1

Teva Investor & Analyst Meeting Shlomo YanaiPresident and CEOFebruary 18th, 2009

President and CEO

Forward Looking Statements

TODAY’S PRESENTATION CONTAINS FORWARD-LOOKING STATEMENTS, WHICH EXPRESS THE CURRENT BELIEFS AND EXPECTATIONSOF MANAGEMENT. SUCH STATEMENTS ARE BASED ON MANAGEMENT'S CURRENT BELIEFS AND EXPECTATIONS AND INVOLVE ANUMBER OF KNOWN AND UNKNOWN RISKS AND UNCERTAINTIES THAT COULD CAUSE OUR FUTURE RESULTS, PERFORMANCE ORACHIEVEMENTS TO DIFFER SIGNIFICANTLY FROM THE RESULTS, PERFORMANCE OR ACHIEVEMENTS EXPRESSED OR IMPLIED BY SUCHFORWARD-LOOKING STATEMENTS. IMPORTANT FACTORS THAT COULD CAUSE OR CONTRIBUTE TO SUCH DIFFERENCES INCLUDE RISKSRELATING TO: OUR ABILITY TO SUCCESSFULLY DEVELOP AND COMMERCIALIZE ADDITIONAL PHARMACEUTICAL PRODUCTS, THEINTRODUCTION OF COMPETING GENERIC EQUIVALENTS, THE EXTENT TO WHICH WE MAY OBTAIN U.S. MARKET EXCLUSIVITY FORCERTAIN OF OUR NEW GENERIC PRODUCTS AND REGULATORY CHANGES THAT MAY PREVENT US FROM UTILIZING EXCLUSIVITYCERTAIN OF OUR NEW GENERIC PRODUCTS AND REGULATORY CHANGES THAT MAY PREVENT US FROM UTILIZING EXCLUSIVITYPERIODS, COMPETITION FROM BRAND-NAME COMPANIES THAT ARE UNDER INCREASED PRESSURE TO COUNTER GENERIC PRODUCTS,OR COMPETITORS THAT SEEK TO DELAY THE INTRODUCTION OF GENERIC PRODUCTS, THE IMPACT OF CONSOLIDATION OF OURDISTRIBUTORS AND CUSTOMERS, POTENTIAL LIABILITY FOR SALES OF GENERIC PRODUCTS PRIOR TO A FINAL RESOLUTION OFOUTSTANDING PATENT LITIGATION, INCLUDING THAT RELATING TO THE GENERIC VERSIONS OF NEURONTIN®, LOTREL® ANDPROTONIX®, THE EFFECTS OF COMPETITION ON OUR INNOVATIVE PRODUCTS, ESPECIALLY COPAXONE® SALES, THE IMPACT OFPHARMACEUTICAL INDUSTRY REGULATION AND PENDING LEGISLATION THAT COULD AFFECT THE PHARMACEUTICAL INDUSTRY THEPHARMACEUTICAL INDUSTRY REGULATION AND PENDING LEGISLATION THAT COULD AFFECT THE PHARMACEUTICAL INDUSTRY, THEDIFFICULTY OF PREDICTING U.S. FOOD AND DRUG ADMINISTRATION, EUROPEAN MEDICINES AGENCY AND OTHER REGULATORYAUTHORITY APPROVALS, THE REGULATORY ENVIRONMENT AND CHANGES IN THE HEALTH POLICIES AND STRUCTURES OF VARIOUSCOUNTRIES, OUR ABILITY TO ACHIEVE EXPECTED RESULTS THOUGH OUR INNOVATIVE R&D EFFORTS, OUR ABILITY TO SUCCESSFULLYIDENTIFY, CONSUMMATE AND INTEGRATE ACQUISITIONS, INCLUDING THE INTEGRATION OF BARR PHARMACEUTICALS INC., POTENTIALEXPOSURE TO PRODUCT LIABILITY CLAIMS TO THE EXTENT NOT COVERED BY INSURANCE, DEPENDENCE ON THE EFFECTIVENESS OFOUR PATENTS AND OTHER PROTECTIONS FOR INNOVATIVE PRODUCTS SIGNIFICANT OPERATIONS WORLDWIDE THAT MAY BEOUR PATENTS AND OTHER PROTECTIONS FOR INNOVATIVE PRODUCTS, SIGNIFICANT OPERATIONS WORLDWIDE THAT MAY BEADVERSELY AFFECTED BY TERRORISM, POLITICAL OR ECONOMICAL INSTABILITY OR MAJOR HOSTILITIES, SUPPLY INTERRUPTIONS ORDELAYS THAT COULD RESULT FROM THE COMPLEX MANUFACTURING OF OUR PRODUCTS AND OUR GLOBAL SUPPLY CHAIN,ENVIRONMENTAL RISKS, FLUCTUATIONS IN CURRENCY, EXCHANGE AND INTEREST RATES, AND OTHER FACTORS THAT ARE DISCUSSEDIN THIS REPORT AND IN OUR OTHER FILINGS WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION ("SEC").

2

3

2008 at a glance2008 at a glance

The future of generics

Biogenerics

Outlook

42008 2008 –– An Extraordinary YearAn Extraordinary YearStrong Financial ResultsStrong Financial Results

1111 085085Sales 99 408408

2007 2008* Change

++1818%%1111,,085085Sales$m

99,,408408 ++1818%%

Net income$m

22,,37437411,,952952 ++2222%%$m

EPS$

22..868622..3838 ++2020%%

* Net income and EPS are non-GAAP results

52008 2008 –– An Extraordinary YearAn Extraordinary Year

Record FinancialResults

Record sales, net income & EPSRecord cash flow from operations: $3.2bnRecord free cash flow: $2.2bn

20082008: an extraordinary year: an extraordinary yearExtending Global Leadership

US: Increased market share International: Exceptional growthEurope: Improved market position in key countriesLeadership Europe: Improved market position in key countries

GrowingPortfolio

US: 28 new launches; 8 Para IV launchesEurope: Record number of generic submissionsPortfolio Europe: Record number of generic submissions

Copaxone® Global #1R d I k t l $2 3bp Record In-market sales: $2.3bn

Azilect® Positive results of ADAGIO and Tyramine studiesAzilect® yRecord in-market sales: $175m

62008 2008 –– An Extraordinary YearAn Extraordinary Year

M j B i itiMajorStrategic Achievements

Barr acquisitionSpain: Bentley acquisitionJapan: Strategic alliance with Kowa

BiogenericsLonza joint ventureCoGenesys acquisitiong y qTevagrastim: 1st Biosimilar launched in EU

7

2008 at a glance

The future of generics The future of generics

Biogenerics

Outlook

8World Population Growing And AgingWorld Population Growing And Aging

World population by age bracket in billionsWorld population by age bracket in billions

9.1

1.9

6.5

1.4

2.3 0.7 60+

40 to 59

2.0 2.5 20 to 39

2.4 2.4

2005 2050

0 to 19

2005 2050

Source: UN, World Population Prospects: The 2002 Revision; World Urbanization Prospects: The 2006 Revision

9Healthcare Spending Growing Healthcare Spending Growing FasterFaster Than GDPThan GDP

