1

Religion and Takeovers

Hua Xin

Rutgers University

Abstract

This study examines whether religiosity at the county level will influence the firms take

over decision. I find robust evidence that firms headquartered in counties with higher levels of

religiosity exhibit lower risky take over decisions. This finding is consistent with the view that

religion, as a set of social norms, helps to curb risky activities by managers.

2

Religion and Takeovers

1. Introduction

I examine the association between religiosity and a firm’s acquisition-investment decisions.

The prediction is that managers of firms located in religious counties pursue less risky

acquisitions and have more money to compensate shareholders. Our study builds on the

argument that religiosity, which has a significant impact on human behavior, also has a

significant impact on constraining opportunistic behavior by managers, particularly their

investment decisions (Ball, 2001; Watts, 2003; Ball and Shivakumar, 2005).

The impact of religiosity on human behavior was first documented in the psychological

literature (Cornwall 1989; Layman et al. 1997a, 1997b), which found its way to the economics

literature, where it is especially documented that religiosity has a significant influence on

individuals’ economic decisions (e.g. Bruce, 1993; Stern et al. 2000; Schultz et al. 2000; Gardner

et al. 2002). Lately, several studies in finance and accounting have also examined whether

religiosity has influence on finance and accounting decisions. The finance literature documents

that managers are more cautious about risky investment projects (Hilary and Hui, 2009). In

another recent study, Callen and Fang (2013) document that the financial crisis has been more

severe in areas with low religiosity, suggesting that religiosity played a significant impact on

human behavior that led to the financial crisis in certain non-religiosity areas. In the accounting

literature, McGuire et al. (2012) document that religiosity is negatively associated with earnings

manipulation through discretionary accrual, whereas Dyreng, et al.(2012) document lower

restatements by firms with headquarters in high religiosity counties. The existing literature thus

provides theoretical justification that behavioral and social norms influenced by religiosity foster

sound moral judgment and ethical behavior in firms (e.g. Weaver and Angle 2002) and also

3

provides empirical evidence that firms with headquarters in high religiosity counties display few

financial reporting irregularities as measured by accounting risk and accounting restatements (e.g.

McGuire, et al. 2012; Dyreng, et al, 2012).

In this study, I extend an examination of the impact of religiosity in acquisition and show

how it influences managers investment decision making and hence dividends. I argue that higher

religious beliefs in a community in which a firm operates will have a significant impact on

human behavior of individuals associated with the firm, which in turn will have a significant

impact on mergers and acquisition decisions. I especially argue that the following factors

associated with religiosity especially reduce risk taking: First, it is argued that religiosity that

has a significant impact on individuals’ ethical behavior creates environment where managers are

more conservatism, they are less risky taking and will be less likely to onverpay for target

companies and undertake value-destroying mergers. Lower discretionary accruals by firms in

high religiosity counties is especially documented by McGuire et al. (2012), and reduction in

fraudulent accounting practices and restatements are documented by Dyreng, et al. (2012). Risk

aversion in the decision making process suggests that firms will choose project which will have

higher potential for success and lower probability for project failure. I argue that higher risk

aversion will result in high assurance for managers on the mergers.

Second, it is argued in the literatures that CEO overconfidence about their future cash flows

may create firm value along some dimensions (i.e. by counteracting risk aversion, inducing

entrepreneurship, allowing firms to make credible threats, or attracting similarly-minded

employees), and engages in mergers that do not warrant the paid premium. I therefore argue that

religiosity creates the environment in which managerial opportunistic behavior is discouraged

and this will reduce risky acquirers.

4

Third, much of the literature focuses on the efficiency gains from mergers (e.g., Lang, Stulz,

and Walkling, 1989; Servaes, 1991; Mulherin and Poulsen, 1998). Religiosity, instead, is closest

to agency theory (Jensen, 1986; Jensen, 1988). Empire-building predicts heightened

acquisitiveness to the detriment of share holders, especially given abundant internal resources

(Harford, 1999). However religious CEOs, unlike traditional empire-builders, believe that they

are acting in the interest of shareholders, and are less likely to select risky projects in considering

the long term profit.

The above arguments that religiosity encourages mangers to be conservatism, less

overconfidence and more long term profit consolidation in firms with their headquarters in high

religiosity areas are also supported by the findings of a study by Grullon, et al. (2010), who

report that firms located in counties with high religiosity values show lower potential for class

action securities lawsuits, are less likely to encourage managers to engage in backdating options

and grant excessive compensation packages to managers, and discourage managers to engage in

aggressive accounting. Based on these arguments and evidence, I present lower merger premium

and thus I expect a negative association between religiosity and acquisition premium. In other

words, I expect comparatively lower acquisition premium for firms with headquarters in high

religiosity counties.

I conduct additional analyses to examine the impact of level of acquisitions on the

association between acquisition premium and religiosity. I examine whether the impact of

religiosity will differ if the level of acquisition is low or high. It is argued in the literatures that

at paying high acquisition premia is value destroying for acquirer shareholders (Laamanen 2007).

Thus, I hypothesize that the association between religiosity and acquisition premium is stronger

for firms with high acquisition premium.

5

Second, I conduct the impact of religiosity on dividend payment. I argue that the managers

with high religious beliefs will challenge agency theory; religious CEOs are more likely to act in

the interest of shareholders and are willing to take the less risky project in the long run. Thus, I

expect to see the association between religiosity and acquisition premium will be moderated if a

firm pays high dividends. So I hypothesize that the association between acquisition premium and

religiosity is stronger for firms with high dividends payment.

Third, I examine the influence of religiosity on goodwill write off. It is argued and

documented in the literatures acknowledge the possibility that management might be

appropriately exercising reporting discretion to reflect deteriorating economic conditions.

(Francis, Hanna, and Vincent (1997). Risk aversion in the decision making process suggests that

firms will choose project which will have higher potential for success and lower probability for

project failure. I argue that higher risk aversion will result in more conservative in M&A

decisions, and will trigger more timely good will write offs afterwards.

In addition to the above analyses, I also examine (1) whether the association between

acquisition premium and religiosity will be impacted within different industries. (2) the

volatility of stock returns, debt ratio; ROA will have an impact on the association between

acquisition premium and religiosity. (3) the target firm takeover factors and state takeover

defenses and target firm religiosity scores have an impact on the acquirer takeover premium.

Our main tests are based on data obtained from the American Religion Data Archive (ARDA)

for the period from 1971-2010. To evaluate the robustness of our findings, I also conduct tests

based on data compiled by the Gallup during 2008-2010. I use the latest acquisition premium

model to conduct regression analyses on the association between acquisition premium and

religiosity. In addition to controlling for different variables affecting acquisition premium that

6

have been used in earlier studies (John et al. (2012)). I also include religiosity-related controls

that have been by earlier religiosity studies in the accounting and Finance literature (e.g.

McGuire et al., 2012; Dyrang, et al. 2012; Hilary and Hui, 2009).

Our results show that there is a negative association between acquisition premium and county

religiosity scores, indicating that firms are less likely to pay higher acquisition premium for the

firms that have headquarters in US counties with higher percentage of religious believers. These

results support our argument that religious beliefs of managers play an important role in the

M&A determination process. These results thus suggest that more ethical behavior and high

morals, which are reflected in more risk aversion, more conservatism, and long term

consideration , and lower possibility of class action legal suits by investors, reduce risk which is

reflected in lower acquisition premium.

Additionally, the results show that the association between acquisition premium and

religiosity are stronger for firms with high acquisition. These results confirm that religiosity

influence is stronger when risk is high.

I evaluate the robustness by conducting different tests. First, I test the robustness of our

results by using the religiosity scores based on the Gallup survey data. The results of these tests

confirm the findings based on ADA data.

I conduct supplementary tests to evaluate whether religiosity will influence the dividends

payment and good will write off, the results of these tests confirm that Risk aversion in the

decision making process suggests that firms will choose project which will have higher potential

for success and lower probability for project failure. I argue that higher risk aversion will result

in less overpay, more dividends yield and more frequent good will write off.

