CONSUMER TRUST AND PERCEIVED RISK IN BUSINESS-TO-CONSUMER (B2C)

E-COMMERCE

Submitted to:

Dr. Muhammad Ziaulhaq Mamun

Professor

Course Instructor: Research Methodology

Institute of Business Administration

University of Dhaka

Submitted by:

Samiha Majid Simi (RH 01)

Shafqat Aurin Siddiqua (RH 04)

Mastura Tasnim (RH 08)

Chowdhury Ashiqur Rahman (ZR 24)

Joya Chowdhury (RH 26)

Muhammad Danial Rafi (ZR 28)

Silma Subah Ahmad (ZR 46)

Rakib Ibnay Hossain(ZR 47)

Tanzir Islam (ZR 51)

Shaadman Ahmed Siddiqui (ZR 58)

Group 2, Section A, BBA 21st Batch

13th

June 2015

Institute of Business Administration, Dhaka University

i | P a g e

June 13, 2015

Dr. Muhammad Ziaulhaq Mamun

Professor

Institute of Business Administration

University of Dhaka

Sir:

Subject: Letter of transmittal for Research Method course (K301) term paper

With due respect, we would like to present to you our term paper “Consumer Trust and

Perceived Risk in Business to Consumer E-commerce,” which has been completed as part of the

Research Method course (K301). The purpose of this report was to conduct a basic research to

discover the level of consumer trust and perceived risk in e-commerce transactions by users. It

was a learning experience as we had the opportunity to utilize the advanced tools and techniques

introduced to us throughout the Research Method course.

Therefore, we hope that you would accept the term paper and our gratitude for allowing us to

work on this intellectually stimulating report. Thank you.

Sincerely Yours

SamihaMajid Simi (01)

Group Leader

Group 2

Sec: A

Batch: BBA 21st

Consumer trust and perceived risk in B2C e-commerce | ii

ACKNOWLEDGEMENT

In completing the term paper, we had to take the help and guideline of some respected persons,

who deserve our greatest gratitude. We would like to show our gratitude to Dr. Muhammad

Ziaulhaq Mamun, Professor, Institute of Business Administration, University of Dhaka, for

giving us guidance for the term paper throughout numerous consultations. We would also like to

expand our deepest gratitude to all those who have directly and indirectly guided us in writing

this assignment.

Many people, especially our classmates, team members and respondents, have made valuable

comments and suggestions on this report which gave us inspiration to improve and refine our

assignment. We‟d like to thank all these people for their incomparable help – directly and

indirectly – to complete our assignment.

Consumer trust and perceived risk in B2C e-commerce | iii

EXECUTIVE SUMMARY

E-commerce is a relatively new field of business in Bangladesh. It was introduced to the country

in 2009 when Bangladesh Bank allowed online transactions for the first time and by 2013, the

market expanded to BDT 2000 million in worth across the country. The introduction of high

speed internet in recent years and the expansion of mobile technology have played a key role in

increasing the scope of e-commerce usage. Despite this recent upsurge, much research remains

to be done on the consumer trust and perceived risk in business to consumer (henceforth referred

to as B2C) e-commerce transactions. The purpose of this research, thus, is to provide insight and

evaluate the current situation of this new field with particular emphasis on the perceived risks

and trusts placed on it by consumers.

In order to understand this further, the research question of consumer trust and perceived rick on

B2C e-commerce has been narrowed down to broad and specific objectives and three null

hypotheses have been developed: a. brand perception, b. consumer perception of high privacy,

and c. consumer perception of high financial security – each positively affect consumer‟s intent

to purchase online.

With that in mind, extensive literature review was conducted with secondary sources from

renowned journals and research papers which have been referenced throughout the report. For

primary source of information, a detailed survey was conducted with e-commerce consumers as

respondents and this is the main source of data in the report. Due to time, finance and

geographical constraints, the respondents were limited to the area of Dhaka city and non-

probabilistic convenience/accidental and judgmental sampling was used. The key demographic

was nearly equally divided between male and female respondents, with mean age of around

twenty and occupation of undergraduate studies. This is expected as e-commerce users are

skewed towards young, educated, tech-savvy users of the country.

In terms of branding perception, the survey found that, as the e-commerce industry of

Bangladesh in relatively new, user experience of brands is limited, with consumers purchasing

from an average of 2 brands. Furthermore, few brands have captured the consumer attention as

114 respondents collectively prefer 24 brands. Even so, most of the respondents have minimum

and moderate brand loyalty towards their current brand and it appears to be difficult to establish

Consumer trust and perceived risk in B2C e-commerce | iv

brand loyalty in electronic market space. Despite that, one-fifth of respondents showed strong

brand loyalty, which may be a credit to their brand of choice or their internal tendency to stay

loyal to their preferences. On average, consumers feel more secure while purchasing from

reputed brands, which is to be expected from any industry – physical or electronic. Majority of

the people also perceive branded products to be of better quality compared to non-branded

products. However, similar to users in the physical marketplace, e-commerce users perceive that

they are not receiving value for money in their purchases.

In terms of perception regarding privacy of information, the research inquiries revealed that most

online sites require a moderate amount of information from their consumers, and that in majority

of cases only a minimal amount of that information is shared publicly. Nearly half of the

respondents claim that the service providers ask them for their permission before sharing any

information and around 3/5th of this sample population is aware of the privacy policies by their

providers. When asked to rate the effectiveness of this privacy policy on a scale of 1 to 10, the

results were diverse, the highest frequencies occurring between 5 and 9 with 1 being very

ineffective and 10 being very effective. Only 6 out of 114 have a history of privacy violation and

5 out of these 6 respondents have also had corrective measures taken on behalf of them by

providers.

In terms of consumer perception of financial security, a number of key insights were revealed.

Most consumers felt that online transactions incurred a „medium‟ element of over-pricing and

one fifth felt that that element was „high‟. Consumer perception seems to be that online

transactions include some form of over-pricing. In case of freight cost, nearly everyone felt that

fixed freight cost pricing was more preferable to percentage pricing and in general, the

perception regarding freight cost was that it was more or less justified, with a mean and mode of

approximately 5 out of 10. Consumer tendency to prefer fixed freight cost may indicate an

affinity for bulk buying to minimize the cost per transaction. Overall, the perceptions regarding

the pricing system in online transactions are positively skewed in this research.

Taking the survey responses into account, SPSS calculations took place to provide cogent results

to the queries placed at the beginning of the research and the three hypotheses were addressed

respectively.

Consumer trust and perceived risk in B2C e-commerce | v

The first null hypothesis regarding brand perception positively impacting consumer intent to

purchase cannot be rejected. There is a negative correlation between purchasing from branded

and non-branded providers and this indicates that perception of high brand image positively

affects a customer‟s trust.

The second null hypothesis, which states that consumer perception of high privacy can positively

impact intent to purchase, cannot be accepted as the calculations do not fall within the

confidence interval chosen by the research. A consumer‟s perception of high privacy of

information does not positively affect his trust on e-commerce transactions.

The third null hypothesis, which states that consumer perception of financial risk can positive

impact the intent to purchase, cannot be rejected as there is a positive correlation between the

two variables. So it can be concluded that consumer‟s perception of financial security positively

affects trust in e-commerce transactions.

To justify these claims, the research conclusions underwent factor analysis. The KMO measure

of greater 0.5 indicated satisfactory sampling adequacy and the regression factor analysis of

factors indicated positive relationship between consumer perception, consumer trust and risk in

e-commerce transactions.

The research has so far revealed that interesting insights into the consumer mindset of B2C

online customers. They perceive brand and financial risk assessments as a key determinant

during purchasing decisions in e-commerce transactions, whereas privacy of information is not

perceived as an important variable in these sort of decisions. Brand is a powerful motivator in all

markets and it is unsurprising that it would have a similar effect in the online market, no matter

how new the market may be. That consumers pay attention to branding in this developing market

is an important signal for online businesses to refocus on marketing strong brand images to new

consumers so as to gain brand loyalty. Privacy of consumer information may not appear so

important to consumers right now due to the flexible payment methods (i.e. on delivery

payment). Concern over privacy is likely to increase if credit card usage increases in the country

or if, with the increase of e-commerce businesses, cases of criminal activity in e-transactions rise

which causes media uproar. Financial risk assessments also indicate that consumers may be

swayed by price centric marketing and business techniques as a significant portion associate

Consumer trust and perceived risk in B2C e-commerce | vi

online shopping to some extent of overpricing, and it may be important for brands to break that

perception in order to garner loyal customers.

The e-commerce industry is at the growth stage and is rapidly expanding in market size. It will

be interesting to see the many kinds of research conclusions that will be made in the future for

this industry and it is hoped that many of the questions and possibilities raised in this project will

be answered and explained in future years in more thorough and extensive research papers. For

now, these are the conclusions to hypotheses raised by this research and every precaution and

step has been taken to ensure authentic data collection, analysis, and evaluation took place

throughout this research.

Consumer trust and perceived risk in B2C e-commerce | vii

TABLE OF CONTENT

ACKNOWLEDGEMENT .............................................................................................................. ii

EXECUTIVE SUMMARY ........................................................................................................... iii

TABLE OF CONTENT ................................................................................................................ vii

1. INTRODUCTION ...................................................................................................................... 1

1.1 Origin of the Report .............................................................................................................. 1

1.2 Research Background ........................................................................................................... 1

1.3 Problems ............................................................................................................................... 2

1.4 Research Question ................................................................................................................ 3

1.5 Objectives ............................................................................................................................. 3

1.5.1 Broad Objective: ............................................................................................................ 3

1.5.2 Specific Objectives: ....................................................................................................... 3

1.6 Hypotheses ............................................................................................................................ 3

1.7 Rationale ............................................................................................................................... 4

1.8 Scope ..................................................................................................................................... 4

1.9 Limitations ............................................................................................................................ 4

2.0 METHODOLOGY ................................................................................................................... 4

2.1 Data Collection ..................................................................................................................... 4

2.1.1 Primary Sources ............................................................................................................. 5

2.1.2 Secondary Sources ......................................................................................................... 5

2.2 Sampling Methods ................................................................................................................ 5

2.3 Sample Size ........................................................................................................................... 5

2.4 Sample Frame ....................................................................................................................... 5

2.5 Purpose of Research .............................................................................................................. 6

2.6 Questionnaire Development.................................................................................................. 6

2.7. Validity ................................................................................................................................ 7

2.8. Reliability ............................................................................................................................. 8

3.0 LITERATURE REVIEW ....................................................................................................... 10

4. E-COMMERCE PENETRATION AMONG RESPONDENTS .............................................. 12

4.1. Awareness of E-commerce ................................................................................................ 12

Consumer trust and perceived risk in B2C e-commerce | viii

4.2. Usage of E-commerce ........................................................................................................ 12

4.3. Awareness to Usage Ratio ................................................................................................. 12

4.4. Percentage of Shopping Budget for E-commerce .............................................................. 13

5. DEMOGRAPHIC OF E-COMMERCE USERS ...................................................................... 14

5.1. Gender ................................................................................................................................ 14

5.2. Age ..................................................................................................................................... 14

5.3. Education Level ................................................................................................................. 14

5.4. Profession ........................................................................................................................... 14

6. PERCEPTION ON BRAND..................................................................................................... 15

6.1. Number of Brands perUser ................................................................................................ 15

6.2. Most Preferred Brands ....................................................................................................... 16

6.3. Measuring Brand Loyalty .................................................................................................. 17

6.4. Perception on Security ....................................................................................................... 18

6.5. Perception on Product Quality ........................................................................................... 18

6.6. Perception on Service Quality ........................................................................................... 19

6.7. Perception on Value for Money ......................................................................................... 20

6.8. Summary of the Findings ................................................................................................... 21

7. PERCEPTION ON PRIVACY OF INFORMATION .............................................................. 22

7.1. Level of Information Needed ............................................................................................. 22

7.2. Level of Information Shared .............................................................................................. 23

7.3. Customer Control over Information Sharing ..................................................................... 23

7.5. Perception on Effectiveness of Privacy Policy .................................................................. 24

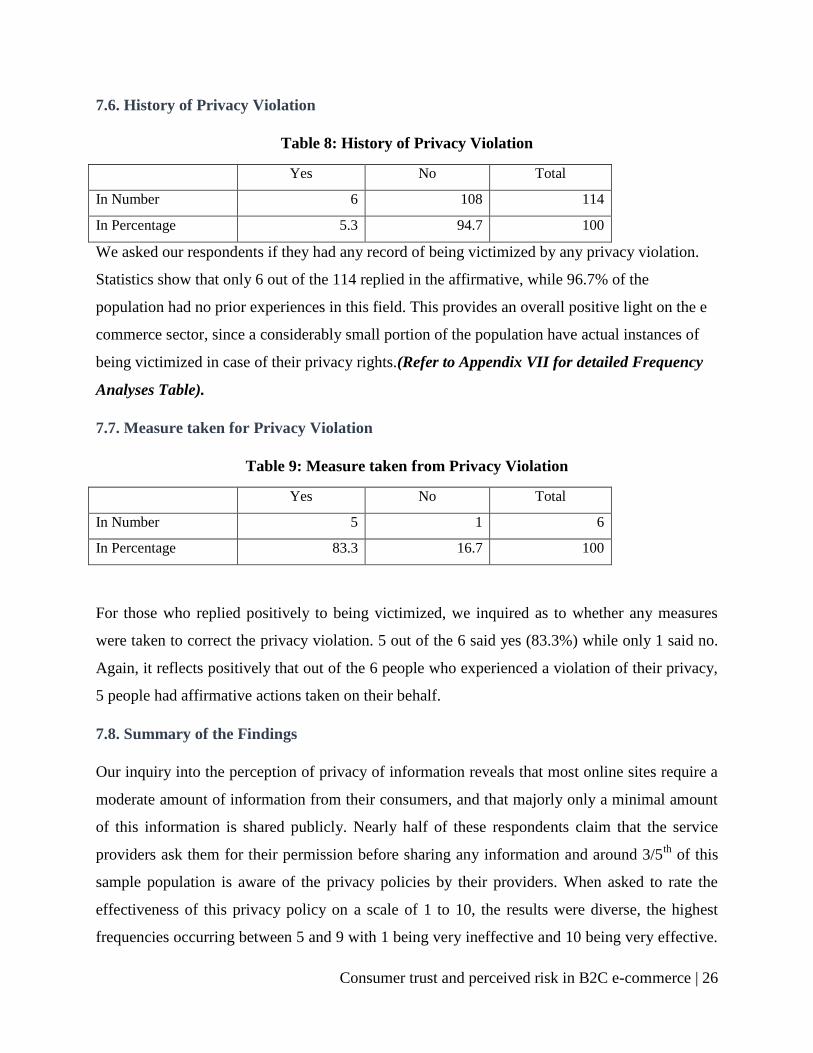

7.6. History of Privacy Violation .............................................................................................. 26