Healthcare spending as % of GDP, U.S. example

Source: NCHC; OECD

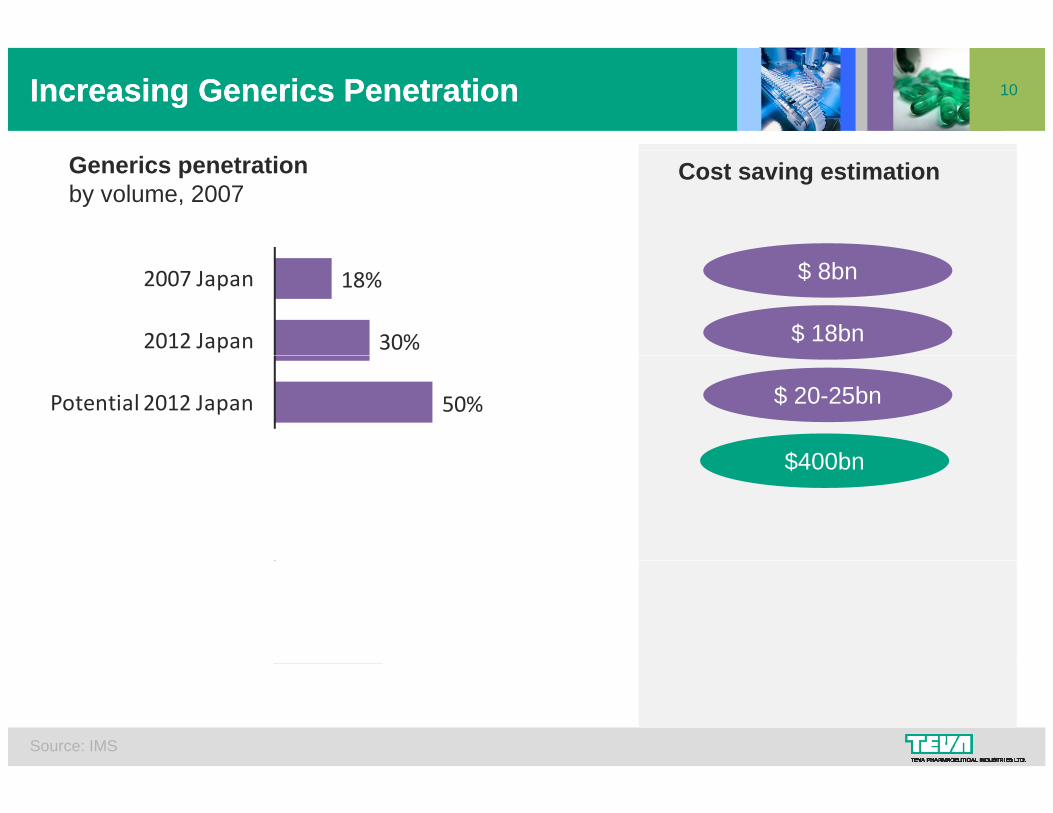

10Increasing Generics PenetrationIncreasing Generics Penetration

Generics penetrationby volume, 2007

Cost saving estimation

18%

30%

2007 Japan

2012 Japan

$ 8bn

$ 18bn

50%Potential 2012 Japan

US

$ 20-25bn

$400bn68%

65%

US

UK

$400bn

54%

34%

Germany

Spain

Source: IMS

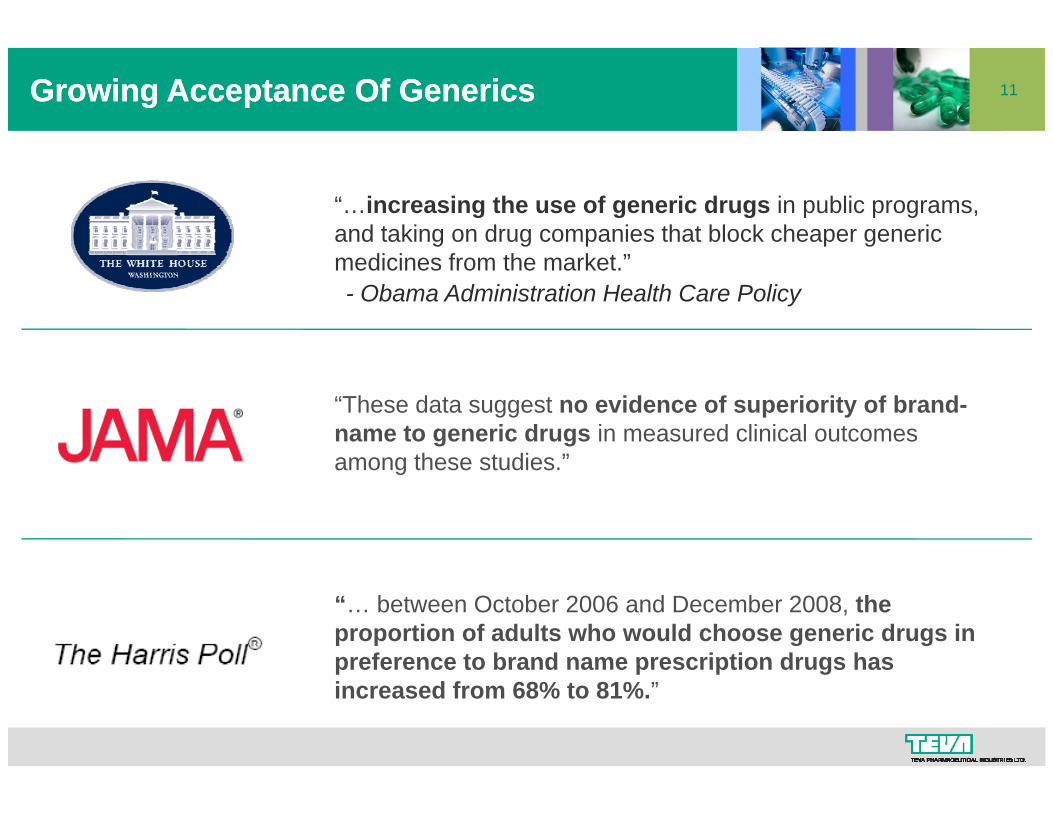

11Growing Acceptance Of GenericsGrowing Acceptance Of Generics

“…increasing the use of generic drugs in public programs,and taking on drug companies that block cheaper generic medicines from the market.”

Q a

- Obama Administration Health Care Policy

“These data suggest no evidence of superiority of brand-name to generic drugs in measured clinical outcomes among these studies ”among these studies.”

“… between October 2006 and December 2008, the proportion of adults who would choose generic drugs in preference to brand name prescription drugs haspreference to brand name prescription drugs has increased from 68% to 81%.”

12Generics Growth Driven By Patent ExpirationsGenerics Growth Driven By Patent Expirations

Sales by patent expiration $ bnSales by patent expiration, $ bn

121121

288

114

288

53

2007 ‐ 2009 2010 ‐ 2012 2013 ‐ 2015 Total

SOURCE 2008-2012: IMS Health, MIDAS, MAT Jun 2008; IMS Therapy Forecaster, Jun 2008; IMS Market Insights Oct 2008Source 2013-2015 Company estimates (including Biologics)

13

2008 at a glance

The future of generics

BiogenericsBiogenerics

Outlook

14BiogenericsBiogenerics –– The OpportunityThe Opportunity

World-wide sales of biologics by patent expiration year, $bn

20

9 59

8

17

1 1 2 1 8

2008 2009 2010 2011 2012 2013 2014 2015 Total

1 3 4 2 3 9 7 4516Number ofmolecules

Source: Mckinsey

15Biogenerics: Barriers to EntryBiogenerics: Barriers to Entry

Technology barriers –development and production

Unclear regulatory path andt k t d lgo-to-market model

High cost and capital intensive

16Biogenerics Biogenerics –– Teva’s VisionTeva’s Vision

Provide biopharmaceuticalsth tGenerics that are:- safe- effective

Generics Value

Proposition- affordableProposition

Become theMarket global leaderin biogenerics

Market Leadership

17Teva And LonzaTeva And LonzaHighly Complementary CapabilitiesHighly Complementary Capabilities

