Presented by:

David B. Iben, CFA

CIO & Lead Portfolio Manager

• Leadership and ownership by investment professionals

• 100% employee owned

• Equity participation for all professionals

• Principals invest alongside clients

• Capacity to be limited, enhancing return potential

2

• Kopernik Global All-Cap

• Kopernik Global Unconstrained

• Kopernik Global Real Asset

• Kopernik International

Managed Assets

Mutual Funds $1,222.27 MM

Private Funds $208.77 MM

UCITS (Sub-advised) $410.77 MM

Separate Accounts $1,070.58 MM

Total Firm AUM $2,912.39 MM

Advisory Only Assets

Separate Accounts $277.57 MM

Total Managed and Advisory Only Assets: $3,189.96 MM

Assets as of September 30, 2017 are preliminary.

Mutual Funds42%

Private Funds

7%UCITS14%

Separate Accounts37%

3

a class of financial adviser that provide

automated, algorithm-driven financial advice or portfolio management

platforms with little to no human interference. The United States is the

clear global robo-advice leader by numbers, having more than 200

robo-advisors as of April 2017.Source: Business Insider, April 2017

still extinct.

4

5

6

-Sir John Templeton

7

8

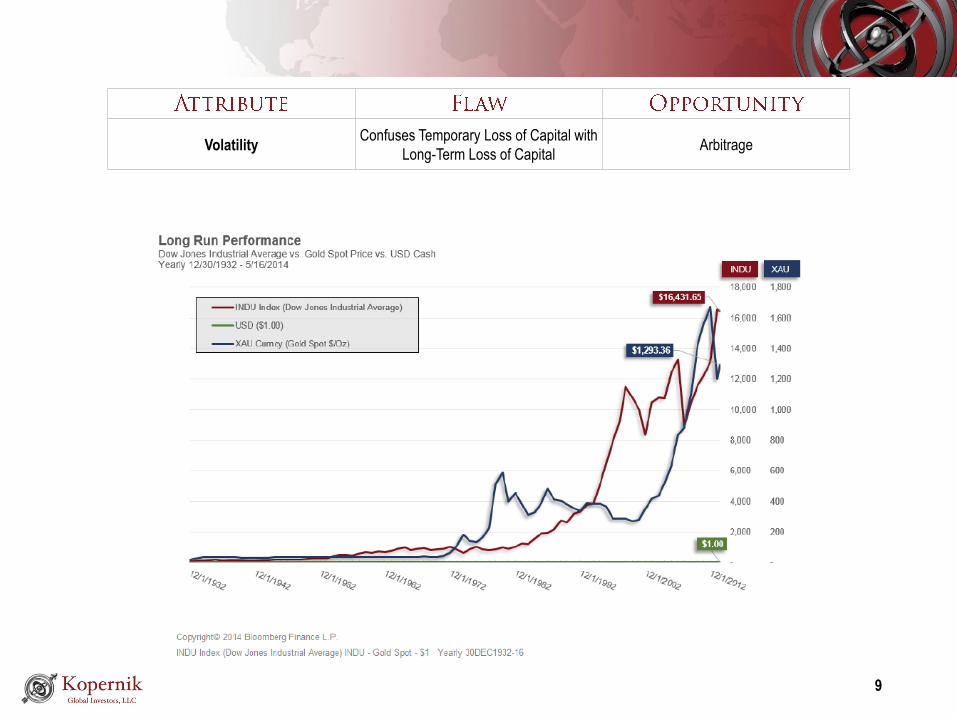

Risk

Volatility

Attempting to Quantify the Unquantifiable (Risk)

Use Common Sense, Not Meaningless Statistics

(Tracking Error, Volatility, Beta)Tracking Error

Uncomfortable IdiosyncrasyFocus is Often on Risk to Manager/Advisor Career Rather Than Risk of

Permanent Loss of Capital in Client’s Portfolio Needs of Client Portfolio are Paramount