7.7. Measure taken for Privacy Violation ................................................................................. 26

7.8. Summary of the Findings ................................................................................................... 26

8. PERCEPTION ON FINANCIAL RISK ................................................................................... 28

8.1. Perception on being overpriced ......................................................................................... 28

8.2. Preferred Method of Freight Cost ...................................................................................... 28

8.3. Perception on Freight Cost................................................................................................. 29

8.4. Overall Perception on Pricing System ............................................................................... 30

8.5. Summary of Findings ......................................................................................................... 30

9. EFFECT OF BRAND, PRIVACY AND FINANCIAL RISK ON CONSUMER TRUST ..... 31

Consumer trust and perceived risk in B2C e-commerce | ix

Hypothesis 1: Brand image positively affects a consumer‟s trust ............................................ 31

Hypothesis 2: A consumer‟s perception of high privacy of information positively affects his

trust ........................................................................................................................................... 34

Hypothesis 3: A consumer‟s perception of financial security positively affects his trust ........ 35

10. FACTOR ANALYSIS ............................................................................................................ 38

10.1 Factor loading ................................................................................................................... 38

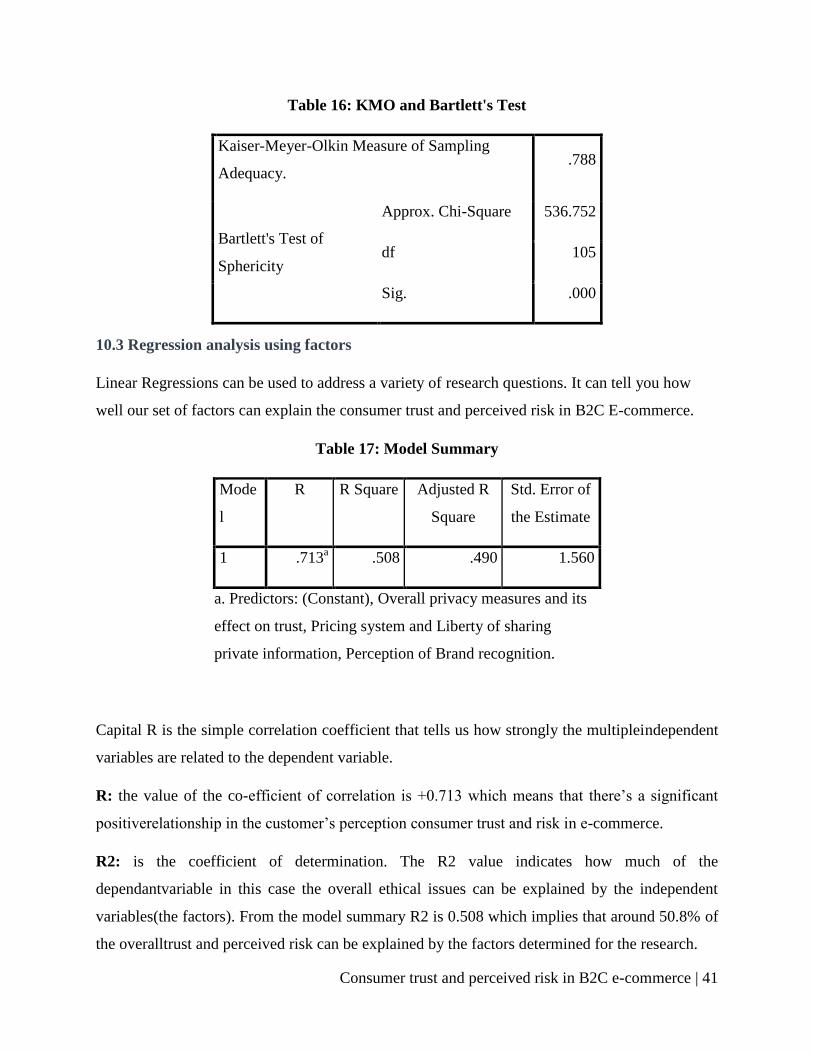

10.2 KMO and Bartlett‟s Test ................................................................................................... 40

10.3 Regression analysis using factors ..................................................................................... 41

10.4 Coefficient of the factors .................................................................................................. 42

10.5 ANOVA test for Significance of the model ...................................................................... 43

11. CONCLUSION ....................................................................................................................... 44

APPENDIX SECTION ................................................................................................................. 46

Appendix I: Questionnaire ............................................................................................................ 46

Consumer trust and perceived risk in B2C E-commerce .............................................................. 46

Respondent Identification details .............................................................................................. 46

A. Respondent‟s orientation to e-commerce ............................................................................. 46

B. Effect of Brand in perceived value and trust ........................................................................ 47

C. Effect of site reputation on buying intent ............................................................................. 48

D. Effects of Privacy in perceived value and trust .................................................................... 48

E. Effects of perceived financial risk ........................................................................................ 50

F. Information about the respondent ......................................................................................... 50

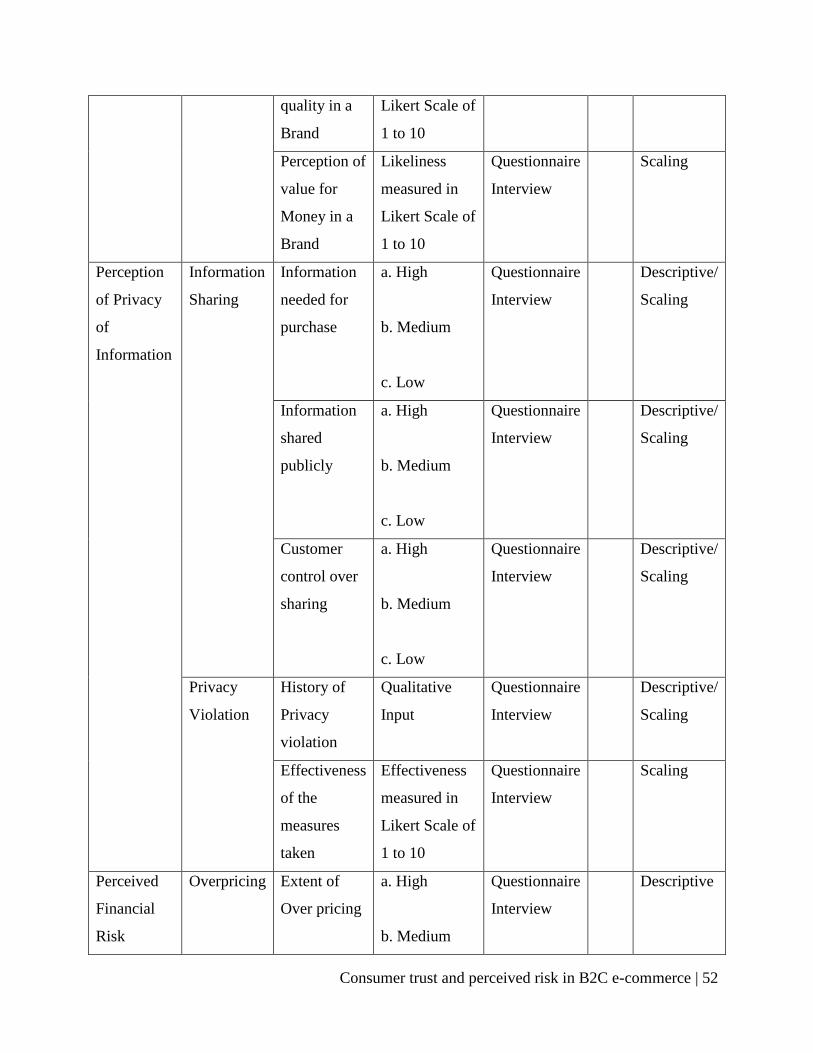

Appendix II: Coordination Schema .............................................................................................. 51

Appendix III: Calculations ............................................................................................................ 53

Appendix IV: Data Analysis for Section 4 ................................................................................... 55

Appendix V: Data Analysis for Section 5..................................................................................... 57

Appendix VI: Data Analysis for Section 6 ................................................................................... 61

Appendix VII: Data Analysis for Section 7 .................................................................................. 70

Appendix VIII: Data Analysis for Section 8 ................................................................................. 77

Appendix X ................................................................................................................................... 84

Bibliography ................................................................................................................................. 85

References ..................................................................................................................................... 85

Consumer trust and perceived risk in B2C e-commerce | x

LIST OF TABLES

1. Reliability Statistics (Cronbach‟s Alpha)………………………………………..8

2. Reliability Statistics (Cronbach‟s Alpha and Split Half Technique)…………….8

3. Number of Brands per Use……………………………………………………..16

4. Level of Information Needed ………………………………………………….22

5. Level of Information Shared ………………………………………………….23

6. Awareness about Privacy Policy……………………………………………….24

7. Effectiveness of Privacy Policy………………………………………………. .24

8. History of Privacy Violation……………………………………………………26

9. Measure taken for Privacy Violation………………………………………….. 26

10. Perception on being overpriced…………………………………………………28

11. Preference of Freight Method ………………………………………………….29

12. Statistics of Hypothesis 1: Brand image positively affects a consumer‟s trust

I. One-Sample Statistics………………………………………………………32

II. One-Sample Test……………………………………………………………32

III. Correlations…………………………………………………………………33

13. Statistics of Hypothesis 2: A consumer‟s perception of high privacy of information

positively affects his trust

I. One-Sample Statistics………………………………………………………34

II. One-Sample Test……………………………………………………………35

14. Statistics of Hypothesis 3: A consumer‟s perception of financial security positively

affects his trust

I. One-Sample Statistics………………………………………………………36

II. One-Sample Test……………………………………………………………36

III. Correlations…………………………………………………………………37

15. Total Variance Explained……………………………………………………….38

16. KMO and Bartlett's Test………………………………………………………...41

17. Regression analysis using factors……………………………………………….41

18. Coefficient of the factors………………………………………………………..42

19. ANOVA………………………………………………………………………...44

1 | P a g e

1. INTRODUCTION

1.1 Origin of the Report

This report titled “Consumer Trust and Perceived Risk in B2C E-commerce” has been prepared

as a requirement for the completion of the course Research Methodology (K301) under the

supervision of our esteemed course instructor Professor Dr. Muhammad ZiaulhaqMamun,

Institute of Business Administration, University of Dhaka.

1.2 Research Background

E-commerce (or electronic commerce) entails the use of marketing and selling products and

services over the internet. It basically delineates the process of buying, selling, transferring, or

exchanging products, services, or information via the medium of the World Wide Web. E-

commerce can be divided into 3 primary categories, namely B2B (Business to Business), B2C

(Business to Consumers), and B2G (Business to Government). For the purpose of this report,

we‟ll focus on B2C only, which refers to the tactics and best practices used by businesses to

promote products and services to consumers online. In e-commerce‟s context, this refers to

marketing products to customers via internet, irrespective of their geographical location. With

the ever dynamic evolution of internet and its widespread usage, e-commerce is becoming one of

the most viable platforms for conducting business, even in Bangladesh. E-commerce started in

Bangladesh in the late 90s, with gift shops targeted towards the Non-Residential Bangladeshis

(NRBs), where people living abroad could buy gifts online and send them to their kin in

Bangladesh. But it officially started in 2009, with Bangladesh Bank allowing online payment in

the country. Another big factor which further propelled e-commerce in Bangladesh to become

the reckoning force that it is today was the lowering of cost of internet usage, and the

introduction of WiMax technology. After this, the Bangladeshi outsourcing community observed

rapid growth. Soon after, online shops and sites of Bangladeshi brands started popping up online,

especially in social media, and after 2013, when Bangladesh Bank gave permission to buy

products and services online using international credit cards, which meant that Bangladeshis

could buy and sell products all over the global marketplace, the sector has only boomed at an

Consumer trust and perceived risk in B2C e-commerce | 2

incredible rate. Ease of transaction, widening markets, and decreased overheads are factors that

make e-commerce solutions more and more attractive, as evident with the growth of online sales.

From governments to multinational companies to one-person start-ups, e-commerce is

increasingly viewed as a key business modality of the future, and with the world becoming

increasingly more digital and tech-savvy, e-commerce.

1.3 Problems

Despite its many advantages, E-commerce in Bangladesh has a host of issues, some of which are

presented below:

(a) Vague or Incorrect Product description: Online stores cannot provide customers with the

option to touch, manipulate, or try on a product before purchasing it; therefore, product

descriptions are paramount. One ecommerce problem occurs when a company fails to

communicate product features that potential customers are interested in. Include size, brand,

dimensions, weight, care instructions, ideas for use, material type information, etc. Make

customers feel confident about the products even though they cannot touch them.

(b) Hidden costs: Some websites or online brands do not mention extra fees or shipping charges

with their products and services. Also, many online companies advertise their products over

social media, but do not mention the price with the products. These additional charges may

infuriate and/or confuse the customers, if they find out about these hidden costs only when

processing their credit card information.

(c) Reactive or zero customer feedback option: With live transactions one has the opportunity to

test out a product, and provide feedback, or ask questions, but online, without the presence of a

FAQ section, or customer feedback tab, it normally cannot be done.

(d) Security and trust: People are cautious to reveal their personal credit information online, or to

conduct transactions through non-secure payment methods. People buy products from online by

placing faith in the sellers, and some businesses don‟t deliver the quality products they promise.

Other issues may include the fear of being hacked, or getting their personal computers virus

infected from business sites.

Consumer trust and perceived risk in B2C e-commerce | 3

These concerns are just the tip of the iceberg when it comes to e-commerce. These, and more,

shall be discussed below.

1.4 Research Question

Is there an effect of consumer trust and perception of risk on buying intent via e-commerce?