Global leaderFinancial strength

Best in class in biologics development

Outstanding clinical, IP

and manufacturing

Existing high-level g ,and RA capabilities

g ginfrastructure

Expertise in many go-to market models

Unmatched know-how and experience

18TevaTeva and and LonzaLonzaHighly Complementary CapabilitiesHighly Complementary Capabilities

Benefits

Global leaderStrong financial poistion

Best in class in biologics development and

•Shorten time to marketpoistion

Outstanding li i l IP d RA

development and manufacturing

Existing high-level i f

market

•Lowerclinical, IP and RA capabilities

infrastructure Lower investment & development cost

Expertise in many go-to market models

Unmatched know-how and experience

•Multiple marketing platforms

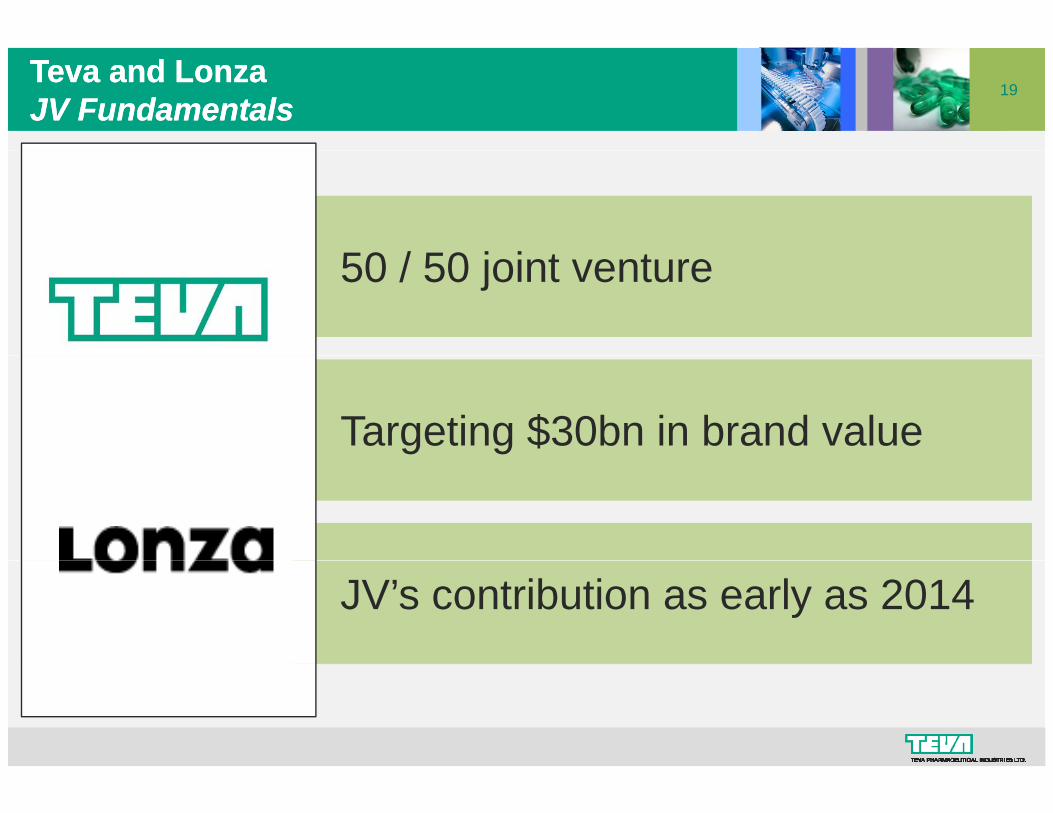

19Teva and LonzaTeva and LonzaJV Fundamentals JV Fundamentals

50 / 50 j i t t50 / 50 joint venture

Targeting $30bn in brand value

JV’s contribution as early as 2014

20

2008 at a glance

The future of generics

Biogenerics

OutlookOutlook

21Barr IntegrationBarr Integration

Cost Over $400m vs. initial estimateSynergies of $300M

Accretion Q3 2009 vs. initial estimateof Q4 2009of Q4 2009

Financial Strength

Financial leverage to return to pre-Barr level in 1 year

22OutlookOutlook

Sales $14 1bn $14 6bn2009 Sales $14.1bn - $14.6bn

EPS* $3.20 - $3.40

*Non-GAAP

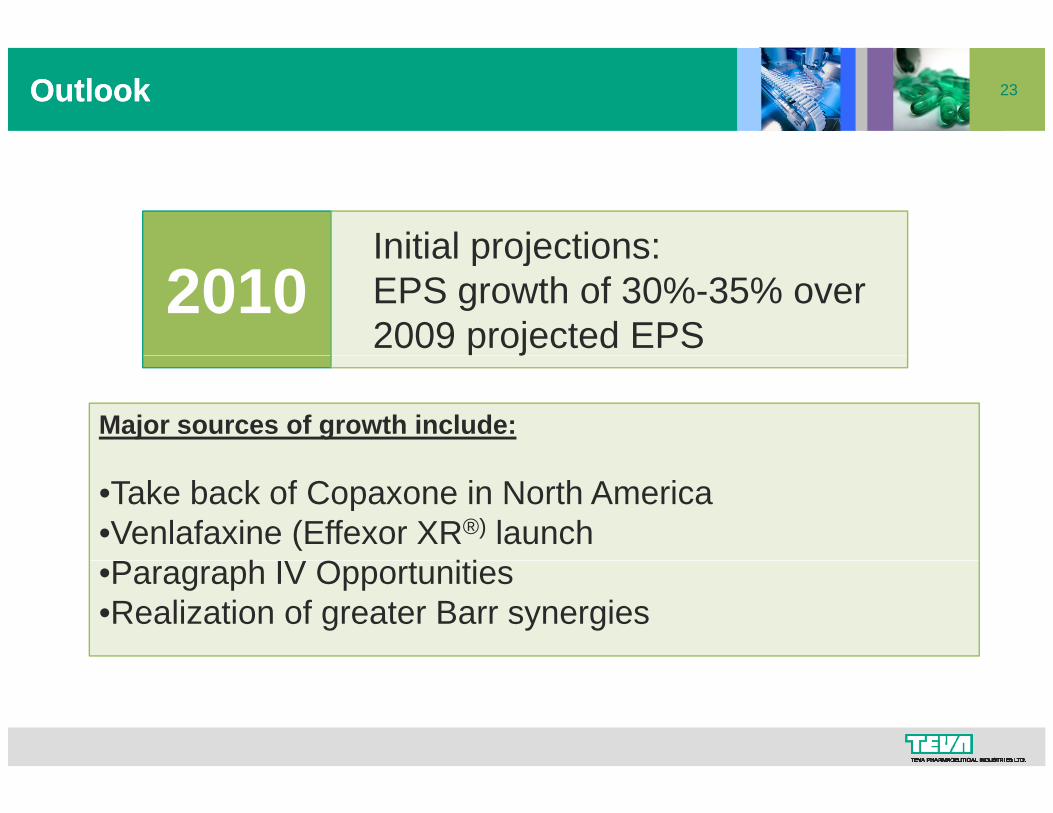

23OutlookOutlook

Initial projections:2010

Initial projections:EPS growth of 30%-35% over 2009 projected EPSj

Major sources of growth include:

•Take back of Copaxone in North America•Venlafaxine (Effexor XR®) launchP h IV O i i•Paragraph IV Opportunities

•Realization of greater Barr synergies

24

Teva Investor & Analyst Meeting Bill MarthPresident and CEO Teva North AmericaFebruary 18th, 2009

President and CEO, Teva North America

25Leadership in U.S. generics% of total Rx’s full year generics only 2008

59823.8 24.0 Teva

% of total Rx s, full year, generics only 20082007Rx’s

thousand

307

223

12.2

8.9

11.9

9.4

Mylan

Watson

189

95

7.5

3.8

8.2

3.9

Sandoz

Mallinckrodt

93

90

3.7

3.6

2.6

3.5

Apotex

Qualitest

~1 6 million Rx’s per day~1 6 million Rx’s per day

78

823.3

3.1

3 1

3.4

3.6

Greenstone

Actavis

~1.6 million Rx s per day

50% more than #2

~1.6 million Rx s per day

50% more than #2

613.1 1.3 Lupin

Source: IMS National Prescription Audit MAT December 2008

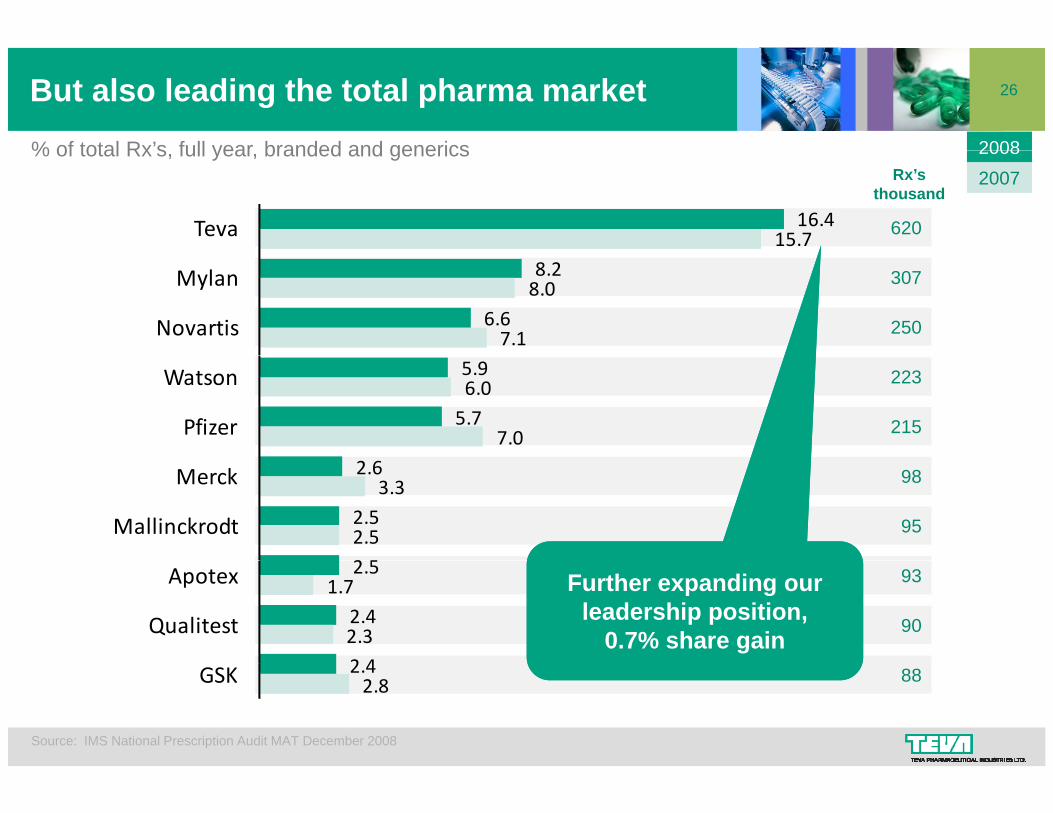

26But also leading the total pharma market% of total Rx’s full year branded and generics 2008

620

% of total Rx s, full year, branded and generics

16.4 15.7 Teva

20082007Rx’s

thousand

307

250

8.2

6.6 8.0

7.1

Mylan

Novartis

223

215

5.9

5.7 6.0

7.0

Watson

Pfizer

98

95

2.6

2.5

2 5

3.3

2.5

Merck

Mallinckrodt

90

932.5

2.4

2 4

1.7

2.3

Apotex

Qualitest

Further expanding our leadership position,

0.7% share gain

Further expanding our leadership position,

0.7% share gain882.4

2.8 GSK

Source: IMS National Prescription Audit MAT December 2008

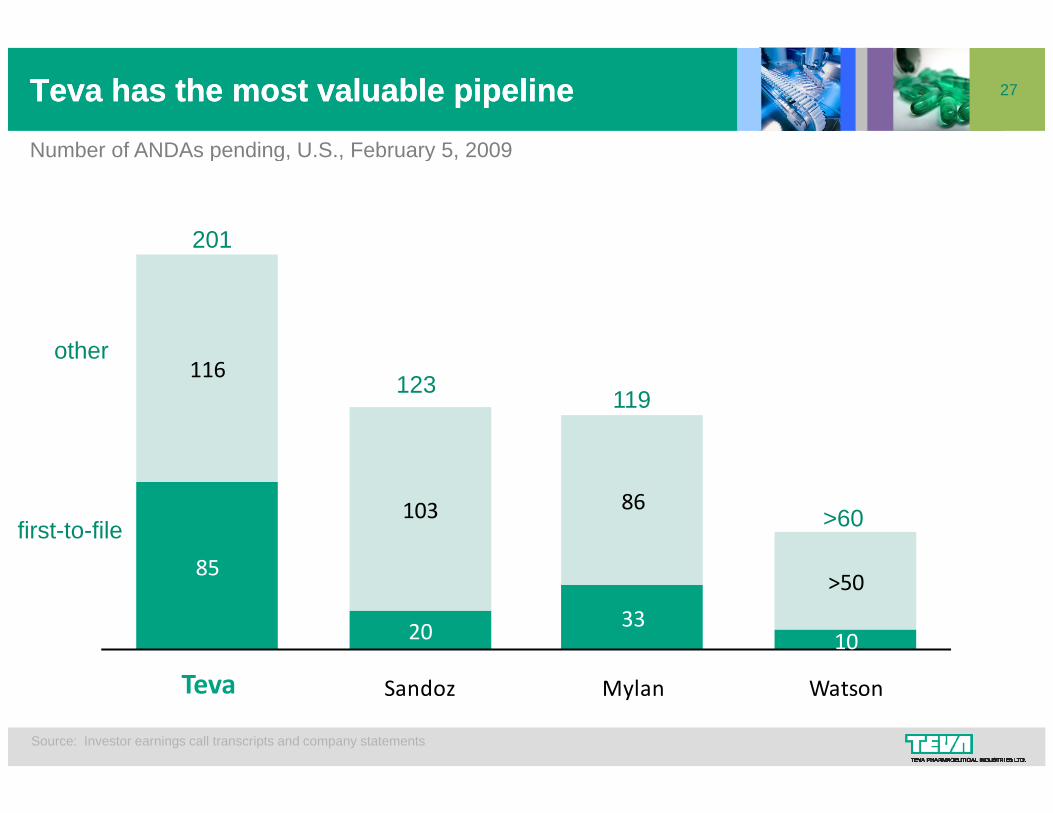

27TevaTeva has the most valuable pipelinehas the most valuable pipeline

Number of ANDAs pending U S February 5 2009Number of ANDAs pending, U.S., February 5, 2009