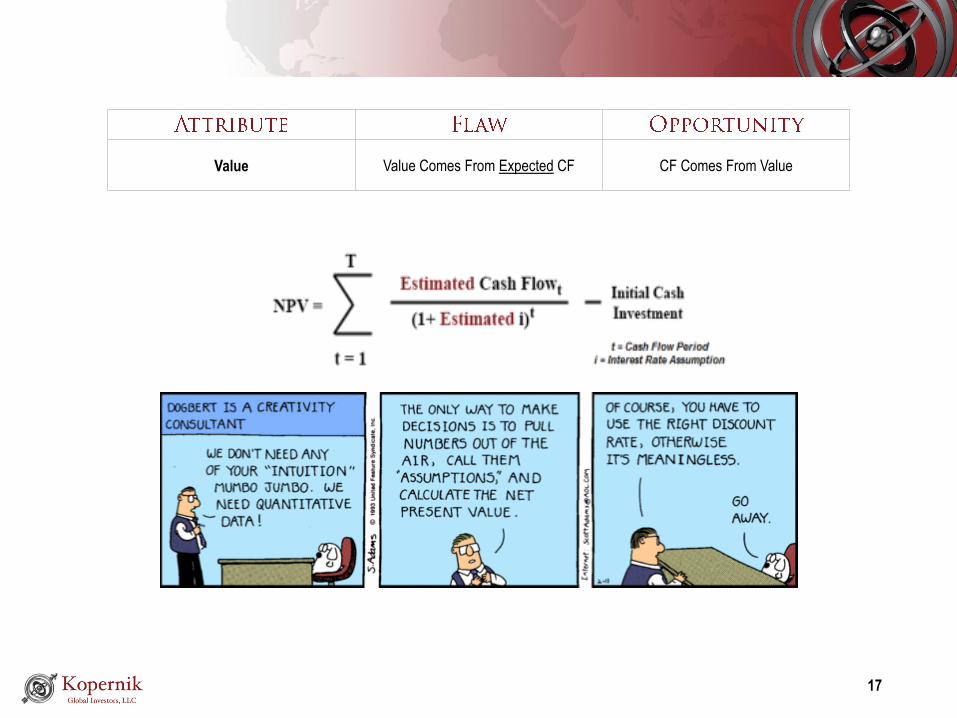

Value

Good and Services Intrinsic Value PV E (FCF) Intrinsic Value FCF

Time Central Bank Intervention Solve for IRR Rather Than NVP

Money Value is Established by Fiat Demand Large Rates of Interest for Fiat Currency

Over-Confidence

Short-termism“In a Complex, Adaptive System, Forecasting Is Impossible”

–Walter White Maintain Long-Term Time Horizon

ForecastingHumans are Notoriously Bad at Forecasting

The Best Investments Often Require Patience Have Patience and Conviction

Passive “Investing” Abrogation of Duty to Perform Price Discovery Due Diligence Know Your Circle of Confidence

9

VolatilityConfuses Temporary Loss of Capital with

Long-Term Loss of CapitalArbitrage

10

Tracking Error See Passive Investing Arbitrage

-Soul Asylum

11

1929 Stock Market Crash 1972 Stock Market Crash

2007 Stock Market Crash 1999 Stock Market Crash

0

50

100

150

200

250

300

350

400

Sep

-20

Sep

-21

Sep

-22

Sep

-23

Sep

-24

Sep

-25

Sep

-26

Sep

-27

Sep

-28

Sep

-29

Sep

-30

Sep

-31

Sep

-32

Sep

-33

Sep

-34

Dow Jones Industrial Average: 1920-1934

0

200

400

600

800

1000

1200

Mar

-72

May

-72

Jul-

72

Sep

-72

No

v-7

2

Jan

-73

Mar

-73

May

-73

Jul-

73

Sep

-73

No

v-7

3

Jan

-74

Mar

-74

May

-74

Jul-

74

Sep

-74

No

v-7

4

S&P 500 Index: 1972-1974

0

1000

2000

3000

4000

5000

6000

6/1

8/1

99

9

8/1

8/1

99

9

10

/18

/19

99

12

/18

/19

99

2/1

8/2

00

0

4/1

8/2

00

0

6/1

8/2

00

0

8/1

8/2

00

0

10

/18

/20

00

12

/18

/20

00

2/1

8/2

00

1

4/1

8/2

00

1

6/1

8/2

00

1

8/1

8/2

00

1

NASDAQ Composite: 1999-2001

0

200400

600

8001000

1200

1400

16001800

S&P Index: 2007-2009

12

13

14

15

$-

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

$3,500.00

$4,000.00

$4,500.00

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Jun

-12

Sep

-12

Dec

-12

Mar

-13

Jun

-13

Sep

-13

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

Dec

-16

Mar

-17

Jun

-17

Sep

-17

Bitcoin Price (Dollars)

