Product Classification and DPFsSession 6

Insurance IFRS Seminar

December 1, 2016

Michael Lockerman

Session 6

2

Agenda

• IFRS 4 Scope

• Current IFRS 4 Product Classification

– Insurance Contracts

– Discretionary Participating Features

• Phase 2 proposals

3

IFRS 4 SCOPE

4

IFRS 4 Scope

• Insurance contracts, including reinsurance contracts, issued by an

entity

• Reinsurance contracts held by an entity

• Investment contracts with discretionary participating features (DPF’s)

Therefore the first step in applying IFRS 4 is to determine the

appropriate product classification

5

Current IFRS 4 Product Classification

6

Product Classification

Does the contract need to

be unbundled?Are any discretionary

participation features present?

Insurance Component Deposit Component

Yes YesNo

Does contract contain

significant insurance

risk?

Investment Contract

(IAS 39)Investment Contract with

discretionary participation

features

Insurance Contract

No

NoYes

Existing

accounting

Amortized Cost or FVExisting accounting with

Liability or equity choice

Does the contract need to

be unbundled?Are any discretionary

participation features present?

Insurance Component Deposit ComponentInsurance Component Deposit Component

Yes YesNo

Does contract contain

significant insurance

risk?

Investment Contract

(IAS 39)Investment Contract with

discretionary participation

features

Insurance Contract

No

NoYes

Existing

accounting

Amortized Cost or FVExisting accounting with

Liability or equity choice

7

IFRS 4 - Insurance Contracts

•Definition of an Insurance Contract• (IFRS 4, Appendix B)

8

IFRS 4 - Insurance ContractDefinition

– A single definition of insurance contracts

“a contract under which one party (the insurer) accepts significant insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event (the insured event) adversely affects the policyholder.”

– “A reinsurance contract is a type of insurance contract.”

9

Insurance Risk

– Distinction between insurance risk and other risks

• Financial risk: Change in interest rate, security price, commodity

price, etc.: NOT insurance risk

• Lapse, persistency or expense risk: NOT insurance risk in direct

contract

• Contracts including both financial risk and significant insurance

risk have insurance risk

• Must relate to uncertain future event that adversely affects the

policyholder

• Must be a pre-existing risk vs. risk created by the contract (

10

Insurance Risk

• Insurance risk evaluated at inception of contract

• A contract that initially does not meet the definition of

insurance may subsequently do so.

• Example: Annuity options

• Once insurance always insurance until all rights and

obligations extinguished

11

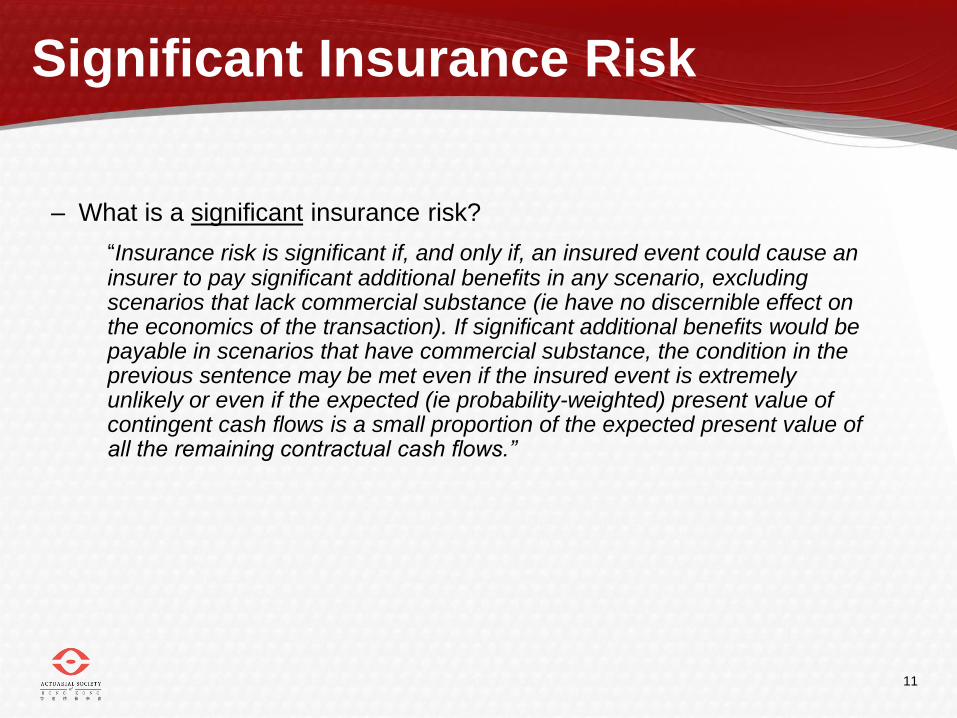

Significant Insurance Risk

– What is a significant insurance risk?