201

other116

other123 119

85

103 86first-to-file >60

85

20 3310

>50

Teva + Barr Sandoz Mylan Watson

Source: Investor earnings call transcripts and company statements

Teva

28

Market coverage of Teva development pipeline

Large market coverage of pipelineLarge market coverage of pipeline

$290bn

Market coverage of Teva development pipeline

40% - $116bnOpportunity

22% - $64bnTeva in development1 in 4 products in

development have not22% - $64bnTeva – in development development have not established market yet

60%

38% - $110 bnTeva - pending approval

2008 U.S. pharma market

Source: IMS, Teva estimates

29U.S. Generic Launches U.S. Generic Launches –– 2008 2008 and and 20092009

2008 - Launched 28 products with brand value of $12.5 billion

Total potential launches in 2009 – Approximately 40Total potential launches in 2009 Approximately 40 potential launches representing brand value greater than $32 billion

2009 potential brand value represents 30% of Teva’s U S generic filed pipelineU.S. generic filed pipeline

30Broadest product portfolioBroadest product portfolio

Number of productsNumber of products

+90%

Source: Investor earnings call transcripts and company statements

31The legislative landscapeThe legislative landscape

2009 - a new administration,a foc s on healthcare reforma focus on healthcare reform

Impact of increased role of government as payer of Rx drugs will influence policymakingpayer of Rx drugs will influence policymaking

25th anniversary of Hatch-Waxman –legislation that saved consumers billions oflegislation, that saved consumers billions of dollars

Biogenerics legislation will open the market toBiogenerics legislation will open the market to competition, creating savings especially important in current economic climate

32Biologics in the U.S.Biologics in the U.S.

Broad agreement that the regulatory pathway

STATUS OF ISSUES

g g y p yshould be:- science driven- led by FDATop of legislative agenda - without unnecessary delays

Need for a process to resolve patent disputes, Teva wants a streamlined process

in 2009 – 2010

Strong consensus for generic biologics Teva wants a streamlined process

Exclusivity remains a focal point of debate,Teva supports a period that makes sense for

generic biologicsamong payers, consumer groups

pp pconsumers, and encourages a healthy/competitive market

33Broader government affairs issuesBroader government affairs issues

Patent settlements

Drug quality and foreign inspections

FDA Funding

Patent reform

34

Teva Investor & Analyst Meeting Eyal DeshehCFOFebruary 18th, 2009

CFO

35

All figures $bn except EPS $

A very good yearA very good year

2 7

Sales Gross profit Operatingprofit Net income EPS

All figures $bn, except EPS, $

+18% +22% +13% +20% +20%

2.32.4

2.7

2006 2007 2008

* Operating income, Net income and EPS are non GAAP results for 2006 and 2008

36Global business Global business –– 1010X in X in 10 10 years years

$11.1 bn$9.4 bn

4% 4%

100% = $1.1 bn $11.1 bn$9.4 bn

Israel

International28% 27%

6%

10% 11%22%

4% 4%

Europe 26%

28% 27%

North America 46%58% 58%

46%

1998 2007 2008

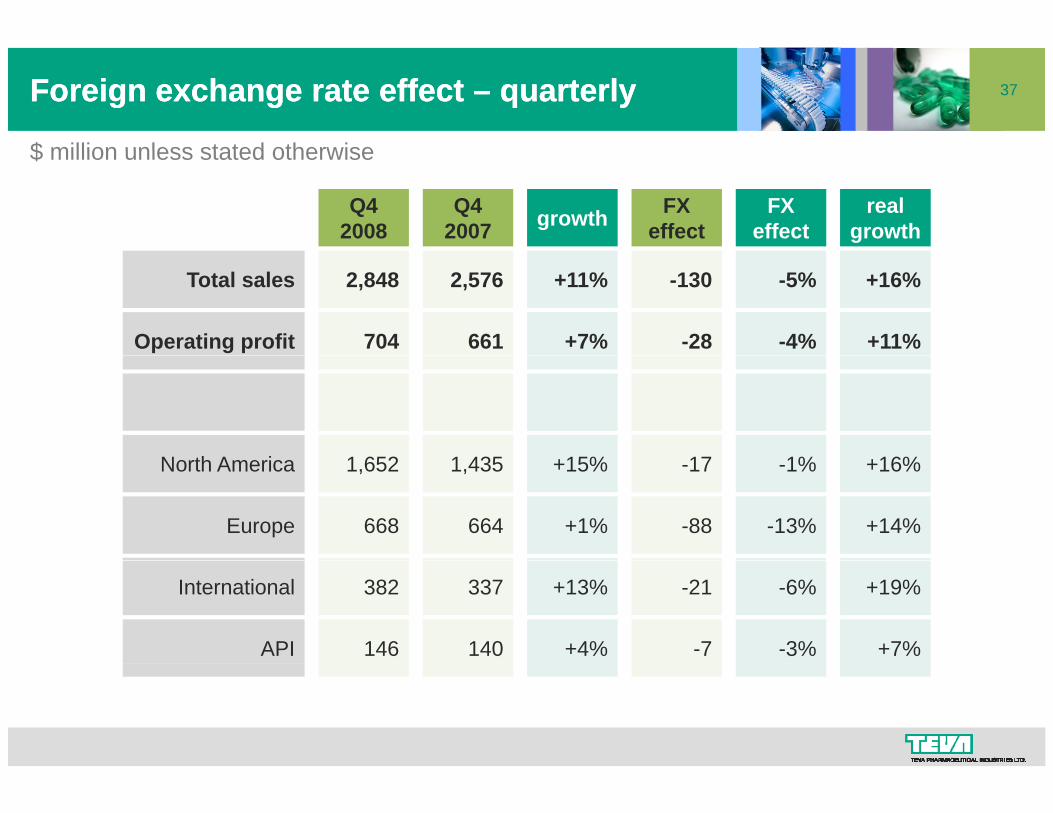

37Foreign exchange rate effect Foreign exchange rate effect –– quarterlyquarterly

$ million unless stated otherwise

Q4 2007

FX effect

Q4 2008

FX effectgrowth real

growth

$ million unless stated otherwise

Total sales 2,576 -1302,848 -5%+11% +16%

Operating profit 661 -28704 -4%+7% +11%

N th A i 1 435 171 652 1%15% 16%North America 1,435 -171,652 -1%+15% +16%

Europe 664 -88668 -13%+1% +14%

International 337 -21382 -6%+13% +19%

API 140 -7146 -3%+4% +7%

38Foreign exchange rate effect Foreign exchange rate effect –– full yearfull year

