Page 1

Storage the ultimate insurance –

Smoothing the Jagged Edges of Energy Markets

Crude Oil Markets and Storage Summit 2015

Page 2 Page 2

Stone Bridge Energy Partners is a leading developer of diversified energy and chemicals projects. Stone Bridge, in partnership with leading strategic and financial investors, is pursuing fundamental opportunities in the North American energy complex. The industry is in a highly dynamic period offering the opportunity to create layers of value in unexpected and at moments non-obvious ways. Directionally Stone Bridge identifies market imperfections, including structural arbitrage opportunities, delivering fast track projects that cover off these seams at lowest cost and lowest risk. Stone Bridge is attracted to high growth markets, with compelling margin opportunities, quality partners and defensible competitive barriers.

Stone Bridge manages commodity-to-commodity risk contractually arranging project

structures at lowest market risk with optimum financial returns. The company’s tolling strategy has been tried and tested over many years from gas storage, to pipelines, to LNG, to power and petrochemicals. Stone Bridge is extending the tolling plus strategy to a range of diverse midstream and downstream opportunities.

Stone Bridge keeps the end in mind from project concept, through development and

structuring. The company anticipates exiting projects through trade sale, MLPs and conventional public offerings.

Confidential - Not for Distribution

About Stone Bridge

Page 3 Page 3 Confidential - Not for Distribution

Agenda

Some Preliminaries Some Fundamentals Some Resources Some Maps Some Numbers Some Truths Some Conclusions Some Doubt Some Need for Insurance !

Page 4 Page 4 Confidential - Not for Distribution

What a difference a year makes

Source EIA

Page 5 Page 5 Confidential - Not for Distribution

Things Keep Moving - Week Ending May 29: Change in Weekly Crude Oil Inventory

Page 6

"

!!!!

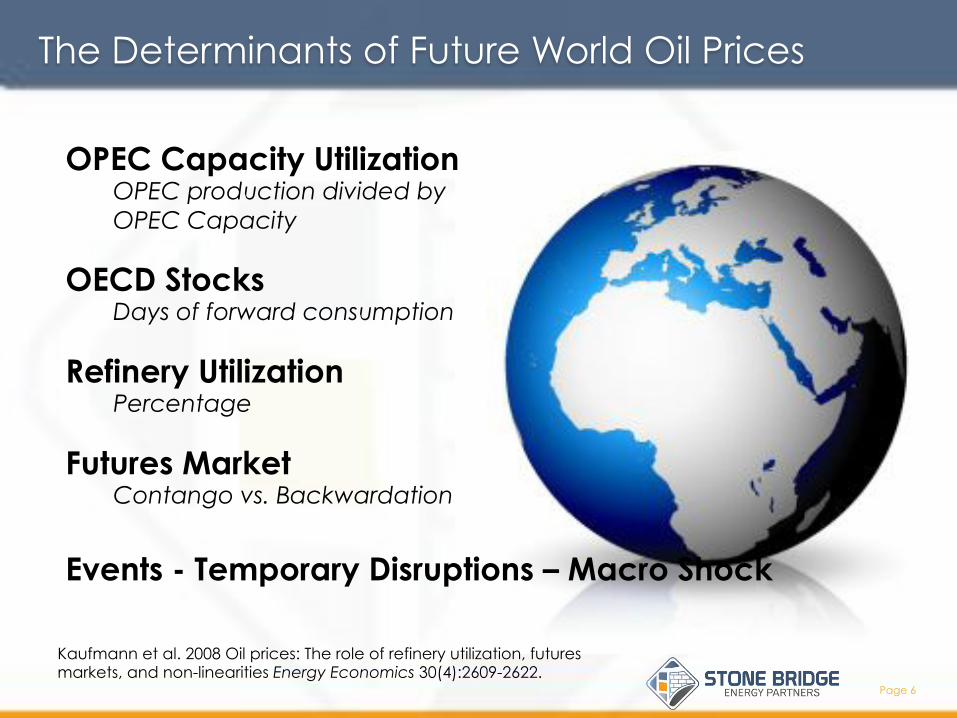

OPEC Capacity Utilization OPEC production divided by OPEC Capacity

Kaufmann et al. 2008 Oil prices: The role of refinery utilization, futures markets, and non-linearities Energy Economics 30(4):2609-2622.

The Determinants of Future World Oil Prices

OECD Stocks Days of forward consumption

Refinery Utilization Percentage

Futures Market Contango vs. Backwardation

Events - Temporary Disruptions – Macro Shock

Page 7 Page 7 Confidential - Not for Distribution

To the Future!

An examination of EIA long-term forecasts from 1994 through 2012 shows that on average, for forecasts over five years in the future, the actual crude oil price was at least 50% higher than the EIA forecast. – WTRG Economics

!

Page 8 Page 8 Confidential - Not for Distribution

To the Future!

Our analysis of NYMEX futures contracts based on the average futures price for all available December contracts demonstrates that on average, the actual price was below the NYMEX price for 1 – 7 years out. Furthermore, in all instances for a time horizon greater than three years, the actual price was higher than the price implied by the NYMEX contracts– WTRG Economics

!

