SEMINAR KEBANGSAAN

PERAKAUNAN DAN PENGAUDITAN

AGENSI AWAM TAHUN 2018

SEMINAR KEBANGSAAN PERAKAUNAN DAN

PENGAUDITAN AGENSI AWAM TAHUN 2018

Zuhairi Bin Dziaruddin

Partner, AljeffriDean, Chartered Accountants

11 December 2018 – 13 December 2018

1

2

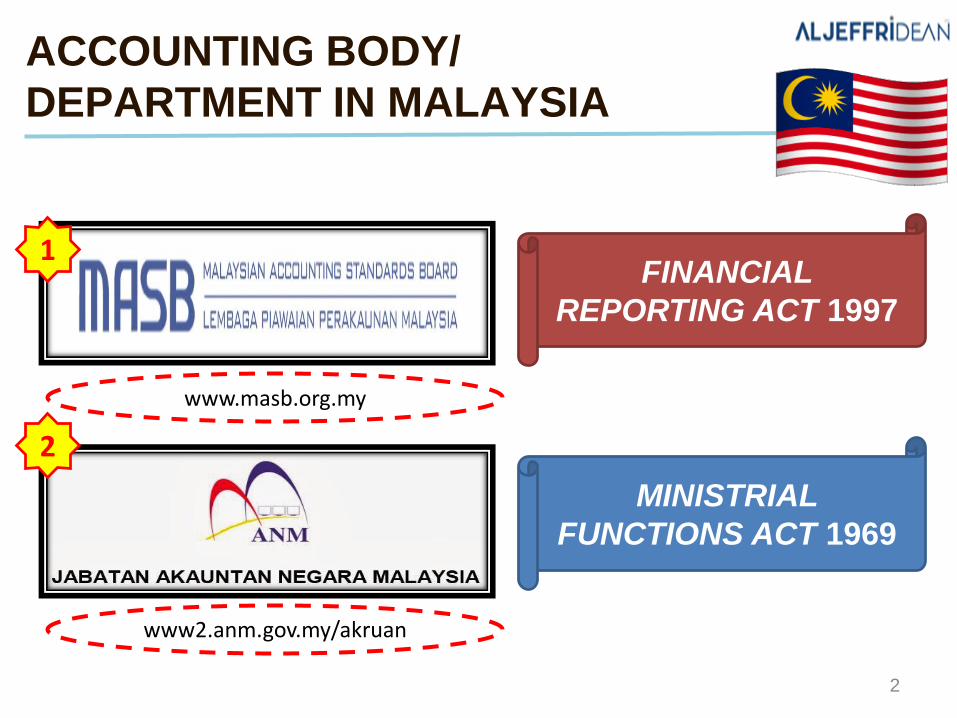

ACCOUNTING BODY/

DEPARTMENT IN MALAYSIA

FINANCIAL

REPORTING ACT 1997

MINISTRIAL

FUNCTIONS ACT 1969

1

2

www.masb.org.my

www2.anm.gov.my/akruan

3

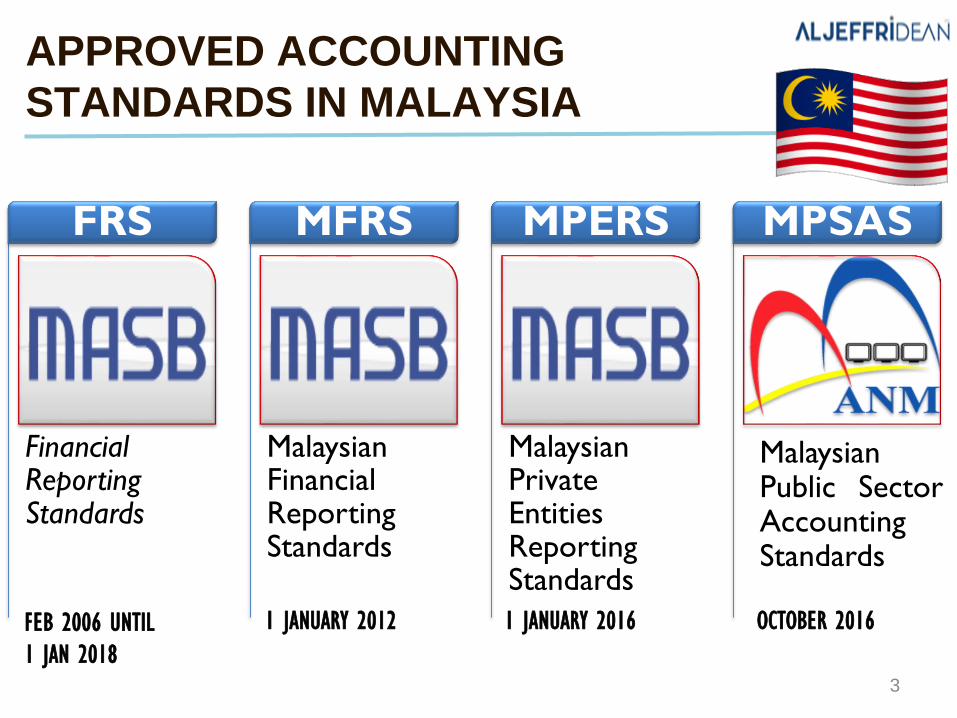

APPROVED ACCOUNTING

STANDARDS IN MALAYSIA

Financial Reporting Standards

FRS

Malaysian Financial Reporting Standards

MFRS

Malaysian Private Entities Reporting Standards

MPERS MPSAS

FEB 2006 UNTIL

1 JAN 2018

1 JANUARY 2012 1 JANUARY 2016 OCTOBER 2016

MalaysianPublic SectorAccountingStandards

4

APPROVED ACCOUNTING

STANDARDS IN MALAYSIA…CONT’D

• Reporting standards adopted by Entities other than privateentities. Entities itself required to submit financial statementsto the Securities Commission (SC) or Bank Negara Malaysia(BNM) or a subsidiary or associate or jointly controlled by anentities which is required to submit the financial statements tothe SC or BNM

MFRS/FRS

• Reporting standards for private companies incorporated underthe Companies Act are not required to submit financialstatements to the SC or BNM and not a subsidiary orassociate company to entities required to submit their financialstatements to the SC or BNM

MPERS

• Established for public sector entities in Malaysia other thanGovernment Business Enterprise. Public sector entitiesinclude Federal Government, State Government and LocalGovernment

MPSAS

5

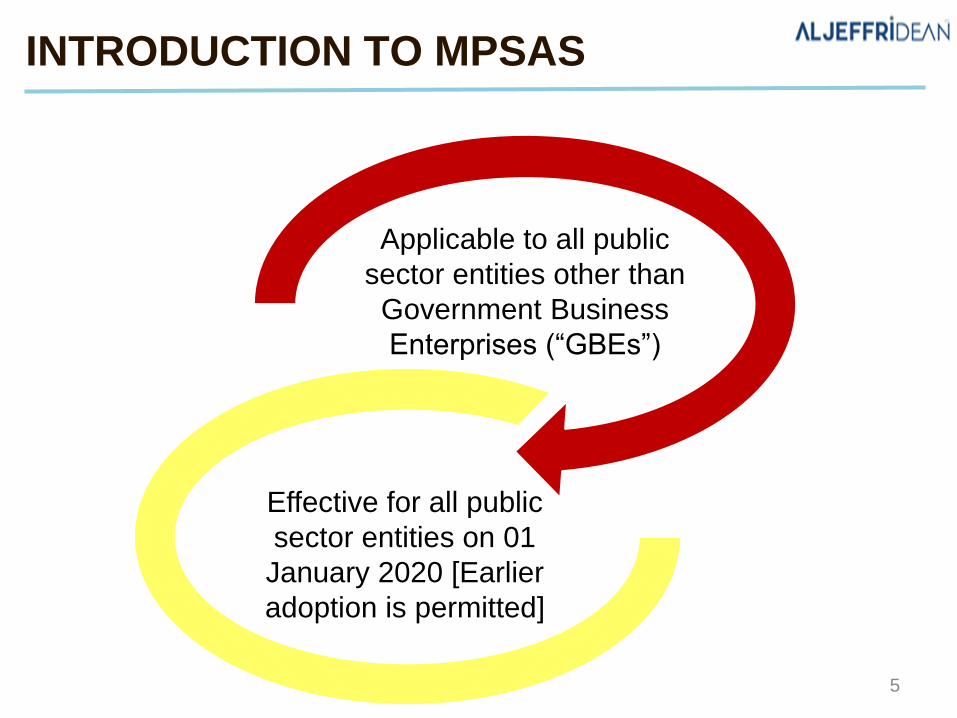

INTRODUCTION TO MPSAS

Applicable to all public

sector entities other than

Government Business

Enterprises (“GBEs”)

Effective for all public

sector entities on 01

January 2020 [Earlier

adoption is permitted]

6

GOVERNMENT BUSINESS

ENTERPRISES

GBE

• An entity with power to

contract in its own name

• Has been assigned the

financial and operational

authority to carry on a

business

• Sell goods and services, in the

normal course of business

with profit or full cost recovery

• Not reliant on continuing

government funding to be a

going concern

• Controlled by a public sector

7

GOVERNMENT BUSINESS

ENTERPRISES… CONT’D

IS IT A GBE

YES NO

CHOICE OF EITHER

MFRS/FRS

MPERS MPSAS

Definition is

being

reviewed to

be less

restrictive

8

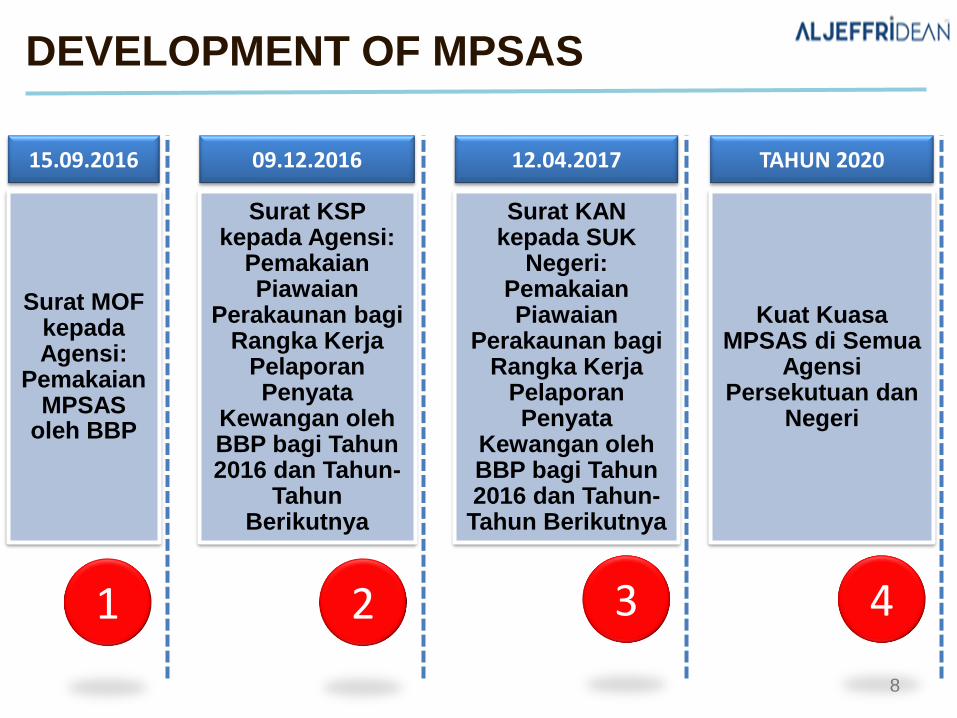

DEVELOPMENT OF MPSAS

1 432

15.09.2016

Surat MOF kepadaAgensi:

PemakaianMPSAS

oleh BBP

09.12.2016 12.04.2017

Surat KAN kepada SUK

Negeri: PemakaianPiawaian

Perakaunan bagiRangka Kerja

PelaporanPenyata

Kewangan oleh BBP bagi Tahun2016 dan Tahun-Tahun Berikutnya

TAHUN 2020

Kuat KuasaMPSAS di Semua

AgensiPersekutuan dan

Negeri

Surat KSP kepada Agensi:

PemakaianPiawaian

Perakaunan bagiRangka Kerja

PelaporanPenyata

Kewangan oleh BBP bagi Tahun2016 dan Tahun-

TahunBerikutnya

9

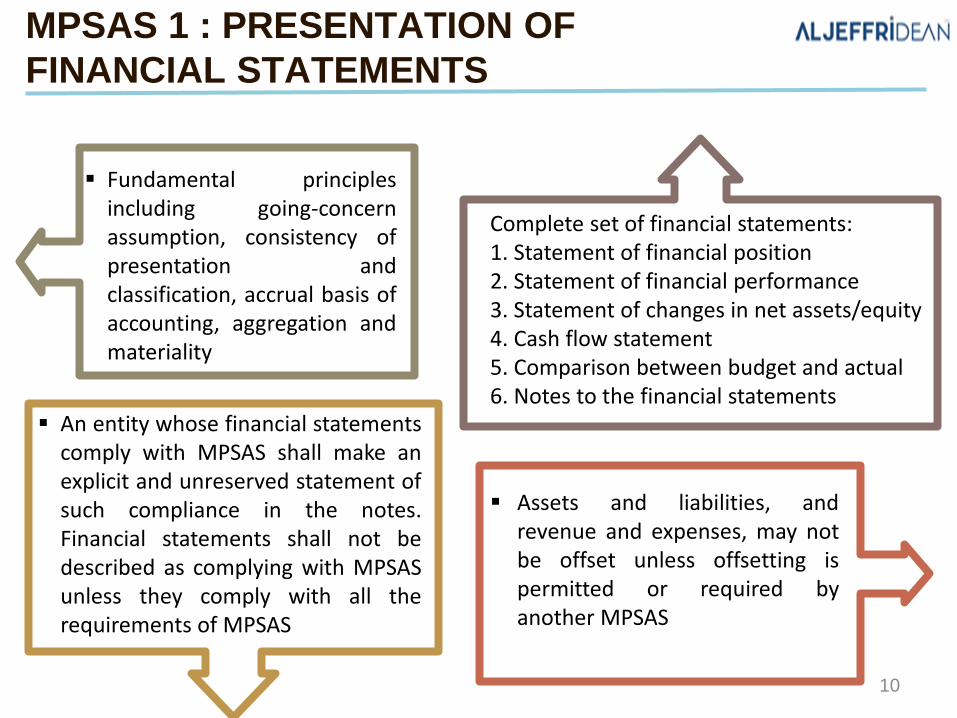

MPSAS

1

▪ Fundamental principlesincluding going-concernassumption, consistency ofpresentation andclassification, accrual basis ofaccounting, aggregation andmateriality

▪ Assets and liabilities, andrevenue and expenses, may notbe offset unless offsetting ispermitted or required byanother MPSAS

Complete set of financial statements:1. Statement of financial position2. Statement of financial performance3. Statement of changes in net assets/equity4. Cash flow statement5. Comparison between budget and actual6. Notes to the financial statements

▪ An entity whose financial statementscomply with MPSAS shall make anexplicit and unreserved statement ofsuch compliance in the notes.Financial statements shall not bedescribed as complying with MPSASunless they comply with all therequirements of MPSAS

MPSAS 1 : PRESENTATION OF

FINANCIAL STATEMENTS

10

MPSAS 1 : PRESENTATION OF

FINANCIAL STATEMENTS... CONT’D

▪ Comparative prior-period information shall be presented for all amountsshown in the financial statements and notes

▪ Comparative information shall be included when it is relevant to anunderstanding of the current period’s financial statements

▪ In the case presentation or classification is amended, comparativeamounts shall be reclassified, and the nature, amount of, and reason forany reclassification shall be disclosed

▪ Financial statements generally to be preparedannually

▪ If the date of the year-end changes, and financialstatements are presented for a period other thanone year, disclosure thereof is required

1

2

11

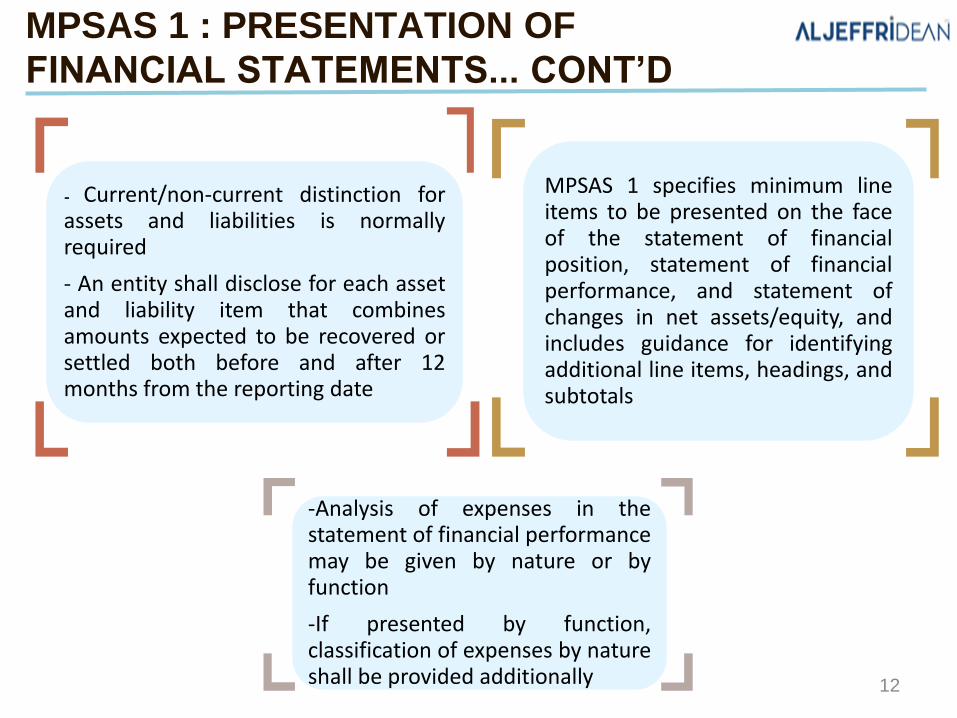

MPSAS 1 : PRESENTATION OF

FINANCIAL STATEMENTS... CONT’D

MPSAS 1 specifies minimum lineitems to be presented on the faceof the statement of financialposition, statement of financialperformance, and statement ofchanges in net assets/equity, andincludes guidance for identifyingadditional line items, headings, andsubtotals

-Analysis of expenses in thestatement of financial performancemay be given by nature or byfunction

-If presented by function,classification of expenses by natureshall be provided additionally

- Current/non-current distinction forassets and liabilities is normallyrequired

- An entity shall disclose for each assetand liability item that combinesamounts expected to be recovered orsettled both before and after 12months from the reporting date

12

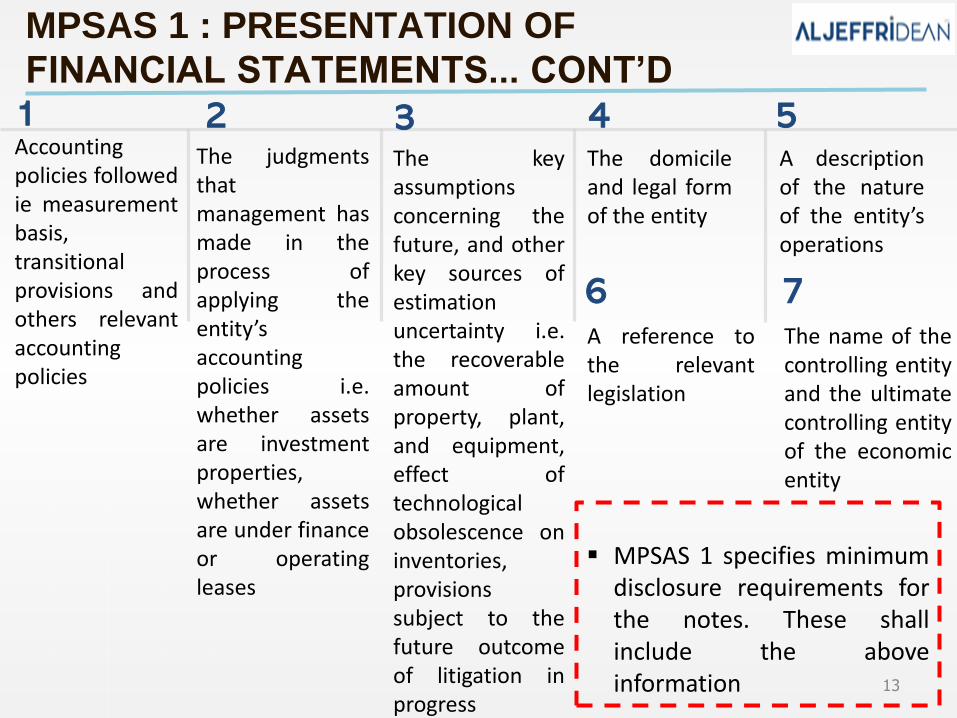

The judgmentsthatmanagement hasmade in theprocess ofapplying theentity’saccountingpolicies i.e.whether assetsare investmentproperties,whether assetsare under financeor operatingleases

A reference tothe relevantlegislation

1Accountingpolicies followedie measurementbasis,transitionalprovisions andothers relevantaccountingpolicies

The keyassumptionsconcerning thefuture, and otherkey sources ofestimationuncertainty i.e.the recoverableamount ofproperty, plant,and equipment,effect oftechnologicalobsolescence oninventories,provisionssubject to thefuture outcomeof litigation inprogress

6

The domicileand legal formof the entity

A descriptionof the natureof the entity’soperations

The name of thecontrolling entityand the ultimatecontrolling entityof the economicentity

7

MPSAS 1 : PRESENTATION OF

FINANCIAL STATEMENTS... CONT’D

2 3 4 5

▪ MPSAS 1 specifies minimumdisclosure requirements forthe notes. These shallinclude the aboveinformation 13

