Patients First, Partners Always

SAMHS eMSM Update 1 Nov 2015

Damon G. Baine

Colonel, USA, MS Chief Operating Officer, SAMHS eMSM

Patients First, Partners Always Patients First, Partners Always

Agenda

• Review of eMSM CONOPS and Governance SAMHS Update – Business Plan – SAMHS Performance Examples – eMSM “Victories”

• Common eMSM Challenges • Key eMSM Executive Skills

Patients First, Partners Always Patients First, Partners Always

MHS Governance Reform Journey

3

DoD Task Force on MHS Governance

September 2011

18th study over 62 years 7th rec “added central

authority” DHA model for MHS

governance

DepSecDef Planning Memo

March 2012

Directed I-Planning for MHS Governance Reform— OASD(HA) DHA Shared Services JTF-CapMed transition eMSMs

DepSecDef “Nine Commandments” Memo

March 2013

Directed implementation of MHS Governance Reform— OASD(HA) & TMA

transition DHA (as CSA) Shared Services NCR Directorate eMSMs

Historical MHS Governance Studies

17 studies over 57 years 8 recs for unified

service/unified joint command 6 recs for added central

authority 3 recs “keep separate

Service lines

1949 - 2006

Patients First, Partners Always Patients First, Partners Always

Evolution to the SAMHS eMSM

4

MSMO

2004

Multi-Service Market Offices established Support new TRICARE

Managed Care Support Contracts

BRAC Law

2005-2007

Mandated several changes Relocated inpatient

medical functions from WHMC to BAMC Transitioned WHMC to

WHASC

Joint Military Medical Command

Execution challenges Many victories: Integrated GME programs

through SAUSHEC STRAC

1987-1991

SAMHS and SAMHS eMSMs

2011 - 2013

2011: SAMHS established by MOA signed by Army and Air Force Chiefs of Staff 2013: DepSecDef memo

established eMSMs—empowered with new authorities

5

Patients First, Partners Always Patients First, Partners Always

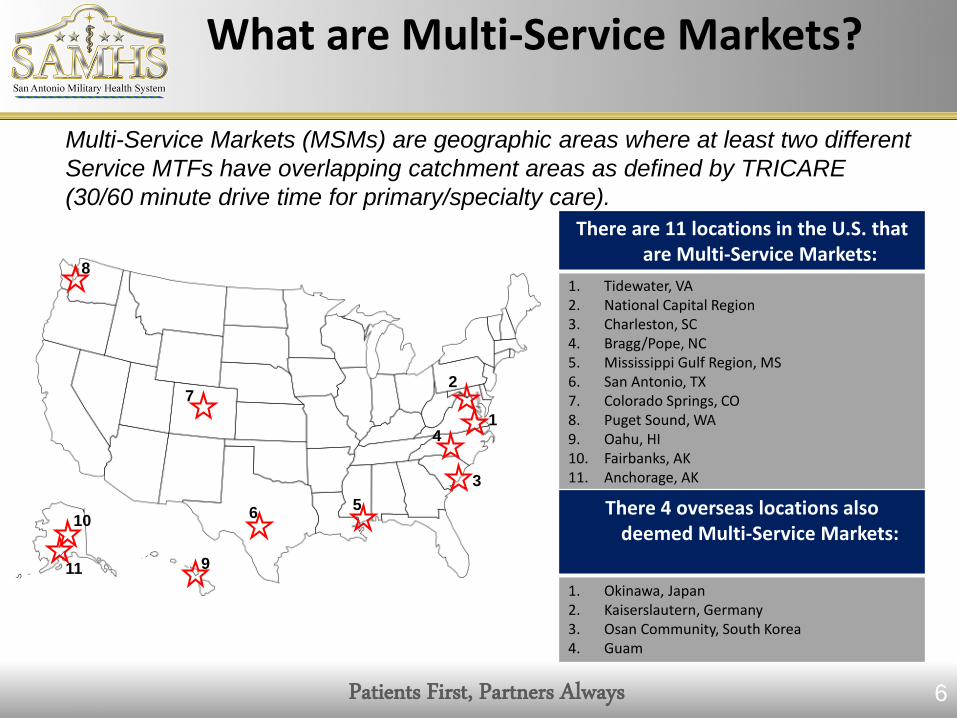

What are Multi-Service Markets?

Multi-Service Markets (MSMs) are geographic areas where at least two different Service MTFs have overlapping catchment areas as defined by TRICARE (30/60 minute drive time for primary/specialty care).

There are 11 locations in the U.S. that are Multi-Service Markets:

1. Tidewater, VA 2. National Capital Region 3. Charleston, SC 4. Bragg/Pope, NC 5. Mississippi Gulf Region, MS 6. San Antonio, TX 7. Colorado Springs, CO 8. Puget Sound, WA 9. Oahu, HI 10. Fairbanks, AK 11. Anchorage, AK

There 4 overseas locations also deemed Multi-Service Markets:

