual properties, although th

speed of improvements varies across countries; and

Government seeking betterments of the public health by making strong investment

into education, infrastructure and healthcare.

Development of disease patterns across the world (% mortality rate)

Source: WHO; Booz & Company analysis

PHARMACEUTICAL TRENDS IN ASIAN MARKETSAsia’s pharmaceutical sector has been expanding rapidly and in line with the region’

strong economic growth and demographic changes, especially in countries belonging t

the Association of Southeast Asian Nations (ASEAN). Several dominant macro trend

such as rising household incomes, increased government expenditure on healthcare

higher life expectancies and consumer health-awareness, have all boosted demands fo

pharmaceutical products in the region. According to the Economist Intelligence Unit (EIU

regional pharmaceutical sales doubled from USD97 billion in 2001 to USD214 billion i

2010, and will reach USD386 billion by 2016, reflecting the 2010 to 2016 CAGR of 10%.

Population growth in Asian countries stems from the combined results of higher birt

rates in some countries, lower infant mortality rates and increased life expectancies

Asian countries that possess lower birth rates, such as China, Japan and Singapore, ar

facing ageing populations, presenting growth opportunities for pharmaceutica

companies to manufacture specialized drugs for the elderly.

The dramatic rise in incomes across Asia over the past ten years has contribute

significantly to the increases in healthcare spending among the regional countrie

About half of Asia still lives in rural areas, but they have greater access to mainstream

medicines and healthcare services, thanks to continual efforts made by both the publ

and private sectors.

Europe

Eastern

Mediterranean

Southeast Asia

The Americas

Africa

Western Pacific

Other

Diabetes mellitus

Respiratory diseases

Injuries

Malignant neoplasms and cancer

Infectious diseases, maternal & perinataconditions, nutritional deficiencies

Cardiovascular diseases

Shift from infectious tocardiovascular diseases

Along with other macro

trends, rise in incomes

across Asia has contributed

significantly to the increase

in healthcare spending within

the regional countries.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 5/28

www.VPBS.com.vn Page |

GNI per capita for selected Asian countries

Source: World Bank

As Asian people have become richer, their diet habits have changed. For instance, th

growing middle class in the region consumes more sweetened food (e.g. candieschocolates) and beverages (e.g. soda, sport drinks). This has led to an increase

prevalence of cardiovascular diseases, cancer and diabetes within the regiona

countries’ populations. Governments in the region have been investing in the healthcar

infrastructure and services in order to alleviate the expenditure burden on household

and adapt to the aforementioned changes in the disease profiles.

Real pharmaceutical spending per capita Healthcare spending per capita (USD)

Source: World Health Organization (WHO) Source: World Health Organization (WHO)

Thanks to the positive macro catalysts mentioned above, Asia has become an attractiv

market for the global pharmaceutical companies. In 2010, the Asia-Pacific regio

accounted for 21% of Bayer AG’s total revenues as compared to only 10% in 1990. I

addition, according to the international data provider fDiMarkets.com, there had bee

653 cross-border investment projects in Asia between 2004 and 2011 worth a total o

USD29 billion, coming from 321 companies in the pharmaceutical (70%) an

biotechnology space (30%). China was the largest recipient with 186 inwar

investments, followed by India (157) and Singapore (94). Global pharmaceutical firm

have been moving into Asian countries in order to lower their production costs and

960 470 7103,540

1,030

20,690

2,000430

5,7201,580

3,420

9,820

2,500

47,210

5,2101,550

19.5%

12.9%

17.0%

10.7%9.3%

8.6%

10.0%

13.7%

0%

5%

10%

15%

20%

25%

0

10,000

20,000

30,000

40,000

50,000

China India Indonesia Malaysia Philippines Singapore Thailand Vietnam

USD 2002 2012 2002 - 2012 CAGR

2% 2%4%

7%

9%9% 10%

12%

0%

3%

6%

9%

12%

15%

383

278

201

97 97 96 9560

0%

4%

8%

12%

16%

20%

0

100

200

300

400

500

2000 2011 2000 - 2011 CAGR2000 – 2009 CAGR

From 2004 to 2011, there

had been 653 cross-border

investment projects flowing

into Asian countries.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 6/28

www.VPBS.com.vn Page |

expand the research and development (R&D) base. R&D accounted for 200 projects o

the 653 cross-border investment projects mentioned above, compared to manufacturin

with 175.

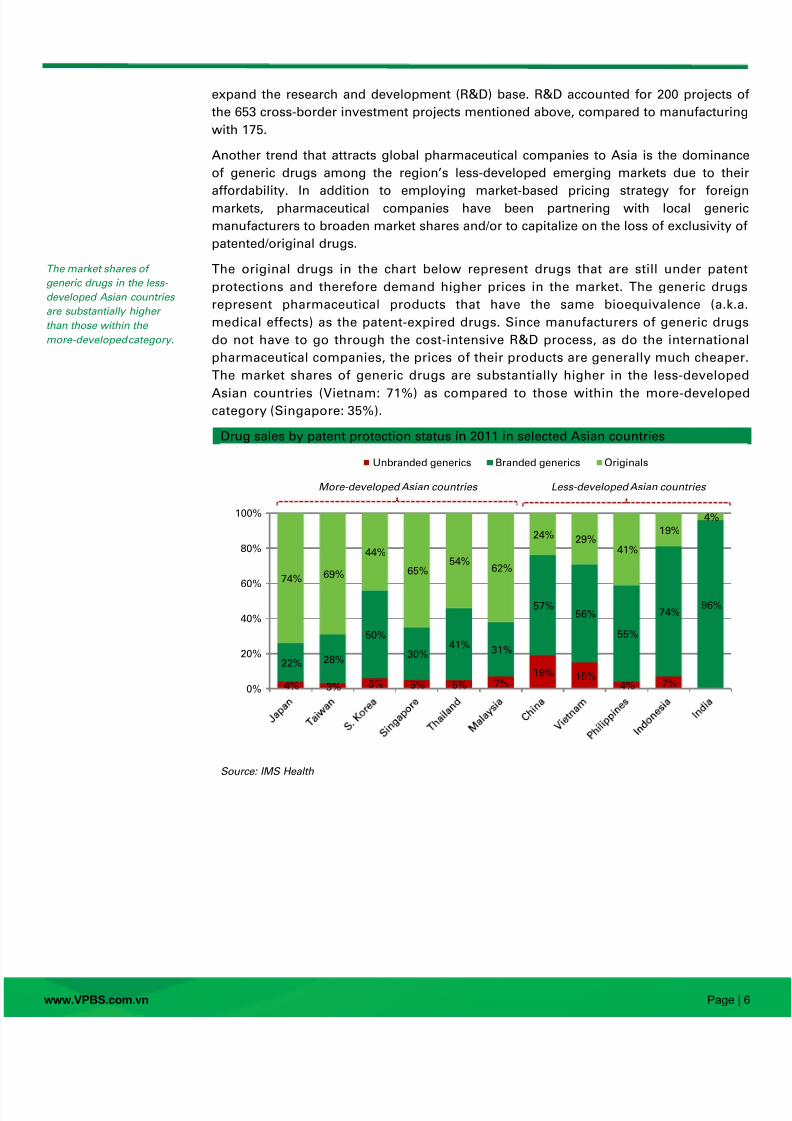

Another trend that attracts global pharmaceutical companies to Asia is the dominanc

of generic drugs among the region’s less-developed emerging markets due to the

affordability. In addition to employing market-based pricing strategy for foreigmarkets, pharmaceutical companies have been partnering with local gener

manufacturers to broaden market shares and/or to capitalize on the loss of exclusivity o

patented/original drugs.

The original drugs in the chart below represent drugs that are still under paten

protections and therefore demand higher prices in the market. The generic drug

represent pharmaceutical products that have the same bioequivalence (a.k.a

medical effects) as the patent-expired drugs. Since manufacturers of generic drug

do not have to go through the cost-intensive R&D process, as do the internationa

pharmaceutical companies, the prices of their products are generally much cheape

The market shares of generic drugs are substantially higher in the less-develope

Asian countries (Vietnam: 71%) as compared to those within the more-developecategory (Singapore: 35%).

Drug sales by patent protection status in 2011 in selected Asian countries

Source: IMS Health

4% 3% 6% 5% 5% 7%19% 15%

4% 7%

22% 28%

50%

30%41%

31%

57%56%

55%

74%96%

74% 69%

44%

65%54%

62%

24% 29%41%

19%

4%

0%

20%

40%

60%

80%

100%

Unbranded generics Branded generics Originals

More-developed Asian countries Less-developed Asian countries

The market shares of

generic drugs in the less-

developed Asian countries

are substantially higher

than those within the

more-developed category.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 7/28