$ million unless stated otherwise

2007 FX effect2008 FX

effectgrowth real growth

$ million unless stated otherwise

Total sales 9,408 +22711,085 2%+18% +15%

Operating profit 2,395 -652,675 -3%12% 14%

N th A i 5 162 76 139 0%19% 19%North America 5,162 +76,139 0%+19% +19%

Europe 2,462 +1462,782 +6%+13% +7%

International 1,223 +601,561 +5%+28% +23%

API 561 +14603 +3%+7% +5%

39Cash generationCash generation

969

106

90139

132

170

179746

806

Cash from operations

710

70079

95106

97142

170

Net asset purchase

Dividends distributed

545Cash from operations

324512 568

443

70079

Free cash flow

Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008

$ $ $$410macquisitions

$366macquisitions

$4,387macquisitions

40

$ bn

Balance sheetBalance sheet

$ bn

ASSETS LIABILITIES

12/31/2007

2.96.0

12/31/2008

1.98.1

Cash and investmentsInventory, receivables

Short-term debtConvertible debentures

12/31/2007

1.81.4

12/31/2008

2.30.6

1.09.9

0.6

1.511.5

0.4

y,Other short-term assets

Short-term assets

Long-term investments

Other short-term liab.Short-term liabilities

Long-term debt

2.15.4

4.3

5.68.5

8.12.5

10.413.6

3.717.321.4

gNet fixed assets

Other long-term assetsLong-term assets

g

Equity 13.8 16.3

23.4 32.9Total assets Total liabilities 23.4 32.9

27% 34%Leverage

41Dividend Dividend –– 3333% increase% increase

NIS

0.60140

0 60

0.65

$ millionNISper share

0.45100

120

0.50

0.55

0.60

127

0.45

0.40

0.3480

100

0 35

0.40

0.45

56 59 5972 75 73 79

95106

9790

40

60

0.25

0.30

0.35

56 59 59

20

40

Q1-06 Q2-06 Q3-06 Q4-06 Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08 Q4-080.15

0.20

12% of net income 15% of net income 17% of net income

42New nonNew non--GAAP GAAP EPSEPS

2006* 2007 2008* 08-09 2009E** 08-09E

$m $m $m % $m %

Reported net income 1,867 1,952 2,374 22% 2,608to 2,791 10%-18%

$m $m $m % $m %

Amortization***

Non-GAAP net income

154

2 021

171

2 123

142

2 516 19%

477

2,928 16%-24%Non GAAP net income

Reported EPS

2,021

2.30

2,123

2.38

2,516

2.86

19%

20%

to 3,111

2.85to 3.05

16% 24%

0%-7%

Amortization***

Non GAAP EPS

0.19

2 49

0.21

2 59

0.17

3 03 17%

0.35

3.20

0.35

6% 12%

* 2006 and 2008 reported net income and EPS are non-GAAP results** 2009 net income and EPS assumes 915 million shares; *** Net of tax

Non-GAAP EPS 2.49 2.59 3.03 17% to 3.40 6%-12%

43

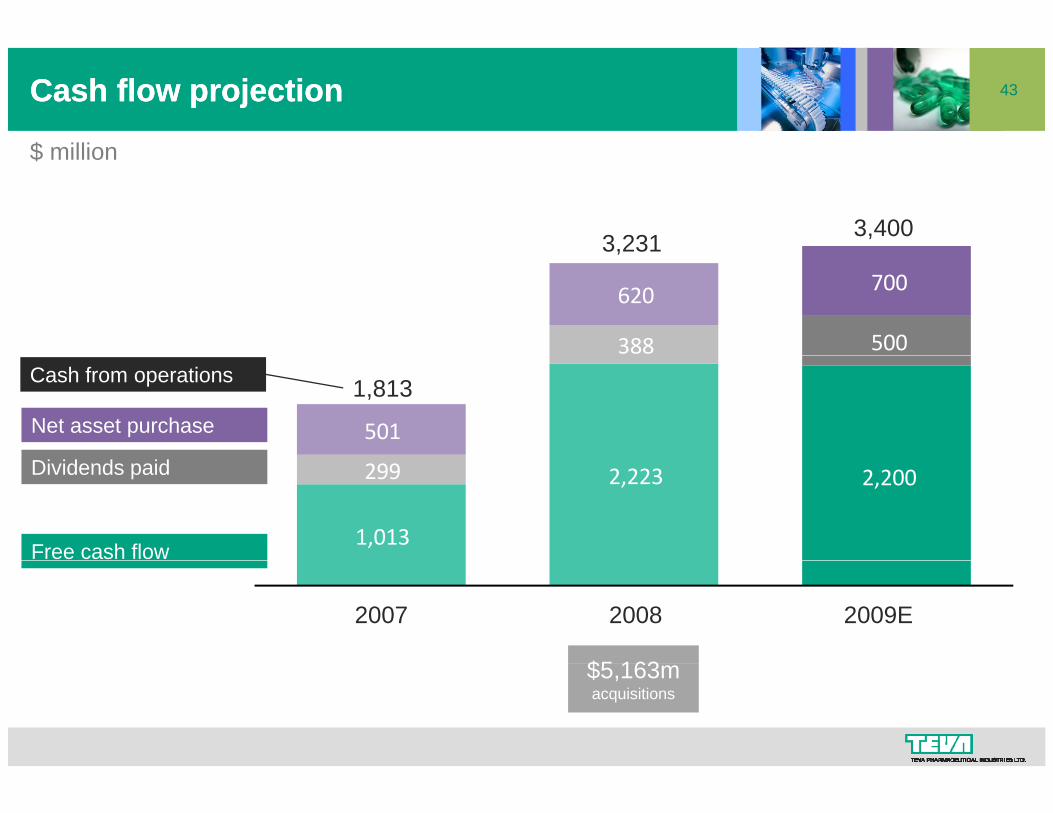

$ million

Cash flow projectionCash flow projection

$ million

3,231 3,400

388 500

620 700

,

501 Net asset purchase

1,813Cash from operations

1,013

2,223 2,200 299 Dividends paid

Free cash flow

2007 2008 2009E

$5 163$5,163macquisitions

44

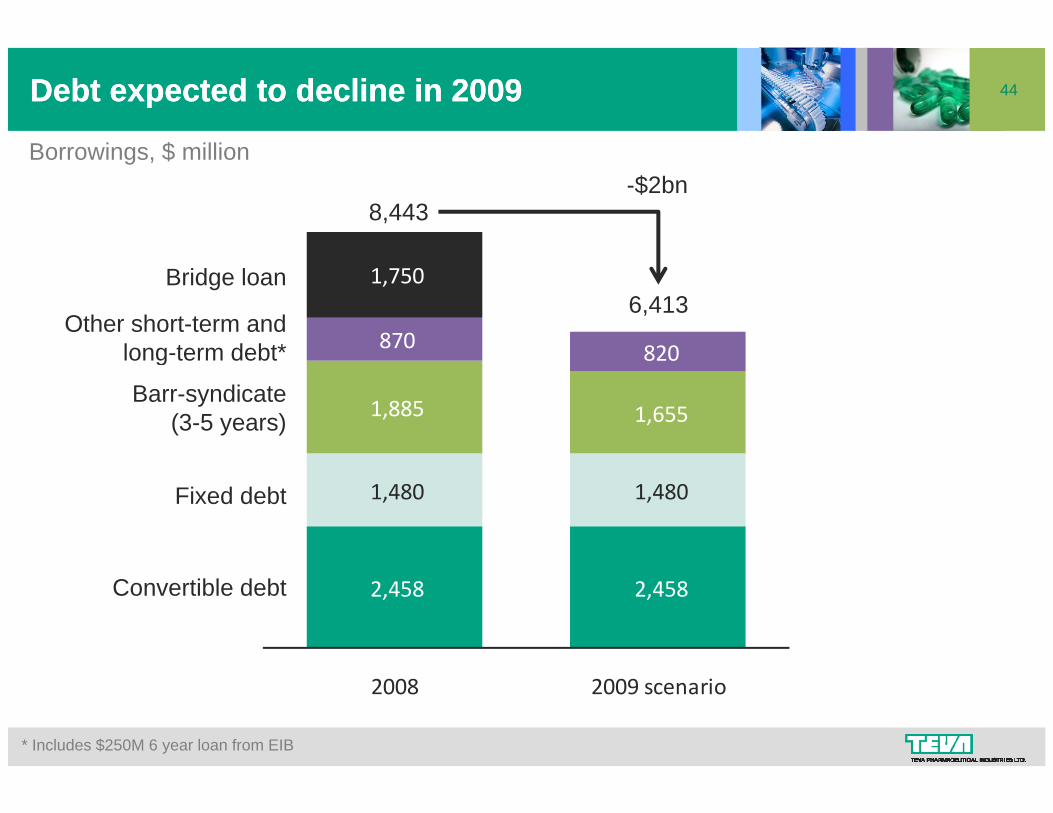

Borrowings $ million

Debt expected to decline in Debt expected to decline in 20092009

Borrowings, $ million

8,443-$2bn

870 820

1,750

Other short-term andlong-term debt*

Bridge loan6,413

1,885 1,655

820 long term debt

Barr-syndicate(3-5 years)

