Blok 6Fra fast ejendomtil bygninger, der

styrkerkampkraften

Flemming Engelhardtadm. Direktør, Newsec Datea

Fra fast ejendom til bygninger, der styrker kampkraften

Ejendomme er blevet dynamisk faktor i virksomhedens kampkraft

Flemming B. Engelhardt

Adm. direktør, Newsec Datea A/S

What we do…..

NEWSEC IN DENMARK

PROPERTY ASSET MANAGEMENT

ADVISORY

NEWSEC DATEA A/SNEWSEC ADVISORY

A/S

Focus on Property Asset Management, Facility Management , leasing and association management

Focus on advisory, sale and leasing

INVESTASSOCIATIO

NS

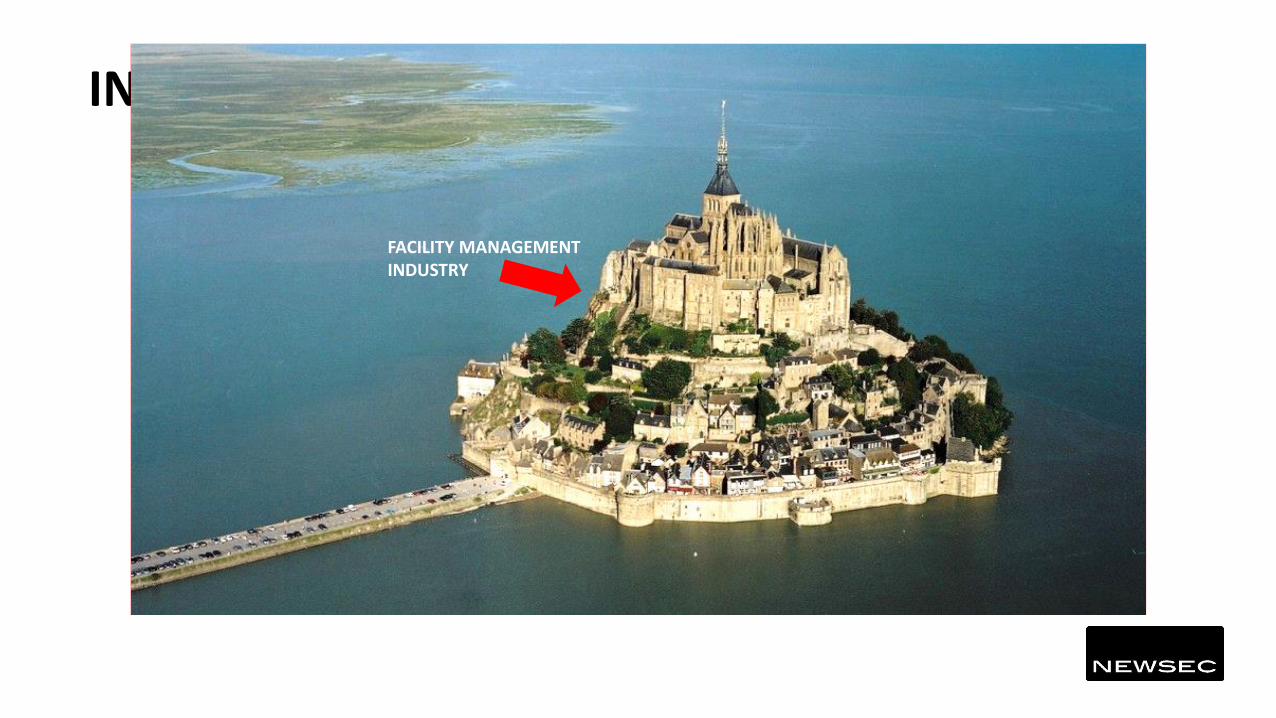

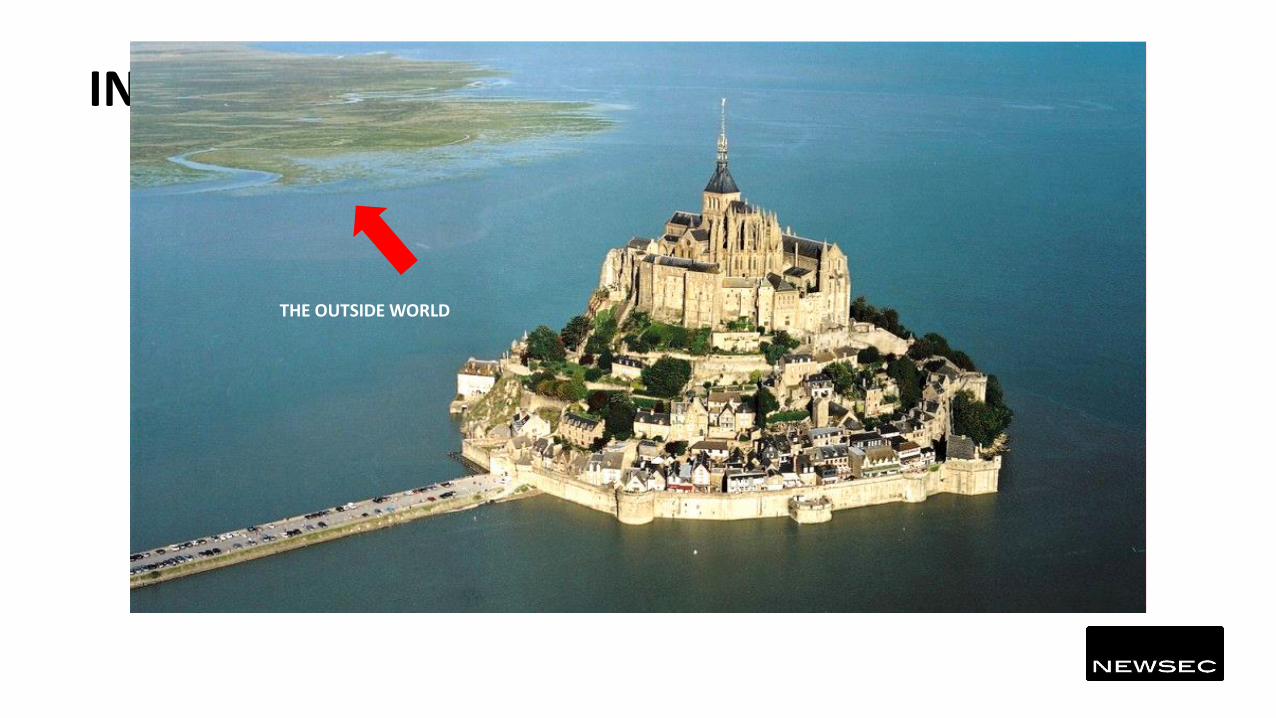

The battlefield – and how technology will shape our industry?