Page 9 Page 9 Confidential - Not for Distribution

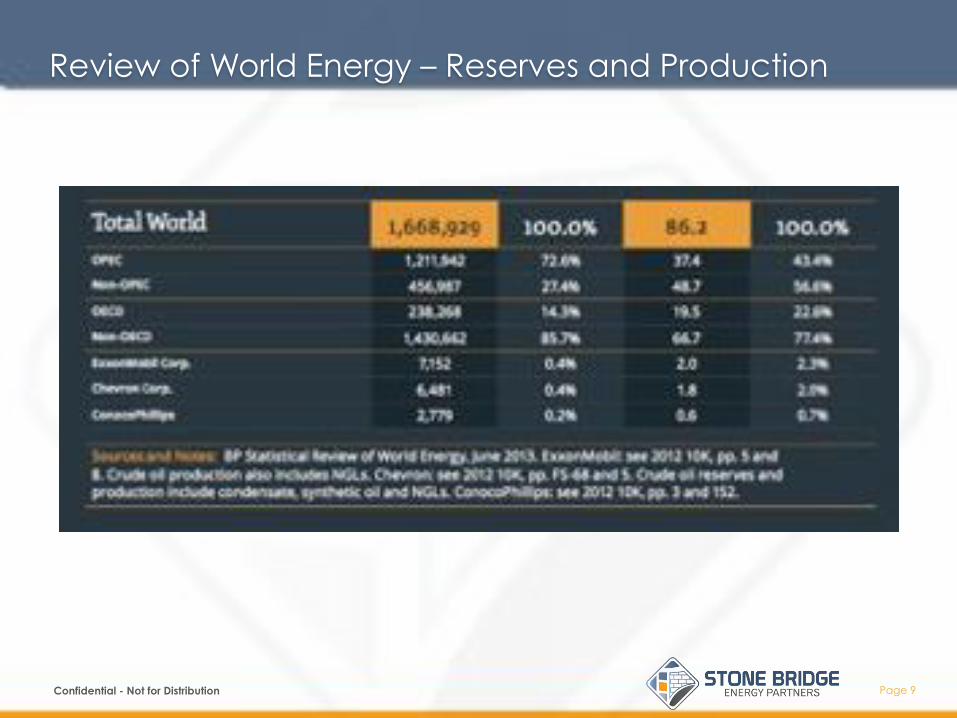

Review of World Energy – Reserves and Production

Page 10 Page 10 Confidential - Not for Distribution

Progress = New Marginal Demand

Page 11 Page 11 Confidential - Not for Distribution

Urbanization and Expanding Middle Class

The magnitude of China’s middle-class growth is transforming the nation.

Share of urban households,1 %

Urban private consumption,1 %

Income segment2 Projected growth of private consumption, CAGR,3 2012-22, %

100% = 256 million

357 million

3 - 9 14

54 54

22

29 16

16

25 20

56 54

14 16

11

10,048 billion renminbi

26,804 billion

renminbi

- 5 2012 2022 2012 2022

Affluent

Upper Middle Class

Mass Middle Class

Poor

10.3

19.6

22.4

-3.3

-1.5

1Figures may not sum to 100%, because of rounding; data for 2022 are projected. 2Defined by annual disposable income per urban household, in 2010 real terms; affluent, >229,000 renminbi (equivalent to >$34,000); upper middle class, 106,000 to 229,000 renminbi (equivalent to $16,000 to $34,000); mass middle class, 60,000 to 106,000 renminbi (equivalent to $9,000 to $16,000); poor, <60,000 renminbi (equivalent to <$9,000). 3Compound annual growth.

Page 12 Page 12 Confidential - Not for Distribution

Urbanization and Expanding Middle Class

Generation 2 – Chinese consumers in their teens and early 20s – takes a more Western approach to shopping.

% of respondents

Confident about personal-income growth

Loyal to brands Willing to trade up 3

Often early adopter of new products/services

Seek feedback/ comments on Internet before buying 3

Upper-middle-class urban Generation 2 members1

Upper-middle-class urban population2

Total urban population

64 58 56 46 43 40 41 36 33 29 25 22 21 16

12

1People born after the mid-1980s and raised in a period of relative abundance. 2Annual household income of 106,000 – 229,000 renminbi (equivalent to $16k - $34k in 2010 terms). 3Personal-care-product example. Source: 2012 McKinsey survey of 10,000 Chinese consumers

Page 13 Page 13 Confidential - Not for Distribution

Urbanization and Expanding Middle Class

Gongzhuling

Beijing

Yulin (Shaanxi)

Linfen

Liuan Shanghai

Wuhan

Chongqing

Leshan

Ziyang

Guangzhou

Shenzhen Foshan

Yongzhou

Zhaotong

Meishan Chengdu

Tier-1 Cities

Selected Tier-2 Cities

Selected Tier-3 Cities

Selected Tier-4 Cities

Share of middle class by type of city, % 16

40

45

31

43

15 - 8 3 -

16

Page 14 Page 14 Confidential - Not for Distribution

Year-Over-Year Change in World Demand for Oil (million barrels per day)

Page 15 Page 15 Confidential - Not for Distribution

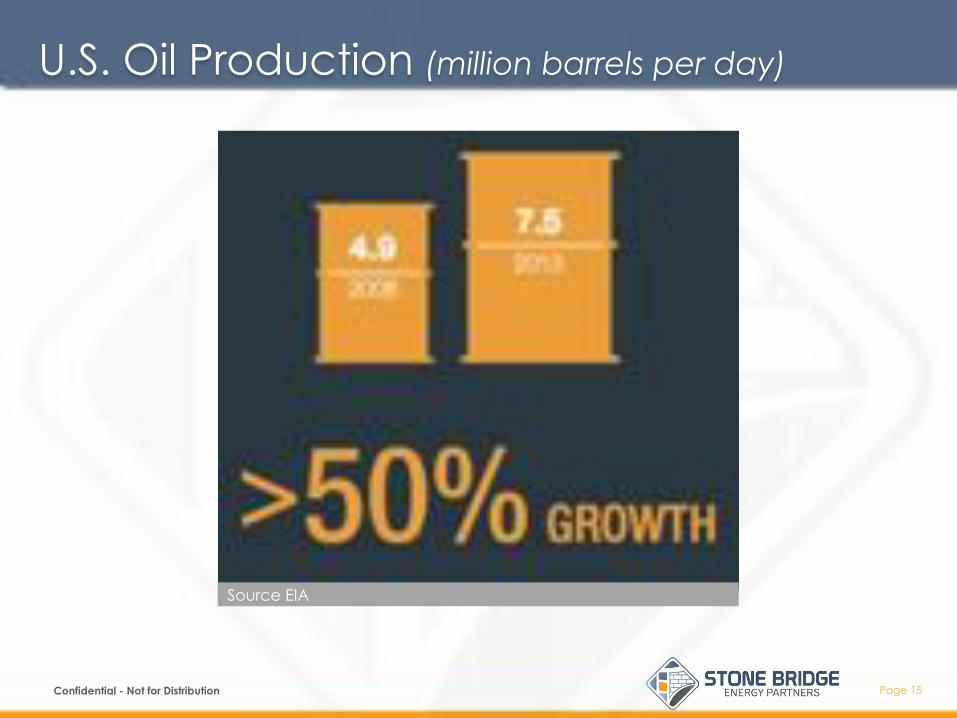

U.S. Oil Production (million barrels per day)

