Download - UNITED OVERSEAS INSURANCE LIMITED

UNITED OVERSEAS INSURANCE LIMITED

(INCORPORATED IN SINGAPORE)

AND ITS SUBSIDIARY

CONTENTS

Principal Activities 3

Chairman’s Statement 4

Corporate Information 6

Corporate Governance 7

Board of Directors 11

Directors’ Report 13

Statement by Directors 15

Auditors’ Report to the Members 16

Income Statements 17

Insurance Revenue Accounts 18

Balance Sheets 20

Consolidated Statement of Changes in Equity 22

Statement of Changes in Equity – Company 23

Consolidated Cash Flow Statement 24

Notes to the Financial Statements 26

Statistics of Shareholdings 43

Notice of Annual General Meeting 44

Notice of Nomination of Auditors 46

Proxy Form

All figures in this Annual Report are in Singapore dollars unless otherwise specified.

2

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

3

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

The Group’s principal activities are the underwriting of general insurance business and reinsurance. General insurance covers

fire, marine, motor, engineering, general accident and liability business.

The Management of the Group is located at 3 Anson Road, #28-01, Springleaf Tower, Singapore 079909 and its Singapore and

international operations are supported by prominent insurance brokers, agents and international reinsurance companies.

Through its wholly-owned subsidiary, UOB Insurance (H.K.) Limited, the Group provides a complete range of general insurance

services in Hong Kong.

The Company provides management services for Overseas Union Insurance, Limited.

PRINCIPAL ACTIVITIES

4

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

CHAIRMAN’S STATEMENT

2003 performance and dividend

The Singapore economy continued to experience structural

adjustment in 2003 under the added weight of rising

unemployment, the Severe Acute Respiratory Syndrome

(SARS) outbreak and the Iraqi war. These factors slowed

down the national GDP growth to 1.1% against 2.2% in

2002.

The local general insurance market is small and matured.

With the presence of many insurance players, competition

remains intense. Against such operating conditions, the

Company managed to grow its gross premium by 11.0%

to $41.8 million. This growth was mainly achieved by

tapping on intra-group synergies and the implementation

of new business strategies that expanded the customer base.

The growth in fire gross premium of 9.9% to $16.6 million

was mainly from property insurance. Gross premium from

Other Accident insurance also increased 12.2% to

$23.6 million due mainly to new business initiatives with

the parent bank.

The Company continued to maintain a tight rein on its Motor

and Workmen’s Compensation business portfolios because

of their inherent volatility. Premium rates were raised to be

commensurate with the higher risks and prudent

underwriting controls were applied to manage the risks

posed by these two classes of insurance.

Improvements in claims were registered across most classes

of insurance. Net incurred claims were lowered slightly to

$4.5 million as compared to $4.6 million in 2002.

The Company’s net underwriting profit grew to $6.3 million

which was 8.7% higher than last year. This growth was

achieved through an unwavering commitment to

underwriting discipline, strict cost control and judicious

claims management.

Investment income also increased to $6.0 million from

$1.7 million in 2002. The increase of $4.3 million was due

mainly to improved market sentiments.

The Company achieved a net profit before tax of $12.3

million due to improvements in both net underwriting profit

and investment income.

The Board proposes to transfer $1.0 million to General

Reserve and recommends payment of a final dividend of

15% (15 cents per share) less 20% income tax. Together

with the interim dividend of 5% (5 cents per share) less

22% income tax, the total dividend for year 2003 is 20%

(20 cents per share).

The Company’s wholly-owned subsidiary, UOB Insurance

(H.K.) Limited in Hong Kong achieved a net profit before

tax of $15,828. Its business will be rationalised with that of

Overseas Union Insurance, Limited (“OUI”) in Hong Kong.

To further grow the business, the subsidiary will be looking

into closer collaboration with OUI in Hong Kong.

2004 prospects

The positive economic outlook, with Singapore GDP growth

estimated at 3.5% to 5.5%, augurs well for the business

environment. We are also optimistic that the Company will

Wee Cho YawChairman

5

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

Comparative Group Growth Data

(figures in $ million)

2003 2002 2001 2000 1999

Gross premium 42.3 38.1 31.5 30.0 26.3

Capital and reserves 97.8 94.3 94.9 90.4 81.1

Total assets 172.9 159.7 149.4 146.1 127.2

Underwriting profit 6.3 5.7 5.2 4.4 4.4(before tax)

take full advantage of the opportunities arising from the

bigger customer base as a consequence of the merger

between Overseas Union Bank and United Overseas Bank.

On 31 October 2003, the High Court of Singapore confirmed

a scheme for OUI to transfer its business portfolio to the

Company as from 1 January 2004. Following the transfer,

OUI has ceased performing all underwriting activities and is

managed by the Company. The combined agency network,

which has more than doubled in size, widens the scope of

fresh marketing initiatives alongside the enhanced activities

in bancassurance by the UOB Group locally and in the region.

Acknowledgements

On behalf of the Board, I wish to thank management and

staff members for their dedication and hard work

throughout the year. My thanks are also extended to our

clients, brokers, agents, reinsurers and shareholders for their

steadfast support. I also wish to express my gratitude to my

colleagues on the Board for their invaluable counsel.

Wee Cho Yaw

Chairman

March 2004

6

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

CORPORATE INFORMATION

BOARD OF DIRECTORS

Mr Wee Cho YawChairman

Mr David Chan Mun WaiManaging Director

Mr Wee Ee CheongMr Hwang Soo JinMr Yang Soo SuanDr Lee Soo Ann

AUDIT COMMITTEE

Mr Yang Soo SuanChairman

Mr Hwang Soo JinDr Lee Soo Ann

NOMINATING COMMITTEE

Mr Hwang Soo JinChairman

Mr Wee Cho YawMr Yang Soo Suan

REMUNERATION COMMITTEE

Mr Wee Cho YawChairman

Mr Hwang Soo JinMr Yang Soo Suan

SECRETARY

Mrs Vivien Chan

SENIOR MANAGER

Ms Faridah Rahmat Ali(Underwriting)

MANAGERS

Ms Chia-Lim Siew Heah(Accounts)

Ms Chia-Sie Lie Ming(Claims)

ASSISTANT MANAGERS

Ms Veronica Sim Bee Heng(Accounts)

Ms Lim Kok Hong(Underwriting)

Ms Diana Leow Dan Liang(Underwriting)

Ms Lee-Lim Bee Geok(Underwriting)

Ms Ng Sze Theng(Electronic Data Processing)

BUSINESS ADDRESS

3 Anson Road#28-01, Springleaf TowerSingapore 079909Telephone: (65) 6222 7733Facsimile: (65) 6327 3869/6327 3870Email: [email protected]: www.uoi.com.sg

REGISTERED OFFICE

80 Raffles PlaceUOB PlazaSingapore 048624Company Registration No.: 197100152RTelephone: (65) 6533 9898Facsimile: (65) 6534 2334

SHARE REGISTRAR

Lim Associates (Pte) Ltd10 Collyer Quay#19-08, Ocean BuildingSingapore 049315Telephone: (65) 6536 5355Facsimile: (65) 6536 1360

AUDITORS

PricewaterhouseCoopers8 Cross Street#17-00, PWC BuildingSingapore 048424Partner-in-charge: Mr Sim Hwee Cher(Appointed on: 9 May 2002)

7

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

CORPORATE GOVERNANCE

The Company is committed to the highest standards of corporate governance. The Board’s approach to corporate governanceis guided by best practice recommendations and the principles in the Code of Corporate Governance issued by the Committeeon Corporate Governance (“Code”).

Board of DirectorsBoard Role and Responsibility: The Board sets the strategic directions for the Company and approves business initiatives, thebusiness plan and annual budget of the Company. In addition, the Board monitors the financial performance of the Company,reviews and approves the quarterly and final financial results of the Company. The Board has formed board committees to assistin the effective discharge of specific responsibilities. Details of these committees are set out below.

Board Composition, Independence and Rotation: The Board is comprised of three executive and three non-executivedirectors, the list of directors being set out on page 6. The Board is of the view that the current board size of six directors isadequate for effective decision-making, having regard to the present scale of operations.

The Board comprises an equal number of independent and non-independent directors. The Nominating Committee is of theview that Messrs Hwang Soo Jin, Yang Soo Suan and Dr Lee Soo Ann are independent.

Except for the Managing Director of the Company, one-third of the directors retire at every Annual General Meeting.Mr Wee Cho Yaw, the Chairman of the Board, is subject to annual re-appointment under Section 153(6) of the Companies Act.

Board Competency: The current board members possess diverse corporate experiences and, as a group, provide corecompetencies relevant to the business of the Company. In particular, two of the directors are chartered insurers. Detailedinformation on the directors’ experience and qualifications can be found on pages 11 to 12.

Guidance is given to all directors on regulatory requirements concerning disclosure of interests, restrictions on dealings insecurities and the duties and responsibilities of directors under Singapore law. Directors are briefed on changes in relevantaccounting standards. The company secretary, to whom the directors have independent access, assists the Board and keeps itapprised of relevant laws and regulations. The directors may also request independent professional advice at the Company’sexpense to help them carry out their responsibilities. The Company has a budget for directors’ training needs.

Board Meetings: The Board meets at least four times a year. Additional meetings are called when necessary. Last year, therewere four board meetings and the directors’ attendance record is set out on page 10.

Directors receive regular financial and operational reports on the Company’s business and also receive regular briefings frommanagement staff. Directors may approach senior management directly for additional information which they may need.

Chairman and Managing Director (“MD”): The Chairman of the Company is Mr Wee Cho Yaw. He provides leadershipand sets agendas for board meetings and ensures that the directors are provided with complete, adequate and timely information.

The Managing Director is Mr David Chan Mun Wai who is also the Principal Officer of the Company. Responsible for the day-to-day running of the Company, the Managing Director ensures that the Board’s decisions and strategies are translated to theworking level.

8

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

CORPORATE GOVERNANCE

Board CommitteesThere are currently three standing board committees. Each committee’s role and responsibilities are set out in a set terms ofreference approved by the Board. The membership of the three standing board committees are set out on page 6.

Nominating Committee (“NC”): The NC reviews nominations of persons for appointment to the Board and board committees.On an annual basis, the NC assesses the independence and performance of the directors and the Board. In carrying out itsassessment, the NC makes reference to a set of criteria. NC members abstain from deliberations in respect of their own nominations/assessment.

The NC meets at least once a year.

Remuneration Committee (“RC”): The RC makes recommendations to the Board on directors’ fees and allowances. RCmembers abstain from deliberations in respect of their own remuneration.

Annually, the Board submits directors’ fees as a lump sum for shareholders’ approval. The sum is divided among the directors ona basis that is reflective of the degree of responsibility borne by each. Details of the total fees and other remuneration of thedirectors are set out on page 10.

The Code recommends that the chairman of the RC should be an independent and non-executive director. In the case of theCompany’s RC, the Board is of the view that Mr Wee Cho Yaw is the best person to chair the RC.

The RC meets at least once a year.

Audit Committee (“AC”): The AC carries out the functions set out in the Code and Companies Act. The AC’s terms ofreference include reviewing the financial statements, the internal and external audit plans and audit reports, the external auditors’evaluation of the system of internal accounting controls, the scope and results of the internal and external audit procedures, theadequacy of internal audit resources, the cost effectiveness, independence and objectivity of external auditors, the significantfindings of internal audit investigations and interested person transactions. The reviews are made with the internal and externalauditors, the financial controller and/or other senior management staff, as appropriate. The AC has reviewed the adequacy ofthe internal controls with the internal and external auditors and submitted its report to the Board.

