5 Year Plan and Strategic Options

Submission to Monitor

31 December 2013

1

The Rotherham NHS Foundation Trust

DRAFT

TRFT – Strategic Direction

Page No.

1. Executive Summary 3 - 6

2. Strategic Direction – principles 7

3. Approach Taken 8 - 10

4. Clinical Sustainability 11

5. Financial Plan 12 - 22

6. Transformation Programme 23 - 28

7. Strategic Options 29 - 32

8. Conclusion 33

9. Potential Areas of Collaboration 34 - 35

10. Key Risks 36 - 37

11. Summary of Actions Over Next 3 Months 38 - 40

2 DRAFT

1.0 Executive Summary - Background

3

• The Trust is required to achieve financial (as well as clinical and operational)

sustainability.

• However, the Trust has not achieved a surplus position over the last 3 years and has

remained in deficit. Historically the provision of significant non-recurrent funding support

from the commissioners has masked the extent of the underlying deficit. The financial

difficulties were exacerbated in June 2012 by the introduction of the Electronic Patient

Record (EPR), resulting in significant operational difficulties which negatively impacted

on the ability to record clinical activity data and therefore to accurately reclaim income

from commissioners, resulting in significant reputational damage. These issues have

largely been resolved.

• However in October 2012, the Trust was found in breach of its Terms of Authorisation by

Monitor and in November 2012, commissioned Bolt Partners to formulate savings plans

(FY13/14 and FY14/15), and identify potential strategic options to achieve long term

financial sustainability.

• This work was financially driven. However, whilst the Trust is clinically sustainable at this

time, like other similarly sized trusts, there will be increasing future pressures on services

in terms of demand, clinical quality including patient expectations, professional, and

regulatory requirements.

• Clinical sustainability will need to be kept under review, to ensure strategies are delivered

where needed to secure long term resilience and continuity of high quality service

provision, affordably, to meet the needs of the population.

DRAFT

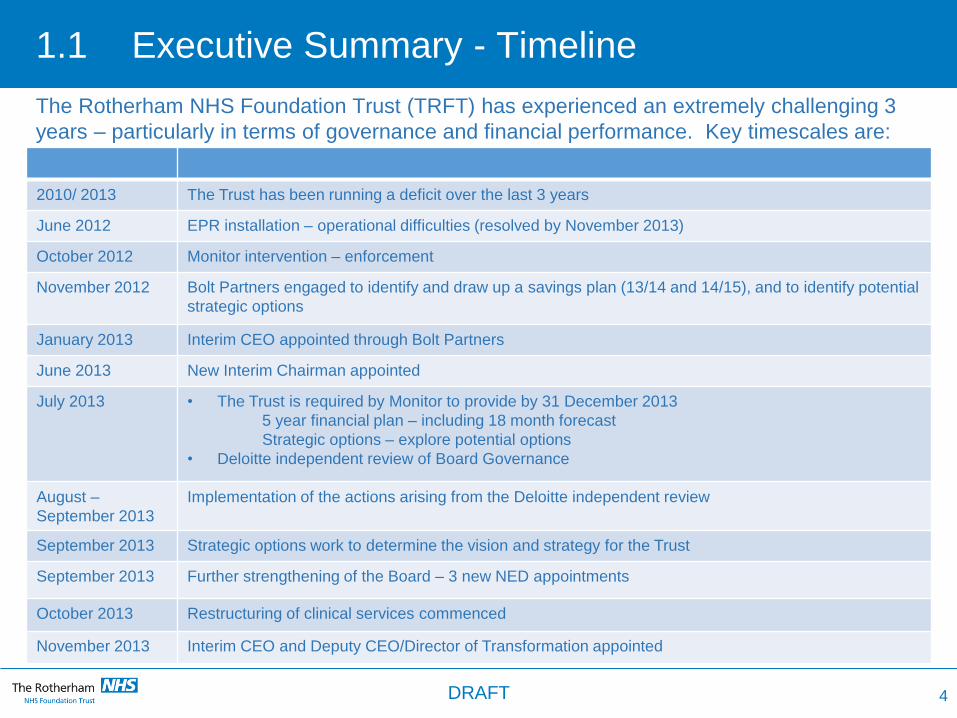

1.1 Executive Summary - Timeline

The Rotherham NHS Foundation Trust (TRFT) has experienced an extremely challenging 3

years – particularly in terms of governance and financial performance. Key timescales are:

4

2010/ 2013 The Trust has been running a deficit over the last 3 years

June 2012 EPR installation – operational difficulties (resolved by November 2013)

October 2012 Monitor intervention – enforcement

November 2012 Bolt Partners engaged to identify and draw up a savings plan (13/14 and 14/15), and to identify potential

strategic options

January 2013 Interim CEO appointed through Bolt Partners

June 2013 New Interim Chairman appointed

July 2013 • The Trust is required by Monitor to provide by 31 December 2013

5 year financial plan – including 18 month forecast

Strategic options – explore potential options

• Deloitte independent review of Board Governance

August –

September 2013

Implementation of the actions arising from the Deloitte independent review

September 2013 Strategic options work to determine the vision and strategy for the Trust

September 2013 Further strengthening of the Board – 3 new NED appointments

October 2013 Restructuring of clinical services commenced

November 2013 Interim CEO and Deputy CEO/Director of Transformation appointed

DRAFT

1.2 Executive Summary

• The outcome of the options work has demonstrated that the Trust is financially viable,

dependent upon achieving cost improvement programmes year on year.

• A savings plan of £12.2m has been established which has been risk rated down to

£10.3m. In its first year, the Trust expects to achieve a monthly surplus from Month 4

FY14/15 and a cumulative surplus by Month 10 FY14/15. This would achieve a Monitor

risk rating of 3.

• The CIP challenge FY14/15 of £10.3m, represents 4.5% of the cost base with savings in

the following 4 years (FY15/16 –FY18/19) of 4.5%, 4.0%, 3.1% and 3.0% respectively.

• The plan assumes an increased level of capital expenditure to support planned and

backlog investment.

• A contingency reserve of 1% (c£2.3m) has been allowed for each year of the plan.

• The CIP challenge, whilst broadly comparable to that facing other similar sized Trusts, will

require major organisational redesign to drive the efficiencies and culture change needed

to maintain/potentially exceed upper quartile performance year on year.

• A range of strategic options were identified and considered by the Trust Board. The three

options were: Option 1- the Trust as a standalone entity; Option 2- vertical integration with

a social care provider; and Option 3 – merger with another acute provider.

5 DRAFT

1.3 Executive Summary

• Following review of all the data and information, the Board decided to pursue Option 1 –

for the Trust to remain in its present form whilst also exploring potential opportunities for

collaboration with other acute providers in the local health economy. Option 2 was

rejected. It was agreed that Option 3 would not be ruled out in the long term, but would not

be pursued at the current time.

• In order to deliver the proposed plan, the Trust will need to apply a level of rigour and

execution to its savings plan which has not previously been demonstrated. A

Transformation Programme supported by a PMO is being established with clear

accountabilities and leadership to deliver the savings required.

• The potential risks and mitigating actions have been identified.

• The Trust is currently embarking on a restructuring of its clinical services and reducing the

number of its clinical divisions from 11 to 4. This aims to achieve improved governance

and efficiency and the clinical leadership and managerial focus necessary.

• To strengthen Trust Board leadership, in July 2013, the Interim Chairman was appointed,

followed in October 2013 by 3 new NEDs and in November 2013, the Interim CEO and

Interim Deputy CEO/Director of Transformation were appointed.

• The Trust Board is fully committed to the proposed plan and has already commenced

actions to ensure early delivery in the new financial year

6 DRAFT

2.0 Strategic Direction - Principles

The following set of principles underpin the plan:

• The need to ensure the continued delivery of high quality acute and community services to

the population of Rotherham and patients served by the Trust.

• The requirement to achieve clinical and financial sustainability.

• To ensure patients are at the heart of what we do, providing them with excellent clinical

outcomes and a first class experience.

• Achievement of current and future quality accreditation standards.

• Continual development of services that meet the changing healthcare needs of the patients

we serve.

• Partnership working across the local health economy to ensure wider sustainability of

healthcare provision.

• Secure arrangements for access to all specialist services.

• A realistic level of CAPEX investment over period of the plan.

7 DRAFT

3.0 Approach Taken

• The options work was overseen by the Trust Board, led by the Chairman and Interim CEO

supported by Bolt Partners, reporting to the CEO.

• At the outset, a 2 day strategic event took place in 2013 that included all key stakeholders,

i.e. commissioners, social services, Trust staff (clinical and managerial), Trust Board,

Governors and patient representation, to identify what the key strategic options should be

for the organisation.

• This resulted in the identification of potential options which were then fully explored with

stakeholders in the development of the plan.

• The clinical challenges currently facing the organisation were considered including: A&E;

maternity and paediatrics; our priority to deliver right care, right time, right place; and scale

of services, in order to assess current viability.

• The options work was also approached from the position that the Trust is currently clinically

sustainable and in particular assumed: on-going provision of a 24 hour A&E service,

supported by appropriate emergency care provision and a comprehensive and safe

maternity service; retention of acute and community services and improved integration.

• The options work was financially driven and focused internally on clinical engagement.

Whilst wider health economy clinical reference groups were not convened, Trust clinicians,

in addition to non-clinical staff, were able to regularly contribute views through Trust-wide

engagement events, the medical staffing committee and staff side.

8 DRAFT

3.1 Approach Taken

• Potential financial advantages of merger were considered at a high level only and

predicated on economies of scale at Trust Board, middle manager and back office levels.

• Data used was obtained from publically available sources such as annual accounts, CQC

and Dr Foster, which provided information on the Trust and organisations in the wider

health economy. These included:

• Strategic needs assessment of population profiles

• Geographical locations and travelling distances for the Trust catchment population

• Size, number and type of specialities and workforce profiles

• Income, expenditure and financial metrics

• Potential partner organisations were approached to secure input and views on the plan in

addition to their potential appetite to work collaboratively in different formats as per Options

1,2, and 3.

• Legal advice was taken to inform the nature of discussions to ensure no prejudice to any

future actions, particularly regarding any potential merger.

• The potential future impact of changes such as 7 days working and changes in clinical and

regulatory requirements was not factored into the assessment at this stage.

9 DRAFT

3.2 Approach Taken

This plan has been developed following engagement of key internal and external

stakeholders, including:

• On-going involvement of main commissioner in plan development to ensure

commissioner supported income levels and to reflect shared priorities including

commissioner and Trust-led initiatives.

• Regular Trust-wide engagement events led by the Chairman and CEO including

Governors, clinical and non-clinical staff and colleagues representing our main

commissioner.

• Discussions with working together partners/neighbouring Trusts on specific work

streams and potential options.

• On-going involvement of Medical Staff Committee and local staff side representatives.