www.VPBS.com.vn Page |

VIETNAM PHARMACEUTICAL INDUSTRY

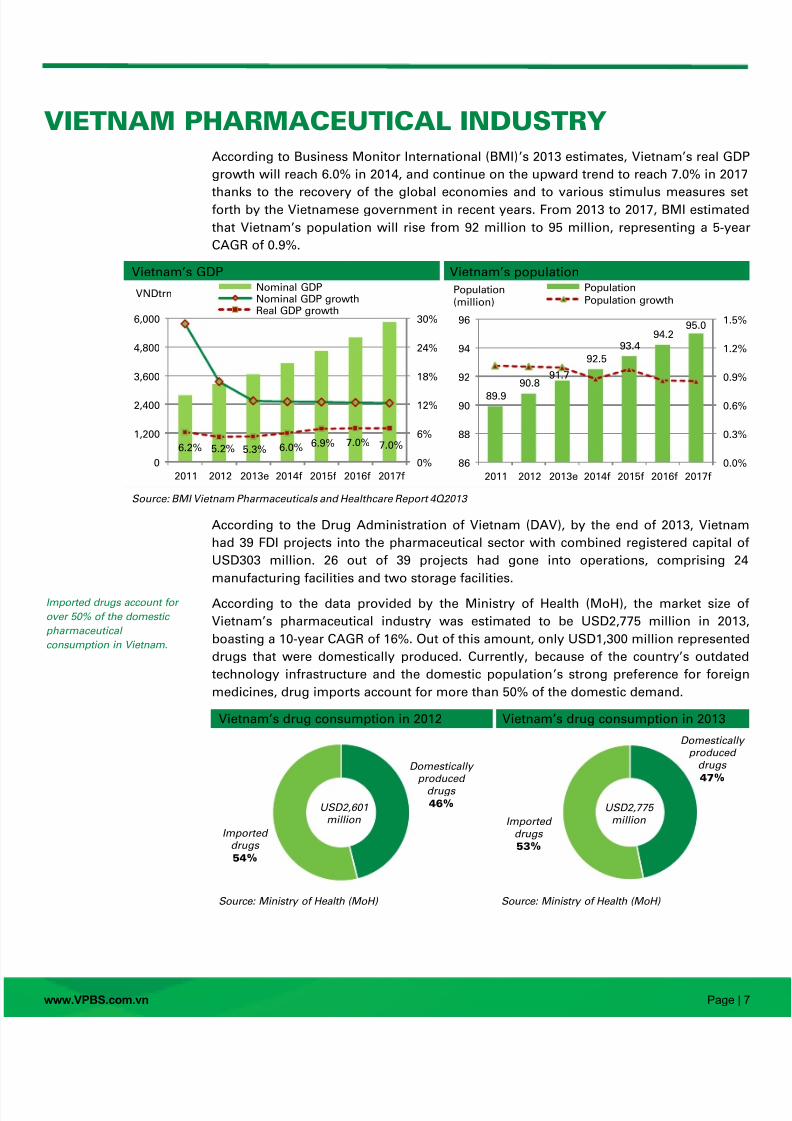

According to Business Monitor International (BMI)’s 2013 estimates, Vietnam’s real GD

growth will reach 6.0% in 2014, and continue on the upward trend to reach 7.0% in 201

thanks to the recovery of the global economies and to various stimulus measures seforth by the Vietnamese government in recent years. From 2013 to 2017, BMI estimate

that Vietnam’s population will rise from 92 million to 95 million, representing a 5-yea

CAGR of 0.9%.

Vietnam’s GDP Vietnam’s population

Source: BMI Vietnam Pharmaceuticals and Healthcare Report 4Q2013

According to the Drug Administration of Vietnam (DAV), by the end of 2013, Vietnam

had 39 FDI projects into the pharmaceutical sector with combined registered capital o

USD303 million. 26 out of 39 projects had gone into operations, comprising 2

manufacturing facilities and two storage facilities.

According to the data provided by the Ministry of Health (MoH), the market size o

Vietnam’s pharmaceutical industry was estimated to be USD2,775 million in 2013

boasting a 10-year CAGR of 16%. Out of this amount, only USD1,300 million represente

drugs that were domestically produced. Currently, because of the country’s outdate

technology infrastructure and the domestic population’s strong pref erence for foreig

medicines, drug imports account for more than 50% of the domestic demand.

Vietnam’s drug consumption in 2012 Vietnam’s drug consumption in 2013

Source: Ministry of Health (MoH) Source: Ministry of Health (MoH)

6.2% 5.2% 5.3% 6.0% 6.9% 7.0% 7.0%

0%

6%

12%

18%

24%

30%

0

1,200

2,400

3,600

4,800

6,000

2011 2012 2013e 2014f 2015f 2016f 2017f

VNDtrnNominal GDPNominal GDP growthReal GDP growth

89.9

90.891.7

92.5

93.494.2

95.0

0.0%

0.3%

0.6%

0.9%

1.2%

1.5%

86

88

90

92

94

96

2011 2012 2013e 2014f 2015f 2016f 2017f

Population(million)

Population

Population growth

Domesticallyproduced

drugs

46%

Importeddrugs

54%

USD2,601million

Domesticallyproduced

drugs

47%

Importeddrugs

53%

USD2,775million

Imported drugs account for

over 50% of the domestic

pharmaceutical

consumption in Vietnam.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 8/28

www.VPBS.com.vn Page |

According to BMI’s research data, the total market size of Vietnam’s pharmaceutica

industry reached USD3,320 million in 2013, up 17% from USD2,840 million in 2012

(These data discrepancies are common in Vietnam, where statistical figures can var

across different governmental agencies.)

Sales of Vietnam’s pharmaceutical industry Vietnam’s pharmaceutical spending per capita

Source: BMI Vietnam Pharmaceuticals and Healthcare Report 4Q2013

We believe that the industry landscape of Vietnam’s pharmaceutical sector is teemin

with potentials. Vietnam’s expanding population, higher levels of health awarenes

among the growing middle class, together with increased access to medicines acros

the country, should provide a roaring engine for the pharmaceutical sector’

acceleration in the upcoming years. Between 2013 and 2017, BMI predicted that th

pharmaceutical sector would achieve a CAGR of 17.1% in sales.

Nevertheless, Vietnam’s pharmaceutical industry is not without its shortcomings an

weaknesses, some more entrenched and enduring than others: Low affordability of medical drugs: Vietnam’s low per capita pharmaceutica

spending (1.9% of GDP per capital in 2013) highlights the country’s poor access t

medical drugs, which is caused by the high prices charged by imported drug

According to the MoH at a conference organized by the DAV in August 2013

imported medicines account for 80% of the total medicines used in hospitals.

Inadequate price-control regime : Medicine cost varies wildly throughout the supp

chain due to the arbitrary price mark-ups by both drug distributors and retail stores

According to a statement by Vietnam’s Health Minister, Ms. Nguyen Thi Kim Tien

there are many instances of the same drugs being sold at significantly differen

prices in various provinces. Not only does this situation erode the affordability o

medicines in various parts of the country, it also severely hurts consumer

confidence in the competence of both the DAV and MOH.

Corruption: There have been numerous accusations regarding the collusion betwee

foreign drug-makers and local distributors in order to keep prices high and doctor

receiving commissions for prescribing certain drugs. Such practices are puttin

medicinal treatments beyond the budgets of many patients in Vietnam. Sinc

August 2012, Vietnam’s social health insurance fund has been running at deficit, i

part due to the mismanagement of funds as well as corruption. In a meetin

organized by the MoH officials in August 2013, it was estimated that the nationa

health insurance fund would face USD47 million in overspending in 2013.

2.12.4

2.83.3

3.9

4.6

5.4

6.2

0%

6%

12%

18%

24%

0

2

4

6

8

2010 2011 2012 2013e 2014f 2015f 2016f 2017f

GrowthUSDbn

Pharmaceuticals industryPharma growth (%)GDP growth (%)

23.127.0

31.236.2

42.4

48.9

55.963.6

0%

5%

10%

15%

20%

0

20

40

60

80

2010 2011 2012 2013e 2014f 2015f 2016f 2017f

GrowthUSDPharmaceuticals spending per capitaGDP growth

While teeming with

opportunities, Vietnam’s

pharmaceutical sector is

hindered by numerous

structural weaknesses.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 9/28

www.VPBS.com.vn Page |

Lack of Intellectual property protection: Since 2004, the Office of the US Trad

Representative (USTR) has been including Vietnam among its list of ‚watch

countries because of Vietnam’s inadequate mechanism for the protection o

intellectual property (IP). According to BMI, a large portion of Vietnam’s gener

drug market actually represents low-quality copies of unproven bioequivalence

Vietnam’s entrance into WTO in 2007 did provide some improvements with th

regard to the country’s intellectual property regimes. That said, without stronge

standards and stricter enforcement, further improvements of Vietnam’s IP protectio

regime will likely come at a very slow pace.

Counterfeit: Counterfeit drugs represent an extremely challenging issue in Vietnam

given the fact that pharmacy distribution in Vietnam is largely handled by privat

dealers. In addition, the country has long and poorly monitored borders wit

neighboring countries such as Laos, China and Cambodia, where the counterfe

drug trade is very active. In February 2010, an arrest warrant was issued for

number of individuals operating under a front company called Viet-Phap (Vietnam

France) Medicine Company. These individuals were indicted for manufacturing an

supplying fake pharmaceutical products.

KEY INDUSTRY PLAYERS

By the end of 2012, Vietnam had 183 drug manufacturers, of which 98 were wester

medicine producers, 80 traditional medicine manufacturers and five vaccine makers

According to BMI’s data, sales of the three largest listed companies in the industry, DH

Pharmaceutical JSC (DHG), Traphaco JSC (TRA), and Domesco Medical Import-Expo

JSC (DMC) accounted for approximately 9% of the total market in 2012.

2012 Revenues of selected pharmaceutical companies in Vietnam

VND in billion Sale PAT

DHG Pharmaceutical JSC* 2,931 491

Traphaco JSC* 1,401 128

Domesco Medical Import-Export JSC* 1,261 90

Mekophar Chemical Pharmaceutical JSC 1,101 70

Pymepharco JSC 1,011 123

Hai Duong PharmaceuticalMedical Materials JSC

859 20

Imexpharm JSC* 818 78

Nam Ha Pharmaceutical JSC 739 12

Ha Tay Pharmaceutical JSC* 677 15

Medipharco-Tenamyd CentralPharmaceutical JSC

644 11

(*):listed companies. Source: VPBS collected

DHG Pharmaceutical JSC (DHG) is currently the largest domestic drug-maker in terms o

both revenues and profits. The company’s main products are generic over-the-counte

(OTC) drugs in the antibiotic and pain-reliever categories. In 2012, revenues from th

sales of antibiotics and painkiller drugs accounted for 38% and 19% of DHG’s tota

revenues. In early 2014, the company had successfully finished and put in operation tw

new production plants that increased total annual production capacity from 4.6 billio

units to 9.6 billion units. In 2013, DGH recorded VND3.5 trillion in net revenues an

VND589 billion in net income, representing a 2009 to 2013 CAGR of 19% and 13%

0

500

1,000

1,500

2,000

2,500

3,000

VNDbn Revenues Profit-after-tax

DHG Pharmaceutical JSC

(DHG), Traphaco JSC (TRA)

and Domesco Medical

Import-Export JSC (DMC)

are the three largest listed

companies.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 10/28

www.VPBS.com.vn Page | 1

respectively. DHG’s gross and net margins were the highest among listed companie

during 2013, recording 47% and 17%, respectively.

