SATS and Life Cycle Cost Research, 1999-2004

Robert N. McGrath, Ph.D.Embry-Riddle Aeronautical

UniversityDaytona Beach, Florida

Presentation Agenda SATS Background Baseline Study Interim Studies Latest Study Conclusion

NASA’s Premise

“One of the most significant emergent forces in the first decade of the 21st century will be the value of human time … human/intellectual capital [will replace] physical capital as the basis for the creation of wealth.”

NASA (continued)

“… significant advancement in doorstop-to-destination speed … is possible, if the challenges can be met for making small aircraft and airports more available to the traveling public … enabling technologies include a new generation of engines, avionics, airframe, navigation, communication and operator training.”

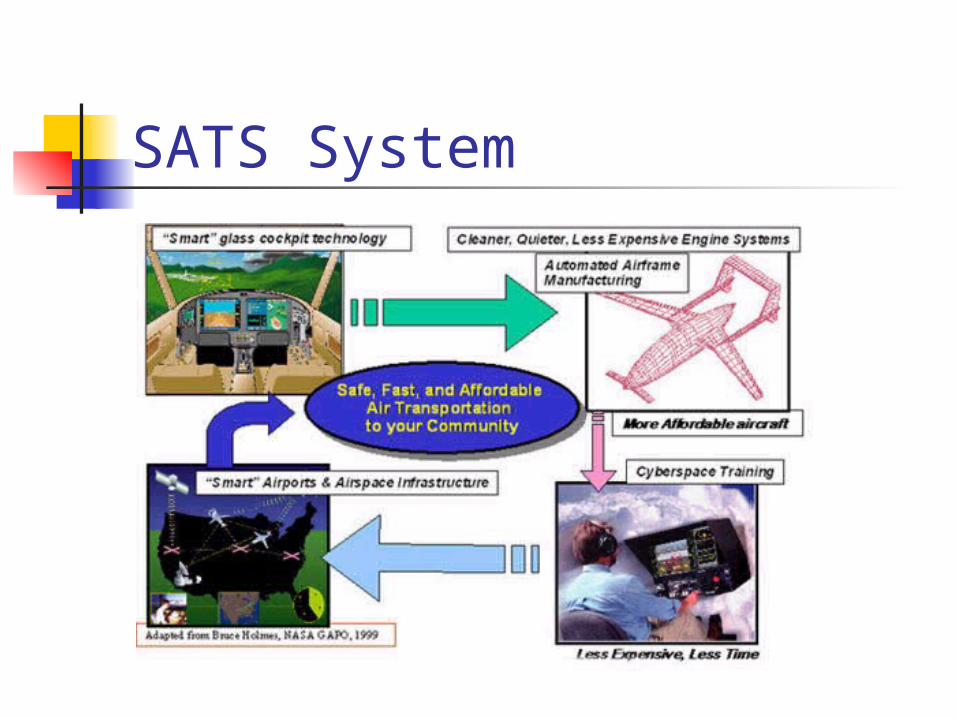

SATS

Small Airplane Transportation System Airplane-based personal transportation Ultimate vision: substitute for autos Near term: industrial / govt. niches NASA+industry+academia+public sector