• Discussions/briefings of local MPs by the Trust.

• External stakeholder briefings on work to develop strategic options, with the opportunity

to contribute views, e.g. with Rotherham Metropolitan Borough Council and social

services.

Feedback received from stakeholders was shared with the Trust Board by the Chairman,

CEO and Bolt Partners and taken into account as part of the decision making process.

10 DRAFT

4.0 Clinical Sustainability

• The outcome of the work undertaken by Bolt Partners identified the Trust as currently clinically viable.

• However, following investigation, whilst no concerns were identified regarding the quality of care, some specialties were found to be potentially suboptimal due to their relative low workload and size. Therefore, further work is needed to assess viability in more depth at specialty level in order to identify strategies to increase resilience in service delivery in the longer term. The impact of future clinical, regulatory and other national pressures such as 7 day working have not yet been taken into account. This is likely to demand increased levels of collaboration with other providers.

• Clinically led, systematic speciality based reviews will commence in early 2014, supported by information on service size, reference costs and clinical outcomes. This is essential to ensure financial and clinical sustainability and does not preclude potential disinvestment in some service lines where it is found that they have a continuous negative value.

• Like other similarly-sized Trusts, clinical viability and sustainability will need to be kept under constant review, to reflect potential changes in future requirements, such as royal college guidelines, accreditation requirements, 7 day working, changes in clinical practice, medical and technological advancement, patient demand and expectations.

• All cost improvement schemes will be subject to mandatory quality impact assessments, which will be signed off by the divisional clinical leads, the Chief Nurse and Medical Director. These will be robustly monitored through the newly formed project management office and quality governance committees.

11 DRAFT

5.0 Financial - Overview

• A 5 year financial plan has been developed.

• The forecast outturn for FY13/14 (as at month 8) is (£3.3m) and the FY14/15 underlying

deficit (after adjustments for non-recurrent items) is (£4.7m).

• After inflationary and other cost pressures, this would require achievement of a savings

target of £9.6m to break even in FY14/15.

• This plan achieves a surplus each year. This is dependent upon achieving CIP of £10.3m

(risk adjusted from £12.2m) in FY14/15, which represents 4.5% of the cost base and

savings in the following 4 years (FY15/16 –FY18/19) of 4.5%, 4.0%, 3.1% and 3.0%

respectively.

• In FY 14/15, the plan achieves in-month surplus by month 4 and cumulative surplus by

month 10

• Key planning assumptions are included in this section.

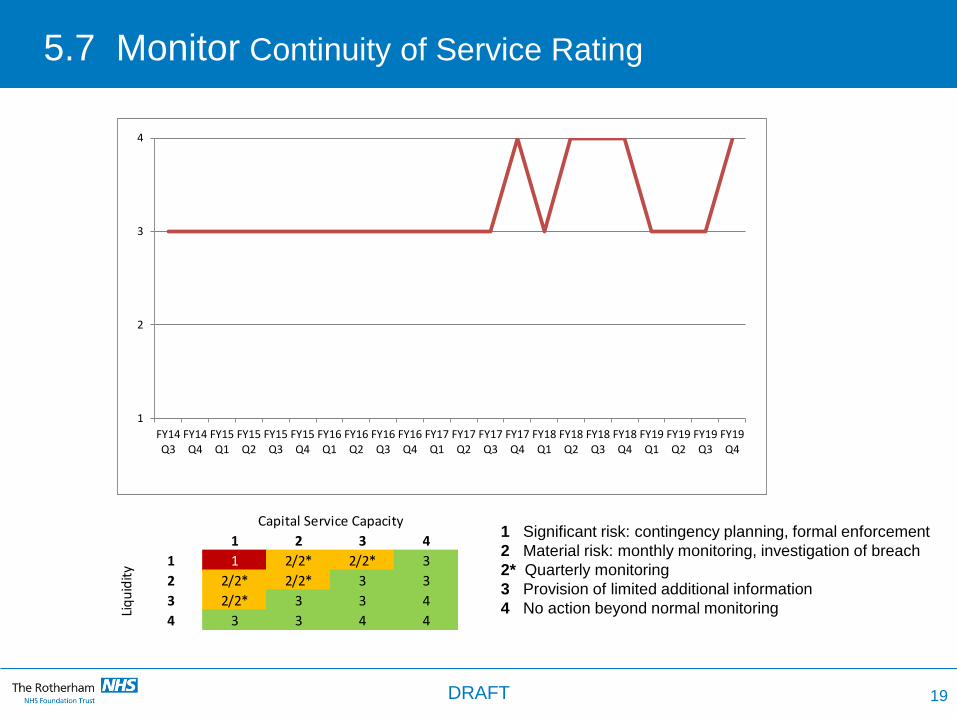

• The plan achieves a continuity of service risk rating of at least 3 throughout the plan period.

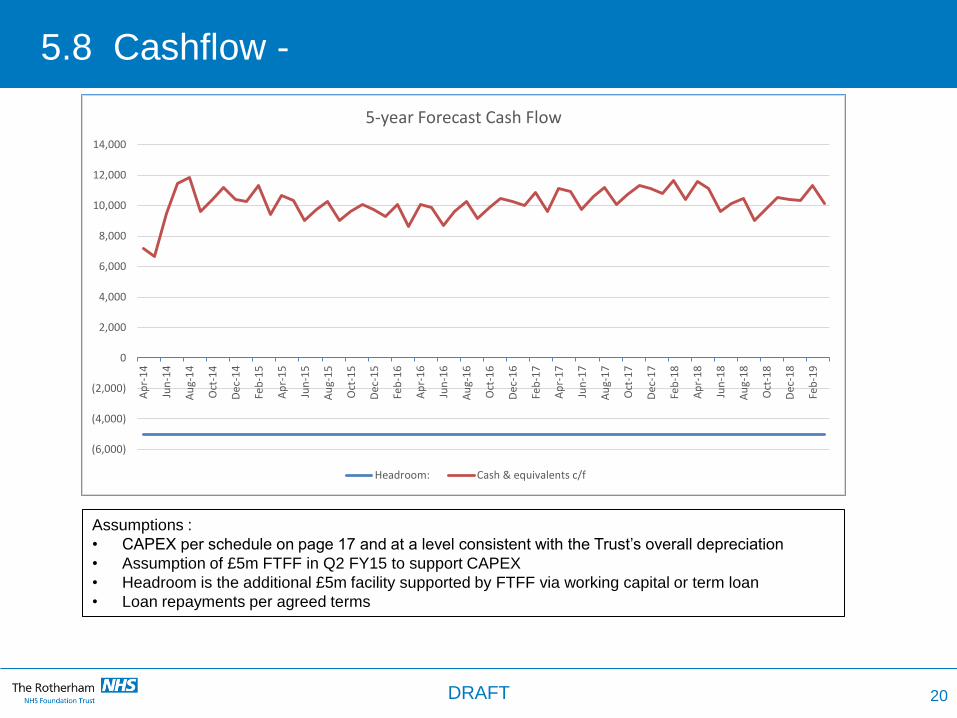

• The Trust has a reasonable cash position throughout the plan period. Whilst this does

include £5m FTFF which underpins the CAPEX position, the cash position is resilient and

commensurate with the surplus I&E position.

• The level of CAPEX provided allows for routine and backlog maintenance and this is

consistent with the level of depreciation in the I&E.

12 DRAFT

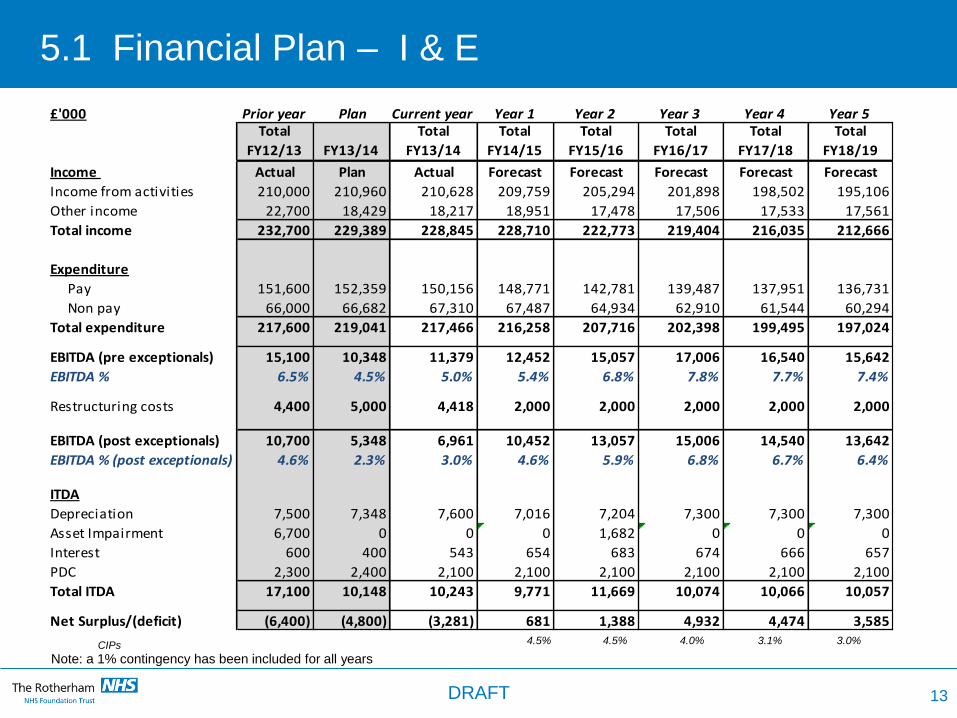

5.1 Financial Plan – I & E

CIPs 4.5% 4.5% 4.0% 3.1% 3.0%

13

£'000 Prior year Plan Current year Year 1 Year 2 Year 3 Year 4 Year 5Total

FY12/13 FY13/14

Total

FY13/14

Total

FY14/15

Total

FY15/16

Total

FY16/17

Total

FY17/18

Total

FY18/19

Income Actual Plan Actual Forecast Forecast Forecast Forecast Forecast

Income from activities 210,000 210,960 210,628 209,759 205,294 201,898 198,502 195,106

Other income 22,700 18,429 18,217 18,951 17,478 17,506 17,533 17,561

Total income 232,700 229,389 228,845 228,710 222,773 219,404 216,035 212,666

Expenditure

Pay 151,600 152,359 150,156 148,771 142,781 139,487 137,951 136,731

Non pay 66,000 66,682 67,310 67,487 64,934 62,910 61,544 60,294

Total expenditure 217,600 219,041 217,466 216,258 207,716 202,398 199,495 197,024

EBITDA (pre exceptionals) 15,100 10,348 11,379 12,452 15,057 17,006 16,540 15,642

