1

Recent Advances in Mathematical Programming Techniques for the Optimization of Process Systems under Uncertainty

Ignacio E. GrossmannRobert M. Apap, Bruno A. Calfa, Pablo Garcia-Herreros, Qi Zhang

Center for Advanced Process Decision-makingDepartment of Chemical Engineering

Carnegie Mellon UniversityPittsburgh, PA 15213, U.S.A.

Presented at PSE2015-ESCAPE 2531 May - 4 June 2015

Copenhagen, Denmark

EWO Seminar, September 15, 2015

2

Motivation Optimization under UncertaintyOptimization models for synthesis, design, planning, scheduling and control often involve uncertainties (parameters)

Design/SynthesisQuality feedstocksKinetic constantsTransfer coefficients

Supply Chain/PlanningProduct demandsPrices productsYields

Basic questions: How to model problems with uncertainty?How to solve them effectively?How to account for historical data/forecasts?

3

History in Process Systems Engineering

Optimal Design under Uncertainty (Stochastic Programming)Takamatsu, Hashimoto, Shioya (1973)Dittmar and Hartmann (1976)Johns, Marketos, Rippin (1976)Grossmann and Sargent (1978)

Planning under Uncertainty (Stochastic Programming)Liu, Sahinidis (1996)Acevedo, Pistikopoulos (1998)Gupta, Maranas (2000)Applequist, Pekny, Reklaitis(2000)

Robust OptimizationFriedman, Rekalitis (1975)Swaney, Grossmann (1985)Lin, SL Janak, CA Floudas (2004)

Chance constrainedArellano-Garcia, Martini, Wendt, Li, Wozny (2003)

Sample papers

4

Stage 1Here & now

RecourseWait & seeu

u1

u2

If deterministic uncertainty set

Robust Optimization: Ensure feasibility over uncertainty set

Approaches to Optimization under Uncertainty Sahinidis (2004)

How to anticipate effects of uncertainty?

If probability distribution functionStochastic Programming: Expected value, recourse actions

Chance Constrained Optimization: Ensure feasibility level confidence

Impact of optimization under uncertaintyhas been limited in industrial practice

Major reasons: ill-defined problem, computational expense

Option: add risk measure

u1

u2

U

5

Several major challenges and barriers:

1. How to avoid overly conservative results in robust optimization?

2. How to effectively solve two- or multi-stage stochastic optimization problems?

3. How to handle complexity of exogenous and endogenous uncertainties in multi-stage stochastic programming?

4. How to incorporate historical data in the generation of scenarios?

Presentation restricted to LP/MILP models

6

Remove uncertain parametersin the objective:

Robust Optimization

Ben-Tal et al. (2009); Bertsimas and Sim (2003)

Major concern: feasibility over uncertainty set

Uncertainty set

LP:

UumibxuAst

xcT

x

,...1)(

min

Uncertainty sets

u1

u2

u1

u2

Semi-infinite programming problem

7

Scheduling: Lin, Janak, Floudas (2004)Bertsimas, Thiele (2006)Li, Ierapetritou (2008)Verderame, Floudas (2010)Vujanic et al. (2012)

Supply Chain:Bertsimas, Sim (2003)Bertsimas, Thiele (2004)Hahn, Kuhn (2012)Gounaris, Wiesemann, Floudas (2013)

Process Synthesis:Tay, Ng, Tan (2013)Kasivisvanathan et al. (2014)

Previous Work Robust Optimization

8

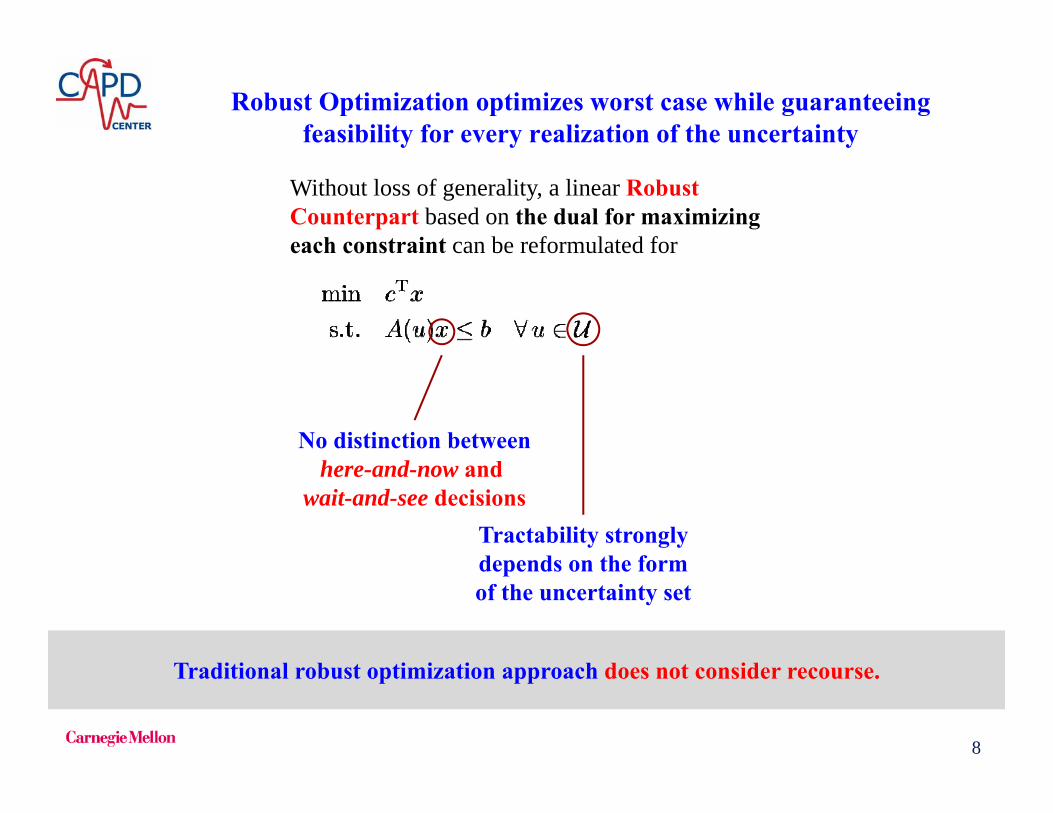

Robust Optimization optimizes worst case while guaranteeing feasibility for every realization of the uncertainty

Without loss of generality, a linear RobustCounterpart based on the dual for maximizingeach constraint can be reformulated for

No distinction betweenhere-and-now and

wait-and-see decisionsTractability stronglydepends on the formof the uncertainty set

Traditional robust optimization approach does not consider recourse.

9

Recourse: Decision rules are optimized with respect to uncertain parameters

Consider the following “two-stage” robust optimization problem:

1st stage 2nd stage

Instead of fixing the 2nd-stage decision variables, consider them to befunctions of the uncertain parameters. → Adjustable Robust Counterpart (ARC)

Recourse since reactive actions dependon the realization of the uncertainty

Ben-Tal et al. (2004). Math Programming.

10

Tractable reformulations can be obtained for the Adjustable Robust Counterpart in certain cases

1. Polyhedral or, more generally, conic uncertainty set:

2. Affine decision rules:

Dependence of parameters:

3. Fixed recourse( independent of ):

nominal values deviation

Affinely Adjustable Robust Counterpart (AARC)Ben-Tal et al. (2004). Math Programming.

where is a convex cone with dual .