1.5 Objectives

1.5.1 Broad Objective:

The broad objective of this research is to investigate consumer trust and perception of risk while

buying via e-commerce.

1.5.2 Specific Objectives:

I. To gauge the effect of known vendors or brands on consumer trust.

II. To measure the effect of perception of privacy of information on a consumer‟s willingness to

buy online.

III. To understand the impact of perceived financial risk on the intent to buy.

1.6 Hypotheses

For specific Objective I Hypothesis 1: Brand image positively affects a consumer‟s intent to buy

For specific Objective II Hypothesis 2: A consumer‟s perception of high privacy of information

positively affects his intention to buy

For specific Objective III Hypothesis 3: A consumer‟s perception of financial security positively

affects his intention to buy

Consumer trust and perceived risk in B2C e-commerce | 4

1.7 Rationale

Since our topic is „consumer trust and perceived risk in B2C e-commerce‟, the research will

provide valuable insights into the main hurdles of trust that consumers face when making an e-

transaction, which ultimately limit consumers choices due to their hesitation to buy online, and

also businesses due to their inability to capture these consumers.

1.8 Scope

Due to a large population of people who may be potential or current consumers via e-

transactions, it will be comparatively easier to access the required sample size. However, our

report only investigates the consumer aspect of the report and this will therefore was limited to

the consumer perspective.

1.9 Limitations

Due to the length and depth of the questionnaire, most respondents did not seem to have

filled the questionnaire attentively, reflected in the missing or hurried answers.

More respondents could not be reached out to due to limitations of time and accessibility.

A lot of respondents approached do not shop online. 114 out of our 140 respondents said that

they were active e commerce users.

Most respondents felt uncomfortable when giving out identification data.

2.0 METHODOLOGY

2.1 Data Collection

The data gathered from the survey results are be the main source of data collection for the report.

The questions of the survey are self-administered and in the cases when the respondents were un-

available due to time or place constraints, they had been contacted via email or telephone, for

their convenience. Reference material for the report has been collected from credible and

qualified journals, articles and reports. Data consolidation has been carried out in numerous

ways, all elucidated below.

Consumer trust and perceived risk in B2C e-commerce | 5

2.1.1 Primary Sources

The primary sources include the first-hand information gathered from the subjected sample

group. The data collected directly from the customers through questionnaires and interviews are

the primary set of information for the report.

2.1.2 Secondary Sources

The secondary sources include a relevant set of sample that would provide information about the

subjected sample. Pertinent data could be collected from sources like e commerce enterprises,

and families. Other information sources include the articles and journals we‟ve used for our

research, of renowned local and foreign origins, and thosewe have used for referencing.

2.2 Sampling Methods

Since the population size is too large and unevenly dispersed, it was very difficult to reach

relevant respondents. So for the purpose of our report, non-probabilistic convenience/accidental

and judgmental sampling method, limited only to Dhaka city, has been used.

2.3 Sample Size

The sampling technique used on a broad scale is non-probabilistic sampling followed by a

combination of judgmental and convenience sampling.

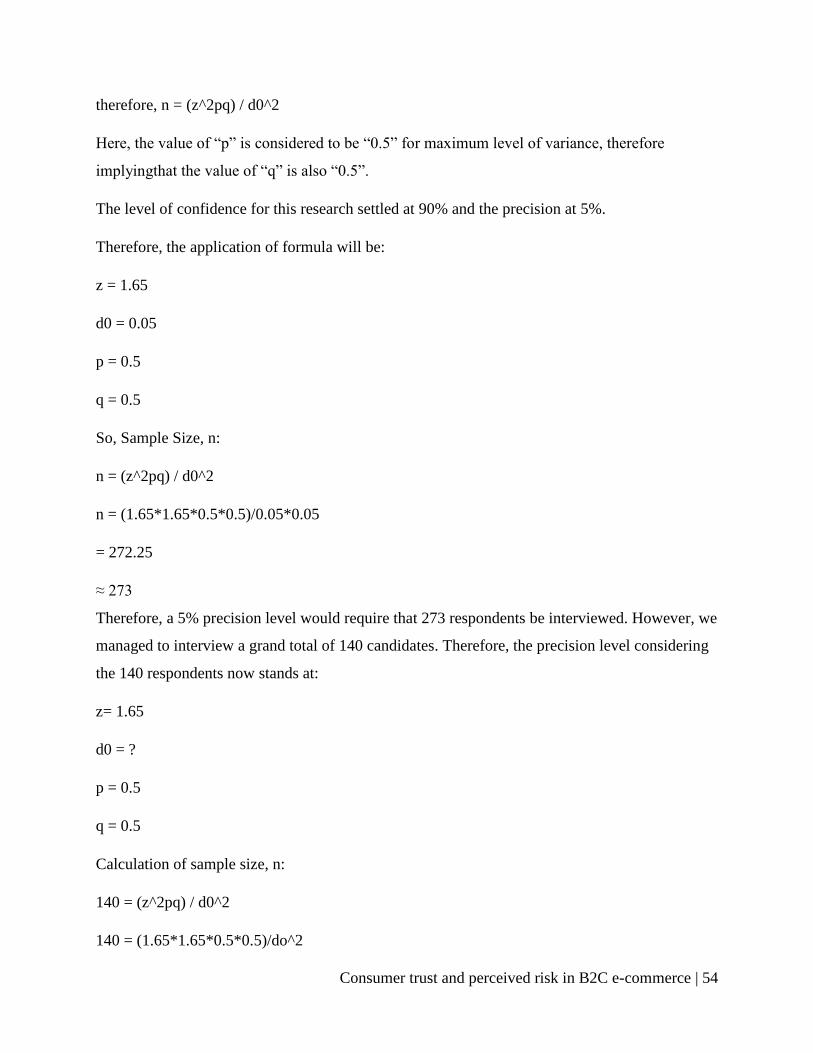

For calculating the sample size, we used statistical techniques (with a level of confidence at 90%

and the precision level at 5%) and found that a theoretical levelof 273 respondents needed to be

interviewed. (Refer to Appendix III: Calculations for detailed calculations of the sample size).

However, due to multiple limitations of time, money and accessibility, we were unable to reach

out to our theoretical sample size, and in the end, we have managed to gather a total of 140

respondents, out of whom 114 actually have been found to conduct purchases over the internet.

2.4 Sample Frame

For the purpose of our research it is impossible to know the sample frame mainly due to the

reason that an extensive portion of the population are internet users, it is improbable to determine

precisely how many may or may not transact over the net. However, as per BTRC (Bangladesh

Consumer trust and perceived risk in B2C e-commerce | 6

Telecommunication Regulatory Commission), there are currently 40,800,000 Internet users in

Bangladesh for June 30, 2014, with a 24.5% internet penetration.

2.5 Purpose of Research

The purpose of the report is to provide insights and evaluate the current situation of B2C e-

commerce in Bangladesh, with an emphasis on the reliability of online transactions, and

consumer perceptions.

2.6 Questionnaire Development

The survey instrument for collecting the data was a questionnaire primarily including mostly

closed-end questions, with a few open-ended ones. The questionnaire consisted of 6 sections.

Part A sought information about the Respondent‟s Orientation to E-commerce. It had been

designed to glean information of whether the respondent is aware of the e-commerce industry in

Bangladesh, and whether he/she uses it, and what is his/her overall perception of trust for it.

Part B was designed to know the Effect of Brand in Perceived Value and Trust. In this section

respondents were asked to indicate specifics about the online brands they purchase from, to rate

the brands, to deduce the percentage spending of respondents for E-commerce out of the total

purchase portfolio, and to mention about their brand preference. Likert scaling was developed

and used in this section to rate opinions regarding branded and non-branded providers, their

quality of products and the service associated with it on an ordinal scale. The Likert scale used is

a 10 point Likert scale(with 1 meaning strongly disagree and 10 meaning strongly agree). The

purpose of constructing a 10 point scale was to eliminate any bias towards central tendency.

Part C was designed to test the Effect of Site Reputation on Buying Intent. In this part there were

two open-ended questions on the name of websites respondents visit and on the percentage of

websites they visit are non-branded. There was also a question where we tested the extent to

which respondents were likely to purchase from a non-branded site, using a Likert scale. It was a

10 point Likert scale.

Consumer trust and perceived risk in B2C e-commerce | 7

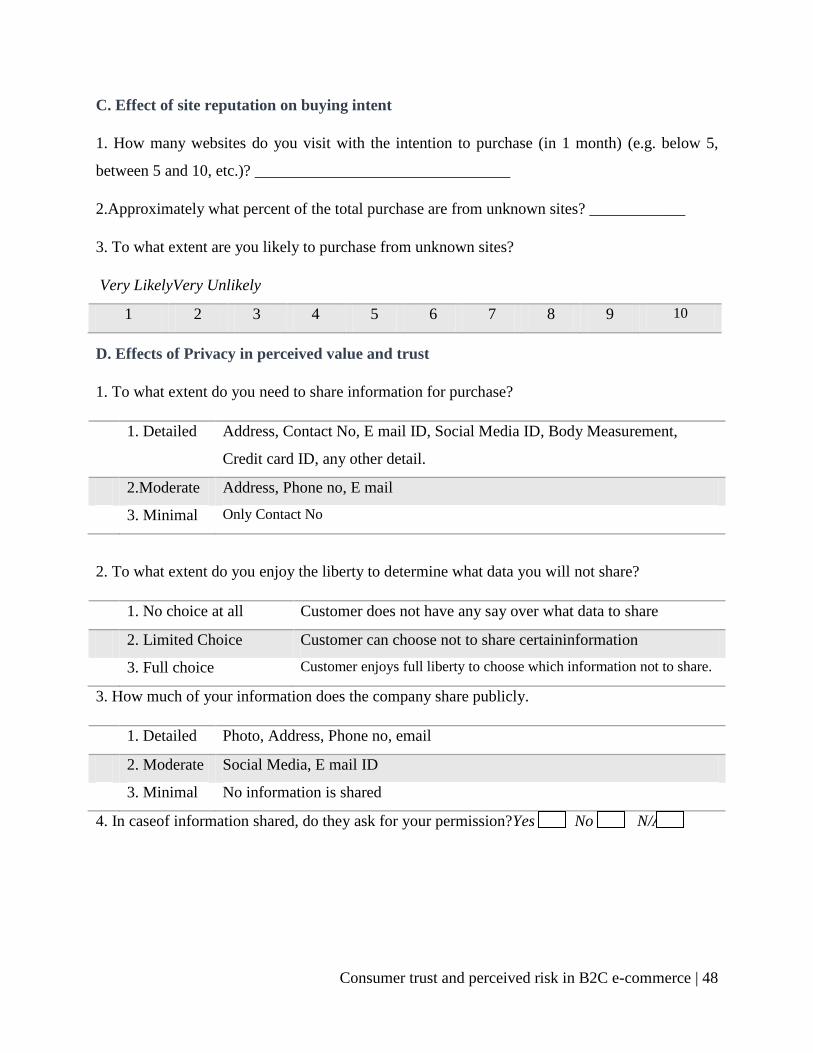

In Part D, we looked for Effects of Privacy in Perceived Value and Trust. The information we

sought include what information is shared and preferred to share, what extent of liberty is there

when it comes to share information, if and to what extent the private information is shared by the

providers publicly, if permission is sought by providers before sharing data, if there is any option

to be able to choose which data were to be shared, if the provider has a privacy policy, if the

privacy policy is effective, if there was any experience of victimization due to privacy violation,

if any rectifying measure was taken, if the measure was effective and if the measures are

satisfactory were the prime concern of this part.

In Part E, we looked into the Effects of Perceived Financial Risk. The prime concern for this part

were-

i) if the pricing was found beyond what it should be

ii) to what extent was the delivery charge justified

iii) what delivery charge method was there to follow

iv) what delivery method was actually preferred

v) if the provider allowed changing the product purchased

vi) to what extent does allowing to change the product affect purchasing habits

vii) how trustworthy was the pricing system.

In Part F, we simply sought generic Information about the Respondent. Specifically about their

gender, age, education level, current profession and monthly shopping budget.

2.7. Validity

A measure is valid if it measures what it is supposed to measure. In case of direct measures,

thevalidity is self-evident; and in case of indirect measures it is only approximate, e.g., indexes

and scales. In fact, there is no exact way to guarantee that an indirect measure is valid

formeasuring a concept.

We have used face validity to test the validity of the variables of this research. Face

validityimplies that the items chosen to measure a variable are logically related to it. From

theliterature reviews, we have logically determined the items to measure the variable.

Consumer trust and perceived risk in B2C e-commerce | 8

2.8. Reliability

Table 1: Reliability Statistics (Cronbach’s Alpha)

Cronbach's alpha is a measure of internal consistency that is, how closely related a set ofitems is

as a group. A "high" value of alpha is often used (along with substantive argumentsand possibly

other statistical measures) as evidence that the items measure an underlying (orlatent) construct.

However, a high alpha does not imply that the measure is one-dimensional.

If, in addition to measuring internal consistency, you wish to provide evidence that the scalein

question is one dimensional, additional analyses can be performed. Exploratory factoranalysis is

one method of checking dimensionality. Technically speaking, Cronbach's alpha isnot a

statistical test - it is a coefficient of reliability (or consistency).

A Cronbach‟s Alpha of 0.50 and above is considered to be reliable. Our Cronbach‟s

Alpha(Alpha Coefficient) for the 46 items is 0.502, suggesting that the items have

acceptableinternal consistency among them.

Table 2: Reliability Statistics (Cronbach’s Alpha and Split Half Technique)

Cronbach's Alpha Part 1 Value .879

N of Items 9a

Part 2 Value .733

N of Items 8b

Total N of Items 17

Correlation Between Forms .374

Spearman-Brown Coefficient Equal Length .544

Unequal Length .545

Guttman Split-Half Coefficient .482

Cronbach's Alpha Cronbach's Alpha Based

on Standardized Items

No. of Items

.502 .600 17

Consumer trust and perceived risk in B2C e-commerce | 9

a. The items are: Grade of Service, Likeliness to stick to the Brand in near future,

Branded Providers more reliable, Branded Providers provide better quality, Branded

providers price higher, Branded providers provide better service, Unlikeliness to

purchase from unknown sites, Does keeping from sharing info affects trust?, Liberty of

sharing info affects judgement.

b. The items are: The company keeps info private, The company asks permission before

sharing info, Privacy Policy Effective?, How effective the measures?, How satisfactory

are privacy measures?, How much is the transport charge justified, how do that affect

your trust?, how effective is the pricing system?.

