Download - Scale Does Matter - gazprom.ru

0 Investor Day 2012

Gazprom Investor Day

Scale Does Matter

February 2012

1

Investor Day 2012 1

Disclaimer

This presentation has been prepared by OJSC Gazprom (the “Company”), and comprises the slides for a presentation to investors concerning the Company.

This presentation does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any

shares or other securities representing shares in the Company, nor shall it or any part of it nor the fact of its presentation or distribution form the basis of, or be

relied on in connection with, any contract or investment decision.

No reliance may be placed for any purposes whatsoever on the information contained in this presentation, or any other material discussed at any presentation

or on its completeness, accuracy or fairness. The information in this presentation should not be treated as giving investment advice. Care has been taken to

ensure that the facts stated in this presentation are accurate, and that the opinions expressed are fair and reasonable. However, the contents of this

presentation have not been verified by the Company. Accordingly, no representation or warranty, express or implied, is made or given by or on behalf of the

Company or any of its members, directors, officers or employees or any other person as to the accuracy, completeness or fairness of the information or

opinions contained in or discussed at this presentation. None of the Company or any of their respective members, directors, officers or employees nor any

other person accepts any liability whatsoever for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection

therewith.

The information in this presentation includes forward-looking statements. These forward-looking statements include all matters that are not historical facts,

statements regarding the Company’s intentions, beliefs or current expectations concerning, among other things, the Company’s results of operations, financial

condition, liquidity, prospects, growth, strategies, and the industry in which the Company operates. By their nature, forward-looking statements involve risks

and uncertainties, including, without limitation, the risks and uncertainties to be set forth in the prospectus, because they relate to events and depend on

circumstances that may or may not occur in the future. The Company cautions you that forward looking statements are not guarantees of future performance

and that its actual results of operations, financial condition and liquidity and the development of the industry in which the Company operates may differ

materially from those made in or suggested by the forward-looking statements contained in this presentation. In addition, even if the Company’s results of

operations, financial condition and liquidity and the development of the industry in which the Company operates are consistent with the forward-looking

statements contained in this presentation, those results or developments may not be indicative of results or developments in future periods.

The information and opinions contained in this presentation are provided as at the date of this presentation and are subject to change without notice. No

person is under any obligation to update or keep current the information contained herein.

By attending the presentation you agree to be bound by the foregoing limitations.

Investor Day 2012

2

Agenda

Export Alexander Medvedev

Deputy Chairman of Gazprom Management Committee

Director General of Gazprom Export

Strategy

Finance

Vlada Rusakova

Member of Gazprom Management Committee

Andrey Kruglov

Deputy Chairman of Gazprom Management Committee

Head of the Department for Finance and Economics

Gazprom Neft

Gazprom Energoholding

Denis Fedorov

Head of Gazprom Directorate for Development of Power Generation Sector

and Power Generation Marketing, General Director of Gazprom

Energoholding

Vadim Yakovlev

Deputy Chairman of the Management Board of Gazprom Neft

First Deputy CEO of Gazprom Neft

2 Investor Day 2012

3

Investor Day 2012

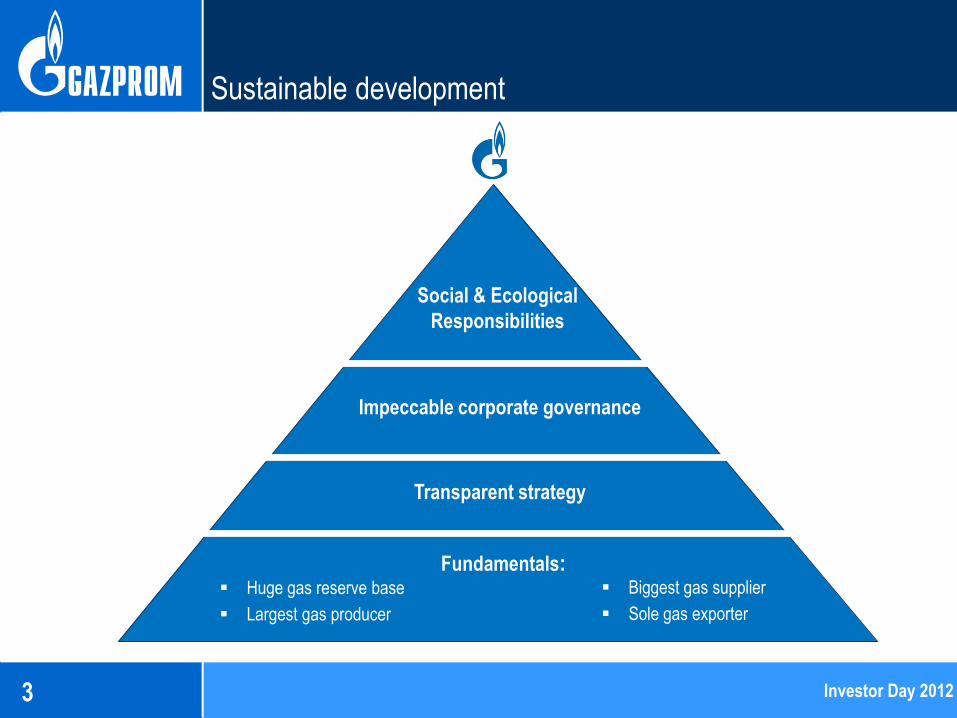

Sustainable development

Investor Day 2012

Fundamentals: Huge gas reserve base

Largest gas producer

Biggest gas supplier

Sole gas exporter

Transparent strategy

Impeccable corporate governance

Social & Ecological

Responsibilities

4

Strategy

Part 1. Vlada Rusakova

Member of Gazprom Management Committee

Investor Day 2012

5

Investor Day 2012

Gas demand 2030

Share of gas in World energy consumption

2009

2030F

21%

26%

– Natural Gas

– Other

Gas consumption by region(1)

– Asia/Oceania

– Latin America

– Europe(2)

– FSU(3)

– Africa

– Middle East

– North America

5.1 tcm

2010 2030F

3.2 tcm

1.1

1.1

0.9

0.8

0.7

0.3 0.2

1. Cubic meter – 8,850 kcal 2. Including Baltic States 3. Excluding Baltic States

Source: Gazprom

Strategy - Investor Day 2012

6

Investor Day 2012

0

1

2

3

4

5

6

2005 2006 2007 2008 2009 2010 2011 2012

1:1 1:2 1:3 1:4 1:5 6:1

5:1

4:1

3:1

2:1

1:1

Oil price (WTI) to gas price (Henry Hub) ratio

US oil and gas prices

Source: Bloomberg

In future, gas consumption will grow faster than was expected in 2010

Using natural gas as motor fuel (for cars, trucks, buses,

ships) and consequent replacing of oil products with natural

gas are raising. The only restriction is lack of infrastructure

An area for further development is electric cars which can

increase consumption of electricity and as a consequence of

natural gas

Strategy - Investor Day 2012

E F

7

Investor Day 2012

– Consumption

– Production

Middle East

Global gas balance

Source: Gazprom

bcm

North America

Latin America

Asia/Oceania

FSU

Africa

Europe

0

300

600

900

1200

1500

2010 2020F 2030F

0

300

600

900

1200

1500

2010 2020F 2030F

0

300

600

900

1200

1500

2010 2020F 2030F

0

300

600

900

1200

1500

2010 2020F 2030F

0

300

600

900

1200

1500

2010 2020F 2030F

0

300

600

900

1200

1500

2010 2020F 2030F 0

300

600

900

1200

1500

2010 2020F 2030F

Europe and Asia are two most important markets

Strategy - Investor Day 2012

8

Investor Day 2012

Strategic tasks of gas business

Retain current position in

the Russian market

Gain 32% in the

European market

Diversify markets by

entering into the most

promising North-East

Asian market (13%

market share)

Expand LNG business

(14% of world production)

Exploration &

Production Transportation & UGS

Distribution &

Marketing

Develop new production

regions:

– Yamal peninsula

– Eastern Siberia & the

Far East

– Russian continental

shelf

Prioritize development of

fields located close to

existing UGSS

infrastructure

Reconstruction within

UGSS

Create gas pipelines to

transport gas from new

production regions

Diversify export pipeline

routes:

– Nord Stream

– South Stream

Develop unified gas

supply system in the

East of Russia

Increase UGS capacity

Strategy - Investor Day 2012

Note: UGS is underground gas storage UGSS is unified gas supply system

9

Investor Day 2012

Shtokman

Prospective sources of Gazprom’s gas production

Eastern Siberia and

the Far East New fields in Nadym-

Pur-Taz

bcm

Yamal

0

100

200

300

400

500

600

700

800

2010 2020F 2030F Currently existing projects New fields in Nadym-Pur-Taz Yamal Megaproject Shtokman Project Eastern Siberia and the Far East