Source EIA

Page 16 Page 16 Confidential - Not for Distribution

Resources

Canada

United States

Mexico Trinidad & Tobago

Venezuela Columbia

Ecuador

Peru Brazil

Argentina

Production (thousand barrels per day)

8,000 to 12,000

2,000 to 8,000

500 to 2,000

0 to 500

Source: BP Statistical Review of World Energy, June 2013

Page 17

North American Resources

Source: OGJ 2012 Confidential - Not for Distribution

Page 18 Page 18 Confidential - Not for Distribution

New Trade Flows Create New Dynamics

1.0 (-0.6)

1.1 (+0.3)

1.2 (+0.6)

1.8 (-0.6)

3.1 (0.3) 4.1

(-0.6) 5.2 (+0.3)

1.6 (-0.2)

0.1 (-0.7)

2.0 (-0.6)

2.2 (+0.8)

1.2 (+0.1)

3.6 (-0.5)

0.5 (-0.0)

1.3 (+0.6)

0.7 (+0.4)

0.3 (0.2)

0.2 (0)

Crude Exports in 2019 & Growth in 2013-19 for Key Trade Routes 1

(million barrels per day)

Red number in brackets denotes growth in period 2013-19 1 Excludes Intra-Regional Trade 2 Includes Chile 3 Includes Israel

Asia imports increase by 2.6 mb/d to 22.1 mb, or 65% of the international crude market.

OECD Americas 2

OECD Europe

OECD Asia

Oceania 3

China

Other Asia

Page 19 Page 19 Confidential - Not for Distribution

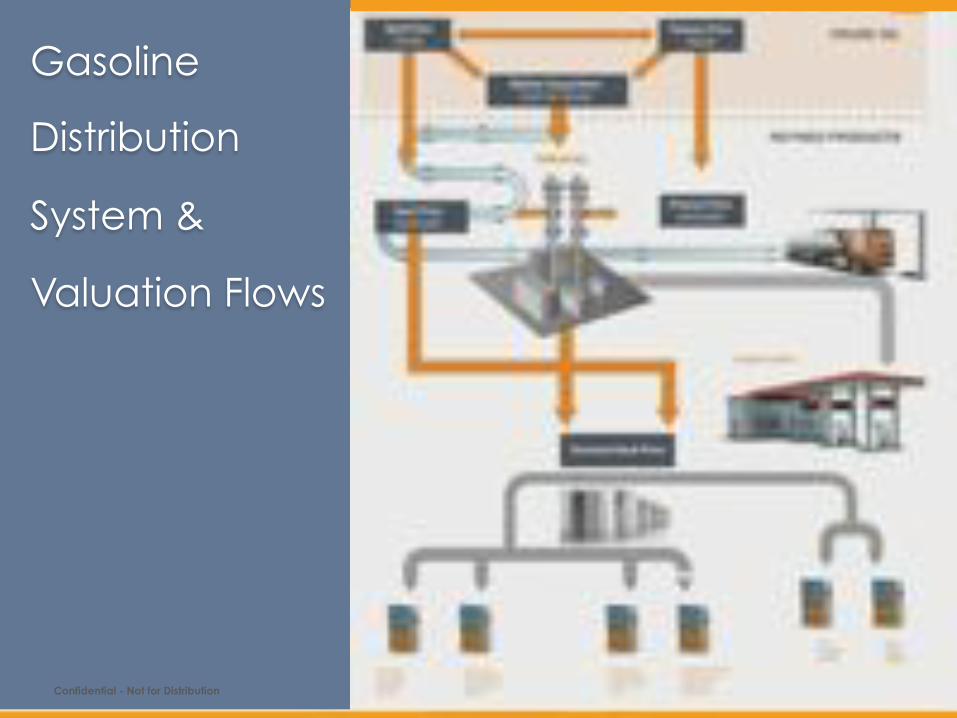

Gasoline

Distribution

System &

Valuation Flows

Page 20 Page 20 Confidential - Not for Distribution

The U.S. Refining Sector

Page 21 Page 21 Confidential - Not for Distribution

Gasoline Pricing

Page 22 Page 22 Confidential - Not for Distribution

U.S. Finished Petroleum Products Demand (million barrels per day)

Source: EIA. Data for 2013 is the average of January through November.

Page 23

-60

-40

-20

0

20

40

60

80

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

"

!!!!

