Universal Access: An internationalUniversal Access: An internationalcomparisoncomparison

The views expressed in this paper are those of the author and do not necessarily reflect the opinions of the ITU orits Membership. Dr Kelly can be contacted by e-mail at [email protected]

Dr Tim Kelly, ITUSession 2: Course on

Telecom Policy, Regulationand Management,

University of Witwatersrand,6-7 May, 1999

Universal Access: An international comparison

Universal Access: An internationalcomparison

lWhat is Universal Service / UniversalAccess?lThe “myth” of subsidised accesslDefining affordabilitylPricing strategies

⇒For universal access⇒For universal service

lTargets for the year 2010

Universal Access: An international comparison

Universal accesslAvailability ...lAccessibility ...lAffordability ...

of basic telephone service“to promote the extension of the benefits ofthe new telecommunication technologies toall the world’s inhabitants”ITU Constitution, Article 1

Universal Access: An international comparison

Universal access andUniversal service

l Universal service:telephone in everyhomel Universal access:

telephone withinreasonabledistance foreveryone

0102030405060708090

100

GDP per capita

Percentage of households with a telephone

Universal access

Universal service

Universal Access: An international comparison

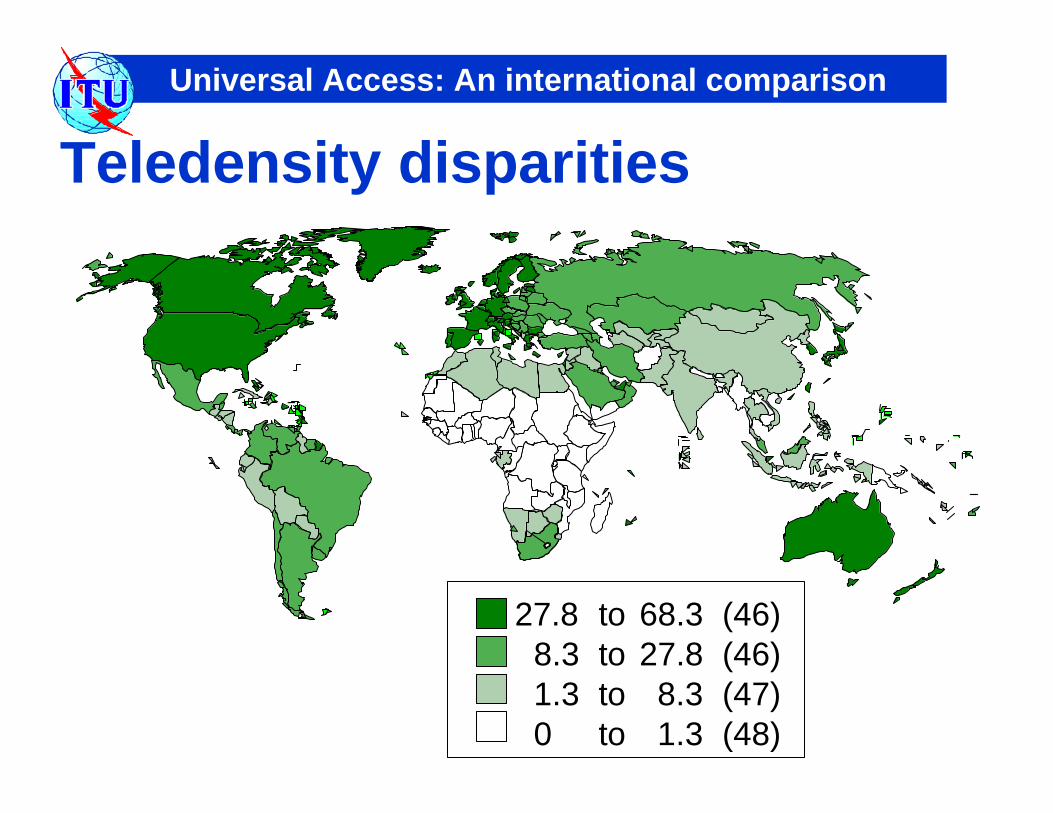

Teledensity disparities

27.8 to 68.3 (46)8.3 to 27.8 (46)1.3 to 8.3 (47)0 to 1.3 (48)