Traphaco JSC (TRA)‘s two most popular products in the market are Bogan

(supplements for liver’s functions) and Hoat Huyet Duong Nao (supplements for brai

functions). In 2012, sale of these two products together accounted for 34% of th

company’s total revenues. TRA’s main competitive advantage is the ability to sourc90% of the raw material needs from its local suppliers while other drug makers in th

same field have to rely on imported products from China. In 2013, TRA recorded VND1.

trillion in sales and VND149 billion in net income, representing a 2009 to 2013 CAGR o

23% and 31%, respectively. Last year, TRA had gross and net margins of 43% and 9%

respectively.

Domesco Medical Import Export JSC (DMC)’s offerings comprise a wide range o

products, from traditional medicines and vitamins & supplements to antibiotic, pain

killer and specialty drugs. DMC’s better known products in the markets are the gener

specialty drugs used for treatments for diabetes and cardiovascular diseases as the

costs are 30% to 40% lower than the imported products. In 2013, DMC recorded VND1.

trillion in net sales and VND106 billion in net income, representing a 2009 to 2013 CAGof 8% and 9%, respectively.

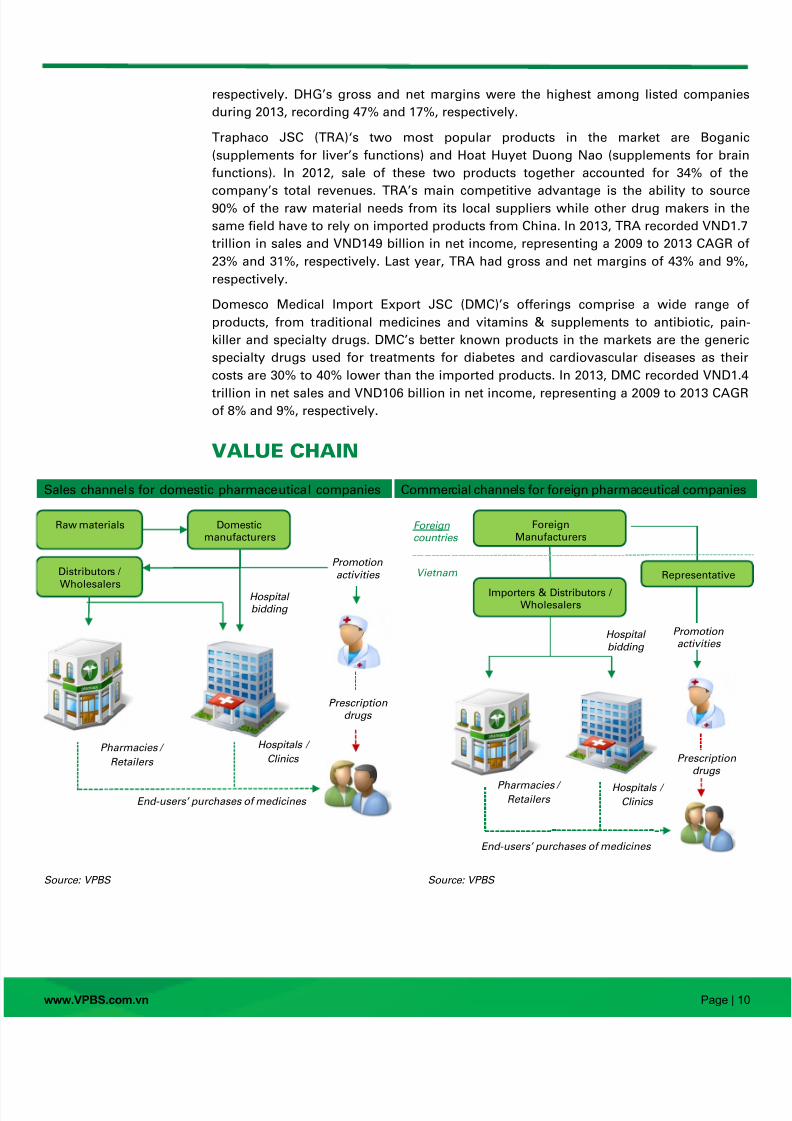

VALUE CHAIN

Sales channels for domestic pharmaceutical companies Commercial channels for foreign pharmaceutical companie

Source: VPBS Source: VPBS

Domestic

manufacturers

Distributors /

Wholesalers

Promotion

activities

Prescriptiondrugs

Raw materials

Hospitalbidding

End- users’ purchases of medicines

Pharmacies /

Retailers

Hospitals /

Clinics

Importers & Distributors /Wholesalers

Promotionactivities

Prescriptiondrugs

Foreign

Manufacturers

Representative

Hospital

bidding

End- users’ purchases of medicines

Foreigncountries

Vietnam

Pharmacies / Retailers

Hospitals /Clinics

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 11/28

www.VPBS.com.vn Page | 1

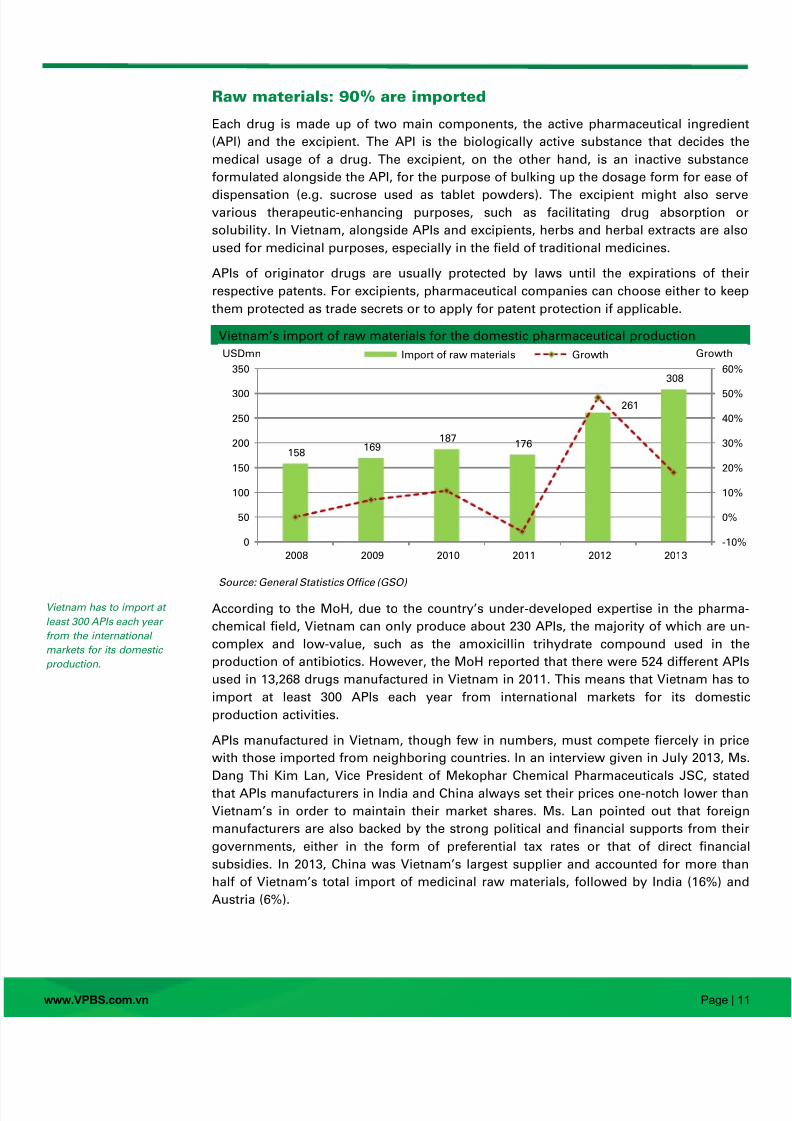

Raw materials: 90% are imported

Each drug is made up of two main components, the active pharmaceutical ingredien

(API) and the excipient. The API is the biologically active substance that decides th

medical usage of a drug. The excipient, on the other hand, is an inactive substanc

formulated alongside the API, for the purpose of bulking up the dosage form for ease o

dispensation (e.g. sucrose used as tablet powders). The excipient might also servvarious therapeutic-enhancing purposes, such as facilitating drug absorption o

solubility. In Vietnam, alongside APIs and excipients, herbs and herbal extracts are als

used for medicinal purposes, especially in the field of traditional medicines.

APIs of originator drugs are usually protected by laws until the expirations of the

respective patents. For excipients, pharmaceutical companies can choose either to kee

them protected as trade secrets or to apply for patent protection if applicable.

Vietnam’s import of raw materials for the domestic pharmaceutical production

Source: General Statistics Office (GSO)

According to the MoH, due to the country’s under-developed expertise in the pharma

chemical field, Vietnam can only produce about 230 APIs, the majority of which are un

complex and low-value, such as the amoxicillin trihydrate compound used in th

production of antibiotics. However, the MoH reported that there were 524 different AP

used in 13,268 drugs manufactured in Vietnam in 2011. This means that Vietnam has t

import at least 300 APIs each year from international markets for its domest

production activities.

APIs manufactured in Vietnam, though few in numbers, must compete fiercely in pric

with those imported from neighboring countries. In an interview given in July 2013, M

Dang Thi Kim Lan, Vice President of Mekophar Chemical Pharmaceuticals JSC, state

that APIs manufacturers in India and China always set their prices one-notch lower tha

Vietnam’s in order to maintain their market shares. Ms. Lan pointed out that foreig

manufacturers are also backed by the strong political and financial supports from the

governments, either in the form of preferential tax rates or that of direct financia

subsidies. In 2013, China was Vietnam’s largest supplier and accounted for more tha

half of Vietnam’s total import of medicinal raw materials, followed by India (16%) an

Austria (6%).