Competitive Market OPEC

Kaufmann, R.K. 1995. A model of the world oil market for Project LINK Economic Modelling 12:165-178

Annual Change in Real Oil Prices

TX Railroad Commission

Page 24 Page 24 Confidential - Not for Distribution

WTI Crude Oil Futures Contracts Traded by Year, 1990 - 2013 (millions of contracts traded)

Page 25

Events cut both ways

Page 26

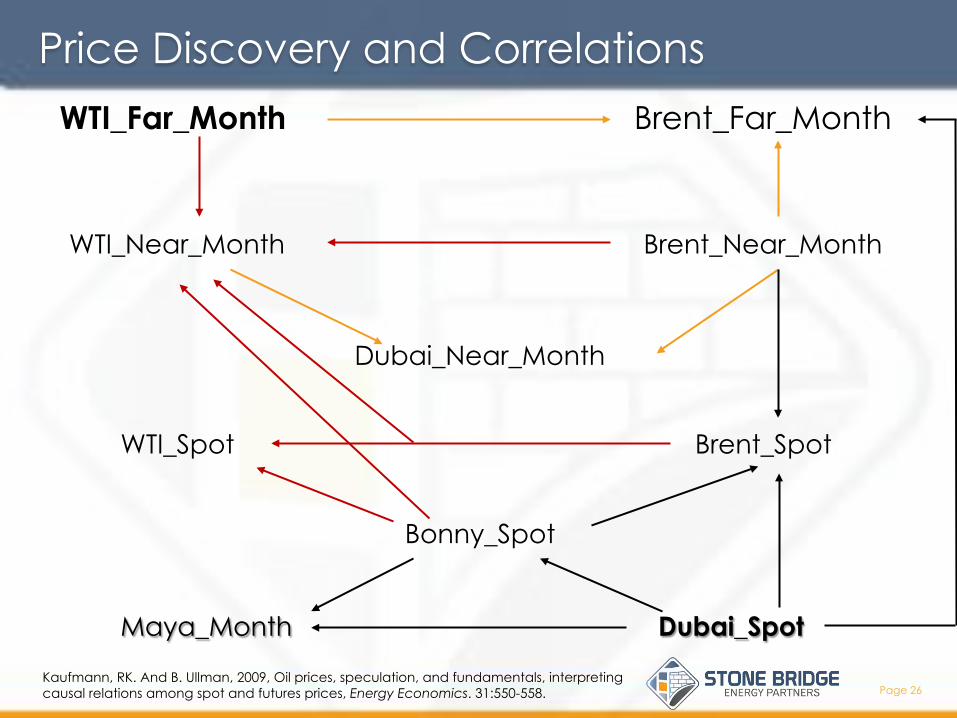

WTI_Far_Month Brent_Far_Month

WTI_Near_Month Brent_Near_Month

Dubai_Near_Month

WTI_Spot Brent_Spot

Bonny_Spot

Maya_Month Dubai_Spot

Kaufmann, RK. And B. Ullman, 2009, Oil prices, speculation, and fundamentals, interpreting causal relations among spot and futures prices, Energy Economics. 31:550-558.