Split half reliability is obtained by taking, at random, half of the variables in the scale,averaging

them into a single variable and then averaging the remaining half, and correlatingthe two

composite variables. The expected value for the random split-half reliability is alpha.It must be

noted that split-half reliability estimate is contingent upon how the items in thetest/scale are

arranged. Reordering of the items and/or regrouping of items in the test/scalecan result in

different reliability estimates using the split-half method. As we can see, thealpha values for the

two halves are .879 and .733 which means the data is reliable (asmentioned before alpha value

should be more than 0.5). Also, the different correlation coefficients suggest that the two halves

are positively correlated and significantly correlated.

Consumer trust and perceived risk in B2C e-commerce | 10

3.0 LITERATURE REVIEW

3.1 E-Commerce in Bangladesh:Bangladesh is a country that has very recently entered the

domain of e-commerce. Naturally, the e-commerce hasn‟t still developed optimally in

Bangladesh, with only 7% penetration, as per population (Mohiuddin, 2014). That being said, e-

commerce is growing at a rapid rate, as evidenced by the increasing transaction from BDT 0.450

million in 2012 to over BDT 2000 million in 2013 ((Mohiuddin, 2014).

3.2 Overview and Features of the E-commerce Industry:To give an insight on how the

current Internet Payments system security works, there are fundamentally two types of electronic

payments, namely the Internet Bank Card Payments System, E-cash internet payments system &

e-purse internet payments system and secondly, the electronic cheque internet payments system

(Jing, 2009). The safety elements are namely the integrity of the information, the validity of

information, the non-repudiation of information, the authenticity of the transaction status, and the

reliability of the system. Also, four different strategies can be considered for strengthening the

different internet payments systems, which are security strategy, legal protection, social moral

norms, and perfect management strategy.

To get a global perspective of countries ranked by e-commerce market size, we analyze

ATKearney‟s The 2013 Global Retail E-Commerce Index. This report lists down top 30

countries of the world in terms of their market size in e-commerce. They argue that countries go

up in the rank mostly because of solid infrastructural strength such as internet penetration,

prevalence of credit cards, and logistics strength for home delivery. However, the report does

recognize that consumers behavior plays a key role in determining the fluctuation in the market

share of e-commerce, e.g. we, Bangladeshis, are traditionally more inclined to shop in shopping

malls, but the increasing product prices and the option of online shopping has made us look

online for “best value” deals. From here, we can infer that perceived risk of e-commerce

transactions too can play a motivating factor for consumers to either opt more or less in the

world of e-commerce. It needs to be noted that the list contains mostly all countries in the world

that have exceptionally strong consumer protection laws.

Consumer trust and perceived risk in B2C e-commerce | 11

3.3 Perceived Risk and Trust factors in E-commerce: To illustrate our claims that security is a

concern for customers, a research paper by Zang and Dran, shows that amongst websites, users

would prefer only e-commerce sites based on howsecure data in the site is. The research paper

discusses the Kano model of customer satisfaction, and further discusses how the Kano Model

can be applicable for Website Quality Model. It explains that for any site to be successful it can‟t

be just only good in one category, but also in other categories that increases the overall quality of

the site.

In our research, we need to very specifically ask consumers that if provided that there is

infrastructural support, would they still be conducting e-commerce transactions in the absence of

strong regulatory or security frameworks. Zang and Dran could have had set up controlled

experiment to evaluate the efficacy of each elements of the websites that determined how high or

low quality a website is, which would have had given a clearer picture whether customer‟s

responses in surveys reflect well in actual websites by looking at their traffic. The ATKearney

report should have included the list of all the countries listed in the United Nations as per the

rankings of their market size of e-commerce. The report was guilty of not evaluating why other

countries are lagging behind in e-commerce, except for a brief case study on India. Thus their

report lacks insight for research on why e-commerce is not doing well in other countries. Jing‟s

suggestion on online security strategy seemed merely assertions, not an analysis on how these

strategies can be applied by e-commerce sites under various contexts, such as national rules and

regulations in countries where they are operating, ease and convenience of usage for consumers

if these strategies are implemented, etc.. Future researches should evaluate legal framework and

consumer trust as a factor for development of e-commerce, and propose newer and more secure

methods of online payment.

From the literature review it is deduced that, in order to measure consumer trust in e-commerce,

three parameters are needed to be considered –

a. Perception of Brand

b. Perception of privacy of information

c. Perceived financial risk

Consumer trust and perceived risk in B2C e-commerce | 12

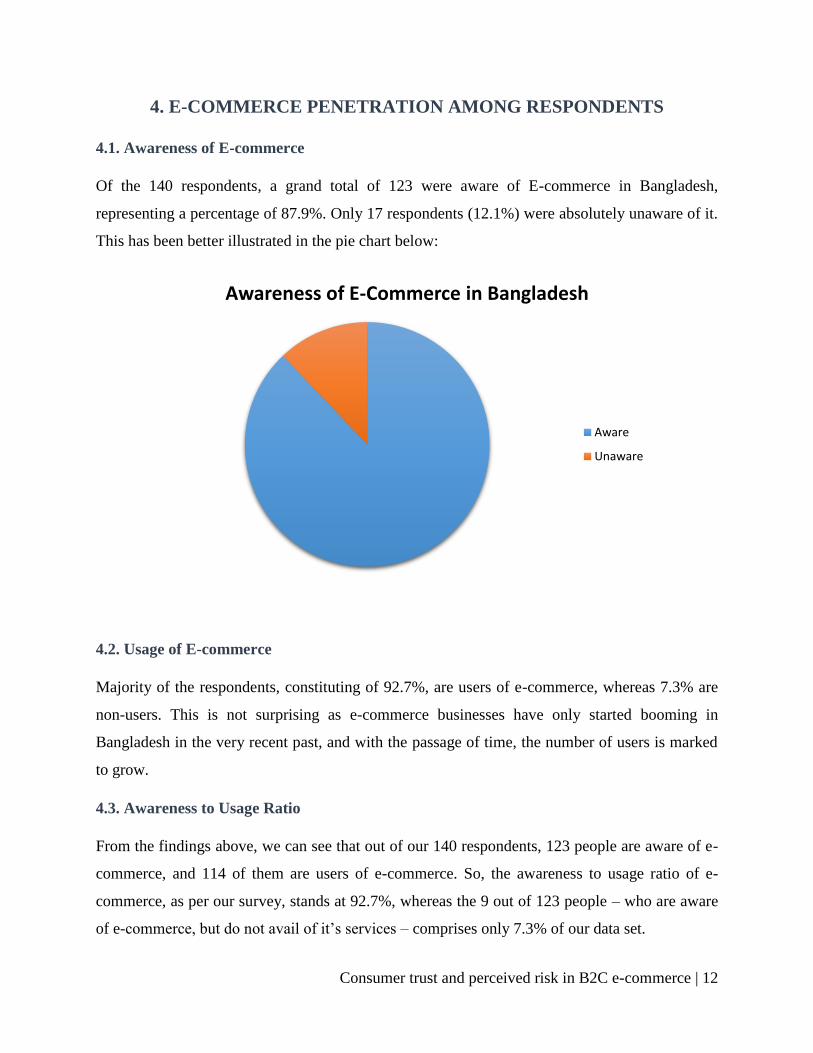

4. E-COMMERCE PENETRATION AMONG RESPONDENTS

4.1. Awareness of E-commerce

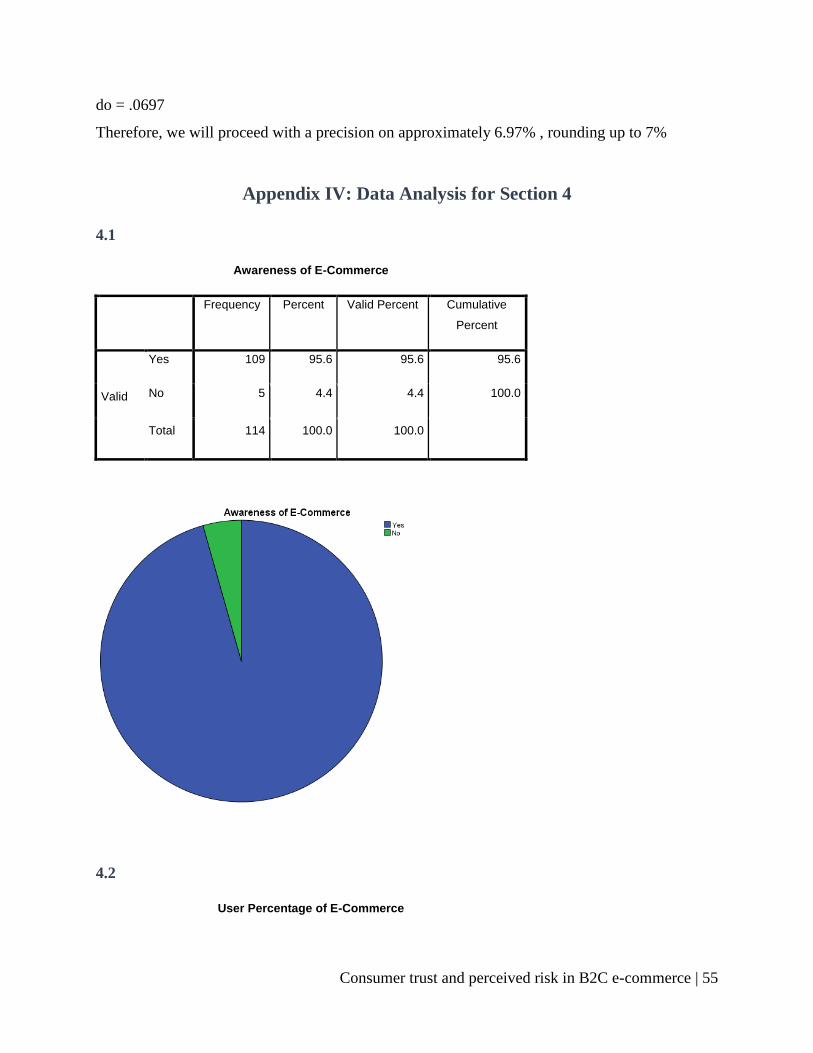

Of the 140 respondents, a grand total of 123 were aware of E-commerce in Bangladesh,

representing a percentage of 87.9%. Only 17 respondents (12.1%) were absolutely unaware of it.

This has been better illustrated in the pie chart below:

4.2. Usage of E-commerce

Majority of the respondents, constituting of 92.7%, are users of e-commerce, whereas 7.3% are

non-users. This is not surprising as e-commerce businesses have only started booming in

Bangladesh in the very recent past, and with the passage of time, the number of users is marked

to grow.

4.3. Awareness to Usage Ratio

From the findings above, we can see that out of our 140 respondents, 123 people are aware of e-

commerce, and 114 of them are users of e-commerce. So, the awareness to usage ratio of e-

commerce, as per our survey, stands at 92.7%, whereas the 9 out of 123 people – who are aware

of e-commerce, but do not avail of it‟s services – comprises only 7.3% of our data set.

Awareness of E-Commerce in Bangladesh

Aware

Unaware

Consumer trust and perceived risk in B2C e-commerce | 13

4.4. Percentage of Shopping Budget for E-commerce

From our survey data, we can infer that the mean shopping budget allocated to e-commerce by

users stands at 14.1% of their total monthly budget, whereas the modal percentage stands a t a far

lower value of only 5%.

This, again, is not unseemly, as people who do actually avail of e-commerce services, are

tentative about trusting this new form of marketing, and a lot of hesitance comes from the

preconceived skepticism about e-commerce.

For the ease of calculation, we have divided our response set into 3 categories of the percentage

of monthly budget spending on e-commerce, classified here as High (More than 70%), Medium

(30% to 70%) and Low (Below 30%). Only 4.6% of our respondents have a high percentage,

compared to 13.8% falling under the medium parameter, and an overwhelming 81.6% with a

monthly e-commerce budget below 30%.(Refer to Appendix IVfor detailed Frequency Analyses

Tables)

Consumer trust and perceived risk in B2C e-commerce | 14

5. DEMOGRAPHIC OF E-COMMERCE USERS

5.1. Gender

About 53.5% of our respondents are female, compared to only 46.5% of male respondents.

5.2. Age

The mean age of our respondents stands at 20.88 years. 11.5% of our respondents are below the

age of 18, whereas 8% are above the age of 24. The rest (80.5%) fall in the 18 to 24 age group.

5.3. Education Level

Education wise, 19 of our respondents, comprising 16.7% are non-graduates, i.e. have not

reached the undergraduate level yet. 74.6% are undergraduate students, and 8.8% are graduates.

This is expected, as majority of our respondents fall in the 18 to 24 age demographic, which is

the age group occupied by most undergraduates.

5.4. Profession

In the case of professions occupied by our respondents, a grand total of 76.3% are students,

compared to only 23.7% of jobholders. This is not totally unexpected, because the younger

generation is more technologically savvy than their predecessors; and not only that, as our survey

Education Level Demographic

Non-Graduate

Undergraduate

Graduates

Consumer trust and perceived risk in B2C e-commerce | 15

was completed mostly by non-graduates and undergraduates, it does make sense that most of

them are not officially employed yet.

6. PERCEPTION ON BRAND

Brand is a name, color, symbol, slogan or a combination of these that aims to create a distinct

identity of a particular offering. In terms of e-commerce, the concept of Brand is slightly

different from that of marketplace. Whereas in marketplace Brands usually represent

manufacturing companies, in e-commerce they represent both the manufacturers and the

retailers. For example, a manufacturing Brand like „Bata‟ can open its own webpage, or it can

sell its product through an established retail page like „Ekhanei.com‟.

Section B and section C from the questionnaire concentrated on consumers perceptions on

different aspects of Brands while shopping via e-commerce. Initially, questions related to

consumers‟ Brand orientation were asked to find out their preferences. Afterwards, survey was

performed to find out respondents‟ Brand loyalty, perception on product and service quality and

value for money.