INTERNAL FACTORS

FACILITY MANAGEMENT INDUSTRY

INTERNAL FACTORS

THE OUTSIDE WORLD

The worlds real estate assets account for

60% of all global assets,

incl. gold, bonds, equities

THE REAL ESTATE INDUSTRY

The estimated value of all developed

real estate in the worlds is

$217 trillion

BUILDINGS ARE INEFFICIENT

IBM – smarter buildings & Townships for a better planet

50%Up to 50% of energy and water in buildings are often wasted

2025By 2025, buildings will be the #1 consumer of energy

30%30% of all commercial space goes unused

NEWSECS PROPERTY ASSET MANAGEMENT AND FACILITY MANAGEMENT SERVICES

Property caretakingTrimming operationHandling faults in property

Property strategySuggestion buy and sellProfitability analysisInvestment (in the property)

Lease administration LeasingRe-negotiationTenant relationsProject development

General supervisionCorrective maintenance

Service notification

ReportingIFRS

Group accounting Legal accounting

Property accountingLease administration

FinancingPortfolio strategyBuy/sell decisions

Larger investments

Property strategyBuy/sell proposal

Profitability analysisProperty development

Investments in the property

ComplianceProcurementSustainabilityTechnical planningEnergy optimisationFacilty Service

LeasingRenegotiation

Tenant relationsProject management

CLIEN

T

NEW

SEC

PORTFOLIO MANAGEMENT

ASSET MANAGEMENT

PROPERTY AND FACILITY MANAGEMENT

PROPERTY CARETAKING

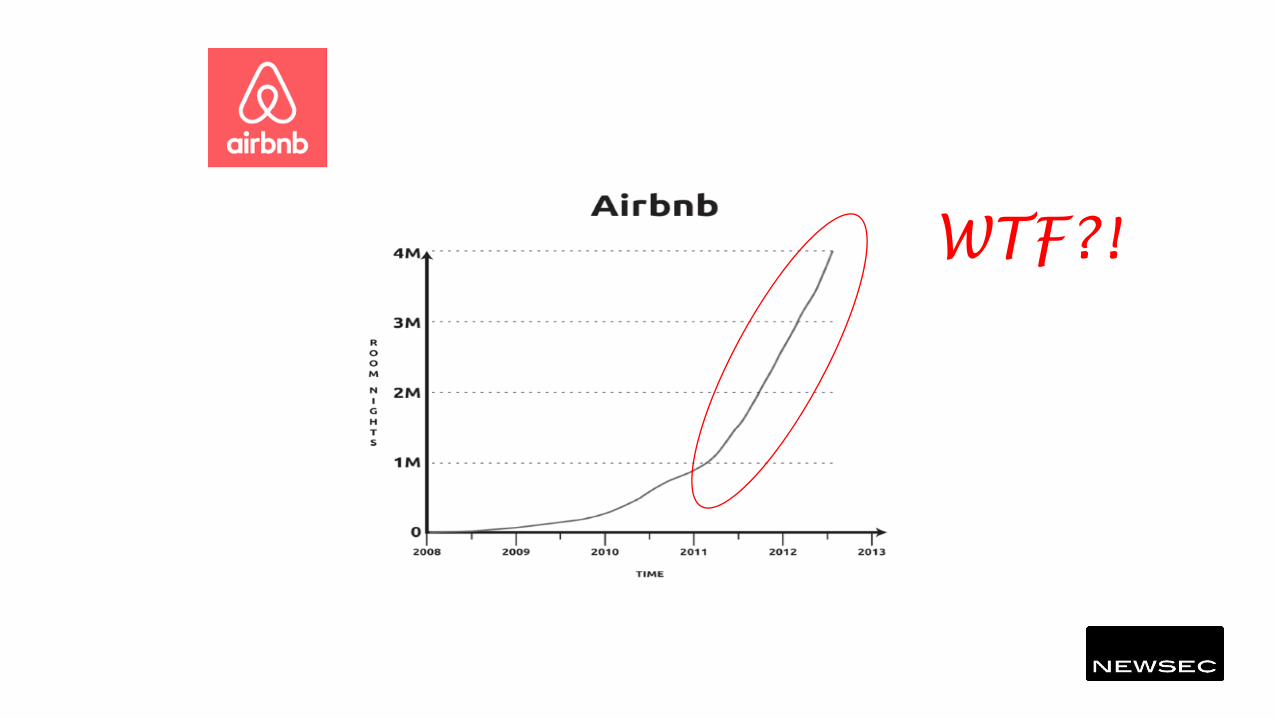

UNICORNS OF TODAYWILL SHAPE THE INDUSTRIES OF TOMORROW

WTF?!

Smart city initiatives are now the driving force for innovation in real estate

All enabled by technology

Artificial intelligence

Cheap sensors

Connectivity

Open APIs

Smart buildings have higher occupancy, higher productivity and higher tenant satisfaction

Buildings will begin to have a voice

The AC is broken

My windowsare dirty

Water is leaking

It is cold…

My radiator need fixing

Fire alarm!

Tenants are consuming services

New shoes (Amazon)

Need more milk (nemlig.com)

Cleaning(Hilfr.dk)

Superbowl (Pay per view)I want a steak

(uber eats)

Redecorating bedroom(Ikea)

BUSINESS MODELS ARE EMERGING WITHOUT PROPERTY OWNERS

EVERYONE WANTS IN ON THE ACTION

HOW WILL THIS IMPACT FACILITY MANAGERS?