The AC also reviews the financial, business and professional relationships between the external auditors and the Company.External auditors are requested to affirm annually that their independence and objectivity has not been affected by any businessor other relationship with the Group. If there are non-audit services provided by the external auditors to the Group, the AC willform its own view on whether the volume and nature of the non-audit services are such as may be likely to affect the independenceand objectivity of the external auditors. Annually, the AC also nominates the external auditors for re-appointment. This year, theAC has recommended that Messrs Ernst & Young be nominated as auditors for shareholders’ approval at the forthcomingAnnual General Meeting because the Company’s parent, United Overseas Bank Limited, is nominating Messrs Ernst & Young forappointment as auditors and SGX Listing Rules require a subsidiary to have the same auditors as its parent.

The AC has the power to conduct or authorise investigations into any matter within its terms of reference and is given reasonableresources for the proper discharge of its duties.

The AC meets separately with the internal auditor and the external auditors and also meet among themselves, in the absence ofmanagement, when necessary. Last year, the AC held five meetings.

Internal AuditThe Company’s internal audit function is provided by the internal audit team of its parent company, United Overseas BankLimited (UOB). The UOB Internal Audit has adopted the Standards for the Professional Practice of Internal Auditing set by theInstitute of Internal Auditors. The internal auditor’s primary line of reporting is to the Chairman of the AC but the internalauditor also reports administratively to the Chairman of the Board. The AC has reviewed the adequacy of the internal auditfunction and is assured that the internal audit function is adequately resourced to perform the necessary functions for theCompany.

9

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

Managing RisksThe Board considers the management of key business risks to be an important and integral part of the Company’s overallinternal control framework. The Company identifies operational and business risks and manages such risks. The Company’s riskplanning and strategy review procedures cover broadly the areas of Underwriting Risk, Performance or Credit Risk of Agency/Agents/Brokers and Reinsurers, Risk of Fraudulent Claims or Inadequate Claim Reserving, Regulatory Risk, Technology Risk andOperations Risk. Various committees, comprising senior executive staff who are responsible for the Company’s businesses, meetregularly to evaluate and approve business and operational matters, including that of risk exposures. Policies on risk for theCompany’s businesses are formulated and these are communicated through risk limits and operational procedures to the variousbusiness units.

The Underwriting Risk is the main risk that arises from the Company’s core general insurance business. In return for a premiumcharge, the insurer assumes a portfolio of risks. Given the complexity of the business environment which is influenced by thepolitical, social, economic and environmental dynamic factors, it is not always possible to charge premiums that accuratelymatch the ultimate financial liability that can arise in future from each and every insurance contract. Any miscalculation in thepremium charged for a contract coupled with the fortuitous nature of risks can give rise to financial loss. To manage suchpossibilities, underwriters have to possess the necessary expertise and experience to assess and rate the individual risks.

In addition, the portfolio of risks will have to be spread and the risk exposure balanced across a portfolio of businesses ofdifferent classes and from diverse territories. Such spreading of risks require the judicious use of reinsurance as a risk managementmechanism that transfers the risks to other reinsurers or retrocessionaires from whom the highest standards of claims paymentcapabilities are expected since they provide the last line of recourse.

The Company must be able to estimate its outstanding claims liabilities so that comprehensive procedures and controls can beput in place to ensure the provisions are adequate to meet the Company’s future liabilities. Furthermore, the appointment ofgeneral insurance actuaries to certify the level of general insurance liabilities, that is, unearned premium reserves and outstandingclaims provision, provide yet another measure for ensuring claims provisions are adequately set in accordance with establishedactuarial principles.

The other major area of risks pertains to Credit Risk, which represents the exposure arising in the event any of the Company’sbusiness partners, namely insurance intermediaries, should fail to meet their contractual obligations. In the case of the Company’score general insurance operations, credit risk may arise if an insurance intermediary fails to meet its premium payment obligations,or if a reinsurer or retrocessionaire is unable to pay a claim. The Company views the management of credit risk as a fundamentaland critical part of operations and therefore adopts a very selective policy as regards the choice of its business partners. A CreditControl Committee, chaired by the Principal Officer, meets regularly to review the debtors’ ageing and assess the credit-worthinessof its business partners. Security vetting of its reinsurance and retrocession partners are conducted regularly when the Company’sreinsurance programmes are put in place and when a new reinsurer or retrocessionaire is chosen as a business partner. Similarly,in the managing of its funds, the Company works closely with its investment manager to comply with investment policies laiddown by the Board. In particular, the Company adopts a stringent set of quantitative and qualitative criteria, including financialstatement analysis, type of securities, credit ratings, quality of management as well as investment limits, in selecting issuers offinancial instruments that the Company invests in.

Communication with ShareholdersThe Board keeps shareholders updated on the business and affairs of the Company through the quarterly release of the Company’sresults and the timely release of relevant information through the MASNET of the Singapore Exchange. The Company’s annualreport is also available on the SGX website. Shareholders may raise relevant questions and communicate their views at shareholders’meetings. The Company does not practise selective disclosure of information.

10

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

Best Practices GuideAs part of its corporate governance, the Company has adopted the SGX-ST’s Best Practices Guide with respect to dealings insecurities and has a Code on dealings in Securities for the guidance of its directors.

Interested Person TransactionsDuring the financial year 2003, the Company entered into the following transactions with Overseas Union Insurance, Limited(“OUI”):

(a) An agreement for the transfer of the main part of OUI’s current business to the Company. In consideration of the transferof business together with its attendant liabilities, OUI will transfer to the Company cash provisions in an amount equal tomeet these liabilities. For a period of three years after the transfer, the Company and OUI would share the underwritingprofits derived from the transferred business with OUI’s share capped at 5% of the UOI Group’s latest audited net tangibleassets, less $10. Details of the transfer can be found in the Company’s announcement of 6 August 2003.

(b) An agreement for a 3-year lease of units at Springleaf Tower by OUI to the Company at market rate, with total rentalamounting to $1,289,070 which is less than 3% of the Group’s net tangible assets.

Directors’ Attendance for 2003

Number of Meetings Attended in 2003

Board of Audit Nominating RemunerationName of Director Directors Committee Committee Committee

Mr Wee Cho Yaw 4 – 1 1

Mr David Chan Mun Wai 4 – – –

Mr Wee Ee Cheong 4 – – –

Mr Hwang Soo Jin 4 5 1 1

Mr Yang Soo Suan 4 5 1 1

Dr Lee Soo Ann 3 5 – –

Number of Meetings Held in 2003 4 5 1 1

Directors Fees and Other RemunerationThe details of the total fees and other remuneration paid/payable by the Company to the directors for the financial year 2003 areas follows:

Directors’ Base or Variable Benefits-in-kindfees fixed salary performance bonus and others Total

% % % % %

$250,000 to $499,999

Mr David Chan Mun Wai 2.8 65.4 18.0 13.8 100.0

Below $250,000

Mr Wee Cho Yaw 100.0 – – – 100.0

Mr Wee Ee Cheong 100.0 – – – 100.0

Mr Hwang Soo Jin 100.0 – – – 100.0

Mr Yang Soo Suan 100.0 – – – 100.0

Dr Lee Soo Ann 100.0 – – – 100.0

CORPORATE GOVERNANCE

11

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

BOARD OF DIRECTORS

Mr Wee Cho Yaw

Chairman

Age 75. A career banker with more than 40 years of

experience. Received Chinese high school education.

Chairman of United Overseas Insurance since 1971.

Appointed to the Board on 17 February 1971. Last

re-appointed as a Director on 8 May 2003. Non-independent

and non-executive Director. Chairman of the Remuneration

Committee and member of the Nominating Committee.

Chairman & CEO of United Overseas Bank since 1974, and

Chairman of its subsidiary, Far Eastern Bank. Chairman of

United International Securities, Haw Par Corporation,

United Overseas Land, Hotel Plaza, Overseas Union

Enterprise, United Industrial Corporation, and Singapore

Land and its subsidiary, Marina Centre Holdings. Former

Director of Singapore Press Holdings.

Member of the Asia-Pacific Advisory Committee, New York

Stock Exchange. Honorary President of Singapore Chinese

Chamber of Commerce & Industry. Named Businessman Of

The Year in 2002 and 1989 in the Singapore Business Awards

that recognise outstanding achievements by Singapore’s

business community.

Mr Wee Ee Cheong

Age 51. A professional banker with more than 20 years of

experience.

Appointed to the Board on 20 March 1991. Last re-elected

as a Director on 9 May 2002. Non-independent and

non-executive Director. Deputy Chairman & President of

United Overseas Bank since 2000. Director of several

subsidiaries and affiliates of United Overseas Bank, including

Far Eastern Bank, United International Securities, United

Overseas Land and Hotel Plaza. Director of Visa International

(Asia Pacific Regional Association) and the Institute of

Banking & Finance. Council Member of the Association of

Banks in Singapore and Singapore Chinese Chamber of

Commerce & Industry. Has served as Deputy Chairman of

Housing & Development Board and Director of Port of

Singapore Authority.

Holds a Bachelor of Science (Business Administration) and

Master of Arts (Applied Economics) from The American

University, Washington DC.

Mr David Chan Mun Wai

Managing Director & Principal Officer

Age 49. A professional insurer with more than 20 years of

experience.

Appointed to the Board on 10 March 1994. Executive and

non-independent Director. Director and member of the

Executive Committee of Singapore Reinsurance Corporation.

Member of the Management Committee of the General

Insurance Association of Singapore.

A Chartered Insurer and Fellow of the Chartered Insurance

Institution. Holds a Bachelor of Business Administration from

the National University of Singapore.

12

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

Mr Hwang Soo Jin

Age 68. A Chartered Insurer with more than 40 years of

professional experience.

Appointed to the Board on 17 February 1971. Last re-elected

as a Director on 8 May 2003. Independent and non-

executive Director. Chairman of the Nominating Committee

and member of the Audit Committee and Remuneration

Committee. Chairman of Singapore Reinsurance

Corporation. Director of Haw Par Corporation, United

Industrial Corporation, Singapore Land, Lee Kim Tah

Holdings and India International Insurance. A Justice of

Peace, Adviser to the Asean Insurance Council and Honorary

Fellow of the Singapore Insurance Institute. Former

Chairman of the Public Accounts Committee of the

Parliament of Singapore.

A Chartered Insurer of the Chartered Insurance Institute,

UK.

Dr Lee Soo Ann

Age 65. An economist in the government and academia

with more than 40 years of experience.

Appointed to the Board on 16 February 2000. Last re-elected

as a Director on 24 May 2000. Independent and

non-executive Director. Member of the Audit Committee.

Director of United International Securities and Overseas

Union Securities. Fellow of the Singapore Institute of

Directors and part-time Senior Fellow in the Department of

Economics, National University of Singapore.

Holds a Bachelor of Arts (Honours) in Economics from The

University of Malaya in Singapore, a Master of Arts (with

Distinction) in Development Economics from Williams

College, Massachusetts, a Master of Christian Studies from

Regent College, Vancouver and a PhD from the University

of Singapore.

Mr Yang Soo Suan

Age 67. An architect by training with more than 35 years

of professional experience.