1,480 1,480 Fixed debt

2,458 2,458 Convertible debt

2008 2009 scenario

* Includes $250M 6 year loan from EIB

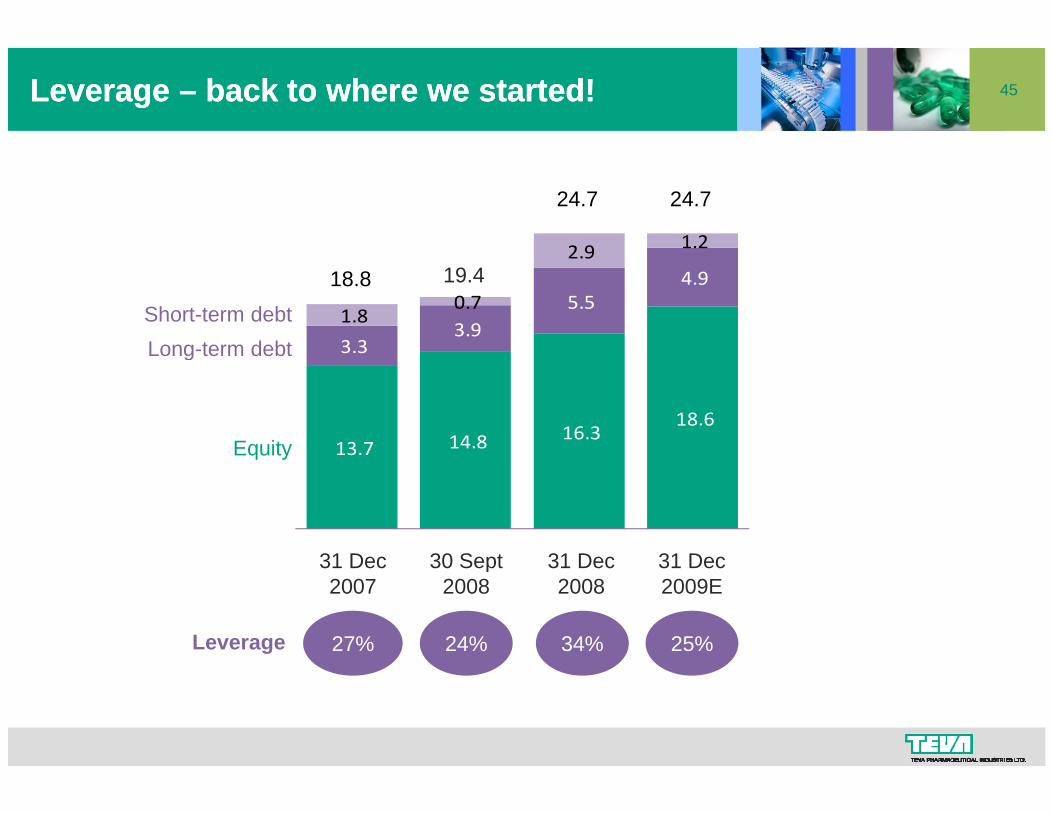

45Leverage Leverage –– back to where we started!back to where we started!

2 9 1.2

24.7 24.7

3.3 3.9

5.5 4.9

1.8 0.7

2.9 18.8 19.4

Long-term debtShort-term debt

13.7 14.8 16.3 18.6

Equity

Long term debt

31 Dec 30 Sept 31 Dec 31 Dec

q y

31 Dec2007

30 Sept2008

31 Dec2008

27% 24% 34%Leverage

31 Dec2009E

25%

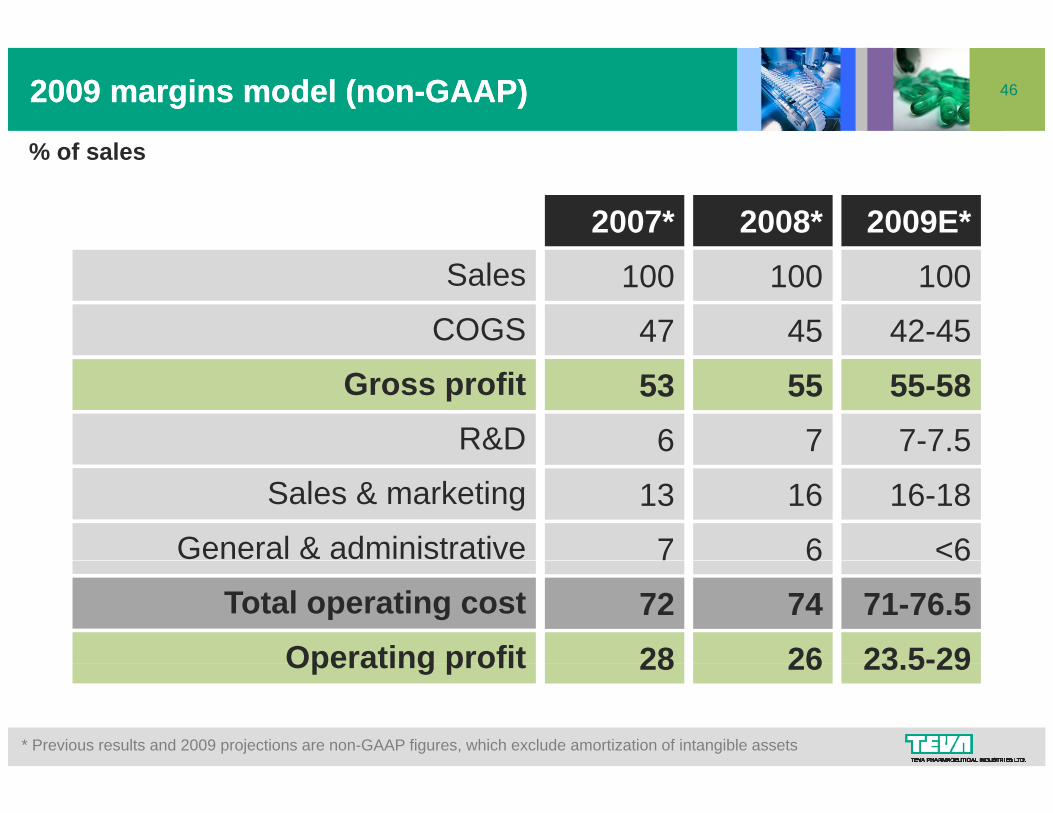

462009 2009 margins model (nonmargins model (non--GAAP)GAAP)