How it feels for decision makers

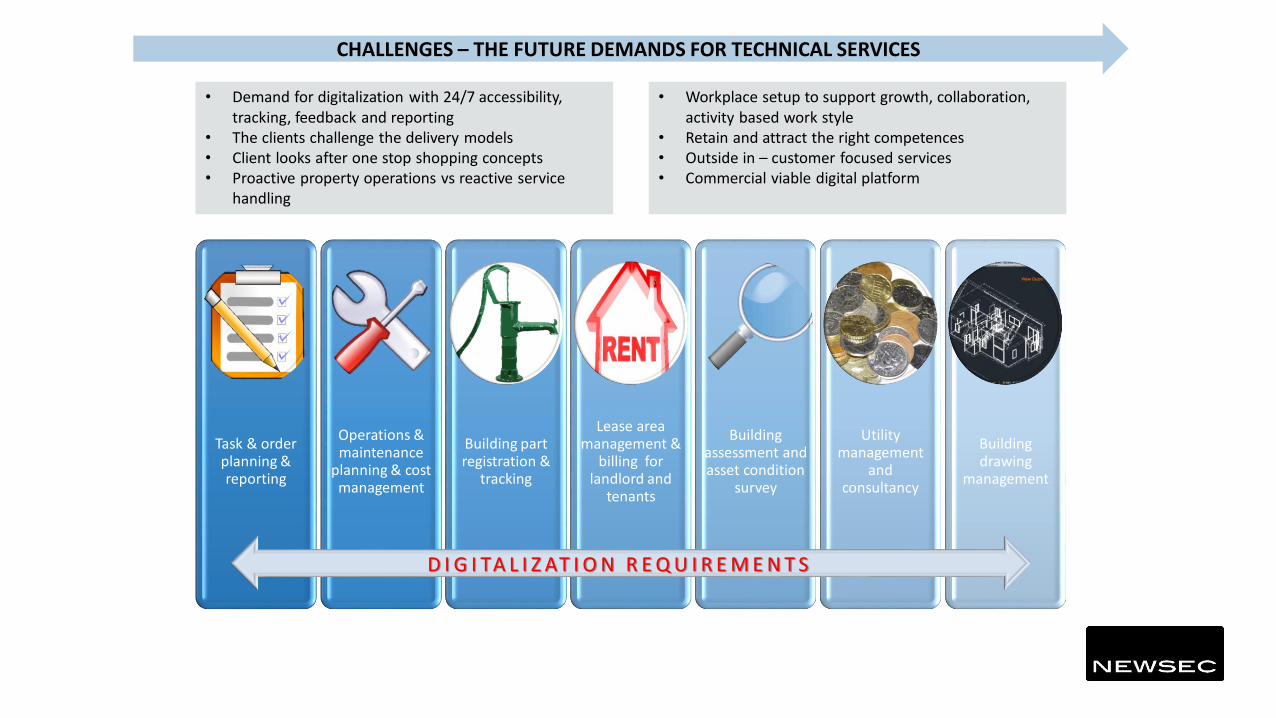

CHALLENGES – THE FUTURE DEMANDS FOR TECHNICAL SERVICES

Task & order planning & reporting

Operations & maintenance

planning & cost management

Building part registration &

tracking

Lease area management &

billing for landlord and

tenants

Building assessment and asset condition

survey

Utility management

and consultancy

Building drawing

management

D I G I TA L I Z AT I O N R E Q U I R E M E N T S

• Demand for digitalization with 24/7 accessibility, tracking, feedback and reporting

• The clients challenge the delivery models • Client looks after one stop shopping concepts• Proactive property operations vs reactive service

handling

• Workplace setup to support growth, collaboration, activity based work style

• Retain and attract the right competences• Outside in – customer focused services• Commercial viable digital platform

