Newsstand Challenges

Steve Burbridge

SVP Sales and Logistics - West

Newsstand Challenges

There are a number of challenges facing the single copy portion of the magazine business. Among the most important are: Profitability of the wholesalers, Challenges from other commodities, and Sluggish unit sales (is flat the new up?) leading to a

push for increased profitability/productivity from retailers

3

Wholesale Landscape Has Changed

Willingness to cut discounts or withhold incentives to retailers

Refusing to distribute products due to cover price and/or discount (e.g., Bauer’s Cocktail)

Confronting publishers over low cover prices on existing, high unit volume titles (e.g., OK)

Cutting titles to be distributed based upon efficiency, discount, etc.

Moving to once/week delivery and geo-routing Reviewing delivery methodology (hybrid of truck and DSD

via 3rd party carriers such as UPS and FedEx) Reviewing pre-weekend and galley delivery approach

Key Retailer Themes

Checkout racks Threats from other CPG companies as well as the

retailers themselves Wrigley going after Over-the-Belt for gum/mints only Soda Coolers at more than every third checkout Gift Cards Self-scan roll-outs Other merchandise such as Slim Jims

Retailers reducing the # of checkouts for magazines and/or going to lower profile racks

Key Retailer Themes

Rack Charges Traditional $22.28 per pocket moved to $25.00 as of 3/3/08

Large retailers seeking - and getting – SBT (scan-based trading)

All retailers are looking for margin improvement and are seeking it from Wholesalers AND Publishers

Retailers looking to reduce their authorized lists and go to more full-faced mainlines

Gum/Mints Over-the-Belt

Wrigley’s acquisition of such brands as Lifesavers and Altoids has them pushing retailers to dedicate space OTB for gum and mints at the expense of magazines Bill Wrigley Jr. making

account calls on retailers’ senior management teams

Soda Coolers

Acquisitions such as Glaceau (Vitamin Water) by Coke, as well as a retailer’s desire to increase gross margin from Private Label water, are driving retailer to place their own coolers at more lanes to try to capture sale in this stagnant category Funding from Coke and

Pepsi as well as the high GM from water (60% or more) is driving this push

Other Commodities

Personal finance productsplus…

…gum / mints OTB.

The worst of all

worlds?

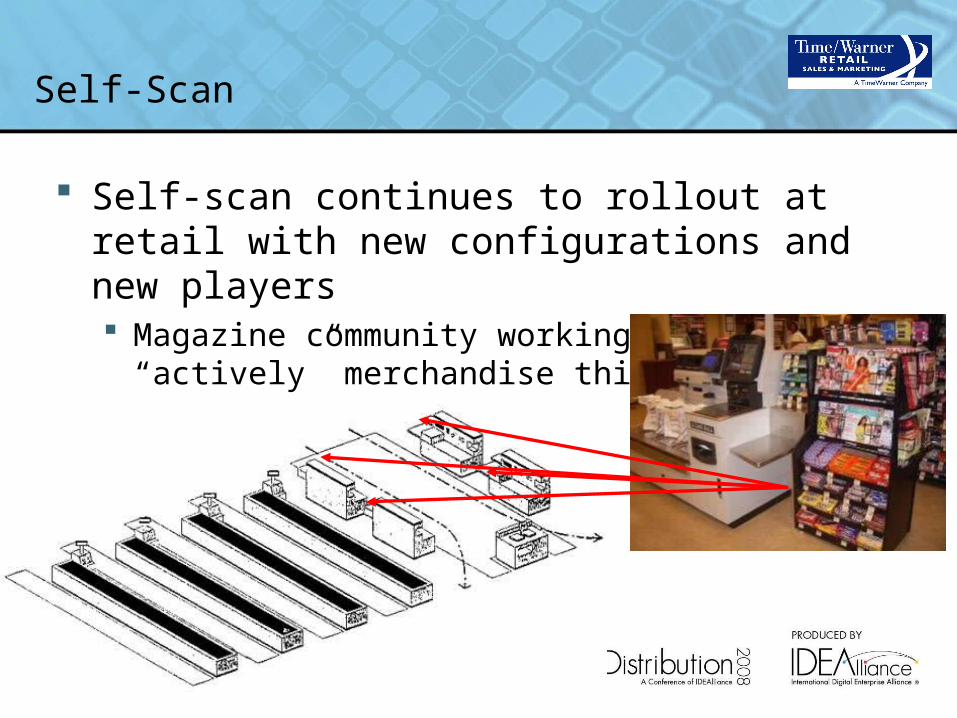

Self-Scan

Self-scan continues to rollout at retail with new configurations and new players Magazine community working to “actively”

merchandise this space

Front-end Configuration

The impact of other commodities, self-scan, coolers, etc., lead to a major loss in real estate

