Potential Combination of Fiat IndustrialPotential Combination of Fiat Industrial and CNH

Analyst & Media CallAnalyst & Media CallMay 30th, 2012

20 Novembre, 2010

Safe harbor statementSafe harbor statementCertain information included in this document is forward

looking and is subject to important risks and uncertainties

that could cause actual results to differ materially. The

issues, agriculture, the environment, trade and commerce and

infrastructure development; actions of competitors in the

various industries in which the Group competes; production

Company's businesses include its capital goods business,

including trucks, commercial vehicles, agricultural equipment,

heavy and light construction equipment, powertrains for the

capital goods and marine business, related service parts and

difficulties, including capacity and supply constraints and

excess inventory levels; labour relations; interest rates and

currency exchange rates; political and civil unrest; and other

risks and uncertainties. Any forward-looking statements

financial services and its outlook is predominantly based on

its interpretation of what it considers to be the key economic

factors affecting these businesses. Forward-looking

statements involve a number of important factors that are

contained in this document are referred to the current date

and, therefore, any of the assumptions underlying this

document or any of the circumstances or data mentioned in

this document may change. Fiat Industrial S.p.A. expressly

subject to change, including: statements regarding the

potential benefits of, and intentions regarding, the proposed

transaction; the many interrelated factors that affect

consumer confidence and worldwide demand for capital

disclaims and does not assume any liability in connection with

any inaccuracies in any of these forward-looking statements

or in connection with any use by any third party of such

forward-looking statements. This document does not

goods and capital goods -related products; factors affecting

the agricultural business including commodities prices,

weather, floods, earthquakes or other natural disasters, and

governmental farm programs; general economic conditions in

represent investment advice or a recommendation for the

purchase or sale of financial products and/or of any kind of

financial services. Finally, this document does not represent

an investment solicitation in Italy, pursuant to Section 1, letter

May 30th, 2012Potential Combination of Fiat Industrial and CNH 2

each of the Group's markets; changes in governmental

policies regarding banking, monetary and fiscal policies,

legislation, particularly that relating capital goods-related

(t) of Legislative Decree no. 58 of February 24, 1998, or in

any other country or state.

A global leader in the capital goods sector

Global top 3 capital goods platformEEQUIPMENTQUIPMENT SSALESALES –– 20112011(1)(1)(€/BN)

A global leader in the capital goods sector

G oba top 3 cap ta goods p at o

Global top 2 in agricultural equipment

Global top 3 in commercial vehicles(2)

Global top tier in construction equipment

Leading powertrain technology with

substantial global scale in medium and heavy g y

diesel engines

Top player in commercial vehicles and heavy

machinery in Brazil

Well positioned for growth in China, Russia

and India

0 10 20 30 40 50

May 30th, 2012Potential Combination of Fiat Industrial and CNH 3

Source: Companies’ annual reports (converted to Euro if required)

(1) Fiat Industrial revenues adjusted to exclude Financial Services(2) Global units sold including China JVs

