The Impact of Payroll Taxes on Informality. The Case of

the 2012 Colombian Tax Reform.

Cristina FernándezLeonardo Villar

Why this might be of interest to SSA and particularly to South

Africa?• Useful for South Africa in the discussion of increasing

its payroll taxes.

• Useful for other countries in Africa that show high payroll taxes as the Cote d’Ivoire, Sudan and Tanzania

• Methodology itself useful in analyzing the impact of labour policies and particularly (but not only) for those countries that do not household panel data.

Colombian Reform Characteristics.• Reduced payroll taxes from

29.5% to 16% of wages.

• It only affects contributionsmade by employers andnot contributions made byworkers.

• The fiscal source of thecontributions was replacedby a profit tax under theassumption that it is betterto tax the capital thanwork.

3% 4%

11%14% 14% 16% 16% 16% 17%

19% 19% 19% 19% 20%21%

25%

29% 29%32%

40%

Hond

uras

Chile

Peru

Ecua

dor

Gua

tem

ala

Uru

guay

Wor

ldLA

CEl

Sal

vado

rCo

lom

bia

Dom

inic

an R

.Pa

ragu

ayBo

livia

Pana

ma

Nic

arag

uaM

exic

o*Co

lom

bia

2013

Arge

ntin

aCo

sta

Rica

Braz

il*

Contributions payable by the employer

Reform characteristics.

Despite this reduction, payroll taxes remainrelatively high at international level.

Source: World Bank * Before the Reform

0.05.0

10.015.020.025.030.035.040.045.0

Braz

ilCo

sta

Rica

Arge

ntin

aCo

lom

bia*

Mex

ico

Cote

d'Iv

oire

Pana

ma

Suda

nBo

livia

Para

guay

Dom

inic

an R

.Co

lom

bia

Cam

eroo

nEl

Sal

vado

rTa

nzan

iaW

orld

Uru

guay SSA

Ghan

aGu

atem

ala

LAC

Ecua

dor

Cong

o D.

R.

Nig

eria

Uga

nda

Peru

Zam

bia

Trin

idad

and

T.

Ethi

opia

Sout

h Af

rica

Chile

Keny

a

Labor tax and contributions (% of profit)

3 HINTS ON THE IMPACT OF THE REFORM

Hint 1: Informality Declined.

Source: Dane GEIH – ECH 13 main metropolitan areas

40%

45%

50%

55%

60%

65%

2000

2002

2004

2006

2008

2010

2012

2014

Informality ratesDifferent measurements.

Firm (newdefinition)

Healthcontributions

Pensioncontributions

Health & pensioncontributions 4.0

4.24.44.64.85.05.25.45.65.86.0

Jan-

09Se

p-09

May

-10

Jan-

11Se

p-11

May

-12

Jan-

13Se

p-13

May

-14

Jan-

15Se

p-15

Mill

ions

of j

obs

Formal and informal workers.