“Insurance risk is significant if, and only if, an insured event could cause an insurer to pay significant additional benefits in any scenario, excluding scenarios that lack commercial substance (ie have no discernible effect on the economics of the transaction). If significant additional benefits would be payable in scenarios that have commercial substance, the condition in the previous sentence may be met even if the insured event is extremely unlikely or even if the expected (ie probability-weighted) present value of contingent cash flows is a small proportion of the expected present value of all the remaining contractual cash flows.”

12

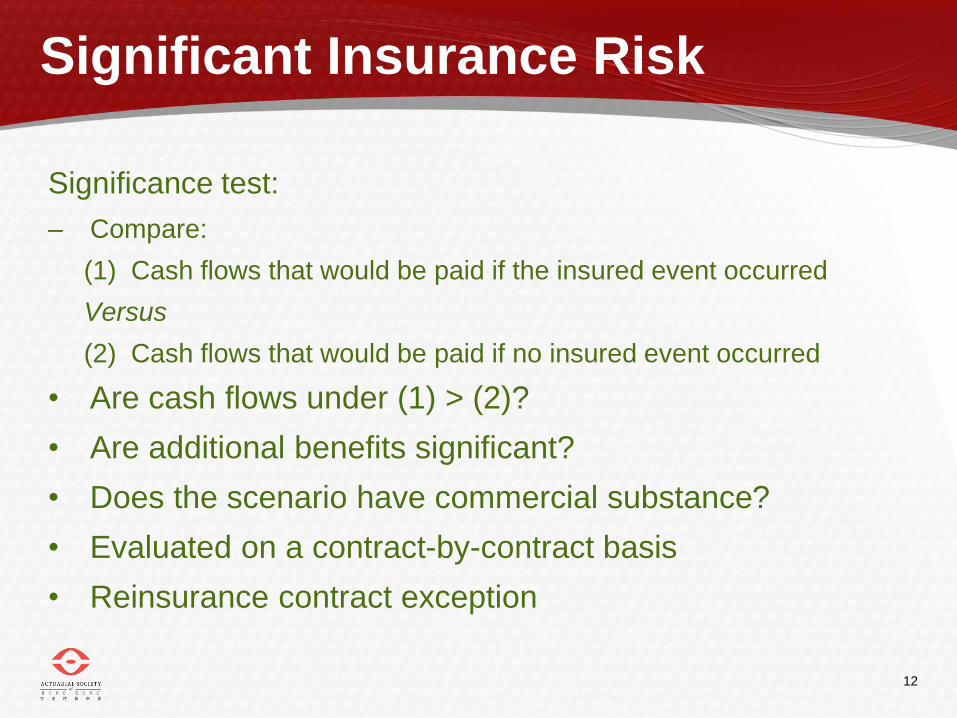

Significant Insurance Risk

Significance test:

– Compare:

(1) Cash flows that would be paid if the insured event occurred

Versus

(2) Cash flows that would be paid if no insured event occurred

• Are cash flows under (1) > (2)?

• Are additional benefits significant?

• Does the scenario have commercial substance?

• Evaluated on a contract-by-contract basis

• Reinsurance contract exception

13

Determining Insurance Risk

Simplified Example of 7 year endowment product. Death benefit equals the endowment benefit.