SATS System

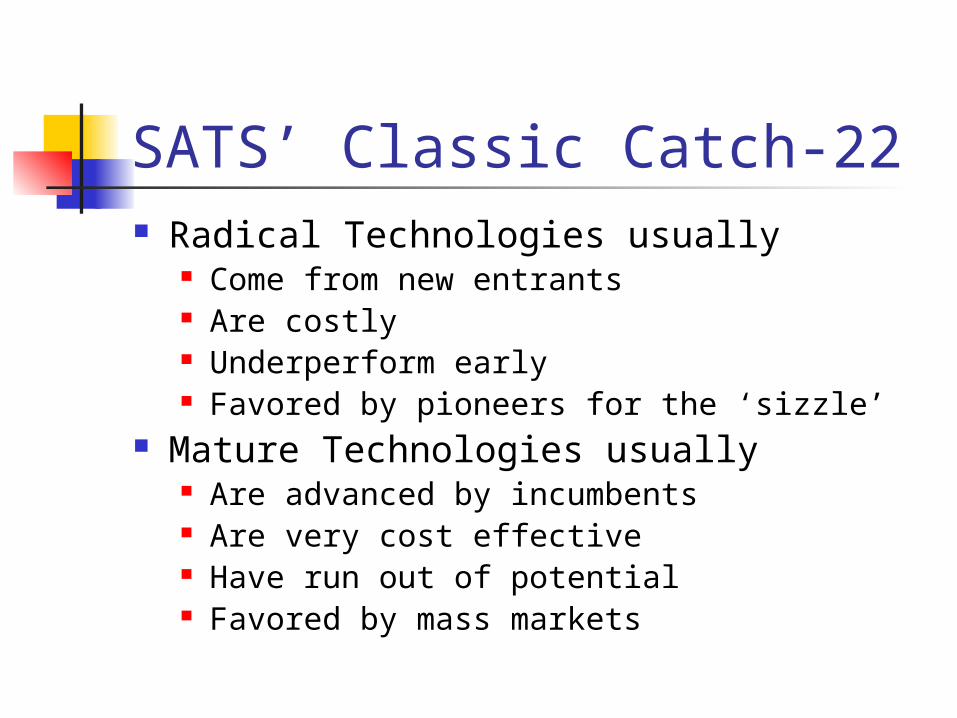

SATS’ Classic Catch-22 Radical Technologies usually

Come from new entrants Are costly Underperform early Favored by pioneers for the ‘sizzle’

Mature Technologies usually Are advanced by incumbents Are very cost effective Have run out of potential Favored by mass markets

