JAPAN INTERNATIONAL COOPERATION AGENCY (JICA)

MINISTRY OF FINANCE THE REPUBLIC OF INDONESIA

STUDY ON FISCAL AND NON-FISCAL INCENTIVES TO ACCELERATE

PRIVATE SECTOR GEOTHERMAL ENERGY DEVELOPMENT

IN THE REPUBLIC OF INDONESIA

FINAL REPORT

(SUMMARY)

JULY 2009

West Japan Engineering Consultants, Inc.

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Table of Contents

Table of Contents ····························································································································· i

List of Tables and Figures ··············································································································· ii

Acronyms and Abbreviations ·············································································································v

Unit ··········································································································································· vii

Chapter 1 Introduction·······················································································································1

Chapter 2 Basic Philosophy and the Process of the Study ····························································2

Chapter 3 Present Status of Geothermal Power Development in Indonesia ·································6

Chapter 4 Conditions for Attractive IPP Projects············································································9

Chapter 5 Evaluation of a Coal-fired IPP Project (Benchmark Price) ········································10

Chapter 6 Evaluation of a Geothermal IPP Project ······································································13

Chapter 7 Benefits of Geothermal Power Development································································17

Chapter 8 Short-term Incentives to Promote Geothermal Development ····································23

Chapter 9 Proposal of Short-term Incentives to Promote Geothermal

Development ·················································································································30

Chapter 10 Evaluation of a Long-term Coal-fired IPP Project ····················································32

Chapter 11 Evaluation of a Long-term Geothermal IPP Project ·················································33

Chapter 12 Long-term Incentives to Promote Geothermal Development ···································34

Chapter 13 Cost and Benefit Analysis of Geothermal Development

Incentives ······················································································································39

Chapter 14 Importance of Feed-in Tariff Incentives ···································································44

Chapter 15 Aiming for Economic Growth through Geothermal

Development ~ A Way to Foster the Geothermal Industry in

Indonesia ~ ····················································································································47

JICA West JEC i

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

List of Tables and Figures

<List of Figures>

Chapter 2

Fig. 2.1-1 CO2 emissions from energy use ···············································································2

Fig. 2.1-2 World CO2 emitters ··································································································2

Fig. 2.2-5 Diffusion of renewable energy and government support ·········································3

Fig. 2.7-1 The role of government in promoting geothermal energy

development ·············································································································4

Chapter 3

Fig. 3.4-1 Selling prices and geothermal activities···································································7

Chapter 4

Fig. 4-1 IPP project and its stakeholders················································································9

Chapter 5

Fig. 5.3-1 Selling Price for coal-fired IPP project (Benchmark Price) ·································12

Chapter 6

Fig. 6.1-1 Geothermal development process for 60 MW plant ············································14

Chapter 7

Fig. 7.2-5 Fuel reduction premium of geothermal power (2007 -2016) ·······························18

Fig. 7.3-1 Export value of fuel saved through use of geothermal power (2007 –

2016) ····················································································································19

Fig. 7.4-1 Selling price composition comparison of geothermal and coal-fired

Power ~ For Benchmark oil price at 100 USD/barrel ~·········································20

Fig. 7.6-1 Total value of benefits of geothermal power generation (2007 –

2016) ····················································································································21

Fig. 7.6-2 Total value of benefits of geothermal power and its beneficiaries ·························21

Fig. 7.7-1 Ripple effect of 60 MW geothermal power plant construction······························22

Chapter 8

Fig. 8.1-3 Estimated selling prices of power by fuel sources ·················································23

Fig. 8.1-4 Estimated selling prices of power taking into account for opportunity

costs························································································································24

Fig. 8.1-5 Estimated selling price of power accounting for environment impact

costs························································································································24

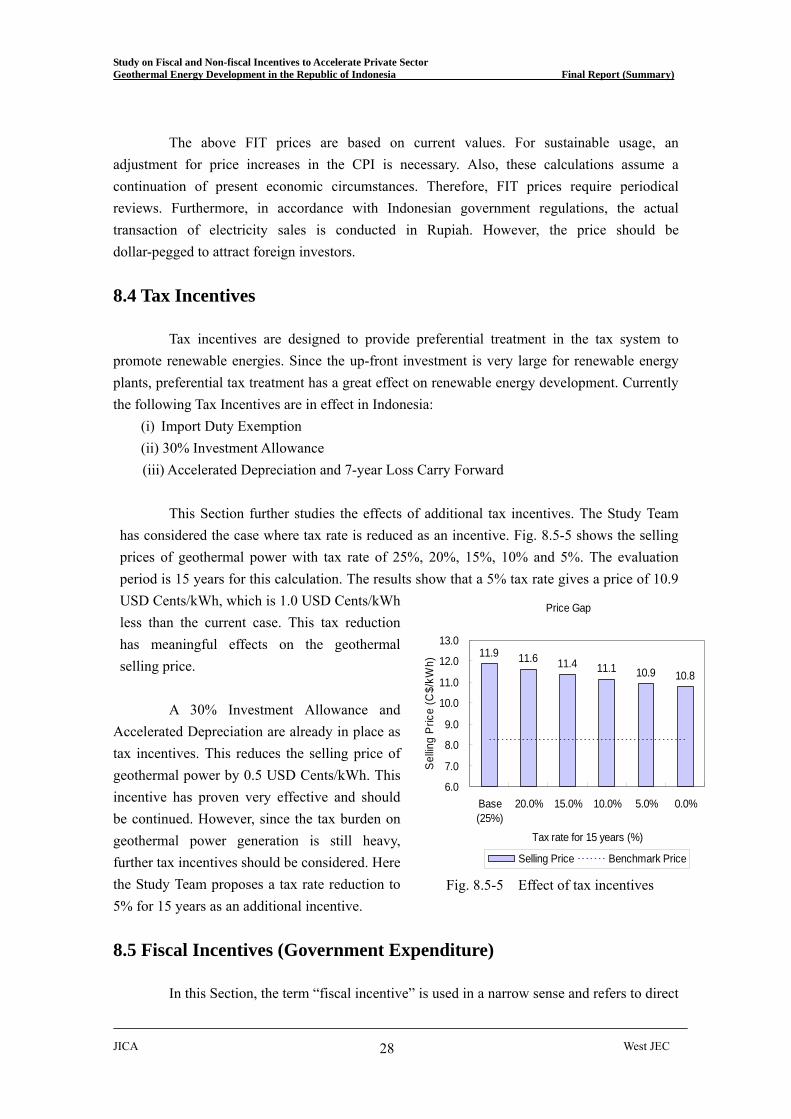

Fig. 8.5-5 Effect of tax Incentives ··························································································28

JICA West JEC ii

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Fig. 8.6-4 Effect of initial governmental survey·····································································29

Fig. 8.6-5 Effect of government survey ··················································································29

Chapter 10

Fig. 10.3-1 Long-term selling price of coal-fired power ··························································32

Chapter 11

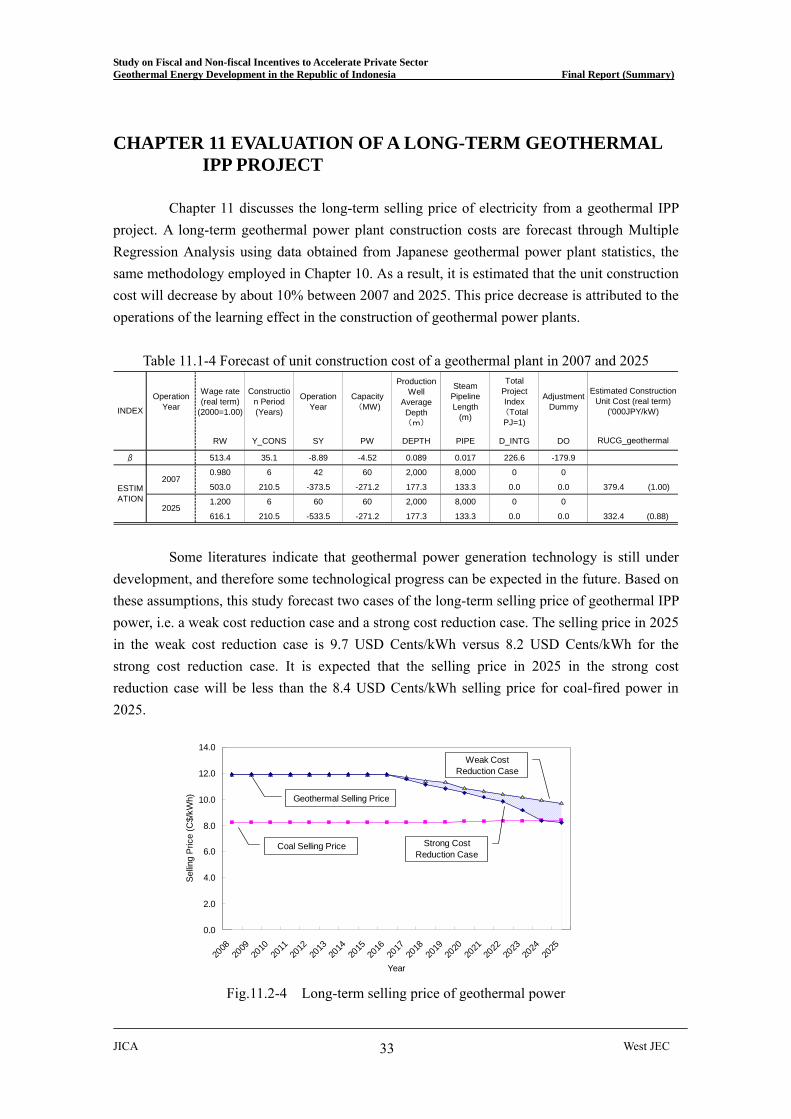

Fig. 11.2-4 Long-term selling price of geothermal power························································33

Chapter 12

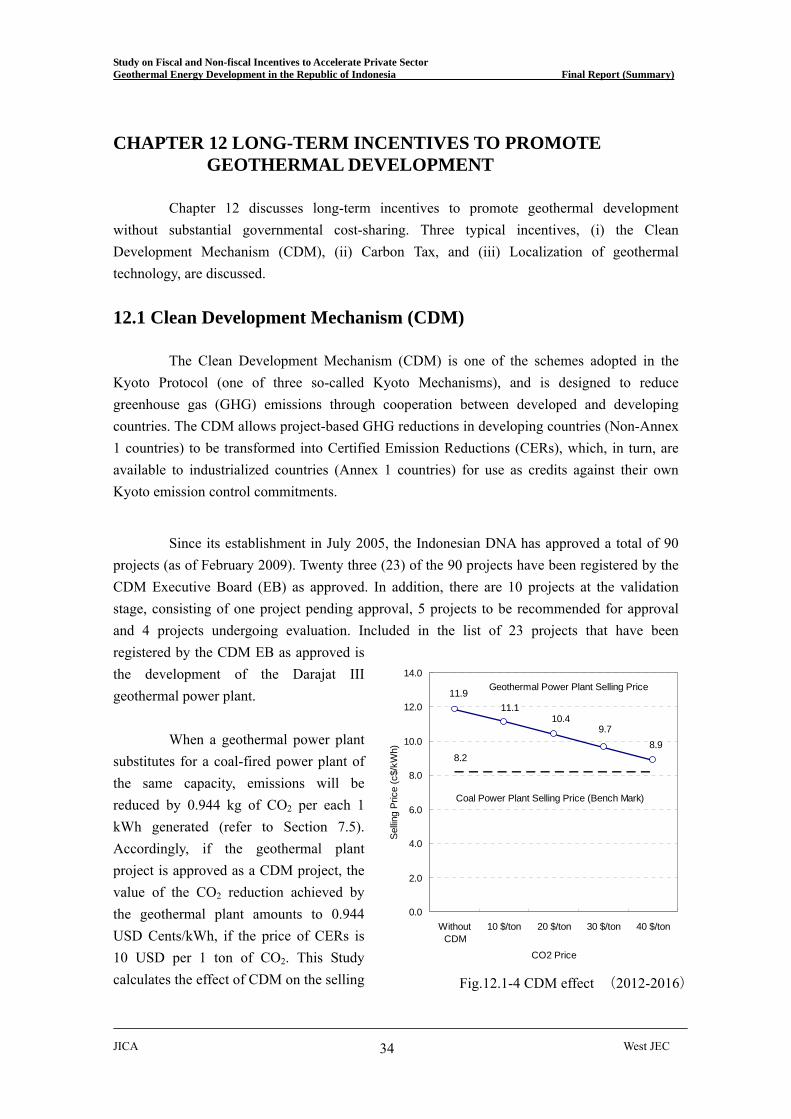

Fig. 12.1-4 CDM effect (2012-2016) ···············································································34

Fig. 12.2-2 Effect of carbon tax (2012-2016)·····································································36