% of sales

2007* 2008* 2009E*

% of sales

Sales

COGS100 100 100

47 45 42-45

Gross profitR&D

53 55 55-586 7 7-7.5

Sales & marketing

General & administrative13 16 16-18

7 6 <6Total operating cost

Operating profit

6 6

72 74 71-76.528 26 23 5-29Operating profit 28 26 23.5-29

* Previous results and 2009 projections are non-GAAP figures, which exclude amortization of intangible assets

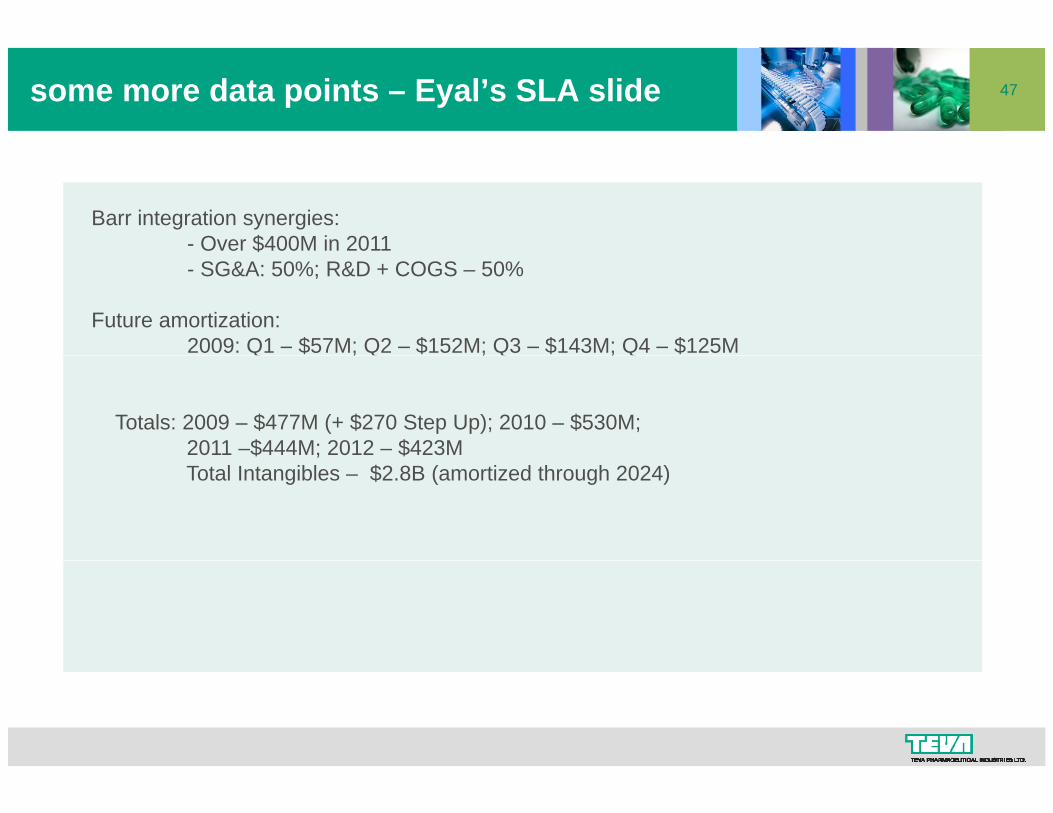

47Eyal’s SLA slide–some more data points

Barr integration synergies:- Over $400M in 2011- SG&A: 50%; R&D + COGS – 50%

Future amortization:2009: Q1 – $57M; Q2 – $152M; Q3 – $143M; Q4 – $125M; ; ;

Totals: 2009 – $477M (+ $270 Step Up); 2010 – $530M; 2011 –$444M; 2012 – $423MTotal Intangibles – $2.8B (amortized through 2024)

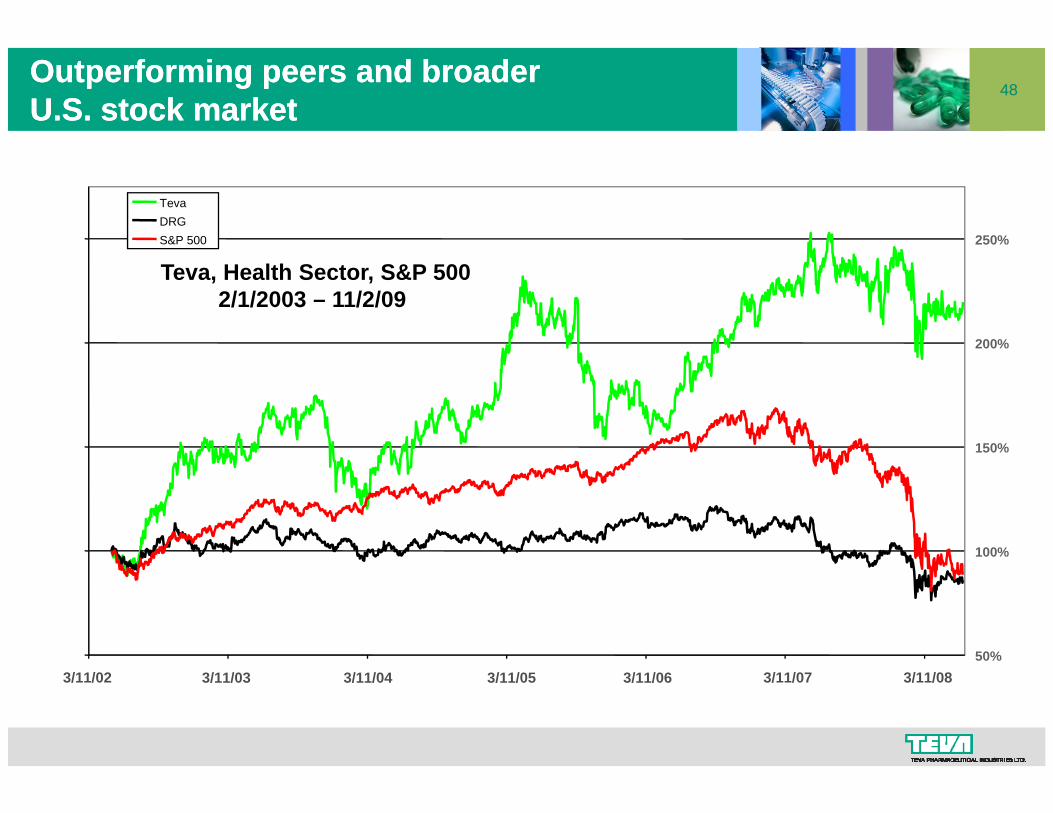

48Outperforming peers and broader Outperforming peers and broader U.S. stock marketU.S. stock market

250%

TevaDRGS&P 500

200%

Teva, Health Sector, S&P 5002/1/2003 – 11/2/09

150%

100%

50%3/11/02 3/11/03 3/11/04 3/11/05 3/11/06 3/11/07 3/11/08

49

Market capitalization $ bn 13 February 2009

Number Number 10 10 on NASDAQon NASDAQ

Market capitalization, $ bn, 13 February 2009

16894

MicrosoftC i 94

898886

C iscoOracleApple

Goog le 8677

6159

Goog leIntel

AmgenQualcomm 59

4639

28

QualcommG ileadTeva

C omcast272724

R IMMAmazonDirecTV

24C elgene

50SummarySummary

A very strong ending to a better then forecasted year

2009 and 2010 look good!

Foreign exchange impact

Very strong cash generationVery strong cash generation

Solid balance sheet, leverage better than planned

Barr integration – better than originally anticipated

51

THANK YOU!