Shampoo Industry in India

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

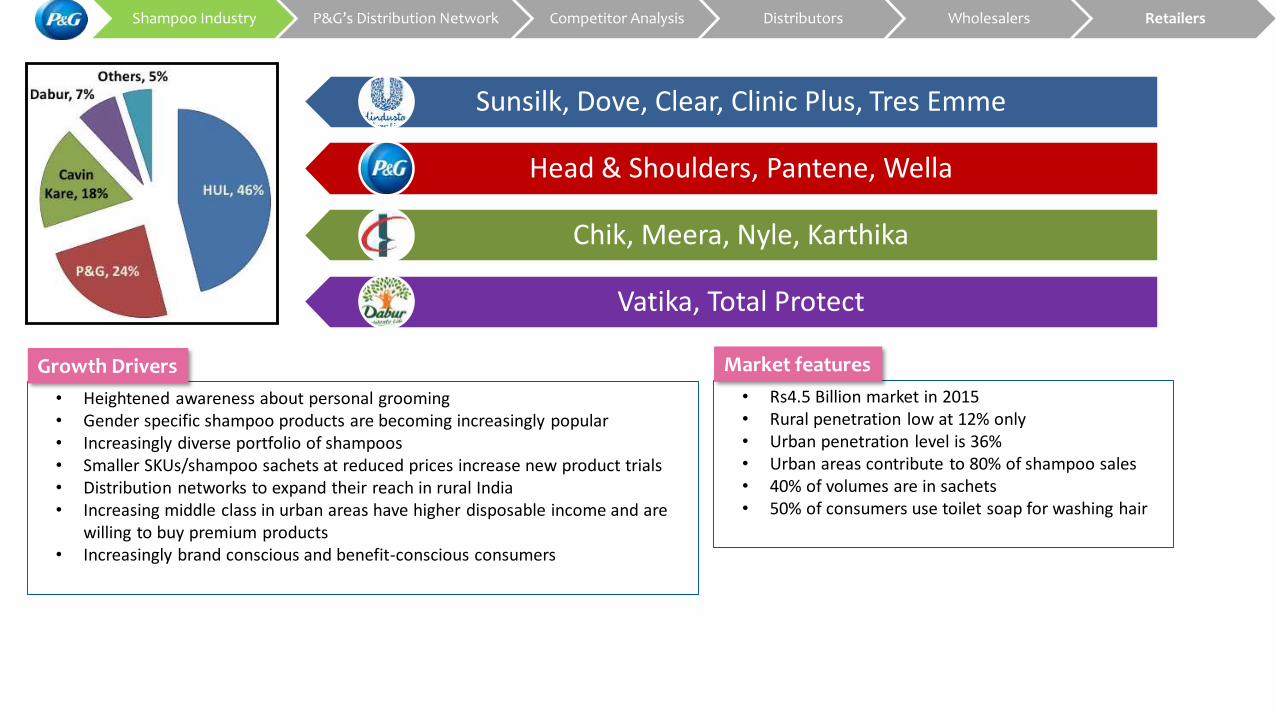

Sunsilk, Dove, Clear, Clinic Plus, Tres Emme

Head & Shoulders, Pantene, Wella

Chik, Meera, Nyle, Karthika

Vatika, Total Protect

• Heightened awareness about personal grooming• Gender specific shampoo products are becoming increasingly popular• Increasingly diverse portfolio of shampoos• Smaller SKUs/shampoo sachets at reduced prices increase new product trials• Distribution networks to expand their reach in rural India• Increasing middle class in urban areas have higher disposable income and are

willing to buy premium products• Increasingly brand conscious and benefit-conscious consumers

Growth Drivers

• Rs4.5 Billion market in 2015• Rural penetration low at 12% only• Urban penetration level is 36%• Urban areas contribute to 80% of shampoo sales• 40% of volumes are in sachets• 50% of consumers use toilet soap for washing hair

