N

g

ie

e

K

N

ThySSeNKRUpp Ag1ST qUARTeR

oCTobeR 01 – deCembeR 31, 2012

Developing the future.

stand: 07.02.2013

CoNTeNTS

ThyssenKrupp in brief

ThyssenKrupp has 150,000 employees in around 80 countries working with passion and expertise to develop solutions for

sustainable progress. Their skills and commitment are the basis of our success. In fiscal year 2011/2012 ThyssenKrupp

generated sales of €40 billion.

For us, innovations and technical progress are key factors in managing global growth and using finite resources in a

sustainable way. With our engineering expertise in the areas of “Material”, “Mechanical” and “Plant”, we enable our customers

to gain an edge in the global market and manufacture innovative products in a cost- and resource-efficient way.

STAMMDATEN DER THYSSENKRUPP AKTIE

ISIN (International Stock Identification Number) DE 000 750 0001

Börsenplätze Frankfurt (Prime Standard), Düsseldorf

Kürzel

Börsen Frankfurt, Düsseldorf TKA

Reuters (Xetra-Handel) TKAG.DE

Bloomberg (Xetra-Handel) TKA GY

THYSSENKRUPP STOCK MASTER DATA

ISIN (International Stock Identification Number) DE 000 750 0001

Stock exchange Frankfurt (Prime Standard), Düsseldorf

Symbols

Frankfurt, Düsseldorf stock exchange TKA

Reuters (Xetra trading) TKAG.DE

Bloomberg (Xetra trading) TKA

C oNTeNTS1 s T q u A r T E r

O cT O b E r 01 – D E c E m b E r 31 , 2012

46RepoRT by The SUpeRviSoRy boARd AUdiT CommiTTee 47CoNTACT ANd 2012/2013 dATeS

31CoNSolidATed STATemeNT of fiNANCiAl poSiTioN 32 CoNSolidATed STATemeNT of iNCome 33 CoNSolidATed STATemeNT of CompReheNSive iNCome 34 CoNSolidATed STATemeNT of ChANgeS iN eqUiTy 35CoNSolidATed STATemeNT of CASh flowS 36SeleCTed NoTeS To The CoNSolidATed fiNANCiAl STATemeNTS

45Review RepoRT

03 STRATegiC developmeNT of The gRoUp 05gRoUp Review 12 bUSiNeSS AReA Review 21 ThySSeNKRUpp SToCK 21 iNNovATioNS 22 employeeS 23 fiNANCiAl poSiTioN 25 SUbSeqUeNT eveNTS 26 expeCTed developmeNTS ANd ASSoCiATed oppoRTUNiTieS ANd RiSKS

02 ThySSeNKRUpp iN figUReS

C o N d e N S e d i N T e R i m f i N A N C i A l S T A T e m e N T S

f U R T h e R i N f o R m A T i o N

i N T e R i m m A N A g e m e N T R e p o R T

This interim report was published on February 12, 2013.

02 Interim Report 1st Quarter 2012/2013 ThyssenKrupp in figures

ThyssenKrupp in figures GROUP

Continuing operations Full Group

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change Change in %

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change Change in %

Order intake million € 9,677 9,642 (35) 0 11,260 11,202 (58) (1)

Sales million € 9,596 8,837 (759) (8) 11,138 10,412 (726) (7)

EBITDA million € 676 458 (218) (32) 412 445 33 8

EBIT million € 256 219 (37) (14) (357) 204 561 ++

EBIT margin % 2.7 2.5 (0.2) — (3.2) 2.0 5.2 —

Adjusted EBIT million € 372 229 (143) (38) 25 74 49 196

Adjusted EBIT margin % 3.9 2.6 (1.3) — 0.2 0.7 0.5 —

EBT million € 102 66 (36) (35) (514) 40 554 ++

Adjusted EBT million € 218 76 (142) (65) (131) (90) 41 31

Earnings net of tax or net income/(loss)

for the period* million € 41 29 (12) (29) (460) 35 495 ++

Basic earnings per share € 0.08 0.06 (0.02) (25) (0.89) 0.07 0.96 ++

Operating cash flow million € (1,327) 78 1,405 ++ (1,815) (140) 1,675 92

Free cash flow million € (1,330) 736 2,066 ++ (2,054) 361 2,415 ++

Employees (Dec. 31) 155,601 150,860 (4,741) (3) 171,312 154,850 (16,462) (10)

Net financial debt (Dec. 31) million € 5,937 5,205 (732) (12)

Total equity (Dec. 31) million € 10,000 4,235 (5,765) (58)

*attributable to ThyssenKrupp AG’s shareholders

BUSINESS AREAS

Order intake (million €)

Sales (million €)

EBIT (million €)

Adjusted EBIT (million €) Employees

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 31. Dez 11 31.12.2012

Components Technology 1,778 1,324 1,753 1,345 169 43 103 42 30,936 27,789

Elevator Technology 1,466 1,616 1,348 1,532 113 171 142 169 46,581 47,897

Plant Technology 871 1,825 943 1,001 125 110 125 110 13,786 14,359

Marine Systems 222 178 366 305 (116) 31 39 30 5,301 3,817

Materials Services 3,201 2,765 3,145 2,815 40 36 40 40 27,910 26,280

Steel Europe 2,705 2,403 2,530 2,253 102 29 102 30 28,273 27,629

Corporate 33 55 35 55 (99) (112) (101) (97) 2,814 3,089

Consolidation (599) (524) (524) (469) (78) (89) (78) (95) 0 0

Continuing operations 9,677 9,642 9,596 8,837 256 219 372 229 155,601 150,860

As part of its strategic development program ThyssenKrupp is divesting its steelmaking and processing plants in Brazil and the USA. At September

30, 2012 the Steel Americas business area met the requirements for classification as a discontinued operation under IFRS. This had been the case

for Stainless Global since September 30, 2012; the combination of the stainless business with the Finnish company Outokumpu was successfully

completed on December 28, 2012. Until the end of December 2012 the Group’s continuing operations comprised the remaining six business areas

and Corporate. At January 01, 2013 the Plant Technology and Marine Systems business areas were combined into the new Industrial Solutions

business area.

Interim Report 1st Quarter 2012/2013 Strategic development of the Group 03

Strategic development of the Group

ThyssenKrupp is a diversified industrial group firmly focused on the markets of the future. As a partner to its customers

the Group uses its leading engineering expertise to develop technological solutions for greater resource efficiency and

sustainable processes and products. With our strategic development program we are pursuing a holistic plan to move

the Group forward competitively and sustainably. The pillars of the program are continuous portfolio optimization,

changes to our corporate culture and our leadership and organizational structure, and a stronger performance

orientation. This will strengthen our financial base and give us freedom to strategically expand our business activities. In

the 1st quarter 2012/2013 we made further progress with our strategic development program.

Portfolio further optimized

The combination of Inoxum, the former Stainless Global business area, and the Finnish stainless steel manufacturer

Outokumpu was successfully completed on December 28, 2012. We have therefore implemented the portfolio measures

announced in May 2011 in the planned time frame. With the closing of the transaction ThyssenKrupp received €1 billion

cash and transferred external financial liabilities of Inoxum to Outokumpu. This led directly to a reduction in the Group’s

net financial debt. Outokumpu also took over pension obligations of Inoxum. ThyssenKrupp holds a 29.9% share in the

new company and has a financial receivable outstanding against Outokumpu.

The sale of Steel Americas is also proceeding to plan. Since November 2012 we have been giving a selection of

potential buyers the opportunity to analyze the plants in a due diligence process and submit binding purchase offers. We

are confident of finding a new way forward for both plants before the end of this fiscal year. The proceeds from the sale

will significantly reduce our net financial debt.

Despite the current financial restrictions we carried out targeted investment measures to stimulate growth in selective

areas in the reporting period. For example the Elevator Technology business area completed the takeover of the

business activities of AMCO Elevator Inc. based in Indianapolis/Indiana, USA on December 31, 2012.

Changes in the leadership system and leadership culture

On November 21, 2012 the Supervisory Board decided to appoint Oliver Burkhard to the Executive Board of

ThyssenKrupp AG effective February 01, 2013. From April 01, 2013 he will take on the function of labor director as

successor to Ralph Labonte, who is leaving the Company at March 31, 2013 for health reasons.

On December 10, 2012 the Supervisory Board followed the recommendation of the Personnel Committee and terminated

the appointments of the Executive Board members Dr. Olaf Berlien, Dr. Jürgen Claassen and Edwin Eichler effective

December 31, 2012. The decision was made in connection with the overall responsibility of the Executive Board for the

management of business and the leadership culture of the Group. Dr. Olaf Berlien, Dr. Jürgen Claassen and Edwin

Eichler were in agreement with the termination of their appointments and are thereby supporting the necessary changes

to the leadership system and the full-scale transformation of the leadership culture in the Group.