16

– John Templeton

17

Value Value Comes From Expected CF CF Comes From Value

18

19

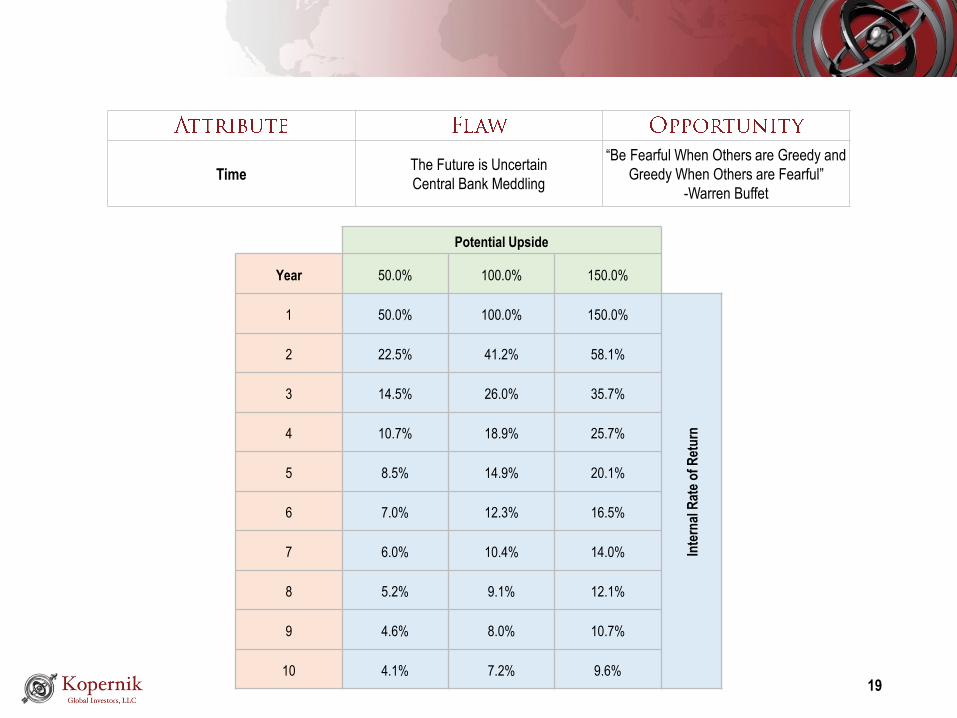

TimeThe Future is Uncertain

Central Bank Meddling

“Be Fearful When Others are Greedy and

Greedy When Others are Fearful”

