The Advanced Biofuel and

Biochemical Overview June 2012

Silicon Valley Bank Cleantech Practice

Table of Contents

I. Introduction

I. Biofuel/Biochemicals Outlook – Macro Observations 3

II. Biofuel/Biochemicals Outlook – Micro Observations 4

III. The Cleantech Ecosystem 5

IV. Market Snapshot: Global Ethanol Production 6

V. Market Snapshot: Global Biodiesel Production 7

VI. Market Snapshot: Ethanol and Biodiesel Production Landscape in the U.S.

8

VII. Market Snapshot: Global Biochemical Production 9

II. Biofuels/Biochemicals Overview

I. What are Biofuels/Biochemicals? 11

II. Types of Biofuels 15

III. Biofuel Feedstocks 16

IV. Comparative Yields 18

V. Petroleum Replacement Overview 21

VI. Conversion Technologies 22

III. The Importance of Biofuels/Biochemicals

I. Compelling Market Opportunity 28

II. Drivers of Biofuels/Biochemicals Growth 29

III. Liquid Demand Statistics 32

IV. Energy Market Growth 34

The Biofuels and Biochem Industry 2

III. The Importance of Biofuels/Biochemicals (Cont.)

V. Liquid Demand Growth from Non-OECD Countries 36

VI. Biofuels for Transportation 38

VII. Increasing Marginal Cost of Production 39

VIII. Oil Market Price and Saudi Breakeven Threshold 42

IX. U.S. Renewable Fuel Standards 43

X. Biofuel Blending Mandates by Country 46

XI. Cellulosic Ethanol Pricing Model 47

IV. Biofuel/Biochemicals Landscape

I. Advanced Biofuel and Biochemicals Value Chain 49

V. Where Are They in Development?

I. Investments in Biofuels/Biochemicals 52

II. Global Players – Milestone Update 54

III. Biofuel/Biochemical IPOs in Pipeline 56

IV. Strategic Partnerships 57

V. Projects to Watch in 2012–2013 58

VI. Appendix 61

VII. Selected Due Diligence Questions 69

VIII. Silicon Valley Bank Cleantech Team 70

Biofuel/Biochemicals Outlook – Macro Observations

• Multiple very large and growing markets

— Total markets will top $1+ trillion. Beyond the well-known fossil-fuel replacement markets is growing demand for non-fuel products like

food supplements, personal care products, and packaging.

• Positive supply/demand dynamics around crude

— The fundamental underlying demand is exacerbated by oil exporting countries’ economic reliance on oil revenue. Meanwhile, the cost of

crude production continues to increase. Biofuels/biochemicals will play an increasingly important role to fill that need.

• Demand drivers – mandates and markets

— Mandate: Primarily for fuels, government mandated goals proliferate with varying degrees of adherence and enforcement. Subsidies of

all types remain important in attracting capital and shifts in policy could alter business plan direction between fuels or chemicals.

— Markets: Growing economic justifications are intersecting with other market demand factors. For example, the U..S Navy’s goal of 50%

energy consumption from alternative sources by 2020 or the Air Force’s initiative to acquire 50% of aviation fuel from alternative blends

by 2016 are policy influencers that also have purchasing power.

• The role of strategic corporate investors

— Always important, corporates from a variety of industries (and led by big energy, chemicals/materials, and consumer products) have

become critical parties in the development and scale-up of the sector. Taking multiple forms of straight investment, joint venture, and

collaboration, investors search for innovation, growth, and information.

• Commodity markets

— Fuels in particular are ultimately commodities. Without policy enhancements, the impact of commodity cycles will continue to challenge

scaling of new technologies.

• Business life cycle

— While the underlying trends and fundamentals may be inexorable, development of the industry and market dynamics is a very long term

process and investment cycle.

OBSERVATIONS

The Biofuels and Biochem Industry 3 TABLE OF CONTENTS

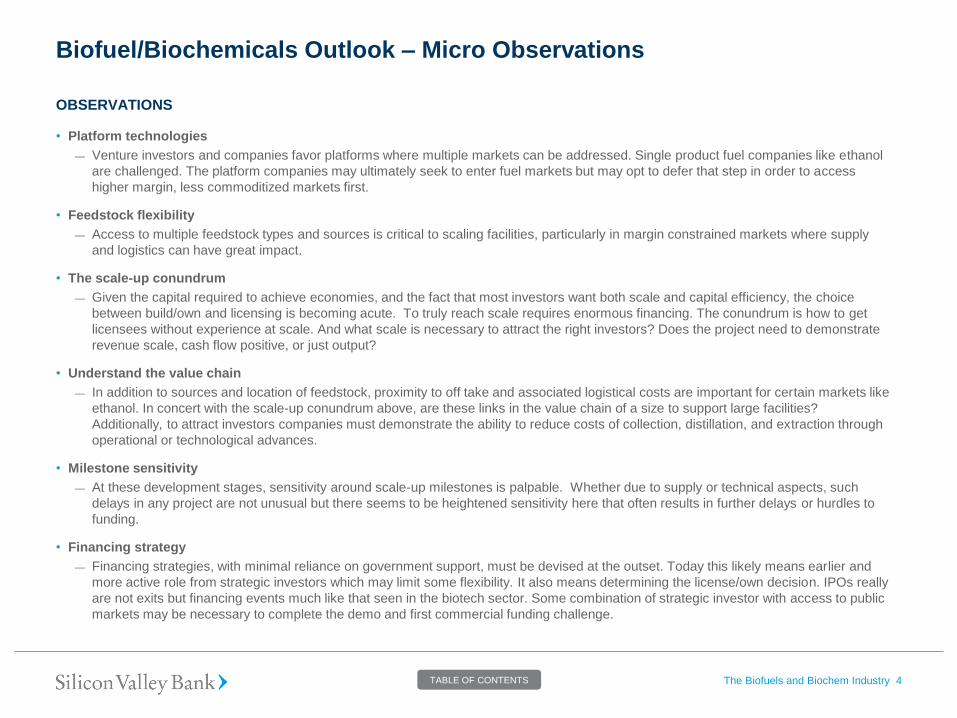

Biofuel/Biochemicals Outlook – Micro Observations

• Platform technologies

— Venture investors and companies favor platforms where multiple markets can be addressed. Single product fuel companies like ethanol

are challenged. The platform companies may ultimately seek to enter fuel markets but may opt to defer that step in order to access

higher margin, less commoditized markets first.

• Feedstock flexibility

— Access to multiple feedstock types and sources is critical to scaling facilities, particularly in margin constrained markets where supply

and logistics can have great impact.

• The scale-up conundrum

— Given the capital required to achieve economies, and the fact that most investors want both scale and capital efficiency, the choice

between build/own and licensing is becoming acute. To truly reach scale requires enormous financing. The conundrum is how to get

licensees without experience at scale. And what scale is necessary to attract the right investors? Does the project need to demonstrate

revenue scale, cash flow positive, or just output?

• Understand the value chain

— In addition to sources and location of feedstock, proximity to off take and associated logistical costs are important for certain markets like

ethanol. In concert with the scale-up conundrum above, are these links in the value chain of a size to support large facilities?

Additionally, to attract investors companies must demonstrate the ability to reduce costs of collection, distillation, and extraction through

operational or technological advances.

• Milestone sensitivity

— At these development stages, sensitivity around scale-up milestones is palpable. Whether due to supply or technical aspects, such

delays in any project are not unusual but there seems to be heightened sensitivity here that often results in further delays or hurdles to

funding.

• Financing strategy

— Financing strategies, with minimal reliance on government support, must be devised at the outset. Today this likely means earlier and

more active role from strategic investors which may limit some flexibility. It also means determining the license/own decision. IPOs really

are not exits but financing events much like that seen in the biotech sector. Some combination of strategic investor with access to public

markets may be necessary to complete the demo and first commercial funding challenge.

OBSERVATIONS

The Biofuels and Biochem Industry 4 TABLE OF CONTENTS

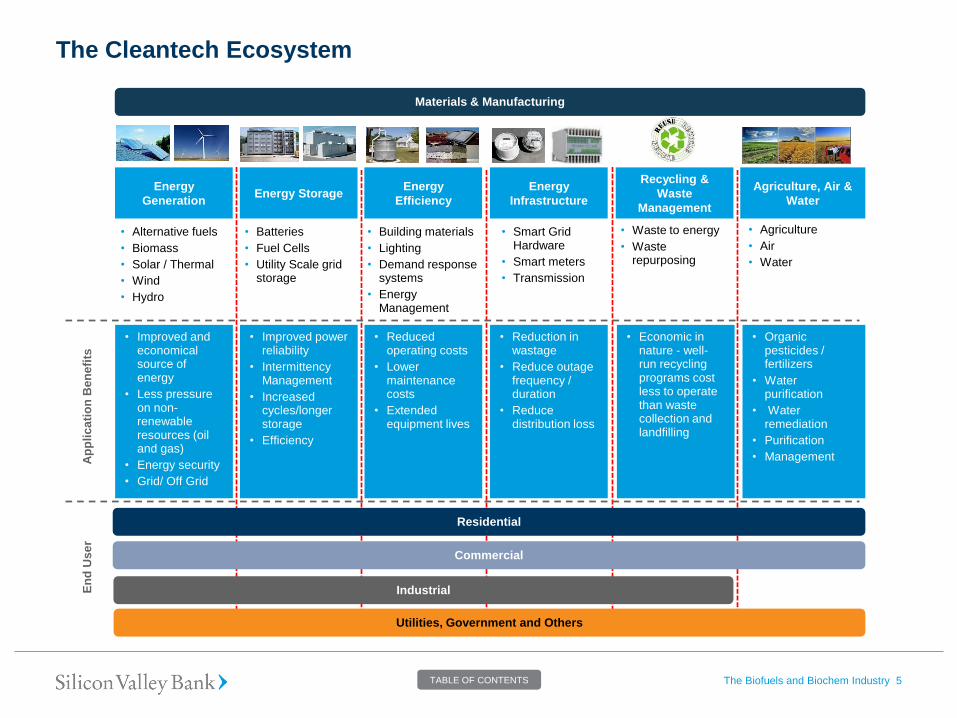

The Cleantech Ecosystem

The Biofuels and Biochem Industry 5

Ap

pli

ca

tio

n B

en

efi

ts

Commercial

Industrial

Utilities, Government and Others

• Batteries

• Fuel Cells

• Utility Scale grid storage

Materials and Manufacturing E

nd

Use

r

• Building materials

• Lighting

• Demand response systems

• Energy Management

• Smart Grid Hardware

• Smart meters

• Transmission

• Agriculture

• Air

• Water

• Improved and economical source of energy

• Less pressure on non-renewable resources (oil and gas)

• Energy security

• Grid/ Off Grid

• Improved power reliability

• Intermittency Management

• Increased cycles/longer storage

• Efficiency

• Reduced operating costs

• Lower maintenance costs

• Extended equipment lives

• Reduction in wastage

• Reduce outage frequency / duration

• Reduce distribution loss

• Economic in nature - well-run recycling programs cost less to operate than waste collection and landfilling

• Organic pesticides / fertilizers

• Water purification

• Water remediation

• Purification

• Management

Residential

• Alternative fuels

• Biomass

• Solar / Thermal

• Wind

• Hydro

Energy

Generation Energy Storage

Energy

Efficiency

Energy

Infrastructure

Recycling &

Waste

Management

Agriculture, Air &

Water

Materials & Manufacturing

• Waste to energy

• Waste repurposing

TABLE OF CONTENTS

Master Layout:

Large Graph

Market Snapshot: Global Ethanol Production

Top Five Countries (2010) Ethanol Production (millions of gallons/year)1

The Biofuels and Biochem Industry 6

Source: 1NREL (National Renewable Energy Laboratory) Data Book, 2011.

Note: Gallons to Liters conversion ratio at 1:3.78.