CONCLUSION

BUILD A GREAT ”MUSIC” SCHOOL

The end – thanks for your attention…

Karina Moll RavnExecutive Director, CBRE

GLOBAL CORPORATE SERVICES

CBRE presents

Strategy Drives Integration – Integration Drives Strategy

Prepared by: Karina Moll Ravn

Date: March 23, 2018

28 DFM© 2017 CBRE | CONFIDENTIAL & PROPRIETARY

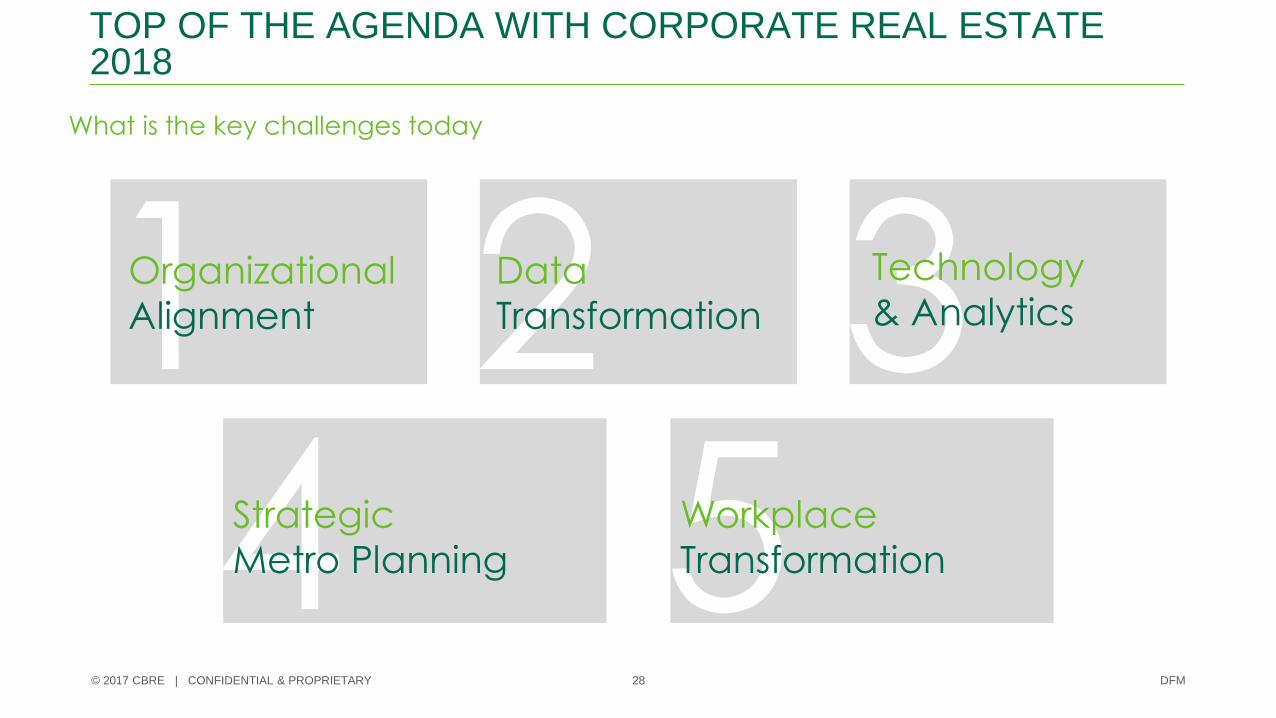

TOP OF THE AGENDA WITH CORPORATE REAL ESTATE 2018

What is the key challenges today

1 2 34 5Strategic

Metro Planning

Data

Transformation

Technology

& AnalyticsOrganizational

Alignment

Workplace

Transformation

29 DFM© 2017 CBRE | CONFIDENTIAL & PROPRIETARY

Day to Day Operation for Corporate Real Estate Teams

LIFECYCLE OF THE CORPORATE PORTFOLIOPLANNING

EXECUTING

OPERATING

WHERE ARE OUR

FUTURE MARKETS?

HOW MUCH SPACE

DO WE REALLY

REQUIRE?

DOES OUR FIT-OUT

MEET THE NEEDS OF

TALENT?

HOW DO WE

MANAGE OUR

COST?

WHAT ARE OUR

TOTALCOMMITMENT

& LIABILITY

WHAT IS THE IMPACT

ON OUR

EMPLOYEES?

LOCATION &

LABOUR

ANALYTICS

SPACE AND

OCCUPANCY

MAANGEMENT

WORKPLACE

STRATEGY

PROJECT

MANAGEMENT

FACILITIES

MANAGEMENT

ENERGY &

SUSTAINABILITY

PORTFOLIO

ANALYTICS

TRANSACTION

MANAGEMENT

CORPORATE REAL ESTATE

30 DFM© 2017 CBRE | CONFIDENTIAL & PROPRIETARY

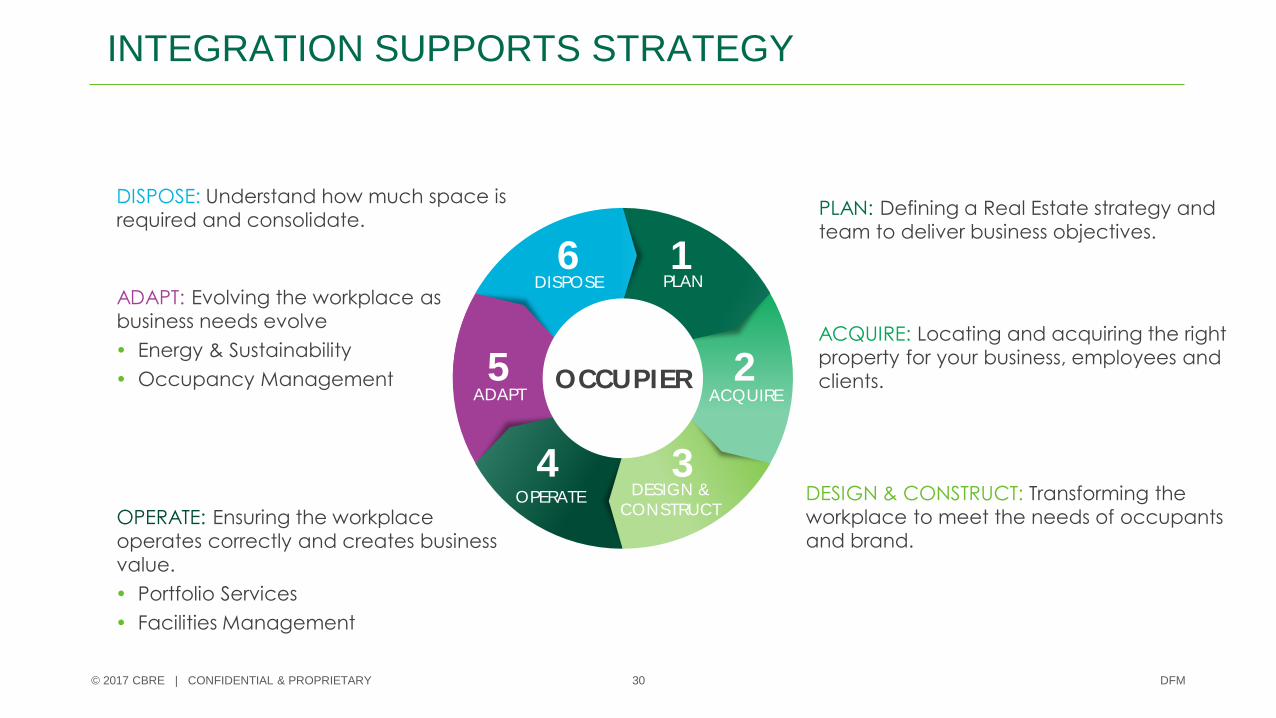

INTEGRATION SUPPORTS STRATEGY

DISPOSE PLAN

ACQUIRE

DESIGN &

CONSTRUCTOPERATE

6 1

2

34

ADAPT5 OCCUPIER

PLAN: Defining a Real Estate strategy and

team to deliver business objectives.

ACQUIRE: Locating and acquiring the right

property for your business, employees and

clients.

DESIGN & CONSTRUCT: Transforming the

workplace to meet the needs of occupants

and brand.OPERATE: Ensuring the workplace

operates correctly and creates business

value.

Portfolio Services

Facilities Management

ADAPT: Evolving the workplace as

business needs evolve

Energy & Sustainability

Occupancy Management

DISPOSE: Understand how much space is

required and consolidate.