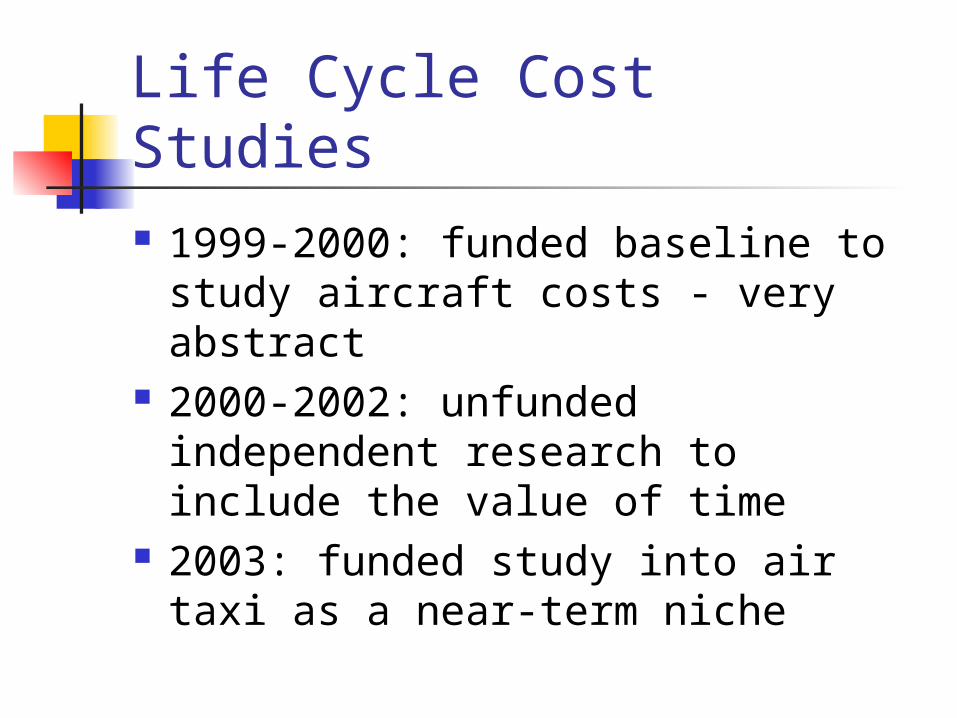

Life Cycle Cost Studies 1999-2000: funded baseline to

study aircraft costs - very abstract 2000-2002: unfunded independent

research to include the value of time

2003: funded study into air taxi as a near-term niche

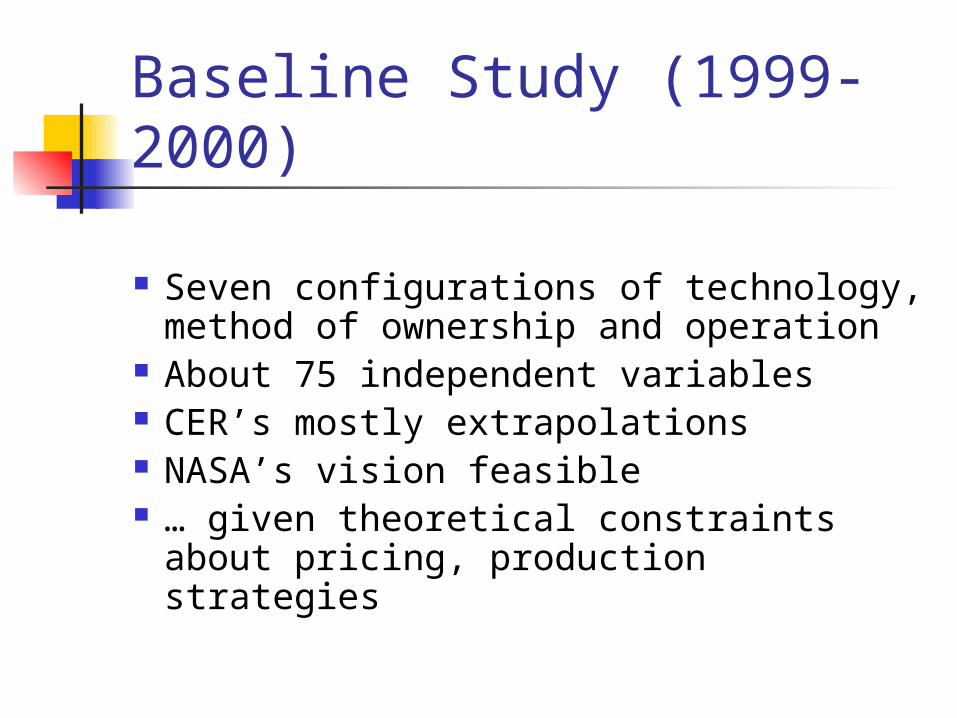

Baseline Study (1999-2000)

Seven configurations of technology, method of ownership and operation

About 75 independent variables CER’s mostly extrapolations NASA’s vision feasible … given theoretical constraints