1. Okinawa, Japan 2. Kaiserslautern, Germany 3. Osan Community, South Korea 4. Guam

1

2

3

4

5 6

7

8

9

10

11

6

Patients First, Partners Always Patients First, Partners Always

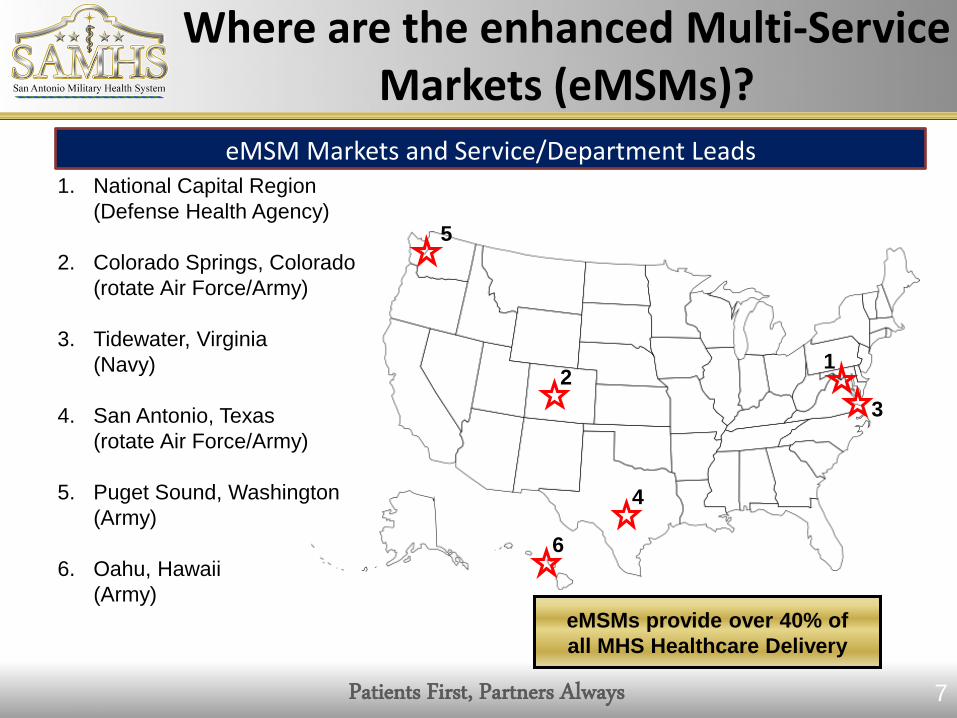

Where are the enhanced Multi-Service Markets (eMSMs)?

eMSM Markets and Service/Department Leads 1. National Capital Region (Defense Health Agency) 2. Colorado Springs, Colorado (rotate Air Force/Army) 3. Tidewater, Virginia (Navy) 4. San Antonio, Texas (rotate Air Force/Army) 5. Puget Sound, Washington (Army) 6. Oahu, Hawaii (Army)

5

2 1

3

4

6

7

eMSMs provide over 40% of all MHS Healthcare Delivery

Patients First, Partners Always Patients First, Partners Always

What is “Enhanced”?

8

No easy task to evolve legacy processes

Single Market Manager Within each eMSM, an appointed market manager has the authority to:

• Manage the allocation of the budget for the market

• Direct common clinical and business functions for the market

• Direct the movement of workload and workforce among the medical treatment facilities

• Develop, execute and monitor the business performance plan

Single Market Plan Within each eMSM, 5-year Business Performance Plans will be: •Fully-integrated across the entire market and will replace current MTF based business plans •Based on a 5-year planning cycle, as opposed to the current 3-year plan •Aligned with budget execution process to ensure continuity

Patients First, Partners Always Patients First, Partners Always

eMSM Concept of Operations

9

Relationships are still evolving

eMSM office sets Business Performance Plan objectives and submission--seeks out opportunities to improve all facets of healthcare delivery while reducing costs.

Market components work with eMSM office to assist in Business Performance Plan execution. Disconnects resolved locally or at MDAG.

MDAG

eMSM Office

MTFs eMSM Partners (Services)

MDAG provides authority to eMSM office to investigate, analyze, and initiate changes across the market.

MTFs provide feedback to eMSM office on what works and what does not—collaborative approach is critical to success.

Patients First, Partners Always

Senior Market Manager

Director

Admin/ITSupport

Directorate ofClinical Operations

Appointing andReferral

Management

Direct CareOptimization/

Capability

Population Health

Case & DiseaseManagement

Readiness

Health Education & Training Ancillary Services

Directorate ofMarket Analysis & Evaluation

MarketPerformancePlanning &Reporting

Data Analysis &Program

Evaluation

Business ProcessReengineering

Directorate ofBusiness Operations

Manpower &Budget

Management

MCSC Operations/Recapture

Management

EmergencyResponse Planning

MOUs/MOAs/Contracting &

Venture Capital

IM/IT Telehealth

FederalPartnerships/Community

Relations

Market BusinessWorkloadReporting/Enrollment

Strategic Communications/

PatientSatisfaction

** Central CLRProcessing

** Central

Appointing** Expanded Functions

eMSM Functional Organizational Structure

Clinical Standardization

Quality Management

Risk Management

Patient Safety

Research

Logistics

Strategic Planning

Reference eMSM CONOPS Organizational Structure

10

Womack AMC

MDAG

Services DHA

ASD(HA)

MOG/MBOG/ MPOG/SAG

eMSM LG

eMSMs

NCR Dir

eMSM

CO

NO

PS eM

SM CO

NO

PS

eMSM MTFs

DepSecDef Memo

DepSecDef Memo

ADCON

OPCON TACON

OPCON TACON

OPCON TACON

NMC San Diego

Tidewater

Puget Sound

San Antonio

Colorado Springs

Hawai’i

As developed and inferred from: • Deputy Secretary of Defense Memorandum, Implementation of Military Health System Governance Reform, 11 Mar 13 • Enhanced Multi-Service Market Concept of Operations, 11 Mar 14 • Includes eMSMs “+2” of Naval Medical Center San Diego and Womack Army Medical Center