0

100

200

300

400

2010 2020F 2030F

0

100

200

300

400

2010 2020F 2030F

0

100

200

300

400

2010 2020F 2030F

0

100

200

300

400

2010 2020F 2030F

bcm

Strategy - Investor Day 2012

10

Investor Day 2012

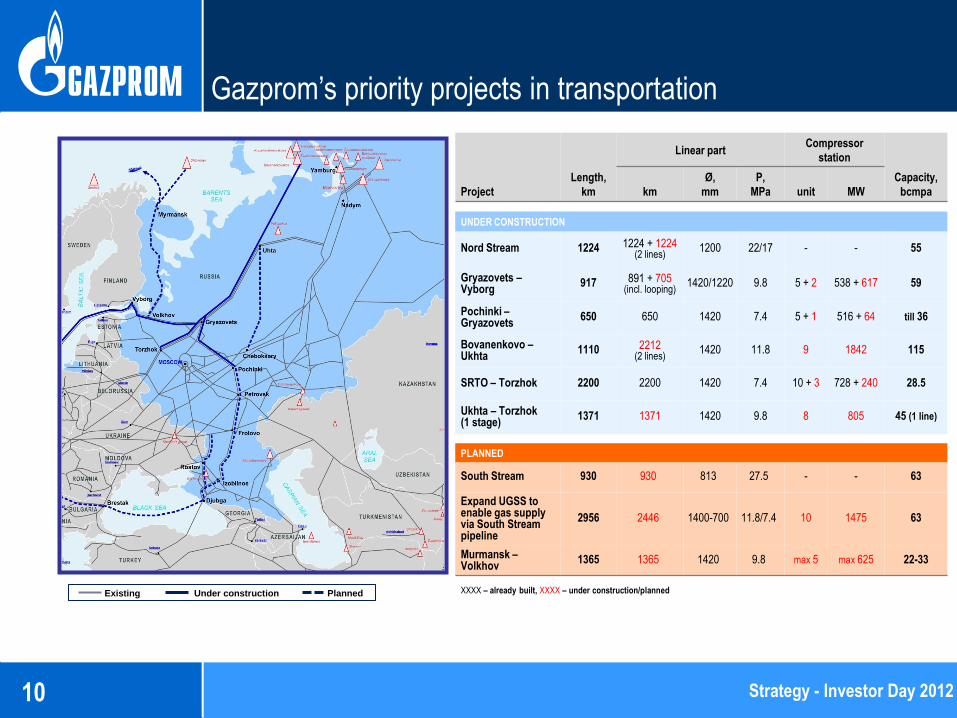

Gazprom’s priority projects in transportation

Existing Under construction Planned

Project

Length,

km

Linear part Compressor

station

Capacity,

bcmpa km

Ø,

mm

P,

MPa unit MW

UNDER CONSTRUCTION

Nord Stream 1224 1224 + 1224 (2 lines)

1200 22/17 - - 55

Gryazovets – Vyborg

917 891 + 705 (incl. looping)

1420/1220 9.8 5 + 2 538 + 617 59

Pochinki – Gryazovets

650 650 1420 7.4 5 + 1 516 + 64 till 36

Bovanenkovo – Ukhta

1110 2212 (2 lines)

1420 11.8 9 1842 115

SRTO – Torzhok 2200 2200 1420 7.4 10 + 3 728 + 240 28.5

Ukhta – Torzhok (1 stage)

1371 1371 1420 9.8 8 805 45 (1 line)

PLANNED

South Stream 930 930 813 27.5 - - 63

Expand UGSS to enable gas supply via South Stream pipeline

2956 2446 1400-700 11.8/7.4 10 1475 63

Murmansk – Volkhov

1365 1365 1420 9.8 max 5 max 625 22-33

XXXX – already built, XXXX – under construction/planned

Strategy - Investor Day 2012

11

Investor Day 2012

0

10

20

30

40

1999 2002 2005 2008 2010

0

5

10

15

2002-2003 2004-2006 2007-2010 2011E-2013F

Energy efficiency

11

Natural gas savings – 30.6 bcm

Heat energy savings – 2,449 th. Gcal

0

250

500

750

1,000

2002-2003 2004-2006 2007-2010 2011E-2013F

Electricity savings – 3,392 mm kWh

36.2 mm tce total energy savings in 2002-2013F

12%

86%

1% 1%

Production

Transportation & underground gas storage

Processing

Other

Gas consumption of Gazprom’s gas trunking processes

0

500

1,000

1,500

2002-2003 2004-2006 2007-2010 2011E-2013F

Strategy - Investor Day 2012

Cm/ mm cm*km

th. Gcal

mm kWh

bcm

12

Investor Day 2012

Development of Gazprom’s business in East Siberia and the Far East

GAS RESERVES (А+В+С1+С2), bcm

Onshore 177 3,756

Offshore - 1,021(1)

Total: 177 4,777

1. Including Gazprom’s 50% share in Sakhalin-2 project

CAPACITY OF GAS TRANSPORTATION SYSTEMS, bcm

Sakhalin — Khabarovsk — Vladivostok (the first start-up complex) - 6

Sakhalin-2 fields — LNG plant - 15

Sobolevo — Petropavlovsk-Kamchatsky - 1

Total: - 22

LNG CAPACITIES, mm t

Sakhalin-2 - 9.6

Strategy - Investor Day 2012

01.01.2007 01.01.2012

13

Investor Day 2012

Potential economic effect as result of innovation

13

Implementation of technological priorities ensures an extra potential economic effect of 450 bln RR

15.7

83.1

55.6

54.6

45.9

18.7

159.2

16.9

NPV, bln RR

Technology to improve gas transportation efficiency

Technology to develop hydrocarbon resources in continental shelf

Gas processing and petrochemical technology

Technology for developing hydrocarbon resources in permafrost areas

Gas sale and utilization technology

Technology to improve gas storage efficiency Hydrocarbon production technology on existing fields

Hydrocarbon fields exploration technology, including

development of alternative resources

450

Strategy - Investor Day 2012

14

Investor Day 2012

Gas CAPEX 2012-2030F

Structure of CAPEX by business segment

(average annual) Structure of CAPEX by major project

(2012F-2030F in total)

EXPLORATION

PRODUCTION

TRANSPORT

(incl. UGS)

PROCESSING

OTHER

47%

31%

6%

8%

8%

700-900 bln RR p.a.

Shtokman project

Yamal Megaproject

Eastern Siberia and the Far East

Transport System Development (incl. UGS)

Reconstruction in Transport

Currently existing projects in Production

Other projects within UGSS

14%

29%

8% 8%

15%

6%

20%

(exploration; new production and drilling

(excl. Yamal and Shtokman); processing;

others)

Strategy - Investor Day 2012

Note: UGS is underground gas storage UGSS is unified gas supply system

Export

Part 2. Alexander Medvedev

Deputy Chairman of Gazprom Management Committee

Director General of Gazprom Export

15 Investor Day 2012

Департамент стратегического развития 16

-10.0%

-6.0%

-2.0%

2.0%

6.0%

10.0%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

E

European natural gas market dynamics

European gas consumption and imports in 2011E

2008 2009 2010 2011E 2011E/10,

bcm

2011E/10,

%

Consumption (bcm) 600.7 565.2 609.8 563.5 -46.4 -7.6%

Domestic production (bcm) 320.0 307.0 311.6 293.8 -17.8 -5.7%

Imports(1) (bcm) 280.3 258.2 298.2 269.7 -28.5 -9.6%

Source: International Energy Agency, Eurostat, Gazprom Export. Gas calorific value: 1cm = 37 MJ

0

10

20

30

40

50

60

70

80

90

0 5,000 10,000 15,000 20,000

Co

nsu

mp

tio

n (m

on

thly

), b

cm

Monthly Weather Index

Net heating & cooling degree days

Source: Gazprom Export (based upon annualized HDD/CDD for Europe)

110 115 120 125 130 135 140 145 150 155 160

95 100 105 110 115 120 125 Co

nsu

mp

tio

n(1

) (q

uar

terl

y), b

cm

Sea

son

ally

Ad

just

ed

GDP SA Index (2001Q1=100)

Natural gas consumption correlates primarily to weather conditions, not GDP

11 Year

Average

Export - Investor Day 2012

+5%

-5%

+10%

-10%

Source: Gazprom Export (based upon monthly HDD/CDD for Europe) 1. Including balance of gas storage