-Warren Buffet

Potential Upside

Year 50.0% 100.0% 150.0%

1 50.0% 100.0% 150.0%

Inte

rnal

Rat

e o

f R

etu

rn

2 22.5% 41.2% 58.1%

3 14.5% 26.0% 35.7%

4 10.7% 18.9% 25.7%

5 8.5% 14.9% 20.1%

6 7.0% 12.3% 16.5%

7 6.0% 10.4% 14.0%

8 5.2% 9.1% 12.1%

9 4.6% 8.0% 10.7%

10 4.1% 7.2% 9.6%

20

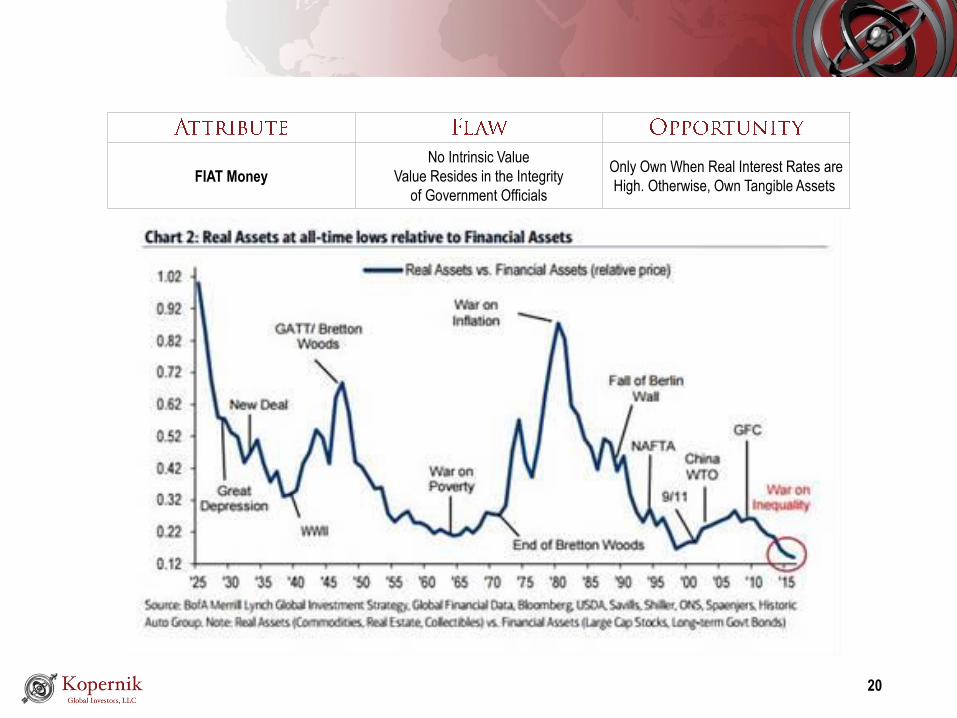

FIAT Money

No Intrinsic Value

Value Resides in the Integrity

of Government Officials

Only Own When Real Interest Rates are

High. Otherwise, Own Tangible Assets

21

22

FIAT Money

No Intrinsic Value

Value Resides in the Integrity

of Government Officials

Only Own When Real Interest Rates are

High. Otherwise, Own Tangible Assets

Source: World Gold Council, FRED: Federal Reserve Economic Data

23

FIAT Money

No Intrinsic Value

Value Resides in the Integrity

of Government Officials

Only Own When Real Interest Rates are

High. Otherwise, Own Tangible Assets

24

Over-Confidence; GrowthUnsustainable

Often Over PricedOnly Buy GARP or Value

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

1.90

MSCI World Value vs. MSCI World Growth 1974 - 2017

Source: Bloomberg

25

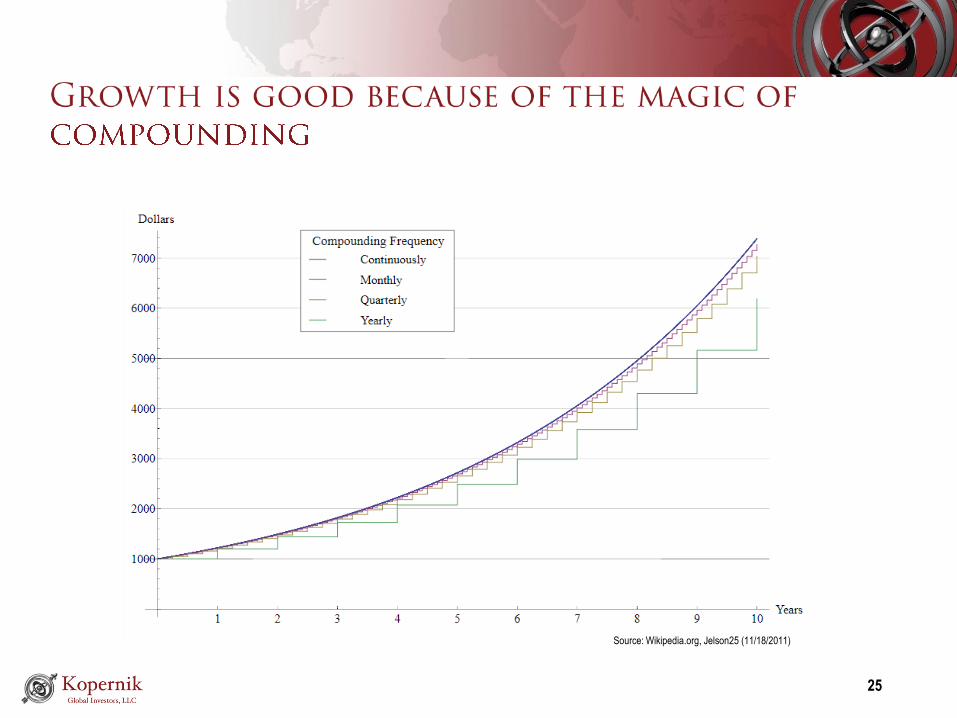

Source: Wikipedia.org, Jelson25 (11/18/2011)

26

Growth Expectations are dashed 95% of the time.