Price Discovery and Correlations

Page 27

0

20

40

60

80

100

120

140

160

180

1900 1920 1940 1960 1980 2000 2020 2040

1 trillion barrels

2.5 trillion barrels

Mill

ion

ba

rre

ls /

Da

y This Will Never Happen… But

Page 28

0

20

40

60

80

100

120

1899 1919 1939 1959 1979 1999 2019 2039 2059 2079 2099

Mill

ion

ba

rre

ls /

Da

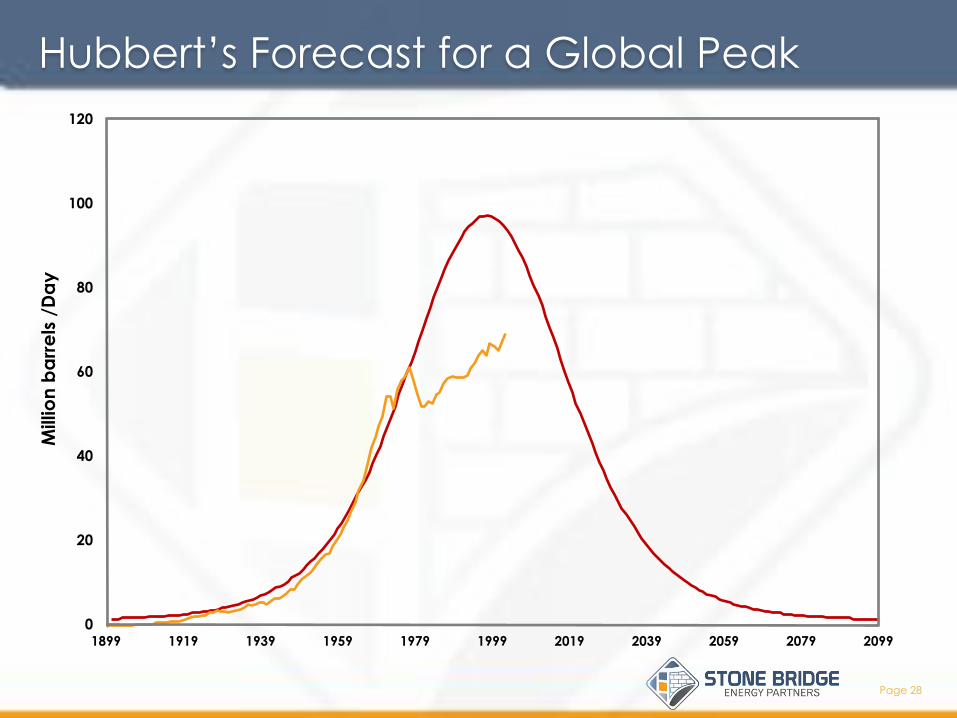

y Hubbert’s Forecast for a Global Peak

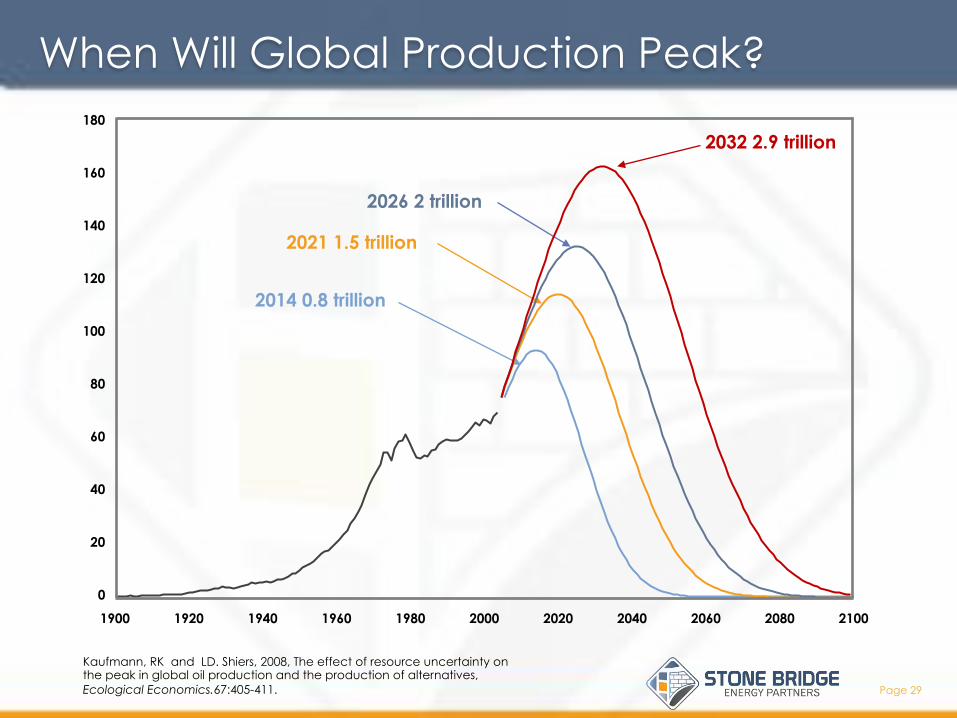

Page 29

0

20

40

60

80

100

120

140

160

180

1900 1920 1940 1960 1980 2000 2020 2040 2060 2080 2100

2014 0.8 trillion

2021 1.5 trillion

2026 2 trillion

2032 2.9 trillion

Kaufmann, RK and LD. Shiers, 2008, The effect of resource uncertainty on the peak in global oil production and the production of alternatives, Ecological Economics.67:405-411.

!

When Will Global Production Peak?

