US Ski Resort Pricing and Volumes: Downhill RacingJanuary 2018

US Ski resorts have dramatically increased prices. Casual skiers have been particularly

hard hit

2

Vail Resorts Effective Ticket Price

31.2

2000 2001 20172002

32.0

20162014 20152009 20132010 201220112003 2004

34.2

2005 2006 2007 2008

+4.7% +5.6%

48.7

55.8 58.2

41.837.7

48.1

34.1

49.0

39.3

56.0

63.4

46.2 47.2

67.965.6

Effective Ticket Price Excluding Pass Holders vs. Inflation (2008 = 100)

2015

80

2016

160

2011

180

2010 2013

120

2012

100

2017

140

20142008 2009

176

113

Indexed US CPIIndexed Vail Resorts Effective Ticket Price (excl. pass holders)

6.5% CAGR

1.7% CAGR

Ticket prices for casual skiers have increased at 4.5x the rate of inflation

since 2008

Average ticket prices have increased at 2.25x the rate of inflation since 2008 (US CPI = 2.1%)

These price increases have led to very strong financial metrics

3

Vail Resorts Margins and ROIC

2000

0

5

20102004 2016

10

2006 20142001 2003 2005 2007 2009 2011 2013

15

20152002 2008 2012

20

2017

EBIT Margin

ROIC

Source: Bloomberg

And high valuations which assume continued price increases

4

Price / BookFY1 P/E

4.7x

30.7x

21.5x

EV / EBIT EV / EBITDA

15.3x

Vail Resorts Valuation Metrics

Source: Bloomberg

Price increases at 2x+ inflation cannot continue indefinitely. Long term

growth must be volume driven

Implies company can

continue to earn returns c.

4x it’s cost of capital on

incremental investments in

perpetuity

What has enabled this? US Resorts are exploiting a perceived lack of competition (from Vail

Resorts 10-K)

5

But these price increases have come at the cost of significant declines in industry volumes

6

Total Skier Days (NSAA)

52,000

54,000

56,000

58,000

60,000

62,000

0

2012

55,658

20142010 2017

55,949

57,641

2008

55,068

57,156

20092007 2015

52,792

57,09856,491

59,214

56,904

53,578

54,761

56,137

59,227

60,540

54,787

50,966

2016

57,354

60,502

2013

54,28753,710

-0.4%

-1.6%

2011

59,787

Total Skier Days 3 Year Rolling Average

Total Skier Days / 1,000 US Residents

100

0

150

50

200

-1.2%

2017

167195

2012 20162015

193 185

20142013

180 174

-2.2%

192177 176 163

199 191 193

162183

170194189 180

167 168

2010200920082007 2011

187

3 Year Rolling AverageTotal Skier Days / Person Skiing in the US has become significantly less popular despite a major economic

expansion since the end of the crisis and continued population growth

Source: NSAA, Bloomberg

As prices continue to increase, skiers will continue to seek out alternatives

• Other types of vacations (e.g. beach)

• Alternative mountain sports (e.g. backcountry skiing)

• New capacity in US (possible given price umbrella)

• Travel to other geographies (e.g. Europe)

• Regulation (e.g. antitrust regulation preventing further acquisitions)

• Recession

7

Example of a threat to US ski industry seen in following pages – NOT THE ONLY ONE (or even the most likely to

have an impact)