Appointed to the Board on 20 March 1991. Last re-elected

as a Director on 24 May 2001. Independent and non-

executive Director. Chairman of the Audit Committee and

member of the Nominating Committee and Remuneration

Committee. Director of United International Securities and

Overseas Union Securities. Retired in 2003 as Chairman of

Architects 61. Appointed Senior Advisor to RSP Architects

Planners & Engineers in 2004. Former Board Member of

Housing & Development Board and former Chairman of the

National Fire Prevention Council. Former Member of the

Board of Architects. Fellow of the Singapore Institute of

Architects. Fellow of the Singapore Society of Project

Managers. Member of the Singapore Institute of Directors.

Holds a Bachelor of Architecture (Honours) in Design, Town

Planning and Building from Melbourne University, Australia.

Awarded BBM in 1996 for Public Service.

BOARD OF DIRECTORS

13

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

DIRECTORS’ REPORTfor the financial year ended 31 December 2003

The directors present their report to the members together with the audited financial statements of the Company and of theGroup for the financial year ended 31 December 2003.

DirectorsThe directors of the Company holding office at the date of this report are:

Mr Wee Cho YawMr David Chan Mun WaiMr Wee Ee CheongMr Hwang Soo JinMr Yang Soo SuanDr Lee Soo Ann

Arrangements to enable directors to acquire shares or debenturesNeither at the end of nor at any time during the financial year was the Company a party to any arrangement whose object wasto enable the directors of the Company to acquire benefits through the acquisition of shares in, or debentures of, the Companyor any other body corporate.

Directors’ interests in shares and share options(a) According to the register of directors’ shareholdings required to be kept under Section 164 of the Singapore Companies

Act, the directors who held office at 31 December 2003 and who held interests in the share capital of the Company andrelated corporations were as follows:

Number of ordinary shares of $1 eachShareholdings in

Shareholdings registered which directors arein name of directors deemed to have an interest

At 31.12.2003 At 1.1.2003 At 31.12.2003 At 1.1.2003United Overseas Insurance LimitedMr Wee Cho Yaw 25,400 25,400 – –Mr Hwang Soo Jin 72,000 72,000 – –

United Overseas Bank LimitedMr Wee Cho Yaw 16,390,248 16,390,248 210,608,142 209,258,142Mr Wee Ee Cheong 2,794,899 2,794,899 144,985,251 143,985,251Mr David Chan Mun Wai 5,600 5,600 – –

(b) There was no change in any of the above-mentioned interests between the end of the financial year and21 January 2004 (being the 21st day after the end of the financial year) except as follows:

Number of ordinary shares of $1 each

Shareholdings in whichdirectors are deemed to have an interest

At 21.1.2004United Overseas Bank LimitedMr Wee Cho Yaw 210,808,142Mr Wee Ee Cheong 145,185,251

14

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

DIRECTORS’ REPORTfor the financial year ended 31 December 2003

Directors’ contractual benefitsSince the end of the previous financial year, no director has received or become entitled to receive a benefit (other than asdisclosed in this report or in the consolidated financial statements) by reason of a contract made by the Company or a relatedcorporation with the director or with a firm of which he is a member or with a company in which he has a substantial financialinterest, except that the directors received remuneration from related corporations in their capacities as directors and/orexecutives of those related corporations.

Share optionsThere were no share options granted by the Company or its subsidiary during the financial year.

No shares have been issued during the financial year by virtue of the exercise of options to take up unissued shares of theCompany or its subsidiary.

There were no unissued shares in the Company or its subsidiary under option at 31 December 2003.

Audit committeeThe Audit Committee comprises three members, all of whom are non-executive independent directors. The members of theAudit Committee are:

Mr Yang Soo SuanMr Hwang Soo JinDr Lee Soo Ann

In its report to the Board of Directors, the Audit Committee reports that it has reviewed with the Company’s internal auditorstheir audit plans and the scope and results of the Company’s internal audit procedures. The Audit Committee has alsoreviewed with the Company’s auditors, PricewaterhouseCoopers, their audit plan, their evaluation of the system of internalaccounting controls, their management letter and the response of management thereto as well as their audit report on thefinancial statements of the Company and the consolidated financial statements of the Group for the year ended31 December 2003. The financial statements of the Company and the consolidated financial statements of the Group for theyear ended 31 December 2003 have been reviewed by the Committee prior to their submission to the Board of Directors. TheAudit Committee has also reviewed the Company’s position with regard to interested person transactions and the assistancegiven by the Company’s officers, in particular the Company’s internal auditors and financial controller, toPricewaterhouseCoopers.

At the date of this report, the Audit Committee is reviewing the nomination of an external audit firm for appointment asauditors of the Company by shareholders at the forthcoming Annual General Meeting.

On behalf of the directors

Wee Cho Yaw David Chan Mun WaiChairman Managing Director

20 February 2004

15

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

In the opinion of the directors:

(a) the accompanying financial statements of the Company and consolidated financial statements of the Group as set outon pages 17 to 42, are drawn up so as to give a true and fair view of the state of affairs of the Company and of theGroup at 31 December 2003, the results of the business and changes in equity of the Company and of the Group andthe cash flows of the Group for the financial year then ended; and

(b) at the date of this statement, there are reasonable grounds to believe that the Company will be able to pay its debts asand when they fall due.

On behalf of the directors

Wee Cho Yaw David Chan Mun WaiChairman Managing Director

20 February 2004

STATEMENT BY DIRECTORSfor the financial year ended 31 December 2003

16

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

We have audited the financial statements of United Overseas Insurance Limited and the consolidated financial statements ofthe Group for the financial year ended 31 December 2003 set out on pages 17 to 42. These financial statements are theresponsibility of the Company’s directors. Our responsibility is to express an opinion on these financial statements based onour audit.

We conducted our audit in accordance with Singapore Standards on Auditing. Those Standards require that we plan andperform our audit to obtain reasonable assurance whether the financial statements are free of material misstatement. Anaudit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Anaudit also includes assessing the accounting principles used and significant estimates made by the directors, as well as evaluatingthe overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion,

(a) the accompanying financial statements of the Company and consolidated financial statements of the Group are properlydrawn up in accordance with the provisions of the Companies Act, Cap. 50 (the “Act”) and Singapore Financial ReportingStandards to give a true and fair view of the state of affairs of the Company and of the Group as at31 December 2003 and the results and changes in equity of the Company and of the Group, and the cash flows of theGroup for the financial year ended on that date; and

(b) the accounting and other records (excluding registers) required by the Act to be kept by the Company have beenproperly kept in accordance with the provisions of the Act.

We have considered the financial statements and auditors’ report of UOB Insurance (H.K.) Limited, which are audited byanother member firm of the worldwide PricewaterhouseCoopers organisation, being financial statements included in theconsolidated financial statements.

We are satisfied that the financial statements of the subsidiary that have been consolidated with the financial statements ofthe Company are in form and content appropriate and proper for the purposes of the preparation of the consolidatedfinancial statements and we have received satisfactory information and explanations as required by us for those purposes.

The auditors’ report on the financial statements of the subsidiary was not subject to any qualification.

PricewaterhouseCoopersCertified Public Accountants

Singapore, 20 February 2004

AUDITORS’ REPORT TO THE MEMBERS OF UNITED OVERSEAS INSURANCE LIMITEDfor the financial year ended 31 December 2003

17

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

The Group The Company

Note 2003 2002 2003 2002$’000 $’000 $’000 $’000

Insurance underwriting profit transferredfrom insurance revenue account 6,254 5,715 6,274 5,774

Other income:Gross dividends from investments 4(a) 2,613 1,746 2,670 1,803Interest income from investments 4(b) 1,765 1,906 1,765 1,906Interest on fixed deposits and

bank balances from:- Holding company 128 204 70 102- Fellow subsidiaries 17 21 17 21- Other financial institutions 84 114 79 107

Miscellaneous income 14 24 13 24Profit/(loss) on sale of investments 882 (427) 882 (427)Loss on sale of fixed assets (28) – (28) –

5,475 3,588 5,468 3,536Add/(Less)Management expenses not charged

to insurance revenue account: 5- Management fees (362) (391) (362) (391)- Other operating expenses (287) (297) (286) (296)

Exchange differences (27) (35) – (35)Write-back of provision/(provision) for

diminution in value of investments 1,211 (1,099) 1,211 (1,099)

Profit before taxation 12,264 7,481 12,305 7,489Taxation 8 (2,364) (1,200) (2,364) (1,200)

Net profit 9,900 6,281 9,941 6,289

Earnings per $1 share 9 24 cents 15 cents

The accompanying notes form an integral part of these financial statements.Auditors’ report – page 16.

INCOME STATEMENTSfor the financial year ended 31 December 2003

18

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

The GroupGeneral 2003 2002

Note Fire accident Marine Total Total$’000 $’000 $’000 $’000 $’000

Gross premium written 16,830 23,856 1,583 42,269 38,098Reinsurance premium ceded (9,554) (18,965) (941) (29,460) (24,934)

Net premium written 7,276 4,891 642 12,809 13,164Movement in net unearned

premium reserves 12 (543) (90) (3) (636) (1,758)

Net earned premiums 6,733 4,801 639 12,173 11,406

LessGross claims paid 3,457 6,188 314 9,959 10,006Reinsurance claims recoveries (2,860) (2,772) (135) (5,767) (4,865)

Net claims paid 13 597 3,416 179 4,192 5,141Change in net outstanding claims 168 68 76 312 (546)

Net claims incurred 13 765 3,484 255 4,504 4,595

Gross commission 2,655 2,816 330 5,801 5,910Reinsurance commission (3,394) (4,619) (407) (8,420) (9,291)

Net commission (739) (1,803) (77) (2,619) (3,381)Management expenses: 5

Staff cost 6 1,436 980 128 2,544 2,566Rental expenses 359 244 32 635 592Management fees 105 13 3 121 123Other operating expenses 443 257 34 734 1,196

Total expenses 2,369 3,175 375 5,919 5,691

Insurance underwriting profittransferred to income statement 4,364 1,626 264 6,254 5,715

The accompanying notes form an integral part of these financial statements.Auditors’ report – page 16.

INSURANCE REVENUE ACCOUNTSfor the financial year ended 31 December 2003

19

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

The CompanyGeneral 2003 2002

Note Fire accident Marine Total Total$’000 $’000 $’000 $’000 $’000

Gross premium written 16,590 23,629 1,577 41,796 37,652Reinsurance premium ceded (9,438) (18,754) (939) (29,131) (24,643)

Net premium written 7,152 4,875 638 12,665 13,009Movement in net unearned

premium reserves 12 (549) (95) (3) (647) (1,744)

Net earned premiums 6,603 4,780 635 12,018 11,265

LessGross claims paid 3,439 6,187 314 9,940 9,962Reinsurance claims recoveries (2,848) (2,771) (135) (5,754) (4,824)

Net claims paid 13 591 3,416 179 4,186 5,138Change in net outstanding claims 173 66 76 315 (560)

Net claims incurred 13 764 3,482 255 4,501 4,578

Gross commission 2,572 2,791 328 5,691 5,791Reinsurance commission (3,306) (4,555) (406) (8,267) (9,138)

Net commission (734) (1,764) (78) (2,576) (3,347)Management expenses: 5

Staff cost 6 1,436 980 128 2,544 2,566Rental expenses 359 244 32 635 592Other operating expenses 361 246 33 640 1,102

Total expenses 2,186 3,188 370 5,744 5,491

Insurance underwriting profittransferred to income statement 4,417 1,592 265 6,274 5,774

The accompanying notes form an integral part of these financial statements.Auditors’ report – page 16.