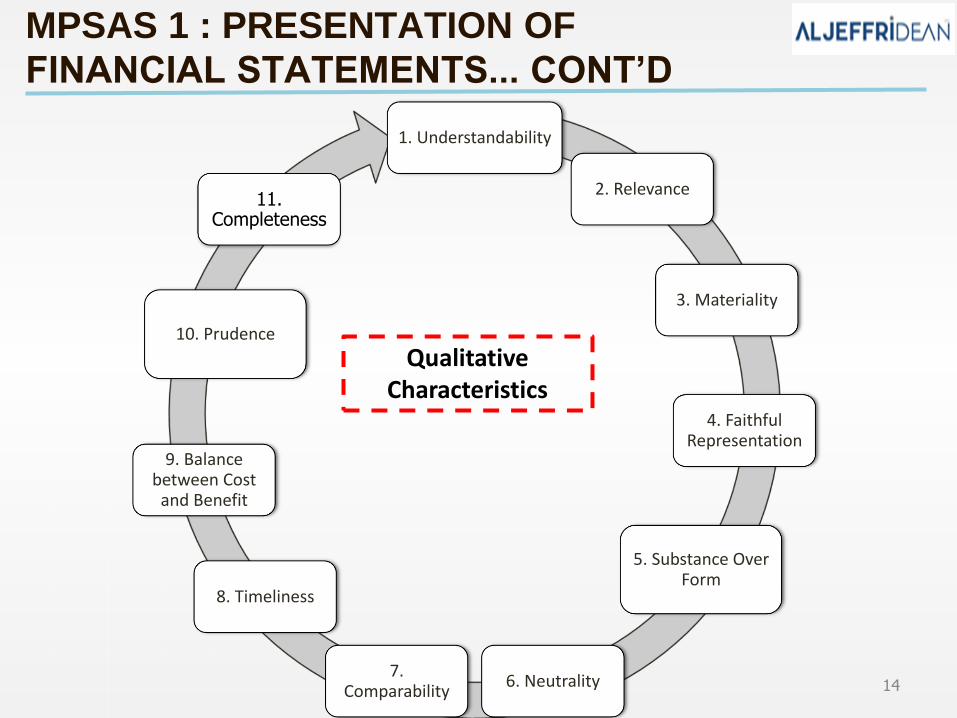

MPSAS 1 : PRESENTATION OF

FINANCIAL STATEMENTS... CONT’D

1. Understandability

2. Relevance

3. Materiality

4. Faithful Representation

5. Substance Over Form

6. Neutrality7.

Comparability

8. Timeliness

9. Balance between Cost

and Benefit

10. Prudence

11. Completeness

Qualitative Characteristics

14

ILLUSTRATIVE STATEMENT OF

FINANCIAL POSITION

15

ILLUSTRATIVE STATEMENT OF

FINANCIAL POSITION… CONT’D

16

ILLUSTRATIVE STATEMENT OF

FINANCIAL PERFOMANCE (1)

17

ILLUSTRATIVE STATEMENT OF

FINANCIAL PERFOMANCE (2)

18

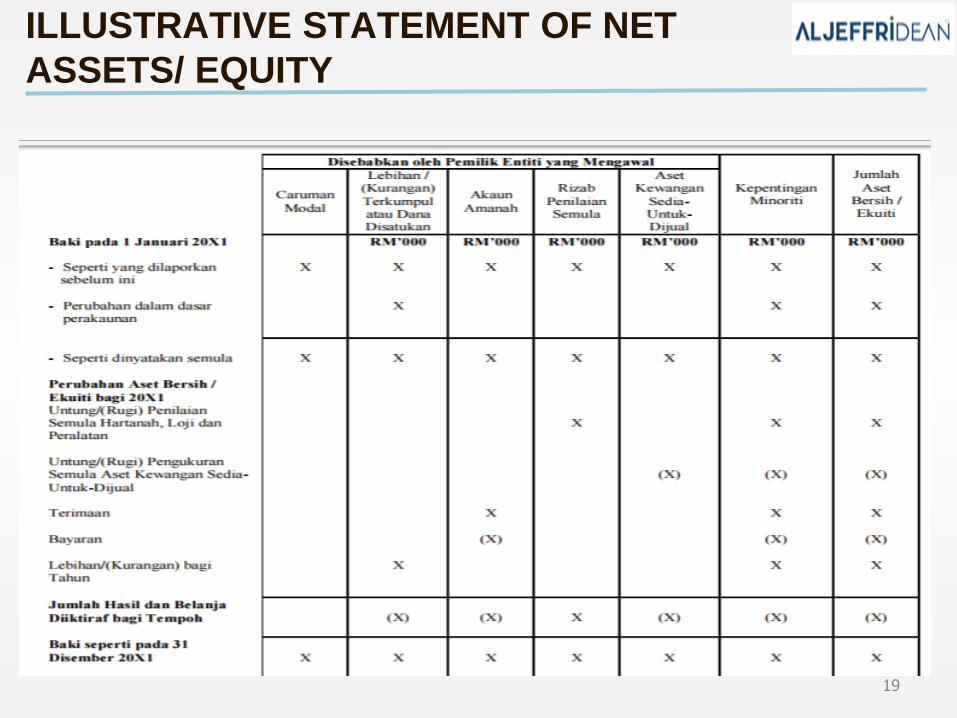

ILLUSTRATIVE STATEMENT OF NET

ASSETS/ EQUITY

19

20

MPSAS

9

MPSAS 9 : REVENUE FROM

EXCHANGE TRANSACTIONS

1. The rendering of services

2. The sale of goods

3. The use of others of entity assetsyielding interest, royalties, anddividends

➢ MPSAS 9 applies to revenue arisingfrom the following exchangetransactions and events:

➢ Revenue shall be measured atthe fair value of theconsideration received orreceivable

Exchange transactions aretransactions in which oneentity receives assets orservices, or has liabilitiesextinguished, and directlygives approximately equalvalue (primarily in the formcash, goods, services, or useof assets) to another entityin exchange

21

MPSAS 9 : REVENUE FROM

EXCHANGE TRANSACTIONS… CONT’D

➢ When the arrangement constitutes afinancing transaction, the fair value ofthe consideration is determined bydiscounting all future receipts using animputed rate of interest determinedeither: (a) The prevailing rate for asimilar instrument of an issuer with asimilar credit rating; or (b) A rate ofinterest that discounts the nominalamount of the instrument to thecurrent cash sales price of the goods orservices. The difference is recognised asinterest revenue

➢ When goods or services areexchanged or swapped for goodsor services that are of a similarnature and value, the exchangeis not regarded as a transactionthat generates revenue

Revenue is recognised when it is probablethat: (a) Future economic benefits or servicepotential will flow to the entity; and (b) Thesebenefits can be measured reliably 22

MPSAS 9 : REVENUE FROM

EXCHANGE TRANSACTIONS… CONT’D

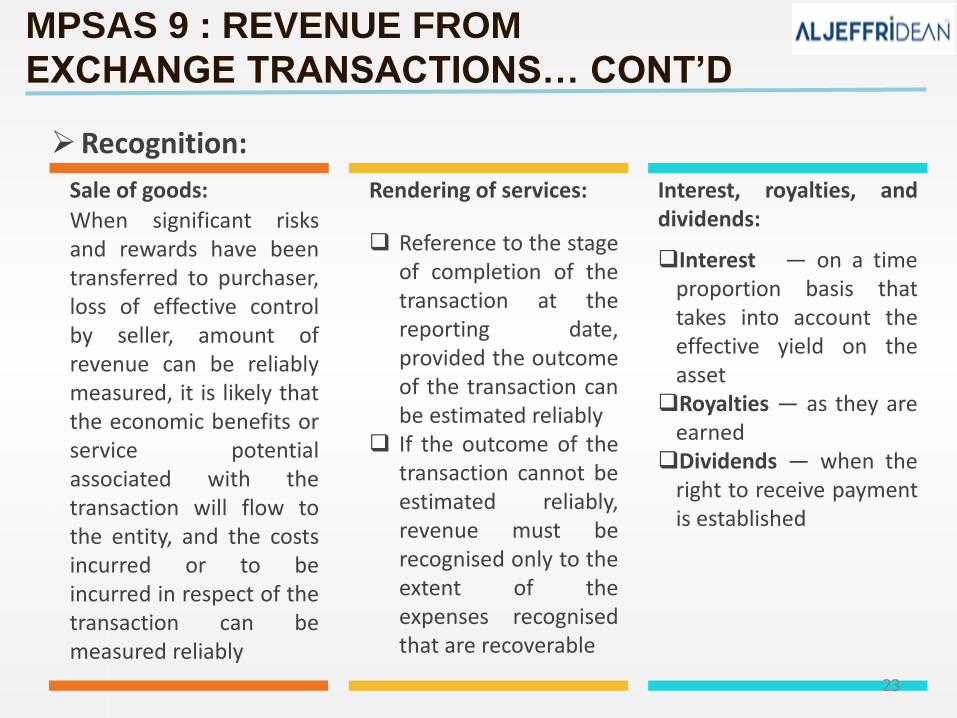

When significant risksand rewards have beentransferred to purchaser,loss of effective controlby seller, amount ofrevenue can be reliablymeasured, it is likely thatthe economic benefits orservice potentialassociated with thetransaction will flow tothe entity, and the costsincurred or to beincurred in respect of thetransaction can bemeasured reliably

❑ Reference to the stageof completion of thetransaction at thereporting date,provided the outcomeof the transaction canbe estimated reliably

❑ If the outcome of thetransaction cannot beestimated reliably,revenue must berecognised only to theextent of theexpenses recognisedthat are recoverable

❑Interest — on a timeproportion basis thattakes into account theeffective yield on theasset

❑Royalties — as they areearned

❑Dividends — when theright to receive paymentis established

➢Recognition:

Sale of goods: Rendering of services: Interest, royalties, anddividends:

23

ACCOUNTING POLICIES

a) Licenses, Registration Fees and Permit

▪ Revenue shall be recognised when licenses and permits are issued

(usually no gap between issuance of permit and license and timing of

payment)

b) Service and Services Fees

▪ Revenue shall be recognised by reference to the stage of completion of

the transaction at the reporting date when ALL of the following conditions

are satisfied:

i. The amount of revenue can be measured reliably

ii. It is probable that the economic benefits or service potential

associated with the transaction will flow to the entity

iii. The stage of completion of the transaction at the reporting date can

be measured reliably

iv. The cost incurred for the transaction and the costs to complete the

transaction can be measured reliably24

ACCOUNTING POLICIES… CONT’D

c) Sales of Goods

▪ Revenue shall be recognised when all the following conditions have been

satisfied:

i. The entity has transferred to the purchaser the significant risks and

rewards of ownership of the goods;

ii. The entity retains neither continuing managerial involvement to the degree

usually associated with ownership nor effective control over the goods

sold;

iii. The amount of revenue can be measured reliably;

iv. It is probable that the economic benefits or service potential associated

with the transaction will flow to the entity; and

v. The costs incurred or to be incurred in respect of the transaction can be

measured reliably.

