July 2018

PT Medikaloka Hermina Tbk1H 2018 Presentation

Hermina – Our Team

Aristo Setiawidjaja15

Years of Experience

MD, Finance and

Strategic

Development

dr. Binsar Parasian

Simorangkir

32

Years of Experience

Co-Founder and MD,

Medical and

Compliance

Yulisar Khiat34

Years of Experience

Co-Founder and MD,

Operational and

General Affairs

dr. Hasmoro34

Years of Experience

President

Director & CEO

#1 Indonesia Original

Brand in Maternity

Hospital (2016)

- SWA

Hospital Group with

the Most Accredited

Hospitals (2015)

- KARS

1

1. Company Overview

Leading National Hospital Chain, with Robust Growth Trajectory

One of the Largest Groups in a Highly Fragmented Indonesian Hospital Market1

Source: Frost & Sullivan.1. As of December 31, 2017.2. Includes Kasih Group (521 beds, 7 hospitals), which Mitra Keluarga acquired in October, 2017.

31 28

19

10 9

3,337 2,780 2,700

889

1,500

# of Hospitals# of Operational Beds

Consistent Growth Year over Year

2

1 4

12

4

14

28

2010 2011 2012 2013 2014 2015 2016 2017 Dec 2017FY2015 FY2016 FY2017

2x Growth - 14 New Hospitals in 7 Years

2

Permata Bunda

Other Selected Top Players, Beyond the Top 5

Name No. of Hospitals No. of BedsType of

Hospital

Permata Group 7 699 Multi-Specialty

Sari Asih 6 858 Multi-Specialty

Ramsey 3 629 Multi-Specialty

Pondok 3 455 Multi-Specialty

Columbia Asia 3 416 Multi-Specialty

Mayapada 2 485 Multi-Specialty

Top 5 Private Operators by Number of Hospitals

3

Total Patient

395K

523K

627K

2.8M

3.6M

4.5M

FY15-FY17 CAGR

Inpatient Days: 26% / Outpatient: 27%

1. As of May 31, 2018.2. Based on Frost & Sullivan’s analysis that within the top private multi-specialty hospital chains, Hermina has the broadest offerings in women & children segment.

Hermina hospitals are a network of general hospitals with a significant strength and wide offering in women and children care

Service Offering Overview

Type B6 hospitals

Type C23 hospitals

Hermina Hospital Facility• 6 Type B general hospitals with fully

advanced center of excellence & sub-specialist care

• 23 Type C full service general hospitals with several sub-specialist care

Pharmacy

Accident &

Emergency

Radiology

Outpatient Clinics

& Homecare

Laboratory

Inpatient

rooms

General X-ray & Ultrasound, Mammography, BMD, MRI, CT Scan, C-Arm, ENT Endoscopy, Pathology-Clinic

Diagnostics / Imaging

Haemodialysis, CAPD,

Gastrointestinal Endoscopy,

Geriatrics Clinic, Oncology -

Chemotherapy

Internal Medicine

Orthopaedics and Traumatology,

Oncology – Chemotherapy,

Neuro surgery, Plastic surgery,

Vascular surgery, Digestive

(Laparoscopy) and Urology

(ESWL & TURP),

Phacoemulsification

Surgical Procedures

A variety of health screening and

treatment such as Cath Lab

Cardiovascular

Service Offerings

Children's health

including tertiary care

such as

Gastroenterology and

Thalassemia

Pediatrics

Specializes in women’s health

including Oncology and

Urogynaecology

Obstetrics & Gynaecology

29hospitals1

Service of ExcellenceGrowth and Development Center which includes Children Bobathto treat Cerebral Palsy and care for Neuromuscular diseases, and Adult Bobath to treat Stroke and Brain Injury

Medical Rehabilitation

Service of Excellence Orthodontics, Conservative Dentistry, Pediatric Dentistry, Prosthodontics, Periodontics and Oral Surgery

Dental Specialists

Ophthalmology Acupuncture PulmonologyNeurology Psychiatry Dermatology & VenereologyPathology-Anatomic Psychology Otorhinolaryngology Anaesthesiology Radiology (ENT)

Other Specialties

Service of Excellence• Perinatology• Neonatal Intensive Care Units (NICU)• Pediatric Intensive Care Units (PICU)

Service of Excellence• Feto-maternal care• Infertility

in Women and Children Care2

Market Leader in Number of Sub-specialty

Service Offerings2

4

Corporate History

# of beds

# of

hospitals29

18 Cities,

10 Provinces

Now

20141997

2002 2008

2016

3

150

6

441

11

786

21

1,611

24

2,115

3,2191

1985

25

1985 1989 1995 1999 2000–02 2003–08 2009–14 2015–16 2017

◼ Established 3 new hospitals and

acquired 2 hospitals

◼ 2005: Pandanaran became the

first Hermina Hospital to receive

general hospital license

◼ 2017: Established 4 new hospitals

◼ Company restructured ownership to

consolidate 28 hospitals under MH

◼ Made the first

acquisition of a

hospital (Podomoro)