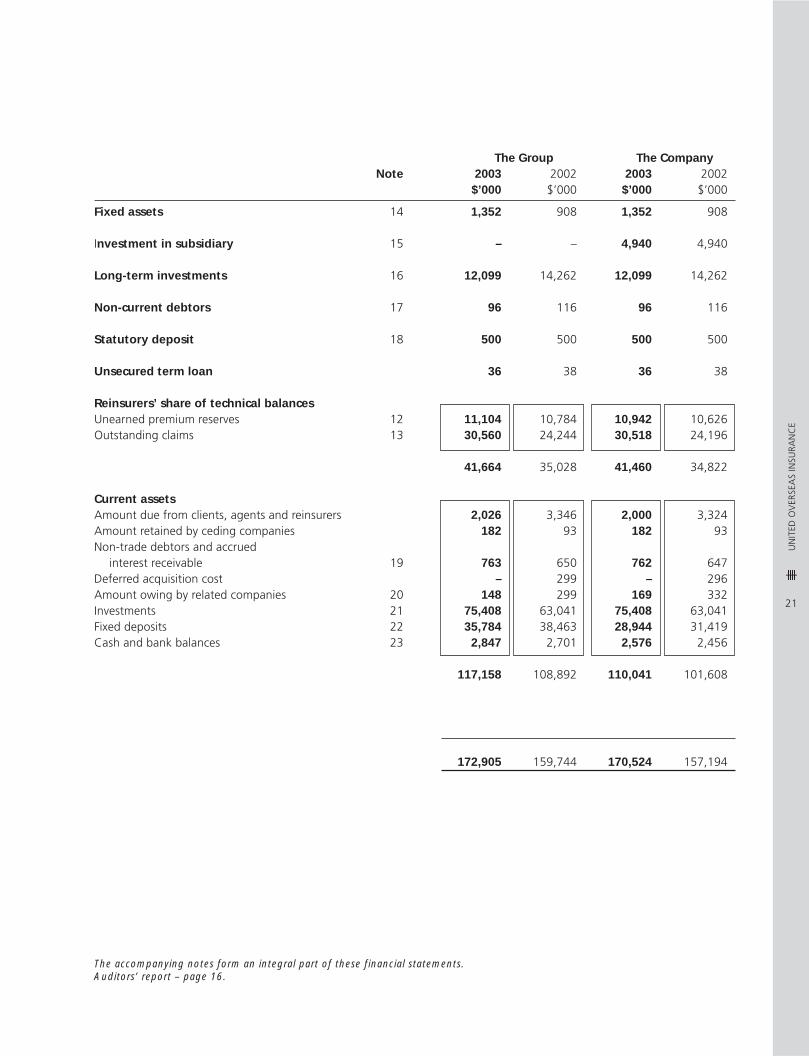

20

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

The Group The CompanyNote 2003 2002 2003 2002

$’000 $’000 $’000 $’000

Share capitalOrdinary shares of $1 each

Authorised 50,000 50,000 50,000 50,000

Issued and fully paid 40,770 40,770 40,770 40,770

ReservesGeneral reserve 14,880 13,880 14,880 13,880Foreign currency translation reserve 500 610 – –Retained profits 41,614 39,074 40,120 37,539

56,994 53,564 55,000 51,419

Total capital and reserves 97,764 94,334 95,770 92,189

Deferred taxation 11 357 272 357 272

Technical balancesUnearned premium reserves 12 17,961 18,043 17,740 17,812Outstanding claims 13 46,169 39,541 46,088 39,451

64,130 57,584 63,828 57,263

Current liabilities and provisionsAmount owing to agents and reinsurers 5,090 4,217 5,050 4,179Non-trade creditors and accrued liabilities 2,205 1,530 2,157 1,484Deferred acquisition cost 736 – 739 –Amount owing to a related

company – non-trade 83 96 83 96Taxation 2,540 1,711 2,540 1,711

10,654 7,554 10,569 7,470

172,905 159,744 170,524 157,194

BALANCE SHEETSas at 31 December 2003

21

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

The Group The CompanyNote 2003 2002 2003 2002

$’000 $’000 $’000 $’000

Fixed assets 14 1,352 908 1,352 908

Investment in subsidiary 15 – – 4,940 4,940

Long-term investments 16 12,099 14,262 12,099 14,262

Non-current debtors 17 96 116 96 116

Statutory deposit 18 500 500 500 500

Unsecured term loan 36 38 36 38

Reinsurers’ share of technical balancesUnearned premium reserves 12 11,104 10,784 10,942 10,626Outstanding claims 13 30,560 24,244 30,518 24,196

41,664 35,028 41,460 34,822

Current assetsAmount due from clients, agents and reinsurers 2,026 3,346 2,000 3,324Amount retained by ceding companies 182 93 182 93Non-trade debtors and accrued

interest receivable 19 763 650 762 647Deferred acquisition cost – 299 – 296Amount owing by related companies 20 148 299 169 332Investments 21 75,408 63,041 75,408 63,041Fixed deposits 22 35,784 38,463 28,944 31,419Cash and bank balances 23 2,847 2,701 2,576 2,456

117,158 108,892 110,041 101,608

172,905 159,744 170,524 157,194

The accompanying notes form an integral part of these financial statements.Auditors’ report – page 16.

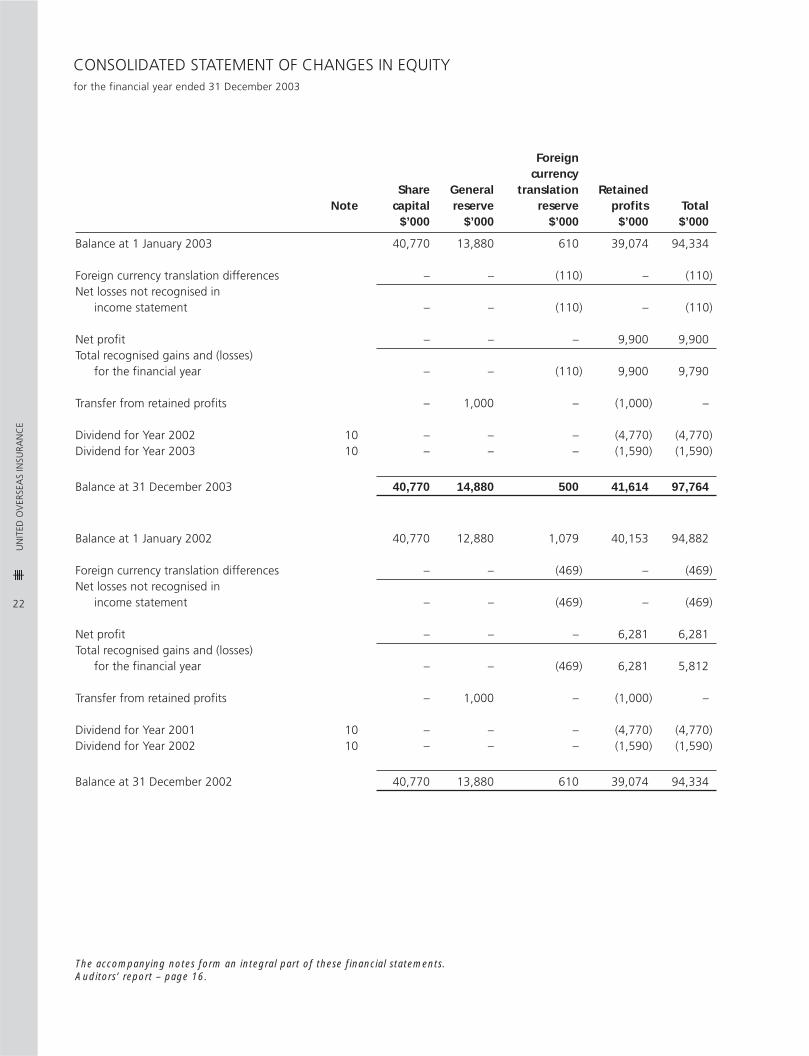

22

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

Foreigncurrency

Share General translation RetainedNote capital reserve reserve profits Total

$’000 $’000 $’000 $’000 $’000

Balance at 1 January 2003 40,770 13,880 610 39,074 94,334

Foreign currency translation differences – – (110) – (110)Net losses not recognised in

income statement – – (110) – (110)

Net profit – – – 9,900 9,900Total recognised gains and (losses)

for the financial year – – (110) 9,900 9,790

Transfer from retained profits – 1,000 – (1,000) –

Dividend for Year 2002 10 – – – (4,770) (4,770)Dividend for Year 2003 10 – – – (1,590) (1,590)

Balance at 31 December 2003 40,770 14,880 500 41,614 97,764

Balance at 1 January 2002 40,770 12,880 1,079 40,153 94,882

Foreign currency translation differences – – (469) – (469)Net losses not recognised in

income statement – – (469) – (469)

Net profit – – – 6,281 6,281Total recognised gains and (losses)

for the financial year – – (469) 6,281 5,812

Transfer from retained profits – 1,000 – (1,000) –

Dividend for Year 2001 10 – – – (4,770) (4,770)Dividend for Year 2002 10 – – – (1,590) (1,590)

Balance at 31 December 2002 40,770 13,880 610 39,074 94,334

The accompanying notes form an integral part of these financial statements.Auditors’ report – page 16.

CONSOLIDATED STATEMENT OF CHANGES IN EQUITYfor the financial year ended 31 December 2003

23

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

Share General RetainedNote capital reserve profits Total

$’000 $’000 $’000 $’000

Balance at 1 January 2003 40,770 13,880 37,539 92,189

Total recognised gain for the financial year- Net profit – – 9,941 9,941

Transfer from retained profits – 1,000 (1,000) –

Dividend for Year 2002 10 – – (4,770) (4,770)Dividend for Year 2003 10 – – (1,590) (1,590)

Balance at 31 December 2003 40,770 14,880 40,120 95,770

Balance at 1 January 2002 40,770 12,880 38,610 92,260

Total recognised gain for the financial year- Net profit – – 6,289 6,289

Transfer from retained profits – 1,000 (1,000) –

Dividend for Year 2001 10 – – (4,770) (4,770)Dividend for Year 2002 10 – – (1,590) (1,590)

Balance at 31 December 2002 40,770 13,880 37,539 92,189

The accompanying notes form an integral part of these financial statements.Auditors’ report – page 16.