To strengthen our performance and enhance our leadership culture Groupwide, the Group leadership structure is

currently being modified. A matrix organizational structure is being introduced to optimize the way business units,

functions and regions work together. Roles, rules and responsibilities will be clarified, processes – where necessary –

redefined, and appropriate structural changes made. With the reorganization of the Executive Board effective January

01, 2013, structural changes have already been implemented. According to their function the business area

management board members now report directly to the Chief Executive Officer, the Chief Financial Officer, or the Chief

Human Resources Officer of ThyssenKrupp AG. This will permit more direct cooperation and more efficient

communication between the operating companies and Group management. At February 01, 2013 the corporate centers

were reduced and reorganized. In the future each corporate center will bear global responsibility for standards and

processes. The business areas will have central functions analogous with the structure at Group level to optimize

cooperation between the Group and business areas. In the coming months all further structures and processes will be

planned in detail also to include the regions. We plan to begin working in this new structure from October 2013.

04 Interim Report 1st Quarter 2012/2013 Strategic development of the Group

Efficiency advantages through combining of business units

At January 01, 2013 the business areas Plant Technology and Marine Systems were combined to form the new Industrial

Solutions business area. The business models of the two units are very similar. Both have strong capabilities in

engineering, project management, and purchasing. The combination allows each area to profit from the strengths of the

other and their management structures to be streamlined. Overall the Group’s successful project business will be further

strengthened. Also effective January 01, 2013 we combined the Group companies Fördertechnik and Polysius within the

Industrial Solutions business area. This will improve our position in the mining, minerals and cement markets served by

the two subsidiaries. It also eliminates unnecessary overlaps and creates efficiency advantages. With five business

areas in the future, the complexity of the Group will be reduced.

Corporate program impact

Since the introduction of impact in May 2011 numerous performance measures have been implemented. With “impact

300” we set ourselves the goal of achieving a positive EBIT effect of €300 million through performance measures in the

2011/2012 fiscal year. We exceeded this target and are now aiming even higher: In the three fiscal years up to and

including 2014/2015 we aim to achieve a cumulative positive EBIT effect of €2 billion through performance measures.

We want to achieve €500 million of this in the current fiscal year, and €750 million in each of the following two years.

The success of many impact measures and initiatives in the past demonstrates that the program has succeeded in

effectively mobilizing employees and managers. We are confident that we will also achieve the targets of “impact 2015”.

Optimization program at Steel Europe with a savings volume of €500 million

On the basis of a market and competition analysis, the new leadership team of the Steel Europe business area has

developed a package of measures to sustainably improve the steel unit’s profitability and competitiveness. The

optimization program plans to achieve a savings volume of €500 million by the 2014/2015 fiscal year. That means the

Steel Europe business area will make an important contribution to improving the performance of the Group as a whole.

The “BiC-reloaded” optimization program is a forceful initial step towards improving the position of the ThyssenKrupp

Group’s European steel operations in a difficult market environment and achieving the profitability and capital efficiency

required of all the Group’s business operations under the Strategic Way Forward.

Under the optimization program, the workforce of Steel Europe will be reduced in a socially responsible way by over

2,000 employees. As a result of possible disposals, the number of employees could be reduced by a further 1,800.

Interim Report 1st Quarter 2012/2013 Group review 05

Group review

Operational and strategic milestones achieved

In a difficult economic environment in the 1st quarter 2012/2013 (October 01 – December 31, 2012) ThyssenKrupp

achieved its operational and strategic goals.

At €229 million, adjusted EBIT from continuing operations was at the top end of the forecast range of around

€200 million. All business areas made a positive contribution to EBIT. With €351 million the capital goods businesses

accounted for a significantly higher share of adjusted EBIT than the materials businesses with €70 million. By contrast

adjusted EBIT from the corporate area including consolidation items came to €(192) million.

The continuing operations’ free cash flow amounted to €736 million, an improvement of around €2.1 billion on the prior-

year quarter reflecting our efforts to optimize the structure of our cash flow profile.

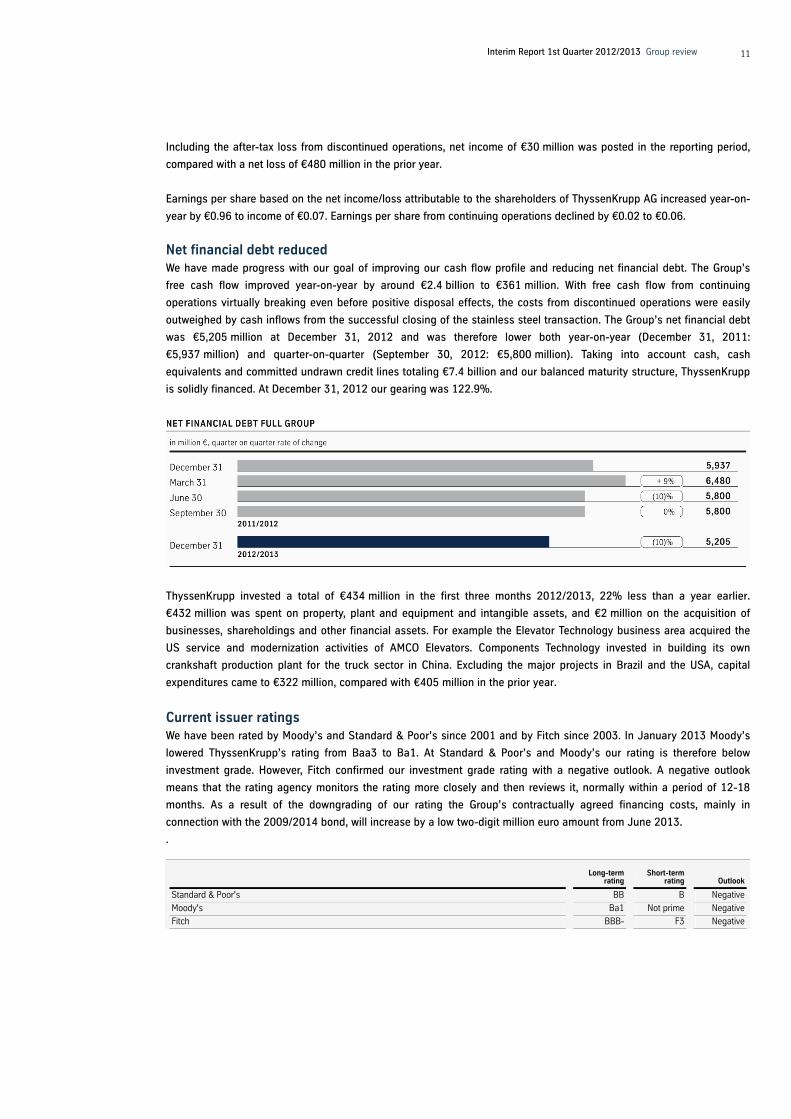

On this basis we succeeded in reducing net financial debt from €5.8 billion to €5.2 billion in the 1st quarter 2012/2013;

in the year-earlier quarter we reported an increase of around €2.2 billion.

The highlights for the first three months 2012/2013:

– Despite the divestments, order intake from continuing operations was almost level with the prior year at €9.6 billion.

The capital goods businesses reported an increase year-on-year. Plant Technology and Elevator Technology each

achieved new record orders. While plant orders more than doubled, elevator orders were up by a strong 10%. However,

weak market demand and low prices weighed on the materials business.

– Sales from continuing operations were 8% lower at €8.8 billion. Plant and elevator sales growth could not offset the

divestments and declines in other business areas.

– Adjusted EBIT from continuing operations came to €229 million, compared with €372 million in the prior-year quarter.

All business areas posted positive earnings; the biggest contribution came from Elevator Technology, which also

succeeded in improving its margin to 11%.

– EBIT from continuing operations was €219 million, down from €256 million in the prior-year period. EBIT margin was

almost unchanged at 2.5% compared with 2.7% a year earlier.

– Earnings per share from continuing operations decreased from €0.08 to €0.06.

– Including the discontinued operations Steel Americas and Stainless Global (sold at December 28, 2012) order intake

for the full Group in the first three months 2012/2013 came to €11.2 billion (prior year: €11.3 billion), and sales to

€10.4 billion (prior year: €11.1 billion). Adjusted EBIT increased from €25 million to €74 million.

– Free cash flow for the full Group improved by around €2.4 billion year-on-year to €361 million. The costs of

discontinued operations were significantly outweighed by cash inflows from the successful closing of the stainless

steel transaction.