31 DFM© 2017 CBRE | CONFIDENTIAL & PROPRIETARY

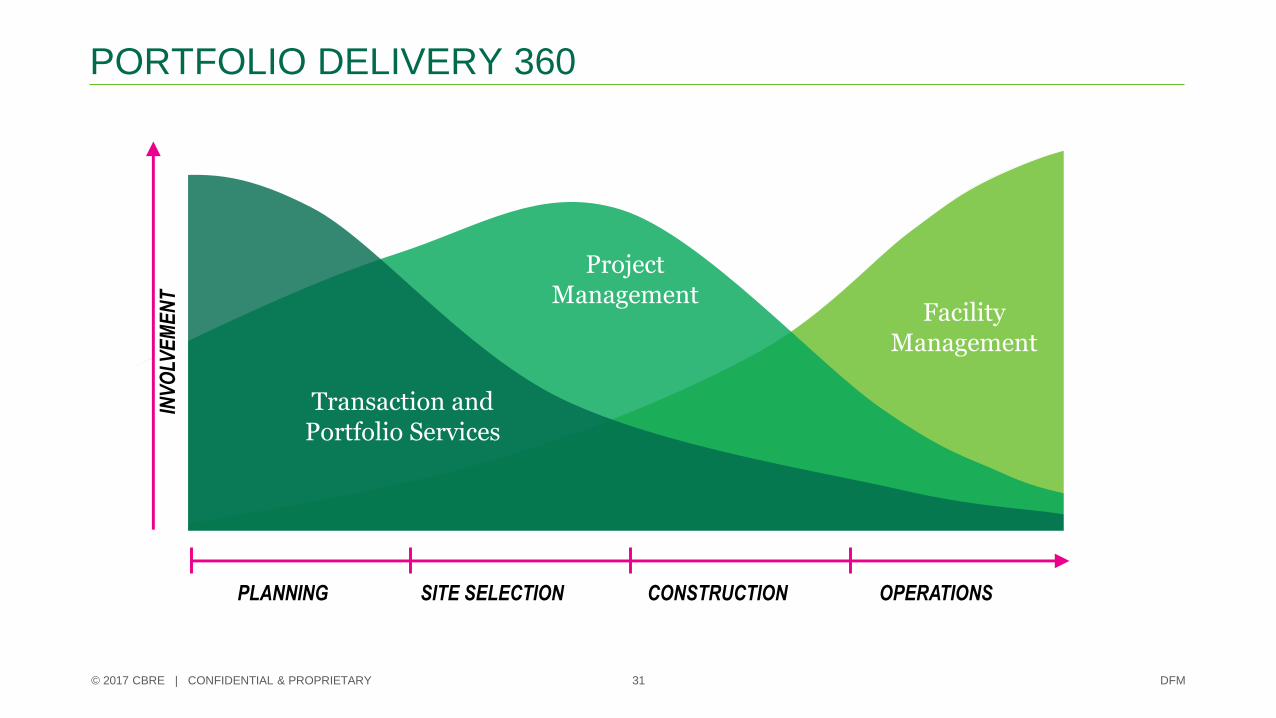

PORTFOLIO DELIVERY 360

INV

OLV

EM

EN

T

PLANNING SITE SELECTION CONSTRUCTION OPERATIONS

Transaction and Portfolio Services

ProjectManagement

FacilityManagement

32CBREPrepared for Grundfos

PORTFOLIO OPTIMIZERCBRE’S PORTFOLIO ANALYSIS, BENCHMARKING AND OPTIMIZATION SYSTEM

33CBREPrepared for Grundfos

SUPPORTING YOUR STRATEGIC DECISIONSCBRE PORTFOLIO OPTIMIZER

Portfolio Summary MetricsInternal Portfolio Benchmarking Portfolio Savings Opportunities

External Benchmarking and Market Context

SEQUENTRA Lease Portfolio Data

34 DFM© 2017 CBRE | CONFIDENTIAL & PROPRIETARY

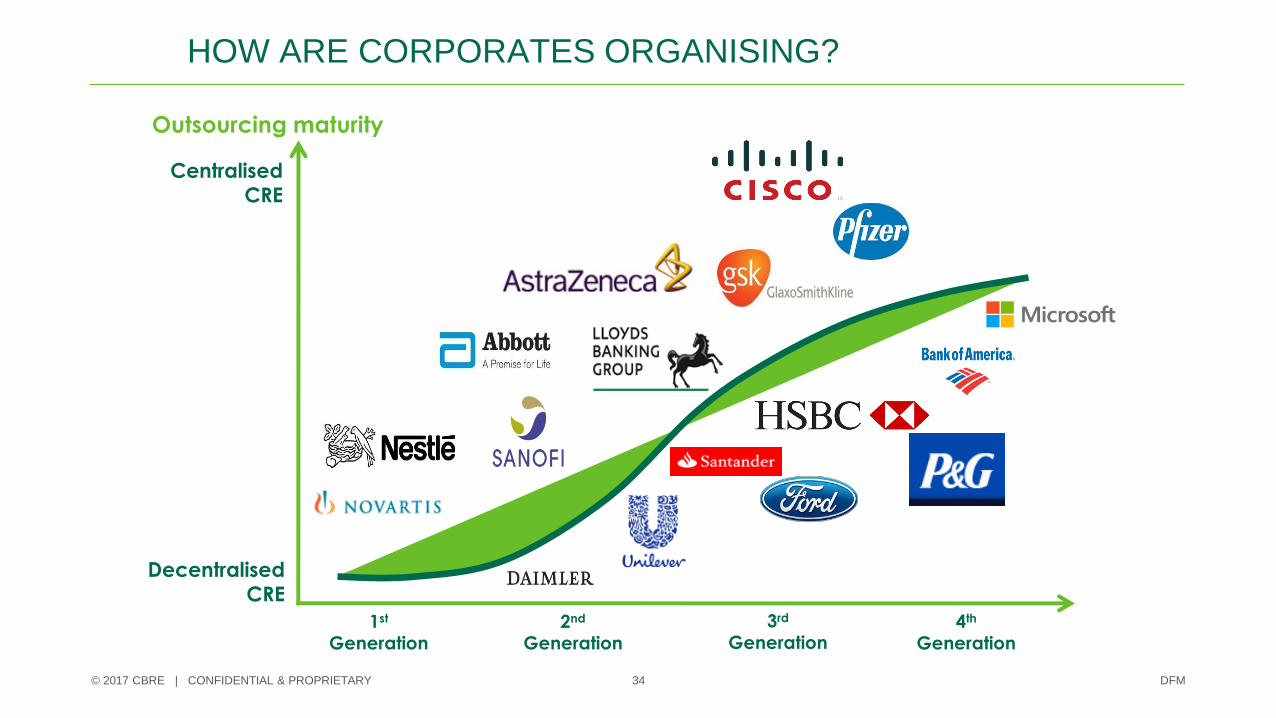

HOW ARE CORPORATES ORGANISING?