STATEMENT OF CHANGES IN EQUITY – COMPANYfor the financial year ended 31 December 2003

24

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

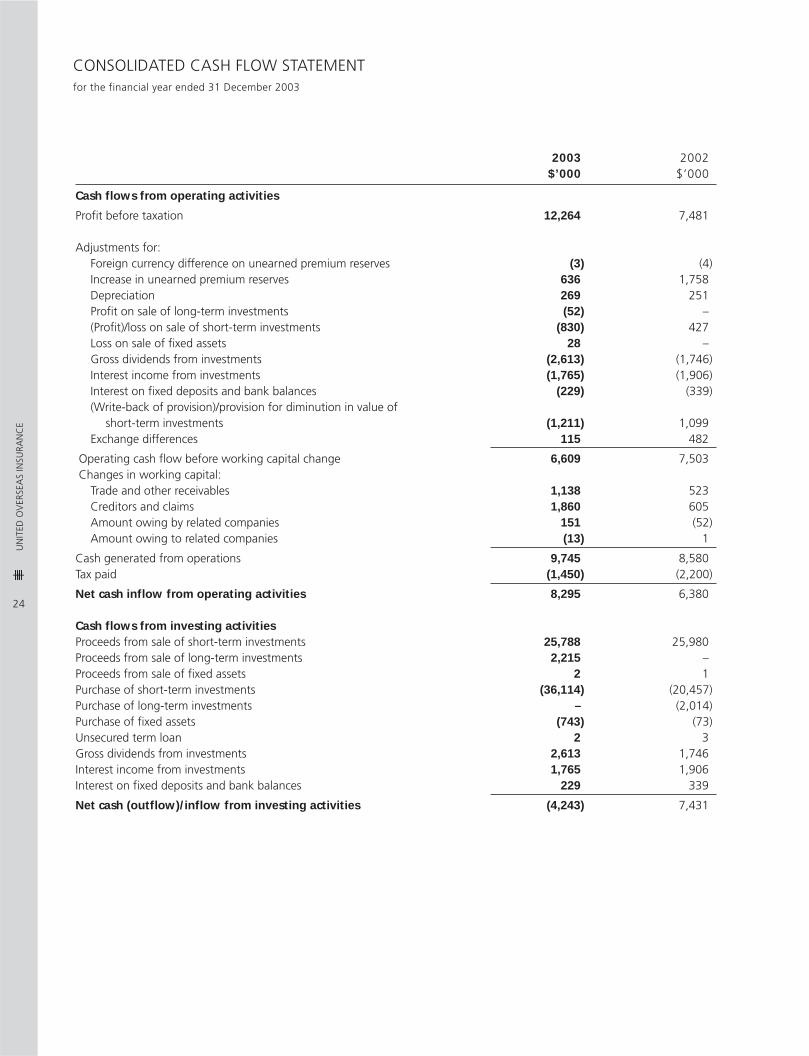

CONSOLIDATED CASH FLOW STATEMENTfor the financial year ended 31 December 2003

2003 2002$’000 $’000

Cash flows from operating activities

Profit before taxation 12,264 7,481

Adjustments for:Foreign currency difference on unearned premium reserves (3) (4)Increase in unearned premium reserves 636 1,758Depreciation 269 251Profit on sale of long-term investments (52) –(Profit)/loss on sale of short-term investments (830) 427Loss on sale of fixed assets 28 –Gross dividends from investments (2,613) (1,746)Interest income from investments (1,765) (1,906)Interest on fixed deposits and bank balances (229) (339)(Write-back of provision)/provision for diminution in value of

short-term investments (1,211) 1,099Exchange differences 115 482

Operating cash flow before working capital change 6,609 7,503 Changes in working capital:

Trade and other receivables 1,138 523Creditors and claims 1,860 605Amount owing by related companies 151 (52)Amount owing to related companies (13) 1

Cash generated from operations 9,745 8,580Tax paid (1,450) (2,200)

Net cash inflow from operating activities 8,295 6,380

Cash flows from investing activitiesProceeds from sale of short-term investments 25,788 25,980Proceeds from sale of long-term investments 2,215 –Proceeds from sale of fixed assets 2 1Purchase of short-term investments (36,114) (20,457)Purchase of long-term investments – (2,014)Purchase of fixed assets (743) (73)Unsecured term loan 2 3Gross dividends from investments 2,613 1,746Interest income from investments 1,765 1,906Interest on fixed deposits and bank balances 229 339

Net cash (outflow)/inflow from investing activities (4,243) 7,431

25

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

2003 2002$’000 $’000

Cash flow from financing activityDividend paid (6,360) (6,360)

Cash outflow from financing activity (6,360) (6,360)Translation difference on foreign subsidiary company (110) (469)

Net (decrease)/increase in cash and cash equivalents (2,418) 6,982Cash and cash equivalents at beginning of year (Note A) 41,164 34,664Effects of exchange rate changes on cash and cash equivalents (115) (482)

Cash and cash equivalents at end of year (Note A) 38,631 41,164

Note A:Cash and Cash EquivalentsCash and cash equivalents included in the consolidated cash flow statement comprise the following balance sheet amounts:

2003 2002$’000 $’000

Cash and bank balances 2,847 2,701 Fixed deposits 35,784 38,463

38,631 41,164

The accompanying notes form an integral part of these financial statements.Auditors’ report – page 16.

26

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

NOTES TO THE FINANCIAL STATEMENTSfor the financial year ended 31 December 2003

These notes form an integral part of and should be read in conjunction with the accompanying financial statements.

1 GeneralThe Company is domiciled and incorporated in Singapore and is listed on the Singapore Exchange. The address of theCompany’s registered office is as follows:

80 Raffles PlaceUOB PlazaSingapore 048624

The address of the Company’s principal place of business is as follows:

3 Anson Road#28-01 Springleaf TowerSingapore 079909

2 Significant accounting policies(a) Effect of changes in Singapore Companies Legislation

Pursuant to the Singapore Companies (Amendment) Act 2002, with effect from financial years commencing on orafter 1 January 2003, Singapore incorporated companies are required to prepare and present their statutoryaccounts in accordance with the Singapore Financial Reporting Standards (“FRS”). Hence, these financial statements,including the comparatives figures, have been prepared in accordance with FRS.

Previously, the Company and the Group prepared their statutory accounts in accordance with Singapore Statementsof Accounting Standards. The adoption of FRS does not have a material impact on the accounting policies andfigures presented in the statutory accounts for the financial year ended 31 December 2002.

(b) Basis of preparationThe financial statements are prepared in accordance with the historical cost convention.

The preparation of financial statements in conformity with Singapore Financial Reporting Standards requires theuse of estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure ofcontingent assets and liabilities at the date of the financial statements and the reported amounts of revenues andexpenses during the year. Although these estimates are based on management’s best knowledge of current eventand actions, actual results may ultimately differ from those estimates.

(c) Basis of consolidationThe consolidated financial statements include the financial statements of the Company and its subsidiary made upto the end of the financial year. Intercompany balances and transactions and resulting unrealised profits or lossesare eliminated in full on consolidation.

(d) Revenue recognition(i) Premium income

Premium is taken up as income at the time a policy is issued, regardless of the period covered by the policy.

Treaty reinsurance is taken up in the revenue account based on statements received up to the time of closingof the books.

(ii) Investment incomeDividend income is recognised when such dividends are declared. Interest income is accounted for on anaccrual basis. Profits or losses on disposal of investments are taken to the income statement.

27

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

2 Significant accounting policies (continued)(e) Unearned premium reserves

(i) Unearned premium reserves, other than for marine cargo and inward treaties, are calculated using the1/24th method based on gross premiums written less premiums on reinsurances in Singapore and premiumson which reinsurers’ deposits are held. Deferred acquisition costs are calculated using the 1/24th method onactual commission.

(ii) Unearned premium reserves on marine cargo direct business are calculated at 25% of the gross premiumswritten less premiums on reinsurances in Singapore and premiums on which reinsurers’ deposits are held.

(iii) Unearned premium reserves on inward treaties are calculated at 40% of gross premiums written less premiumson reinsurances in Singapore.

(f) ClaimsProvision is made for the estimated costs of all claims notified but not settled at the date of the balance sheet, lessreinsurance recoveries, using the best information available at that time. Any difference between the estimatedcost and subsequent settlement is dealt with in the revenue account of the year in which settlement takes place.For reinsurance, an additional provision is made based on developmental trends as discerned in the running-off ofoutstanding claims in respect of prior underwriting years.

(g) ProvisionProvisions are recognised when the Group has a legal or constructive obligation as a result of past events, it isprobable than an outflow of resources will be required to settle the obligation, and a reliable estimate of theamount can be made.

(h) DebtorsBad debts are written off and specific provisions are made for those debts considered to be doubtful. Generalprovisions are made on the balance of trade debtors to cover unexpected losses which have not been specificallyidentified.

(i) Fixed assets and depreciationDepreciation is calculated so as to write off the cost of fixed assets on a straight-line basis over the expected usefullives of the assets concerned. The annual rates used for this purpose are:

%

Furniture and fixtures 10Renovation 20Office equipment 20Motor vehicles 20

28

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

NOTES TO THE FINANCIAL STATEMENTSfor the financial year ended 31 December 2003

2 Significant accounting policies (continued)(j) Investments

(i) Investments that are intended to be held for the long term, including investment in subsidiary, are stated atcost less impairment losses in the Company’s balance sheet. Where an indication of impairment exists, thecarrying amount of the investment is assessed and written down to its recoverable amount.

(ii) Short-term quoted investments are stated at the lower of cost and market value and short-term unquotedinvestments are stated at the lower of cost and net realisable value, determined on an aggregate basis.

Short-term quoted investments comprise equity shares, debentures, Singapore Government securities andother government securities.

Short-term unquoted investments comprise unit trusts and debentures.

(iii) Cost is determined on the weighted average method.

(k) Foreign currency translation(i) Measurement currency

Items included in the financial statement of each entity in the Group are measured using the currency thatbest reflects the economic substance of the underlying events and circumstances relevant to that entity(“the measurement currency”). The financial statements of the Company and the Group are presented inSingapore dollars, which is the measurement currency of the Company.

(ii) Transactions and balances and foreign subsidiary companiesForeign currency monetary assets and liabilities, including those in foreign subsidiary companies, are convertedto Singapore dollars at the rates of exchange ruling at the balance sheet date. Foreign currency transactionsduring the year are converted into the measurement currency using the rates of exchange ruling on thetransaction dates and the results of foreign subsidiary companies are converted at the rates of exchangeruling on the balance sheet date. Exchange differences are taken up in the insurance revenue account or tothe income statement as appropriate except for those arising from the retranslation of the opening netinvestment in foreign subsidiary companies, which are taken directly to the foreign currency translationreserve.

(l) Forward contractsForward exchange contracts are undertaken for hedging purposes and are valued at the closing settlement prices.Resulting profits and losses from the hedged transactions are amortised over the period of the hedge.

(m) TaxationDeferred income tax is provided in full, using the liability method, on temporary differences arising between thetax bases of assets and liabilities and their carrying amounts in the financial statements. Tax rates enacted orsubstantively enacted by the balance sheet date are used to determine deferred income tax.

Deferred tax assets are recognised to the extent that it is probable that future taxable profit will be availableagainst which the temporary differences can be utilised.

Deferred income tax is provided on temporary differences arising on investment in subsidiary, except where thetiming of the reversal of the temporary differences can be controlled and it is probable that the temporary differencewill not reverse in the foreseeable future.

29

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

2 Significant accounting policies (continued)(n) Cash and cash equivalents

Cash and cash equivalents are carried in the balance sheet at cost. For the purposes of the cash flow statement,cash and cash equivalents comprise cash on hand and deposits with banks.

(o) DividendsDividends are recorded in the Group’s financial statements in the period in which they are approved by the Group’sshareholders.

3 Principal activityThe principal activity of the Company and its subsidiary is the underwriting of general insurance business.