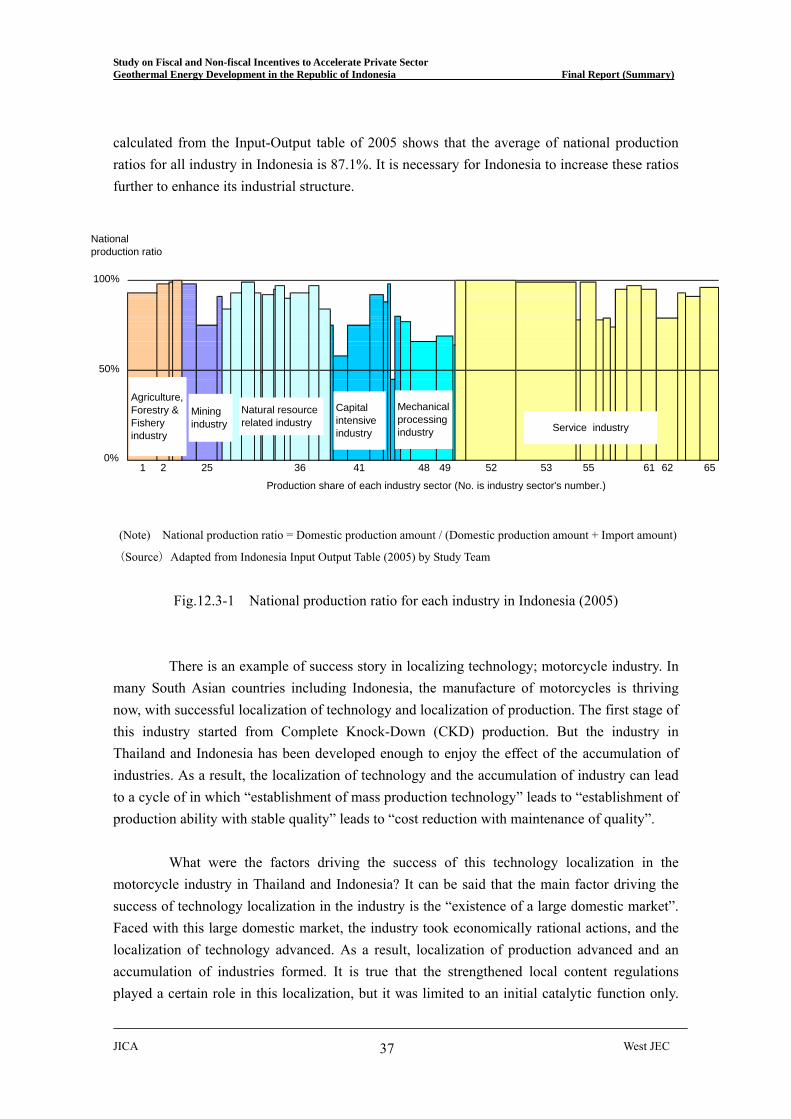

Fig. 12.3-1 National production ratio for each industry in Indonesia (2005) ························37

Chapter 13

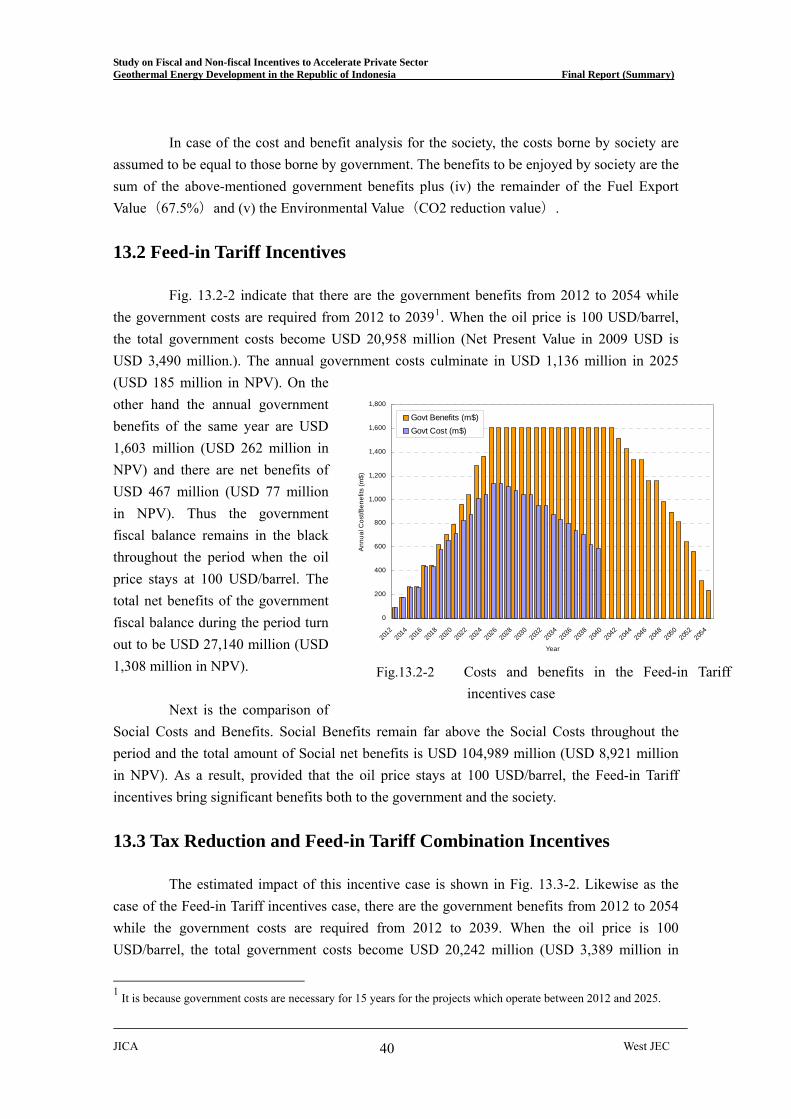

Fig. 13.2-2 Costs and benefits in the Feed-in Tariff incentives case ······································40

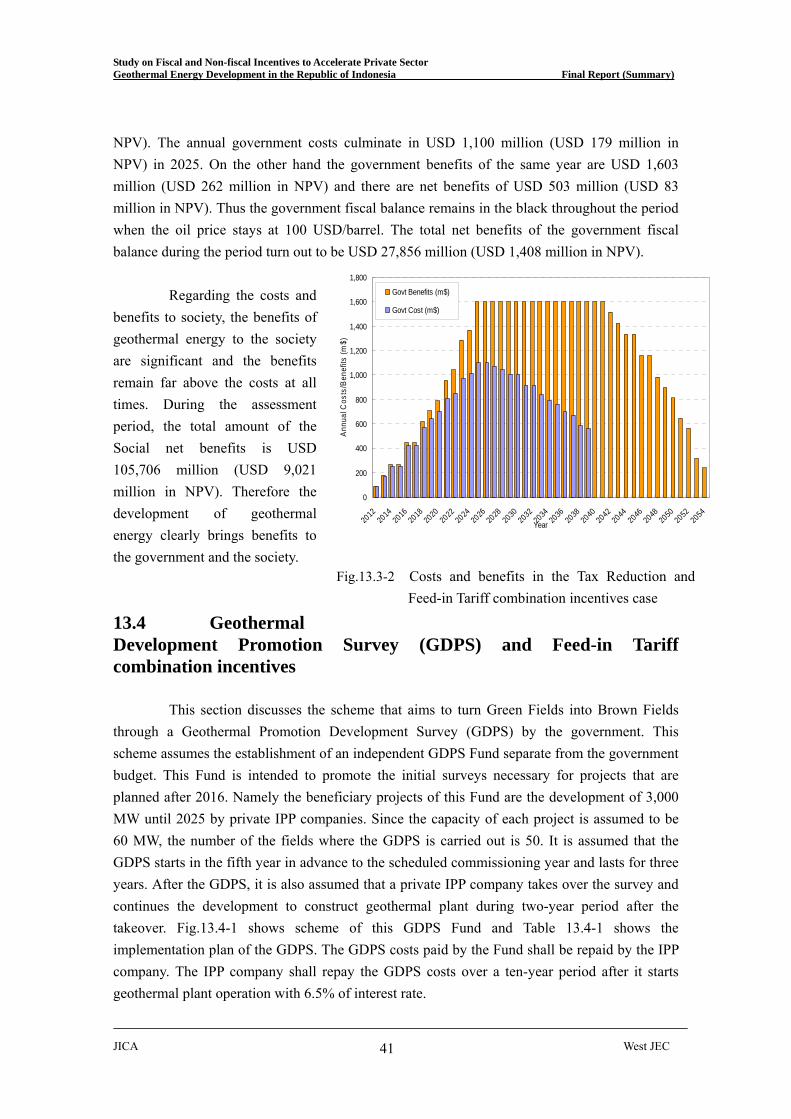

Fig. 13.3-2 Costs and benefits in the Tax Reduction and Feed-in Tariff

combination incentives case ·················································································41

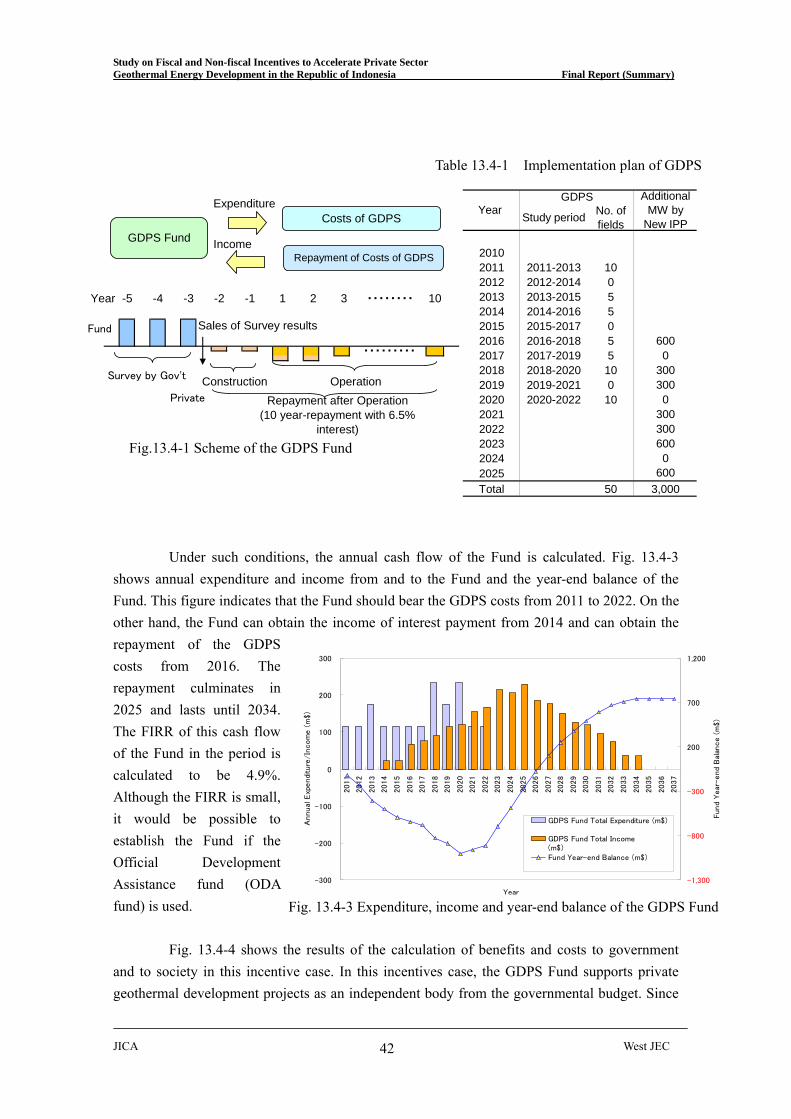

Fig. 13.4-1 Scheme of the GDPS Fund ··················································································42

Fig. 13.4-3 Expenditure, income and year-end balance of the GDPS Fund ···························42

Fig. 13.4-4 Costs and benefits in the GDPS and Feed-in Tariff combination

incentives case ······································································································43

Chapter 14

Fig. 14.1-1 Geothermal development outlook in the JICA Master Plan Study ······················45

Chapter 15

Fig. 15.1-4 Green New Deal Policy of Indonesia ···································································46

<List of Tables>

Chapter 2

Table 2.10-4 Future fuel prices used in this study·········································································5

Chapter 5

Table 5.1-1 Specifications of benchmark coal-fired IPP project···············································10

Chapter 6

Table 6.1-1 Specification of geothermal IPP project·································································13

Table 6.3-1 Assumptions for calculation of Geothermal Price ·················································16

Chapter 7

Table 7.2-4 Thermal power fuel reduction effect of geothermal power (Volume)

(2007 -2016) ·········································································································18

JICA West JEC iii

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Chapter 8

Table 8.2-1 Classification of Renewable Energy Promotion Policies·······································26

Table 8.3-6 Proposal of FIT prices ····························································································27

Table 8.3-10 Proposal of FIT prices (20 MW or less capacity case) ········································27

Chapter 10

Table 10.2-4 Forecast of unit construction cost of coal-fired plant in 2007 and

2025························································································································32

Chapter 11

Table 11.1-4 Forecast of unit construction cost of geothermal plant in 2007 and

2025························································································································33