7

Our findings make the following contributions to the literature. First, the findings confirm

that religiosity has a significant impact on risk aversion and hence it is an important determinant

of M&A value. This finding suggests that the investment value estimation models need to be

expanded to include the religiosity factor. Second, these findings supplement the findings of

agency theory to add psychology factors. Third, target firms location, incorporate law, takeover

defenses, and religiosity should also be incorporated in the decision making process. Findings

show that goodwill write-offs by firms in the high religiosity areas are timely and more

comprehensive, which make reported information more useful for investors. Fourth, acquisition

size, industries, dividend payment, debt financing have a significant influence in establishing the

relationship between M&A premium and religiosity. Religiosity has a stronger impact on the

risk aversion. This line of research can be extended to international arena and future research

studies should examine whether religiosity plays a role in the M&A premium determination

process across countries.

The remainder of the paper is designed as follows. Part II presents background and

hypotheses for the study. Research design is explained in part III. This part also provides details

on data used in the study and discusses different aspects of the acquisition premium model.

Findings are presented in part IV, and part V contains conclusion of the study.

2. Literature Review

The impact of religious beliefs and ethical values on human behavior is well recognized

in the social sciences literature (Sunstein 1996; Kennedy and Lawson 1998). It is well

documented in the psychology and religion literature that religious beliefs exert a significant

influence on individual behavior (Cornwall 1989; Layman et al. 1997a, 1997b). The results of a

8

survey also confirm that individuals with strong religious beliefs show a higher level of ethical

judgment (Longenecker et al. 2004). 1

Several authors have extended research on religiosity to

evaluate the association between religious beliefs and human behavior in economics (Bruce 1993;

Shariff et al. 2007; Norenzayan 2008) and business (Stern et al. 2000; Schultz et al. 2000;

Gardner et al. 2002). Hilary and Hui (2009) extend research on religiosity and focus on human

behavior within the corporate environment, and they especially examine whether religiosity has

an effect on managerial decisions. They conclude that firms with headquarters in the US counties

with high level of religiosity exhibit lower risk exposure.

With regard to the impact of religion on business, it is argued that individuals with

strong religious beliefs are generally more ethical because they find it morally rewarding and

satisfying, and this is especially explained by the theoretical framework developed by Weaver

and Agle (2012). The authors argue that influence of religion on business ethics is determined

by the importance of religion in an individual’s life. In other words, how important is religion in

an individual’s self-identity. As religion assumes greater importance in individual’s self-identity,

his/her behavior is more and more guided by the religious and social norms (Zahn 1970). This

aspect is also explained by Parboteeah et al. (2008) in a different way; they argue that an

individual’s participation in the religious services enhances his/her interaction with other

individuals who have similar beliefs and moral values, and this strengthens their beliefs.

Weaver and Agle’s (2012) theoretical framework suggests that as religion becomes an

important element of an individual’s self-identity, individual’s outlook and behavior are

significantly molded by the religious and ethical values. Individuals do not feel comfortable

1 Barro and McCleary (2003), Guiso et al. (2003), and Lehrer (2004) have previously also examined the impact of

religion on individuals’ economic and business behavior. Whereas Lehrer (2004) focused on the religion’s impact

on economic decisions by individuals, Barro and MCleary (2003) and Guiso et al. (2003) examined the overall

economic outcome as a result of the influence of religion on human economic behavior.

9

when their behavior and actions are considered to be outside the religious and social norms.

They especially try to keep their behavior within the boundaries of religious and social norms to

avoid any emotional distress and guilt feeling (Sunstein 1996; Weaver and Agle 2002). The

significant impact of religion in molding individual ethical behavior is also supported by the

evidence provided by empirical studies (Batson et al. 1993; Singelis et al. 1995; Karahanna et al.

2002). In a recent study, Longeneck et al. (2004) conclude that individuals with religious

commitments are associated with higher business ethics. Overall, their findings suggest that

religious believers generally do not engage in unethical behavior; instead they are more likely to

maintain high moral and ethical standards and their decision-making process in the business

environment is guided by their moral and ethical values.

Findings of some studies especially emphasize the role of ethics in Financial Reporting.

Based on an experimental study, Conroy and Emerson (2004) find that religiosity is negatively

associated with the use of “accounting tricks to conceal”, and their findings show that the use of

accounting manipulation is lower for individuals with higher church attendance. McGuire et al.

(2012) report that firms with headquarters in the higher religious areas engage less in financial

reporting irregularities compared to the firms with headquarters in non-religious or lower

religious area. They especially find a negative association between religiosity and abnormal

accruals. They, however, find a positive association between religiosity and real earnings

management, suggesting that managers do not consider real earnings management as unethical.

In fact, managers view real earnings management as ethical and less risky compared to the

accruals based earnings management. Dyreng et al. (2012) report that religious adherents are

associated with a lower likelihood of financial restatements and that there is a lower risk that the

financial statements will misrepresent earnings because of overstatement (understatement) of

10

revenues/assets (expenses/liabilities). Calleng and Feng (2013) find that religiosity will also

constrain managers to hoard bad news, and this will result in timely, reliable, and comprehensive

disclosure of information, which will reduce potential risk for legal suits and thus there will be

reduction in risk.

Our study also makes an important contribution to the literature on takeover premium.

Considerable evidence exists on the positive takeover premium paid in acquisitions of publicly

traded targets (e.g., Schwert 1996). Fuller, Netter, and Stegemoller (2002) and Officer (2007)

suggest that the price paid by a bidder for its target is lower when the target is less liquid. Many

earlier articles also examine the role of its target is lower when the target is less liquid. Many

earlier articles also examine the role of taxes or information acquisition in explaining the

difference in takeover premium between publicly traded targets that receive cash payments and

stock payments (i.e., Huang and Walkling 1987 for the taxation explanation; i.e., Eckbo and

Langohr 1989 for the information explanation)2. Our paper contributes to this literature by

providing social norms into the takeover premium received by publicly traded targets. Our

results support the predictions of our theory, which is based on religiosity even after I control for

mode of payment, liquidity, and other considerations.

Finally, our article is related to the literature on the impact of religiosity on risk aversion.

In particular, Callen and Fang (2013) find robust evidence that firms headquartered in counties

with higher levels of religiosity exhibit lower levels of future stock price crash risk. Our main

2 Recently, Bargeron et al. (2008) find that private bidders, such as private equity funds, offer smaller premiums to

their targets compared with public bidders. They argue that the differences in managerial ownership and managerial

incentives contribute to the different premiums paid by private bidders and public bidders. Officer (2003) and Bates

and Lemmon (2003) also find the impact of target termination agreement on takeover premium, and Betton, Eckbo,

and Thorburn (2008, 2009), Jarrell and Poulsen (1989), and Ravid and Spiegel (1999) find the relation between

bidder toehold and takeover price.

11

results suggest that firms headquartered in religious counties are less likely to pay high takeover

premium.

3. Hypothesis

Religiosity and Takeover premium

The existing studies on the role of religiosity in the corporate environment examine

managers’ risk aversion in investment decisions and earnings manipulations. Hilary and Hui

(2009) document that managers’ religious beliefs lead to risk aversion, meaning that religious

beliefs do not encourage managers to engage in risk-taking activities. Instead, religious believers

feel more comfortable if they can avoid risk and religion provides solace for not getting involved

in activities exposing them to risky situations (Malinowski 1925; Miller and Hoffman 1995;

Gaspar and Clore 1998).3

Additionally, it is documented that religious believers being highly ethical avoid

violating religious, morale and social norms (e.g. Boone, et al. 2013). Instead, they stay within

the boundaries of these norms and act in accordance with the guidelines provided by them. This

aspect of religiosity suggests that religion acts as a deterrent for any activity that is considered to

be outside the religious and social norms. Religious believers will feel guilty if they engage in

unreligious activities and they fear punishment by God for violating the religious guidelines. In

fact, this aspect of religion serves as a sanctioning system in the business and corporate

environment and discourages managers to engage in an opportunistic behavior. Instead, it

encourages them to behave ethically and report financial information truthfully. Recent empirical

findings confirm that religious managers avoid earnings manipulations by overstating the

3 Hilary and Hui (2009) discuss the negative association of religious beliefs with various types of risk-taking

behaviors.

12

revenues and assets and understating the liabilities and expenses (McGuire et al. 2012) and they

also avoid restatements (Dyreng et al. 2012).