EBITDA % 6.5% 4.5% 5.0% 5.4% 6.8% 7.8% 7.7% 7.4%

Restructuring costs 4,400 5,000 4,418 2,000 2,000 2,000 2,000 2,000

EBITDA (post exceptionals) 10,700 5,348 6,961 10,452 13,057 15,006 14,540 13,642

EBITDA % (post exceptionals) 4.6% 2.3% 3.0% 4.6% 5.9% 6.8% 6.7% 6.4%

ITDA

Depreciation 7,500 7,348 7,600 7,016 7,204 7,300 7,300 7,300

Asset Impairment 6,700 0 0 0 1,682 0 0 0

Interest 600 400 543 654 683 674 666 657

PDC 2,300 2,400 2,100 2,100 2,100 2,100 2,100 2,100

Total ITDA 17,100 10,148 10,243 9,771 11,669 10,074 10,066 10,057

Net Surplus/(deficit) (6,400) (4,800) (3,281) 681 1,388 4,932 4,474 3,585

Note: a 1% contingency has been included for all years

DRAFT

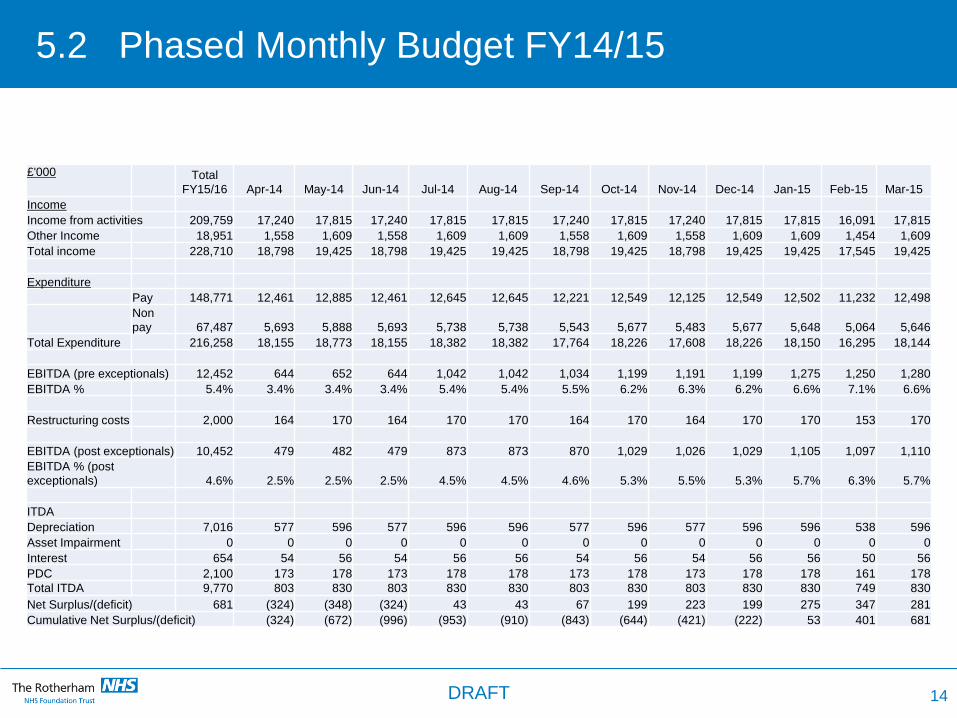

5.2 Phased Monthly Budget FY14/15

14

£'000 Total

FY15/16 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15

Income

Income from activities 209,759 17,240 17,815 17,240 17,815 17,815 17,240 17,815 17,240 17,815 17,815 16,091 17,815

Other Income 18,951 1,558 1,609 1,558 1,609 1,609 1,558 1,609 1,558 1,609 1,609 1,454 1,609

Total income 228,710 18,798 19,425 18,798 19,425 19,425 18,798 19,425 18,798 19,425 19,425 17,545 19,425

Expenditure

Pay 148,771 12,461 12,885 12,461 12,645 12,645 12,221 12,549 12,125 12,549 12,502 11,232 12,498

Non

pay 67,487 5,693 5,888 5,693 5,738 5,738 5,543 5,677 5,483 5,677 5,648 5,064 5,646

Total Expenditure 216,258 18,155 18,773 18,155 18,382 18,382 17,764 18,226 17,608 18,226 18,150 16,295 18,144

EBITDA (pre exceptionals) 12,452 644 652 644 1,042 1,042 1,034 1,199 1,191 1,199 1,275 1,250 1,280

EBITDA % 5.4% 3.4% 3.4% 3.4% 5.4% 5.4% 5.5% 6.2% 6.3% 6.2% 6.6% 7.1% 6.6%

Restructuring costs 2,000 164 170 164 170 170 164 170 164 170 170 153 170

EBITDA (post exceptionals) 10,452 479 482 479 873 873 870 1,029 1,026 1,029 1,105 1,097 1,110

EBITDA % (post

exceptionals) 4.6% 2.5% 2.5% 2.5% 4.5% 4.5% 4.6% 5.3% 5.5% 5.3% 5.7% 6.3% 5.7%

ITDA

Depreciation 7,016 577 596 577 596 596 577 596 577 596 596 538 596

Asset Impairment 0 0 0 0 0 0 0 0 0 0 0 0 0

Interest 654 54 56 54 56 56 54 56 54 56 56 50 56

PDC 2,100 173 178 173 178 178 173 178 173 178 178 161 178 Total ITDA 9,770 803 830 803 830 830 803 830 803 830 830 749 830

Net Surplus/(deficit) 681 (324) (348) (324) 43 43 67 199 223 199 275 347 281

Cumulative Net Surplus/(deficit) (324) (672) (996) (953) (910) (843) (644) (421) (222) 53 401 681

DRAFT

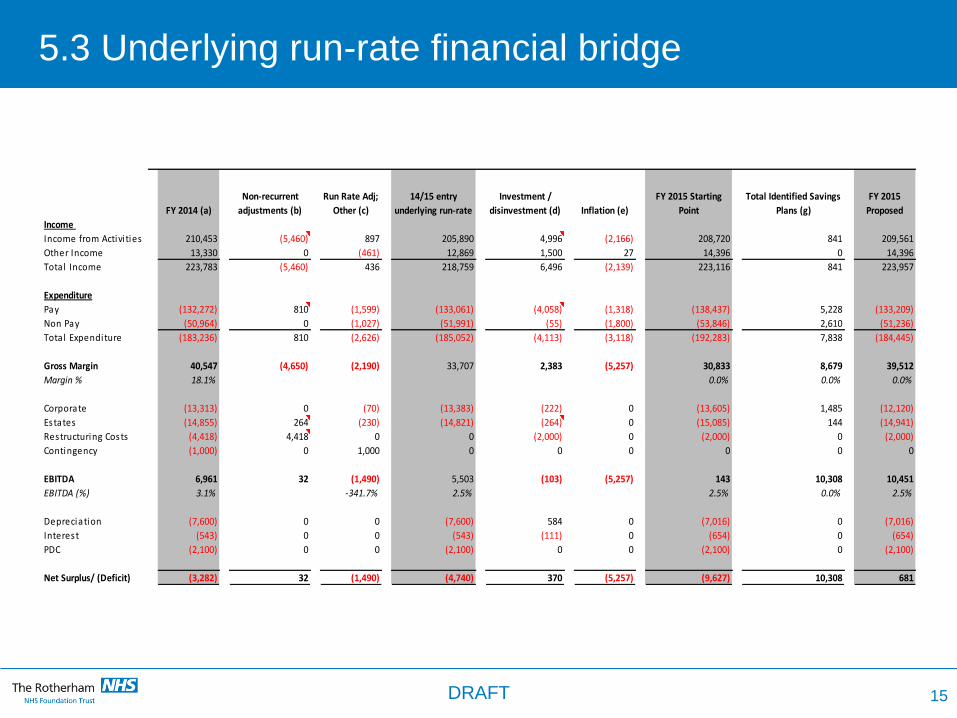

5.3 Underlying run-rate financial bridge

FY 2014 (a)

Non-recurrent

adjustments (b)

Run Rate Adj;

Other (c)

14/15 entry

underlying run-rate

Investment /

disinvestment (d) Inflation (e)

FY 2015 Starting

Point

Total Identified Savings

Plans (g)

FY 2015

Proposed

Income

Income from Activi ties 210,453 (5,460) 897 205,890 4,996 (2,166) 208,720 841 209,561

Other Income 13,330 0 (461) 12,869 1,500 27 14,396 0 14,396

Total Income 223,783 (5,460) 436 218,759 6,496 (2,139) 223,116 841 223,957

Expenditure

Pay (132,272) 810 (1,599) (133,061) (4,058) (1,318) (138,437) 5,228 (133,209)

Non Pay (50,964) 0 (1,027) (51,991) (55) (1,800) (53,846) 2,610 (51,236)

Total Expenditure (183,236) 810 (2,626) (185,052) (4,113) (3,118) (192,283) 7,838 (184,445)

Gross Margin 40,547 (4,650) (2,190) 33,707 2,383 (5,257) 30,833 8,679 39,512

Margin % 18.1% 0.0% 0.0% 0.0%

Corporate (13,313) 0 (70) (13,383) (222) 0 (13,605) 1,485 (12,120)

Estates (14,855) 264 (230) (14,821) (264) 0 (15,085) 144 (14,941)

Restructuring Costs (4,418) 4,418 0 0 (2,000) 0 (2,000) 0 (2,000)

Contingency (1,000) 0 1,000 0 0 0 0 0 0

EBITDA 6,961 32 (1,490) 5,503 (103) (5,257) 143 10,308 10,451

EBITDA (%) 3.1% -341.7% 2.5% 2.5% 0.0% 2.5%

Depreciation (7,600) 0 0 (7,600) 584 0 (7,016) 0 (7,016)

Interest (543) 0 0 (543) (111) 0 (654) 0 (654)

PDC (2,100) 0 0 (2,100) 0 0 (2,100) 0 (2,100)

Net Surplus/ (Deficit) (3,282) 32 (1,490) (4,740) 370 (5,257) (9,627) 10,308 681

15 DRAFT

(12,000)

(10,000)

(8,000)

(6,000)

(4,000)

(2,000)

-

2,000

(3,282)

(5,460) 5,492

(1,490) 370

(3,118) (9,627)

681

(4,740)

(2,139)