Chapter 13

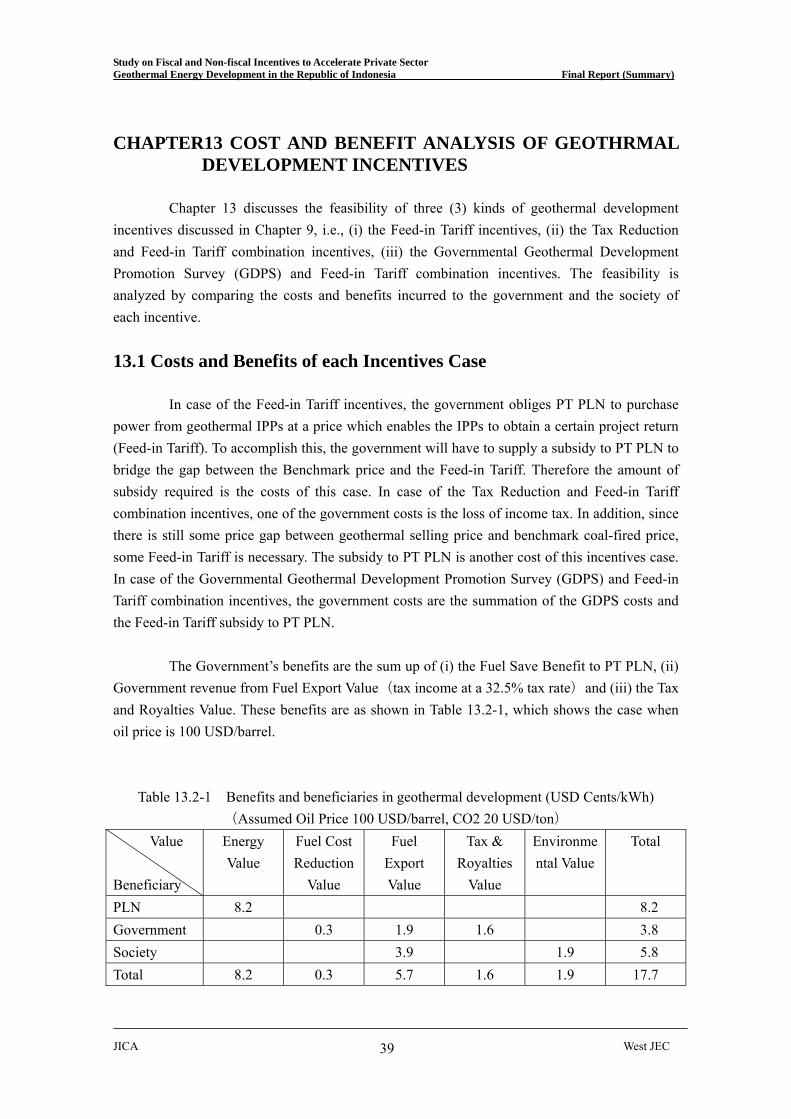

Table 13.2-1 Benefits and beneficiaries in geothermal development ········································39

Table 13.4-1 Implementation plan of GDPS ·············································································41

Chapter 14

Table 14.1-1 Comparison between the First and Second Crash Programs ····································44

JICA West JEC iv

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Acronyms and Abbreviations

BAU Business as Usual

CAPM Capital Asset Price Model

CDM Clean Development Mechanism

CERs Certified Emission Reductions

CGPI Corporate Goods Price Index

CKD Complete Knock-Down

CO2 Carbon Dioxides

CPI Consumer Price Index

CRIEPIR Central Research Institute of Electric Power Industry Review

DGEEU Directorate General of Electricity and Energy Utilization

DGGMR Directorate General of Geology and Mineral Resources

DGMCG Directorate General of Mineral, Coal and Geothermal

DNA Designated National Authority

DOE Designated Operational Entity

EB Executive Board

EPC Engineering, Procurement and Construction

EqIRR Equity Internal Rate of Return

EqIRRc Equity Internal Rate of Return Criteria

FIRR Financial Internal Rate of Return

FIT Feed-in Tariff

FOM Fixed O&M Fee

GDP Gross Domestic Production

IEA International Energy Agency

IPP Independent Power Producer

IUP Geothermal Energy Business Permit

JBIC Japan Bank for International Cooperation

JICA Japan International Cooperation Agency

JOC Joint Operation Contract

LNG Liquefied Natural Gas

MEMR Minister of Energy and Mineral Resources

MOF Minister of Finance

JICA West JEC v

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

MOU Minutes of Understanding

NOx Nitrogen Oxides

NPV Net Present Value

O&M Operation and Maintenance

OECD Organization for Economic Cooperation and Development

PGE Pertamina Geothermal Energy

PPA Power Purchase Agreement

PPP Purchase Power Parity / Public Private Partnership

PQ Prequalification

PrIRR Project Internal Rate of Return

PrIRRc Project Internal Rate of Return Criteria

PT PLN PT Perusahaan Listrik Negara (National Electric Company)

RMc Commercial Risk Margin

RMr Resource Risk Margin

RMt Technical Risk Margin

RPS Renewable Energy Portfolio Standard

RUPTL Power Development Program of PT PLN

SOP Share of Proceeds

SOx Sulfur Dioxides

UNFCCC United Nations Framework Convention on Climate Change

VAT Value Added Tax

VOM Variable O&M Fee

WACC Weighted Average of Capital Cost

WASP Wien Automatic System Planning

JICA West JEC vi

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Unit Prefixes

k : kilo- =103

M : mega- =106

G : giga- =109

T : tera- =1012

Units of Length km : kilometer

Units of Area km2 : square kilometer ha : hectare

Units of Volume m3 : cubic meter l : liter kl : kiloliter barrel : barrel (1 barrel = 0.159 kl) SCF : standard cubic feet (1 SCF = 0.0283 kl)

Units of Mass kg : kilogram t : ton (metric)

Units of Energy kWh : kilowatt-hour MWh : megawatt-hour GWh : gigawatt-hour MMBTU : million British thermal unit (1 MMBTU = 0.252*106 kcal) TOE : ton of oil equivalent (1*107 kcal) KTOE : kilo ton of oil equivalent (1*1010 kcal)

Units of Temperature ℃ : degree Celsius

Units of Electricity kW : kilowatt MW : megawatt kV : kilovolt kVA : kilovolt-ampere

Units of Currency IDR (Rp) : Indonesian Rupiah USD ($) : US Dollar JPY (¥) : Japanese Yen

JICA West JEC vii

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

EXECTIVE SUMMARY

Energy consumption in Indonesia has increased rapidly with the high economic growth rate of recent years. Indonesia’s CO2 emissions from energy use have increased rapidly and have made the country the 15th largest CO2 emitter in the world. Energy diversification is one of the main ways to reduce the dependency on fossil fuel and to mitigate CO2 emissions. Indonesia has a variety and large scale of natural energy resources – not only oil, gas and coal but also geothermal energy and other renewable energy like hydro, bio, and wind. Among these sources of renewable energy, Indonesia has the largest geothermal energy potential in the world – approximately 27.0 GW. It is strongly expected for Indonesia to make use of these affluent geothermal resources to reduce CO2 emissions. The geothermal generation capacity has reached 1,196MW in Indonesia. Although Indonesia is the fourth largest producer of geothermal power in the world, it is far from exploiting this huge potential of geothermal energy as well as possible.

The barriers which hinder smooth development of geothermal energy are the

development risks of underground resources and the burden of enormous up-front investment. Therefore, the purchase price of geothermal energy should include a reward for challenging these barriers. Consequently, although it is lower than the price of diesel or heavy-oil power plant energy, the price of geothermal energy becomes higher than that of coal-fired plant energy. However, PT PLN, a buyer of geothermal energy, has a mission to supply inexpensive power to consumers and this mission makes it reluctant to increase the purchase price it pays for geothermal energy. The unattractive purchase price of PT PLN causes private IPP companies hesitation in investing geothermal projects in Indonesia.

Solutions to this problem are not be obtained if the problem is left only in the hands of

the private IPP company and PT PLN, and no more geothermal development can be expected. However, it is necessary to pay attention to the fact that government can be a key player in realizing the benefits of geothermal development by private IPP. When geothermal energy is exploited, the society is likely to obtain several benefits. It is one of the important missions of the government to realize these geothermal benefits and endow the society with them.

In this Study, the oil price is assumed to be 100 USD/barrel, and coal 90 USD/ton

(5,300 kcal/kg), referring to the latest forecasts of the International Energy Agency (IEA) and the Electric Power Development Plan (RUPTL 2009-2018) of PT PLN. Theses prices are assumed to stay this level until 2025 to simplify the analysis.

As a benchmark, the selling price of a 600 MW coal-fired IPP project is calculated.

Based on a requirement of 11.2% Project IRR and 12.0% Equity IRR, it is calculated as 8.2 USD Cents/KWh. Similarly the selling price of a 60 MW geothermal IPP project is calculated.

JICA West JEC ES-1

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Based on a requirement of 17.1% Project IRR and 17.0% Equity IRR, it is calculated as 11.9 USD Cents/KWh. There is a 3.7 USD Cents/kWh difference between this price and the price for the benchmark coal-fired IPP project. The objective of the policy is to bridge this price gap by fiscal and non-fiscal incentives.

Geothermal energy has several values. These values are calculated as follows: (i)

energy value (a benchmark price) at 8.2 USD Cents/kWh, (ii) fuel cost reduction value at 0.3 USD Cents/kWh, (iii) saved fuel export value at 5.7 USD Cents/kWh, (iv) increased tax revenue value at 1.6 USD Cents/kWh and (v) carbon dioxide reduction value at 1.9 USD Cents/kWh. The total value is 17.7 USD Cents/kWh. These values can be divided by beneficiaries. PT PLN receives 8.2 USD Cents/kWh as (i) energy value. The government receives 3.8 USD Cents/kWh of which the breakdown is: (ii) fuel cost reduction value as subsidy reduction to PT PLN, (iii) 32.5% (tax rate) of saved fuel export value, and (iv) increased tax revenue value. The society receives 5.8 USD Cents/kWh as the remaining of (iii) saved fuel export value and (v) carbon dioxide reduction value. These benefits show that geothermal energy can bring remarkable benefits to PT PLN, the government and the society, if it is well exploited. In addition to these values in operation stage, geothermal energy brings about other benefits in construction stage. Geothermal power plant construction relies heavily on the procurement of work and services from the vicinity of the construction site. That stimulates the domestic economy. These ripple effects are calculated that a 60 MW geothermal plant construction will have a significant job-creating effect as large as 10,060 opportunities.

Based on these discussions, the following incentives are considered appropriate for Indonesia:

(A) Incentives for Green Field development (a-1) Feed-in Tariff incentives of 11.9 USD Cents/kWh, or

(a-2) Tax Reduction of 5% corporate income tax rate for 15 years and Feed-in Tariff of 10.9 USD Cents/kWh.

(B) Measures to change Green Field to Brown Field (b) Geothermal Development Promotion Survey (GDPS) in initial stage carried out by the

government (C) Measures for risk free participation (c) Public-Private Partnership (PPP) development

The cost and benefit analysis of these incentives indicates that all these incentives

bring significant benefits both to the government and the society.

Currently the Indonesia government is planning to start the Second Crash Program. The program aims at a 4,616 MW geothermal development during 2010-2014. This is an ambitious target and the government needs to make utmost efforts to attain the target. For the implementation of the

JICA West JEC ES-2

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Second Crash Program, the most important and urgent policies are the pricing incentives. The Feed-in Tariff incentives can be said to be the easiest, the most important and the most urgent incentives to adopt under the current situation.

Indonesia, with 150 volcanoes and more than 27,000 MW of geothermal resource

potential, is the world’s richest country in geothermal resources. This is a good time for Indonesia to adopt a Green New Deal strategy focused on the development of geothermal energy, when many countries are beginning to identify the type of renewable energy development in which they can achieve a comparative advantage. When the geothermal industry is well developed and serves a large domestic market, the localization of technology will start, triggering the next round of cost reductions and leading to the further expansion of the domestic market. Investment in geothermal projects has a far larger effect in stimulating the national economy and creating more new employment than coal-fired projects. Therefore, the encouragement of investment in geothermal energy raises the likelihood of economic growth and employment expansion. This can be called the Green New Deal policy of Indonesia. For this purpose, the first step should be to implement the incentives to accelerate geothermal energy development proposed in this Study, and to continue the incentives for a certain period to convince everyone inside and outside of Indonesia of the golden future that lies ahead for Indonesia geothermal development.

JICA West JEC ES-3

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

CHAPTER 1 INTRODUCTION 1.1 Background of the Study

Indonesia is said to have the largest geothermal potential in the world. According to the Indonesian Ministry of Energy and Mineral Resources, there are more than 250 prospective geothermal fields in Indonesia, and potential power generation is estimated to be 27,000 MW or more. However, the development of geothermal resources lags behind other energy resource development, and the current geothermal power generation capacity is around 1,000MW only. The Indonesian government is keenly interested in promoting geothermal energy in order to address climate change issues and to diversify energy sources to reduce over-dependency on oil-based energy. This Study is initiated to promote geothermal energy through cooperation between the Indonesian Ministry of Finance and the Japanese side.