158169

187176

261

308

-10%

0%

10%

20%

30%

40%

50%

60%

0

50

100

150

200

250

300

350

2008 2009 2010 2011 2012 2013

GrowthUSDmn Import of raw materials Growth

Vietnam has to import at

least 300 APIs each year

from the international

markets for its domestic

production.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 12/28

www.VPBS.com.vn Page | 1

Countries that export raw materials to Vietnam’s pharmaceutical sector (2013)

USD in thousands Import values

China 160,404

India 50,807

Austria 19,357

Spain 14,203

Germany 8,894

Italy 6,622

France 6,337

South Korea 4,317

Switzerland 4,273

Britain 3,377

Others 29,860

Total 308,451

Source: Ministry of Industry and Trade (MoIT)

With regard to the production of traditional medicines, Vietnam has to impo

approximately 70% of the raw materials (herbs and herbal extracts) from China eac

year, even though the country is home to approximately 4,000 types of medicinal plantsyielding between 10,000 and 20,000 tons of herbal products each year. There are thre

main reasons behind this apparent paradox:

Lack of large-scale farming projects : The growing and harvesting of medicinal herb

in Vietnam are fragmented, and typically organized at the family or commune levels

The small regional distributors or foreign merchants will usually procure the good

directly from farmers and then distribute them to the domestic buyers. Chines

merchants will usually acquire raw plants from farmers in Vietnam, process them i

China, and then sell the extracts or processed-plants back to the domestic firms a

much higher prices.

Concerns over the quality of home-grown products: In a study conducted in ear2013, the National Institute of Drug Quality Control of Vietnam discovered that 60%

of the samples obtained from government-owned traditional-medicine clinics fail t

meet the required standards. Some of the samples had been mixed with sand

cement and other toxic ingredients.

Under-developed technological infrastructure : Herbal extracts are one of the mai

ingredients that go into the production of traditional medicines. However, Vietnam’

current technological infrastructure is inadequate to perform the chemica

extractions of certain high-value medicinal herbs (e.g. aloe wood). This inevitabl

leads to the country’s export of these raw herbs and import of their extracts from

the more developed countries.

We believe that Vietnam’s strong reliance on foreign countries for the sourcing of raw

materials is one of the key reasons why international pharmaceutical companies hav

not been enthusiastic about setting up production facilities in Vietnam.

China52%

India16%

Austria6%

Spain

5%

Germany3%

Others18%

USD308million

For the traditional medicine

segment, Vietnam has to

import approximately 70% of

the raw material needs from

China.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 13/28

www.VPBS.com.vn Page | 1

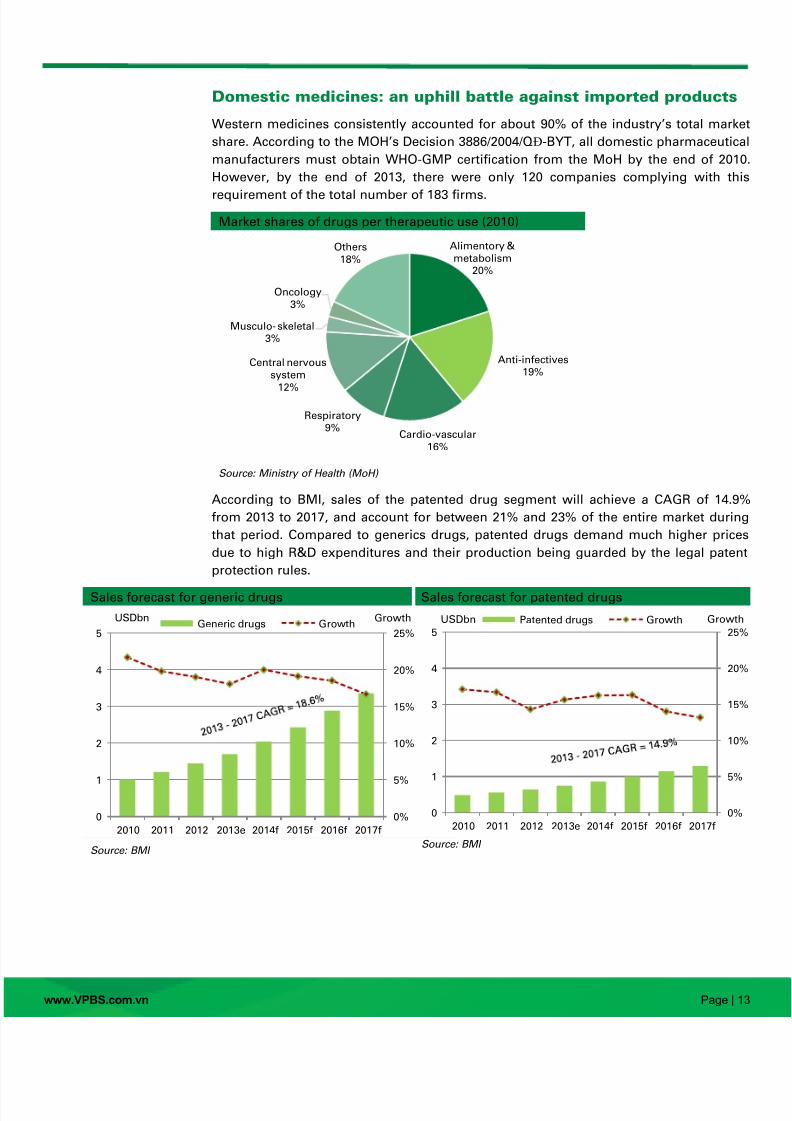

Domestic medicines: an uphill battle against imported products

Western medicines consistently accounted for about 90% of the industry’s total marke

share. According to the MOH’s Decision 3886/2004/QĐ-BYT, all domestic pharmaceutica

manufacturers must obtain WHO-GMP certification from the MoH by the end of 2010

However, by the end of 2013, there were only 120 companies complying with th

requirement of the total number of 183 firms.

Market shares of drugs per therapeutic use (2010)

Source: Ministry of Health (MoH)

According to BMI, sales of the patented drug segment will achieve a CAGR of 14.9%

from 2013 to 2017, and account for between 21% and 23% of the entire market durin

that period. Compared to generics drugs, patented drugs demand much higher price

due to high R&D expenditures and their production being guarded by the legal paten

protection rules.

Sales forecast for generic drugs Sales forecast for patented drugs

Source: BMISource: BMI

Alimentory &metabolism

20%

Anti-infectives19%

Cardio-vascular16%

Respiratory9%

Central nervoussystem

12%

Musculo- skeletal3%

Oncology3%

Others18%

0%

5%

10%

15%

20%

25%

0

1

2

3

4

5

2010 2011 2012 2013e 2014f 2015f 2016f 2017f

GrowthUSDbnGeneric drugs Growth

0%

5%

10%

15%

20%

25%

0

1

2

3

4

5

2010 2011 2012 2013e 2014f 2015f 2016f 2017f

GrowthUSDbn Patented drugs Growth

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 14/28

www.VPBS.com.vn Page | 1

Currently, all drugs that contain patented APIs are manufactured abroad and must b

imported for local consumption. As such, added fees such as imported tariffs (5% at th

moment), transportation costs and under-the-table dealings severely erode the

affordability in the market. Within this segment, patented specialty drugs, such as thos

treating the central nervous system, musculoskeletal oncology diseases, will exhib

strong growth as unhealthy life styles (e.g. smoking and drinking) and toxi

environment conditions are on a steady rise in Vietnam. According to the MoH’s data

around 150,000 people contract cancer each year in Vietnam, with the mortality rat

standing around 50%. Considering the shift in disease profiles discussed at th

beginning of this report, the patented drug segment will be a very lucrative market i

the upcoming years.

Local pharmaceutical companies in Vietnam, however, are not keen on investing in R&

in order to develop new patented drugs due to the huge expenditure and long tim

horizon usually associated with the development of a new drug. According to a stud

conducted in 2011 by InnoThink Center for Research in Biomedical Innovation, a Unite

States-based think tank, it costs at least USD3.6 billion and a period of five years i

order to develop a new drug. At the moment, pharmaceutical companies in Vietnam

ar

content with producing generic drugs and only hold patents for the trade names of the

products, but not for the drug formulas. For example, Traphaco JSC only holds th

patent for ‚Boganic‛, the trade name of its liver-function supplement drug.

At the moment, pharmaceutical production in Vietnam is still limited in term of offering

as most local companies choose to produce similar products to minimize business risk

According to data provided by the DAV, at the end of 2011, 524 APIs were used in th

domestic production of 13,268 pharmaceutical products (averaging 25 products per

API) while 927 APIs were present in 15,552 imported medicines (averaging 16 product

per API). The domestic companies manufacture mostly generics and low-value drugs

such as antibiotics, and painkillers while the high-value specialty drugs (e.g. oncology

diabetes medication) are usually imported. Vietnam offers strong potential for thgeneric market due to the country’s consumer purchasing power being quite low i

relation to the pricing of the patented drugs. However, in this category, the loca

pharmaceutical market is also dominated by foreign products.