– Net financial debt for the Group as a whole amounted to €5,205 million at December 31, 2012 and was therefore down

both year-on-year (December 31, 2011: €5,937 million) and quarter-on-quarter (September 30, 2012: €5,800 million).

Taking into account cash and cash equivalents and undrawn committed credit lines totaling €7.4 billion as well as our

balanced maturity structure, ThyssenKrupp is solidly financed. At December 31, 2012 gearing was 122.9%.

Interim Report 1st Quarter 2012/2013 Group review 06

Economic growth still weak

The economic environment remained extremely weak last year. Growth in global GDP slowed further to only 2.8% in

2012. There were significant differences in growth between the industrialized and the emerging countries.

The industrialized countries recorded GDP growth of only 1.3% in 2012. This reflected in particular the slowdown in the

euro zone, where economic output fell by a total of 0.6%. The economies of southern Europe in particular are in

recession due to the ongoing debt crisis. However, German GDP increased by a moderate 0.7% thanks to high exports

and rising consumer spending due to the positive labor market situation.

The US economy recovered only moderately in 2012. The only slow improvement on the labor market and the pressure

to consolidate public-sector budgets weighed on the economy. Nevertheless, a slight increase in consumer spending

and higher business spending contributed to growth of 2.2%. In Japan GDP grew by 1.6% due to disaster-related

reconstruction; the strong yen slowed the growth in exports.

In the emerging economies the previously mainly high growth rates slowed slightly. GDP growth in these countries fell to

5.0% overall in 2012, also due to the flat economy in Europe. Nevertheless, China and India still grew relatively strongly

at 7.8% and 5.6% respectively.

Situation in the sectors mixed

Flat carbon steel – The weak economic climate also weighed on the international steel markets. Based on provisional

estimates, global demand for finished steel increased by only 2% to roughly 1.42 billion metric tons in 2012. Global

crude steel output rose by 1% to 1.55 billion metric tons; in the 4th quarter 2012 output showed a year-on-year increase

of 3%. The smaller increase in global steel consumption was mainly due to slower growth in China, where demand

climbed by only 3% to 654 million tons in 2012. EU steel demand fell by 9% to 143 million tons. In Germany demand

decreased by 7% to 38.4 million tons. German crude steel production at 42.7 million tons was 4% down from the albeit

very high prior-year level. US finished steel demand increased by 8% to 96 million tons, mainly due to buoyant auto

industry activity.

Interim Report 1st Quarter 2012/2013 Group review 07

Demand on the European flat steel market showed a sharp decline in 2012. Above all in the southern European countries

demand from key customer sectors such as the automotive and construction industries slumped dramatically. Strongly

export-oriented customers in Germany too recently reported lower utilization levels. The fall in demand was exacerbated

by a large inventory drawdown. In the final quarter 2012 flat steel use in the EU is expected to show a further year-on-

year decline. However, the economic cycle may have reached its low point. With imports remaining moderate, European

flat steel suppliers recently recorded a slight recovery in orders. Prices on the European spot markets have also

bottomed out. However the moderate upturn towards the end of the reporting period was mainly due to a significant rise

in iron ore prices. After previously dropping sharply, prices in North America also recovered slightly in the course of the

4th quarter 2012. Alongside the automotive and energy industries, the housing construction sector recently generated

positive impetus again for steel demand.

Automotive – Global automobile production increased by an estimated 6% to just under 79 million cars and light trucks

in 2012. However there were very marked regional differences. In the USA, strong pent-up demand as a result of the

aging vehicle fleet led to a 16% increase in production to 9.8 million vehicles. Sales in the USA climbed 13% to

14.4 million vehicles; 4th-quarter sales showed a year-on-year rise of 10% to 3.6 million units. China produced an

estimated 17.3 million vehicles in 2012, 8% more than a year before. After the disaster-related slump the year before,

Japan increased its production by 19% to 9.4 million vehicles.

In western Europe an estimated 14.0 million cars and light trucks rolled off the production lines in 2012, almost 8%

fewer than the year before. Particularly in southern Europe sales declined sharply as a result of the debt crisis. New

registrations in the EU decreased by 8% to 12.1 million cars altogether, and by 10% to 2.7 million units in the 4th

quarter 2012. The German car market performed better by comparison. For the full year new registrations were down by

3% at 3.1 million vehicles, in the 4th quarter 2012 they slipped 6% to 0.7 million vehicles. Output remained virtually

unchanged; however, due to statistical changes a 7% decline in production to 5.7 million cars and light trucks will be

reported.

Machinery – Due to weaker capital spending in many countries the sector was unable to sustain the prior year’s very

high rate of expansion in 2012. Growth in machinery production slowed to 6% in the USA and to 12% in China.

Production in Japan showed a slight decline of 1%.

German machinery manufacturers increased their output by 1% in 2012, but only thanks to a high order backlog from

the prior year. New orders from the domestic market fell by 8%, while foreign orders remained stable in the course of the

year. In the 4th quarter 2012 the order situation in the German machinery sector brightened. Overall orders increased by

3% year-on-year. Demand for elevators and escalators in 2012 was down from the year before .

Construction – The construction sector in the industrialized countries was mainly weak in 2012. While the US property

market stabilized at a low level in the course of the year, there were further declines in the countries of southern Europe.

The emerging countries China and India achieved higher growth in construction output, with increases of 7.9% and 6.8%

respectively.

The German construction industry was in robust shape in 2012. Housing construction in particular showed strong

growth, benefiting from low mortgage rates and from the uncertainties emanating from the financial markets. German

construction output increased by an estimated 2% in 2012.

Interim Report 1st Quarter 2012/2013 Group review 08

ThyssenKrupp: Orders stable, sales lower

Against the background of the continuing difficult economic situation, ThyssenKrupp delivered a robust performance

overall in the 1st quarter 2012/2013. Order intake was down only slightly year-on-year while sales showed a steeper

decline mainly for cyclical reasons but also on account of disposals.

CONTINUING OPERATIONS IN FIGURES

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

Order intake million € 9,677 9,642 0

Sales million € 9,596 8,837 (8)

EBITDA million € 676 458 (32)

EBIT million € 256 219 (14)

EBIT margin % 2.7 2.5 —

Adjusted EBIT million € 372 229 (38)

Adjusted EBIT margin % 3.9 2.6 —

EBT million € 102 66 (35)

Adjusted EBT million € 218 76 (65)

Income/(loss) net of taxes (attributable to ThyssenKrupp AG's shareholders) million € 41 29 (29)

Basic earnings per share € 0.08 0.06 (25)

Operating cash flow million € (1,327) 78 ++

Free cash flow million € (1,330) 736 ++

Employees (Dec. 31) 155,601 150,860 (3)

In the first three months of the fiscal year the continuing operations achieved new orders of €9.6 billion, roughly level

with the year before. Growth was achieved in Plant Technology and Elevator Technology, with both reporting record

orders. However, orders for industrial components and materials were down, reflecting reduced demand and disposals.

Lower volumes and above all lower prices additionally weighed on steel business in Europe and global materials sales.

Sales from continuing operations decreased 8% year-on-year to €8.8 billion. Growth achieved at Elevator Technology

and Plant Technology could not offset weaker sales in the other business areas.

Including the discontinued operations Steel Americas and Stainless Global, order intake in the Group in the first three

months 2012/2013 slipped 1% to €11.2 billion, sales were 7% lower at €10.4 billion.

Adjusted EBIT €229 million

In a difficult economic environment 1st quarter adjusted EBIT from continuing operations decreased to €229 million

from €372 million a year earlier. Nevertheless all business areas reported positive earnings, with the largest contribution

coming from the Elevator Technology business area.

Interim Report 1st Quarter 2012/2013 Group review 09

Adjusted EBIT from continuing operations was lower year-on-year. In the more cyclical materials operations this was

chiefly the result of weaker volumes and in particular weaker prices. In the capital goods businesses, profits dipped

temporarily at Plant Technology and Marine Systems, and were lower year-on-year at Components Technology as a

result of disposals and reduced demand. However, Elevator Technology reported significantly higher earnings and an

improved margin of 11%. Overall the capital goods businesses delivered a significantly larger contribution to adjusted

EBIT (€351 million) than the materials businesses (€70 million). By contrast adjusted EBIT from Corporate including

consolidation items came to €(192) million.

Adjusted EBIT margin from continuing operations decreased year-on-year from 3.9% to 2.6%.

Including Stainless Global and Steel Americas the Group’s adjusted EBIT increased from €25 million to €74 million, and

adjusted EBIT margin from 0.2% to 0.7%.

Special items with negligible effect on EBIT from continuing operations

In the 1st quarter 2012/2013 net positive special items contributed €10 million to EBIT from continuing operations.

Special items were mainly reported at Corporate for severance payments to former Executive Board members. They also

include restructuring expenses, in particular at the Materials Services business area.

