Download - Overview of the Luxembourg Budgeting System

Public finance in Luxembourg

Overview

of the

Luxembourg Budgeting System

Version 1.0

Raymond.Bausch @ igf.etat.lu

32nd Annual Meeting of OECD Senior Budget Officials

Luxembourg, 6 June 2011

National Motto

Mir wölle bleiwe wat mir sin

National Motto

Mir wölle bleiwe wat mir sin

We want to remain what we are

What we are :

• Innovative

What we are :

• Innovative in

• Steel

What we are :

• Innovative in

• Steel

• Finance

What we are :

• Innovative in

• Steel

• Finance

• Satellites

What we are :

• Innovative in

• Steel

• Finance

• Satellites

• Other …

What we are :

• Innovative

• International

What we are :

• Innovative

• International

• Small,

but beautiful

What we are :

• Innovative

• International

• Small,

but beautiful

Public Finance in Luxembourg

• The current state – Some figures

– Public sector organization

– Public finance

– Budget implementation

– 5 budget principles

– Exceptions

– Fiscal rules

• Reform – Guidelines

07/06/2011 Inspection générale des Finances

Ministère des Finances, Luxembourg 12

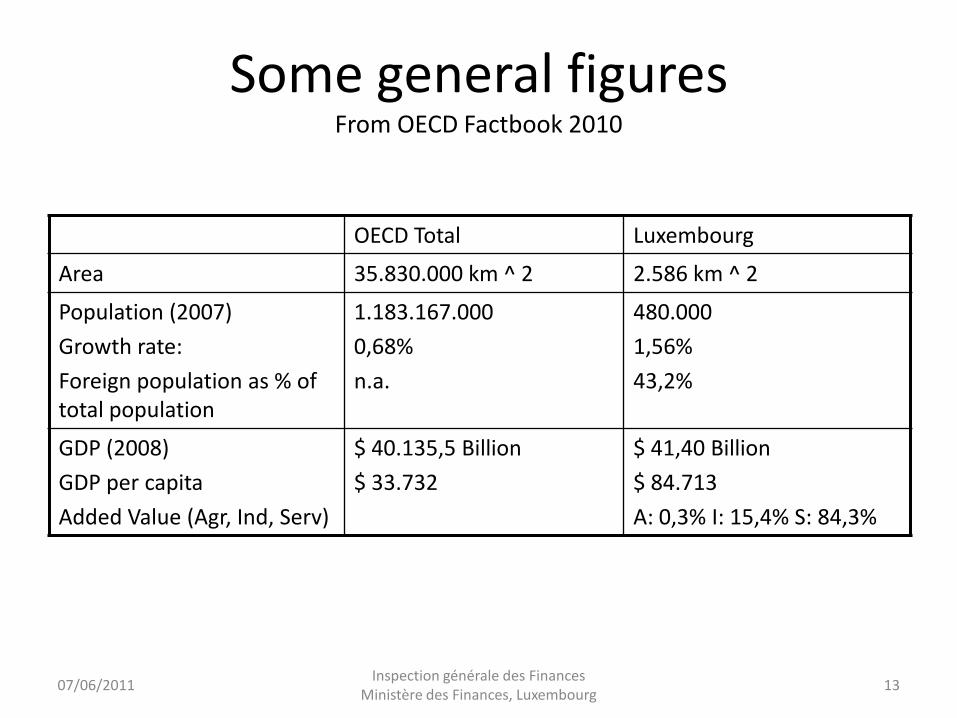

Some general figures From OECD Factbook 2010

OECD Total Luxembourg

Area 35.830.000 km ^ 2 2.586 km ^ 2

Population (2007)

Growth rate:

Foreign population as % of total population

1.183.167.000

0,68%

n.a.

480.000

1,56%

43,2%

GDP (2008)

GDP per capita

Added Value (Agr, Ind, Serv)

$ 40.135,5 Billion

$ 33.732

$ 41,40 Billion

$ 84.713

A: 0,3% I: 15,4% S: 84,3%

07/06/2011 Inspection générale des Finances

Ministère des Finances, Luxembourg 13

Source: OECD Economic Outlook 88 database

Government net lending, as a percentage of GDP

-10

-8

-6

-4

-2

0

2

4

6

8

19951996

19971998

19992000

20012002

20032004

20052006

20072008

20092010

20112012 Luxembourg

Euro area (14 countries)