6.1. Number of Brands perUser

Respondents were asked to answer the number of Brands they usually purchase from. Out of 114

e-commerce users, 96 purchases from 3 or less number of Brands, which is 84.2% of the total

respondent. The Mean number of Brands a user purchase from is 2.19 and the Mode is 2 brands

per person (35 respondents), followed by 1 Brand per person (33 respondents) and 3 Brands per

person (20 respondents). No respondent purchases from more than 7 Brands.(Refer to Appendix

VI for detailed Frequency Table with Histogram)

Consumer trust and perceived risk in B2C e-commerce | 16

Table 3: Number of Brands per User

Number of Brands Respondents (In Number) Respondents (In Percentage)

0 8 7

1 33 28.9

2 35 30.7

3 20 17.5

4 9 7.9

5 5 4.4

6 2 1.8

7 2 1.8

Total 114 100

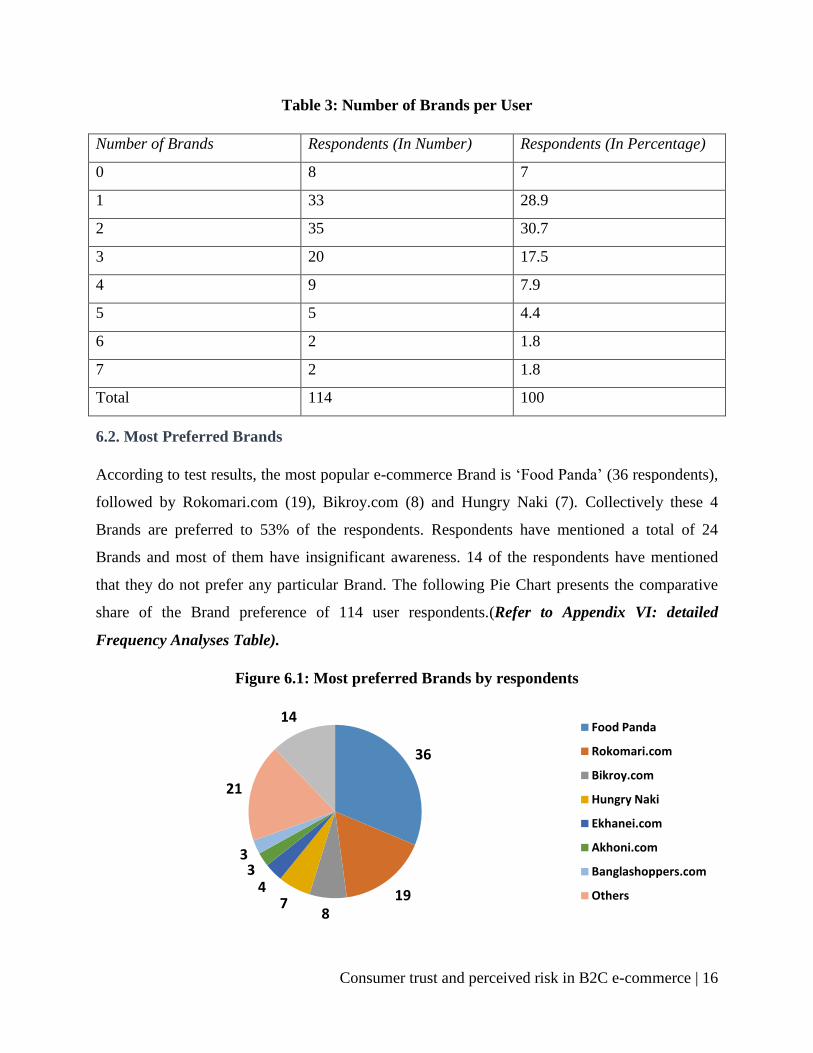

6.2. Most Preferred Brands

According to test results, the most popular e-commerce Brand is „Food Panda‟ (36 respondents),

followed by Rokomari.com (19), Bikroy.com (8) and Hungry Naki (7). Collectively these 4

Brands are preferred to 53% of the respondents. Respondents have mentioned a total of 24

Brands and most of them have insignificant awareness. 14 of the respondents have mentioned

that they do not prefer any particular Brand. The following Pie Chart presents the comparative

share of the Brand preference of 114 user respondents.(Refer to Appendix VI: detailed

Frequency Analyses Table).

Figure 6.1: Most preferred Brands by respondents

36

198

74

33

21

14Food Panda

Rokomari.com

Bikroy.com

Hungry Naki

Ekhanei.com

Akhoni.com

Banglashoppers.com

Others

Consumer trust and perceived risk in B2C e-commerce | 17

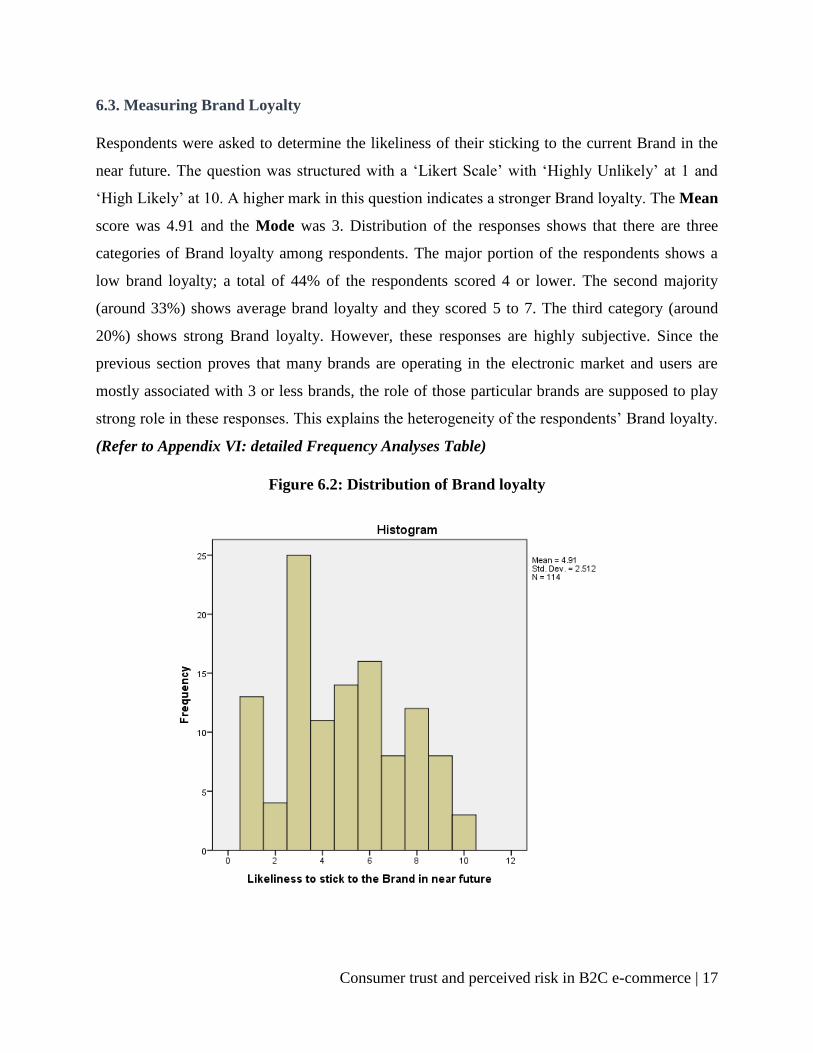

6.3. Measuring Brand Loyalty

Respondents were asked to determine the likeliness of their sticking to the current Brand in the

near future. The question was structured with a „Likert Scale‟ with „Highly Unlikely‟ at 1 and

„High Likely‟ at 10. A higher mark in this question indicates a stronger Brand loyalty. The Mean

score was 4.91 and the Mode was 3. Distribution of the responses shows that there are three

categories of Brand loyalty among respondents. The major portion of the respondents shows a

low brand loyalty; a total of 44% of the respondents scored 4 or lower. The second majority

(around 33%) shows average brand loyalty and they scored 5 to 7. The third category (around

20%) shows strong Brand loyalty. However, these responses are highly subjective. Since the

previous section proves that many brands are operating in the electronic market and users are

mostly associated with 3 or less brands, the role of those particular brands are supposed to play

strong role in these responses. This explains the heterogeneity of the respondents‟ Brand loyalty.

(Refer to Appendix VI: detailed Frequency Analyses Table)

Figure 6.2: Distribution of Brand loyalty

Consumer trust and perceived risk in B2C e-commerce | 18

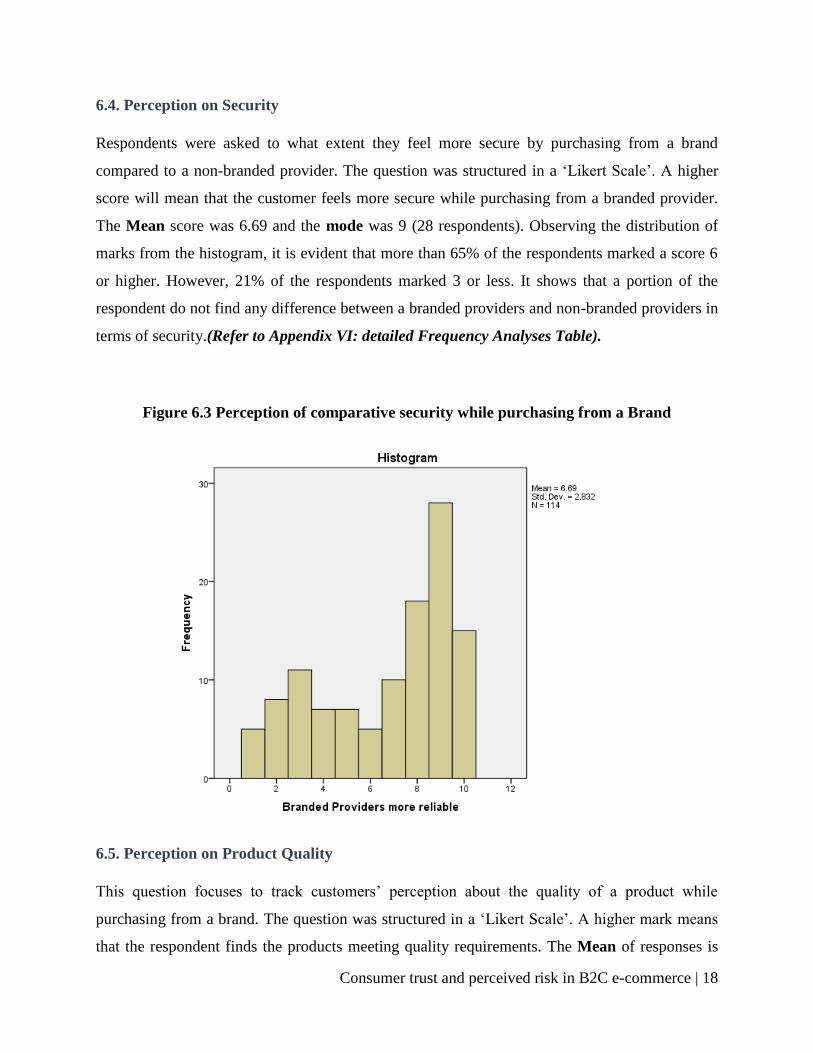

6.4. Perception on Security

Respondents were asked to what extent they feel more secure by purchasing from a brand

compared to a non-branded provider. The question was structured in a „Likert Scale‟. A higher

score will mean that the customer feels more secure while purchasing from a branded provider.

The Mean score was 6.69 and the mode was 9 (28 respondents). Observing the distribution of

marks from the histogram, it is evident that more than 65% of the respondents marked a score 6

or higher. However, 21% of the respondents marked 3 or less. It shows that a portion of the

respondent do not find any difference between a branded providers and non-branded providers in

terms of security.(Refer to Appendix VI: detailed Frequency Analyses Table).

Figure 6.3 Perception of comparative security while purchasing from a Brand

6.5. Perception on Product Quality

This question focuses to track customers‟ perception about the quality of a product while

purchasing from a brand. The question was structured in a „Likert Scale‟. A higher mark means

that the respondent finds the products meeting quality requirements. The Mean of responses is

Consumer trust and perceived risk in B2C e-commerce | 19

6.29 and the Mode is 8. This shows that, overall consumers are moderately satisfied with the

product quality. However, all the consumers are not homogenous in this regard. The major

portion (55.3%) marked 7 or higher. These are the people who can be termed as „satisfied‟. 20%

of the respondents scored 5 and 6. These are the people who are neither satisfied nor dissatisfied

with the quality of product. The rest 23% marked 4 or lower; these are the consumers who are

more dissatisfied with the quality of the product.(Refer to Appendix VI for detailed Frequency

Analyses Table).

Figure 6.4 Perception of product quality while purchasing from a Brand

6.6. Perception on Service Quality

Beside product quality, service quality is another significant measurement in e-commerce. This

section focuses to track customers‟ perception of service quality by „Likert Scale‟. A higher

score represents a more positive perception on service quality while purchasing from e-

commerce brands. The Mean is 6.29 and the Mode is 8. Furthermore,distribution of the scores

show that 65% of the respondents marked 6 or higher. This shows that the overall perception of

Consumer trust and perceived risk in B2C e-commerce | 20

service quality is high in the industry. (Refer to Appendix VI: detailed Frequency Analyses

Table).