SPECIAL ITEMS FROM CONTINUING OPERATIONS IN MILLION €

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

EBIT 256 219 (14)

+/- Disposal losses/gains (52) (5) 90

+ Restructuring expense 32 13 (59)

+ Impairment 155 (1) --

+ Other non-operating expense 9 6 (33)

- Other non-operating income (28) (3) 89

Adjusted EBIT 372 229 (38)

EBT from continuing operations lower year-on-year

In the reporting period the continuing operations achieved EBIT of €66 million, compared with €102 million a year earlier.

All operating business areas generated positive earnings. The materials operations achieved unconsolidated earnings of

€37 million, the capital goods businesses €275 million. Elevator Technology and Marine Systems significantly increased

their earnings contributions year-on-year. The Corporate area reported a loss before taxes of €163 million. Including the

discontinued operations the Group as a whole reports EBT of €40 million (prior year: €(514) million). Net income for the

full Group came to €30 million, up €510 million from the prior year.

Interim Report 1st Quarter 2012/2013 Group review 10

MILLION €

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012

Change in %

Adjusted EBIT Group 25 74 196

Special items (382) 130 ++

EBIT - Group (357) 204 ++

- Depreciation of capitalized borrowing costs eliminated in EBIT (11) (3) 73

+ Interest income 314 130 (59)

- Interest expense (459) (284) 38

- Items of interest income, net assigned to EBIT based on economic classification (1) (26) --

+ Items of interest expense, net assigned to EBIT based on economic classification 0 19 —

EBT - Group (514) 40 ++

- EBT Steel Americas 285 90 (68)

- EBT Stainless Global 331 (64) --

EBT from continuing operations 102 66 (35)

Analysis of the statement of income

At €8,837 million, net sales from continuing operations in the 1st quarter 2012/2013 were €759 million or 8% lower than

in the corresponding prior-year period. The cost of sales from continuing operations decreased by altogether €658 million

or 8% in parallel with the fall in sales, mainly reflecting a sales-related reduction in materials expense. Gross profit from

continuing operations decreased to €1,386 million, while gross margin remained unchanged at 16%.

The €10 million rise in research and development cost from continuing operations was chiefly attributable to the Plant

Technology and Steel Europe business areas.

Selling expenses from continuing operations decreased by €5 million, mainly reflecting lower expenses for sales-related

freight and insurance charges. General and administrative expenses from continuing operations fell by €10 million,

primarily due to lower restructuring expenses.

The €107 million reduction in other expenses from continuing operations was mainly due to the absence of the goodwill

impairment charges recognized in the prior-year quarter in connection with the sale of the civil operations of

Blohm + Voss.

Other gains and losses attributable to continuing operations were €60 million lower than a year earlier. This mainly

reflects the absence of the gains on the disposal of the Xervon group and the Brazilian Automotive Systems operations

recognized in the 1st quarter 2011/2012.

The €194 million reduction in financing income was caused primarily by exchange rate effects in connection with finance

transactions. The €203 million lower financing expense from continuing operations mainly resulted from currency losses

in connection with finance transactions.

Tax expense from continuing operations of €33 million resulted in an effective tax charge of 50% in the reporting period,

level with a year earlier.

After taking into account income taxes, the profit from continuing operations came to €33 million.

The after-tax loss from discontinued operations decreased by a substantial €531 million to €3 million. This is mainly the

result of a €265 million impairment charge for Stainless Global recognized in the prior-year quarter set against a

preliminary profit of €146 million from the disposal of the stainless steel business to Outokumpu provisionally recognized

in the reporting period pending completion of the purchase price allocation in connection with the 29.9% share in

Outokumpu.

Interim Report 1st Quarter 2012/2013 Group review 11

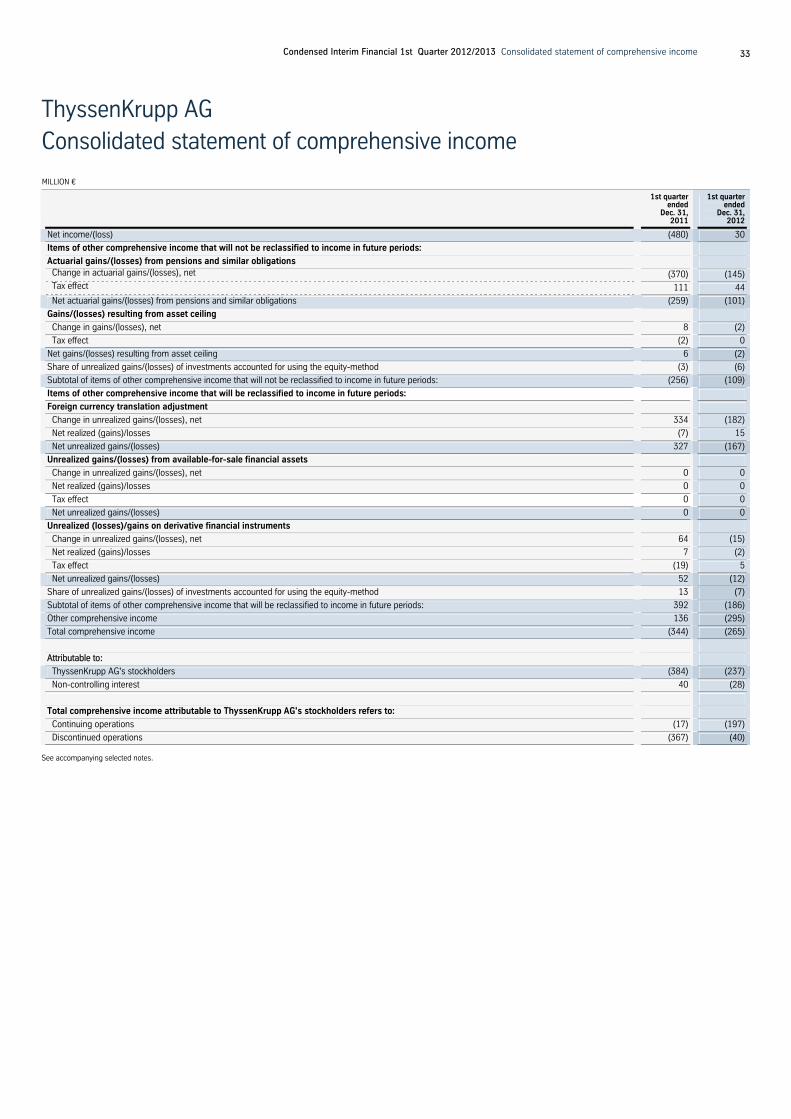

Including the after-tax loss from discontinued operations, net income of €30 million was posted in the reporting period,

compared with a net loss of €480 million in the prior year.

Earnings per share based on the net income/loss attributable to the shareholders of ThyssenKrupp AG increased year-on-

year by €0.96 to income of €0.07. Earnings per share from continuing operations declined by €0.02 to €0.06.

Net financial debt reduced

We have made progress with our goal of improving our cash flow profile and reducing net financial debt. The Group’s

free cash flow improved year-on-year by around €2.4 billion to €361 million. With free cash flow from continuing

operations virtually breaking even before positive disposal effects, the costs from discontinued operations were easily

outweighed by cash inflows from the successful closing of the stainless steel transaction. The Group’s net financial debt

was €5,205 million at December 31, 2012 and was therefore lower both year-on-year (December 31, 2011:

€5,937 million) and quarter-on-quarter (September 30, 2012: €5,800 million). Taking into account cash, cash

equivalents and committed undrawn credit lines totaling €7.4 billion and our balanced maturity structure, ThyssenKrupp

is solidly financed. At December 31, 2012 our gearing was 122.9%.

ThyssenKrupp invested a total of €434 million in the first three months 2012/2013, 22% less than a year earlier.

€432 million was spent on property, plant and equipment and intangible assets, and €2 million on the acquisition of

businesses, shareholdings and other financial assets. For example the Elevator Technology business area acquired the

US service and modernization activities of AMCO Elevators. Components Technology invested in building its own

crankshaft production plant for the truck sector in China. Excluding the major projects in Brazil and the USA, capital

expenditures came to €322 million, compared with €405 million in the prior year.

Current issuer ratings

We have been rated by Moody’s and Standard & Poor’s since 2001 and by Fitch since 2003. In January 2013 Moody’s

lowered ThyssenKrupp’s rating from Baa3 to Ba1. At Standard & Poor’s and Moody’s our rating is therefore below

investment grade. However, Fitch confirmed our investment grade rating with a negative outlook. A negative outlook

means that the rating agency monitors the rating more closely and then reviews it, normally within a period of 12-18

months. As a result of the downgrading of our rating the Group’s contractually agreed financing costs, mainly in

connection with the 2009/2014 bond, will increase by a low two-digit million euro amount from June 2013.