Market features

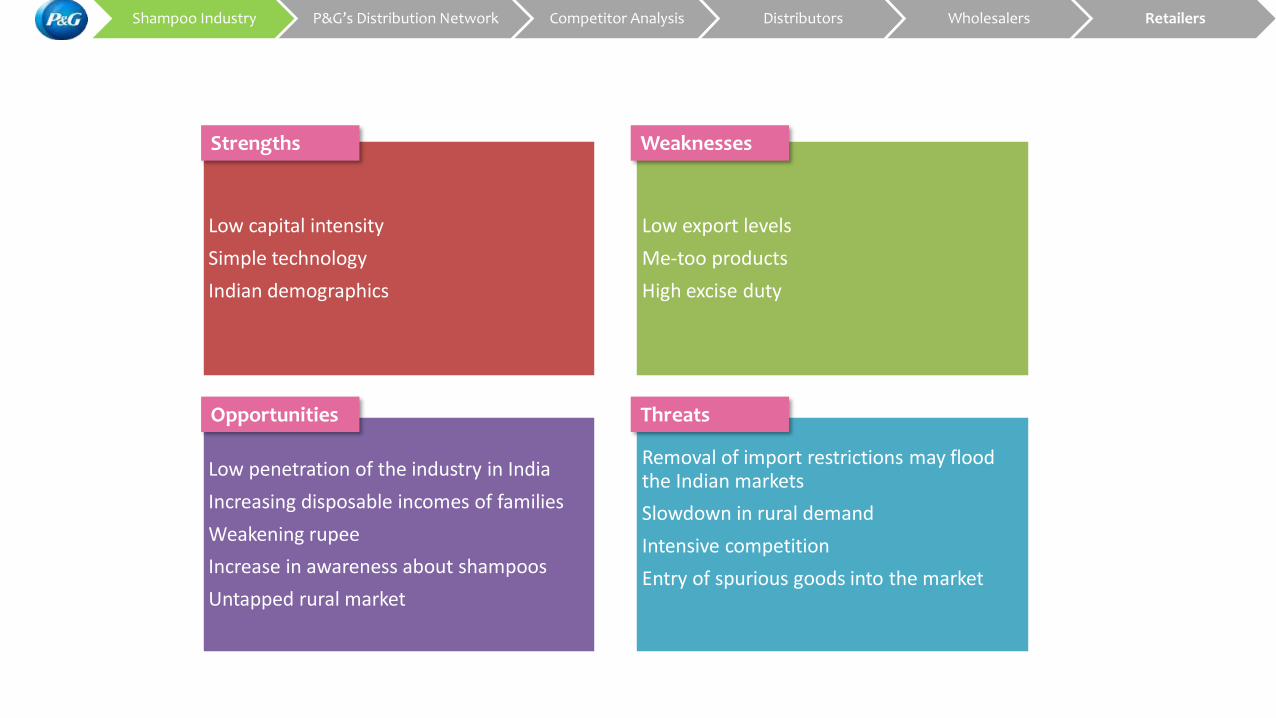

Low capital intensity

Simple technology

Indian demographics

Low export levels

Me-too products

High excise duty

Low penetration of the industry in India

Increasing disposable incomes of families

Weakening rupee

Increase in awareness about shampoos

Untapped rural market

Removal of import restrictions may flood the Indian markets

Slowdown in rural demand

Intensive competition

Entry of spurious goods into the market

Strengths Weaknesses

Opportunities Threats

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

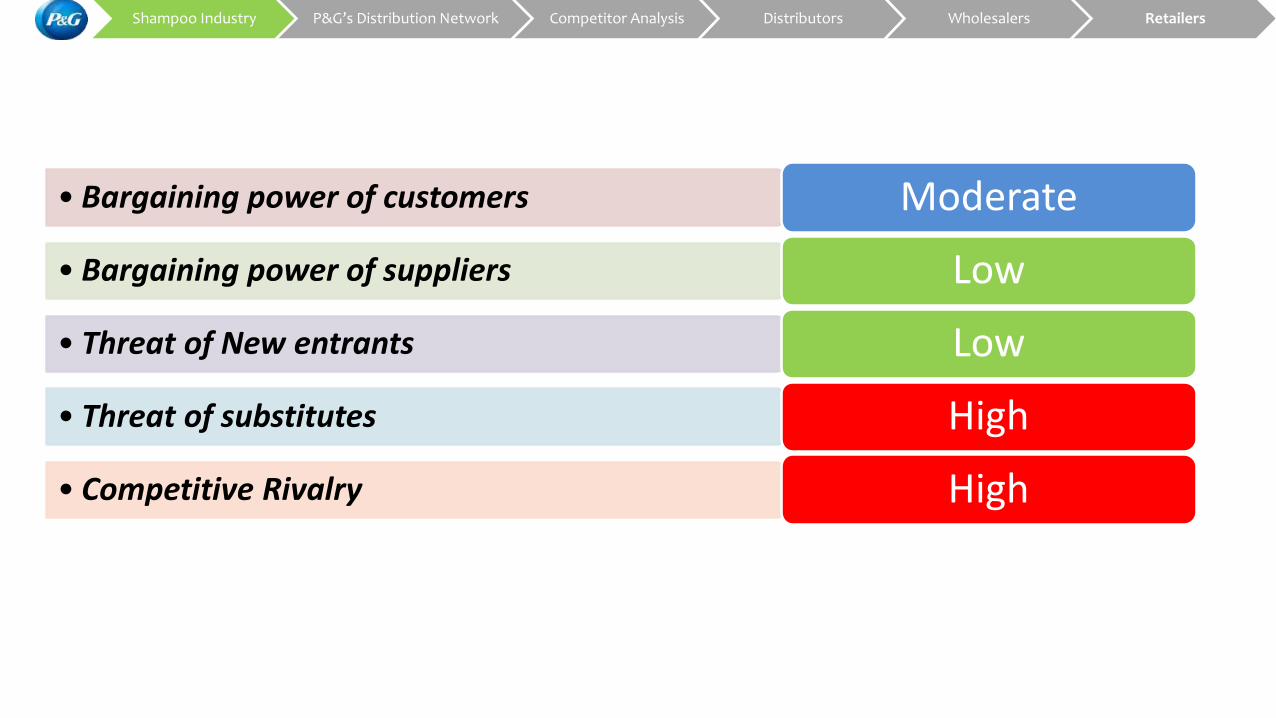

• Bargaining power of customers Moderate

• Bargaining power of suppliers Low

• Threat of New entrants Low

• Threat of substitutes High

• Competitive Rivalry High

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

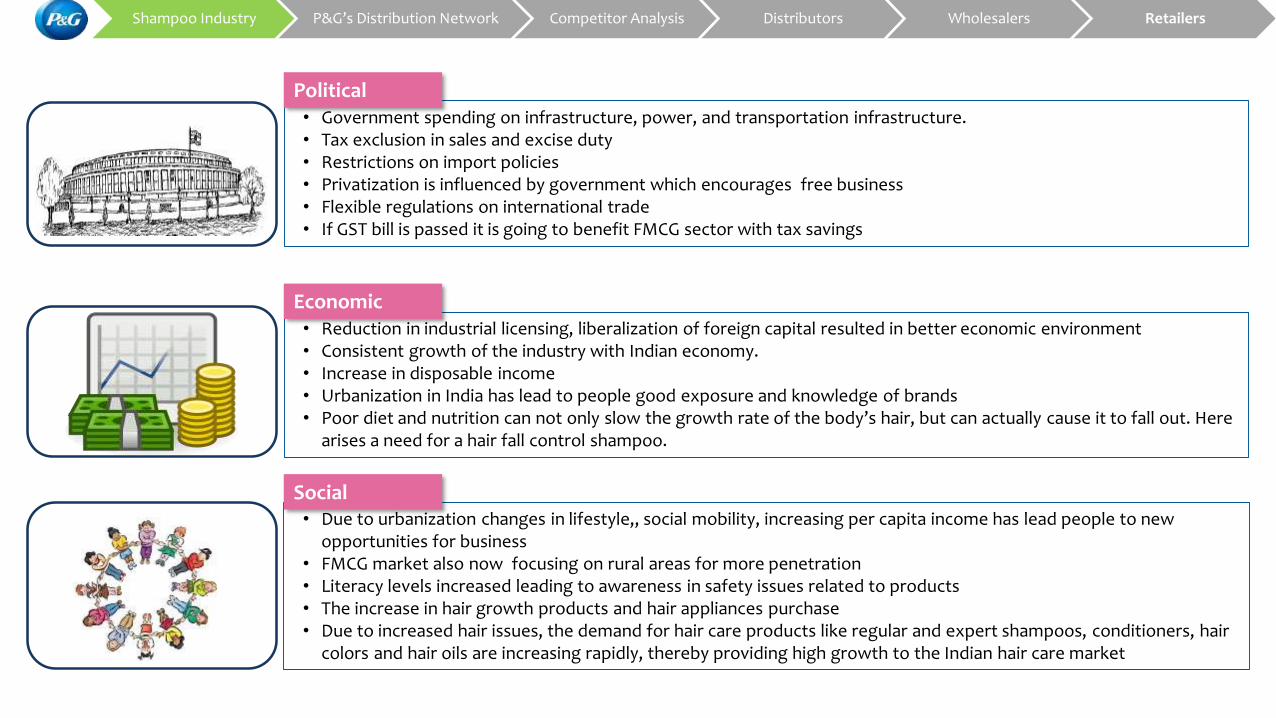

• Government spending on infrastructure, power, and transportation infrastructure.• Tax exclusion in sales and excise duty• Restrictions on import policies• Privatization is influenced by government which encourages free business• Flexible regulations on international trade• If GST bill is passed it is going to benefit FMCG sector with tax savings

• Reduction in industrial licensing, liberalization of foreign capital resulted in better economic environment• Consistent growth of the industry with Indian economy.• Increase in disposable income • Urbanization in India has lead to people good exposure and knowledge of brands • Poor diet and nutrition can not only slow the growth rate of the body’s hair, but can actually cause it to fall out. Here

arises a need for a hair fall control shampoo.

• Due to urbanization changes in lifestyle,, social mobility, increasing per capita income has lead people to new opportunities for business

• FMCG market also now focusing on rural areas for more penetration • Literacy levels increased leading to awareness in safety issues related to products• The increase in hair growth products and hair appliances purchase • Due to increased hair issues, the demand for hair care products like regular and expert shampoos, conditioners, hair