The Global Renewable

Fuels Alliance (GRFA)

forecasts ethanol

production to hit 88.7

billion litres in 2011

TABLE OF CONTENTS

Master Layout:

Large Graph

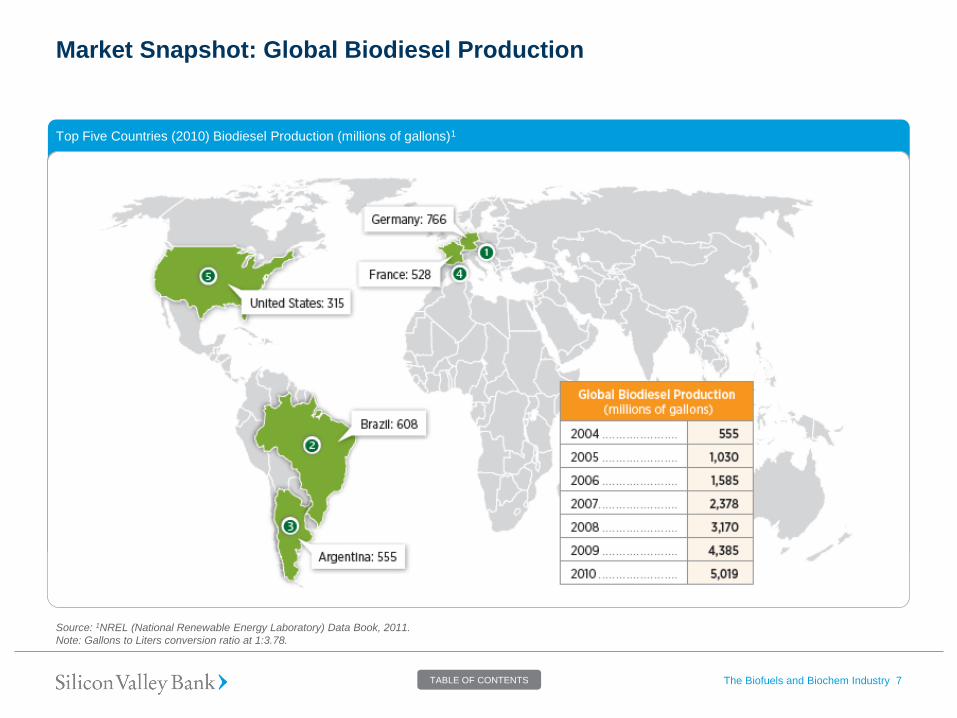

Market Snapshot: Global Biodiesel Production

Top Five Countries (2010) Biodiesel Production (millions of gallons)1

The Biofuels and Biochem Industry 7

Source: 1NREL (National Renewable Energy Laboratory) Data Book, 2011.

Note: Gallons to Liters conversion ratio at 1:3.78.

TABLE OF CONTENTS

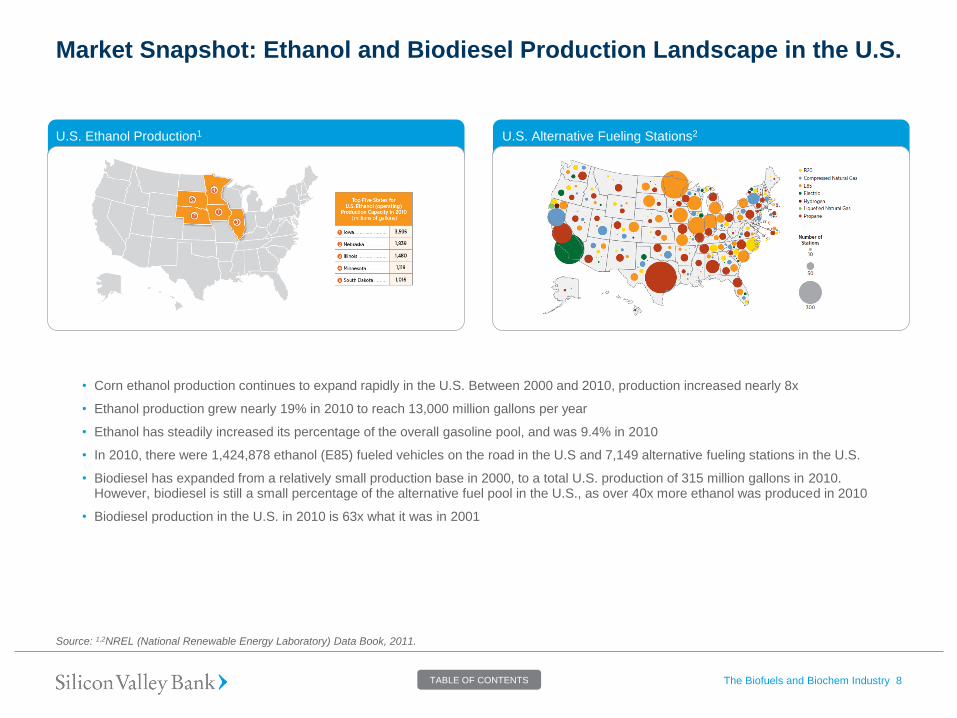

Market Snapshot: Ethanol and Biodiesel Production Landscape in the U.S.

U.S. Ethanol Production1 U.S. Alternative Fueling Stations2

The Biofuels and Biochem Industry 8

Source: 1,2NREL (National Renewable Energy Laboratory) Data Book, 2011.

• Corn ethanol production continues to expand rapidly in the U.S. Between 2000 and 2010, production increased nearly 8x

• Ethanol production grew nearly 19% in 2010 to reach 13,000 million gallons per year

• Ethanol has steadily increased its percentage of the overall gasoline pool, and was 9.4% in 2010

• In 2010, there were 1,424,878 ethanol (E85) fueled vehicles on the road in the U.S and 7,149 alternative fueling stations in the U.S.

• Biodiesel has expanded from a relatively small production base in 2000, to a total U.S. production of 315 million gallons in 2010. However, biodiesel is still a small percentage of the alternative fuel pool in the U.S., as over 40x more ethanol was produced in 2010

• Biodiesel production in the U.S. in 2010 is 63x what it was in 2001

TABLE OF CONTENTS

Master Layout:

Large Graph

Market Snapshot: Global Biochemical Production

Overview of Biochemicals

• Like the biofuels industry, the biochemical industry uses bioprocesses and biomass to replace petroleum as the important building block for a number of products including plastics, lubricants, waxes and cosmetics.

• According to the American Chemistry Council dated July 2011, the market size of the global chemical industry (Basic Chemicals, Intermediate Chemicals, Finished Chemical Products)1 was approximately $3.0 trillion as of July 2011

• Specialty chemicals compete more on desired effect than cost and as a result present less price‐sensitive, higher ASP markets for renewable chemical firms to target

• In the U.S. ~200,000 barrels of oil per day are required to fulfill demand for plastic packaging

Specialty Biochemicals

The Biofuels and Biochem Industry 9

Source: Elevance Renewable Sciences Filings.

Note: 1Basic Chemicals include Butadiene, Propylene, Ethylene, Benzene; Intermediate Chemicals include Butanediol, Acrylic acid, Ethlyene glycol; Finished Products include

BR, PBT, SBR, Polyacrylics, PE, PET, Nylon-6.

Name Characteristics Uses

Adhesives Liquid or semi-liquid compound that bonds items together

via drying, heat or pressure

Paper products, labeling, packaging, plastic bags,

stamps, lamination

Cationic Surfactants Organic compound consisting of phospholipids and

proteins with positively charged heads that lower the

surface tension between liquids and other surfaces

Soaps, detergents, shampoos, toothpastes

Geraniol Clear to pale yellow that is insoluble in water Commonly used in perfumes or fruit flavoring

Industrial Lubricants Oil-based compound that reduces friction between moving

surfaces

Used in operation of manufacturing, mining and

transportation equipment and more

Linalool Naturally occurring alcohol found in flowers and spice

plants

Scents for perfumes and cleaning agents, insecticides,

used to make Vitamin E

Nonionic Surfactant Organic compound consisting of phospholipids and

proteins with non-charged heads

Lower the surface tension of liquids or between liquids

and another surface

O2 Scavenger Compounds that inhibit oxidation or other molecules Used to prevent the corrosion metal by oxygen

Plasticizer Additives that increase the workability, flexibility and

fluidity of a substance allowing for easier changing of

shape

Used for plastics, concrete and dry wall

Specialty Emollients Lipids that attract water and retain moisture Used in lotions and make-ups to prevent dry skin

Squalane Saturated form of squalene making it less susceptible to

oxidation

Used in personal care products such as moisturizers

Consumer

Products

Polymers

and

Coatings

Lubricants

and Additives

4.6 MM

tonnes/yr

4.0 MM

tonnes/yr

73.0 MM

tonnes/yr

• Specialty surfactants

• Soy petrolatum

• Performance waxes

• Candles

• Base oils

• Fuel additives

Building blocks for

• Specialty polymideds, polyols, polyesters

• Epoxies and polyurethanes

• Coatings and cross linkers

TABLE OF CONTENTS

Biofuels/Biochemicals Overview

The Biofuels and Biochem Industry 10 TABLE OF CONTENTS

What are Biofuels/Biochemicals? – Summary

• The Biofuels and Biochemicals industry refers to the set of companies focused on developing fuels and chemicals from Biomass rather than

from fossil fuels

• In 2010, approximately 700 million barrels of biofuels were produced globally. Over 45% of this was corn‐based ethanol in the U.S. and

>25% produced was sugarcane‐based ethanol in Brazil

• Biofuels/ Biochemicals are distinguished as either first , second or third generation. Focus is more on second generation and beyond as first

generation is a mature technology

— Corn and sugarcane will continue to be the most abundant feedstock for biofuels and biochemicals in the near term

— Companies utilizing food‐competitive feedstock (e.g., corn, soy, wheat) face higher price volatility and potential for societal push‐back

— Cellulosic feedstock does not face the “food‐vs.‐fuel” argument but requires more specialized and expensive enzymes that are yet to be

completely commercialized

— Waste is a unique feedstock and companies that can successfully convert the biomass to fuels and chemicals will benefit significantly

— “Energy‐dedicated” crops are emerging and will be vital to the growth of cellulosic biofuel and biochemical production

— Algae offer the highest oil yields of any biofuel feedstock, but challenges around cost have created challenges for commercial use

• Due to the importance of feedstock to the overall value chain, several companies are developing business models and technologies focused

on the “upstream” segment of the value chain

• Numerous conversion technologies exist each with distinct advantages and disadvantages

• The United States and Brazil currently produce and consume the vast proportion of global biofuels due to size of ethanol industries, and is

expected to remain the most important countries for biofuel production/consumption in the near‐term

• Biofuel and Biochemical companies are aiming to compete in large established markets in fuels and specialty chemicals

The Biofuels and Biochem Industry 11 TABLE OF CONTENTS

Master Layout:

Large Graph

What are Biofuels/Biochemicals?

Renewable Energy Share of Global Final Energy Consumption, 2010

The Biofuels and Biochem Industry 12

• A biofuel/ biochemical is a product made from biomass – organic material with stored chemical energy.

Biofuels/Biochemicals can be made from plant materials such as sugarcane, corn, wheat, vegetable oils,

agriculture residues, grass, wood and algae.

• Biofuels/Biochemicals currently comprise only a small part of today’s global energy consumption. Liquid

biofuels accounted for a modest 2.7% of global road-transport fuels in 2010 and only 0.6% of the global

final energy consumption. However, by 2030, this is forecast to increase to 9%, equivalent to 6.5 million

barrels of oil a day.

• Renewable energy overall (bio-energy, hydro, solar, etc) represented 16.0% of total energy demand in 2010.

Source: Renewables 2011, Global Status Report.

Note: 1Traditional biomass means unprocessed biomass, including agricultural waste, forest products waste, collected fuel wood, and animal dung, that is burned in stoves or

furnaces to provide heat energy for cooking, heating, and agricultural and industrial processing, typically in rural areas.2Modern bioenergy comprises biofuels for transport,

and processed biomass for heat and electricity production.