Департамент стратегического развития 17

77

101 97 97

57 70 71 75

$61 $89 $111

$159 $202

$232

$301 $320

0

50

100

150

200

250

300

350

0

20

40

60

80

100

120

2005 2006 2007 2008 2009 2010 2011E 2012F

Volumes Average FSU Price

154 156 153 160 141 139

150 154

156 162 169 168

148 148 160

164

$192

$262 $269

$407

$297 $302

$384 $415

0

150

300

450

600

0

50

100

150

2005 2006 2007 2008 2009 2010 2011E 2012F

Export Volumes Other Deliveries Average European Price

27%

73%

30%

70%

Gazprom Other Suppliers

32%

68%

17

Gazprom sales to European and FSU markets

USD/mcm

Gazprom Group gas deliveries to Europe

Projected Gazprom European market share

Gazprom Group gas deliveries to FSU

Gazprom’s portfolio includes long term

contracts ensuring Minimum Annual

Quantities (MAQ) of 4 trillion cubic meters

of gas to Europe over the period

2012 - 2030

Source: Gazprom estimates

bcm bcm USD/mcm

2011E 2020F 2030F

Export - Investor Day 2012

Департамент стратегического развития 18

0

100

200

300

400

500

600

700

800

900

2010

2011

E

2012

F

2013

F

2014

F

2015

F

2016

F

2017

F

2018

F

2019

F

2020

F

2021

F

2022

F

2023

F

2024

F

2025

F

2026

F

2027

F

2028

F

2029

F

2030

F

bcm

Range of production forecasts Range of consumption forecasts Production consensus forecast Consumption consensus forecast

270

bcm

370

bcm

400

bcm

The gap is widening between European indigenous production and consumption

The gap is widening…

Source: Consensus projections derived from EIA, CERA, Greenpeace, IEA, EuroGas, PIRA, EC, Cedigaz

Export - Investor Day 2012

Департамент стратегического развития 19

800

529

1,154

756

986

831

1,653 1,517

0

500

1000

1500

2000

2010 2030 Average IEA HIS CERA EGAF Eurogas Eurelectric

TW

h

965

625

Electricity produced from natural gas in 2030 carbon reduction road maps

Anticipated market - Marine bunkering sector Anticipated market - Automotive sector

Natural gas demand growth potential by sector

bcm bcm

217

90

49

191

80

28 24

-50

50

150

250

2010

2011

E

2012

F

2013

F

2014

F

2015

F

2016

F

2017

F

2018

F

2019

F

2020

F

2021

F

2022

F

2023

F

2024

F

2025

F

2026

F

2027

F

2028

F

2029

F

2030

F

Global consumption, CERA Global consumption, Pace Global

European consumption, Pace Global

-50

50

150

250

2010

2011

E

2012

F

2013

F

2014

F

2015

F

2016

F

2017

F

2018

F

2019

F

2020

F

2021

F

2022

F

2023

F

2024

F

2025

F

2026

F

2027

F

2028

F

2029

F

2030

F

Global consumption, CERA European consumption, Pace Global

European consumption, CERA European consumption, Eurogas

2010 2030F

Export - Investor Day 2012

Update: December 2011

1,000

Департамент стратегического развития 20

180 mm t

coal (1)

20

Renewable subsidies and other

incentives are equal to €820 bln

or 53% of the total All-In cost of

renewable generation over the

next 20 years.

Cumulative cost advantages of gas-optimized scenario, Euro bln

Subsidies 53%

€820 bln

€1550 bln

Source: Pace Global

700 1650

1200 2500

850

capital expenditures

350- 400

operational expenditures

450- 500 total

savings 150 bcm

natural gas

135 mm t

fuel oil (1)

Exp

ort

vo

lum

es i

n 2

011E

= =

1. by calorific value

CO2 emissions

278 m t 525 m t 415 m t

Gas is the best fossil fuel and the cheapest path to reach EU CO2 reduction targets

Gas-optimized

scenario

Renewables

60%

Source: McKinsey for the European Gas Advocacy Forum

2030F 2050F

Export - Investor Day 2012

Департамент стратегического развития 21

Hub and contract prices

Sources: BMWi, Bloomberg, European Central Bank

Hybrid pricing - cornerstone of the European market

USD per mcm

Importers are disadvantaged by reforms, not Gazprom

USD per mcm

Hub Prices

Contract Prices

Churn ratio remains below 5 at all continental hubs

A large portion of natural gas traded at the hubs is

derived from long term oil-indexed contracts

Hybrid pricing mechanism should be adjusted to

facilitate synergies and fairness in competition

“Free riders” produce no gas and have no import

contracts. They do not pay full cost for gas storage

and structuring of deliveries

Export - Investor Day 2012

! Only for small volumes

0

100

200

300

400

500

600

Jan-08 Jun-08 Nov-08 Apr-09 Sep-09 Feb-10 Jul-10 Dec-10 May-11 Oct-11

NWE long-term contracts proxy (Platts) BAFA TTF month ahead LNG import price, Japan

Департамент стратегического развития 22

174.9

184.4

220.6

247.1 257.3 264.5 266.0

280.6

0

50

100

150

200

250

300

2008 2009 2010 2011E 2012F 2013F 2014F 2015F

4%

6%

8%

10%

12%

14%

16%

18%

2001-2005 Headline slopes as low as 4-6%,

S-curves

2005-2006 Discussions on

S-curve eliminations

Late 2006-2008 Record high

slopes agreed: 16-17%

2009-2010 14.85% - benchmark slope

for conventional LNG, 14-14.5% for CBM/FLNG

with S-curve

2011E-2012F Market remains tight as

nuclear situation in Japan takes time to

resolve

Long term contracts - oil parity level development in

the Asia-Pacific region

The Asia-Pacific region is a main source of growth: demand is strong with

prices continuing to rise, boosted by the earthquake in Japan

Asia attracts spare LNG volumes, including those redirected from Europe

LNG supply growth is limited in the next few years: the situation is unlikely

to change dramatically

Lack of excess LNG volumes will support European long-term contracts

pricing mechanisms

Asian market – Key pillar for LNG growth

Global LNG production volume

Source: Woodmac

Source: Bloomberg, Platts Source: Gas Strategies, Platts, Poten

CAGR

2011E-2015F

12%

CAGR

2011E-2015F

3%

0

2

4

6

8

10

12

14

16

18

20

22

0

2

4

6

8

10

12

14

16

18

20

22

Sep 10

Oct 10

Nov 10

Dec 10

Jan 11

Feb 11

Mar 11

Apr 11

May 11

Jun 11

Jul 11

Aug 11

Sep 11

Oct 11

Nov 11

Dec 11

Jan 12

Feb 12

Mar 12

Apr 12

May 12

Forward curves

USD/mm btu

Brent HH NBP JKM

Oil Parity

Kashiwazaki-

Kariwa power

plant

shutdown

Fears about LNG

demand surge in

the US

New LNG

projects

announced

Earthquake in

Japan, nuclear

power plants

shutdowns

Export - Investor Day 2012

mm t

+$14

+$5

Департамент стратегического развития 23

Russia

Nigeria

Egypt

Qatar

Australia

USA

Japan

India

China

Korea

Taiwan

Thailand

Dubai

Kuwait

UK

Portfolio supply sources and destinations (2011E)

Gazprom LNG portfolio shows steady growth

Geographic diversification increases, both in terms of supply sources and marketing destinations – presence in both

Atlantic and Pacific basins

Access to shipping capacity supports portfolio flexibility

Long-term charter agreements for two newly build LNG carriers signed in addition to existing fleet of chartered

LNG vessels

Gazprom – growing presence in LNG market

Traded volume dynamics (1)

Export - Investor Day 2012

1.2

2.1

1.2

0.2 0.3 0.4 0.5

0.7

0.4 1.8

0.2 0.3 0.4 0.5

1.8

2.4

3.0

2005 2006 2007 2008 2009 2010 2011E

Russia Non-Russia

1. Totals may not sum due to rounding

bcm delivered

Investor Day 2012

25

Finance

Part 3. Andrey Kruglov

Deputy Chairman of Gazprom Management Committee

Head of the Department for Finance and Economics

Investor Day 2012

25

Investor Day 2012

70%

85%

100%

115%

130%

J F M A M J J A S O N D

Gazprom MICEX

Investing in Gazprom should be viewed as safe and liquid

2%

4%

6%

8%

J F M A M J J A S O N D J Gazprom 6.51% due 2022 Russia 5% due 2020

6.8

9.0

11.8 11.1

7.3

4.9 4.4 4.0

12.7

10.3 9.4

11.2

9.3 10.0 8.7 8.3

0

5

10

15

2004 2005 2006 2007 2008 2009 2010 2011E

Gazprom Oil&Gas Majors median

4.9

6.2

8.0 7.4

5.1 4.2

3.7 3.2

5.7 5.0

4.6 5.6

4.6 4.7 4.3 4.1

0

2

4

6

8

10

2004 2005 2006 2007 2008 2009 2010 2011E

Gazprom Oil&Gas Majors median

Gazprom shares and bonds: liquid Russian securities

Gazprom share price performance (2011) Bonds YTM (2011)

Source: Gazprom data, Bloomberg, FactSet 1. Average 1-year forward multiples. Oil & Gas Majors are the top 10 oil and gas companies by market capitalization as of the beginning of 2012,excluding Gazprom

EV/EBITDA multiple evolution(1) P/E multiple evolution(1)