colors and hair oils are increasing rapidly, thereby providing high growth to the Indian hair care market

Political

Economic

Social

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

• Technology enables the incorporation of new ingredients in shampoos, leaving hair cleaner and better conditioned• Shampoo technology will also improve as new ingredients are developed by raw material suppliers. Some important

advances are being made in the development of compounds such as polymers, silicones, and surfactants. These materials will be less irritating, less expensive, more environmentally friendly, and also provide greater functionality and performance.

• Production optimization along with equipment standardization is helping to reduce investments in factories.• Packaging innovation is ensuring lightweight bottles o as to reduce the quantities of plastics used• The multi stage Viscoprop impellers are helping in mixing different densities of constituents decreasing mixing time• Investment in IT is reducing costs in supply chain by easing information access

• Product Information Package is to be provided as per Law.• Drug and Magic Remedies (Objectionable Advertisement) Act, 1954

Technological

Legal

• Dryness care & Heat defence emphasis due to climatic changes• When there is very little humidity in the air and conditions are very dry breakage is common• Desalinated water can cause harmful scalp build-up that leads to hair breaking off above the external root sheath. • Other environmental factors such weather, climate changes affect industry• Due to global warming environmental laws and regulations are getting tougher which affects firm’s production

procedures, steps taken for remedies• Greenwashing is increasingly a common trend• Shampoo bottles made from sugarcane are the newest development in sustainable packaging. It uses 70% less fossil

fuel in its production. P&G reports that using plant-based material for plastic bottles decreases greenhouse gas output by 170%.