10,308

16

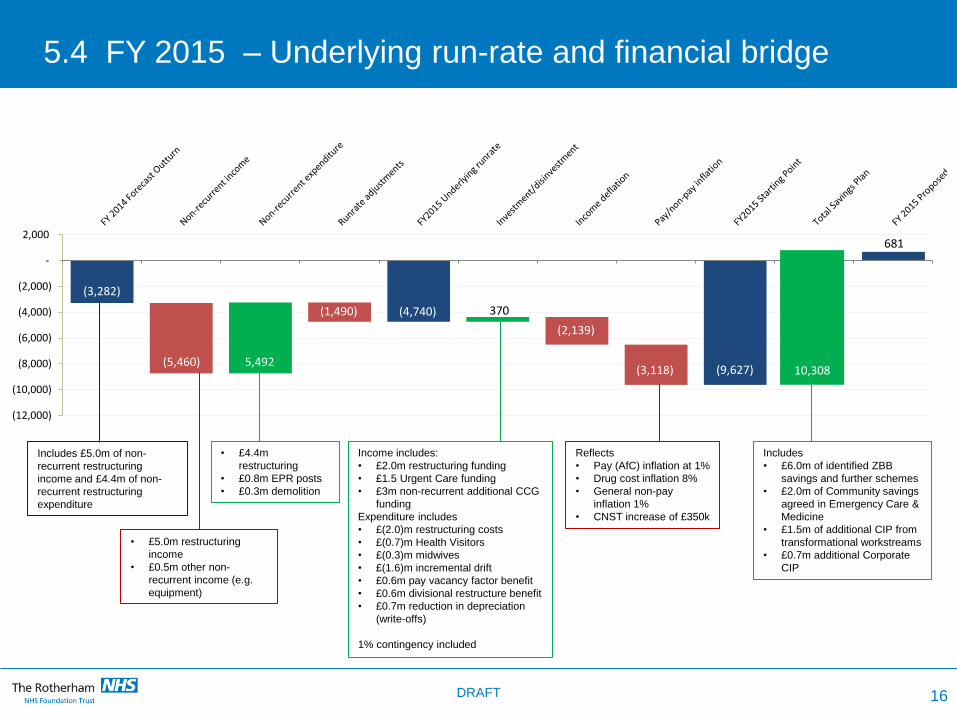

5.4 FY 2015 – Underlying run-rate and financial bridge

Includes £5.0m of non-

recurrent restructuring

income and £4.4m of non-

recurrent restructuring

expenditure

• £5.0m restructuring

income

• £0.5m other non-

recurrent income (e.g.

equipment)

• £4.4m

restructuring

• £0.8m EPR posts

• £0.3m demolition

Income includes:

• £2.0m restructuring funding

• £1.5 Urgent Care funding

• £3m non-recurrent additional CCG

funding

Expenditure includes

• £(2.0)m restructuring costs

• £(0.7)m Health Visitors

• £(0.3)m midwives

• £(1.6)m incremental drift

• £0.6m pay vacancy factor benefit

• £0.6m divisional restructure benefit

• £0.7m reduction in depreciation

(write-offs)

1% contingency included

Reflects

• Pay (AfC) inflation at 1%

• Drug cost inflation 8%

• General non-pay

inflation 1%

• CNST increase of £350k

Includes

• £6.0m of identified ZBB

savings and further schemes

• £2.0m of Community savings

agreed in Emergency Care &

Medicine

• £1.5m of additional CIP from

transformational workstreams

• £0.7m additional Corporate

CIP

DRAFT

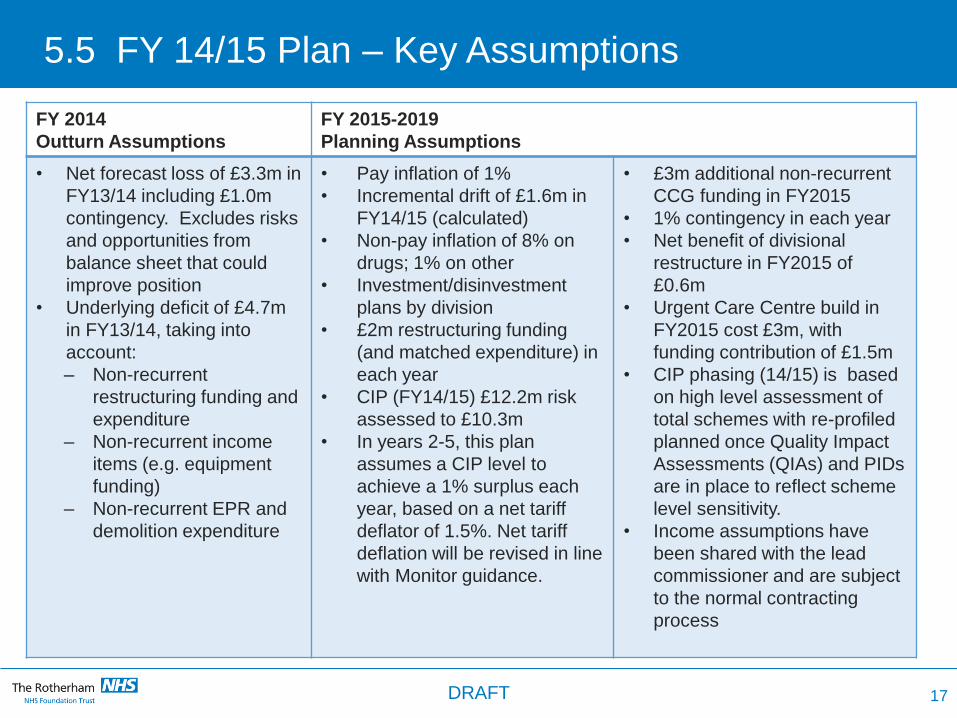

5.5 FY 14/15 Plan – Key Assumptions

FY 2014

Outturn Assumptions

FY 2015-2019

Planning Assumptions

• Net forecast loss of £3.3m in

FY13/14 including £1.0m

contingency. Excludes risks

and opportunities from

balance sheet that could

improve position

• Underlying deficit of £4.7m

in FY13/14, taking into

account:

– Non-recurrent

restructuring funding and

expenditure

– Non-recurrent income

items (e.g. equipment

funding)

– Non-recurrent EPR and

demolition expenditure

• Pay inflation of 1%

• Incremental drift of £1.6m in

FY14/15 (calculated)

• Non-pay inflation of 8% on

drugs; 1% on other

• Investment/disinvestment

plans by division

• £2m restructuring funding

(and matched expenditure) in

each year

• CIP (FY14/15) £12.2m risk

assessed to £10.3m

• In years 2-5, this plan

assumes a CIP level to

achieve a 1% surplus each

year, based on a net tariff

deflator of 1.5%. Net tariff

deflation will be revised in line

with Monitor guidance.

• £3m additional non-recurrent

CCG funding in FY2015

• 1% contingency in each year

• Net benefit of divisional

restructure in FY2015 of

£0.6m

• Urgent Care Centre build in

FY2015 cost £3m, with

funding contribution of £1.5m

• CIP phasing (14/15) is based

on high level assessment of

total schemes with re-profiled

planned once Quality Impact

Assessments (QIAs) and PIDs

are in place to reflect scheme

level sensitivity.

• Income assumptions have

been shared with the lead

commissioner and are subject

to the normal contracting

process

17 DRAFT

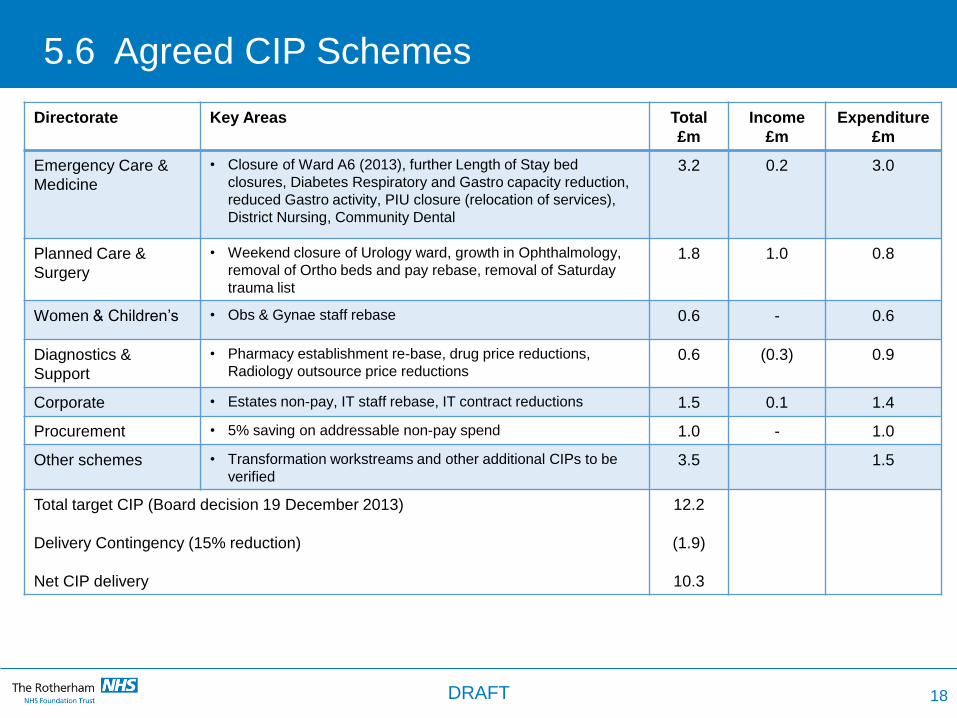

5.6 Agreed CIP Schemes

18

Directorate Key Areas Total

£m

Income

£m

Expenditure

£m

Emergency Care &

Medicine

• Closure of Ward A6 (2013), further Length of Stay bed

closures, Diabetes Respiratory and Gastro capacity reduction,

reduced Gastro activity, PIU closure (relocation of services),

District Nursing, Community Dental

3.2 0.2 3.0

Planned Care &

Surgery

• Weekend closure of Urology ward, growth in Ophthalmology,

removal of Ortho beds and pay rebase, removal of Saturday

trauma list

1.8 1.0 0.8

Women & Children’s • Obs & Gynae staff rebase 0.6 - 0.6

Diagnostics &

Support

• Pharmacy establishment re-base, drug price reductions,

Radiology outsource price reductions 0.6 (0.3) 0.9

Corporate • Estates non-pay, IT staff rebase, IT contract reductions 1.5 0.1 1.4

Procurement • 5% saving on addressable non-pay spend 1.0 - 1.0

Other schemes • Transformation workstreams and other additional CIPs to be

verified 3.5 1.5

Total target CIP (Board decision 19 December 2013)

Delivery Contingency (15% reduction)

Net CIP delivery

12.2

(1.9)

10.3

DRAFT

5.7 Monitor Continuity of Service Rating

1 2 3 4

1 1 2/2* 2/2* 3

2 2/2* 2/2* 3 3

3 2/2* 3 3 4

4 3 3 4 4

Liq

uid

ity

Capital Service Capacity1 Significant risk: contingency planning, formal enforcement