11

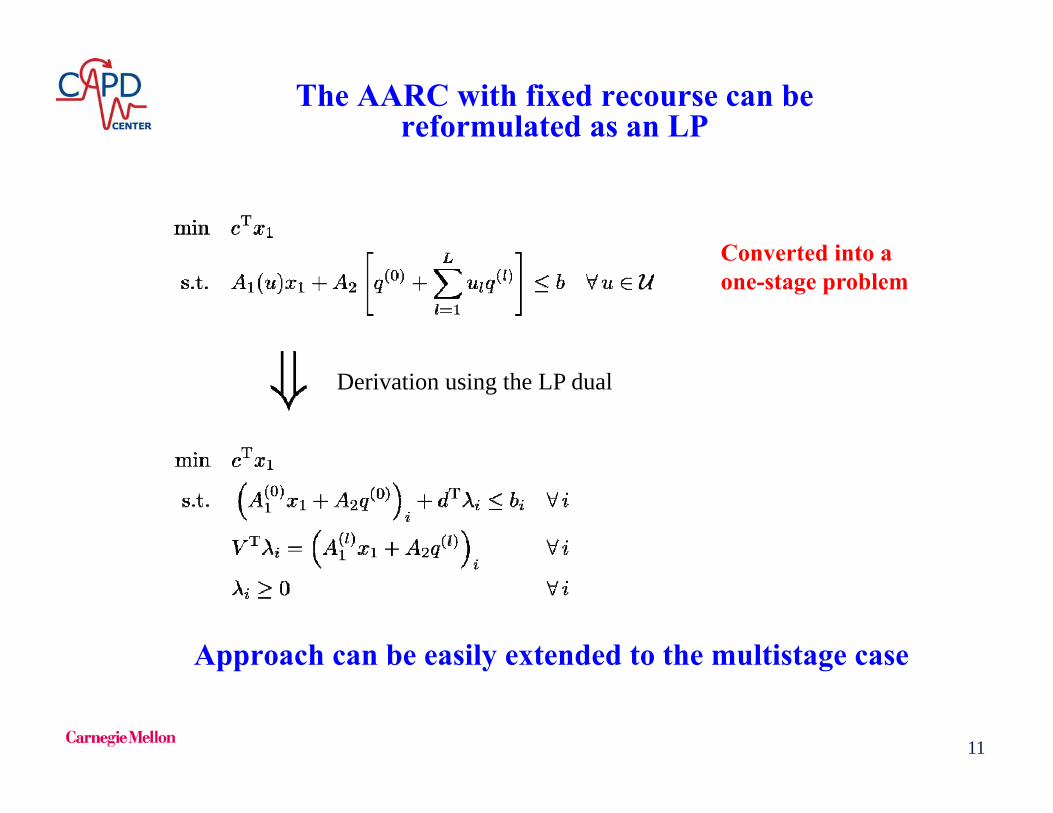

The AARC with fixed recourse can bereformulated as an LP

Derivation using the LP dual

Converted into aone-stage problem

Approach can be easily extended to the multistage case

12

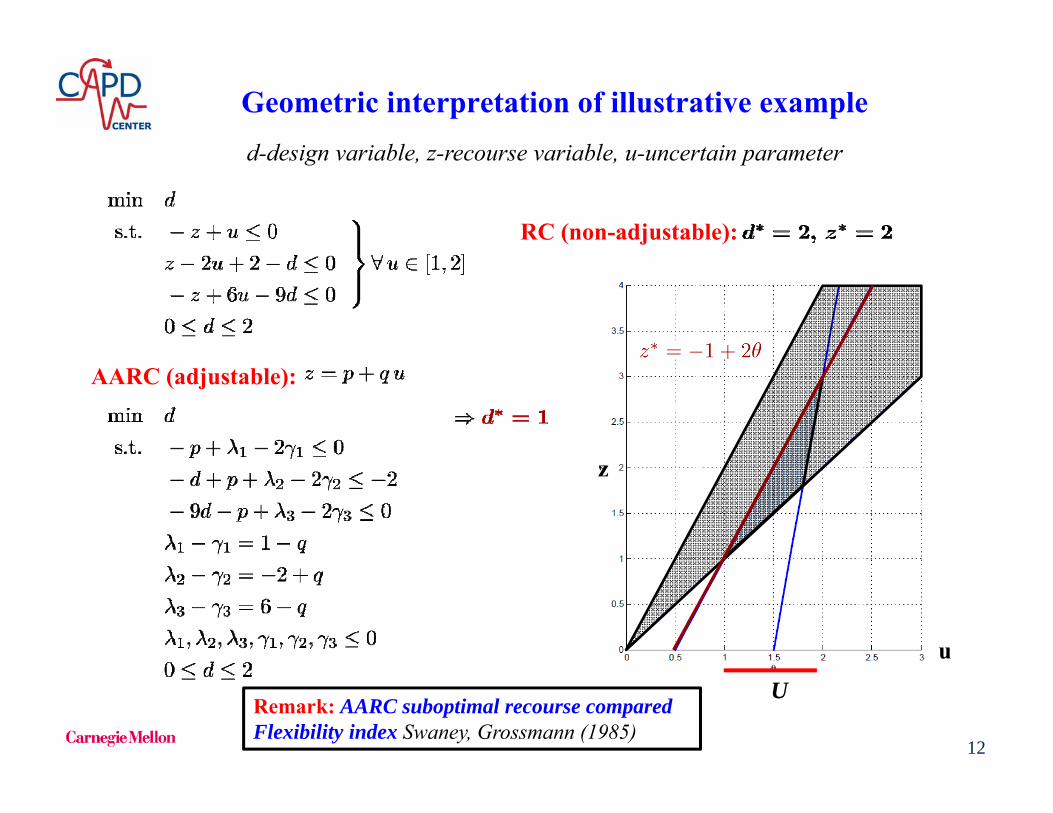

Geometric interpretation of illustrative example

RC (non-adjustable):

AARC (adjustable):

Remark: AARC suboptimal recourse comparedFlexibility index Swaney, Grossmann (1985)

z

u

d-design variable, z-recourse variable, u-uncertain parameter

U

13

Industrial case study: Integrated Air Separation Unit (ASU)-Cryogenic Energy Storage (CES) participates in two electricity markets*

Liquid inventory

Driox

Gas demand

Liquid demand

CES inventory

Electricity generation

Electricenergy market

ASU

Operating reserve market

LO2, LN2, LAr

LO2, LN2

GO2, GN2Vented gas

Sold electricity

Provided reserve

Purchased electricity

For internal use

Air

Purchasedliquid

LO2, LN2

Uncertainty in reserve demand

Zhang, Heuberger, Grossmann, Pinto, Sundramoorthy (2015)

14

AARC formulation ensures feasible schedule makingthe provision of operating reserve capacity possible.

• Multistage formulation: first stage: base plant operation, reserve capacity• recourse: liquid produced (linear with reserve demand)• Large-scale MILP: 53,000 constraints, 55,000 continuous variables, 2,500 binaries

CPLEX 12.5 , 10 min CPU-time (1% gap)

-0.1

-0.05

0

0.05

0.1

0

0.2

0.4

0.6

0.8

0 12 24 36 48 60 72 84 96 108 120 132 144 156 168

In a

nd O

ut F

low

s

CE

S In

vent

ory

Time [h] Liquid Flow into CES Tank Converted to Power for Internal Use Converted to Power to be Sold Committed Reserve Capacity CES Inventory Spinning Reserve Price Electricity Price

-0.1

-0.05

0

0.05

0.1

0

0.2

0.4

0.6

0.8

0 12 24 36 48 60 72 84 96 108 120 132 144 156 168

In a

nd O

ut F

low

s

CE

S In

vent

ory

Time [h]

-0.1

-0.05

0

0.05

0.1

0

0.2

0.4

0.6

0.8

0 12 24 36 48 60 72 84 96 108 120 132 144 156 168

In a

nd O

ut F

low

s

CE

S In

vent

ory

Time [h]

-0.1

-0.05

0

0.05

0.1

0

0.2

0.4

0.6

0.8

0 12 24 36 48 60 72 84 96 108 120 132 144 156 168

In a

nd O

ut F

low

s

CE

S In

vent

ory

Time [h]

-0.1

-0.05

0

0.05

0.1

0

0.2

0.4

0.6

0.8

0 12 24 36 48 60 72 84 96 108 120 132 144 156 168

In a

nd O

ut F

low

s

CE

S In

vent

ory

Time [h]

CES inventory profile plotted for the case of no dispatch

15

0

0.5

1

0.67 0.81 0.84

Prob

abili

ty

Uncertain Parameter Value

Stochastic programming is a scenario-based framework for optimization under uncertainty (Birge & Louveaux, 2011)

LM

H

0 1 2 Time horizon is divided into a set of

discrete time points

Uncertain parameters are described by adiscretized probability distribution

Stochastic Programming

Discretized distribution gives rise to Scenario Tree

L M H

u1 u2 u3

16

min )]...]()([...)()([ 222112

NNNuu uxucEuxucExcz N

s.t. 111 hxW

)()()( 222211 uhuxWxuT

)()()()( 111 uhuxWuxuT NNNNNNN

1,...,2,0)(,01 Ntuxx tt

…

Multistage Stochastic Programming

Special case: two-stage programming (N=2)