about pricing, production strategies

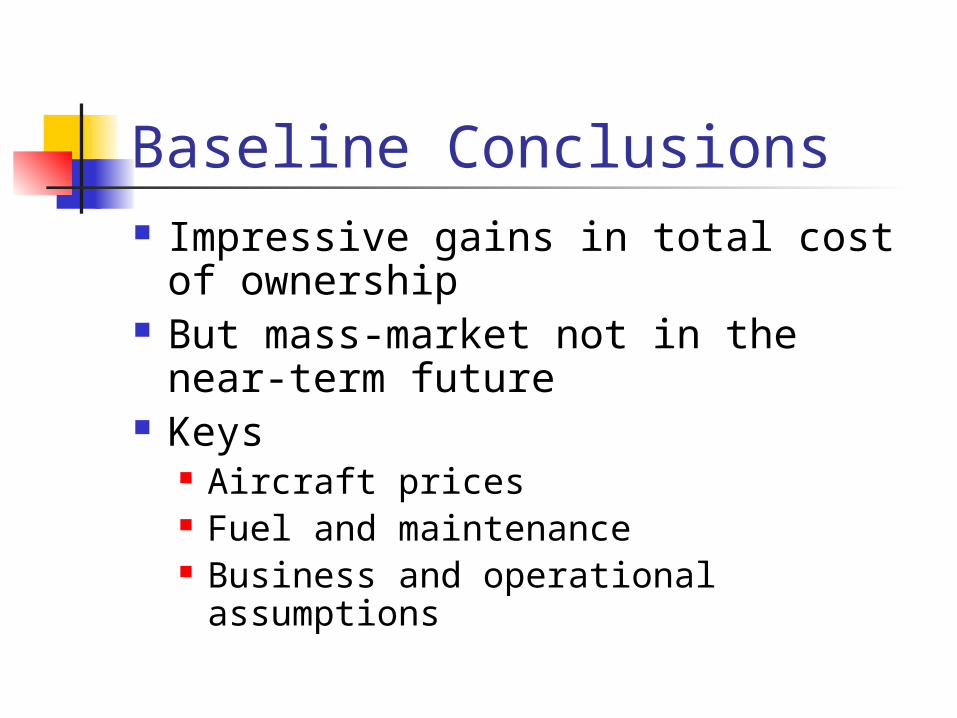

Baseline Conclusions Impressive gains in total cost of

ownership But mass-market not in the near-

term future Keys

Aircraft prices Fuel and maintenance Business and operational assumptions

Interim Independent Studies

… what about ‘time?’ Used the original model as baseline Modified to include value of time

and compare SATS Bizjets to executive travel on airlines

Modified to include value of time and compare autos and SATS Bizjets

What is the Value of Time?