▪ Revenue shall be measured at the fair value of the consideration received or

receivable

▪ The amount of the cost of goods sold must be expensed to the surplus/deficit

simultaneously with the recognition of revenue25

ACCOUNTING POLICIES… CONT’D

d) Rentals

▪ Rental earned shall be recognised as revenue on straight line basis

over the lease term

e) Interest

▪ Revenue shall be recognised on a time proportion basis that takes into

account the effective yield of the asset

▪ Revenue shall be measured at the fair value of the consideration

received or receivable

f) Dividend

▪ Revenue shall be recognised when the shareholder's or the entity's

right to receive payment is established

▪ Revenue shall be measured at the fair value of the consideration

received or receivable

26

ACCOUNTING POLICIES… CONT’D

g) Fines and Penalties

▪ Revenue shall be recognised when the fine/penalty is being imposed

▪ Revenue shall be measured at the fair value of the consideration

received or receivable, taking into consideration the expected timing of

settlement, where there is a separation between the event and

collection

h) Services In-kind

▪ An entity may, but is not required to, recognise services in-kind as

revenue and as an asset

27

28

MPSAS

12

29

MPSAS 12 : INVENTORIES

Inventories are required to be measured at the lower of cost and net realisable value1

▪ Costs include all purchase cost, conversion cost (materials, labour, and overhead),and other costs to bring inventory to its present location and condition, but notforeign exchange differences and selling costs

▪ Trade discounts, rebates, and other similar items are deducted in determining thecosts of purchase

However, inventories are required to be measured at the lower of cost and currentreplacement cost where they are held for:

1. Distribution at no charge or for a nominal charge2. Consumption in the production process of goods to be distributed at no charge or

for a nominal charge

Where inventories are acquired through a non exchange transaction, their cost shallbe measured as their fair value as at the date of acquisition

2

3

4

30

MPSAS 12 : INVENTORIES… CONT’D

5

For interchangeable items, cost isdetermined on either a first-in, first-out or weighted-average basis. Last-in, first-out is not permitted

▪ Write-downs to net realisablevalue are recognised as an expensein the period the loss or the write-down occurs

▪ Reversals arising from an increasein net realisable value arerecognised as a reduction of theinventory expense in the period inwhich they occur

▪ When inventories are sold,exchanged, or distributed, thecarrying amount shall berecognised as an expense in theperiod in which the relatedrevenue is recognised

▪ If there is no related revenue, theexpense is recognised when thegoods are distributed or relatedservices have been rendered

For inventory items that are notinterchangeable, specific costs areattributed to the specific individualitems of inventory

For inventories with a differentnature or use, different costformulas may be justified

6

7

10

9

An entity shall apply the same costformula for all inventories havingsimilar nature and use to the entity; adifference in geographical location ofinventories by itself is not sufficientto justify the use of different costformulas

8

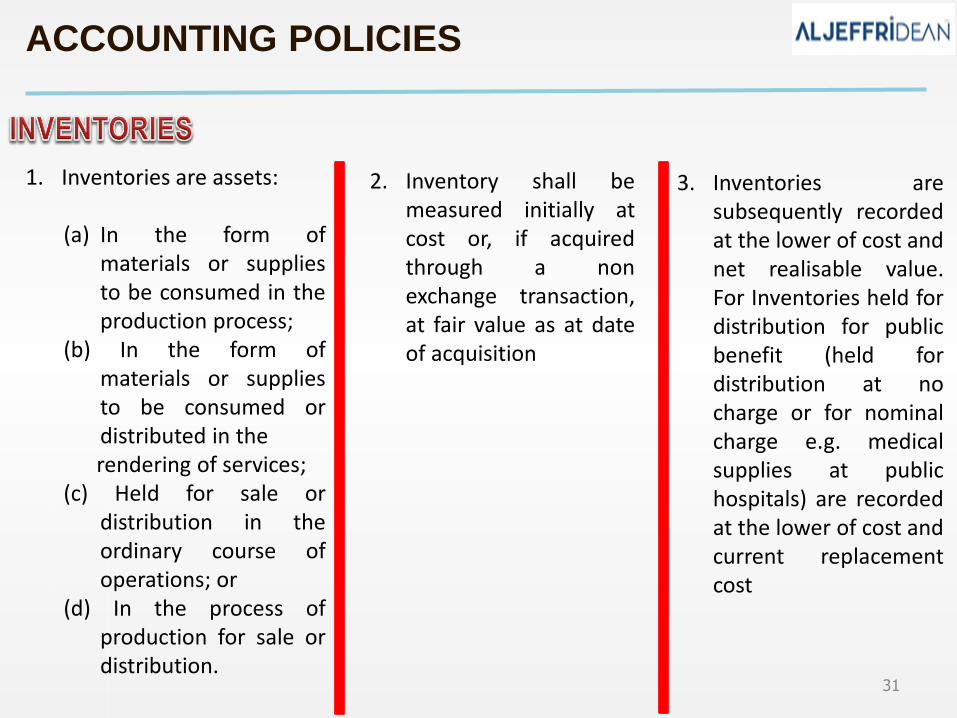

ACCOUNTING POLICIES

1. Inventories are assets:

(a) In the form ofmaterials or suppliesto be consumed in theproduction process;

(b) In the form ofmaterials or suppliesto be consumed ordistributed in therendering of services;

(c) Held for sale ordistribution in theordinary course ofoperations; or

(d) In the process ofproduction for sale ordistribution.

2. Inventory shall bemeasured initially atcost or, if acquiredthrough a nonexchange transaction,at fair value as at dateof acquisition

3. Inventories aresubsequently recordedat the lower of cost andnet realisable value.For Inventories held fordistribution for publicbenefit (held fordistribution at nocharge or for nominalcharge e.g. medicalsupplies at publichospitals) are recordedat the lower of cost andcurrent replacementcost

31

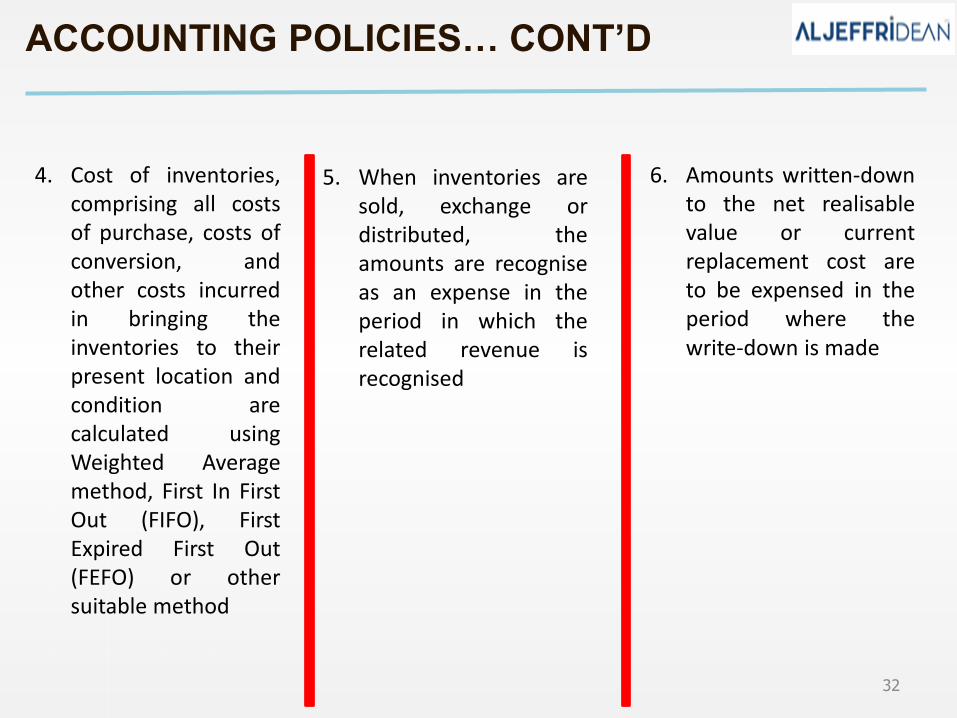

ACCOUNTING POLICIES… CONT’D

4. Cost of inventories,comprising all costsof purchase, costs ofconversion, andother costs incurredin bringing theinventories to theirpresent location andcondition arecalculated usingWeighted Averagemethod, First In FirstOut (FIFO), FirstExpired First Out(FEFO) or othersuitable method

5. When inventories aresold, exchange ordistributed, theamounts are recogniseas an expense in theperiod in which therelated revenue isrecognised

6. Amounts written-downto the net realisablevalue or currentreplacement cost areto be expensed in theperiod where thewrite-down is made

32

33

Subsequent Measurement

Lower of cost and net realisable value (NRV). However the NRV for inventories at

no charge or nominal charge are determined by reference to the current

replacement cost

Discussion on the Accounting Treatment

EXAMPLE :

33

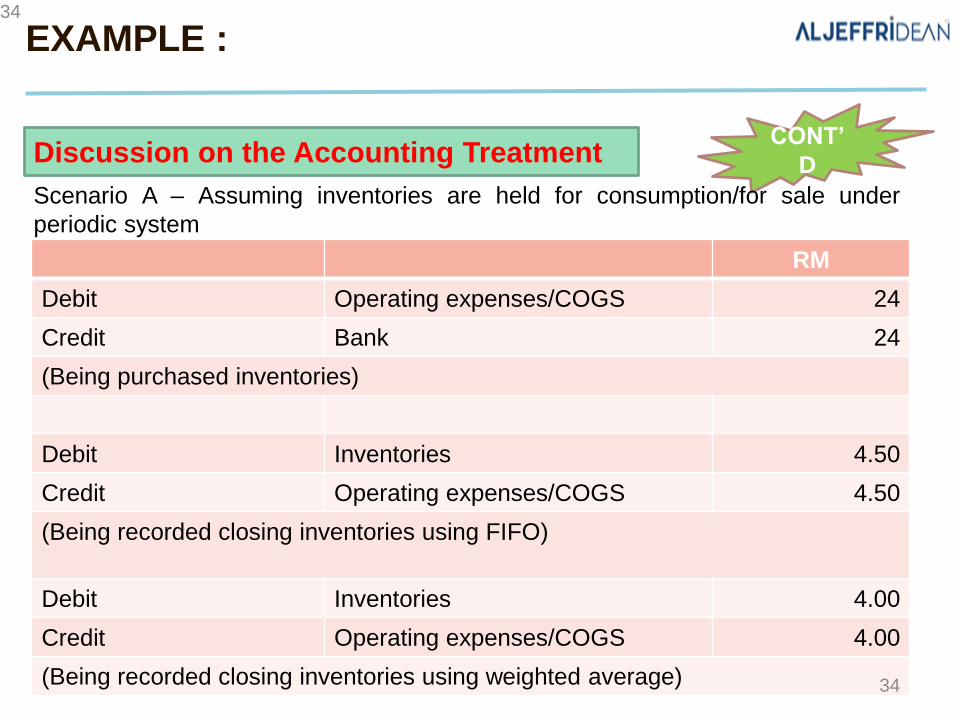

34

Discussion on the Accounting TreatmentCONT’

D

Scenario A – Assuming inventories are held for consumption/for sale under

periodic system

RM

Debit Operating expenses/COGS 24

Credit Bank 24

(Being purchased inventories)