0 10 20 30 40 50

Broad presence and uniquely diversified business modelbusiness model

RoW,

GROUP REVENUES BY GEOGRAPHYFY 2011: €24.3BN

FY 2011 INDUSTRIAL OPERATIONSREVENUES BY BUSINESS

CNH AG IvecoCNH CE

€9.4bnEurope,

43%Latin

America, 17%

RoW, 15%

€2.8bn€10.2bn

North America,

25%

Europe, 26%

RoW, 12%

GROUP TRADING PROFIT BY GEOGRAPHYFY 2011: €1.7BN

26%Latin

America, 17%

FPT INDUSTRIAL

€3.2bn

May 30th, 2012Potential Combination of Fiat Industrial and CNH 4

North America,

45%

FPT INDUSTRIAL

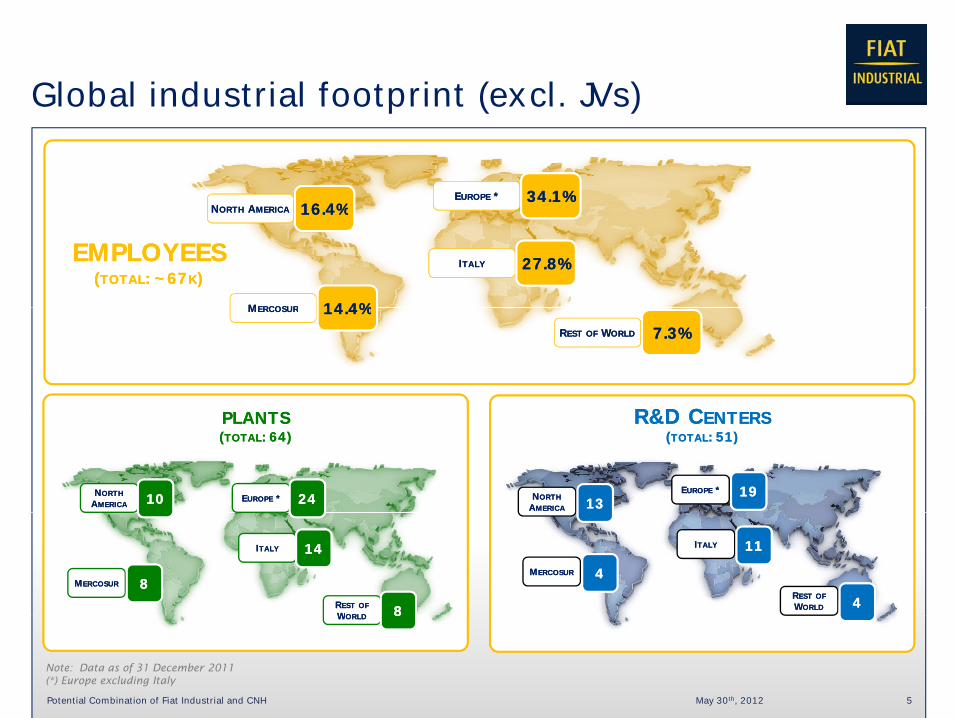

Global industrial footprint (excl. JVs)

Fiat Industrial Worldwide (FY ’10)NN AA 16 4%16 4%EEUROPEUROPE ** 34.1%34.1%

Global industrial footprint (excl. JVs)

Fiat Industrial Worldwide (FY 10)WW Industrial presence and employees

NNORTHORTH AAMERICAMERICA 16.4%16.4%

IITALYTALY 27.8%27.8%

MMERCOSURERCOSUR 14 4%14 4%

EMPLOYEESEMPLOYEES((TOTALTOTAL: ~67: ~67KK))

R&D CR&D C

MMERCOSURERCOSUR 14.4%14.4%RRESTEST OFOF WWORLDORLD 7.3%7.3%

PLANTSPLANTS((TOTALTOTAL: 64): 64)

R&D CR&D CENTERSENTERS((TOTALTOTAL: 51): 51)