Patients First, Partners Always Patients First, Partners Always

eMSM Governance Structure

Senior Leader Council

BAMC Commander COL Renz

Other Army Clinics

SAMMC DCCS Col

Pendergrass

WHASC CD COL Ekstrand

Other Air Force Clinics

Clinical Operations

Col Lloyd

Business Operations LTC DeVries

Board of Directors

Chief Operating Officer COL Baine

SAMHS Maj Gen Iddins – MM

BG Holcomb– Vice MM

59th MDW Commander Maj Gen Iddins

Chief Nurse Executive Col Foulk

Allied Health COL Fryar

eMSM Business Planning

eMSM Analytics

Sr Enlisted Liaison SGM Adams

Patients First, Partners Always Patients First, Partners Always

MTF Footprint

13

Patients First, Partners Always Patients First, Partners Always

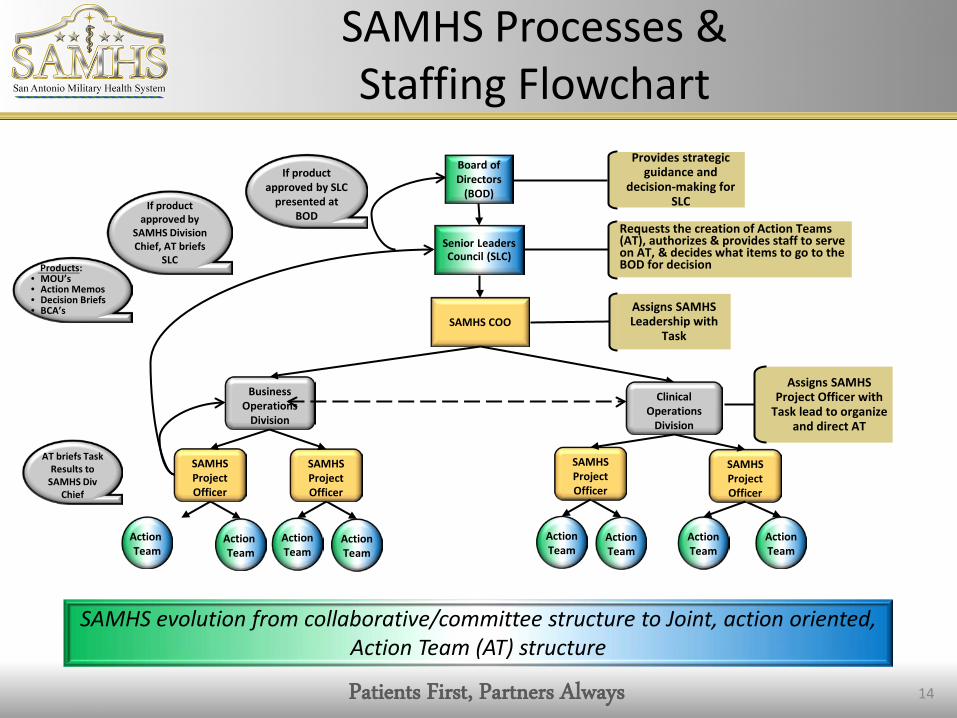

SAMHS Processes & Staffing Flowchart

14

SAMHS evolution from collaborative/committee structure to Joint, action oriented, Action Team (AT) structure

Board of Directors

(BOD)

Senior Leaders Council (SLC)

Provides strategic guidance and

decision-making for SLC

SAMHS COO

Clinical Operations

Division

Business Operations

Division

SAMHS Project Officer

Action Team

Action Team

SAMHS Project Officer

Action Team

Action Team

SAMHS Project Officer

Action Team

Action Team

SAMHS Project Officer

Action Team

Action Team

Requests the creation of Action Teams (AT), authorizes & provides staff to serve on AT, & decides what items to go to the BOD for decision

Assigns SAMHS Leadership with

Task

Assigns SAMHS Project Officer with

Task lead to organize and direct AT

If product approved by

SAMHS Division Chief, AT briefs

SLC

AT briefs Task Results to

SAMHS Div Chief

If product approved by SLC

presented at BOD

Products: • MOU’s • Action Memos • Decision Briefs • BCA’s

Patients First, Partners Always Patients First, Partners Always 15

SAMHS Action Teams

SAMHS Lines of Effort Access

to Care

Behavioral

Health

Data Quality

Orthopedic R

ecapture

Patient E

xperie

nce

Primary

Care

Pharmacy

Quality & Sa

fety

Strategic C

ommunicatio

n & M

arketin

g

Surgica

l

Reporting ScheduleTransform Access Safety & Quality Patient Experience Enrollment Growth Behavioral Health Pharmacy PT Recapture

Communities of Interest:

Research

Clinical Support: LAB/RADMedical Education & Training

SAMHS Action Teams & Lines

of Effort Matrix

Patients First, Partners Always Patients First, Partners Always

The eMSM Business Plan

- 17 -

For Official Use Only

The eMSM Performance Review Process

1. Develop & send Performance Plan & data to DHA Analytics Cell

3. Analyze issues, develop

actionable recommendations

4. Leaders review & take action on

recommendations

MARKETS DHA ANALYTICS LEADERS

2. Collect data, develop eMSM

Report Card

Patients First, Partners Always

FY15-19 Business Performance Plan Executive Summary

Capability Overview

• # ORs: Physical: 144 Staffed: 136 • # Total Beds:

• Physical: 1,791 Staffed: 1,508 • # Skill Type 1 & 2: 4831.39 • Total DHP Direct Care Funding*: $5.8B *(including MILPERS)

FY14 Population Eligible MTF-Enrolled MCSC-Enrolled

1,724,135 877,455 150,396

Mod Study Target

Recapture ($)

Annual Recapture ($M)