Figure 6.5 Perception of service quality while purchasing from a Brand

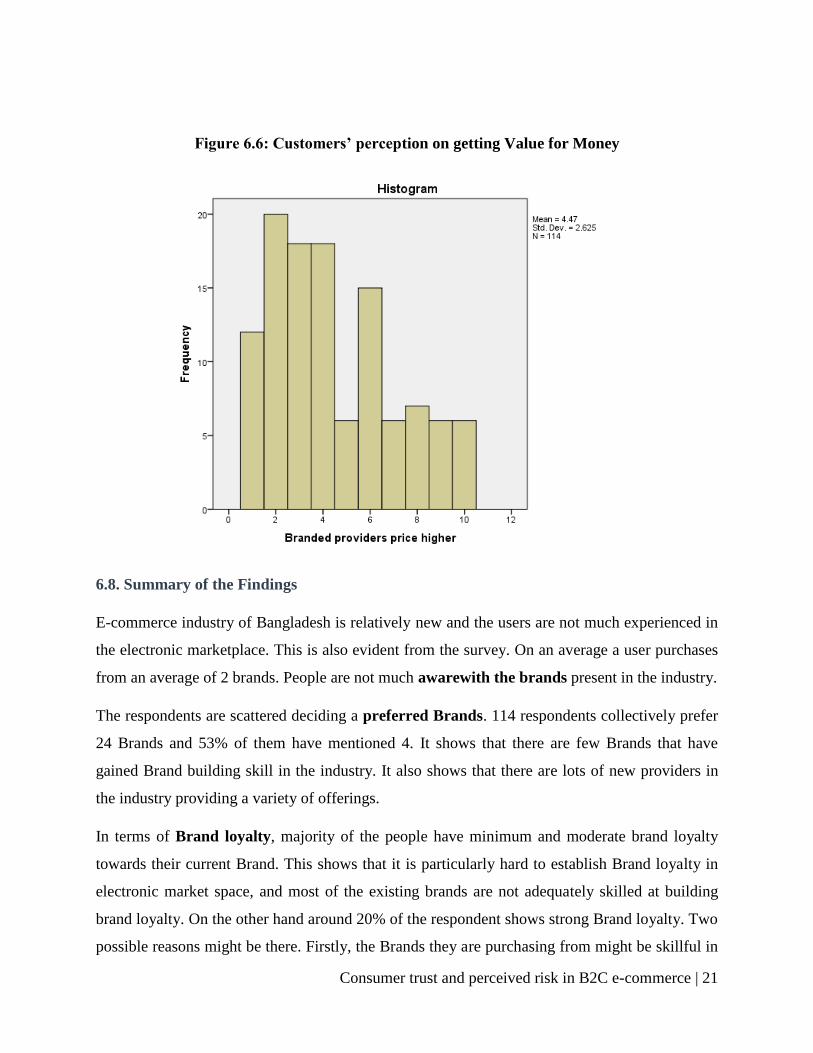

6.7. Perception on Value for Money

Though consumers are overall satisfied in the product quality and service quality provided by

Brands; they show dissatisfaction when it comes to the question of value for money. The term

„value for money‟ means the perception of getting the appropriate quality product in comparison

to the price paid to purchase it. A higher score in the Likert Scale means higher satisfaction.

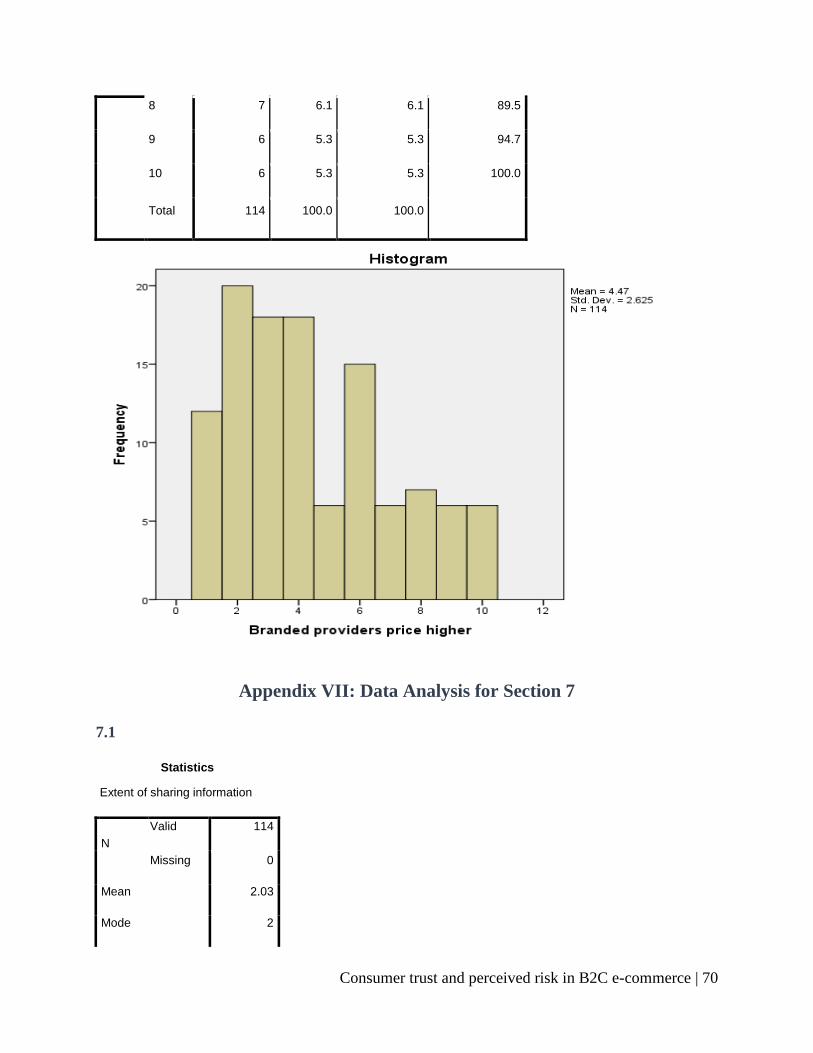

According to the responses of 114 users, the Mean score is 4.47 and Mode is 2. This certainly

shows that customers do not feel that they get the value for money. The following Histogram

shows the distribution of the responses.(Refer to Appendix VI: detailed Frequency Analyses

Table).

Consumer trust and perceived risk in B2C e-commerce | 21

Figure 6.6: Customers’ perception on getting Value for Money

6.8. Summary of the Findings

E-commerce industry of Bangladesh is relatively new and the users are not much experienced in

the electronic marketplace. This is also evident from the survey. On an average a user purchases

from an average of 2 brands. People are not much awarewith the brands present in the industry.

The respondents are scattered deciding a preferred Brands. 114 respondents collectively prefer

24 Brands and 53% of them have mentioned 4. It shows that there are few Brands that have

gained Brand building skill in the industry. It also shows that there are lots of new providers in

the industry providing a variety of offerings.

In terms of Brand loyalty, majority of the people have minimum and moderate brand loyalty

towards their current Brand. This shows that it is particularly hard to establish Brand loyalty in

electronic market space, and most of the existing brands are not adequately skilled at building

brand loyalty. On the other hand around 20% of the respondent shows strong Brand loyalty. Two

possible reasons might be there. Firstly, the Brands they are purchasing from might be skillful in

Consumer trust and perceived risk in B2C e-commerce | 22

building Brand loyalty. Secondly, to build loyalty it requires a minimum number of purchases,

these people might be used to purchasing from their current Brands for quite some time and more

loyal than other people.

Brand in E-commerce provide customers with a sense of security. On average the respondents

feels more secure while purchasing from a reputed Brand. This is normal for any business in any

form and the role of Brand is proved equally important in electronic market space.

In Product and ServiceQuality, majority of the people perceive Branded products to be of

better quality compared to a non-Brand product. However, though comparatively few in number,

some of the respondents disagree to this common phenomenon. The reason behind that is more

likely to be individual trait. It is established that many people think that they are not influenced

by Brands.

However, similar to usual marketplace e-commerce users perceive that they are not receiving the

appropriate level of value for the money they are paying.This is a general perception of the

consumers and it is same in the e-commerce field.

7. PERCEPTION ON PRIVACY OF INFORMATION

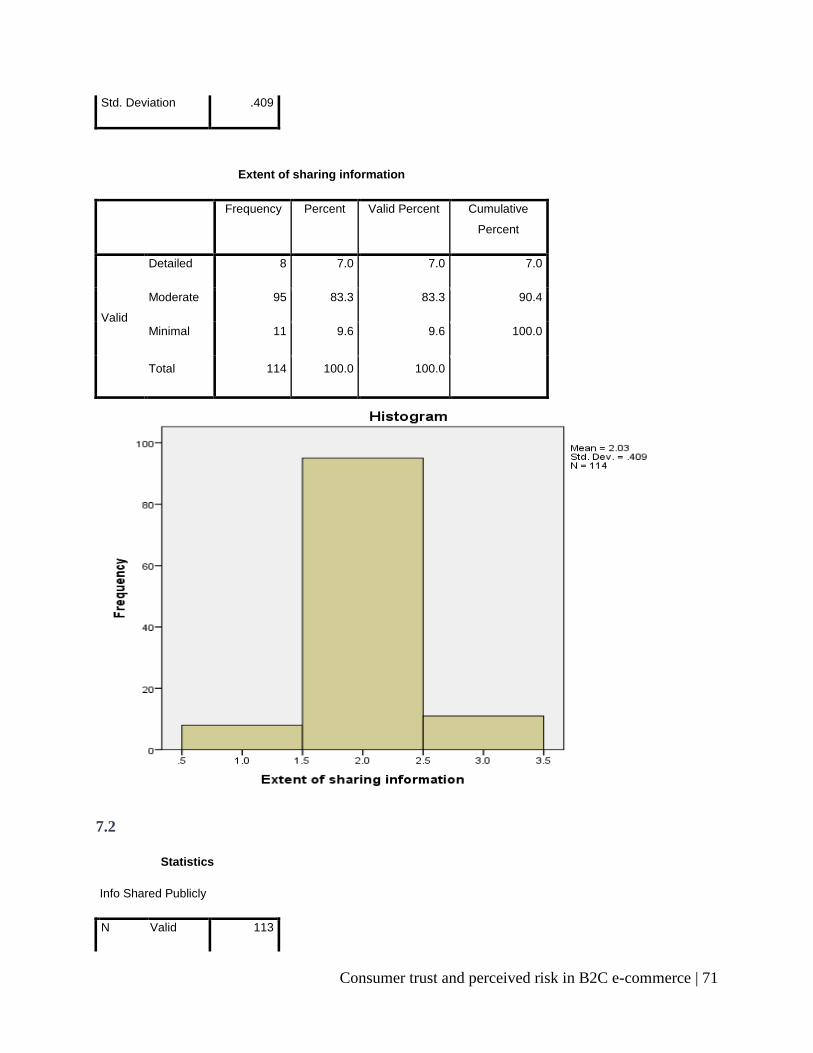

7.1. Level of Information Needed

Table 4: Level of information needed

Detailed Moderate Minimal Total

In Number 8 95 11 114

In Percentage 7 83.3 9.6 100

Our questionnaire had 3 levels defining the extent to which information was required by the e

commerce websites, namely detailed, moderate and minimal. Detailed entailed most of the

personal details such as address, contact number, e mail ID, social media ID, body measurement

(for clothing purchases), credit card ID, etc. Moderate information required included a few

selected details such as address, phone number, email ID, etc, while minimal required only a few

mandatory requirements such as the contact number or address necessary to deliver the

purchases. Findings reveal that the highest number of people (95 out of 114) stated that they

were required to share a moderate amount of information, which comprises of 83.3% of the

Consumer trust and perceived risk in B2C e-commerce | 23

respondents. 11 people or 9.6% said they were only asked for a minimal level of information

while 8 respondents or 7% declared that they were required to share details. The mode for this is

therefore number 2 (moderate information), as per the questionnaire arrangement.(Refer to

Appendix VII: detailed Frequency Analyses Table).

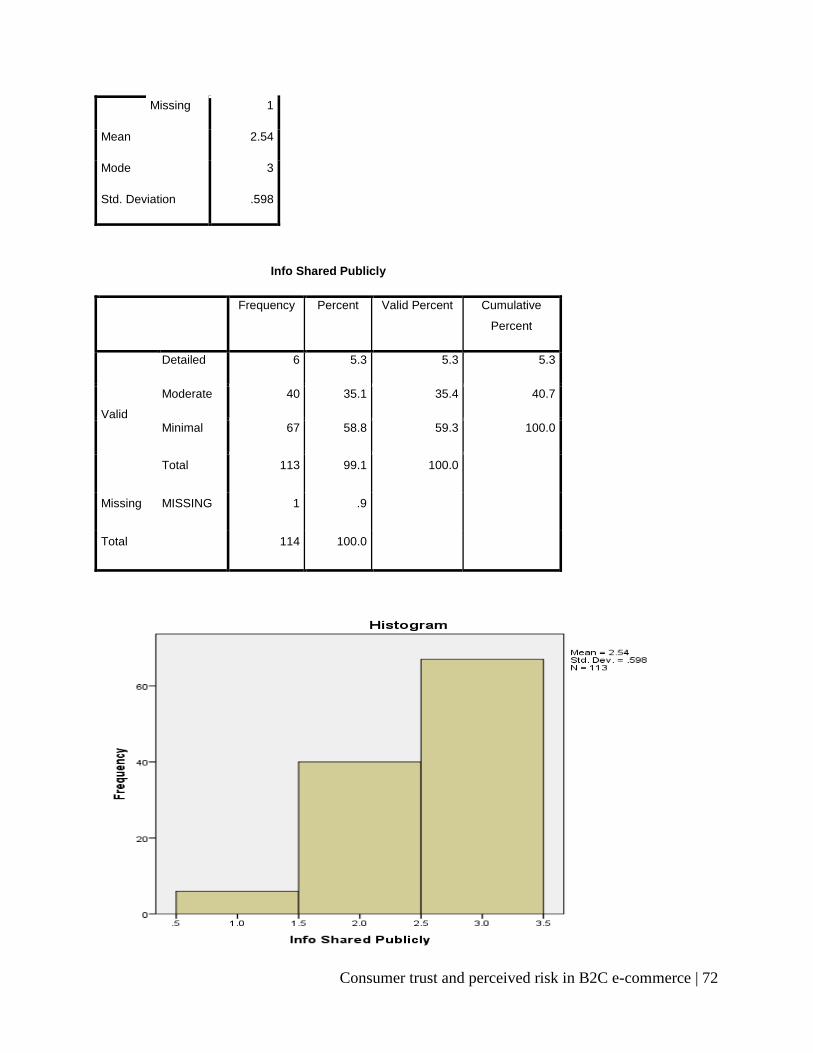

7.2. Level of Information Shared

Table 4: Level of Information shared

Detailed Moderate Minimal Total

In Number 6 40 67 113

In Percentage 5.3 35.4 59.4 100

Respondents were asked how much of their information the e commerce companies were sharing

publicly again using the 3 levels of detailed (Photo, Address, Phone no, email, etc), moderate

(Social Media, E mail ID) and minimal (little or no information shared). A majority of the

population replied that minimmal information was shared by the companies, and this is

representative of 67 or 59.4% of the sample population. 40 or 35.4% had moderate information

shared while 6 people or only 5.3% had more information revealed.