◼ Established the first

maternity hospital in

Jatinegara

1997

◼ Changed the non-profit

organization status into a

corporation named

Medikaloka Hermina (MH)

◼ Established 7 new hospitals

and acquired 3 hospitals

◼ 2011: Opened first hospital

outside Java in Palembang

◼ Established

hospitals in Depok,

Daan Mogot, and

Bogor

◼ Jatinegara was

upgraded to

Women & Children

hospital

◼ Established the

third hospital in

Bekasi

◼ Established 2 new hospitals

and acquired 1 hospital

◼ 2016: Hermina Tower was

opened

Company Milestones

Evolution on Number of Hospitals

5

◼ Opened 1 new hospital in

Samarinda in April 2018

2018

2017

28

2,780

Our Nationwide Hospital Network

Type B Hospitals Type C Hospitals

Total Hospitals

29 Hospitals

across 18 Cities in

• Pasteur

• Pandanaran

• Malang

• Sukabumi

• Tangerang

• Grand Wisata

• Arcamanik

• Galaxy

• Palembang

• Ciputat

• Cileungsi

• Serpong

• Banyumanik

• Solo

• Ciruas

• Yogya

• Bitung

• Makassar

• Balikpapan

• Medan

• Podomoro

• Purwokerto

• Samarinda

Jatinegara

Depok

Kemayoran

Daan Mogot

Bekasi

Bogor

Our Nationwide Hospital Network

6

2. Financial Update

267.3 314.7

20.9% 20.8%

0.0%

10.0%

20.0%

30.0%

80.0

280.0

480.0

680.0

1H17 1H18

EBITDA EBITDA Margin

569.9 664.2

44.5% 43.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

200.0

700.0

1,200.0

1H17 1H18

Gross Profit Gross Margin

1,281.8 1,515.4

1H17 1H18

Robust Growth in Revenue and Stable Margin Profile

Growth: 18.2%

Total Revenue(IDR billions)

EBITDA & EBITDA Margin1

(IDR billions, %)

1. EBITDA is calculated by operating income + depreciation and amortization + adjustment for non-operating items (disposal of fixed asset, impairment of fixed asset, and other income (expense)) and adjustment for non-cash items (allowance for impairment of account receivable and post-employment benefit expense) + professional expenses related to IPO (IDR1.5bn), which is recognized as part of general adminitrative expense.

Gross Profit & Gross Margin(IDR billions, %)

8

PAT & PATMI(IDR billions)

124.7

99.3

70.6 70.0

0.0

50.0

100.0

150.0

1H17 1H18

PAT PATMI

As opposed to PAT in 1H17, PAT in 1H18

was impacted by interest expense related

to purchase of minority interest in 2H17

Key Balance Sheet Items – Working Capital Turnover Days

Trade Receivable Days1

(Days)

Net Working Capital(IDR billions)

Trade Payable Days(Days)

Cash Conversion Cycle Days(Days)

Inventory Days(Days)

91. Trade receivable days in 2016 and 2017 are calculated based on average balance of trade receivables.

11.813.0

11.0 9.7

2015 2016 2017 1H18

76.6

205.4

361.4 355.0

2015 2016 2017 1H18

3.2

11.1

21.7 27.5

2015 2016 2017 1H18

33.7 36.8

53.6 63.1

2015 2016 2017 1H18

42.3 38.8 42.9 45.3

2015 2016 2017 1H18

281K363K

1H17 1H18

Strong Growth in Patient Visits

Inpatient Days Inpatient Admissions by Payor Type

Outpatient VisitOutpatient Visits by Payor Type

1H17 1H18

1H17 1H18

10

Growth: 29.0%

2.1M

2.6M

1H17 1H18

Growth: 24.4%

JKN, 53%

Non-JKN, 47% JKN,

67%

Non-JKN, 33%

JKN, 41%Non-

JKN, 59%

JKN, 49%

Non-JKN, 51%

EBITDA Calculation Methodology

(IDR billions) 1H17 1H18 YoY Growth

Revenue 1,281.8 1,515.4 18.2%

EBIT 196.6 210.3 7.0%

% Margin 15.3% 13.9%

Depreciation and Amortization (D&A) 64.4 93.0

Adjustment for back non-cash items1 13.0 13.2

Post-employment benefits 11.4 12.2

Allowance for impairment losses 1.6 0.9

Adjustment for non-operational income / (expense) (6.7) (1.8)

Net Loss Disposal of fixed asset 0.6 1.4

Other income (expense) 2 (7.3) (5.1)

IPO related expenses - 1.9

EBITDA (EBIT + D&A + Adjustments) 267.3 314.7 17.7%

% Margin 20.9% 20.8%

111. Methodology is consistent with the EBITDA calculation methodology of the peer group of Siloam and Mitra Keluarga2. Other income and expenses include items that are non-operational in nature such as sponsorship income, seminar income, patient overpayment, CSR and charitable donation expenses, and other miscellaneous income and expenses.