Recently, Callen and Fang (2013) have argued that high moral values, anti-manipulative

ethos of religion also discourage managers to withhold bad news from investors. They present

that social norms operate in the following three ways to discourage managers to hoard bad news.

First, religious managers are more likely to internalize the social norms associated with risk

aversion, which discourage them to pay a high takeover premium. Second, managers are likely

to pay a high price in terms of social stigma if they are caught violating this social norm. Third,

religiosity will encourage potential whistle blowers to feel religion-bound to unmask

manipulators (e.g. Javers, 2011).

Grullon, et al (2010) have advanced another argument to explain the impact of

religiosity on firms. The argue and document that firms located in counties with higher levels of

religiosity are less likely to be the targets of class action securities lawsuits, engage in backdating

options, and grant excessive compensation packages to their managers. Their argument and

evidence are consistent with the argument that high religiosity environment encourage firms to

behave in ethical and moral way that does not involve risky takeovers that is important for

investors. Consequently, legal risk is reduced and there are lower class action securities law

suits.

The arguments and evidence that religiosity constrains managerial behavior of earnings

manipulation, discourages them to engage in risky projects and without bad news, which is

reflected in potential low class action suits is low, suggest high religiosity values reduce legal

risk for firms. This argument also suggests that the impact of these factors will also have a

significant moderating effect on risk taking make managers making M&A decisions. Thus, I

13

argue that managers are less likely to take risky project if the client firm’s headquarters is located

in counties that associated with high religiosity values. Risk aversion will in turn have a

moderating effect on takeover price target firms received, which leads us to hypothesize that

takeover premium are lower for firms that have their headquarters in counties with high

religiosity.

On the other hand, if managers have low religious beliefs, it will have a negative impact

on their ethical and moral values, and they are likely to be in the best interest of other

stakeholders. In order to ensure the long term profit for these firms, managers will be less likely

to take risky projects. Consequently, this will result in lower takeover price.

Based on the above discussion, I develop the following hypothesis to test the impact of

managers’ religious beliefs on takeover price:

H1a: Takeover premium is lower if the parent headquarters are located in US counties

with high religiosity.

H1b: Takeover premium is higher if the target headquarters are located in US counties

with high religiosity.

Religiosity and Goodwill write off

H2: Goodwill write off will be lower if the parent headquarters are located in US

counties with high religiosity.

Religiosity and High Risk

H3: The negative association between takeover premium and religious beliefs is

especially strong if the parent belongs with high risk.

Religiosity and Dividends Yield

14

H4: Dividend yield will be lower if the parent headquarters are located in US counties

with high religiosity.

Religiosity and Stock Payment

H5: Stock Payment will be lower if the parent headquarters are located in US counties

with high religiosity.

4. Sample and Research Design

4.1.Sample and Data Selection

Following Hilary and Hui (2009), I obtain religiosity data from the American Religion

Data Archive (ARDA). Once every decade, the Glenmary Research Center collects data from

surveys on religious affiliation in the U.S. (1971, 1980, 1990 and 2000). Based on the survey

results, the centre reports county-level data on the number of churches and the number of total

adherents and the number of total adherents by religious affiliation. These reports are available

on ARDA’s website under the title “Churches and Church Membership.” Our main variable of

interest is the degree of religiosity at time t (RELt) of the county in which the firm’s headquarter

is located. I calculate RELt as the number of religious adherents in the county to the total

population the county as reported by ARDA. 4 Following previous studies (e.g., Hilary and Hui

(2009) and Alesina and La Ferrara (2000)), I linearly interpolate the data to obtain the values for

missing years (1972 to 1979, 1981 to 1989, 1991 to 1999, and 2001 to 2010).

4 ARDA indicates that “for[the] purposes of this study, adherents were defined as ‘all members’, including full

members, their children and the estimated number of other regular participants who are not considered as

communicant, confirmed or full members, for example, the ‘baptized,’ ‘those not confirmed,’ ‘those not eligible for

communion’ and the like.”

15

I also use another Religiosity data base, developed by Gallup organizations, to obtain

data on religious and demographic variables. The final sample consists of 1,788 observations for

678 firms with headquarters in 194 US counties from 2007-2010.

In addition, I collect takeover data from CDS. Compustat also provides information on

the location of firms’ headquarters. Following prior research (e.g., Coval and Moskowitz (1999),

Ivkovic and Weisbenner (2005), Loughran and Schultz (2004), irinsky and Wang (2006), and

Hilary and Hui (2009)), I define a firm’s location as the location of its headquarters “given that

corporate headquarters are close to corporate core business activities (Pirinsky and Wang

(2006))”.Geographic data is collected from U.S. Consensus Bureau.

The sample selection details are provided in Table 1.

------------------------------

Table 1

---------------------------

5. Empirical setting and results

5.1. Main specifications

I follow the literatures include a takeover model (Chatterjee et.al. 2012)

Takeover Premium=Religiosity+Geographic Controls+Percentageof stock+Diversify+Tender+Hostile

+Competing offer+Toehold dummy+Ratio+Target market cap.+Target market-to-book

+Target institutionalinvestor holding+Adjusted target turnover+Target merger liquidityindex

+Target's analyst dispersion in[-126,-64]+Dummyof high target analyst dispersion

+Target'ΔHold in window[-126,-64]+Target'sΔBreadth in window[-126,-64]

+Target's idiosyncratic volatility

16

All variables are defined in Appendix A. In order to test our hypotheses H2 and H3, I

include the variables of acquisition size and good will writes off.

In order to test target state takeover defenses law, I follow Barzuza’s (2009) classification

of state antitakeover laws, summarized in table .Based on data on a firm’s state of incorporation

taken from Compustat, I generate qualitative variables describing the antitakeover laws to which

firms in each state are subject. In order to simplify the analysis, I create a poison pill

endorsement indicator variable equal to one if a firm is incorporated in a state with a strong or

intermediate poison pill endorsement statue and equal to zero otherwise. Similarly, I create

another constituency statue dummy equal to one if the firm is incorporated in state with a strong

or intermediate other constituency statue and zero otherwise. I also create binary variables for

firms in states that apply Unocal, this time equal to 1 if the state follows the enhanced fiduciary

standard and 0 if they reject it. As described in the introduction, I omit Delaware firms. First,

courts in states with weak statues- Illinois and Wisconsin- applied Unocal. Second, courts in

states that had no statues at all when the case was decided- Arkansas, Florida, Indiana, Kansas,

Maryland, and Minnesota- applied unocal, except for one case applying New York law (before

the original statue was enacted), where the court suggested it would not recognize enhanced

duties.

5.2.Main results

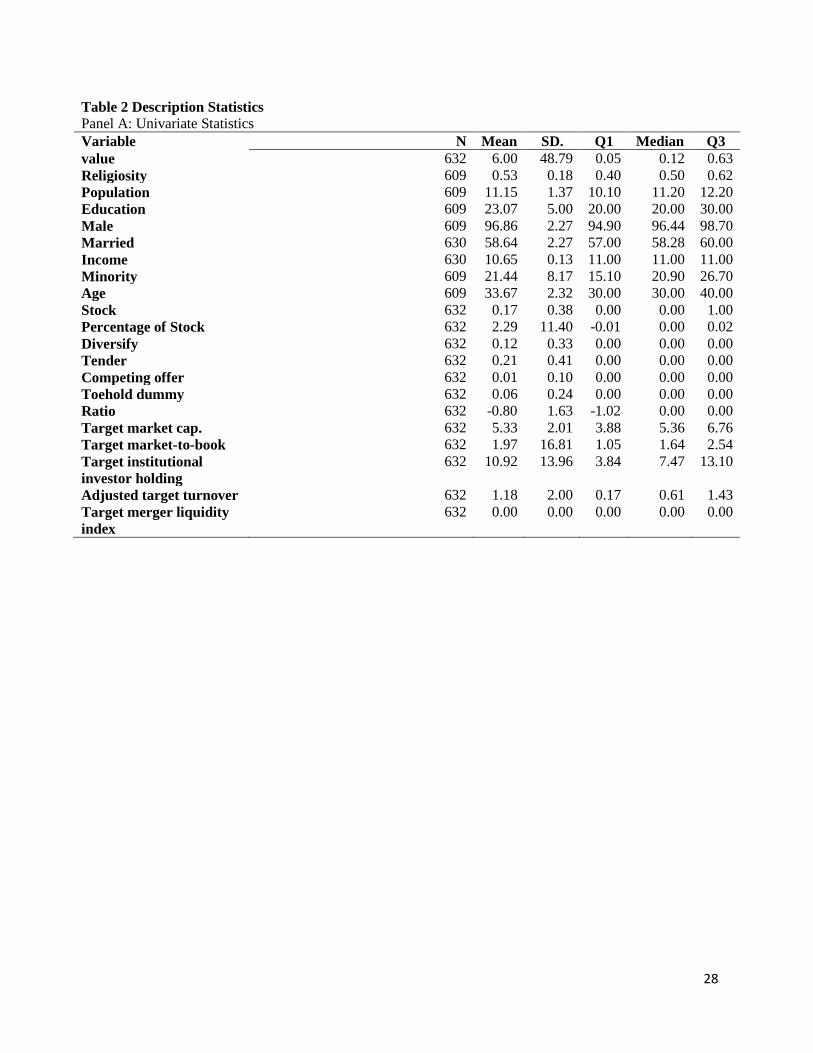

Descriptive Statistics

Descriptive statistics on religiosity are provided in Table 2.