27

Over-Confidence Forecasting Exercise Patience and Conviction

Short-Termism Best Investments Require Patience Arbitrage

28

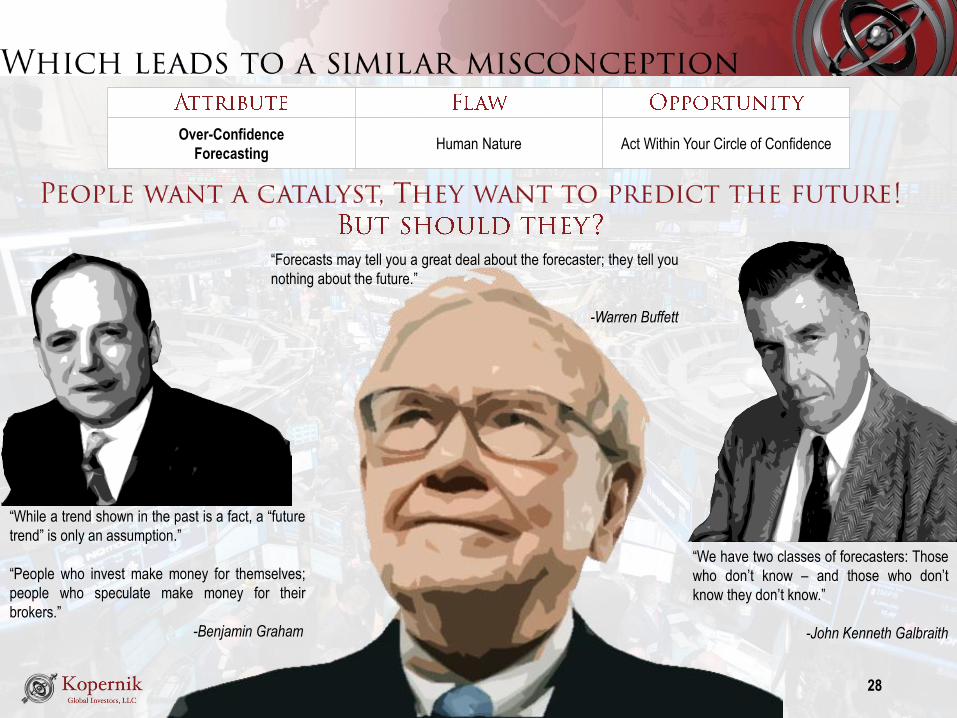

“Forecasts may tell you a great deal about the forecaster; they tell you

nothing about the future.”

-Warren Buffett

“While a trend shown in the past is a fact, a “future

trend” is only an assumption.”

“People who invest make money for themselves;

people who speculate make money for their

brokers.”

-Benjamin Graham

“We have two classes of forecasters: Those

who don’t know – and those who don’t

know they don’t know.”