Page 30 Page 30 Confidential - Not for Distribution

Changes in Saudi Arabia Production v WTI

Page 31 Page 31 Confidential - Not for Distribution

Historical World Spare Oil Production Capacity & WTI Spot Price

Average Quarterly, 1995 - 2013

Page 32 Page 32 Confidential - Not for Distribution

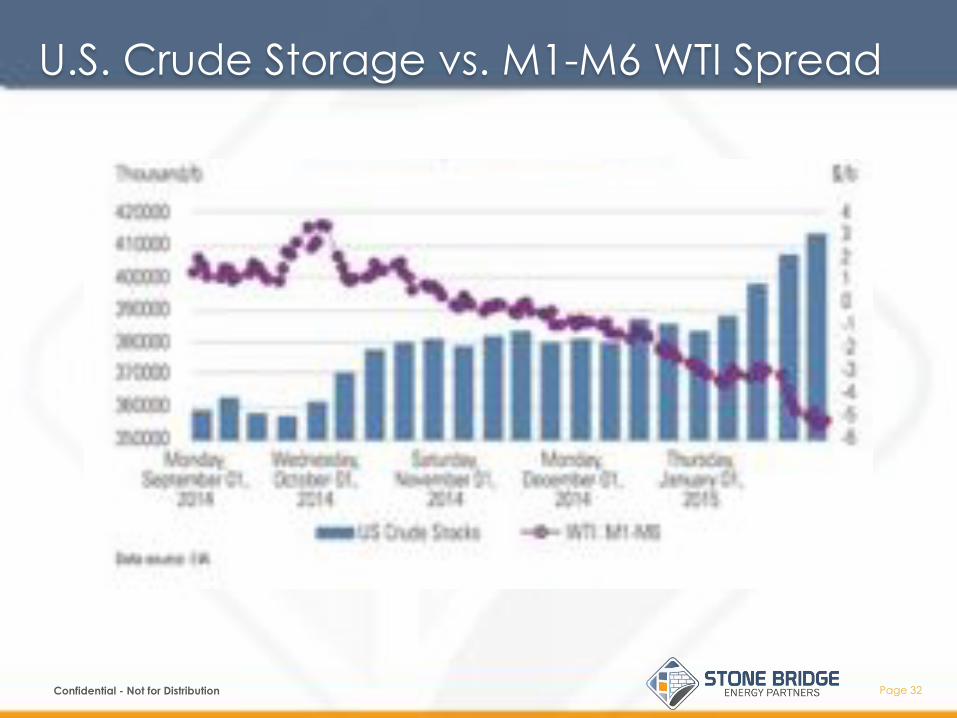

U.S. Crude Storage vs. M1-M6 WTI Spread

Page 33 Page 33 Confidential - Not for Distribution

Imports Displaced

Page 34 Page 34 Confidential - Not for Distribution

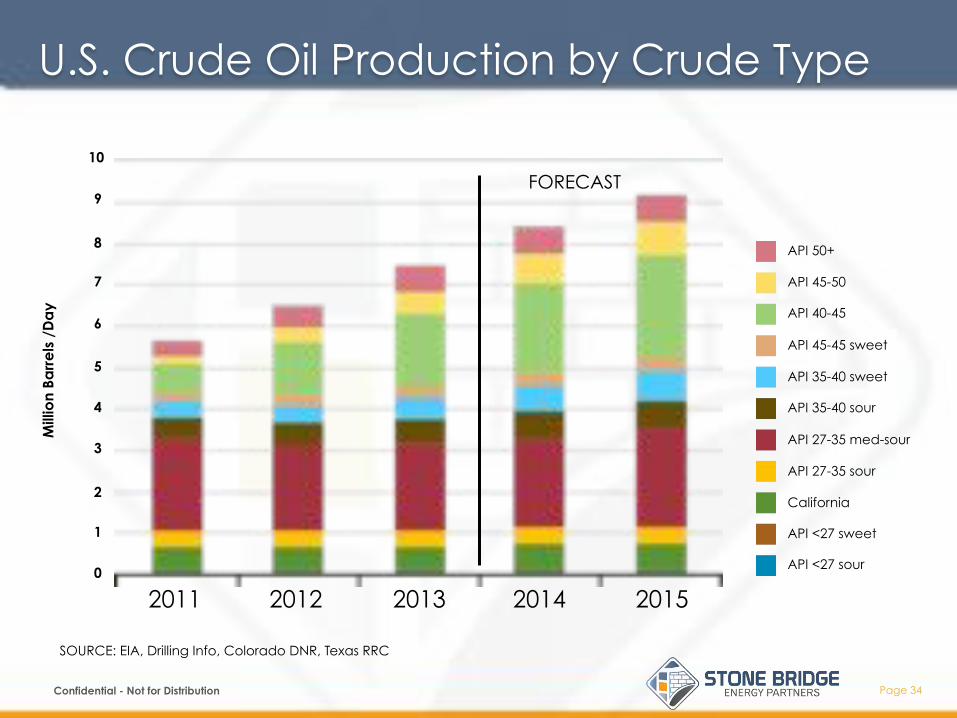

U.S. Crude Oil Production by Crude Type

SOURCE: EIA, Drilling Info, Colorado DNR, Texas RRC

FORECAST

Mill

ion

Barr

els

/D

ay

10

9

8

7

6

5

4

3

2

1

0

2011 2012 2013 2014 2015

API 50+

API 45-50

API 40-45

API 45-45 sweet

API 35-40 sweet

API 35-40 sour

API 27-35 med-sour

API 27-35 sour

California

API <27 sweet

API <27 sour

Page 35 Page 35 Confidential - Not for Distribution

Imports by Crude Oil Quality (million barrels per day)

Source: Import volumes from EIA. 2013 data is through November. Note: Heavy, Medium and Light are characterized by the oil’s API gravity in the following manner: <28: Heavy; 28-33: Medium; >33: Light. The sweet/sour characterization is defined by the oil’s sulfur content, with <=0.42% Sulfur characterizing “Sweet” oil.

Page 36 Page 36 Confidential - Not for Distribution

Global Crudes & Their Physical Characteristics – Density & Sulphur

Oil%Sands!

Permian%Basin!

0 0.5 1 1.5 2 2.5 3 3.5 4

Sulphur%content%%!

API

De

gre

e

10

15

20

25

30

35

40

45

50

IEA Aggregate

BFOE Brent

Page 37 Page 37 Confidential - Not for Distribution

Domestic Crude Oil First Purchase Prices for Selected Crude Streams

0

20

40

60

80

100

120

140 A

pr-

2011

Jun-

2011

Aug

-201

1

Oc

t-20

11

De

c-2

011

Feb

-201

2

Ap

r-20

12

Jun-

2012

Aug

-201

2

Oc

t-20

12

De

c-2

012

Feb

-201

3

Ap

r-20

13

Jun-

2013

Aug

-201

3

Oc

t-20

13

De

c-2

013

Feb

-201

4

Ap

r-20

14

Alaska No. Slope

Cali. Kern River

Cali. Midway-Sunset

Heavy La. Sweet

Light La. Sweet

Mars Blend

West Tx. Intermediate

West Tx. Sour

Wyoming Sweet

Page 38 Page 38 Confidential - Not for Distribution

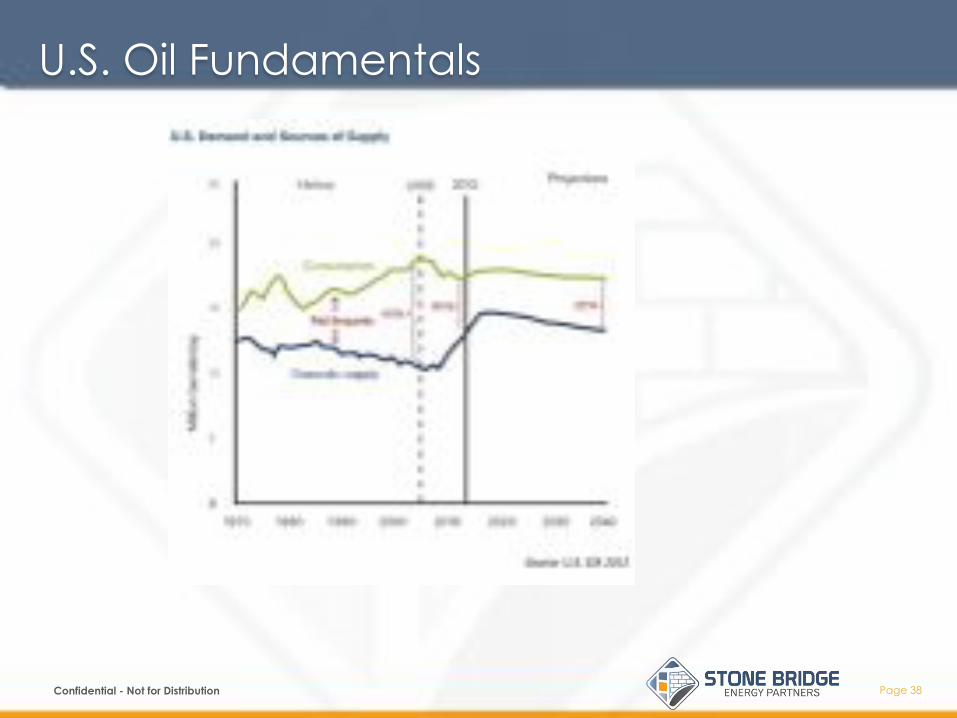

U.S. Oil Fundamentals

Page 39 Page 39 Confidential - Not for Distribution

A function of resources

Source EIA

Page 40 Page 40 Confidential - Not for Distribution

WCSB Takeaway Capacity vs. Supply Forecast (millions barrels per day)

Page 41 Page 41 Confidential - Not for Distribution

Canadian Oil Production (million barrels per day)