While traditional

biomass1 constitutes an

important part of the

energy mix, so far

modern biomass2 use

makes up only a small

share of total global

energy consumption

Several economical,

political, technological,

and environmental

factors will drive growth

in the Biofuels/

Chemicals industry

Nuclear 2.8%

Fossil

Fuels 81%

Renewable 16.2%

Wind/Solar/Biomass/Geothermal Power Generation 0.7%

Transport Biofuels 0.6%

Biomass/Solar/Geothermal/

Hot Water/Heating 1.5%

Hydropower 3.4% Traditional

Biomass 10%

16.2%

TABLE OF CONTENTS

Global Average Annual Growth Rates of Renewable Energy Capacity and Biofuels Production, 2005–2010

Biofuels/Biochemicals Growth Rates

The Biofuels and Biochem Industry 13

• Global energy consumption rebounded strongly in 2010 after an overall downturn in 2009, with annual growth of 5.4%. Renewable energy, which had no

downturn in 2009, continued its strong growth in 2010 as well.

• During the period from the end of 2005 through 2010, total global capacity of many renewable energy technologies – including solar photovoltaic (PV), wind

concentrating solar power (CSP), solar water heating systems, and biofuels – grew at average rates ranging from around 15% to nearly 50% annually.

• Solar PV increased the fastest of all renewables technologies during this period, followed by biodiesel and wind. For solar power technologies, growth

accelerated during 2010 relative to the previous four years.

• At the same time, growth in total capacity of wind power held steady in 2010, and the growth rates of biofuels have declined in recent years, although ethanol

was up again in 2010.

• Hydropower, biomass power and heat, and geothermal heat and power are growing at more ordinary rates of 3–9% per year, making them more comparable

with global growth rates for fossil fuels (1–4%, although higher in some developing countries). In several countries, however, the growth in these renewable

technologies far exceeds the global average.

Source: 1Renewables 2011, Global Status Report.

72%

81%

25%

77%

3%

3%

16%

17%

7%

49%

60%

27%

25%

4%

3%

16%

23%

38%

Solar PV

Solar PV(grid -connected only)

Wind Power

Concentrating Solar Thermal Power

Geothermal power

Hyderopower

Solar hot water/heating

Ethanol production

Biodiesel production

Year-end 2005-2010(5-year Period)

2010

In 2010, approximately

700 million barrels of

biofuels were produced.

Over 45% of this was

corn‐based ethanol in

the U.S. and >25%

produced was

sugarcane‐based

ethanol in Brazil

TABLE OF CONTENTS

Main Feedstock Sources

Crops used for Biofuels/Biochemicals

Biofuel Vehicle and Pumps

Feedstock is typically the largest component of biofuel &

biochemical production cost. Feedstock cost is estimated to

represent >30%‐50% of the operating costs of most projects.

The main sources of biofuels are:

1. Oil-seed crops: Oil –seed crops include soybean, rapeseed and

sunflower. These go through a process called “transesterification” and

the oils of these oilseeds are converted into methyl esters. Methyl

esters are liquid fuel that can either be blended with petro-diesel or

used as pure biodiesel.

2. Grains, cereals and starches: These come from corn, wheat, sugar

cane, sugar beet and cassava, which undergo a fermentation process

to produce bio-ethanol.

3. Non oilseed crops: Oil from the Jatropha fruit shows most promise.

The fruit is poisonous, so it is not affected by the “food-or-fuel” tug of

war; and it grows well on arid soils which means it does not need felling

of forests. It is very resilient and needs less fertilizer and it can be

developed into plantations like any oilseed crop.

4. Organic waste: Waste cooking oil, animal manure and household

waste. Waste cooking oils can be converted into biodiesel while the rest

are converted to biogas methane.

5. Cellulosic materials: These are grasses, crop waste, municipal waste

and wood chips that are converted to ethanol. The conversion process

is more complex than the two process aforementioned. There is also

the option of converting these to gases such as methane or hydrogen

for vehicle use or to power generators.

The Biofuels and Biochem Industry 14

Source: Broker Research and websites.

TABLE OF CONTENTS

Types of Biofuels

Biofuels/Biochemicals are

distinguished as either first, second

or third generation.

Most of the Biofuels today come from

corn-based ethanol and sugar-based

ethanol.

The current debate over biofuels/

biochemicals produced from food

crops has pinned a lot of hope on

"2nd-generation processes"

produced from crop and forest

residues and from non-food energy

crops.

Second generation conversion

technologies are key to progress and

sustainability.

The Biofuels and Biochem Industry 15

Source: UNEP Assessing Biofuels Report.

Note: Litre: Gallon = 1:0.26; Gallon: Barrel = 1: 0.0322; Tonne of Oil Equivalent (toe): Barrel of Oil Equivalent (boe) = 1: 7.4.

First generation: Commercially produced using conventional technology. The basic feedstock are seeds, grains, or whole plants

from crops such as corn, sugar cane, rapeseed, wheat, sunflower seeds or oil palm. These plants were originally selected as food or

fodder and most are still mainly used to feed people. The most common first-generation biofuels are bioethanol (currently over 80%

of liquid biofuels production by energy content), followed by biodiesel, vegetable oil, and biogas.

Second generation: Produced from a variety of non-food sources. These include waste biomass,

the stalks of wheat, corn stover, wood, and special energy or biomass crops (e.g. Miscanthus).

Second-generation biofuels/biochemicals use biomass to liquid (BTL) technology, by

thermochemical conversion (mainly to produce biodiesel) or fermentation (e.g. to produce

cellulosic ethanol). Many second-generation biofuels/biochemicals are under development such

as biohydrogen, biomethanol, Fischer-Tropsch diesel, biohydrogen diesel, and mixed alcohols.

The commercial-scale production costs of 2nd-generation biofuels have been estimated by the

IEA to be in the range of US $0.80 - 1.00/liter of gasoline equivalent (lge) [US $3.02-$3.79 per

gallon] for ethanol and at least US $1.00/liter [$3.79 per gallon] of diesel equivalent for synthetic

diesel. This range broadly relates to gasoline or diesel wholesale prices (measured in USD /lge)

when the crude oil price is between US $100-130 /bbl . (However, many companies within SVB’s

universe are estimating crude oil parity without subsidy of between US$60 -80/bbl or $1.50 to

$2.00/gal at scale).

Third generation: Algae fuel, also called oilgae, is a biofuel/biochemical from algae and

addressed as a third-generation petroleum replacement. Algae is a feedstock from aquatic

cultivation for production of triglycerides (from algal oil) to produce petroleum replacement

products. The processing technology is basically the same as for biodiesel from second-

generation feedstock. Other third-generation biofuels include alcohols like bio-propanol or bio-

butanol, which due to lack of production experience are usually not considered to be relevant as

fuels on the market before 2050.

TABLE OF CONTENTS

First Generation Feedstocks

The Biofuels and Biochem Industry 16

Source: Clean Tech Energy Report by Robert Baird.

Note: Litre: Gallon = 1:0.26; Gallon: Barrel = 1: 0.0322; Tonne of Oil Equivalent (toe): Barrel of Oil Equivalent (boe) = 1: 7.4.

Sugar cane has been used to produce bioethanol in Brazil since the 1970s. It is a perennial plant that needs few inputs, such as fertilizers, and has long root systems

that can store carbon in the soil. It has a good net Greenhouse Gases (GHG) balance (up to 90% reduction in GHGs from ethanol produced from sugar cane,

compared with conventional gasoline). Sugar Cane is one of the most heavily utilized feedstock for biofuels production and the highly developed infrastructure of the

sugarcane industry in Brazil will continue to make the country a hot‐spot for Biofuel/BioChemical firms. According to the U.S. Department of Energy, Brazilian

Sugarcane is not only the most abundant, but the cheapest available feedstock for ethanol production. Brazilian sugarcane offers several economic advantages to corn,

which in the Unites States is the principal ethanol crop. Sugarcane produces around 15 dry tons per acre per year yielding roughly 600 gallons of ethanol per acre.

Corn is a cereal grain that was domesticated in Central America. Corn can be used as a feedstock to make biobutanol and bioethanol. Corn is the most abundant crop

grown in the U.S. and the backbone of the current U.S. Biofuel industry. Approximately 80 million acres of land in the U.S. are dedicated to growing corn, and the U.S.

accounts for ~20% of global corn exports. For 2010, the USDA estimates the national corn crop to yield 154.3 bushel/acre, which corresponds to a dry weight of ~3.7

t/acre. Currently, one bushel of corn produces around 2.75 gallons of ethanol equating to 400 to 500 gallons per acre. Corn yields have experienced a long term general

uptrend from 70 bushels/acre in 1970 to the current yield as a result of enhanced seed research and development following the mapping of the corn genome. Corn ears

are widely used as a feedstock for first‐generation ethanol, but corn stover, the above‐ground portion of the plant that is left in the field after harvest, is increasingly being

utilized for second generation ethanol production.

Wheat is a grass that is cultivated worldwide. Wheat grain is used to make flour for breads, biscuits, pasta and couscous; and for fermentation to make beer, alcohol or vodka.

Wheat can be used as a feedstock to make bioethanol, and it has few sustainability issues. Wheat can also be used to make biobutanol.

Sweet sorghum is one of the many varieties of sorghum which have a high sugar content. Sweet sorghum will thrive better under drier and warmer conditions than many other crops

and is grown primarily for forage, silage, and syrup production. Sorghum has a very limited breeding history and as a result there has not been the same degree of testing for yield

improvements through genetic optimization as in other major biofuel feedstocks such as corn and sugarcane. While sorghum isn’t as well‐suited as sugarcane for the production of

refined sugar, it has value for ethanol, and its high lignocellulosic biomass content opens up the potential for use in the production of additional biofuels.

Soybeans are a class of legumes native to East Asia. The crop is primarily harvested as a food source due to its exceptionally high protein content (~40% of dry weight). In

addition to their protein, soybeans are also valued for their oil content which accounts for ~20% of the dry weight of the beans. According to the USDA, approximately 17% of soy

oil is used in industrial products. These products include biodiesel, inks, paints, plasticizers and waxes, among many others. China is the world’s largest producer of soybeans oil

with more than 10M tons in 2010. Global production of soy oil exceeded 41 million metric tonnes (90 billion pounds) in the 2010/2011 season.

Rapeseed is a yellow flowering plant of the mustard family that produces a seed which yields ~40% oil. It naturally contains 45+% euracic acid which is mildly toxic to

humans. Rapeseed is often grown as a high‐protein animal feed and also used in lubricants, soaps, and plastics manufacturing. According to the USDA, approximately 30%

of rapeseed oil is used in industrial products. In Europe, Rapeseed has become a preferred feedstock for biofuels as it has higher oil yields per unit of land than other crops

including soy beans, which only contain ~18‐20% oil. According to the Agricultural Marketing Resource Center, worldwide production was 61million tons in 2011 with China

and India being the largest producers at 14.7 million and 7.3 million tons respectively. The European Union accounted for 23 million tons of rapeseed output.

TABLE OF CONTENTS

Second and Third Generation Feedstocks

The Biofuels and Biochem Industry 17

Source: Clean tech Energy Report by Robert Baird, June 2011.

Note: Litre: Gallon = 1:0.26; Gallon: Barrel = 1: 0.0322; Tonne of Oil Equivalent (toe): Barrel of Oil Equivalent (boe) = 1: 7.4.

Miscanthus is a tall perennial grass closely related to sugar cane. Though native to the tropical and subtropical climates of Africa and Southeast Asia, it is also

being grown by at least 10 countries in Europe explicitly for use as an energy feedstock. It has entered into favor due to its high expected commercial yields of

12-13 BDT/acre (as reported by Mendel Biotechnology in LA and MS) with low moisture content in the range of 15‐20% if harvested in late winter or spring.