Theoretical

potential

Theoretical

potential

Finance - Investor Day 2012

26

Investor Day 2012

Strong financials: potential for future growth

11%

7% 9%

8%

3% 1%

0%

5%

10%

15%

Revenue EBITDA Net income

CAGR Gazprom for 2006-2010 CAGR of oil & gas majors’(1) on average for 2006-2010

1. Oil & Gas Majors are the top 10 oil and gas companies by market capitalization as of the beginning of 2012,excluding Gazprom 2. Converted using the annual average exchange rate as of the respecting period 3. Adjusted EBITDA is defined as operating profit before depreciation and changes in assets, impairment provision (impairment of accounts receivable and prepayments, assets under construction, investments and

other long-term assets, inventory) 4. Data are converted in USD using exchange rate USD 1 = 30.24 RR at the end of 2009, USD 1 = 30.48 RR at the end of 2010, USD 1 = 30.40 at the end of 9m2010, USD 1 = 31.88 at the end of 9m2011 5. Net of custom duties and VAT

2009 2010 9m 2010 9m 2011 2011E

Total sales revenue(2)(5)

USD bln 94.2 118.4 82.5 114.6 155

Adj. EBITDA(2)(3), USD bln 34.3 44.7 31.7 47.9 63

Adj. EBITDA margin 36% 38% 38.4% 41.8% 41%

Gazprom’s net income —

the highest in the industry

2009 2010 9m 2010 9m 2011 2011E

Net Debt(4), USD bln 45.4 28.6 32.0 32.8 34

Total debt(4), USD bln 53.8 43.2 42.5 44.9 48

T. Debt / Adj. EBITDA (LTM) 1.49x 0.97x 1.0x 0.8x 0.8x

(1)

Comparative 5Y CAGR

Gazprom’s financials

Finance - Investor Day 2012

High net income is expected to deliver increased dividend payout

27

Investor Day 2012

Well-managed CAPEX

.

1. Data are converted in USD using exchange rate USD 1 = 30.36 RR in 2010; USD 1 = 28.3 RR in 2011 and Gazprom’s budget exchange rate forecast for 2012 (USD 1 = 28.7 RR in 2012)

0

10

20

30

40

50

60

2010 2011E 2012F

34 USD bln (1) 35 USD bln (1)

50 USD bln (1)

USD bln

Transportation

Production

Other segments

(Including gas storage,

gas processing and

Gas distribution)

Power & heat

generation

Gazprom Neft

CAPEX structure to provide:

– Production growth, depending on market

requirements

– Flexible company strategy in the future

Meticulous project prioritization allows rational

fund allocation

Cash CAPEX wholly financed with operating CF

Finance - Investor Day 2012

Gazprom Group cash CAPEX breakdown

Investment policy will allow Gazprom to respond to future market requirements and gas demand

28

Investor Day 2012

33.6 38.6

40.2 43.0 45.7

21.4%

-7.2%

12.2% 18.7% 10.7%

0

10

20

30

40

50

60

2008 2009 2010 2011E 2012F

Unit cost of gas production Producer price index

459.2

528.5

532.5

582.6 702.1

90.0(3)

272.0(3)

672.6

974.1

21.4%

-7.2%

12.2%

18.7% 10.7%

0

200

400

600

800

1,000

2008 2009 2010 2011E 2012F

Unit cost of gas production Mineral Extraction Tax (MET)

Producer price index

Effective cost management

Unit cost of gas production (1) Unit cost of gas transportation (2)

RR/1000 cm RR* 1000 cm/100km

1. Unit cost of gas production per 1000 cm of sale gas among 7 majors Gazprom ‘s subsidiaries . Excludes cost of OAO Gazprom 2. Unit cost of gas transportation includes cost per1000 cm of gas transported 100 km by Gazprom’s gas transportation subsidiaries. Excludes cost of OAO Gazprom. 3. Unit cost increase of gas production due to MET growth

Increase in cost of gas production and transportation (excluding one-off MET increase) is in line with current

inflation rate

Finance - Investor Day 2012

29

Investor Day 2012

0

500

1000

1500

2000

2500

3000

3500

4000

0

50

100

150

200

250

300

350

400

450

500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

Consumption in Russia Gazprom's account receivables turnover, days Gazprom's average domestic gas price

179d

98d 98d

48d

42d 36d 35d 38d

40d 49d

+16%

58d 59d +29%

In 2009 obligatory prepayments

for gas deliveries on the

domestic market were cancelled

Development of Russian gas market

+3% +2% -1% -7%

+7%

0%

+3%

+22% +2%

+4% +4%

+27% +31% +20%

+23% +11% +15%

+26%

+16%

+26%

+15% +8%

Average price,

RR/mcm

Consumption,

bcm +1%

Improvement of payment discipline

Sustainability of gas supply

Price liberalization

Recovery of gas consumption in Russian market

Finance - Investor Day 2012

2012F 2013F

-1%

Revenue growth due to price increase and volume recovery

30

Investor Day 2012

Impeccable credit history

45.4

28.6 32.8 34

8.4

14.6 12.1 12

48

0

10

20

30

40

50

60

2009 2010 9m2011LTM 2011E 2012F

Net debt Cash and equivalents Total debt

1.5

1.0 0.8 0.8 0.8

0.0

0.4

0.8

1.2

1.6

2009 2010 9m2011LTM 2011E 2012F

Total debt / adjusted EBITDA

Total and net debt(1)

USD bln

Main debt ratios

11.6

24.4 14.7

35.1

64.7

52.2

0

20

40

60

80

2007 2008 2009 2010 9m2011 2012F

Adjusted EBITDA/Gross interest

1%

3%

5%

7%

9%

2003 2004 2005 2006 2007 2008 2009 2010 9m2011

Weighted average fixed interest rate

Weighted average floating interest rate

Weighted average interest rate

Cost of debt financing

Finance - Investor Day 2012

Gazprom maintains a comfortable level of debt

(2)

1. Data are converted in USD using exchange rate USD 1 = 30.24 RR at the end of 2009, USD 1 = 30.48 RR at the end of 2010, USD 1 = 31.88 at the end of 9m2011 2. Gross interest is calculated as Interest expenses from Operating activities.

Max level 1.5-1.7

31

Investor Day 2012

Gazprom’s credit strength

1. S&P/Moody’s/ Fitch 2. Rating reflects bond ratings and not company ratings 3. Interpolated secondary curve spread to mid-swaps (MS) 4. Difference between 5Y MS-spread and interpolated Sovereign secondary MS-spread 5. The spreads are as of closing 7-February 6. Estimation, as Sovereign USD curve does not exist

Baa1/BBB/BBB

Baa1/BBB/BBB

Yes

+371bps

+140bps

Baa1/BBB/BBB

Baa1/BBB/BBB

Baa1/BBB/BBB

Yes

+204bps

+81bps

Baa1/BBB/BBB

A1/A+/A+

Aa3/AA-/A+

Yes

+141bps

-2bps(6)

Aa3/AA-/A+

Bond ratings(1)(2):

Sovereign rating:

State-controlled:

5Y MS-spread(3)(5):

Spread to

Sovereign(4)(5):

Company ratings:

A3/BBB/BBB

Baa2/BBB/BBB

Yes

+232bps

+137bps

A3/BBB/BBB

Finance - Investor Day 2012

Despite Gazprom’s strong credit ratings our bonds are trading at higher spreads than the international debt

capital market peers

32

Investor Day 2012

0.8% 0.8% 0.3%

1.3%

2.0%

4.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2006 2007 2008 2009 2010 2011E

Increase of dividend payouts up to 25% of Net Income

Dividend payouts for the coming years have been approved at the level of 25% of net income (RAS)(1)

Dividend payout amounts forecasts:

2012F – 198 bln RR

2013F – 180 bln RR

2014F – 210 bln RR

2.54 2.66

0.36

2.39

3.85

8.39

0

2

4

6

8

10

2006 2007 2008 2009 2010 2011E

1. As envisaged by OAO Gazprom budget approved by the BoD in December 2011. Subject to the final approval by Annual General Shareholders Meeting in June 2012

Finance - Investor Day 2012

Dividend Per Share Dividend Yield

High dividend yield increases attractiveness of Gazprom shares

RR

33

Investor Day 2012

Social and ecological responsibility

Social Initiatives

Gazprom to Children Program

Sponsorships and charity

Gasification Program for

Russian Regions

Social projects and cultural

projects

Ecological Developments

Environmental

Management System

Emissions Reduction

Program

Energy saving Program

Finance - Investor Day 2012

Social and ecological activities provide for sustainable long-term development of Gazprom and Russia

34

Investor Day 2012 Finance - Investor Day 2012

Conclusion

Gazprom’s strategy responds to the global trend of growing gas demand

Natural gas – the future of world energy

Conservative financial strategy ensures Gazprom’s stable financial position

Gazprom’s securities should be viewed as defensive investments on Emerging markets