.

Long-term

rating Short-term

rating Outlook

Standard & Poor's BB B Negative

Moody's Ba1 Not prime Negative

Fitch BBB- F3 Negative

12 Interim Report 1st Quarter 2012/2013 Business area review

Business area review

Components Technology

COMPONENTS TECHNOLOGY IN FIGURES

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

Order intake million € 1,778 1,324 (26)

Sales million € 1,753 1,345 (23)

EBIT million € 169 43 (75)

EBIT margin % 9.6 3.2 —

Adjusted EBIT million € 103 42 (59)

Adjusted EBIT margin % 5.9 3.1 —

Employees (Dec. 31) 30,936 27,789 (10)

The business area supplies a range of high-tech components for general engineering, construction equipment and wind

turbines. In the auto sector our activities are focused on crankshafts, camshafts, steering systems, dampers, springs,

stabilizers and the assembly of axle modules.

Order intake and sales lower

At Components Technology the disposals of the previous fiscal year resulted in a structurally lower volume of business

in the 1st quarter 2012/2013. Order intake was 26% down from the prior-year quarter at €1.3 billion. Excluding the

disposals, order intake was 9% lower. The economic slowdown, particularly in western Europe, impacted demand for

auto and truck components. The midsize and premium car segments were also affected. By contrast in the USA, Brazil

and China the automotive business showed a positive performance. From the beginning of the new fiscal year the heavy

truck market declined sharply in particular in Europe and the USA, and also in Brazil and China there was no noticeable

recovery in demand. In the wind energy sector the uncertain investment climate, caused in part by the debate

surrounding the expiry of subsidy programs in the USA, resulted in project deferrals. In China further delays in

connecting existing wind turbines to the grid led to weakened demand and orders for component supplies. In western

Europe and China slower demand for infrastructure projects also impacted sales of building machinery components.

In line with the trend in orders, sales decreased year-on-year by 23% to €1.3 billion on account of the disposals.

Excluding the disposals, sales were 6% lower.

Earnings down

At €43 million, Components Technology’s EBIT in the reporting period was down from the high prior-year figure, which

included positive special items relating to the proceeds from the sale of the chassis component manufacturer

ThyssenKrupp Automotive Systems Industrial do Brasil and the once-only savings for healthcare at the US foundry

Waupaca. Adjusted EBIT was likewise lower year-on-year at €42 million. This reflected the absence of Waupaca’s

operating profit, the slowdown in the western European market for car and heavy truck components, and the ramp-up of

the new plants in China and India. Added to this was continued weak demand in the wind energy and infrastructure

sectors. Adjusted EBIT margin fell to 3.1%.

Interim Report 1st Quarter 2012/2013 Business area review 13

Elevator Technology

ELEVATOR TECHNOLOGY IN FIGURES

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

Order intake million € 1,466 1,616 10

Sales million € 1,348 1,532 14

EBIT million € 113 171 51

EBIT margin % 8.4 11.2 —

Adjusted EBIT million € 142 169 19

Adjusted EBIT margin % 10.5 11.0 —

Employees (Dec. 31) 46,581 47,897 3

The Elevator Technology business area supplies passenger and freight elevators, escalators and moving walks,

passenger boarding bridges, stair and platform lifts as well as service for the entire product range. Over 900 locations

worldwide form a tight-knit sales and service network that keeps us close to customers.

Two-digit growth in orders and sales

Elevator Technology continued its successful business performance in the 1st quarter 2012/2013. Both orders and sales

showed significant growth. Order intake was 10% higher year-on-year at €1.6 billion. In particular on the Chinese market

for new installations and on the North and South American markets, order intake continued to show a very positive

trend. The level of business in Europe was steady overall, with difficult conditions on some southern European markets,

such as Spain, being offset by positive trends on other markets.

Sales in the 1st quarter 2012/2013 were 14% higher at €1.5 billion. This pleasing growth was based on very positive

business with new installations on the Asian markets. Some sizable sales increases were also achieved in North and

South America. Overall volumes in both the new installations and the service and modernization businesses grew

continuously. In the service business the number of maintenance units under contract increased in all key regions.

Adjusted EBIT €169 million

Elevator Technology achieved EBIT of €171 million in the 1st quarter 2012/2013. Adjusted EBIT came to €169 million

and was therefore higher than in the 1st quarter of the prior year. This improvement resulted from both increased sales

and positive effects from the restructuring measures initiated in the last fiscal year. Adjusted EBIT margin was increased

to 11.0%.

Growth and investment program continued

To strengthen Elevator Technology’s competitiveness even further, we continued the growth and investment program in

the reporting period. The elevator plant in Neuhausen near Stuttgart is being expanded into a state-of-the-art

technology park. Central to this will be a development center for high-speed elevators. In addition a new technology and

customer center is to be built.

Interim Report 1st Quarter 2012/2013 Business area review 14

Plant Technology PLANT TECHNOLOGY IN FIGURES

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

Order intake million € 871 1,825 110

Sales million € 943 1,001 6

EBIT million € 125 110 (12)

EBIT margin % 13.3 11.0 —

Adjusted EBIT million € 125 110 (12)

Adjusted EBIT margin % 13.3 11.0 —

Employees (Dec. 31) 13,786 14,359 4

The Plant Technology business area is a leading international provider of specialized engineering and construction

services with strong innovative capabilities. The product portfolio includes chemical plants and refineries, equipment for

the cement industry, innovative solutions for the mining and extraction of raw materials, and production systems for the

auto industry. The business area’s equipment and processes open up new possibilities for environmental protection and

sustainability. At January 01, 2013 the Plant Technology and Marine Systems business areas were combined into the

new Industrial Solutions business area. More information on this is provided in the section “Strategic development of the

Group”.

Steep rise in orders, continued strong sales

Plant Technology delivered an outstanding performance particularly in chemical plant construction. In the first reporting

three months new orders with a total value of €1.8 billion were won, with the result that order intake more than doubled

from the prior-year figure of €871 million. Due to the low price of gas in North America, demand for fertilizer plants is

currently high. As a result ThyssenKrupp’s plant technology business succeeded in winning a mega-order in the USA for

two fertilizer plants worth €1 billion. The low price of gas will continue to open up opportunities for further chemical

plant construction projects in the North America over the long term. Demand for production systems for the automotive

industry and products for the mining and minerals sector was down slightly from the high prior-year level. Although the

market for cement plants is relatively stable overall, project deferrals have recently been observed.

In the 1st quarter 2012/2013 Plant Technology’s sales were 6% higher than a year earlier at €1.0 billion, confirming the

stable trend. The high order backlog of €7.4 billion at December 31, 2012 continues to secure a good workload.

EBIT only slightly down from high prior-year level

With EBIT of €110 million in the 1st quarter 2012/2013, the high level of the prior year was not quite reached due to

billing technicalities. EBIT margin slipped to 11.0%. Since there were no special items, adjusted EBIT and adjusted EBIT

margin were the same.

Interim Report 1st Quarter 2012/2013 Business area review 15

Marine Systems MARINE SYSTEMS IN FIGURES

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

Order intake million € 222 178 (20)

Sales million € 366 305 (17)

EBIT million € (116) 31 ++

EBIT margin % (31.7) 10.2 —

Adjusted EBIT million € 39 30 (23)

Adjusted EBIT margin % 10.7 9.8 —

Employees (Dec. 31) 5,301 3,817 (28)

Marine Systems is focused exclusively on naval shipbuilding. The business area’s core activities include the

development, construction and refit of submarines and naval surface vessels as well as extensive associated services.

After the completion of the sale of the civil shipbuilding operations in the prior year, work was started at the beginning of

the reporting year on further streamlining the organization of the naval shipbuilding operations and preparing the unit for

incorporation into the new Industrial Solutions business area. More information on this is provided in the section

“Strategic development of the Group”.

Order intake and sales holding up well

The markets of Marine Systems continue to perform positively; there are a number of promising projects worldwide. At

December 31, 2012 Marine Systems’ order backlog reached a record level of €9 billion.

In the 1st quarter 2012/2013 order intake amounted to €178 million. Major orders received included the modernization

of two type U206 submarines acquired by the Republic of Colombia from the German navy, and orders from the Swedish

navy. On an adjusted basis order intake was therefore higher year-on-year; the €222 million reported in the comparable

prior-year quarter included orders of €94 million in civil shipbuilding.

Sales came to €305 million. The prior-year figure of €366 million likewise contained the sales of the since sold civil

shipbuilding operations in the amount of €89 million.