Environmental

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

Excessive fragmentation

New product development

Salon services

Demand for professional shampoos

Herbal shampoos

Penetrative pricing- value packs

Selling online

Digital marketing

Current Trends

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

P&G is headquartered in downtown Cincinnati, Ohio

Started n 1837 by William Procter and James Gamble

Markets 250+ brands to 5billion consumers in 140 countries

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

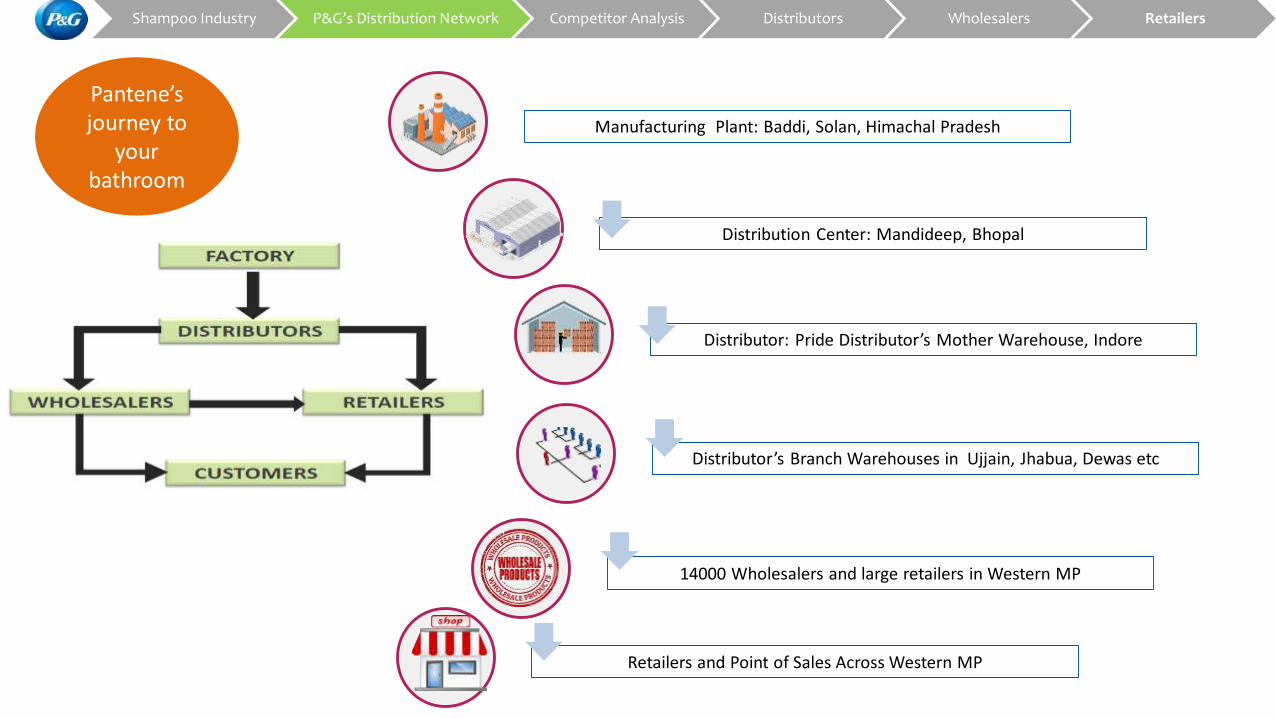

Manufacturing Plant: Baddi, Solan, Himachal Pradesh

Distribution Center: Mandideep, Bhopal

Distributor: Pride Distributor’s Mother Warehouse, Indore

Distributor’s Branch Warehouses in Ujjain, Jhabua, Dewas etc

14000 Wholesalers and large retailers in Western MP

Retailers and Point of Sales Across Western MP

Pantene’s journey to

your bathroom

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

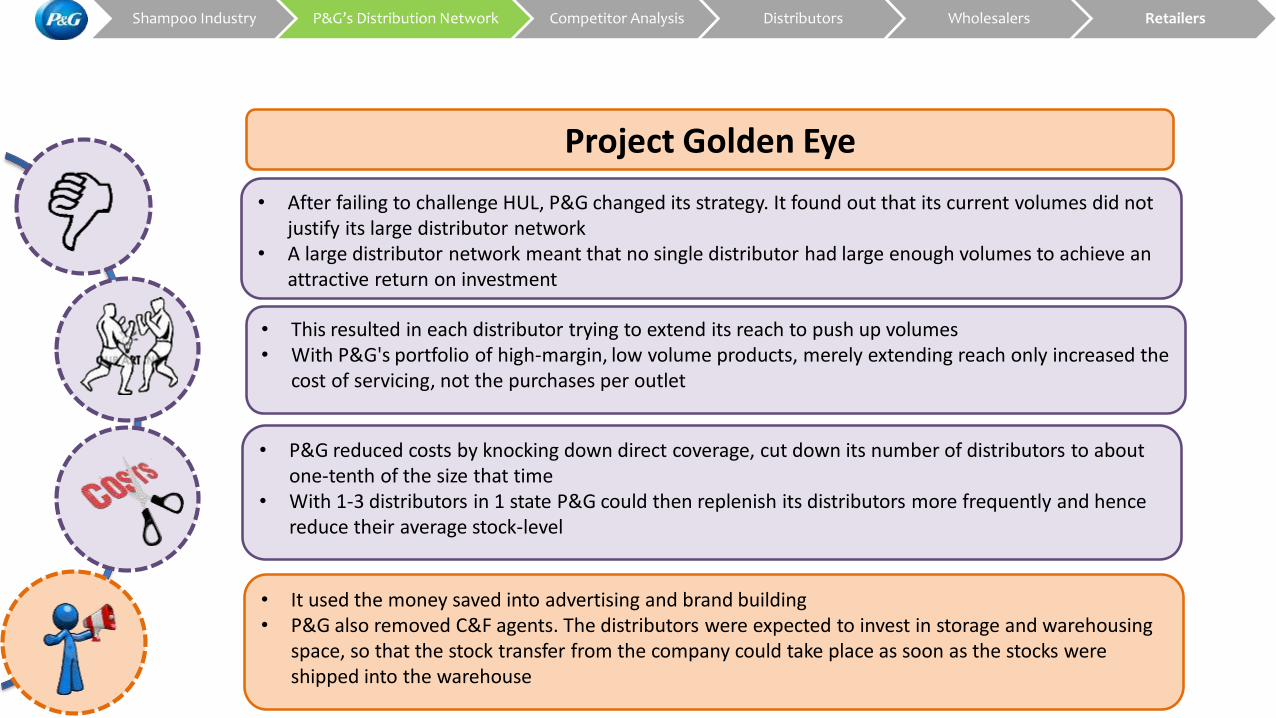

• After failing to challenge HUL, P&G changed its strategy. It found out that its current volumes did not justify its large distributor network

• A large distributor network meant that no single distributor had large enough volumes to achieve an attractive return on investment