Total FY15 FY16 FY17 FY18 FY19

961.2 130.2 197.1 239.2 257.0 259.1 1,082.7

Total 5-Yr Prime Enrollment Change 109 K*

Enrollment Target

Targeted Annual Enrollment (K) Total 5-Yr

Change FY15 FY16 FY17 FY18 FY19

1,039 943 993 1,038 1,050 1,052 109

Total 5-Yr Recapture $1.08B**

Impact on Quadruple Aim Readiness Health Healthcare Cost

28 Total Market Initiatives 22 of 28

initiatives address

14 of 28 initiatives address

25 of 28 initiatives address

25 of 28 initiatives address

Total 5-Yr Productivity Change (Work) 1.17 M 271,859

Productivity Target

Targeted Annual Productivity (work RVUs) (K) Total 5-Yr

Change FY15 FY16 FY17 FY18 FY19

829 9,075 9,699 10,073 10,227 10,244 1,172

Total 5-Yr Net Estimated Savings $1.02 B

Financial Impact (Savings) ($M)

FY15 FY16 FY17 FY18 FY19 5-Yr Total

Savings 137.3 205.7 249.2 267.3 269.3 1,129.0 Costs 15.4 22.3 25.1 25.3 25.4 113.6 Net 121.9 183.3 224.0 241.9 243.8 1,015.3

*Calculated as projected market enrollment in FY19-projected enrollment in FY15. Enrollment numbers include Prime and Plus.

**Excludes all pharmacy-related dollars, as pharmacy is not included in the Mod Study target

18

Patients First, Partners Always

APPROVED SAMHS FY15-19 Business Performance Plan— Executive Summary

Capability Overview

• # MTFs: __10__ • # ORs: Physical:__33__ Staffed:_32___ • # Total Beds: Physical: _425_ Staffed:_366__ • # Skill Type 1 & 2: _888.96_ • Total DHP Direct Care Funding*: $1.6B *(including MILPERS)

FY14 Population Eligible MTF-Enrolled MCSC-Enrolled

247,969 123,326 15,736

Total 5-Yr Net Estimated Savings

$173.3M

Mod Study Target Recapture ($)

Annual Recapture ($M) Total FY15 FY16 FY17 FY18 FY19

$272.3M $34.2M $51.5M $53.9M $53.9M $53.9M $247.6M

Financial Impact (Savings) ($M)

FY15 FY16 FY17 FY18 FY19 5-Yr Total

Savings $34.2M $51.5M $53.9M $53.9M $53.9M $247.6M

Costs $10.3M $15.4M $16.1M $16.1M $16.1M $74.2M

Net $23.9M $36.0M $37.7M $37.7M $37.7M $173.3M

Total 5-Yr Prime Enrollment Change

6,334

Enrollment Target

Targeted Annual Enrollment (K) Total 5-

Yr Change

FY15 FY16 FY17 FY18 FY19

138K 133K 138K 140K 140K 140K 6K

Total 5-Yr Recapture

$247.6M

Initiative

Impact on Quadruple Aim Net Cost Savings ($000)

Imple-mentation

Costs ($000)

Total Produc-

tivity Change

Total Enroll-ment

Change

Total Recapture ($000) Readi-ness Health

Health-care

Cost

Inpatient Transfer X X X $32.3M $13.8M 2,839 RWPS N/A $46.1M

Behavioral Health Recapture

X X X X $14.6M $6.3M

18,615 MH Bed Days 128,000 paRVUs

N/A $20.9M

Orthopedics Recapture X X X $8.6M $3.7M 60,600 paRVUs

N/A $12.3M

Enrollment Growth X X X - *TBD - 6,334 -

Productivity Enhancement Plan (Less BH, Ortho and Inpt)

X X X X $117.7M $50.4M

Production Plan RWPS,

pa RVUS, APCS and MH Bed

Days

- $168.2M

Pharmacy Recapture** X $121.5M $36.5M N/A N/A $173.6M

AGGREGATE TOTAL: $294.7M $110.7M - 6,334 $421.1M

TOTAL LESS PHARMACY: $173.2M $74.2M - 6,334 $247.6M

Total 5-Yr Productivity Change (Work)

271,859

Productivity Target

Targeted Annual Productivity (work RVUs) (M) Total 5-Yr

Change FY15 FY16 FY17 FY18 FY19

343,614 2.34M 2.47M 2.61M 2.61M 2.61M 271,859

- Decimal rounding results in numbers total discrepancies - Enrollment Change is difference between FY15 Target and FY19 Target; present day growth is 11,147 (PRIME) - Skill Type I & II is A & B MEPRS Only; - Pharmacy included in initiatives for tracking; 4% decrease year over year prescribed for FY14-FY18 BPP - Implementation cost is the DHA Prescribed 30% planning factor - ** Pharmacy Recapture not to be counted in totals as will be accounted for through Shared Service - SAMHS Assessment on recapture is ~$247.6M of the $272.3M Modernization Target and 271K work RVUS of the 343K Target.