1.2 Objective of the Study

The objective of this Study is to clarify the mid- and long-term fiscal and non-fiscal incentives promoting private sector-led geothermal energy development through cooperation between the Indonesian Ministry of Finance and the Japanese side. 1.3 Contents of the Study

This Study is to consider necessary fiscal incentives from the perspective of potential investors. Investors are reluctant to invest in geothermal energy projects today, because the selling price which they can obtain a certain return from their investments is higher than the current purchase prices of PT PLN which is based on the selling prices of coal-fired thermal plants. So it would be useful to consider fiscal measures which fill the gap of selling prices of geothermal energy and coal-fired thermal plants. By carefully examining power generation costs and possible selling prices of each power source, this Study aims to materialize practical policy options to promote geothermal energy investments. This Study with the following items:

(1) Current situation of geothermal energy development (2) Conditions of the power generation business (3) Economic evaluation of coal-fired power generation business (benchmark) (4) Economic evaluation of geothermal power generation business (5) Benefits of geothermal power generation (6) Short-term incentives to promote geothermal energy development (7) Proposals for short-term incentives (8) Long-term incentives to promote geothermal energy development (9) Cost and benefit analysis of incentives

JICA West JEC 1

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

JICA West JEC 2

CHAPTER 2 BASIC PHILOSOPHY AND THE PROCESS OF THE STUDY

2.1 Current Status of Energy Use and CO2 Emission in Indonesia

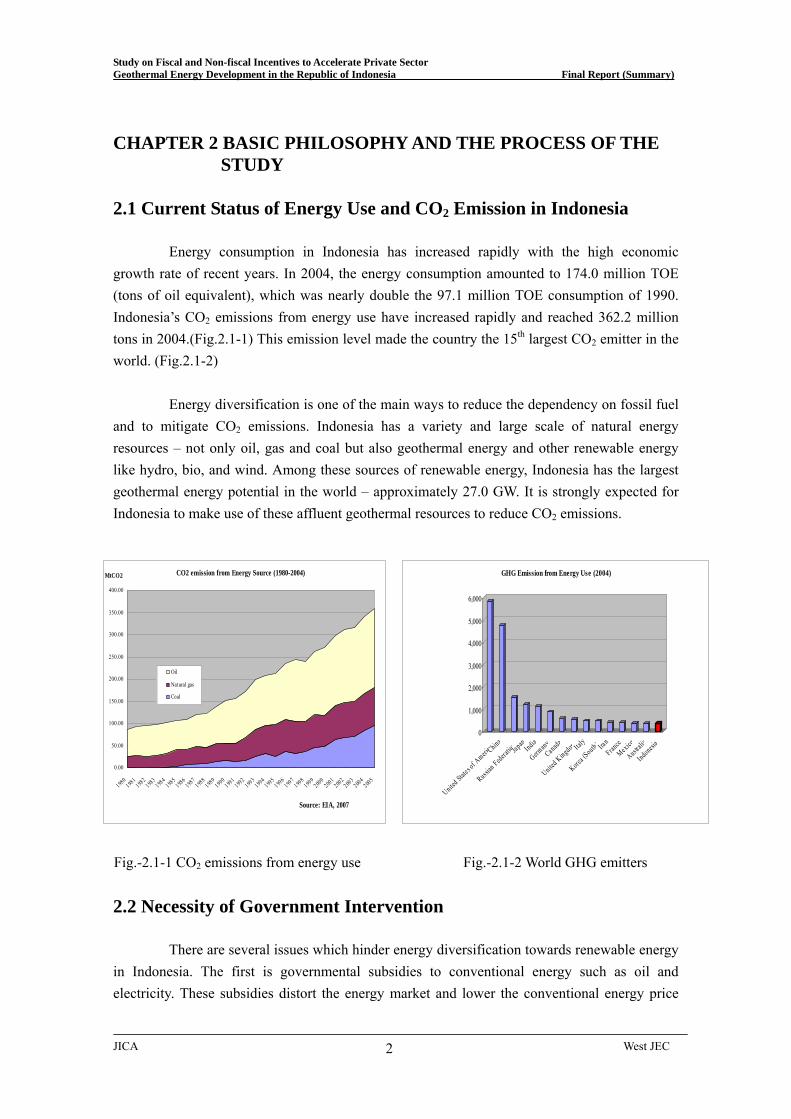

Energy consumption in Indonesia has increased rapidly with the high economic

growth rate of recent years. In 2004, the energy consumption amounted to 174.0 million TOE (tons of oil equivalent), which was nearly double the 97.1 million TOE consumption of 1990. Indonesia’s CO2 emissions from energy use have increased rapidly and reached 362.2 million tons in 2004.(Fig.2.1-1) This emission level made the country the 15th largest CO2 emitter in the world. (Fig.2.1-2)

Energy diversification is one of the main ways to reduce the dependency on fossil fuel

and to mitigate CO2 emissions. Indonesia has a variety and large scale of natural energy resources – not only oil, gas and coal but also geothermal energy and other renewable energy like hydro, bio, and wind. Among these sources of renewable energy, Indonesia has the largest geothermal energy potential in the world – approximately 27.0 GW. It is strongly expected for Indonesia to make use of these affluent geothermal resources to reduce CO2 emissions.

0

1,000

2,000

3,000

4,000

5,000

6,000

United State

s of AmericC

hina

Russian Federa

tionJapanIndia

Germany

Canada

United Kingdom Ital

y

Korea (S

outh) IranFran

ceMexico

Australia

Indonesia

GHG Emission from Energy Use (2004)

0.0

98

0

0

1 0

1 0

2 0

2 0

3 0

3 0

4 0

01981

19821983

19841985

19861987

19881989

19901991

19921993

19941995

19961997

19981999

20002001

20022003

20042005

50.0

00.0

50.0

00.0

50.0

00.0

50.0

00.0

1

Oil

Natural gas

Coal

CO2 emission from Energy Source (1980-2004)

Source: EIA, 2007

Mt 2CO

Fig.-2.1-1 CO2 emissions from energy use Fig.-2.1-2 World GHG emitters 2.2 Necessity of Government Intervention

There are several issues which hinder energy diversification towards renewable energy

in Indonesia. The first is governmental subsidies to conventional energy such as oil and electricity. These subsidies distort the energy market and lower the conventional energy price

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

level, increasing energy consumption. The second issue is that many sources of renewable energy are still in the introductory stage, the learning effect and economies of mass production have yet to bring down supply prices. Therefore, the prices of renewable energy are higher than those of conventional energy, and a certain governmental support is necessary to make them competitive with conventional energy in the market.

Many sources of renewable energy remain in the initial stage of exploitation, where neither the learning curve nor the mass production effect has yet had a chance to reduce their supply price. However, these effects gradually contribute to a reduction in the supply price, if the introduction of renewable energy proceeds with the support of the government. As a result, if the supply price is decreased enough, the emergence of a situation in which renewable energy prices are lower than conventional energy supply prices can be expected. Once this is the situation, the diffusion of renewable energy will proceed automatically even without governmental support for it. It is expected that the government support to renewable energy will continue until such a situation arises.

(Source) Lund (2007), “Effectiveness of policy measures

in transforming the energy system”, Energy Policy

Fig.2.2-5 Diffusion of renewable energy and government support

2.3 Significance of Geothermal Energy and Barriers to its Development Geothermal energy has the following advantages:

- Value as energy of high supply reliability - Value as domestically produced energy - Value as stable energy - Value as environmentally friendly energy - Value as energy which can contribute to the local society.

Although geothermal energy has the above-described virtues, it is true that geothermal

development is progressing more slowly than expected even in Indonesia, which is blessed with a lot of geothermal resources. There are two big barriers which hinder smooth development of geothermal energy: the “development risks of underground resources” and the “burden of enormous up-front investment.”

The development risks of underground resources mean that the project developers can

JICA West JEC 3

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

JICA West JEC 4

not exactly know the characteristics of resources, i.e. the depth, the capacity, the quality, etc., in the planning stage and can know them after they completed the development. In this sense, uncertainty in a geothermal development project is remarkably large. This uncertainty inhibits private companies from entering geothermal development projects. The burden of enormous up-front investment means that geothermal projects need a long gestation period from the star of exploration to the actual plant operation and the developers should bear the large cost burden during this period. 2.4 Importance of the Role of Government

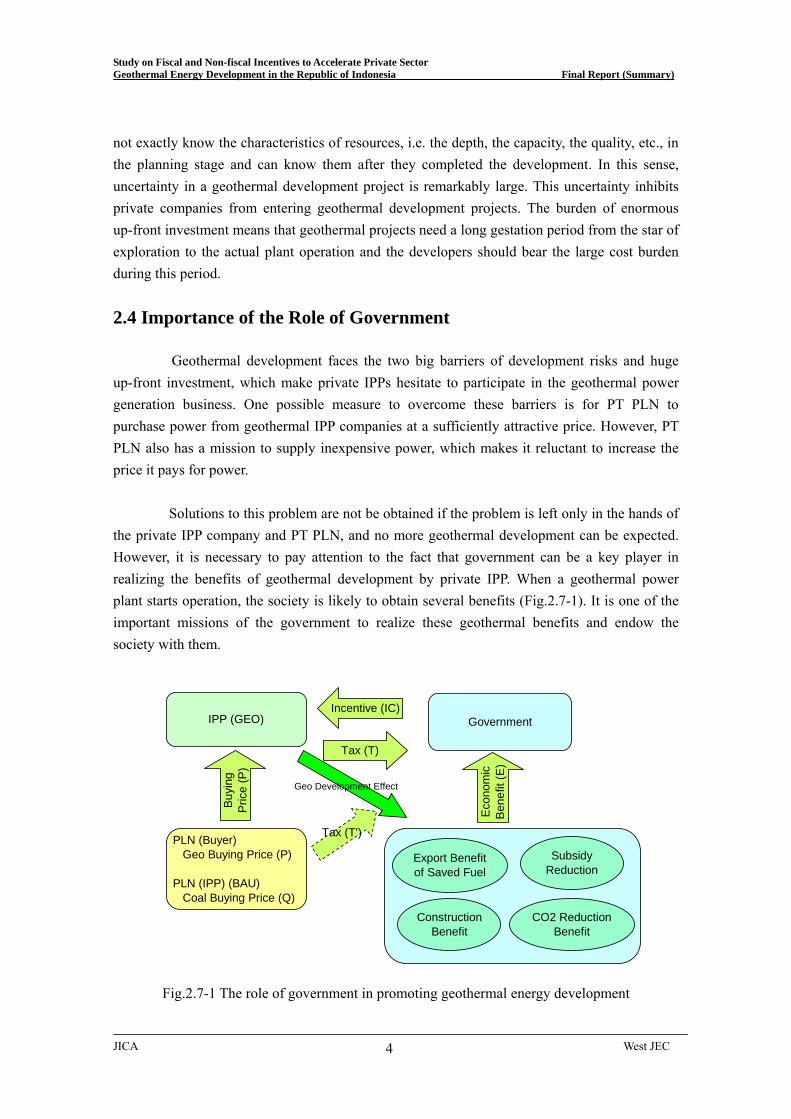

Geothermal development faces the two big barriers of development risks and huge up-front investment, which make private IPPs hesitate to participate in the geothermal power generation business. One possible measure to overcome these barriers is for PT PLN to purchase power from geothermal IPP companies at a sufficiently attractive price. However, PT PLN also has a mission to supply inexpensive power, which makes it reluctant to increase the price it pays for power.

Solutions to this problem are not be obtained if the problem is left only in the hands of the private IPP company and PT PLN, and no more geothermal development can be expected. However, it is necessary to pay attention to the fact that government can be a key player in realizing the benefits of geothermal development by private IPP. When a geothermal power plant starts operation, the society is likely to obtain several benefits (Fig.2.7-1). It is one of the important missions of the government to realize these geothermal benefits and endow the society with them.

IPP (GEO)

PLN (Buyer) Geo Buying Price (P)

PLN (IPP) (BAU) Coal Buying Price (Q)

GovernmentIncentive (IC)

Tax (T)

Tax (T')

Econ

omic

Ben

efit

(E)

Buyi

ngPr

ice

(P)

SubsidyReduction

Export Benefitof Saved Fuel

CO2 ReductionBenefit

Geo Development Effect

ConstructionBenefit

Fig.2.7-1 The role of government in promoting geothermal energy development

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Government disposes of various policy tools to promote renewable energy. One of them is a so-called “compulsory type policy” which unilaterally imposes the cost of the promotion of renewable energy on power companies. Another is a so-called “incentive type policy” in which the government bears this cost. Typical compulsory type policies are the “fixed buying price system” and the “renewable energy quota system”. In an incentive type policy, there are three types of incentives; tax incentives, fiscal incentives, and financial incentives. By considering the effects and the costs of each policy, this Study considers the most effective incentives to promote the private geothermal IPP business in Indonesia. 2.5 Methodology of the Study In this Study, “short-term” is defined as the period up to 2016. This time range is set in consideration of the fact that geothermal development requires a long lead time in exploration, development and construction. According to the JICA Master Plan Study, the amount of power developable by 2016 is presumed to be approximately 3,300 MW under the shortest lead time scenario. As for the study method, the Study Team uses a profitability simulation program to calculate a benchmark coal–fired power project and a geothermal power project (that is, the calculation of the profit and loss statement and the cash flow statement are carried out.). Through these profitability simulations, the Study Team tries to determine the incentives which are necessary to attract private companies to participate in geothermal projects in the short–term range. In this study “mid-term” and “long-term” are defined as 2017-2025. The goal is to achieve 9,500 MW of geothermal power generation. Considering the long-term trends of generation costs in geothermal and coal-fired, the cost and benefit analysis of various incentive policies are studied. 2.6 Assumptions of the Study

The following assumptions are used in this Study: Exchange rates are; 1 USD =

10,000 IDR = 100 JPY. The foreign currency interest rate is assumed to be 6.5% based on the “Arrangement on Officially Supported Export Credits” of OECD. The inflation effect is not considered and the evaluation is done in real terms (in 2009 USD). As for the fuel prices, the latest forecasts of the International Energy Agency (IEA) and the Electric Power Development Plan (RUPTL 2009-2018) of PT PLN are referred. Based on these forecast, the fuels prices shown in Table 2.10-4 are used in this Study. Theses prices are assumed to stay this level until 2025 to simplify the analysis.

Table 2.10-4 Future fuel prices used in this Study

Fuel PriceCrude Oil 100 USD/bblCoal 90 USD/tonHSD 140 USD/bblMFO 110 USD/bblNatural Gas 6 USD/MMBTULNG 13 USD/MMBTU

JICA West JEC 5

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

CHAPTER 3 PRESENT STATUS OF GEOTHERMAL POWER DEVELOPMENT IN INDONESIA

3.1 Geothermal Power Potential in Indonesia

Indonesia may have the largest geothermal resource capacity in the world, with the about forty (40) percent (equivalent to approximately 27,000 MW) of the world’s geothermal resources concentrated in Indonesia. Geothermal power generation has been conducted in seven (7) fields, namely Kamojang, Darajat, Wayang-Windu, Salak in western Java, Dieng in central Java, Sibayak in north Sumatra, and Lahendong in north Sulawesi. The generation capacity has reached 1,196MW. Although Indonesia is the fourth largest producer of geothermal power in the world, it is far from exploiting this huge potential of geothermal energy as well as possible. The Ministry of Energy and Mineral Resources (MEMR) formulated a Geothermal Development Road Map to develop 9,500 MW in total by 2025.