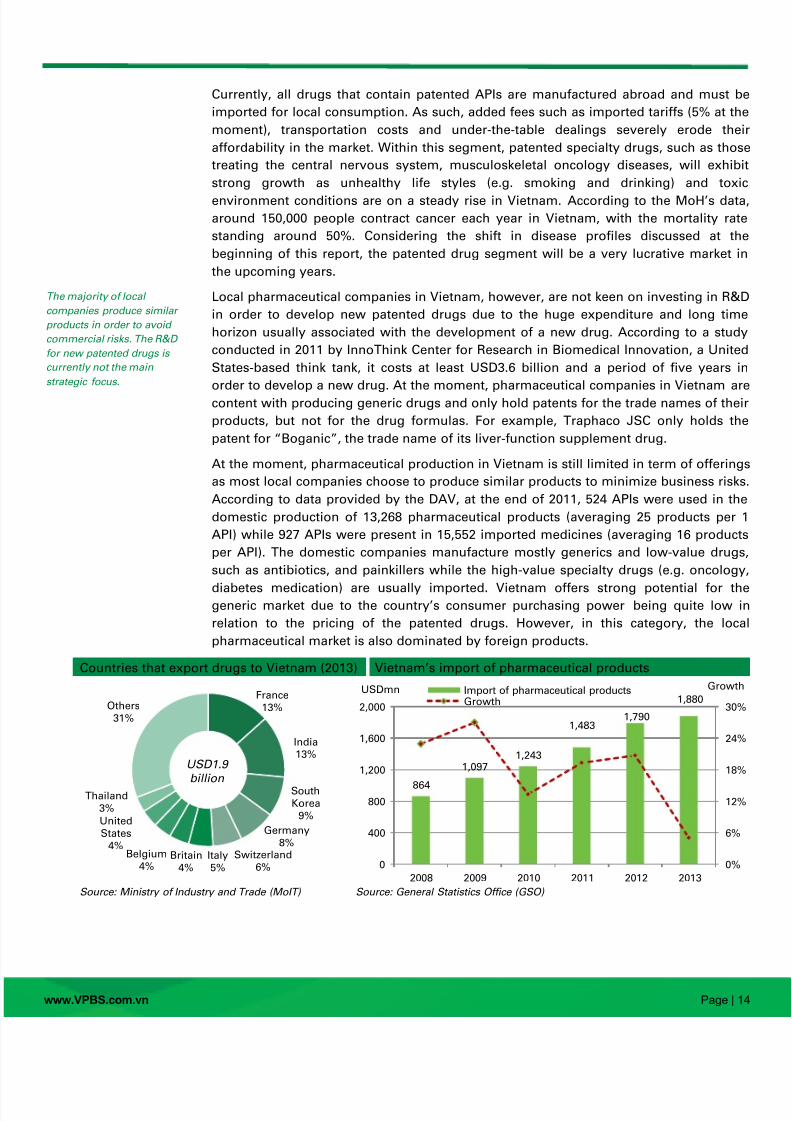

Countries that export drugs to Vietnam (2013) Vietnam’s import of pharmaceutical products

Source: Ministry of Industry and Trade (MoIT) Source: General Statistics Office (GSO)

France13%

India13%

SouthKorea

9%

Germany8%

Switzerland6%

Italy5%

Britain4%

Belgium4%

UnitedStates

4%

Thailand3%

Others31%

USD1.9

billion864

1,0971,243

1,4831,790

1,880

0%

6%

12%

18%

24%

30%

0

400

800

1,200

1,600

2,000

2008 2009 2010 2011 2012 2013

GrowthUSDmn Import of pharmaceutical productsGrowth

The majority of local

companies produce similar

products in order to avoid

commercial risks. The R&D

for new patented drugs is

currently not the main

strategic focus.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 15/28

www.VPBS.com.vn Page | 1

The dominance of the imported generic drugs is the result of several factors:

Local preference: Both local purchasers and doctors have a strong preference fo

imported products. The general perception in the market is that domestic drugs ar

manufactured from outdated production facilities with dismal quality control.

Unfair regulations of promotion activities: Promotion expenses for domest

pharmaceutical companies are curbed at 15% of annual revenues (per MOH’

regulation), while foreign pharmaceutical firms are allowed to spend up to 30% fo

this activity. As such, it is common for foreign companies to organize all-paid-fo

overseas conferences for local doctors and their families in order to promote the

products, with the unstated real purpose actually being sight-seeing and shopping.

Unscrupulous practices: Doctors and pharmacists enjoy much higher sa

commissions and (under-the-table) kickbacks when they prescribe foreign product

to patients. According to unofficial estimates, these commissions and kickbacks, th

most common form of which is wholesale discount, can amount up to 30% of th

drugs’ full prices.

Lax import policies : Vietnam’s regulations are extremely lax toward importe

pharmaceutical products. Currently, in order to sell their products in Vietnamforeign pharmaceutical companies need to provide cost, insurance and freight (CIF

pricing, certification of quality from the country or origins and a small applicatio

fee of approximately USD200. The MoH’s local review process does not require an

local testing for the bioequivalence and bioavailability of the drugs. Meanwhile, i

order for the domestic companies to export their products abroad, they have t

submit elaborate clinical testing results and undergo strict scrutinizing from th

foreign countries’ regulatory bodies.

Vietnam’s policies for pharmaceutical imports appear quite lacking compared t

neighboring countries. Indonesia, for example, severely limits the import of gener

drugs for which domestic alternatives are available; while Thailand requires that a

foreign drugs must undergo domestic clinical testing before they can be distributed tthe mass population. In 2011, approximately 3,000 trading licenses were granted t

imported drugs in Vietnam as compared to only 26 in Thailand.

Recent investigations, however, have discovered that imported pharmaceutical product

do not always mean higher quality as compared to the domestically produce

medicines. For example, in December 2013, the DAV revoked the licenses for th

distribution of Roxley 150 (Roxithromycin 150mg) produced in India, and Tatumcef 2

(Ceftazidim) produced in Taiwan.

The over-the-counter (OTC) segment, by definition, comprises drugs that patients ca

purchase without doctor’s prescriptions. The products in this category typically includ

vitamin supplements, common flu medicines, pain relievers and traditional medicineIn Vietnam, patients usually purchase medicines based on advice obtained from clerk

working in drug stores and friends, rather than from pharmacists and from

appointments with doctors. Moreover, as Vietnam’s consumers gradually gain mor

health-awareness, they become more confident toward the self-medication approach

especially in the case of the low-income population. However, a downside associate

with this trend is the increasing abuse of antibiotics among Vietnamese people

According to a 2010 study published by Karolinska Institute, 71% children with mil

respiratory infections are being given antibiotics. As a result, nearly 70% of the bacteri

carried by people living in urban areas of Vietnam are resistant to penicillin.

The generic segment is

currently dominated by

imported pharmaceutical

products.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 16/28

www.VPBS.com.vn Page | 1

With regard to the traditional medicine segment, we note that great opportunitie

abound if Vietnam is able to attract or initiate investments into the country’s extractio

technologies and into large-scale farming projects for local medicinal herbs. A

mentioned above, Vietnam is home to approximately 4,000 types of medicinal plants

yielding between 10,000 and 20,000 tons of herbal products each year.

Thanks to the encouraging key-drivers observed above, BMI forecasted that sales fothis segment will achieve a CAGR of 15.9% for the period from 2013 to 2017.

Distribution channel: of maze and matrix According to the MOH, in 2011, there were 10,250 private pharmacies, and a total o

44,000 drug retailers in the public and private sectors. On average, there was one dru

retailer for every 2,000 people in Vietnam in 2011. In addition, there are currentl

approximately 1,200 companies (comprising 300 foreign and 900 local companies

engaging in the distribution of pharmaceutical products in Vietnam.

Pharmaceutical spending as percentage of total healthcare spending (2009)

Source: OECD Health at a glance: Asia Pacific 2012

Vietnam’s unorganized and heavily fragmented distribution network, in combinatio

with the country’s inadequate price-control regime, is the one of the few main reason

why drugs prices are quite high in Vietnam. Indeed, pharmaceutical spending as

percentage of total healthcare spending was highest in Vietnam as compared t

selected neighboring countries in 2009.

Given the multitude of distribution links between various market participants, it is not

surprise that drug prices can be pushed up substantially before they reach the hand o

the individual patients. According to the unofficial statistics provided by various new

sources, retail prices offered to end users can amount to three or four times th

wholesale prices obtained from the drug manufacturers.

9%

18%

18%

35%

41%

43%

44%

46%

47%

51%

0% 10% 20% 30% 40% 50% 60%

Malaysia

Singapore

Indonesia

Philippines

India

China

Thailand

Myanmar

Bangladesh

Vietnam

Drug prices in Vietnam are

being pushed up

significantly because of

both under-table dealings

and the labyrinth-like

distribution channels.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 17/28

www.VPBS.com.vn Page | 1

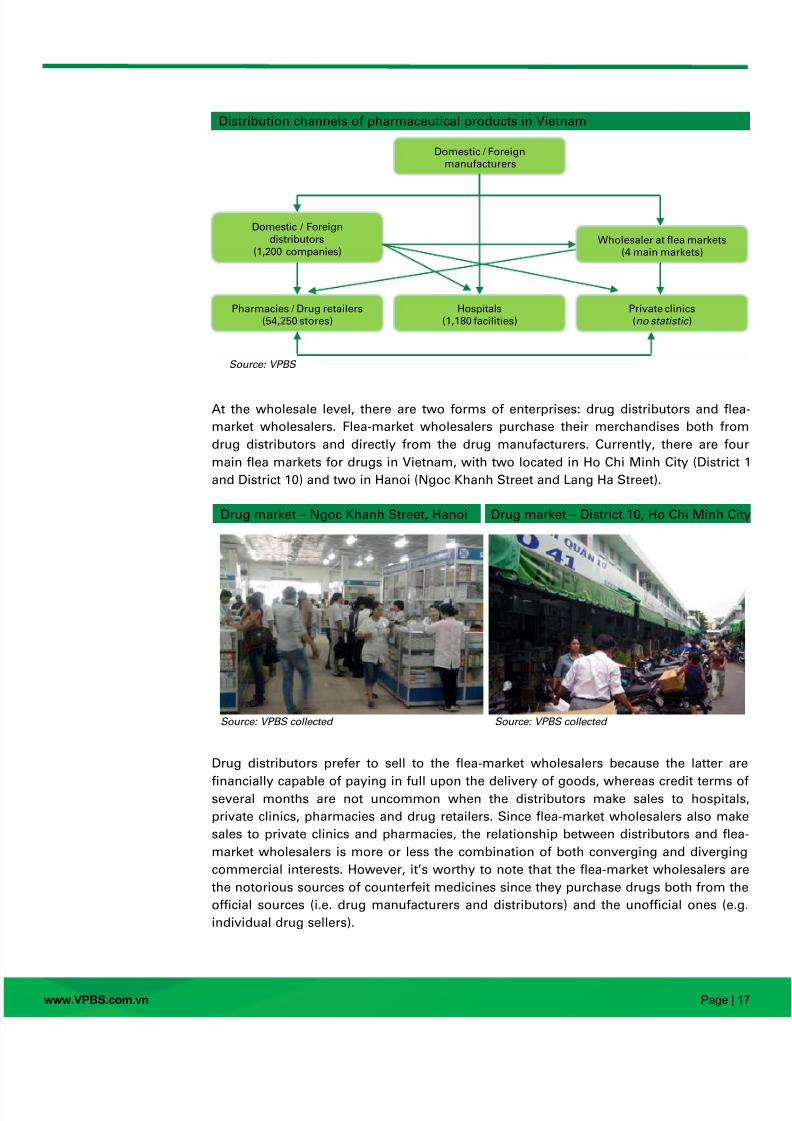

Distribution channels of pharmaceutical products in Vietnam

Source: VPBS

At the wholesale level, there are two forms of enterprises: drug distributors and flea

market wholesalers. Flea-market wholesalers purchase their merchandises both from

drug distributors and directly from the drug manufacturers. Currently, there are fou

main flea markets for drugs in Vietnam, with two located in Ho Chi Minh City (District

and District 10) and two in Hanoi (Ngoc Khanh Street and Lang Ha Street).