Birge & Louveaux, 1997; Sahinidis, 2004

Exogeneous uncertainties(e.g. demands)

x1 stage 1 u x2 recourse (stage 2)

u

17

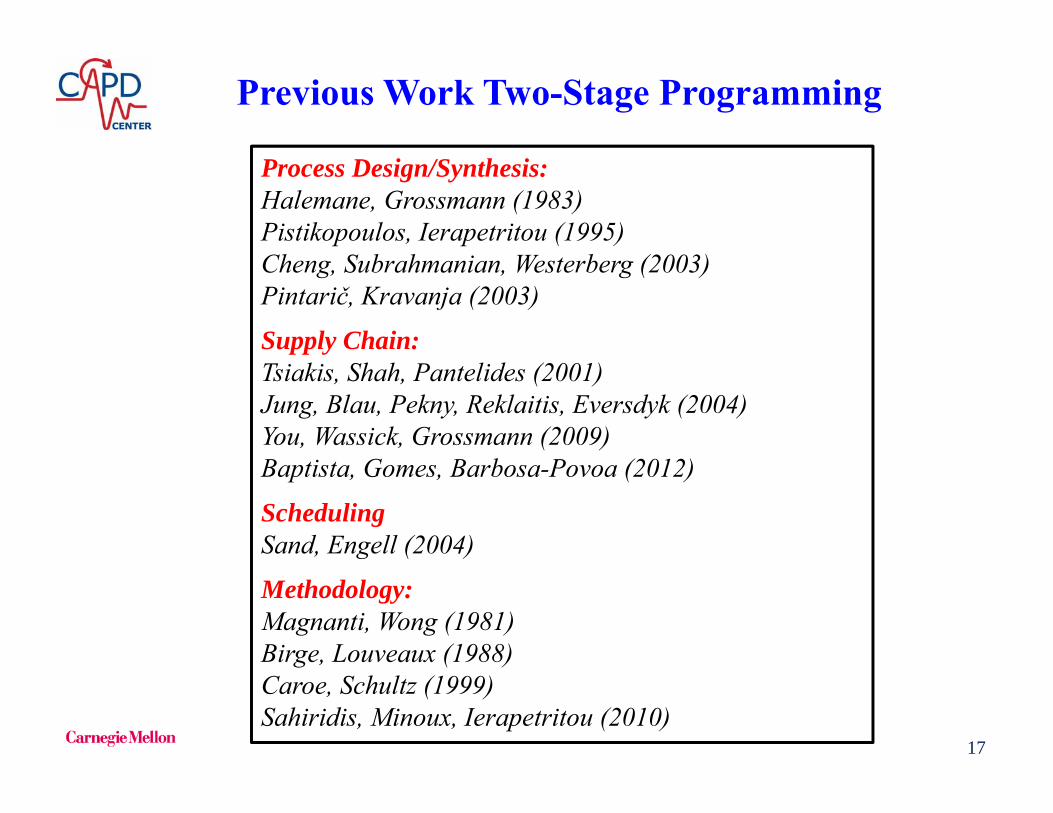

Process Design/Synthesis:Halemane, Grossmann (1983)Pistikopoulos, Ierapetritou (1995)Cheng, Subrahmanian, Westerberg (2003)Pintarič, Kravanja (2003)

Supply Chain:Tsiakis, Shah, Pantelides (2001)Jung, Blau, Pekny, Reklaitis, Eversdyk (2004)You, Wassick, Grossmann (2009)Baptista, Gomes, Barbosa-Povoa (2012)

SchedulingSand, Engell (2004)

Methodology: Magnanti, Wong (1981)Birge, Louveaux (1988)Caroe, Schultz (1999)Sahiridis, Minoux, Ierapetritou (2010)

Previous Work Two-Stage Programming

18

Decomposition Techniques

18

A

D1

D3

D2

Complicating Constraints

max

1,..{ , 1,.. , 0}

T

i i i

i i

c xst Ax b

D x d i nx X x x i n x

x1 x2 x3

Lagrangean decompositionGeoffrion (1972) Guinard (2003)

complicatingconstraints

D1

D3

D2

Complicating Variables

A

x1 x2 x3y

1,..max

1,..0, 0, 1,..

T Ti i

i n

i i i

i

a y c x

st Ay D x d i ny x i n

complicatingvariables

Benders decompositionBenders (1962), Magnanti, Wong (1984)

Multistage Stochastic ProgrammingTwo-stage Stochastic Programming

19

Supply plant

Candidate locations for DCs with risk of major disruption earthquakes, fires, strikes

Customers with deterministic demands for multiple commodities

Scenarios given by the combination of disruptions

Selecting DCs among candidate locations

Determining storage capacity in selected DCs

Allocating demands in every scenario

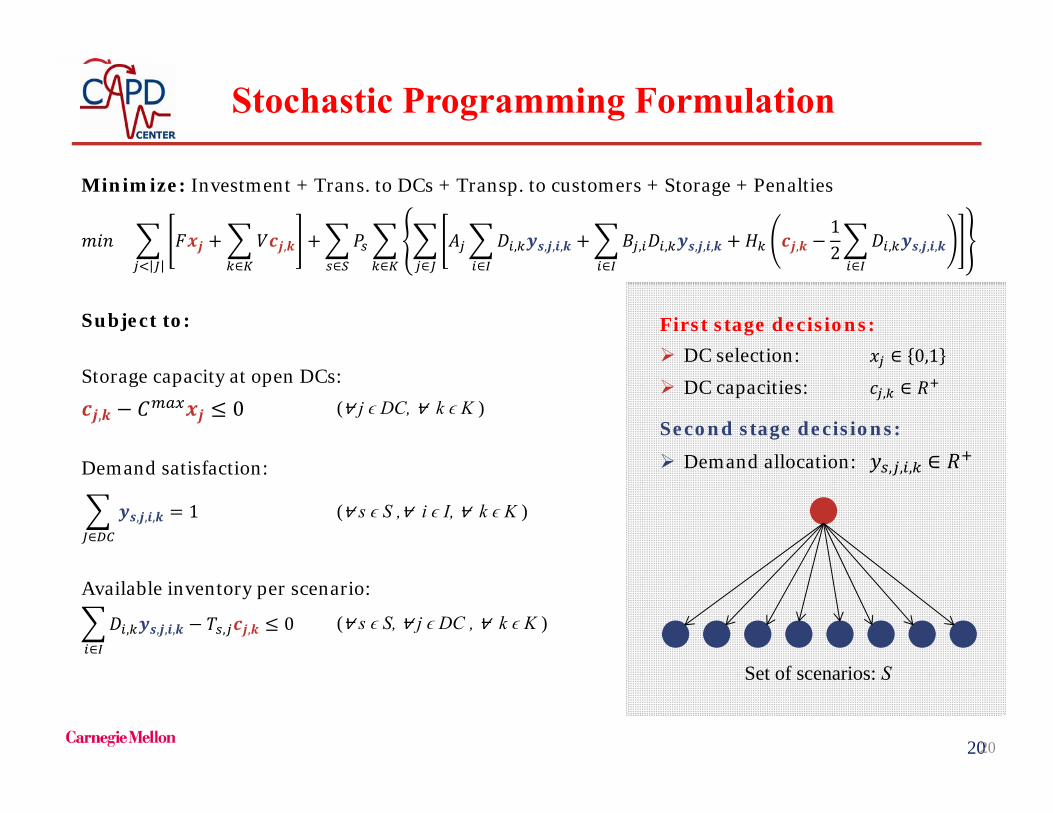

Supply Chain Design with Risk of Disruptions

Given:

Minimize cost by:

DCs=Distribution Centers

Garcia-Herreros, Wassick, Grossmann (2014)

2020

Minimize: Investment + Trans. to DCs + Transp. to customers + Storage + Penalties

,∈

, , , ,∈

, , , , ,∈

,12 , , , ,

∈∈∈∈

Subject to:

Storage capacity at open DCs:

, 0

Demand satisfaction:

, , ,∈

1

Available inventory per scenario:

, , , ,∈

, , 0

(⩝ s ϵ S ,⩝ i ϵ I, ⩝ k ϵ K )

(⩝ j ϵ DC, ⩝ k ϵ K )

(⩝ s ϵ S, ⩝ j ϵ DC , ⩝ k ϵ K )

Stochastic Programming Formulation

Set of scenarios: S

First stage decisions: DC selection: ∈ 0,1

DC capacities: , ∈

Second stage decisions:

Demand allocation: , , , ∈

21

(You & Grossmann, 2008)

Supply chain network: 1 production plant 3 candidate locations for DCs 6 customers 1 commodity

Deterministicformulation

Resilientformulation

Computationalstatistics

Problem type MILP MILPNo. of constraints 13 76No. of continuous variables 31 199No. of binary variables 3 3Solution time 0.058s 0.405s