Extant research nonexistent Employee time assumed in Bizjets Aircraft modeled in Travel$ense Samples of city pairs capturing

likely trip ranges Various levels of cost

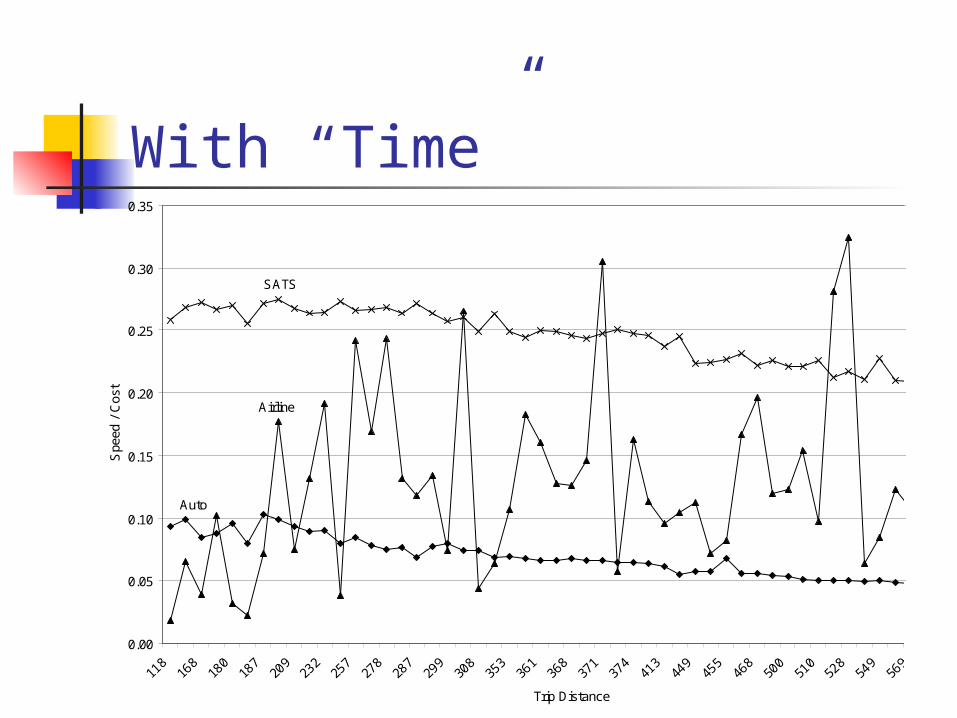

Interim Conclusions Without considering the value of

time SATS often appeared competitive in

some costs When considering the value of

time SATS often appeared superior in

many costs by wide margins

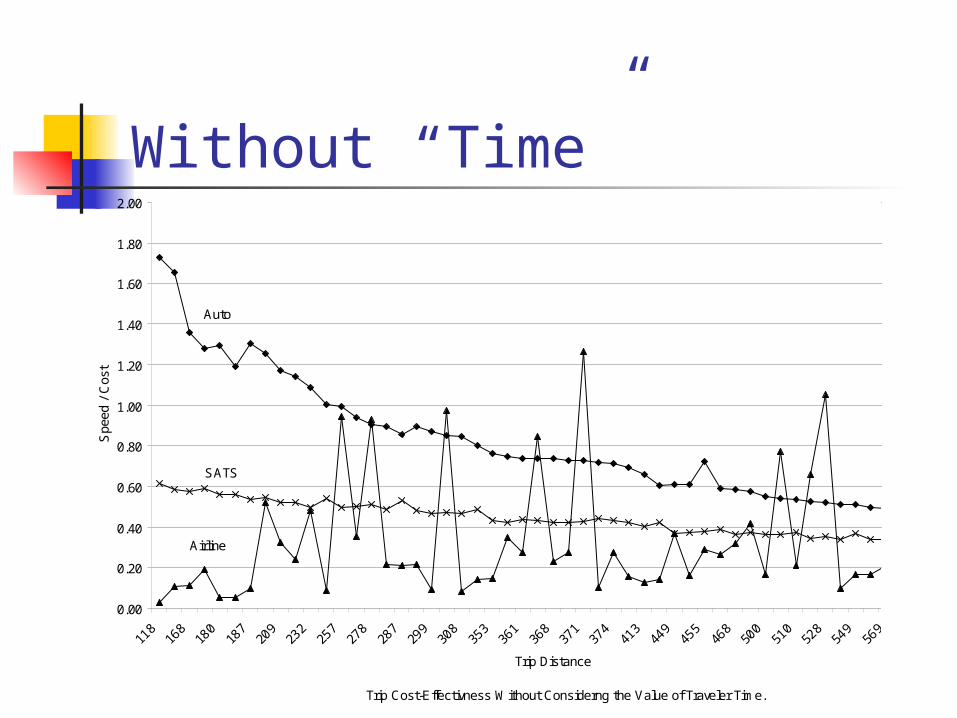

Without “Time”

Trip Cost-Effectivness Without Considerng the Value of Traveler Time.

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

118

168

180

187

209

232

257

278

287

299

308

353

361

368

371

374

413

449

455

468

500

510

528

549

569

Trip Distance

Spe

ed /

Cos

t

Auto

SATS

Airline

With “Time”

Trip Cost-Effectiveness Considering the Value of Traveler Time.

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

118

168

180

187

209

232

257

278

287

299

308

353

361

368

371

374

413

449

455

468

500

510

528

549

569

Trip Distance

Spe

ed /

Cos

t

SATS

Airline

Auto

The 2003 Study

One of several “business case” studies Not macro/market/economic … … Focused on an air taxi business Compared an entrepreneur’s choice of

Beech Bonanza 33 (4 seats) Beech King Air 200 (8 seats) Eclipse 500 (6 seats)

Beech Bonanza 33Eclipse

Bonanza

Beech King Air

Eclipse 500

The 2003 Study (continued)

Hypothetical Air Taxi Enterprise Today’s “rules of the game” Minimal “SATS” infrastructure Two strategic objectives

Low overhead / organizational infrastructure Operating capacity large enough to exploit

