Recent CESEE lending and NPL dynamics – the experience of Austrian banks Philip Reading Director Financial Stability and Bank Inspections Department Oesterreichische Nationalbank Regional Workshop – Building Efficient Debt Resolution Systems Vienna, February 14, 2012

1. Recent dynamics in CESEE lending – the Austrian perspective

www.oenb.at [email protected] - 3 -

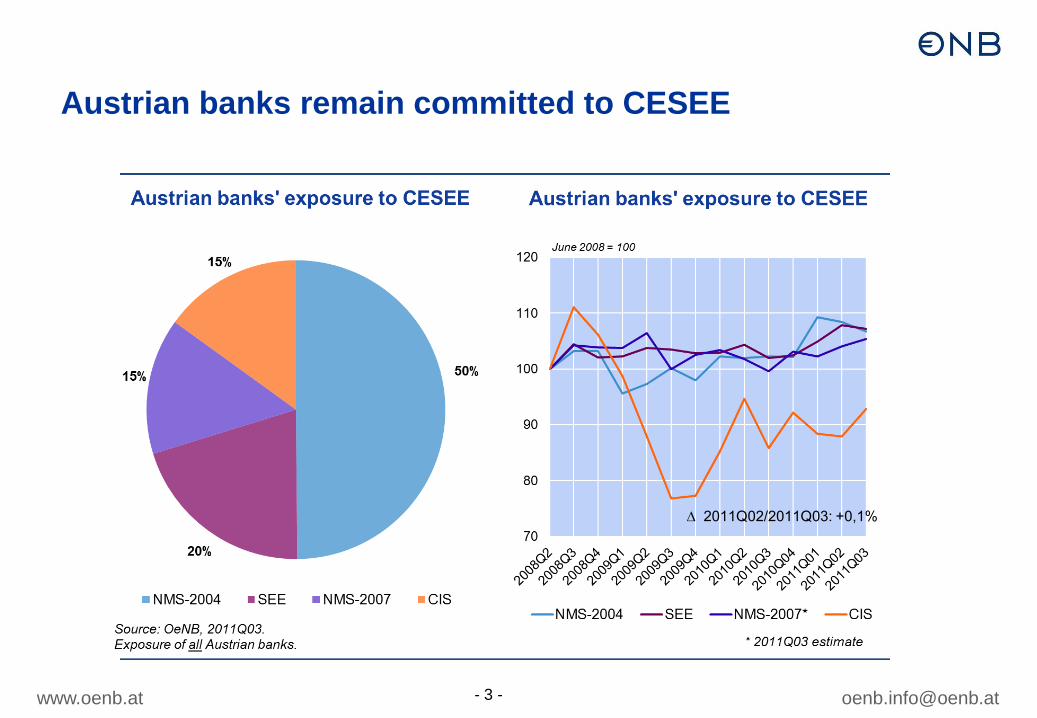

Austrian banks remain committed to CESEE

∆ 2011Q02/2011Q03: +0,1%

www.oenb.at [email protected] - 4 -

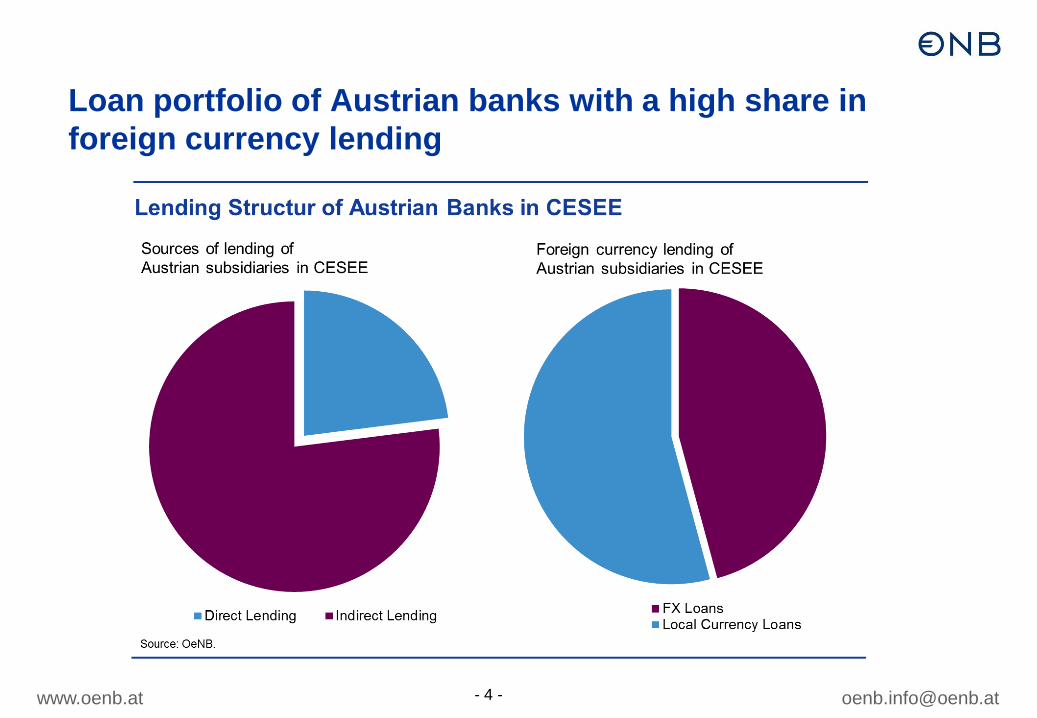

Loan portfolio of Austrian banks with a high share in foreign currency lending

www.oenb.at [email protected] - 5 -

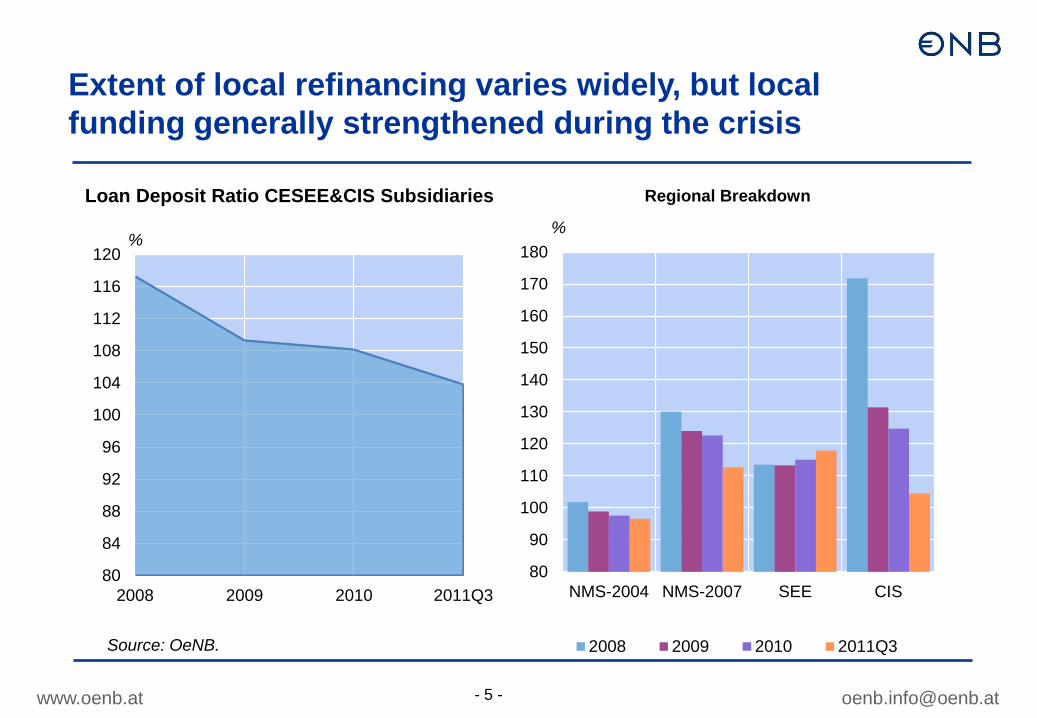