4 Investment incomeThe Group The Company

2003 2002 2003 2002$’000 $’000 $’000 $’000

(a) Dividend income (gross) from:Quoted equity investments 2,482 1,614 2,482 1,614Unquoted equity investments

in a subsidiary company – – 57 57Other unquoted equity investments 131 132 131 132

2,613 1,746 2,670 1,803

(b) Interest income from:Singapore Government securities 77 84 77 84Other government securities 398 433 398 433Other quoted investments 1,019 1,030 1,019 1,030Other unquoted investments 271 359 271 359

1,765 1,906 1,765 1,906

30

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

NOTES TO THE FINANCIAL STATEMENTSfor the financial year ended 31 December 2003

5 Management expensesIncluded in management expenses are the following:

Charge toCharge insurance

to income revenue 2003 2002statement account Total Total

$’000 $’000 $’000 $’000(a) The Group

Depreciation on:Furniture and fixtures – 8 8 7Office equipment – 245 245 227Motor vehicles – 16 16 17

– 269 269 251Auditors’ remuneration:

Payable to the auditors of the Company- Current year – 69 69 63- Under provision in respect of prior year – 9 9 –

Payable to other auditors – 24 24 22

– 102 102 85Other fees paid/payable to auditors of Company*:

- Current year – – – 20- Under provision in respect of prior year – 17 17 15

– 17 17 35

Foreign exchange (gain)/loss – (4) (4) 5Loss on sale of fixed assets (28) – (28) –

(b) The CompanyDepreciation on:

Furniture and fixtures – 8 8 7Office equipment – 245 245 227Motor vehicles – 16 16 17

– 269 269 251Auditors’ remuneration:

Payable to the auditors of the Company- Current year – 69 69 63- Under provision in respect of prior year – 9 9 –

– 78 78 63Other fees paid/payable to auditors of Company*:

- Current year – – – 20- Under provision in respect of prior year – 17 17 15

– 17 17 35

Foreign exchange (gain)/loss – (4) (4) 5Loss on sale of fixed assets (28) – (28) –

* Include fees in respect of audit-related work required by laws and regulation.

31

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

6 Staff informationThe Group and The Company

2003 2002$’000 $’000

Wages and salaries 2,155 2,226Retrenchment benefits and ex-gratia 87 –Central Provident Fund contribution 273 302

2,515 2,528

The Group and The Company2003 2002

$’000 $’000

Number of persons employed at the end of year 46 53

7 Directors’ remunerationThe number of directors of the Company whose total remuneration from the Group falls into the following bands is:

2003 2002

$250,000 to $499,999 1 1Below $250,000 5 6

Total 6 7

32

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

NOTES TO THE FINANCIAL STATEMENTSfor the financial year ended 31 December 2003

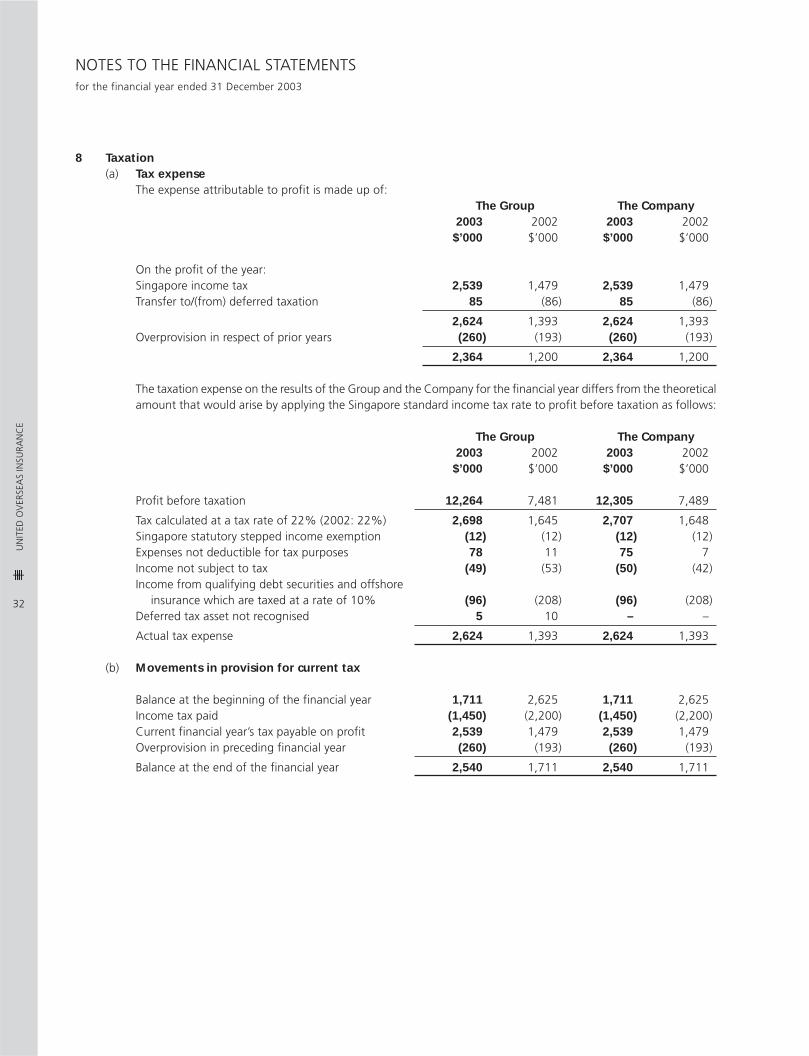

8 Taxation(a) Tax expense

The expense attributable to profit is made up of:The Group The Company

2003 2002 2003 2002$’000 $’000 $’000 $’000

On the profit of the year:Singapore income tax 2,539 1,479 2,539 1,479Transfer to/(from) deferred taxation 85 (86) 85 (86)

2,624 1,393 2,624 1,393Overprovision in respect of prior years (260) (193) (260) (193)

2,364 1,200 2,364 1,200

The taxation expense on the results of the Group and the Company for the financial year differs from the theoreticalamount that would arise by applying the Singapore standard income tax rate to profit before taxation as follows:

The Group The Company2003 2002 2003 2002

$’000 $’000 $’000 $’000

Profit before taxation 12,264 7,481 12,305 7,489

Tax calculated at a tax rate of 22% (2002: 22%) 2,698 1,645 2,707 1,648Singapore statutory stepped income exemption (12) (12) (12) (12)Expenses not deductible for tax purposes 78 11 75 7Income not subject to tax (49) (53) (50) (42)Income from qualifying debt securities and offshore

insurance which are taxed at a rate of 10% (96) (208) (96) (208)Deferred tax asset not recognised 5 10 – –

Actual tax expense 2,624 1,393 2,624 1,393

(b) Movements in provision for current tax

Balance at the beginning of the financial year 1,711 2,625 1,711 2,625Income tax paid (1,450) (2,200) (1,450) (2,200)Current financial year’s tax payable on profit 2,539 1,479 2,539 1,479Overprovision in preceding financial year (260) (193) (260) (193)

Balance at the end of the financial year 2,540 1,711 2,540 1,711

33

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

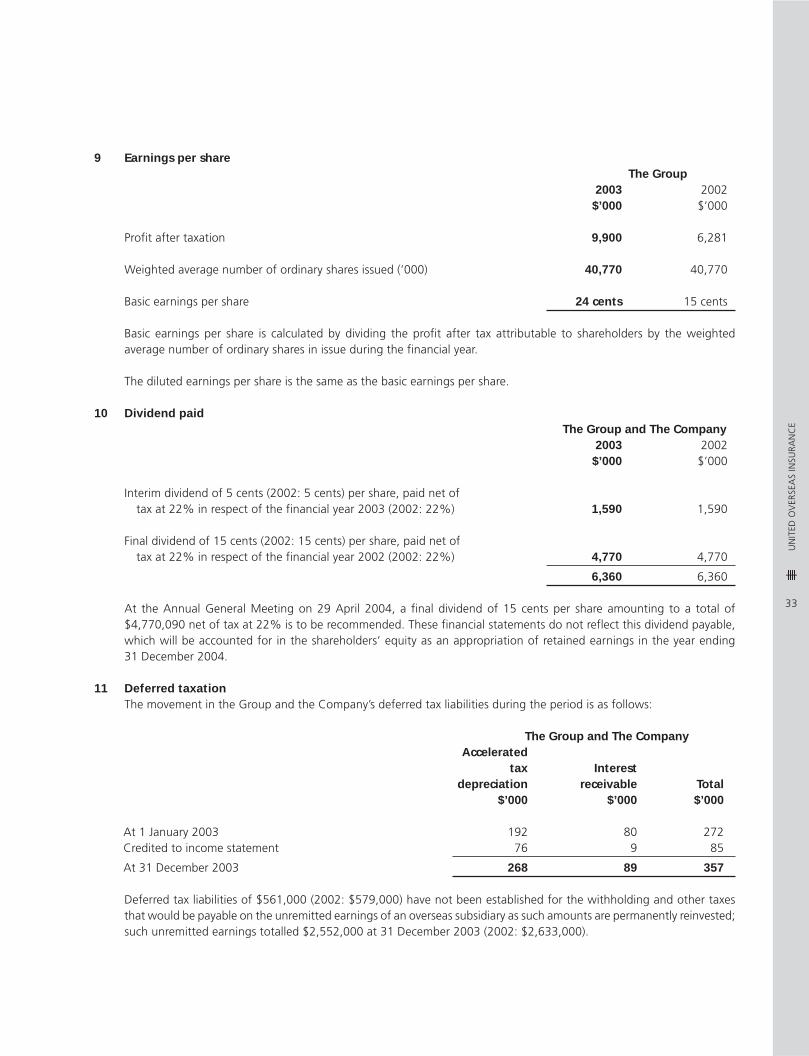

9 Earnings per shareThe Group

2003 2002$’000 $’000

Profit after taxation 9,900 6,281

Weighted average number of ordinary shares issued (’000) 40,770 40,770

Basic earnings per share 24 cents 15 cents

Basic earnings per share is calculated by dividing the profit after tax attributable to shareholders by the weightedaverage number of ordinary shares in issue during the financial year.

The diluted earnings per share is the same as the basic earnings per share.

10 Dividend paidThe Group and The Company

2003 2002$’000 $’000

Interim dividend of 5 cents (2002: 5 cents) per share, paid net oftax at 22% in respect of the financial year 2003 (2002: 22%) 1,590 1,590

Final dividend of 15 cents (2002: 15 cents) per share, paid net oftax at 22% in respect of the financial year 2002 (2002: 22%) 4,770 4,770

6,360 6,360

At the Annual General Meeting on 29 April 2004, a final dividend of 15 cents per share amounting to a total of$4,770,090 net of tax at 22% is to be recommended. These financial statements do not reflect this dividend payable,which will be accounted for in the shareholders’ equity as an appropriation of retained earnings in the year ending31 December 2004.

11 Deferred taxationThe movement in the Group and the Company’s deferred tax liabilities during the period is as follows:

The Group and The CompanyAccelerated

tax Interestdepreciation receivable Total

$’000 $’000 $’000

At 1 January 2003 192 80 272Credited to income statement 76 9 85

At 31 December 2003 268 89 357

Deferred tax liabilities of $561,000 (2002: $579,000) have not been established for the withholding and other taxesthat would be payable on the unremitted earnings of an overseas subsidiary as such amounts are permanently reinvested;such unremitted earnings totalled $2,552,000 at 31 December 2003 (2002: $2,633,000).