possible economies of scale … 10 a/c, 6 flights/day, 10 year life cycle

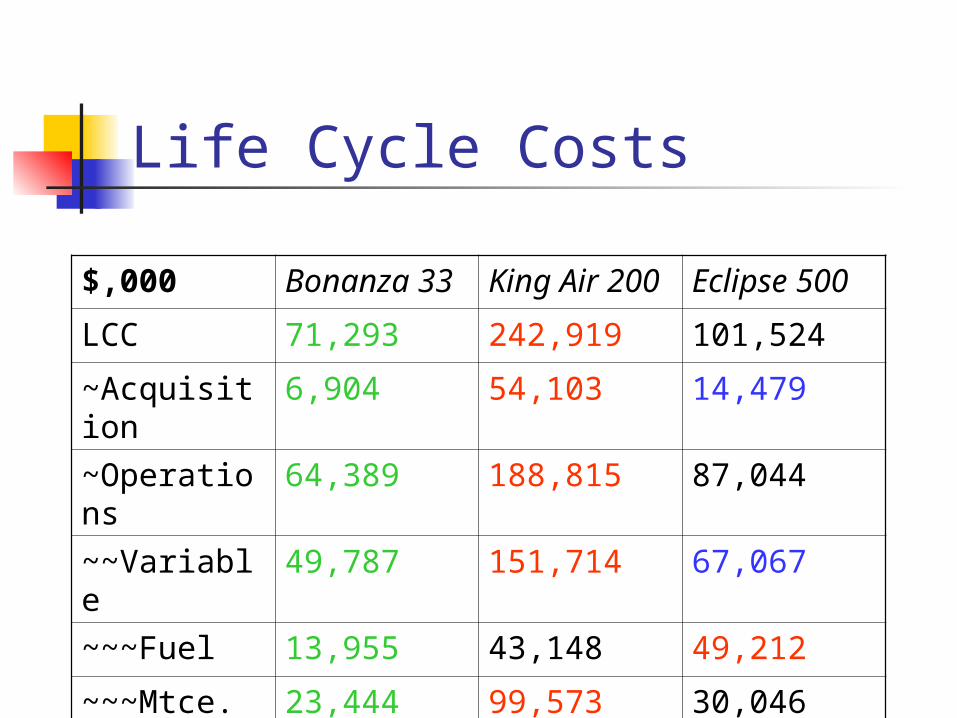

Life Cycle Costs

$,000 Bonanza 33

King Air 200

Eclipse 500

LCC 71,293 242,919 101,524

~Acquisition

6,904 54,103 14,479

~Operations

64,389 188,815 87,044

~~Variable

49,787 151,714 67,067

~~~Fuel 13,955 43,148 49,212

~~~Mtce. 23,444 99,573 30,046

Cost-Effectiveness Analysis

Three measures Cost per Mile Cost per Seat Mile Cost per Hour

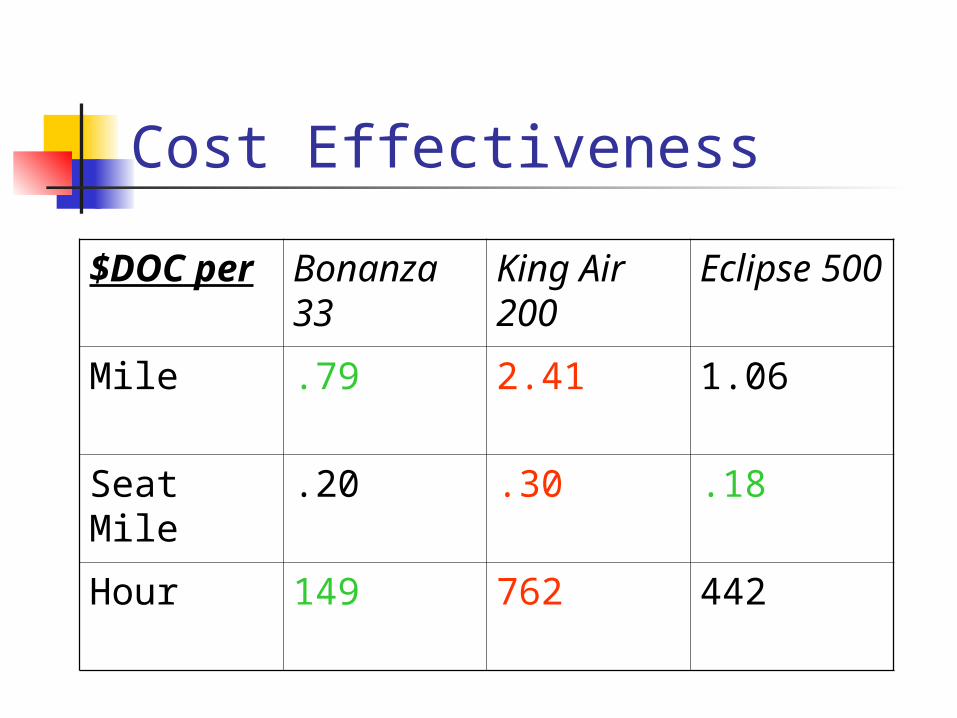

Cost Effectiveness

$DOC per

Bonanza 33

King Air 200

Eclipse 500

Mile .79 2.41 1.06

Seat Mile .20 .30 .18

Hour 149 762 442

Cost Effectiveness (continued)