NNORTHORTHAAMERICAMERICA 1010 EEUROPEUROPE ** 2424 NNORTHORTH

AAMERICAMERICA 1313EEUROPEUROPE ** 1919

MMERCOSURERCOSUR 88

IITALYTALY 1414

RRESTEST OFOFWWORLDORLD 88

MMERCOSURERCOSUR 44

IITALYTALY 1111

RRESTEST OFOFWWORLDORLD 44

May 30th, 2012Potential Combination of Fiat Industrial and CNH 5

Note: Data as of 31 December 2011(*) Europe excluding Italy

WWORLDORLD 88

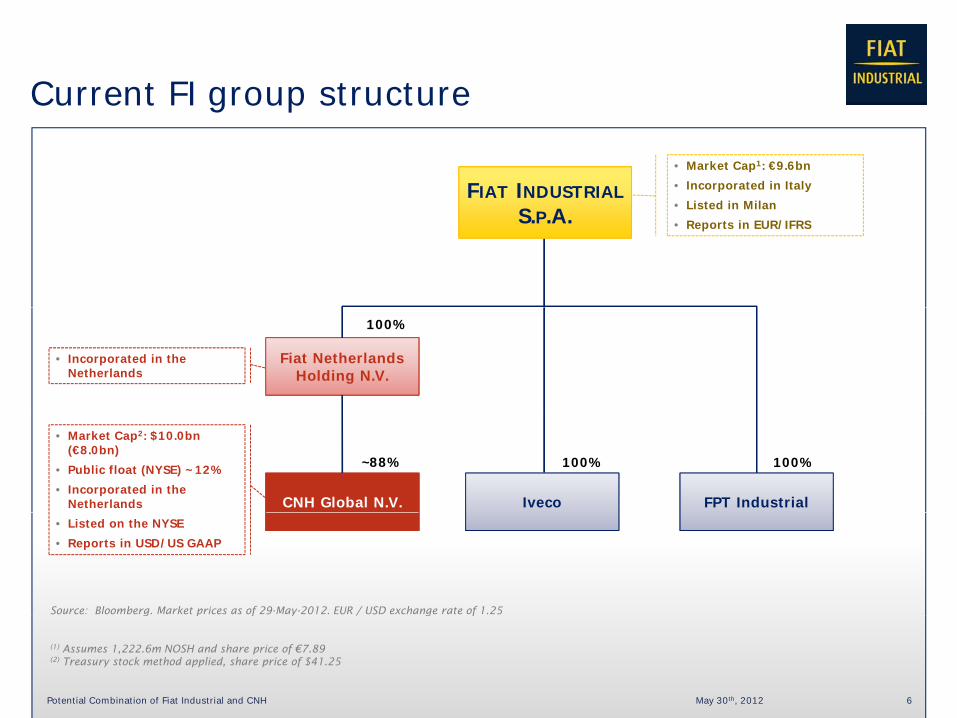

Current FI group structureCurrent FI group structure

FIAT INDUSTRIAL• Market Cap1: €9.6bn• Incorporated in Italy• Listed in MilanS.P.A. • Listed in Milan• Reports in EUR/IFRS

Fiat Netherlands Holding N.V.

100%

• Incorporated in the Netherlands

IvecoCNH Global N.V.

~88%

FPT Industrial

100% 100%

• Market Cap2: $10.0bn (€8.0bn)

• Public float (NYSE) ~12%• Incorporated in the

Netherlands

Source: Bloomberg. Market prices as of 29-May-2012. EUR / USD exchange rate of 1.25

• Listed on the NYSE• Reports in USD/US GAAP

May 30th, 2012Potential Combination of Fiat Industrial and CNH 6

g p f y / g f

(1) Assumes 1,222.6m NOSH and share price of €7.89 (2) Treasury stock method applied, share price of $41.25

Assessment of the current situation

• The existence of two distinct equity securities for FI and CNH listed on

Assessment of the current situation

separate markets is the result of a series of transactions pursued in the

past by FIAT Group

• The current situation is cumbersome and inefficient in several respects Small public float and liquidity of CNH

Constrains the Group’s valuation Limits ability by top US capital goods investors to build meaningful positions in CNH Creates holding company discount at FI group level

Limits the Group’s ability to capture strategic opportunities using equity Multiple jurisdictions and layers of governance complicate intra-group dealingsMultiple jurisdictions and layers of governance complicate intra group dealings

• These issues have been magnified following the demerger because of the

greater prominence of CNH within FI Group

May 30th, 2012Potential Combination of Fiat Industrial and CNH 7

greater prominence of CNH within FI Group

FI and CNH trading at a significant discount vs. peersvs. peers

2012E EV/EBITDA T2012E EV/EBITDA TRADINGRADING MMULTIPLESULTIPLES

6.4 x6.1 x

4.9 x 4 9 x 4 8 x

6.3 x 6.1 x

5.1 x

4.3 x

3.2 x

4.9 x 4.9 x 4.8 x

FI CNH Scania MAN Volvo Navistar Paccar Deere CAT AGCO

May 30th, 2012Potential Combination of Fiat Industrial and CNH 8

Source: Companies’ latest filings, presentations and websites; IBES Estimates; Bloomberg. Market prices as of 29-May-2012

Note: EV calculated as Market Cap + Industrial Net Debt + Pension Liabilities + Minority Interest - Associates/JVs - Book Value of Financial Services Subsidiaries