-------------------------------------

Insert Table 2 Here

17

-------------------------------------

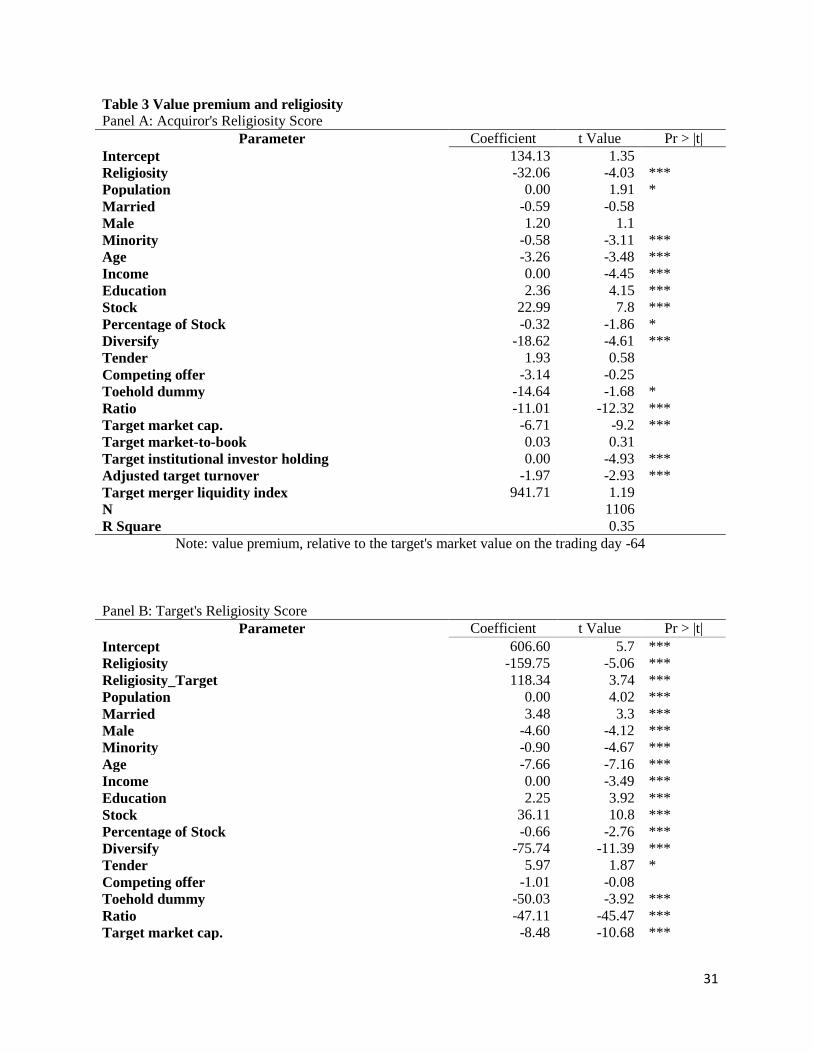

Association between Religiosity and Takeover premium

The results are contained in Table 3.

-------------------------------------

Insert Table 3 here

-------------------------------------

I first evaluate the association between takeover premium and religiosity based on county

scores of religiosity. I validate the above results based on the religiosity scores developed for the

Gallup religiosity data base. I use five different measures for calculating the religiosity scores.

Overall, the results (untabulated) of these analyses are consistent with the results reported in

Table 3. The results show that the RELIGIOSITY coefficient is negative and statistically

significant. The results based on individual elements show that the element of “belonging to a

religious group” especially plays an important role in one’s life, which in turn has an impact on

the individual’s behavior in the business environment.

In addition, I incorporate target firms’ religiosity in the regression. I find that target firms’

religiosity is positively correlated with acquisition premium, which means that target firms’

manager will charge a higher premium in the religiosity areas. The results are consistent with the

theory that religiosity reduce the agency problems.

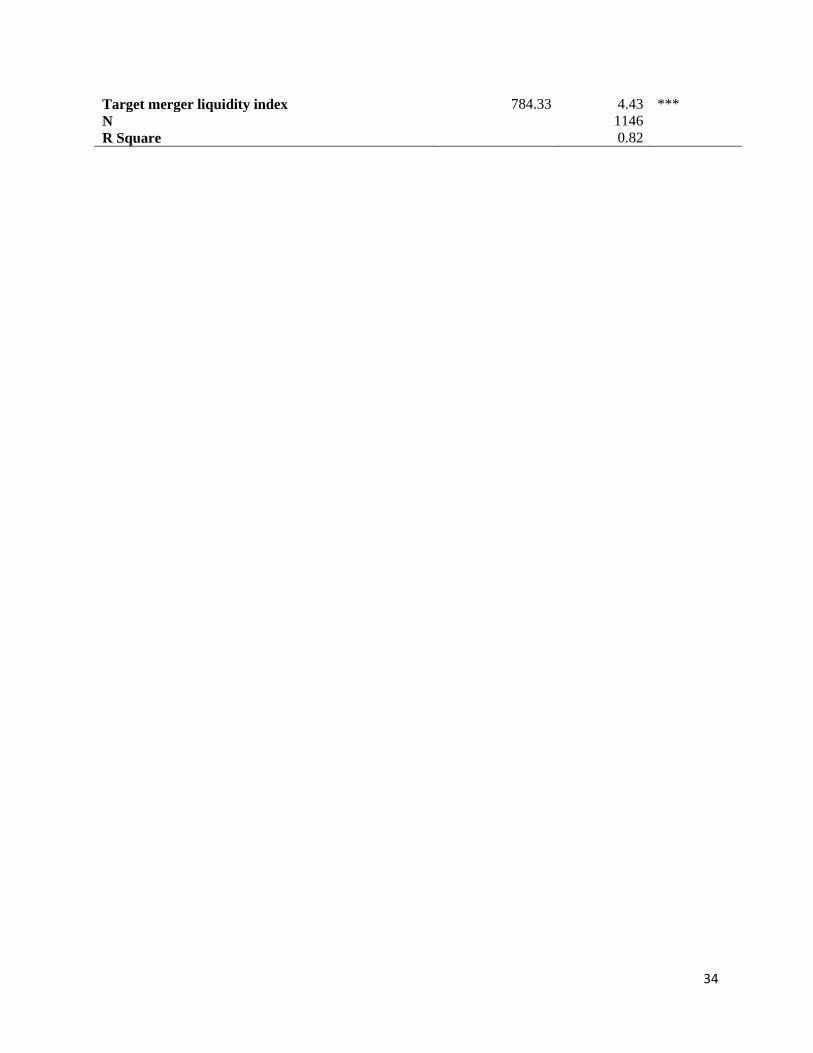

The impact of religiosity and dividend payment

Then I put the number of dividend payment in the model. I find that there is a negative

and significant relation between religiosity and dividend payment.