Extent of local refinancing varies widely, but local funding generally strengthened during the crisis

80

84

88

92

96

100

104

108

112

116

120

2008 2009 2010 2011Q3

Loan Deposit Ratio CESEE&CIS Subsidiaries

%

Source: OeNB.

80

90

100

110

120

130

140

150

160

170

180

NMS-2004 NMS-2007 SEE CIS

2008 2009 2010 2011Q3

Regional Breakdown

%

www.oenb.at [email protected] - 6 -

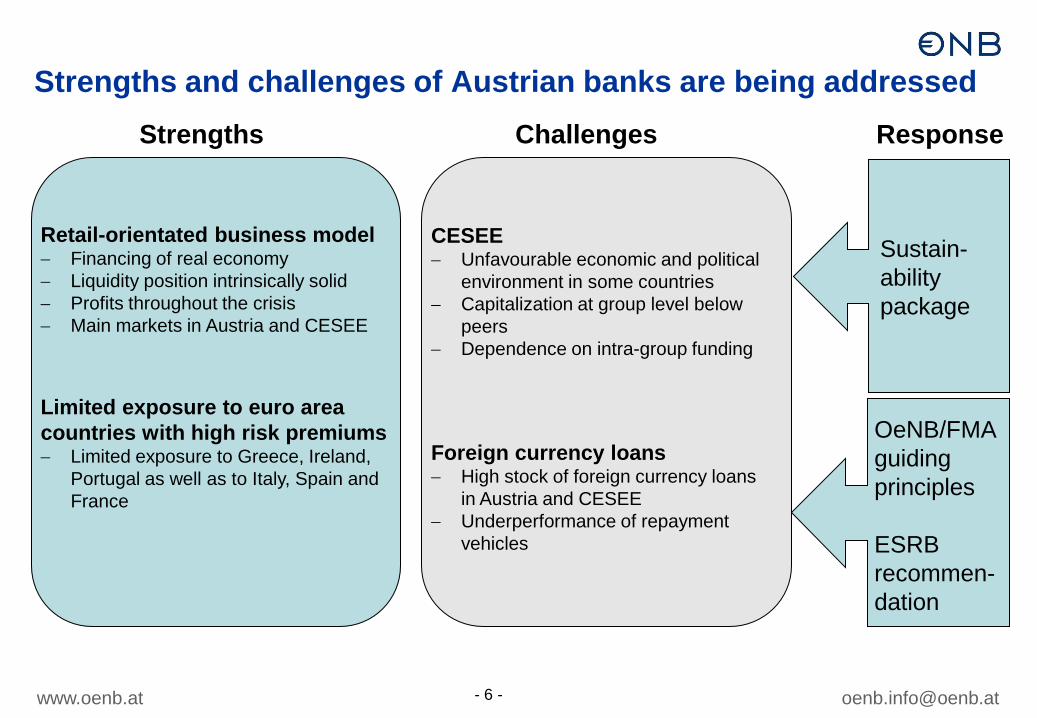

Strengths and challenges of Austrian banks are being addressed Strengths Challenges Response

Retail-orientated business model − Financing of real economy − Liquidity position intrinsically solid − Profits throughout the crisis − Main markets in Austria and CESEE

Limited exposure to euro area countries with high risk premiums − Limited exposure to Greece, Ireland,