2 Material risk: monthly monitoring, investigation of breach

2* Quarterly monitoring

3 Provision of limited additional information

4 No action beyond normal monitoring

1

2

3

4

FY14Q3

FY14Q4

FY15Q1

FY15Q2

FY15Q3

FY15Q4

FY16Q1

FY16Q2

FY16Q3

FY16Q4

FY17Q1

FY17Q2

FY17Q3

FY17Q4

FY18Q1

FY18Q2

FY18Q3

FY18Q4

FY19Q1

FY19Q2

FY19Q3

FY19Q4

19 DRAFT

5.8 Cashflow -

(6,000)

(4,000)

(2,000)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000A

pr-

14

Jun

-14

Au

g-1

4

Oct

-14

Dec

-14

Feb

-15

Ap

r-1

5

Jun

-15

Au

g-1

5

Oct

-15

Dec

-15

Feb

-16

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

Dec

-16

Feb

-17

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

Dec

-17

Feb

-18

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

Dec

-18

Feb

-19

5-year Forecast Cash Flow

Headroom: Cash & equivalents c/f

20

Assumptions :

• CAPEX per schedule on page 17 and at a level consistent with the Trust’s overall depreciation

• Assumption of £5m FTFF in Q2 FY15 to support CAPEX

• Headroom is the additional £5m facility supported by FTFF via working capital or term loan

• Loan repayments per agreed terms

DRAFT

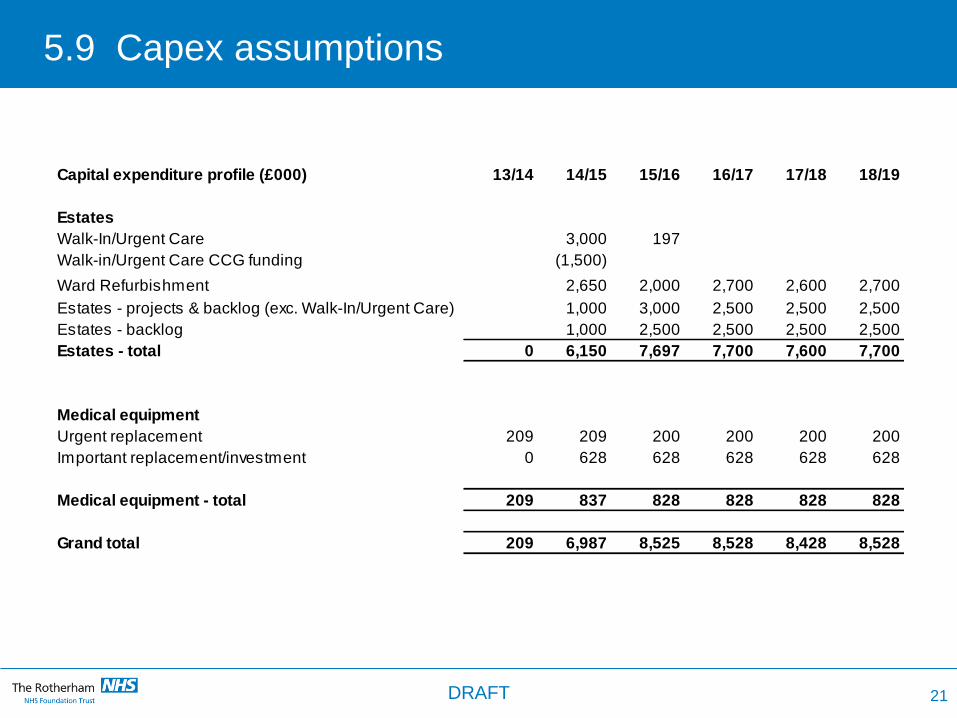

5.9 Capex assumptions

Capital expenditure profile (£000) 13/14 14/15 15/16 16/17 17/18 18/19

Estates

Walk-In/Urgent Care 3,000 197

Walk-in/Urgent Care CCG funding (1,500)

Ward Refurbishment 2,650 2,000 2,700 2,600 2,700

Estates - projects & backlog (exc. Walk-In/Urgent Care) 1,000 3,000 2,500 2,500 2,500

Estates - backlog 1,000 2,500 2,500 2,500 2,500

Estates - total 0 6,150 7,697 7,700 7,600 7,700

Medical equipment

Urgent replacement 209 209 200 200 200 200

Important replacement/investment 0 628 628 628 628 628

Medical equipment - total 209 837 828 828 828 828

Grand total 209 6,987 8,525 8,528 8,428 8,528

21 DRAFT

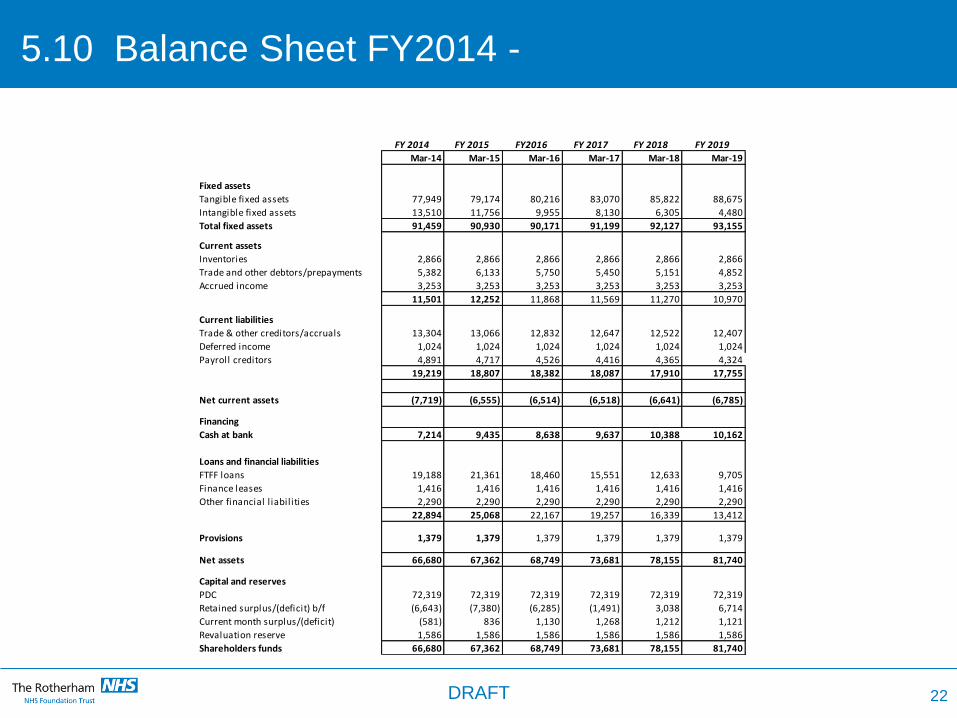

5.10 Balance Sheet FY2014 -

Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Mar-19

Fixed assets

Tangible fixed assets 77,949 79,174 80,216 83,070 85,822 88,675

Intangible fixed assets 13,510 11,756 9,955 8,130 6,305 4,480

Total fixed assets 91,459 90,930 90,171 91,199 92,127 93,155

Current assets

Inventories 2,866 2,866 2,866 2,866 2,866 2,866

Trade and other debtors/prepayments 5,382 6,133 5,750 5,450 5,151 4,852

Accrued income 3,253 3,253 3,253 3,253 3,253 3,253

11,501 12,252 11,868 11,569 11,270 10,970

Current liabilities

Trade & other creditors/accruals 13,304 13,066 12,832 12,647 12,522 12,407

Deferred income 1,024 1,024 1,024 1,024 1,024 1,024

Payroll creditors 4,891 4,717 4,526 4,416 4,365 4,324

19,219 18,807 18,382 18,087 17,910 17,755

Net current assets (7,719) (6,555) (6,514) (6,518) (6,641) (6,785)

Financing

Cash at bank 7,214 9,435 8,638 9,637 10,388 10,162

Loans and financial liabilities

FTFF loans 19,188 21,361 18,460 15,551 12,633 9,705

Finance leases 1,416 1,416 1,416 1,416 1,416 1,416

Other financial l iabilities 2,290 2,290 2,290 2,290 2,290 2,290

22,894 25,068 22,167 19,257 16,339 13,412

Provisions 1,379 1,379 1,379 1,379 1,379 1,379

Net assets 66,680 67,362 68,749 73,681 78,155 81,740

Capital and reserves

PDC 72,319 72,319 72,319 72,319 72,319 72,319

Retained surplus/(deficit) b/f (6,643) (7,380) (6,285) (1,491) 3,038 6,714

Current month surplus/(deficit) (581) 836 1,130 1,268 1,212 1,121

Revaluation reserve 1,586 1,586 1,586 1,586 1,586 1,586

Shareholders funds 66,680 67,362 68,749 73,681 78,155 81,740

FY 2019FY 2014 FY 2015 FY2016 FY 2017 FY 2018

22 DRAFT

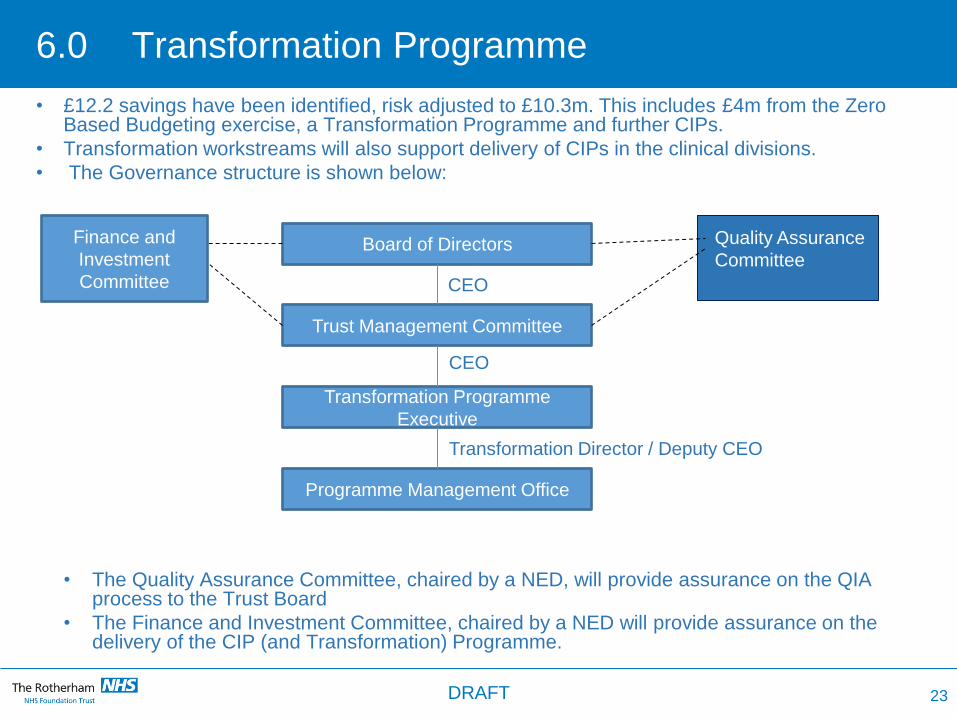

6.0 Transformation Programme

• £12.2 savings have been identified, risk adjusted to £10.3m. This includes £4m from the Zero Based Budgeting exercise, a Transformation Programme and further CIPs.