OECD - Total

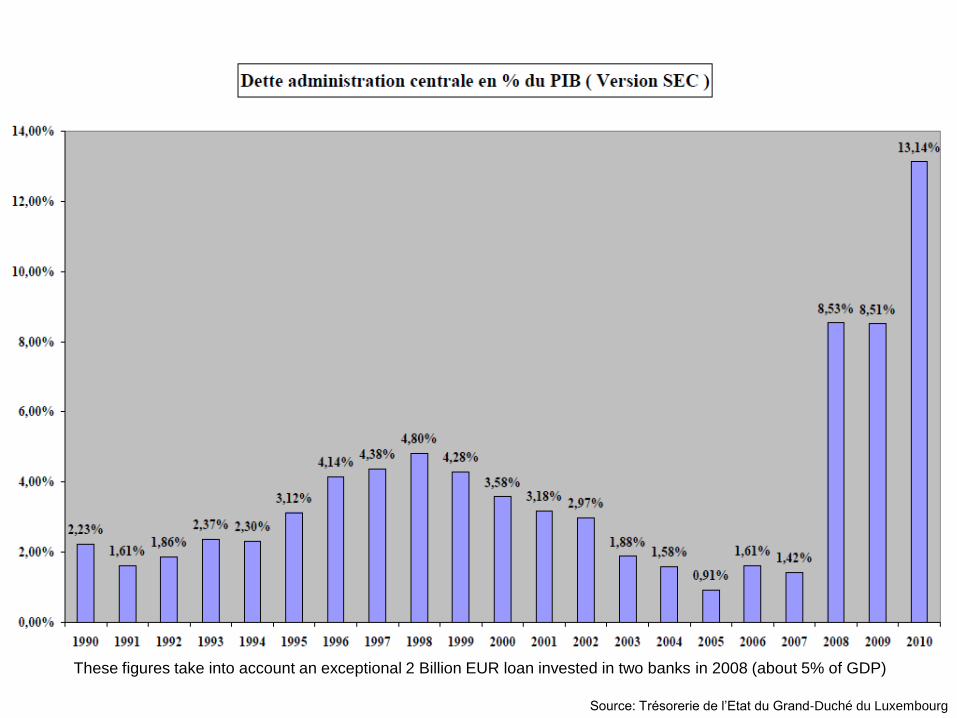

Source: Trésorerie de l’Etat du Grand-Duché du Luxembourg

These figures take into account an exceptional 2 Billion EUR loan invested in two banks in 2008 (about 5% of GDP)

Public sector organization

• Administrative subdivisions of Luxembourg:

– 3 districts, 12 cantons, 116 municipalities

• Ministries, administrations, public institutions, associations

• Parliament (Chamber of Deputies)

• Court of Accounts

• General Inspectorate of Finance

– an administration of the Ministry of Finance

07/06/2011 Inspection générale des Finances

Ministère des Finances, Luxembourg 16

Public finances

• They include central governement finance, municipality finance and social security finance

• One annual law provides annual permits for all revenues and all expenditures

• The revenues are linked to the budget exercice where they are received

• The expenditures are linked to the budget exercice where a commitment has been made

07/06/2011 Inspection générale des Finances

Ministère des Finances, Luxembourg 17

Proposal of a commitment

1. Control

2. Control

Commitment/ Order

Receipt of the object or service

Invoice

Decision of the payment

Payment

5 budget principles

• Principles of unity, annuality and universality

• Principle of non-earmarking of the revenues

• Principle of specification of the expenditures

07/06/2011 Inspection générale des Finances

Ministère des Finances, Luxembourg 19

Exceptions

• Some budget line are

– irrespective of the budget exercises

– unlimited (an overrun may be authorized by the Minister of Finance)

– some transfers are possible

• Special Acts (projects> 40 million euros)

• Special Funds

• Services with separate management

07/06/2011 Inspection générale des Finances

Ministère des Finances, Luxembourg 20

Fiscal rules

• Each public loan must be authorized by a law stating the purpose (eg Rails Fund)

• The municipalities may use a loan to balance their capital budget provided, however, the regular budget margins must be sufficient to repay the loan (section 118 of the Municipal Act)

• Fiscal rules (set by law) specify the public financial contribution to Social Security

• The Government Programme 2009-2014 (see next page)

• Speech on the State of the Nation: "The government will continue its policy of savings to ensure that public finances - with their three components, central government, municipalities and social security systems - are in balance in 2014"

• Annual budget circular (eg -10% in expert fees)

07/06/2011 Inspection générale des Finances

Ministère des Finances, Luxembourg 21

Excerpt from the Government Program 2009-2014

Public Finance • Compliance with the objectives of the Stability and Growth Pact of the European

Union. • an anti-cyclical finance policy • the Government will seek to avoid, at the end of the program for economic

recovery, growth in government spending that exceeds the economic growth in the medium term.

– maintain capital spending at a high level – inhibit the growth of spending on social transfers by introducing more social selectivity – review the subsidies and tax breaks on their purpose and fiscal and social impact – limit the growth in operating expenses of the State – avoid new measures having a significant impact on the growth of government spending – do not increase Taxation of individuals during the economic crisis – maintain a competitive tax environment for business taxation.

07/06/2011 Inspection générale des Finances

Ministère des Finances, Luxembourg 22

Reform

In a dual concern for modernization of government operations and efficiency of public spending,

the Government will examine ways to improve the process of elaboration, implementation and evaluation of the budget.

(Excerpt of the Government Program 2009-2014)

07/06/2011 Inspection générale des Finances

Ministère des Finances, Luxembourg 23

What we are :

• Innovative

• International

• Small,

but beautiful