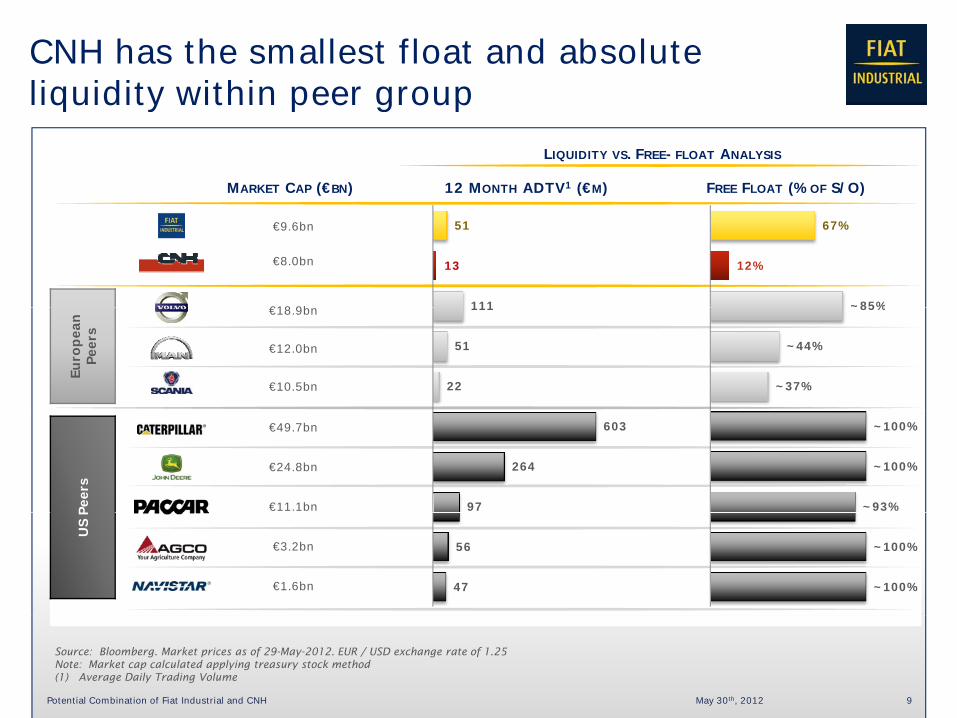

CNH has the smallest float and absolute liquidity within peer group

LIQUIDITY VS. FREE-FLOAT ANALYSIS

MARKET CAP (€BN) 12 MONTH ADTV1 (€M) FREE FLOAT (% OF S/O)

liquidity within peer group

€9.6bn

€8.0bn

€18 9b

67%

12%

~85%

51

13

111

Euro

pean

Pe

ers

€18.9bn

€12.0bn

€10.5bn

~85%

~44%

~37%

111

51

22

Peer

s

€49.7bn

€24.8bn

€11.1bn

~100%

~100%

~93%

603

264

97

US

P

€3.2bn

€1.6bn

~100%

~100%

56

47

May 30th, 2012Potential Combination of Fiat Industrial and CNH 9

Source: Bloomberg. Market prices as of 29-May-2012. EUR / USD exchange rate of 1.25Note: Market cap calculated applying treasury stock method(1) Average Daily Trading Volume