Earnings at good prior-year level

Marine Systems’ EBIT at €31 million and adjusted EBIT at €30 million were level with the prior-year quarter minus the

civil shipbuilding operations. Adjusted EBIT margin was 9.8%, equaling the good prior-year level (without civil

shipbuilding).

German naval shipbuilding operations combined

To further optimize our organizational structure, we began combining our naval shipbuilding sites in Germany at the start

of the current fiscal year. This process was completed at the beginning of 2013. As a full-range supplier we provide

customers with naval vessels from a single source as well as extensive services. Our naval shipbuilding sites in Germany

are now combined under the name ThyssenKrupp Marine Systems GmbH.

Interim Report 1st Quarter 2012/2013 Business area review 16

Materials Services MATERIALS SERVICES IN FIGURES

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

Order intake million € 3,201 2,765 (14)

Sales million € 3,145 2,815 (10)

EBIT million € 40 36 (10)

EBIT margin % 1.3 1.3 —

Adjusted EBIT million € 40 40 0

Adjusted EBIT margin % 1.3 1.4 —

Employees (Dec. 31) 27,910 26,280 (6)

With 500 locations in more than 30 countries the Materials Services business area specializes in materials distribution

including technical services.

Further decline in demand – continued price and margin pressure

Materials Services achieved order intake of almost €2.8 billion in the 1st quarter 2012/2013, down 14% from the

corresponding prior-year period. Sales were 10% lower at €2.8 billion; on a like-for-like basis, excluding the Xervon

group from the prior-year figures, sales fell by 7%. In the warehousing business sales of carbon steel, stainless steel,

tubes and nonferrous metals decreased by 1.5% to just over 1.2 million tons.

The decline in workloads and demand in the main customer industries continued, the economic slowdown was

increasingly noticeable. Warehouse sales of metals dipped slightly year-on-year, while demand fell more steeply above

all towards the end of the quarter. This was the case in all markets and regions with the exception of North America.

Price and margin pressure was universally high. This also affected our international direct-to-customer and project

business. Intense competition and increasing order deferrals were the order of the day. However, our materials and

service operations for the aerospace industry achieved further growth. Plastics sales mirrored the performance of

metals.

Demand for metallurgical raw materials was impacted by numerous production cutbacks and stoppages in the steel

industry. Thanks to several special projects in the 1st quarter, capacity utilization and sales of our steel mill services

were almost maintained at the prior-year level.

EBIT stable at prior-year level

Despite the significant slide in sales, adjusted EBIT was level with the year-earlier period at €40 million. Cost reduction

measures at all levels, particularly in logistics and administration, contributed to this. After special items, EBIT was down

from the year before at €36 million; as a result EBIT margin in the traditionally weaker 1st quarter remained at 1.3%;

adjusted EBIT margin came to 1.4%.

Interim Report 1st Quarter 2012/2013 Business area review 17

Steel Europe STEEL EUROPE IN FIGURES

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

Order intake million € 2,705 2,403 (11)

Sales million € 2,530 2,253 (11)

EBIT million € 102 29 (72)

EBIT margin % 4.0 1.3 —

Adjusted EBIT million € 102 30 (71)

Adjusted EBIT margin % 4.0 1.3 —

Employees (Dec. 31) 28,273 27,629 (2)

The Steel Europe business area brings together the Group’s flat carbon steel activities, mainly in the European market.

Premium flat products are supplied to customers in the auto industry and other steel-using sectors. The range also

includes products for attractive specialist markets such as the packaging industry.

Orders and sales lower on account of selling prices

The persistent market weakness above all in the euro zone continued to impact the performance of the Steel Europe

business area in the 1st quarter 2012/2013. Order intake was down 11% year-on-year at €2.4 billion. Since order

volumes increased slightly, the decline was due to the lower prices at which these orders were booked.

Sales were likewise 11% lower at €2.3 billion. This too primarily reflects the softening of average selling prices against

the prior year. However, compared with previous months prices remained largely stable. Overall shipments were roughly

equal with the year before. Lower sales to the automotive industry and its suppliers, the transformer sector and other

industrial customers were offset by increased deliveries to the packaging and tubes industries. Shipments to distributors

and steel service centers were also higher year-on-year.

Production cutbacks continue

Crude steel production including supplies from Hüttenwerke Krupp Mannesmann at 2.6 million tons was 7% lower than

in the prior-year quarter when blast furnace 9 was still in operation. With demand remaining weak, it has not yet been

necessary to restart the newly relined unit. Lower operating levels also remained necessary in the downstream rolling

and coating operations. Short time working continued at numerous plants.

EBIT down sharply

EBIT fell to €29 million and EBIT margin to 1.3% in the reporting period. The main reason for this drop in earnings was

the persistent market weakness in Europe with selling prices down from the prior year. The Groupwide improvement

program impact was again only partly able to offset the negative cost and market effects. Special items had virtually no

effect on earnings: Adjusted EBIT was €30 million, adjusted EBIT margin 1.3%.

Interim Report 1st Quarter 2012/2013 Business area review 18

Corporate at ThyssenKrupp AG Corporate comprises the Group’s head office including management of the business areas. It also includes the business

services activities in the areas of finance, communications, IT and human resources, as well as non-operating real estate

and inactive companies. Sales of services by Corporate companies to Group companies in the 1st quarter 2012/2013

came to €55 million, up from €35 million a year earlier.

EBIT amounted to €(112) million, compared with €(99) million in the prior-year period. Adjusted EBIT came to €(97)

million, compared with €(101) the year before.

Steel Americas (discontinued operation) STEEL AMERICAS IN FIGURES

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

Order intake* million € 583 560 (4)

Sales* million € 498 488 (2)

EBIT million € (288) (87) 70

EBIT margin % — — —

Adjusted EBIT million € (288) (87) 70

Adjusted EBIT margin % — — —

Employees (Dec. 31) 4,081 3,990 (2)

* including internal orders/sales within the Group

With its steelmaking and processing plants in Brazil and the USA, the Steel Americas business area is tapping into the

North American market for premium flat steel products. As part of the strategic development program, ThyssenKrupp is

to dispose of these plants. More information on this is provided in the section “Strategic development of the Group”. At

September 30, 2012 Steel Americas met the requirements for classification as a discontinued operation under IFRS.

Order intake and sales lower due to selling prices

In the 1st quarter 2012/2013 the Steel Americas business area’s order intake was 4% down from a year earlier at

€560 million. In a difficult business environment sales at €488 million were likewise 2% lower year-on-year as a result of

selling prices, while production and shipments showed a slight overall increase. The steel mill in Brazil produced around

0.9 million tons of slabs in the 1st quarter 2012/2013 which it supplied to the US processing plant, Steel Europe and

customers in Brazil and North America. Altogether the business area sold 0.6 million tons of flat steel to North American

customers and 0.1 million tons of slabs on the Brazilian and North American markets, and supplied 0.2 million tons of

slabs to Steel Europe.

Steel Americas made further progress with customer certification. The certification processes were rigorously expedited

particularly in the automotive industry and almost completed in the pipe & tube sector.

EBIT improved from year earlier

EBIT improved in the reporting period by €201 million to €(87) million, there were no special items. The improvement

resulted from progress made on the operational side – in particular with cost optimization, the amount and composition

of reducing agents consumed, and an increased focus on customer segments with stronger margin potential. Also, the

classification as a discontinued operation resulted in the absence of depreciation expenses for non-current assets,

which in the first three months 2012/2013 would have come to €111 million; these were reported in the earnings of the

prior-year quarter in the amount of €91 million. The main reason for the continued negative earnings was the difficult

business environment on the North American market with an unsatisfactory price level above all in service center

business, which is particularly important for the startup. In addition the inefficient utilization of capacities in the

prevailing climate also weighed on earnings.

Interim Report 1st Quarter 2012/2013 Business area review 19

Technical ramp-up of Brazilian steel mill completed

The technical ramp-up of the integrated iron and steel mill in Brazil was completed in the 2011/2012 fiscal year. The

final hot-dip galvanizing line at the US processing plant is ready to start operation depending on market demand.

Stainless Global (discontinued operation) STAINLESS GLOBAL IN FIGURES

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

Order intake* million € 1,372 1,319 (4)

Sales* million € 1,438 1,402 (3)

EBIT million € (321) 72 ++

EBIT margin % (22.3) 5.1 —

Adjusted EBIT million € (56) (69) (23)

Adjusted EBIT margin % (3.9) (4.9) —

Employees (Dec. 31) 11,630 0 --

* including internal orders/sales within the Group

The discontinued operation Stainless Global, which was sold at December 28, 2012, produces premium stainless steel

flat products and high-performance materials such as nickel alloys, titanium and zirconium. The business now belongs

to the Finnish stainless steel producer Outokumpu. More information is provided in the section “Strategic development

of the Group”.