Outsourcing maturity

1st

Generation4th

Generation

DecentralisedCRE

Centralised CRE

2nd

Generation

3rd

Generation

35 DFM© 2017 CBRE | CONFIDENTIAL & PROPRIETARY

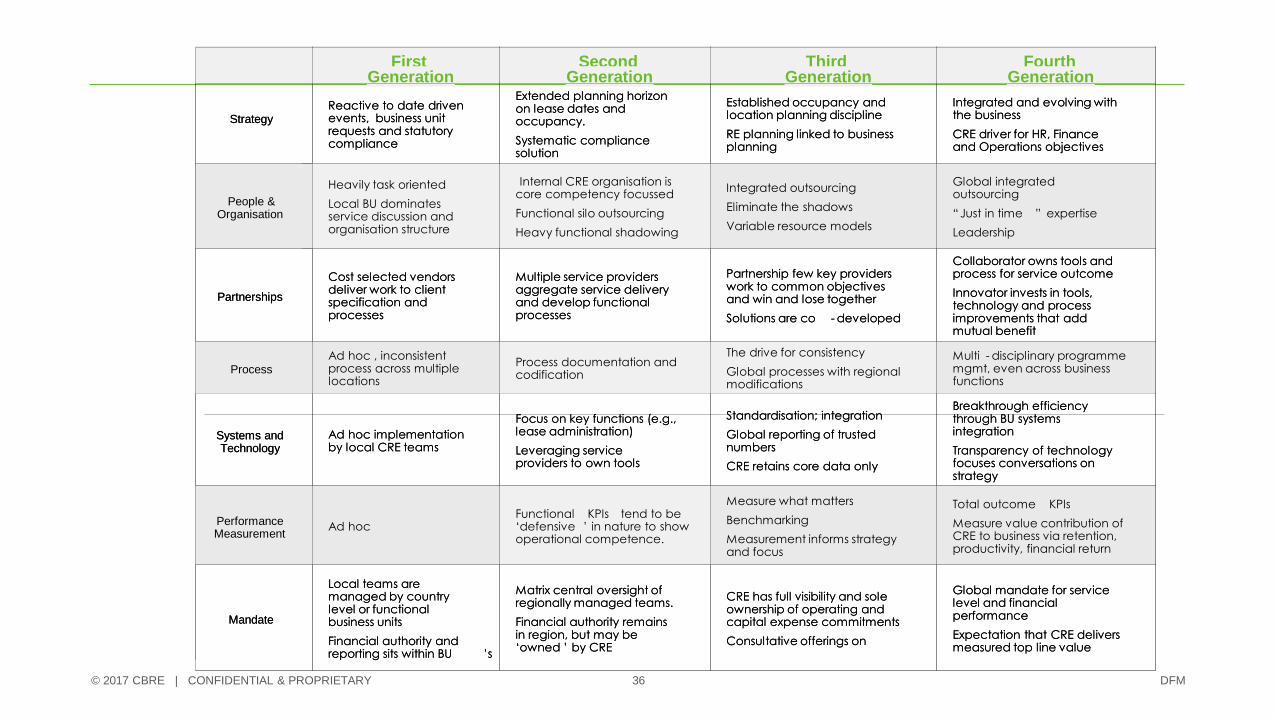

EVOLUTION OF CRE FUNCTIONS

StrategyS

TechnologyT

ProcessesP

AlliancesA

OrganisationO

36 DFM© 2017 CBRE | CONFIDENTIAL & PROPRIETARY

Global mandate for service level and financial performance

Expectation that CRE delivers measured top line value

CRE has full visibility and sole ownership of operating and capital expense commitments

Consultative offerings on

Matrix central oversight of regionally managed teams.

Financial authority remains in region, but may be ‘owned ’ by CRE

Local teams are managed by country level or functional business units

Financial authority and reporting sits within BU ’s

Mandate

First Generation

Second Generation

ThirdGeneration

Fourth Generation

StrategyReactive to date driven events, business unit requests and statutory compliance

Extended planning horizon on lease dates and occupancy.

Systematic compliance solution

Established occupancy and location planning discipline

RE planning linked to business planning

Integrated and evolving with the business

CRE driver for HR, Finance and Operations objectives

People &Organisation

Heavily task oriented

Local BU dominates service discussion and organisation structure

Internal CRE organisation is core competency focussed

Functional silo outsourcing

Heavy functional shadowing

Integrated outsourcing

Eliminate the shadows

Variable resource models

Global integrated outsourcing

“Just in time ” expertise

Leadership

Partnerships

Cost selected vendors deliver work to client specification and processes

Multiple service providers aggregate service delivery and develop functional processes

Partnership few key providers work to common objectives and win and lose together

Solutions are co - developed

Collaborator owns tools and process for service outcome

Innovator invests in tools, technology and process improvements that add mutual benefit

ProcessAd hoc , inconsistent

process across multiple locations

Process documentation and codification

The drive for consistency

Global processes with regional modifications

Multi - disciplinary programme mgmt, even across business functions

Systems and Technology

Ad hoc implementation by local CRE teams

Focus on key functions (e.g., lease administration)

Leveraging service providers to own tools

Standardisation; integration

Global reporting of trusted numbers

CRE retains core data only

Breakthrough efficiency through BU systems integration

Transparency of technology focuses conversations on strategy

Performance Measurement

Ad hocFunctional KPIs tend to be

‘defensive ’ in nature to show operational competence.

Measure what matters

Benchmarking

Measurement informs strategy and focus

Total outcome KPIs

Measure value contribution of CRE to business via retention, productivity, financial return

Global mandate for service level and financial performance

Expectation that CRE delivers measured top line value

CRE has full visibility and sole ownership of operating and capital expense commitments

Consultative offerings on

Matrix central oversight of regionally managed teams.