Gazprom’s operating and financial performance continue to grow

Core values, flexibility and consistent development – our key to strengthening our export position

35

Investor Day 2012

Contacts for investors

Department for Finance & Economics

Capital Markets Directorate

Fax: (007) (495) 719-35-41

Oleg NAGOVITSYN

Deputy Head of Capital Markets Directorate

Phone: (007) (495) 719-26-25

E-mail: [email protected]

Andrei BARANOV

Investor Relations

Phone: (007) (495) 719-25-89

E-mail: [email protected]

Finance - Investor Day 2012

Investor Day 2012

36

Gazprom Neft

Part 4. Vadim Yakovlev

Deputy Chairman of the Management Board of Gazprom Neft

First Deputy CEO of Gazprom Neft

Investor Day 2012

Investor Day 2012 37

1. Gazprom Neft estimates 2. Including GPN share in EBITDA of joint ventures 3. Adjusted foe one-off items

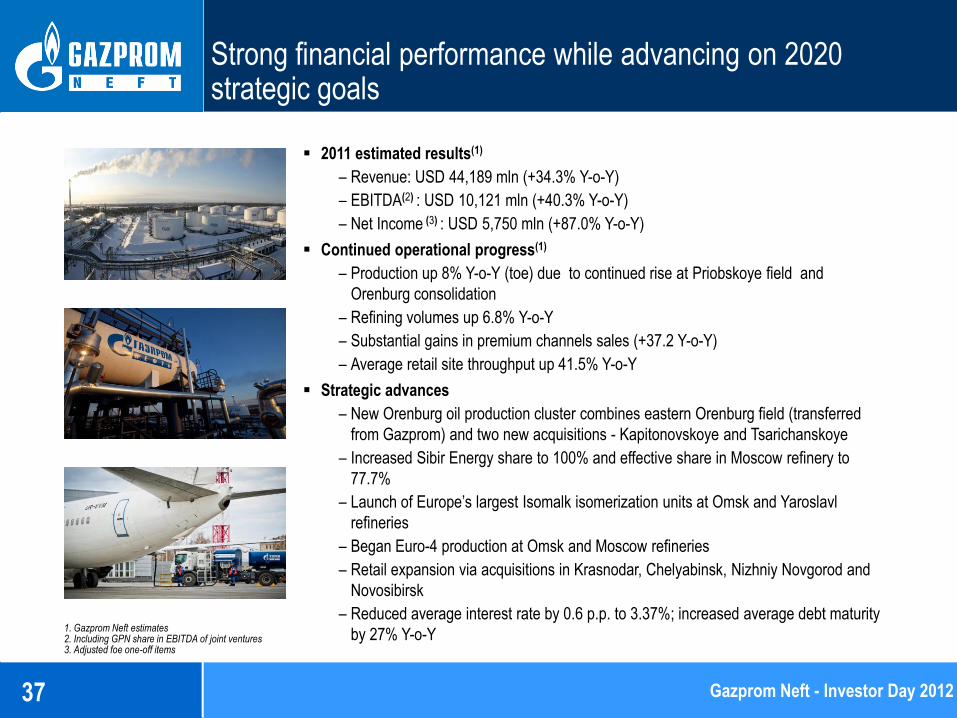

Strong financial performance while advancing on 2020 strategic goals

2011 estimated results(1)

– Revenue: USD 44,189 mln (+34.3% Y-o-Y)

– EBITDA(2) : USD 10,121 mln (+40.3% Y-o-Y)

– Net Income (3) : USD 5,750 mln (+87.0% Y-o-Y)

Continued operational progress(1)

– Production up 8% Y-o-Y (toe) due to continued rise at Priobskoye field and

Orenburg consolidation

– Refining volumes up 6.8% Y-o-Y

– Substantial gains in premium channels sales (+37.2 Y-o-Y)

– Average retail site throughput up 41.5% Y-o-Y

Strategic advances

– New Orenburg oil production cluster combines eastern Orenburg field (transferred

from Gazprom) and two new acquisitions - Kapitonovskoye and Tsarichanskoye

– Increased Sibir Energy share to 100% and effective share in Moscow refinery to

77.7%

– Launch of Europe’s largest Isomalk isomerization units at Omsk and Yaroslavl

refineries

– Began Euro-4 production at Omsk and Moscow refineries

– Retail expansion via acquisitions in Krasnodar, Chelyabinsk, Nizhniy Novgorod and

Novosibirsk

– Reduced average interest rate by 0.6 p.p. to 3.37%; increased average debt maturity

by 27% Y-o-Y

Gazprom Neft - Investor Day 2012

Investor Day 2012 38

8% organic production growth in 2011

Gazprom Neft

Hydrocarbon production, mm toe

Peer comparison Hydrocarbon

production increase 2011E vs 2010

Gazprom Neft - Investor Day 2012

44.7 48.7 50.2 52.8

57.3

0

10

20

30

40

50

60

70

2007 2008 2009 2010 2011E

-4%

0.3%

1%

3%

8%

-10% -5% 0% 5% 10%

Lukoil

TNK-BP

Surgutneftegas

Rosneft

Gazprom Neft

Investor Day 2012 39

1. Domestic refining only for all companies

Downstream: well positioned for profitable growth, maximum utilization of high refining margins

Gazprom Neft - Investor Day 2012

Gazprom Neft

Refining throughput, mm t

Peer comparison

Throughput increase 2011 vs 2010

26.2 28.4

33.4 37.9

40.5

0

9

18

27

36

45

2007 2008 2009 2010 2011E

0.2%

0.3%

0.3%

2.6%

8.9%

-10% -5% 0% 5% 10%

Lukoil

Surgutneftegas

Rosneft

TNK-BP

Gazprom Neft

(1)

Investor Day 2012 40

Focus on high margin retail sales and network growth

Gazprom Neft - Investor Day 2012

Retail sales, mm t

4.3 5.9

8.2

11.6

15.7

0

3

6

9

12

15

18

2007 2008 2009 2010 2011E

783 865

1,546 1,596 1,689

8.0

9.1

7.1 7.7

10.9

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

0

500

1,000

1,500

2,000

2,500

3,000

2007 2008 2009 2010 2011E

Filling sations (LHS) Av. daily throughput (RHS)

Retail Network

units tonnes

Investor Day 2012 41

- Bunkering

- Aviation

- Lubricants

2011E premium sales growth

Continued development of other high margin channels

Gazprom Neft - Investor Day 2012

51%

53%

51%

35%

0% 30% 60% 90% 120%

Retail

Bunkering

Lubricants

Aviation

Investor Day 2012 42

Revenue, USD mm EBITDA(1), USD mm

Net income(2), USD mm Net debt / EBITDA

Continuing strongly positive financial trends

1. Including GPN share in EBITDA of joint ventures 2. Adjusted for one-off items

Gazprom Neft - Investor Day 2012

22,768

33,870

24,166

32,912

44,189

0

10,000

20,000

30,000

40,000

50,000

2007 2008 2009 2010 2011E

6,601

8,610

5,977 7,212

10,121

0

2,000

4,000

6,000

8,000

10,000

12,000

2007 2008 2009 2010 2011E

4,143 4,658

3,013 3,075

5,750

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2007 2008 2009 2010 2011E

0.46

0.21

1.08

0.75 0.57

0.00

0.20

0.40

0.60

0.80

1.00

1.20

2007 2008 2009 2010 2011E

Investor Day 2012 43

19.6 21.1

17.9

14.0

26.3 25.8 24.9

20.3

0

5

10

15

20

25

30

Lukoil Rosneft Gazprom Neft TNK-BP

9M10 9M11

Growth and operating performance deliver industry-leading results

EBITDA USD / boe

ROACE 12M trailing, % Total Shareholder Return(1) 2011 %

EBITDA growth 9M11vs. 9M10

1. TSR = (Price end of the period – Price beginning of the period + Dividends per share)/Price beginning of the period

Gazprom Neft - Investor Day 2012

50% 48%

28% 25%

0%

10%

20%

30%

40%

50%

60%

Gazprom Neft TNK-BP Lukoil Rosneft

25.1

14.3 14.2 13.6

37.1

20.3 17.3 16.4

0

10

20

30

40

TNK-BP Gazprom Neft Rosneft Lukoil

2010 2011E

16%

2%

-2% -2%

3%

9%

3% 1%

19.0%

10.6%

1.7%

-0.9% -5%

0%

5%

10%

15%

20%

-5%

0%

5%

10%

15%

20%

Gazprom Neft TNK-BP Lukoil Rosneft

Capital gain Dividend yield TSR

Investor Day 2012 44

2012 outlook: 4% production growth from organic investment projects

2012F Highlights(1) Investments(1), USD bln

Organic Capex (4.1) USD bln (5.4) USD bln

M&A and

Divestments (1.3) USD bln (0.07) USD bln

2011E 2012F

Hydrocarbon

production(2) 57.3 mm toe 59.6 mm toe

Refining 40.5 mm t 40.1 mm t

Retail products sales

via premium channels 19.5 mm t 19.5 mm t

Source: Gazprom Neft data;