Expectedcostsunderriskofdisruptions

Investment ($) 279,900 419,850Transportation to DCs ($) 70,098 68,971Transportation to customers ($) 59,029 54,683Storage ($) 1,593 2,927Penalties ($) 674,703 54,244Total ($): 1,085,323 600,675

Solution Storage capacity 298/‐ /501 400/400/400

Illustrative Example

22

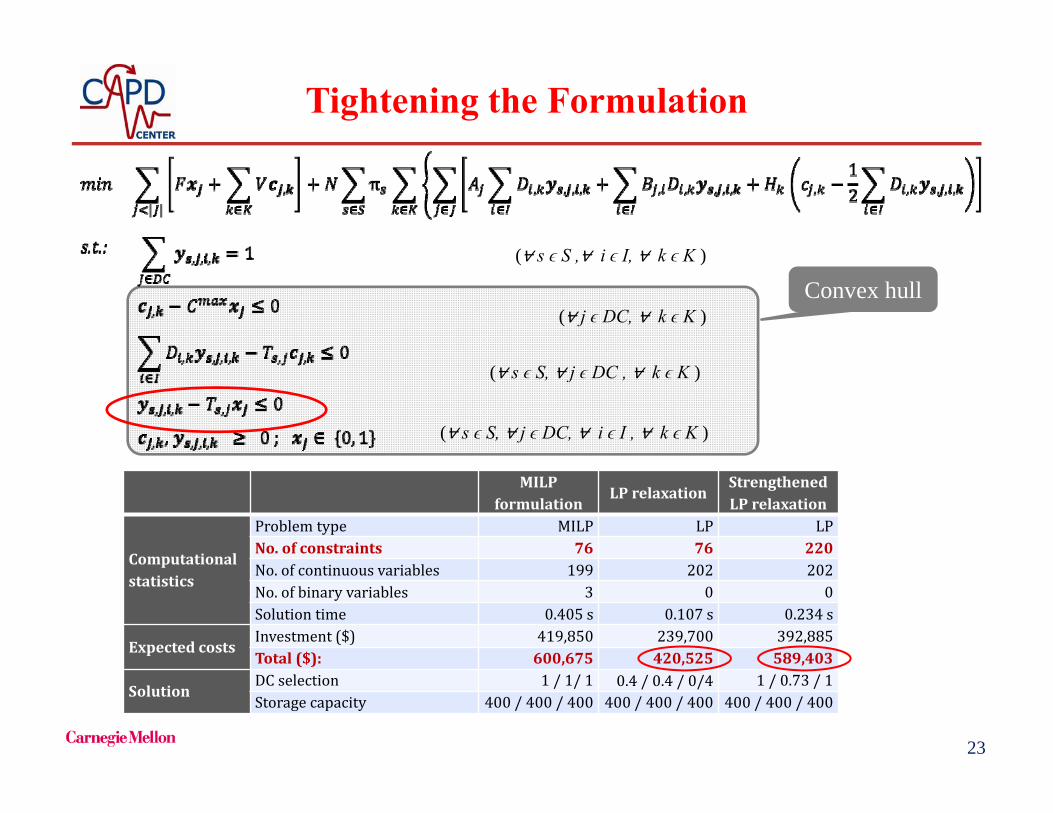

Challenges

Relaxation

Weak LP relaxation Time consuming for

Branch-and-bound

Scenarios’ probabilities

Different orders of magnitude among scenario probabilities

Number of scenarios

Exponential growth with number of candidate DCs

Approaches

Relaxation

Tightening constraints

Strengthen Benders master problem by including first scenario

Scenarios’ probabilities

Select the relevant subset of scenarios

Find deterministic bounds on the remaining scenarios

Number of scenarios

Solve a subset of scenarios Multicut Benders

decomposition

23

(⩝ s ϵ S ,⩝ i ϵ I, ⩝ k ϵ K )

(⩝ j ϵ DC, ⩝ k ϵ K )

(⩝ s ϵ S, ⩝ j ϵ DC , ⩝ k ϵ K )

(⩝ s ϵ S, ⩝ j ϵ DC, ⩝ i ϵ I , ⩝ k ϵ K )

Convex hull

MILPformulation

LPrelaxationStrengthenedLPrelaxation

Computationalstatistics

Problem type MILP LP LPNo. of constraints 76 76 220No. of continuous variables 199 202 202No. of binary variables 3 0 0Solution time 0.405s 0.107s 0.234s

ExpectedcostsInvestment ($) 419,850 239,700 392,885Total ($): 600,675 420,525 589,403

SolutionDC selection 1/1/1 0.4/0.4/0/4 1/0.73 /1Storage capacity 400/400/400 400/400/400 400/400/400

Tightening the Formulation

24

Reduction Number of Scenarios

- Sampling: ProbabilisticSampling Average Approximation (Shapiro & Homem-de-Mello (2000)

Predict probabilistic lower/upper bounds

- Scenario tree reduction: DeterministicOptimal scenario reduction (Heitsch, Roemisch, 2003; Li, Floudas, 2012))

Exclude scenarios within certain probability distance

- Reduction based on magnitude of probabilitiese.g. Supply chain disruptions

Probabilities of no disrupt > up to 1 > up to 2 > up to 3...

25

Assignment policyFind an upper bound by calculating the cost in the subset of neglected scenarios of a policy that is always feasible

Policy: attempt main-scenario assignments for all demands• If assignment is feasible (DC is active) => cost of main-scenario• If assignment is infeasible (DC is disrupted) => cost of penalty

The proportion in which assignments (y1,j,i,k) are feasible is given by the conditionalprobability of disruption at DC j ( ) in the subset of neglected scenarios ( )

Properties of scenarios generated from independent disruption probabilities

25

Bounds on Neglected Scenarios

26

Algorithmic Implementation Benders Decomposition

Subset Scenarios

Indistinguishable Scenarios

Multi-cuts

Pareto cuts

Parallel computation

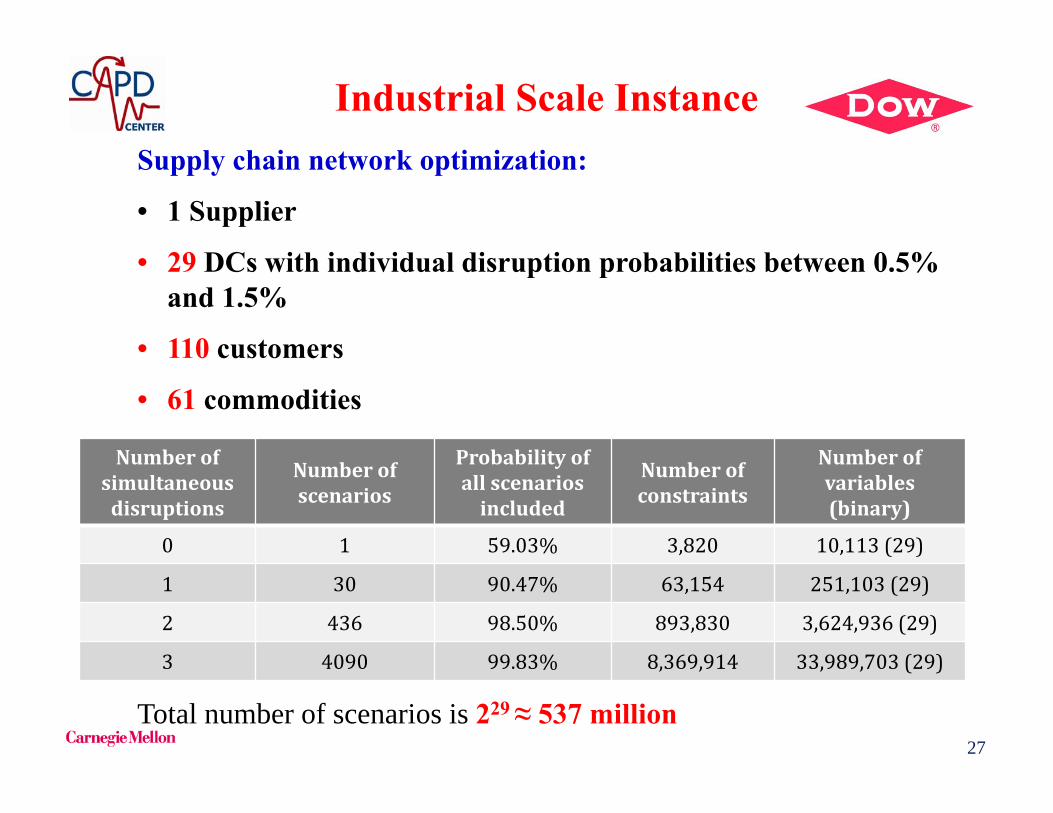

27

Industrial Scale InstanceSupply chain network optimization:

• 1 Supplier

• 29 DCs with individual disruption probabilities between 0.5% and 1.5%

• 110 customers

• 61 commodities

Total number of scenarios is 229 ≈ 537 million

Numberofsimultaneousdisruptions

Numberofscenarios

Probabilityofall scenariosincluded

Numberofconstraints

Numberofvariables(binary)

0 1 59.03% 3,820 10,113(29)

1 30 90.47% 63,154 251,103(29)

2 436 98.50% 893,830 3,624,936(29)

3 4090 99.83% 8,369,914 33,989,703(29)

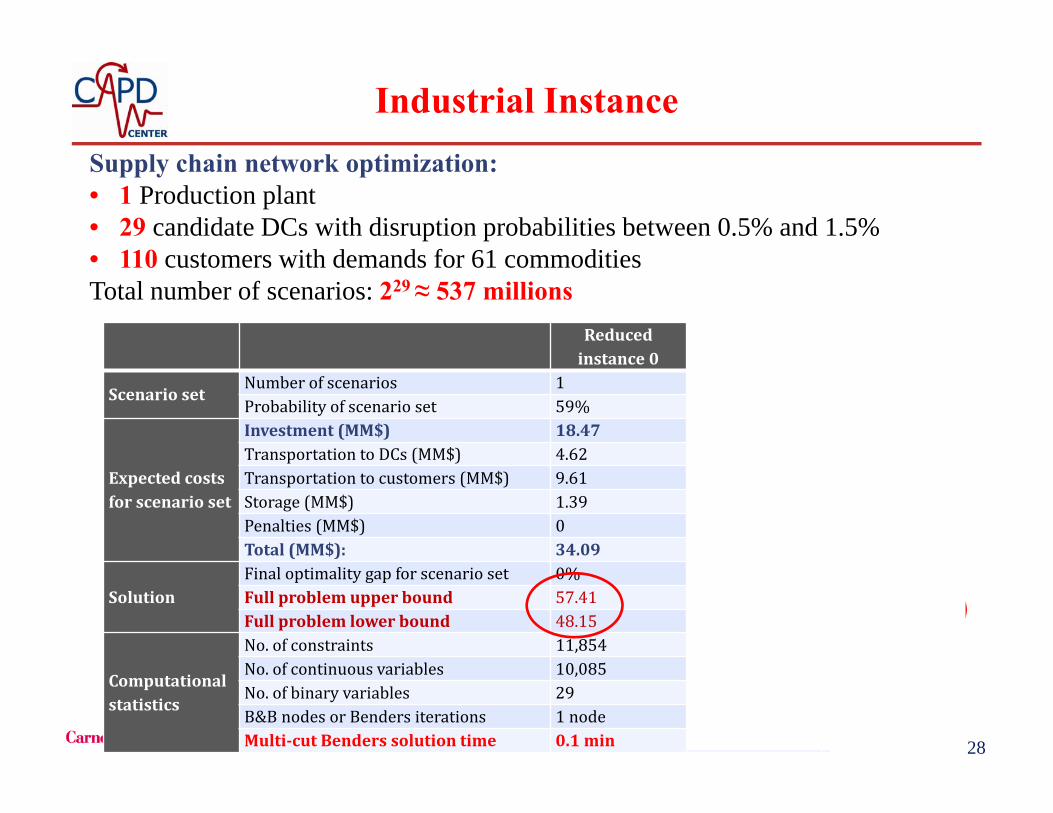

28

Supply chain network optimization:• 1 Production plant• 29 candidate DCs with disruption probabilities between 0.5% and 1.5%• 110 customers with demands for 61 commoditiesTotal number of scenarios: 229 ≈ 537 millions

28

Reducedinstance0

Reducedinstance1

Reducedinstance2

ScenariosetNumber of scenarios 1 30 436Probability of scenario set 59% 90.5% 98.5%

Expectedcostsforscenarioset

Investment (MM$) 18.47 18.77 21.56Transportation to DCs (MM$) 4.62 11.11 11.72Transportation to customers (MM$) 9.61 13.12 16.73Storage (MM$) 1.39 2.37 3.31Penalties (MM$) 0 3.31 0.54Total (MM$): 34.09 48.68 53.85

SolutionFinal optimality gap for scenario set 0% 0.78% 0.77%Full problem upper bound 57.41 56.31 55.10Full problem lower bound 48.15 52.87 53.87

Computationalstatistics

No. of constraints 11,854 304,261 4,397,989No. of continuous variables 10,085 251,191 3,626,675No. of binary variables 29 29 29B&B nodes or Benders iterations 1 node 4iterations 6iterationsMulti‐cut Benders solution time 0.1 min 84min 1762min

Industrial Instance

29

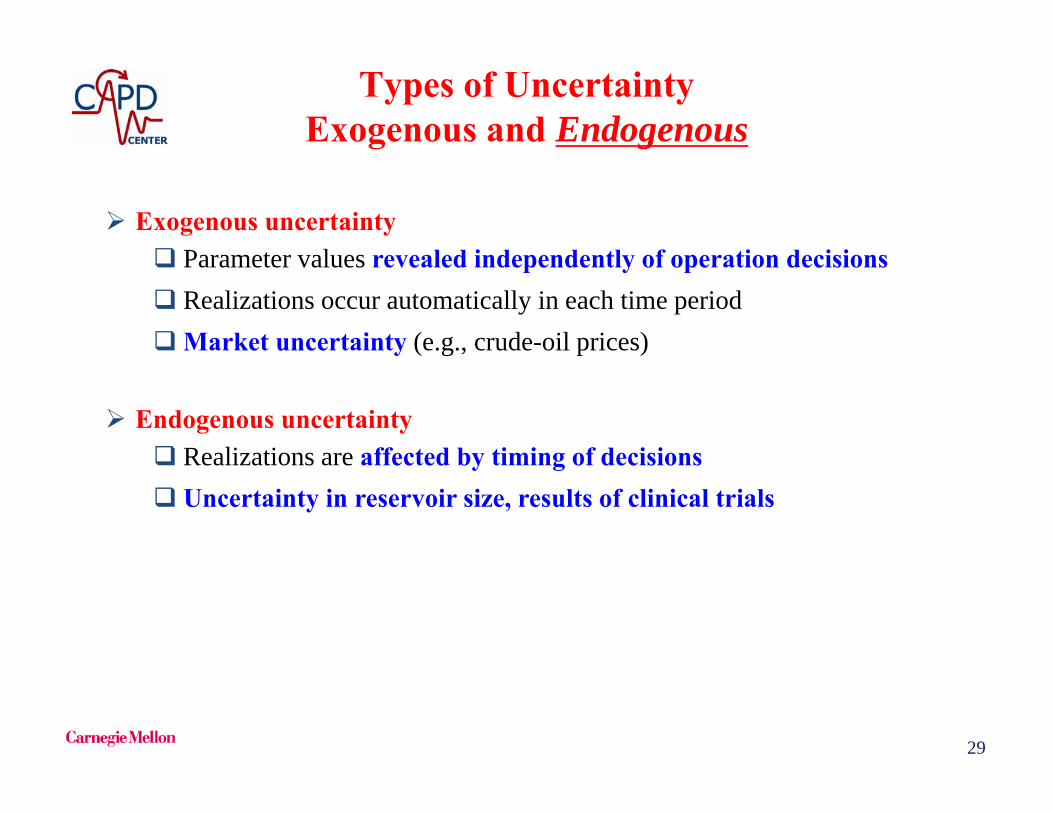

Types of UncertaintyExogenous and Endogenous

Exogenous uncertainty Parameter values revealed independently of operation decisions Realizations occur automatically in each time periodMarket uncertainty (e.g., crude-oil prices)

Endogenous uncertainty Realizations are affected by timing of decisions Uncertainty in reservoir size, results of clinical trials