• Transformation workstreams will also support delivery of CIPs in the clinical divisions.

• The Governance structure is shown below:

• The Quality Assurance Committee, chaired by a NED, will provide assurance on the QIA process to the Trust Board

• The Finance and Investment Committee, chaired by a NED will provide assurance on the delivery of the CIP (and Transformation) Programme.

Board of Directors

Trust Management Committee

Transformation Programme

Executive

Programme Management Office

CEO

CEO

Transformation Director / Deputy CEO

23

Quality Assurance

Committee

Finance and

Investment

Committee

DRAFT

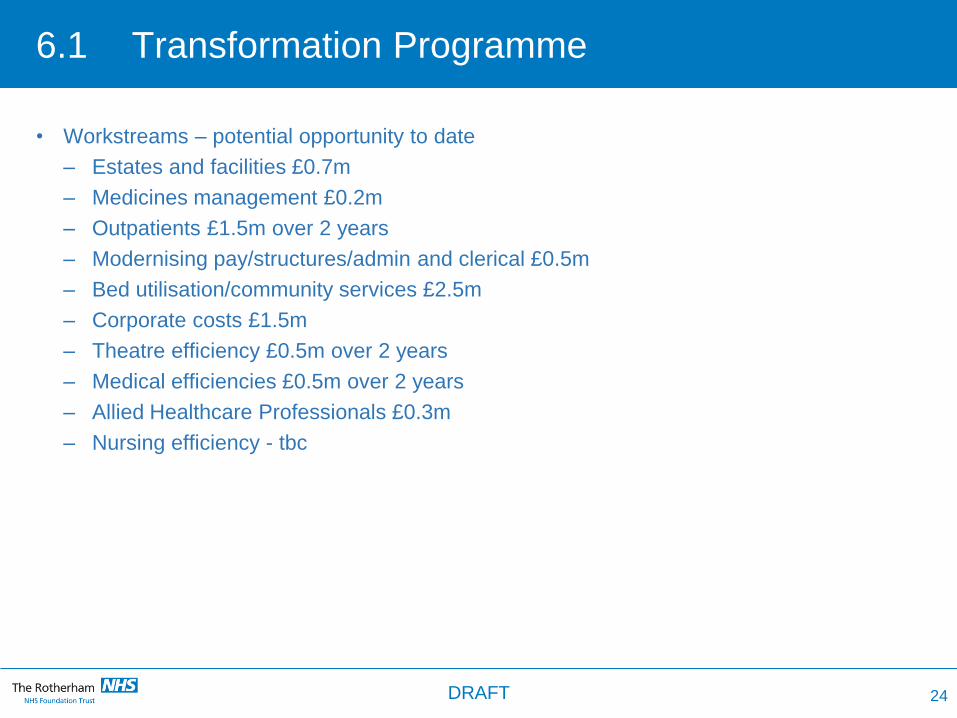

6.1 Transformation Programme

• Workstreams – potential opportunity to date

– Estates and facilities £0.7m

– Medicines management £0.2m

– Outpatients £1.5m over 2 years

– Modernising pay/structures/admin and clerical £0.5m

– Bed utilisation/community services £2.5m

– Corporate costs £1.5m

– Theatre efficiency £0.5m over 2 years

– Medical efficiencies £0.5m over 2 years

– Allied Healthcare Professionals £0.3m

– Nursing efficiency - tbc

24 DRAFT

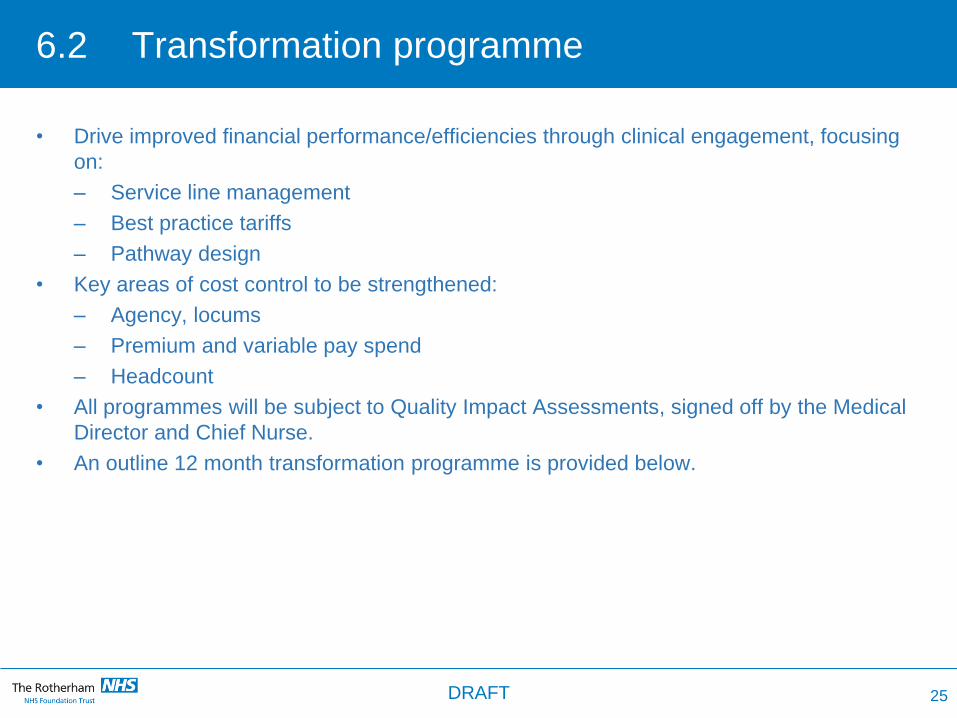

6.2 Transformation programme

• Drive improved financial performance/efficiencies through clinical engagement, focusing

on:

– Service line management

– Best practice tariffs

– Pathway design

• Key areas of cost control to be strengthened:

– Agency, locums

– Premium and variable pay spend

– Headcount

• All programmes will be subject to Quality Impact Assessments, signed off by the Medical

Director and Chief Nurse.

• An outline 12 month transformation programme is provided below.

25 DRAFT

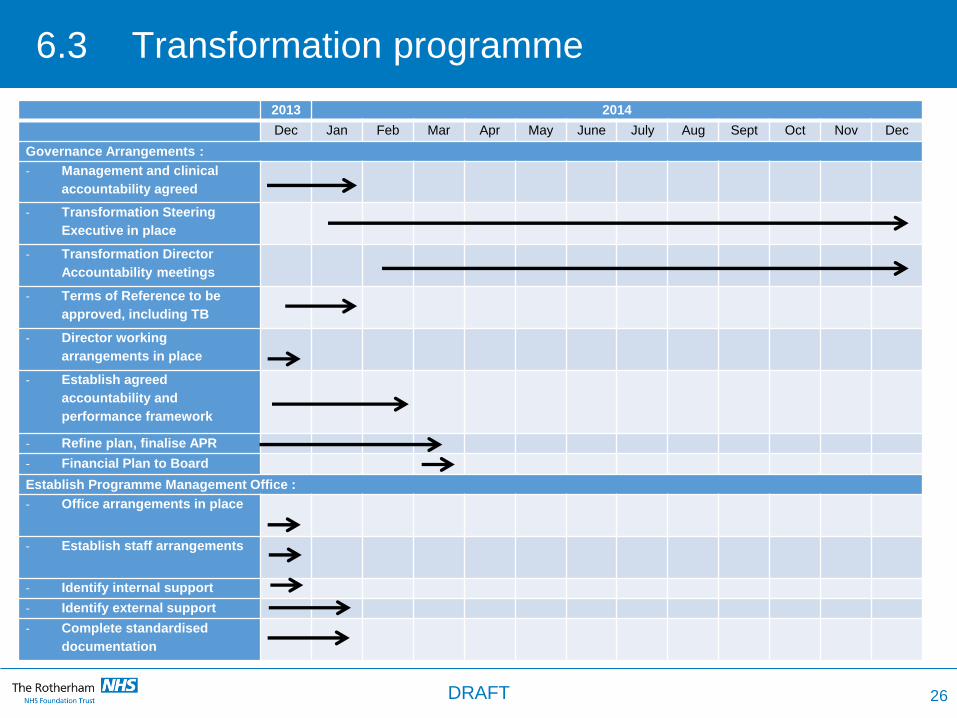

6.3 Transformation programme

26

2013 2014

Dec Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

Governance Arrangements :

- Management and clinical

accountability agreed

- Transformation Steering

Executive in place

- Transformation Director

Accountability meetings

- Terms of Reference to be

approved, including TB

- Director working

arrangements in place

- Establish agreed

accountability and

performance framework

- Refine plan, finalise APR

- Financial Plan to Board

Establish Programme Management Office :

- Office arrangements in place

- Establish staff arrangements

- Identify internal support

- Identify external support

- Complete standardised

documentation

DRAFT

6.4 Transformation programme

2013 2014

Dec Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

Workstreams :

- Confirm workstreams to be

adopted

- Confirm leadership and

accountability arrangements

for workstreams

- Agree targets and timescales

for all workstreams

- Complete programme

documentation for all

workstreams

Trust Cost Improvement Programme :

- Confirm and agree Divisional

CIP targets

- Quality assure all CIP

schemes

- Ensure project

documentation completed

for all current schemes

- Develop new Divisional CIPs

- Ensure robust quality impact

assessments for all CIPs and

on-going monitoring

- Monthly Divisional CIP

Performance meetings

27 DRAFT

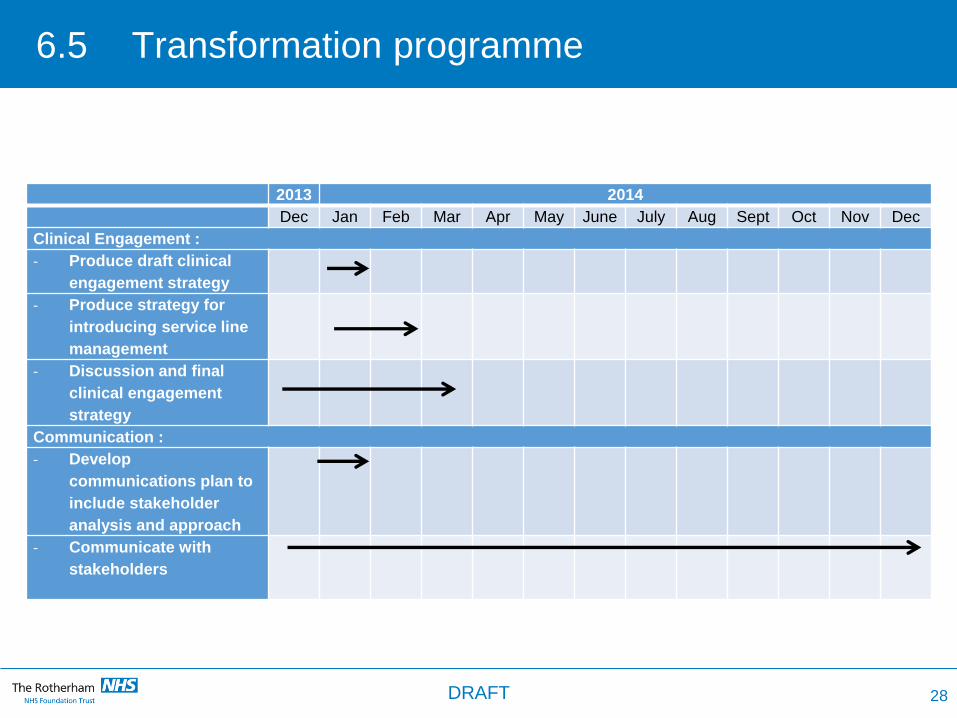

6.5 Transformation programme

2013 2014

Dec Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

Clinical Engagement :

- Produce draft clinical

engagement strategy

- Produce strategy for

introducing service line

management

- Discussion and final

clinical engagement

strategy

Communication :

- Develop

communications plan to

include stakeholder

analysis and approach

- Communicate with

stakeholders

28 DRAFT

7.0 Strategic Options

Options were identified and then explored to determine the strategic direction of the Trust.