Patients First, Partners Always Patients First, Partners Always

SAMHS eMSM Performance

Examples

Patients First, Partners Always Patients First, Partners Always

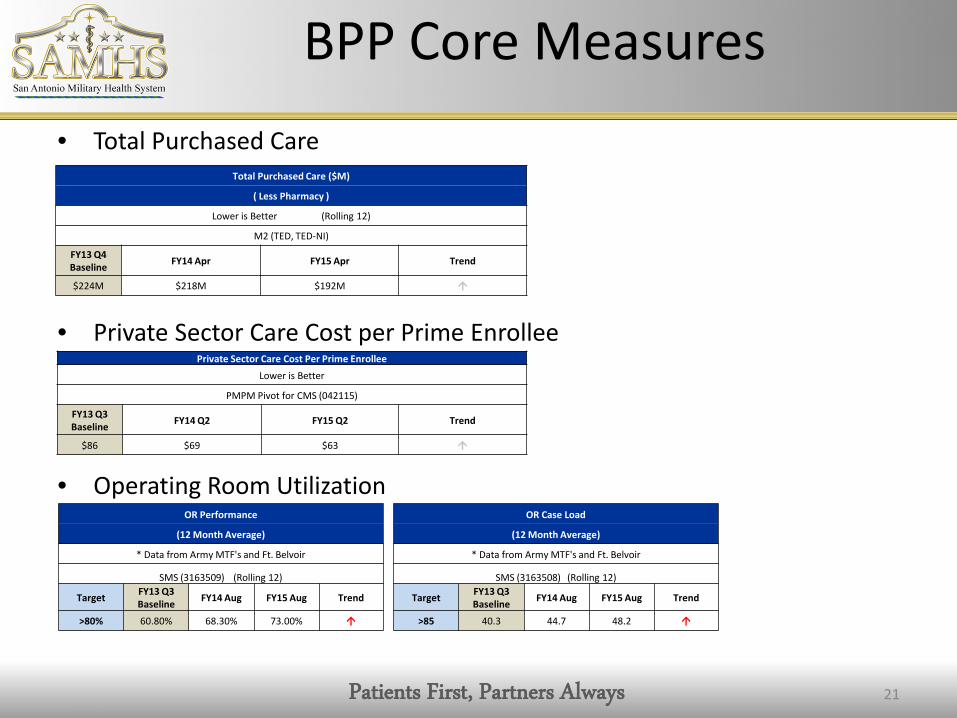

BPP Core Measures

21

• Total Purchased Care

• Private Sector Care Cost per Prime Enrollee

• Operating Room Utilization

Total Purchased Care ($M)

( Less Pharmacy )

Lower is Better (Rolling 12)

M2 (TED, TED-NI)

FY13 Q4 Baseline FY14 Apr FY15 Apr Trend

$224M $218M $192M

Private Sector Care Cost Per Prime Enrollee Lower is Better

PMPM Pivot for CMS (042115)

FY13 Q3 Baseline FY14 Q2 FY15 Q2 Trend

$86 $69 $63

OR Performance

(12 Month Average)

* Data from Army MTF's and Ft. Belvoir

SMS (3163509) (Rolling 12)

Target FY13 Q3 Baseline FY14 Aug FY15 Aug Trend

>80% 60.80% 68.30% 73.00%

OR Case Load

(12 Month Average)

* Data from Army MTF's and Ft. Belvoir

SMS (3163508) (Rolling 12)

Target FY13 Q3 Baseline FY14 Aug FY15 Aug Trend

>85 40.3 44.7 48.2

Patients First, Partners Always Patients First, Partners Always

BPP Core Measures continued

22

• Prime Enrollment

• Non-Prime Primary Care Workload

• Overall Satisfaction w/ Healthcare – Inpatient

Prime Enrollment Higher is Better

M2 (TRICARE Detail)

Target FY13 Q3 Baseline FY14 Sep FY15 Sep Trend

133,763 119,958 124,968 126,858

Non Enrollee Primary Care Workload (FFS)

(RVUs + APCs, Excludes Coast Guard & VA)

Higher is Better (Rolling 12)

IRIS Database Pull

Target FY13 Q3 Baseline FY14 Aug FY15 Jul Trend

686,373 648,252 597,462

Overall Satisfaction - Inpatient (Recommend Hospital)

Higher is Better

TRISS

Target FY13 Q3 Baseline FY15 Q1 FY15 Q2 Trend

71.00% 85% 83.30% 82.70%

Overall Satisfaction - Inpatient

(Rate Hospital)

Higher is Better

TRISS

Target FY13 Q3 Baseline FY15 Q1 FY15 Q2 Trend

71.00% 81.00% 80.00% 78.80%

Patients First, Partners Always Patients First, Partners Always 23

• Per Member Per Month

• Percent Retail Pharmacy Spend

• Primary Care Leakage

Per Member Per Month

(Dollar Amount)

Lower is Better

PMPM Pivot for CMS (042115)

FY13 Q3 Baseline FY14 Q2 FY15 Q2 Trend

$419 $438 $464

Per Member Per Month Growth Rate

(Percent Change Quarter Over Quarter)

Lower is Better

PMPM Pivot for CMS (042115)

Target FY13 Q3 Baseline FY14 Q2 FY15 Q2 Trend

<=2.0% 5.60% -1.10% 5.60%

Percent Retail Pharmacy Spend Lower is Better (1 Month)

M2 (PDTS)