18

-------------------------------------

Insert Table 4 Here

-------------------------------------

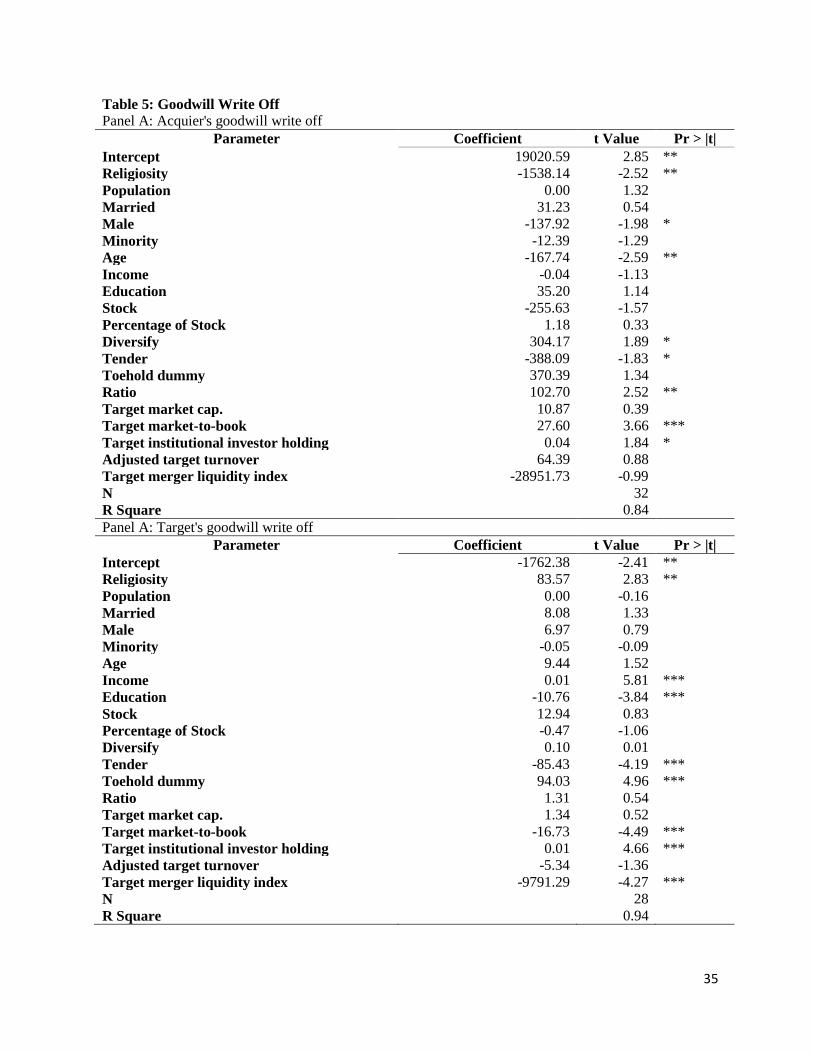

Impact of Goodwill Write-off and Religiosity

I also put the goodwill like a measure of acquisition premium. I find the religiosity is

significantly negative with goodwill write off for acquirer, but significantly positively correlated

with targets’ goodwill write off, which means the target firms located in religious areas will write

down their assets.

-------------------------------------

Insert Table 5 Here

-------------------------------------

Impact of Percentage Stock Payment and Religiosity

I also put the percentage of stock payment in the model and find that acquirer’s

religiosity is significantly negative with stock percentage payment, but not targets’ religiosity,

which means the acquirer located in religiosity areas will be more likely to select cash payments

to avoid the takeover risk.

-------------------------------------

Insert Table 6 Here

-------------------------------------

19

Robustness Tests

I conduct tests to evaluate the robustness of our findings. First, I conduct a test using the

religiosity score calculated based on the Metropolitan Statistical Area (MSA). The number of

observations is reduced to because some sample observations are not in any MSA. The results of

this test are also contained in Panel B of Table 3 (Column 1 and 2). Column 1 contains the

results based on the religiosity score calculated using the factor analysis, whereas Column 2

contains the results based on the average religiosity score. The results for both columns show

that the coefficients are significantly negative, and thus these results are similar to the main

results.

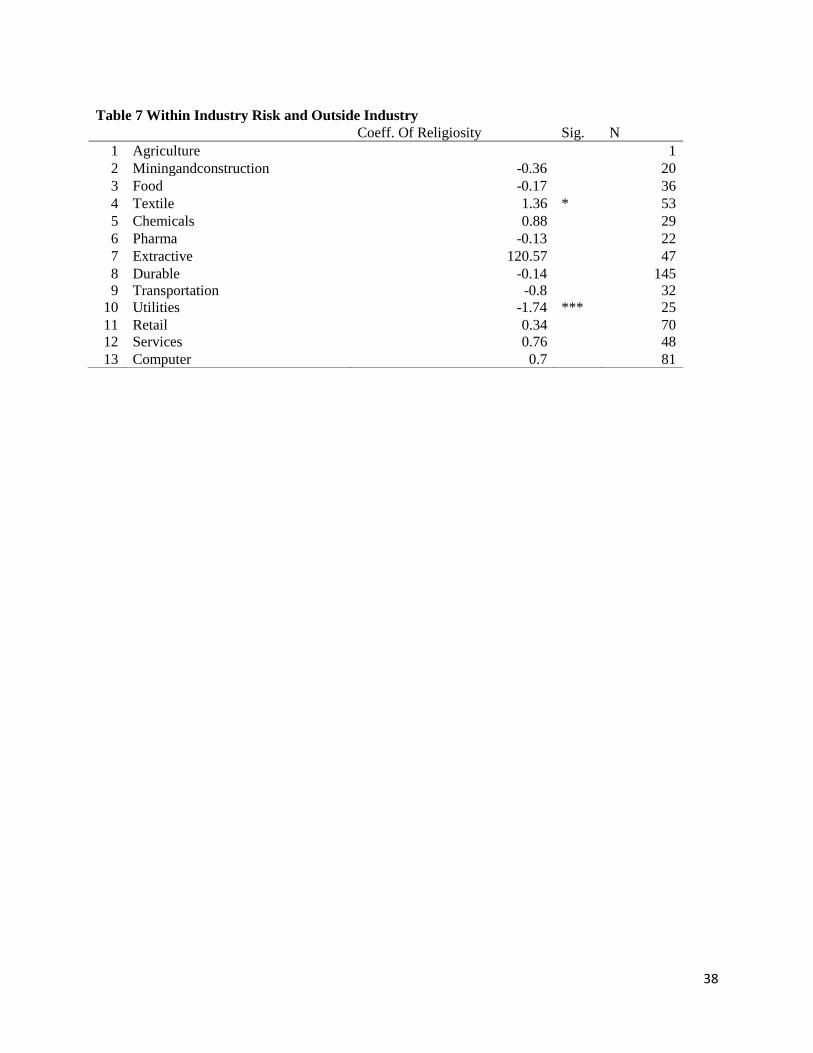

The impact of industry on the association of takeover price and religiosity

I also find in different industries, the religiosity effect is different. Especially in mining

and construction, there is a positive correlation between religiosity and acquisition premium.

-------------------------------------

Insert Table 7 Here

-------------------------------------

The impact of debt ratio on the association of takeover price and religiosity

Our results show that if the firm is financed by debt, I find a negative and significant

correlation between religiosity and acquisition premium.

-------------------------------------

Insert Table 7 Here

-------------------------------------

20

6. Conclusion

It is well documented in the social sciences literature that religious beliefs have a significant

impact on individual behavior. Consistent with this argument, the business and accounting

studies also document that managers with strong religious beliefs do not engage in earnings

manipulations and misrepresentations that may distort information and make it unreliable for

users. These arguments suggest that the quality of information prepared by managers with high

religious values is generally of a higher quality compared to information disclosed by managers

with lower religious values. In this study, I extend this line of research and argue that high

quality of information issued by firms that are located in counties with high religious beliefs and

values will also have an impact on takeover price the target firms received. In view of risk

aversion, CEOs will be less likely to take risky projects. This in turn will result in lower

takeover premium for firms with headquarters in counties with high religious values. The results

of our empirical tests confirm that there is a negative association between religiosity and

takeover premium.

21

Bibliography:

Alesina, A., La Ferrara, E., 2000. Participation in heterogeneous communities. Quarterly Journal

of Economics 115 (3): 847-904.

Barro, R. J., and R. M. McCleary. 2003. Religion and economic growth across countries.