Waste is a unique feedstock since it can often generate additional revenue from tip‐fees, but its heterogeneous characteristic makes it difficult to convert to biofuels

and chemicals. Municipal Solid Waste (MSW) and Commercial & Industrial (C&I) waste are two waste streams that several companies in the industry are working to

convert into fuels and chemicals. According to Pike Research, the market research and consulting firm that provides in-depth analysis of global clean technology

markets, the global market for thermal and biological waste-to-energy technologies is set to reach at least $6.2 billion in 2012 and grow to $29.2 billion by 2022.

Jatropha is a genus covering ~150 types of plants, shrubs, and trees which produce seeds with oil content of up to 40%. Making it even more attractive as a

feedstock is its ability to grow on poor quality land and its resistance to drought and pests. It is native to South America and typically only grows in tropical or

subtropical environments. One drawback of Jatropha is that it also contains toxic matter which necessitates it be carefully processed before use in production. It

is estimated that Jatropha nuts are capable of providing up to 2,270 liters of biodiesel per hectare, and the plant is currently the subject of several trials for use in

biodiesel applications including a collaborative effort between Archer Daniels Midland, Bayer CropScience AG, and Daimler AG.

Southern pine presents a rich biomass source in the Southeastern portion of the U.S. These trees typically reach heights of 60‐120 feet (depending on species) and

are characterized by their rounded tops, long needles, and rapid growth rates. According to the DOE, there are roughly 200 million tons of no-merchantable forest

material alone and total forestland in the US is estimated to be 750 million acres.

Switchgrass is a perennial warm season grass native to North America. It can grow to heights of almost nine feet and an established stand has a lifespan of up to 10 years.

One of its defining characteristics is its large, underground root system which can weigh as much as 6-8 tons per acre, making the plant particularly adept at accumulating

carbon dioxide .The energy efficiency of producing ethanol from switchgrass is estimated to be much higher than corn with an energy input to output rate of 1:4 vs. 1:1.3. As

reported by the USDA, various switchgrass crops yield 5-9.4 tons per acre.

Algae offer the highest oil yields of any biofuel feedstock, but issues around capital cost have created challenges for commercial use: Algae are simple‐celled

organisms capable of creating complex organic compounds from inorganic molecules through photosynthetic pathways. Interest in using algae as a feedstock for

biofuel production has increased rapidly and more than 30 U.S. based firms are now working to commercialize such technology. Algae offer attractive yields

estimated to be upward of 4,000 to 5,000 gallons per acre. The DOE considers open pond algal configurations to have the most promise estimating 2012 fuel

costs to be $9.28/ gal with a roadmap to $2.27/ gal.

Camelina is an annual flowering plant and member of the mustard family, regarded for its oil properties. It typically stands 1‐3 feet tall, is heavily branched, and produces

small seeds high in oil content. It is able to grow effectively on land of marginal quality, needs minimal water input, and can withstand cold climates. Because of its high

oil‐yield of 35‐38% (~2x that of soybeans), it is specifically being studied for use in biodiesel applications.

TABLE OF CONTENTS

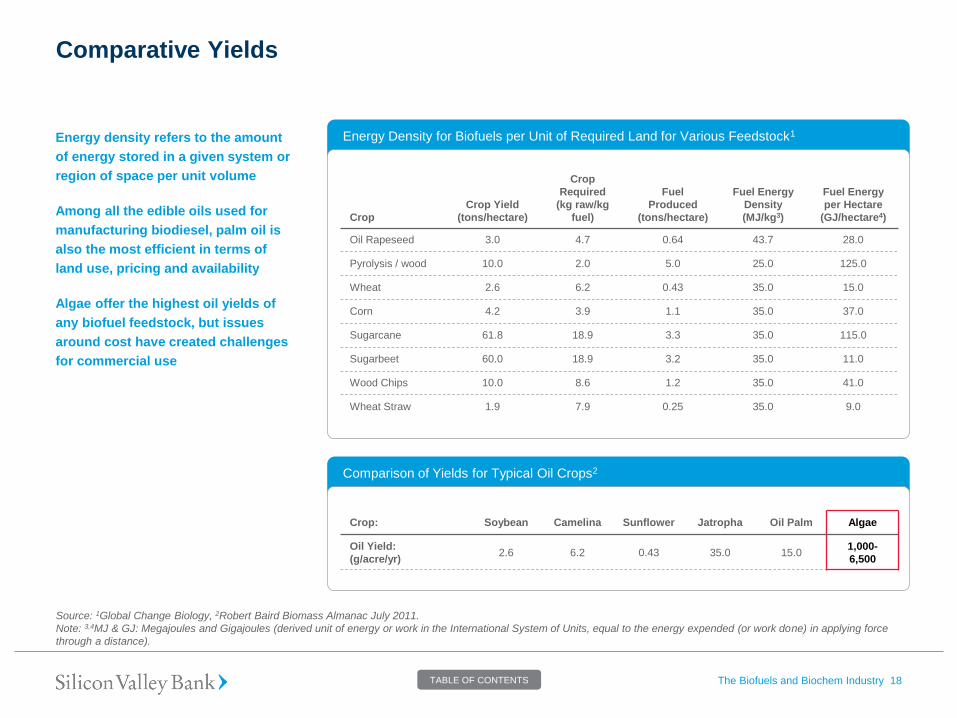

Comparative Yields

Energy density refers to the amount

of energy stored in a given system or

region of space per unit volume

Among all the edible oils used for

manufacturing biodiesel, palm oil is

also the most efficient in terms of

land use, pricing and availability

Algae offer the highest oil yields of

any biofuel feedstock, but issues

around cost have created challenges

for commercial use

The Biofuels and Biochem Industry 18

Source: 1Global Change Biology, 2Robert Baird Biomass Almanac July 2011.

Note: 3,4MJ & GJ: Megajoules and Gigajoules (derived unit of energy or work in the International System of Units, equal to the energy expended (or work done) in applying force

through a distance).

Energy Density for Biofuels per Unit of Required Land for Various Feedstock1

Crop

Crop Yield

(tons/hectare)

Crop

Required

(kg raw/kg

fuel)

Fuel

Produced

(tons/hectare)

Fuel Energy

Density

(MJ/kg3)

Fuel Energy

per Hectare

(GJ/hectare4)

Oil Rapeseed 3.0 4.7 0.64 43.7 28.0

Pyrolysis / wood 10.0 2.0 5.0 25.0 125.0

Wheat 2.6 6.2 0.43 35.0 15.0

Corn 4.2 3.9 1.1 35.0 37.0

Sugarcane 61.8 18.9 3.3 35.0 115.0

Sugarbeet 60.0 18.9 3.2 35.0 11.0

Wood Chips 10.0 8.6 1.2 35.0 41.0

Wheat Straw 1.9 7.9 0.25 35.0 9.0

Comparison of Yields for Typical Oil Crops2

Crop: Soybean Camelina Sunflower Jatropha Oil Palm Algae

Oil Yield:

(g/acre/yr) 2.6 6.2 0.43 35.0 15.0

1,000-

6,500

TABLE OF CONTENTS

Comparative Advantages and Disadvantages of Feedstock

The Biofuels and Biochem Industry 19

Source: Robert Baird Biomass Almanac July 2011.

Corn Sweet Sorghum Sugarcane Soybean Oil Rapeseed Oil Pine Oil

P

O

S

I

T

I

V

E

S

Ethanol industry

experienced with using

corn as a feedstock

Corn stover offers

potential for use in

cellulosic fuel

applications

Annual crop – short

growth cycle (90‐120+

days) allows for multiple

cuts (2‐3) to be made in

a given year

Low water requirements

and adaptable to wide

variety of environments

Less residual waste

biomass from harvesting

Cheapest available crop

(non‐cellulosic) for

ethanol production

Does not have to be

transitioned from a

complex carbohydrate to

a simple sugar prior to

fermentation

Does not compete as a

food source

Good oil content makes it

suitable for biodiesel

production

Seeds have very high oil

content by volume at

~40%

Can be used as an

animal feed as well as in

lubricants and plastics

manufacturing

High energy density and

saturated fat content

I

S

S

U

E

S

Use for corn in biofuels

stokes the “food vs. fuel”

argument

Subject to commodity

pricing volatility

High quality land required

as well as significant

water and fertilizer needs

Lower sugar yields

compared to sugarcane

Yields mixed sugars as

opposed to pure sucrose,

making it less conducive

for production of refined

sugars

Due to harvest timelines,

average mills only

operate an average of

~185 days per year

Requires high quality

land and significant water

and fertilizer inputs

Vegetative propagation

can lead to overcrowding

Competes as a food

source

Oil content lower than

many competing crops

used as targets for

biofuels

Production of biodiesel

from soybean oil results

in a net energy loss of

~30%

Shares significant

demand with Canola oil

which could add to price

volatility

Burning of peatland to

clear room for new

plantations leading to

significant deforestation

and GHG emissions

TABLE OF CONTENTS

Switchgrass Camelina Miscanthus Municipal Solid Waste Jatropha Southern Pine

P

O

S

I

T

I

V

E

S

Reliable biomass yields

due its propensity for

accumulating CO2

Higher energy content

than corn for ethanol

production

Wide adaptability and

capable of growth in dry

climates

ESelf‐seeding, requiring

no replanting after

harvesting

Can be grown on

marginal lands, in cold

climates, and with

minimal water

Short crop that can be

rotated with wheat

High oil yields of 35‐38%

Reliable biomass yields

Capable of relatively high

yields today

Can be grown effectively

without fertilizers – less

leaching

Can generate a

significant revenue

stream from tip‐fees

Continuously generated

– no need for agriculture

and spending

Collection and hauling

logistics and

infrastructure is in place

Can be grown on low

quality land

Naturally resistant to

drought and pests –

though yields shown to

be significantly higher

when irrigated

Does not compete as a

food source as it is

non‐edible

Shuttering of paper &

processing mills in U.S.

have led to a growth

surplus

Wood waste offers an

inexpensive source of

biomass

Trees have longer

growth cycles than other

energy crops

I

S

S

U

E

S

Additional research

required before

commercially viable

Additional time/research

needed before

commercially viable

Limited adoption thus far

in North America

Studies have found it

dries up soil more than

other crops which can

reduce surface water

supplies

Heterogeneous

characteristic makes

conversion difficult

Often requires

gasification which can

carry high CAPEX

requirements

Contains toxic matter

which must be separated

before used in production

Still requires significant

yield improvements

before economically

viable at commercial

scale

Collection processes for

residual wood waste still

need development

Rising demand for pulp

globally could provide

upward pricing pressures

Cannot be utilized as

feedstock by

non‐cellulosic conversion

technologies

Comparative Advantages and Disadvantages of Feedstock (con’t)

The Biofuels and Biochem Industry 20

Source: Robert Baird Biomass Almanac July 2011.

TABLE OF CONTENTS

Petroleum Replacement Overview

The Biofuels and Biochem Industry 21

Source: ZeaChem,, Inc..