3.2 Recent Investment Environment for Geothermal Projects

Under the Indonesian constitutional framework, Indonesia's geothermal resources are

controlled by the state. A new Geothermal Law was enacted on October 22, 2003 in order to provide a stronger legal basis for upstream geothermal energy developments, including private investment in the sector. The new Geothermal Law is also intended to accommodate expanded regional autonomy in Indonesia. Within their respective jurisdictions, provincial and local governments are given the authority to regulate, supervise and license geothermal energy developments. In the period until the Asian Economic Crisis in 1997, PT PLN had bought geothermal energy at the price between 6.90 USD Cents/kWh and 8.46 USD Cents/kWh. However, to cope with the crisis, PT PLN reviewed the purchase prices and decided to set forth the ceiling of 5 USD Cents/kWh from 1999 to 2003. As a result, the purchase prices of geothermal were remarkably reduced and, it was 4.85 USD Cents/kWh in 2005 in the Darajat II project case for example. This reduction obviously discouraged the private geothermal development activities (Fig. 3.4-1). In addition no IUP pursuant to the new geothermal law has been issued since new law’s promulgation in 2003. The following factors explain Indonesia’s lagging development of its geothermal resource for generating electricity: ① Commercial development of geothermal energy requires electrical power plant

development onsite, and this requirement may limit the resource to a small local market or one not well connected to a larger load center.

② Development entails high initial capital costs, including initial exploration, and requires a commitment to purchase a large portion of generated energy at the stage of start-up of development wells. Long-term operating costs, however, are quite low. Thus, geothermal

JICA West JEC 6

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

contracts require base load status and long term price security in order to justify development.

③ Several significant benefits of geothermal development are not effectively represented in the valuation of the electricity. These benefits include the long-term low cost operation, contributions to preserving the environment, and the resultant diversification of supply with an indigenous, distributed resource.

( Source ) Schlumberger Business Consulting, Improving the economics of geothermal development through an oil and gas industry approach

Fig.3.4-1 Selling prices and geothermal activities 3.3 Evaluation of Recent Geothermal Incentives

< Geothermal Work Area Bidding System > From 2008, the Ministry of Energy and Mineral Resources (MEMR) started bidding

for geothermal working areas. First, the government made bids for the geothermal fields of Cisoroku-Cisukarame, Tangkuban Parahu and Gunung Tampomas, all in West Java. By this bidding, however, some working areas development went to corporations who are not considered to be well experienced. It is pointed out that the strict Pre-Qualification (P/Q) process is needed and that the system of bidding a possible electric selling price should be reformed.

< Bench-mark Purchase Price of Geothermal Electricity> To promote geothermal power development in the country, the MEMR set the

benchmark electric purchase price from the geothermal power in January 2006. The benchmark prices were revised annually through DGEEU under the MEMR. The benchmark prices was calculated as a percentage of the present average generating costs of PT PLN at each of 21 subsystems of 14 power systems. Geothermal power development was divided into two categories: 10 MW to 55 MW and more than 55 MW. For the 10 MW to 55 MW class, 85% of the present generating cost was specified as the benchmark price, and this fell to 80% for 55 MW class geothermal plants. The benchmark prices were at slightly less than 5 USD Cents/kWh in West Sumatra where large-scale geothermal plants are expected. There were several complaints from geothermal investors about these benchmark prices. The complaints were that the price would fluctuate every year, that the procedure of price calculation was not disclosed

JICA West JEC 7

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

and not clear, that the prices did not take into account geothermal resource potentials in the areas, that the prices were too low to attract geothermal investment, and so on. A new price guideline has been definitely required to accelerate geothermal power development.

<Guidelines for Electric Power Purchase Price by PT PLN (MEMR Regulation No. 5/2009)>

In the backdrops of these complaints, Ministry of Energy and Mineral Resources announced the Ministerial Regulation on Guidelines for Electric Power Purchase price by PT PLN (MEMR regulation No.5/2009) in March, 2009. This regulation abolished the provisions of the benchmark purchase price of geothermal energy designated by MEMR, and instead newly stipulates that PT PLN can set forth the self-estimation price for renewable energy and can purchase renewable energy at the price when it is approved by MEMR. At the same time, the government obliged PT PLN to purchase renewable energy up to 10 MW capacity. As for this new regulation, however, there is an opinion that this regulation is incomplete as an energy policy.

JICA West JEC 8

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

JICA West JEC 9

CHAPTER 4 CONDITIONS FOR ATTRACTIVE IPP PROJECTS IPP projects have various stakeholders, as shown in Fig.4-1. An IPP project is obliged

to distribute the promised returns to these stakeholders through sound operation of the project. For this purpose, the project must earn sufficient revenues. As an indicator for profitability of the project as a whole, Project IRR (internal rate of return) may be useful. The stakeholders must manage to maintain Project IRR higher than their criteria level (PrIRR )c to secure sufficient profit. Also, as the first stakeholder, the investors need to be confident of the project’s future profitability against their initial equity investments. For this purpose, the investors pay attention to the level of Equity IRR. They commit to invest only when the Equity IRR of a project is higher that their criteria level (EqIRRc). Therefore, in order to realize a project, the profitability forecast of project must satisfy these 2 conditions stated above.

Pr (4.1) cIRRIRR Pr≥

(4.2) cEqIRREqIRR ≥

In executing a project, another factor more important than profitability is the business

risk. The business risk is the possibility of the project failing to achieve the expected rate of return. If the possibility of the project failing is big, the project is considered to be high risk. Therefore, another condition for realizing an IPP project is the following.

Project Risk → zero or minimal (4.3)

E L

Shareholders Lenders

EPC OM

Off Taker

Equity

DividendLoan Repayment

Interest

PPA

Construction FOM,VOM

Fuel Supplier

FSA

E L

Shareholders Lenders

EPC OM

Off Taker

Equity

DividendLoan Repayment

Interest

PPA

Construction FOM,VOM

Fuel Supplier

FSA

Fig. 4-1 An IPP project and its stakeholders

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

CHAPTER 5 EVALUATION OF A COAL-FIRED IPP PROJECT (BENCHMARK PRICE)

5.1 Assumptions

This Chapter aims to calculate the selling price of electricity from a coal-fired IPP

project. Generation capacity is assumed to be 600 MW, which is commonly found in Indonesia. The construction cost is assumed to be USD 726 million (1,210 USD/kW) over a 4-year construction period. The heat value of coal used in this calculation is 5,300 kcal/kg and its price is assumed to be 90 USD/ton for the evaluation period.

Table 5.1-1 Specifications of benchmark coal-fired IPP project

Items Specifications Remarks

Capacity 600 MW 1unit Construction cost USD 726 million

(w/o interest) USD 800 million (with interest)

Construction cost per kW 1,210 USD/kW (w/o interest)

1,340 USD/kW (with interest)

Construction Period 4 years Heat efficiency 38% Heat value of fuel 5,300 kcal/kg Fuel price 90 USD/ton See research assumption Operation term 30 years Price calculation is based on a

15-year term

The assumed leverage ratio is 30% equity and 70% loan. The loan conditions comply with the “Arrangement on officially supported export credits” of OECD, and the assumed interest rate is 6.5%. The assumed loan period is 15 years (including a 3-year grace period). Lenders are all assumed to be foreign banks and no domestic banks are included.

The Weighted Average Capital Cost (WACC) of a coal-fired IPP project is as shown in

the following formula:

⎟⎠⎞

⎜⎝⎛

++⎟

⎠⎞

⎜⎝⎛

+=

DEEr

DEDrWACC ed ** (5.1)

References: rd:Capital Costs for Loan(Interest)

re:Capital Costs for Equity D:Loan amount

JICA West JEC 10

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

E;Equity amount

The Capital Costs for Equity can be calculated by CAPM(Capital Asset Price Model)theory, which makes the Capital Costs for Equity as follows:

(5.2) )(* fmfe rrrr −+= β

rf:Rate of Return of risk-free business rm:Average Rate of Return in the market β:coefficient β of investor

In this Study, participating investors are assumed to be from any country, not limited

to Indonesia or Japan alone. Therefore, the 10-year maturity US Treasury Bond, which has yielded an average of 5% during the last 15 years, is taken as the risk-free business reference. Also, the Average Rate of Return in the market is assumed to be 10% for the 15 years of record. Considering the fact that the major participants of IPP projects are power companies, β=1 is applied, assuming the same risk as in the market. Based on these assumptions:

%10%)5%10(*1%5 =−+=er (5.2’)

After factoring in the 2% country risk, we have: re=12% (5.2”)

This yields the following WACC: %15.8%30*%12%70*%5.6 =+=WACC (5.1’) 5.2 Risk Analysis

Typical examples of possible commercial risks for coal-fired IPP projects are interest rate fluctuation during construction, construction cost increases, inflation after commencement of commercial operation, exchange rate fluctuations after commercial operation begins, and so on. These risk factors are evaluated by using Monte Carlo method. As a result, the Study Team adopts a Commercial Risk Margin (RMc) of 3% in order to account for a case where each factor takes an unfavorable value. RMc = 3% (5.4)

As for the technical risks, unlike the geothermal IPP business, the coal-fired IPP business does not have significant technical risks. Thus, the Study Team assumes a Technical Risk Margin (RMt) of 0%.

RMt = 0% (5.5) The above conditions give a Project IRR requirement of 11.2%.

JICA West JEC 11

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

%2.11%3%15.8Pr =+=++= RMtRMcWACCIRR (5.6) Also, the Equity IRR requirement is 12%. EqIRR=12% (5.7) 5.3 Benchmark Price

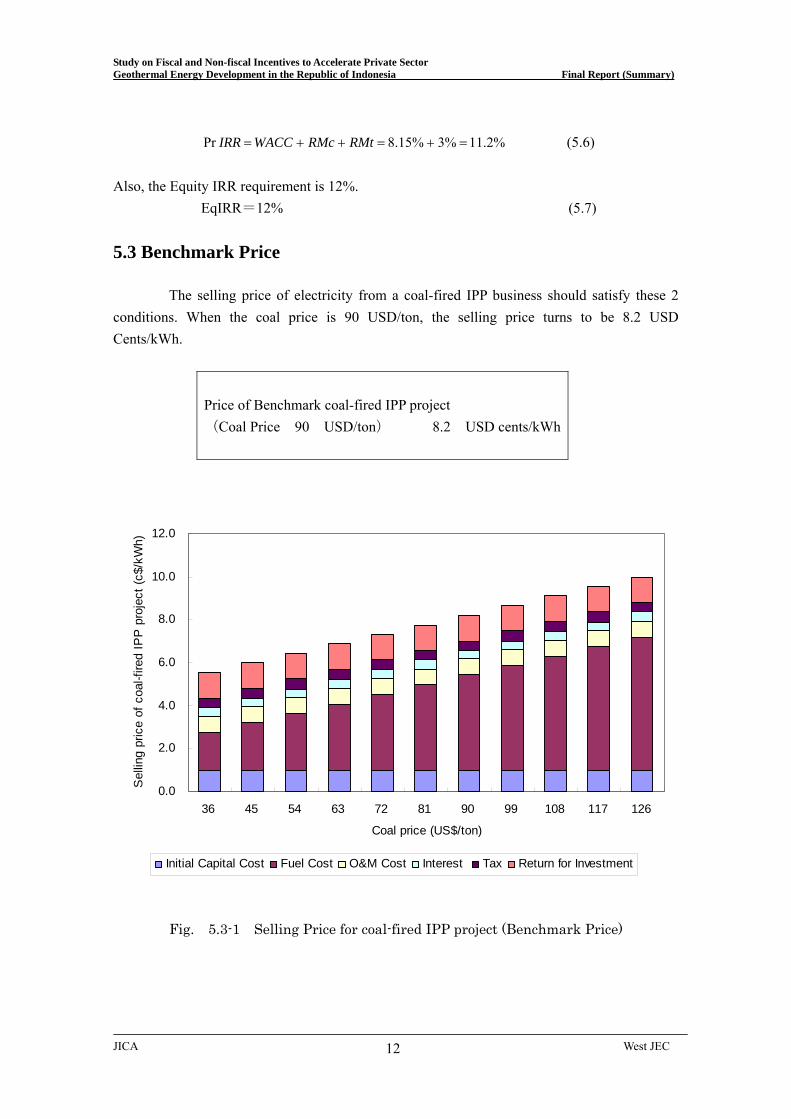

The selling price of electricity from a coal-fired IPP business should satisfy these 2 conditions. When the coal price is 90 USD/ton, the selling price turns to be 8.2 USD Cents/kWh.

Price of Benchmark coal-fired IPP project (Coal Price 90 USD/ton) 8.2 USD cents/kWh

0.0

2.0

4.0

6.0

8.0

10.0

12.0

36 45 54 63 72 81 90 99 108 117 126

Coal price (US$/ton)

Sel

ling

pric

e of

coa

l-fire

d IP

P p

roje

ct (c

$/kW

h)

Initial Capital Cost Fuel Cost O&M Cost Interest Tax Return for Investment

Fig. 5.3-1 Selling Price for coal-fired IPP project (Benchmark Price)

JICA West JEC 12

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

CHAPTER 6 EVALUATION OF A GEOTHERMAL IPP PROJECT 6.1 Assumptions

This Chapter aims to calculate the selling price of electricity generated by a

geothermal IPP project. Major characteristics of the model case are as shown in Table 6.1-1.