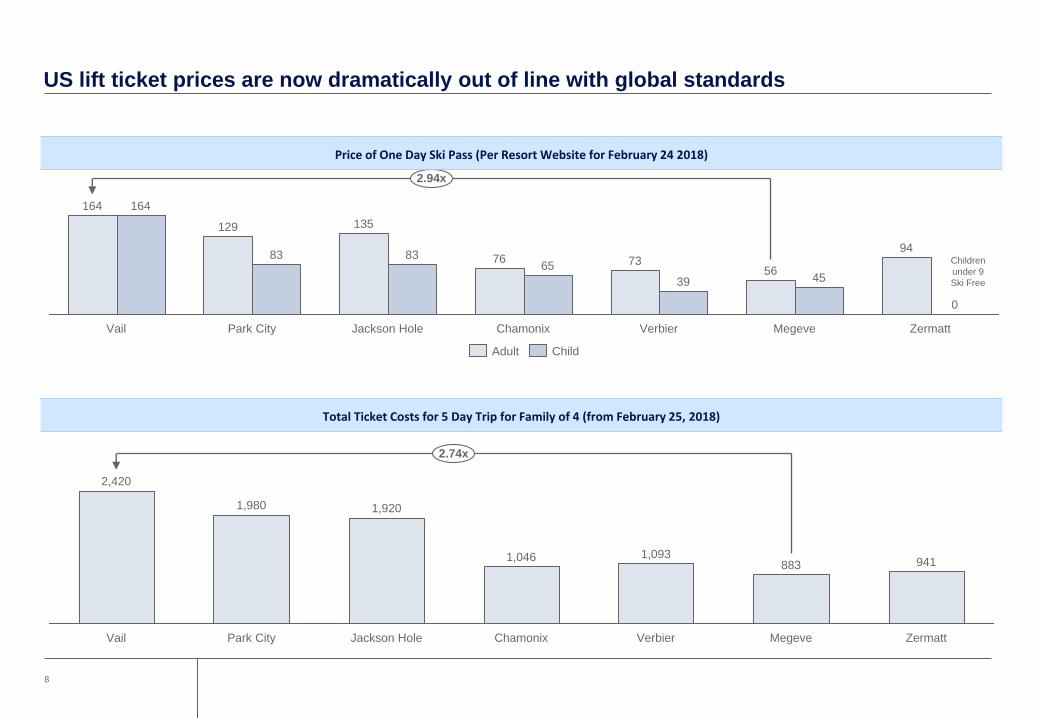

US lift ticket prices are now dramatically out of line with global standards

8

2.94x

Vail

129

83

164

Park City Jackson Hole

135

164

Chamonix

83

MegeveVerbier

65

39 45

73

0

Zermatt

7656

94

Adult Child

Price of One Day Ski Pass (Per Resort Website for February 24 2018)

Total Ticket Costs for 5 Day Trip for Family of 4 (from February 25, 2018)

1,920

Jackson HoleVail

1,980

2,420

Park City

2.74x

1,046 1,093883 941

Chamonix Verbier ZermattMegeve

Children

under 9

Ski Free

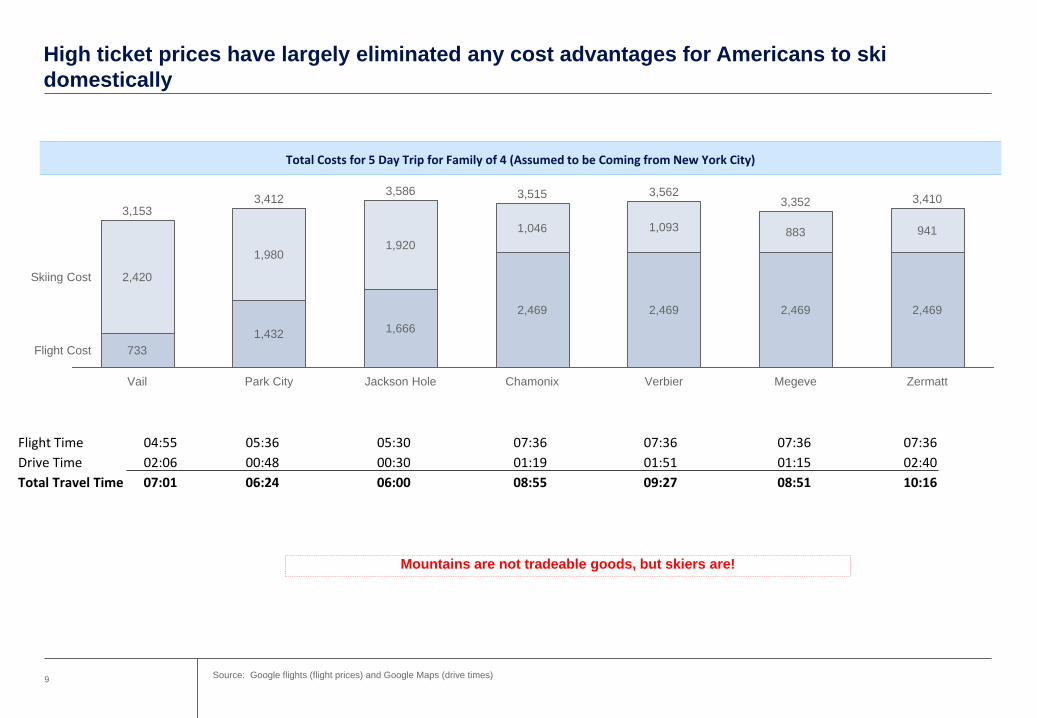

High ticket prices have largely eliminated any cost advantages for Americans to ski

domestically

9

Total Costs for 5 Day Trip for Family of 4 (Assumed to be Coming from New York City)

3,562

VerbierChamonix

3,410

Megeve Zermatt

3,352

1,666

1,920

2,469

1,093

2,469

1,046

2,469

883

1,980

941

1,432

2,469

733

2,420Skiing Cost

Flight Cost

Park City

3,4123,586

Vail

3,153

3,515

Jackson Hole

Flight Time 04:55 05:36 05:30 07:36 07:36 07:36 07:36

Drive Time 02:06 00:48 00:30 01:19 01:51 01:15 02:40

Total Travel Time 07:01 06:24 06:00 08:55 09:27 08:51 10:16

Mountains are not tradeable goods, but skiers are!