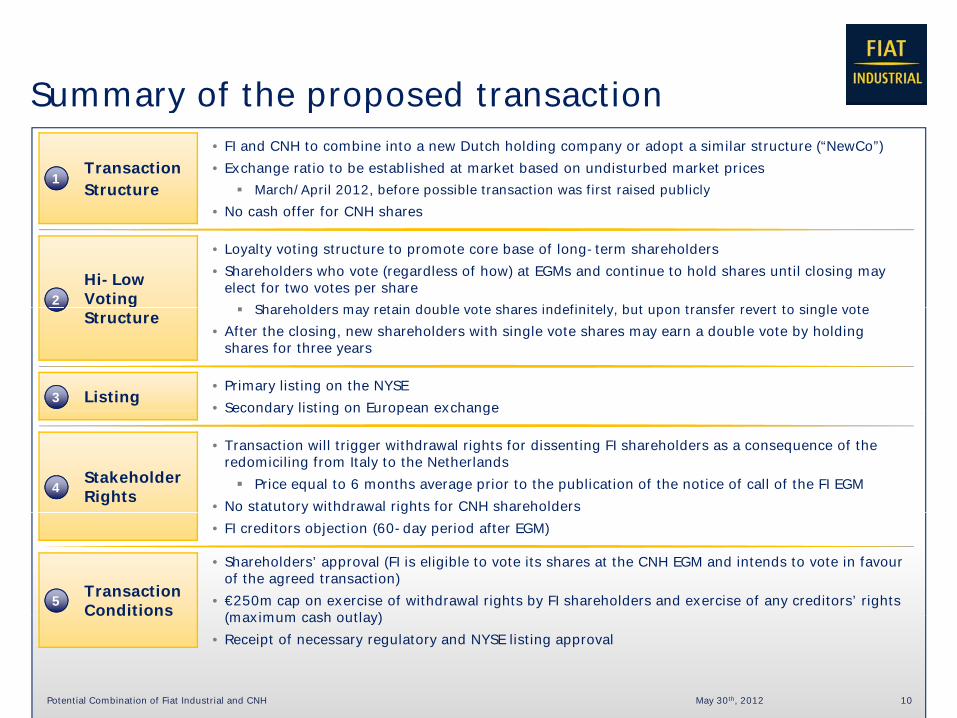

Summary of the proposed transactionSummary of the proposed transaction

TransactionStructure

• FI and CNH to combine into a new Dutch holding company or adopt a similar structure (“NewCo”)• Exchange ratio to be established at market based on undisturbed market prices

March/April 2012, before possible transaction was first raised publicly1

• No cash offer for CNH shares

Hi-Low Voting

• Loyalty voting structure to promote core base of long-term shareholders• Shareholders who vote (regardless of how) at EGMs and continue to hold shares until closing may

elect for two votes per share Shareholders may retain double vote shares indefinitely but upon transfer revert to single vote2

Structure Shareholders may retain double vote shares indefinitely, but upon transfer revert to single vote• After the closing, new shareholders with single vote shares may earn a double vote by holding

shares for three years

Listing• Primary listing on the NYSE• Secondary listing on European exchange

3Secondary listing on European exchange

Stakeholder Rights

• Transaction will trigger withdrawal rights for dissenting FI shareholders as a consequence of the redomiciling from Italy to the Netherlands Price equal to 6 months average prior to the publication of the notice of call of the FI EGM

• No statutory withdrawal rights for CNH shareholders4

y g• FI creditors objection (60-day period after EGM)

Transaction Conditions

• Shareholders’ approval (FI is eligible to vote its shares at the CNH EGM and intends to vote in favour of the agreed transaction)

• €250m cap on exercise of withdrawal rights by FI shareholders and exercise of any creditors’ rights (maximum cash outlay)

5

May 30th, 2012Potential Combination of Fiat Industrial and CNH 10

Conditions (maximum cash outlay)• Receipt of necessary regulatory and NYSE listing approval

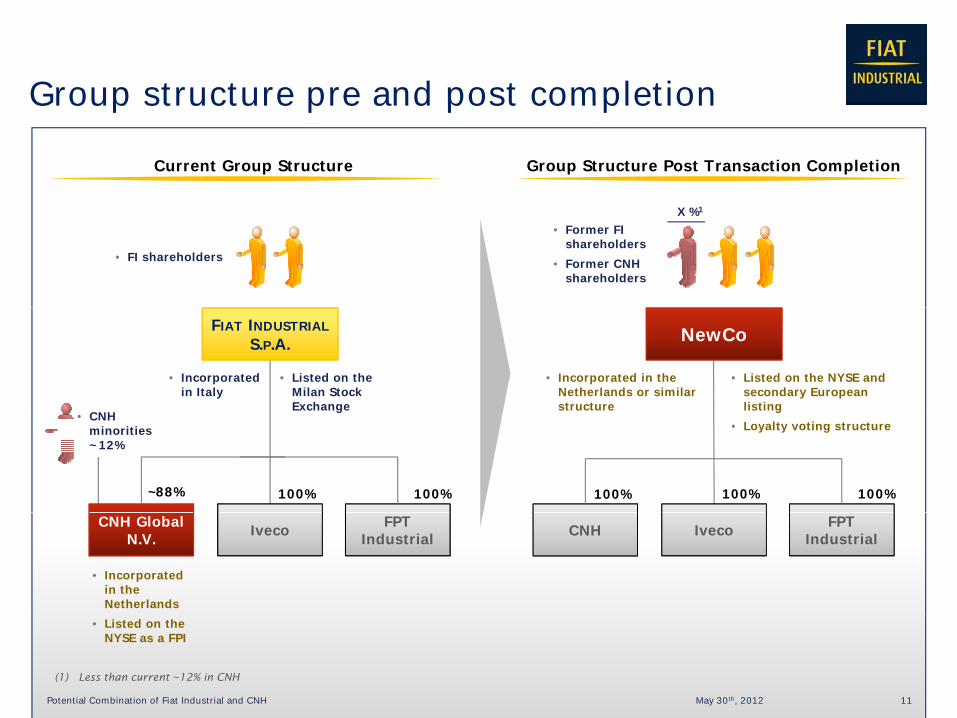

Group structure pre and post completionGroup structure pre and post completion

Current Group Structure Group Structure Post Transaction Completion

• Former FI shareholders

• Former CNH shareholders

• FI shareholders

X %1

FIAT INDUSTRIALS.P.A.