Order intake and sales lower

Stainless Global’s business performance in the 1st quarter 2012/2013 was impacted by declining prices for key raw

materials such as nickel. The lower prices for raw materials caused alloy surcharges to slip, and order intake fell by 4%

year-on-year to €1.3 billion.

Due to the lower price level and reduction in alloy surcharges, sales too were down 3% at €1.4 billion.

EBIT higher year-on-year

Including provisional deconsolidation income of €146 million, EBIT improved in the reporting quarter to €72 million, EBIT

margin to 5.1%. The continued difficult market environment for stainless steel flat products and the associated price

pressure weighed on the generally weaker earnings situation. In addition the lower nickel price had a negative impact.

Earnings also include the losses from the ramp-up of the new US stainless steel mill. At Stainless Global, too, the

classification as a discontinued operation meant that depreciation no longer had to be recognized for non-current

assets. In the first three months 2012/2013 these expenses would have amounted to €52 million; in the prior-year

quarter depreciation of €46 million was reported.

Adjusted EBIT amounted to €(69) million compared with €(56) million a year earlier, adjusted EBIT margin slipped to

(4.9)%. The decline in earnings was mainly due to ramp-up costs for the new facility in the USA; without this adjusted

EBIT came to €(24) million.

Stainless steel mill in the USA on schedule

At the US site in Calvert construction work and the ramp-up of already commissioned equipment is continuing as

planned. The ramp-up of the hot-rolled annealing and pickling line in the cold-rolling mill is almost complete. The

acceptance test certificate for the hot band annealing line was issued in December 2012. The ramp-up of the 1 million

ton per year capacity melt shop also began as planned in December 2012. Until the melt shop is fully ramped up the

location will continue to be supplied with hot band and slabs from the European mills.

Interim Report 1st Quarter 2012/2013 Business area review 20

ThyssenKrupp Group FULL GROUP

1st quarter ended

Dec. 31, 2011

1st quarter ended

Dec. 31, 2012 Change in %

Order intake million € 11,260 11,202 (1)

Sales million € 11,138 10,412 (7)

EBITDA million € 412 445 8

EBIT million € (357) 204 ++

EBIT margin % (3.2) 2.0 —

Adjusted EBIT million € 25 74 196

Adjusted EBIT margin % 0.2 0.7 —

EBT million € (514) 40 ++

Adjusted EBT million € (131) (90) 31

Net income/(loss) (attributable to ThyssenKrupp AG's shareholders) million € (460) 35 ++

Basic earnings per share € (0.89) 0.07 ++

Operating cash flow million € (1,815) (140) 92

Free cash flow million € (2,054) 361 ++

Employees (Dec. 31) 171,312 154,850 (10)

Including Steel Americas and Stainless Global, order intake for the Group as a whole came to €11.2 billion, 1% lower

than a year earlier. Sales slipped 7% to €10.4 billion. EBIT for the full Group improved from €(357) million to

€204 million. Accordingly EBIT margin increased from (3.2)% to 2.0%.

Interim Report 1st Quarter 2012/2013 ThyssenKrupp stock / Innovations 21

ThyssenKrupp stock

As a key pillar of the strategic development program, our portfolio measures substantially reduce capital employed in

the Group, particularly in our materials businesses. Together with structural improvements in our earnings and cash flow

profile and a higher proportion of more stable capital goods businesses, this should increase the potential of our stock

and improve our capital market valuation.

The visible progress made with the implementation of the Group’s strategic development program had a positive

influence on the performance of ThyssenKrupp’s stock. In addition news of steel price increases in Europe and the USA

boosted steel stocks. The subject of the debt crisis in Europe began to recede into the background.

In this environment ThyssenKrupp’s stock outperformed the DAX and DJ STOXX indices in the 1st quarter 2012/2013. In

particular the announcement of the boardroom restructuring, the publication of the annual financial statements, and the

closing of the stainless disposal in December 2012 were recognized by the capital market as visible signs of our

accelerated culture change and increased transaction confidence.

Towards the end of the 1st quarter on December 28, 2012 ThyssenKrupp’s share price stood at €17.76, 7% higher than

on September 30, 2012. In the same period the DAX and DJ STOXX indices gained 5.5% and 4.2% respectively.

Innovations

Innovations and technical progress are key factors in managing global growth and using finite resources in a sustainable

way. The following examples represent a selection of the many innovations in which our researchers and developers use

their engineering expertise to create new and resource-efficient products for our customers.

Vertical mill with individually driven rollers for the cement industry

The cement industry is responsible for 5% of global CO2 emissions. Mega trends such as population growth and

urbanization will lead to further rising demand for cement and as a result increasing emissions in the future.

Interim Report 1st Quarter 2012/2013 Innovations / Employees 22

One way of reducing these emissions is to produce high-quality cements which can be mixed with additives such as

limestone, granulated blast furnace slag or fly ash and still deliver the same concrete strength as conventional cement.

Waste products from other industrial processes such as steel manufacture are often used as additives. This places high

demands on the grinding systems, so that vertical roller mills currently in use featuring a centrally driven table are now

reaching their mechanical limits. The solution to this problem is the new QUADROPOL-RD grinding system from the Plant

Technology business area: Instead of a single drive system and a large central gear unit, it features individually driven

rollers – similar to an all-wheel drive vehicle. RD stands for “Roller Drive”. Significantly smaller standard gear units can

now be used to transmit the grinding forces. This enhances reliability and substantially reduces energy and water

consumption.

Assembled rotor shaft for electric vehicles

Our camshaft specialists in the Components Technology business area have adapted Presta’s proven joining process for

assembled camshafts for use on a rotor shaft for electric motors. This is the first time this technique – a combination of

positive and non-positive joining – has been used in the area of electric mobility.

Electric motors for battery-powered vehicles generally have to be extremely powerful but of low size and weight. The new

rotor shaft, which is supplied to customers ready-to-install, meets the associated requirements to a high degree thanks

to a load-dependent combination of different materials on a single shaft. Alongside the cams, other components such as

bearings, shaft sealing rings and closure caps can also be joined simply to the rotor shaft. In addition, rotor cooling and

sensor systems can be integrated in the hollow rotor. We have already received our first production order from a German

auto manufacturer.

Employees

ThyssenKrupp employed 150,860 people in its continuing operations on December 31, 2012, 4,741 or 3.0% fewer than

a year earlier. The decline was due to restructuring measures and in particular to disposals in connection with the

strategic portfolio optimization and affected the business areas Components Technology, Marine Systems, Materials

Services and Steel Europe. Elevator Technology and Plant Technology recruited new employees.

Compared with September 30, 2012 the number of employees decreased by 1,263 or 0.8%. The workforce in Germany

decreased by 346 or 0.6% to 58,101; its share in the total workforce was 38.5%. At the end of December 2012, 20.8%

of all employees were based in Europe outside Germany, 12.4% in North and Central America, 11.5% in South America,

15.9% in Asia and the Pacific region – in particular China and India – and 0.9% in Africa.

Including Steel Americas ThyssenKrupp had 154,850 employees worldwide at the end of December 2012, 16,462 or

9.6% fewer than a year earlier. Compared with September 30, 2012 the workforce decreased by 13,111 or 7.8%. The

employees of Stainless Global are no longer included in the Group’s numbers at December 31, 2012.

Interim Report 1st Quarter 2012/2013 Financial position 23

Financial position

Analysis of the statement of cash flows

The amounts taken into account in the statement of cash flows correspond to the item “Cash and cash equivalents” as

reported in the statement of financial position and also include the cash and cash equivalents relating to the disposal

groups including the discontinued operations. For the reporting period and the corresponding prior-year quarter the

discontinued operations comprise the activities of Steel Americas and Stainless Global.

In the 1st quarter 2012/2013 the net cash outflow from operating activities showed a significant year-on-year reduction

of €1,675 million to €140 million. Cash inflow from continuing operations amounted to €78 million, an improvement of

€1,405 million against the prior-year quarter. This was mainly due to a considerable improvement in funds tied up in

inventories and trade accounts receivable by altogether €1,063 million. In the discontinued operations, operating cash

flow improved by €270 million to €(218) million, due in particular to a smaller net loss before depreciation and deferred

taxes.

Investing activities resulted in a net cash inflow of €501 million, compared with a cash outflow of €239 million a year

earlier. In the continuing operations there was a cash inflow of €658 million compared with a cash outflow of €3 million

in the prior-year quarter. The main reason for the €661 million improvement was the disposal of the stainless steel

business to Outokumpu, which after taking into account the divested cash and cash equivalents resulted in proceeds of

€916 million; this was offset mainly by the absence of the proceeds from the sale of the Xervon group and the Brazilian

Automotive Systems operations recognized in the year-earlier quarter. In the discontinued operations the cash outflow

from investing activities was €79 million lower, above all due to reduced capital expenditure for property, plant and

equipment at Steel Americas.