American Sociological Review 68 (5): 760-781.

Batson, C. D., P. Schoenrade, and W. L. Ventis. 1993. Religion and the individual: A social-

psychological perspective. Oxford University Press New York.

Beasley, M. S. 1996. An empirical analysis of the relation between the board of director

composition and financial statement fraud. The Accounting Review 71 (4): 443-465.

Bebchuk, L. A., and M. S. Weisbach. 2010. The state of corporate governance research. Review

of Financial Studies 23 (3): 939-961.

Bruce, S. 1993. Religion and rational choice: A critique of economic explanations of religious

behavior. Sociology of Religion 54 (2): 193-205.

Callen, J. L. and X. Fang. 2013. Religion and stock price crash risk. Journal of Financial and

Quantitative Analysis (forthcoming).

Chalfant, H. P. and P. L. Heller. 1991. Rural/urban versus regional differences in religiosity.

Review of Religious Research 33 (1): 76-86.

Chang, W.-J., S. J. Monahan, A. Ouazad. 2013. The Higher Moments of Future Return on

Equity. Working Paper, Insead University.

Cornett, M. M., A. J. Marcus, and H. Tehranian. 2008. Corporate governance and pay-for-

performance: The impact of earnings management. The Journal of Financial Economics 87

(2): 357-373.

Conroy S. J., and T. L. N. Emerson. 2004. Business ethics and religion: Religiosity as a

predictor of ethical awareness among students. Journal of Business Ethics 50 (4): 383-396.

Cornwall, M. (1989). The determinants of religious behavior: A theoretical model and empirical

test. Social Forces 68 (2): 572-592.

Dechow, P. M. and I. D. Dichev. 2002. The quality of accruals and earnings: The role of accrual

estimation errors. The accounting review 77 (s-1): 35-59.

Doyle, B., W. Ge, and S. McVay. 2007. Determinants of weakness in internal control over

financial reporting. Journal of Accounting and Economics 44 (1/2): 192-223.

Dyreng, S. D., W. J. Mayew, and C. D. Williams. 2012. Religious social norms and corporate

financial reporting. Journal of Business Financial & Accounting 39 (7-8): 845-875.

Duru, A., and D. M. Reeb. 2002. International diversification and analysts' forecast accuracy

and bias. The Accounting Review 77 (2): 415-433.

Gardner, G. T. and P. C. Stern. 2002. Environmental problems and human behavior. Pearson

Custom Pub.

Gasper, K., and G. Clore. 1998. The persistent use of negative affect by anxious individuals to

estimate risk. Journal of Personality and Social Psychology 74 (5): 1350–1363.

Gompers, P., J. Ishii, and A. Metrick. 2003. Corporate governance and equity prices. The

Quarterly Journal of Economics 118 (1): 107-156.

Guiso, L., P. Sapienza, and L. Zingales. 2006. Does culture affect economic outcomes? Journal

of Economic Perspectives 20 (2): 23-48.

22

Grullon, G., G. Kanatas, and J. Weston. 2010. Religion and Corporate (Mis)behavior. Working

Paper, Rice University.

Hilary, G., and K. W. Hui. 2009. Does religion matter in corporate decision making in America?

Journal of Financial Economics 93 (3): 455-473.

Javers, E. 2011. Religion, not money, often motivates corporate whistleblowers. CNBC, Feb 12.

Karahanna, E., J. R. Evaristo, and M. Srite. 2002. Levels of culture and individual behavior: An

integrative perspective. Advanced Topics in Global Information Management 30.

Kennedy, E. J. and L. Lawton. 1998. Religiousness and business ethics. Journal of business

ethics 17 (2): 163-175.

Layman, G. C. 1997a. Religion and political behavior in the United States: The impact of

beliefs, affiliations, and commitment from 1980 to 1994. Public Opinion Quarterly: 288-

316.

Layman, G. C. and E. G. Carmines. 1997b. Cultural conflict in American politics: Religious

traditionalism, postmaterialism, and US political behavior. Journal of Politics 59 (3): 751-

777.

Lehrer, E. L. G., J.A. McKinney, and C. W. Moore. 2004. Religion as a determinant of

economic and demographic behavior in the United States. Population and Development

Review 30 (4): 707-726.

Longenecker, J. G., J. A. McKinney, and C. W. Moore. 2004. Religious intensity, evangelical

Christianity, and business ethics: An empirical study. Journal of business ethics 55 (4): 371-

384.

Malinowski, B. 1925. Magic, science and religion. In: Needham, J. (Ed.), Science, Religion and

Reality. Macmillan, New York: 19–94.

McGuire, S. T., T. C. Omer, and N. Y. Sharp. 2012. The impact of religion on financial

reporting irregularities. The Accounting Review 87 (2): 645-673.

Miller, A., and J. Hoffmann. 1995. Risk and religion: an explanation of gender differences in

religiosity. Journal for the Scientific Study of Religion 34 (1): 63–75.

Norenzayan, A. and A. F. Shariff. 2008. The origin and evolution of religious prosociality.

Science 322 (5898): 58-62.

O'Brien, P. C. and R. Bhushan. 1990. Analyst following and institutional ownership. Journal of

Accounting Research 28 (Supplement): 55-76.

Parboteeah, K. P., M. Hoegl, and J. B. Cullen. 2008. Ethics and religion: An empirical test of a

multidimensional model. Journal of Business Ethics 80 (2): 387–398.

Petersen, M.A. 2009. Estimating standard errors in finance panel data sets: Comparing

approaches. Review of Financial Studies 22 (1): 435-480.

Schultz, P. W., L. Zelezny, N. J. Dalrymple. 2000. A multinational perspective on the relation

between Judeo-Christian religious beliefs and attitudes of environmental concern.

Environment and Behavior 32 (4): 576-591.

Shariff, A. F., and A. Norenzayan. 2007. God Is Watching You Priming God Concepts

Increases Prosocial Behavior in an Anonymous Economic Game. Psychological Science 18

(9): 803-809.

Singelis, T. M., and W. J. Brown. 1995. Culture, self, and collectivist communication linking

culture to individual behavior. Human Communication Research 21 (3): 354-389.

Stanny, E., and K. Ely. 2008. Corporate environmental disclosures about the effects of climate

change. Corporate Social Responsibility and Environmental Management 15 (6): 338-348.

23

Stern, P. C. 2000. New environmental theories: toward a coherent theory of environmentally

significant behavior. Journal of Social Issues 56 (3): 407-424.

Sunstein, C. R. 1996. Social norms and social rules. Columbia Law Review 96 (4): 903–968.

Tittle, C., and M. Welch. 1983. Religiosity and Deviance: Toward a Contingency Thoery of

Constraining Effects. Social Forces 61 (3): 653-682.

Urcan, O. 2007. Geographical Location and Corporate Disclosures. Working paper, London

Business School.

Uysal V. B., S. Kedia, and V. Panchapagesan. 2008. Geography and acquirer returns. Journal of

Financial Intermediation 17 (2): 256-275.

Weaver, G. R., and B. R. Agle. 2002. Religiosity and ethical behavior in organizations: A

symbolic interactionist perspective. Academy of management review 27 (1): 77-97.

Zahn, G. C. 1970. The commitment dimension. Sociology of Religion 31 (4): 203–208.

24

Appendix A: List of Variables

Test Variable:

Religiosity: The ratio of the number of religious adherents in the county (as reported by ARDA)

to the total population of the county (as reported by the US Census Bureau).

Demographic control variables:

Population : the size of the population in the county.

Education: educational attainment, defined as the percentage of people 25 years and over having

a bachelor’s, gradulate, or professional degree.

Male: the male-to-female ratio in the state.

Married: the percentage of married people in the state.

Money: average state money income.

Minority: the percentage of minorities in the state.

Age: the median age of each state.

Dependent variables:

Takeover Premium: the percentage premium of the value of the bidder’s offer over the market

value of the target’s equity on the trading day -64(with adjustments).

Return-based premium: the cumulative target abnormal return in the trading day window [-

63,126].

Percentage of stock: the percentage of target’s shares owned by the bidder.

Toehold dummy: equals one if, prior to the takeover announcement, the bidder owns more than 5%

of the target’s shares.

Ratio: the log ratio of the target’s market value of equity to the bidder’s market value of equity

on the trading day -64.