Load factors affect business viability of a/c

In the enterprise, the market was assumed constant …

… i.e., regardless of a/c chosen, the same # of passengers would board

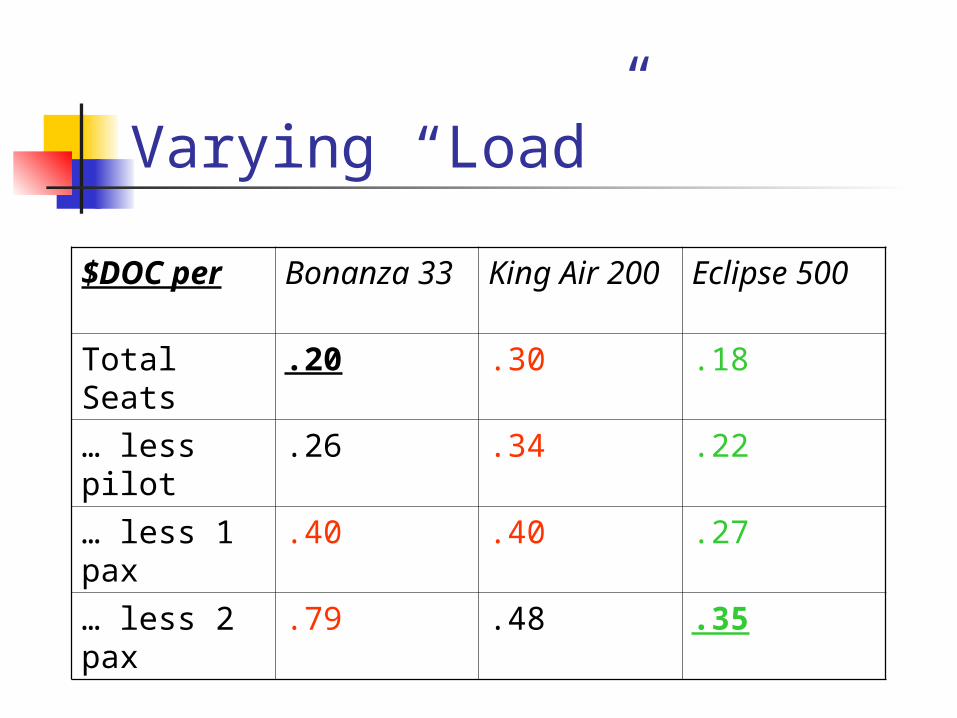

Varying “Load”

$DOC per Bonanza 33

King Air 200

Eclipse 500

Total Seats .20 .30 .18

… less pilot .26 .34 .22

… less 1 pax

.40 .40 .27

… less 2 pax

.79 .48 .35

Load Factor C-E Summary

Extraordinary degradation as passengers removed

The fewer the total seats, the greater the effect

Eclipse emerged as the best, Bonanza and King Air became comparable

Many “mental experiments” can change conclusions

Sensitivity Analysis

Above pointed to uncertainty/risk in: price fuel maintenance capacity utilization (or scale

economy)

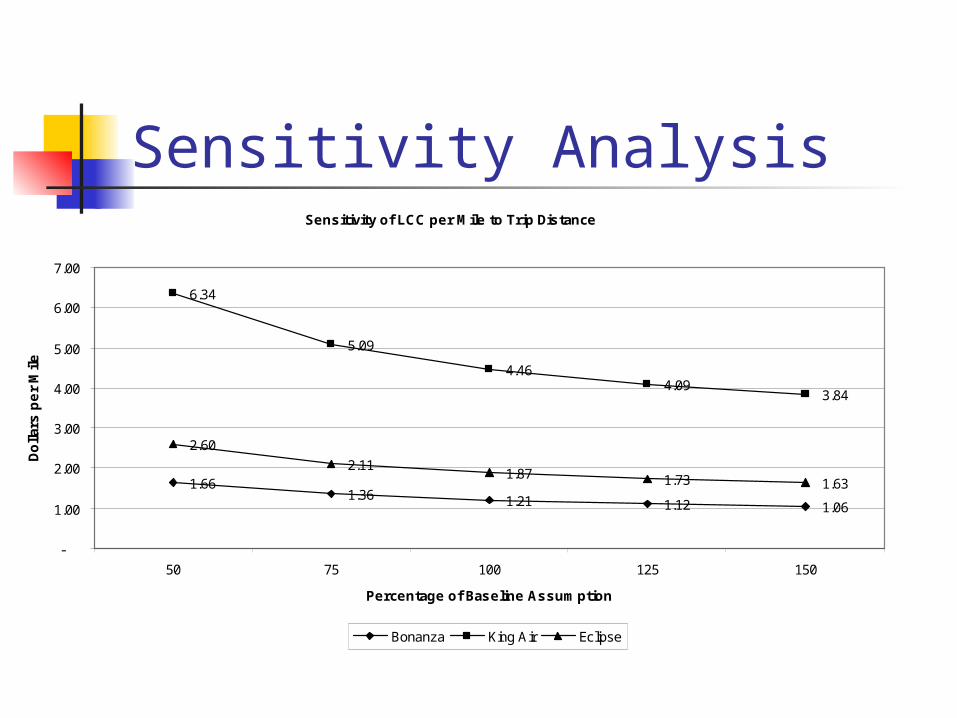

Sensitivity AnalysisSensitivity of LCC per Mile to Trip Distance

1.661.36 1.21 1.12 1.06

6.34

5.09

4.464.09

3.84

2.60

2.111.87 1.73 1.63

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

50 75 100 125 150

Percentage of Baseline Assumption

Do

llars

pe

r M

ile

Bonanza King Air Eclipse

Air Taxi and SATS

Technology must be aligned with capacity must be aligned with market share

Business innovations (models) are needed as well as technological and marketing innovation

Conclusion

Markets, technologies, etc. will show dynamic and recursive cause and effect

SATS is proceeding in ways that business theory explains well …

Models of technology / industry cycles are robust