Table 6.1-1 Specification of geothermal IPP project

Items Specifications Remarks Capacity 60 MW 1unit Construction costs USD 180 million

(w/o interest) USD 190 million (with interest)

Construction costs per kW 3,010 USD/kW (w/o interest)

3,170 USD/kW (with interest)

Construction period 6 years Production well depth 2,000 m Production well steam output 8 MW/well Generation efficiency 7.0 t/h/MW Operation term 30 years Price calculated based on

15 year term Make up wells One every 5 years

As for the development process, the following is assumed: - Surface survey - Resource confirmation survey: 2 years - Development(Resource evaluation): 2 years - Construction: 2 years ( Total development lead time): (6 years) - Commercial Operation: 30 years

Geothermal energy development involves significant risks during the surface survey,

resource confirmation and development stages. Since a project has little chance of obtaining financial support in the early stages, its early stage development may need to be conducted with equity alone. After a certain level of progress, the project can acquire funding from banks, leveraged with a ratio of 70% debt to 30% equity. Like the coal-fired plant case, the interest rate is assumed to be 6.5%. The loan period is 15 years.

JICA West JEC 13

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Lead Time Development Stage Activity Finance

2 Years

2 Years

2 Years

30 Years

Surface Survey Stage

Resource Confirmation Stage

Construction Stage

Development Stage(Reservoir Evaluation Stage)

Operation Stage

Development Process of 60 MW Model Case

Surface survey (Geology,Geochemical, Geophysics MT, etc)

To Find steam (Approximately 10%)Drilling 2 wells → 1 well success

To confirm 40% of steam,Drilling 3 wells → 2 well success

To obtain 100% steam,Drilling 8 wells → 6 well success

Equity 100%

Equity 30% Debt 70%

Equity 100% Debt 0%

Equity 100%

Operation & Maintenance Expenditure

Fig. 6.1-1 Geothermal development process for 60 MW plant

The WACC of the geothermal IPP project is calculated as follows:

⎟⎠⎞

⎜⎝⎛

++⎟

⎠⎞

⎜⎝⎛

+=

DEEr

DEDrWACC ed ** (6.1)

References: rd:Capital Costs for Loan(Interest)

re:Capital Costs for Equity D:Loan amount E;Equity amount

Note: E=E1+E2+E3

E1:Equity to cover early stage survey E2:Equity to cover development stage E3:Equity to cover construction stage

The CAPM theory is also applied to Capital Costs for Equity. CAPM gives as follows:

r (6.2) )(* fmfe rrr −+= β

rf:Rate of Return of risk-free business rm:Average Rate of Return of market β:coefficient β of investor

In case of model geothermal IPP project, the Rate of Return of risk-free business is

JICA West JEC 14

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

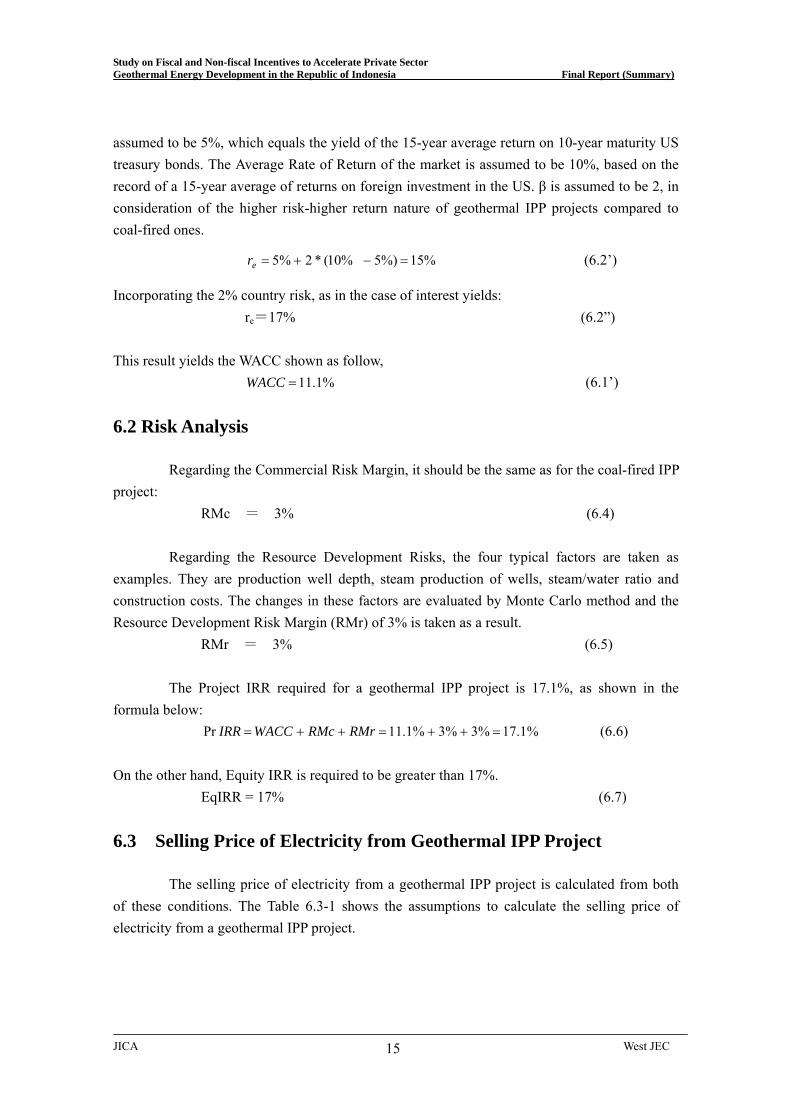

assumed to be 5%, which equals the yield of the 15-year average return on 10-year maturity US treasury bonds. The Average Rate of Return of the market is assumed to be 10%, based on the record of a 15-year average of returns on foreign investment in the US. β is assumed to be 2, in consideration of the higher risk-higher return nature of geothermal IPP projects compared to coal-fired ones.

%15%)5%10(*2%5 =−+=er (6.2’)

Incorporating the 2% country risk, as in the case of interest yields: re=17% (6.2”)

This result yields the WACC shown as follow, (6.1’) %1.11=WACC 6.2 Risk Analysis

Regarding the Commercial Risk Margin, it should be the same as for the coal-fired IPP project: RMc = 3% (6.4)

Regarding the Resource Development Risks, the four typical factors are taken as examples. They are production well depth, steam production of wells, steam/water ratio and construction costs. The changes in these factors are evaluated by Monte Carlo method and the Resource Development Risk Margin (RMr) of 3% is taken as a result. RMr = 3% (6.5)

The Project IRR required for a geothermal IPP project is 17.1%, as shown in the formula below: %1.17%3%3%1.11Pr =++=++= RMrRMcWACCIRR (6.6) On the other hand, Equity IRR is required to be greater than 17%. EqIRR = 17% (6.7) 6.3 Selling Price of Electricity from Geothermal IPP Project

The selling price of electricity from a geothermal IPP project is calculated from both of these conditions. The Table 6.3-1 shows the assumptions to calculate the selling price of electricity from a geothermal IPP project.

JICA West JEC 15

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Table 6.3-1 Assumptions for calculation of Geothermal Price

Items Specifications Depreciation period Wells : 8 years

Generation machines and equipment: 8 years (Originally category –III applies to geothermal plants, but category –II can apply as a tax incentive since 2008.)

Depreciation method Double declining balance method Tax rate Corporate tax: 25% (From 2010)

Withholding tax on dividends: 10% Tax incentives 1. 7 years loss carry forward

2. 30% Investment Allowance (5% per ann., 6 years)

The above assumptions yield a selling price of 11.9 USD Cents/kWh.

Electricity price of Geothermal IPP project 11.9 USD Cents/kWh

There is a 3.7 USD Cents/kWh difference between this price and the price for the

benchmark coal-fired IPP project, which is 8.2 USD Cents/kWh. The objective of this Study is to bridge this price gap by fiscal incentives.

Price for Geothermal IPP project 11.9 USD Cents/kWh Price for Benchmark Coal-fired IPP project 8.2 USD Cents/kWh Price Gap 3.7 USD Cents/kWh

JICA West JEC 16

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

CHAPTER 7 BENEFITS OF GEOTHERMAL POWER DEVELOPMENT

7.1 Power Demand and Supply Simulation

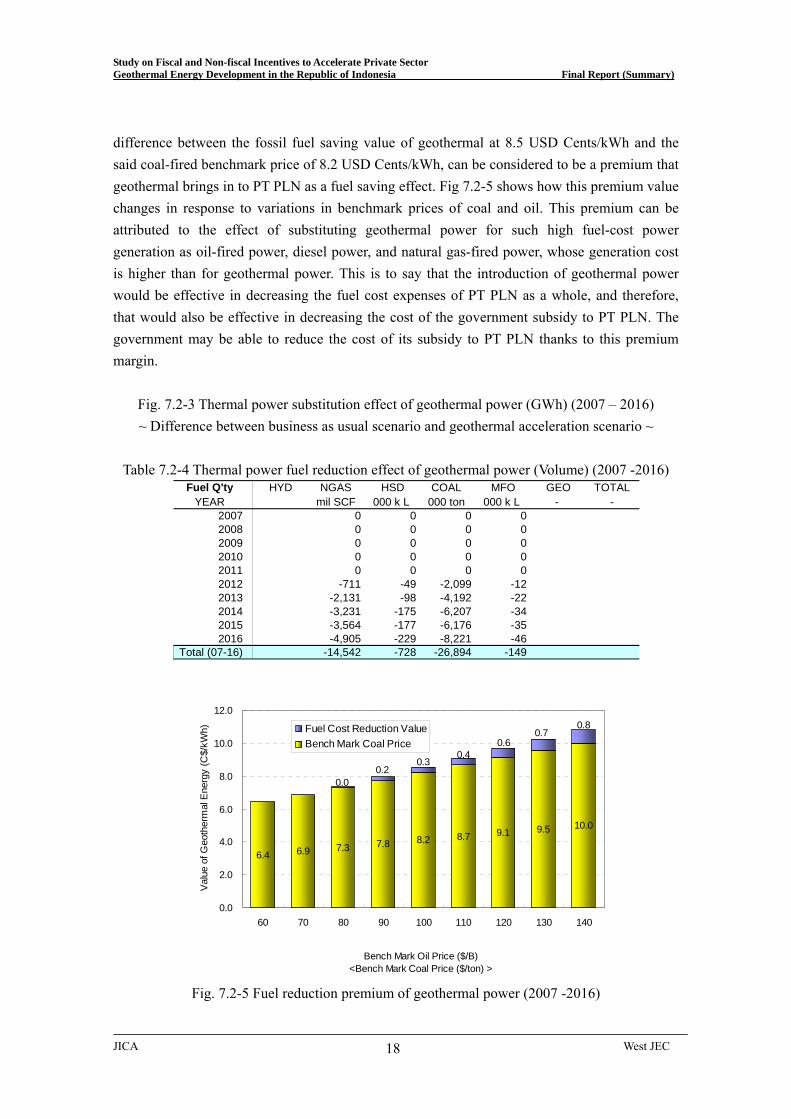

Prior to consider incentives, the benefits of geothermal power development are discussed in Chapter 7. In order to calculate the geothermal energy benefits, two cases of power demand and supply scenario are simulated, i.e. the business as usual case and the geothermal promotion case. The benefits of geothermal energy are derived from comparing fuel consumptions in two cases. The simulation period is from 2007 to 2016. While 23,400 MW new power plants are needed by 2016 in both cases, all of them are coal-fired plants in the business as usual case. On the other hand, in the geothermal promotion case, 2,400 MW of them are geothermal power plants and the rest are coal-fired power plants. 7.2 Fuel Saving Benefit (Reduction of PT PLN Generation Costs) Table 7.2-3 shows the differences between two cases in the fuel types of generated energy. The simulations reveal that when an additional 2,400 MW of geothermal power is developed by the year 2016, the generated geothermal energy would be 59,151 GWh and would substitute for a sum of 54,396 GWh (92.0%) of coal-fired power, 2,527 GWh (4.3%) of gas-turbine and diesel power, 1,577 GWh (2.7%) of natural gas-fired power and 535 GWh (0.9%) of oil-fired power. Considering installed capacities, 2,400 MW of geothermal power would substitute for the same capacity of coal-fired power, but considering the generated energy, geothermal would substitute not only for coal-fired but also for gas-turbine and diesel power, natural gas-fired power and oil-fired power, though the substituted energy for this oil-related power is considerably smaller than that for coal-fired power. This difference of energy generation can be translated into the difference of the volumes and values of fuels saved by geothermal energy. This translation reveals that the introduction of geothermal power would save a remarkable amount of fossil fuel consumption over the 5 years from 2012 to 2016: 26,894,000 tons of coal, 728,000 kl of diesel oil (HSD), 14,542 million SCF of natural gas and 149,000 kl of heavy oil (MFO). When oil price is at 100 USD/barrel, these volume savings turn to be the monetary savings of USD 5,034 million over the 5 years. As mentioned above, 59,151 GWh of geothermal power will be generated over this period. Thus, the fossil fuel saving value of geothermal power is 8.5 USD Cents/kWh. By the way, the selling price of electricity from coal-fired power plants, or the benchmark price, is 8.2 USD Cents/kWh where the coal unit price is 90 USD/ton, corresponding to the benchmark oil price of 100 USD/barrel. Thus, 0.3 USD Cents/kWh, the

JICA West JEC 17

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

JICA West JEC 18

difference between the fossil fuel saving value of geothermal at 8.5 USD Cents/kWh and the said coal-fired benchmark price of 8.2 USD Cents/kWh, can be considered to be a premium that geothermal brings in to PT PLN as a fuel saving effect. Fig 7.2-5 shows how this premium value changes in response to variations in benchmark prices of coal and oil. This premium can be attributed to the effect of substituting geothermal power for such high fuel-cost power generation as oil-fired power, diesel power, and natural gas-fired power, whose generation cost is higher than for geothermal power. This is to say that the introduction of geothermal power would be effective in decreasing the fuel cost expenses of PT PLN as a whole, and therefore, that would also be effective in decreasing the cost of the government subsidy to PT PLN. The government may be able to reduce the cost of its subsidy to PT PLN thanks to this premium margin.

