Stretching Scarce Resources: State Strategies to Design Effective, Affordable Benefit Packages

Anne Markus, J.D., Ph.D.Senior Research Scientist

The George Washington University Medical Center

Definitions

• Premium: Set amount of dollars per defined payment period (usually monthly) paid to obtain health insurance coverage.

• Cost-sharing: Patient exposure to out-of-pocket costs associated with health service delivery. Includes:

• Deductible• Coinsurance• Copayment

Purposes of Cost-sharing

• General reasons:– Enticing families to be more cost conscious in seeking

care– Fostering a sense of ownership/personal responsibility– Directing consumers toward more cost-effective care– Deterring unnecessary utilization– Raising revenues to reduce sponsor costs of health care

coverage

Purposes of Cost-sharing (cont.)

• Additional reasons for states: – Making public health insurance programs

aimed at the poor look more like private insurance

– Limiting substitution and crowd-out of private insurance

Recent Trends

• Private sector

– No significant changes to contribution strategies, but changes to benefit structure

• Medicaid/SCHIP– HIFA initiative

• Medicare– Pharmacy Plus initiative

Cost-sharing Rules in Public Programs

• Medicaid– Premiums prohibited

with some exceptions

– “Nominal” cost-sharing allowed

with some exceptions

– No overall cap specified

• SCHIP– Premiums allowed

– Cost-sharing allowed

– Overall cap of 5% of family income

• State employee benefit plans– Premiums allowed

– Cost-sharing allowed

– May or may not impose overall cap

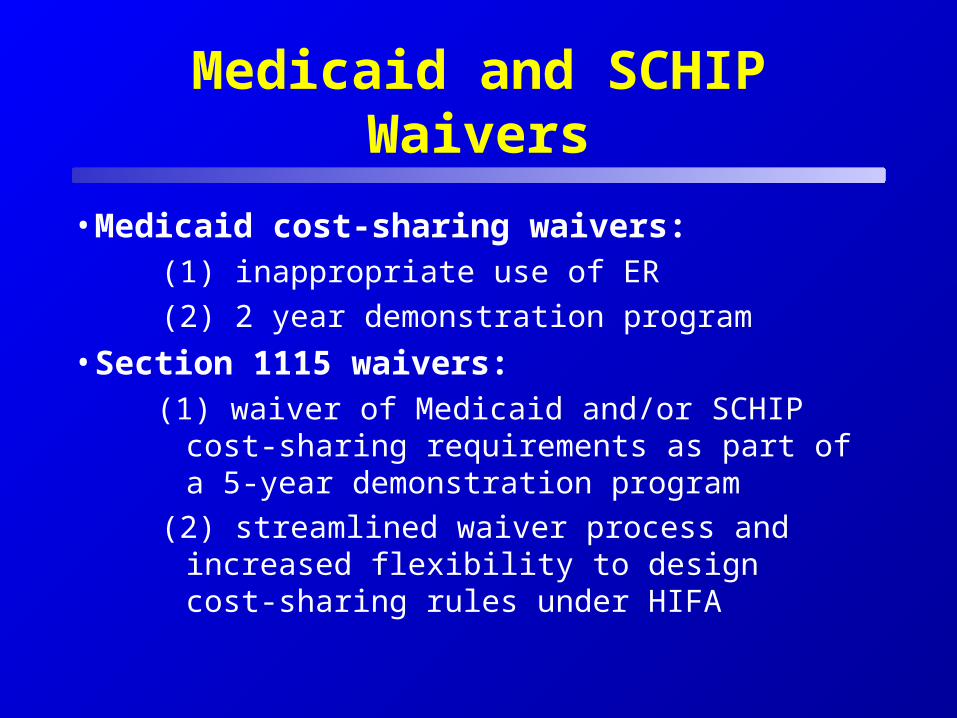

Medicaid and SCHIP Waivers

• Medicaid cost-sharing waivers: (1) inappropriate use of ER

(2) 2 year demonstration program

• Section 1115 waivers: (1) waiver of Medicaid and/or SCHIP cost-sharing

requirements as part of a 5-year demonstration program

(2) streamlined waiver process and increased flexibility to design cost-sharing rules under HIFA