Scenario 1

• Policyholder dies in first

policy month and received

134k

Scenario 2

• Policyholder survives to

endowment and receives

134k, PV = 90k

14

IFRS 4 - Insurance ContractsInsurance Risk

• Lapse risk

• Not a pre-existing risk for the insurer

• Becomes an insurance risk if transferred to a reinsurer

– Financial guarantees

• Either under IFRS 4 or under IAS 39

– Mortgage guarantees

• Either under IFRS 4 or under IAS 39

15

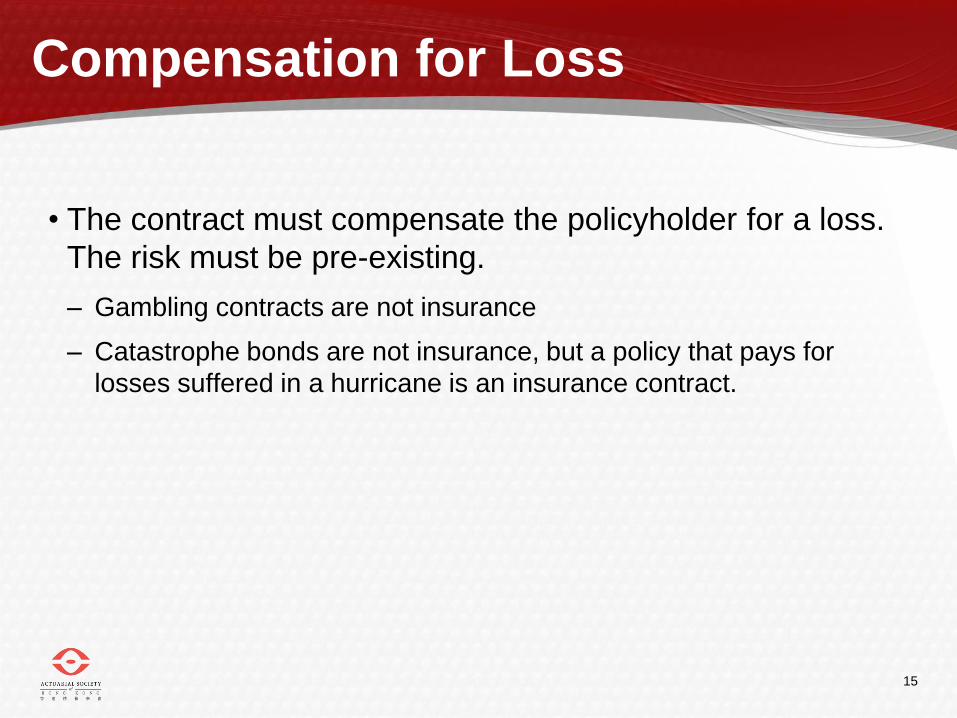

Compensation for Loss

• The contract must compensate the policyholder for a loss.

The risk must be pre-existing.

– Gambling contracts are not insurance

– Catastrophe bonds are not insurance, but a policy that pays for

losses suffered in a hurricane is an insurance contract.