• Listed on the Milan Stock Exchange

NewCo

• Incorporated in the Netherlands or similar structure

• Incorporated in Italy

• Listed on the NYSE and secondary European listing

~88%

Exchange

100% 100% 100% 100%100%

structure listing• Loyalty voting structure

• CNH minorities ~12%

IvecoCNH Global N.V.

FPT Industrial Iveco FPT

IndustrialCNH

• Incorporated in the Netherlands

May 30th, 2012Potential Combination of Fiat Industrial and CNH 11

• Listed on the NYSE as a FPI

(1) Less than current ~12% in CNH

Rationale for the transaction

FFULLULL COMBINATIONCOMBINATION OFOF FIFI ANDAND CNHCNH HASHAS SEVERALSEVERAL POTENTIALPOTENTIAL BENEFITSBENEFITS FORFOR BOTHBOTH SETSSETS OFOF SHAREHOLDERSSHAREHOLDERS

• Create a single class liquid stock listed in New York with secondary listing in Europe

• Build a true peer to the major North American-based capital goods companies

• Increase liquidity and attract new capital goods-focused investor base and analyst coverage in the CapitalMarkets and Valuation

q y p g y gUS

• Capitalize on scarcity value deriving from being the only significant agricultural equipment player listed in Europe

• Eliminate CNH illiquidity discount and achieve, over time, a valuation more in line with global q y gcapital goods peers

• Improve credit profile and access a broader liquidity pool

• Create opportunities for regional consolidation of Financial Services platforms or common development of new infrastructures in developing markets

Strategic and Operational

development of new infrastructures in developing markets

• Acquire greater scale in key emerging markets, such as China, Brazil, Argentina, translating into more effective local execution

• Simplify intra-group dealings

May 30th, 2012Potential Combination of Fiat Industrial and CNH 12

• Secure powertrain know-how for CNH

• Increase flexibility to pursue strategic transactions and reward long-term shareholding

Summary process timelineSummary process timeline

May 30th

FI approach to CNH

BoD to approve formal Merger Plans

SEC registration and NYSE listing approval

EGMs

60-day period for FI creditors' opposition

Secondary EU listing

Double vote mechanism implementation

Closing

Closing targeted by

May 30th, 2012Potential Combination of Fiat Industrial and CNH 13

Closing targeted by year-end 2012

APPENDIXAPPENDIX

20 Novembre, 2010

CNH – Evolution of Fiat / FI shareholding since 1991since 1991

80%

Acquisition of 80% stake of Ford New Holland from Ford

Ford maintain a 20% stake

~70%IPO on NYSE of ~30% stake

~85%Stake increased via conversion of US$1.4bn of “advance to capital” provided by Fiat

~90%Automatic conversion of Preference shares into common shares

1995 19961991 1999 2006 Today2000 2003… … … … …

100% ~70%Acquisition of 100% of CASE for $4.6bn, entirely financed with debt

Creation of CNH Global NV

~85%Issuance of 8mn convertible Preference shares to Fiat in exchange for

Stake progressively increased to 100% via:

~88%

~2% dilution related to shares issued for incentive compensationCreation of CNH Global NV g

$2bn of debt owed to Fiat

i) Acquisition of Ford stake and

ii) Capital increase of $594mn subscribed by Fiat only

compensation schemes

May 30th, 2012Potential Combination of Fiat Industrial and CNH 15

ContactsContacts

FIAT INDUSTRIAL INVESTOR RELATIONSFIAT INDUSTRIAL INVESTOR RELATIONS

- MANFRED MARKEVITCH – HEAD OF INVESTOR RELATIONSMANFRED MARKEVITCH HEAD OF INVESTOR RELATIONS

- FEDERICO DONATI – INVESTOR RELATIONS OFFICER

EMAIL: [email protected]

WEBSITE: www.fiatindustrial.com

May 30th, 2012Potential Combination of Fiat Industrial and CNH 16