30

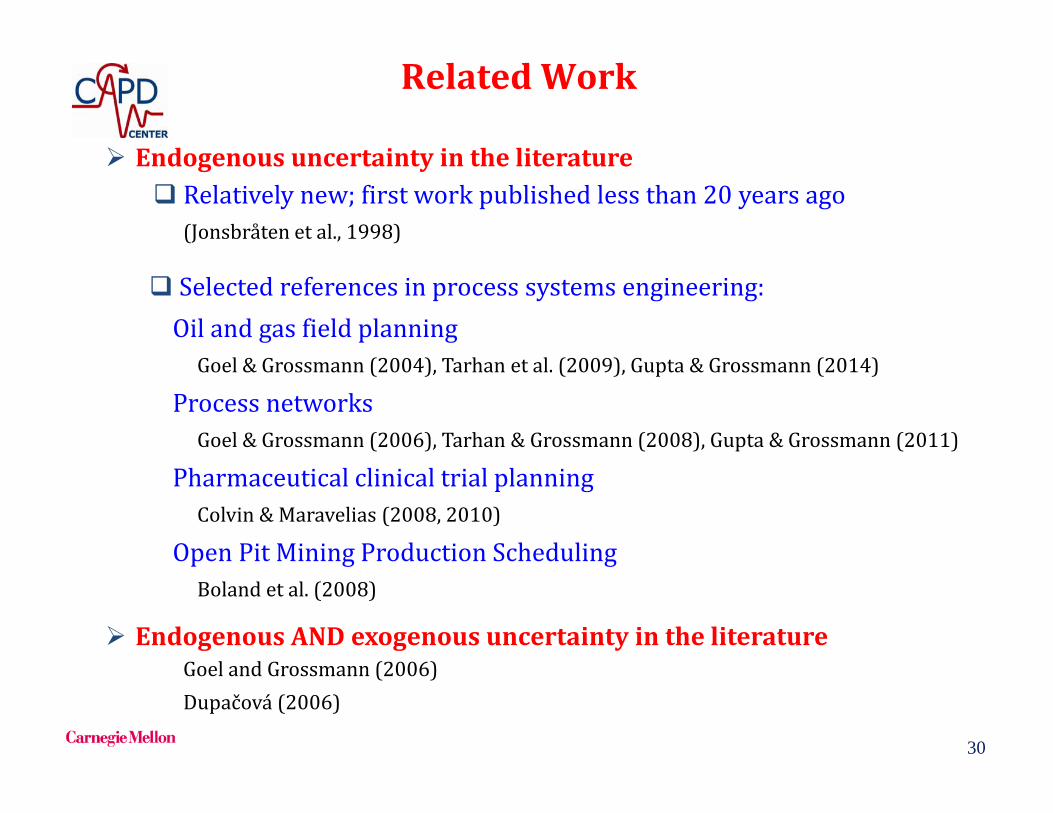

RelatedWork

Endogenousuncertaintyintheliterature Relativelynew;firstworkpublishedlessthan20yearsago

(Jonsbråten etal.,1998)

EndogenousANDexogenousuncertaintyintheliteratureGoel andGrossmann(2006)Dupačová (2006)

Selectedreferencesinprocesssystemsengineering:OilandgasfieldplanningGoel &Grossmann(2004),Tarhan etal.(2009),Gupta&Grossmann(2014)

ProcessnetworksGoel &Grossmann(2006),Tarhan &Grossmann(2008),Gupta&Grossmann(2011)

PharmaceuticalclinicaltrialplanningColvin&Maravelias (2008,2010)

OpenPitMiningProductionSchedulingBolandetal.(2008)

31

MSSP: Exogenous Uncertainty

Decision

Recourse action

Resolution of uncertainty for

0 1 2

1 2 3 4

1

2

0

1 2 3 4

1

2

0

Recourse action

DecisionResolution of uncertainty for

Fixed scenario treeNon-anticipativity

Ruszczynski (1997)

32

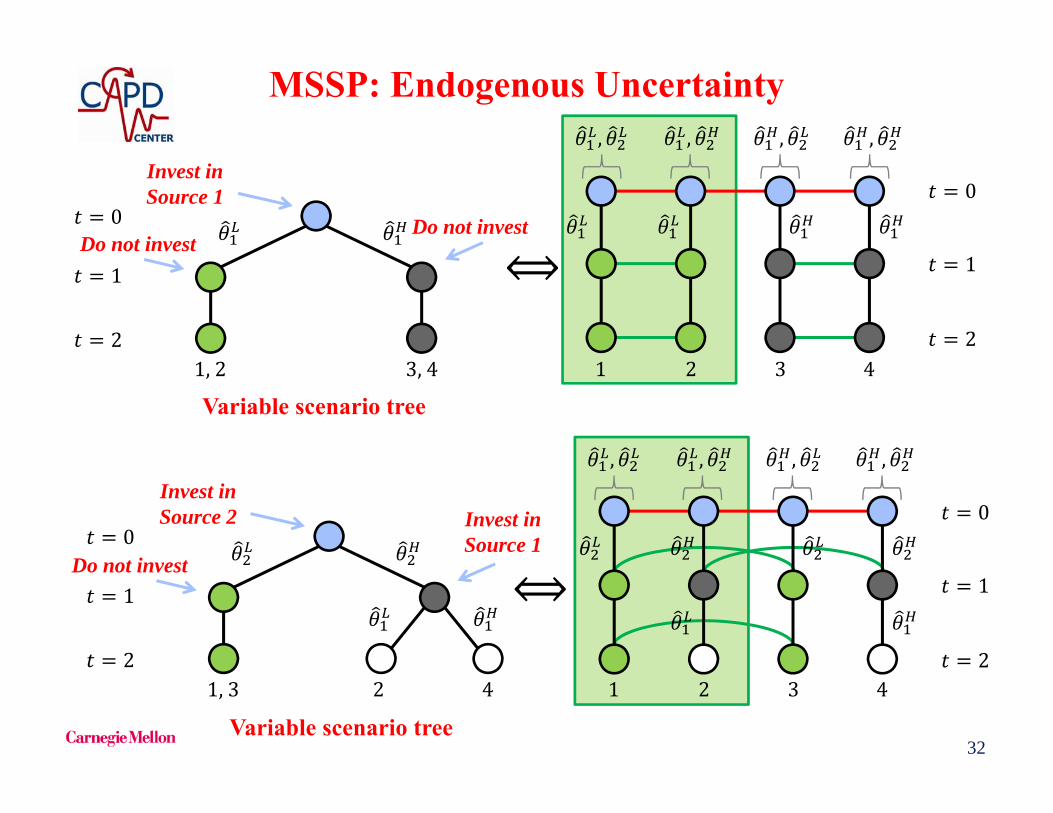

MSSP: Endogenous Uncertainty

1 2 3 4

1

2

0

, , , ,

Do not invest

1,2 3,4

Invest in Source 1

1

2

0Do not invest

Variable scenario tree

1 2 3 4

1

2

0

1,3 2 4

Invest in Source 2 Invest in

Source 1

1

2

0

, , , ,

Do not invest

Variable scenario tree

33

MSSP: Endogenous Uncertainty

33

Decision

Recourse action

Resolution of uncertainty

0 1 2

Recourse action

DecisionResolution of uncertainty

1 2 3 4

, , , ,

1

2

0,

⋁ ,

, ,

If ,

If , If ,

Superstructure scenario tree

34

MSSP: Endogenous and Exogenous Uncertainty

1 2 3 4

, , , ,

1

2

0

1 2 3 4

1

2

0

≔ ∈ ∈ Θ ,

, , … , , , … , ,, , … , ,

,

Θ ,∈∈

1, 2, … ,

≔ ∈ ∈ Ξ ,

, , … , , , … , ,, , … , ,

,

Ξ ,∈∈

1, 2, … ,

Exogenous

Endogenous

35

MSSP: Endogenous and Exogenous Uncertainty

‘Composite’ scenariotree

Endogenous and Exogenous

,

1

2

0

1 2 3 4

Subtree1

,

5 6 7 8

Subtree2

,

9 10 11 12

Subtree3

,

13 14 15 16

Subtree4

≔, , … , , , , , … , , , … , , , … , , , ,

, , … , ,, , … ,

,, , … , ,

, , , , … , , , … , ,, , … , ,

, , ,, , … , ,

,

1, 2, … ,

Endogenous

Exogenous subtrees

36

MSSP Formulation: Endogenous & Exogenous

Objectivefunction(minimizeexpectedcost)