Universal Access: An international comparison

05

1015

202530354045

Teledensity

Num

ber

of e

cono

mie

s

Teledensity <1: 43 economies

1-5: 36 economies

5-10: 26 economies

1 5 10 20 30 40 50 60 70 80

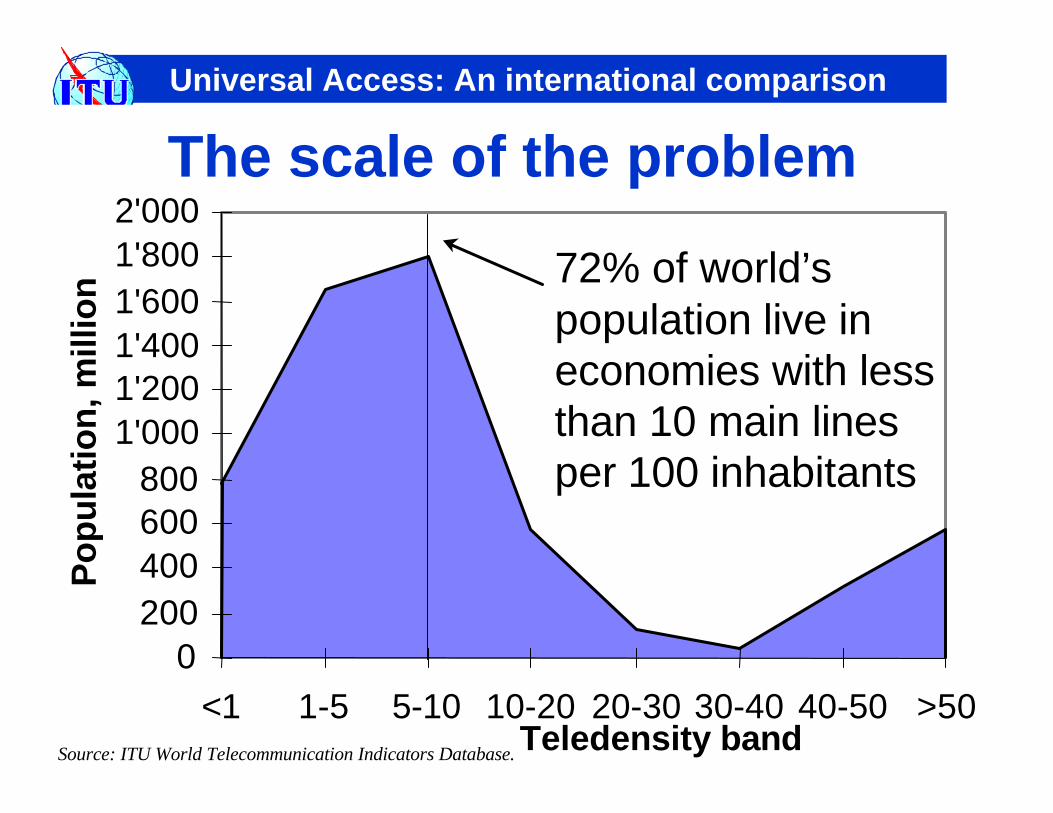

The nature of the problem

Source: ITU World Telecommunication Indicators Database.

Universal Access: An international comparison

0200400600800

1'0001'2001'4001'6001'8002'000

<1 1-5 5-10 10-20 20-30 30-40 40-50 >50Teledensity band

Pop

ulat

ion,

mill

ion

The scale of the problem

Source: ITU World Telecommunication Indicators Database.

72% of world’spopulation live ineconomies with lessthan 10 main linesper 100 inhabitants

Universal Access: An international comparison

Teledensity transition

<1 1-10 5- 10- 20- 30- 40- >50 10 20 30 40 50

0

10

20

30

40

50

No. of countries:

Average

Best

1 10 20 30 40 50

43 37 29 28 22 17 19 25

Tele-density:

Years

Source: ITU World Telecommunication Development Report 1998: Universal Access.

Universal Access: An international comparison

Have telephone

29%

No access18%

NearbyPublic phone

36%

Neigh-bours 6%

Nearby5%

Not Near-by 6%

Anot

her

phon

e South Africa9 million

households

Source: Statistics South Africa.<http://www.statssa.gov.za/>

Teledensity: 10.7Cellular density: 3.7Total telephone

density: 14.4Household

telephonepenetration: 29%

Universal accesspenetration (% ofhouseholds withaccess totelephone): 82%

Measures of Accessibility: SA

Universal Access: An international comparison

8

16

17

18

23

27

29

31

46

55

N. Prov.

E. Cape

North West

M'langa

Free State

Kwazulu-Natal

RSA

Northern Cape

Gauteng

Western Cape

South Africa . % of households with a telephone, By province, 1996Source: Statistics South Africa.