A new 40-in, 750-mile pipeline of one million bbls/day capacity from Montrealto deep-water East Coast ports and refineries, with a right-of-way paralleling the TransCanada Highway, could be built for $4 billion. Assuming an average pipeline toll of $8/bbl and an average throughput of 1.5 million bbls/day over a 50-year life, total pipeline revenue of $220 billion is ten to twenty times the capital and operating costs for the pipeline. This is a terrific project business return by any measure – though pipeline tolls and return on capital must be approved by shippers and regulators. The real value of this pipeline is economic. Based on a value of $200/bbl for refined products, two million bbls/day of Canadian bitumen extracted, upgraded, pipelined to eastern Canada and there refined, and consumed or exported, will contribute more than $150 billion/year to Canada's economy and balance of payments. And those economic benefits do not include spin-off benefits to local economies and governments associated with upgrading, pipelining, refining, petro-chemicals and port activities.

Page 42 Page 42 Confidential - Not for Distribution

Energy Partners

Page 43 Page 43 Confidential - Not for Distribution

Shipping Oil

Page 44 Page 44 Confidential - Not for Distribution

Midstream Collapses Arbs

Page 45 Page 45 Confidential - Not for Distribution

Convergence Club

Page 46 Page 46 Confidential - Not for Distribution

Global Activity

Page 47 Page 47 Confidential - Not for Distribution

U.S. and Canada Pipes – Concentrated and Inflexible

Page 48 Page 48 Confidential - Not for Distribution

U.S. Oil Pipelines

Page 49 Page 49 Confidential - Not for Distribution

U.S. Crude Oil Storage Capacity Utilization Now Up to 60% March 24, 2015

Page 50 Page 50 Confidential - Not for Distribution

Oil Infrastructure Snap

Page 51 Page 51 Confidential - Not for Distribution

Success follows Success

Page 52 Page 52 Confidential - Not for Distribution

Rail – Big and Flexible

Page 53 Page 53 Confidential - Not for Distribution

Canadian Movements to USGC

Page 54 Page 54 Confidential - Not for Distribution

Everything is moving

Page 55 Page 55 Confidential - Not for Distribution

Events

Page 56 Page 56 Confidential - Not for Distribution

North American Oil Market

Page 57 Page 57 Confidential - Not for Distribution

Canadian Infrastructure

Page 58 Page 58 Confidential - Not for Distribution

Go West

Page 59 Page 59 Confidential - Not for Distribution

East too – maybe North?