Decision‐governing&period‐linkingconstraints

Bounds&integralityrestrictions

First‐periodNACs

s. t. , , , , , ,∈

∀ ∈ , ∈

FixedendogenousNACs

, , ∀ , ∈ , ∈ ∀ , ∈

∀ , , ∈ , ∈

, , ∀ , , ∈ , ∈ , ∈

∀ , , ∈ , ∈

min, ,

∈ , ,

∈∈

∀ ∈ , ∈ , ∈, ∈ 0,1 , ∈ , ∈ , ∈, ∈ , , , ∈ 0,1 ∀ , , ∈ , ∈

, ⇔ , , , , … , , ∀ , , ∈ , ∈ , ,

ConditionalendogenousNACs

Endogenousindistinguishabilityconstraints

1 , 1 , ∀ , , ∈ , ∈

1 ,, , 1 , ∀ , , ∈ , ∈ , , ∈

1 , 1 , ∀ , , ∈ , ∈ ,

ExogenousNACs∀ , , ∈

∀ , , ∈, , ∀ , , ∈ , ∈

VerylargenumberofconstraintsNACs

Apap, Grossmann (2015)

37

Eliminating Redundant NACs

1 2

1 5 13 1 2 5 6

1 2 3 4

Evenaftereliminatingredundantconstraints,modelsaretypicallystilltoolarge tobesolveddirectly

Specialsolutionmethods: Sequentialscenariodecomposition (SSD)heuristic Lagrangeandecomposition (LD)

Property1Symmetry

Properties2a&2bAdjacency

TransitivityProperties3&4

GroupingProperty5

Goel Gupta, Apap

38

Planningover5years Determineoptimalinvestmentandoperatingdecisions Here‐and‐nowdecisions:FPSOinstallationsandexpansions,field‐

FPSOconnections(9possible),well‐drillingschedule(30potentialwells) Recoursedecisions:Oilproductionrate

Objective: MaximizetotalexpectedNPV

GuptaandGrossmann,2014a

Totaloil/gasproduction

Oil/gasprice=?Exogenous

(Size=?)Endogenous

(Size=560MMbbls)(Size=500MMbbls)

*

FieldIFieldII

FieldIII

*www.rigzone.com

FPSO: floating production, storage and offloading

Example: Oilfield Development Planning

Piece-wise linearapproximationreservoir production

39

(2realizationsforsize)(1uncertainsize) 2endogenouscombinations

(2endogenouscombinations) (32exogenouscombinations) 64scenarios

(2realizationsforprice)(5timeperiods) 32exogenouscombinations

Totaloil/gasproduction

Oil/gasprice=?Exogenous

(Size=?)Endogenous

(Size=560MMbbls)(Size=500MMbbls)

*

FieldIFieldII

FieldIII

Example: Oilfield Development Planning

*www.rigzone.com

40

Totaloil/gasproduction

Oil/gasprice=?Exogenous

(Size=?)Endogenous

(Size=560MMbbls)(Size=500MMbbls)

FieldIFieldII

FieldIII

Example: Oilfield Development Planning

Begininstallingallinfrastructureinfirstyear:FPSO1,FPSO2

Drillingcannotstartuntilyear4duetoleadtimeforFPSOinstallation

Drillfieldswithknownsizefirst

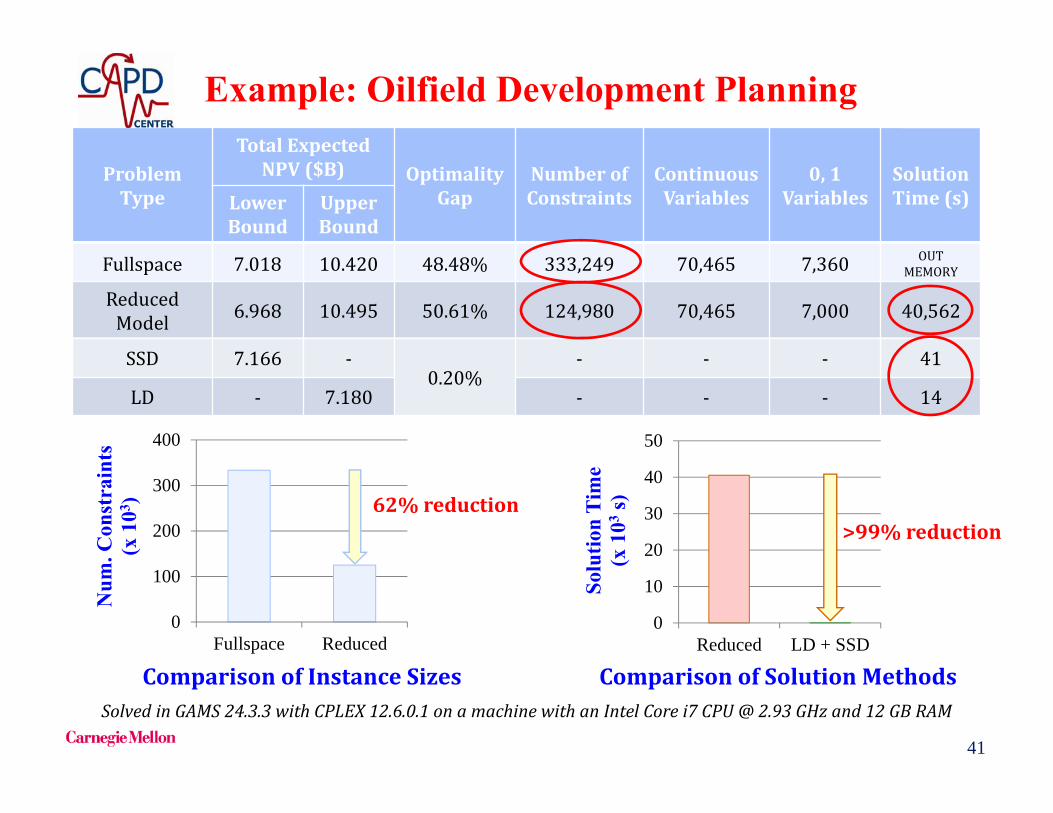

E[NPV] = $7.166 x 109

41

ProblemType

TotalExpectedNPV($B) Optimality

GapNumberofConstraints

ContinuousVariables

0,1Variables

SolutionTime(s)Lower

BoundUpperBound

Fullspace 7.018 10.420 48.48% 333,249 70,465 7,360 OUTMEMORY

SolvedinGAMS24.3.3withCPLEX12.6.0.1onamachinewithanIntelCorei7CPU@2.93GHzand12GBRAM

ComparisonofInstanceSizes

0

100

200

300

400

Fullspace Reduced

Num

. Con

stra

ints

(x

103 )

0

10

20

30

40

50

Reduced LD + SSD

Solu

tion

Tim

e (x

103

s)

>99%reduction62%reduction

ComparisonofSolutionMethods

Example: Oilfield Development Planning

ReducedModel 6.968 10.495 50.61% 124,980 70,465 7,000 40,562

SSD 7.166 ‐0.20%

‐ ‐ ‐ 41

LD ‐ 7.180 ‐ ‐ ‐ 14

42

Quality of input data?Data-Driven Modeling of Uncertainty

• Application: Two-Stage Stochastic Programming (TSSP) problem:

• Some shortcomings of the above formulation in practice: The true distribution of may not be known Need to discretize (unknown) distribution

Birge & Louveaux (2011)

How to generate scenarios given historical and forecast data?– Compute outcomes and their probabilities

Calfa, Agarwal, Grossmann, Wassick (2015)