Measures ofAccessibility: byprovince

Universal Access: An international comparison

The “myth” of subsidisedaccessl It is commonly argued that telephone

access should be priced at a low rate sothat as many people as possible canafford itlBut,

⇒ this may result in ‘subsidies’ from non-telephoneusers to telephone owners, who are typicallybusiness, government and richest 1% of population

⇒ if revenues do not cover costs, then the waitinglist will grow

Universal Access: An international comparison

“Socially desirable” pricing

• Rates are keptartificially low

• Affordable price,maybe < break-even

• Initial group oftelephone users areclustered in thelargest city and arenot poor

Percentage of households in Lima, Peru with a telephone, by income, 1996100%

84%

37% 36%

7%

A B Lima C D

A = Richest 25%B = Second 25%C = Third 25%D = Poorest 25%

Source: OSIPTEL.

• May not generateenough revenue fornetwork expansion

Universal Access: An international comparison

Defining affordabilitylRelative affordability, e.g., <5 per cent of

average family income⇒BUT, initial telephone users are are not necessarily

“average⇒In low income countries, costs for network

installation may be high, but incomes are low

l“Best practice” cost of operating anetwork⇒Methodology must be refined for residential and

business users⇒Costs must be split between one-time & recurring

Universal Access: An international comparison

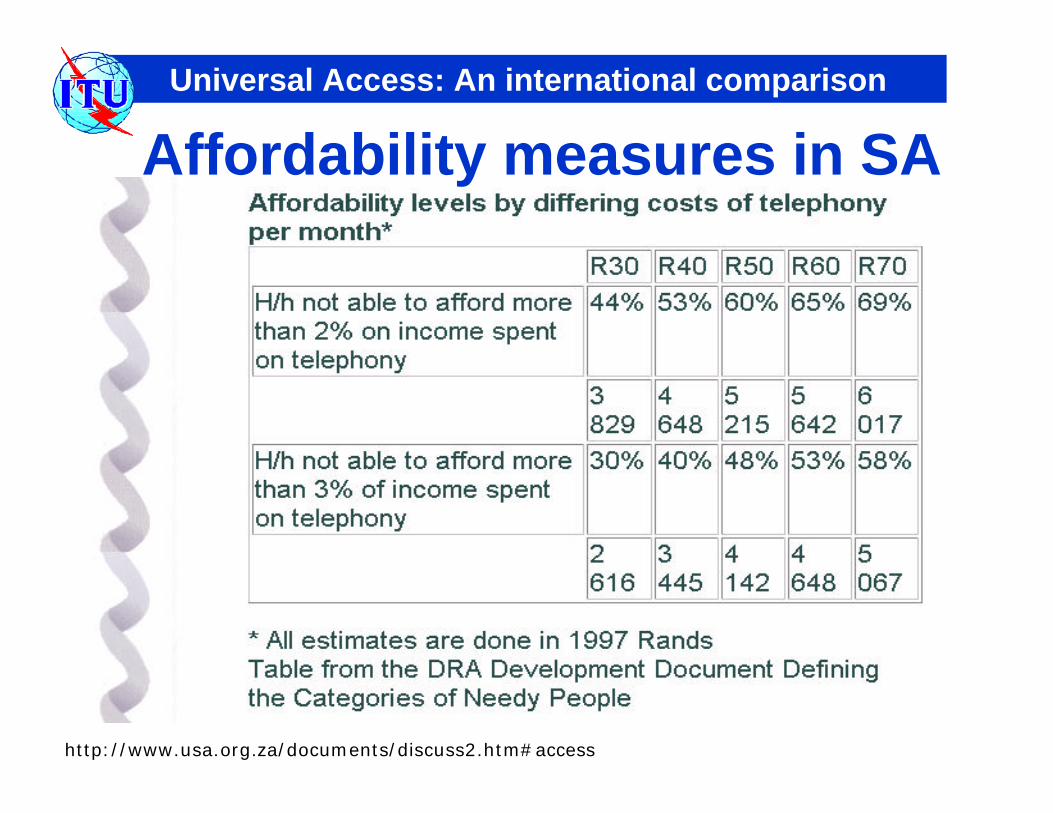

http://www.usa.org.za/documents/discuss2.htm#access

Affordability measures in SA

Universal Access: An international comparison

-

20

40

60

80

100

0% 2% 4% 6% 8% 10%Telephone charges as % of household expenditure

Per

cent

of h

ouse

hold

s w

ith

tele

phon

e

Telephone charges relative tohousehold income, 1995

Note: The annual telephone charges data are a basket based on one tenth of the installation charge, annual subscription in the largest local network, 700 local calls and 130 long-distance calls. Taxes are included.

Source: TU World Telecommunication Development Report 1998: Universal Access.