Debt and Leverage Ratio

Total Debt / Net Debt / Leverage Ratio(IDR billions, x)

Note: Debt is calculated by short-term bank loans + current portion of long-term liabilities + medium term notes + long-term liabilities net of current portion: bank loans + mandatory convertible notes. 12

<1 yr maturity

15%

1-5 yr maturity

85%

Maturity Profile (June 2018)

354.1

607.7

1,422.0

865.2

235.3

404.5

1,099.6

343.3

0.70.8

1.9

0.5

-1

-0.5

0

0.5

1

1.5

2

0

500

1000

1500

2000

2500

2015 2016 2017 1H18

Total Debt Net Debt Net Debt/EBITDA

IDR

865.2 bn

Cash Flow and Capital Expenditure

Cash Flow(IDR billions)

1. Includes acquisition of fixed assets + acquisition of other assets + advance purchase of fixed assets 13

Cash and Cash Equivalents(IDR billions)

Capital Expenditure1

(IDR billions, %)

118.8

203.2

322.4

521.9

2015 2016 2017 1H18

331.4 393.6 439.7 207.7

176.5 170.2

1,142.4

446.3

(526.7) (485.7)

(1,462.8)

(454.5)

2015 2016 2017 1H18

Cash Flow from Operations Cash Flow from Financing Activities

Cash Flow from Investing Activities

528.9 534.4

716.1

450.3

30.9%

23.9%26.7%

29.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

150

350

550

750

950

1150

1350

2015 2016 2017 1H18

Capital Expenditure % of Revenue

3. Hospital Development

15

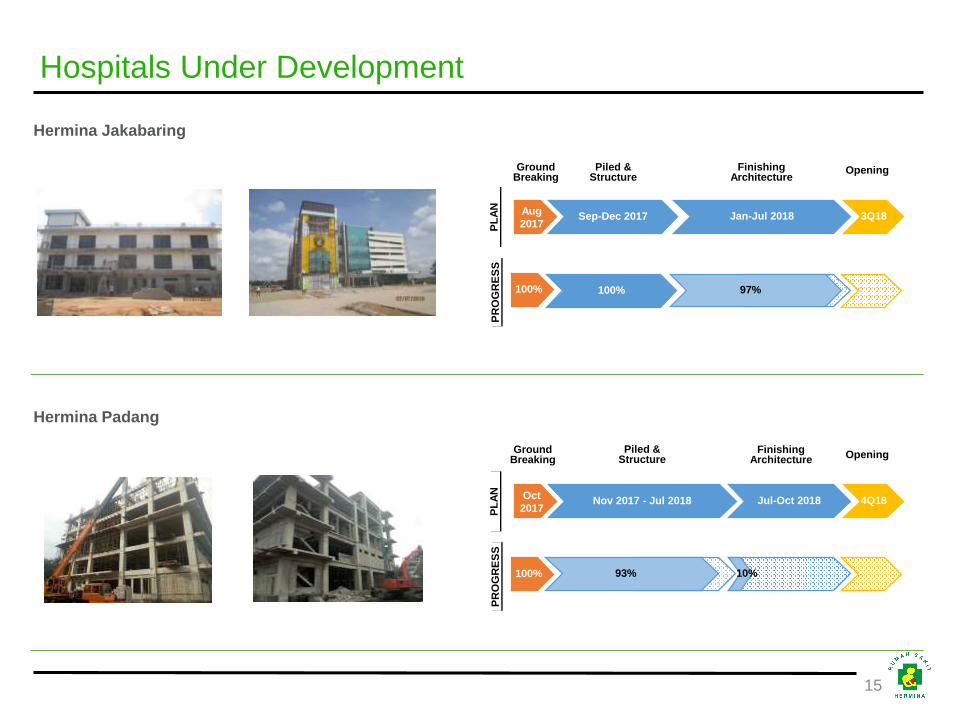

Hospitals Under Development

Hermina Jakabaring

Hermina Padang

Aug

2017Jan-Jul 2018Sep-Dec 2017 3Q18

OpeningGroundBreaking

Piled & Structure

Finishing Architecture

PL

AN

100% 97%

PR

OG

RE

SS

100%

Oct

2017Jul-Oct 2018Nov 2017 - Jul 2018 4Q18

OpeningGround

BreakingPiled &

StructureFinishing

Architecture

PL

AN

100% 93%

PR

OG

RE

SS

10%

PT Medikaloka Hermina Tbkwww.herminahospitals.com