Fig. 7.2-3 Thermal power substitution effect of geothermal power (GWh) (2007 – 2016) ~ Difference between business as usual scenario and geothermal acceleration scenario ~

Table 7.2-4 Thermal power fuel reduction effect of geothermal power (Volume) (2007 -2016)

Fuel Q'ty HYD NGAS HSD COAL MFO GEO TOTALYEAR mil SCF 000 k L 000 ton 000 k L - -

2007 0 0 0 02008 0 0 0 02009 0 0 0 02010 0 0 0 02011 0 0 0 02012 -711 -49 -2,099 -122013 -2,131 -98 -4,192 -222014 -3,231 -175 -6,207 -342015 -3,564 -177 -6,176 -352016 -4,905 -229 -8,221 -46

Total (07-16) -14,542 -728 -26,894 -149

6.4 6.9 7.3 7.8 8.2 8.7 9.1 9.5 10.0

0.80.7

0.60.4

0.30.2

0.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

60 70 80 90 100 110 120 130 140

Bench Mark Oil Price ($/B)<Bench Mark Coal Price ($/ton) >

Val

ue o

f Geo

ther

mal

Ene

rgy

(C$/

kWh) Fuel Cost Reduction Value

Bench Mark Coal Price

Fig. 7.2-5 Fuel reduction premium of geothermal power (2007 -2016)

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

JICA West JEC 19

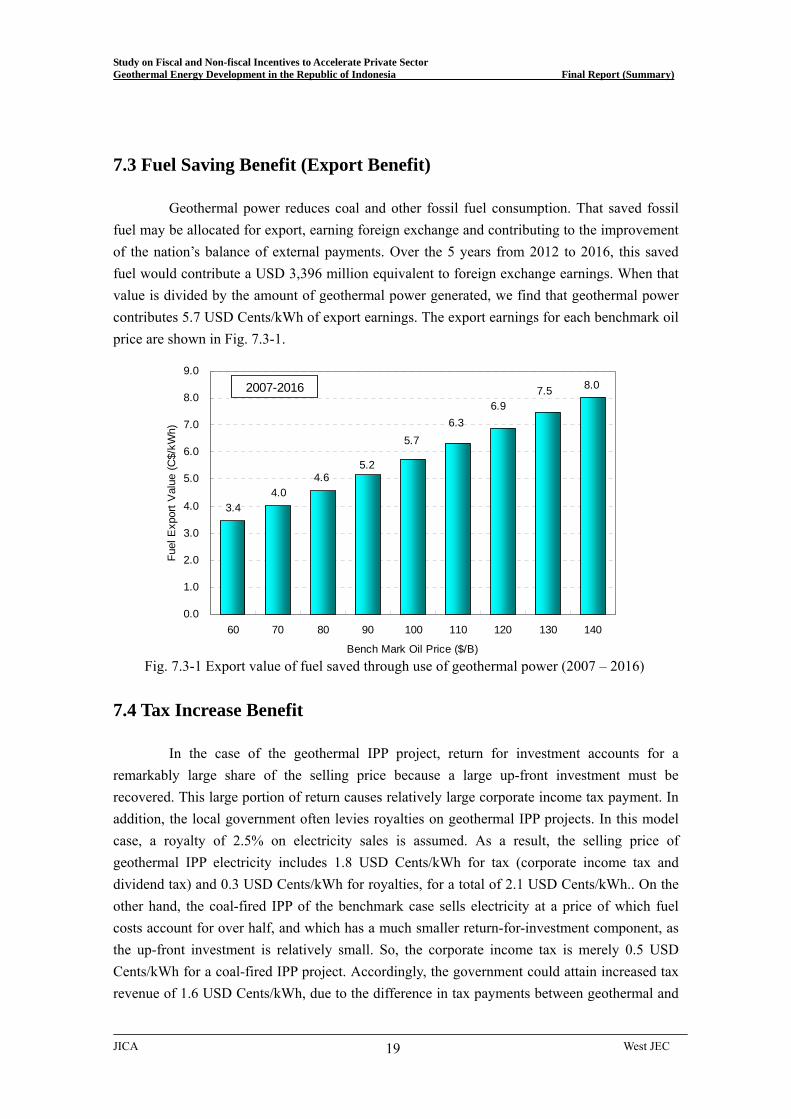

7.3 Fuel Saving Benefit (Export Benefit) Geothermal power reduces coal and other fossil fuel consumption. That saved fossil fuel may be allocated for export, earning foreign exchange and contributing to the improvement of the nation’s balance of external payments. Over the 5 years from 2012 to 2016, this saved fuel would contribute a USD 3,396 million equivalent to foreign exchange earnings. When that value is divided by the amount of geothermal power generated, we find that geothermal power contributes 5.7 USD Cents/kWh of export earnings. The export earnings for each benchmark oil price are shown in Fig. 7.3-1.

8.0

3.44.0

4.65.2

5.76.3

6.97.5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

60 70 80 90 100 110 120 130 140

Bench Mark Oil Price ($/B)

Fuel

Exp

ort V

alue

(C$/

kWh)

2007-2016

Fig. 7.3-1 Export value of fuel saved through use of geothermal power (2007 – 2016)

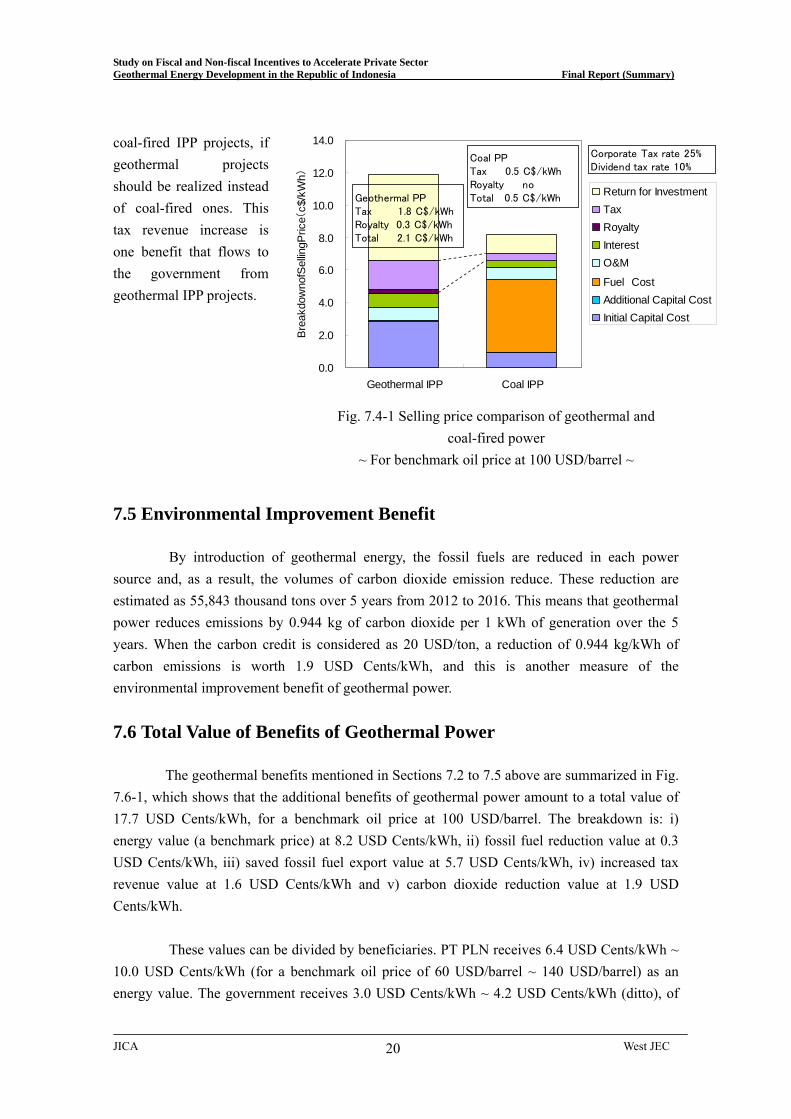

7.4 Tax Increase Benefit In the case of the geothermal IPP project, return for investment accounts for a remarkably large share of the selling price because a large up-front investment must be recovered. This large portion of return causes relatively large corporate income tax payment. In addition, the local government often levies royalties on geothermal IPP projects. In this model case, a royalty of 2.5% on electricity sales is assumed. As a result, the selling price of geothermal IPP electricity includes 1.8 USD Cents/kWh for tax (corporate income tax and dividend tax) and 0.3 USD Cents/kWh for royalties, for a total of 2.1 USD Cents/kWh.. On the other hand, the coal-fired IPP of the benchmark case sells electricity at a price of which fuel costs account for over half, and which has a much smaller return-for-investment component, as the up-front investment is relatively small. So, the corporate income tax is merely 0.5 USD Cents/kWh for a coal-fired IPP project. Accordingly, the government could attain increased tax revenue of 1.6 USD Cents/kWh, due to the difference in tax payments between geothermal and

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

0.0

2.0

4.0

6.0

8.0

10.0

12.) 0

14.0

Geothermal IPP Coal IPP

Bre

akdo

wno

fSel

lingP

rice(

c$/k

Wh

Return for Investment TaxRoyaltyInterestO&M

Fuel CostAdditional Capital Cost Initial Capital Cost

Geothermal PPTax 1.8 C$/kWhRoyalty 0.3 C$/kWhTotal 2.1 C$/kWh

Coal PPTax 0.5 C$/kWhRoyalty noTotal 0.5 C$/kWh

Corporate Tax rate 25%Dividend tax rate 10%

coal-fired IPP projects, if geothermal projects should be realized instead of coal-fired ones. This tax revenue increase is one benefit that flows to the government from geothermal IPP projects.

Fig. 7.4-1 Selling price comparison of geothermal and coal-fired power

~ For benchmark oil price at 100 USD/barrel ~

7.5 Environmental Improvement Benefit By introduction of geothermal energy, the fossil fuels are reduced in each power source and, as a result, the volumes of carbon dioxide emission reduce. These reduction are estimated as 55,843 thousand tons over 5 years from 2012 to 2016. This means that geothermal power reduces emissions by 0.944 kg of carbon dioxide per 1 kWh of generation over the 5 years. When the carbon credit is considered as 20 USD/ton, a reduction of 0.944 kg/kWh of carbon emissions is worth 1.9 USD Cents/kWh, and this is another measure of the environmental improvement benefit of geothermal power.

7.6 Total Value of Benefits of Geothermal Power The geothermal benefits mentioned in Sections 7.2 to 7.5 above are summarized in Fig. 7.6-1, which shows that the additional benefits of geothermal power amount to a total value of 17.7 USD Cents/kWh, for a benchmark oil price at 100 USD/barrel. The breakdown is: i) energy value (a benchmark price) at 8.2 USD Cents/kWh, ii) fossil fuel reduction value at 0.3 USD Cents/kWh, iii) saved fossil fuel export value at 5.7 USD Cents/kWh, iv) increased tax revenue value at 1.6 USD Cents/kWh and v) carbon dioxide reduction value at 1.9 USD Cents/kWh.