34

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

NOTES TO THE FINANCIAL STATEMENTSfor the financial year ended 31 December 2003

12 Unearned premium reservesThe Group The Company

2003 2002 2003 2002$’000 $’000 $’000 $’000

Gross unearned premiums 17,961 18,043 17,740 17,812Unearned premiums on reinsurance ceded (11,104) (10,784) (10,942) (10,626)Net deferred acquisition cost 736 (299) 739 (296)

7,593 6,960 7,537 6,890

Movements in unearned premium reserves are as follows:Balance at beginning of the financial year 6,960 5,206 6,890 5,146Foreign currency translation difference (3) (4) – –Transfer from revenue account 636 1,758 647 1,744

Balance at end of the financial year 7,593 6,960 7,537 6,890

13 Outstanding claimsThe Group The Company

2003 2002 2003 2002$’000 $’000 $’000 $’000

Gross outstanding claims 46,169 39,541 46,088 39,451Amount recoverable from reinsurers (30,560) (24,244) (30,518) (24,196)

15,609 15,297 15,570 15,255

Movements in outstanding claims are as follows:Balance at beginning of the financial year 15,297 15,843 15,255 15,815Net claims paid (4,192) (5,141) (4,186) (5,138)Net claims incurred 4,504 4,595 4,501 4,578

Balance at end of the financial year 15,609 15,297 15,570 15,255

35

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

14 Fixed assets(a) The Group and The Company

Furnitureand Office Motor

Renovation fixtures equipment vehicles Total$’000 $’000 $’000 $’000 $’000

CostAt 1 January 2003 256 198 1,372 82 1,908Transfer (3) 3 – – –Additions – 132 611 – 743Disposals (253) (146) (193) – (592)

At 31 December 2003 – 187 1,790 82 2,059

DepreciationAt 1 January 2003 256 152 534 58 1,000Transfer (3) 3 – – –Charge for the year – 8 245 16 269Disposals (253) (116) (193) – (562)

At 31 December 2003 – 47 586 74 707

Net book value at 31 December 2003 – 140 1,204 8 1,352

Net book value at 31 December 2002 – 46 838 24 908

(b) Fully depreciated assetsOriginal cost of fully depreciated assets still in use as at 31 December 2003 amounted to $65,000 (2002: $575,000).

15 Investment in subsidiary2003 2002$’000 $’000

Unquoted equity shares, at cost 4,940 4,940

The wholly-owned subsidiary is UOB Insurance (H.K.) Limited*, incorporated in Hong Kong. The subsidiary underwritesgeneral insurance business in Hong Kong.

* Audited by a PricewaterhouseCoopers firm outside Singapore.

36

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

NOTES TO THE FINANCIAL STATEMENTSfor the financial year ended 31 December 2003

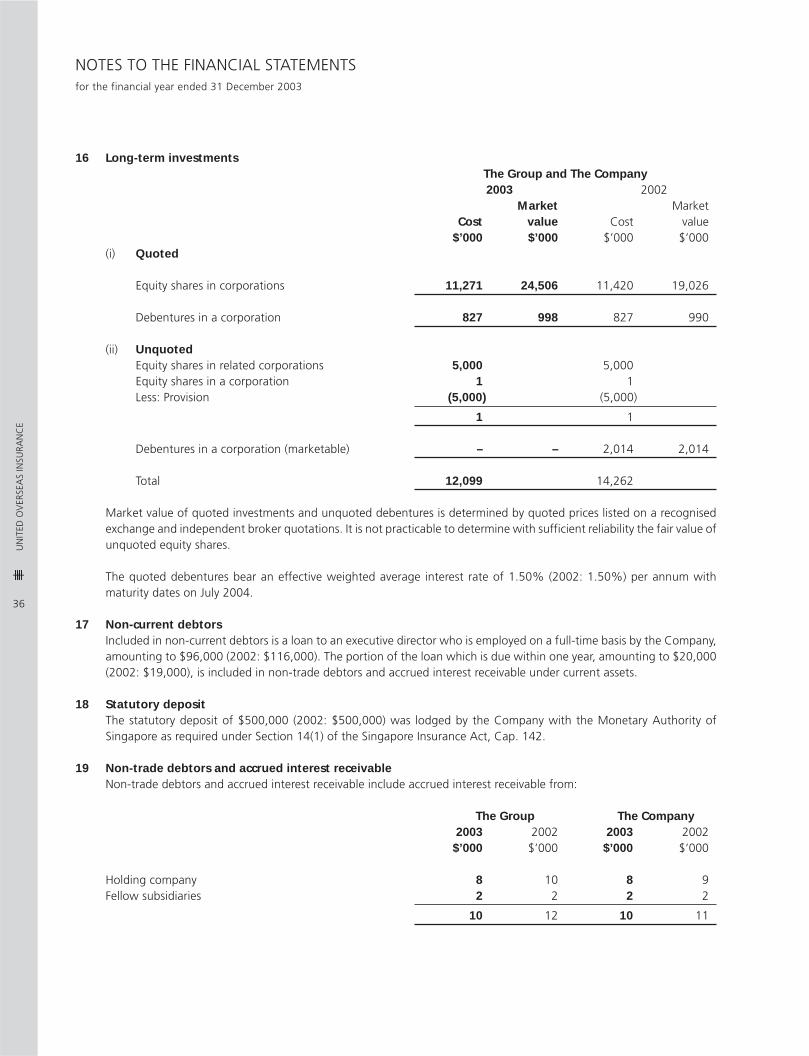

16 Long-term investmentsThe Group and The Company2003 2002

Market MarketCost value Cost value

$’000 $’000 $’000 $’000(i) Quoted

Equity shares in corporations 11,271 24,506 11,420 19,026

Debentures in a corporation 827 998 827 990

(ii) UnquotedEquity shares in related corporations 5,000 5,000Equity shares in a corporation 1 1Less: Provision (5,000) (5,000)

1 1

Debentures in a corporation (marketable) – – 2,014 2,014

Total 12,099 14,262

Market value of quoted investments and unquoted debentures is determined by quoted prices listed on a recognisedexchange and independent broker quotations. It is not practicable to determine with sufficient reliability the fair value ofunquoted equity shares.

The quoted debentures bear an effective weighted average interest rate of 1.50% (2002: 1.50%) per annum withmaturity dates on July 2004.

17 Non-current debtorsIncluded in non-current debtors is a loan to an executive director who is employed on a full-time basis by the Company,amounting to $96,000 (2002: $116,000). The portion of the loan which is due within one year, amounting to $20,000(2002: $19,000), is included in non-trade debtors and accrued interest receivable under current assets.

18 Statutory depositThe statutory deposit of $500,000 (2002: $500,000) was lodged by the Company with the Monetary Authority ofSingapore as required under Section 14(1) of the Singapore Insurance Act, Cap. 142.

19 Non-trade debtors and accrued interest receivableNon-trade debtors and accrued interest receivable include accrued interest receivable from:

The Group The Company2003 2002 2003 2002

$’000 $’000 $’000 $’000

Holding company 8 10 8 9Fellow subsidiaries 2 2 2 2

10 12 10 11

37

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

20 Amount owing by related companiesThe Group The Company

2003 2002 2003 2002$’000 $’000 $’000 $’000

Amount owing by :Holding company – trade 2 153 2 153Fellow subsidiaries – trade 146 146 146 146Subsidiary – non-trade – – 21 33

148 299 169 332

The non-trade balance due from the subsidiary is unsecured, interest-free and has no fixed terms of repayment.

21 InvestmentsThe Group and The Company

2003 2002Market Market

Cost value Cost value$’000 $’000 $’000 $’000

(i) QuotedEquity shares in corporations 30,587 37,906 18,242 17,612Less: Provision

At beginning of the financial year (955) –Write-back of provision/(provision) for

diminution in value made during thefinancial year 955 (955)

At end of the financial year – (955)

30,587 37,906 17,287 17,612

Debentures in corporations 21,783 21,823 20,806 21,602Less: Provision

At beginning of the financial year (6) –Write-back of provision/(provision) for

diminution in value made during thefinancial year 6 (6)

At end of the financial year – (6)

21,783 21,823 20,800 21,602

Singapore Government securities 1,559 1,641 2,010 2,182

Other government securities 6,639 6,538 7,625 7,625Less: Provision

At beginning of the financial year – (214)(Provision)/write-back of provision for

diminution in value made during thefinancial year (101) 214

At end of the financial year (101) –

6,538 6,538 7,625 7,625

38

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

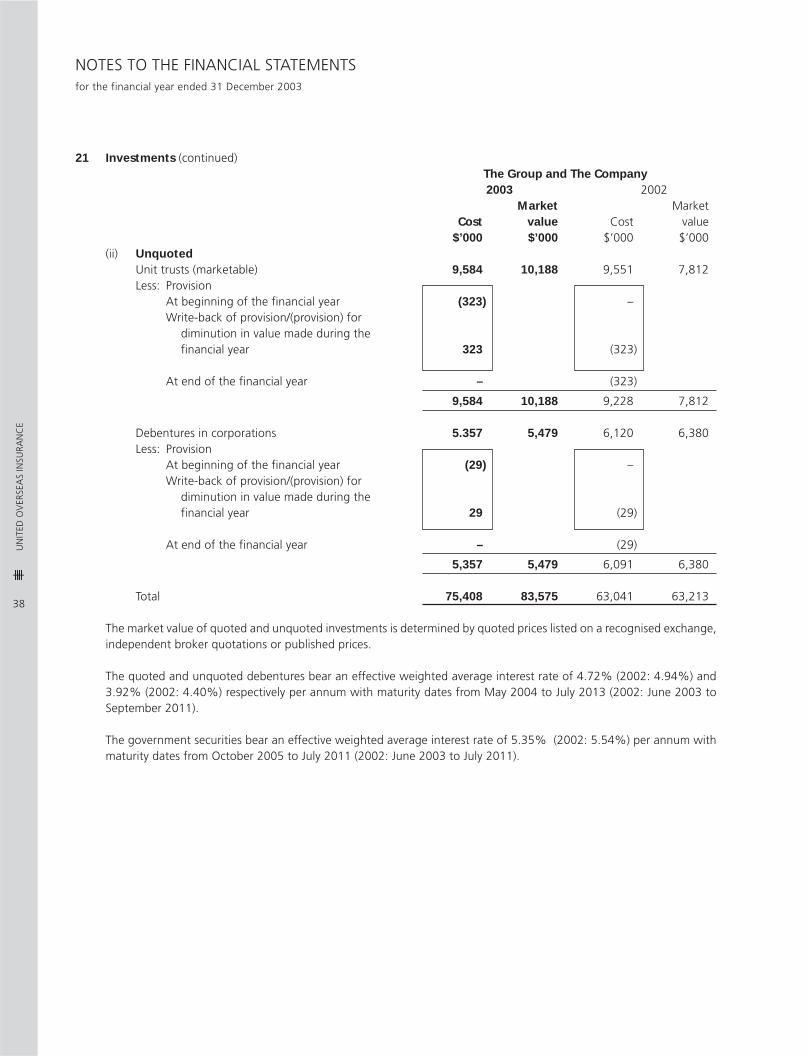

21 Investments (continued)The Group and The Company2003 2002

Market MarketCost value Cost value

$’000 $’000 $’000 $’000(ii) Unquoted

Unit trusts (marketable) 9,584 10,188 9,551 7,812Less: Provision

At beginning of the financial year (323) –Write-back of provision/(provision) for

diminution in value made during thefinancial year 323 (323)

At end of the financial year – (323)

9,584 10,188 9,228 7,812

Debentures in corporations 5.357 5,479 6,120 6,380Less: Provision

At beginning of the financial year (29) –Write-back of provision/(provision) for

diminution in value made during thefinancial year 29 (29)

At end of the financial year – (29)

5,357 5,479 6,091 6,380

Total 75,408 83,575 63,041 63,213

The market value of quoted and unquoted investments is determined by quoted prices listed on a recognised exchange,independent broker quotations or published prices.