• This resulted in each distributor trying to extend its reach to push up volumes• With P&G's portfolio of high-margin, low volume products, merely extending reach only increased the

cost of servicing, not the purchases per outlet

• P&G reduced costs by knocking down direct coverage, cut down its number of distributors to about one-tenth of the size that time

• With 1-3 distributors in 1 state P&G could then replenish its distributors more frequently and hence reduce their average stock-level

• It used the money saved into advertising and brand building• P&G also removed C&F agents. The distributors were expected to invest in storage and warehousing

space, so that the stock transfer from the company could take place as soon as the stocks were shipped into the warehouse

Project Golden Eye

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

Wholesalers and retailers pointed out that margins are same for products of both the companies. They also mentioned that frequency of visits by sales people are also same

As HUL has higher number of products, it takes up a larger shelf space compared to P&G’s products

P&G pays higher slotting fee to give sufficient to its limited portfolio

Wholesalers mentioned that demand for HUL products are more as they have more products and variants within Shampoos

Undercutting is common for HUL products

There are only 2 promoters from P&G that are associated with a supermarket and are taking care of all product lines. HUL has 1 promoter for each product line

P&G’s sales staff is on distributor’s payrolls unlike HUL

vs

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

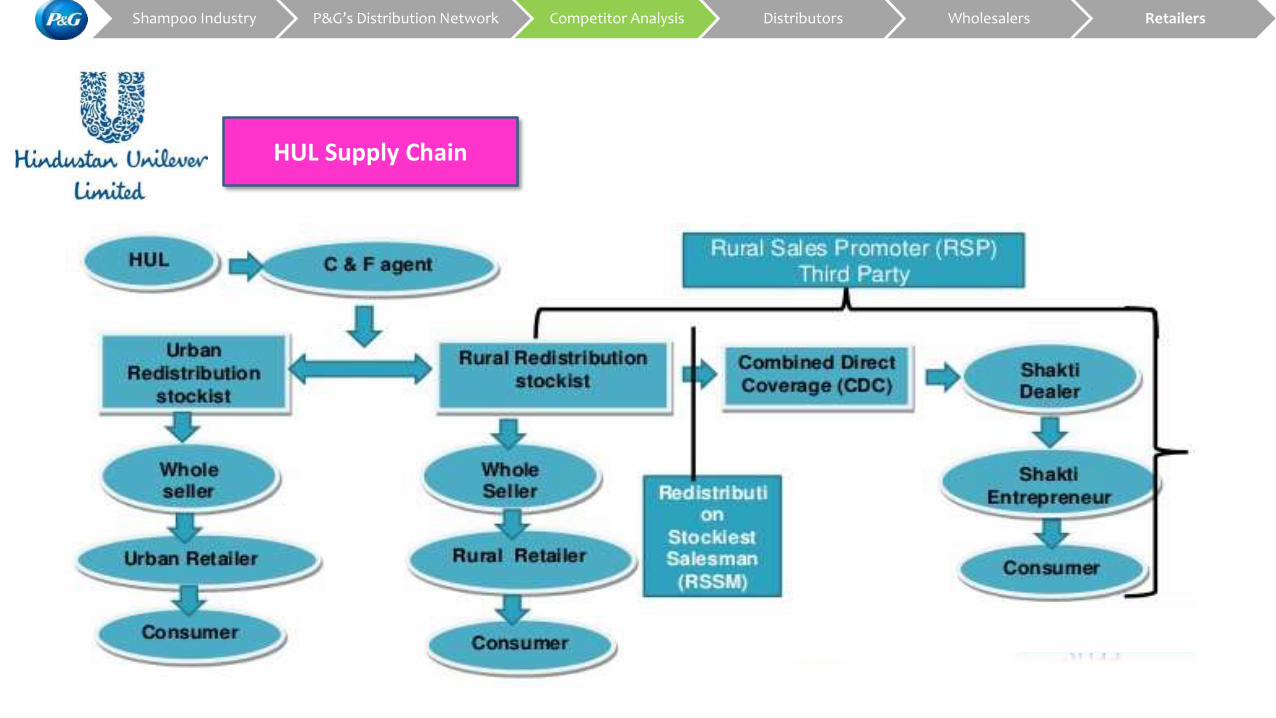

HUL Supply Chain

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

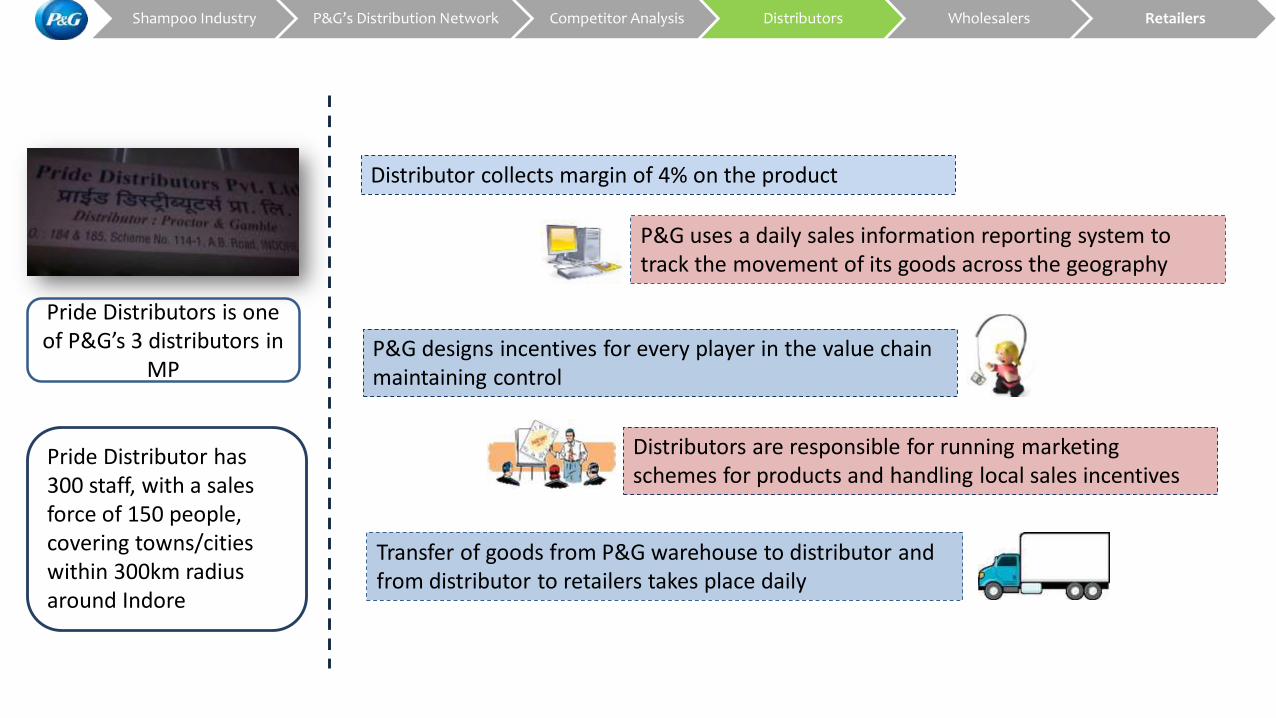

P&G designs incentives for every player in the value chain maintaining control

P&G uses a daily sales information reporting system to track the movement of its goods across the geography

Transfer of goods from P&G warehouse to distributor and from distributor to retailers takes place daily

Distributor collects margin of 4% on the product

Distributors are responsible for running marketing schemes for products and handling local sales incentives

Pride Distributor has 300 staff, with a sales force of 150 people, covering towns/cities within 300km radius around Indore

Pride Distributors is one of P&G’s 3 distributors in

MP

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

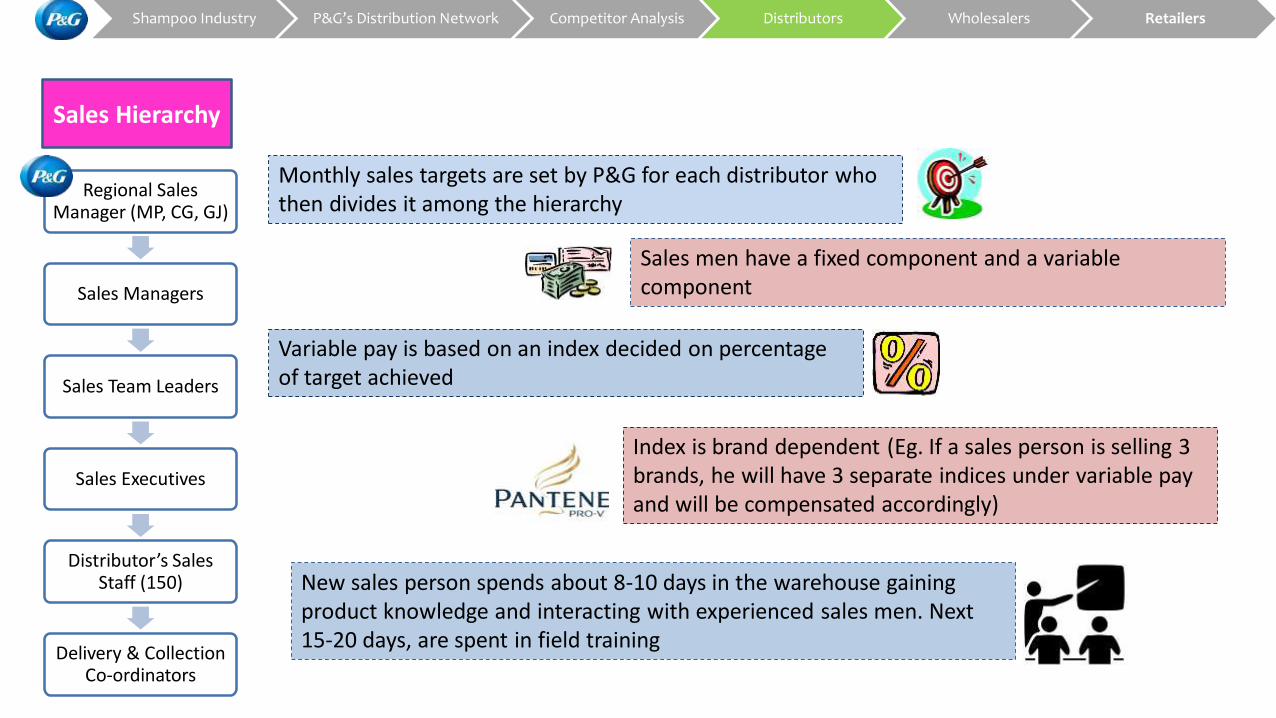

Regional Sales Manager (MP, CG, GJ)

Sales Managers

Sales Team Leaders

Sales Executives

Distributor’s Sales Staff (150)

Delivery & Collection Co-ordinators

Sales Hierarchy

Variable pay is based on an index decided on percentage of target achieved

Sales men have a fixed component and a variable component

New sales person spends about 8-10 days in the warehouse gaining product knowledge and interacting with experienced sales men. Next 15-20 days, are spent in field training

Monthly sales targets are set by P&G for each distributor who then divides it among the hierarchy

Index is brand dependent (Eg. If a sales person is selling 3 brands, he will have 3 separate indices under variable pay and will be compensated accordingly)