These values can be divided by beneficiaries. PT PLN receives 6.4 USD Cents/kWh ~ 10.0 USD Cents/kWh (for a benchmark oil price of 60 USD/barrel ~ 140 USD/barrel) as an energy value. The government receives 3.0 USD Cents/kWh ~ 4.2 USD Cents/kWh (ditto), of

JICA West JEC 20

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

JICA West JEC 21

6.4 6.9 7.3 7.8 8.2 8.7 9.1 9.5 10.0

0.00.0

0.00.2

0.30.4

0.60.7

0.8

3.44.0

4.65.2

5.76.3

6.97.5

8.0

1.61.6

1.6

1.6

1.6

1.6

1.6

1.6

1.6

1.91.9

1.9

1.9

1.9

1.9

1.9

1.9

1.9

0.0

5.0

10.0

15.0

20.0

25.0

60 70 80 90 100 110 120 130 140

Bench Mark Oil Price ($/B)<Bench Mark Coal Price ($/ton)>

Valu

e o

f G

eot

herm

al E

nerg

y (

C$/k

Wh)

CO2 Reduction Value (20$/ton)

Tax Value

Fuel Export ValueFuel Cost Reduction Value

Bench Mark Coal Energy Price

2007-2016

14.4

22.321.2

20.018.9

17.716.6

15.5

13.4

<54> <63> <72> <81> <90> <99> <108> <117> <126>

which the breakdown is: (i) fuel cost reduction value as subsidy reduction to PT PLN, (ii) 32.5% (tax rate) of fuel export value, and (iii) tax increase value. The society receives 4.2 USD Cents/kWh ~ 7.3 USD Cents/kWh as the remaining fuel export value and environment value (at 20 USD/ton CO2 credit price). These benefits show that geothermal power can bring remarkable benefits to PT PLN, the government and the society, if it is well developed.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Value component Beneficiary

Valu

e of

Geo

ther

mal

Ene

rgy

(C$/

kWh)

Environmental Value

Energy ValuePLN

Social

GovernmentTax Value

Fuel Export Value

Fuel Cost Reduction Value

x 32.5% Tax rate

Fig. 7.6-1 Total value of benefits of geothermal power generation (2007 – 2016)

Fig. 7.6-2 Total value of benefits of geothermal power and its beneficiaries

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

Ripple effect of cons uction investment of 60 MW class geothermal power plant in Indonesian trbRP: billion Rupia

Purchase in domesticmarket

Production increase(primary)

Demand increase in each industry

Wage increaseEmployment increase

(primary)

Employment increase(secondary)

Production increase(secondary)

Consumption increase

Prim

ary

effect

Seconda

ry e

ffect

1,043 bRp

2,596 psn

7,464 psn

83 bRp

150 bRp

136 bRp

1,526 bRp

Employment increase(primary + secondary)

Production increase(primary + secondary)

Tota

l eff

ect

1,662 bRp(multiplier effect 1.59 times)

10,060 psn

7.7 Construction Effects of Geothermal Power Plants

While a thermal power plant can be completed largely off-site, construction of a

Fig. 7.7-1 Ripple effect of 60 MW geothermal power plant construction

geothermal power plant is site-specific and involves a lot of drillings and civil work at the site. So geothermal power plant construction relies heavily on the procurement of work and services from the vicinity of the construction site. That induces domestic demand increases in the country and stimulates the domestic economy. These ripple effects are calculated using the Input-Output Table for Indonesia. As a result, it is calculated that a direct domestic procurement from local industries amounting to IDR 1,043 billion in a model geothermal project case brings about an increase of domestic production of IDR 1,662 billion which is about a 1.59 multiplier effect on the initial procurement. In terms of employment, it is also calculated that geothermal plant construction will have a significant job-creating effect as large as 10,060 opportunities.

JICA West JEC 22

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

JICA West JEC 23

CHAPTER 8 SHORT-TERM INCENTIVES TO PROMOTE GEOTHERMAL DEVELOPMMENT

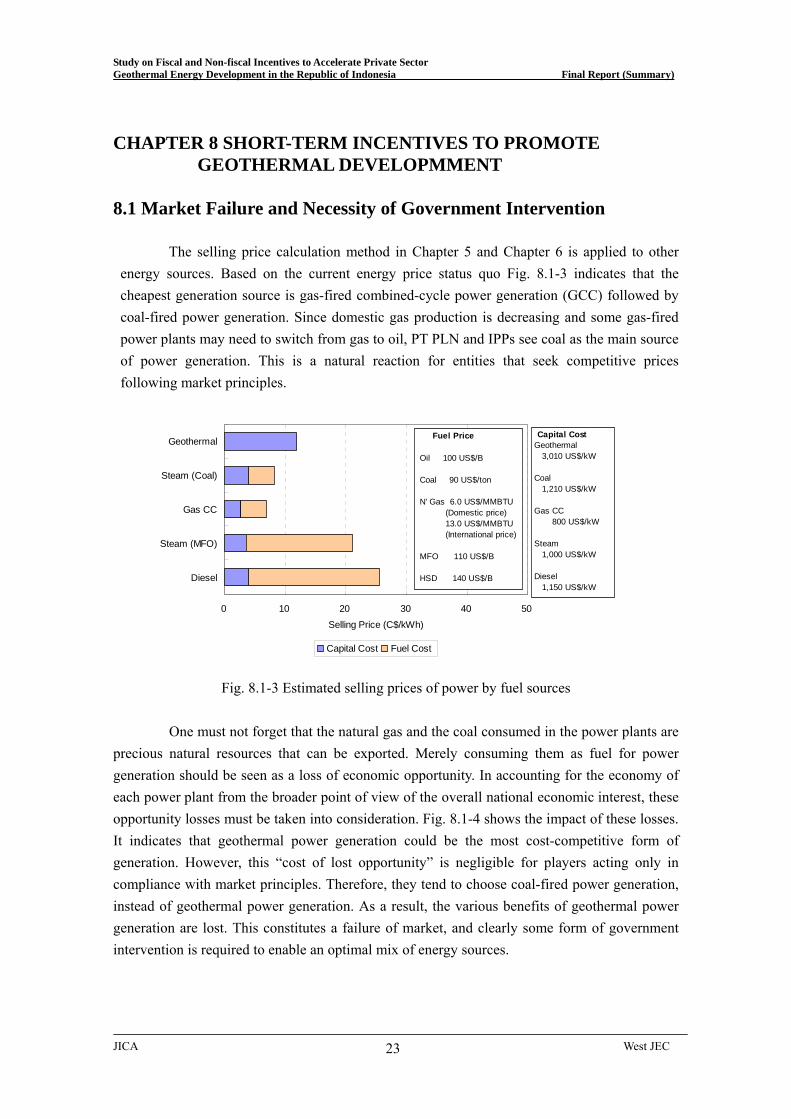

8.1 Market Failure and Necessity of Government Intervention

The selling price calculation method in Chapter 5 and Chapter 6 is applied to other energy sources. Based on the current energy price status quo Fig. 8.1-3 indicates that the cheapest generation source is gas-fired combined-cycle power generation (GCC) followed by coal-fired power generation. Since domestic gas production is decreasing and some gas-fired power plants may need to switch from gas to oil, PT PLN and IPPs see coal as the main source of power generation. This is a natural reaction for entities that seek competitive prices following market principles.

0 10 20 30 40 50

Diesel

Steam (MFO)

Gas CC

Steam (Coal)

Geothermal

Selling Price (C$/kWh)

Capital Cost Fuel Cost

Fuel Price

Oil 100 US$/B

Coal 90 US$/ton

N' Gas 6.0 US$/MMBTU (Domestic price) 13.0 US$/MMBTU (International price)

MFO 110 US$/B HSD 140 US$/B

Capital CostGeothermal 3,010 US$/kW

Coal 1,210 US$/kW

Gas CC 800 US$/kW

Steam 1,000 US$/kW

Diesel 1,150 US$/kW

Fig. 8.1-3 Estimated selling prices of power by fuel sources

One must not forget that the natural gas and the coal consumed in the power plants are precious natural resources that can be exported. Merely consuming them as fuel for power generation should be seen as a loss of economic opportunity. In accounting for the economy of each power plant from the broader point of view of the overall national economic interest, these opportunity losses must be taken into consideration. Fig. 8.1-4 shows the impact of these losses. It indicates that geothermal power generation could be the most cost-competitive form of generation. However, this “cost of lost opportunity” is negligible for players acting only in compliance with market principles. Therefore, they tend to choose coal-fired power generation, instead of geothermal power generation. As a result, the various benefits of geothermal power generation are lost. This constitutes a failure of market, and clearly some form of government intervention is required to enable an optimal mix of energy sources.

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

JICA West JEC 24

0 10 20 30 40 50

Diesel

Steam (MFO)

Gas CC

Steam (Coal)

Geothermal

Selling Price (C$/kWh)

Capital Cost Fuel Cost Opportunity Cost

Oppotunity Cost (= Fuel Cost)Geothermal NO Coal 4.2 C$/kWh Gas CC (for LNG) 9.3 C$/kWh

Steam 17.6 C$/kWh

Diesel 21.7 C$/kWh

Fig. 8.1-4 Estimated selling prices of power taking into account opportunity costs

Furthermore, we can consider the environmental impact of thermal power plants. Thermal power plants emit greenhouse gases such as SOx, NOx, dust and CO2. Although the global trend is to reduce greenhouse gas emissions, these environmental costs are not considered to be the responsibility of emitters. This means that the emissions of power suppliers are an externality which the local government pays a price for. Fig. 8.1-5 represents these impacts. Economics sees these externalities created by “demerit goods” as indicating a failure of markets and the necessity of encouraging government intervention. Geothermal power generation brings direct and indirect benefits to society and the government. However, these benefits are not considered in the power generation market, and they are therefore lost in the market mechanism. In order to realize these benefits, the government needs to intervene in the market.

0 10 20 30 40 50

Diesel

Steam (MFO)

Gas CC

Steam (Coal)

Geothermal

Selling Price (C$/kWh)

Capital Cost Fuel Cost Opportunity Cost Environmental Cost

CO2 Price 20 US$/ton CO2

CO2 EmissionFactorGeothermal 0.002 kg/kWh Coal 0.957 kg/kWh Gas CC 0.421 kg/kWh

Steam 0.734 kg/kWh

Diesel 0.702 kg/kWh

(Note) CO2 emission factor of geothermal refers to CRIEPI Review No.45 2001 (Nov)

CO2 emission factor of other fuel refers to 2006 IPCC Guideline for National Greenhouse Gas Inventories

Fig. 8.1-5 Estimated selling price of power accounting for environmental impact costs

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

JICA West JEC 25

8.2 Geothermal Energy Promotion Policy

Geothermal energy promotion policy can be divided into compulsory-type policy, which obliges power companies (or end-users) to bear the costs, and incentive-type policy, in which the government bears the costs. Compulsory-type policy includes a fixed price buying system and a renewable energy quota system. On the other hand, incentive-type policy includes tax incentives, fiscal incentives and financial incentives. Table 8.2-1 shows the characteristics of these policies.

Geothermal power generation brings about various benefits for the society and the government. However, because of its higher price compared with benchmark coal-fired power generation, the market alone does not promote geothermal power generation automatically. Therefore, government interventions are required to realize the benefits of geothermal power generation.

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

JICA West JEC 26

Table 8.2-1 Classification of Renewable Energy Promotion Policies

Type Policy Contents Cost bearer Advantages Disadvantages Examples Fixed Buying Price System

・The government specifies the purchase price for the forced purchase of renewable energy (RE).

・The price is specified as a certain rate (e.g. 90 %) of the tariff or an absolute price (e.g. 7.0 USD cents/kWh)

・ If the price level is appropriate, it will expedite RE rapidly (examples: wind power in Germany and Denmark).

・ RE power company is able to make the investment stable.

・ The cost to utilities is heavy. ・ There is little incentive to

reduce RE costs. ・ The setting of the price level

is difficult and when it is set too low, the RE introduction does not proceed.

PURPA law (U.S.A.) Power purchase law (Germany)

Compulsory Type

Quota System ・ To make the introduction of REs compulsory, government forces power companies to generate a certain amount of electricity from RE itself or purchase RE from outside.

・ The method in which the ratio of REs to the total generated energy is specified is called “Renewable Portfolio Standard” (RPS).

・ Acknowledging certification of RE is issued and the purchase price is decided by the market for tradable green certificates (TGC).

Power company (Utility)

・ Cost competition can be created among REs and cost-reduction incentives start to work.

・ The relationship between the purpose of introduction of REs and the target amount of REs becomes clear.

・ Because the price of TGCs is decided in the market, it is likely to be unstable, making the investment risk for RE larger.

RPS law (U.S.A., UK, Japan and others)

Tax Incentives ・ Preferential tax rate, tax holidays, or tax credits are applied to the RE business and introduction of RE generation equipment.

・ The reduction of tax produces an incentive, but no actual money is needed for incentives.

・Because it is a kind of passive policy, thinducement-attraction is weak.

e Production tax credit (U.S.A.)

Fiscal Incentives (Government Expenditure)

・ The government directly supports the promotion of REs by means of fiscal expenditure such as a subsidy for construction costs.

・This is direct support for the promotion of RE projects and the effect is remarkable.

・The government finance burden is heavy

Construction cost subsidy (Denmark, Japan)

Incentive type

Financial Incentives

・Financial support for the promotion of RE by financing at low interest rates from governmental banks.

Government

・ Because this financing is repayable, it maintains the entrepreneur’s consciousness of ownership.

・A large amount of initial funds are needed as capital for financing.

Low interest rate loans (Japan, U.S.A., Germany etc.)

Study on Fiscal and Non-fiscal Incentives to Accelerate Private Sector Geothermal Energy Development in the Republic of Indonesia Final Report (Summary)

8.3 The Feed-in Tariff (FIT) Scheme

Many countries oblige power companies to purchase power from renewable energy sources at fixed prices to promote renewable energy. The fixed purchase price can be specified as a certain ratio (e.g. 90%) of the retail tariff or as a definite price (e.g. 15 Euro cents/kWh) for each renewable energy source. Nowadays, the Feed-in Tariff scheme seen in Germany and the EU, typical example of the latter, is becoming popular.

FIT may be introduced to Indonesia. The selling price calculation for geothermal power generation indicated that 11.9 USD Cents/kWh is necessary if no specific incentives are provided. Therefore, this figure becomes a provisional FIT price for the case in which there are no incentives. Note that this calculation assumed a 15-year period of economical evaluation for investors. Accordingly, the FIT purchase term shall be 15 years. The FIT price does not have to be fixed; it can change in phases. Therefore the followings are the FIT price designs for Indonesia.

Table 8.3-6 Proposal for FIT prices

60 MW case Term

Fixed FIT price 2 stage FIT price (Case-3)

Without Tax Incentive Y 1-8 Y 8-15

11.9 C$/kWh 11.9 C$/kWh

12.8 C$/kWh 8.1 C$/kWh

With Tax Incentive (15years, 5 % Tax)

Y 1-8 Y 8-15

10.9 C$/kWh 10.9 C$/kWh

11.8 C$/kWh 7.4 C$/kWh