Financial authority remains in region, but may be ‘owned ’ by CRE

Local teams are managed by country level or functional business units

Financial authority and reporting sits within BU ’s

Mandate

First Generation

Second Generation

ThirdGeneration

Fourth Generation

StrategyReactive to date driven events, business unit requests and statutory compliance

Extended planning horizon on lease dates and occupancy.

Systematic compliance solution

Established occupancy and location planning discipline

RE planning linked to business planning

Integrated and evolving with the business

CRE driver for HR, Finance and Operations objectives

People &Organisation

Heavily task oriented

Local BU dominates service discussion and organisation structure

Internal CRE organisation is core competency focussed

Functional silo outsourcing

Heavy functional shadowing

Integrated outsourcing

Eliminate the shadows

Variable resource models

Global integrated outsourcing

“Just in time ” expertise

Leadership

Partnerships

Cost selected vendors deliver work to client specification and processes

Multiple service providers aggregate service delivery and develop functional processes

Partnership few key providers work to common objectives and win and lose together

Solutions are co - developed

Collaborator owns tools and process for service outcome

Innovator invests in tools, technology and process improvements that add mutual benefit

ProcessAd hoc , inconsistent process across multiple locations

Process documentation and codification

The drive for consistency

Global processes with regional modifications

Multi - disciplinary programme mgmt, even across business functions

Systems and Technology

Ad hoc implementation by local CRE teams

Focus on key functions (e.g., lease administration)

Leveraging service providers to own tools

Standardisation; integration

Global reporting of trusted numbers

CRE retains core data only

Breakthrough efficiency through BU systems integration

Transparency of technology focuses conversations on strategy

Performance Measurement

Ad hocFunctional KPIs tend to be ‘defensive ’ in nature to show operational competence.

Measure what matters

Benchmarking

Measurement informs strategy and focus

Total outcome KPIs

Measure value contribution of CRE to business via retention, productivity, financial return