1. 2012F Capex subject to final review

2. Including investments into JV projects

+/-0%

2012 Planned Capex and Investments (2)

Gazprom Neft - Investor Day 2012

5.5 5.4

(2)

0

1

2

3

4

5

6

2011E 2012F

Upstream brownfield Upstream greenfield Refining Marketing & distribution NIS Other M&A

+/-0%

Investor Day 2012 45

expected production

I stage Production growth

II stage Stabilization

III stage 10-30% annual decline

0 stage Preparation for development

Priobskoye

Zymnee

Orenburg

SeverEnergy

Vyngapurovskoye

IV stage 2-3% annual decline

Messoykha

Novoport

Value growth

Upstream project pipeline will deliver substantial oil production growth

Gazprom Neft - Investor Day 2012

Investor Day 2012 46

1

2

3

Prirazlomnoye (offshore)

Dolginskoye (offshore)

Novoport (YANAO)

3

The Arctic

Ocean

Kara

Sea

Rotterdam

Long term project pipeline includes synergistic offshore Arctic developments

▪ Oil field license transfers underway from Gazprom

▪ Gazprom Neft offshore production would reach 6.6 mm t of oil

by 2020, with an 8 year plateau

▪ Consolidation of Prirazlomnoye and Dolginskoye oil fields

▪ Synergy with Novoport project in the Northern Sea route

logistics

Barents Sea

Novaya

Zemlya

Prirazlomnoye Dolginskoye

Reserves (Recoverable С1, mm t)

74.4 68.5

Production start up (year)

2012 2018-2020

Peak production (oil, mm t)

6.6 6.2

Platforms 1 1

Yamal

peninsula

Gazprom Neft - Investor Day 2012

Investor Day 2012 47

Analyst target prices imply a 20% undervaluation of Gazprom Neft stock

Broker

Date

EBITDA (USD mm)

Recommendation

Target price (rubles) 2011E 2012F

Alfa Bank 09/07/11 7,392 6,679 overweight 165.0

Citi Investments 06/30/11 9,277 7,176 buy 175.5

Deutsche Bank 12/02/11 8,022 7,108 buy 195.1

Goldman Sachs 05/23/11 8,848 9,417 neutral 169.4

IC Otkritye 02/06/12 6,957 3,499 sell 105.4

JP Morgan 01/31/12 8,441 7,701 overweight 175.7

Troika Dialog 10/11/11 8,034 7,491 buy 165.6

UniCredit 09/15/11 8,302 8,137 buy 182.5

Uralsib Capital 02/03/12 8,391 7,978 buy 175.0

VTB Capital 01/26/12 7,497 7,596 buy 269.4

Average 178

Gazprom Neft - Investor Day 2012

Consensus

SELL BUY

150

178

Current price Av. target price

Investor Day 2012 48

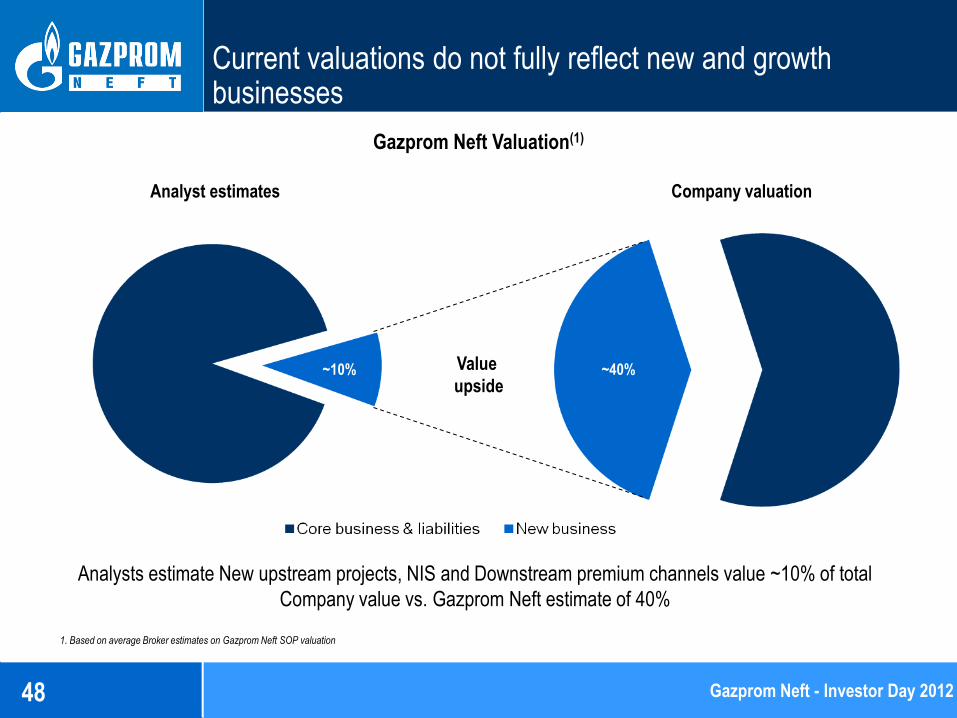

Current valuations do not fully reflect new and growth businesses

Gazprom Neft Valuation(1)

1. Based on average Broker estimates on Gazprom Neft SOP valuation

Analysts estimate New upstream projects, NIS and Downstream premium channels value ~10% of total

Company value vs. Gazprom Neft estimate of 40%

Analyst estimates Company valuation

~10% ~40% Value

upside

Gazprom Neft - Investor Day 2012

Investor Day 2012 49

New projects and other positives provide additional valuation upside

Gazprom Neft valuation vs Market capitalization, USD bln

Source: Gazprom Neft estimates

23

37

28 27

1 3

8

3

Market cap 31.12.2011 Russian multiples NIS New upstream projects Downstream premium channels

Estimated value Analyst consensus

Value upside

+ 61%

Gazprom Neft - Investor Day 2012

Investor Day 2012 50

Operational performance, financial discipline, long term growth and unrecognized value

Leading Russian company in 2011 by production growth

Strong mid-term and long-term Upstream project pipelines

Incremental opportunities to optimize natural gas use

Most advantaged Russian refining portfolio

Diverse and fast growing premium products channels

Continuous operating improvement and financial discipline

Strongly positive financial trends and valuation upside

Gazprom Neft - Investor Day 2012

Investor Day 2012 51

Gazprom Neft - Investor Day 2012

Contacts for investors

Department of Corporate Finance

Investor Relations

Tel: (007) (812) 385-9548

Alexey Kokorev

Head of Corporate Finance Department

Phone: (007) (812) 648-3117

E-mail: [email protected]

Anna Sidorkina

Head of Investor Relations

Phone: (007) (812) 385-9548

E-mail: [email protected]

Investor Day 2012 52

Gazprom Energoholding

Part 5. Denis Fedorov

Head of Gazprom Directorate for Development of Power Generation Sector and

Power Generation Marketing, General Director of Gazprom Energoholding

Investor Day 2012 53

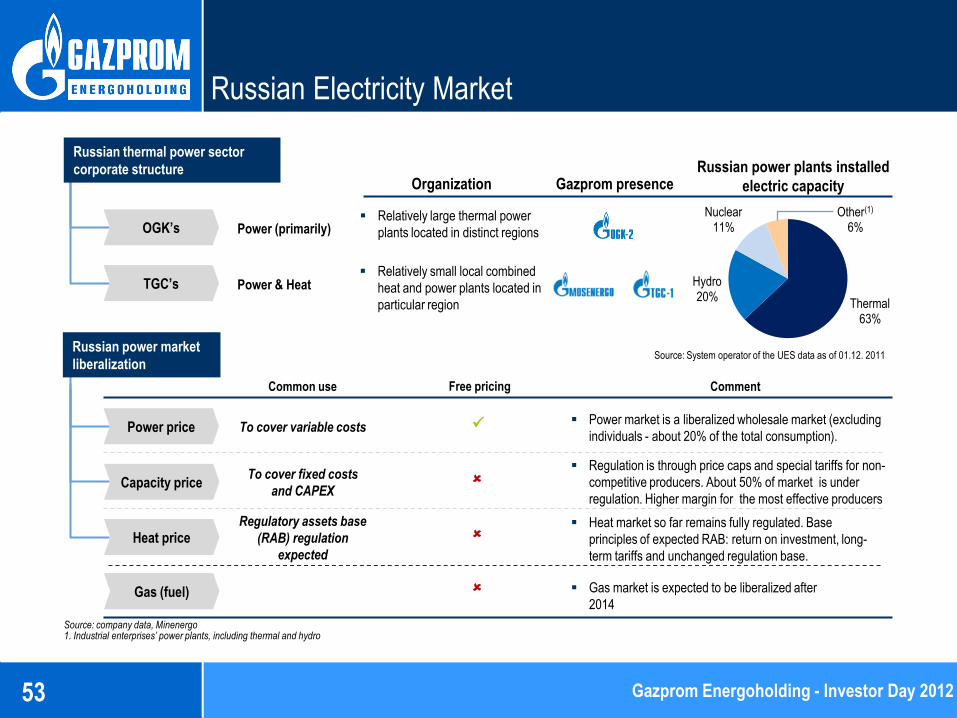

Russian Electricity Market

Gazprom presence Organization

OGK’s

TGC’s

Russian thermal power sector

corporate structure

Power & Heat

Power (primarily)

Russian power plants installed

electric capacity

Source: System operator of the UES data as of 01.12. 2011

Source: company data, Minenergo 1. Industrial enterprises’ power plants, including thermal and hydro

Relatively small local combined

heat and power plants located in

particular region

Relatively large thermal power

plants located in distinct regions

To cover variable costs

Capacity price

Heat price

Free pricing

Comment

Power price

Regulation is through price caps and special tariffs for non-

competitive producers. About 50% of market is under

regulation. Higher margin for the most effective producers

Power market is a liberalized wholesale market (excluding

individuals - about 20% of the total consumption).