Drug market – Ngoc Khanh Street, Hanoi Drug market – District 10, Ho Chi Minh Cit

Source: VPBS collected Source: VPBS collected

Drug distributors prefer to sell to the flea-market wholesalers because the latter ar

financially capable of paying in full upon the delivery of goods, whereas credit terms oseveral months are not uncommon when the distributors make sales to hospital

private clinics, pharmacies and drug retailers. Since flea-market wholesalers also mak

sales to private clinics and pharmacies, the relationship between distributors and flea

market wholesalers is more or less the combination of both converging and divergin

commercial interests. However, it’s worthy to note that the flea-market wholesalers ar

the notorious sources of counterfeit medicines since they purchase drugs both from th

official sources (i.e. drug manufacturers and distributors) and the unofficial ones (e.g

individual drug sellers).

Domestic / Foreign

manufacturers

Domestic / Foreigndistributors

(1,200 companies) Wholesaler at flea markets

(4 main markets)

Pharmacies / Drug retailers (54,250 stores)

Hospitals

(1,180 facilities) Private clinics (no statistic )

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 18/28

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 19/28

www.VPBS.com.vn Page | 1

In addition, foreign distribution companies still hold substantial competitive advantage

as compared to their domestic counterparts primarily because of their long-standin

relationships with the foreign pharmaceutical companies and their technologically

advanced storage infrastructures (e.g. warehouses, transportations). As such, thes

foreign distribution companies will remain the key players with regard to the imports o

imported pharmaceutical products, especially specialty drugs, for the foreseeable future

Within the last few years, several large domestic pharmaceutical companies have bee

developing their own distribution channels to gain more control over the commercia

flows of their products. For example, DHG Pharma Corporation has approximately 8,00

distribution centers and wholesale stores throughout the country. Not only does th

distribution system help increase the availability of DHG’s products, it also gives th

company more control over their logistics and sale prices.

Hospitals: opaque auction processes

According to the Joint Annual Health Review report published in 2013, the entir

country had 1,180 public and private hospitals with a total of over 200,000 beds

achieving 25.04 beds per 10,000 patients. Distribution of drugs to hospitals is conductethrough a decentralized bidding process. Once or twice a year, the drug committees a

nationwide hospitals will initiate requests for biddings, to which pharmaceutical firm

and distribution companies can submit their offers. When an offer is chosen, th

contract prices are fixed until the end of the contract.

This auction process is organized separately by each hospital and there is very little,

any, cooperation between them. Since hospitals are given significant leeway in settin

up and managing their own auction process, corruption and collusion between doctor

and representatives from various pharmaceutical companies are not uncommon. Thi

corruption usually manifests in the forms of direct bribes to individual doctors

kickbacks offered to the hospitals or, more subtly, invitations to conferences oversea

extended to doctors’ families.

A direct result of bidding corruption is that drugs are often sold at vastly different price

throughout the provinces of Vietnam. For example, in an investigation conducted in lat

2012 by the MoH, the drug Perabact (manufactured by Parex Pharmaceutical) was price

at VND18,000 per unit at hospitals in Dong Thap Province, but costs VND30,000 in thos

located in Can Tho Province.

In 2013, in efforts to make the drug auction process more transparent and support th

consumption of domestically produced medicines, Regulation 43/2013/QH13 was issue

by the Ministry of Planning and Investment (MPI) and Circular 36/2013/TTLT-BYT-BT

(revision to Circular 01/2012/TTLT-BYT-BTC issued in June 2012) was jointly issued b

the MoH and MoF. In essence, Regulation 43/2013/QH13 forbids the submission obidding for any imported drugs for which a domestically produced alternative

available. The alternative must be deemed by the MoH as having the sam

bioequivalence, quality and availability as compared to the imported drugs. Circula

36/2013/TTLT-BYT-BTC, on the other hand, specifies in details the scoring system b

which each pharmaceutical product and each bidder should be evaluated during th

bidding process. In addition, Circular 36/2013/TTLT-BYT-BTC and Circular 01/2012/TTLT

BYT-BTC working jointly to ensure hospital bidding processes must give priority t

pharmaceutical products that offer the cheapest prices while scoring at or above certai

technical base point.

Opaque drug-bidding

auctions in hospitals give

rises to numerous

instances of corruptions

and collusions.

Several circulars have been

issued by the industry’s

regulatory bodies in order

to bring drug prices in

Vietnam in check.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 20/28

www.VPBS.com.vn Page | 2

Pharmacies and retail stores: small and largely unchecked

By the end of 2012, there were approximately 54,000 pharmacies and drug retailer

throughout Vietnam, presenting an average of 6.3 outlets per 10,000 people. In Vietnam

patients can get over-the-counter access to most drugs without prescriptions at privat

pharmacies or drug retailers, albeit usually at higher prices compared to pharmacie

located within hospitals. Despite various rules and measures imposed by the MoH tcounter this, the fact that only few outlets are examined and audited by the MoH eac

year means that this phenomenon will likely persist in the foreseeable future.

In addition, the majority of drug outlets in Vietnam are individually-owned and smal

scale in nature. The largest retail chains (e.g. My Chau Pharmacies) boasts between 2

and 30 stores at most. In contrast, drug retail chains in Vietnam’s more develope

neighboring countries are much larger. Philippine-based Mercury drug retail chain

owned more than 500 stores and accounted for 60% of the country’s total market shar

in 2010, according to the retail chain’s websites.

Staying nimble and small helps Vietnamese pharmacies and retail drug stores to sta

below the regulators’ radar, which, in turn, allows them to adjust the retail price o

drugs at will. In a survey conducted by students of HCMC’s Medicine and Pharmac

University in mid-2009, drugs prices varied from 10% to 38% across sampled retail outlet

Rises in costs of pharmaceutical and healthcare products

Note: Base year 2008 = 100%. Source: General Statistics Office

Due to Vietnam’s strong reliance on imports of both medicines and raw materials, and

the labyrinthine drug distribution channels discussed above, the resultant rises in cost

of pharmaceutical and healthcare products have outpaced the country’s consumer pric

index (CPI) in recent years. We noted that price hikes in 2012 correlated with strongrowth in import values of both pharmaceutical products (up 21% y-o-y) and raw

materials (up 48% y-o-y) in that year.

In July 2012, the MoH stated that drugs are being sold in China and Thailand at the pric

level one to six times higher than in Vietnam. However, the results of the survey ar

considered by many to be unconvincing, because the ministry looked at only 36 ove

10,000 imported products available in the market.

Since 2011, there has been a drive by the MoH in order to increase the number of GPP

compliant pharmacies and drug retail stores in Vietnam. However, according to th

0%

50%

100%

150%

200%

250%

2009 2010 2011 2012 2013 02/2014

CPI Pharmaceutical &healthcare products and services

CPI of pharmaceutical and

healthcare segments has

outpaced overall CPI in

Vietnam since 2012.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 21/28

www.VPBS.com.vn Page | 2

JAHR published in 2013, the GPP compliance rate throughout the country by the end o

August 2012 was only 39%.

Pharmaceutical advertising

In Vietnam, prescription drugs cannot be advertised directly to consumers. Howeve

these products can be promoted to health officers and doctors via visits b

representatives of the pharmaceutical companies and through conferences and healt

seminars. In addition, foreign firms are required to obtain permission from a provincia

health department before holding any conference and that department must be mad

aware of any pharmaceutical displays.

Meanwhile, the advertising laws are more liberal for OTC products. Consume

marketing of OTC products is permitted via magazines and newspapers, as well a

leaflets and brochures. However, in order to be advertised through broader mass med

outlets such as television and radios, pharmaceutical companies must first subm

requests to the DAV for approval.

On the opposite, the DAV has banned the advertisement of nutritional supplement

effective from April 26, 2013 due to the chaotic state of the advertising system. In ainterview given in October 2012, Mr. Nguyen Thanh Phong, DAV’s Deputy Directo

asserted that preventing advertising violations was difficult as some advertisin

agencies were not registered with the authorities. There is a lack of cooperatio

between various regulatory bodies and rule enforcements are weak.

LEGAL FRAMEWORK

Regulatory bodies

The main regulatory authorities in Vietnam are the MoH and the DAV. However, bot

agencies often cooperated with other ministries such as the MoF and MoIT in order t

draft and issue regulations concerning the import, trading and distributing o

pharmaceutical products. One example of such cooperation is Circular 36/2013/TTLT

BYT-BTC, which was jointly issued by the MoH and the MoF in December 2013.