Formal

Informal

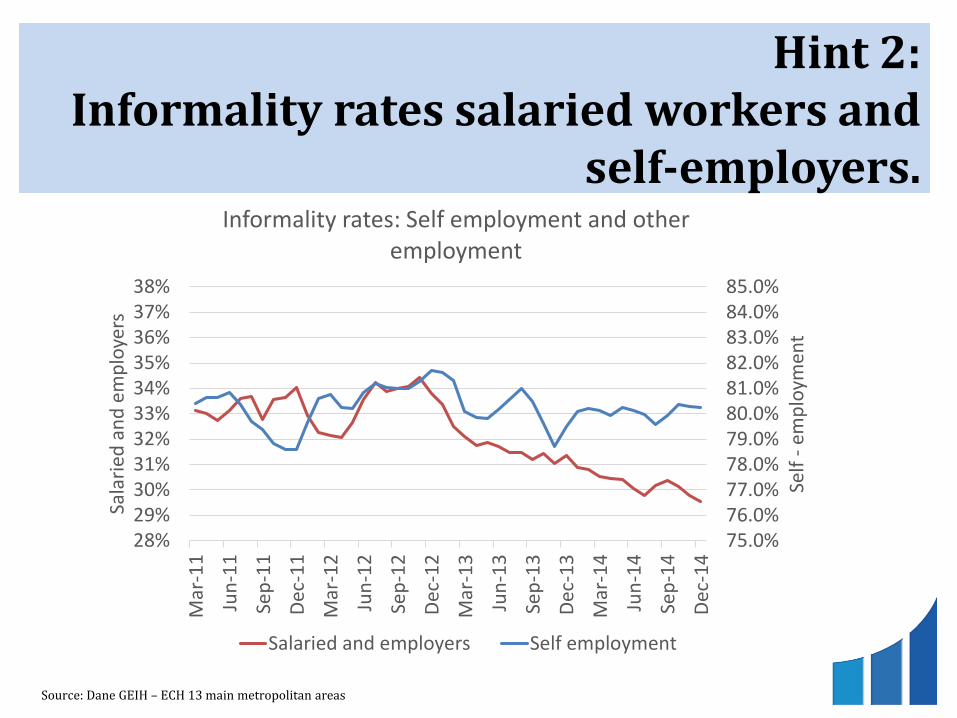

Hint 2: Informality rates salaried workers and

self-employers.

75.0%76.0%77.0%78.0%79.0%80.0%81.0%82.0%83.0%84.0%85.0%

28%29%30%31%32%33%34%35%36%37%38%

Mar

-11

Jun-

11

Sep-

11

Dec-

11

Mar

-12

Jun-

12

Sep-

12

Dec-

12

Mar

-13

Jun-

13

Sep-

13

Dec-

13

Mar

-14

Jun-

14

Sep-

14

Dec-

14

Self

-em

ploy

men

t

Sala

ried

and

empl

oyer

s

Informality rates: Self employment and other employment

Salaried and employers Self employment

Source: Dane GEIH – ECH 13 main metropolitan areas

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

40%

42%

44%

46%

48%

50%

52%

54%

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Brec

ha d

el p

rodu

cto

Tasa

de

form

alid

adFo

rmal

ity R

ate

Out

put g

ap

Hint 3: Relationship informality - growth

Source: GEIH y Fedesarrollo

--- Formality Rate (OIT, 10). Informality Rate (OIT, 5).Output Gap

Correlations

(2002-2013)

(2002-2015)

0.74** 0.46*

Formality in Colombia is pro-cyclical, except in the most recent period

METHODOLOGY

Objetive: How much of the reduction in informality was due to the reform

To isolate the impact of other variables affecting informality as:• Growth• A general tax increase, including the creation of the

profit tax• Increases in the state payroll (the share fell 3.9% to

3.7% ). • The increase in the minimum wage (adjusted by

productivity) which increased in 1.8 p.p. per year. (increases informality)

Differences in Differences.

• It compares the change in the probability of being informally within the control group with the change in the probability of being informal in the treated group.

• Nets factors that simultaneously affects both groups such as growth.Before After

Treatmenteffect

Control cms Treatment cms

Baseline 100 90

Followup

120140

Differences 20 50

Differences in Differences 30

Differences in Differences.

In the case of the Colombian Reform.

• Treatment group (beneficiaries)– Earn between 1 and 10 salaries.– Do not work at universities / NGOs.– More than two workers

• Control group (neutral)– Earn less than the minimum wage or more than 10

minimum wages.– University workers / NGOs.– Self employment (alternatively excluded)

Government and no reported income - excluded

Graphic Analysis.

• Analysis period:– 2012

(before the reform)

– 2014 (after the reform).

• Long moving averages (volatility).

y = -0.000017x + 0.944726

y = -0.000021x + 1.650880

70%

72%

74%

76%

78%

80%

18.0%

20.0%

22.0%

24.0%

26.0%

28.0%

Mar

-09

Aug-

09Ja

n-10

Jun-

10N

ov-1

0Ap

r-11

Sep-

11Fe

b-12

Jul-1

2De

c-12

May

-13

Oct

-13

Mar

-14

Aug-

14Ja

n-15

Jun-

15N

ov-1

5

Cont

rol g

roup

Trea

ted

grou

p

Informality rates (13 metropolitan areas - 3 month MA)

Treated informality rate No treated informality rate

!stw

aive

r

2nd

wai

ver

Appr

oval

Implementation of the econometric exercise.

If you don’t have a panel, create a panel, the model conducting this procedure is called differences in differences with matching

developed by Heckman et al (1997).