CBRE

Interview: Michael Ertmannafdelingsleder, Favrskov Kommune

Interview: Jacob Mørch-Sørensenforretningsudvikler, Freja Ejendomme

Debat

Opsamling og afrunding afkonferencen

v/Svend Biedirektør DFM netværk

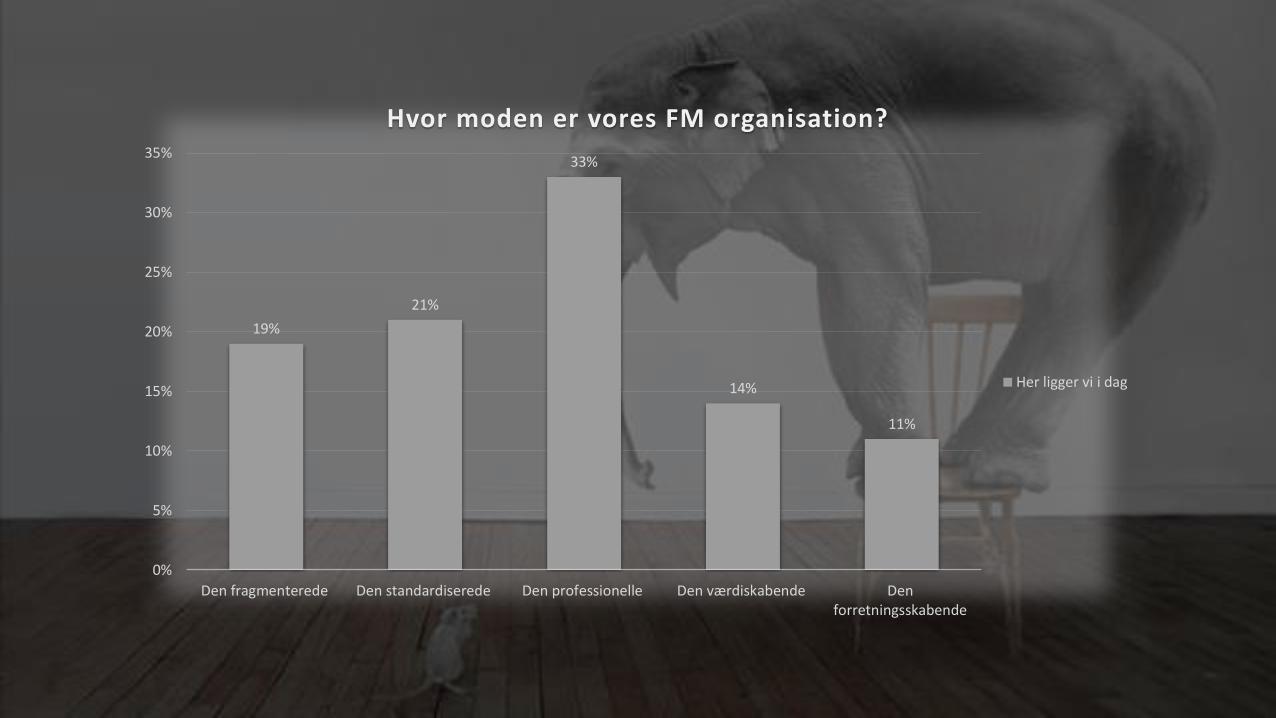

Resultater fra medlemsundersøgelsen

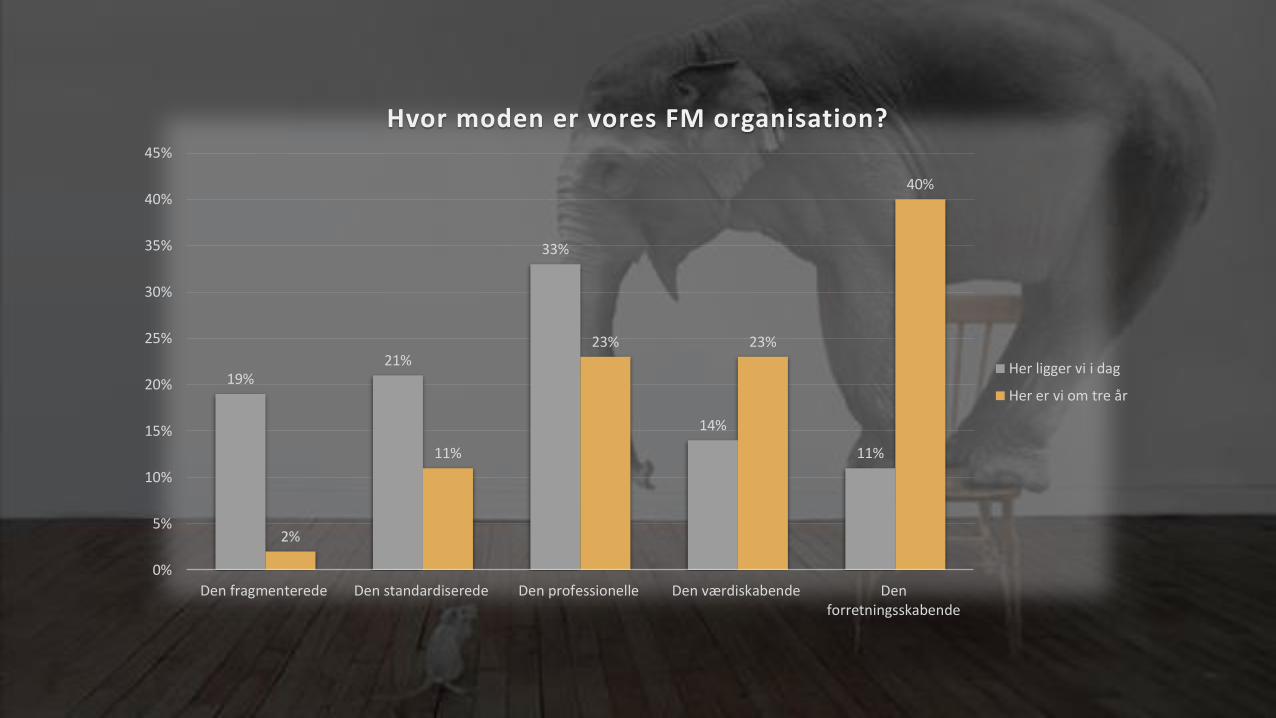

19%

21%

33%

14%

11%

0%

5%

10%

15%

20%

25%

30%

35%

Den fragmenterede Den standardiserede Den professionelle Den værdiskabende Denforretningsskabende

Hvor moden er vores FM organisation?

Her ligger vi i dag

19%21%

33%

14%

11%

2%

11%

23% 23%

40%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Den fragmenterede Den standardiserede Den professionelle Den værdiskabende Denforretningsskabende

Hvor moden er vores FM organisation?

Her ligger vi i dag

Her er vi om tre år

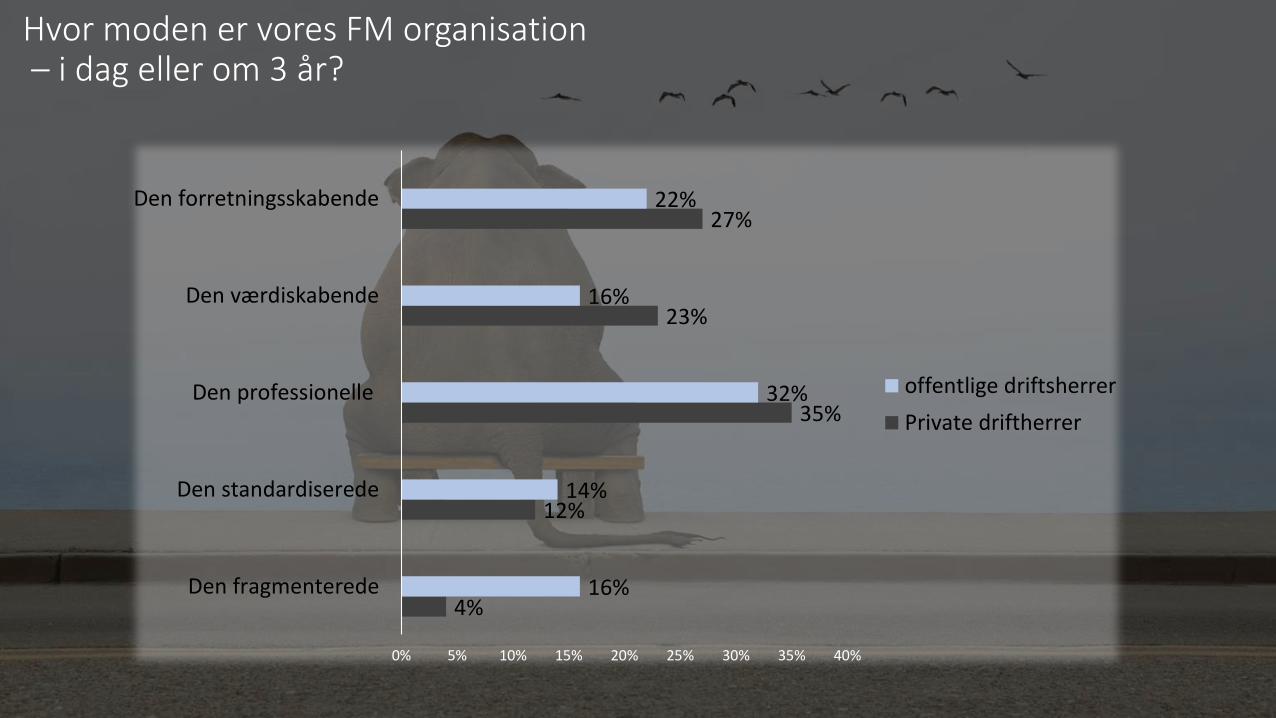

4%

12%

35%

23%

27%

16%

14%

32%

16%

22%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Den fragmenterede

Den standardiserede

Den professionelle

Den værdiskabende

Den forretningsskabende

offentlige driftsherrer

Private driftherrer

Hvor moden er vores FM organisation– i dag eller om 3 år?

Poul Henrik Due Ole Emil Malmstrøm

Tibbe Knudsen

Verner BentzenChristian Fredberg

Karina Lykkegaard Lotte Nielsen Cille Haugaard

Rolf Ejlertsen

Holdet bag Årskonferencen 2018

Svend Bie

Tak for i år

vi ses i 2019