Portugal as well as to Italy, Spain and France

CESEE − Unfavourable economic and political

environment in some countries − Capitalization at group level below

peers − Dependence on intra-group funding

Foreign currency loans − High stock of foreign currency loans

in Austria and CESEE − Underperformance of repayment

vehicles

Sustain- ability package

OeNB/FMA guiding principles ESRB recommen- dation

2. Recent dynamics in CESEE NPLs

www.oenb.at [email protected] - 8 -

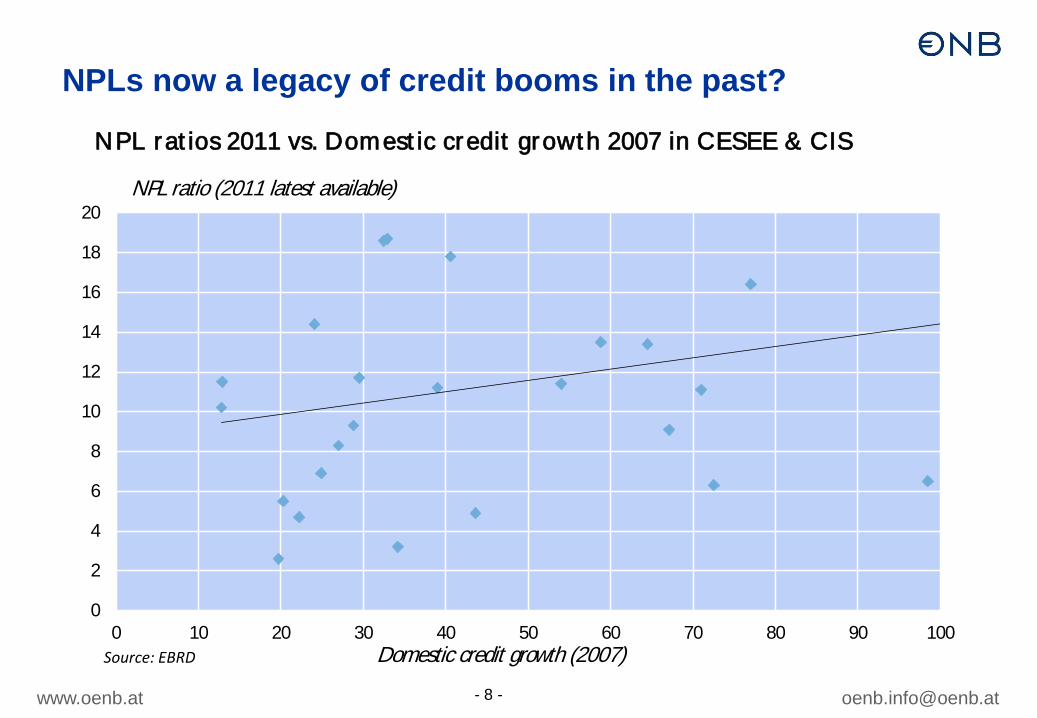

NPLs now a legacy of credit booms in the past?

0

2

4

6

8

10

12

14

16

18

20

0 10 20 30 40 50 60 70 80 90 100Domestic credit growth (2007)

NPL ratio (2011 latest available)