Debit Inventories 4.50

Credit Operating expenses/COGS 4.50

(Being recorded closing inventories using FIFO)

Debit Inventories 4.00

Credit Operating expenses/COGS 4.00

(Being recorded closing inventories using weighted average)

EXAMPLE :

34

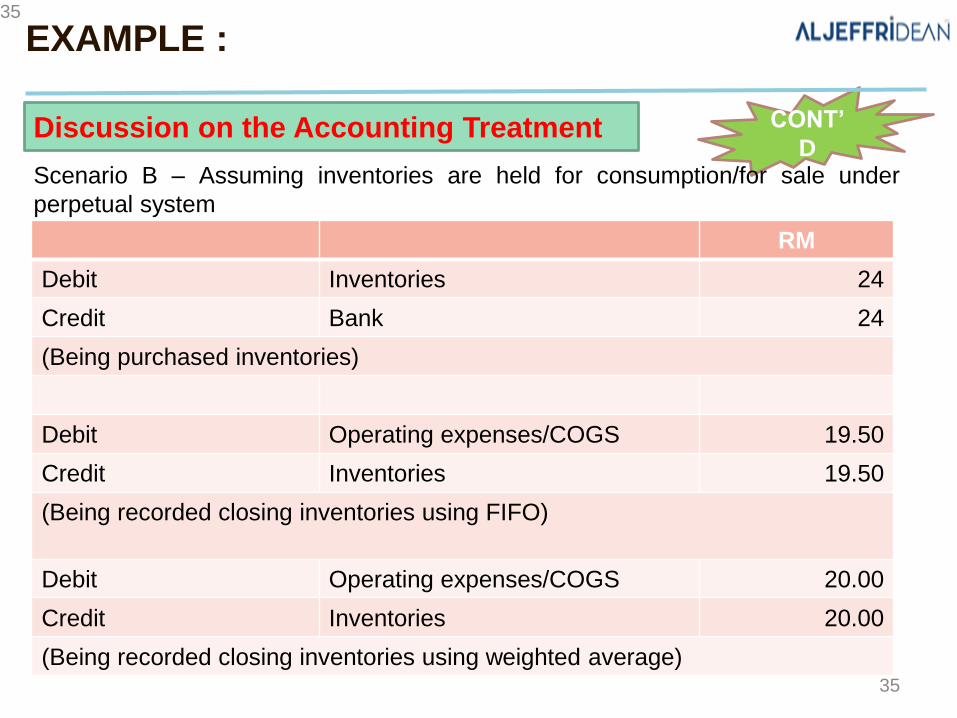

35

Discussion on the Accounting Treatment CONT’

DScenario B – Assuming inventories are held for consumption/for sale under

perpetual system

RM

Debit Inventories 24

Credit Bank 24

(Being purchased inventories)

Debit Operating expenses/COGS 19.50

Credit Inventories 19.50

(Being recorded closing inventories using FIFO)

Debit Operating expenses/COGS 20.00

Credit Inventories 20.00

(Being recorded closing inventories using weighted average)

EXAMPLE :

35

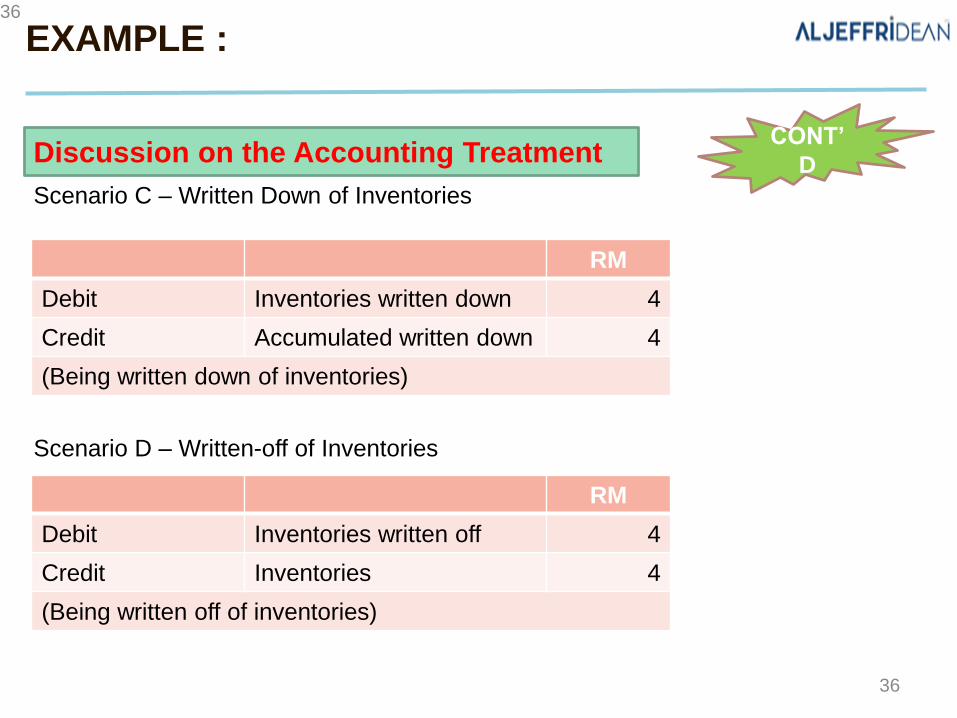

36

Discussion on the Accounting TreatmentCONT’

D

Scenario C – Written Down of Inventories

RM

Debit Inventories written down 4

Credit Accumulated written down 4

(Being written down of inventories)

Scenario D – Written-off of Inventories

RM

Debit Inventories written off 4

Credit Inventories 4

(Being written off of inventories)

EXAMPLE :

36

37

MPSAS

16

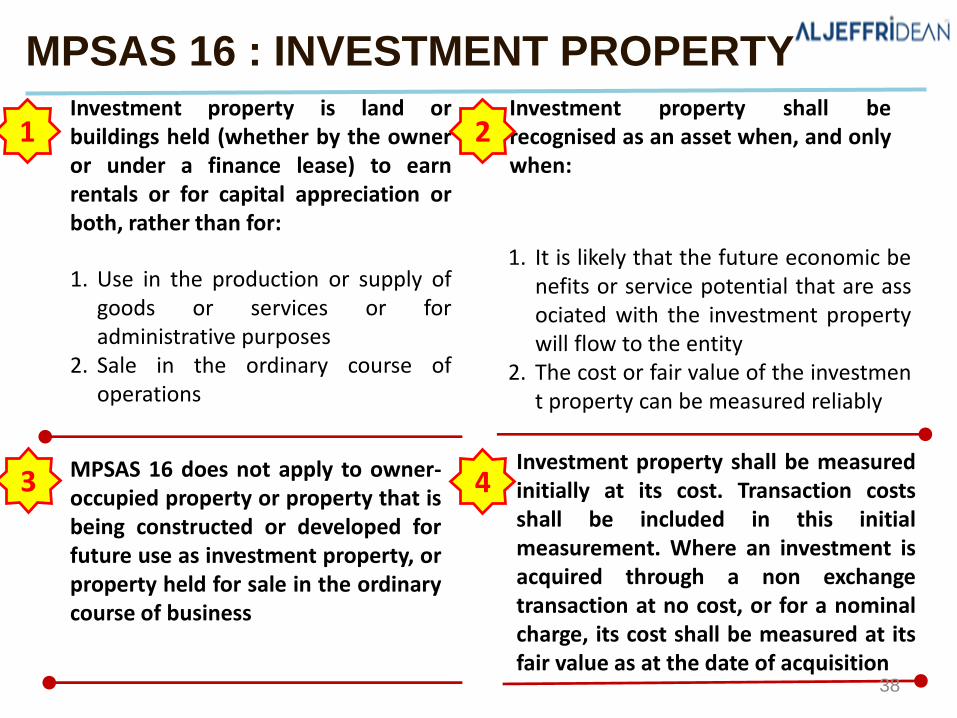

1. Use in the production or supply ofgoods or services or foradministrative purposes

2. Sale in the ordinary course ofoperations

Investment property is land orbuildings held (whether by the owneror under a finance lease) to earnrentals or for capital appreciation orboth, rather than for:

Investment property shall be measuredinitially at its cost. Transaction costsshall be included in this initialmeasurement. Where an investment isacquired through a non exchangetransaction at no cost, or for a nominalcharge, its cost shall be measured at itsfair value as at the date of acquisition

MPSAS 16 does not apply to owner-occupied property or property that isbeing constructed or developed forfuture use as investment property, orproperty held for sale in the ordinarycourse of business

1. It is likely that the future economic benefits or service potential that are associated with the investment propertywill flow to the entity

2. The cost or fair value of the investment property can be measured reliably

Investment property shall berecognised as an asset when, and onlywhen:

MPSAS 16 : INVESTMENT PROPERTY

1 2

3 4

38

MPSAS 16 : INVESTMENT PROPERTY… CONT’D

The chosen measurement model shall be applied to all of the entity’sinvestment property

1. Fair value model:▪ Investment property is measured at fair value, and changes in fair value arerecognised in surplus or deficit for the period in which it arises

2. Cost model:▪ Investment property is measured at depreciated cost, less any accumulatedimpairment losses▪ Fair value of the investment property shall still be disclosed

After recognition, an entity shall choose as its accounting policy either the fairvalue model or cost model:5

6

39

MPSAS 16 : INVESTMENT PROPERTY… CONT’D

If an entity uses the fair value model but, when a particular property is acquired,there is clear evidence that the entity will not be able to determine fair value on acontinuing basis, the cost model is used for that property — and it shall continue tobe used until disposal of the property

➢A property interest held by a lessee under an operating lease can qualify asinvestment property provided that the lessee uses the fair value model ofMPSAS 16

➢ In this case, the lessee accounts for the lease as if it were a finance lease

Change from one model to the other shall be made only if the change will result ina more appropriate presentation (highly unlikely for change from fair value to costmodel)

➢ In that case, the residual value of the investment property shall be assumed tobe zero

7

8

40

ACCOUNTING POLICIES

Investment Properties (IP) shall be initially recognised as an asset at

cost when and only when:

i. it is probable that future economic benefits or service potential

associated with the investment property will flow to the entity; and

ii. the cost or fair value of the item can be measured reliably

Where an IP is acquired through a non-exchange transaction, its cost

shall be measured at its fair value as at the date of acquisition

41

ACCOUNTING POLICIES… CONT’D

IP shall be subsequently measured using Fair Value Model or Cost model:

i. Fair Value Model• Measure at fair value unless the fair value is not reliably determinable on a

continuous basis• Gain or loss arising from the change in the fair value is recognised in the surplus

or deficit for the period in which it arises• A property interest held by lessee under an operating lease may be classified

and accounted for as IP if it meets the definition of IP and the use of fair valuemodel is mandatory

ii. Cost ModelMeasure at cost less accumulated depreciation and accumulated impairmentlosses. Depreciation is charged on a straight-line basis at rates calculated toallocate the cost or valuation of an item of IP value measured at cost less anyestimated residual value, over its remaining useful life

For freehold land, it is not necessary to depreciate but for leasehold land, it shallbe amortised over the lease period. The depreciation charge for the period isrecognised in surplus or deficit 42