Target By FY18

FY13 Q3 Baseline FY14 Apr FY15 Apr Trend

25% 31.10% 30.00% 52.20%

Primary Care Leakage Lower is Better

PCM Leakage data_16FEB2015

Target FY13 Q3 Baseline FY14 Feb FY15 Feb Trend

<24% 26.10% 29.00% 30.00%

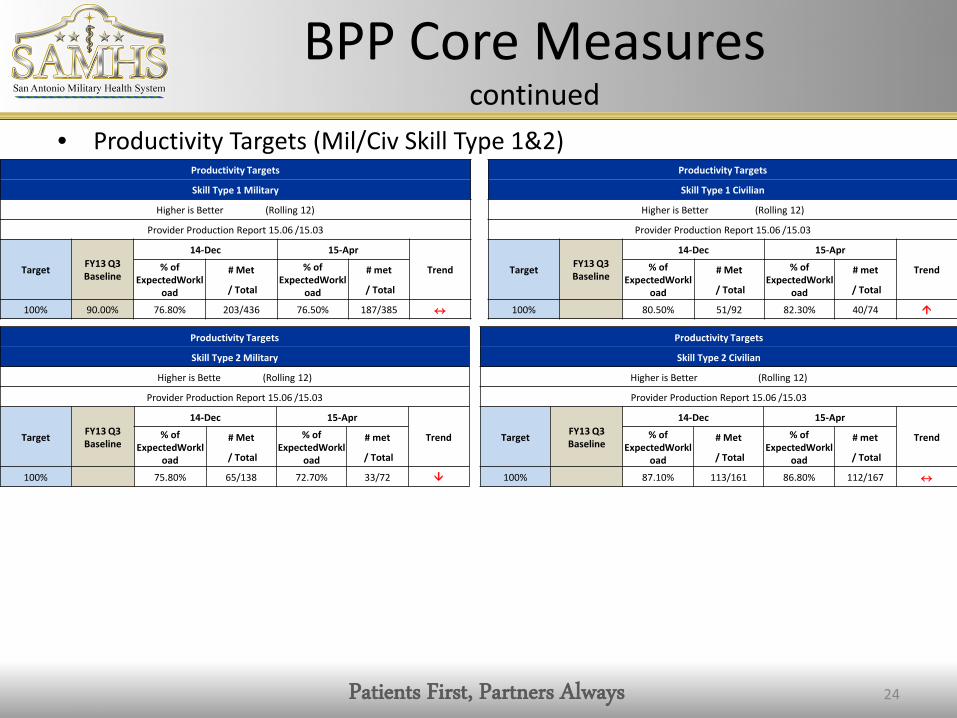

BPP Core Measures continued

Patients First, Partners Always Patients First, Partners Always 24

• Productivity Targets (Mil/Civ Skill Type 1&2)

Productivity Targets

Skill Type 1 Military

Higher is Better (Rolling 12)

Provider Production Report 15.06 /15.03

Target FY13 Q3 Baseline

14-Dec 15-Apr

Trend % of ExpectedWorkl

oad

# Met % of ExpectedWorkl

oad

# met

/ Total / Total

100% 90.00% 76.80% 203/436 76.50% 187/385 ↔

Productivity Targets

Skill Type 1 Civilian

Higher is Better (Rolling 12)

Provider Production Report 15.06 /15.03

Target FY13 Q3 Baseline

14-Dec 15-Apr

Trend % of ExpectedWorkl

oad

# Met % of ExpectedWorkl

oad

# met

/ Total / Total

100% 80.50% 51/92 82.30% 40/74

Productivity Targets

Skill Type 2 Military

Higher is Bette (Rolling 12)

Provider Production Report 15.06 /15.03

Target FY13 Q3 Baseline

14-Dec 15-Apr

Trend % of ExpectedWorkl

oad

# Met % of ExpectedWorkl

oad

# met

/ Total / Total

100% 75.80% 65/138 72.70% 33/72

Productivity Targets

Skill Type 2 Civilian

Higher is Better (Rolling 12)

Provider Production Report 15.06 /15.03

Target FY13 Q3 Baseline

14-Dec 15-Apr

Trend % of ExpectedWorkl

oad

# Met % of ExpectedWorkl

oad

# met

/ Total / Total

100% 87.10% 113/161 86.80% 112/167 ↔

BPP Core Measures continued

Patients First, Partners Always

SAMHS Right of First Refusal TRO-South

Patients First, Partners Always

TOP SPECIALTIES BASED ON NUMBER OF REFERRALS (italicized

rows include ties)

ROFRs Referred to

MTF1

ROFRs Accepted by

MTF2

% ROFRs Accepted by

MTF

ROFRs Actively

Rejected by MTF3

% ROFRs Actively

Rejected by MTF

ROFRs Passively Rejected by MTF4

Physical Therapy, general 229 47 21% 182 79% 0Dermatology, general 144 97 67% 47 33% 0Gynecology (Non-Maternity) 99 94 95% 5 5% 0Ophthalmology, general 95 92 97% 3 3% 0Ear Nose & Throat, general 88 87 99% 1 1% 0Cardiology, general 83 81 98% 2 2% 0Orthopedics, knee & shoulder 64 43 67% 21 33% 0Urology, general 53 52 98% 1 2% 0Neurosurgery, general 45 41 91% 4 9% 0General Surgery 41 40 98% 1 2% 0

Monthly TotalApr 15 545 356 65% 189 35% 0May 15 488 254 52% 234 48% 0Jun 15 580 296 51% 284 49% 0

Quarterly Total 1613 906 56% 707 44% 0

'This table shows the number of non-urgent referrals by specialty that were sent to the MTF for this quarter and how many referrals were accepted or rejected.1ROFRs Referred- number of referrals that were sent to the MTF for acceptance 2ROFRs Accepted – number of referrals the MTF accepted3ROFRs Rejected- Number of referrals rejected by the MTF (including the passive denials- MTF takes no action within one business day)4ROFRs Passively Rejected: number of referrals the MTF passively denied (MTF takes no action within one business day)

'ROFR data extracted from Humana Military Report Gallery for Apr- Jun 2015

SAMHS eMSM- TOP 10 SPECIALTIES BASED ON NUMBER OF REFERRALS (italicized rows include ties)