NPL rat ios 2011 vs. Domest ic credit growth 2007 in CESEE & CIS

Source: EBRD

www.oenb.at [email protected] - 9 -

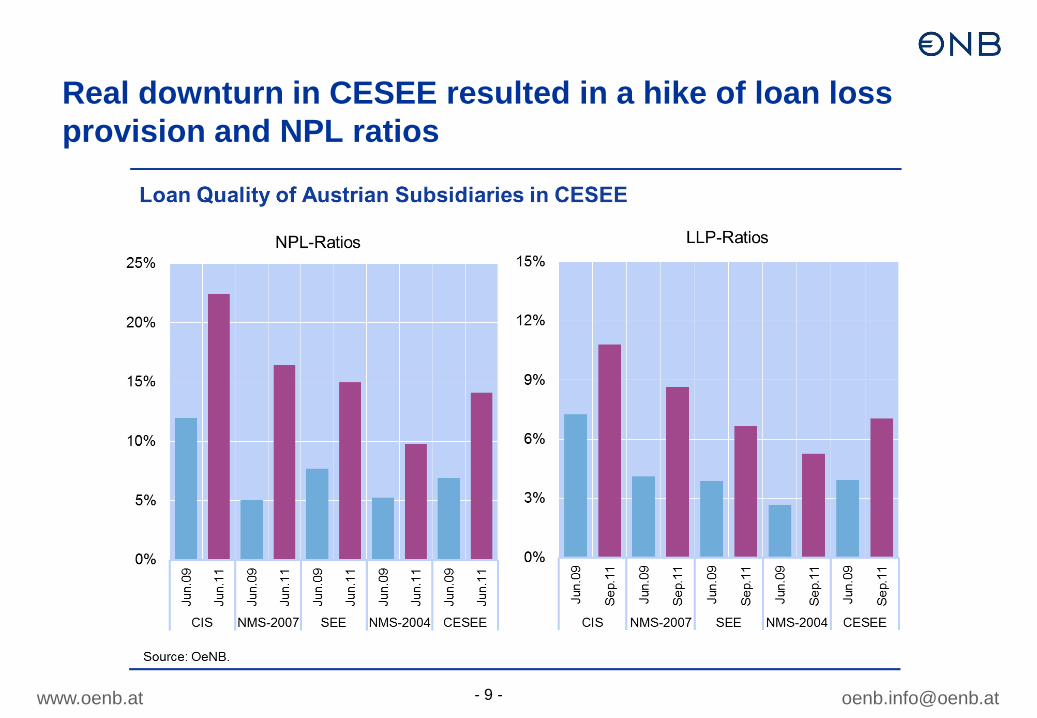

Real downturn in CESEE resulted in a hike of loan loss provision and NPL ratios

www.oenb.at [email protected] - 11 -

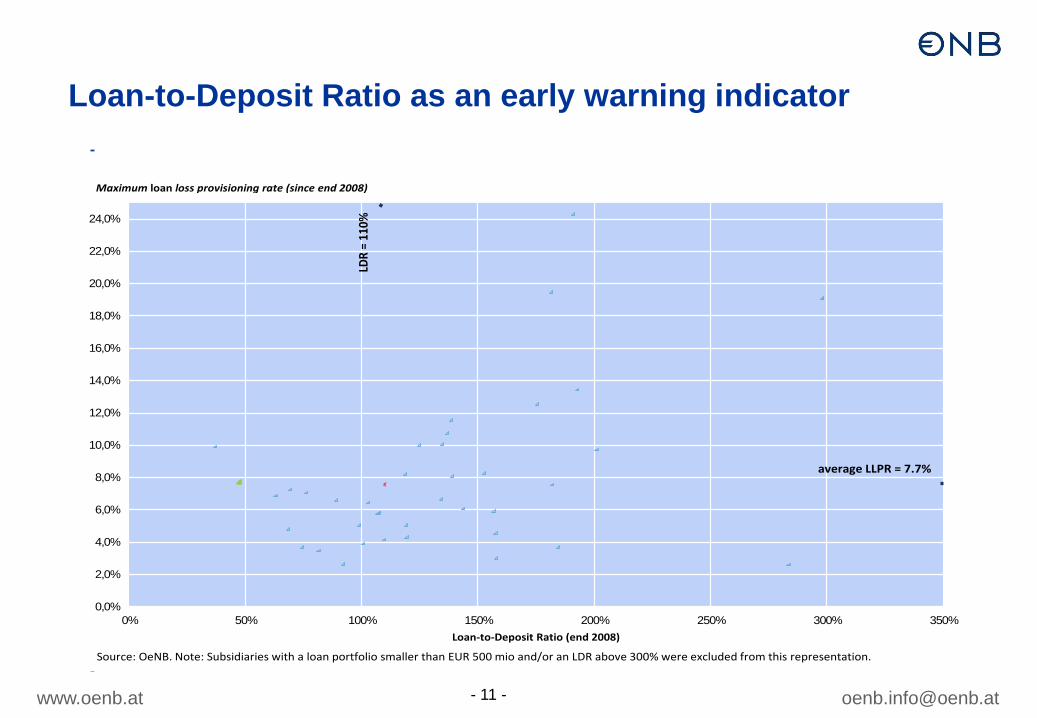

Loan-to-Deposit Ratio as an early warning indicator

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

18,0%

20,0%

22,0%

24,0%

0% 50% 100% 150% 200% 250% 300% 350%Loan-to-Deposit Ratio (end 2008)

Maximum loan loss provisioning rate (since end 2008)

Source: OeNB. Note: Subsidiaries with a loan portfolio smaller than EUR 500 mio and/or an LDR above 300% were excluded from this representation.

LDR

= 11

0%

average LLPR = 7.7%

3. AT measures to prevent future NPL crisis

www.oenb.at [email protected] - 13 -

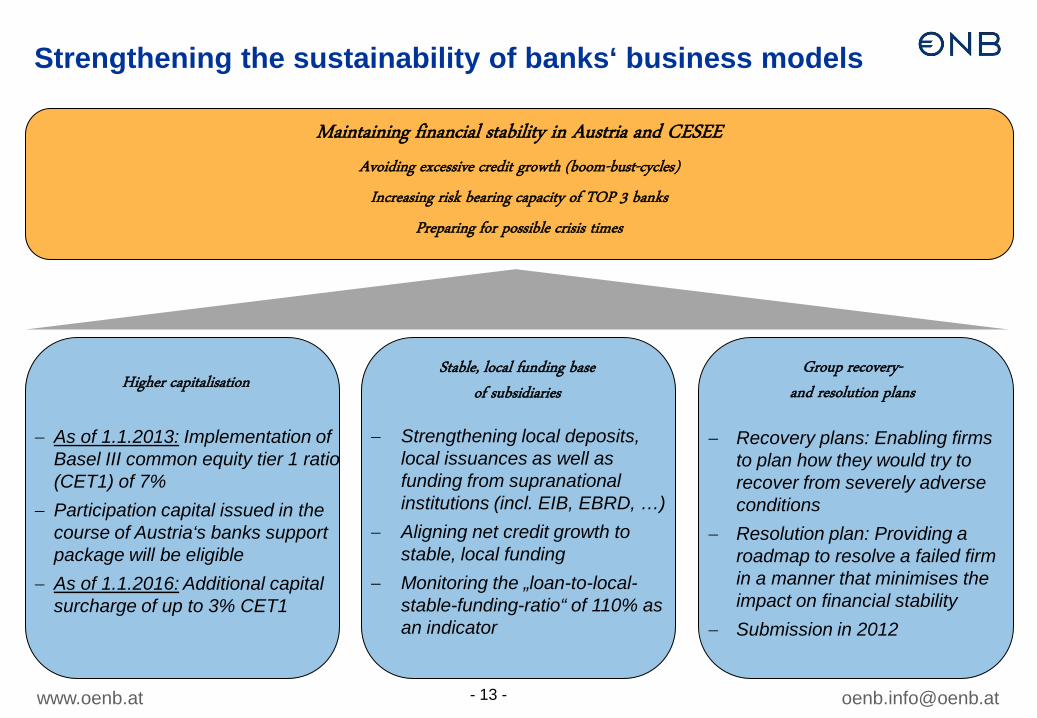

Strengthening the sustainability of banks‘ business models

Higher capitalisation

Stable, local funding base of subsidiaries

Group recovery- and resolution plans

− Recovery plans: Enabling firms to plan how they would try to recover from severely adverse conditions

− Resolution plan: Providing a roadmap to resolve a failed firm in a manner that minimises the impact on financial stability

− Submission in 2012

− Strengthening local deposits, local issuances as well as funding from supranational institutions (incl. EIB, EBRD, …)

− Aligning net credit growth to stable, local funding

− Monitoring the „loan-to-local-stable-funding-ratio“ of 110% as an indicator

− As of 1.1.2013: Implementation of Basel III common equity tier 1 ratio (CET1) of 7%

− Participation capital issued in the course of Austria‘s banks support package will be eligible

− As of 1.1.2016: Additional capital surcharge of up to 3% CET1

Maintaining financial stability in Austria and CESEE

Avoiding excessive credit growth (boom-bust-cycles)