The options considered were as follows:

• Option 1 – The Trust as a standalone entity - This option sought to assess the feasibility

of the Trust remaining in its current form, as a standalone entity, i.e. The Rotherham

NHS Foundation Trust, the implication of this option being that it did not consider formal

merger or acquisition by another organisation, but did include the potential for

collaboration with other healthcare organisations

• Option 2 – Vertical integration with a social care provider – This option considered

potential benefits and the feasibility of formally integrating with a social care

organisation. For clarity, this did not rule out the opportunity for closer working between

health and social care.

• Option 3 – Merger with another acute provider – This option explored the willingness of

potential partners to merge with the Trust.

Key issues for each of the options are summarised below.

29 DRAFT

7.1 Option 1

Option 1 – The Trust as a standalone entity

• Option 1 is dependent on achieving significant levels of CIP particularly in the first year

(FY14/15)

• The importance of driving improved internal efficiencies year on year is paramount

• The opportunity to properly integrate community and acute services is significant and must

be progressed

• There is overwhelming support from the lead commissioner to retain locally–run services

for the population of Rotherham, led and managed by TRFT

• The Trust’s cash position must be kept under close scrutiny and there must be rigorous

performance management frameworks in place.

• There is a significant number of potential opportunities that would be realised through

closer working and collaboration with other providers without recourse to merger. These

are discussed in more detail in section 9.

30 DRAFT

7.2 Option 22 Option 2

Option 2 - Vertical Integration with a social care provider

• There was no interest from potential social care partners to formally integrate with the

Trust

• The Trust has a poor track record in vertical integration, with an outstanding objective to

effectively integrate community services.

• Nevertheless it is still important to integrate further with social care through closer

working with Rotherham Metropolitan Borough Council and other social care providers

31 DRAFT

7.3 Option 3

Option 3 – Merger with another acute provider

• Neighbouring acute providers include:

- Sheffield Teaching Hospitals

- Sheffield Children’s Hospital

- Barnsley

- Doncaster and Bassetlaw

- Mid Yorks and Chesterfield - greater distance but still potential partners

• Clinical and patient benefits but would need to be confirmed through clinically-led

discussions

• Significant potential challenges, not commissioner preferred option

• Could provide efficiencies through back office and support function rationalisation

• Timescale for merger is a number of years – so option 1 still needed in addition to option 3

• Investment for investigating the options before any deal

32 DRAFT

8.0 Conclusion

The Board has agreed to pursue Option 1.

With a focused programme of transformation and efficiency the Trust is financially viable.

However, there are significant risks associated with this option and increasingly national

pressures such as 7 day working will create additional challenges for the Trust. As a result,

the Trust Board has decided to pursue this option of retaining the Trust in its present form

whilst also exploring potential opportunities for collaboration with other providers in the local

health economy. This is important to achieve further efficiencies and improve the quality of

services provided to patients.

Key risks and mitigating factors are summarised in section 10.0.

33 DRAFT

9.0 Potential Areas of Collaboration

• Working together (provider and commissioner workstreams)

• TRFT taking a more proactive role in both Commissioner-led and Provider-led

workstreams;

- commissioner-led : Cardiology & Stroke, Paediatrics & Neonates, Smaller

Specialities, Out of Hospital Care

- provider-led : Sharing Information, Consistency of Care, Smaller Specialities,

Specialised Services, Locums and Procurement

• Maternity services –

• Part of the Yorkshire clinical network for maternity and paediatric services led by

Leeds

• Explore collaborative links with neighbouring Trusts

• We recognise more work is required to take the service forward in a collaborative

way

• Forms of collaboration with other providers

- Clinical and non-clinical (e.g. including corporate functions)

- Clinical network models

- Hub and spoke arrangements

- Federated service model

- Alternative service provision/service line disinvestment

34 DRAFT

9.1 Potential Areas of Collaboration

• Undertake a joint review with the Lead Commissioner to:

– Assess and implement benefits of integration across the acute, community and

social care

– Identify potential quality improvements and cost efficiencies e.g. reducing hospital

length of stay

– Identify best practice models

– Include GPs, consultants and other healthcare professionals

– Include district nursing and its relationship with GP practices

– Specialist nursing across both community and acute sectors.

• Undertake a joint review with a specialist tertiary provider on the provision of specialised

and non-specialised paediatric services in Rotherham

– Clinically led, include reviewing models of care

– Commissioner supported - top priority (working together partnership)

35 DRAFT

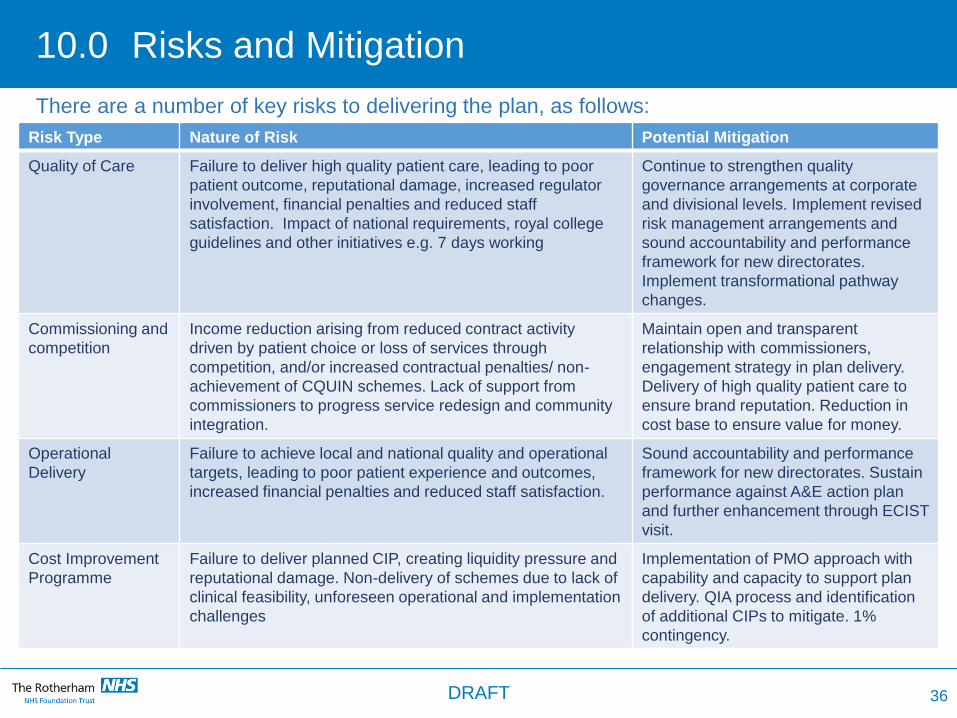

10.0 Risks and Mitigation

Risk Type Nature of Risk Potential Mitigation

Quality of Care Failure to deliver high quality patient care, leading to poor

patient outcome, reputational damage, increased regulator

involvement, financial penalties and reduced staff

satisfaction. Impact of national requirements, royal college

guidelines and other initiatives e.g. 7 days working

Continue to strengthen quality

governance arrangements at corporate

and divisional levels. Implement revised

risk management arrangements and

sound accountability and performance

framework for new directorates.

Implement transformational pathway

changes.

Commissioning and

competition

Income reduction arising from reduced contract activity

driven by patient choice or loss of services through

competition, and/or increased contractual penalties/ non-

achievement of CQUIN schemes. Lack of support from

commissioners to progress service redesign and community

integration.

Maintain open and transparent

relationship with commissioners,

engagement strategy in plan delivery.

Delivery of high quality patient care to

ensure brand reputation. Reduction in

cost base to ensure value for money.

Operational

Delivery

Failure to achieve local and national quality and operational

targets, leading to poor patient experience and outcomes,

increased financial penalties and reduced staff satisfaction.

Sound accountability and performance

framework for new directorates. Sustain

performance against A&E action plan

and further enhancement through ECIST

visit.

Cost Improvement

Programme

Failure to deliver planned CIP, creating liquidity pressure and

reputational damage. Non-delivery of schemes due to lack of

clinical feasibility, unforeseen operational and implementation

challenges

Implementation of PMO approach with

capability and capacity to support plan

delivery. QIA process and identification

of additional CIPs to mitigate. 1%

contingency.