ACCOUNTING POLICIES… CONT’D

Disposal

Impairment

❖ Where an asset’s recoverable amount is less than its carrying amount, it is reported at itsrecoverable amount and an impairment loss is recognised. The main reason for holding someassets is to generate cash

❖ For these assets the recoverable amount is the higher of the amount that could be recoveredby sale (after deducting the costs of sale) or the amount that will be generated by using theasset through its useful life

❖ Some assets do not generate cash and for those assets, if the recoverable service amount isless than its carrying amount, the assets shall be reported at its recoverable service amount

❖ Losses resulting from impairment are reported in the statement of financial performance,unless the asset is carried at a revalued amount in which case any impairment loss is treatedas a revaluation decrease

❖ Gains or losses arising from disposal of IP are recognised in the statement of financialperformance in the period in which the transaction occurs

43

44

MPSAS

17

1

2

3

4

Items of property, plant and equipment shall be recognised as assets if, andonly if, it is probable that the future economic benefits or service potentialassociated with the item will flow to the entity, and the cost or fair value ofthe item can be measured reliably

MPSAS 17 does not require or prohibit the recognition of heritage assets. Anentity which recognises heritage assets is required to comply with thedisclosure requirements of MPSAS 17 with respect to those heritage assetsthat have been recognised and may, but is not required to, comply with otherrequirements of MPSAS 17 in respect of those heritage assets

Infrastructure assets, such as road networks, sewer systems, andcommunication networks, shall be accounted for in accordance with thisMPSAS

Initial recognition at cost, which includes all costs necessary to get the assetready for its intended use. Where an asset is acquired at no cost, or for anominal cost, its cost is its fair value as at the date of acquisition. If payment isdeferred, interest shall be recognised

MPSAS 17 : PROPERTY, PLANT AND EQUIPMENT

45

5

1. Cost model: The asset is carried at cost, less accumulated depreciation andimpairment losses

2. Revaluation model: The asset is carried at revalued amount, which is fairvalue at revaluation date, less subsequent depreciation and impairmentlosses

Subsequent to acquisition, MPSAS 17 allows a choice of accounting model foran entire class of property, plant and equipment:

6 o Under the revaluation model, revaluations shall be carried out regularly. Allitems of a given class shall be revalued

o Revaluation increases shall be credited directly to revaluation surplus.Increase shall be recognised as revenue in surplus or deficit to the extentthat it reverses a revaluation decrease of the same class of assets previouslyrecognised as an expense in surplus or deficit

o Revaluation decreases are debited first against the revaluation surplusrelated to the same class of assets and any excess against surplus or deficit

o When the revalued asset is disposed of, the revaluation surplus istransferred directly to accumulated surpluses or deficit

MPSAS 17 : PROPERTY, PLANT AND

EQUIPMENT… CONT’D

46

7 Revaluation increases and decreases related to individual assets within aclass of property, plant and equipment must be offset against oneanother within that class but must not be offset in respect of assets indifferent classes

88

Each part of an item of property, plant and equipment with a cost that issignificant in relation to the total cost of the item shall be depreciatedseparately

• Depreciation is charged systematically over the asset’s useful life• The residual value must be reviewed at least annually and shall equal

the amount the entity would receive currently if the asset werealready of the age and condition expected at the end of its useful life

• If operation of an item of property, plant and equipment (forexample, an aircraft) requires regular major inspections, when eachmajor inspection is performed, its cost is recognised in the carryingamount of the asset as a replacement, if the recognition criteria aresatisfied

• If expectations differ from previous estimates, the change must beaccounted for as a change in an accounting estimate in accordancewith MPSAS 3

9

MPSAS 17 : PROPERTY, PLANT AND

EQUIPMENT… CONT’D

47

10 • Land and buildings are separable assets and are accounted forseparately, even when they are acquired together

• Land normally has an unlimited useful life, and therefore is notdepreciated

11 To determine whether an item of property, plant and equipment isimpaired, an entity applies MPSAS 21 or MPSAS 26, as appropriate

All exchanges of property, plant and equipment shall be measured at fairvalue, including exchanges of similar items, unless the exchange transactionlacks commercial substance or the fair value of neither the asset receivednor the asset given up is reliably measurable

12

The carrying amount of an item of property, plant and equipment must bederecognised:1. On disposal; or2. When no future economic benefits or service potential is expected from

its use or disposal

13

MPSAS 17 : PROPERTY, PLANT AND

EQUIPMENT… CONT’D

48

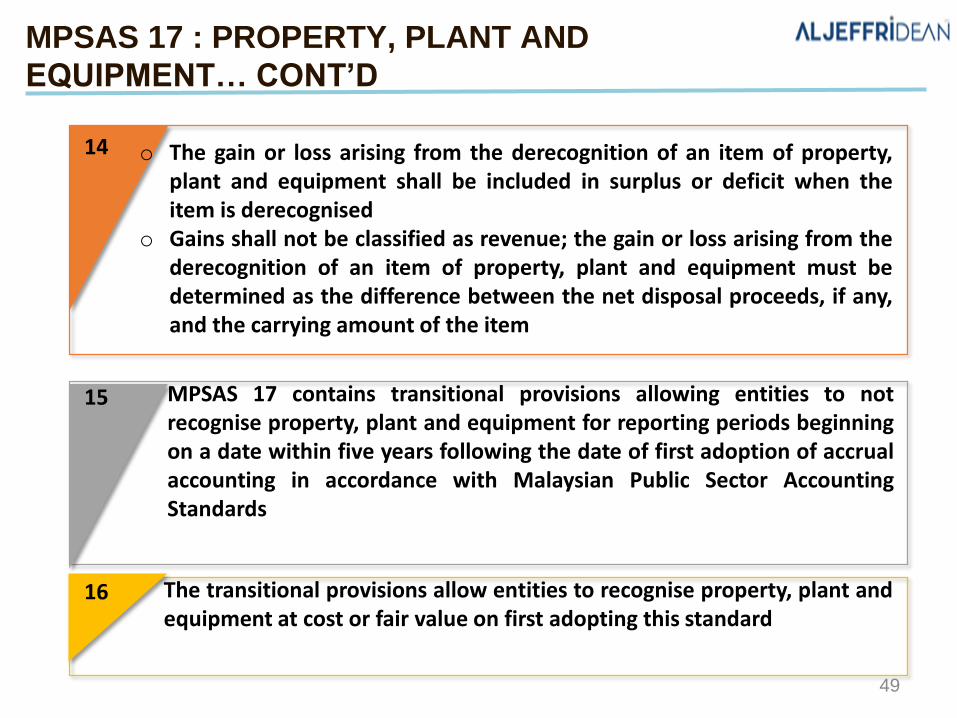

14

15

16

o The gain or loss arising from the derecognition of an item of property,plant and equipment shall be included in surplus or deficit when theitem is derecognised

o Gains shall not be classified as revenue; the gain or loss arising from thederecognition of an item of property, plant and equipment must bedetermined as the difference between the net disposal proceeds, if any,and the carrying amount of the item

MPSAS 17 contains transitional provisions allowing entities to notrecognise property, plant and equipment for reporting periods beginningon a date within five years following the date of first adoption of accrualaccounting in accordance with Malaysian Public Sector AccountingStandards

The transitional provisions allow entities to recognise property, plant andequipment at cost or fair value on first adopting this standard

MPSAS 17 : PROPERTY, PLANT AND

EQUIPMENT… CONT’D

49

ACCOUNTING POLICIES

▪ Property, plant, and

equipment are tangible

items that:

i. Are held for use in the

production or supply of

goods or services, for

rental to others, or for

administrative purposes;

and

ii. Are expected to be used

during more than one

reporting period

▪ PPE shall be initially

recognised as an asset at

cost if, and only if:

i. It is probable that future

economic benefits or service

potential associated with

the item will flow to the entity;

and

ii. The cost or fair value of the

item can be measured

reliably

50

ACCOUNTING POLICIES… CONT’D

▪ Asset acquired through a non-exchange transaction shall be measuredat its fair value at date of acquisition

▪ Proposed capitalisation threshold for PPE is RM2,000 per item subjectto review from time to time

▪ Asset below RM2,000 or low value assets shall be expensed off butrecorded in the assets register for record and control purpose

▪ Replacement cost for part of an asset that increases the economicbenefits, service potential and life span of an asset shall be is capitalisedwith a corresponding derecognition of the parts that are replaced

▪ Repair and maintenance expenses shall not be capitalised

51

ACCOUNTING POLICIES… CONT’D

▪ Subsequently, PPE shall be measured using Cost model or Revaluation model:

i. Cost Model• Carried at cost, less accumulated depreciation and any accumulatedimpairment losses• Depreciation is charged on a straight-line basis at rates calculated toallocate the cost or valuation of an item of PPE over its remaining usefullife• For freehold land, it is not necessary to depreciate but for leaseholdland, it shall be amortised over the lease period. The depreciation chargefor the period is recognised in surplus or deficit

ii. Revaluation Model• Carried at revalued amount, being the fair value at the date of the

revaluation, less any subsequent accumulated depreciation andsubsequent accumulated impairment losses

• Revaluation is to be credited directly to revaluation surplus orexpensed in surplus or deficit

52

ACCOUNTING POLICIES… CONT’D

Disposal

Impairment

❖ Where an asset’s recoverable amount is less than its carrying amount, it is reported at itsrecoverable amount and an impairment loss is recognised. The main reason for holding someassets is to generate cash

❖ For these assets the recoverable amount is the higher of the amount that could be recoveredby sale (after deducting the costs of sale) or the amount that will be generated by using theasset through its useful life

❖ Some assets do not generate cash and for those assets, if the recoverable service amount isless than its carrying amount, the assets shall be reported at its recoverable service amount

❖ Losses resulting from impairment are reported in the statement of financial performance,unless the asset is carried at a revalued amount in which case any impairment loss is treatedas a revaluation decrease

❖ Gains or losses arising from disposal of PPE are recognised in the statement of financialperformance in the period in which the transaction occurs

❖ Any balance attributable to the disposed asset in the asset revaluation reserve is transferredto accumulated surpluses or deficits