Market Size Customers

Conversion

Technology

Propionic

C3 Propanol Propylene

Butyric

C4

Acetic

C2

Butanol Butene

Alkylate/

Polygas

Poly-

propylene

Acrylics

Alkylate

Acetic

Sales

Ethanol Ethylene

Drop-in

Gasoline/Alkylate

Automative/

Packaging

Rayon/Filters

VAM

Acetic

Anhydride

Paint/Adhesives

Packaging

PET

Rubber/Plastics

Drop-in Gasoline

Gasoline Blending

Jet/Diesel

Cellulosic

Acetate

Ethylene glycol

Linear a-

olefins

EVA

Poly-ethylene

Super-Absorbents

$485 billion Refiners

$110 billion

Consumer

Products

Chemical

Companies

$180 billion

Consumer

Products

Paint Companies

Chemical

Companies

$245 billion

$60 billion

$1 billion

Airlines/Dod

Refiners

Refiners

Consumer

Products

TABLE OF CONTENTS

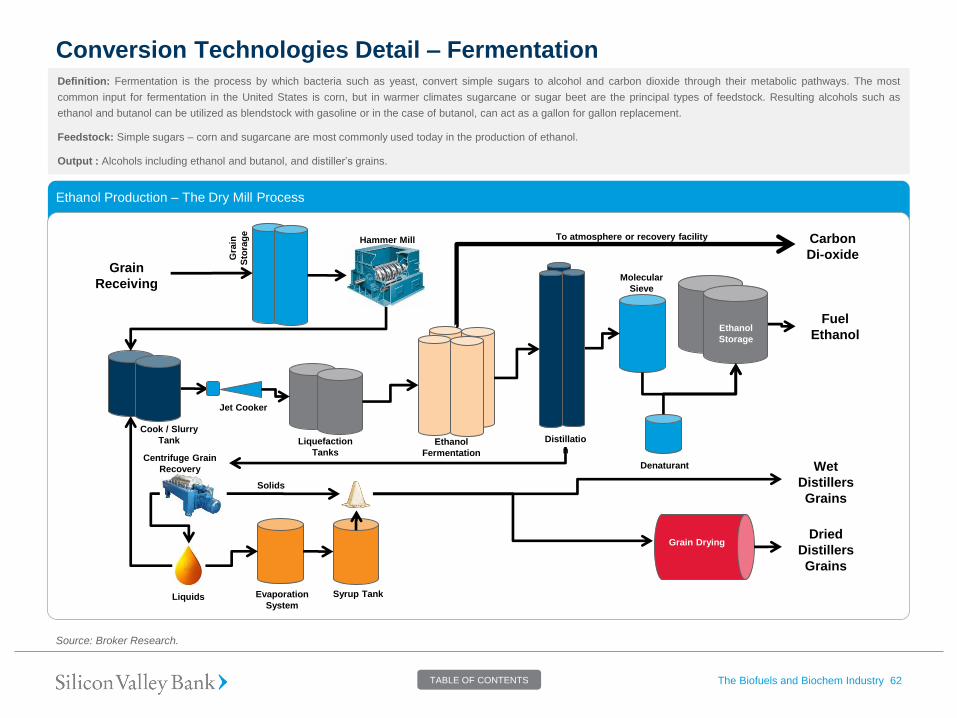

Conversion Technologies – Fermentation and Fluid Catalytic Cracking

The Biofuels and Biochem Industry 22

Fermentation Fluid Catalytic Cracking

TECHNOLOGY

Definition: Fermentation is the process by which bacteria such

as yeast, convert simple sugars to alcohol and carbon dioxide

through their metabolic pathways. The most common input for

fermentation in the United States is corn, but in warmer climates

sugarcane or sugar beet are the principal types of feedstock.

Resulting alcohols such as ethanol and butanol can be utilized

as blendstock with gasoline or in the case of butanol, can act as

a gallon for gallon replacement

Feedstock: Simple sugars – corn and sugarcane are most

commonly used today in the production of ethanol

Output : Alcohols including ethanol and butanol, and distiller’s

grains

Definition: Fluid Catalytic Cracking (FCC) is a proven process

in the petroleum industry used to convert crude oil into higher

value products such as gasoline and naptha. FCC reactions

occur at extremely high temperatures (up to 1,000+ F°) and

use fine, powdery catalysts capable of flowing likely a liquid

which break the bonds of long‐chain hydrocarbons into smaller

carbon‐based molecules. FCC technology is applied to organic

sources of carbon such as woody biomass to convert the

cellulosic content into usable hydrocarbons with equivalence to

crude oils – this process is referred to as Biomass Fluid

Catalytic Cracking (BFCC). FCC was first commercialized in

1942, and is presently used to refine ~1/3 of the U.S.s’ total

annual crude volume

Feedstock: Feedstock agnostic – can utilize cellulosic biomass

Output: Biocrude, gases

POSITIVES

Ability to genetically modify metabolic pathways of

organisms to yield different carbon molecule outputs

(ethanol, butanol)

Process already demonstrated at commercial scale via

first‐generation ethanol production

Common outputs such as ethanol / butanol have existing

markets in both fuels and chemicals

Commercially proven technology in the petroleum industry

Can process low‐cost cellulosic biomass

ISSUES

Costly to develop/purchase enzymes to break down

cellulosic materials to make simple sugars available for

fermentation

First‐generation feedstock susceptible to commodity price

volatility

High capital costs for facilities

Proven for petroleum but limited to demonstration testing for

biomass

Source: Robert Baird, Clean Tech report July 2011.

TABLE OF CONTENTS

Conversion Technologies – Anaerobic Digestion and Gasification

The Biofuels and Biochem Industry 23

Source: Robert Baird, Clean Tech report July 2011.

Anaerobic Digestion Gasification

TECHNOLOGY

Definition: Anaerobic digestion is the process by which

bacteria decompose wet organic matter in the absence of

oxygen. The result is a byproduct known as biogas which

consists of ~60% methane and ~40% carbon dioxide. Biogas

can then be combusted in the presence of oxygen to generate

energy. Effectively any feedstock can be converted to biogas

via digestion including human and animal wastes, crop

residues, industrial byproducts, and municipal solid waste.

Anaerobic digestion is the same process that created natural

gas reserves found throughout the world today

Feedstock: Starches, celluloses, municipal solid waste, food

greases, animal waste, and sewage

Output: Biogas

Definition: Gasification is a process by which carbon‐based

materials such as coal, petroleum coke, and biomass are

separated into their molecular components by a combination of

heat and steam, forming a gaseous compound known as

synthesis gas or syngas as it is commonly called

Feedstock flexibility: Feedstock flexible including use of

municipal solid waste

Output: Syngas which has the capacity to be used in a variety

of applications including the production of transportation fuels,

electricity, and heat. Other byproducts include sulphur and slag

POSITIVES

Commercially proven technology

Can be used to process wet organic matter

Resulting materials can be processed into valuable fertilizer

Utilization of methane to produce biogas reduces impact of

GHG emissions from landfill gas

Low capital and costs and potential for low operating cost

Input flexibility allows costs to be reduced through lower cost

feedstock

Energy conversion ratio potentially higher than competing

technologies because biomass‐to‐liquid (BTL) gasification

can convert all of the cellulosic material into transportation

fuels

Lower emission levels than traditional power production

ISSUES

Slower process than many alternatives

Cannot be used to convert lignin

Accumulates heavy metals and contaminants in the

resulting sludge

Gas clean‐up has disrupted projects in the past

Gas quality suffers from irregularity due to challenges in

removing tar content– energy density ~50% of natural gas

High capital and operating costs – this could be reduced in

future by co‐location next to feedstock sources

TABLE OF CONTENTS

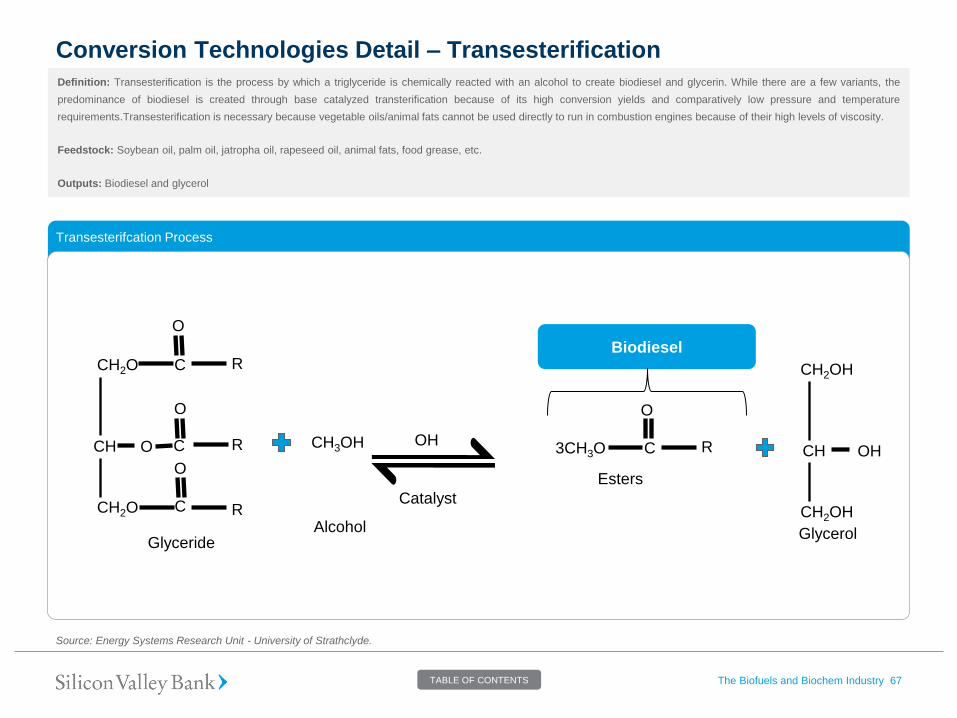

Conversion Technologies – Pyrolysis and Transesterification

The Biofuels and Biochem Industry 24

Source: Robert Baird, Clean Tech report July 2011.

Pyrolysis Transesterification

TECHNOLOGY

Definition: Pyrolysis is the process by which organic materials

are decomposed by the application of intense heat in the

absence of oxygen to form gaseous vapors which when cooled

form charcoal and/or bio‐oil can potentially be used as a direct

fuel substitute or an input for the manufacture of transportation

fuels

Feedstock: Capable of using a wide variety of feedstock

including agriculture crops, solid waste, and woody biomass

(currently most common)

Output: Bio‐oil (energy density of ~16.6 megajoules/liter) which

must be processed further before it can be utilized as a

transportation fuel. It also yields syngas and biochar

Definition: Transesterification is the process by which a

triglyceride is chemically reacted with an alcohol to create

biodiesel and glycerin. While there are a few variants, the

predominance of biodiesel is created through base catalyzed

transterification because of its high conversion yields and

comparatively low pressure and temperature requirement.

Transesterification is necessary because vegetable oils/animal

fats cannot be used directly to run in combustion engines

because of their high levels of viscosity

Feedstock: Soybean oil, palm oil, jatropha oil, rapeseed oil,

animal fats, food grease, etc.

Outputs: Biodiesel and glycerol

POSITIVES

Flexibility of feedstock diversifies risk related to feedstock

supply/demand pressures

Marketable biochar output provides secondary revenue

stream from production

Results in lower‐viscosity biodiesel allowing it to replace

petroleum in diesel engines

Glycerin byproduct can be sold to generate secondary

revenue stream

Low cost and high availability of methanol and sodium

hydroxide reduces input costs

Relatively low reaction temperature of 60 degrees C keeps

utility costs down

ISSUES

Potentially corrosive characteristics requiring specialized

components in fuel systems to adequately house it

Viscosity increases during storage meaning it must be used

more frequently than traditional fossil fuels

Requires separation/recovery of base catalyst / glycerin from

solution

Free fatty acid and water contamination can result in

negative reactions

TABLE OF CONTENTS

Conversion Technologies – Syngas Fermentation

The Biofuels and Biochem Industry 25

Source: Coskata Inc, LanzaTech Inc, Advanced Biofuels USA “Syngas Fermentation, The Third Pathway for Cellulosic Ethanol.