36

There are a number of key risks to delivering the plan, as follows:

DRAFT

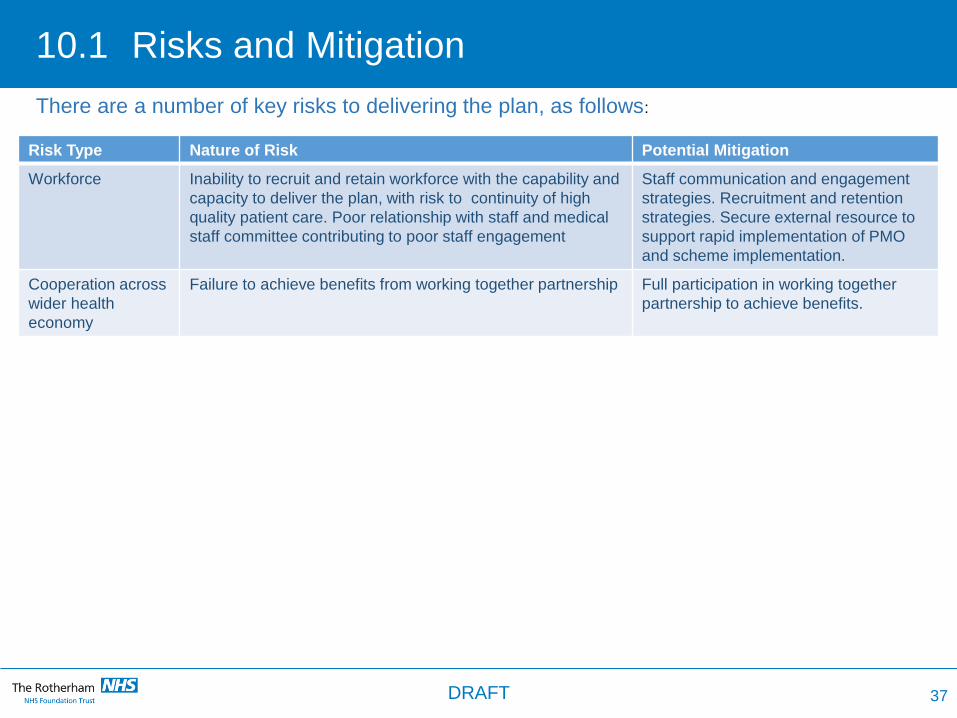

10.1 Risks and Mitigation

Risk Type Nature of Risk Potential Mitigation

Workforce Inability to recruit and retain workforce with the capability and

capacity to deliver the plan, with risk to continuity of high

quality patient care. Poor relationship with staff and medical

staff committee contributing to poor staff engagement

Staff communication and engagement

strategies. Recruitment and retention

strategies. Secure external resource to

support rapid implementation of PMO

and scheme implementation.

Cooperation across

wider health

economy

Failure to achieve benefits from working together partnership Full participation in working together

partnership to achieve benefits.

37

There are a number of key risks to delivering the plan, as follows:

DRAFT

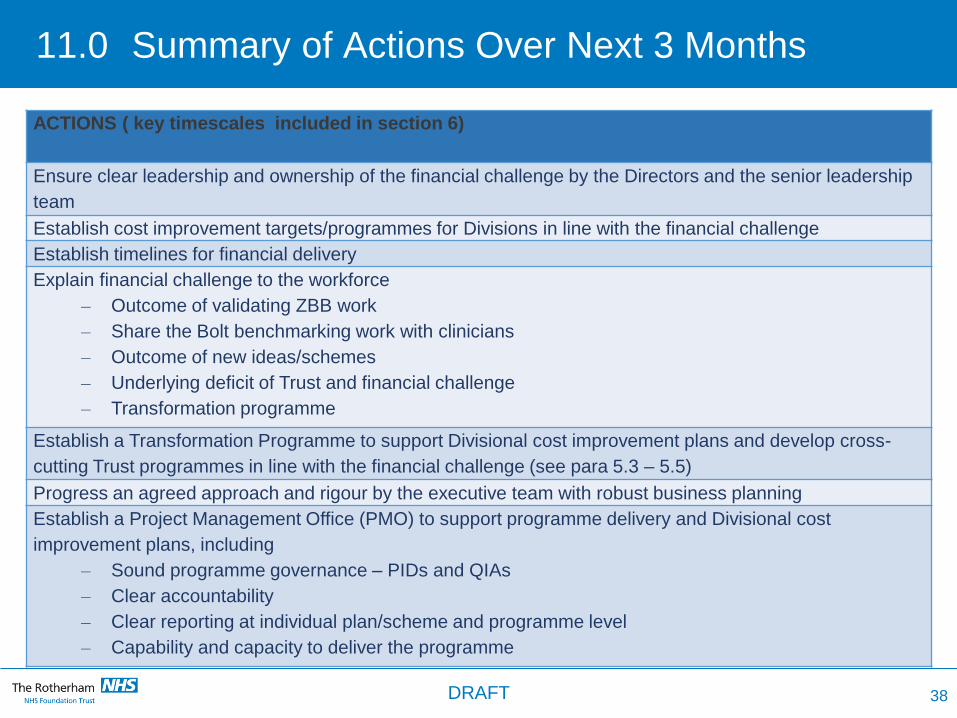

11.0 Summary of Actions Over Next 3 Months

38

ACTIONS ( key timescales included in section 6)

Ensure clear leadership and ownership of the financial challenge by the Directors and the senior leadership

team

Establish cost improvement targets/programmes for Divisions in line with the financial challenge

Establish timelines for financial delivery

Explain financial challenge to the workforce

– Outcome of validating ZBB work

– Share the Bolt benchmarking work with clinicians

– Outcome of new ideas/schemes

– Underlying deficit of Trust and financial challenge

– Transformation programme

Establish a Transformation Programme to support Divisional cost improvement plans and develop cross-

cutting Trust programmes in line with the financial challenge (see para 5.3 – 5.5)

Progress an agreed approach and rigour by the executive team with robust business planning

Establish a Project Management Office (PMO) to support programme delivery and Divisional cost

improvement plans, including

– Sound programme governance – PIDs and QIAs

– Clear accountability

– Clear reporting at individual plan/scheme and programme level

– Capability and capacity to deliver the programme

DRAFT

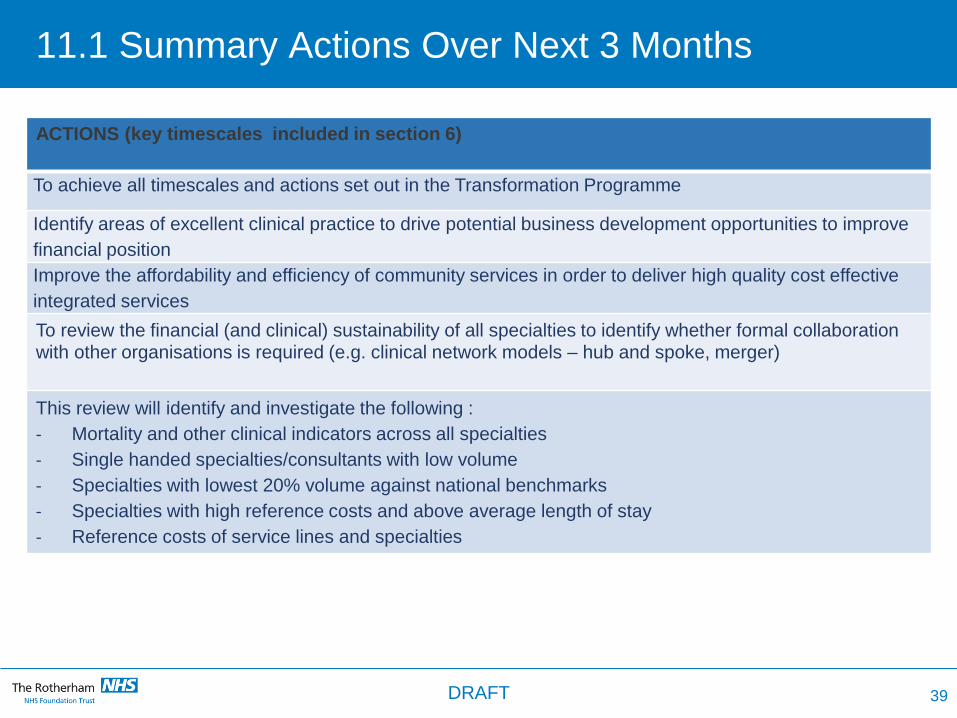

11.1 Summary Actions Over Next 3 Months

ACTIONS (key timescales included in section 6)

To achieve all timescales and actions set out in the Transformation Programme

Identify areas of excellent clinical practice to drive potential business development opportunities to improve

financial position

Improve the affordability and efficiency of community services in order to deliver high quality cost effective

integrated services

To review the financial (and clinical) sustainability of all specialties to identify whether formal collaboration with other organisations is required (e.g. clinical network models – hub and spoke, merger)

This review will identify and investigate the following :

- Mortality and other clinical indicators across all specialties

- Single handed specialties/consultants with low volume

- Specialties with lowest 20% volume against national benchmarks

- Specialties with high reference costs and above average length of stay

- Reference costs of service lines and specialties

39 DRAFT

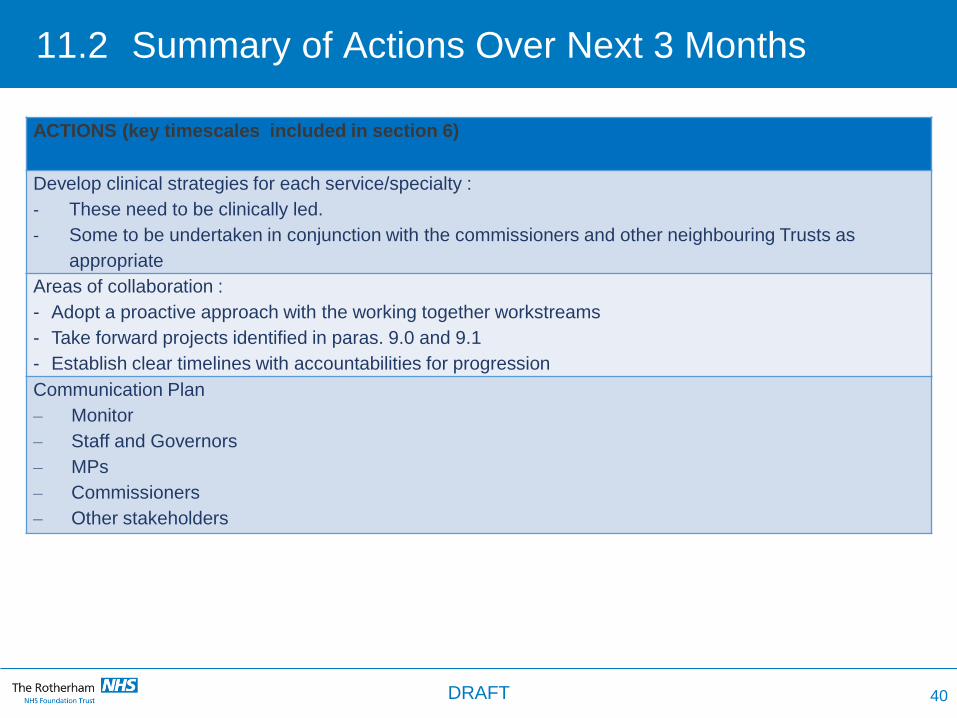

11.2 Summary of Actions Over Next 3 Months

ACTIONS (key timescales included in section 6)

Develop clinical strategies for each service/specialty :

- These need to be clinically led.

- Some to be undertaken in conjunction with the commissioners and other neighbouring Trusts as

appropriate

Areas of collaboration :

- Adopt a proactive approach with the working together workstreams

- Take forward projects identified in paras. 9.0 and 9.1

- Establish clear timelines with accountabilities for progression

Communication Plan

– Monitor

– Staff and Governors

– MPs

– Commissioners

– Other stakeholders

40 DRAFT