Target market capitalization: the log of the target’s market value of equity on the trading day -64,

i.e., the day before my measurement window of the total takeover premium.

Target’s market to book ratio: the ratio of the target’s market value divided book value.

25

Target’s institutional investor holding: the percentage of the target’s shares hold by institutional

investors in the first reporting date reported by CDA/Spectrum prior to the trading day -63.

Adjusted target turnover: the ratio of stock trading turnover to the market average turnover,

where stock turnover is trading volume in shares divided by shares outstanding -63.

Target liquidity index: the ratio of the value of mergers in the target’s industry to the total book

value of assets of the firms in the target’s industry. The target’s industry is defined by the two-

digit SIC code.

CDA Variables:

Percentage of stock: fraction of the value of stock component in the whole payment package.

Dummy of all-cash offers

Dummy of all-stock offers

Tender: tender offer.

Hostile: Dummy of hostile takeovers. following the SDC’s definition.

Competing offers: 1 if there is more than one bidder who bids for the target.

Diversify: 1, if the bidder and the target operate in different industries, as defined by the two-

digit SIC codes.

26

Appendix B:

Variation in State Law This table presents the distribution of state law as classified and reported by Barzuza (2009). Year the

statute became effective is in parentheses.

Pill Endorsement

Statutes

Strong GA (1989), MD (1999), VA (1990), CO

(1989),

Intermediate CT (2003), FL (1989), HI (1988), ID (1988),

IL (1989), IN (1986), IA (1989), KY (1984),

ME (2003), MI (2001), NV (1999), NJ (1989),

OH (1986), OR (1989), PA (1989), RI (1990),

SD (1990), SC (2001), TN (1989), UT (1989),

WA (1998), WI (1987)

Weak NY (1988), NC (1990)

Other Constituency

Statutes

Strong IN (1989), MD (1999), NV (1991), NC

(1993), OH (1984), PA (1990), VA (1988)

Intermediate AZ (1987), CT (1997), HI (1989), ID (1988),

IL (1985), IA (1989), KY (1989), LA (1988),

MA (1989), MN (1987), MI (1990), MO

(1989),

NJ (1989), NM (1987), ND (1993), OR

(1989),

RI (1990), SD (1990), TN (1988), TX (2006),

VT (1998)

Weak

FL (1989), GA (1989), ME (1986), NE

(2007),

NY (1987), WI (1987)

Unocal Yes AR,CA,DE,FL,IL,KS,MI,MN,MO,OR,TX,WI

Yes(language) FL (1989), GA (1989), ME (1986), NE

No IN, MD,MA,NV,NJ,NY,NC,OH,PA,VA,

No (language)

AZ, CT (1997), HI (1989), ID (1988),

IL (1985), IA (1989), KY (1989), LA (1988),

MA (1989), MN (1987), MI (1990)

NJ (1989), NM (1987), ND (1993), OR

(1989),

RI (1990), SD (1990), TN (1988), TX (2006),

VT (1998)

27

Table 1 Sample Selection

28

Table 2 Description Statistics Panel A: Univariate Statistics

Variable N Mean SD. Q1 Median Q3

value 632 6.00 48.79 0.05 0.12 0.63

Religiosity 609 0.53 0.18 0.40 0.50 0.62

Population 609 11.15 1.37 10.10 11.20 12.20

Education 609 23.07 5.00 20.00 20.00 30.00

Male 609 96.86 2.27 94.90 96.44 98.70

Married 630 58.64 2.27 57.00 58.28 60.00

Income 630 10.65 0.13 11.00 11.00 11.00

Minority 609 21.44 8.17 15.10 20.90 26.70

Age 609 33.67 2.32 30.00 30.00 40.00

Stock 632 0.17 0.38 0.00 0.00 1.00

Percentage of Stock 632 2.29 11.40 -0.01 0.00 0.02

Diversify 632 0.12 0.33 0.00 0.00 0.00

Tender 632 0.21 0.41 0.00 0.00 0.00

Competing offer 632 0.01 0.10 0.00 0.00 0.00

Toehold dummy 632 0.06 0.24 0.00 0.00 0.00

Ratio 632 -0.80 1.63 -1.02 0.00 0.00

Target market cap. 632 5.33 2.01 3.88 5.36 6.76

Target market-to-book 632 1.97 16.81 1.05 1.64 2.54

Target institutional

investor holding

632 10.92 13.96 3.84 7.47 13.10

Adjusted target turnover 632 1.18 2.00 0.17 0.61 1.43

Target merger liquidity

index

632 0.00 0.00 0.00 0.00 0.00

29

Panel B: Correlation among Religiosity, M&A, and Control Variables

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11)

(1) value -0.03 0.00 0.16 0.21 0.13 0.06 -0.10 -0.01 0.26 -0.02

(2) Religiosity -0.14 -0.11 -0.09 0.18 -0.28 -0.19 -0.15 -0.01 0.05

(3) Population 0.24 -0.30 -0.44 0.33 0.05 0.06 -0.10 0.12

(4) Education 0.00 -0.26 0.84 -0.08 0.52 0.25 0.12

(5) Male 0.58 -0.03 0.05 -0.45 0.08 -0.14

(6) Married -0.37 -0.37 -0.15 0.01 -0.10

(7) Income -0.04 0.43 0.16 0.07

(8) Minority -0.32 -0.04 -0.10

(9) Age 0.18 0.11

(10) Stock 0.08

(11) Percentage of Stock

(12) Diversify

(13) Tender

(14) Competing offer

(15) Toehold dummy

(16) Ratio

(17) Target market cap.

(18) Target market-to-book

(19) Target institutional investor holding

(20) Adjusted target turnover

(21) Target merger liquidity index

(12) (13) (14) (15) (16) (17) (18) (19) (20) (21)

(1) value -0.04 -0.06 -0.01 -0.03 -0.40 -0.35 -0.01 -0.04 -0.04 0.13

(2) Religiosity 0.07 -0.10 -0.05 0.03 -0.03 0.02 0.08 -0.02 -0.06 0.05

(3) Population -0.04 -0.10 0.00 0.05 0.03 -0.02 -0.03 0.09 0.05 0.00

(4) Education 0.01 0.02 -0.04 0.04 -0.26 0.00 -0.03 -0.04 0.01 0.11

(5) Male -0.01 -0.01 0.05 -0.07 -0.07 -0.13 0.03 -0.02 0.09 0.10

30

(6) Married -0.01 0.04 -0.05 -0.06 0.00 -0.10 0.05 0.01 -0.03 0.09

(7) Income 0.04 0.00 0.00 0.02 -0.24 0.05 -0.05 -0.02 0.04 0.05

(8) Minority 0.04 0.03 0.09 -0.03 0.09 0.02 -0.01 0.00 0.08 0.03

(9) Age -0.01 0.08 -0.06 0.04 -0.14 0.10 -0.03 -0.04 -0.10 0.05

(10) Stock 0.20 -0.14 0.07 0.04 -0.35 -0.03 -0.04 -0.10 0.00 0.13

(11) Percentage of Stock 0.04 0.12 0.01 0.77 -0.11 0.03 0.00 -0.08 -0.02 -0.04

(12) Diversify -0.12 0.01 0.07 -0.28 -0.04 -0.07 -0.02 0.04 0.12

(13) Tender 0.06 0.08 0.10 0.01 0.01 -0.03 -0.09 -0.08

(14) Competing offer 0.04 -0.02 -0.01 -0.01 -0.03 0.01 0.04

(15) Toehold dummy -0.14 0.02 0.00 -0.09 0.01 0.01

(16) Ratio 0.25 0.11 -0.01 -0.06 -0.09

(17) Target market cap. 0.01 -0.40 0.07 -0.03

(18) Target market-to-book 0.05 -0.25 0.00

(19) Target institutional investor holding -0.05 -0.05

(20) Adjusted target turnover 0.05

(21) Target merger liquidity index

31

Table 3 Value premium and religiosity

Panel A: Acquiror's Religiosity Score

Parameter Coefficient t Value Pr > |t|

Intercept 134.13 1.35

Religiosity -32.06 -4.03 ***

Population 0.00 1.91 *

Married -0.59 -0.58

Male 1.20 1.1

Minority -0.58 -3.11 ***

Age -3.26 -3.48 ***

Income 0.00 -4.45 ***

Education 2.36 4.15 ***

Stock 22.99 7.8 ***

Percentage of Stock -0.32 -1.86 *

Diversify -18.62 -4.61 ***

Tender 1.93 0.58

Competing offer -3.14 -0.25

Toehold dummy -14.64 -1.68 *

Ratio -11.01 -12.32 ***

Target market cap. -6.71 -9.2 ***

Target market-to-book 0.03 0.31

Target institutional investor holding 0.00 -4.93 ***

Adjusted target turnover -1.97 -2.93 ***

Target merger liquidity index 941.71 1.19

N

1106

R Square

0.35

Note: value premium, relative to the target's market value on the trading day -64