In general, it is a common perception that the regulation of pharmaceutical products i

Vietnam is not sufficiently effective due primarily to vague terms in the regulation

because rule enforcement is not strict enough to prevent violations and corruption. Fo

example, MOH’s Decision 19/2005/QQD-BYT required that all domestic drug-maker

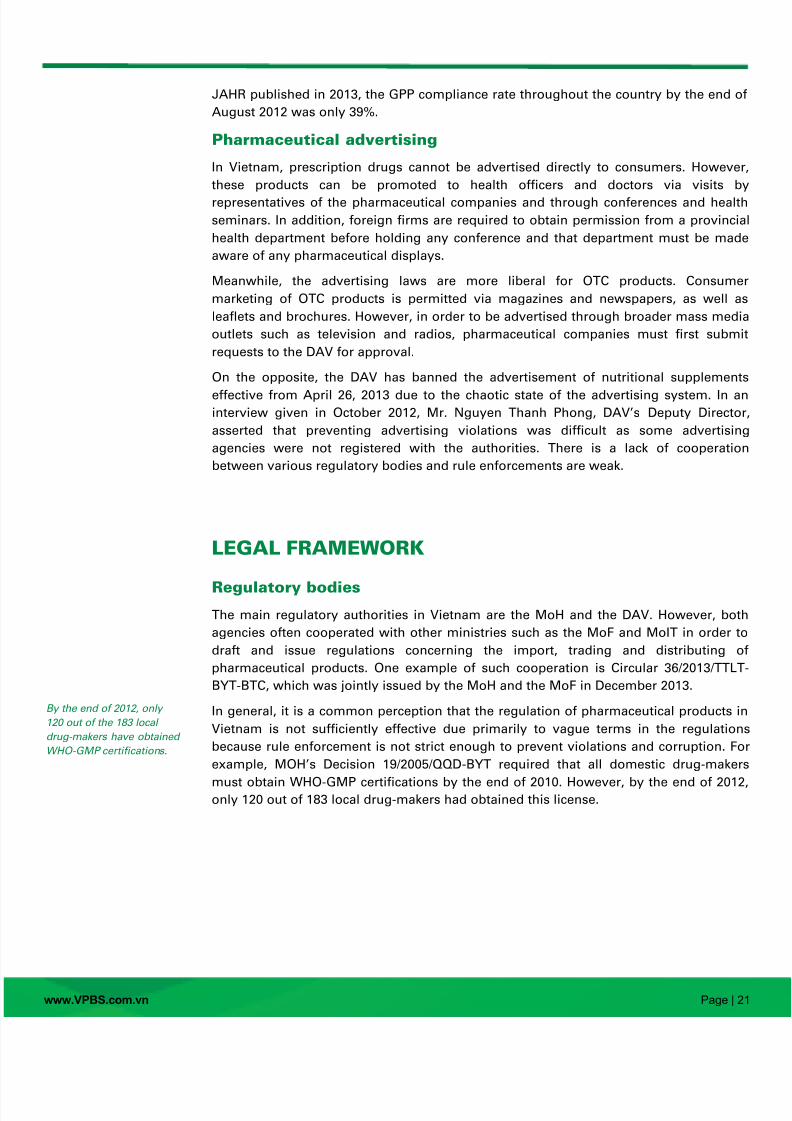

must obtain WHO-GMP certifications by the end of 2010. However, by the end of 2012only 120 out of 183 local drug-makers had obtained this license.

By the end of 2012, only

120 out of the 183 local

drug-makers have obtained

WHO-GMP certifications.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 22/28

www.VPBS.com.vn Page | 2

Number of firms that obtained GP standards

Source: DAV

In 2007, Vietnam was accepted as a member of the World Trade Organization (WTO

Through its membership, foreign enterprises have been given the right to ope

branches in Vietnam and import medicines directly, although they are still barred from

distributing their products. However, foreign drug distributors are able to participate i

the domestic distribution of medicines through both partnerships with local companie

and other means, such as providing storage and transportation services for loca

distribution firms.

Intellectual property protection

Vietnam's accession to the WTO in January 2007 has resulted in the overa

improvement of the country’s intellectual property (IP) legal framework. Specifically, th

country needed to follow and implement IP standards as required by the WTO’s Trade

Related Aspects of Intellectual Property Rights (TRIPS) agreement. For example, one o

the IP standards calls for a 20-year patent term and a five-year market exclusivity o

undisclosed and other test data to be granted for original medicines.

Despite such improvements, there are many shortcomings in Vietnam’s IP protectio

legal framework. IP enforcement is generally viewed as patchy and disorganized i

Vietnam since many agencies can independently decide whether to take action or not o

just refer the complaints to another regulatory body. In addition, the legal system ha

little experience in the interpretation and enforcement of patent laws.

Due to the country’s inadequate IP regime, the Pharmaceutical Research an

Manufacturers of America (PhRMA) association listed Vietnam among its ‚close

watch‛ countries, a status unchanged since 2004. According to the report, PhRMA

member companies continue to face delays in the granting of patents, which erodes th

terms of patent protections available for innovative medicines. In addition, PhRMA

highlighted various reasons for such delays; the most prominent being insufficien

personnel capacity at the relevant regulatory bodies. The association further suggeste

that Vietnam should adopt more effective mechanisms in preventing the infringement o

patents prior to the granting of marketing approval for follow-on products.

0

32

64

96

128

160

Number offirms

Good manufacturing practices Good labaratory practices

Good storage practices

Vietnam is listed among

PhRMA’s list of “closely

watch” countries due to the

country’s weak intellectual

property protection regime.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 23/28

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 24/28

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 25/28

www.VPBS.com.vn Page | 2

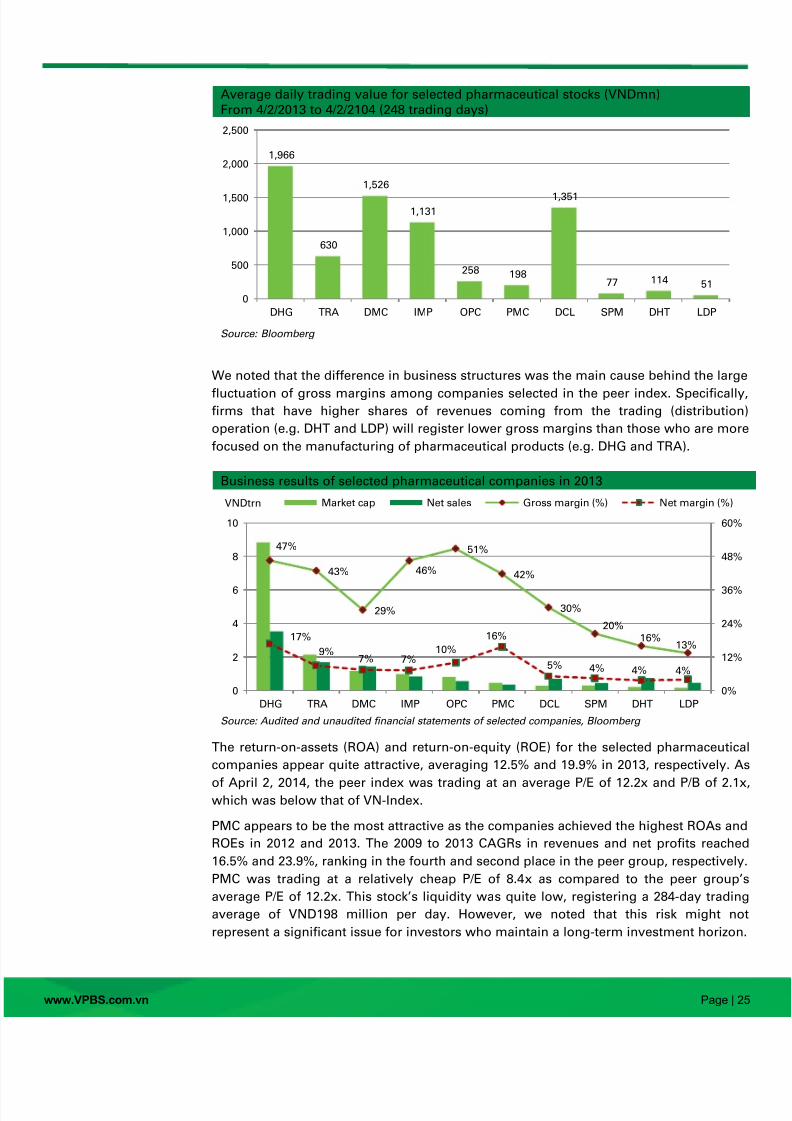

Average daily trading value for selected pharmaceutical stocks (VNDmn)

From 4/2/2013 to 4/2/2104 (248 trading days)

Source: Bloomberg

We noted that the difference in business structures was the main cause behind the larg

fluctuation of gross margins among companies selected in the peer index. Specificallyfirms that have higher shares of revenues coming from the trading (distribution

operation (e.g. DHT and LDP) will register lower gross margins than those who are mor

focused on the manufacturing of pharmaceutical products (e.g. DHG and TRA).

Business results of selected pharmaceutical companies in 2013

Source: Audited and unaudited financial statements of selected companies, Bloomberg

The return-on-assets (ROA) and return-on-equity (ROE) for the selected pharmaceutica

companies appear quite attractive, averaging 12.5% and 19.9% in 2013, respectively. A

of April 2, 2014, the peer index was trading at an average P/E of 12.2x and P/B of 2.1xwhich was below that of VN-Index.

PMC appears to be the most attractive as the companies achieved the highest ROAs an

ROEs in 2012 and 2013. The 2009 to 2013 CAGRs in revenues and net profits reache

16.5% and 23.9%, ranking in the fourth and second place in the peer group, respectively

PMC was trading at a relatively cheap P/E of 8.4x as compared to the peer group

average P/E of 12.2x. This stock’s liquidity was quite low, registering a 284-day tradin

average of VND198 million per day. However, we noted that this risk might no

represent a significant issue for investors who maintain a long-term investment horizon

1,966

630

1,526

1,131

258 198

1,351

77 114 51

0

500

1,000

1,500

2,000

2,500

DHG TRA DMC IMP OPC PMC DCL SPM DHT LDP

47%

43%

29%

46%

51%

42%

30%

20%16%

13%17%

9%7% 7%

10%

16%

5% 4% 4% 4%

0%

12%

24%

36%

48%

60%

0

2

4

6

8

10

DHG TRA DMC IMP OPC PMC DCL SPM DHT LDP

VNDtrn Market cap Net sales Gross margin (%) Net margin (%)

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 26/28

www.VPBS.com.vn Page | 2

Data as of April 2, 2014. Source: Companies ’ financial statements, Bloomberg

Stock price Sale grow th Net income grow th

Ticker Market

Capital April 2

YTD

change

52-

Week

Hi h

52-

Week

Low

FY2012 FY2013 FY09-13

CAGR FY2012 FY2013

FY09-1

CAG

VNDbn VND VND VND

DHG DHG Pharmaceutical JSC 8,824 135,000 18.4% 150,000 77,000 17.7% 20.3% 19.2% 16.9% 21.3% 13.3%TRA Traphaco JSC 2,134 86,500 2.4% 97,500 44,390 31.8% 20.1% 22.5% 31.2% 28.3% 30.8%