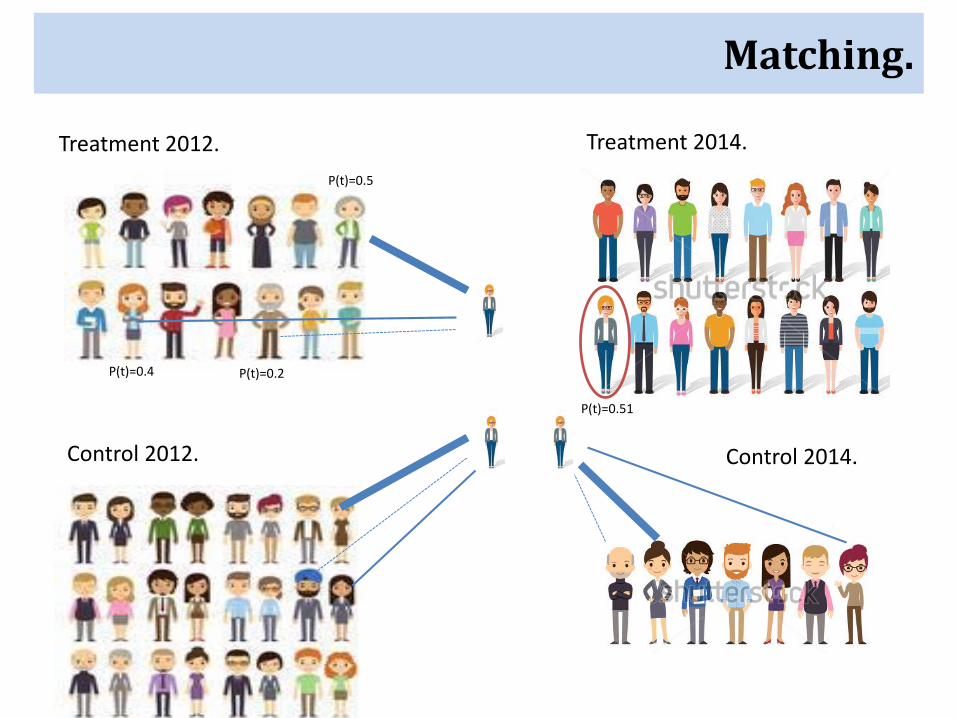

Matching.

P(t)=0.5

P(t)=0.4 P(t)=0.2

Treatment 2012. Treatment 2014.

Control 2014.

P(t)=0.51

Control 2012.

Matching.Treatment 2012. Treatment 2014.

Control 2012. Control 2012.

RESULTS

Control Informality Treatment Informality

Baseline(2012) 76% 28%

Follow Up(2014)

75% 23%

Differences -1% -5%

Differences in Differences -4.3%

% treated 38%

Impact of informality rate -1.6%

Differences in Differences (13 areas).Including self-employment in the control group

Control Informality Treatment Informality

Baseline(2012) 61% 28%

Follow Up(2014)

62% 23%

Differences 1% -5%

Differences in Differences -6.8%

% treated 38%

Impact of informality rate -2.6%

Differences in Differences (13 areas).Excluding self-employment in the control group

Robustness Tests.

• Common Support (similar range of p-scores)

• Quality of Matching (Rubin’s criteria hold)

• Placebo Test (2009-2012: no significant)

Results of past exercises.

• Anton (2014), the recent reform reduced the rate of informality between 2.9 p.p. and 3.4 p.p. Theoretical model.

• Kugler and Kugler (2009), an increase of 10 % in payroll taxes reduces formal employment between 4% and 5 %.

• Mondragón et al (2010), a 10% increase in payroll contributions increases the probability of being informal between 5 % and 8%.

• More recent work on the impact of recent reforms show that the number of formal workers increased between 3.1 and 3.4 p.p. (IDB) and 1 p.p 2014 , 2 p.p. for 2016 and 5.6 p.p. 2018 (Central Bank-preliminar) .

DISTRIBUTION EFFECT

Informality rate by income quintiles.They benefit more those who receive similar income to a minimum because a restriction carving more at this point where wages are not flexible downward shifted.

MDID by economic sector.Including self-employment

• Students with high-school education or less were most favored by the reform.

Baseline (2012) Follow Up (2014)DID

Control Treatment Control Treatment

Low Educated(Primary or less)

92% 49% 92% 39% -10.4%

High school 56% 25% 66% 22% -13%

Tertiary education or

higher56% 14% 54% 11% -1.2% (n.s.)

Male 25-45 years

75% 26% 75% 21% -5%

Source: Own calculations, based on GEIH 2007-2015 *Male 25 – 45 years * Not significant. All the other results aresignificant 99%.

Conclusions.

• The 13.5 points reduction in payroll taxes decreased the informality rate in Colombia in between 4.3 and 6.8 p.p. that impacted the informality rate in between 1.6 and 2.6 points.

• Men in productive years with low levels of education (high school or less) were most favored by the reform.