16

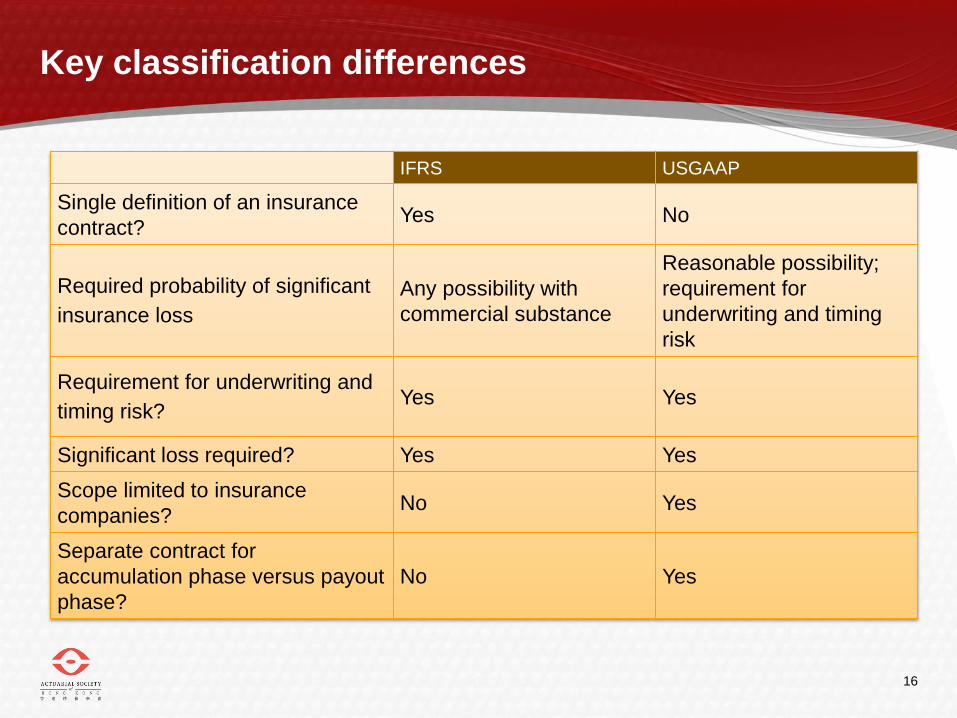

Key classification differences

IFRS USGAAP

Single definition of an insurance

contract?Yes No

Required probability of significant

insurance loss

Any possibility with

commercial substance

Reasonable possibility;

requirement for

underwriting and timing

risk

Requirement for underwriting and

timing risk?Yes Yes

Significant loss required? Yes Yes

Scope limited to insurance

companies?No Yes

Separate contract for

accumulation phase versus payout

phase?

No Yes

17

IFRS 4 Product Classification

Does the contract need to

be unbundled?Are any discretionary

participation features present?

Insurance Component Deposit Component

Yes YesNo

Does contract contain

significant insurance

risk?

Investment Contract

(IAS 39)Investment Contract with

discretionary participation

features

Insurance Contract

No

NoYes

Existing

accounting

Amortized Cost or FVExisting accounting with

Liability or equity choice

Does the contract need to

be unbundled?Are any discretionary

participation features present?

Insurance Component Deposit ComponentInsurance Component Deposit Component

Yes YesNo

Does contract contain

significant insurance

risk?

Investment Contract

(IAS 39)Investment Contract with

discretionary participation

features

Insurance Contract

No

NoYes

Existing

accounting

Amortized Cost or FVExisting accounting with

Liability or equity choice

18

Discretionary Participation Features

• A contractual right to receive, as a supplement to guaranteed benefits, additional benefits:

• that are likely to be a significant portion of the total contractual benefits;

• whose amount or timing is contractually at the discretion of the issuer; and

• that are contractually based on:

the performance of a specified pool of contracts or a specified type of contract;

realised and/or unrealised investment returns on a specified pool of assets held by the issuer; or

the profit or loss of the company, fund or other entity that issues the contract.

19

Discretionary Participation Features

• May, but need not, report the fixed element separately from the

discretionary participation feature

• Should classify unallocated surplus arising from discretionary

participation features as either a liability or equity (not as an

intermediate category that is neither liability nor equity).

• Consider possible separation of embedded derivatives (apply IAS 39

to in-scope embedded derivatives with specific exemption for DPF

surrender options).

• Should, in all respects not described above, continue its existing

accounting policies for such contracts, unless it demonstrates that a

change in those accounting policies would result in more

understandable, relevant, reliable and comparable financial

statements.

20

Phase II Proposals

21

Insurance Contracts

• Retain IFRS 4 definition

‘A contract under which one party (the issuer) accepts significant insurance risk from

another party (the policyholder) by agreeing to compensate the policyholder if a

specified uncertain future event (the insured event) adversely affects the policyholder’

• Significance measured using present values

• Underwriting or timing risk but additional guidance that timing delays may reduce

uncertainty

• Requires a scenario in which present value of cash outflows exceeds present value of

premiums. Evaluated on a contract by contract basis. Thus insurance risk can be

significant even if the chance of losses on the portfolio is remote

• Reinsurance exception: If a reinsurance contract transfer substantially all of the

insurance risk of the reinsured portions of the underlying contracts, then it is an

insurance contract

• Financial guarantee contracts generally excluded from the scope (included in 2010

version)

22

Discretionary Participating Features

• Definition of DPF is the same as in current IFRS 4

• Investment contracts with DPF are included in the scope if the entity also issues insurance contracts.

• Guidance is basically the same for investment contracts with DPF as for insurance contracts.

• Modification of some guidance to reflect that there is no insurance risk contract boundary, coverage period)

Thank You