SAMHS Right of First Refusal TRO-South –Top 10

Patients First, Partners Always

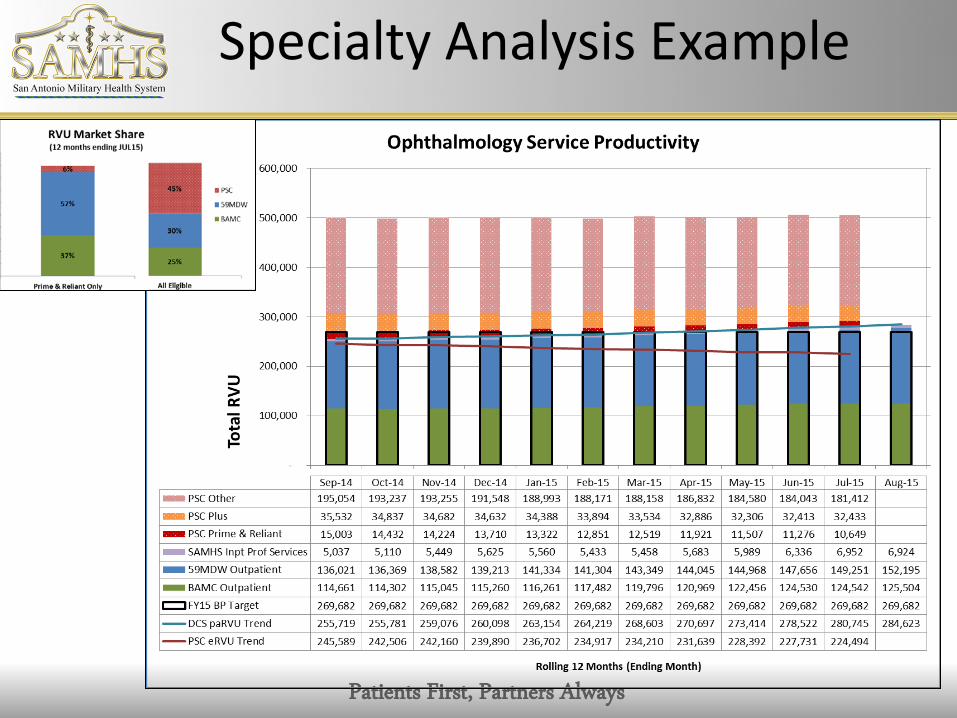

Specialty Analysis Example

Patients First, Partners Always Patients First, Partners Always 28

Specialty Analysis Example Continued

Patients First, Partners Always Patients First, Partners Always 29

Specialty Analysis Example Continued

-

2,000

4,000

6,000

8,000

10,000

12,000KI

M,Y

U HY

ON

HAYE

S,BA

RTLE

TT H

TOW

NLE

Y,JA

MES

RIC

HARD

III

SUHR

,ABR

AHAM

WO

NDU

KW

ELCH

,MAR

KSM

ITH,

BEN

JAM

IN H

EBER

CALD

WEL

L,M

ATTH

EW C

RUBI

NAT

E,LA

URA

STEI

GLE

MAN

,WAL

TER

AGR

ANT,

AARO

N D

ANIE

LEV

ANGE

LIST

A,CH

ARIS

MA

BAUT

ISTA

BRAM

BLET

T,GR

EGO

RY T

HOM

ASGE

DWIL

VALE

NTI

N,F

RAN

K E

SHER

OL

VEGD

IETH

OM

AS,S

COTT

AM

AUFF

RAY,

RAN

DY O

DRAY

PAU

CRO

SJN

FRIE

DMAN

,MIR

IAM

SMIT

H,RO

BERT

EBA

SKIN

,DAR

RELL

ECH

ACKO

,BEN

JAM

INKO

HDAV

JOHN

SON

,AN

THO

NY

JAM

ESAN

DERS

ON

,DAN

IEL

MHA

RRJN

ROBE

RTS,

SAN

FORD

EBO

WES

,HAR

RISO

N N

ESBI

T JR

DAVI

ES,B

RETT

WAP

SEYD

VUVI

NPA

NDA

Y,VA

SUDH

A AR

UNA

MIT

TELB

CRO

LEY,

JAN

IS K

HAAA

ROLE

UJES

STH

EJAR

LAUC

YNCA

LDCH

RIGR

AKEN

ROHL

UI

HERR

MAR

CGR

OVE

S,LU

CAS

LEE

RODR

IGU

EZ,C

HRIS

TOPH

ER J

MO

SES,

ARIA

N A

ROE,

JOSH

UA

RO

DEA,

TAM

ANN

AM

ADSE

N,M

ICHA

EL H

OW

ARD

LUTM

ER,S

EAN

MIC

HAEL

BEN

NIO

N,JO

HN L

MIC

HEL,

RYAN

JOSE

PHPO

WEL

L,M

ARIO

N R

CRO

SKRE

Y,JA

SON

AGI

LLIS

,JOHN

FGA

LLAG

HER,

COLI

N F

RAN

CIS

Wor

k RV

Us (

Actu

al in

clud

es P

rimar

y an

d Ad

ditio

nal P

rovi

der)

Individual Provider Productivity Ophthalmology SEP14 to AUG14

Actual Work RVU Target

Annual work RVU Target: AD, CIV: 4,731

CON: 5,144

[-----------Residents--------------

Individual Provider Data by Name

Patients First, Partners Always Patients First, Partners Always 30

Specialty Analysis Example Continued

Provider Information Productivity (M2) Distribution of Time (DMHRSi)

Provider Name Prov Type Actual Work RVU

Months (>10 RVU) Target MGMA

(Annual FY16) Paid FTE Clinical Time GME Time Admin Time Other Available Non Available