Increasing risk bearing capacity of TOP 3 banks

Preparing for possible crisis times

www.oenb.at [email protected] - 14 -

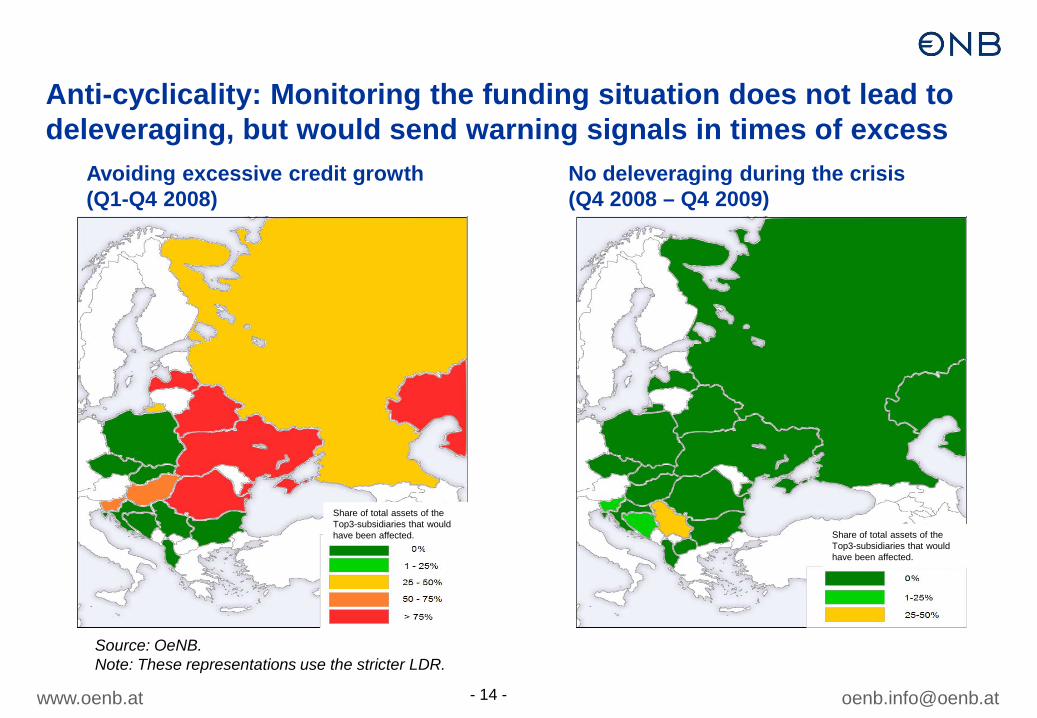

Anti-cyclicality: Monitoring the funding situation does not lead to deleveraging, but would send warning signals in times of excess

Avoiding excessive credit growth (Q1-Q4 2008)

Source: OeNB. Note: These representations use the stricter LDR.

No deleveraging during the crisis (Q4 2008 – Q4 2009)

Share of total assets of the Top3-subsidiaries that would have been affected.

Share of total assets of the Top3-subsidiaries that would have been affected.

www.oenb.at [email protected] - 15 -

Positive effects outweigh potential drawbacks

• Improved risk-bearing capacity at group level • The Austrian initiative

• Expedites the implementation of Basel III capital requirements • Therefore improves quantitative and qualitative aspects of capitalisation on a

permanent basis beyond the EBA June 2012 targets • Stability is not costless, yet higher capital further increases the resilience of

banks to adverse shocks … • … and thus further facilitates the pursuit of a low volatility retail banking model

• Strengthening of the local, stable funding base of subsidiaries • Sustainable growth instead of boom-bust cycles • Monitoring of the linkage between lending and local, stable funding • Improved stability of home and host economies and their banking systems • Continuation of the Vienna Initiative spirit (no deleveraging in crisis times)

4. Some concluding remarks on the general outlook of NPL resolution

www.oenb.at [email protected] - 17 -

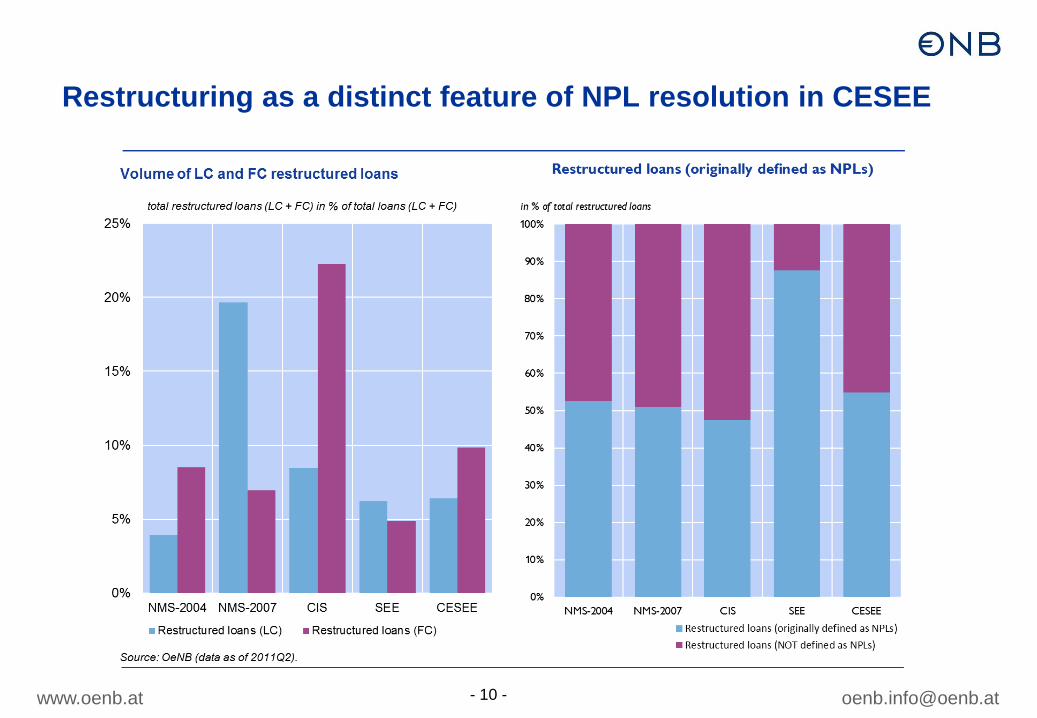

Lending forbearance/evergreening: NPL management tool or gamble for resurrection?

The Good…

Loan restructuring / lending forbearance is a viable tool to manage underperforming loans at the micro-level

…the Bad…

Empirical evidence (most prominently from Japan) shows that insolvent “zombie” banks are stuck in lending to

insolvent “zombie” borrowers in a “gamble for resurrection” no new lending Inefficient firms might anticipate forbearance (creating moral hazard)

…and the Ugly

When this behaviour becomes systemic (e.g. after a boom-bust-cycle) it poses a risk for the economic recovery