US

can

Tra

dition

al c/out

Cig

arette c/o

ut

Expre

ss

US

canU

Scan

US

can

Expre

ss

Tra

dition

al c/out

Tra

dition

al c/out

Tra

dition

al c/out

Tra

dition

al c/out

= magazine fixturing= other products= coolers

= possible opportunities (very limited pockets)

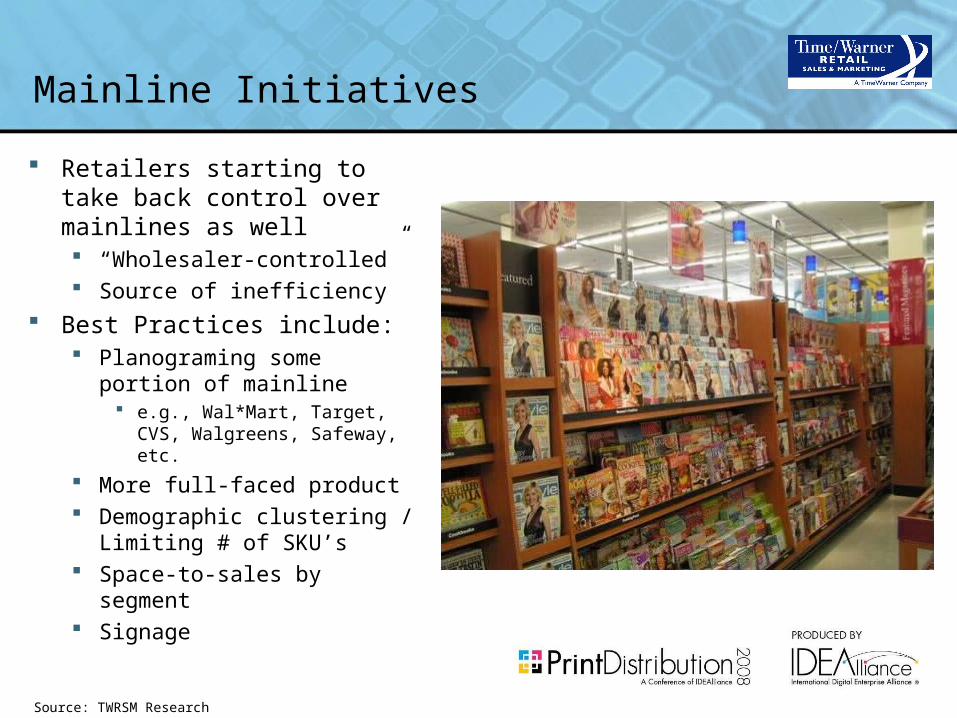

Mainline Initiatives

Retailers starting to take back control over mainlines as well “Wholesaler-controlled” Source of inefficiency

Best Practices include: Planograming some portion

of mainline e.g., Wal*Mart, Target, CVS,

Walgreens, Safeway, etc.

More full-faced product Demographic clustering /

Limiting # of SKU’s Space-to-sales by segment Signage

Source: TWRSM Research

Other Retailer Themes

Scan-based Trading SBT can be a good thing for the category as it reduces check-in

and check-out time. However, high shrink rates and the cost of absorbing store-level inventory can lead to less profitability to wholesalers

Growth of store perimeter and kiosks impacting display As “fresh” becomes more important, retailers grow produce,

bakery, etc. that forces mainline space to become smaller Retailers adding in-store kiosks and services – Starbucks, etc., -

“squeezes” the front-end and results in less merchandising space at checkout

Little to no growth in traditional retail outlets Most growth at retail coming from chains with no magazine

programs (such as Kohl’s, Trader Joe’s, etc.) or those with small programs (Walgreens, Target, etc.)

The Future

No traditional checkouts? RFID Handheld scanners

WWWD/WWTD What Will Wal*Mart Do? / What Will Target Do?

What else?