7.3. Customer Control over Information Sharing

Seeking of Permission

Yes No N/A Total

In Number 50 23 34 107

In Percentage 45.8 21.5 31.8 100

We asked the respondents if the service providers asked them for their permission before sharing

their information with others, and 45.8% comprising of 50 people, claimed that yes, the

providers did indeed ask for their consent. 21.5% or 23% responded negatively while 31.8% (34

people) marked the question as „not applicable‟. There is however, always a distinct possibility

that the service providers may be providing information to other companies such as insurance or

Consumer trust and perceived risk in B2C e-commerce | 24

telecom companies trying to recruit customers, without the consumers‟ knowledge. .(Refer to

Appendix VII for detailed Frequency Analyses Table)

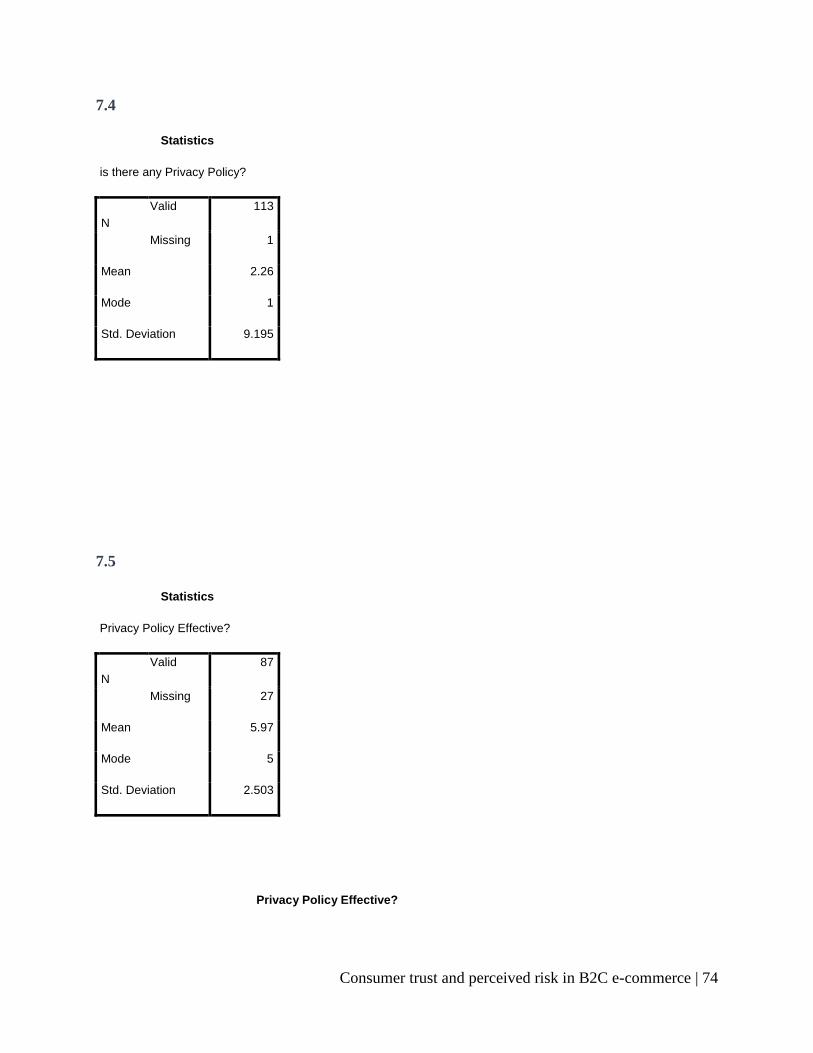

7.4. Awareness about Privacy Policy

Table 6: Awareness about Privacy Policy

Yes No Total

In Number 68 44 113

In Percentage 60.2 39.8 100

Respondents were asked if their providers had a privacy policy, and 60.2% responded that their

providers did indeed have a privacy policy, while 39.8% of the sample population stated that

their provider did not have any such policy. It seems that around 3/5th

of the population are

aware of their providers‟ policies regarding privacy.(Refer to Appendix VII for detailed

Frequency Analyses Table).

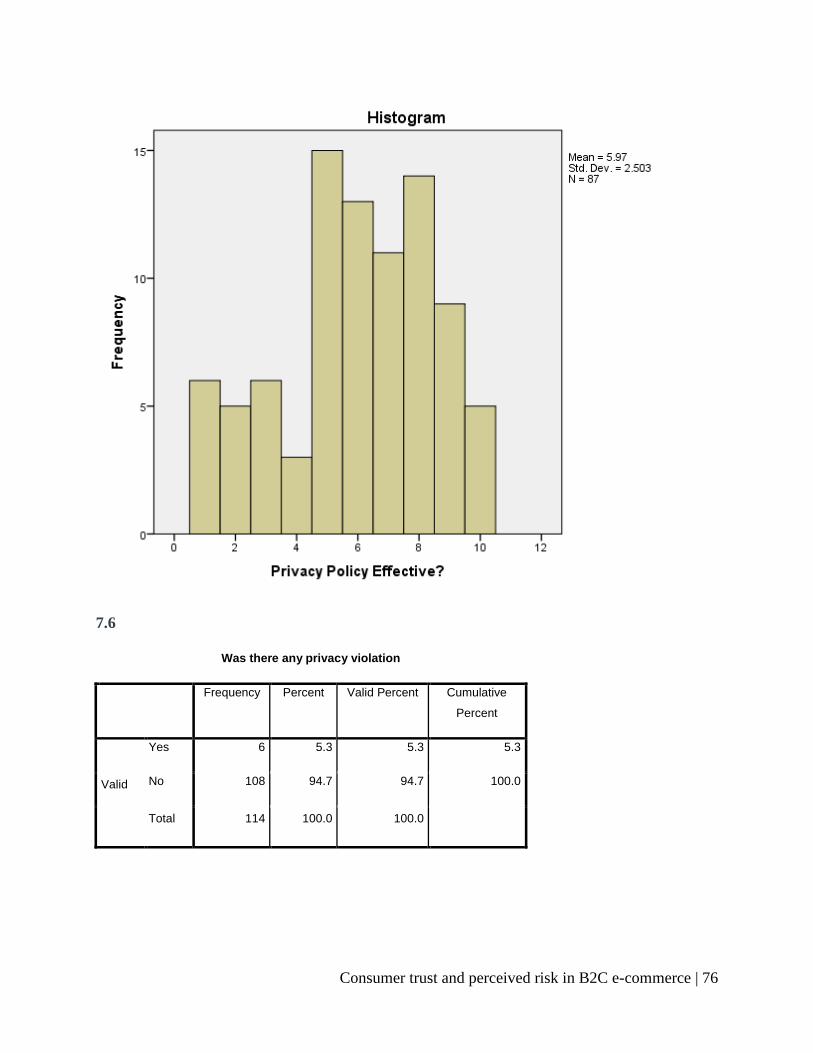

7.5. Perception on Effectiveness of Privacy Policy

The distribution of the respondents‟ marked answers is presented below:

Table7 : Effectiveness of Privacy Policy

Frequency Percent Valid Percent Cumulative Percent

Valid

1 6 5.3 6.9 6.9

2 5 4.4 5.7 12.6

3 6 5.3 6.9 19.5

4 3 2.6 3.4 23.0

5 15 13.2 17.2 40.2

6 13 11.4 14.9 55.2

7 11 9.6 12.6 67.8

8 14 12.3 16.1 83.9

9 9 7.9 10.3 94.3

10 5 4.4 5.7 100.0

Consumer trust and perceived risk in B2C e-commerce | 25

Total 87 76.3 100.0

Missing MISSING 27 23.7

Total 114 100.0

When inquiring as to whether the respondents found their providers‟ privacy policies effective,

we provided a likert scale so as to signify the extent to which they thought the privacy policies

were found effective, 1 being very ineffective and 10 being very effective. The mode here is a

rating of 5, by 13.2% of the population, although the mode is not staggeringly distinct. A not too

distant 12.3% rate their providers as 8. 6 people or 5.3% find the policies absolutely ineffective

while 5 people or 4.4% find it very effective. Other statistics are shown in detail in tabulated

form above. The bar chart below demonstrates the same information, showing that most people

have actually rated the effectiveness to be between 5 and 9.

Consumer trust and perceived risk in B2C e-commerce | 26

7.6. History of Privacy Violation

Table 8: History of Privacy Violation

Yes No Total

In Number 6 108 114

In Percentage 5.3 94.7 100

We asked our respondents if they had any record of being victimized by any privacy violation.

Statistics show that only 6 out of the 114 replied in the affirmative, while 96.7% of the

population had no prior experiences in this field. This provides an overall positive light on the e

commerce sector, since a considerably small portion of the population have actual instances of

being victimized in case of their privacy rights.(Refer to Appendix VII for detailed Frequency

Analyses Table).

7.7. Measure taken for Privacy Violation

Table 9: Measure taken from Privacy Violation

Yes No Total

In Number 5 1 6

In Percentage 83.3 16.7 100

For those who replied positively to being victimized, we inquired as to whether any measures

were taken to correct the privacy violation. 5 out of the 6 said yes (83.3%) while only 1 said no.

Again, it reflects positively that out of the 6 people who experienced a violation of their privacy,

5 people had affirmative actions taken on their behalf.

7.8. Summary of the Findings

Our inquiry into the perception of privacy of information reveals that most online sites require a

moderate amount of information from their consumers, and that majorly only a minimal amount

of this information is shared publicly. Nearly half of these respondents claim that the service

providers ask them for their permission before sharing any information and around 3/5th

of this

sample population is aware of the privacy policies by their providers. When asked to rate the

effectiveness of this privacy policy on a scale of 1 to 10, the results were diverse, the highest

frequencies occurring between 5 and 9 with 1 being very ineffective and 10 being very effective.

Consumer trust and perceived risk in B2C e-commerce | 27

Only 6 out of 114 have a history of privacy violation and 5 out of these 6 respondents have also

had corrective measures taken on behalf of them by providers.

Consumer trust and perceived risk in B2C e-commerce | 28

8. PERCEPTION ON FINANCIAL RISK

The consumer perception regarding pricing can have a powerful effect on purchasing decisions

and so it was important for this research to deduce the overall perception regarding pricing of e-

commerce transactions. The respondents were asked a number of questions in this section to

overview their perception on the pricing system, freight cost and over-pricing tendency in e-

commerce purchases.

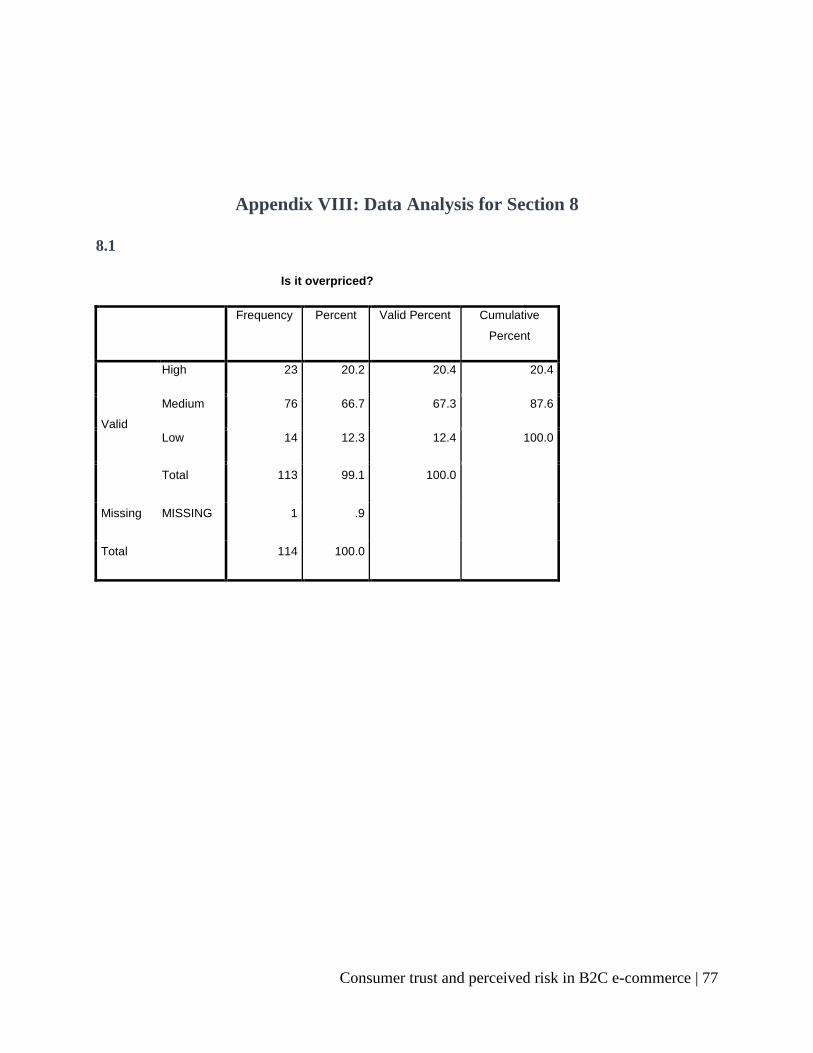

8.1. Perception on being overpriced

The respondents were asked to rank to what extent they perceived over-pricing occurred in e-

commerce transactions, with options ranging from „low‟, „medium‟ and „high‟. The mode

response to the question was „medium‟ extent of over-pricing was perceived, with 76

respondents or 67.3% of the respondents choosing this. On the other hand, nearly one-fifth (20.4

% of total respondents) felt that a „high‟ degree of over-pricing occurred, and the rest (12.4% of

total respondents) felt that the over-pricing was actually „low‟. The overall perception was that e-

commerce transactions were to a certain extent over-priced and this perception is ingrained into

customer minds. (Refer to Appendix VIII for detailed Frequency Analyses Table).