Free cash flow, i.e. the sum of operating cash flows and cash flows from investing activities, in the continuing operations

improved significantly year-on-year by €2,066 million to €736 million. This was mainly the result of higher cash inflow

from operating activities. In the discontinued operations negative free cash flow was almost halved to €(375) million

thanks to reduced cash outflows from both operating activities and investing activities. Overall, free cash flow thus came

to €361 million.

Cash inflow from financing activities in the continuing operations came to €1,289 million, compared with a cash outflow

of €247 million in the prior-year quarter. The €1,536 million change resulted from a €783 million increase in net

borrowings and a €388 million reduction in cash outflow in connection with the financing of discontinued operations.

There was also a cash inflow from other financing activities of €74 million, compared with a cash outflow of €268 million

the year before. This €342 million change came about because compared with the year before the level of reductions in

liabilities to associated companies was significantly lower and smaller amounts were transferred to the factoring

company in connection with payments received from customers for already sold receivables. Cash inflow from financing

activities of discontinued operations decreased by €336 million; both in the reporting period and the prior-year quarter,

the financing activities mainly related to the inclusion of Steel Americas and Stainless Global in the Group financing

system. Overall cash inflow from financing activities increased by €1,200 million to €1,599 million.

24 Interim Report 1st Quarter 2012/2013 Financial position

Analysis of the statement of financial position

Compared with September 30, 2012 total assets decreased by a total of €1,017 million to €37,267 million. This includes

a currency translation-related reduction of €440 million, mainly due to movements in the US dollar exchange rate.

Non-current assets increased by €1,824 million. This sharp rise related mainly to two transactions resulting from the

combination of Stainless Global and the Finnish stainless steel producer Outokumpu implemented on December 28,

2012. In this connection ThyssenKrupp has a financial receivable outstanding against Outokumpu; this led to a

€1,199 million increase in non-current financial assets. In addition, ThyssenKrupp has a 29.9% share in the new

company; this resulted in particular in €481 million higher investments accounted for according to the equity method.

Deferred tax assets were €192 million higher, largely as a result of the increase in tax-deductible losses in Germany and

abroad.

Current assets decreased by a significant €2,841 million, of which €344 million related to currency translation effects.

Inventories stood at €6,566 million on December 31, 2012, up €199 million from September 30, 2012. The increase

mainly related to the Materials Services business area.

Trade accounts receivable were €504 million lower at €4,622 million. In particular this reflected measures to reduce

funds tied up in the Materials Services business area.

Of the steep €1,993 million increase in cash and cash equivalents, €736 million resulted from the positive free cash flow

in the reporting period – mainly due to a €1,000 million cash inflow from Outokumpu in connection with the disposal of

the stainless steel business at the end of December 2012 – and €1,577 million from net borrowings. This was partly

offset by cash outflows of €350 million in connection with the financing of discontinued operations.

Assets held for sale decreased by €4,607 million to €4,860 million. Of this sharp reduction, €4,383 million related to the

completed disposal of Stainless Global to Outokumpu. In addition, there was a €207 million reduction at Steel Americas

as a result of continuing business operation.

Total equity at December 31, 2012 was €4,235 million, down €291 million from September 30, 2012. The main factors

were the net actuarial losses from pensions and similar obligations (€101 million after taxes) recognized in other

comprehensive income, and unrealized losses from foreign currency translation (€167 million). The equity ratio fell

slightly from 11.8% to 11.4%.

Non-current liabilities increased by a net €1,382 million. This was mainly due to a €1,047 million increase in non-current

financial debt. The €45 million rise in accrued pension and similar obligations resulted in particular from the updated

interest rates used for the revaluation of pension and healthcare obligations at December 30, 2012, and allocations

recognized in income; this was offset by outpayments. The increase in other non-current provisions was influenced in

particular by provisions for possible effects from requirements under merger control law in connection with the disposal

of the stainless steel business to Outokumpu. Deferred tax liabilities were €105 million higher, mainly due to increased

opportunities for offsetting deferred tax assets and liabilities as a result of higher tax-deductible losses.

Interim Report 1st Quarter 2012/2013 Financial position / Subsequent events 25

Current liabilities decreased overall by €2,108 million, of which €139 million related to exchange rate effects.

Current provisions for employee benefits decreased by €87 million, mainly due to utilization. Current financial debt was

€510 million higher, mainly as a result of increased liabilities to financial institutions.

Trade accounts payable were €169 million lower, mainly due to reductions in the Components Technology and Materials

Services business areas.

Other current financial liabilities increased by €57 million mainly as a result of higher interest amounts payable. The

€79 million rise in other current non-financial liabilities mainly reflected higher advance payments.

Liabilities associated with assets held for sale decreased by €2,449 million to €1,465 million, primarily due to the

aforementioned disposal of Stainless Global to Outokumpu in December 2012 (€2,323 million). In addition, reductions of

€102 million in the Steel Americas business were the result of continuing business operation.

Subsequent events

Subsequent events between the end of the 1st quarter reporting period (December 31, 2012) and the date of

authorization for issuance (February 08, 2013) are presented in Note 11 to the interim financial statements.

Interim Report 1st Quarter 2012/2013 Expected developments 26

Expected developments and associated opportunities and risks Global economic growth remaining weak

There are still no signs of a full-scale global economic recovery this year. The reasons are the unsolved debt problems in

particular in the euro zone and slower rates of growth in the emerging economies. After 2.8% last year, global economic

growth of 3.0% is expected in 2013, with the emerging countries expanding overall by 5.3% and the industrialized

counties by only 1.4%. Stronger economic momentum is not expected before 2014.

High sovereign debt, the need for fiscal consolidation, and cautious capital investment are hampering growth in the euro

zone; GDP is therefore expected to fall slightly again in 2013. The recessionary trend in the southern European countries

is likely to continue. In Germany GDP could grow by 1.0% in 2013 – driven mainly by consumer and business spending

In the USA the pace of economic recovery will show little change. Increased consumer and business spending is

expected to lead to growth of 2.1%. In Japan, where impetus from the rebuilding process after the natural disaster is

slowing, growth of only 1.0% is forecast for 2013.

The current weaker pace of expansion in many emerging countries will continue. Nevertheless, the BRIC countries are

expected to remain the growth pillars of the global economy in 2013. GDP growth of 8.0% is forecast for China, and

6.5% for India.

Growth in sectors

Flat carbon steel – Against the background of the weak global economic recovery, the prospects for the steel market

remain subdued. Global finished steel demand is expected to increase by almost 4% to 1.47 billion metric tons in 2013;

this corresponds to crude steel production of 1.6 billion metric tons. The main impetus will come from the emerging

markets in Asia, Latin America and the Middle East. As in 2012 the growth in demand in these regions will be much

lower than in previous years. This is particularly true of China, where a 4% increase is forecast for 2013. In the USA steel

market growth will weaken to just under 4%. For the EU market we expect steel demand in 2013 to stabilize at the prior-

year level. Steel demand in Germany will be only slightly higher year-on-year at 39 million metric tons.

Automotive – The international auto market will continue to grow in 2013. Worldwide production of cars and light trucks

is expected to increase by just under 3% year-on-year to almost 81 million units. Chinese vehicle production will again

grow by 8%. In the USA growth will slow from the high prior-year level to 6%. The Brazilian auto market will recover

again, with around 4% expansion. After the catch-up effects of the prior year, auto production in Japan will show a slight

decline of around 2%. The Western European auto market remains subdued. Flat demand will cause production to fall

below the already very weak prior-year level.

Machinery – Growth in machinery production will weaken in 2013, with capital spending in many countries subdued.

Growth could slow to 2.5% in the USA and 10.5% in China. For Germany’s export-oriented machinery sector we expect

production to remain at the prior-year level.

Interim Report 1st Quarter 2012/2013 Expected developments 27

Construction – Construction activity will continue to show regional differences in 2013. In Western Europe construction

output will decrease year-on-year due mainly to continued steep declines in the southern countries. With housing

demand remaining strong, construction activity in Germany will increase slightly. The US construction sector could make

a noticeable recovery. Construction activity in India and China will remain strong with growth rates of 8.5% and over

10% respectively.

SITUATION ON IMPORTANT SALES MARKETS

2012 2013*

Demand for finished steel, million tons

World 1,419 1,471

Germany 38.4 39.0

USA 96 100

China 654 679

Vehicle production, million cars and light trucks

World 78.6 80.7

Western Europe/Turkey 14.0 13.9

Germany 5.7 5.7

USA 9.8 10.5

Japan 9.4 9.2

China 17.3 18.7

Brazil 3.0 3.2