Panel B: Target's Religiosity Score

Parameter Coefficient t Value Pr > |t|

Intercept 606.60 5.7 ***

Religiosity -159.75 -5.06 ***

Religiosity_Target 118.34 3.74 ***

Population 0.00 4.02 ***

Married 3.48 3.3 ***

Male -4.60 -4.12 ***

Minority -0.90 -4.67 ***

Age -7.66 -7.16 ***

Income 0.00 -3.49 ***

Education 2.25 3.92 ***

Stock 36.11 10.8 ***

Percentage of Stock -0.66 -2.76 ***

Diversify -75.74 -11.39 ***

Tender 5.97 1.87 *

Competing offer -1.01 -0.08

Toehold dummy -50.03 -3.92 ***

Ratio -47.11 -45.47 ***

Target market cap. -8.48 -10.68 ***

32

Target market-to-book 0.42 4.63 ***

Target institutional investor holding 0.00 -6.41 ***

Adjusted target turnover -2.84 -4.09 ***

Target merger liquidity index 290.59 0.32

N

1146

R Square 0.91

33

Table 4: Dividend Payment

Panel A: Acquirer Dividend Payment

Parameter Coefficient t Value Pr > |t|

Intercept 200.43 9.5 ***

Religiosity -3.32 -0.53

Religiosity_Target -15.13 -2.41 **

Population 0.00 2.52 **

Married 1.29 6.16 ***

Male -2.08 -9.42 ***

Minority -0.18 -4.67 ***

Age -2.18 -10.31 ***

Income 0.00 2.24 **

Education 0.02 0.18

Stock 21.27 32.09 ***

Percentage of Stock -0.23 -4.86 ***

Diversify -0.50 -0.38

Tender -1.53 -2.41 **

Competing offer 0.42 0.16

Toehold dummy 7.37 2.91 ***

Ratio 3.05 14.85 ***

Target market cap. 0.60 3.8 ***

Target market-to-book -0.02 -0.92

Target institutional investor holding 0.00 -3.15 ***

Adjusted target turnover 0.14 1.02

Target merger liquidity index 679.89 3.81 ***

N

1146

R Square

0.82

Panel B: Target Dividend Payment

Parameter Coefficient t Value Pr > |t|

Intercept 220.16 10.53 ***

Religiosity -4.39 -0.71

Religiosity_Target -12.08 -1.94 *

Population 0.00 1.62

Married 0.94 4.54 ***

Male -2.06 -9.41 ***

Minority -0.21 -5.49 ***

Age -2.25 -10.73 ***

Income 0.00 3.21 ***

Education -0.10 -0.88

Stock 20.47 31.16 ***

Percentage of Stock -0.18 -3.83 ***

Diversify -3.87 -2.96 ***

Tender -1.13 -1.8 *

Competing offer 0.12 0.05

Toehold dummy 5.74 2.29 **

Ratio 2.86 14.03 ***

Target market cap. 0.49 3.11 ***

Target market-to-book -0.09 -4.94 ***

Target institutional investor holding 0.00 -3.49 ***

Adjusted target turnover 0.26 1.88 *

34

Target merger liquidity index 784.33 4.43 ***

N

1146

R Square 0.82

35

Table 5: Goodwill Write Off

Panel A: Acquier's goodwill write off

Parameter Coefficient t Value Pr > |t|

Intercept 19020.59 2.85 **

Religiosity -1538.14 -2.52 **

Population 0.00 1.32

Married 31.23 0.54

Male -137.92 -1.98 *

Minority -12.39 -1.29

Age -167.74 -2.59 **

Income -0.04 -1.13

Education 35.20 1.14

Stock -255.63 -1.57

Percentage of Stock 1.18 0.33

Diversify 304.17 1.89 *

Tender -388.09 -1.83 *

Toehold dummy 370.39 1.34

Ratio 102.70 2.52 **

Target market cap. 10.87 0.39

Target market-to-book 27.60 3.66 ***

Target institutional investor holding 0.04 1.84 *

Adjusted target turnover 64.39 0.88

Target merger liquidity index -28951.73 -0.99

N

32

R Square

0.84

Panel A: Target's goodwill write off

Parameter Coefficient t Value Pr > |t|

Intercept -1762.38 -2.41 **

Religiosity 83.57 2.83 **

Population 0.00 -0.16

Married 8.08 1.33

Male 6.97 0.79

Minority -0.05 -0.09

Age 9.44 1.52

Income 0.01 5.81 ***

Education -10.76 -3.84 ***

Stock 12.94 0.83

Percentage of Stock -0.47 -1.06

Diversify 0.10 0.01

Tender -85.43 -4.19 ***

Toehold dummy 94.03 4.96 ***

Ratio 1.31 0.54

Target market cap. 1.34 0.52

Target market-to-book -16.73 -4.49 ***

Target institutional investor holding 0.01 4.66 ***

Adjusted target turnover -5.34 -1.36

Target merger liquidity index -9791.29 -4.27 ***

N

28

R Square 0.94

36

Table 6 Percentage of Stock

Panel A: Acquiror's Religiosity Score

Parameter Coefficient t Value Pr > |t|

Intercept 9.22 10.97 ***

Religiosity -0.69 -9.89 ***

Population 0.00 -6.17 ***

Married 0.01 1.54

Male -0.07 -8.16 ***

Minority -0.01 -8.08 ***

Age -0.08 -9.68 ***

Income 0.00 1

Education 0.01 1.41

Percentage of Stock 0.01 6.7 ***

Diversify 0.00 0.13

Tender -0.25 -9.04 ***

Competing offer 0.16 1.55

Toehold dummy -0.40 -5.08 ***

Ratio -0.10 -14.22 ***

Target market cap. 0.04 6.17 ***

Target market-to-book 0.00 0.17

Target institutional investor holding 0.00 -5.37 ***

Adjusted target turnover -0.01 -2.41 **

Target merger liquidity index 67.01 9.83 ***

N

1146

R Square

0.55

Note: value premium, relative to the target's market value on the trading day -64

Panel B: Target's Religiosity Score

Parameter Coefficient t Value Pr > |t|

Intercept 11.65 13.19 ***

Religiosity -0.54 -1.92

Religiosity_Target -0.13 -0.44

Population 0.00 -6.52 ***

Married 0.02 1.97 **

Male -0.09 -9.7 ***

Minority -0.01 -8.74 ***

Age -0.11 -12.38 ***

Income 0.00 4.71 ***

Education -0.01 -1.55

Percentage of Stock 0.01 4.42 ***

Diversify 0.19 3.28 ***

Tender -0.16 -5.51 ***

Competing offer 0.28 2.37 **

Toehold dummy -0.52 -4.62 ***

Ratio -0.14 -17.43 ***

Target market cap. 0.03 4.14 ***

37

Target market-to-book 0.00 1.53

Target institutional investor holding 0.00 -5.37 ***

Adjusted target turnover 0.00 -0.39

Target merger liquidity index 48.57 6.15 ***

N

1146

R Square 0.55

38

Table 7 Within Industry Risk and Outside Industry

Coeff. Of Religiosity Sig. N

1 Agriculture 1

2 Miningandconstruction -0.36

20

3 Food -0.17

36

4 Textile 1.36 * 53

5 Chemicals 0.88

29

6 Pharma -0.13

22

7 Extractive 120.57

47

8 Durable -0.14

145

9 Transportation -0.8

32

10 Utilities -1.74 *** 25

11 Retail 0.34

70

12 Services 0.76

48

13 Computer 0.7 81