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

They were delighted to meet Ronak and Abhinav

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

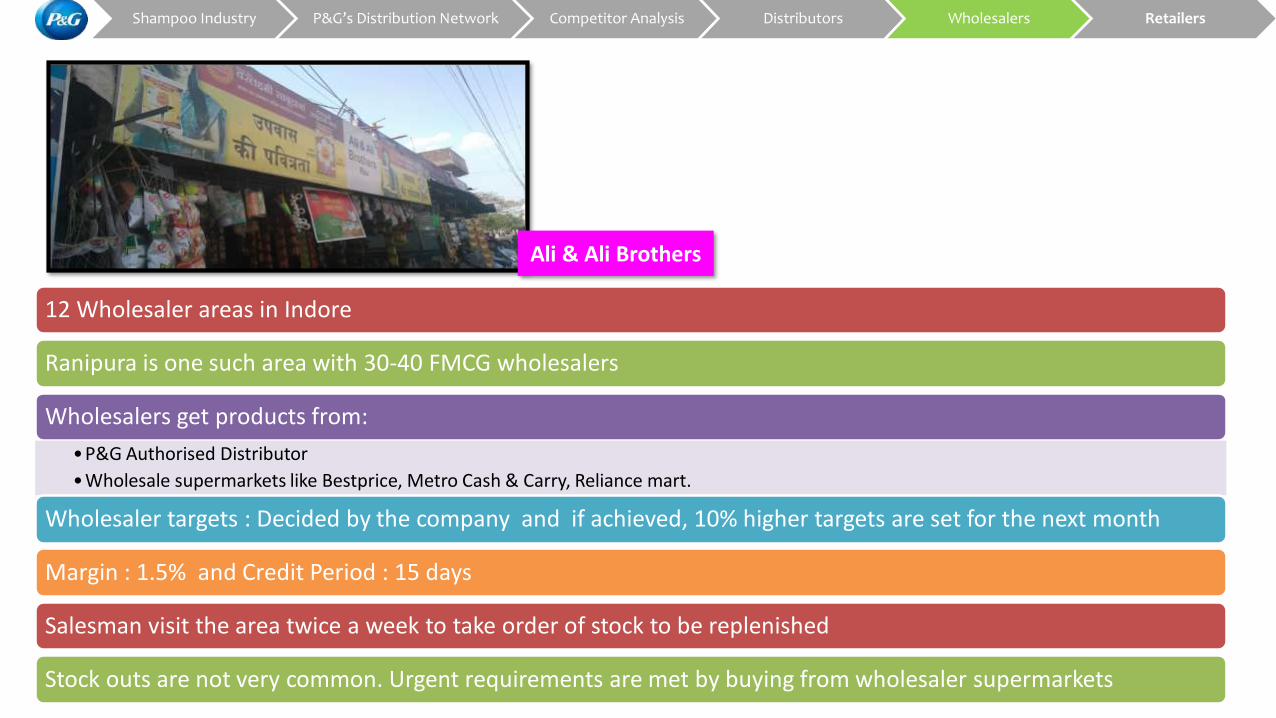

12 Wholesaler areas in Indore

Ranipura is one such area with 30-40 FMCG wholesalers

Wholesalers get products from:

•P&G Authorised Distributor

•Wholesale supermarkets like Bestprice, Metro Cash & Carry, Reliance mart.

Wholesaler targets : Decided by the company and if achieved, 10% higher targets are set for the next month

Margin : 1.5% and Credit Period : 15 days

Salesman visit the area twice a week to take order of stock to be replenished

Stock outs are not very common. Urgent requirements are met by buying from wholesaler supermarkets

Ali & Ali Brothers

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

Volume wise sales

• Sachets : 70%

• Bottles :30%

Typical customers for wholesalers

• Local kirana stores

• Medical stores

Typical customer buys about 10 -15 sachets of Pantene and Head& Shoulders

Wholesalers pass on parts of discounts/incentives to retailers

Quantity based incentive schemes are run by P&G to encourage wholesalers to meet targets