• Misallocation of credit to “zombie” instead of healthy borrowers

• In this environment restructuring creates hidden credit risks due to migration from NPL to performing loan

class

• Stagnation of Japan’s economy in the 1990ies was inter alia attributable to lending forbearance (Kobayashi et

al., 2002, Caballero et al., 2008)

www.oenb.at [email protected] - 18 -

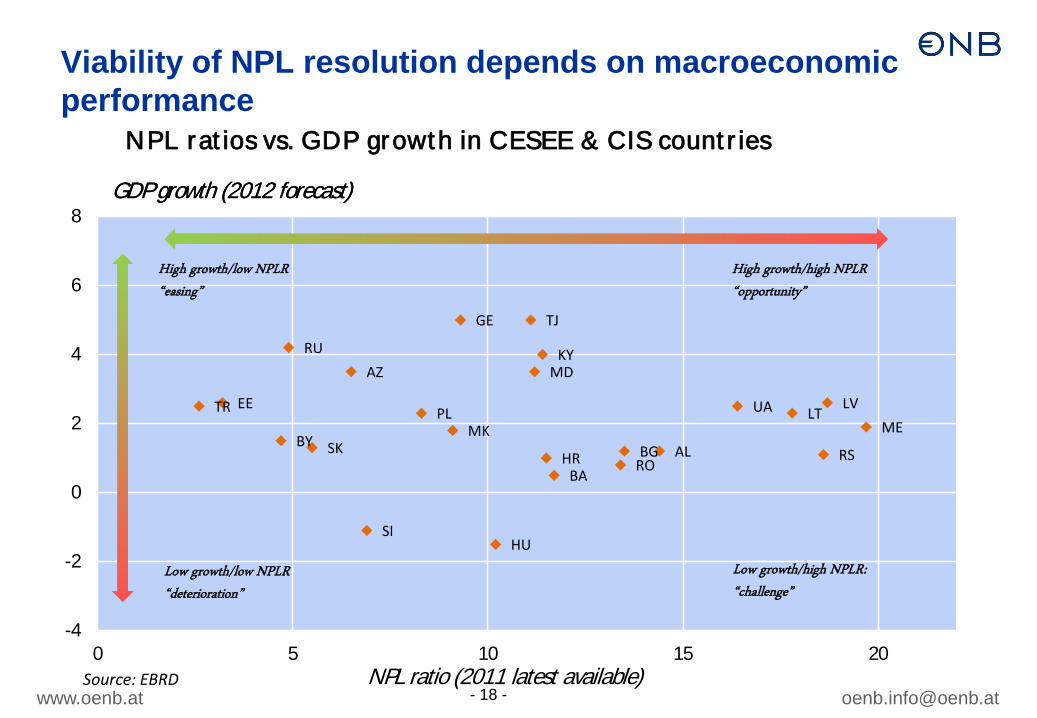

HR

EE

HU

LVLTPL

SK

SI

AL

BA

BGMK ME

RORS

AZ

BY

GE

MD

UATR

RU KY

TJ

-4

-2

0

2

4

6

8

0 5 10 15 20NPL ratio (2011 latest available)

GDP growth (2012 forecast)

NPL rat ios vs. GDP growth in CESEE & CIS count r ies

GDP growth (2012 forecast)

Source: EBRD

Viability of NPL resolution depends on macroeconomic performance

Low growth/high NPLR: “challenge”

High growth/high NPLR “opportunity”

High growth/low NPLR “easing”

Low growth/low NPLR “deterioration”

APPENDIX

www.oenb.at [email protected] - 20 -

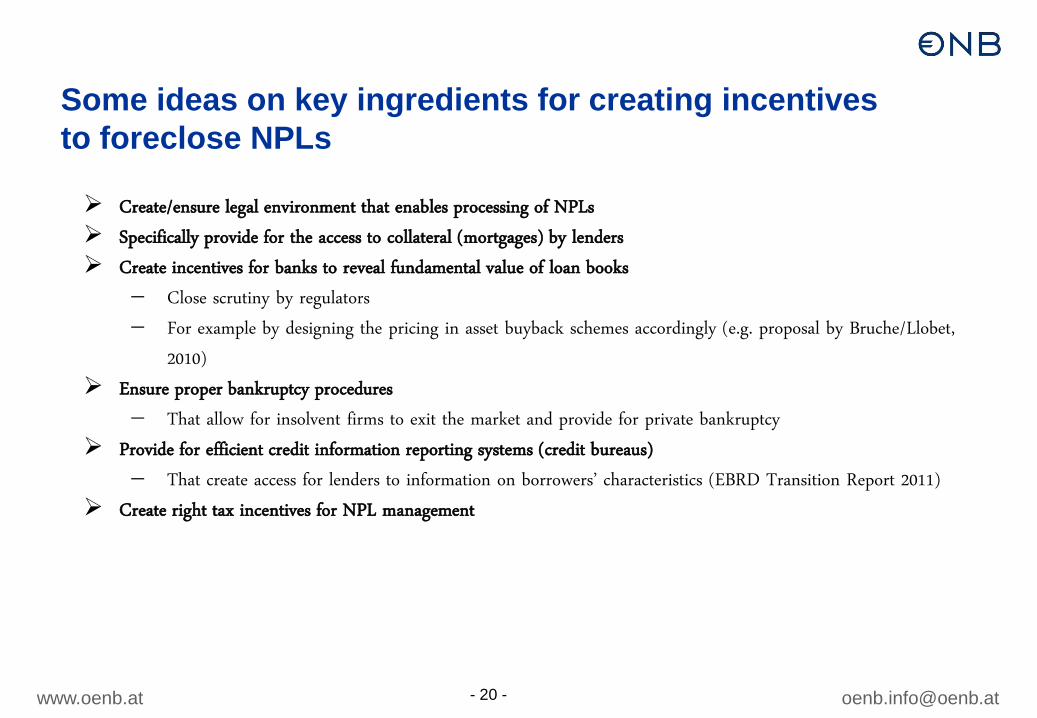

Some ideas on key ingredients for creating incentives to foreclose NPLs

Create/ensure legal environment that enables processing of NPLs

Specifically provide for the access to collateral (mortgages) by lenders

Create incentives for banks to reveal fundamental value of loan books

− Close scrutiny by regulators

− For example by designing the pricing in asset buyback schemes accordingly (e.g. proposal by Bruche/Llobet,

2010)

Ensure proper bankruptcy procedures

− That allow for insolvent firms to exit the market and provide for private bankruptcy

Provide for efficient credit information reporting systems (credit bureaus)

− That create access for lenders to information on borrowers’ characteristics (EBRD Transition Report 2011)