Syngas Fermentation

TECHNOLOGY

Definition: Syngas Fermentation is the process by which

gasification breaks the carbon bonds in the feedstock and

converts the organic matter into synthesis gas. The syngas is

sent to bioreactor where microorganisms directly convert the

syngas to a fuels and/or chemicals

Feedstock: Capable of using a wide variety carbon containing

feedstocks including agricultural crops, solid waste, woody

biomass and fossil fuels such as coal and natural gas

Output: Ethanol, 2.3-BDO, Acetic Acid, Acetone, Propanol,

Butanol, MEK, Isoprene, Acrylic Acid, Butadiene, Succinic Acid

POSITIVES

Process does not rely on expensive enzymes or

pretreatment chemicals thus operating costs should be lower

than non-gasification based technology

Ability to convert nearly all feedstock into energy with

minimal by-products. Microorganisms are able to produce

only one fuel/chemical under low temperature and pressure

ISSUES

Imperative to keep the right nutrient and chemical balance in

order to keep the microorganisms alive and productive. Any

contaminants could spread quickly through the bioreactor

Reliability and Continuous Operations: Since the organisms

live off the energy contained in the synthesis gas, it is critical

that they continue to be through a well operating system

design

TABLE OF CONTENTS

The Importance of Biofuels/Biochemicals

The Biofuels and Biochem Industry 26 TABLE OF CONTENTS

Biofuels/Biochemicals Growth – Summary

• The sector has received increasing attention from both public and private investors due to several growth drivers including the desire for

energy independence, the increasing demand for liquid fuels for transportation especially in emerging markets, technological advances

across the industry’s value chain and environmental concerns (Green house gas (GHG) emissions). The most important driver, however,

spurring investment in the industry is the continued volatility and high price of crude oil.

• Biofuels/Biochemicals constitute a 3% share in the total global chemicals & fuels market in 2010 and is expected to touch 17% in 2025.

• As “easy“ conventional oil resources continue to decline and more expensive nonconventional liquid sources make up the difference,

biofuels/ biochemicals will play an increasing role in diversifying the liquid energy landscape.

• Liquids demand is growing mainly driven by rapidly-growing non- Organization for Economic Co-operation and Development (OECD)

economies and will be met by supply growth from Organization of the Petroleum Exporting Countries (OPEC) and the Americas. China (+8

million barrels per day), India (+3.5 million barrels per day), and the Middle East (+4 million barrels per day) account for nearly all of the net

global increases.

• Liquid biofuels accounted for a modest 2.7% of global road-transport fuels in 2010 , but will play an expanded role of meeting liquid demand.

• OPEC’s critical position in the oil market grows given its oil reserve position while the Americas also play an expanding role by utilization of

new recovery technologies in tight oil formations and Canadian oil sands.

• Exporting oil producing nations, “petro-states”, rely heavily on oil revenues to support their economies (50-90% of GDP). Oil price decreases

can cause major deficits, budget cuts, considerable social turmoil, and political change creating an incentive for petro states to keep

production in line with demand.

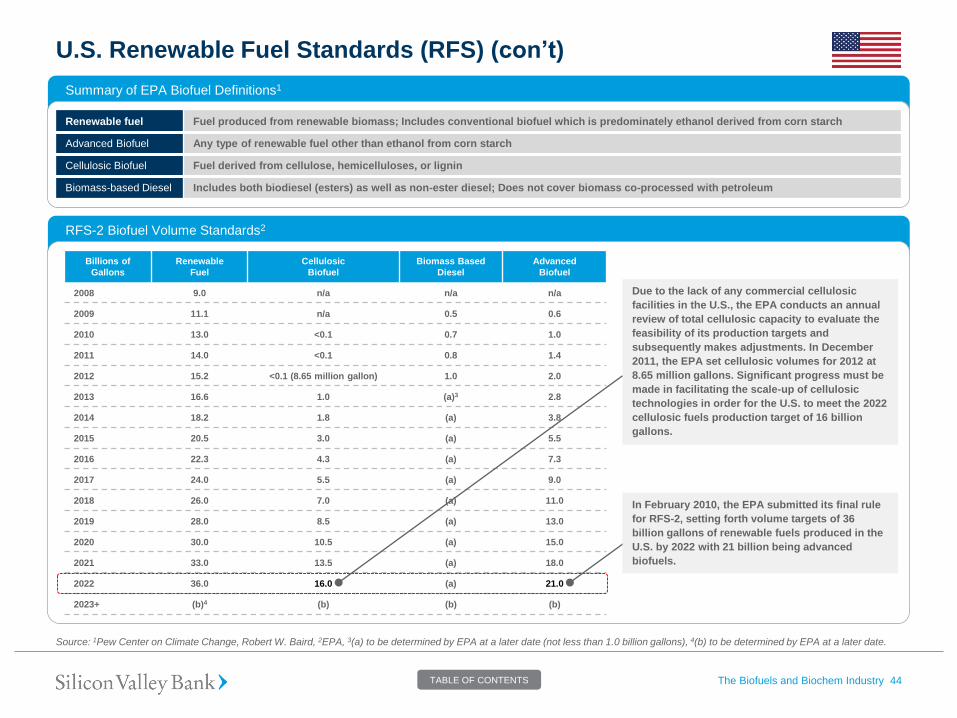

• Government legislation is driving the adoption of renewable fuels

— In February 2010, the US Environmental Protection Agency (EPA) submitted its final rule for Renewable Fuels Standard 2 (RFS-2),

setting forth volume targets of 36 billion gallons of renewable fuels produced in the U.S. by 2022 with 21 billion being advanced biofuels.

— The EU is targeting 10% of transport energy from renewables by 2020, counting both sustainable biofuels and electric vehicles.

The Biofuels and Biochem Industry 27 TABLE OF CONTENTS

Master Layout:

Call Out Text Left, Table Right

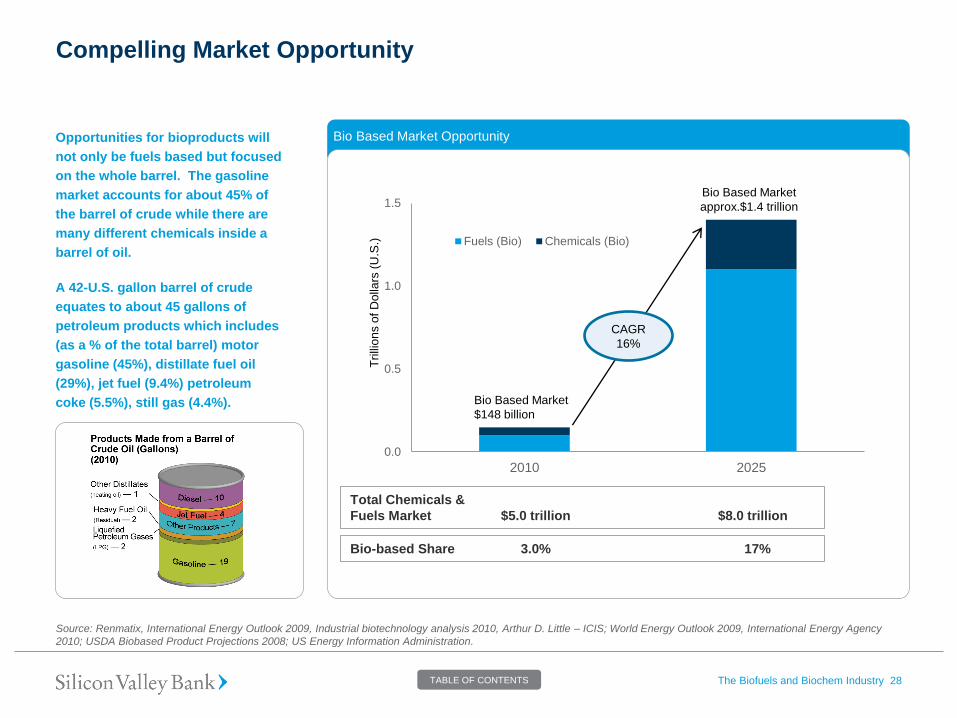

Compelling Market Opportunity

Bio Based Market Opportunity Opportunities for bioproducts will

not only be fuels based but focused

on the whole barrel. The gasoline

market accounts for about 45% of

the barrel of crude while there are

many different chemicals inside a

barrel of oil.

A 42-U.S. gallon barrel of crude

equates to about 45 gallons of

petroleum products which includes

(as a % of the total barrel) motor

gasoline (45%), distillate fuel oil

(29%), jet fuel (9.4%) petroleum

coke (5.5%), still gas (4.4%).

The Biofuels and Biochem Industry 28

Source: Renmatix, International Energy Outlook 2009, Industrial biotechnology analysis 2010, Arthur D. Little – ICIS; World Energy Outlook 2009, International Energy Agency

2010; USDA Biobased Product Projections 2008; US Energy Information Administration.

Total Chemicals &

Fuels Market $5.0 trillion $8.0 trillion

Bio-based Share 3.0% 17%

0.0

0.5

1.0

1.5

2010 2025

Fuels (Bio) Chemicals (Bio)

CAGR

16%

Tri

llio

ns o

f D

olla

rs (

U.S

.)

Bio Based Market

$148 billion

Bio Based Market

approx.$1.4 trillion

TABLE OF CONTENTS

Drivers of Biofuels/Biochemicals Growth

The rising cost of oil will create an

incentive for producers of

petroleum‐derived products to seek

renewable alternatives that provide

greater stability in pricing.

Strong public sentiment for the U.S.

to reduce its dependence on foreign

petroleum reserves is thus one of the

major drivers of the renewable fuel

industry.

U.S. oil imports drop due to rising

domestic output & improved

transport efficiency; EU imports to

overtake those of U.S. around 2015

and China expected to be the largest

importer by 2020.

The Biofuels and Biochem Industry 29

Source: 1Bloomberg, 2World Energy Outlook 2011.

Crude Oil Monthly spot prices ($ per barrel)1

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

$160.0 The volatility and price increases of oil are

the most significant drivers in the growth of

the Biofuel/Biochemical Industry: The

increasing demand for petroleum products,

supply shocks, and other factors have led to

volatile and high oil prices over the past

decade. In January 2000, European Brent

Crude spot prices were below $24/barrel

before peaking at over $140/barrel in 2008.

After some price relief in the midst of the global

economic downturn, Brent Crude is

~$97/barrel currently, representing a CAGR of

~13.5% from 2000‐2011.

Net Imports of Oil2

Biofuels and Biochemicals help reduce U.S.

dependence on foreign oil: U.S. reliance on

foreign imports has increased significantly

since the mid‐1980’s. It can be argued that as

the world’s current economic superpower and

the largest consumer of petroleum, the U.S.

will continue to command a reliable oil supply

from producing nations. However, with the

emergence of rapidly growing and

industrializing economies in China and India,

the global supply of oil may be spread

increasingly thin putting additional upward

pressure on energy prices 0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

China India EU U.S. Japan

2000 2010 2035

Million barrels/day

TABLE OF CONTENTS

Drivers of Biofuels/Biochemicals Growth (con’t)

By 2035, the EIA projects that

transportation sector will account for

73% of all liquid fuels consumption.

Key drivers of transportation growth

include population expansion and

rising real disposable income which

leads to more frequent travel .

The global passenger vehicle fleet

doubles to 1.7 billion in 2035; most

cars are sold outside the OECD by

2020, making non-OECD policies key

to global oil demand.

The development and subsequent

scale‐up of cellulosic technologies

offers a clear advantage to reducing

price volatility of biofuel feedstock

and will play major role in driving

down the costs of renewable

fuels/chemicals.

The Biofuels and Biochem Industry 30

Source: 1World Energy Outlook 2011, 2Bloomberg, 3EIA, DOE, Timber Mart-South.

Note: OECD- Organization for Economic Co-operation and Development.

Vehicles per 1000 people in Selected Markets1

Increase in transportation applications driving

growth in liquid fuels consumption: The Energy

Information Administration (EIA) projects that U.S.

consumption of liquid fuels will increase from 19.1 million

barrels per day in 2009 to more than 21.9 million gallons

per day by 2035. The increase is expected to be driven

almost entirely by an increase in the use of liquid fuels for

transportation applications which is forecasted to grow

from 13.6 million barrels per day in 2009 to 16.1 million

barrels per day by 2035 .

Cellulosic biofuel technologies unlock non‐food

feedstock and reduce input cost volatility: Cellulose (corn

stover, switchgrass, miscanthus, woodchips etc) is not used

for food and can be grown in all parts of the world. The entire

plant can be used when producing cellulosic products. While

the U.S. is the world’s largest producer of the crop, corn

competes as a food source and is subject to significantly

more price volatility than residual waste biomass. Over the

past decade the value of the IMF’s Commodity Food Price

Index increased at a CAGR of 8.7% annually. This is ~3.6x

faster than the rate of inflation as measured by the

Consumer Price Index which had a CAGR of 2.4% annually

over the same period. From 2000 to 2011, the maximum 12-

month price increase was 18% for pine woodchips versus

50% for corn, 46% for sugar and 51% for West Texas

Intermediate crude according to average quarterly data from

Timber Mart-South, the USDA and the EIA.