Ali & Ali Brothers

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

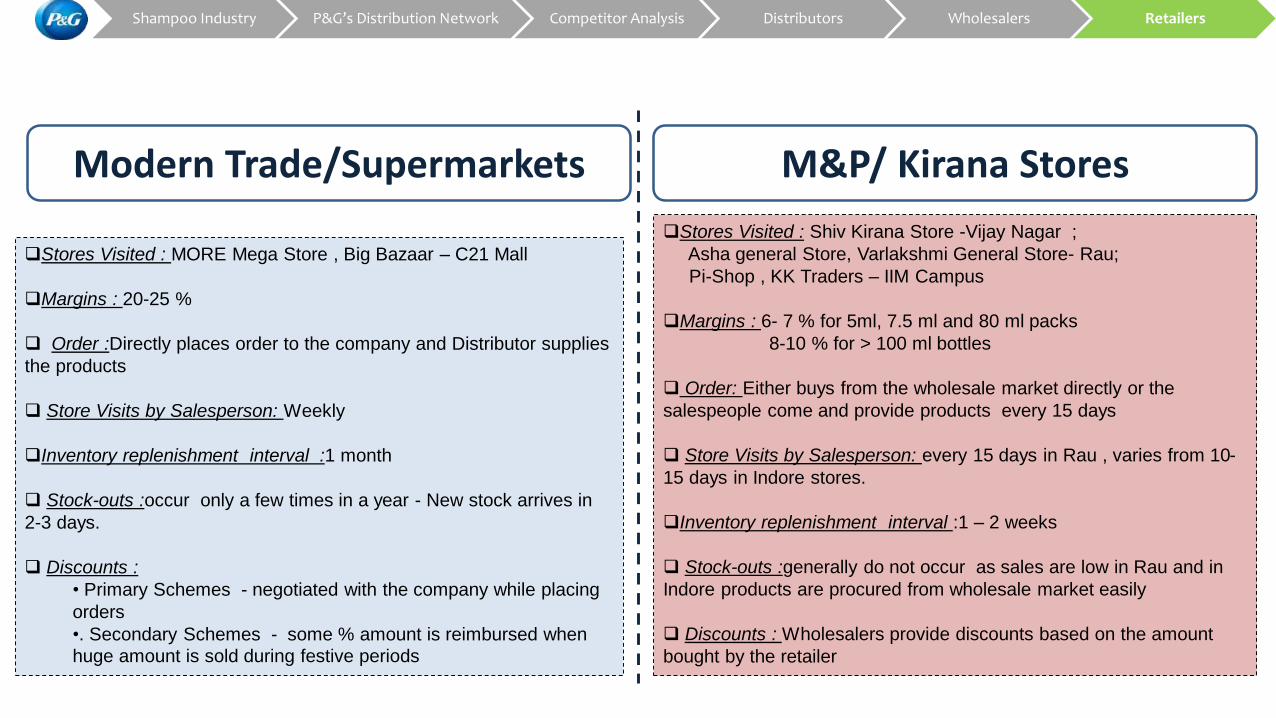

Stores Visited : MORE Mega Store , Big Bazaar – C21 Mall

Margins : 20-25 %

Order :Directly places order to the company and Distributor supplies

the products

Store Visits by Salesperson: Weekly

Inventory replenishment interval :1 month

Stock-outs :occur only a few times in a year - New stock arrives in

2-3 days.

Discounts :

• Primary Schemes - negotiated with the company while placing

orders

•. Secondary Schemes - some % amount is reimbursed when huge amount is sold during festive periods

Stores Visited : Shiv Kirana Store -Vijay Nagar ;

Asha general Store, Varlakshmi General Store- Rau;

Pi-Shop , KK Traders – IIM Campus

Margins : 6- 7 % for 5ml, 7.5 ml and 80 ml packs

8-10 % for > 100 ml bottles

Order: Either buys from the wholesale market directly or the

salespeople come and provide products every 15 days

Store Visits by Salesperson: every 15 days in Rau , varies from 10-

15 days in Indore stores.

Inventory replenishment interval :1 – 2 weeks

Stock-outs :generally do not occur as sales are low in Rau and in

Indore products are procured from wholesale market easily

Discounts : Wholesalers provide discounts based on the amount

bought by the retailer

Modern Trade/Supermarkets M&P/ Kirana Stores

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers

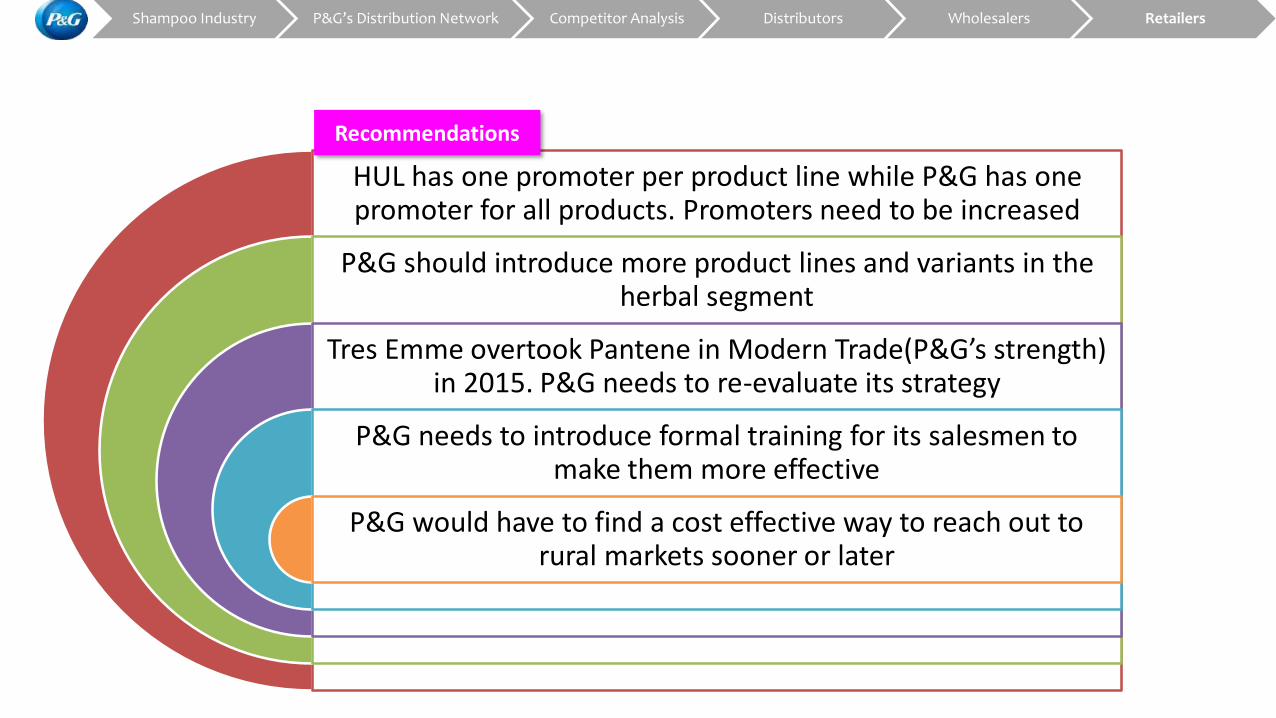

HUL has one promoter per product line while P&G has one promoter for all products. Promoters need to be increased

P&G should introduce more product lines and variants in the herbal segment

Tres Emme overtook Pantene in Modern Trade(P&G’s strength) in 2015. P&G needs to re-evaluate its strategy

P&G needs to introduce formal training for its salesmen to make them more effective

P&G would have to find a cost effective way to reach out to rural markets sooner or later

Recommendations

Shampoo Industry P&G’s Distribution Network Competitor Analysis Distributors Wholesalers Retailers