Heat market so far remains fully regulated. Base

principles of expected RAB: return on investment, long-

term tariffs and unchanged regulation base.

Gas (fuel) Gas market is expected to be liberalized after

2014

Common use

To cover fixed costs

and CAPEX

Regulatory assets base

(RAB) regulation

expected

Russian power market

liberalization

Gazprom Energoholding - Investor Day 2012

Thermal 63%

Hydro 20%

Nuclear 11%

Other(1) 6%

Investor Day 2012 54

St. Petersburg

Moscow

Krasnoyarsk

Surgut

Installed electric capacity 37.0 GW

Installed heat capacity 54.015 GCal/h

Installed electric capacity 12.3 GW

Installed heat capacity 35.083 GCal/h

Market capitalization USD 2.5 bln(2)

53.5%

Installed electric capacity 6.8 GW

Installed heat capacity 14.616 GCal/h

Market capitalization USD 1.2 bln(2)

51.8%

Installed electric capacity 17.9 GW

Installed heat capacity 4.316 GCal/h

Market capitalization USD 1.6 bln(3)

57.6% (1)

GEH fuel mix

Key Assets Overview

Gazprom Energoholding - Investor Day 2012

Gas

88%

Coal

11%

Oil-fuel

1%

1. Since OGK-2 and OGK-6 merged at November 1st, 2011 2. As of 01.02.2012 3. As of 01.02.2012 (Includes the additional issue (1-02-65105-D-004D), traded since 22.12.2011)

Gazprom Energoholding is a leading power and heat generator in Russia operating through the wholesale market

Investor Day 2012 55

Other 83% Other 92%

Leading Positions in Electricity and Heat Generation

Installed capacity 2011E, GW Heat capacity 2011E, Gcal/h ths

Source: company data

Electricity generation, 2011E Heat generation, 2011E

Source: companies’ data as of 31.12.2011

172.7 bln

kWh (Е)

17%

98.8 mm

Gcal

8%

Gazprom Energoholding - Investor Day 2012

37 35 29

24 20

16 10 9

Rus

Hyd

ro

Inte

r R

AO

Ros

atom

Eur

oSib

Ene

rgo

IES

Hol

ding

E.O

N

Ene

l

67

54

21 16 16 14 10

IES

Hol

ding

GE

H

Inte

r R

AO

SU

EK

Qua

dra

LUK

OIL

FO

RT

UM

Investor Day 2012 56

15

Electricity consumption

Cooperation of Gas and Electricity Business

Gazprom share(1) of total electricity consumption in

Russia, 2010

GEH share in total gas consumption by Russia power

plants, 2010 15 bln kWh

Source: Rosstat, company data 1. Energy consumption of key Gazprom subsidiaries operating in gas extraction, transportation, storage and refining businesses

Source: company data

Product

cooperation

Project

cooperation

Strategy

cooperation

Electricity supply for Gazprom investment projects

Gazprom

investment projects

Gazprom power sector

investment project

Shtokman field

development Power plant in Teriberka

Astrakhan gas refinery

reconstruction Astrakhan TPP

North-East

Asia

Europe

Cooperation in possible geographic expansion

Gazprom Energoholding - Investor Day 2012

29% Other 71%

2% Other 98%

Investor Day 2012 57

65.4 69.9 66.4

26.9 28.8 26.1

6.8 6.7 6.3

2009 2010 2011E 2009 2010 2011E 2009 2010 2011E

61.7 65.0 64.6

26.8 27.2 28.4

76.1 82.5 79.7

2009 2010 2011E 2009 2010 2011E 2009 2010 2011E

Operating Results

Electricity

Generation,

kWh bln

Heat

Generation,

Gcal mm

+5.3% -0.6%

+1.5% +4.4%

+8.4% -3.4%

+6.9% -5.0%

+7.1% -9.4%

-1.5% -6.0%

+6.1% -1.1%

+6.4% -6.3%

(¹)

Source: company data 1. Management reporting data. 12m2011 of consolidated OGK-2 and 10m2011 of OGK-6 included

Gazprom Energoholding - Investor Day 2012

2009 2010 2011E

2009 2010 2011E

105.4 99.1 98.8

174.7 164.6 172.7

Investor Day 2012 58

12.4

17.2 14.9

2009 2010 2011E

4.5

7.6

10.4

3.4 3.6 3.6 4.5 6.0

0.9(2)

2009 2010 2011E 2009 2010 2011E 2009 2010 2011E

17.8 21.0

24.6

7.9 9.3 9.4 8.7 10.8

5.3

2009 2010 2011E 2009 2010 2011E 2009 2010 2011E

112.2 143.8 160.8

38.4 50.6 57.7 82.6

103.9 105.0

2009 2010 2011E 2009 2010 2011E 2009 2010 2011E 2009 2010 2011E

34.4 41.1 39.3

2009 2010 2011E

Financial Results (RAS)

Sales,

RR bln

EBITDA,

RR bln

+28.2% +11.8%

+31.8% +14.0%

+25.8% +1.1%

+27.9% +8.4%

+18.0% +17.1%

+17.7% +1.1% +24.1% -50.9%

-4.4% +19.5%

Source: company data 1. Management reporting data. 12m2011 of consolidated OGK-2 and 10m2011 of OGK-6 included 2. Management reporting data: OGK-2 expects RR 1,138 mm consolidated net profit for 2011. Net loss of OGK-6 is expected at the amount RR 293 mm for 10 month 2011

Gazprom Energoholding - Investor Day 2012

298.3

233.2

323.5

(¹)

Net Profit,

RUR bln

+68.9% +36.8%

+5.9% 0%

+33.3% -85.0% -13.4%

+38.7%

Investor Day 2012 59

Key Investment Projects

Innovative projects (CSA included)

Key projects, 2012-2014

Serovskaya GRES

(OGK-2) 420 MW

Troitskaya GRES

(OGK-2) 660 MW

Stavropolskaya GRES

(OGK-2)

420 MW

Cherepovetskaya

GRES

(OGK-2)

420 MW

TPP-16

(Mosenergo) 420 MW

TPP-20

(Mosenergo) 420 MW

TPP-12

(Mosenergo) 220 MW

Central TPP

(TGC-1)

100 MW

Novocherkasskaya

GRES (OGK-2) 330 MW

800MW combined cycle gas turbine power

facility based on existing steam turbine using

modern Siemens gas-turbine power unit

Novocherkasskaya GRES (OGK-2)

First Russian 330 MW modern

power facility with circulating boiling

layer equipment

Kirishskaya GRES (OGK-2)

Key projects, 2010-2011

Ryazanskaya GRES

(OGK-2) 420 MW

Yuzhnaya TPP-22

(TGC-1) 450 MW

TPP-26 (Mosenergo) 420 MW

Pervomayskaya TPP-14

(TGC-1) 180 MW

Kirishskaya GRES

(OGK-2) 800 MW

Investment program status

Total investment

Program 9 GW

42.2%

Adlerskaya TPP

(OGK-2) 360 MW

51(1)

48(1)

11m 2011 2012E

RR bln

Source: company data, media 1. Net of Adlerskaya TPP investments

Gazprom Energoholding - Investor Day 2012

Commissioned

capacity 3.8 GW

Investor Day 2012 60

Completion of the OGK2 and OGK6 Merger: Creation of a Leading Thermal Generation Company

Installed capacity

8.7 GW Installed capacity

9.2 GW

Synergy effect

Creation of a leading heat generating

company in Russia

Total installed capacity 17.9 GW.