Million barrels/day

0

100

200

300

400

500

600

700

800

UnitedStates

EuropeanUnion

China India Middle East

2010 2035

Commodity Food Price Index vs. CPI2

Million barrels/day

Relative Prices of Wood, Sugar, Soy Oil,

Corn, Nat Gas and Crude Oil Since 20003

0

50

100

150

200

250

300

350

400

450

500

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Ind

ex

(Q

1 2

00

0=

10

0)

World raw sugar (No.11, spot) Corn (No.2 yellow, Chicago spot)

US Nat Gas Industrial Price WTI Crude (Spot, FOB Cushing, OK)

Pine Pulpwood (Delivered AL)

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

Commodity Food Price Index CPI

TABLE OF CONTENTS

Drivers of Biofuels/Biochemicals Growth (con’t)

While in the near term proven

reserves are expected to increase

with new exploration efforts and

technological developments that

increase certainty of quantity, in the

long term, new sources of energy

must be discovered to satisfy global

energy demands.

Lifecycle GHG emissions are the

aggregate quantity of GHGs related

to the full fuel cycle, including all

stages of fuel and feedstock

production and distribution, from

feedstock generation and extraction

through distribution and delivery and

use of the finished fuel. The lifecycle

GHG emissions of the renewable fuel

are compared to the lifecycle GHG

emissions for gasoline or diesel.

The Biofuels and Biochem Industry 31

Source: 1BP Website, 2EPA.

Note: GHG - Greenhouse Gas.

Biofuels in Transportation1

Petroleum is a finite resource and

substitutes must be found: Petroleum is

naturally formed by the anaerobic decay of

organic matter in the presence of intense heat

and pressure which is thought to occur over

hundreds of thousands or even millions of

years. With such a long formation cycle, the

earth is not capable of regenerating its

reserves of oil at the same rate to which

humanity draws upon them for energy use.

Biofuel Lifecycle GHG Impact Relative to Gasoline2

Environmental concerns, particularly with

regard to global warming driving adoption

of “cleaner and greener” alternatives: The

EIA projects that CO2 emissions from the

combustion of liquid fuels will grow by ~28%

from 2007 to 2035. China is the largest

contributor to the rising pollution levels with

CO2 emissions growth estimated to be 2.9%

annually driven by its rapidly expanding

demand for liquid fuels in its industrial and

transportation sectors. The U.S., however, is

expected to remain the world’s largest polluter

with ~2.6 billion metric tons of emission in

2035. A wider push to renewable fuel sources

is viewed as a major step towards reversing

the pattern of global warming.

100%105%

82%

134%

82% 74%104%

20%

74%

-24% -16%

-40.0%

0.0%

40.0%

80.0%

120.0%

160.0%

Gaso

line

Co

rn E

thanol(N

at. g

as d

ry

mill)

Co

rn E

thanol(B

est C

ase

Nat.g

as d

ry m

ill)

Co

rn E

thanol (

Coal d

ry

mill)

Co

rn E

thanol (

Bio

mass D

ry

Mill)

Co

rn E

thanol (

Bio

mass D

ry

Mill w

ith

CH

P)

So

y-b

ased B

iodie

sel

Waste

Gre

ase B

iodie

sel

Sug

arc

an

e E

thanol

Sw

itch

gra

ss E

thanol

Co

rn S

tover E

thanol

2010 2035

Other fuels:

91.0% Other fuels:

97.3%

Biofuels: 2.7% Biofuels: 9.0%

TABLE OF CONTENTS

Master Layout:

Call Out Text Left, Table Right

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

4000.0

4500.0

5000.0

1990 1995 2000 2005 2010 2015 2020 2025 2030

North America South & Central America Europe & Eurasia Middle East Africa Asia Pacific

Liquid Demand Statistics

Total Liquids Consumption by Region1 Liquids demand growth from non-

OECD countries will be met by

supply growth from OPEC and the

Americas

Liquids demand growth is driven by

non-OECD transport while OECD

demand falls across all sectors

Overall consumption growth will be

constrained by stronger crude oil

prices seen in recent years,

technological advances, a range of

new policies, and the continued,

gradual reduction of non-OECD

subsidies

The Biofuels and Biochem Industry 32

Source: 1BP Energy Outlook 2030: January 2012.

Note: OECD- Organization for Economic Co-operation and Development.

Note: Litre: Gallon = 1:0.26; Gallon: Barrel = 1: 0.0322; Tonne of Oil Equivalent (toe): Barrel of Oil Equivalent (boe) = 1: 7.4.

3,148 3,271 3,571 3,908 4,028 4,166 4,378 4,562 4,719 Total Liquids

Consumption

(MTOE)

Million tones of oil equivalent

(MTOE)

7.1

153.2

9.2

90.0

8.5

116.8

19.9 59.3

188.0 of which

biofuels

TABLE OF CONTENTS

Master Layout:

Call Out Text Left, Table Right

Liquid Supply Statistics

Total Liquids Production by Region1 Rising supply to meet expected

demand growth should come

primarily from OPEC, where output is

projected to rise by nearly 12 Mb/d.

The largest increments of new OPEC

supply will come from NGLs2, as well

as conventional crude in Iraq and

Saudi Arabia

OPEC’s critical position in the oil

market grows while the Americas

also play an expanding role

Non-OPEC supply will continue to

rise, growing by 5 Mb/d, due to

strong growth in the Americas from

U.S. and Brazilian biofuels, Canadian

oil sands, Brazilian deepwater, and

U.S. shale oil, offsetting continued

declines in a number of mature

provinces

The Biofuels and Biochem Industry 33

Source: 1BP Energy Outlook 2030: January 2012, 2Natural Gas Liquids.

Note: OPEC- Organization of the Petroleum Exporting Countries. Mb/d – Million Barrels per Day.

Note: Litre: Gallon = 1:0.26; Gallon: Barrel = 1: 0.0322; Tonne of Oil Equivalent (toe): Barrel of Oil Equivalent (boe) = 1: 7.4.

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

4000.0

4500.0

5000.0

1990 1995 2000 2005 2010 2015 2020 2025 2030

North America South & Central America Europe & Eurasia Middle East Africa Asia Pacific

3,172 3,284 3,612 3,907 3,914 4,089 4,263 4,398 4,512 Total Oil

Production

(MTOE)

Million tones of oil equivalent

(MTOE)

7.1

153.2

9.2

90.0

8.5

116.8

19.9 59.3

188.0 of which

biofuels

TABLE OF CONTENTS

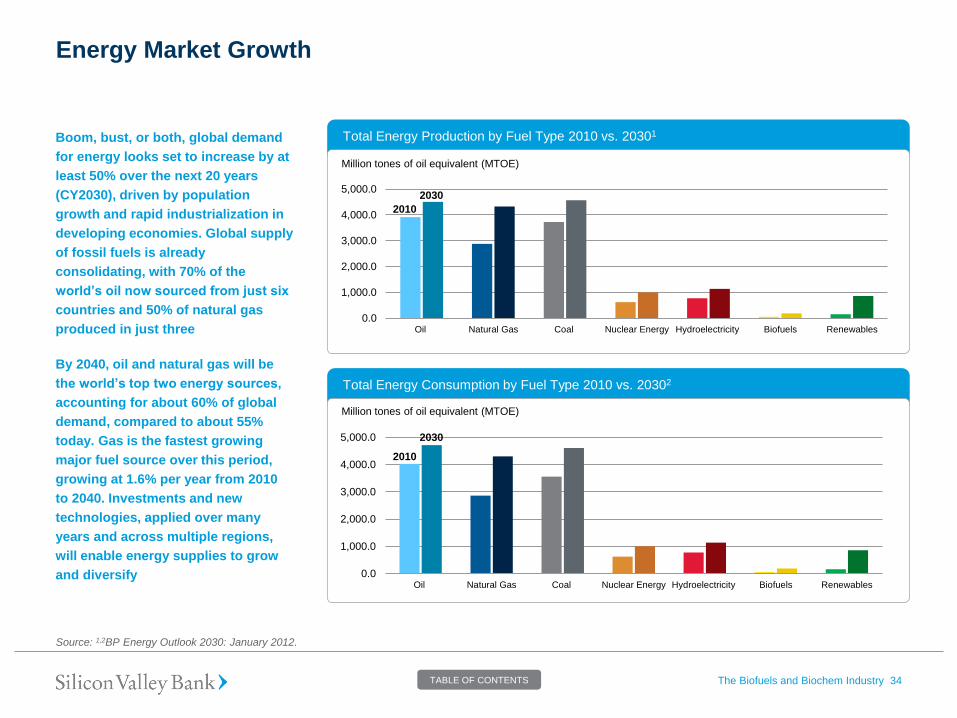

Energy Market Growth

Boom, bust, or both, global demand

for energy looks set to increase by at

least 50% over the next 20 years

(CY2030), driven by population

growth and rapid industrialization in

developing economies. Global supply

of fossil fuels is already

consolidating, with 70% of the

world’s oil now sourced from just six

countries and 50% of natural gas

produced in just three

By 2040, oil and natural gas will be

the world’s top two energy sources,

accounting for about 60% of global

demand, compared to about 55%

today. Gas is the fastest growing

major fuel source over this period,

growing at 1.6% per year from 2010

to 2040. Investments and new

technologies, applied over many

years and across multiple regions,

will enable energy supplies to grow

and diversify

The Biofuels and Biochem Industry 34

Source: 1,2BP Energy Outlook 2030: January 2012.

Total Energy Production by Fuel Type 2010 vs. 20301

Total Energy Consumption by Fuel Type 2010 vs. 20302

Million tones of oil equivalent (MTOE)

Million tones of oil equivalent (MTOE)

0.0

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

Oil Natural Gas Coal Nuclear Energy Hydroelectricity Biofuels Renewables

0.0

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

Oil Natural Gas Coal Nuclear Energy Hydroelectricity Biofuels Renewables

2010

2030

2010

2030

TABLE OF CONTENTS

Energy Market Growth (con’t)

The Biofuels and Biochem Industry 35

Source: 1,3BP Energy Outlook 2030: January 2012, 2World Energy Outlook 2011.

Note: Litre: Gallon = 1:0.26; Gallon: Barrel = 1: 0.0322; Tonne of Oil Equivalent (toe): Barrel of Oil Equivalent (boe) = 1: 7.4.