53

54

MPSAS

19

MPSAS 19 : PROVISIONS, CONTINGENT

LIABILITIES AND CONTINGENT ASSETS

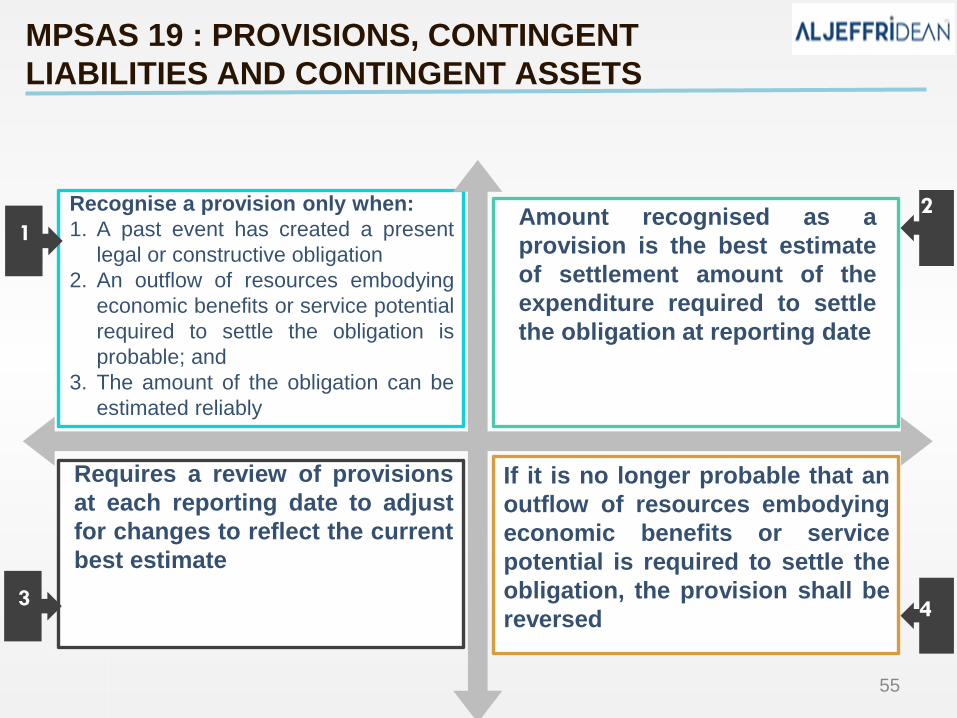

Recognise a provision only when:

1. A past event has created a present

legal or constructive obligation

2. An outflow of resources embodying

economic benefits or service potential

required to settle the obligation is

probable; and

3. The amount of the obligation can be

estimated reliably

Amount recognised as a

provision is the best estimate

of settlement amount of the

expenditure required to settle

the obligation at reporting date

If it is no longer probable that an

outflow of resources embodying

economic benefits or service

potential is required to settle the

obligation, the provision shall be

reversed

Requires a review of provisions

at each reporting date to adjust

for changes to reflect the current

best estimate

1

3

2

4

55

MPSAS 19 : PROVISIONS, CONTINGENT

LIABILITIES AND CONTINGENT ASSETS… CONT’D

Utilise provisions only for thepurposes for which they wereoriginally intended

1.Onerous contracts2.Restructuring provisions3.Warranties4.Refunds5.Site restoration

Examples of provisions may include:

1.Necessarily entailed by therestructuring

2.Not associated with theongoing activities of the entity

A restructuring provision shallinclude only the directexpenditures arising from therestructuring, which are thosethat are both:

1.There is a possible obligation to be confirmedby a future event that is outside the control ofthe entity

2.A present obligation may, but probably willnot, require an outflow of resourcesembodying economic benefits or servicepotential

3.A sufficiently reliable estimate of the amountof a present obligation cannot be made

Contingent liability arises when:7

5

6

8

56

MPSAS 19 : PROVISIONS, CONTINGENT

LIABILITIES AND CONTINGENT ASSETS… CONT’D

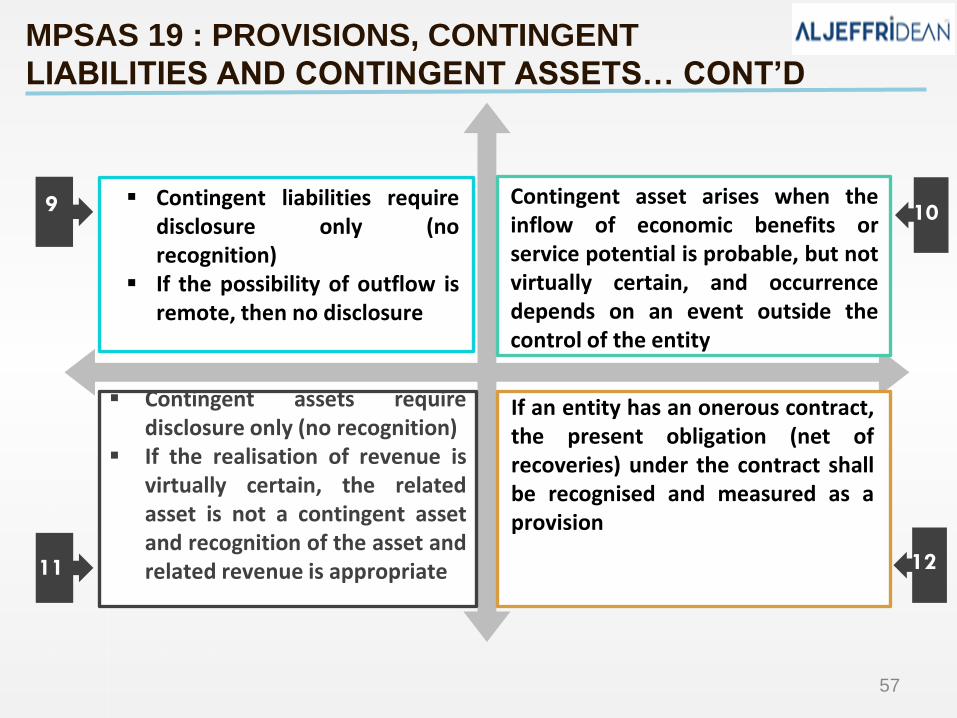

▪ Contingent assets requiredisclosure only (no recognition)

▪ If the realisation of revenue isvirtually certain, the relatedasset is not a contingent assetand recognition of the asset andrelated revenue is appropriate

▪ Contingent liabilities requiredisclosure only (norecognition)

▪ If the possibility of outflow isremote, then no disclosure

Contingent asset arises when theinflow of economic benefits orservice potential is probable, but notvirtually certain, and occurrencedepends on an event outside thecontrol of the entity

If an entity has an onerous contract,the present obligation (net ofrecoveries) under the contract shallbe recognised and measured as aprovision

11

9 10

12

57

ACCOUNTING POLICIES

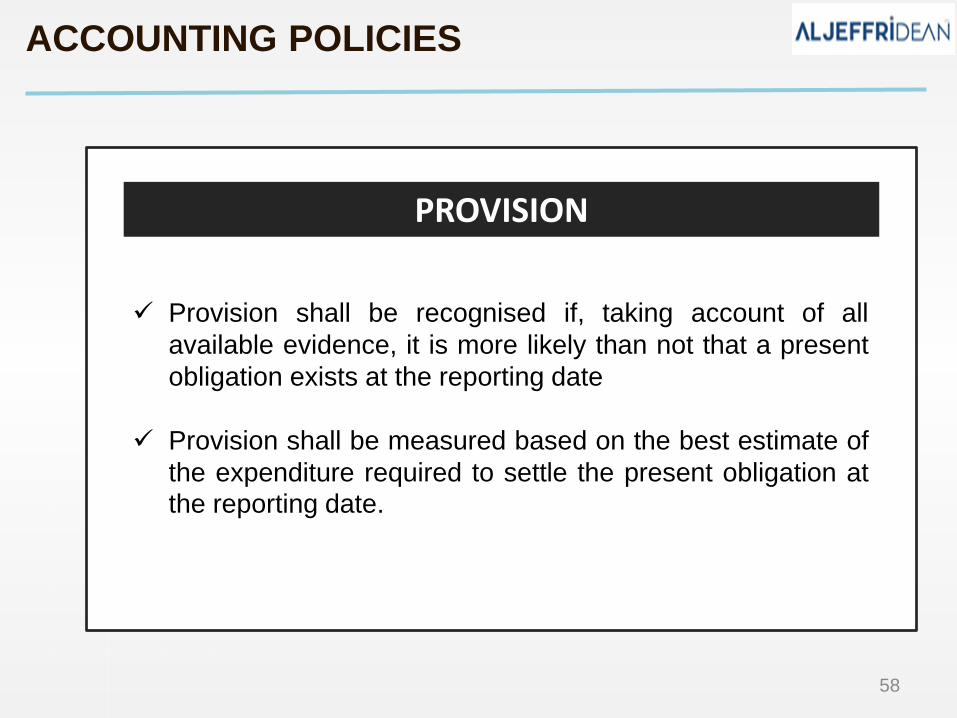

PROVISION

✓ Provision shall be recognised if, taking account of all

available evidence, it is more likely than not that a present

obligation exists at the reporting date

✓ Provision shall be measured based on the best estimate of

the expenditure required to settle the present obligation at

the reporting date.

58

The expected value of a provision at the end of year 5 is RM2,000. This expected

value has not been risk-adjusted. An appropriate discount rate that takes account

of the risk associated with this cash flow has been estimated at 12%.

Calculations: Increase of Provisions

Current time: Present value = 2000/(1.12)5 = 1,134.85

End of Year 1: Present value = 2000/(1.12)4 = 1,271.04 136.18

End of Year 2: Present value = 2000/(1.12)3 = 1,423.56 152.52

End of Year 3: Present value = 2000/(1.12)2 = 1,594.39 170.83

End of Year 4: Present value = 2000/(1.12)1 = 1,785.71 191.33

End of Year 5: Present value = 2000/(1.12)0 = 2,000.00 214.29

EXAMPLE :

59

60

ExampleCONT’D

EXAMPLE :

60

61

MPSAS

23

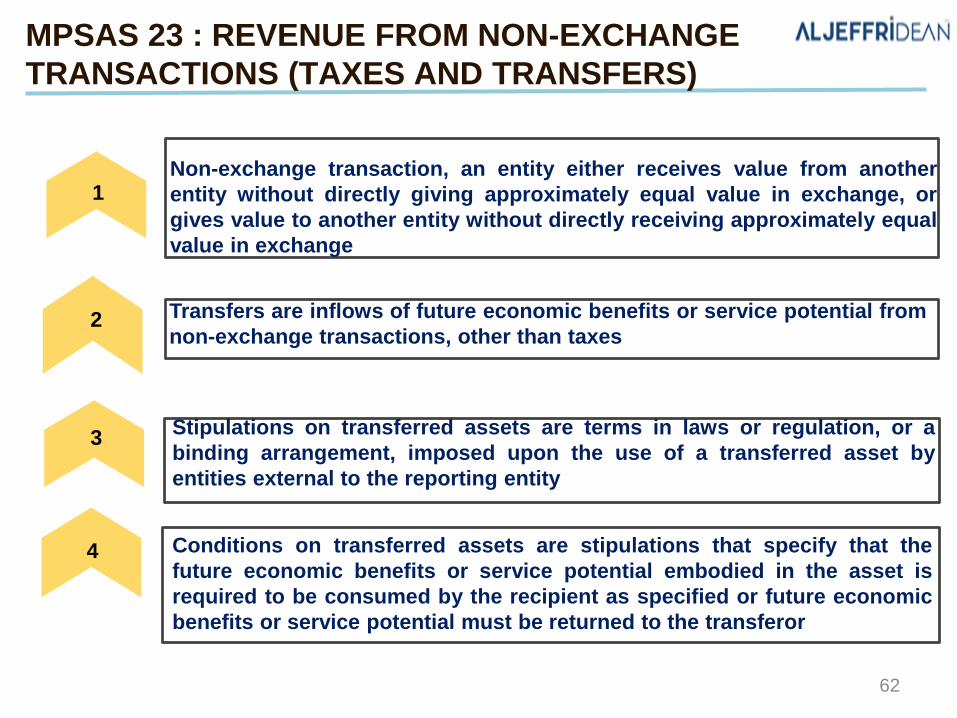

1Non-exchange transaction, an entity either receives value from another

entity without directly giving approximately equal value in exchange, or

gives value to another entity without directly receiving approximately equal

value in exchange

2 Transfers are inflows of future economic benefits or service potential from

non-exchange transactions, other than taxes

3Stipulations on transferred assets are terms in laws or regulation, or a

binding arrangement, imposed upon the use of a transferred asset by

entities external to the reporting entity

4 Conditions on transferred assets are stipulations that specify that the

future economic benefits or service potential embodied in the asset is

required to be consumed by the recipient as specified or future economic

benefits or service potential must be returned to the transferor

MPSAS 23 : REVENUE FROM NON-EXCHANGE

TRANSACTIONS (TAXES AND TRANSFERS)