Create right tax incentives for NPL management

www.oenb.at [email protected] - 21 -

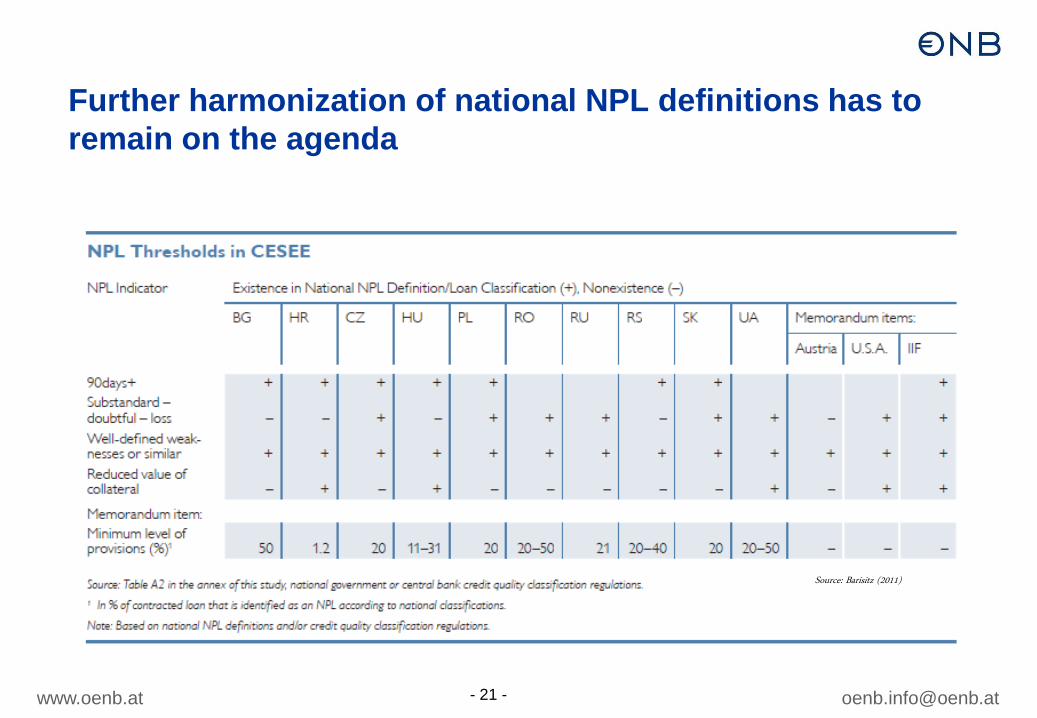

Further harmonization of national NPL definitions has to remain on the agenda

Source: Barisitz (2011)

www.oenb.at [email protected] - 22 -

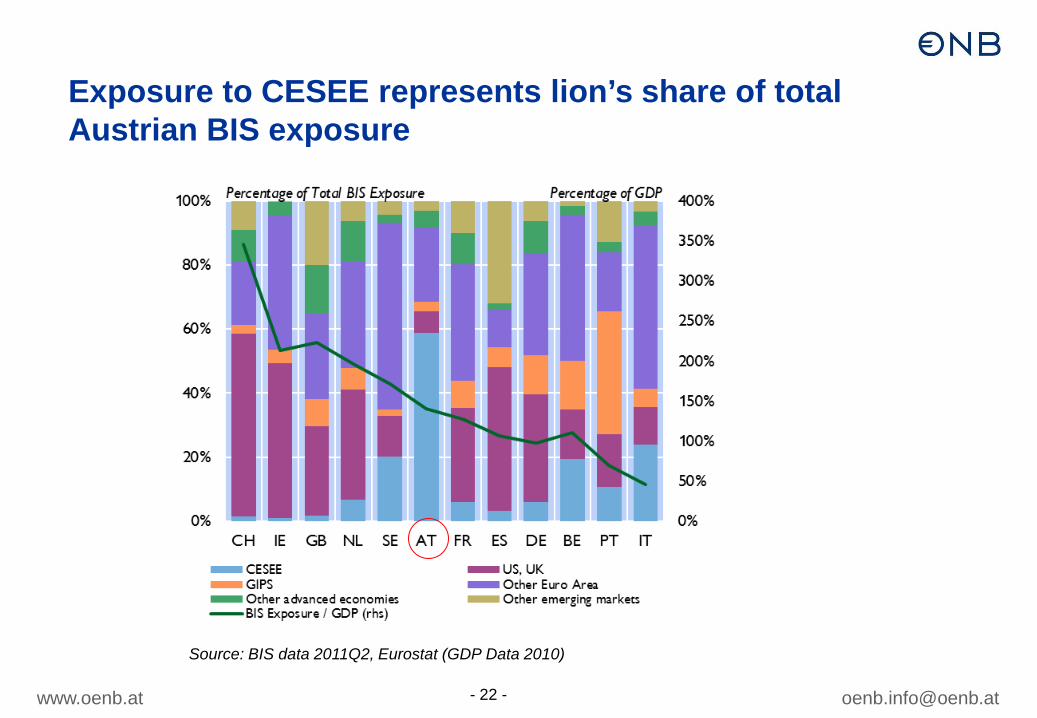

Exposure to CESEE represents lion’s share of total Austrian BIS exposure

Source: BIS data 2011Q2, Eurostat (GDP Data 2010)