Total Energy Consumption by Region1 Shares of Energy Sources in World Primary Energy Demand2

0.0

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

30,000.0

OECD Non-OECD European Union Europe Former Soviet Union US China

Total Growth of Energy Consumption to 20303

Million tones of oil equivalent (MTOE)

Total energy consumption will increase from 12,002.4 mtoe in 2010 to 16,631.6 MTOE

in 2030. Global energy demand is expected to increase by one-third from 2010 to 2035,

with China & India accounting for 50% of the growth

0%

10%

20%

30%

40%

50%

Oil Coal Gas

Biomass & waste Nuclear Other Renewables

Hydro

Total Growth of Energy Consumption to 20303

0.0

0.5

1.0

1.5

2.0

2.5

Transport Industry Other

Coal Oil Biofuels Gas Electricity

-0.5

0.0

0.5

1.0

1.5

2.0

Transport Industry Other

China & India OECD Middle East ROW

Billion tones of oil

equivalent (BTOE)

Billion tones of oil

equivalent (BTOE) Final Energy Use Final Energy Use By Sector & Region By Sector & Fuel

TABLE OF CONTENTS

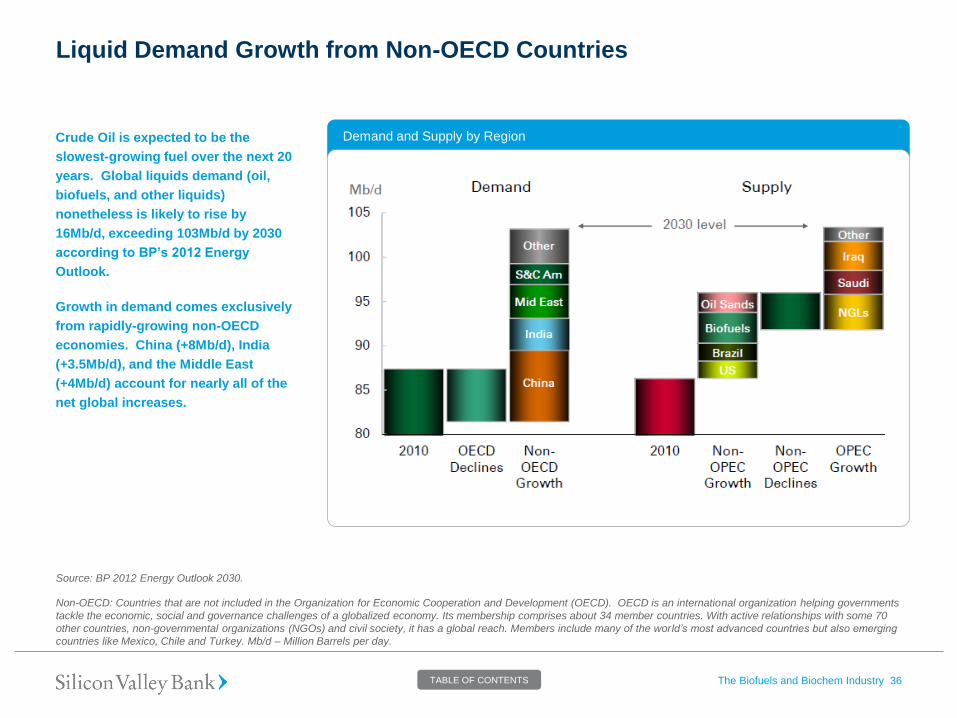

Liquid Demand Growth from Non-OECD Countries

Crude Oil is expected to be the

slowest-growing fuel over the next 20

years. Global liquids demand (oil,

biofuels, and other liquids)

nonetheless is likely to rise by

16Mb/d, exceeding 103Mb/d by 2030

according to BP’s 2012 Energy

Outlook.

Growth in demand comes exclusively

from rapidly-growing non-OECD

economies. China (+8Mb/d), India

(+3.5Mb/d), and the Middle East

(+4Mb/d) account for nearly all of the

net global increases.

The Biofuels and Biochem Industry 36

Source: BP 2012 Energy Outlook 2030.

Non-OECD: Countries that are not included in the Organization for Economic Cooperation and Development (OECD). OECD is an international organization helping governments

tackle the economic, social and governance challenges of a globalized economy. Its membership comprises about 34 member countries. With active relationships with some 70

other countries, non-governmental organizations (NGOs) and civil society, it has a global reach. Members include many of the world’s most advanced countries but also emerging

countries like Mexico, Chile and Turkey. Mb/d – Million Barrels per day.

Demand and Supply by Region

TABLE OF CONTENTS

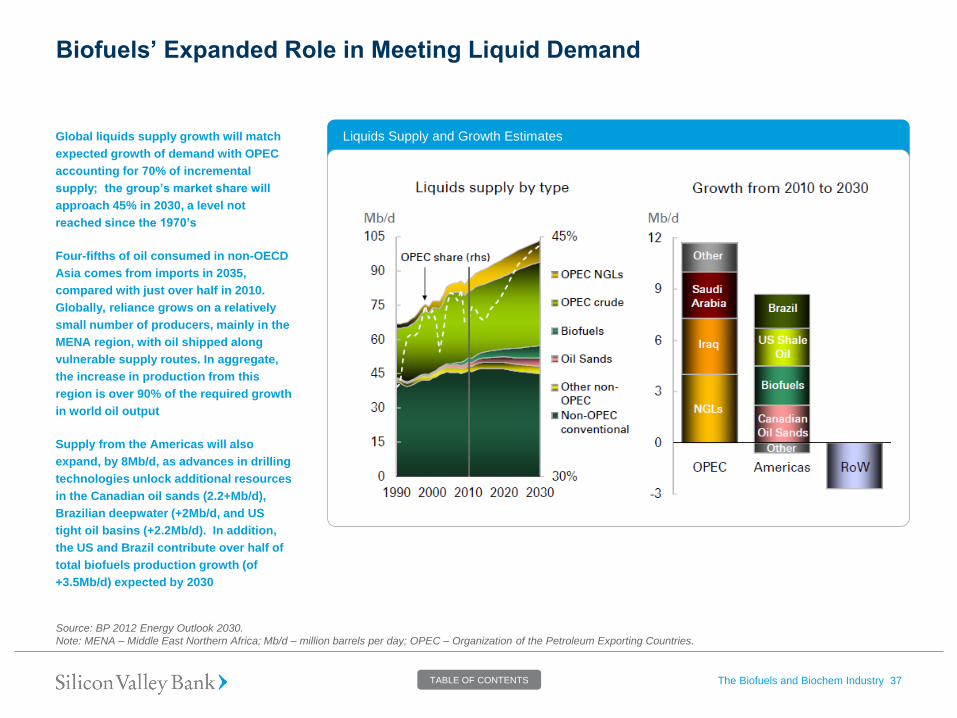

Biofuels’ Expanded Role in Meeting Liquid Demand

Global liquids supply growth will match

expected growth of demand with OPEC

accounting for 70% of incremental

supply; the group’s market share will

approach 45% in 2030, a level not

reached since the 1970’s

Four-fifths of oil consumed in non-OECD

Asia comes from imports in 2035,

compared with just over half in 2010.

Globally, reliance grows on a relatively

small number of producers, mainly in the

MENA region, with oil shipped along

vulnerable supply routes. In aggregate,

the increase in production from this

region is over 90% of the required growth

in world oil output

Supply from the Americas will also

expand, by 8Mb/d, as advances in drilling

technologies unlock additional resources

in the Canadian oil sands (2.2+Mb/d),

Brazilian deepwater (+2Mb/d, and US

tight oil basins (+2.2Mb/d). In addition,

the US and Brazil contribute over half of

total biofuels production growth (of

+3.5Mb/d) expected by 2030

The Biofuels and Biochem Industry 37

Source: BP 2012 Energy Outlook 2030.

Note: MENA – Middle East Northern Africa; Mb/d – million barrels per day; OPEC – Organization of the Petroleum Exporting Countries.

Liquids Supply and Growth Estimates

TABLE OF CONTENTS

Biofuels for Transportation

• Demand for liquid transport fuels is expected to increase by 2 million

barrels per day over the next two decades and nearly 40% of the growth

will be supplied by biofuels, the first time that non-fossil fuels will be the

major source of supply growth.

• Liquid biofuels make a small but growing contribution to fuel usage

worldwide.

— Provided about 2.7% of global road transport fuels in 2010

— Accounted for higher shares in some countries (e.g., 4% in the U.S.)

and regions (3% in the EU) and provided a very large contribution in

Brazil, where ethanol from sugar cane accounted for 41.5% of light

duty transport fuel during 2010

• The U.S. was the world’s largest producer of biofuels, followed by Brazil

and the EU. Despite continued increases in production, growth rates for

biodiesel slowed again in 2010, whereas ethanol production growth

picked up new momentum.

• In 2010, global production of fuel ethanol reached an estimated 86 billion liters, an increase of 17% over 2009

— The U.S. and Brazil accounted for 88% of ethanol production in 2010, with the U.S. alone producing 57% of the world’s total

— Long the world’s leading ethanol exporter, Brazil continued to lose international market share to the U.S, particularly in its traditional markets in Europe

— Adverse weather conditions hampered global harvesting of sugar cane, pushing up prices. As a result, U.S. corn-based ethanol became relatively

cheaper in international markets (although it was subsidized, unlike Brazilian ethanol)

• Global biodiesel production increased 7.5% in 2010, to nearly 19 billion liters, a five-year average (end-2005 through 2010) growth of 38%

— Biodiesel production is far less concentrated than ethanol, with the top 10 countries accounting for just under 75% of total production in 2010

— Germany remains the world’s top biodiesel producer at 2.9 billion liters in 2010, followed by Brazil, Argentina, France, and the U.S.

— The EU remained the center of biodiesel production, but due to increased competition with relatively cheap imports, growth in the region continued to

slow. The diversity of players in the advanced biofuels industry continued to increase with the participation of young, rapidly growing firms, major

aviation companies, and traditional oil companies

The Biofuels and Biochem Industry 38

Ethanol and Biodiesel Production, 2000–20101

17.0 19.0

21.0

24.0 29.0 31.0

39.0

52.0

66.0 73.0

86.0

0.8 1.0 1.4 1.9 2.4 3.7 6.6

11.0

16.0

17.0

19.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Ethanol Biodiesel

Billion liters

World ethanol production for transport fuel tripled between 2000 and 2007 from 17

billion liters to more than 52 billion liters, while biodiesel expanded eleven-fold

from less than 1 billion liters to almost 11 billion liters

Source: 1F.O. Licht (world-renowned renewable fuels research agency).

Note: Litre: Gallon = 1:0.26; Gallon: Barrel = 1: 0.0322; Tonne of Oil Equivalent (toe): Barrel of Oil Equivalent (boe) = 1: 7.4.

TABLE OF CONTENTS

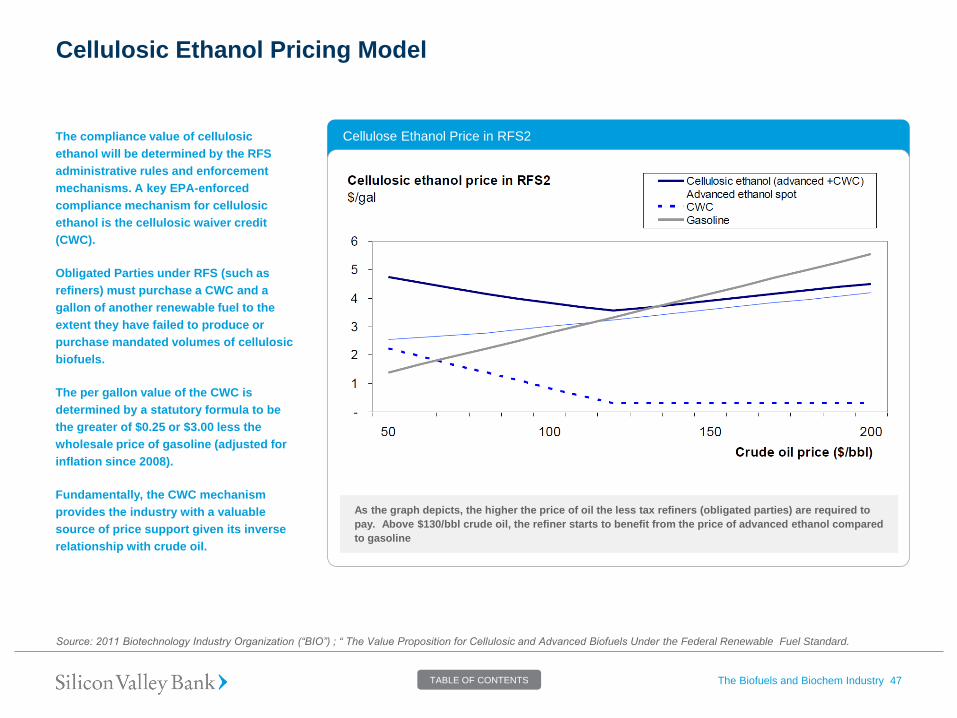

Increasing Marginal Cost of Production

Advanced biofuel and chemical