Universal Access: An international comparison

Establish average operatingcosts for telephone network

US$ 200 - 400 per subscriberper year

Derive an average tariff US$ 64 - 122 per year

Determine how manyhouseholds can afford service

Where 5% of household income> US$ 1’340 - 3’200

Choose a policy for families thatcannot afford service

Financial assistance, widespreadpayphones, etc.

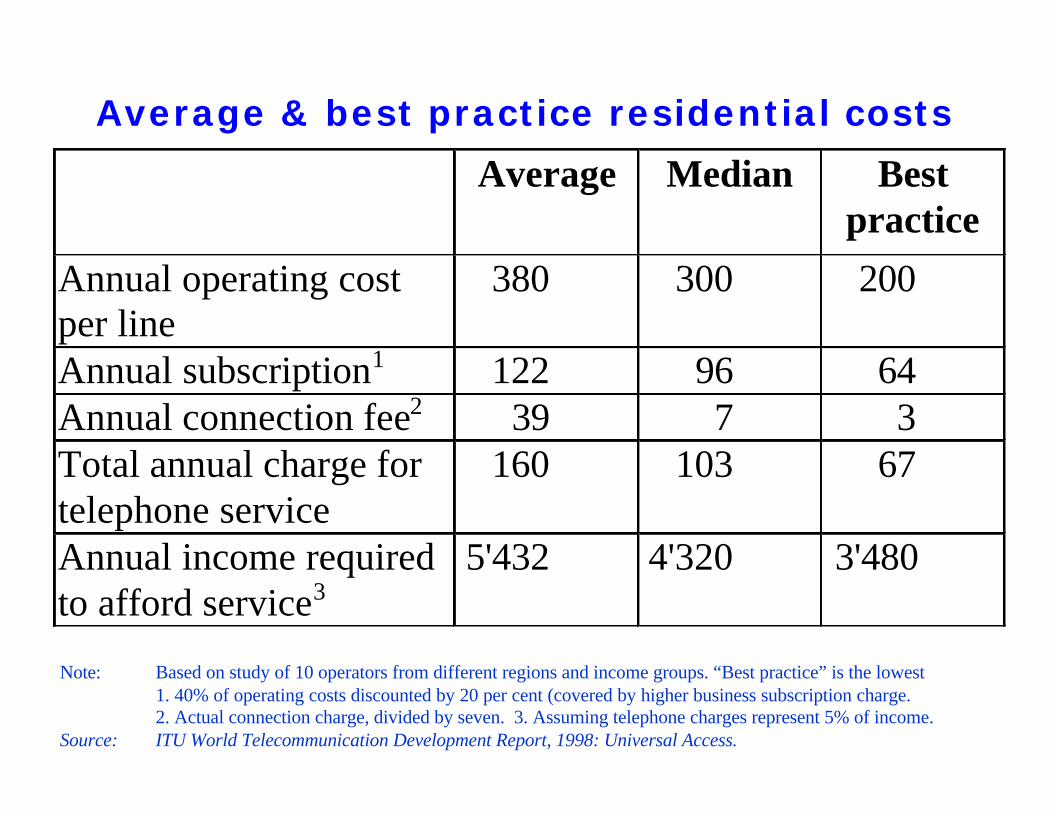

Methodology for determiningaverage and best practice costs

Source: TU World Telecommunication Development Report 1998: Universal Access.

Average Median Bestpractice

Annual operating costper line

380 300 200

Annual subscription1 122 96 64Annual connection fee2 39 7 3Total annual charge fortelephone service

160 103 67

Annual income requiredto afford service3

5'432 4'320 3'480

Average & best practice residential costs

Note: Based on study of 10 operators from different regions and income groups. “Best practice” is the lowest1. 40% of operating costs discounted by 20 per cent (covered by higher business subscription charge.2. Actual connection charge, divided by seven. 3. Assuming telephone charges represent 5% of income.

Source: ITU World Telecommunication Development Report, 1998: Universal Access.

Universal Access: An international comparison

Global measures ofAffordability

Source: ITU World Telecommunication Development Report, 1998: Universal Access.

0

100

200

300

400

500

600

700

WithService

OnWaitlist

Couldafford

Couldnot

afford

~1'500 million households in the world

Without telephone service

Universal Access: An international comparison

Pricing strategies forextending Universal Accessl Installation charges initially high, but

coming down over timelResidential subscription charges should

reflect cost of servicing line (typicallyUS$5-10 per month)lSet separate charges for residential and

business subscriberslLower prices for payphone or community

telephone accesslTariff options, e.g., for low-volume users

Universal Access: An international comparison

$0

$500

$1'000

$1'500

$2'000

$2'500

'92 '93 '94 '95 '96 '92 '93 '94 '95 '960

5

10

15

20

Installation charge (left scale)

Teledensity (right scale)

Telecom Argentina TeleBrás

Installation charges and teledensityin Argentina and Brazil, US$

Source: ITU World Telecommunication Development Report, 1998: Universal Access.