Consolidated revenue in 2011 is expected to exceed RR 100 bln

Efficiency increase in electricity production and sales Electricity production in 2011 is estimated at 79.7 bln KW∙h

Centralized procurement and optimization

of management structure

‘Scale effect’ implementation in the process of operating and management costs decrease

Optimization of investment

program funding

Investment program is over 4 GW, guaranteed by Capacity Supply

Agreements. Investment Program equals to RR 165 bln

Potential merger synergies are expected to be at RR 7.8 bln in 2011-2015

Total installed

capacity

17.9 GW +

Gazprom Energoholding - Investor Day 2012

Investor Day 2012 61

Value Drivers Summary

Capacity supply agreements

Prices growth potential

Gazprom Energoholding investment program

Current market undervaluation

Efficiency increase

Gazprom Energoholding - Investor Day 2012

The undervaluation, completed investment projects and expected price trends provide solid upside relative to

Gazprom Energoholding’s current valuation

Investor Day 2012 62

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

150%

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Value Drivers [1/5]: Undervaluation due to Current Market Uncertainty

Multiples

Developed markets(1)

Russian market(2)

Gazprom Energoholding

Government opposes

the sector reformations

The sector’s reformations get

government support

Chubais declares

the intention to

leave the sector Tariffs curb declared

by the government

Market liberalization is

supported

Potential

industry

upside

Source: Bloomberg, JP Morgan Cazenove 1. European top-5 multiples average 2. Average Russian power generation sector multiples

Relative dynamics of MICEX Power Index versus MICEX Index

EV/Sales 0.9x

0.7x

0.5x

EV/IC 1.1x

>0.2x

<0.2x

Gazprom Energoholding - Investor Day 2012

Investor Day 2012 63

Mcap - 5.3

12.1 Net debt - 1.3

6.7

1.7

3.7

Current EV Old capacity valuation Capacity under construction New installed capacity Total

Value Drivers [2/5]: Undervaluation of Significant Progress in Investment Program Completion

Source: company data 1. According to construction costs of USD 1,100/kW for gas consuming capacities and USD 1,800/kW for coal consuming 2. Valuation according USD 200/kW EV/IC multiple which is consistent with 4.0x EV/EBITDA for Russian energy sector

Costs based valuation shows upside

1.8x

USD bln

Gazprom Energoholding - Investor Day 2012

According to current investments, the company’s existing capacity is priced too low which implies solid

potential for unlocking the company’s value

(2) (1)

Investor Day 2012 64

120(2)

440(2)

Regular capacity New capactiy under capacity supply agreements

491

661

Spark spread: old power plants Spark spread: power plants with new blocks

Value Drivers [3/5]: Capacity Supply Agreements

Over 95% of the investment program is associated with Capacity Supply Agreements program, assuming increased

tariffs after power plants commissioning, which provides basis for increasing the company’s value

Increased new capacity profitability

+35%

Increased price for new capacity

RR/ KW month

3.6x price

increase for

CSA capacities

Source: company data and analysis

RR/ KW year

Source: company data and analysis 1. Spark spread = revenue from electricity sales per 1 KW – fuel expense per 1 KW 2. Average price for Mosenergo, TGC-1 and OGK-2 in 2011

Gazprom Energoholding - Investor Day 2012

Russia existing

capacity average

price

(1) (1)

Investor Day 2012 65

2.9%

3.0%

4.3%

5.7%

5.9%

70 - 80

93

108

128

138

140

152

153

165

190

Russia

France

Sweden

Portugal

Poland

UK

Austria

Spain

Germany

Italy

Value Drivers [4/5]: Expected Price Growth

Electricity prices for industrial consumers Margins: Gazprom Energoholding vs. European Top-5

USD/MWh Net income margin(1)

USD 141

Source: European Energy Portal, Russian Energy Trade System Administrator, company data and analysis 1. IFRS data

Source: Bloomberg, company data

Expected price growth

will likely add up to

Gazprom

Energoholding’s

margins

Gazprom Energoholding - Investor Day 2012

Russian industrial

electricity price is

43% below

European average

Russian electricity prices are >40% below European averages which implies further growth potential through gradual

increase in coal and gas prices

Given existing prices Gazprom Energoholding operates with margins which are in line with the top European peers

Investor Day 2012 66

Value Drivers [5/5]: Efficiency Increase

I. Expected efficiency increase

for new capacity

II. Heat sales III. Operating expenses

optimization

Moscow Government

negotiations for load

capacities optimization and

optimization of heat

transmission

Development of Advanced

Health Safety Environment

System (HSE)

Further optimization

Consolidation of heat

network of Saint Petersburg

and heat load capacities

optimization

Hydro power assets utilization

Increase efficiency of variable

cost

Interest payments economy

Synergy effect of consolidation

OGK-2 and OGK-6

Development infrastructure for

different coal-type acceptance

<not applicable>

Fuel consumption, gfe/kW

Fuel consumption, gfe/kW

Fuel consumption, gfe/kW

1. Indicative estimate of yearly economy on fuel consumption decrease on new blocks assuming 74% capacity load for new capacities and following 3% capacity price decrease

Gazprom Energoholding - Investor Day 2012

265 219

896

Old capacity New blocks Effect , RR mm

341 245

1,127

Old capacity New blocks Effect , RR mm

368 322

621

Old capacity New blocks Effect , RR mm

(1)

(1)

(1)

Focus on increasing operational efficiency, which is expected to save over RR2.6bln annually after 2012

provides an additional value driver

Investor Day 2012 67

7.1 39.0

Current EV Potential EV

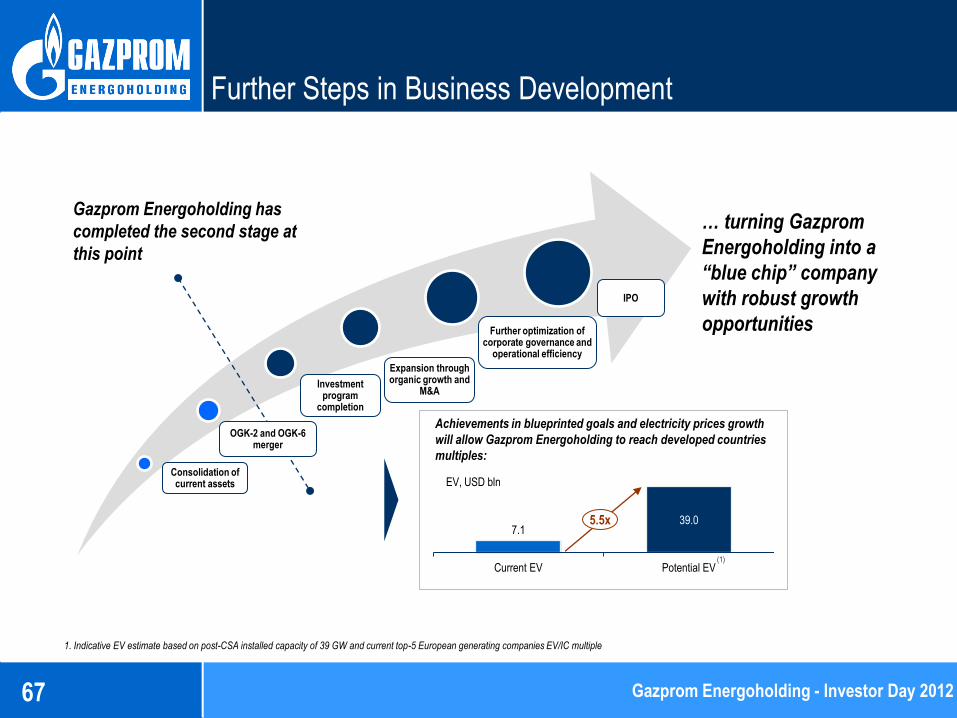

Further Steps in Business Development

Consolidation of current assets

Investment program

completion

Expansion through organic growth and

M&A

Gazprom Energoholding has

completed the second stage at

this point

IPO

OGK-2 and OGK-6 merger

Achievements in blueprinted goals and electricity prices growth

will allow Gazprom Energoholding to reach developed countries

multiples:

5.5x

1. Indicative EV estimate based on post-CSA installed capacity of 39 GW and current top-5 European generating companies EV/IC multiple

EV, USD bln

… turning Gazprom

Energoholding into a

“blue chip” company

with robust growth

opportunities Further optimization of corporate governance and

operational efficiency

Gazprom Energoholding - Investor Day 2012

(1)

Investor Day 2012 68

Contacts for investors

Gazprom Energoholding

Investor Relations

Tel: (007) (495) 428 47 83

Sergey Fil

Director of Corporate and Legal Development Gazprom Energoholing

Phone: (007) (495) 428 47 83 (ext.: 46-32)

E-mail: [email protected]

Ekaterina Pavlova

Head of IR Gazprom Energoholding

Phone: (007) (495) 428 47 83 (ext.: 46-07)

E-mail: [email protected]

Gazprom Energoholding - Investor Day 2012