The quoted and unquoted debentures bear an effective weighted average interest rate of 4.72% (2002: 4.94%) and3.92% (2002: 4.40%) respectively per annum with maturity dates from May 2004 to July 2013 (2002: June 2003 toSeptember 2011).

The government securities bear an effective weighted average interest rate of 5.35% (2002: 5.54%) per annum withmaturity dates from October 2005 to July 2011 (2002: June 2003 to July 2011).

NOTES TO THE FINANCIAL STATEMENTSfor the financial year ended 31 December 2003

39

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

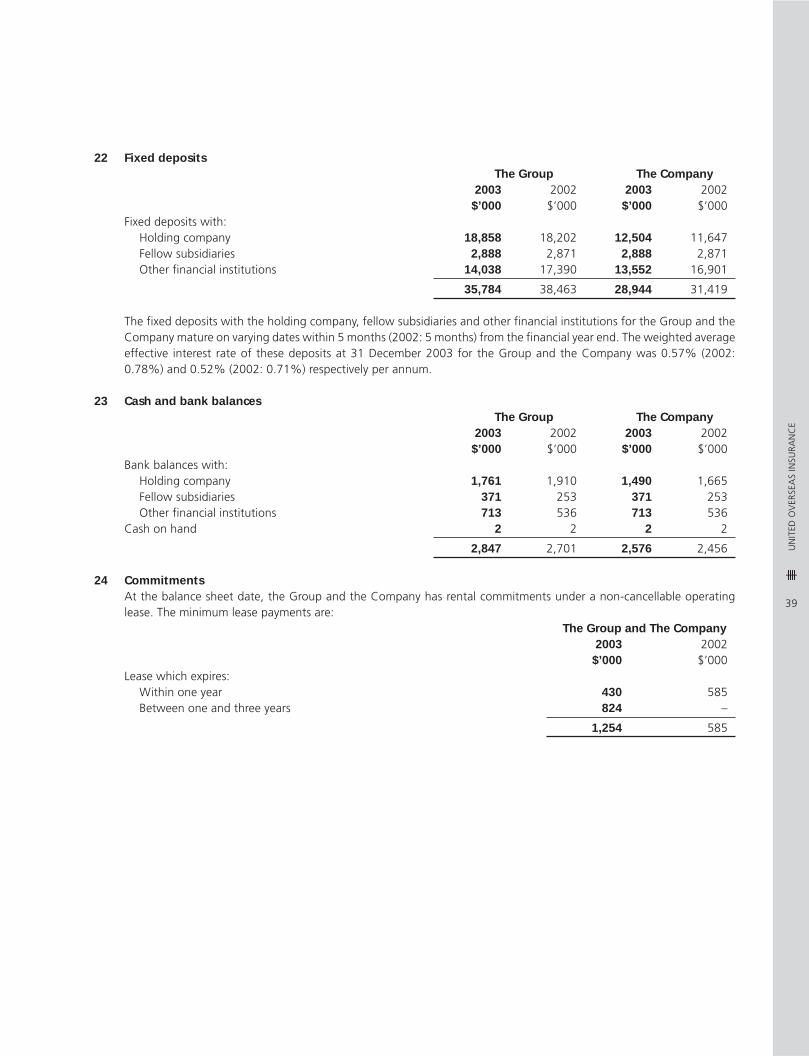

22 Fixed depositsThe Group The Company

2003 2002 2003 2002$’000 $’000 $’000 $’000

Fixed deposits with:Holding company 18,858 18,202 12,504 11,647Fellow subsidiaries 2,888 2,871 2,888 2,871Other financial institutions 14,038 17,390 13,552 16,901

35,784 38,463 28,944 31,419

The fixed deposits with the holding company, fellow subsidiaries and other financial institutions for the Group and theCompany mature on varying dates within 5 months (2002: 5 months) from the financial year end. The weighted averageeffective interest rate of these deposits at 31 December 2003 for the Group and the Company was 0.57% (2002:0.78%) and 0.52% (2002: 0.71%) respectively per annum.

23 Cash and bank balancesThe Group The Company

2003 2002 2003 2002$’000 $’000 $’000 $’000

Bank balances with:Holding company 1,761 1,910 1,490 1,665Fellow subsidiaries 371 253 371 253Other financial institutions 713 536 713 536

Cash on hand 2 2 2 2

2,847 2,701 2,576 2,456

24 CommitmentsAt the balance sheet date, the Group and the Company has rental commitments under a non-cancellable operatinglease. The minimum lease payments are:

The Group and The Company2003 2002

$’000 $’000Lease which expires:

Within one year 430 585Between one and three years 824 –

1,254 585

40

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

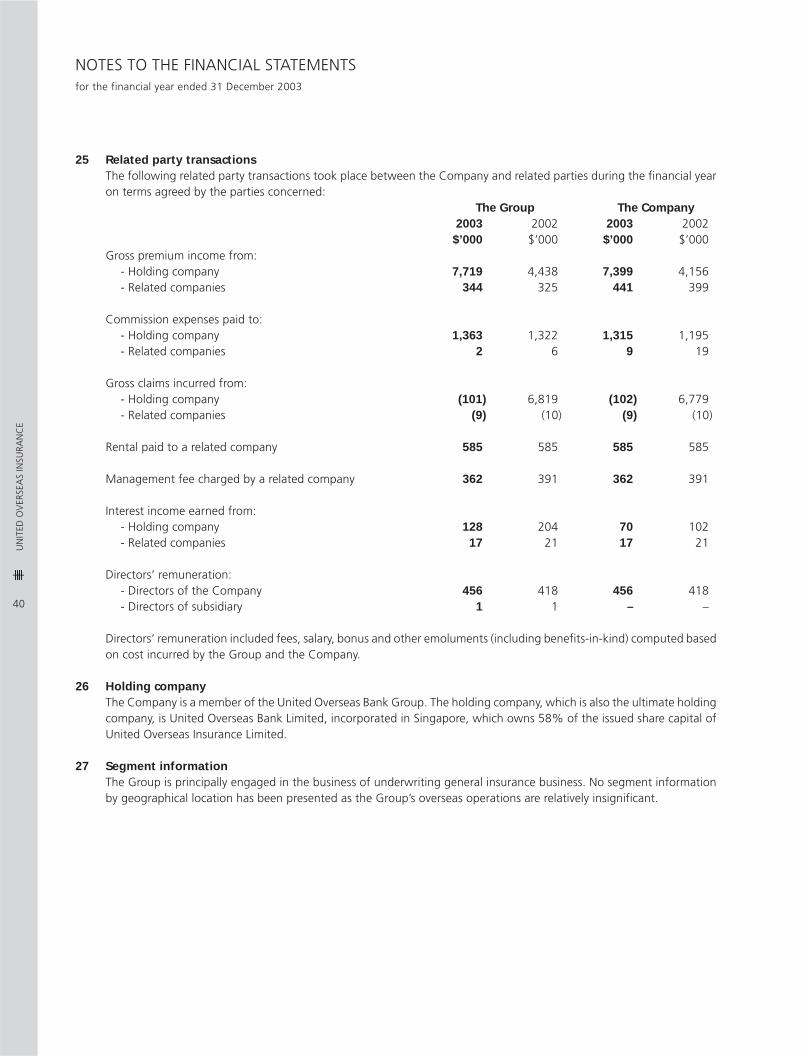

25 Related party transactionsThe following related party transactions took place between the Company and related parties during the financial yearon terms agreed by the parties concerned:

The Group The Company2003 2002 2003 2002

$’000 $’000 $’000 $’000Gross premium income from:

- Holding company 7,719 4,438 7,399 4,156- Related companies 344 325 441 399

Commission expenses paid to:- Holding company 1,363 1,322 1,315 1,195- Related companies 2 6 9 19

Gross claims incurred from:- Holding company (101) 6,819 (102) 6,779- Related companies (9) (10) (9) (10)

Rental paid to a related company 585 585 585 585

Management fee charged by a related company 362 391 362 391

Interest income earned from:- Holding company 128 204 70 102- Related companies 17 21 17 21

Directors’ remuneration:- Directors of the Company 456 418 456 418- Directors of subsidiary 1 1 – –

Directors’ remuneration included fees, salary, bonus and other emoluments (including benefits-in-kind) computed basedon cost incurred by the Group and the Company.

26 Holding companyThe Company is a member of the United Overseas Bank Group. The holding company, which is also the ultimate holdingcompany, is United Overseas Bank Limited, incorporated in Singapore, which owns 58% of the issued share capital ofUnited Overseas Insurance Limited.

27 Segment informationThe Group is principally engaged in the business of underwriting general insurance business. No segment informationby geographical location has been presented as the Group’s overseas operations are relatively insignificant.

NOTES TO THE FINANCIAL STATEMENTSfor the financial year ended 31 December 2003

41

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

28 Financial risks managementFinancial risk factorsThe Group’s activities expose it to a variety of financial risks, including the effects of changes in debt and equity marketprices, foreign currency exchange rates and interest rates. The Group’s overall risk management programme focuses onthe unpredictability of financial markets and seeks to minimise potential adverse effects on the financial performance ofthe Group. The Group uses derivative financial instruments such as forward contracts to hedge certain exposures.

(i) Foreign exchange riskThe Group’s business is exposed to foreign exchange risk arising from various currency exposures. Where practicable,the Group uses forward contracts to hedge the investment exposure to foreign currency risk in the local reportingcurrency.

(ii) Interest rate riskThe Group’s income and operating cash flows are substantially independent of changes in market interest rates.The Group’s interest-bearing assets are mainly in fixed income securities with fixed interest rates and short termfixed deposits where future variations in interest rates will not have a significant impact on net profit.

(iii) Credit riskThe Group has no significant concentrations of credit risk. The Group has credit control policies in place to ensurethat sales made to customers are duly collected.

(iv) Liquidity riskPrudent liquidity risk management implies maintaining sufficient cash and marketable securities.

Due to the nature of the business and type of assets owned, liquidity risks are minimised.

29 Fair values of financial instrumentsThe financial assets and financial liabilities of the Group and the Company comprise its current assets and currentliabilities, with the exception of taxation. Other than the fair values of quoted and unquoted investments as detailed inNote 21, the fair values of the financial assets and financial liabilities as at the balance sheet date approximate theircarrying amounts as shown in the balance sheet.

42

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

NOTES TO THE FINANCIAL STATEMENTSfor the financial year ended 31 December 2003

30 Event occurring after balance sheet dateOn 1 January 2004, the following assets and liabilities of a related party of its holding company, Overseas Union Insurance,Limited were transferred to the Company in accordance with the Scheme for Transfer dated 29 August 2003 andconfirmed by the High Court on 31 October 2003:

$’000AssetsDue from insured, agents and reinsurers (net of provision) 1,558Claim recoveries 373Amount retained by ceding companies 89Cash and bank balances 28,809

30,829

LiabilitiesAmount due to agents and reinsurers (1,661)Amount retained from reinsurers (1,073)Outstanding claims (net) (22,108)Unearned premium reserves (net) (5,987)

(30,829)

Net –

31 Authorisation of financial statementsThe financial statements were authorised for issue in accordance with a resolution of the directors on 20 February 2004.

43

UN

ITED

OV

ERSE

AS

INSU

RAN

CE

STATISTICS OF SHAREHOLDINGSas at 12 March 2004

Substantial shareholder as at 12 March 2004Other shareholding

Shareholding registered in which the substantialin the name of shareholder is deemed

Substantial shareholder substantial shareholder to have an interest