… lead to fastergrowth rates

Monthly residential subscription charges, US$

$-

$2

$4

$6

$8

$10

1990 1991 1992 1993 1994 1995 1996

UruguayMalaysia

Hungary

MoroccoPercentage of households with telephone

0

10

20

30

40

50

60

70

1990 1991 1992 1993 1994 1995 1996

MalaysiaHungaryUruguay

Morocco

Higher monthlysubscription

charges ...

Source: ITU World TelecommunicationDevelopment Report, 1998: Universal Access.

Universal Access: An international comparison

Demand-side measures forextending Universal Access

lTariff cross-subsidies⇒Traditional method, but may not benefit those for

which it is intended

lUniversal Service Fund⇒Targeted assistance for special needs (e.g., rural areas,

disabled), but may create administrative burden

lDirect Financial Assistance to users⇒Targeted assistance using non-telecom-specific

criteria, but may be difficult to control abuses

lCommunity-wide initiatives⇒e.g., Payphone in every village, community

Universal Access: An international comparison

Supply-side measures forextending Universal Access

lMarket liberalisation⇒e.g., allowing new suppliers to enter market, liberalising

equipment market, giving financial autonomy to PTO,encouraging foreign investment, Build/Transfer/Operateconcessions

lPayphone liberalisation⇒e.g., permitting private installation and ownership of

payphones, community telephone shops, telecentres

lTechnical solutions⇒e.g., Mobile cellular, Wireless Local Loop, GMPCS,

combined cable TV/telephony

Universal Access: An international comparison

Pricing strategies to achieveUniversal ServicelTargeted tariff options

⇒e.g., for low-volume users, the elderly, thedisabled, foreign migrants

lPrepaid calling cards⇒for fixed-line and mobile networks

lSupport for incoming calls⇒e.g., to allow families to receive calls from

family members working abroad, for instancethrough voicemail, email, telecentres, call-turnaround, foreign sales of calling cards etc

Universal Access: An international comparison

Achieving Universal service

0%

20%

40%

60%

80%

100%

1960 1970 1980 1990 1996

France Japan

Sweden

Canada

Australia

USA

0%

20%

40%

60%

80%

100%

1970 1980 1990 1998

Mauritius

SouthAfrica

Botswana

SADC*

Percentage of households with a telephone

Universal Access: An international comparison

% of house-YearDEVELOPED holds with 90%ECONOMIES telephone reached

1 Canada 98.7 19712 United States93.9 1970 3 Australia 96.8 1986 4 Japan 96.1 † 19895 New Zealand 96.0 19766 Austria 90.0 19957 Belgium 92.0† 19948 Denmark ‡ 19829 Finland 90.0 198710 France 97.0 198511 Germany 94.7† 199512 Greece 98.1† 199313 Italy 97.5 199214 Luxembourg ‡ 198915 Netherlands 96.5 199016 Spain 94.7† 199417 Sweden ‡ 197518 UK 91.1 1994

% of house- YearDEVELOPINGholds with 90%ECONOMIES telephone reached

19 Bahrain ‡ 199220 Brunei ‡ 199321 Cyprus ‡ 199022 Hongkong ‡ 198623 Israel 95.0 198924 Korea (Rep.) 95.2 199025 Kuwait ‡ 199326 Macau ‡ 199227 Malta ‡ 198728 Qatar ‡ 198329 Singapore ‡ 198330 Taiwan-China ‡ 199031 UAE 93.5 † 1995

Note: % of households with telephone obtained fromcensus surveys and refer to year 1996. † Residentialtelephone lines per 100 households. ‡ Residentialtelephone lines per 100 households is greater than100 due to 2nd telephone lines.

Source: ITU World Telecommunication DevelopmentReport 1998.

Achieving Universal service

Universal Access: An international comparison

1996 2010 1996 2010 1996 2010

WORLD 12.80 34.4 1.55

Developing 5.07 10 16.3 >50 0.84 2 Low income 2.44 5 8.5 >20 0.57 1 excluding China 1.22 4.1 0.21

TeledensityHousehold telephonepenetration

Payphonesper 1’000people

Year 2010 GoalsGoal: Provide reasonable access to telecommunications

for all of humanity by the year 2010

Source: ITU World Telecommunication Development Report, 1998