KIM,YU HYON Active Duty 10,114 12 4,731 4,731 HAYES,BARTLETT H Active Duty 7,219 12 4,731 4,731 TOWNLEY,JAMES RICHARD III Active Duty 6,820 12 4,731 4,731 SUHR,ABRAHAM WONDUK Active Duty 6,610 12 4,731 4,731 WELCH,MARK Active Duty 6,477 12 4,731 4,731 SMITH,BENJAMIN HEBER Active Duty 5,966 12 4,731 4,731 CALDWELL,MATTHEW C Active Duty 5,196 12 4,731 4,731 RUBINATE,LAURA Active Duty 5,107 12 4,731 4,731 STEIGLEMAN,WALTER A Active Duty 4,249 12 4,731 4,731 GRANT,AARON DANIEL Active Duty 3,960 12 4,731 4,731

EVANGELISTA,CHARISMA BAUTISTA Active Duty 3,764 10 3,943 4,731

BRAMBLETT,GREGORY THOMAS Active Duty 3,532 12 4,731 4,731 GEDWIL Civilian 3,519 12 4,731 4,731 VALENTIN,FRANK E Active Duty 3,477 12 4,731 4,731 SHEROL Contractor 3,106 12 5,144 5,144 VEGDIE Contractor 3,043 12 5,144 5,144 THOMAS,SCOTT A Contractor 3,000 12 5,144 5,144 MAUFFRAY,RANDY O Active Duty 2,798 12 4,731 4,731 DRAYPAU Active Duty 2,511 9 3,548 4,731 CROSJN Active Duty 2,395 9 3,548 4,731 FRIEDMAN,MIRIAM Contractor 2,364 12 5,144 5,144 SMITH,ROBERT E Contractor 2,340 12 5,144 5,144 BASKIN,DARRELL E Active Duty 2,168 8 3,154 4,731 CHACKO,BENJAMIN Contractor 1,545 12 5,144 5,144 KOHDAV Contractor 1,429 12 5,144 5,144 JOHNSON,ANTHONY JAMES Active Duty 1,214 7 2,760 4,731 ANDERSON,DANIEL M Active Duty 1,010 7 2,760 4,731 HARRJN Active Duty 960 12 4,731 4,731 ROBERTS,SANFORD E Contractor 714 12 5,144 5,144 BOWES,HARRISON NESBIT JR Contractor 679 11 4,715 5,144 DAVIES,BRETT W Active Duty 608 3 1,183 4,731 APSEYD Contractor 594 12 5,144 5,144 VUVIN Active Duty 514 7 2,760 4,731 PANDAY,VASUDHA ARUNA Contractor 490 5 2,143 5,144 MITTELB Active Duty 361 6 2,366 4,731 CROLEY,JANIS K Contractor 333 12 5,144 5,144 HAAARO Active Duty 202 5 1,971 4,731 LEUJESS Active Duty 188 3 1,183 4,731 THEJAR Active Duty 14 1 394 4,731

Individual Providers by

Name

Patients First, Partners Always Patients First, Partners Always

SAMHS eMSM “Victories”

• Single, Unified Business Plan • Standardized 2 Appointment Types

– Family Medicine, Pediatrics, Internal Medicine

• Integrated Dermatology, Cytology • Single Consult Review • Roll-up dashboards • Distributed Care Collaboration • Wilford Hall Academy • One Call Resolution • Inpatient Integration Initiative

Patients First, Partners Always Patients First, Partners Always

Common eMSM Challenges • Leadership: perspective, maturity, development • Strategy: eMSM Strategy vs Service priorities

– High Reliability Organization(s)? – Integrated vs Federated vs other? – The “Service-led” eMSM?

• Performance: Performance Management System (synergistic) – Data overload: MTFs, eMSM, regional HQ, TRO, Services, DHA, etc. = Noisy – Incentive Systems: IRIS, etc.

• Drivers: – Enrollment….Access to Care…Productivity….Containment/Recapture – Patient Satisfaction – Collision of Compliance, Accreditation, and Governance

• Distribution of Assets – Integrated manning documents – Movement of personnel, equipment, monies

• Governance Structures and Workflow – Issue identification, Prioritization, and Decision Making

• System Support to eMSMs – Intermediate Headquarters’ processes

Patients First, Partners Always Patients First, Partners Always

The Way Forward

• Single market strategy – How to continue transformation to an HRO? – Distribution of Assets

• Key Market Engagement – Federal Health Care Consortium – CEO Forum – BoD/Administrative Coordination Meeting

• Synergy with MHS Review – Leadership, Safety, Performance Management – Quality, Access, Production, Containment/Recapture

• Refining our Integrative Governance Processes – Single Department Chairs? – Single Credentialing?

Patients First, Partners Always Patients First, Partners Always

Executive Skills

Patients First, Partners Always Patients First, Partners Always

Key Skills in an eMSM

• Using Perspective: eMSM-wide and/or MHS-wide • Leading Transformation & Change

– Leadership – Management

• Trusting and Relying on Partnership – Cooperation/Collaboration vs Command/Control

• Leveraging novel workflows – eMSM workflow vs MTF workflow – Formal vs Informal; minimizing beuracracy

• Find “common ground” – Obvious consensus vs what is needed/what is right

• Communicating effectively • Exhibiting patience, stamina, and tenacity

Patients First, Partners Always Patients First, Partners Always

Key Takeaways

• The greatest transformation in MHS History • A fully Integrated, High-Performing Health System Team • While Cost is important……focus on the patient and the care

team is key – Medically & Dentally Ready Force – Ready Medical and Dental Force – Quality, Clinical Outcomes and a “System of Health”

• Courage to “Do the Right Thing” • Developing, shaping, and empowering strategically informed

leaders is imperative to our success

36

Patients First, Partners Always

Federal Healthcare Consortium