www.oenb.at [email protected] - 23 -

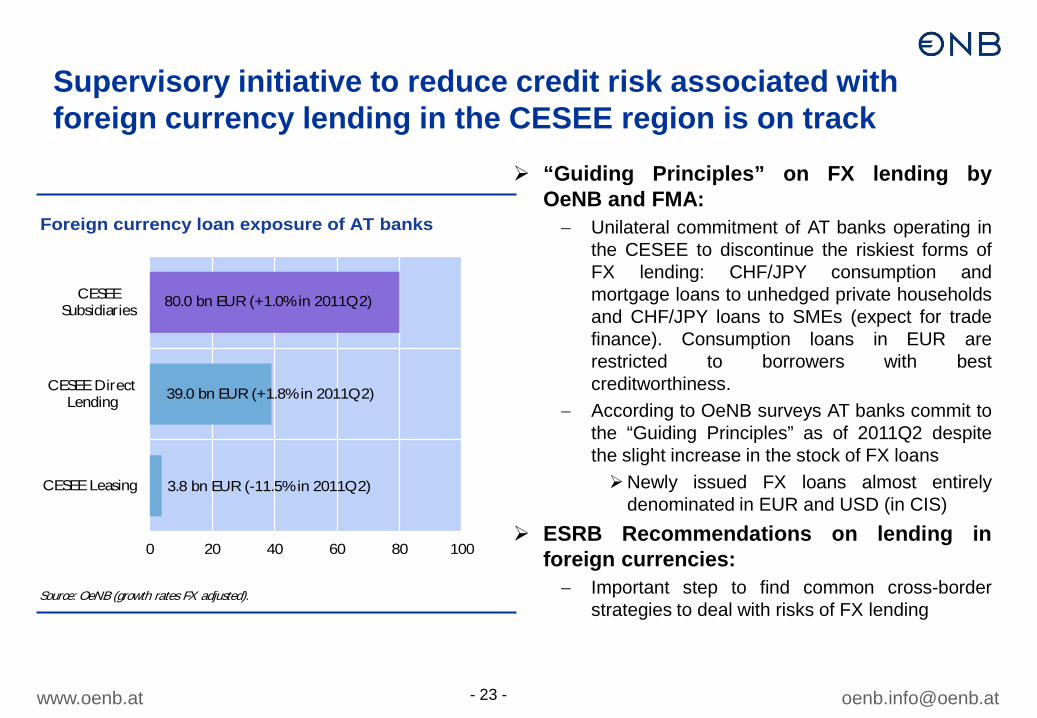

Supervisory initiative to reduce credit risk associated with foreign currency lending in the CESEE region is on track

0 20 40 60 80 100

CESEE Leasing

CESEE DirectLending

CESEESubsidiaries

Foreign currency loan exposure of AT banks

3.8 bn EUR (-11.5% in 2011Q2)

80.0 bn EUR (+1.0% in 2011Q2)

39.0 bn EUR (+1.8% in 2011Q2)

Source: OeNB (growth rates FX adjusted).

“Guiding Principles” on FX lending by OeNB and FMA: − Unilateral commitment of AT banks operating in

the CESEE to discontinue the riskiest forms of FX lending: CHF/JPY consumption and mortgage loans to unhedged private households and CHF/JPY loans to SMEs (expect for trade finance). Consumption loans in EUR are restricted to borrowers with best creditworthiness.

− According to OeNB surveys AT banks commit to the “Guiding Principles” as of 2011Q2 despite the slight increase in the stock of FX loans Newly issued FX loans almost entirely

denominated in EUR and USD (in CIS) ESRB Recommendations on lending in

foreign currencies: − Important step to find common cross-border

strategies to deal with risks of FX lending

www.oenb.at [email protected] - 24 -

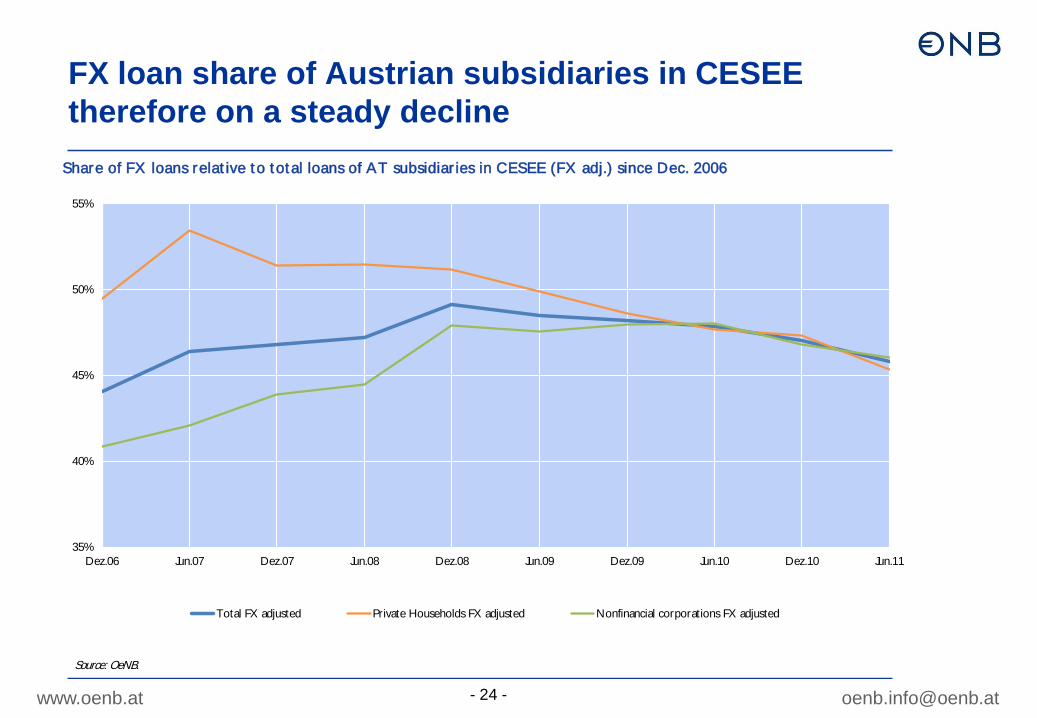

FX loan share of Austrian subsidiaries in CESEE therefore on a steady decline

35%

40%

45%

50%

55%

Dez.06 Jun.07 Dez.07 Jun.08 Dez.08 Jun.09 Dez.09 Jun.10 Dez.10 Jun.11

Total FX adjusted Private Households FX adjusted Nonfinancial corporations FX adjusted

Share of FX loans relat ive to total loans of AT subsidiar ies in CESEE (FX adj.) since Dec. 2006

Source: OeNB.

www.oenb.at [email protected] - 25 -

Strengthening the local stable funding base of subsidiaries A general guideline for achieving a sensible balance

• Guideline only applicable to subsidiaries with an LLSFR above 110% • Flexibility and proportionality concerns are given due consideration 1. Large subsidiaries: Net new lending limits with a degree of flexibility

• Net new lending should not exceed 110% of the increase in local stable funding, but…

• Flow ratio may be exceeded in extraordinary circumstances (clear limits)…

• Any over-shooting should be (over-)compensated at the respective subsidiaries over the following three years.

2. Smaller subsidiaries – Proportionality principle* • Net new lending limits do not apply

• Reduction of the (stock) LLSFR over the medium term

* This exemption will only be applicable to a limited amount of banks.