62

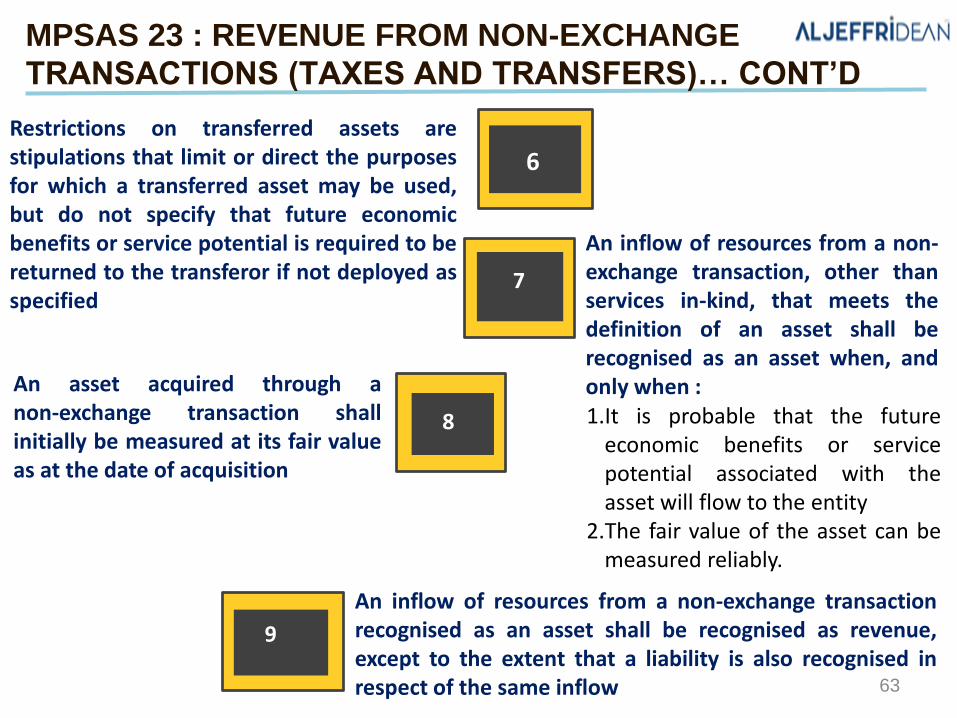

An inflow of resources from a non-exchange transactionrecognised as an asset shall be recognised as revenue,except to the extent that a liability is also recognised inrespect of the same inflow

An asset acquired through anon-exchange transaction shallinitially be measured at its fair valueas at the date of acquisition

1.It is probable that the futureeconomic benefits or servicepotential associated with theasset will flow to the entity

2.The fair value of the asset can bemeasured reliably.

An inflow of resources from a non-exchange transaction, other thanservices in-kind, that meets thedefinition of an asset shall berecognised as an asset when, andonly when :

Restrictions on transferred assets arestipulations that limit or direct the purposesfor which a transferred asset may be used,but do not specify that future economicbenefits or service potential is required to bereturned to the transferor if not deployed asspecified

7

8

9

6

MPSAS 23 : REVENUE FROM NON-EXCHANGE

TRANSACTIONS (TAXES AND TRANSFERS)… CONT’D

63

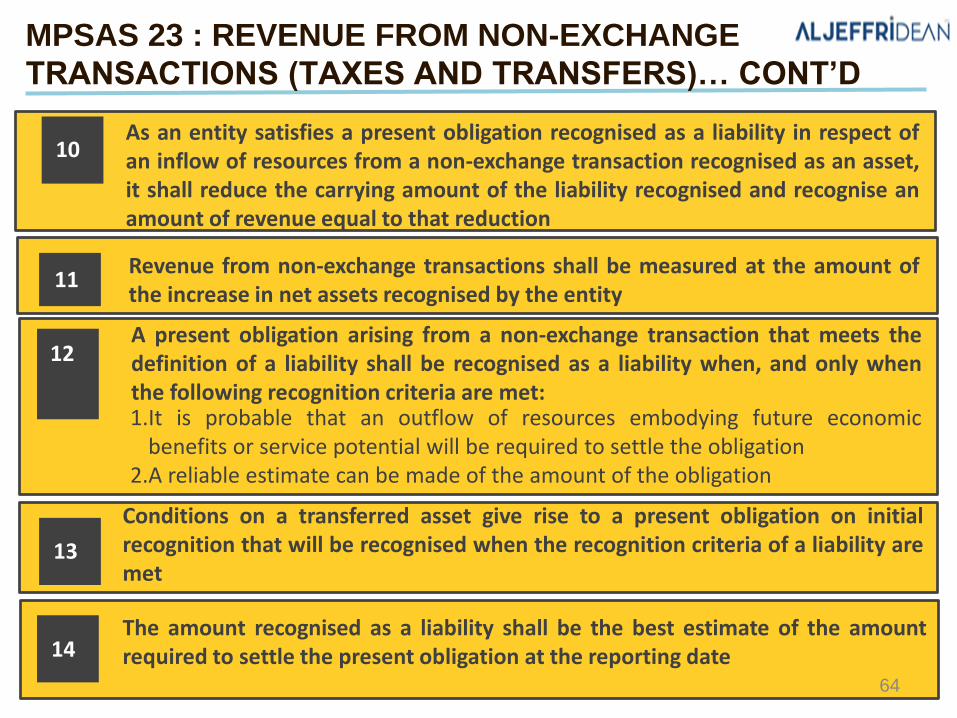

As an entity satisfies a present obligation recognised as a liability in respect ofan inflow of resources from a non-exchange transaction recognised as an asset,it shall reduce the carrying amount of the liability recognised and recognise anamount of revenue equal to that reduction

10

Revenue from non-exchange transactions shall be measured at the amount ofthe increase in net assets recognised by the entity

1.It is probable that an outflow of resources embodying future economicbenefits or service potential will be required to settle the obligation

2.A reliable estimate can be made of the amount of the obligation

A present obligation arising from a non-exchange transaction that meets thedefinition of a liability shall be recognised as a liability when, and only whenthe following recognition criteria are met:

Conditions on a transferred asset give rise to a present obligation on initialrecognition that will be recognised when the recognition criteria of a liability aremet

The amount recognised as a liability shall be the best estimate of the amountrequired to settle the present obligation at the reporting date

11

12

14

13

MPSAS 23 : REVENUE FROM NON-EXCHANGE

TRANSACTIONS (TAXES AND TRANSFERS)… CONT’D

64

o An entity shall recognise an asset in respect of taxes when the taxableevent occurs and the asset recognition criteria are met

15

o Taxation revenue shall be determined at a gross amount. It shall not bereduced for expenses paid through the tax system

o Taxation revenue shall not be grossed up for the amount of taxexpenditures

o An entity recognises an asset in respect of transfers when thetransferred resources meet the definition of an asset and satisfy thecriteria for recognition as an asset

o However, an entity may, but is not required to, recognise services in-kindas revenue and as an asset

16

17

18

MPSAS 23 : REVENUE FROM NON-EXCHANGE

TRANSACTIONS (TAXES AND TRANSFERS)… CONT’D

65

1.The amount of revenue from non-exchange transactions recognisedduring the period by major classesshowing separately taxes and transfers

2.The amount of receivables recognisedin respect of non-exchange revenue

3.The amount of liabilities recognised inrespect of transferred assets subject toconditions

4.The amount of assets recognised thatare subject to restrictions and thenature of those restrictions

5.The existence and amounts of anyadvance receipts in respect of non-exchange transactions

6.The amount of any liabilities forgiven

1. The accounting policies adopted forthe recognition of revenue from non-exchange transactions

2. For major classes of revenue fromnon-exchange transactions, the basison which the fair value of inflowingresources was measured

3. For major classes of taxation revenuewhich the entity cannot measurereliably during the period in which thetaxable event occurs, informationabout the nature of the tax

4. The nature and type of major classesof bequests, gifts, donations showingseparately major classes of goods in-kind received

19 20An entity shall disclose either onthe face of, or in the notes to, thegeneral-purpose financialstatements:

An entity shall disclose in thenotes to the general-purposefinancial statements:

MPSAS 23 : REVENUE FROM NON-EXCHANGE

TRANSACTIONS (TAXES AND TRANSFERS)… CONT’D

66

ACCOUNTING POLICIES

Transfer Recognized as revenue

Fines when the receivable meets the definition of an asset and satisfies the

criteria for recognition as an asset

Gifts and When it is probable that the future economic benefits or service potential

donations will flow to the entity and the fair value of the assets can be measured

reliably.

Services in-kind An entity may, but is not required to, recognize services in-kind as revenue

and as an asset.

Concessionary Where an entity determines that the difference between the transaction

loans price (loan proceeds) and the fair value of the loan on initial recognition is

non-exchange revenue, an entity recognizes the difference as revenue,

Public service Where service is rendered

Licenses & Point of licenses and permits issued

registration67

Example 1:The government (transferor) makes a grant of RM 10 million to a local

government in a socioeconomically deprived area. The local

government (reporting entity) is required under its constitution to

undertake various social programs; however, it has insufficient

resources to undertake all of these programs without assistance. There

are no stipulations attached to the grant and no performance obligation,

so the transfers are recognised as assets and revenue in the general

purpose financial statements of the reporting period in which they are

received or receivable by the local government

EXAMPLE : TREATMENT OF GRANT

68

Example 2:The government (transferor) grants RM 10 million to a provincial government

(reporting entity) to be used to improve and maintain mass transit systems.

Specifically, the money is required to be used as follows: 40 percent for

existing railroad and tramway system modernization, 40 percent for new

railroad or tramway systems, and 20 percent for rolling stock purchases and

improvements. The agreement requires the grant to be spent as specified in

the current year or be returned to the national government

The provincial government recognises the grant money as an asset. The

provincial government also recognises a liability in respect of the condition

attached to the grant. As the province satisfies the condition, that is, as it

makes authorized expenditures, it reduces the liability and recognises

revenue in the statement of financial performance of the reporting period in

which the liability is discharged

EXAMPLE : TREATMENT OF GRANT… CONT’D

69

SESI Q & A

SEKIAN, TERIMA KASIH

70