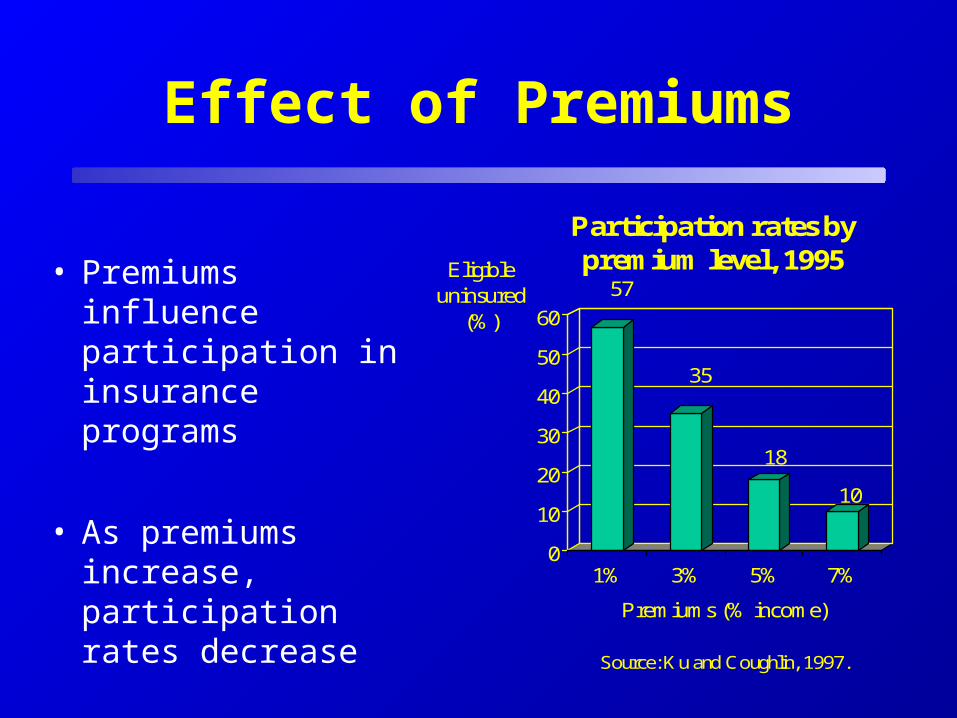

Effect of Premiums

• Premiums influence participation in insurance programs

• As premiums increase, participation rates decrease

57

35

18

10

0

10

20

30

40

50

60

Eligible uninsured

(%)

1% 3% 5% 7%

Premiums (% income)

Source: Ku and Coughlin, 1997.

Participation rates by premium level, 1995

Effects of Cost-sharing

• Use of services– Cost-sharing influences the

use of services

– As cost-sharing increases, use of services decreases

• outpatient care

• inpatient care

• prescriptions

• preventive services

• emergency room

• Health outcomes– Cost-sharing may have an

effect on health outcomes

– In general, cost-sharing has been found to have a minimal or no effect on health outcomes except for the poorest populations

Effect Across Population Groups

• Research shows that cost-sharing has a deterrent effect across the board:– children and adults– people who are healthy and people who have chronic conditions– rich and poor

• Existing body of knowledge also suggests that cost-sharing may have a more pronounced negative effect on low income people: – studies on premiums in state programs– non-Medicaid studies on cost-sharing– Medicaid studies on cost-sharing

SCHIP Experiences

• All States with separate SCHIP programs have some form of cost-sharing

• Research in this area thus far focuses on the effect of premiums on initial participation but also on continued participation in program

• Anecdotal evidence also suggests that collecting and processing premiums and other cost-sharing contributions is administratively burdensome and/or not worth the cost

Implications

• Income-related, sliding scale for premium and cost-sharing schedule

• Low premiums

• Limited cost-sharing

• Broaden the definition of preventive services exempt from cost-sharing

• Individuals with special needs

HIFA Cost-sharing Rules

• Mandatory eligibility groups (e.g., all children up to 100% FPL): same rules as Medicaid

• Optional eligibility groups (e.g., children beyond the mandatory eligibility levels): no cost-sharing rules specified other than an annual cap of 5% of family income for deductibles, copayments and coinsurance

• “Expansion” eligibles (e.g., nondisabled single working age adults, childless couples): no cost-sharing rules specified

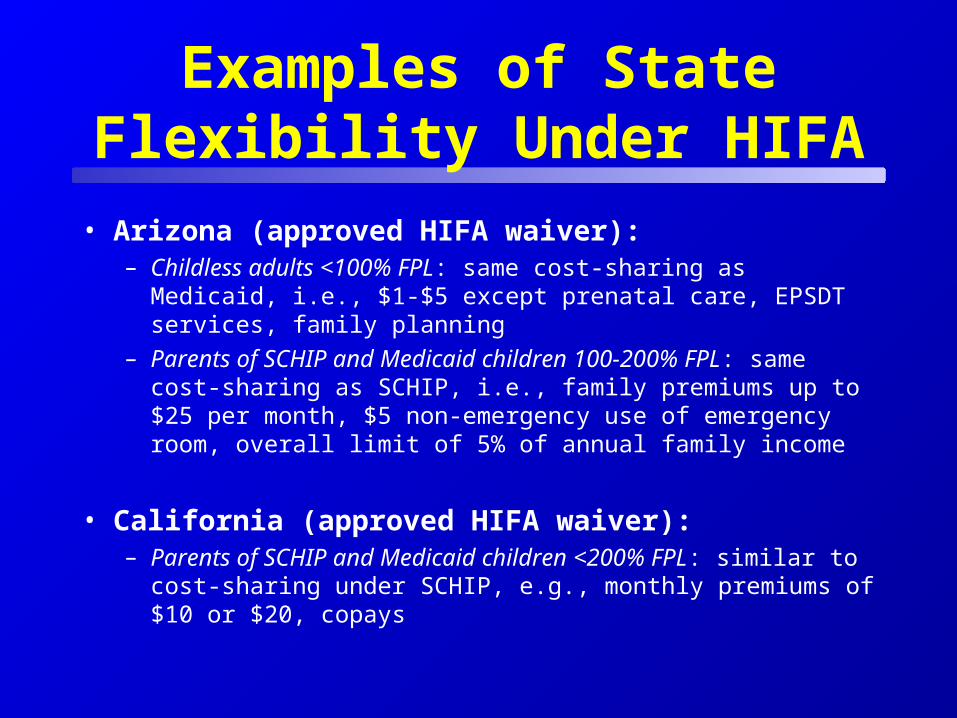

Examples of State Flexibility Under HIFA

• Arizona (approved HIFA waiver): – Childless adults <100% FPL: same cost-sharing as Medicaid, i.e.,

$1-$5 except prenatal care, EPSDT services, family planning

– Parents of SCHIP and Medicaid children 100-200% FPL: same cost-sharing as SCHIP, i.e., family premiums up to $25 per month, $5 non-emergency use of emergency room, overall limit of 5% of annual family income

• California (approved HIFA waiver):– Parents of SCHIP and Medicaid children <200% FPL: similar to

cost-sharing under SCHIP, e.g., monthly premiums of $10 or $20, copays