DMC Domesco Medical Import Export JSC 1,175 44,000 39.5% 50,500 18,667 11.3% 13.4% 7.6% 12.6% 17.7% 8.6%

IMP Imexpharm Pharmaceutical JSC 984 60,000 60.9% 72,000 29,800 5.4% 3.0% 6.3% 0.0% -21.4% -1.8%

OPC OPC Pharmaceutical JSC 807 63,000 -1.6% 75,500 56,000 23.1% 11.9% 11.0% 10.4% 0.9% 3.3%

PMC Pharmedic Pharmaceutical Medicinal 467 50,000 14.9% 52,800 27,000 14.9% 17.9% 16.5% 14.8% 25.5% 23.9%

DCL Cuu Long Pharmaceutical JSC 286 28,800 21.5% 34,700 12,800 -2.9% 14.3% 5.1% n/a 87.3% -10.8%

SPM SPM Corporation 300 21,800 -18.7% 35,800 19,000 33.5% 4.1% 15.1% 8.6% -69.8% -25.2%

DHT Hatay Pharmaceutical JSC 207 33,000 40.4% 44,000 19,100 7.5% 9.7% 5.5% -12.3% 81.8% 16.8%

LDP Lam Dong Pharmaceutical JSC 163 48,000 27.0% 63,000 30,000 19.8% 9.5% 20.8% -12.1% -8.6% 4.7%

Average 20.5% 16.2% 12.4% 13.0% 7.8% 16.3% 6.4%

Median 20.0% 16.3% 12.7% 13.1% 10.4% 19.5% 6.6%

ROA ROE FY 2013

Ticker Foreign

owned FY2012 FY2013 FY2012 FY2013

Net

sales Gross profits Net income

Cash

ratio

Current

ratio

Debt to

Equity

% % % % VNDbn VNDbn % margin VNDbn % margin % % %

DHG 49.0% 22.5% 21.8% 31.7% 32.1% 3,527 1,640 46.5% 589 16.7% 76% 217% 6% 1 4.97x 4.45

TRA 46.0% 14.2% 16.6% 35.1% 26.3% 1,682 721 42.9% 149 8.9% 77% 232% 15% 15.13x 3.12

DMC 49.0% 10.7% 11.6% 15.8% 17.8% 1,430 412 28.8% 106 7.4% 15% 184% 17% 1 1.07x 1.87

IMP 47.4% 9.2% 7.1% 10.9% 8.5% 842 391 46.4% 61 7.2% 163% 468% 0% 16.51x 1.36

OPC 16.3% 11.6% 10.9% 17.3% 16.0% 564 286 50.7% 56 10.0% 16% 177% 20% 14.40x 2.23

PMC 12.8% 27.7% 29.5% 36.1% 39.0% 357 149 41.7% 56 15.6% 133% 350% 0% 8.37x 2.94

DCL 16.2% 2.5% 5.6% 8.0% 13.3% 699 208 29.7% 36 5.1% 5% 123% 88% 7.70x 1.03SPM 5.9% 6.0% 1.7% 10.4% 2.9% 448 91 20.3% 18 3.9% 45% 298% 23% 17.15x 0.44

DHT 0.4% 4.9% 9.9% 11.7% 19.5% 743 118 15.9% 27 3.6% 27% 163% 73% 7.74x 1.58

LDP 9.3% 12.7% 10.3% 28.1% 23.6% 463 62 13.4% 18 3.9% 12% 151% 0% 9.08x 2.07

Average 12.2% 12.5% 20.5% 19.9% 1,076 408 33.6% 111 8.2% 57% 236% 24% 12.21x 2.11

Median 11.1% 10.6% 16.5% 18.6% 721 247 35.7% 56 7.3% 36% 200% 16% 12.73x 1.97

Company name

Trailing

P/B

Trailing

P/E

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 27/28

www.VPBS.com.vn Page | 2

CONCLUSIONWe believe that Vietnam’s pharmaceutical industry holds tremendous potential fo

future growth, in spite of numerous structural weaknesses . Indeed, the country

growing population, in combination with heightened health-awareness among th

middle-class segment, should provide ample fuel for growth in the domesticonsumption of pharmaceutical products. These positive macro trends will undoubtedl

enable domestic pharmaceutical companies to remain profitable in the upcoming years

In the medium to long term, we predict that the pharmaceutical industry as a whole wi

be further consolidated, although the rate of the consolidation might be moderate

Domestic drug-makers will pursue mergers and acquisitions (M&A) as a mean t

vertically integrate their operations and to expand their distribution networks. In 201

and 2013, Traphaco JSC (TRA) had successfully purchased 43% and 49% stake in Quan

Tri Pharmaceuticals & Medical Company and Thai Nguyen Pharmaceuticals & Medica

Company, respectively, in order to increase the number of distribution centers acros

the country.

At the same time, we believe that domestic pharmaceutical companies will continue t

allocate budgets for the technical upgrades of their production facilities. These upgrade

will increase the number of domestic companies that meet WHO-GMP standards an

broaden the portfolio of products that can be manufactured domestically.

While we maintain a positive outlook with regard Vietnam’s pharmaceutical stocks (e.g

DHG, TRA and PMC), we do not deem the sector attractive enough for foreign investor

to engage in direct capital investment, at least not at the moment. We encourage foreig

pharmaceutical companies to wait for the outcome of the TPP agreements, whic

should be finalized this year, before contemplating any long-term direct investment i

Vietnam’s pharmaceutical sector.

8/11/2019 Vietnam Pharmaceutical Industry

http://slidepdf.com/reader/full/vietnam-pharmaceutical-industry 28/28

DisclaimerResearch report is prepared and issued by VPBank Securities Co. Ltd. (‚VPBS‛). This report

not directed to, or intended for distribution to or use by, any person or entity who is a citizen o

resident of or located in any locality, state, country or other jurisdiction where such distribution

publication, availability or use would be contrary to law or regulation. This document is not fo

public distribution and has been furnished to you solely for your information and must not b

reproduced or redistributed to any other person. Persons into whose possession this documen

may come are required to observe restrictions.

Each research analyst involved in the preparation of a research report is required to certify tha

the views and recommendations expressed therein accurately reflect his/her personal viewabout any and all of the securities or issuers that are the subject matter of this research repor

and no part of his/her compensation was, is and will be directly or indirectly related to specifi

recommendations or views expressed by the research analyst in the research report. Th

research analyst involved in the preparation of a research report does not have authorit

whatsoever (actual, implied or apparent) to act on behalf of any issuer mentioned in suc

research report.

Any research report is provided, for information purposes only, to institutional investor an

retail clients of VPBS. A research report is not an offer to sell or the solicitation of an offer t

buy any of the securities discussed herein.

The information contained in a research report is prepared from publicly available information

internally developed data and other sources believed to be reliable, but has not bee

independently verified by VPBS and VPBS makes no representations or warranties with respec

to the accuracy, correctness or completeness of such information and they should not be relie

upon as such. All estimates, opinions and recommendations expressed herein constitut

judgment as of the date of a research report and are subject to change without notice. VPB

does not accept any obligation to update, modify or amend a research report or to otherwis

notify a recipient of a research report in the event that any estimates, opinions an

recommendations contained herein change or subsequently becomes inaccurate or if

research report is subsequently withdrawn.

Past performance is not a guarantee of future results, and no representation or warranty

express or implied, is made regarding future performance of any security mentioned in thi

research report. The price of the securities mentioned in a research report and the income the

produce may fluctuate and/or be adversely affected by market factors or exchange rates, an

investors may realize losses on investments in such securities, including the loss of investmen

principal. Furthermore, the securities discussed in a research report may not be liqu

investments, may have a high level of volatility or may subject to additional and special risk

associated with securities and investments in emerging markets and/or foreign countries tha

may give rise to substantial risk and are not suitable for all investors. VPBS accepts no liabilit

whatsoever for any loss arising from any use or reliance on a research report or the informatiocontained herein.

The securities in a research report may not be suitable for all types of investors and suc

reports do not take into account particular investment needs, objectives and financia

circumstances of a particular investor. An investor should not rely solely on investmen

recommendations contained in this research report, if any, as a substitution for the exercise o

their own independent judgment in making an investment decision and, prior to acting on an

of contained in this research report, investors are advised to contact his/her investment advise

to discuss their particular circumstances.

VPBS and its affiliated, officers, directors and employees world-wide may, from time to tim

have long or short position in, and buy or sell the securities thereof, of company (ies

mentioned herein or be engaged in any other transaction involving such securities and ear

brokerage or other compensation or act as a market maker in the financial instruments of th

company (ies) discussed herein or act advisor or lender/borrower to such company (ies) o

have other potential conflict of interest with respect to any recommendation and relate

information and opinions.

Any reproduction or distribution in whole or in part of a research report without permission o

VPBS is prohibited.

If this research report has been distributed by electronic transmission, such as e-mail, then suc

transmission cannot be guaranteed to be secure or error-free as information could b

intercepted, corrupted, lost, destroyed, arrive late, in complete, or contain viruses. Should

research report provide web addresses of, or contain hyperlinks to, third party web sites, VPB

has not reviewed the contents of such links and takes no responsibility whatsoever for th

contents of such web site. Web addresses and/or hyperlinks are provided solely for th

recipient’s convenience and information, and the content of third party web sites is not in an

way incorporated into this research report. Recipients who choose to access such we

Barry David WeisblattHead of [email protected]

Luu Bich HongDirector - Fundamental [email protected]

Nguyen Huu Toan

Research [email protected]

Hanoi Head Office362 Hue Street,Hai Ba Trung District, Hanoi

T - +84 (0) 4 3974 3655

F - +84 (0) 4 3974 3656

Ho Chi Minh City Branch76 Le Lai Street,District 1, Ho Chi Minh City

T - +84 (0) 8 3823 8608

F - +84 (0) 8 3823 8609

Danang Branch112 Phan Chau Trinh Street,Hai Chau District, Danang

T - +84 (0) 511 356 5419

F - +84 (0) 511 356 5418