Table 10: Perception of being overpriced

High Medium Low Total

In Number 23 76 14 113

In Percentage 20.4 67.3 12.4 100

8.2. Preferred Method of Freight Cost

Currently, there are two methods of charging freight cost, or delivery cost, for the goods

transported in e-commerce transactions. One method charges consumers a fixed amount of

freight cost per transaction, and the other method charges consumers a certain percentage of the

cost of the products purchased. Respondents were asked which method they preferred while

conducting e-commerce transactions, and most of them (86.7% of total respondents) preferred to

have a fixed charge of freight cost per transaction. The rest 13.2% of respondents preferred the

percentage basis costing of freight. This may indicate a tendency of buying in bulk so as to offset

Consumer trust and perceived risk in B2C e-commerce | 29

the disadvantages of fixed freight cost.(Refer to Appendix VIII for detailed Frequency Analyses

Table).

Table 11: Preference of Freight method

Fixed Percentage based Total

In Number 99 15 114

In Percentage 86.8 13.2 100

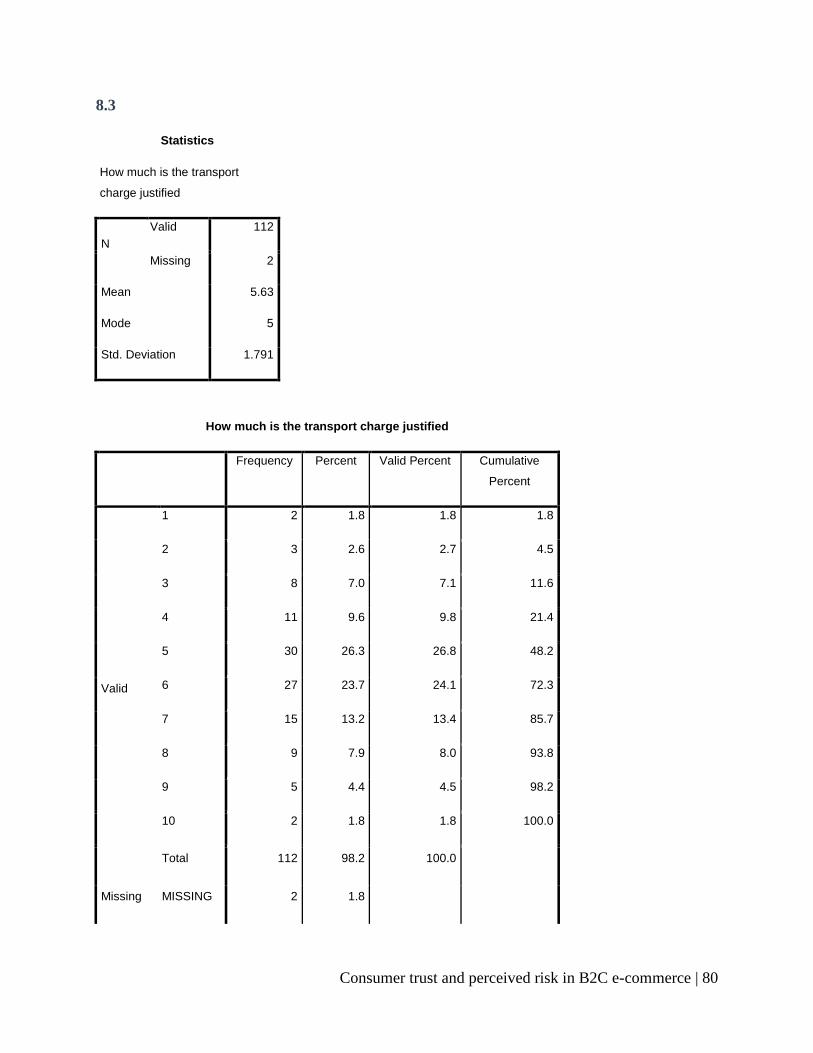

8.3. Perception on Freight Cost

Perception on freight cost can impact consumer buying behavior in e-commerce transactions.

The research thus asked respondents to rank their perception of freight cost – to what extent they

felt it was justified to charge as much as they did. The mean (5.63) and mode (5) were essentially

equal and revealed that consumer perception was essentially in the middle, with most people

feeling that freight cost was somewhat justified but not completely so. The distribution table

generated from the data for this question was almost a normal distribution curve. (Refer to

Appendix VIII for detailed Frequency Analyses Table).

Consumer trust and perceived risk in B2C e-commerce | 30

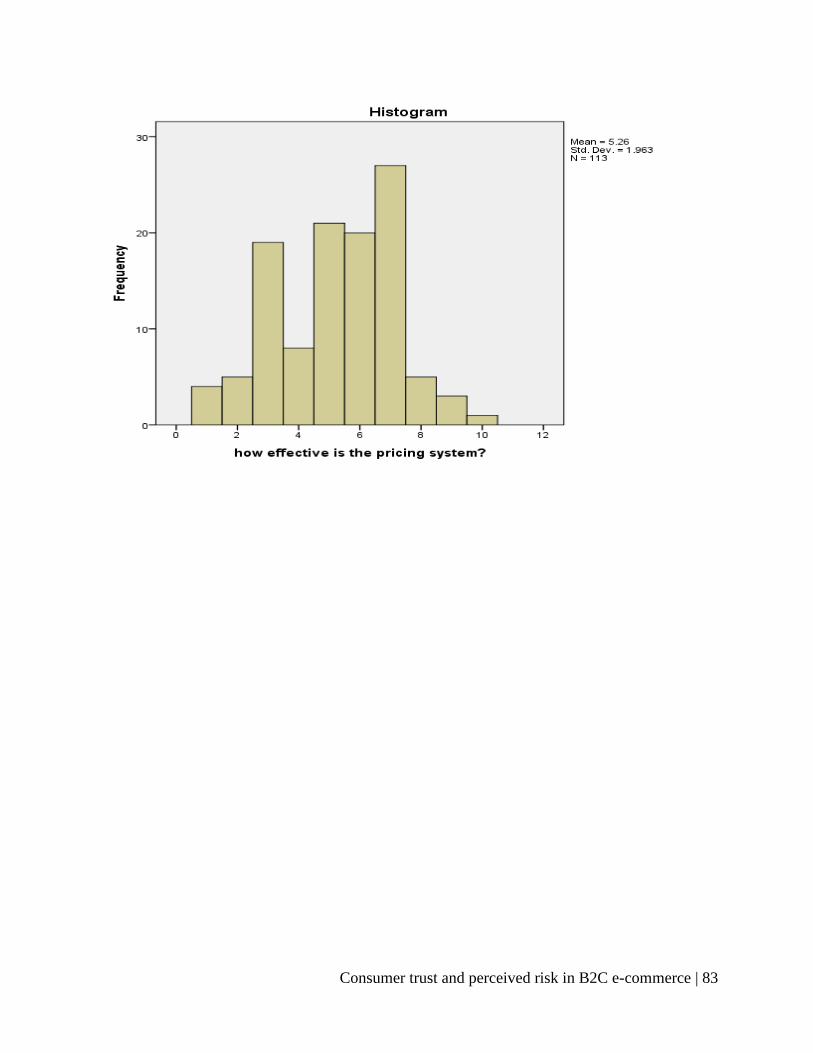

8.4. Overall Perception on Pricing System

Finally, the consumers were asked about their overall perception regarding the pricing system in

online transactions, and were asked to rank this from 1 to 10, with ten being most positive and

one being least positive. The mean response for this was 5.26 while the mode was 7. Hence, we

can deduce that most people felt that that the overall pricing system was slightly more than

acceptable and the average respondent felt that it was at least acceptable. However, although the

curve is skewed towards the more positive side of the responses, there is also a peak at the less

positive side, indicating there are pockets of dissatisfaction with the pricing system as well.

(Refer to Appendix VIII for detailed Frequency Analyses Table).

8.5. Summary of Findings

This part of the research has revealed a number of consumer insights. Most consumers (67.3% of

total respondents) felt that online transactions incurred a „medium‟ element of over-pricing and

one fifth (20.6%) felt that that element was „high‟. Consumer perception seems to be that online

transactions include some form of over-pricing, and this may be an important aspect to mitigate

if e-commerce businesses wish to garner trust from consumers.

Consumer trust and perceived risk in B2C e-commerce | 31

In case of freight cost, nearly everyone (86.8 of total respondents) felt that fixed freight cost

pricing was more preferable to percentage pricing. In general, the perception regarding freight

cost was that it was more or less justified, with a mean and mode of approximately 5 out of 10.

Consumer tendency to prefer fixed freight cost may indicate an affinity for bulk buying to

minimize the cost per transaction.

Overall, the perceptions regarding the pricing system in online transactions are positively

skewed in this research. This is contrary to the perception that a medium extent of over-pricing

exists in e-commerce transactions. This may indicate that consumers expect a certain level of

over-pricing for the benefit of shopping at home, and this may leave room for price sensitive

marketing by online businesses.

9. EFFECT OF BRAND, PRIVACY AND FINANCIAL RISK ON

CONSUMER TRUST

Hypothesis 1: Brand image positively affects a consumer’s trust

H0: µ ≥ 5; the perception of Brand image does not positively affect a consumer‟s trust.

Ha: µ < 5; the perception of Brand image positively affects a consumer‟s trust

Now,

Statistics

Likeliness to

stick to the

Brand in near

future

Branded

Providers

more reliable

Branded

Providers

provide

better quality

Branded

providers

price higher

Branded

providers

provide

better service

N

Valid 114 114 114 114 114

Missing 0 0 0 0 0

Mean 4.91 6.69 6.29 4.47 6.29

Consumer trust and perceived risk in B2C e-commerce | 32

Mode 3 9 8 2 8

Std. Deviation 2.512 2.832 2.541 2.625 2.523

We shorten the four Likert scale variables, take their mean, and from their distribution, derive the

hypothesis test through one sample t test.

One-Sample Statistics

N Mean Std.

Deviation

Std. Error

Mean

Effect of Brand

image in Buying

Intention

5 5.730

0 .97581 .43639

One-Sample Test

Test Value = 5

t df Sig. (2-

tailed)

Mean

Difference

90% Confidence Interval of

the Difference

Lower Upper

Effect of

Brand

image in

Buying

Intention

1.673 4 .170 .73000 -.2003 1.6603

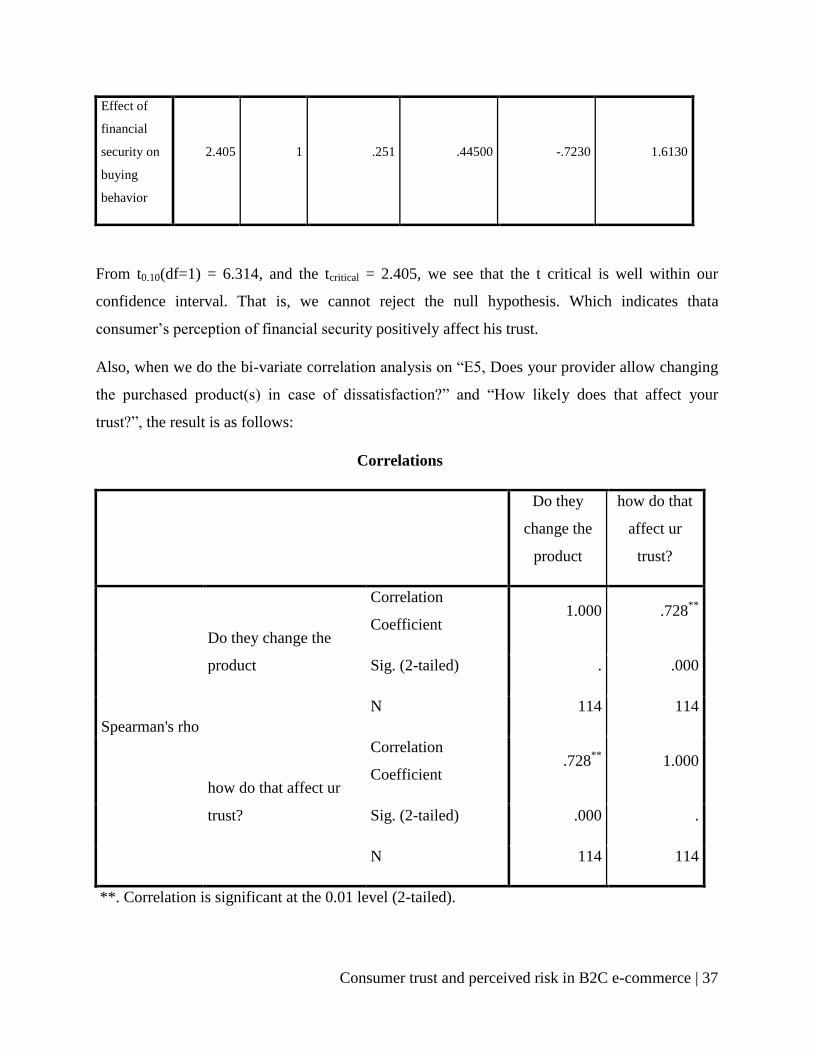

Consumer trust and perceived risk in B2C e-commerce | 33

From t0.10(df=4) = 2.776, and the tcritical = 1.673, so we see that the t critical is well within our

confidence interval. That is, we cannot reject the null hypothesis. Which indicates, A consumer‟s

perception of high brand image positively affects his trust.

Also, correlating „percentage of purchase from branded providers‟ and „percentage of purchase

from non-branded providers‟ gives us the following results:

Correlations

% Purchase

from

Branded

% Purchase

from Non-

Branded

% Purchase from

Branded

Pearson

Correlation 1 -.361

**

Sig. (2-tailed) .000

N 114 114

% Purchase from Non-

Branded

Pearson

Correlation -.361

** 1

Sig. (2-tailed) .000

N 114 114

**. Correlation is significant at the 0.01 level (2-tailed).

We can see that the correlation coefficient is -0.361, meaning that there is a negative correlation

between purchasing from branded and non-branded providers. This also indicates that perception

of high brand Image positively affects a customer‟s trust.

Consumer trust and perceived risk in B2C e-commerce | 34

Hypothesis 2: A consumer’s perception of high privacy of information positively affects his

trust

As the Likert scale goes up, the perceived positive affect increases.

H0: µ ≥ 5; the perception of high privacy of information positively affects trust.

Ha: µ < 5; the perception of high privacy of info does not positively affect trust.

Now,

Statistics

Does 'not

sharing info'

affects trust?

Liberty of

choosing to

share info

affects trust

The company

keeps info

private

The company

asks

permission

before

sharing info

Interpretation

N

Valid 113 113 113 113 From „Seems

Untrustworth

y‟ to Seems

trustworthy