Page 60 Page 60 Confidential - Not for Distribution

Take Away Capacity Constraints

Page 61 Page 61 Confidential - Not for Distribution

Invitation to Invest

Page 62 Page 62 Confidential - Not for Distribution

St James Growing but Not for Storage

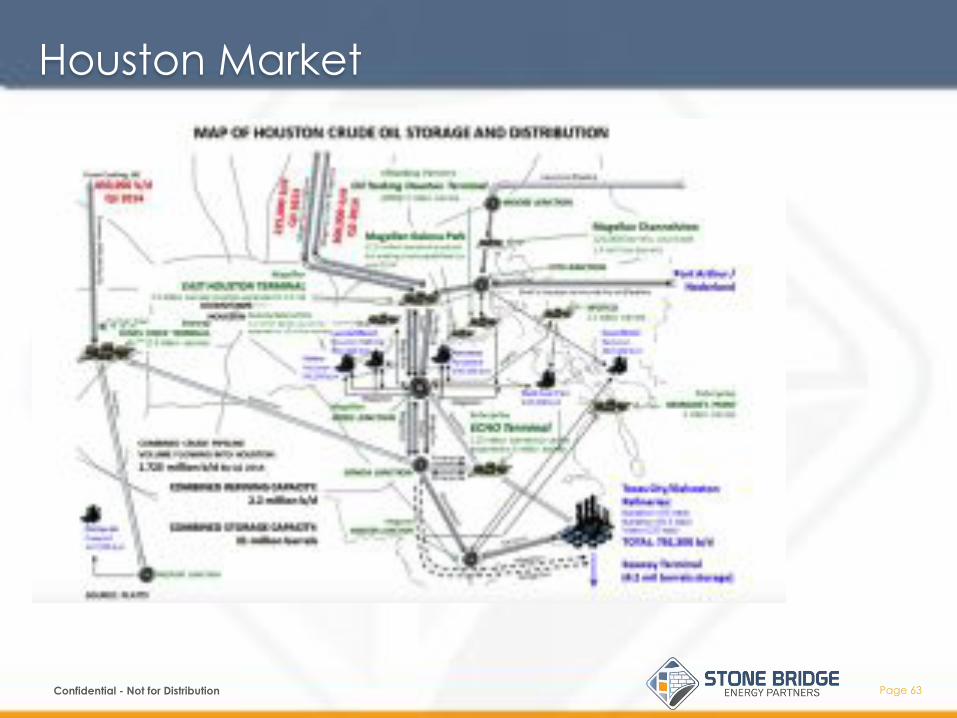

Page 63 Page 63 Confidential - Not for Distribution

Houston Market

Page 64 Page 64 Confidential - Not for Distribution

Houston Market “The development of over 1.7 million b/d of pipeline capacity to bring U.S. crude production to Houston by 2014 has set the stage for a new spot market and created the need for a new marker that reflects both U.S. Gulf Coast and global crude fundamentals,” said Esa Ramasamy, Platts editorial director, strategic oil markets development. “As new pipelines and other forms of transportation enable domestic crude to flow to the Gulf Coast rather than being trapped inland, the U.S. market is rapidly resetting itself. The change is already evident in the narrowing price spread between WTI and Brent, two global benchmarks. The rise in U.S. domestic crude oil production is beginning to be felt globally.” Houston, currently the location for several Americas refined products benchmarks, is the largest refining center in the U.S. with 2.2 million b/d of refining capacity. With the rebirth of U.S. crude production nearby, the Gulf Coast port city is undergoing a massive infrastructure renaissance, evidenced by the development of 31 million barrels of crude oil storage and the expansion of local pipeline capacity between storage terminals and refineries by the middle of 2014. Pipelines, including Enterprise/Enbridge’s Seaway and Magellan’s Longhorn, are connecting inland production centers to the U.S. Gulf Coast, with Houston as the main target of these shifting crude oil flows. “Houston’s superior refining capacity, storage, and waterborne loading infrastructure positions it to become a key pricing hub in the Americas,” said Suzanne Evans, senior manager, Platts’ Price Group. “The prolific Permian Basin – the home of WTI – and the Eagle Ford shale are in Houston’s backyard. This new crude oil production, combined with movements of Domestic Light Sweet from the Cushing, Oklahoma, hub to Houston via the Seaway Pipeline, is creating a vibrant light, sweet spot market in Houston.”

Page 65 Page 65 Confidential - Not for Distribution

So Louisiana Market Access – 5 million barrels

Page 66 Page 66 Confidential - Not for Distribution

Some Storage Data from Above

About 126 MM barrels of U.S. and Canadian crude oil storage are visible to the Genscape system. More than 50% of the total, or 82 MM barrels of the total are in Cushing. The next largest storage hub is Hardesty at 17 MM, followed (in order of size) by Patoka, Edmonton, Midland, Wichita Falls, Colorado City, Hardisty-Caverh, Kerrobert, and Wink. The construction sites are tracked by Genscape’s aerial photography. In addition to Cushing, there are about 3 MM bbls under construction at Hardesty, and around 1 MM bbls each at Edmonton, Midland, and Patoka. There are several unit train terminals (100+ rail car loading facilities) being built in the Bakken to relieve pipeline transportation constraints in the region. (see A Perfect Storm in the Bakken.) There are only two places in the country that can handle receipt of these unit trains without breaking them up and losing the efficiencies of unit train transportation: St. James, LA (home of Light Louisiana Sweet) and Stroud near Cushing, OK (home of West Texas Intermediate and the CME/NYMEX futures delivery point). Few refineries have the available land necessary to build one of these facilities. [James Cairns, Vice President, Petroleum and Chemicals, CN Rail] Source: RBN

Page 67

Crystal Balls have always been broken – and the next resource play…

Confidential - Not for Distribution

Page 68 Page 68

These materials have been provided to you by Stone Bridge Energy Partners LLC (SBE) for discussion purposes only and may not be used or relied upon for any purpose other than as specifically contemplated by a definitive agreement with Stone Bridge Energy Partners LLC (SBE). In addition, these materials may not be disclosed, in whole or in part, or summarized or otherwise referred to except as agreed in writing by Stone Bridge Energy Partners LLC (SBE). Stone Bridge Energy Partners LLC (SBE) assumes no responsibility for independent verification of the information enclosed. Stone Bridge Energy Partners LLC (SBE) does not make any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein including any financial projections and shall not have any liability for the information contained in, or any omissions from, this presentation. These materials were designed for use by individuals and specific persons familiar with the business and the affairs of your company and Stone Bridge Energy Partners LLC (SBE) and assumes no obligation to update or otherwise revise these materials.

Confidential - Not for Distribution

Disclaimer

Page 70 Page 70 Confidential - Not for Distribution

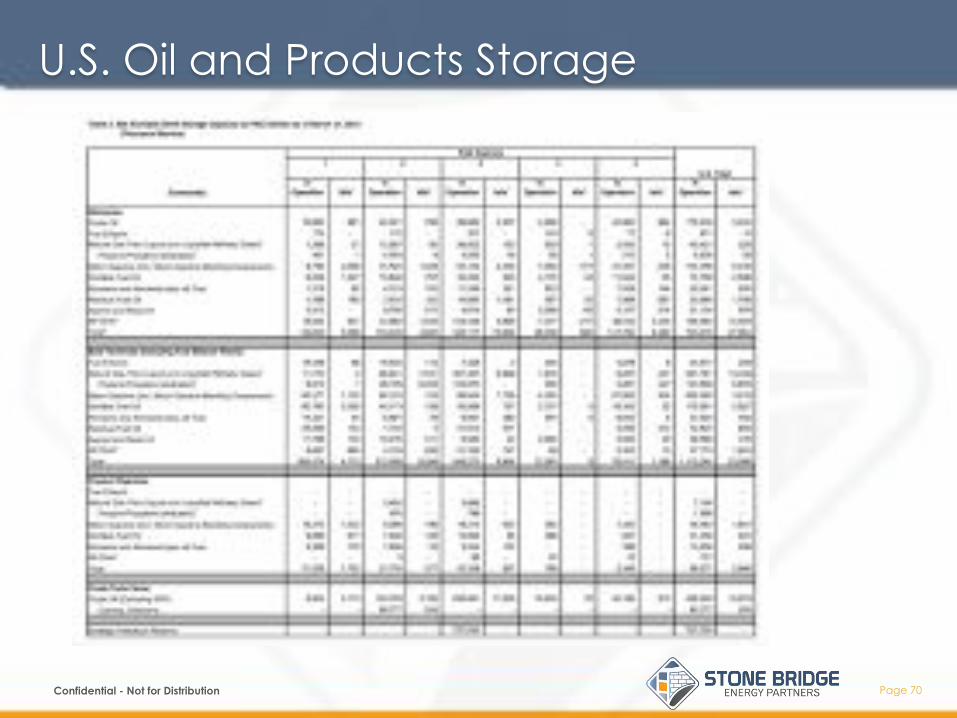

U.S. Oil and Products Storage

Page 71 Page 71 Confidential - Not for Distribution

SPR Storage Sites

Bryan Mound

Big Hill

West Hackberry

Bayou Choctaw

Page 72 Page 72 Confidential - Not for Distribution

U.S. Petroleum Balance Sheet, Week Ending 2/27/2015