-John Kenneth Galbraith

Over-Confidence

ForecastingHuman Nature Act Within Your Circle of Confidence

29

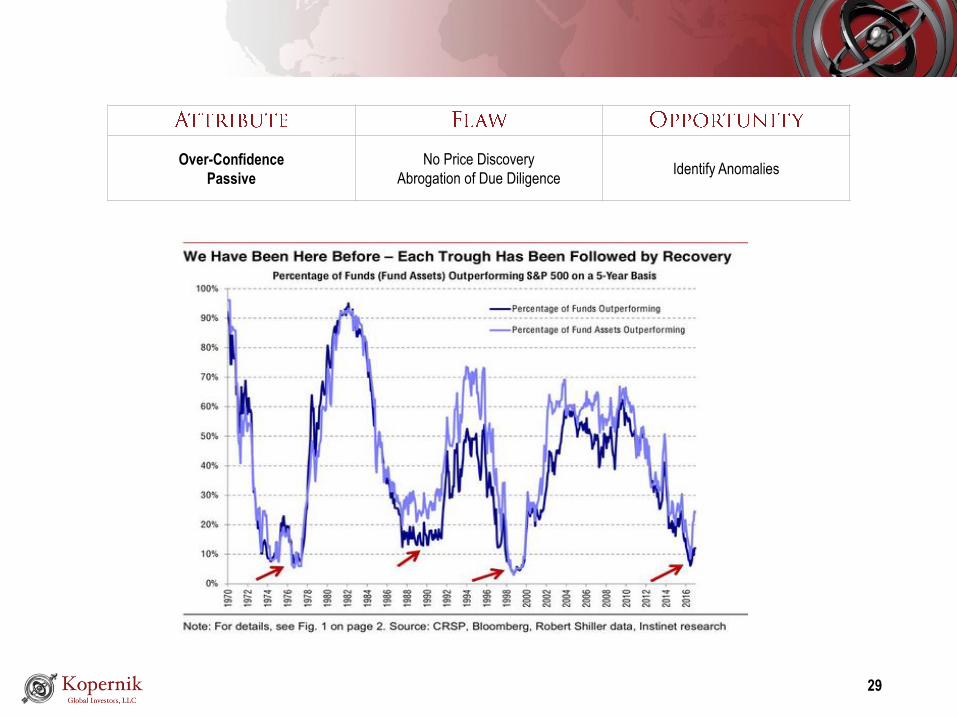

Over-Confidence

Passive

No Price Discovery

Abrogation of Due DiligenceIdentify Anomalies

30

Soren Kierkegaard, 1840

Danish philosopher, theologian, poet, social critic and religious author

-Seth A. Klarman

Chief Executive and Portfolio Manager of the Baupost Group

311929 Stock Market Crash Japan Stock Market Crash

$-

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

$400.00

Sep

-20

Sep

-21

Sep

-22

Sep

-23

Sep

-24

Sep

-25

Sep

-26

Sep

-27

Sep

-28

Sep

-29

Sep

-30

Sep

-31

Sep

-32

Sep

-33

Sep

-34

DOW Price

32

Refers to a portfolio management strategy where the manager makes specific investments with the goal of outperforming an

investment benchmark index. In passive management, investors expect a return that closely replicates the investment weighting

and returns of a benchmark index and will often invest in an index fund.

Benefits of Active Portfolio Management

Opportunity for Outperformance

Additional Risk Management

Ability to adjust portfolios to a changing environment

Opportunity for investors to find the “right match”

Extinction?

“Two men were examining the output of the new computer

in their department. After an hour or so of analyzing the

data, one of them remarked: "Do you realize it would take

400 men at least 250 years to make a mistake this big?”

-Nicholas Negroponte

Chairman Emeritus of Massachusetts Institute of Technology’s Media Lab

33

-Albert Einstein

34A copy of this presentation is available on www.kopernikglobal.com.

We view ourselves as owners of businesses:

• Market inefficiencies present numerous opportunities to identify quality businesses that we believe are mispriced

• Independent research of a company’s business, industry supply/demand, competitive positioning and management

uncovers opportunities

We predicate our intensive, original research on:

• A global perspective to enhance understanding of markets and companies

• A long-term investment horizon to allow for inherent value to be realized

• Value as a prerequisite, not a philosophy

• Bottom-up, fundamental analysis to gain a thorough understanding of a company’s business and valuation

• Industry-tailored valuation metrics to assess distinct industry characteristics and success drivers

36

• Far-reaching investment experience in global markets with a long record of success

• Searching for market anomalies with industry specialists who have diverse backgrounds and distinct perspectives

• Group vetting to challenge ideas and develop high conviction

37

Additionally, Kopernik’s analyst team is supported by the team of research associates: Seamus Sullivan, Hailey Ferrara, and Lillian Cousins.

The information presented herein is proprietary to Kopernik Global Investors, LLC. This material is approved for a presentation to authorized individuals only and, accordingly, this

material is not to be reproduced in whole or in part or used for any purpose except as authorized by Kopernik Global Investors, LLC.

Please consider all risks carefully before investing. The accounts managed according to the Global All-Cap investment strategy are subject to certain risks such as market,

investment style, interest rate, deflation, and illiquidity risk. Investments in small and mid-capitalization companies also involve greater risk and portfolio price volatility than

investments in larger capitalization stocks. Investing in non-U.S. markets, including emerging and frontier markets, involves certain additional risks, including potential currency

fluctuations and controls, restrictions on foreign investments, less governmental supervision and regulation, less liquidity, less disclosure, and the potential for market volatility,

expropriation, confiscatory taxation, and social, economic and political instability. Investments in energy and natural resources companies are especially affected by

developments in the commodities markets, the supply of and demand for specific resources, raw materials, products and services, the price of oil and gas, exploration and

production spending, government regulation, economic conditions, international political developments, energy conservation efforts and the success of exploration projects. There

can be no assurances that investment objectives will be achieved.

Kopernik Global Investors, LLC is an investment adviser registered under the Investment Advisers Act of 1940, as amended.

This document, as of October 19, 2017 is descriptive of how the Kopernik team manages the Global All-Cap strategy. There is no guarantee that any strategy’s investment

performance objectives will be achieved. This profile is not legally binding on Kopernik Global Investors, LLC or its affiliates.

© 2017 Kopernik Global Investors, LLC | Two Harbour Place | 302 Knights Run Avenue Suite 1225 | Tampa, Florida 33602 | 813.314.6100 | www.kopernikglobal.com

38