Source: Google flights (flight prices) and Google Maps (drive times)

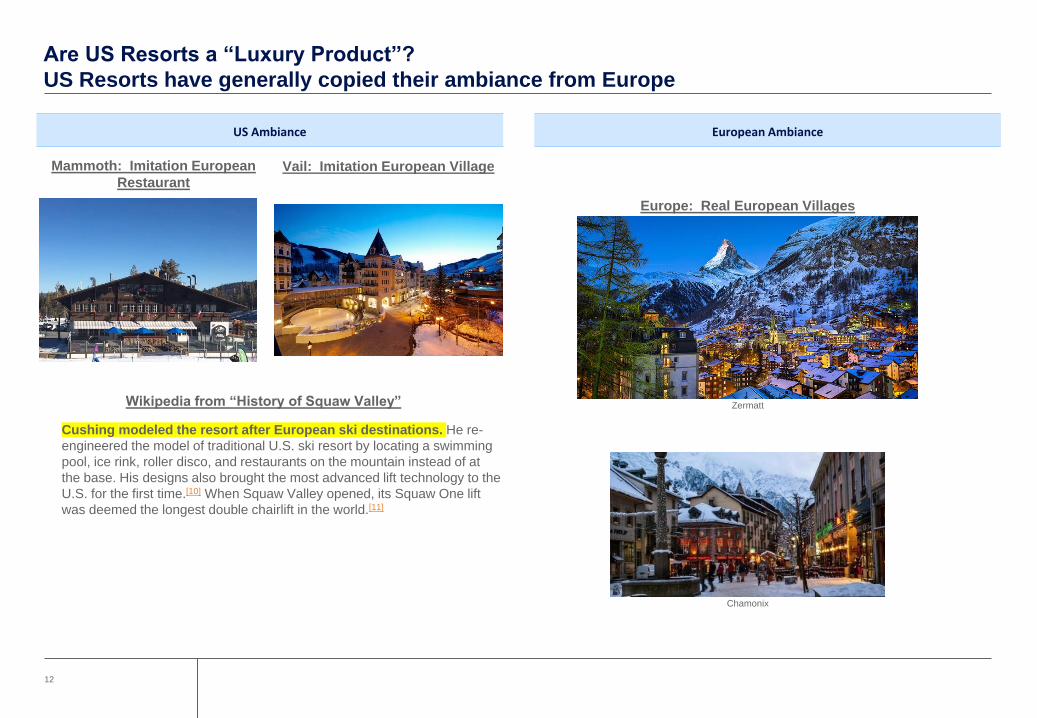

Are US Resorts a “Luxury Product”?

Europe has a superior product to the US along the most utilized quantitative metrics

10

Comparison of US vs. European Resort Size (KM of Trails)

1.7x

Megeve

412

140

360

Zermatt

445

Km of Trails

VerbierChamonixVail Park City

234 265

Comparison of US vs. European Resort Size (Skiable Acres)

Verbier

Skiable Acres

3.6x

Vail Jackson Hole

2,500

ChamonixPark City

5,289

26,000

7,300

15,000

Vertical Drop

3,1003,450

Vail

4,139

Park City

6,922

Jackson Hole

1.7x

Vertical Drop

3,835

6,837

Chamonix Verbier

5,580

Megeve Zermatt

Source: Resort websites, Wikipedia, OnTheSnow, Snow-Forecast.com

Are US Resorts a “Luxury Product”?

European amenities are generally superior to those in the US

11

US Ski Lunch (Granite Grill, Jackson Hole) Zermatt Ski Lunch (Chez Vrony)

Not a “luxury product”

Are US Resorts a “Luxury Product”?

US Resorts have generally copied their ambiance from Europe

12

Mammoth: Imitation European

RestaurantVail: Imitation European Village

Europe: Real European Villages

Zermatt

Chamonix

Cushing modeled the resort after European ski destinations. He re-

engineered the model of traditional U.S. ski resort by locating a swimming

pool, ice rink, roller disco, and restaurants on the mountain instead of at

the base. His designs also brought the most advanced lift technology to the

U.S. for the first time.[10] When Squaw Valley opened, its Squaw One lift

was deemed the longest double chairlift in the world.[11]

Wikipedia from “History of Squaw Valley”

US Ambiance European Ambiance

Are US Resorts a “Luxury Product”?

European and US après ski scenes are not comparable

13

European Apres Ski (La Follie Douce, Megeve) American Après Ski