43

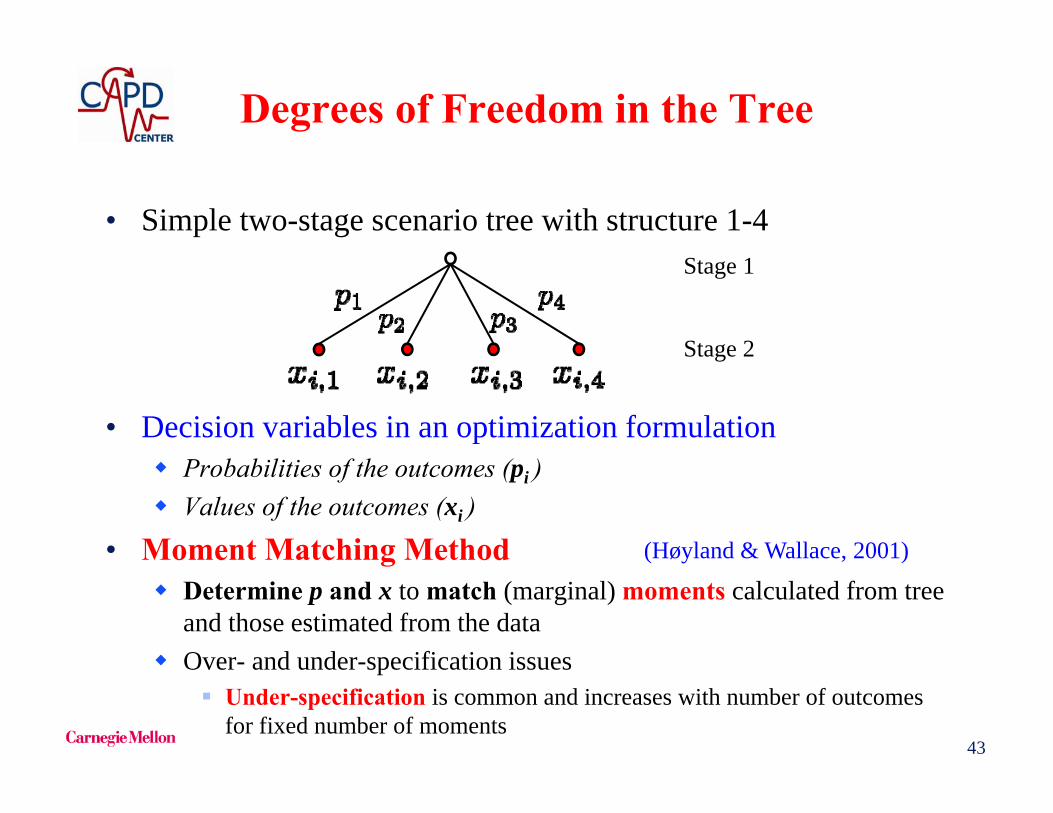

Degrees of Freedom in the Tree

• Simple two-stage scenario tree with structure 1-4

• Decision variables in an optimization formulation Probabilities of the outcomes (pi ) Values of the outcomes (xi )

• Moment Matching Method Determine p and x to match (marginal) moments calculated from tree

and those estimated from the data Over- and under-specification issues

Under-specification is common and increases with number of outcomes for fixed number of moments

Stage 1

Stage 2

(Høyland & Wallace, 2001)

44

Mitigating Under-Specification

• Each outcome has two sets of variables: and• Each moment specification has one piece of information• Consequences:

Multiple combinations of x and p satisfy moments Probabilities may not capture the shape of the underlying distribution

• Additional information: marginal (Empirical) Cumulative Distribution

Cumulative Probability

Nonlinear, nonconvex optimization problem. L1 formulation can be reformulated as an LP for fixed node values (Ji et al., 2005) 45

Min weighted error between tree and data

Probabilitiesadd up to 1

Moments calculatedfrom the tree

Covariances calculatedfrom the tree

Bounds on variables

L2 Moment Matching Problem (L2 MMP)

Nonlinear, nonconvex optimization problem. L1 formulation can be reformulated as an LP for fixed node values (Ji et al., 2005) 46

Min weighted error between tree and data

Probabilitiesadd up to 1

Moments calculatedfrom the tree

Covariances calculatedfrom the tree

Bounds on variables

ECDF information

L2 Distribution Matching Problem (L2 DMP)

47

Scenario Tree Generation and ForecastingMultistage Problems

• Final result

NLP Approach: calculate both probabilities and outcome values. LP Approach: fix outcome values, calculate probabilities.

Past Present Future

48

Motivating Example: Process Network

• Network of chemical plants

• 1 raw material (A), 1 intermediate product (B), two finished products (C and D)

• Only D can be stored and C can be purchased from elsewhere

Case 1: uncertain yield

Case 2: uncertain demands

49

Case 1: Uncertain Yield Process 1

• Historical data for production yield of facility P1

• Skewed to the right• Tail effects (extreme values) are not negligible• Approaches: Original MMP and L2 DMP (2 moments + ECDF)• TSSP, where first stage is t = 1 and second stage is t = 2, …, 4

50

Two-Stage Scenario Trees• Heuristic Approach

0.3 0.4 0.5 0.6 0.7

0.1

0.2 0.4 0.2

0.1

• L2 DMP Approach

0.14 0.66 0.76 0.83 0.90

0.02

0.21 0.28 0.270.23

Approach Expected Profit [$]Heuristic 62.77L2 DMP 72.45

51

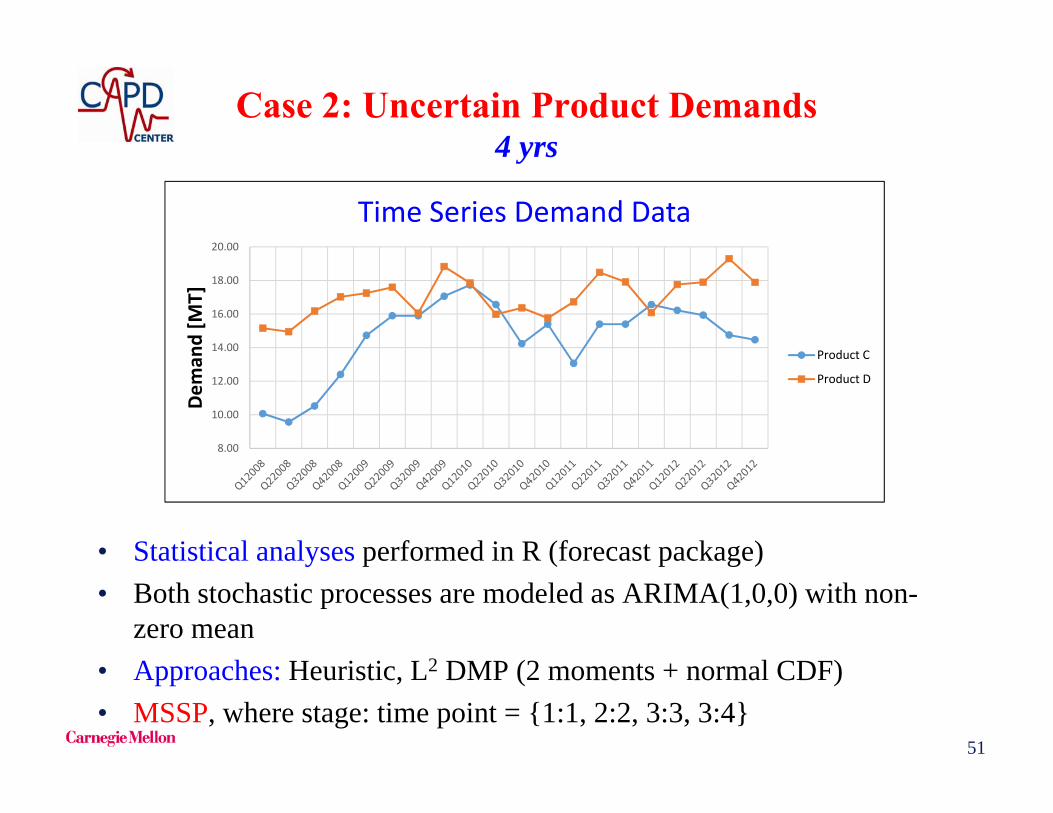

Case 2: Uncertain Product Demands4 yrs

• Statistical analyses performed in R (forecast package)• Both stochastic processes are modeled as ARIMA(1,0,0) with non-

zero mean• Approaches: Heuristic, L2 DMP (2 moments + normal CDF)• MSSP, where stage: time point = {1:1, 2:2, 3:3, 3:4}

8.00

10.00

12.00

14.00

16.00

18.00

20.00

Dem

and [M

T]Time Series Demand Data

Product C

Product D

52

• Heuristic Approach

Multi-Stage Scenario Trees

• L2 DMP Approach

NLPs: 12.3 sec (IPOPT)Heuristic L2 DMP

79.95 82.39

Expected profits [$]

53

Conclusions1. Can avoid overly conservative results in robust optimization with

linear decision rules (recourse) Cryogenic energy storage

2. To effectively solve two- or multi-stage stochastic optimization problemswith decomposition: tighten relaxation, reduce scenarios, multicut Benders

Supply chain under disruptions

3. Handling both exogenous and endogenous uncertainties in multi-stagestochastic programming yields challenging models: reduction non-anticipativityconstraints, specialized algorithms and Lagrangean decomposition

Oilfield planning

4. Historical data should be used for the generation of scenarios using moment and cumulative matching process network

Open questions/challenges:- How to extend to MINLP models with uncertainty?

- How to help users interpret solutions from these models?

54

Acknowledgments

NSF Grant CBET-1159443

Fulbright Program